14 minute read

Titanium Industry Asks: Is it Time for an Aerospace Ascent, or Another Nosedive?

By Tom Captain

(This is the fourth in a series of annual guest articles by Tom Captain, offering his insight and observations on the commercial aerospace industry.)

Just when it looked like the aerospace industry was overcoming the setbacks from the Covid-19 pandemic, along comes the labor shortages, supply chain crunch, high fuel costs, war in Ukraine, and high inflation. Will the predicted recession dash any hopes of a recovery in the industry? Let’s look at what has happened since we wrote in August 2021 about the industry’s prospects for recovery, and offer some new predictions.

Prior prediction

In August 2021, in Part Three of this series, we forecasted aircraft sales and production to return to its prepandemic levels by early 2023, which is now roughly six to nine months away. That would mean that industry original equipment manufacturers (OEMs) would sell about 1,800 large commercial aircraft annually and production would return to about 1,600 aircraft per year. Is that prediction still on course or will we see another nosedive or something less severe?

The pandemic and its impact

As of this writing, the global official death toll from the pandemic is estimated by the World Health Organization (WHO) to be 6.5 million, on a base of 550 million infection cases, but others indicate the impact is much larger. However, with

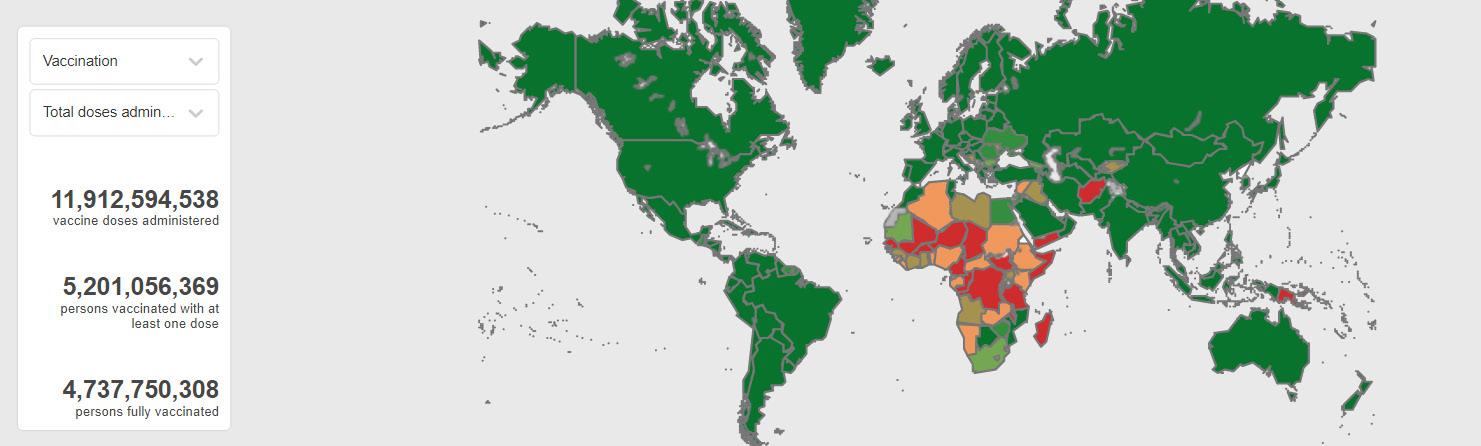

increased levels of vaccinations, the death toll has significantly been reduced. It’s estimated that 5.2 billion people have been administered at least one vaccination dose, almost three-quarters of all humanity, and recent reports indicated that vaccinations have been responsible for averting another 20 million deaths. This is a remarkable achievement of science and technology. The following WHO Tom Captain chart illustrates the remarkable rate of vaccination globally, a key to recovery of the airline industry and their suppliers:

*Note: green are highly vaccinated countries; red are low vaccinated countries

Since our writings of last August, the airline industry has staged quite a rebound from a pandemic low of 10 percent of normal flight operations, being 2019. Average load factors are increasing dramatically, especially in the domestic markets approaching pre-pandemic levels in Europe and the US, but less so in the Asia Pacific region. In 2021 according to IATA, global domestic traveler numbers were 61 percent of 2019 levels. International travel was 27 percent of 2019 levels.

Impact on commercial aircraft production levels

The impact of the pandemic has been existential, not only due to the freefall in demand for air travel, cancellation of aircraft orders, but also due to the Boeing 737 MAX crashes and its aftermath, and production challenges on the 787 program. Never in the history of commercial jet powered commercial aircraft has the industry experienced the magnitude of its circumstances. The following chart illustrates the dramatic fall in production in 2020 and 2021, especially when compared to 2016 thru 2018. Also note that the industry order activity also experienced a steep nosedive 2019 thru 2021, with a nascent recovery starting in 2021.

Year 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Net Aircraft Orders 2,036 2,858 2,888 1,848 1,078 2,021 1,640 681 - 203 1,042 Production 1,189 1,274 1,352 1,397 1,436 1,481 1,606 1,243 723 951 YOY Production Change 17.6% 7.1% 6.1% 3.3% 2.8% 3.1% 8.4% -22.6% -41.8% 31.5% *Note- green numbers are peak order and production years; red are pandemic low years

Recovery, albeit halting, of commercial aircraft production in 2021 and the first half of 2022 is due to recovery of air travel demand. This has been largely due to the progressive removal of restrictions by governments, as more people are vaccinated, infection rates decrease and the realization of the economic and social hardship damage that is caused by travel restrictions. Although masks are still required in many markets, additional testing requirements have been removed for international travel by many countries. Air travel is on the rebound.

Labor problems

Load factors may be up, but passenger counts aren’t as high as would be expected in a rebound. This is partly due to cancelled flights and reduced operating capacity of airlines. Much of this is due to the shortage of available pilots and operations personnel. During the pandemic, many pilots, and flight crew were furloughed due to the significantly reduced demand for travel during the pandemic. Some simply retired by taking advantage of buy-out packages. Also, many aspects of the labor market changed, such as working from home, “quitting,” sitting out and people moving to remote areas due to their ability to work from anywhere – the online “Zoom” effect.

This has had a large impact on personnel available to fly those commercial aircraft, resulting in many routes being temporarily curtailed or worse yet, flights being cancelled. Coming back from furloughs is tough. Pilots are required to maintain currency in competence to fly those aircraft, and required recurrent training after returning from furlough, which takes time to become recertified.

Who would have thought within the span of 2 years, the industry could go from a mass furlough scenario to one where airlines are paying hiring bonuses due to the shortage of staff. As of mid-year 2022, cancellations and delays have become the norm for major US based airlines, with a sampling of data below:

Delays and Cancellations - June 2022

Airline Delays Cancellations

Southwest 34,250 2,687

United 8,440 189

Delta 11,057 106

American 20,418 2,423 situation may not improve in the short term, as witnessed in some recent headlines: • “American Airlines CEO says it will hike pay for 14,000 pilots even higher than originally proposed, as the industry faces a crippling labor shortage” • “Summer travel might not take off as expected due to ‘challenging’ labor shortages, pilot warns” • “Pilot shortages add to U.S. travel chaos as airlines struggle to meet demand”

Supply chain problems

In general, aerospace supply chain companies also had labor shortage problems, due to similar causes cited above. This has led to operating capacity constraints on aerospace suppliers, which caused a significant and unprecedented impact on the global aerospace supply chain. The gradual return to service of aircraft over the last two years has resulted in an uneven return of the aerospace supply chain, due to shortages, labor adjustments, training issues and loss of “corporate memory.”

For the maintenance, repair and overhaul (MRO) industry, the pandemic-induced fall in flight hours reduced demand for parts during the last two years. With so many aircraft grounded, airlines swapped

out aircraft and green-time engines to avoid maintenance. Purchase of new parts was stopped or delayed by aircraft operators and MRO organizations to reduce costs, which severely impacted the aftermarket supply chain of sales revenue. The starvation, albeit temporary, of the commercial aerospace supply chain industry serving the OEM and aftermarket business, created a void, and it created a delay to reenergize the industry in order to restore its functionality.

Ukraine war

However, the more insidious and potentially existential threat to the industry is the Ukraine war and its impact on titanium supplies. The escalating conflict between Russia and Ukraine is fueling concerns in the aerospace supply chain, with key producers of raw materials, metal and alloy located on both sides of the border serving global customers. Sanctions and embargoes could threaten a substantial portion of the titanium sponge market. VSMPOAvisma based in Russia, is the largest titanium producer in the world, with an operating capacity of 34,000 tons per year, with a 20-percent global market-share. They supply a large portion of titanium used by aircraft OEMs in their products.

However, engine makers for Boeing Co. and Airbus SE jets are working to diversify sources of titanium away from major suppliers in Russia, as the conflict in Ukraine threatens access to the metal needed to make critical plane equipment. Suppliers and OEMs are increasing their backstock of materials, investigating alternative sources and utilizing advanced technologies.

Fuel costs

Russia’s invasion of Ukraine is a major reason that aircraft fuel prices have increased. Russia is one of the largest oil exporters globally. In December it produced an estimated eight million barrels of oil and other petroleum products for global markets, five million of them as crude oil, however, very little of that went to the United States. An estimated 60 percent of Russian oil in 2021 went to Europe and 20 percent went to China. However, a key reason for high oil prices is that oil is a global commodity and is priced accordingly. Thus, the loss of Russian oil impacts prices globally, no matter its location of use.

Other reasons for the crude oil price spike include the ferocious rebound of demand. Oil prices plunged when stay-at-home restrictions crushed demand in the second quarter of 2020, when crude was trading very low. As a response, OPEC members and Russia, drastically cut crude oil production to support prices. Demand returned sooner than expected, but they kept crude oil production low creating an imbalance.

During the pandemic, a factor keeping oil prices low was the surge of Covid cases, and the especially strict lockdown rules in China. Given its significant global thirst for oil, China’s significant drop in demand for oil contributed to low global prices. As Covid started to retreat, lockdowns are being lifted in major cities such as Shanghai. A rebound in oil demand in China, without the aforementioned

Supply chain shortages of titanium will continue to be an issue, as regulations regarding the use of restricted materials from foreign suppliers may become a problem, with potential further restrictions from Russia. OEMs and engine manufacturers will have implemented adequate risk-mitigation measures such as alternate titanium sources to meet increased demand for aircraft production. The aerospace industry is resilient and will not only survive but eventually thrive on the demand for air travel. That is reason for hope.

increased supply, has contributed to the oil price increases.

However, to put this in perspective, the price of oil has significantly increased of late, but on an inflation adjusted basis, we are returning to the levels experienced from 2014 thru the early 2020, before the pandemic started. Despite this, increased fuel costs are certainly impacting the costs for flying and airlines globally are increasing passenger fares to recover this increase in costs. On April 24, 2020, the price of a barrel of West Texas Intermediate Crude Oil (WTI) was $20.89. On June 24, 2022, the price of a barrel of WTI is $107.62 for a whopping 515-percent increase.

A recent cause for optimism is the nascent trend in reduced oil prices in the mid and late summer, caused by lowered demand, which in turn are caused by high prices at the pump, recession worries and increased interest rates.

Inflation and Potential for Recession

Notwithstanding the above discussion regarding increases in labor pay and oil prices, there is a general imbalance of supply and demand throughout the UK, United States and global economies. This in turn is causing generalized economic inflation in many countries. In the United Kingdom, the inflation rate as of June 2022 was a whopping 9.4 percent. In the United States, during the same period, the annual inflation rate was 9.1 percent, the highest monthly rate since 1981. To put this in perspective, the average CPI index inflation rate from 2015-2021 was 3.01 percent annually. The following chart illustrates the dramatic increase in inflation rates in just the last two years:

Inflation is not a theoretical concept, but a real one for the aerospace industry. The prices of labor rates for pilots, mechanics, and suppliers are rising. The prices of new and used aircraft, MRO services, supply chain parts and systems are rising. The price of jet fuel is rising. This in turn translates into higher prices for airline tickets. This is turn is likely to moderate demand for travel. As demand is reduced not only for airline travel but for goods and services in the general economy, there is concern that we will experience a recession in the near term. As the U.S. Federal Reserve and various central banks globally come to terms with how high and how soon to increase interest rates, there will be a careful balancing act without going too far and tipping the global economy into recession. Time will tell if demand and supply can reach equilibrium in a non-destructive manner.

New predictions

Pilot shortages should be largely addressed by early to mid-2023, with completion of recurrent training for furloughed pilots and entry to the workforce by student pilots undergoing flight school training. Increased pilot pay should draw others such as from the military, general aviation and private pilots to the industry. This in turn should reduce cancelled and delayed flights, as well as open up routes that have been cancelled. Recent headlines underscore the efforts underway: • “United opens flight school, airlines find creative solutions as industry faces looming pilot shortage - United projects the academy to recruit 5000 pilots by 2030” • “Delta tries to fix the national pilot shortage and accelerate training using private charter company in new partnership” • “Airlines Are Rushing to Train

New Pilots After Pandemic-

Caused Shortage” • The Montreal-based International

Air Transport Association (IATA) predicts air travel to rebound almost fully by the end of 2023 and grow beyond pre-pandemic levels by 2024, as illustrated in the following chart:

Commercial Air Traffic Difference from 2019, a "normal" year

Overall travel Domestic travel International travel 2019

100%

100%

100% 2021

47%

61%

27% 2022

83%

93%

69% 2023

94%

103%

82% 2024

103%

111%

92%

Supply chain shortages of titanium will continue to be an issue, as regulations regarding the use of restricted materials from foreign suppliers may become a problem, with potential further restrictions from Russia. Shortages of machined parts, subassemblies and systems will start to be alleviated as the industry works out its own labor shortages. Orders for materials should improve as the supply chain network works toward supply/demand equilibrium. OEMs and engine manufacturers will have implemented adequate risk mitigation measures such as alternate titanium sources, and increased back stock in place to meet increased demand for aircraft production. Thus we expect that many of the key supply bottlenecks that impact aircraft OEM production progress will get back to a “new normal” in the late 2023 and early 2024 timeframe.

We predict domestic commercial airline travel to improve to 90 percent of 2019 levels by yearend 2022 and international commercial airline travel to improve to 70 percent by year-end 2022. We predict globally that over four billion passengers will be flying annually by late 2024 and early 2025, over nine trillion revenue passenger kilometers (RPKs) will be flown, with over 100,000 flights taking to the skies globally per day. All this again would return the industry to 2019 levels or better - back to the “new normal.” We expect by 2025 to see global aircraft OEMs to produce over 1,600 aircraft annually. Thus, it will have taken 5 years for the industry to recover to the 2019 levels of economic activity.

Bottom Line

With the “interruptions” as described above to the recovery from the pandemic, the aerospace industry is facing a delay, not a backward step. We do not foresee a “nosedive”, but rather a halting and delayed recovery, moving in a positive direction. After all, there is an insatiable appetite for family, business and leisure passenger travel, and for air cargo due to the internet shopping and “Amazon” effect. The pandemic itself was an interruption, as was the subsequent fuel price increases and labor shortages, not to mention the Ukraine war, and production delays on the 737 MAX and the 787 programs, plus the possibility of a recession in late 2022 and early 2023. The industry is resilient and will not only survive, but eventually thrive on the demand for air travel—it always has. That is reason for hope. n (Editor’s note: Tom Captain is the managing director of Captain Global Advisory, LLC, headquartered in Mercer Island, WA, and is a 40-year industry veteran and expert in the aerospace, defense and space sector. He is the retired vice chairman of a Big Four consultancy where he led their global industry practice. Captain currently serves on the boards of several industry-related organizations.)