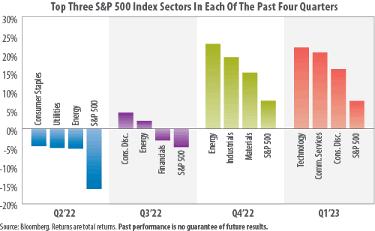

Unfortunately, banks have demonstrated an uncanny propensity to act dumb on a fairly regular basis throughout history. Financial crises and bank panics have been taking place since the days of the Roman Empire. Records of financial panics stretch as far back as 33 A.D. during the reign of Emperor Tiberius. Civilization may have evolved, but human nature remains stubbornly unchanged.

Interestingly, every financial crisis possesses eerily similar characteristics. While each one contains different characters, the basic plot and ending is almost always the same. They begin with acts of greed or stupidity which lead to a crisis of confidence and trust. They end with a restructuring of the industry driven by the size and nature of the crisis. Eventually the bad behavior, or policies, which caused the crisis change (for a while!), and lost confidence and trust is restored.

Fast forward from 33 A.D. to March 12, 2023, when the collapse of Silicon Valley Bank (SVB), the 16th largest bank in the country, set in motion our most recent banking crisis.

In classic, and at least somewhat predictable bank panic fashion, fear first spread close to home with the fall of New York-based Signature Bank and an emergency rescue of SVB’s west coast neighbor First Republic Bank. The share prices of many small and even regional banks have fallen by 20 to 50%. The crises then

went global as struggling Credit Suisse was acquired by its rival UBS in an emergency deal brokered by the Swiss government.

It would take another 20 pages for me to describe the details and causes of these bank failures and rescues. The stories are still unfolding, but it looks like a toxic combination of bad government policies and oversight, corporate greed, blatant stupidity, and overall failure to identify and manage risk. As Warren Buffett might summarize it, a lot of people got dumb. In short, it looks an awful lot like every other financial crisis we’ve experienced and eventually overcome.

Where Are We Now? This particular financial crisis is only a month old, so we are still in the stage of trying to identify the potential fallout and additional risks. Are there other banks or financial firms with similar characteristics to SVB? We do not believe this will become widespread at this point. We know that a huge amount of assets has moved from smaller banks to the largest banks, and even out of the banking system altogether. This is how bank panics always work, as customers look for safety first and ask questions later. Remember poor George Baily in the film, “It’s a Wonderful Life”? The key point is this: we don’t believe this crisis needs to get bigger or spread further for it to have economic ramifications for years to come.

“Banking is a very good business if you don’t do anything dumb”.

Warren Buffett Chairman and CEO Berkshire Hathaway, Inc.

What Happens Next? Once we get past the finger pointing, political grandstanding, outrage and calls for punishment, we will start to gain a clearer picture of how this crisis is likely to impact the economy and markets. The hard and honest truth, at this point, is that no one really knows. If you want proof of how difficult it is to forecast economic conditions, look no further than the Federal Reserve (Fed). At last count, the Fed employs no fewer than 400 Ph.D.-trained economics and financial analysts, and their track record of being wrong every quarter is nearly flawless.

While it’s impossible to know with certainty the impact of the current crises, we can look to the past for guidelines of what we may see coming and how to best prepare now. We strongly believe that the following three events and actions will all be seen to some degree.

1. Increased Regulation. It has long been said that governments never let a good crisis go to waste. I expect this one will be no different. There is already talk of imposing stricter regulations on small and mid-sized banks, and even requiring them to pass annual stress tests which currently only apply to our nation’s largest banks. This could help to stabilize the banking industry, but it comes with the risk of not allowing smaller banks to effectively perform their primary intermediary function of connecting savers and borrowers. In our opinion, there is probably no amount of regulation that can prevent occasional dumb decision making in banking or any other industry.

2. Consolidation in the Banking Industry. This is already well underway. Merger and acquisition activity has increased as smaller and distressed banks look for partners and new sources of capital. Large pieces of SVB were purchased via auction by First Citizens Bancshares. Bargain hunters, like Warren Buffett, are no doubt analyzing bank balance sheets and looking for opportunities

to strengthen their own companies through strategic acquisitions. This was summed up best by Jamie Dimon, Chairman and CEO of JPMorgan Chase when he said, “Don’t do anything stupid. And don’t waste money. Let everybody else waste money and do stupid things; then we’ll buy them.”

3. Recession. I’ve saved the worst for last. We’ve heard talk about a potential recession for over a year. It’s now widely believed that the current banking crisis greatly increases the probability of the U.S. experiencing a recession within the next 12-18 months. The reason is that small and midsized local banks are the main lending sources for small businesses. Given the loss of deposits I mentioned, and the potential for more regulations, these banks will tighten their credit standards. This will make it much more difficult for small business owners to obtain loans to finance or grow their operations. Small businesses still employ the majority of working Americans, and this credit tightening cycle, as in the past, will likely lead to job cuts and higher unemployment. A very high correlation between financial crises and recessions exists in our nation’s history. At this point, it appears any recession will be mild and nothing close to what we experienced in 20082009.

How is

This Impacting Your Portfolio?

Mark and I continue to focus on preparing over predicting. We are continuing to monitor this situation and adjusting what is appropriate and necessary. In terms of our investment management process and your investments, we are focusing a great deal of our attention on these areas.

Financial Services Sector- It’s obvious by now that this is where most of the action and volatility is taking place. Mark and I continue to invest in this sector, but we are concentrating on the large companies who we believe eventually stand to benefit from the transfer of funds away from smaller banks as well as

mergers and acquisitions. The banking and financial services industry continues to play a critical role in the global economy. It will undoubtedly change as a result of the current crises, but it isn’t going away. If this plays out as most expect, the stronger companies will emerge even stronger. We want you to own the kind of companies following the advice of Warren Buffett and Jamie Dimon.

Quality, Quality, Quality- Nothing really new on this point. In almost every meeting or call with you, it’s likely you have heard me or Mark talk about our emphasis on investing in only high quality stocks and bonds. This is one of our core investment philosophies and beliefs. We think quality works in any economic environment, but it’s even more important now. In your portfolio, we favor companies generating current cash flow and reserves to carry them through difficult periods. As banks tighten credit standards, and borrowing rates increase, companies with less debt are much less vulnerable in a potential recession.

Diversification- This past month is a perfect example of how quickly the environment can change, and how fast a single company can go from thriving to out of business. SVB was not a new company. They had established a strong reputation lending to start-up companies over the past 40 years. Unfortunately, their management team failed to prepare the bank for a rising interest rate environment, and they found themselves in the hands of the Federal Deposit Insurance Corporation (FDIC) in a matter of only a couple days. The stock price is near zero, and anyone with large investments in this single bank stands to lose everything. Mark and I seek to avoid this kind of single company risk by investing your portfolio over a wide variety of companies across many sectors whenever possible.

As we entered 2023, I don’t recall seeing an impending banking crisis on anyone’s worry

list. Yet here we are only one quarter of the way through the year and the country’s 16th and 23rd largest banks have failed. There’s a saying that the Federal Reserve raises rates until something breaks, and it happened again in March 2023. How the Fed responds to this crisis is anyone’s guess. I assure you that Mark and I do not allocate your investments by trying to predict what the Fed will do next. I hope this letter helps to reassure you. As in the past, this crisis will pass. Capitalism, along with help from our government, will determine the winners and losers. As always, we are here for you if you want to discuss our strategies and your specific portfolio.

Quote of the Quarter

Former FDIC ChairmanBook Recommendation

“Killers of the Flower Moon: The Osage Murders and the Birth of the FBI”

by David Grann

by David Grann

This book is a well-written and researched account of a dark page in our history. Once I started, I couldn’t put it down.

The Spring edition takes us guide for surviving in just about planning.

Many of my friends tell me everyone, and I believe there thoughts when you can. I always

Sincerely,

Jeffrey Brayton Financial Advisor Branch ManagerTHE BIG PICTURE WITH JEFF BRAYTON

“Unburdened with the experience of the past, each new generation of bankers believes it knows best, and each new generation produces some who have to learn the hard way.”

Irvine Sprague