PRESENTED BY:

TITLE SPONSORS:

FOUNDED

May 11, 1966

FOUNDER/EDITOR

Ed Clayton

Immortalis Memoria

PUBLISHER/EDITOR

J. Lowell Ware

Immortalis Memoria

The Atlanta Voice honors the life of J. Lowell Ware.

PUBLISHER

Janis Ware jlware@theatlantavoice.com

PRESIDENT/ GENERAL MANAGER

James A. Washington jaws@theatlantavoice.com

EDITOR IN CHIEF

Marshall A. Latimore mlatimore@theatlantavoice.com

MANAGING EDITOR, PUBLISHING

Martel Sharpe info@theatlantavoice.com

MANAGING EDITOR, DIGITAL

Itoro Umontuen iumontuen@theatlantavoice.com

ART DIRECTOR

Vincent Christie vchristie@theatlantavoice.com

DIRECTOR, DIGITAL MEDIA

Jeremiah Long jlong@theatlantavoice.com

DIRECTOR OF VISUALS

Trarell Torrence t.torrence@theatlantavoice.com

ADVERTISING, SALES & CIRCULATION

VP, BUSINESS DEVELOPMENT

Richard Dunn dunn@theatlantavoice

ADVERTISING ADMINISTRATOR

Chia Suggs advertising@theatlantavoice.com

CIRCULATION MANAGER

Terry Milliner SALES

R.D.W. Jackson rdwadman@gmail.com

CONTACT INFORMATION

633 Pryor Street, S.W. Atlanta, GA 30312

Office: 404-524-6426 Fax: 404-527-5464

The Atlanta Voice corrects all errors of fact published in its newspaper. To report an error of fact, send correction to newsroom@theatlantavoice.com.

It’s homebuying season! Despite the economic challenges brought on by the coronavirus, there are people who are able to continue the process to make their goal of homeownership a reality. At the same time, we do realize that for many other families, financial setbacks during this difficult time have forced them to put the goal of owning a home on hold for now. That’s disheartening; however, there’s still an opportunity to learn more about the homeownership process and create a plan to reach your goal. I would like to remind you this Homeownership Month that a setback in your homeownership journey does not necessarily mean you have to abandon your dream of owning a home.

Wells Fargo is again proud to sponsor the Atlanta Voice Homeownership Month supplement, especially this year when things are very different for so many people. We want to take this opportunity to share information inside the publication that will help consumers protect themselves and provide guidance to keep moving toward that homeownership dream even if it has to be delayed for the time being.

For aspiring homeowners who are taking time to evaluate finances and determine the right path forward for homeownership, now is a good time to take advantage of resources

that can help. For example, many organizations provide homebuyer counseling that can provide personalized guidance based on your situation to help you make better decisions for you during your homeownership

journey. Homebuyer counseling is a one-onone session with a HUD-approved counselor who can talk to you about your situation. Activities often include budgeting, identifying credit challenges, guidance to improve credit score, debt reduction strategies and helping to determine affordability. Wells Fargo also helps to offer financial tools that you can navigate on your own like the Hands on Banking® program at HYPERLINK “http:// www.handsonbanking.com” www.handsonbanking.com

At Wells Fargo, we continue the important work of doing what we can to increase homeownership among African Americans. In the third year of our 10-year, $60 billion African-American lending commitment, we have helped more than 60,000 African-American families become homeowners and supplied $8.5 million to support homebuyer education and counseling efforts.

Owning a home remains a dream for many African American families and homeownership is the foundation for wealth building and strengthening our communities. Setbacks don’t mean you have to give up on that goal, but it’s important to use resources that are available to determine the best path forward.

We hope that everyone stays safe and healthy.

Your home can be a place of solace and of joy, a haven to create fun memories with family, an office to work remotely, a gym to burn off steam and recharge. Whatever your reasons for becoming a homebuyer, we’re ready to help you every step of the way through:

•personal support throughout the home financing process

•low down payment options

•online tools and resources for your convenience

No two homes are alike; no two buyers are either. We look forward to working together to help you achieve your unique home financing goals. Let’s connect.

To learn more, call 1-866-875-7068. Or visit wellsfargo.com/mortgage

BY STACY M. BROWN Contributing Writer @StacyBrownMedia

Wells Fargo officials said the bank remains committed to providing the financial access, guidance, and support customers need to focus on theirs and their lovedones well-being.

Since the beginning of the novel coronavirus pandemic, Wells Fargo has suspended residential property foreclosure sales, evictions, and involuntary automobile repossessions.

On a case-by-case basis, the bank offers fee waivers, payment deferrals, and other expanded assistance for credit card, auto, mortgage, small business, and personal lending customers who contact Wells Fargo.

“We have created many options for customers to engage with us,” said Carmen Bell, SVP, Home Lending Servicing Customer Contact and Default Decisioning, Wells Fargo.

“When COVID hit, we recognized the significant potential impact to consumers, we quickly expanded our options to engage,” Bell stated.

The engagement includes creating an easy-to-understand process within Wells Fargo online banking.

“In a prevalent way when you log onto online banking you see an option asking if you need payment relief,” Bell said. “Customers are able to review if payment relief is right for them and have the ability to receive initial 3 months payment suspension online, without having to wait to speak to a Wells Fargo employee.

Customers then receive a confirmation letter in the mail outlining the forbearance. If Wells Fargo has a valid email address, customers will receive a confirmation online.

“We want to provide customers the ability to interact with us how, where and when they choose and so many customers in today’s environment choose to interact digitally,” Bell said.

“When COVID first hit, there was so much uncertainty, customers wanted immediate assurance so that they had peace of mind. We wanted them to be assured that their mortgage payment would

be okay until they knew more out their situation,” she said.

For homeowners fearful of the forbearance process or afraid of late mortgage payments, Bell said it’s crucial they reach out to Wells Fargo or respond through our digital options as early as possible.

“Our goal is to help customers through challenging times and help them maintain homeownership. We do the proactive outbound calling. It’s not a collections type of call; it’s a check-in to see how we can assist them and if COVID has impacted them. We’re here to help you,” Bell noted.

“Some are just fearful of the process, and we try to relieve that fear by having a conversation with them whether that is digital or verbal,” she said.

Many customers weren’t initially sure, how the pandemic, and government officials began might affect them publicly encouraging everyone to call their mortgage provider, Bell said.

“In June, we will be reaching out to customers who received initial 3 months of forbearance that will be expiring to provide them options

to extend forbearance additional 3 months if they still need more time to recover or if they are ready to resume making payments we will provide them options to make up the suspended payments. Bell said Customers will have options based on their specific investor on their loan which They may have the option to do a repayment plan, so taking the three months of missed payments and adding them to your next 3 to 6 months of payments.”

However, Bell added that many might not choose that option because the pandemic has left many in a financial bind.

She said Wells Fargo would follow specific investor guidelines and their own portfolio to make the repayment process easier when customers are ready to resume payments.

Some guidelines will extend the term of the loan by the three months of the forbearance, while others will do a partial claim in which the missed payments are added to the end of the loan as a balloon payment.

“An example of a partial claim would be your payment was $1,000

per month. You’ll then have $3,000 placed in a non-interest bearing account that will be due at the end of your mortgage, such as if you pay off your mortgage or refinance,” Bell said.

Wells Fargo is aware that fraud continues to be a concern for most.

“There is, unfortunately, a lot of fraud in general. I haven’t personally seen any yet in this space although just over the weekend I was out to dinner with a friend who said she got an email from her bank asking her to verify all of her account information. She didn’t respond because she thought it odd that the bank would not have her information anyway. I advised her never to respond to those, always call or login to your secure account,” Bell said.

“We ask customers to be on the lookout for suspicious email or text messages that try to convince you as a consumer to share sensitive information such as username and password or someone who may have impersonated company security or a government agency. We will never ask personal information or login credentials through

email or text,” she said.

“We also have a Wells Fargo Stories piece that provides more information about coronavirus fishing scams. https://stories.wf.com/ beware-coronavirus-phishing-scams/ I would also just add that a consumer’s best avenue is always to engage with us directly or through an approved counselor such as all of the HUD counselors versus thinking that someone who’ll reach out to them will be more of a help than their servicer would.”

Forbearance is a temporary postponement of mortgage payments. It is a form of repayment relief granted by the lender or creditor in lieu of forcing a property into foreclosure. Loan owners and loan insurers may be willing to negotiate forbearance options because the losses generated by property foreclosure typically fall on them.

Georgia Dream provides affordable mortgages and down payment assistance for eligible first-time home buyers, as well as home buyer education to ensure that their investments lead to sustainable homeownership.

This program expands the opportunity for homeownership to the low-to moderate-income market by providing down payment assistance which removes a primary barrier to homeownership: documented source of down payment and closing costs.

The program is funded from tax-exempt mortgage revenue bonds from the Georgia Housing and Finance Authority (GHFA). The longevity of the program is attributed to strategic partnerships with lenders, real estate professionals, bond underwriters, rating agencies, housing counselors and federal agencies.

DCA acts as the secondary market for lenders who want to provide an affordable mortgage product to low- and moderate-income Georgians. These lenders are dedicated to the process and will work with individuals from the application process to the closing.

Georgia Dream is a statewide program available to all first-time home buyers as well as those who have not owned a home in the last three years. The Georgia Dream program provides funding for down payments and closing costs.

Potential home buyers apply with participating lenders for Georgia Dream loans. The loans are insured or guaranteed by FHA, VA, USDA-RD or conventional uninsured loans.

Once the application is submitted to Georgia Dream by the lender, a compliance review will be conducted. Applicants must have a minimum middle credit score of 640, meet income and purchase-price limits, and complete a home-

buyer education course.

Once the compliance review is completed, applicants will be cleared to close. The entire home-buying process is approximately 45-60 days.

The standard loan amount for eligible home buyers is $5,000. In addition, DCA offers a Protectors, Educators and Nurses (PEN) program that provides $7,500 for borrowers who are employed in the following industry types: Public Protection, Education, Health Care or are Active Military. To be eligible for the PEN program, the employer is required to fall within one of the previously mentioned industry. Eligibility is not based upon the borrower’s position or job title.

The second mortgage loan has a zero-percent interest rate; there is never a monthly payment. When you sell or refinance your home, the amount of the loan is absorbed with the current equity and the proceeds helps the next generation of home buyers.

For more information on the Georgia Dream program, visit gadream.com or call 1-800-359-HOME (4663).

Asistencia disponible en Español

can help turn this into a reality.

• Available for eligible first-time home buyers across GA

• Receive $5,000 or $7,500 for down payment assistance

• Obtain home buyer

• Asistencia disponible en Español

HOME ATLANTA 4.0

HOME Atlanta 4.0 gives you 3.5% of theloan amount and you don’t have to pay it back!

Household earning limits:

• $81,060 for 1 person

• $92,680 for 2 people

• $104,300 for 3 people

• $115,780 for 4 people

• $125,160 for 5 people

VINE CITY RENAISSANCE INITIATIVE (VCRI)

VCRI gives you $10,000 towards your down payment and closing costs, and is compatible with a home renovation loan.

Household earning limits:

• $81,060 for 1 person

•

•

•

• $92,680 for 2 people

ATLANTA AFFORDABLE HOMEOWNERSHIP PROGRAM (AAHOP)

Get up to $14,000 for your down payment and closing costs.

Household earning limits:

• $44,650 for 1 person

• $51,000 for 2 people

• $57,400 for 3 people

• $63,750 for 4 people

• $68,850 for 5 people

ATL HOME RENOVATION ADVANTAGE

Get $10,000 towards your down payment and closing costs to use with a home renovation loan.

Household earning limits:

• $69,480 for 1 person

• $79,440 for 2 people

• $89,400 for 3 people

How to Choose a Real Estate Agent

Tuesday, June 16, 2020 from 6-8 PM

Featuring Lynnise N. Knowles and Jerilyn Lewis of Area West Realty RSVP: https://iachoosearealestateagent.eventbrite.com

How to Find Down Payment Assistance Programs

Tuesday, June 23, 2020 from 6-8 PM

Featuring Michele J Lewis and Felicia Neal of Invest Atlanta RSVP: https://iafinddownpaymentassistance eventbrite com

Or join us on the Invest Atlanta Facebook page for a live stream of the webinars on the same dates and times.

INTOWN MORTGAGE ASSISTANCE PROGRAM (IMAP)

Get $10,000 towards your down payment and closing costs.

Household earning limits:

• $69,480 for 1 person

• $79,440 for 2 people

• $89,400 for 3 people

• $99,240 for 4 people

• $107,280 for 5 people

The steps to homeownership with Invest Atlanta Homebuyer Incentives are listed below with links to redirect you to important information on our website.

It’s easy to get started.

1. Complete Invest Atlanta’s Q & A Session online.

gage loan.

4. Find a home located within the city limits of Atlanta. To determine if the property is in the city of Atlanta.

5. Close with a Participating Closing Attorney.

Additional information on each program can be found using the links below.

General Information:

http://www.investatlanta.com/homebuyers/homebuyer-programs-downpayment-assistance

Frequently Asked Questions: http://www.investatlanta.com/homebuyers/additional-resources/faqs

BY LEE ROSS Contributing Writer

One of the greatest deterrents when it comes to keeping a home safe is a home security alarm system. Given an opportunity to select from homes to target, burglars often bypass those outfitted with alarm systems. Several books address not only the need for home security, but also the added benefits to homeowners in installing systems and becoming proactive in protecting their homes. Here are a few of the Atlanta Voice’s favorite.

Fundamentals of Home Security: How to Improve the Security of Your Home by

Anthony Ekanem

It has been reported that burglary and breakin happen almost every 15 seconds of the day. As a result, the chances of your home being at risk of a break-in are greatly increased, and it does not matter where you live in the world. When we talk of a break-in, people think of someone entering their home by

breaking some windows or smashing down doors. Yet, there are things that extend an invitation to burglars and intruders to try at getting into your home. There are many places in the home that are vulnerable to attack by intruders. Therefore, you must put in place a routine that will give intruders and burglars fewer opportunities to attempt a break-in. This book discusses the weak areas in your home security which you should pay attention to, to prevent any kind of break-in from occurring.

Home Security Systems: Home Security Tips Revealed by Joel Maughan

This e-book offers sound advice on how to secure your home –and become security savvy in the process. When you take action to protect your home, your family will have the security they need to survive such harsh worldly conditions. Taking action means to set up alarms, as well as securing your doors, windows, etc. The more security you supply to your home, the better chance you will

have. While there is no such thing as complete home security, there are measures you can take to protect your home.

Security Mom: An Unclassified Guide to Protecting Our Homeland and Your Home by Juliette Kayyem

In her insider’s look at American emergency and disaster management, Kayyem distills years of professional experience into smart, manageable guidelines for keeping your family safe in an unpredictable world. From stocking up on coloring books to stashing duplicate copies of valuable papers out of state, Kayyem’s wisdom does more than just prepare us to survive in an age of mayhem—it empowers us to thrive. Security Mom is an utterly modern tale about the highs and lows of having-it-all parenthood and a candid, sometimes shocking, behindthe-scenes look inside the high-stakes world of national security. Kayyem uses the motto

“don’t scare, prepare!”

Prepared Not Scared: Your Go-To Guide for Staying Safe in An Unsafe World by Bill Stanton Prepared Not Scared, is the ultimate guidebook for protecting yourself and your family from the terrifying dangers surrounding us all. Written by Bill Stanton, arguably the nation’s most recognized and respected expert in personal security and protection, the book extracts more than 500 years of combined security experience and advice from experts in criminology, psychology, military science, self-defense, technology, and emergency preparedness. With each chapter you read, you will increase your chances of protecting yourself from ever becoming a victim of crimes including, child abduction, home invasion, and cybercrime.

BY MARSHA JOHNSON VP, Diverse Segment Market Consultant, Wells Fargo Home Mortgage

Homeownership is important to many Americans – both those buying for the first time and those wanting to make their next home purchase -- but the recent crisis may have many wondering how to proceed.

While the COVID-19 crisis has certainly caused some disruption to the traditional spring buying season, recent market data shows that many buyers and sellers are continuing to move forward with their home buying plans. If you’re a prospective homeowner, here are a few things to think about:

Take stock of your personal homebuying goals and finances.

Did the crisis change what you’re looking for at all? Is a home office more important or a backyard patio? What about your finances? Do you feel secure in your job? Do you already have savings set aside for a down payment as well as for a rainy day fund?

Know what you can afford.

The recent health crisis reinforces the reality of economic ups and downs and the fact that disasters can happen without warning. It reinforces the importance of not overextending yourself in buying; you want to be able to weather any economic cycle. As you consider this, know that a bright spot is that mortgage rates are very low right now, which helps stretch your dollars when you decide to buy.

Start your house hunt from home.

If you’re worried about venturing out, rest easy in knowing you can do a lot of the groundwork from home. As a result of COVID-19, virtual tours, agent-led video walk-throughs, and video chat tours have all been added to the mix of showing homes. Lenders are available to serve you remotely, too, and are always available to have phone conversations about the lending process.

Understand your down payment options.

There are still financing options available that don’t require you to put 20 percent down. Low down-payment options include our own yourFirst Mortgage® program and

JOHNSON, VP, Diverse Segment Market Consultant,

government programs like VA and FHA. How much you put down is a financial decision to weigh as you look at your own finances and personal situation. It’s important to note that putting more down can reduce your monthly payments, which can free up dollars for other parts of your budget, including savings.

Double down on your rainy day fund.

t’s always been a good idea to have a little to fall back on. Owning a home means you’ll have expenses for repairs and updates. The economic uncertainty caused by the COVID-19 crisis reinforces the importance of having money to fall back on if you have an unexpected expense or loss in income.

Just like shopping for your perfect house, you can apply for a home loan from your kitchen; you never really need to step into a bank. Many tasks can be handled online, from starting the loan applications to signing disclosures and uploading needed documents during the loan process.

The current crisis has many Americans reflecting on their living spaces and thinking about their long-term financial goals. While no one knows exactly what will happen in the economy, if you are weighing whether buying is right for you, take a minute to focus in on your own unique goals, opportunities and circumstances and make the best decision for you.

In challenging times, many people working together can do the greatest good. It’s an honor to be a member of this brave community, where so many give so much, every day, to keep all of us hopeful, safe, and strong.

BY STACY M. BROWN Contributing Writer @StacyBrownMedia

The coronavirus has put a financial strain on many families and businesses. The government, financial institutions and other organizations are rallying to support those in need. As more support is offered to Americans and businesses that are struggling financially, the threat of fraud is increasing.

It is important for consumers and business owners to pay close attention to any communication they receive regarding COVID-19, especially as it relates to financial assistance. Recognizing scams and knowing how to avoid them will help protect you from fraud.

Wells Fargo is proactively advancing our security, and the company continues to invest in account safety measures and customer education to help consumers and businesses during this time. Here are a few tips that can help keep your accounts and information secure.

Know what you can afford.

The IRS will not call, email, or text you asking to verify or provide your financial in-

formation to get your stimulus checks faster. If you receive an unexpected request that appears to be from the IRS, do not respond, click on links or open attachments.

Also, be suspicious of any communication from an organization that claims it can help put a rush on your payment.

To learn more about economic impact payments, including eligibility and payment amounts, visit IRS.gov/coronavirus.

Beware of unexpected requests and offers for financial assistance

Look out for emails and text messages that include an urgent request for you to update your information, verify your identity or take advantage of a special offer. Fraudulent financial aid and loan offers are also common on social media. You may be prompted to call a phone number, sign on to a spoofed website, or respond with personal or account information.

Be sure to look closely at the email address or text message for any COVID-19 communication you receive. On the surface, it may appear to be from a reputable or trusted source

like your financial institution or a major nonprofit, but if the sender’s email domain looks different from other communications (e.g. “wells-fargo.info” instead of “wellsfargo.com”), then it could be a scam. For text messages, be cautious when receiving a text from an unknown phone number. Text scams may contain unusual language or text treatments, ID numbers, all caps or punctuation like exclamation points.

If you receive a suspicious request that appears to be from your bank or other legitimate company, do not respond, click on links or open attachments. Call the number on the company’s website or the back of your debit or credit card to verify the request.

Verify a company or charity before opening your wallet

Other popular schemes include medical supply scams and fraudulent donation sites that impersonate a company, charity, or government agency to convince you to make purchases or donations on spoofed websites or do business with a phony vendor. Do your research to help ensure you are working with a legitimate vendor or organization.

BRIGITTE KILLINGS, VP, Divisional Diverse Segments Manager, East Coast, Wells Fargo Home Mortgage

Running a small business? Take note of these additional tips

First, be sure to reconcile accounts daily to detect suspicious activity.

Make sure to verify all account changes, including changes to payment instructions from vendors. If you receive a request to change payment details such as bank account or invoice information, verify the request using a different method of contact to make sure it’s authentic. For example, if the vendor contacts you by email, confirm the information by phone. Be sure to use the information you have for the contact on file, not the contact information contained in the request you received.

If you detect it, report it.

For suspicious requests that claim to be from Wells Fargo: forward the email or send an email with the text message copy (no screenshots) to reportphish@wellsfargo.com.

You also can report scams to the Federal Trade Commission at HYPERLINK “http:// www.ftc.gov/complaint” www.ftc.gov/complaint.

BY ALLEN UPCHURCH President and CEO Credit Union of Atlanta

Now more than ever Americans are being reminded of the many racial and socioeconomic disparities prevalent in our nation. Disparity of homeownership is one of them. There continues to be a significant racial homeownership gap across the U.S. as well as in Atlanta, however there are tools available to help consumers of all races achieve the American dream of home ownership.

According to a recent report published by the National Association of REALTORS®, the homeownership rate for non-Hispanic white Americans was consistently above 71% from 2016 to 2019 while the rate for black Americans was just above 41% (a rate that is virtually unchanged from 50 years ago). For Hispanic Americans, the homeownership rate held above 45%, and for Asian Americans, just above 53%. Disparity is also evident when you look at median household income levels by race. A report published by the U.S. Census Bureau in 2019 shows the real median income for Asian households is $87,194, non-Hispanic white households is $70,642, Hispanic households is $51,450 and African American households is $41,692.

Specific to the metro Atlanta area, homeownership among the city’s total population at 45.4% is lower than the national average of 63.9% and although 50.7% of the city’s population is black or African American, this population’s homeownership rate sits at just 24%. In fact, Atlanta ranked number 7 among 50 of the largest U.S. cities with the lowest percentage of black homeowners in a study by The Lending Tree.

Since homeownership continues to be one of the principal ways consumers can build wealth, these statistics show that many consumers – many Atlantans – are at a sincere disadvantage when it comes to economic mobility. A prosperous city like Atlanta depends on leadership, organizations and tools that stimulate economic development for its residents. The good news is, there are resources available to help propel more Atlantans toward home ownership...more than some might think.

One primary issue is many consumers, whether because of low income, credit status, current debt load, or another reason, do not believe they can obtain mortgage financing, but there are opportunities for everyone. From financial counseling geared toward debt management and credit score improvement to special financing options for first-time homebuyers, low down payment programs, veteran loans and homebuyer education programs…there are

ALLEN UPCHURCH, President and CEO, Credit Union of Atlanta

solutions available. In addition, there are specific Community Development Financial Institutions (CDFI), designated by the U.S. Treasury, committed to delivering responsible, affordable lending to help low-income, low-wealth and other disadvantaged people and communities join the economic mainstream and start the journey to build wealth. Programs and organizations are available to help, consumers just need to know where to look for assistance.

As we celebrate National Homeownership Month in June, there is much work that still needs to be done to close – even narrow– the racial disparity gap related to homeownership in Atlanta and across the nation. However by focusing on the tools available today to help consumers in underserved areas access home ownership, we can begin to nudge the needle. With home loan rates at unprecedented levels due to the pandemic and associated financial crisis, more consumers should be able to access funding to achieve the great American dream.

If you’re shopping for a home, consider reaching out to a CDFI to get started. Every single consumer’s path to homeownership looks different. Whether you’re able to get into a home right away, or need to do some preparation to get there, you too can become a homeowner and help Atlanta thrive.

Allen Upchurch is President and CEO of Credit Union of Atlanta, a not-for-profit financial institution, a designated Minority Depository Institution and Community Development Financial Institution (CDFI) aimed at providing affordable financial solutions to residents of the metro Atlanta community.

Quest Communities, founded in 2001, has as its mission “to develop affordable housing and provide needs-based community services to enhance the quality of life for underserved individuals and families.” Quest provides services for homeless, very low income, and marginally housed persons on Atlanta’s Westside. Comprehensive supportive services coupled with stable housing is essential for client healing and self-sufficiency.

Quest’s current portfolio includes 4 commercial properties, 390 multi-family units, and 14 single-family homes. As a nonprofit developer, Quest plans to add 452 additional affordable housing units on Atlanta’s Westside over the next three years totaling nearly $100 million. Also, Quest currently manages the personal finances of well over 500 clients throughout the state of Georgia for those who receive Social Security and/or Veteran Administration benefits.

In 2019, Quest was ranked #1 in quality among all other Atlanta homeless service providers. Although Quest is known as an affordable housing developer, we are rooted in service and forged by a deep connection to our residents. We recognize that the more our residents feel valued and supported, the more self-sufficient they become. Quest’s quality is the result of impactful intentions, humbling efforts, and ingenious skills. We research and execute evidenced-based practices that will enhance the residential experi-

ences at Quest.

Much of Quest’s diligent work from the preceding three years has culminated in a groundswell of activity that brought forth several projects converging into manifestation simultaneously. Quest currently has five affordable housing projects under construction and four new projects in pre-development. This equates to $42 million in total development cost in progress and $10 million of construction work in place.

One of the core aspects of the work performed by Quest is to promote the concept of self-sufficiency among our residents. The ultimate goal is for our residents to acquire a single-family home. Homeownership often represents a gateway to generational wealth. The privilege of buying and maintaining a home is a major milestone for many Americans. However, some countless individuals and families are unable to take advantage of the American dream of homeownership for a variety of reasons, namely the inability to

afford even a modest dwelling. This is particularly relevant in metro Atlanta. The City of Atlanta has the highest income disparity of any other major US city. Quest develops affordable housing for underserved individuals and families and reduces barriers to economic mobility. Quest revitalizes, not only the communities we serve but the people who reside there. Quest owns and operates affordable housing units that serve as vehicles for anti-displacement and resident stabilization. We strive to build stable and vibrant communities for those who have been disenfranchised. Our approach positions communities and residents to break the cycle of generational poverty.

Quest will complete the construction of the Quest Westside Impact Center (QWIC) in summer 2020. This 30,000 sq. ft. facility will offer two pillars of community development – affordable housing and economic inclusion. Additional programs and services will include a fresh food market, flexible office space, community meeting space, and community collective impact spaces.

Since Quest has already completed the construction of a workforce development facility across the street from the planned QWIC, we will integrate housing, job readiness/placement, and economic inclusion into a seamless service delivery system. For instance, a resident who participates in a job training program at Westside Works will also receive financial management classes from On the Rise Financial Center and will be eligible for affordable housing through Quest.

Also, Quest is currently constructing Quest Commons West, a 53-unit multi-family, affordable housing facility. The complex is located immediately behind the QWIC. Quest has partnered with Columbia Residential to co-develop this project. Construction is scheduled to be completed in December 2020. Both projects represent a $25 million investment in the Vine City neighborhood on Atlanta’s Westside.

Finally, Quest is very excited to introduce our newest health and housing model for vulnerable populations positioned as a solution to this COVID-19 Pandemic. We all were asked to stay home, quarantine yourself if you experience symptoms, educate your children from home, and if still employed to work remotely but remember there is a homeless population that does not have a place to call home. So, what happens to them? Quest is working with local partners to develop a site on Atlanta’s Westside to address a seamless supportive affordable environment for those that are without. Follow us for more details.

If you’re interested in volunteering at Quest or making a donation, please visit our website at www.questcommunities.org

BY LEE ROSS

Contributing Writer

1. Don’t provide places for thieves to hide Trim trees and bushes that may give someone a place to hide or unnoticeable access to your windows. Trim any shrubs that are high enough to block a window or provide covering to those attempting to surveil your home.

2. Light your property with motion detectors or entry lighting to ensure you can see clearly those nooks and crannies that are normally very dark and may allow a thief access to your home under the cover of darkness.

3. Don’t let thieves know you are not home Years ago many Black families placed announcements in Black newspapers about their vacation plans – but also made it clear who from the neighborhood would be house-sitting in their absence. Today, through social media, many of announce we our plans and document it from the time we lock the front door until our planes touch down a week later. In the process, we give home invaders a trusty guide to our movements and essentially announce our homes are primed for break in. Save the vacation snaps until your return, have a friend housesit, and / or entrust a friend or neighbor to pick up mail or check on the house daily.

4. Install a home alarm system Alarms may deter burglaries, but also provide the added advantage of alerting neighbors and bringing law enforcement to your home quickly. Those systems that offer surveillance as well as the alarm, have been amazing at helping to track down would-be robbers by capturing their images for law enforcement.

5. Take precautions to protect windows Ensure that windows have working locks and that windows are screened for extra protection. Also, if purchasing new windows for your home, invest in shatterproof glass to prevent invaders from breaking windows to gain entry. For the more frugal, consider adding a security film to windows. Security window films are used to enhance the safety of regular glass by strengthening it. Security films for windows are used to help protect against break-ins, vandalism, accidents, terrorist bomb attacks, and natural disasters. This will prevent the glass from shattering upon breaking and may deter thieves from continuing their attempt to break in.

6. Secure sliding glass doors Sliding glass doors have incredibly flimsy locks. A thief can easily pop them in an instant, giving quick access to your home. Installing a

security bar for sliding doors would make gaining access to your home more difficult. This measure of protection is a must-have for all sliding doors and windows.

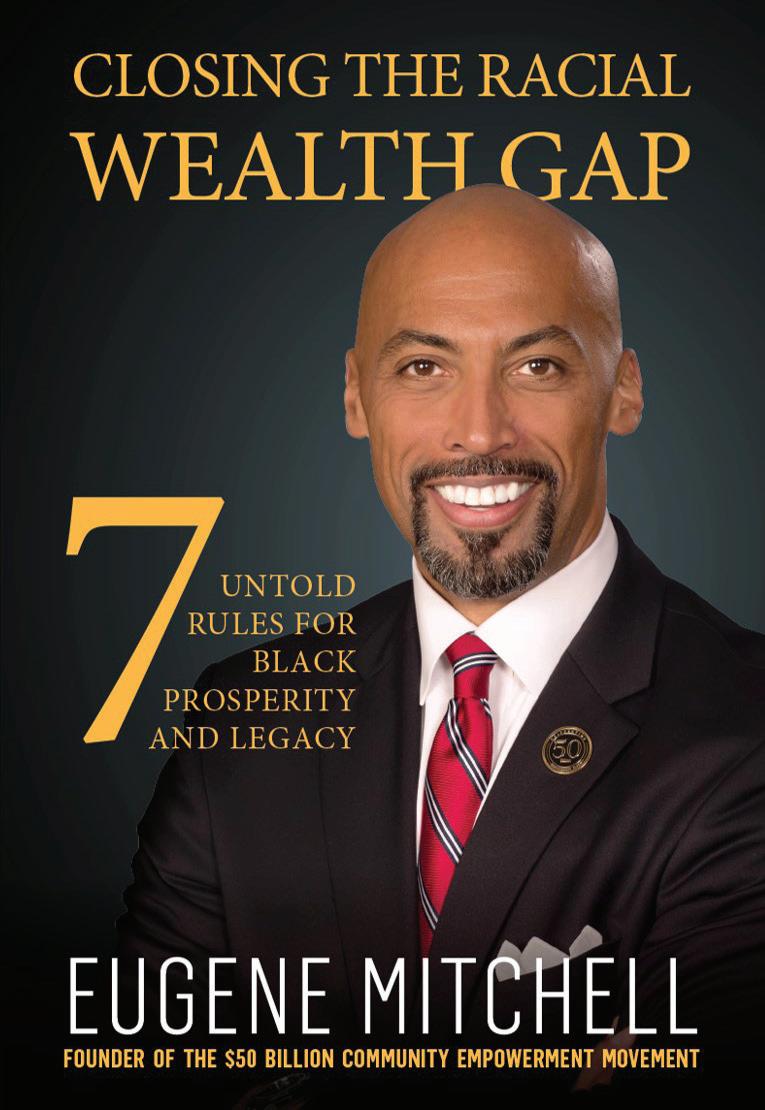

A major question for many in our communities is: How can I obtain the $50–$100,000, or even $250,000, down payment to buy a home? Since the answer to this eludes many of us, it delays or even keeps us from ever acquiring one of the greatest financial assets for families. In doing so we miss the opportunity to take advantage of home-equity appreciation—which can be tapped for cash; tax advantages; and a home as a cherished source of family experiences. There’s also pride that

comes from ownership and the creation of a legacy that can be passed from generation to generation.

I have an answer to the down payment dilemma that so many in our communities face: It’s an interesting, creative strategy that I observed other, non-Black communities using. I’m here to share it so more in our communities can do so as well!

I witnessed this method at a Fortune 100 company where, over my 17-year-career and vantage point as a senior executive, I saw how families (from diverse racial backgrounds) creatively used funds from their insurance plans for lump-sum home down payments. The method may sound simple, but its impact is vast.

The best example I like to share is from one family with 20 members who took out a million dollars in life insurance on their two eldest family members, and the other 18 pooled their funds to pay the premiums. They didn’t view this approach as profiting off of the deaths of these two seniors in their household, but as a way to honor them as the family matriarch and patriarch whose policies created an intergenerational financial legacy. They used funds from the $2 million face

values of those policies to pay for the college educations of each of the grandchildren; as down payments for homes; and as startup capital for new businesses as the children grew. This forward thinking and planning ensured the family’s financial stability, growth opportunities, and self-sufficiency.

Think about that: That meant that the youngest family members didn’t have to worry about student loans anchoring them down before they even got started on their life journeys. Imagine being able to put down 20% on a property in a gentrifying neighborhood—perhaps a brownstone or multi-unit property that can generate rental income immediately.

The ability to put down a 20% down payment or higher also means eliminating the PMI (private mortgage insurance) mandatory for buyers who can only do deposits under 20%. With a $2 million policy, a family could purchase not one but multiple units and place them into a family trust. Think about being able to start a business with the financial backing of your own family—without bank approval processes, racial biases, or financial collateral.

For the last 20 years I’ve explored innovative financing methods (primarily leveraging life insurance) and provided tips, tools, and strategies for wealth building in Black communities. The financial services company I worked at for most of my career has been around for 175 years, and I discovered that many families (in non-Black communities) knew how to take advantage of the strategy I described since the inception of my former employer’s firm.

This enabled families and communities who were “in the know” to stay ahead of the game. However, this approach was foreign to many African-American families. This troubled me. Now you know this strategy, too—if you didn’t before! In our communities we can’t continue to think that we can simply use education and hard work alone to close the wealth gap. We need to employ these types of deceptively simple, yet savvy, approaches as well.

Creating generational wealth requires a different financial-planning approach, so both current and future generations have access to financing and funding once hidden from us—and at certain points in history even denied to us. I call this strategy: funding your own inheritance.

My sister and I shared the insurance concept I described with our parents, on multiple occasions. Because it was a new idea and way of thinking, we knew it would take some time to break through. Eventually our parents acquiesced, allowing my sister and me to acquire a smaller version of the policy described above, to benefit their grandchildren

and great-grandchildren.

We made it clear to our parents that my sister and I already have our educations and houses, so it’s not about us. What we do know is that there are eight children between me and my sister, and five grandchildren, and without this plan we really wondered how we would be able to afford to put all of them through school?

We also wouldn’t be in a position to help them with down payments for their homes (which parents in other communities frequently do). Nor could we encourage them to be entrepreneurs on the level we’d always dreamed they could—and be able to provide seed money. Those insurance policies enabled us to do that.

The wealthy plan for generations. Can you imagine if your grandparents had started doing this? It’s not a problem if they didn’t because, like my parents, most likely: they simply didn’t know. Now that you know, like my sister and me, would you like to explore this concept?

You can find more tips, tools, and strategies like this in my book, Closing the Racial Wealth Gap: 7 Untold Rules for Black Prosperity and Legacy I have a team of advisors ready to assist if you want more information on this

Even when homeowners think they live in a safe neighborhood, they could be at risk for a burglary. If they find their possessions missing or damaged after a burglary, homeowners could file a claim with their insurance company. However, after experiencing a home theft several times, homeowners could see their insurance premiums rise. By installing a home security system with burglar alarms, homeowners can deter thieves from breaking into their homes. Ninety percent of convicted burglars said they would avoid homes with alarm systems. With the frequency of home theft, homeowners should consider whether a security system is worth it, not only to protect their belongings, but also save on insurance.

If you install a monitored home alarm, there is less of a chance that you will be robbed and, therefore, that your insurance company will have to shell out thousands of dollars to cover your losses. Reduced risk for

your provider means a reduced premium for you.

The risk-cost benefits of an alarm system don’t stop with crime reduction, either. There’s another reason for that insurance discount: fire safety. Modern alarm systems also help protect against fire damage, one of the costliest claims for insurance companies. In fact, fire and lightning claims account for almost 10 times the number of insurance claims of theft and burglary. So, protecting your home from fire damage means even less risk for your insurance company – and the reason for that serious discount on your homeowners’ insurance.

Here are five ways to reduce insurance costs with a security system:

1. Boost home safety

Insurers may provide a discount on insurance premiums if homeowners have a security system, which can help increase home safety. The decrease in incidents that could

result in damaged properties could show insurance companies that homeowners are less of a risk and could qualify them for discounts.

2. Save up to 20 percent on insurance premiums

-Homeowners could see their insurance premiums drop between 15 and 20 percent if they install a comprehensive home security system, according to the Insurance Information Institute. Not only can they reduce their insurance costs, they can also save money on buying these security systems if they ask about discounts.

3. Lower risk of cost hikes

To avoid higher insurance costs, homeowners should make sure that they carefully read their policies. Home insurance companies may decide to increase home insurance in case a burglary occurs, according to The Simple Dollar.

4. Reduce theft claim quota

Security systems can also help save neighbors money by limiting the total theft claim quota. The Simple Dollar recommended homeowners ensure their neighborhood has not reached their theft claim quota, or the number of thefts within a certain area.

5. Install systems with other safety features

Additionally, homeowners can look for other safety features to lower their insurance premiums. These include smoke alarms and deadbolts. The combination of a security system and other ways to protect their home could save them the stress of worrying about safety and money.

CoverHound specializes in online search tools to save on homeowners’ insurance.

To learn more, call 1-866-875-7068. Or visit wellsfargo.com/mortgage Home is where the heart is.

A home is so much more than brick and mortar. It can feel like the heartbeat of your community. It says, “I belong here.” We’re invested in igniting that spirit. understand that successful homeownership helps make individuals, families, and communities stronger. That’s why we’re working hard to support homebuyers by preparing them to become homeowners. Let’s keep our communities growing strong together.