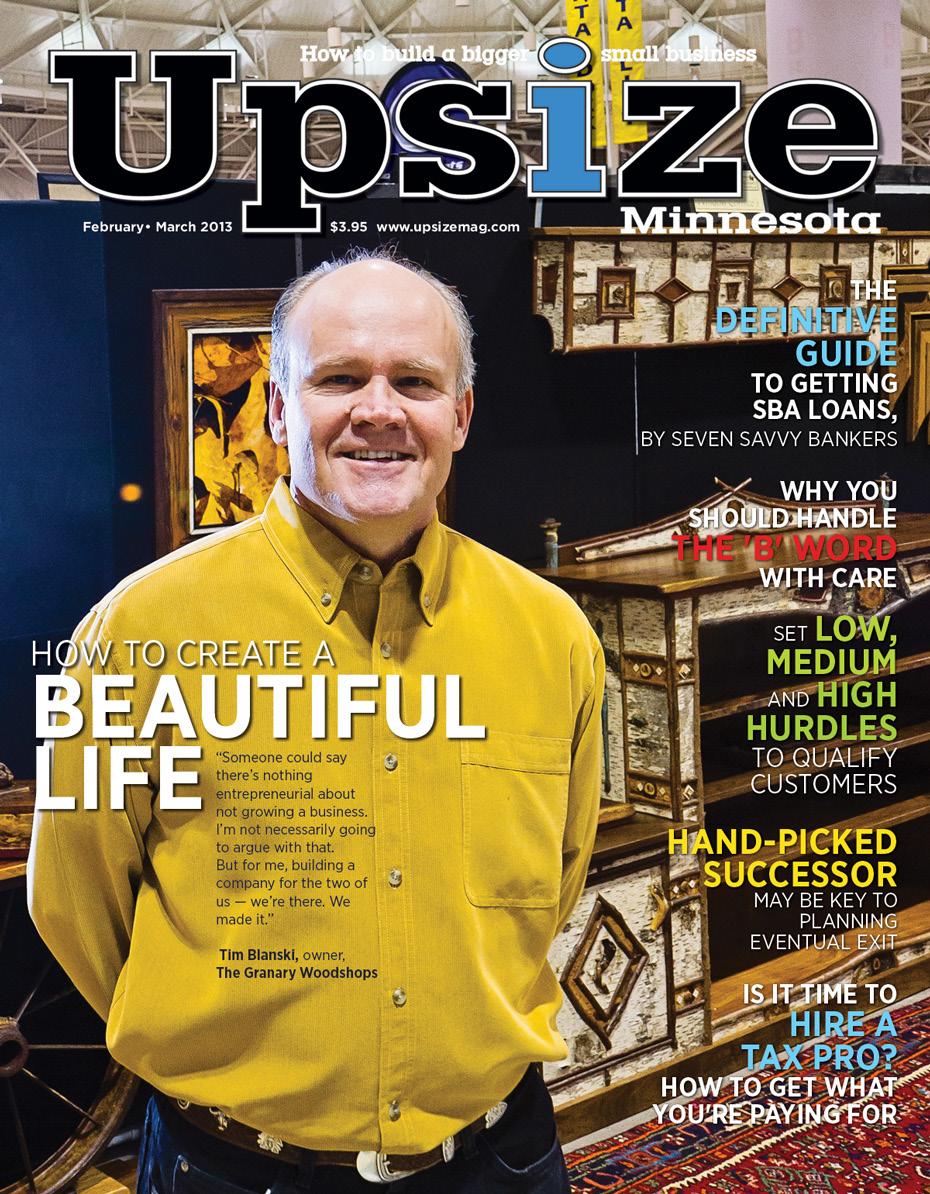

Subscribe to Upsize Minnesota at www.upsizemag.com/subscribe CAPITAL CONUNDRUM TIMES ARE TOUGHER, BUT MONEY’S STILL OUT THERE ALSO: MEDA’S DOROTHY BRIDGES: MEET THE NEW BOSS CATCHING UP: TIM BLANSKI, THE GRANARY WOODSHOPS PLUS: PEP TALK FROM A SHARK TANK JUDGE DIPESH PATEL, CEO of Postmatic

Minneapolis Location: 952.358.7400 St. Paul Location: 651.330.8062 Website: ssm-lawfirm.com Email: info@ssm-lawfirm.com CONTACT US By adding Mendoza to our name, we expand our areas of practice, and we enhance our opportunity to do great things for our clients. Please join us in welcoming Tony Mendoza and team to the Schindel Segal family. Schindel Segal UpSizes PRESENTING Schindel Segal Mendoza Law Firm

Happy Holidays

As 2022 comes to a close we want to thank our clients for another great year. We are grateful for your partnership and we look forward to helping you create new possibilities in 2023. What can we make possible for your business?

EDINA • 6600 FRANCE AVENUE S • 952-285-5800 | CROWN-BANK.COM MEMBER FDIC EQUAL HOUSING LENDER

CONTENTS

November • December 2022 • Vol. 21 No. 6 • www.upsizemag.com

PAGE 12

Cover story

Interest rates are up. Inflation and a likely recession have dampened optimism in recent months. But money is still available to companies that know where to look. Business owners and lenders weigh in on how finding financing differs during difficult times

BY ANDREW TELLIJOHN Cover photograph by Tom Dunn

BY ANDREW TELLIJOHN Cover photograph by Tom Dunn

PAGE 4

Founder’s Forum: Shark Tank Judge Barbara Corcoran provides business owners with a pep talk to help them through tough times

PAGE 4

Staff list: Who’s who at Upsize magazine and how to reach us.

Upsize Minnesota (USPS 024-029) is published bi-monthly by Broad Axe Media, 2908 W 71 1/2 St., Richfield, MN 55423. Periodicals postage paid at St. Paul, MN and additional mailing offices.

Postmaster: Send address changes to Upsize Minnesota, PO Box 23238, Richfield, MN 55423-0238

BUSINESS BUILDERS

PAGE 6

BANKING

Simple steps you can follow to manage your cash flow by Craig Veurink, U.S. Bank

PAGE 8

LAW

Practical steps you must take to get the best result possible when customers file bankruptcy by Matthew Bialick,, MJB Law Firm PLLC

PAGE 10

SOCIAL MEDIA

Maximizing the effect of your social media plan involves getting top executives active by Alison Buckneberg, Words At Work

PAGE 10

TECHNOLOGY

Basic information about understanding the new world of Web3 by Megan Effertz, ,Emerald

COLUMNS

PAGE 18

FEATURE

New MEDA CEO Dorothy Bridges discusses why she came out of retirement to take the job and what she hopes to accomplish

PAGE 22

CATCHING UP

It’s been 22 years since Tim Blanski and Lisa Catton left busy corporate jobs for the slower pace of Spring Grove, MN and his Granary Workshops business

PAGE 28

BACK PAGE

EOS Worldwide Franchisor Sara Stern wrote the book “Family Business: A Handbook for Spouses of Family Business Owners” to help them deal with challenging situations

Get more from your money.

Credit cards make purchasing convenient and simple. And when you have the right solution for your business, they can also maximize your rewards and give you the purchasing power you need.

Find out how to earn more. Get a complete spend analysis from an experienced business banking consultant. Our experts make it easy for you to get the most from your business credit card, so the only change you’ll notice is the extra money on your balance sheet.

Learn how to earn more without doing more.

Request your complimentary analysis and consultation. Scan the QR code.

The creditor and issuer of these cards is U.S. Bank National Association, pursuant to a license from Visa U.S.A. Inc. ©2022 U.S. Bank

FOUNDING PUBLISHER

Wes Bergstrom

EDITOR AND PUBLISHER

Andrew Tellijohn atellijohn@upsizemag.com

FOUNDING EDITOR

Beth Ewen bewen@upsizemag.com

DESIGN DIRECTOR

Jonathan Hankin jhankin@upsizemag.com

CHIEF FINANCIAL OFFICER

Dan O’Connell dano@upsizemag.com

PHOTOGRAPHER

Tom Dunn tom@tomdunnphoto.com

HOW TO REACH US

To subscribe visit www.upsizemag.com/subscribe

With story ideas email Andrew Tellijohn, atellijohn@upsizemag.com

To advertise email Andrew Tellijohn, advertising@upsizemag.com

To order reprints backissues@upsizemag.com

To order extra or back issues email backissues@upsizemag.com

To suggest Web resource links, info@upsizemag.com

BROAD AXE MEDIA

P.O. Box 23238 Richfield, MN 55423

Main: 612.827.5290 www.upsizemag.com

© 2022 Upsize Minnesota Inc. all rights reserved

A pep talk from a famous ‘Shark Tank’ judge

“T

he best time to move ahead is the worst times.”

So declares Barbara Corcoran, the fast-talking New York real estate mogul and judge on ABC’s hit show “Shark Tank,” who’s the perfect interview as business owners everywhere face tough times.

I got a boost from her in an inter view recently that I had to share, even though she’s not local as my typical sources are. “Established works against you in bad times because you protect your turf. I can tell you so many times that I could sniff out a weakness in my competitors—cockiness. They were cocky, big and protecting,” Corcoran said. “The larger companies in bad times hide. It’s prudent to wait it out, because they have a lot of money and they don’t want to lose it.”

She recalls trying to sell New York residences when interest rates hit 18 percent. (Remember that? It makes today’s 6.5 percent seem almost free.) “People were losing faith. I didn’t have an answer: nobody was buying anything. We were starving at Corcoran Group. I was really trying to stay in business, maybe one more week,” she says.

A large insurance company wanted her to sell 88 apartments scattered throughout several Class C buildings, “a smorgasbord of losers,” as she recalls.

“I told them there really wasn’t any way,” but then got to thinking about her mother, who once took her passel of children to see a chicken farmer across the river in New Jersey, selling puppies out of a box.

“They were so adorable, and there was a line of fancy cars. The people get ting out of the cars looked like freaks. They had makeup on, they had fancy clothes on, they were New Yorkers! And they were getting in line to buy pup pies” because there were only seven available.

She had her brokers announce a secret sale, one day only, only for their best clients. “When I hit the sales office,

there were 150 waiting in line for the 88 apartments. We sold them within an hour,” she said.

On “Shark Tank,” where entrepre neurs compete to gain an investment from the judges, she looks for one main quality. “I’m trying to ascertain if the person is good at bouncing back. There’s no such thing as a business plan that works. The minute you get on the street, nothing goes to plan,” she said. “People steal, markets fall down, interest rates go up three points. You’re going to be assured you’re going to walk into a changed environment every year.”

The entrepreneurs she tries to avoid? “They lack one quality, they feel sorry for themselves. When I find an en trepreneur that starts blaming—the minute people are pointing outward versus just shut up. ‘I have a problem. How am I going to fix it?’” is what she’s waiting to hear.

“These are the best times to move ahead, when everybody’s scared, be cause the checkerboard gets rewritten. Your customer you’re doing business with, they change in changing times. They want something differently, you catch them differently,” she said.

What about you? How will you catch your customers differently, during a rocky today and an uncertain tomorrow?

—Beth Ewen founding editor bewen@upsizemag.com

4 UPSIZE NOVEMBER • DECEMBER 2022

www.upsizemag.com

We develop and rely on best practices to help create a tailored experience for all our clients. Whether you’re working with me or any advisor on the team, you receive the same commitment to advocacy, disciplined processes, and a cohesive client experience that JNBA is driven to deliver.

Elise Huston, CFP®

A client-first and conflict-free philosophy: that’s how JNBA Financial Advisors has operated since our founding days over 40 years ago. Since we began tracking in 2001, we have been fortunate to maintain a client-retention rate of 97 percent. And, Barron’s has ranked JNBA and CEO Richard S. Brown #1 in Minnesota on its Top 1,200 list for two consecutive years.

To learn more about how advice driven by advocacy®could help you and your family, begin a conversation with our team by calling us or visiting JNBA.com.

® MINNEAPOLIS: 952.844.0995

DULUTH: 218.249.0044

BONITA SPRINGS, FL: 800.675.4793 | JNBA.COM As seen in the 3/15/21 & 3/14/22 issues of Barron‘smagazine. Barron‘sis a trademark of Dow Jones & Company, Inc. All Rights Reserved. Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if JNBA is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, JNBA did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of JNBA by any of its clients. ANY QUESTIONS: JNBA’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking. Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by JNBA Financial Advisors, LLC (“JNBA”)) or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation or prove successful. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement. Please see important disclosure information at www.jnba.com/disclosure.

Advisor - Advisory Services Manager JNBA Financial Advisors

Advice driven by advocacy

|

|

banking

Manage your cash flow in a few simple steps

by Craig Veurink

TIPS

1. Set a realistic goal for when you want to break even. This will help you to focus your efforts and provide a numerical benchmark for projecting your cash flow in the near future

2. Put cash flow before profits. It might seem counterintuitive, but if you aren’t organizing your cash flow, you’ll run into problems that a profitable quarter might not be able to fix

3. Secure credit ahead of time. Most small business owners should secure as much credit as possible. This is the best way to be prepared for the unexpected

4. Consider using a payroll service. Having the professionals take care of collecting payroll taxes saves them an enormous amount of time, helps streamline their cash flow

5. Schedule your payments. Don’t go delinquent but do divide your payments into categories such as “must pay,” “important to pay” and “flexible payment terms.” This can help keep sufficient cash on hand.

Small businesses are usually founded by entrepreneurs who have a unique vision and a passion that drives them to work late hours, take chances and believe in what they’re doing. But, just as Thomas Edison once said that genius is 1 percent inspiration and 99 percent perspiration, successfully run ning a small business requires rolling up your sleeves and putting in signifi cant time on more mundane, day-today matters.

You can be driven, impassioned and have a great idea to fill a niche or serve customers in new ways, but if you don’t attend to the details of the busi ness, you can create for yourself a heap of problems.

Here, we’ll look at one of the most important of these business details: managing cash flow. Especially for early startups, knowing how much cash is coming in and going out, and accurately forecasting sales and expenses, is key to maintaining your company’s health.

No matter where you are in your business, keep these things top of mind:

1. Know when you will break even

Every small business owner keeps at the front of their mind the question:

“When do I start to turn a profit?”

Rather than wonder, set a realistic goal for when you want to break even. This will help you to focus your efforts and provide a numerical benchmark for projecting your cash flow in the near future.

2. Put cash-flow management before profits

This might seem counterintuitive, since profits are how you survive. However, if you aren’t organizing your cash flow, you’ll run into problems that a profitable quarter might not be able to fix. Keep things organized and well managed so you can be ready for whatever success comes your way.

3. Secure credit ahead of time

Too often, small business owners wait until they need it to secure credit. This can cause a lot of unnecessary stress, or worse. Talk to experienced business owners in your area and industry ahead of time to know how much revenue you’ll need up front. Take a realistic look at the situation and plan. You might have sufficient cash reserves or a rich uncle who is only a call away, but most small busi ness owners should secure as much credit as possible. This is the best way to be prepared for the unexpected.

6 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

BUSINESS BUILDERS

Use a dedicated software to manage your finances

Even if you’re running a small operation and you think that a simple spreadsheet will suffice, it won’t. Think bigger. Most accounting or online banking software that is avail able today allows you to both focus on the details and look at the big picture of your finances. There are, of course, plenty of other advantages these programs offer, but above all, using a dedicated system to manage your cash flow will keep you organized and on top of your financial dealings and hence, your business.

5. Use a payroll service

It’s tempting to think that you can do payroll all on your own. However, many small business owners have found that having the professionals take care of collecting payroll taxes saves them an enormous amount of time, helps streamline their cash flow and is fully worth the cost.

6. Accounts payable improvements

There is more than one way to save a dollar and there is more than one way to spend a dollar. Small business owners are always looking for ways to improve efficiencies and reduce costs. In addition to this, they should look at how they are paying their bills. Many credit cards have a cash-back bonus program. Even if you get just 1 percent cash back that could equate to as much as several thousand dollars a month, depending on the amount you spend. However, because credit cards tend to have a higher interest rate, you should only use them if you are sure you will be able to pay your balance off in full.

7. Schedule your payments

You don’t have to pay everything at

once; in fact, you shouldn’t. This is not to say you should be delinquent on any payment; rather, to keep suf ficient cash on hand, consider dividing your bills into three categories:

• Category 1: Must pay — This includes payroll, taxes or rent, things that you must pay in order to keep operating.

• Category 2: Important to pay — Sometimes utility bills and insurance payments have penalty-free grace periods, in which case, you might want to take advantage of this.

• Category 3: Payment is flexible — Many vendors and suppliers are happy to work out a flexible payment plan. Be honest with them, keep com munication open and pay at the agreed-upon time.

8. Keep up on cash coming in Making sure you get paid is, of course, one of the most important parts of your business operations. The sooner you get paid, the sooner you can put money back into your business and grow. Therefore, it’s vital to send out your invoices in a timely manner and establish clear terms of payment ahead of time. Explore payment options from your bank or another provider that allow your cus tomers to quickly and easily pay for your services in-person and online.

Be sure to factor in the fact that people and other companies are often late with payments, so if you want to receive payment within a month, make your payment terms 14 days.

Contact: Craig Veurink is Midwest business banking regional executive at U.S. Bank: craig.veurink@usbank.com; www.usbank.com; /in/craig-veurink-63ab7a4/

7 www.upsizemag.com NOVEMBER • DECEMBER 2022 UPSIZE

“Especially for early startups, knowing how much cash is coming in and going out, and accurately forecasting sales and expenses, is key to maintaining your company’s health.”

Craig Veurink U.S. Bank

law

My customer declared bankruptcy — now what?

by Matthew Bialick

TIPS

1. You’ll fare better in a bankruptcy if your debt has been secured by being granted a security interest in an identifiable asset, or class of assets, owned by the debtor

2. Security interests are obtained through things such as mortgages, UCC security agreements, or by operation of statute, such as mechanic’s liens. The interest also must be perfected, which is the process of putting the public on notice of your interest

3. Unsecured creditors are separated into their own class and basically receive a proportional share of what, if anything, is left. They typically fare poorly, if they receive anything at all

4. Upon a default, you should act quickly to exercise creditors’ remedies so that your collection action can be completed or a settlement reached before bankruptcy is filed

5. Unsecured debt can be converted to secured debt that will withstand bankruptcy if you can reach agreement with the debtor on terms specifying such a change at least 90 days before the bankruptcy is filed

Past due receivables can cause significant stress among business own ers. Emotions can reach a boiling point when, instead of a much-anticipated check, you receive a “Notice of Bank ruptcy Case.” What does this mean and what can you do to protect yourself?

What does it mean that your customer declared bankruptcy?

From a practical perspective, a bank ruptcy filing means three things:

• Your customer is experiencing financial distress that impairs its ability to pay off debts

• You need to immediately stop all collection activities

• You need to appropriately participate in the bankruptcy process

The main types of bankruptcy you are likely to face are a Chapter 7 bank ruptcy or a Chapter 11 bankruptcy. A Chapter 7 bankruptcy is a liquidation of all non-exempt assets. A Chapter 11 bankruptcy is a corporate restructur ing seeking a modified payment plan with all creditors over time. A Chapter 7 is what you are likely to see if your customer is an individual or a sole proprietor operating under a DBA. Since corporations or limited liability corporations typically just go defunct when insolvent, they rarely file Chapter 7 bankruptcies. They’re more likely to file under Chapter 11.

How well your business will fare in a bankruptcy depends primarily on one thing — is your debt secured or unse cured? A secured debt is one where you have been granted a security interest in an identifiable asset or a class of assets owned by the debtor. Security interests are obtained through things such as mortgages, UCC security agreements,

or by operation of statute, such as me chanic’s liens.

That said, a security interest alone is insufficient to make the creditor “secured” for the purposes of bank ruptcy. That security interest must be “perfected.” Perfection is the process of putting the public on notice of your security interest through taking an action such as recording a mortgage with the county, filing a UCC financing statement with the Minnesota Secretary of State or recording a mechanic’s lien statement with the county. If a security interest is not perfected as of the date of the bankruptcy filing, then it is not valid and you’ll be treated as an unsecured creditor.

A secured creditor will either be paid the value of the collateral, or else will likely be able to ask the court to remove the collateral from the bankruptcy pro ceedings so the asset can be monetized through processes such as foreclosure. As such, secured creditors will likely eventually be made whole or will escape with a moderate haircut.

Unsecured creditors are a different story. These creditors are aggregated as a class and receive a proportional share of any non-exempt, unencumbered property owned by the debtor and liqui dated during the bankruptcy. Property is “exempt” if it is subject to a statutory protection. Property is unencumbered if it is not subject to a mortgage, secu rity interest or statutory lien.

As you may imagine, most property owned by a debtor tends to be either exempt or encumbered, so unsecured creditors generally fare very poorly in a bankruptcy, typically receiving no more than 10 percent of what they are owed.

What to do if your customer declares bankruptcy

What to do depends on your creditor status and which bankruptcy chapter is

8 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

BUSINESS BUILDERS

declared.

If you are an unsecured creditor in a Chapter 7 bankruptcy, there is little or nothing to do. The initial bankruptcy notice will specify whether the bank ruptcy is expected to be a “no asset” case, which means it is not expected that any money will be available for unsecured creditors. In that case, there is nothing for you to do and you likely will never recover anything from your customer.

If you are an unsecured creditor in a case where a distribution to unsecured creditors is anticipated, you will need to submit a “proof of claim” form to the bankruptcy court by the deadline specified in the bankruptcy notice. This form and its submission instructions can be found online at the Minnesota Bankruptcy Court website.

If you are a secured creditor, or if the bankruptcy is a Chapter 11 bankruptcy, you should contact an attorney as soon as possible to preserve your legal rights. You will need to take steps that typi cally go well beyond the simple submis sion of a proof of claim.

was commenced. This lien — called a judgment lien — survives bankruptcy if it is in place at least 90 days prior to the bankruptcy filing.

“Security” refers to the process of turning otherwise unsecured debt into secured debt that will fare much better in bankruptcy. Security can either be taken on the front end — by adding a grant of a security interest in the initial contract or documents executed between your business and your cus tomer — or on the back end through the negotiation of what is referred to as a “forbearance agreement.”

A forbearance agreement between you and a customer who owes you money provides that you will tem porarily forego collection action in exchange for the customer’s agreement to do certain things, such as grant a security interest to secure the prior debt. Through this process, unsecured debt can be transformed in secured debt that can withstand bankruptcy, if the security interest was granted at least 90 days before bankruptcy is filed.

Only two things can protect your business against a customer’s bank ruptcy — speed and security.

“Speed” refers to exercising credi tors’ remedies upon default so quickly that your collection action can be completed, or a settlement can be reached, prior to the customer’s bank ruptcy. Even if the collection is not fully “completed” the mere act of being far enough along in the process can increase protection.

For example, if you sue your cus tomer and obtain a judgment, that judgment, once docketed, becomes a lien on all real property owned by the debtor in the county where the lawsuit

In either a front-end or back-end case, consulting an attorney can ensure that the granting provision is properly drafted to meet all applicable legal re quirements and to ensure that another creditor does not already have a prior security interest in these same assets. Holding a subordinate security interest in an asset is functionally valueless if the customer has no equity in the asset.

Conclusion

Bankruptcy is an imposing process that radically affects your ability to collect a past due receivable. The risk of bankruptcy cannot be eliminated, but can be mitigated through proper documentation and being expeditious in collection action.

Contact: Matthew Bialick is an attorney at MJB Law Firm PLLC: 952.239.3095; matthew@mjblawmn.com; www.mjblawmn.com; in/matthew-bialick-35b7a438

Matthew Bialick

MJB Law Firm PLLC

Matthew Bialick

MJB Law Firm PLLC

9 www.upsizemag.com NOVEMBER • DECEMBER 2022 UPSIZE

What should you do to protect against future customer bankruptcies?

“How well your business will fare in a bankruptcy depends primarily on one thing—is your debt secured or unsecured? A secured debt is one where you have been granted a security interest in an identifiable asset or a class of assets owned by the debtor.”

social media

Getting your CEO active on social media: A battlecard

by Alison Buckneberg

TIPS

1. More than one in three online users say they go to social media when looking for more information about a brand or a product. Get your CEOs and senior leadership online presence going before your competitors do

2. Your weekly presence doesn’t have to take long. Do a single post on an issue of importance weekly and then spend around 15 minutes a day scrolling, engaging with company posts, reviewing connection requests and interacting with relevant stakeholder posts

3. You control the narrative on social media. You share the information you want people to know. And if someone does post an opposing viewpoint, responding in an engaging and honest way can win you even greater support

4. Studies have found that employees want to work for and consumers want to buy from companies whose executives are active on social media. They are found to be more transparent and accessible

5. Employees look to senior management for guidance. If they see people in leadership positions participating in company initiatives and actively engaging on social media, workers are more likely to do the same

If you’re part of a small- to medium-sized business, chances are you’re already investing in social media. In fact, 77.6 percent of small businesses report using a combina tion of social platforms to engage with customers and drive business. Depending on your resources, you may have a team — or a savvy, multiple-hat-wearing pro — develop ing strategy and quality content for social media channels like LinkedIn, Twitter, Facebook, Instagram or even TikTok. Your company is also probably (hopefully) further invest ing in these platforms with paid ads, influencer campaigns, LIVE events and even LinkedIn Sales navigator for better social media selling.

So, where’s the voice of your CEO and your leadership team? CEOs and other high-level executives are often the missing piece of the social media branding puzzle — and they have the knowledge and experience that can take your presence to the next level — turning fair-weather-fans into super fans in the process.

But, according to AdWeek, 61 percent of Fortune 500 CEOs have no presence on social media what soever.

While it may be a daunting task, it’s time to convince your CEO and

other senior leadership that they must get active — at any level — to help your efforts be successful and make the most of the company’s social media investments. You’re probably wondering how to go about this challenging endeavor, and you’re not alone. To empower your efforts, try these talk tracks as an initial battle card:

They say: “Our competitors’ CEOs aren’t on social.”

Truth: According to Small Busi ness Trends, more than one in three online users say they go to social media when looking for more infor mation about a brand or a product. Make sure to let them know that if your competitors’ CEOs aren’t on social media now, they will be later. Therefore, the only option is to be the leader on social as well and get in the game to engage with employees, customers and the industry or get left behind — or worse, forgotten. They say: “I don’t have time and don’t know where to start.”

Truth: All it takes is 15 minutes a day. Pick one platform (e.g. LinkedIn or Twitter), download the app and spend 15 minutes scrolling, engaging with company posts, reviewing con nection requests, liking customer/ employee/stakeholder posts, and

10 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

BUSINESS BUILDERS

saying “congrats” to others with big news. Then, once a week, post about something that happened in the busi ness and add a few thoughts. Easy. Short on ideas? Your internal social media or agency team can help.

They say: “I don’t want to deal with trolls.”

You say: The beauty of social media is that YOU can control the narrative. CEOs and other leaders can share only the key messages they want people to know about the company — and this message is broadcast to thousands in real-time. While there’s always a chance some one could add an opposite viewpoint, opinion, or negative comment, executives who respond directly and honestly can win more support by being transparent, honest and engag ing on the platform. Your in-house or agency social media team can offer much needed guidance and support here.

They say: “Nobody cares what I think.”

Truth: Believe it or not, your employees, stakeholders and cus tomers actually do. According to a survey by advisory firm Brunswick Group, employees prefer working for business leaders who are active on social media by a ratio of four to one. The firm found that executives who are visible online are seen as more transparent and accessible — which is key for employee retention and recruitment. But it’s not just em ployees. Brands Get Real found that 38 percent of consumers say a CEO’s transparency on social would inspire them to show a brand more loyalty and 32 percent would purchase more from that business. It’s hard to argue with increased loyalty and purchases.

They say: “My people are there so I don’t need to be.”

Truth: Lead by example. If your

company is investing in social media, then executives need to sup port any company efforts from the top down. Senior leadership buy-in is essential for internal adoption because employees look to execu tives for guidance. If they see people in leadership positions participating in company initiatives and actively engaging on social media, workers are more likely to do the same.

They say: “Where’s the ROI?”

Truth: More than half of market ers using social media marketing tactics for at least two years have reported improved sales. When executed with the right goals in mind, social media can be more cost effective and bring about a better return than many traditional brand-building tactics. Whether you are mapping the buying journey or getting to better understand dark social, social media is an essential part of brand building in today’s world. Savvy social media teams can measure success by leads generated, followers, engagement, web traffic, impressions, downloads, number of attendees and more.

Having some hesitation before diving into this challenge is under standable — getting CEOs to try something new isn’t for the faint of heart. But don’t fret. Go ahead and dive right in as many before you have been able to walk into the CEO’s office months later with data points that show their efforts are making a difference. Just remember to smile and avoid the urge to say I told you so.

Alison Buckneberg

Words At Work

Contact: Alison Buckneberg is vice president of PR and social media for Words

At Work: ali.buckneberg@wordsatwork.com; www.wordsatwork.com; in/ alisonbuckneberg

11 www.upsizemag.com NOVEMBER • DECEMBER 2022 UPSIZE

“Lead by example.

If your company is investing in social media, then executives need to support any company efforts from the top down. Senior leadership buy-in is essential for internal adoption because employees look to executives for guidance.”

technology

Business, brands embrace Web3

by Megan Effertz

TIPS

1. The simplest way to enter Web3 is investing in digital assets. Before investing, a business’s board and leadership team need to understand the risks associated with such investments and agree upon their risk tolerance

2. Many large consumer-facing brands are accepting crypto payments for goods and services. Most use third-party payment providers such as Flexa or Bitpay, which makes it easier for brands to convert assets to Fiat to avoid accounting and tax complications

3. Non-fungible tokens (NFTs) are digitally designed so they can’t be replicated and are created with blockchain technology that provides unique ID codes

4. Brands are minting NFTs as a way to build brand loyalty, offering limited edition collectables often designed by a well-known artist. Their rarity makes them popular and valuable

5. The metaverse is another example that is gaining a lot of momentum but it’s also the most resource intense to start. Many larger businesses are setting up shop and consumers are interested

Web3 is the next evolution of the internet with a promise of transparency and decentralization creating a more secure and private place for users to conduct business. The internet is in a constant evolu tion from Web1 where users searched for answers but couldn’t create or interact with content to Web2 where users can create content and share info, but they don’t control their data, big corporates do. Web3 is the promise to shift that control back to the users and provide more trans parency through distributed ledgers otherwise known as blockchain technology.

In theory, blockchain technology has the power to disrupt the way business is done today, potentially eliminating the need for many thirdparty services. It also offers new ways to generate revenue. A hand ful of popular brands are already embracing Web3 and setting the bar for other businesses to compete. There are many entry points into Web3, some easier than others to get started. From easiest to more com plex these options include investing in digital assets, accepting crypto as payment, minting an NFT (nonfungible token) and setting up shop in the metaverse.

Investing in digital assets

The simplest way to enter Web3 is investing in digital assets. Bitcoin and Ethereum are the two most known digital assets. Companies like MicroStrategy are quite bull ish on their investments with these alternative assets. Before investing, a business’s board and leadership team need to understand the risks associ ated with each of these alternative assets and agree upon their risk tolerance, especially as regulation of this area continues to evolve.

Companies can custody these as sets directly through an exchange or use a third party that helps elimi nate some of the complexity from these types of investments. Not all exchanges are created equal as we saw earlier this year. It is critical that before investing, a business should understand how the assets and ex changes they are considering work, as many are not regulated and there potentially is a lot of risk associated with such investments.

Accepting crypto payments

If using a third party, the next way to engage in Web3 is accepting crypto as payment. Consumer-facing brands are leading the way with popular brands such as Microsoft, Overstock, Whole Foods, Starbucks,

12 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

BUSINESS BUILDERS

Home Depot, AT&T and the Dal las Mavericks accepting crypto payments for goods and services. Most are using third-party payment processing providers such as Flexa or Bitpay. That makes it easier for brands to embrace Web3 and convert digital assets to Fiat to avoid ac counting and tax complications.

Minting NFTs

An NFT is a non-fungible token and is digitally designed so it can’t be replicated. It’s created using blockchain technology that gives it a unique identification code. Most people think of art when they hear NFT but an NFT can be anything digital. There are no rules for creat ing NFTs and creativity is the only limit in making them, which is also known as minting.

Brands are minting NFTs as a way to build brand loyalty, offering limited edition collectables often designed by a well-known artist. Some brands sell them, some offer them as contests, either way they are wildly popular with brand enthusi asts. It’s the rarity that makes them popular and valuable. Recent suc cessful brand NFT projects include Hot Wheel’s NFT Garage Series that capitalized on the collectible aspects of Hot Wheels. Another example is Taco Bell’s taco-themed NFTs where brand loyalists essentially bought and resold digital tacos. NFTs can be bought and sold at trading platforms like Rarible, OpenSea and Crypto. com.

Welcome to the metaverse

The metaverse is another example that is gaining a lot of momentum but it’s also the most resource intense to start. Businesses are setting up shop and consumers are buying in. Nike is a great example. The company built parks and sport courts where brand enthusiasts can play — and they can pick up new Nike gear while they are there.

Stella Artois has built virtual rac ing tracks where you can breed and race your own horse. There are lim itless possibilities that brands can do to grow new audiences, create new revenue streams and capitalize on truly unique customer experi ences.

These are just a few examples but there are many more ideas and proj ects under development that could disrupt business quickly if they take hold. Web3 is in its infancy, but with technology, change happens quickly.

Businesses need to be educated on what is happening now and what future possibilities are so they can keep their competitive advantage or create one. Although there is a wealth of information available, there has been a lack of content available that deciphers all of the in formation and presents it in a way a business can quickly understand and consume the information. That’s starting to change.

Contact: Megan Effertz is a Twin Cities-based vice president, Web3 at D2 and Emerald, which provides education to business leaders on the Web3 space: 774.505.8036; www.emeraldx.com; in/meganeffertz

13 www.upsizemag.com NOVEMBER • DECEMBER 2022 UPSIZE

“In theory, blockchain technology has the power to disrupt the way business is done today, potentially eliminating the need for many third-party services. It also offers new ways to generate revenue.”

Megan Effertz Emerald

Tightening pursestrings

MONEY AVAILABLE FOR

When Dipesh Patel acquired Post matic two years ago, he was looking to rapidly expand the manufacturer of equipment for mailing, packaging and semiconductor industries that also does contract work for original equipment manufacturers.

In the last three months, Postmatic has acquired another company and purchased real estate aimed at eliminating the cost of rent and facilitating the company’s ability to take on larger builds.

So, Patel is familiar with what it takes to get financing, both in good times and bad.

During these recent transactions, he worked with the same banker who first helped him acquire the company, so they have a comfort level together. The process was transparent, but it took a long time and rising interest rates have made it harder to pinpoint the company’s true costs.

“It’s getting a little bit more administrative in tensive to secure all checked boxes on the lender’s side,” Patel says. “The process has been lengthy.”

And there also has been some uncertainty about what the deal’s structure would look like with increases in interest rates.

“It makes it a little unclear what you are getting into,” he says.

Financing, costlier, but still available

When Patel was acquiring Postmatic he met with John Thwing after his broker suggested they

by Andrew Tellijohn photographs by Tom Dunn

connect. He liked Thwing’s transparent approach and his advice, which built a level of trust. Thwing has since switched companies, but Patel stayed with him for the latest transactions.

“We stay in touch, make sure he’s aware of what I’m doing,” Patel says.

That’s important all the time, financial services industry sources say, but it can be especially helpful during difficult times. Because right now, Thwing says, it isn’t just interest rates making deals a bit more challenging.

Labor shortages, supply chain challenges and the increasing cost of capital have affected small businesses recently. Those factors haven’t com pletely depleted the availability of financing, at least through the U.S. Small Business Administration, says Thwing, who does mergers, acquisitions and expansion deals for Live Oak Bank.

He acknowledged that inflation can be a drag on margins but adds that most markets have been accepting of price increases, important as compa nies manage their financial health and viability for growth.

Thwing recommends companies take a thorough look over all their finances as they prepare to seek funding.

“Owners understandably focus on the income statement when looking at their performance, but don’t ignore the balance sheet when looking at your company’s financial health,” he says. “Pandemicrelated stimulus funds like SBA EIDL (economic

Interest rates are up and the economy is challenging, but that didn’t stop Dipesh Patel of Postmatic from acquiring a company and a building in order to grow.

14 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

WELL-PLANNED COMPANIES

COVER STORY

injury disaster loans) are great sources of capital, but that additional debt can impact your borrowing capacity.”

A visit to your lender can help determine appropriate debtto-equity structures and financing amounts and terms. Some banks, Thwing adds, have started increasing their underwrit ing requirements while others with healthy loan portfolios are continuing to lend as they did previously. That said, with the prime rate up significantly in recent months, “a business that qualified for financing in a low/flat rate environment may not qualify for financing in a moderate/raising rate environment,” he says. “For healthy businesses with good trends, margins and cash flow, SBA financing should continue to be available.”

Demand still strong

As noted, there are several significant factors affecting the availability and ease of acquiring funding right now. The cost of equipment in many industries has gone up significantly, as well. But that hasn’t killed demand, which remains strong in capital equipment leasing and financing, says Brian Bourne, who does business development for KLC Financial.

“That’s unfortunate for the business owner, but they still need the equipment,” he says. “With seemingly almost everyone I talk to, you ask them what their biggest issue is, it’s staffing. They just don’t have enough people to man the machines.”

CONTACT:

BRIAN BOURNE does business development for KLC Financial: 952.595.5528; brian@klcfinancial.com; www.klcfinancial.com; in/brian-bourne-849a4081

KRISTIN ERICKSON is senior vice president and managing director of SLR Business Credit: 651.470.8420; kerickson@slrbusinesscredit.com; www.slrbusinesscredit.com; in/Kristin-erickson-ab9832a

MIKE HEIL is senior vice president of commercial lending at Fidelity Bank: 952.830.7254; mheil@fidelitybankmn.com; www.fidelitybankmn.com; in/mike-heil-b855378

GARY NOEL is CEO of B&E Tool: gary.noel@betoolmfg. com; www.betoolmfg.com; in/gary-noel-474324a

DIPESH PATEL is CEO of Postmatic: 763.784.6046; dpatel@postmatic.net; www.postmatic.net; in/dspatel0153

JOHN THWING does M&A and expansion financing for Live Oak Bank: 612.505.9751; john.thwing@liveoak.bank; www.liveoakbank.com; in/john-thwing-sbaguy

That’s driving companies to purchase equipment to help au tomate, to maintain their output with fewer people hours to run it. Companies are willing to pay a bit more right now because it’s been harder to get equipment in a timely manner and that may not improve in the near term, he says.

“Those folks who say, ‘this is 10 percent more expensive, 20 percent more expensive than it was this time a year ago, I really don’t want to pay that,’” Bourne says, also realize that if they wait, the costs might go up again and it might take even longer to get the equipment.

“The whole pipeline of equipment being so far delayed is still driving a lot of the demand and decision making,” he says. “It certainly is tougher to be a business owner. Yet, they still need this equipment, so they are still willing to pay the inflated prices. Their costs to customers are going up too.”

That’s almost the exact situation that was facing Gary Noel, owner and president of B&E Tool. Noel bought the company in 2018. It’s a precision machine facility in Fridley with 11 employ ees. The company specializes in high-mix, low-volume parts for test systems, medical devices, military equipment and other industries. So, each employee will work several jobs a week.

“We’re not huge, but some of the stuff these guys do is just amazing,” says Noel, CEO. “There’s nothing these guys can’t do.”

The company has gotten into Swiss manufacturing, a charac teristic of which is someone running 10,000s of parts in a run. B&E purchased a Swiss machine about two years ago and has been successful with it. The company can do products up to 20 millimeters in diameter on its existing equipment but wants to add another machine that will allow for manufacturing slightly larger parts, up to 38 millimeters.

As many are saying now, Noel was cautious because of rising interest rates. But he also felt strongly the company needed the new equipment to continue meeting growth goals and also believed it could cash flow the machine quickly. So, he attended the International Manufacturing Technology Show (IMTS) in Chicago in September and, as a result, was looking at a couple different machines. One company indicated it could make such equipment available by early 2024. That wasn’t going to work.

“That was a huge deal for us,” Noel says. “One of the things we’ve been able to do with some of our customers is we’ve been able to create some capacity with the way we do things with these machine purchases. We give them delivery dates other people can’t or won’t. But if you’re waiting 18 months for a ma chine, it’s tough to have the capacity you need.”

Another company, however, had one where if Noel acted quickly, he could have the machine in-house and up-andrunning by the end of November. Noel met KLC’s Bourne at a networking event tied to IMTS show. They had some good con versations there and arrived at a deal that had some flexibility where B&E could pay a bit to buy down its interest rate if it saw

16 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

COVER STORY

Equipment manufacturer Postmatic went through a lengthier, more intensive application process for SBA financing for its latest acquisitions, but the funds were still made available

the anticipated growth with its new machine quickly enough.

“They were able to respond in a timely manner,” Noel says, adding that B&E has already had productive conversations with at least one surgical instrument customer eager to do business with a manufacturer that can turn parts quickly.

“Brian and his team actually made it quite easy, as far as financing,” Noel says. “This acquisition made sense for what we are doing and what we are wanting to do, get into some new markets.”

Bourne says KLC Financial has tightened its credit require ments on deals on certain industries where the current eco nomic environment has made business tough, but it’s still not impossible even for companies in struggling markets to get financing under the right circumstances.

“A year ago on the fence, we’d probably have leaned in and said let’s go ahead and take on the risk,” he says. “Now, those borderline deals, well, we’ll be willing to do it but maybe we need more money down or additional collateral to secure our loan to debt ratios. The process has not changed, but what the terms ultimately look like, we’re a little more cautious.”

Tightening at traditional banks

Money will be available from traditional banks, as well, though there will likely be a general tightening, says Mike Heil, senior vice president of commercial lending at Fidelity Bank. At the same time, with the government money that was available to get through the pandemic, many small businesses are in better shape heading into a recession than has typically been true in the past.

“For those that managed their way through this, took advan tage of PPP funds, built some cash up and were very success ful in most industries in earning record-year profits, they’re uniquely poised going into this recession in better shape than they historically have been,” he says.

17 www.upsizemag.com

NOVEMBER • DECEMBER 2022 UPSIZE

COVER STORY

B&E Tool in Fridley moved forward with a recent machine purchase despite higher interest rates because the company expects to add new customers with the increased capacity and capabilities.

Heil says Fidelity will be looking for clients to have strong liquidity and capital ratios and diversified revenue sources that will help them through a recession when their businessto-business customers are going to be pulling back on inven tory.

He wants to see businesses that have a plan, that are regu larly projecting out and refreshing their cash flow forecasts and that are planning for some ups and downs. And it can’t be overstated how important it is to have the ability to pick up the phone and call your banker.

“The thing I would emphasize the most from a small business provider’s perspective is make sure you have that ongoing relationship with your lender,” Heil says. “With the entrance of fintech companies and technology-based credit sources where getting credit was easy, those are going to tighten up. Without having a good story to tell or a lender who knows who you are and understands your ability to manage through ups and downs, who knows your business well, it’s going to be harder for small business owners to obtain the financing they need.”

Business picking up in factoring

Kristin Erickson is senior vice president and managing director at SLR Business Credit, which is a collateral driven working capital provider that does receivables-based financ ing and asset-based lending.

She’s seen business pick up the last month as it appears that the seemingly never-ending pool of pandemic loans has ended.

“Since COVID hit, there’s been round after round after round of free money from the government, some of which folks needed and some of which they didn’t, but it came re gardless,” she says. “It just sort of kept coming. I think we’re at the end of that. … During COVID, it was ‘why borrow from me if you can get it free.’”

But the company’s collateral driven working capital prod uct is a good fit in times of distress or in times of fast growth. With the complicated economic factors facing businesses these days, Erickson says her phone is getting busy.

“Our clients are either growing too fast or they’re strug gling,” she says. “For whatever reason they don’t fit into the conventional bank financing box.”

A downside of these types of loan products is higher interest rates. Some customers stay with SLR longer than they have to because the company often does deals with few or no covenants, Erickson says. But often, when they can, they’ll find another lender that can offer lower interest costs.

“If you’re looking for a new credit facility and the one the bank is offering has a lot of covenants you think you’re going to trip and be in default, you’re going to want to think long and hard about that,” she says. “It’s easier to look for financing when you’re not under the gun like that.”

Erickson would counsel people to be mindful of how rising interest rates, inflation or supply chain issues might affect them and be realistic about their financial projections for the next couple years. She also wants to see companies come to the table with a well-constructed plan.

“We’re going to want to know if they’ve experienced some recent struggles or they have supply chain issues or their margins have shrunk because their input costs have gone up,” she says.

“Just what is the plan. Be able to articulate the go-forward plan in a credible way.”

18 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

Leadership is lonely. We build your tribe. Find your tribe at www.coalition9.com

Dorothy Bridges retired from her last job at the Federal Reserve Bank of Minneapolis in 2018 after four decades in banking and financial services. She was serving on a few boards, most notably those of U.S. Bancorp and the Metropolitan Economic Development Association (MEDA), while pondering whether there were jobs out there that might lure her back into the workforce.

When MEDA’s previous CEO, Alfredo Mar tel, moved on, Bridges found her answer. The former Franklin National Bank of Minneapo lis president and CEO took the job and has spent the last couple months meeting with stakeholders and determining next steps. She shared some early thoughts with Up size Editor Andy Tellijohn.

Tellijohn: How are things going?

by Andrew Tellijohn

Bridges: Well, it’s like anything else. Transition to new leadership takes some getting used to especially, and I’m talking from the perspective of the staff and other key stakeholders. What makes it a little bit more manageable is the fact that I’ve been in this space for quite a bit of my profes sional career and so at least externally on the key stakeholders, I’m a known entity. So, there’s not that concern of ‘what will they do?’

I think the key external stakeholders have a pretty good sense of my passion for what MEDA does and how it fulfills its mission. So that kind of level setting is less onerous. In terms of staff, there are a couple people that I have known for many, many years and have worked with for many years with my profession as a banker and utilizing MEDA in the past for some of our

20 www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

Twin Cities banking industry veteran Dorothy Bridges came out of retirement to become CEO of the Metro politan Economic Develop ment Association.

bank customers.

And so, the two words that I might use are stabilize and strengthen.

Stabilization because this is a staff that we have to ac knowledge has gone through some significant transition and so committing to them that we will be in a position of stabilization and working quite diligently and with an alacrity to do that.

We’re also experiencing the same things that other corporations are experiencing and that’s attrition for reasons other than conscious transition of the leader ship staff. And so, we’re having to move quite quickly to backfill some key positions. I’m really thrilled that we have the people in place that are doing that for us. And we are meeting with some great results.

Tellijohn: What kinds of positions are you hiring for?

Bridges: There were a couple positions that were open. These were budgeted positions that were added probably in 2022 that we needed to fill.

And then we have individuals who were retiring. We knew that. And so, having that mindset to fill that role is always top of mind for any great chief people officer, right?

Tellijohn: You’ve mentioned your time in the bank ing profession and your passion for the organization, but you also were retired and presumably not desperate for a new role. What made you want it?

Bridges: I retired from the Federal Reserve Bank of Minneapolis in 2018. Part of the retirement really, you know, you think about some of those things that you would love to do and you wouldn’t mind doing if you were called out of retirement.

So, I had that kind of conversation and it’s always been about my passion for growing our communities, particularly BIPOC (Black, Indigenous, people of color) communities, and how I see communities benefiting and growing with what MEDA does.

MEDA helps to build the economy, the local economy. When you have viable, sustainable businesses located in these communities and you have consumers patronizing these businesses you begin to see some physical mani festations of economic viability in these communities.

Creation of jobs is very important for BIPOC communi ties and having businesses who hire from the commu nity at large has always been an important data point for MEDA clients and for MEDA for that matter. So, job creation as well as being a part of an ecosystem that is healthy and growing and thriving,

Tellijohn: What have you got in mind for your goals for this?

Bridges: So, the immediate goal is just to have my feet firmly planted in the organization as the CEO and leading in some key areas, building the relationship with our key stakeholders. Those are our funders; those are our clients. Those are other partners that we work with to make magic happen on behalf of our clients.

As you know, MEDA has several different initiatives and several different programs that we bring to the table when we are dealing with our clients. It’s not just about lending or having capital. It’s about really build ing a strong foundation for businesses as they look at how they want to establish themselves, grow and prosper. Those wraparound services, such as business consulting, are vitally important. And so having that connection with those partners is vitally important to me so that I have a really good sense of the expecta tions. I think I know what the expectations are, but there’s nothing like getting in front of somebody and sitting around across the table from them to hear what they’re saying.

So, that’s job number one. That’s the biggest priority. Of course, the key stakeholder in all of this is of course our board of directors. Getting out and getting in front of the board of directors because they in most instances represent our other key stakeholders, the big corpora tions of our area having people who want to contribute their time, talent, and treasure to keep MEDA’s reputa tion and visibility in those major corporations alive. And so really making sure that I’m connecting with them and helping to really move what we have in our strategic plan along.

Tellijohn: That plan was set in 2020. It’s been a wild couple of years. How do those efforts stand?

Bridges: We’re taking a look at that and how it’s changed. The landscape has changed on MEDA and everybody else. Civil unrest, all of these things. And so, we’re making sure that we are touching what we need to touch in terms of the strategic plan to say how has it changed and where do we need to pivot in order to achieve what we set out to achieve a couple of years ago? And also too, do we need to take a look at what we set out to achieve? Is that even relevant anymore? So, for the first six months, that’s what I’m doing. I’m just sort trying to firmly plant myself.

EDITOR’S NOTE: A longer version of this article will appear on the Upsize website, www.upsizemag.com.

Contact: Dorothy Bridges is president and CEO of the Metropolitan Economic Development Association: 612.332.6332; dbridges@meda.net; www.meda.net; /in/dorothy-bridges-7830446/

www.upsizemag.com NOVEMBER • DECEMBER 2022 UPSIZE

21

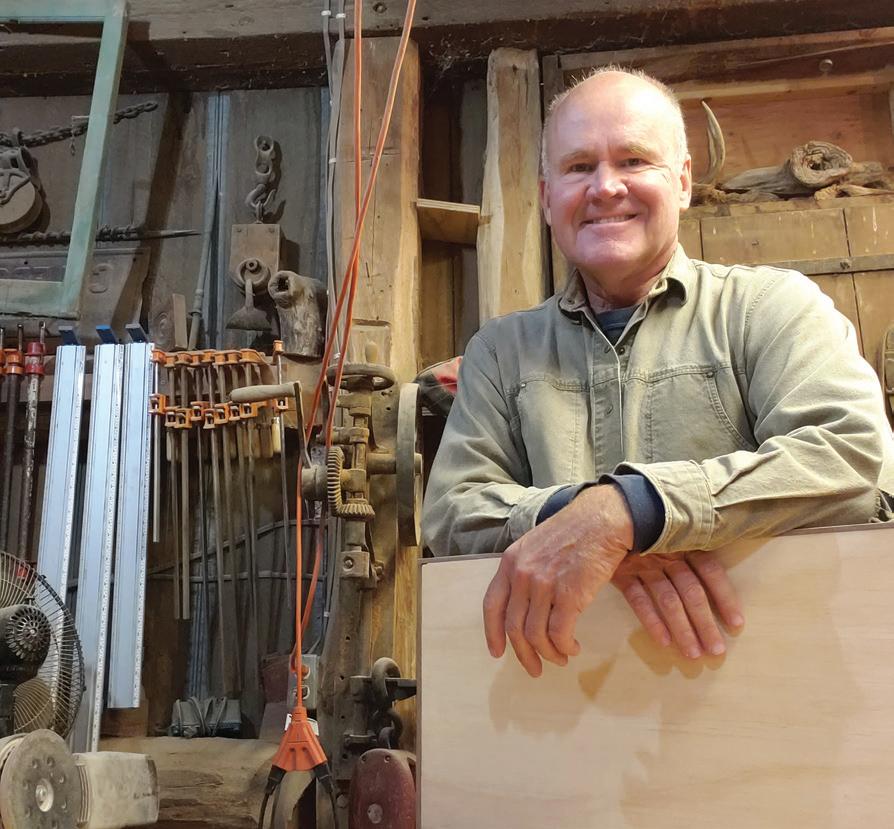

catching up

by Andrew Tellijohn

TOP PHOTO BY JONATHAN HANKIN, BOTTOM PHOTO COURTESY OF THE GRANARY WOODSHOPS

Still building: Blanski left corporate America, never looked back

It’s been 22 years since Tim Blanski and Lisa Catton sold what had been their dream house in St. Paul, left their busy jobs and re-settled in Spring Grove, nearly three hours to the southeast and not far from both the Wisconsin and Iowa borders.

They went in search of a sim pler life and found what they were looking for on a historic hobby farm there where they started The Granary Woodshops.

“Like a lot of people, we wres tled with more, more, more, faster, faster, faster at work and at home, for that matter,” says Blanski, who makes elegant, rustic furniture pieces out of recycled wood. “We just said ‘Let’s not do that.’ And we threw all that away, kind of crossing our fingers and hoping that, well, we’ll find our way.”

What’s the update?

It helped that they didn’t have kids and he wasn’t setting out to build a company that would require hiring employees. He just wanted to do enough projects to bring in some money and stay busy. He’s busy enough where he doesn’t have to market his wares regularly on the show circuit like he did early on, having built up a regular client base.

“That was fairly prescient at the time,” he says of his decision to work on antique, recycled or re claimed wood. “That’s really kind of exploded and become a big deal.”

And he turns down orders when they don’t fit his interests. For example, he has been asked to make kitchen cabi nets, or teak or hickory dining room tables.

“They weren’t building barns out of hickory, they weren’t building build ings out of hickory,” he says. “So, it just isn’t my wheelhouse. I prefer to stick with what I’m good at and I think that’s allowed me to focus.”

Lisa does finish work on some of his projects and maintains a small book keeping and tax prep client list.

“So, you can’t ask for much more than that,” he says. “You’ve got every thing you need all under one roof.”

Never

plans to stop Blanski is in his early 60s and they have a lot of friends they keep in touch with from the Twin Cities. Many of them are talking about retirement, but uncertain of what to do after leaving the workforce. Blanski says that’s not a problem for him — he sees himself doing his woodworking through his entire life.

“I always hope to have some work to do,” he says. “It’s always work that is generating revenue, which is a good thing. We continue to pay the bills. We moved ourselves years ago to basically a debt-free environment. We own our home, we own the property. And so, our bills are low.”

One thing working alone did was shield the couple from the worst of the COVID-19 pandemic. There were no worries about going into work each day

www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022

22

Tim Blanski and Lisa Catton left busy jobs two decades ago to resettle on a hobby farm in Spring Grove, MN, where he now makes rustic furniture out of recycled wood.

because he works alone in a building just across his driveway.

“COVID almost didn’t even happen in our life because we just stayed here and live on the farm anyway,” he says. “There was no quarantine and all that other stuff.”

Lessons learned

One thing Blanski wishes he’d picked up on more quickly was sticking to his niche. At the beginning, he spent a lot of time making figurines and characters out of wood that he had to sell for $45 or $65.

“You can’t make a living doing that,” he says, adding that it took a couple years of fine-tuning the model to real ize he wasn’t pricing his larger pieces high enough and shouldn’t spend his time on those smaller items.

The inflexible work rules at the time also played a role in the move. One of the reasons Catton was willing to leave

her job, Blanski says, was Catton’s desire to work from home for a day or so each week. As incredible as it sounds now, her request was denied. “She was looking for a day,” he says. “Well then,

boom. One day everyone is at home and employers kind of all of a sudden discovered that it’s not actually impos sible, and maybe a lot of people work better.”

23 www.upsizemag.com NOVEMBER • DECEMBER 2022 UPSIZE

The Granary Woodshops

Description: : Maker of elegant rustic furniture

Headquarters: Spring Grove, MN

Founded: 2001

CEO: Tim Blanski Employees: 2 Website: www.granarywoodshops.com

Whiskey on the side

While he’s long committed to his woodwork, Blanski did get involved, if only briefly, in a side project. About five years ago he stumbled upon Christian Myrah, who was looking to start a bourbon distillery.

Blanski had recently been on a barbecue trip in Texas that involved visiting a couple distilleries, so when he found out about Myrah’s plans, he said they should keep in touch.

“I’d love to sell that story all day long,” he says

About a half-year later, they ran into each other again in the grocery store parking lot and Myrah’s still had been delivered just the day before.

“I went over there the following day and I basically never left,” Blanski

says. “I said ‘if you’re making whiskey, I’m going to be a part of it, whether you like it or not.’”

Soon after, the RockFilter Distillery was born. One of two other minority partners sold Blanski enough shares to provide 10 percent ownership in exchange for some early-stage market ing and branding efforts. It’s become an award-winning product.

In keeping with his downsized life style, when the chase for growing the start-up Rock Filter Distillery became more work than expected, Blanski sold his shares. But he enjoyed taking part in the company’s early stages.

“It was unbelievable. It was really fun, really exciting coming back around full circle,” he says. “It was a reacquainting myself with the fact that growing a busi ness, a growing business, and a business that hires people and makes a product and tries to sell it is way difficult. And that’s not what I came down here to do.”

But he remains an outspoken fan and brand advocate.

“I’m officially,” he says, “an unpaid, fully equipped-with-bourbon brand ambassador for RockFilter Distillery.”

Contact: Tim Blanski owns The Granary Woodshops: 612.499.0826; thefarm@granarywoodshops.com; www.granarywoodshops.com

‘Let’s

Tim Blanski The Granary Woodshops

“�Like a lot of people, we wrestled with more, more, more, faster, faster, faster, at work and at home for that matter. We just said,

not do that.’ And we threw all that away, kind of crossing our fingers and hoping that, well, we’ll find our way.”

www.upsizemag.com UPSIZE NOVEMBER • DECEMBER 2022 24

catching up

PHOTOS COURTESY OF THE GRANARY WOODSHOPS

BANK

UPSIZE RESOURCE DIRECTORY

BOOKKEEPING

CFO SERVICES

Crown Bank

6600 France Avenue South, Suite 125

Edina, Minnesota 55435

Ph: (952) 285-5800

www.crown-bank.com • Jeff Wessels, President & COO

At Crown Bank, we want to be partners in your possibilities. Because possibilities are what the future is made of. From something as personal as growing your savings, to something as big as growing your business, our bankers and staff have the expertise and energy to partner with you to make that happen.

Three Pillars Bookkeeping

838 S Lake Street, Forest lake, MN 55025 Office 651-899-2002 www.threepillarsbookkeeping.com

We offer a full range of bookkeeping, Payroll and accounting services, such as entering and paying bills, invoicing, recording deposits, reconciliation and updating vendors and customers. We’re your outsourced CFO, affordable to retain with no loss of quality.

Integrated Consulting

Cathy Sedacca, managing director 612-802-1784 (c)

Cathy.Sedacca@integrated-consulting.net www.integrated-consulting.net

Integrated Consulting delivers Chief Financial Officers to small businesses on a fractional basis. From projections to cash flow tools to assistance with all things financial. We provide 30 years of expertise on a small business budget.

BANK

Highland Bank

Rick Wall, CEO | 952.858.4753

Troy Rosenbrook, President | 952.858.4810 952.858.4888 | www.highland.bank

Founded in 1943, Highland Bank is focused on business lending and is an SBA “Preferred” Lender, making us uniquely qualified to help your business obtain the financing it needs expeditiously. Work directly with the decision-makers who will treat you like a business partner. Member FDIC.

BUSINESS BROKER

Sunbelt Business Advisors

Peggy DeMuse, pdemuse@sunbeltmidwest.com 651-288-1627

Lisa Meyer, lmeyer@sunbeltmidwest.com 612-361-4918 www.sunbeltmidwest.com

Thinking about buying or selling a business? Sunbelt is the world’s largest seller of private companies. We work with business owners to help them under stand the current value of their business and how to maximize their net proceeds at the time of sale. Sunbelt will provide business own ers with a completely confidential, no-obligation value range.

COMMERCIAL PHOTOGRAPHER

Tom Dunn Photography

308 Prince Street Studio 242

651-368-2047 www.tomdunnphoto.com Tom Dunn tom@tomdunnphoto.com

Tom is a commercial photographer who has been help ing businesses tell their unique story with photographs for websites and marketing materials since 2006. Tom works closely with his clients to understand their business and branding strategy and creates images that support their mission and success.

COMPUTER CONSULTING

Intertech

1575 Thomas Center Drive • Eagan, MN 55122 www.intertech.com • Ryan McCabe at rmccabe@intertech.com or 651.288.7000

Intertech consultants are leading software developers who focus on more than simply “heads down” programming. We provide comprehensive software services – consulting, project delivery and mentoring – for all leading technologies, most notably Java, .NET and mobile. Intertech consultants are highly experienced and among the IT industry’s top contributors at conferences, technology journals and user groups.

EXIT STRATEGIES

Exit Planning Institute

Twin Cities Metro Area chapter 763-208-9119 exit-planning-institute.org

Jessica Hawthorne, Administrator admin@e-officeconnection.com

https://www.poisedforexit.com/

Through the Certified Exit Planning Advisor (CEPA) credential, the Exit Planning Institute provides professional advisors with the content, tools, and training needed to gain more access to business owners, strengthen relationships, and become the most valued advisor.

Member FDIC

Follow us on

ADVERTISING SECTION NOVEMBER • DECEMBER 2022 UPSIZE 25 www.upsizemag.com Show Content • Best Practices to Grow Enterprise Value • Business Owners Share their Exit Stories • Learn what it takes to exit on your terms! • Guests share need-to-know advice for lucrative outcomes • Episodes are all under 30 minutes Subscribe on Apple, Spotify, Google, iHeart, Stitcher Sponsorship Opportunities! Download episodes and order the book!

UPSIZE RESOURCE DIRECTORY

LAW FIRM

Winthrop & Weinstine, P.A.

Capella Tower, Suite 3500

225 S. Sixth St. • Minneapolis, MN 55402 Tel: 612.604.6400 • www.winthrop.com

Winthrop & Weinstine is a business with a deliberate culture of enterprise and fresh thinking. Our clients have big ideas, and our lawyers help turn those ideas into successful businesses. We represent clients in the early stages of their business in matters such as entity formation, capital raising, employment matters, vendor and customer agreements, and others. We provide counseling as your business grows, and work closely with clients to smooth the path to success.

HUMAN RESOURCES

Optima HR Solutions

Steve Schad, sschad@OptimaAdvisoryllc.com Ph: 651.587.0588 www.OptimaAdvisoryllc.com

Attracting and retaining the right people will fuel your growth. Take the guesswork and headache out of the people side of your business with help from Optima HR Solutions. Smart HR will get you to the next level - assessment, strategy, fractional HR leadership, and tactical HR support and recruiting.

LEADERSHIP DEVELOPMENT

Prouty Project

6385 Old Shady Oak Road, Suite 260

Eden Prairie, MN 55344

952.942.2922 | www.proutyproject.com

Kari Baltzer | stretch@proutyproject.com

Our leadership development engagements and cohort-based leadership programs – Prouty L3 and Prouty i•will – link behavior to team performance in your workplace through the lenses of Leading Self, Leading Others and Leading the Business. We focus on STRETCHing participants to lead business within internal and international divisions. Give us a call or stop by.

MERGERS & ACQUISITIONS

Lingate Financial Group

7575 Golden Valley Road, Suite 100 Minneapolis, MN 55427

763-546-8201 www.Lingate.com

Greg Loeschke — Managing Principal

Founded in 1945, Lingate Financial Group is a leading provider of lower middle market merger & acquisition advisory services, representing privately held businesses of all types with revenues of $5 – 50 million. Lingate helps business owners with market-based valuations, business sales, mergers, acquisitions, recapitalizations, and internal transitions among family members, partners and management. We get deals done.

GROW OR DIE

Move your business forward with investment capital generation, deep-level network connections and strategic refinement consultation from Brimacomb and Associates. We partner with emerging companies and professional services firms to offer unparalleled access to professional resources, executive suites and financing sources. www.brimacomb.com 612.803.3169 • rick@brimacomb.com

MERGERS & ACQUISITIONS

True North M&A

Peggy DeMuse, pdemuse@sunbeltmidwest.com Lisa Meyer, lmeyer@sunbeltmidwest.com www.tnma.com

We help business owners achieve their exit goals. True North Mergers and Acquisitions serves companies with $5 million to $150 million in revenue and their strategic advisors. We specialize in business owner exits, business valuations, and acquisition services in the lower middle market. If you are considering exiting your company, contact our team today.

SBA LENDER

Highland Bank

Troy Rosenbrook, President | 952.858.4810

Kim Storey, SBA Lending Manager | 952.858.4590 952.858.4888 | www.highland.bank

Founded in 1943, Highland Bank is focused on small business lending and is an SBA “Preferred” Lender, making us uniquely qualified to help your business obtain the financing it needs expeditiously. Work directly with the decision-makers who will treat you like a business partner. Member FDIC.

Follow us on

SBA LENDER

21st Century Bank

2335 Highway 36 W Suite 202 Roseville, MN 55113 612-372-2178 • www.21stcb.com

At 21st Century Bank, we know what it takes for businesses to survive, grow, and prosper in today’s market. For over 100 years, we have been your community partner. A family-owned bank, with expertise in all SBA and conventional lending programs covering all stages of your business. We tailor solutions that respond to your unique business and banking needs.

SBA LENDER

Sunrise Banks

David Reiling, CEO

Phone: 651.265.5600 www.sunrisebanks.com

Sunrise is headquartered in St. Paul, MN, and has four retail banking branches located in the urban core of Minneapolis and St. Paul. Its primary business lines include: Commercial Lending and Leasing, Relation ship Banking, Treasury Management, Prepaid Cards, Fintech Partnerships, New Markets Tax Credits, and Small Business Administration Lending.

Member FDIC

ADVERTISING SECTION 26 UPSIZE NOVEMBER • DECEMBER 2022

www.upsizemag.com

STRATEGIC PLANNING

Prouty Project

6385 Old Shady Oak Road, Suite 260

Eden Prairie, MN 55344

952.942.2922 | www.proutyproject.com

Kari Baltzer | stretch@proutyproject.com

We start with a blank sheet of paper to elevate your clarity on vision and purpose, create alignment in your strategy to achieve your vision and gain commitment to execute. What are your “market, product/service, people, and financial” strategies over the next 1-5 years?

Can you articulate your strategic plan on one page?

Join us in our Creative Think Tank to stretch your thinking and ignite your creativity.

TRANSITION PLANNING

KeyeStrategies

Minneapolis, MN

Keyestrategies.com 763-350-5563

Julie Keyes, Founder/CEPA

“KeyeStrategies LLC advises business owners in Transition and Exit Planning. Julie Keyes is both a Certified Exit Planning Adviser (CEPA) and Value Growth Adviser. She is also a faculty member for the Exit Planning Institute’s Global organization and President of its local Chapter.”

venture capital

Brimacomb + Associates

TCF Tower, Suite #1600, 121 South Eighth St., Minneapolis, MN 55402 612-803-3169 * www.brimacomb.com

Rick Brimacomb, rick@brimacomb.com Chief Strategy and Relationship Officer

Results-oriented advisory firm with unparalleled access to executive suites and financing sources. Emerging companies and established professional services firms rely on our depth of knowledge and deep-network connections to grow client lists, assemble project resources and secure new sources of funding.

WEALTH MANAGEMENT

JNBA Financial Advisors

8500 Normandale Lake Blvd., Suite 450

Minneapolis, MN 55437

952.844.0995 www.jnba.com

Cärin Viertel, Director of Client Services