The Atlanta Voice honors the life of J. Lowell Ware.

PUBLISHER

Janis Ware jlware@theatlantavoice.com

PRESIDENT/ GENERAL MANAGER

James A. Washington jaws@theatlantavoice.com

EDITOR IN CHIEF

Marshall A. Latimore mlatimore@theatlantavoice.com

MANAGING EDITOR

Itoro Umontuen iumontuen@theatlantavoice.com

ART DIRECTOR

Vincent Christie vchristie@theatlantavoice.com

COPY CHIEF

Martel Sharpe info@theatlantavoice.com

DIRECTOR, DIGITAL MEDIA

Jeremiah Long jlong@theatlantavoice.com

DIRECTOR OF VISUALS

Trarell Torrence t.torrence@theatlantavoice.com

ADVERTISING, SALES & CIRCULATION

VP, BUSINESS DEVELOPMENT

Richard Dunn dunn@theatlantavoice

ADVERTISING ADMINISTRATOR

Chia Suggs advertising@theatlantavoice.com

CIRCULATION MANAGER

Terry Milliner

SALES

R.D.W. Jackson rdwadman@gmail.com

CONTACT INFORMATION

633 Pryor Street, S.W.

Atlanta, GA 30312

Office: 404-524-6426

Fax: 404-527-5464

The Atlanta Voice corrects all errors of fact published in its newspaper. To report an error of fact, send correction to newsroom@theatlantavoice.com.

Get smart about finances

Wells

Fargo has resources to learn about money management

CERITA BATTLES SVP, Head of Retail Diverse Segments, Wells Fargo Home Mortgage

Financial literacy is important for achieving many goals in life. Wells Fargo is proud to serve as the title sponsor of The Atlanta Voice’s 2019 Financial Literacy Supplement.

Get Smart About Credit Day, an annual financial education outreach campaign sponsored by the American Bankers Association (ABA) is on Oct. 17, making this month the perfect time to bring awareness to this important topic.

We appreciate the Voice’s leadership in providing helpful information to its readers focused on financial education and we are glad to be included.

Wikipedia defines “financial literacy” as the “possession of the set of skills and knowledge that allows an individual to make informed and effective decisions with all of their financial resources.”

Having a sound understanding of credit – including how to use it responsi-

bly – is essential. Good credit may make it easier to borrow money, may lower interest rates on loans or credit cards, may reduce insurance premiums, and may make it easier to rent an apartment and buy a home.

When you understand money and credit, you are more informed and can be more confident in the financial decisions that you make. In addition, it can make the journey to reach your financial goals an enjoyable and successful one whether that’s purchasing a car, becoming a homeowner, starting a business or even planning for retirement.

Not understanding financial requirements and implications for goals like these can delay then or even mean not achieving them at all.

As we recognize Get Smart About Credit this month, I encourage everyone to be proactive about financial literacy.

Learn everything you can about the financial goals you want to achieve. There

are many resources to help. You can find assistance online, by phone and even in person, many times at no cost.

At Wells Fargo, our Financial Health bankers provide our customers with personalized support, proactive guidance and encouragement, and convenient financial resources they need to take action and improve their financial health.

The Hands-on Banking® online learning center offers resources for anyone who wants to learn more about money management.

There are articles to read and even self-guided courses to help improve financial literacy on a number of topics.

Financial literacy is a solid foundation to start the journey to achieve many of life’s financial goals.

And Wells Fargo is committed to helping people establish better financial health – setting them on a path towards financial stability and reaching their full potential.

A simpler path to your new home

With me by your side and these online resources at your fingertips, you’ll have the support you need to navigate the home loan process.

Prepare for successful homeownership with helpful videos and interactive online programs like My FirstHome®. These tools are designed to help you understand the mortgage process and plan your home purchase.

Find the mortgage that’s right for you by comparing loan features, interest rates, monthly payments, closing costs, and more.

Apply the simpler way with an online mortgage application that can import information and lets you upload documents quickly and conveniently.

Track your mortgage application with yourLoanTrackerSM . See your loan status and upcoming tasks, upload documents, and get text alerts when you reach key milestones.1

To determine if a home loan is available with yourLoanTracker features, talk to a home mortgage consultant.

View all your accounts together and manage your mortgage with Wells Fargo Online®.

Enjoy personalized support from me every step of the way, with guidance and information to meet your unique needs.

Call, stop by, or click today!

250 E Ponce De Leon Ave Floor 02

Decatur, GA 30030-3440 (404) 929-4731

wfhm.com/loans/decatur/index-branch.page

Buying a home: Before you purchase

Make sure you understand all the costs associated with buying a new home

MARSHA JOHNSON VP, Diverse Segments Market Consultant, Wells Fargo Home Mortgage

Buying a home is one of life’s most delightful achievements and a goal most Americans hope to achieve.

In Wells Fargo’s latest “How America Views Homeownership” survey, more than half of the respondents (70 percent) say that owning a home is seen as a sign that someone is a “successful adult.”

If your goal is to be a homeowner, it’s important be aware of costs associated with the home buying decision. Not only do you want to know what it takes to finance the mortgage, but also what’s needed to help you stay in the home and be a successful homeowner.

Here are some associated costs with homeownership that buyers should keep in mind.

Downpayment: Most home purchases require a downpayment. While a downpayment could be as low as 3 percent, that amount can be a homeownership barrier, especially for many low-to-moderate income homebuyers.

More than one in four respondents to the Wells Fargo survey said that the downpayment is the No. 1 hurdle to purchasing a home.

For those who qualify, there are programs that could help families reach the amount they need for that downpayment.

The NeighborhoodLIFT program has helped more than 22,000 families achieve homeownership with downpayment assistance since 2012.

Homebuyers should also check nonprofits and even their local governments for programs that offer bonds and/or downpayment assistance programs.

Closing Costs: These costs are due when you sign the final documents at the closing transaction for your home purchase.

Closing costs may include attorney, lender and real estate agent fees, and prepaid items such as escrow payments.

Closing costs are often 3 to 5 percent of your total loan amount. So even if you have the funds for the downpayment, make sure you have enough saved to cover closing costs.

Property taxes and insurance: Many homeowners have their property taxes and insurance paid through an escrow account.

That means you do not have to save for these separately because they are part of the monthly payment you make to your lender where a part goes toward the principal and interest of the mortgage and the other part goes into the escrow account.

Property taxes and insurance premiums may change over time, so your lender may conduct an annual review and make adjustments to make sure you have enough to cover the costs of the taxes when they are due.

Your lender may require having an escrow account, especially if your downpayment is less than 20 percent.

If you have that choice and want to pay the taxes on your own, it’s important to budget correctly so that you have the funds available when they are due. Not paying your taxes on time can result in additional fees and could lead to foreclosure.

Repairs and Maintenance: If you don’t already have a rainy day fund, you definitely want to have one as a homeowner. Regular maintenance is one thing but repairs can pop up at any time.

Making sure you also are prepared for unexpected repairs plays an important role in being a successful homeowner. Some lenders also look at your savings when considering you for loan approval.

Planning to become a homeowner is an exciting decision. Help that journey be as enjoyable as you can by understanding and being prepared for all of the financial obligations of being a homeowner.

Financial health is everything

Try out these

eight simple steps to achieve better financial health

CHRIS STUBBS VP, Regional Banking District Manager, Wells Fargo

Everyone knows the old adage: An apple a day keeps the doctor away.

And while there may be some truth to this, we also know there are other steps involved in maintaining good health – from exercising and eating right, to getting enough sleep every night.

The same can be said for your overall financial health –several things contribute to being financially healthy.

Unfortunately, many Americans struggle with where to start.

Research shows that 57 percent of Americans are struggling financially, according to findings released in a 2016 consumer study by the Center for Financial Services Innovation.

Further, 44 percent say they would not be able to cover a

$400 emergency expense without selling something or borrowing money, according to a 2017 study by the FED Board of Governors.

That’s why it’s important to stay on top of your financial health. Just like visiting your doctor for a routine check-up, it’s essential for everyone to understand the daily financial decisions they can make to establish healthy financial habits.

Each good decision moves you forward in your journey to better financial health. These actions can help you make meaningful financial changes in your life.

Like eating an apple a day, small habit-forming actions to support your financial health can make a big difference over time.

Here are eight steps that can help you stay on track and can have a big impact on your financial health:

• Pay yourself first – set aside some income for savings, about 5 to 10 percent

• Track your spending –make sure you know where your money is going each month

• Create a safety net –build up emergency savings to cover 3-6 months’ of expenses

• Pay down your highinterest debt – pay down the debt that costs you the most

• Pay on time, every time –pay bills on time to improve and maintain your credit score

•Know where your credit stands – check your credit report annually

•Review your insurance annually – protect what counts by checking coverage annually

• Save for a better retirement –save at least 10 percent of your income each year

THINKSTOCK

PHOTOS

How to create a spending plan

Here’s a no-frills guide to understanding and making a plan for your finances

Budgeting can seem tough. You can make it less intimidating by thinking of it as creating a spending plan — a well-thoughtout and flexible document that details how you’re going to spend your money in the weeks, months, and eventually, years to come.

Having a spending plan can help you support your current lifestyle while setting you up for future needs. Here’s how to get started:

Review what you spend

Tiffany Aliche, founder of financial education website The Budgetnista Blog and author of The One Week Budget, recommends you start by taking stock of your financial situation. She notes, “It’s OK to have goals, but before we even identify those, [ask], ‘Where are you?’”

To get a sense of where your money is coming from and where it’s going, look over your bank and credit card statements from the past two months. If you don’t have these statements, begin tracking your expenses for the next month.

Do you regularly spend more than you earn? If so, finding ways to cut back should be your first order of business.

Check out the Hands-on Banking® Budget Toolkit for a detailed outline of what to consider when reviewing your earnings and spending.

Organize your expenses into a spending plan

Once you’ve reviewed your spending habits, organize your spending by organizing the payments you make into a spending plan. You can write these out on paper or use online tools such as the Budget Watch.

An effective way to categorize your expenses is by identifying what is fixed, flexible, and discretionary:

• Fixed expenses are those you pay regularly and cost the same each time, such as loan payments, insurance, and rent or mortgage.

• Flexible expenses are paid regularly, but the amount can change, such as groceries or utility bills.

• Discretionary expenses are things you choose to spend on, like going out to eat or shopping for clothes. Categorizing your spending this way can help you get a better picture of where your money goes and determine where you may want to cut back.

You should also write or enter in the timing of these payments — whether you make them weekly, monthly, or yearly.

By paying attention to timing, you can better prioritize what needs to be paid first and possibly spread out payments throughout the month.

This way, you are not overwhelmed with

due dates in one specific week.

Another advantage to knowing this schedule? When you have a fixed payment due, such as insurance or car payment, you can set money aside each paycheck for that expense.

Make your spending plan achievable

It’s important to make sure your spending plan is achievable on a day-to-day basis. To help with that, you can do one or all of the following as you’re able to:

• Track cell phone usage in the same way you track your spending habits. Consider what features you use most, and try to eliminate paying for extras you don’t need.

• Weigh your transportation options. Frequent ride-sharing can drain your income, so consider carpooling or taking mass transit if the rates are less expensive.

• Adjust your plan for the unexpected. Keep tabs on your emergency fund so you can leverage it when urgent expenses, like a medical bill, pop up.

Though your spending plan will be a work in progress, paying bills on time should always be your top priority.

Late fees and interest can add up quickly and may hurt any short-term benefits you gained by prioritizing other financial goals.

To avoid these pitfalls, try setting up:

• Notifications on when a bill or payment will be due ahead of time so you can make sure you have enough to cover it.

• Automatic payments so that you don’t forget to pay any bills.

• Automatic transfers from your checking account to your savings account so you can ensure you’re putting away as much of your paycheck each month as you intended.

Add your financial goals to your spending plan

Your spending plan details can also tell you how much money you have to put toward your financial goals via savings, investing and other types of accounts. Some goals to consider could be:

• Paying off debt

• Buying a car

• Moving to a new home

• Building an emergency fund

Because your spending plan helps you see where your money is going, you can incorporate your goals into it and use it to decide how to change your spending habits to meet them.

Set target dates for reaching goals, and calculate how much you will need to contribute on a weekly or monthly basis. This may mean temporarily paring down some discretionary spending, but make sure to be realistic and give yourself enough time to reach those goals.

Regardless of your expenses and goals, your spending plan should account for all of your activities involving money — and help you to take charge.

By managing your spending habits, you can feel empowered to get where you want to be when it comes to your finances.

Adjust your finances as life happens

Update your spending to make sure you’re making the right decisions for you

A spending plan is a well-thought-out strategy that turns a budget into a manageable part of everyday life. If you already have a plan, what’s next?

Most people understand the importance of sticking to a plan, but as your life changes and you work toward new goals, your spending habits will likely shift as well. When you don’t account for these changes, it’s easy to fall short of your goals.

Learning to adapt to changes is key to creating a healthy relationship with your finances. Taking control of your money means customizing your plans to your needs, so it’s important to remember to be flexible and open to change.

Know when to adjust your spending plan

To make sure your spending plan works, track and adjust your spending on a regular basis. Here’s what that might look like.

1. Your income changes. This includes both increases and decreases: events like a pro-

motion, a job loss, a raise, or other changes.

2. Your situation changes. This includes moving, getting married, having a child, or having a loved one pass away.

3. Your financial goals change. Maybe you’re ready to start saving for a wedding or a down payment on a house. Or, maybe you want to pay off student loans or credit card debt in the near future.

Adjust expenses in your spending plan

Look for opportunities within your expenses to make changes. Here’s how to do so:

1. Re-examine where your money is going. It’s valuable to keep regular tabs on how you are spending money. Keep an eye out for “lifestyle creep” — these are small changes you’ve gradually made, such as going out to eat more or making slightly more expensive purchases.

Perhaps you’ve been promoted at work and want to splurge a little on yourself with new clothes. It’s OK to enjoy your accom-

plishments, but be sure to think about how this may affect the rest of your spending plan in the long-term.

Look for balance. if you want to start spending 10 percent of your income on clothing or entertainment when you used to spend 5%, then look for ways to cut in other areas.

2. Find opportunities to reduce spending. As you re-evaluate your plan, look for things you continue to pay for but don’t actually use. This might be a subscription or service that doesn’t offer what you need anymore.

For example, if you recently got married, you and your spouse may want to consider consolidating your subscriptions to help cut costs.

Be sure to review expenses that are coming out of your account automatically that you may have forgotten about.

3. Find opportunities for discounts and deals. Every year or so, take another look at what you’re paying for items like insurance, internet, or other utilities. You could benefit

from finding a new service provider or negotiating a lower rate.

Perhaps you’ve even shopped at a store enough that you’re eligible for discounts. Being aware of these opportunities can help with your financial goals.

Small changes like this can add up and make a big difference when you’re working toward a goal such as saving up for a down payment on a house or paying off student loan debts.

No matter what, remain flexible

Don’t forget to make adjustments to your plan as you go through these steps. To be valuable, your spending plan needs to be flexible.

By both meeting current financial goals and knowing when it’s time to adjust, you can make sure you’re getting the most out of your resources. Still, they can give you an idea of where you stand.

Financial literacy for the next generation Fifth Third Bank offers a wide range of literacy options for Georgia consumers

One of the major financial challenges for Americans is saving money and staying out of debt: Average American household debt has increased by 11 percent annually in recent years, and topped $137,000 in 2016, according to research from NerdWallet.

As American adults creep further into uncertain territory—57 million say they have no savings at all—the next generation faces more challenges in creating their own financial stability.

With so many households under strain, it’s no surprise that children and teenagers aren’t picking up positive financial habits at home. Unfortunately, most are not learning about finances at school either: only 17 states require high school students to take a course in personal finance, according to the Council for Economic Education.

In addition, less than 20 percent of teachers say they feel competent to teach personal finance topics, according to the National Endowment for Financial Education.

That lack of training in financial topics translates into another generation of Americans who are unprepared to handle money effectively.

Review what you spend

Tiffany Aliche, founder of financial education website The Budgetnista Blog and author of The One Week Budget, recommends you start by taking stock of your financial situation. She notes, “It’s OK to have goals, but before we even identify those, [ask], ‘Where are you?’”

To get a sense of where your money is coming from and where it’s going, look over your bank and credit card statements from the past two months. If you don’t have these statements, begin tracking your expenses for the next month.

Do you regularly spend more than you earn? If so, finding ways to cut back should be your first order of business.

Check out the Hands-on Banking® Budget Toolkit for a detailed outline of what to consider when reviewing your earnings and spending.

Financial iIlliteracy curtails long-term goals

Entering the world without appropriate knowledge of managing finances sets up young people for failure.

For instance, more than 50 percent of student loan holders did not inquire on how much their future monthly payments would be before they opened their loans, and 53 percent said they would make a change if they could go through the process of taking out loans all over again, ac-

cording to research from the Global Financial Literacy Excellence Center.

Fifth Third Bank has several financial literacy programs including Young Bankers Club, Empower U®, the Financial Empowerment Mobile and Finance Academy to try to prevent these types of occurrences, and instead help families prepare for financial success.

“Fifth Third Bank believes that lives are improved when people have the knowledge and tools they need to make wise financial decisions,” said Tracee Smith, Community and Economic Development Manager for Fifth Third Bank (Georgia). “That’s why we administer our L.I.F.E. “Lives Improved Through Financial Empowerment®” programs which work to deliver financial education to people at all ages and stages of life.”

Fifth Third’s L.I.F.E. “Lives Improved Through Financial Empowerment®” programs

The Young Bankers Club is a financial literacy program that teaches children about the importance of good education, finances, and personal responsibility. The signature program is for elementary school students and provides a customized curriculum that meets national educational

standards for fifth-grade mathematics.

In the last two years, the Bank has taken more than 500 students through the Young Bankers Club at schools such as Barack Obama Elementary, Bolton Academy, and Marietta Elementary.

Once elementary students graduate from the program they understand how to save, the basics of the stock market, how to create budgets and study spending, how to examine interest and credit cards, how to manage a bank account and how to create a business plan for a small business.

Empower U® is another Fifth Third’s financial literacy program, but is geared towards adults. Taught by Fifth Third professionals, each Empower U class is 30 minutes and covers specific finance topics. Participants learn anything from managing and eliminating debt, to improving your credit score, to how to obtain homeownership.

Fifth Third has partnered with organizations such as the Atlanta Fire and Rescue Department, Hosea Helps, Atlanta Public Schools and Fulton County Board of Health to offer Empower U® sessions.

Fifth Third also brings banking assistance directly to the community with its financial empowerment mobile. The mission of the mobile is to take quality finan-

cial services directly to underbanked communities and empower residents to take control of their financial future.

The mobile is a 40-foot retrofitted city bus that is equipped with computer workstations in a classroom setting and has internet connectivity through satellite technology. On the mobile, Bank employees volunteer to provide credit counseling, provide information about opening bank savings accounts, use a Job Seeker’s Toolkit online module to help individuals find employment and provide free tax preparation.

Other services on the mobile include home mortgage assistance and money management planning and guidance. In the last two years, Fifth Third has served more than 5,000 metro Atlanta residents on the mobile.

For those schools and teachers who want to provide much-needed financial education for their students, the Fifth Third Bank Finance Academy® is the option for them.

The program provides financial literacy course to high school students in the Company’s 10-state footprint at no cost to schools or taxpayers.

—

Presented by Fifth Third Bank

She’s thinking ahead. So are we.

Most experts agree: the sooner kids learn about money, the better. That’s why every year we visit dozens of classrooms to teach fifth-graders about money management. A child’s future is invaluable. The Young Bankers Club® helps by investing in it now. Learn more at 53.com/ybc.

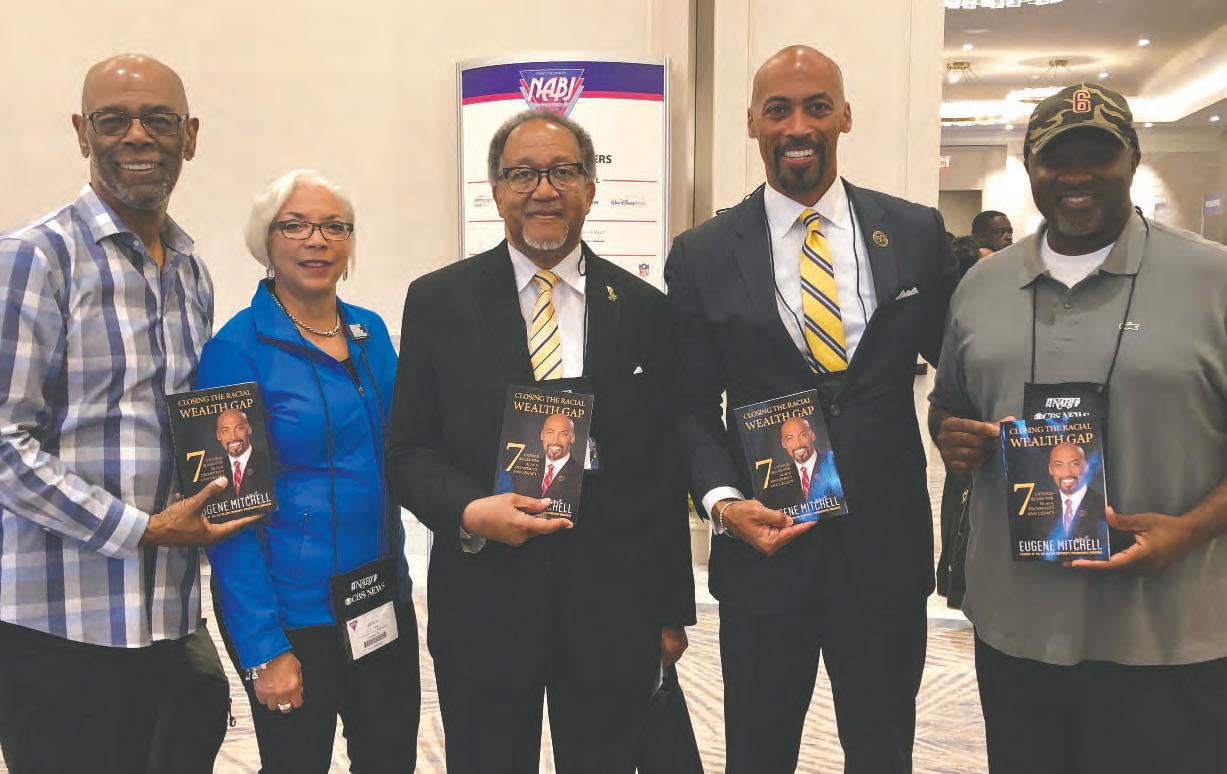

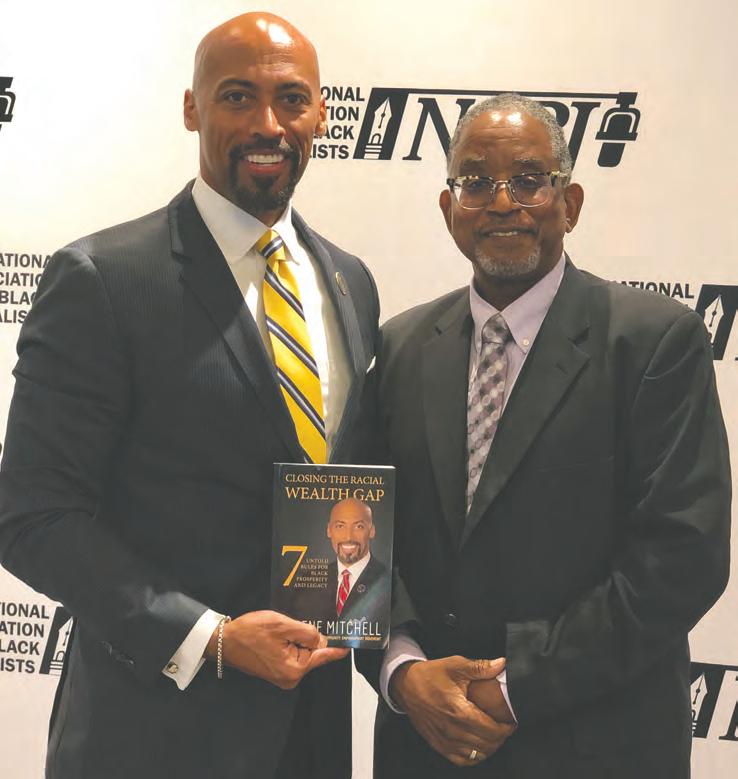

Mitchell releases new book, ‘Closing the Racial Wealth Gap: 7 Untold Rules’

For close to 20 years, Eugene Mitchell observed how other races, religions and ethnic groups used financial tools and strategies in ways that were vastly different to those being employed in African-American communities.

Eugene Mitchell serves as president and CEO of E. Mitchell Enterprises, Inc., a financial consulting and services firm. Prior to starting his own company, Eugene spent nearly two decades as a corporate vice president and “African-American Market” manager at New York Life Insurance Company, leading over 1,500 financial professionals nationwide.

When Eugene Mitchell left his senior-level position at a prominent New York insurance company after almost two decades, he had two primary goals: (1) teach the Black Community how to apply the tools, tips, and financial strategies to build wealth that have been withheld, underutilized, or under-leveraged in the community; and, (2) provide insight, inspiration, and aspiration for everyone to join a NEW movement just as revolutionary and essential as the Civil Rights Movement—The #Next50BILLION.

Noticing a difference in implementation and access, Mitchell initiated the $50 Billion Empowerment Plan for creating Black wealth in America. The initiative amassed $50 Billion of income protection and future income for over 340,000 Black families, using life insurance as the foundational asset.

In his new book, “Closing the Racial Wealth Gap: 7 Untold Rules for Black Prosperity and Legacy,” Mitchell shares valuable information and insight that anyone can use to create prosperity for himself or herself, as well as leave a lasting legacy for his or her family and community.

The rules are simple and easy to follow, and the book provides resources and ways to get started. With his book and movement, Eugene is amplifying the legacy call and response of the community: “If we ever come together... there is nothing we can’t do!”

“This book shares simple steps to longterm financial success, said Willie Jolley, Sirius XM radio host and bestselling author. “It should be required reading!”

Former New York State Senator, Antoine M. Thompson exclaimed, “(It) is a mustread for elected and government officials, business, civic, and faith leaders.”

InAugust2019,Eugenewaspresentedwith an Outstanding Book Award at the National Association of Black Journalists’ annual

Closing the Racial Wealth Gap: 7 Untold Rules for Black Prosperity and Legacy by Eugene Mitchell

convention in Aventura, Florida and was interviewed by Douglas C. Lyons during the convention’s Authors Showcase. Beyond the book, Eugene has created an opportunity to join a movement to create the next $50 Billion of income protection and future income for hundreds of thousands of Black families—and more importantly, Black communities.

—Staff Report

What does my credit score mean?

Need to understand how credit works? This comprehensive guide will help.

Do you know your credit score and do you understand what it means? If not, don’t worry. Here’s information that will help.

If you need help understanding your credit score, or to learn more about how to improve your credit, stop by a Synovus branch and talk with us.

What is a credit score?

While the terms “credit report” and “credit score” are often used interchangeably, they are actually quite different.

Think of your credit report as a report card — It’s a summary of all your financial information and behavior.

For example, when you pay your bills on time, you miss a payment, or when an account goes to collections, it will appear in your report.

Your credit score, on the other hand, is like your final grade. It’s a three-digit number that reflects how responsible you are when it comes to borrowing money, based on all the information in your credit report.

Creditors consider this number when deciding to approve you for a credit card, loan, and more. The higher your credit score, the better.

Understanding your FICO score

Actually, you have multiple credit scores. Depending on the scoring model and credit bureau, your credit scores can vary from one to the next.

However, the score that’s used by 90% of top lenders is your FICO score. FICO scores range from 300 to 850 and are based on the information that the three major credit bureaus — Experian, Equifax, and TransUnion — have on file for you. It’s a good idea to keep tabs on all three.

Credit score factors

Though the exact algorithm used to calculate your credit score is proprietary, we do know the five major factors that influence your FICO score:

Payment history (35 percent): This is the most important factor in determining your credit score. Missing one payment can negatively affect your score while always paying your bills on time will boost your score. Amount owed (30 percent): Lenders like to see that you aren’t too reliant on credit. Maxing out your credit cards is a red flag. In fact, experts recommend utilizing no more than 30 percent of your total available credit.

The day you move into your new home will be a dream come true for you and your family. And it may be easier than you think with our affordable mortgage programs. Let’s start your home financing conversation today.

Length of credit history (15 percent): A short credit history or no credit history at all can hurt your score because your behavior is less predictable. The longer you’ve been using credit, the better.

New credit (10 percent): Opening a lot of accounts within a short period of time can be a red flag. It’s a good idea to pace yourself when opening new credit cards or taking out loans.

Credit mix (10 percent): Finally, lenders like to see that you can handle a variety of credit types. A mix of credit cards and different types of loans will help your score.

Credit score ranges

So what’s considered good credit? And when should you worry? Experian breaks down the FICO score ranges:

• Exceptional = 800+

• Very Good = 740 to 799

• Acceptable = 670 to 739

• Fair = 580 to 669

• Poor = 579 and lower People with “very good” and “exceptional” credit scores will be able to borrow money at the lowest interest rates. Those with “fair” and “poor” scores will have to pay more to

borrow money — if they’re approved at all.

How to check your credit report

and credit score

It’s important to regularly check your credit report and credit score.

Once a year, you can check your credit report from all three of the major credit bureaus for free at annualcreditreport.com. Review your credit reports for any errors that could negatively affect your score.

If you do find an error, you can dispute it online through that credit bureau’s website or give them a call:

• Equifax – 1-800-685-1111

• Experian – 1-888-397-3742

• TransUnion – 1-800-888-4213

Credit reports don’t include your credit score, unfortunately. However, most credit card companies offer free FICO scores to their customers.

There are also sites, such as Credit Karma and Credit Sesame, that provide free credit scores, though they do not offer FICO scores. Still, they can give you an idea of where you stand.

Presented by Synovus,

the bank of here.

Father, daughter co-author children’s book about understanding money

A kid-friendly introduction to the basics of financial literacy, this illustrated book for children aged 6 to 10 explains what money is for, why it’s important, and how to handle it.

Co-author Milton D. Jones—he also wrote “Don’t Be a Happy Meal for the Banks” (2017)— is a debt-relief attorney, which gives him an informed perspective.

With the debut of his co-author Amber P. Jones, his daughter, the elder Jones stresses that parental involvement in educating children about financial literacy is important.

The Joneses also recommend reading the book aloud. Overall, the information provided here will give young kids a good start.

However, the content may be a little simplistic for older children. The cartoonish, full-color digital illustrations have rather flat, geometric backgrounds and reuse

some images, but they do capture some of the City Market’s bustle.

At the City Market in Savannah, Georgia, two African-American girls, Jai and Kara, are dancing along to the beat of nearby African drummers when the rhythm suddenly changes.

Jai’s father quotes an African proverb that gives this book its title, “When the rhythm of the drumbeat changes, the dance steps must adapt.”

When Jai’s dad gives her $10 to tip the drummers, a conversation arises about money and how kids adapt to their new responsibilities. He takes Jai to meet Jamila Harris, his financial adviser—someone who “helps you decide what to do with the rest of your money” after you “pay for your basic living expenses.”

Jamila says that money is used to pay for goods and services, and can be in cash or “stored in computers like credit cards.”

When Jai gets some money, Harris suggests that Jai should save half and use the rest for fun or to help others. Jai could also consider starting a business, such as a lemonade stand, to earn more money, the adviser says.

Jai’s father says that he’ll help her set up a savings account. He also effectively models some examples of assistance; for example, he makes saving more appealing by giving Jai a beautifully decorated jar as her first piggy bank.

In time, Jai will learn about debt, investment, and taxes. The book closes with motivational quotations.

—Kirkus Reviews

When The Rhythm Of The Drum Beat Changes: A Child’s First Book about Money by Milton D. Jones and Amber P. Jones ABOUT THE BOOK:

A checklist for changing careers

Just how prepared are you to take the leap from one career to another?

JOHN MARSHALL Wells Fargo Advisors

If you’re considering a job or career change, it’s important to do some homework before you make the leap.

Many benefits from your current position could be tied to specific dates and time frames.

Gathering the right information can help you strategically time your exit and set yourself up for greater success. Consider these steps before you resign:

4 Decide if you’d prefer to quit now or wait until you have an offer.

This decision requires you to factor in how unhappy you are in your current position and whether you’re able to live off your savings for a while.

If you’re in a traditional industry, such as sales, it might be better to find a new opportunity while you’re employed.

But if you’re in high-tech, biotech, private equity, or a similar industry, there may be less risk in taking some time off.

4 Check your employment contract and noncompete agreement.

Have a labor attorney review any legal documents you signed when you were hired to evaluate their terms and enforceability.

Some contracts may require you to pay back relocation money, education

grants, or bonuses if you don’t stay for a certain period of time.

Others include “golden handcuffs” that mean you will lose unvested options, restricted stock, deferred compensation, and other benefits upon resignation.

Still others may require waiting for a specified length of time before taking a job with a competitor.

4 Review your retirement benefits.

Check the vesting schedule for your employer’s 401(k) contributions and profit-sharing contributions to see how long you have to work to claim your portion of the money.

Many plans require you be employed on the last day of the plan year to get employer contributions for that year.

You may want to wait until after the plan year ends before you terminate employment so you don’t lose those contributions.

4 Check the terms of stock options, restricted stock, or other forms of non-salary compensation.

You may want to delay your departure if a valuable number of options will vest in the near future.

If you’re already vested, find out if you’re still subject to the same trading

windows and how much time you have to exercise your vested options once you resign. I n many cases, options expire if they aren’t exercised within a certain time frame—typically 90 days after your departure.

4 Manage your health insurance.

If you don’t already have a new position or if your new employer’s health plan has a waiting period, figure out where you will get cover-age to fill the gap.

If your company has 20 or more full time employees, you’ll be able to keep your current plan for up to 18 months after you stop working under the federal law COBRA (you’ll likely have to pay your share and your employer’s share of the premium).

You may want to compare those costs with coverage available on the government’s health insurance marketplace.

Remember, if you live in a state with a health insurance mandate and you can afford but do not purchase coverage, you may have a tax penalty.

4 Spend your FSA accounts.

If you put pretax money into a flexible spending account (FSA), try to spend down the account before you re-

sign. FSAs typically operate on a useit-or-lose-it basis (though you may be able to extend with COBRA).

In contrast, if you have money in a health savings account (HSA), that money is yours to keep.

4 Consider a group life and disability insurance conversion.

If you have life or disability coverage through your employer, you may be able to convert your group policy to an individual policy.

Often you have a short window after your resignation to apply with the insurer for continued coverage.

This can be an especially good option if insurers consider you a risk because of your age or medical condition.

4 Consult a financial advisor.

Whether you’re planning to take some time off or go right into to a new job, an advisor can provide valuable financial guidance through the transition.

This article was written for Wells Fargo Advisors and provided courtesy of John Marshall, Financial Advisor in Washington, D.C. at 202-861-4458.

When disaster strikes, financial preparations are as important as food and batteries

Financial preparedness checklist — steps you can take today:

Arrange for direct deposit of my paycheck, Social Security checks, or other income sources.

Review my insurance coverage.

Review my will and trust documents.

Review IRA and employer plan beneficiary designations.

Discuss a family disaster plan in the event of an unexpected evacuation.

Sign up for Wells Fargo Online® banking with Bill Pay and Wells Fargo Mobile® banking for quick access to my account activity and to pay bills, transfer money, and deposit checks from my mobile phone or tablet1

Review my savings options for emergencies.

Call, stop by, or click today!

250 E Ponce De Leon Ave | Floor 02 Decatur, GA 30030-3440 | (404) 929-4731 wfhm.com/loans/decatur/index-branch.page