Value Chain Asia Magazine | Vol.2 Issue No.3 (2024)

“Welcome to our last issue for 2024. No year end season is complete without most businesses asking what the next year will look like, and more importantly, is there growth to look forward to? In this issue, we focus on Southeast Asia and startups. I get asked constantly who we are targeting for Value Chain Asia. Our audience is the community of professionals who work in supply chain and logistics. We aim to deliver a digital media platform helping to connect these groups, whether it is the new professionals looking for information about the industry, the mid-career professional who is seeking career growth and seeing how to get up to speed on latest trends and finally we profile leaders and companies who are sharing their latest updates with you, our dear reader.

In this issue, we put the spotlight on Southeast Asia. One would have to be living under a rock to not have read the news of DSV’s successful acquisition of Schenker. Amid the creation of logistic giants, where global players such as DHL and Kuehne and Nagel dominate, we ask the question, is there still room for startups to flourish in the logistics space? Does technology help spark new, innovative services to plug the gaps possibly peaking through the shadows of behemoths? Moreover, in an era where sustainability has become a focal point for businesses, would a focus on sustainability naturally help new startups get a foothold in the market, we share insights with Jakarta-based Sealog who is leading the change towards a more sustainable supply chain.

Southeast Asia’s growing importance in the global supply chain doesn’t stop with just a flourishing startup scene. The region is undoubtedly increasingly attracting investors as sourcing strategies evolve. With trends moving towards near-shoring and reducing dependency from a singular China option previously, we examine if Southeast Asia is ready to take on this critical role, by taking a closer look at SIJORI and highlighting its potential strategic importance.

No update on supply chain is complete without a lens on technology. Industry 4.0, or the 4th Industrial revolution, continues to bring innovations in this realm. As automation, artificial intelligence, big data and other tech advances spring up, we take a look at how industry 4.0 is changing supply chains. Within automation, we are pleased to share an insightful article from OnRobot on how robots, particularly cobots (don’t we all love new words being invented to catch up with the invention of all things new), are being introduced to modernize the operations of warehouses.

The logistics and supply chain industry connects people frequently through conferences, seminars, online or in

person. I found these invigorating in the connections we make in thought and in the networks we create with like-minded professionals. No supply chain conference or seminar is complete without the topic on the importance of lean supply chains- I learnt plenty in the recent two industry events I attended where lean was talked about. Given how disrupted the supply chain environment is and continues to be, we explore whether lean supply chains are truly achievable or if they remain to be more of a myth versus reality.

This issue comes at the end of the year. No matter which holiday you celebrate around November, December and January, the year-end season of festivities is afoot. Supply chain management plays a crucial role during every holiday season by ensuring the smooth flow of goods to meet heightened consumer demand. We look at the role supply chain management plays in ensuring a season of prosperity or panic, depending on how well laid plans play out.

Finally, no sourcing strategy is complete without an ocean freight option. In this issue, we examine Asia’s biggest seaports, the vital hubs in the global supply chain, and their significance in the ability to connect with global markets.

From all of us at Value Chain Asia, we wish you a peaceful holiday season ahead and happy reading!

For editorial inquiries, contact editor@valuechainasia.com

Sincerely,

Wee Wee Chia Co-Editor-in-Chief

FOUNDER, CO-EDITOR-IN-CHIEF

AMOS TAY

SENIOR EXECUTIVE (MEDIA)

MATTHEW PARRA

WEE WEE CHIA WHO ARE WE?

MULTIMEDIA ARTIST

MARK BRANDO BALOLOY

PRECIOUS ROMATICO

CO-EDITOR-IN-CHIEF

STAFF WRITER

TRISHA ANJANETTE BALLADARES

SHERAZ AHMED

LLOYD CAB

MUHAMMED YASSIN

GRAPHIC DESIGNER

YASMIN ISMONO

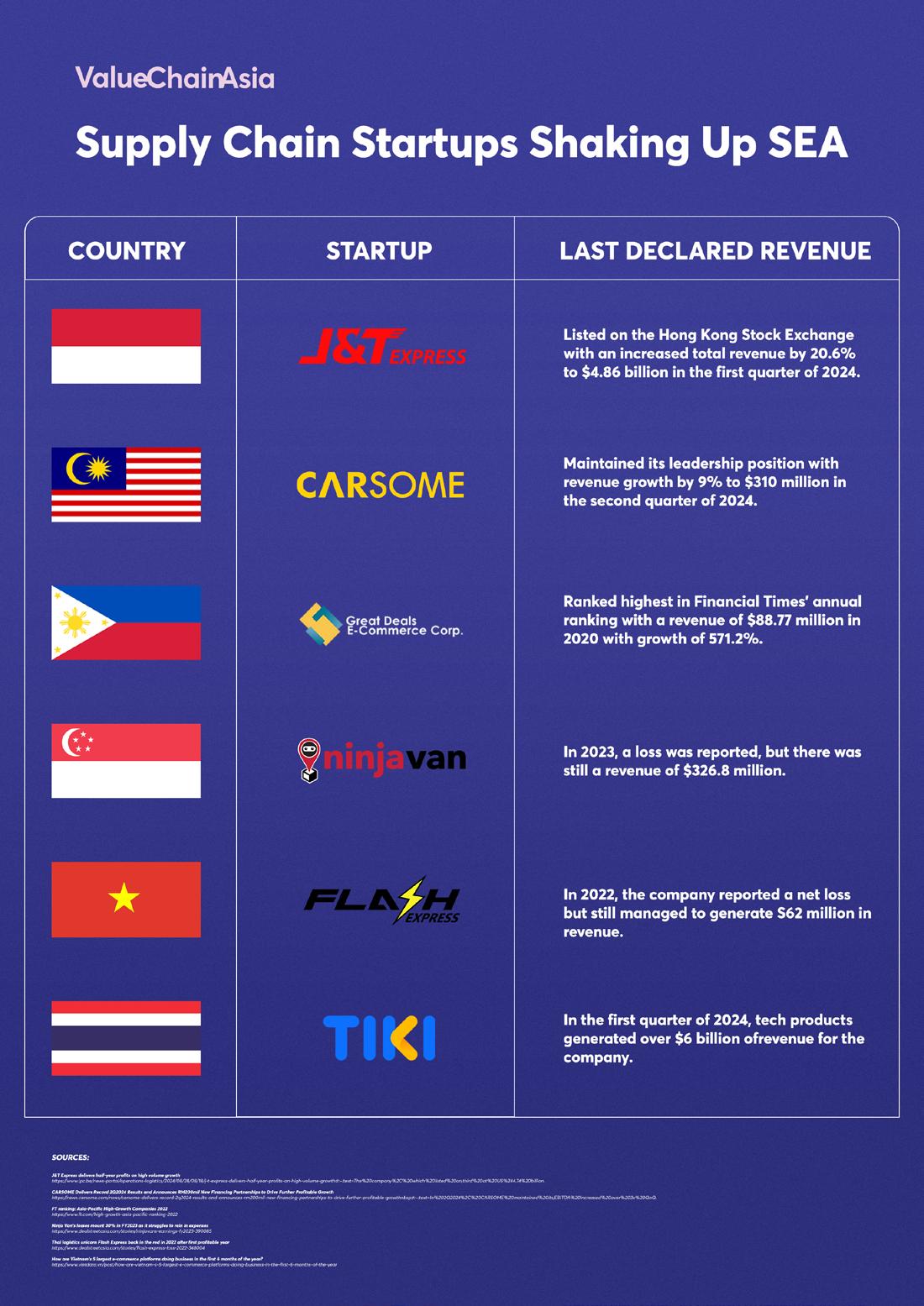

SEA startups grow amid corporate giants and tech advancements

Sealog: How a small start-up is pioneering sustainable logistics in Indonesia

16: Sijori’s Impact: What Singapore manufacturers and distributors need to know

21: Are Lean Supply Chains a myth? Examining resilience amidst disruptions

25: Building the future: Data centers in SEA set to reshape regional supply chains

SUSTAINABILITY

Redefining sourcing in Asia: Navigating the new era of regionalized and resilient supply chains

34: Asia’s Supply Chain 4.0: Thriving in the Fourth Industrial Revolution

38: Logistics, Small and Medium Enterprises, and an Unappealing Outlook: Is there a Solution

SUPPLY CHAIN & MANUFACTURING

42: The holidays are coming; What does supply chain management have to do with it?

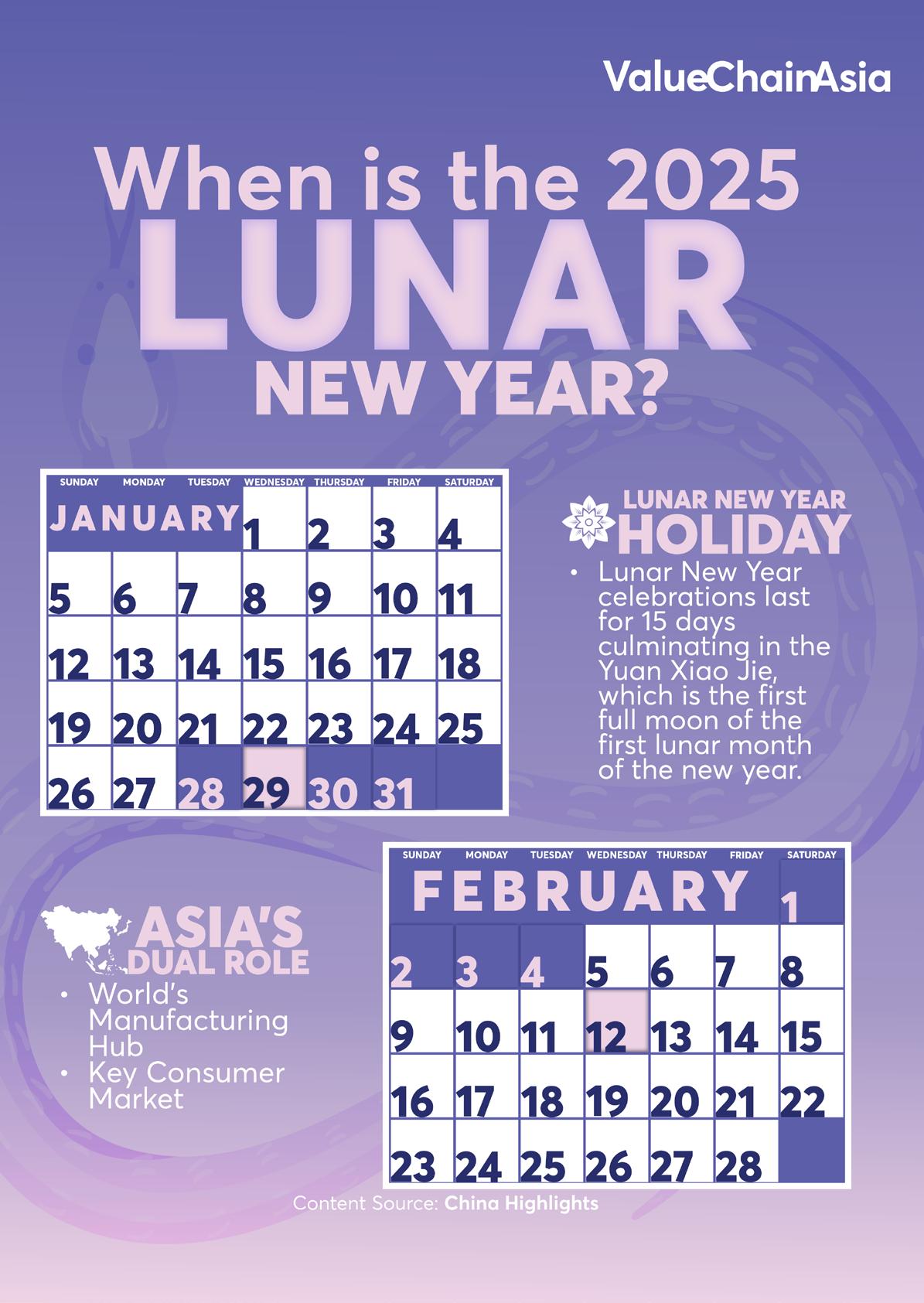

45: When is the 2025 Lunar New Year?

46: Biggest seaports in Asia and the significance they hold on the supply chain

THE

SEA startups grow amid corporate giants and tech advancements

BY MATTHEW PARRA

Asthe global supply chain evolves, one trend stands out: industry giants are consolidating at an unprecedented pace. Companies that were once formidable on their own are now combining forces, creating corporate giants with vast global reach and unmatched resources. Simultaneously, the advancement of technology is changing supply chain dynamics.

Automation, artificial intelligence and data-driven logistics are reshaping operations and forcing all players to adapt.

But amid these shifts, the question arises: where do startups fit into this ecosystem? Can they thrive in a space where larger corporations seem to have an unbreakable hold, or will they remain on the fringes?

Giants in the supply chain: Still dominant, but for how long?

Traditional players in the industry continue to dominate through large-scale mergers and acquisitions. A standout example is DSV’s record-breaking $16 billion acquisition of Schenker from Deutsche Bahn. This marked the company’s largest transaction to date.

Similarly, CEVA Logistics’ acquisition of Bolloré demonstrates how these companies are expanding their global footprint to stay competitive.

These industry giants offer a wide range of supply chain services. This makes them capable of employing thousands of people worldwide and generating billions in revenue, which strengthens their market position and influence.

Economies of scale, through massive assets, have been their key competitive edge ever since. This raises the entry barriers in the supply chain industry. However, technology is changing the playing field.

According to a report by Deloitte, while these giants have a firm grip on the industry, their legacy systems and large operations make them slower to adapt to the rapidly changing tech landscape. This is due to more traditional peers lacking the flexibility and speed to respond to quickly changing dynamics.

This is where startups are stepping in, leveraging their digital-first approach to gain ground. Startups are capitalizing on these trends with the rise of Internet-ofThings, big data analytics and digital platforms.

A Deloitte survey showed that the business models of these startups are uniquely tech-driven. They are built

“Logistics is notorious for being an old-fashioned business, but changing shipper expectations, new market players, and eroded margins have prompted industry leaders to reassess strategies, says Freightos CEO Zvi Schreiber.

on agile, asset light and tech-driven infrastructure. This enables them to rapidly adapt to market needs, scale up efficiently and offer services without the heavy capital investment.

Unlike their traditional counterparts, new players take a more focused approach. They focus on providing very specific types of services and solutions. For example, some offer platforms for price comparison and booking services. While some companies provide short-distance transport within the city.

As such, many of these startups play a role in freight brokerage, last-mile delivery, convenient solutions and supply chain analytics.

Startups making their mark in Southeast Asia

This technological shift is seen in Southeast Asia’s (SEA) booming startup ecosystem. According to the Association of Southeast Asian Nations, more than 10 SEA startups have become unicorns since 2012. Unicorns are startup companies valued at over $1 billion.

Venture capital firm Jungle Venture also reports that startups in the region had a combined valuation of $340 billion. The firm predicts that the number will triple by 2025.

“ If you look at the growth rate of the last 3 to 5 years in Southeast Asia, if it continues, which by all means it will, you’re going to head to a trillion dollars even before 2025, says Jungle Venture CEO Amit Anand.

This growth stems from a combination of factors. With over 460 million people connected to the internet as of 2022, the region has an 80% internet penetration rate. Alongside this digital boom, SEA has seen a flood

of support from both private and public sectors. Governments across the region have supported startups through policy, while investments from tech powerhouses like Alibaba and Tencent have fueled innovation. Since 2015, over $15 billion has been invested in SEA’s startup ecosystem.

Another driving force behind this momentum is the tensions between the United States and China. This has made SEA an attractive alternative for those seeking stability and growth outside the two global powerhouses.

READ: Chinese companies turn to SEA amid China’s economic, regulatory challenges

As a result, the region’s emerging markets have become hotbeds of opportunity, especially in e-commerce.

According to the International Trade Administration, the region’s e-commerce market is expected to reach $330 billion by 2025.

Notably, asset-light logistics startups are taking the stage in SEA. Companies such as Logivan, Lalamove and Ninja Van are thriving in this market by focusing on logistics without heavy reliance on physical assets like trucks or warehouses.

Instead, they focus on digital solutions that optimize logistics, enhance delivery efficiency and enable rapid scalability. By leveraging software, these startups match independent truckers with available freight or tap into drivers’ personal vehicles to power their delivery networks.

One of SEA’s most recent logistic unicorns is Indonesia’s J&T Express. The express delivery provider was valued at $8 billion, ranking as the 16th-largest unicorn in the world.

Where are startups thriving in the value chain?

The internet economy of Southeast Asia is projected to reach $295 billion by 2025, offering significant opportunities for tech-driven startups in the supply chain industry.

One area where startups are making a significant impact is digital freight solutions. These solutions leverage technology to optimize and streamline the freight process, from booking to delivery. For example, Ninja Van, a Singapore-based logistics startup, is leading the way with its digital-first approach to last-mile delivery.

The company has developed tech-driven platforms to optimize delivery routes and directly connect online merchants with customers, providing a more efficient and cost-effective logistics service than traditional players.

Another key player is the Hong Kong startup Lalamove. They operate in SEA and provide on-demand logistics through a mobile app, connecting businesses with a fleet of drivers for quick, local deliveries.

Lalamove’s asset-light model allows it to quickly adapt to changing customer demands, offering a level of flexibility that larger logistics companies often lack.

Startups are also thriving in the supply chain visibility and analytics sector. For instance, Singapore-based

Parcel Perform is revolutionizing shipment tracking by providing real-time tracking and analytics. This enables businesses to monitor their entire supply chain from start to finish.

A critical service they provide is their delivery prediction model, consolidating past data and providing customers with expected delivery dates. They also offer analytics on how well multiple carriers are performing. This transparency is crucial for companies seeking to optimize operations.

Furthermore, startups are addressing sustainability and green logistics. Companies like Sealog in Indonesia focus on reducing carbon emissions through electric cargo bikes and railways. They serve as delivery agents for agritech and retail companies, delivering goods directly to customers.

A supply chain ecosystem for everyone

The supply chain industry is evolving to become more digital. While large corporations still hold significant power due to their scale and resources, startups are carving out spaces to complement and enhance the existing value chain.

By focusing on innovation and tech-driven solutions, startups are proving that there is room for everyone in this evolving ecosystem. V

Sealog: How a small start-up is pioneering sustainable logistics in Indonesia

BY MATTHEW PARRA

In an era where sustainability has become a focal point for businesses, Jakarta-based Sealog is leading the change towards sustainable supply chains.

Mathan Kumar, the founder and CEO of Sealog, emphasized the importance of greener supply chains. He stated the necessity

of returning the planet to future generations as it was entrusted to us

In an interview with Matthew Parra, a writer at Value Chain Asia, Kumar provided insights into Sealog’s initiatives in delivering green logistics in Jakarta.

Established in 2010, Sealog started its service to reduce carbon emissions through railways. They provided shipping containers from East to West Java, covering around 900 kilometers. Early clients included notable names such as Toshiba and sugar producers.

By 2013, Sealog expanded its operations by introducing its trucks. They later shifted to focus on last-mile delivery with their trademark e-cargo bikes.

“From that period of time we thought of providing a unique service which can be a sustainable one. That was when we invented our own cargo bikes and started to provide door to door services to various retail companies, said Kumar

Since 2019, Sealog bikes have traveled over 150,000 km in West Jakarta saving 2,300 kg of carbon emissions. This is equivalent to 31.7 flight hours, 33 mature trees, 476 liters of gasoline and electricity to power 1.7 homes for a year.

RELATED: The 3R in the “Go Green” initiative: Can it improve e-waste management?

Sealog’s all-in-one delivery solution

Sealog’s fleet has a variety of bikes and e-bikes. However, its standout feature is the custom-designed electric cargo bikes, which are unmatched by any company in Indonesia.

These unique bikes are fixed with a cargo box at the front, capable of holding 35 kg of cargo. Powered by 1000watt hub drives, the bikes can reach up to 50 km per hour and cover a distance of 120 km.

The cargo box features thermal insulation and a hygrometer. It provides optimal cold storage and humidity control.

These bikes produce zero emissions and are easy to use, making them ideal for urban spaces. They can hold various goods, and their small size enhances visibility, improving safety and ease of locating riders.

Their zero-emission output and adaptability for urban spaces make them highly competitive in the industry. The compact design enhances visibility and improves rider safety while delivering goods.

“Our bicycles we made it to have a box in front that can carry 50 kilos. So it is very easy to move in every place. So I don’t think they are stuck in any part of the traffic. [They are] much faster than motorcycles because we don’t have many rules and regulations.” added Kumar.

In 2024, Sealog started developing new bike models. The latest versions include designs capable of carrying up to 200 kilograms, with cargo boxes mounted at the rear.

Beyond selling bikes, the company also reduces emissions with its electric box trucks. The trucks are provided on a monthly rental basis.

Recently, Sealog is also looking to integrate its 20 and 40-foot containers back to its operations. The company is looking to travel through East Java via railway as it once did in 2010.

“The railway gives environmental support and reduces Co2 by 300-400 kg per trip. So the railway is much more efficient,” added Kumar.

RELATED: Is the Asian Railway Shipping Industry Profitable?

This commitment to sustainability is also seen in Sealog’s diverse service sectors. More than its vehicles, they also provide services directly to businesses.

The Sealog riders

At the heart of Sealog’s operations are their riders. Unlike its competitors, Sealog offers a fixed monthly salary, providing financial stability and enhancing service quality.

“When it comes to Sealog, we should give our riders a monthly salary. Because giving the whole value is very important. [This approach has been instrumental in attracting customers], as this has enabled us to partner with companies such as Decathlon and Ikea. Kumar stressed.

To Sealog, a stable monthly salary for the rider was crucial to ensure the rider’s prompt and consistent response. This was essential to their operations because they provided a monthly subscription service to companies like Decathlon.

This approach has driven up operational costs for Sealog, but the company remains committed to supporting its riders and aligning with the Sustainable Development Goals (SDG).

“So when we talk about our SDG goals, this happens to contradict with the cost price because you have to pay a full wage salary for your employees. You cannot pay them on a call service like Grab and other companies. So that leaves the costing price for us to be quite expensive. [Especially] when it comes to the environment[al] perspective in last-mile-delivery.” added Kumar

A look ahead

“So this is where we would like to revamp and modify everything when it comes to the delivery. Because revenue cannot be stuck,” says Kumar.

sustainability and a deep commitment to community and environmental values. As the world continues to grapple with the impact of climate change, initiatives like Sealog’s offer hope and a path toward a more sustainable future.

“We get free oxygen and free plants; that’s why I hope leaders in bigger places don’t take all the resources for granted. I hope green delivery will always flourish in all companies, Kumar ends.

Founded in 2010 by Mathan Kumar, Sealog is a Jakarta-based logistics company leading the way in sustainable last-mile delivery. Starting with rail transport, Sealog now focuses on zero-emission e-cargo bikes, cutting carbon emissions by over 2,300 kg since 2019. Serving corporate clients through a subscription-based model, Sealog partners with major brands like Decathlon to deliver eco-friendly logistics solutions across Indonesia. Value Chain Asia is excited about Sealog’s potential to reshape logistics in the region, combining efficiency with eco-conscious solutions.

ABOUT SEALOG

BUSINESS AND ECONOMY

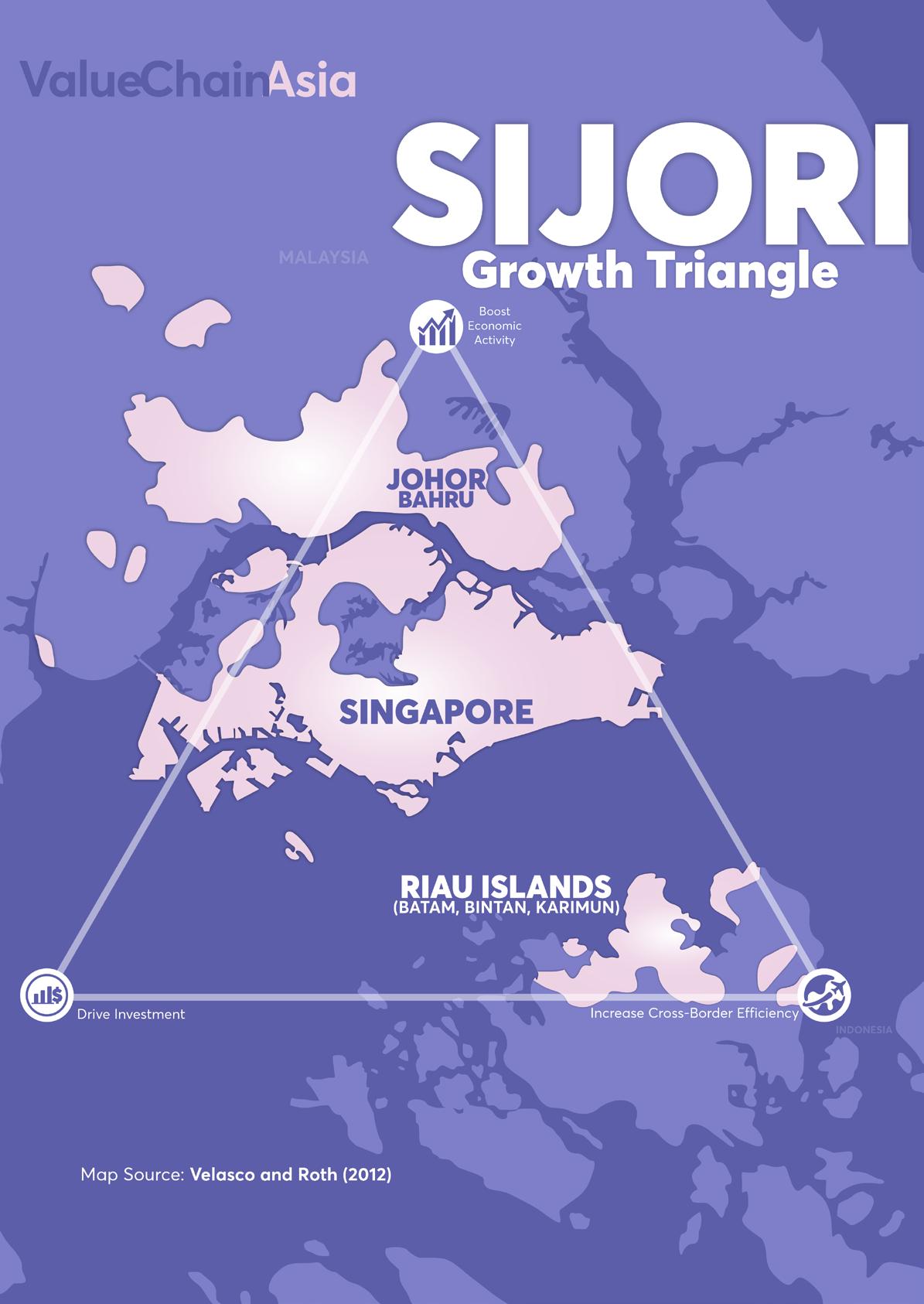

SIJORI’s Impact: What Singapore manufacturers and distributors need to know

BY TRISHA ANJANETTE BALLADARES

The SIJORI Growth Triangle—a collaboration between Singapore, Johor (Malaysia), and the Riau Islands (Indonesia)—has been positioned as a strategic partnership to bolster economic activity, drive investment, and increase cross-border efficiency between the three regions

As an alliance between three distinct countries, SIJORI presents unique opportunities and

challenges for Singapore-based manufacturers and distributors. With increasing production costs in Singapore, the initiative holds potential as a cost-effective alternative for businesses in lower-value-added industries. However, the practicalities of navigating customs, varying regulations, and limited infrastructure raise important questions about SIJORI’s viability.

Here’s an in-depth look at SIJORI’s impact, what to anticipate, and what Singapore’s manufacturers and distributors need to know.

Anticipated Challenges for Singaporean Businesses in SIJORI

SIJORI’s multi-country nature inherently brings challenges that differ from single-country economic zones like China’s Greater Bay Area (GBA), which involves only cities within China, such as Hong Kong, Guangzhou, and Shenzhen. In the SIJORI triangle, each region operates under different national regulations, customs procedures, and legal systems. This creates a layer of complexity in cross-border activities, as each country’s standards may differ on labor laws, environmental regulations, and even safety protocols.

Unlike GBA’s relative ease with shared governance structures and a unified customs approach, SIJORI must bridge three distinct administrations.

Singaporean companies operating within SIJORI must stay vigilant in understanding and complying with these differing regulations. For instance, Malaysia’s labor laws may differ significantly from those in Indonesia, affecting labor cost expectations and hiring practices.

Additionally, customs processes are not harmonized, which could lead to delays or added paperwork. For manufacturers and distributors, such regulatory disparities may increase administrative burdens, adding extra layers of compliance requirements that can slow production timelines and increase costs.

The Customs and Regulatory Bottleneck: Logistics Companies’ Expectations

A streamlined customs and regulatory process is vital for logistics companies and shippers to ensure that goods move smoothly across borders. In the context of SIJORI, some regulatory adjustments and support from each country’s government are crucial to achieve this efficiency.

For example, the Singapore Ministry of Trade (MOT) might explore ways to establish clearer customs frameworks, potentially advocating for special trade zones or bonded warehouses that allow easier movement of goods between the three areas.

One possibility is for SIJORI to adopt a customs agreement similar to the ASEAN Single Window, which promotes paperless trade and eases customs clearance procedures. Such a framework could reduce port waiting times and simplify customs paperwork, creating a more conducive environment for logistics operations.

Logistics companies also hope that government bodies within SIJORI will provide better digital solutions for tracking shipments across borders. A unified system could allow stakeholders from each country to monitor goods and documents as they progress through customs,

reducing paperwork and the potential for errors.

The Absence of Target Investment Figures: A Cause for Concern?

No target investment amounts for SIJORI were announced during the Supply Chain Connect 2024 event by the Singapore Economic Development Board, a point a Singapore government agency raised with the Ministry of Finance. The lack of clear investment goals or financial commitments might indicate the infancy of plans and the implementation stage in the SIJORI initiative’s feasibility

READ: Singapore announces second airport logistics park to strengthen global transshipment role

While such projects generally announce target investments to signal commitment and attract interest, the omission could suggest underlying difficulties in setting realistic financial benchmarks.

One possible reason for this is the logistical and regulatory complexities mentioned earlier. Setting precise investment goals could be challenging without a clear framework for harmonized regulations and customs processes. The absence of investment targets might also mean that governments are cautious, opting to assess investor interest and regulatory alignment before committing to specific financial figures. This ambiguity may make it challenging for Singaporean manufacturers to gauge SIJORI’s stability, leaving some companies uncertain about when—or if—they should begin operations within this zone.

Investment Interest and Research: Can Companies Gauge Financial Commitment?

Specific companies’ interest in SIJORI could be observed through branding and logos at the event, but the absence of published investment amounts adds an element of uncertainty. While direct investment figures are not always disclosed in public forums, companies can monitor industry news, government announcements, or media reports for indicators of financial commitment.

Singaporean manufacturers and distributors can also keep tabs on other businesses within the SIJORI framework through industry publications, business councils, and chambers of commerce to stay informed on investment patterns.

However, the lack of transparency in investment data might impact confidence. Companies typically look at these figures to assess the level of commitment and potential support from the government. In the case of SIJORI, the Ministry of Trade could periodically release updates on the initiative’s investment achievements, which would reassure Singaporean businesses of the zone’s growth potential.

Johor

vs. BBK (Batam, Bintan, Karimun): Different Levels of Excitement and Potential

Interestingly, SIJORI discussions reveal that Johor seems to garner more enthusiasm compared to Batam, Bintan, and Karimun (BBK). This discrepancy likely stems from Johor’s stronger infrastructure and proximity to Singapore, which gives it a competitive edge as an investment destination. Johor’s accessibility via two road links to Singapore—the Causeway and the Second Link— provides a more convenient transport option than BBK, which relies solely on sea connections.

Johor’s proximity and established industrial base make it an attractive alternative for manufacturers, especially those in sectors requiring a high level of logistical flexibility and quick response times. By contrast, BBK may still be appealing due to lower costs and favorable labor conditions, but the reliance on sea transport introduces an element of unpredictability.

Sea routes may face delays, and shipping costs fluctuate depending on fuel prices and regional trade activity. Therefore, while Johor might be a direct extension for Singapore-based operations, BBK could be suited for less time-sensitive manufacturing needs, where cost savings outweigh logistical challenges.

SIJORI as a Cost-Effective Alternative to Singapore’s Rising Expenses

A significant driving force behind SIJORI’s establishment is the recognition that Singapore has become a relatively expensive location for businesses, particularly in costsensitive and low-value-added industries. High real estate

prices, labor costs, and complex compliance standards make Singapore less feasible for some production types.

For certain industries, such as pharmaceuticals, compliance requirements are particularly stringent and highly specific—adding a substantial barrier to entry depending on the regulatory needs of each sector. While these regulations vary case-by-case, they collectively contribute to Singapore’s challenging environment for companies prioritizing cost efficiency.

In contrast, SIJORI offers a means to distribute operations to nearby locations with lower operational expenses, enabling Singaporean manufacturers to focus on higher-value-added activities within Singapore. At the same time, lower-value-added work can be shifted to Johor or BBK.

For CEO and founder Willy Koh,

“As a business, we are looking at the long term. During the periods (of political uncertainty), a lot of foreign businesses in Malaysia diversified their projects, some went back to Singapore and in my case, I turned to Batam.

Johor, for instance, offers more affordable land prices and a larger labor pool, allowing companies to scale

operations without incurring prohibitive costs. Similarly, BBK provides low-cost manufacturing options, with the Indonesian government offering various incentives, such as tax holidays, to attract foreign investment. SIJORI effectively allows companies to leverage each region’s strengths while retaining operational oversight from Singapore, which remains the strategic and financial hub.

Strategic Recommendations for Singaporean Manufacturers and Distributors

For Singapore-based manufacturers and distributors considering SIJORI, here are some strategic considerations:

• Understand Regulatory Differences: Engage legal or regulatory consultants to navigate the different compliance requirements in each region. This is crucial for companies intending to operate across all three regions and can help mitigate costly regulatory missteps.

• Assess Logistical Viability: Evaluate whether your business model requires rapid, predictable logistics or can accommodate slower, more cost-effective transport. For instance, Johor’s road connections with Singapore may be advantageous for time-

• Monitor Regional Investment Trends: Track investments flowing into SIJORI, as these can serve as indicators of the initiative’s growth trajectory. Notable infrastructure and business development increases in Johor, or BBK, could signal strengthening regional support and reliability.

Moving Forward with SIJORI: Opportunities and Preparedness for Singaporean Businesses

The SIJORI Growth Triangle holds significant promise for Singapore manufacturers and distributors looking to optimize costs and broaden their operational footprint within Southeast Asia. However, the success of this initiative for businesses hinges on strategic preparedness to navigate its unique regulatory and logistical complexities. With effective planning and flexibility, Singaporean companies can leverage the strengths of Johor and BBK while retaining Singapore as a core hub for higher-value operations. Moving forward, those ready to adapt and capitalize on these emerging cross-border synergies will be best positioned to thrive in the evolving landscape of SIJORI.

V

Are lean supply chains a myth? Examining resilience amidst disruptions

BY SHERAZ AHMED

Lean supply chains have been the default for companies seeking to lower costs through managing minimum inventories and manufacturing only-in-time, yet the recent years with constant unplanned disruptions and shifting

supply chains seem to suggest this may not be optimal from a management of cost versus ensuring demand from customers are met. Can lean supply chains truly withstand a turbulent market?

South Korean tech company Samsung Electronics adopts a similar approach. Utilizing lean practices in their operations, Samsung decreases overstocking of inventory. This has also helped the company in reducing waste in production.

As per reports of 2023 for the company, the strategy prevented major production delays and safeguarded against potential revenue drops of up to 15%. A growth of 7% was recorded in revenue year-over-year helping it to its market presence during global disruptions. Additionally, this model contributes to sustainability by reducing waste and emissions. Sustainable objectives as a result of a decrease of 12% in waste were achieved. Also, environmental benefits were achieved due to strong supply chain as indicated by the Samsung Sustainability Report 2023

Data analytics is an integral part of application Lean Six Sigma principles in manufacturing. It helps to identify inefficiencies and opportunities for improvement in the production process. For example, Toshiba Corporation used data analytics to enable predictive maintenance, which is a Lean principle. It aims to minimize downtime and reduce costs by identifying potential equipment failures before they occur.

Another benefit of lean supply is that it decreases inventory and overproduction. For example, Toyota uses the Just-in-Time (JIT) inventory system. This model delivers materials only when needed, reducing the costs of holding excess stock.

Toyota schedules its production according to customer demand so that there will be timely availability of the materials. Thus, it reduces the stockouts and inventory overstocking. Also, it helps to decrease the warehousing and insurance costs.

However, during the COVID-19 pandemic, Toyota’s Just-In-Time (JIT) inventory system faced significant challenges due to semiconductor shortages. In response, Toyota doubled its raw material inventory in 2023. It was to achieve a record output of 10.7 million vehicles despite supply issues.

This strategic move led to an 8% revenue increase, underscoring the benefits of pairing lean efficiency with inventory buffers. Through close collaboration with its suppliers and JIT processes, it responded efficiently to changes in markets and utilization of resources in the volatile market.

In recent months, Toyota revised its fiscal year production target down by 1% after halting operations in Japan and the U.S. Investigations revealed fraudulent crash test data and incorrect airbag testing, prompting recalls and contributing to a 20% drop in second-quarter operating profits, the first such decline in two years.

Toyota also faces increasing competition from Chinese automakers, particularly in China, where demand has softened. The company lowered its annual vehicle sales

target, citing intensified market pressures. These cases demonstrate evolving lean supply chains through targeted inventory strategies and diversified suppliers. Companies that adopt resilient practices not only protect against disruptions but achieve consistent revenue growth and environmental benefits.

Lean supply chains: A fragile balance?

Lean supply chains aim to streamline available resources, eliminate waste, and operate with minimal stock. However, it falls in between efficiency and fragility. For example, the COVID-19 pandemic locked down all the major manufacturing hubs of the world, such as China and Southeast Asia. Disrupted supply chains and production made outputs come to a standstill. Similarly, U.S. and China trade tensions exposed the flaws behind lean models when tariffs, along with shipping delays affected production processes.

Lean supply chains are essentially JIT inventory. Because the inventory is kept low to minimize costs, very little space is available in case of disruptions. For example, during the COVID-19 pandemic, the lack of inventory buffers caused shortages to persist for months in sectors ranging from automotive to healthcare.

Companies could not source critical components quickly enough. McKinsey estimates that about 73% of

companies faced supply issues early in the pandemic because of lean inventory strategies, causing many to question the model’s practicality

Lean models tend to rely on a few specialized suppliers in an effort to reduce costs, which increases vulnerability when these sources are disrupted. This risk was highlighted through the semiconductor shortage, as tensions with Taiwan centralized its production, affecting industries worldwide.

For example, the semiconductor shortage in 2020 exposed significant gaps within companies like Tesla and BYD. Low stock levels and the lack of backup inventory made electric vehicle (EV) companies face production delays. This challenged lean supply chains in high-tech manufacturing. The semiconductor shortage served as a wake-up call for lean-dependent industries.

Bloomberg notes that up to 90% of high-performance chips come from Taiwan, causing a bottleneck that strikes various industries, including automotive, electronics, and defense when tensions rise

The dependency of the EV industry on highly specific and often scarce components makes risks from lean supply chains worse. Substitutions might be possible in consumer goods, but EV production requires very specific parts, making lean supply chains particularly vulnerable when disruptions happen.

Building resilience into lean: Strategies for modern supply chains

Companies are adopting ways of developing either lean efficiency or resilience to adapt to today’s volatile environment. Such adopted strategies include:

1. Diversification of Suppliers: Apple and Samsung diversify from using one single supplier to a set of suppliers. A diversified network reduces dependence on one source. In return, it decreases the vulnerabilities of the supply chain against disruptions. As an example, sourcing the components from different locations reduces the risk. As a delay by a single supplier might disrupt Apple’s entire production line. Therefore, supplier diversification has become an absolute need, particularly among those companies that are running very lean supply chains with many businesses where even slight delays turn into millions of dollars.

2. Strategic Safety Stock: It is normally used in the lean model to avoid all kinds of inventory stockout. Safety stock proves crucial and helpful in times of disruptions. For example, firms with semiconductor reserves could run operations during times of shortage. While other firms will incur delays and costs. Safety stock has evolved rather than a cost center and has been seen as a productive investment. Strategic safety stock for key components always ensure continuity without relatively giving up on lean efficiency for high-tech industries.

3. Predictive Technologies: Both Alibaba and JD.com embrace the implementation of predictive analytics in the supply chain through AI and machine learning. This provides an early warning system where proactive response can be developed to respond to the expected disturbance. Predictive analytics help quite a lot in lean supply chains as firms adjust before there is a disruption. In these technologies, the principles of being lean are balanced with being resilient because they predict the shifting demand and prepare for it.

4. Hybrid Models: Like the hybrid supply chain models, companies are now embracing many of the traditional inventory management techniques but ones which are embedded with lean principles. Hybrid will create an agility and resilience system that brings together lean efficiency with some degree of flexibility. This enables companies to adapt quickly to global changes and ensure continuity without losing all lean and ideals.

5. Local sourcing and nearshoring: With the supply chain risks happening worldwide, companies now turn to local sourcing or nearshoring so that they have fewer risks in a very distant geographic supplier. Indeed, a short supply chain can create a very strong sense of control. It will be well within lean principles and build resilience at the same time. U.S. companies source closer to home so they avoid long shipping delays from Asia. It is expensive but stable and is something lean supply chains globally lack to provide.

A new beginning amidst global challenges

The pandemic and other black swan events have caused shipping disruptions. This caused undeniable revision to free trade practices that exposed vulnerabilities in relying on minimal inventory and a narrow supplier base.

The lesson learnt is clear. Resilience must become the cornerstone of modern supply chains. Lean principles remain valuable but require transformation. This doesn’t mean leaving the approach entirely.

Instead, it calls for an evolution—pairing efficiency with foresight, agility and adaptability. Strategies like supplier diversification, strategic inventory management and nearshoring are no longer optional—they are essential lifelines in an unpredictable global landscape.

Supply chain professionals now face an important decision. The challenge is not just technical. It’s about delivering stability, sustainability, and trust to businesses and the communities they serve.

Building the future: Data centers in SEA set to reshape regional supply chains

BY MUHAMMAD YASSIN

I

n recent years, Southeast Asia (SEA) has become one of the most significant regions for the building of new data centers. The development is facilitated by the growing demand for cloud computing, the digitalization of industries and the ever-increasing number of internet-connected devices.

The SEA data center market is anticipated to be valued at $17.73 billion by 2029, which shows the region’s importance in the global digital economy. It is estimated that Indonesia, Malaysia and the Philippines are critical nodes in regional data flows and are becoming strategically essential locations for investments in data infrastructure.

Companies such as Microsoft, Amazon Web Services, and Google have acknowledged the growth potential of SEA and are making ongoing investments in the development of data centers tailored to the region’s transition into digital.

Local governments have vigorously promoted investments via policies that create an enabling business environment and support initiatives for sustainable infrastructure. All these are in line with new international emphases on environmental, social and governance objectives.

The increasing and expanding demand for real-time analytics enabled by highly powered artificial intelligence requires data centers in the SEA region to strengthen their technological capabilities, ultimately enhancing and supporting the management of regional supply chain frameworks.

Today, data centers also increasingly support logistics, e-commerce and banking with this kind of analytics. This capability enables businesses to make informed decisions based on demand forecasts.

The speed of processing has increased due to advancements in data infrastructure which optimizes the ecology of supply chains. Organizations across regions benefit from such optimization resulting in improved efficiency, decreased operational costs and better customer experiences.

Indonesia: The Epicenter of Data Center Growth

Indonesia has become a significant leader in SEA’s development of data centers, with investments from some of the world’s largest companies. The attraction was the potential for growth through digital means, which brought the companies to develop high-capacity facilities for addressing the growing need in the region.

Such investments will correspond to the very ambitious ‘Making Indonesia 4.0’ strategy. This underpins the integration of the fourth industrial revolution digital technologies from manufacturing to financial services. The government has been announcing a number of strategic moves including tax incentives and fewer regulatory obstacles which place Indonesia as a pre-eminent location for data infrastructure investments.

Accordingly, the data center capacity in Indonesia will have to jump exponentially to over 1 GW by the end of the decade, when it stands at around 514 MW at present. Drivers here are mainly increased applications of IoT (Internet of Things) and AI penetrating the region; low-latency services and localized data solutions will dominate.

Indonesia is preparing for the growth in data centers with growth in energy, particularly renewable energy.

Data centers require enormous amounts of energy. The Indonesian government has committed to increasing the proportion of renewable energy sources such as solar and geothermal energy to power data centers (Indonesia Ministry of Energy).

Indonesia is equating growth in data centers with growth in renewable energy. Data centers require enormous amounts of energy. Global estimates indicate they account for about 1% of total electricity use. In Indonesia, the data center industry consumed approximately 1.5% of the nation’s total electricitygenerating capacity in 2014, with projections suggesting this could rise.

The Indonesian government has set ambitious renewable energy targets to address the growing energy demands. The goal is to achieve a 23% share of renewable energy in the primary energy supply by 2025 and 31% by 2050.

The EDGE1 facility in Jakarta built by Digital Edge and runs on geothermal energy alone. It is a prime example of Indonesia’s capacity to combine technical advancement with environmental awareness; this facility has set a new standard for energy-efficient data centers.

Indonesia’s sustainable business owners seek opportunities in the local data center market which meets not only the demand of Indonesia’s IT sector but also attracts investors seeking business targets which cross the

areas of the environment, society and sound financials. These will influence the two most popular e-commerce platforms, Tokopedia and Shopee as well as new IT companies entering the market. This indicates an allrounded approach to meeting digital needs through both local capacity and international aid.

Data Center Investment Comparison by Country

The Philippines: Strategic Digital Hub

The Philippines is emerging as a significant digital hub in SEA, with initiatives like the Digital Cities program transforming urban centers into high-tech

INDONESIA PHILIPPPINES MALAYSIA

economic zones. Cities such as Manila and Cebu have become competitive destinations for global players, including Digital Edge and Equinix. These companies are establishing carrier-neutral data centers to serve both domestic and international clients. This reduces data transfer latency and ensures data sovereignty for businesses operating in the Philippines

This will be significant infrastructure support from these data centers for the country’s fast-growing Information Technology - Business Process Management (IT-BPM) sector which relies on secure and high-speed data handling for global outsourcing services.

This increased connectivity not only provides realtime data analytics but also fosters businesses that can provide competitive and low-latency services necessary in companies such as finance, customer service and healthcare.

The data centers in the Philippines are showing very advanced cooling technologies such as at Digital Edge’s NARRA1 facility in Manila. These are balanced by relatively humid climates.

On its part, the Digital Cities program has contributed to the workforce development of local talent to meet growth expectations in the IT-BPM sector. Such an interest in talent development promotes the country as a great destination for high-tech companies that support sustainable growth in data services and high-tech employment.

Malaysia: Leading in Connectivity and Sustainability

Malaysia is rapidly emerging as a preferred location for data centers in SEA, offering strategic connectivity through an extensive fiber optic network and a favorable regulatory environment. Its proximity to Singapore, which faces limitations on land and energy for data center development. It makes Malaysia an attractive alternative for companies seeking regional data processing solutions.

The Malaysian government has launched the Malaysia Digital Economy Blueprint to boost the digital economy by attracting digital infrastructure investments. This initiative aims to position Malaysia as a leader in the digital economy by enhancing connectivity and fostering innovation.

Malaysia’s data center industry is advancing rapidly particularly with the emergence of green data centers that align with global sustainability goals. Prominent players like Equinix and TM ONE are progressively transitioning their Malaysian data centers to renewable energy, a critical step in fostering greener infrastructure.

Across SEA, major investors are prioritizing environmental, social, and governance (ESG) considerations, acknowledging the value of sustainable practices in their business strategies. A key initiative in Malaysia’s journey towards sustainable data center growth is the Green Lane Pathway, introduced in 2023 which streamlines power permit approvals for upcoming data center projects.

The Green Lane Pathways simplified licensing procedure shortens the time required to launch data centers which can be operationalized in as little as one year.

Johor remains a strategic destination for data center investments due to its proximity to Singapore, enhancing connectivity possibilities with potential low-latency dark fiber communications. This reduces data transfer times between Malaysia and neighboring countries and bolsters cross-border information

The thrust toward sustainability, investment in connectivity and talent development through Malaysia’s Green Lane Pathway policy has enabled it to establish itself as a critical digital hub in SEA.

All these advantages position Malaysia as a critical digital hub with the capability to serve multiple complex data needs in logistics and healthcare, e-commerce and finance sectors at the center of the shifting supply chain ecosystem.

Impact on SEA’s Supply Chains

The fast and massive expansion of data centers in SEA is changing the management of current supply chains today by making logistics, inventory and demand trends visible in real-time.

This enables businesses to implement agile models for supply chains, hence facilitating a quick response to demand. Better demand forecasting and reduction in holding costs of inventories along with the swift change in

response time to changes in consumer behavior or market conditions that will be supported by lowered latency from localized data centers.

Localized data centers also ensure compliance by keeping data onshore allowing businesses greater control over sensitive information and reducing exposure to external data privacy risks. This local storage offers reassurance to companies handling personal or confidential data as it aligns with national data protection laws and minimizes vulnerabilities associated with crossborder data handling.

Vehicle performance, delivery patterns and environmental conditions are used among other data for the anticipation and mitigation of problems such as equipment failures and road closures before potential impacts on the supply chain.

This approach reduces the time that equipment is stopped and improves efficiency while overall service reliability is enhanced. For example, in complex distribution networks like automotive and consumer electronics the predictive data center capabilities offer tremendous value in smoothing and uninterrupted operations.

Shaping the Future: Data Centers Redefining Southeast Asia’s Supply Chains

The rapid expansion of data centers across Southeast Asia is set to revolutionize the region’s supply chains. These facilities enhance operational efficiency, reduce latency and support agile decision-making by enabling real-time data processing and analytics.

This transformation allows businesses to optimize inventory management, improve demand forecasting and respond swiftly to market changes. Moreover, localized data centers ensure compliance with national data privacy regulations, providing companies greater control over sensitive information.

As Southeast Asia continues to invest in digital infrastructure, it positions itself as a pivotal player in the global supply chain ecosystem leveraging data-driven insights to drive growth and competitiveness. V

Redefining sourcing in Asia: Navigating the new era of regionalized and resilient supply chains

BY TRISHA ANJANETTE BALLADARES

Global sourcing strategies have undergone significant shifts in recent years as companies have sought to enhance their supply chains by making them more resilient, regionalized, and adaptable to emerging challenges. The COVID-19 pandemic, ongoing geopolitical tensions, and supply chain disruptions have highlighted vulnerabilities

in traditional global supply chain models. Consequently, businesses are reevaluating their sourcing strategies, especially in Asia, which has long been the world’s manufacturing hub. A new era has emerged—one focused on “regionalized production” (or “Region for Region”), sourcing closer to customer bases, and creating localized supply chains like “China for China.”

significant questions about the adaptability of various industries to these shifts. Can all types of production and manufacturing accommodate these changes? Are specific sectors better suited to regionalization, or are there inherent limitations? Furthermore, how are sourcing strategies in Asia evolving, and what challenges do companies face as they seek to implement these localized and near-customer models?

The Evolution of Sourcing in Asia: A Response to Global Disruptions

Asia has long been the global manufacturing powerhouse, with countries like China, Vietnam, India, and Indonesia playing critical roles in producing goods for multinational corporations and smaller companies. The region has benefitted from competitive labor costs, a wellestablished industrial base, and a favorable investment climate. However, this reliance on globalized supply chains has been increasingly challenged recently.

Recent conflicts, such as the war in Ukraine, and rising geopolitical tensions in regions like the South China Sea have intensified scrutiny over the reliability of sourcing from certain areas. These geopolitical upheavals have prompted businesses to reconsider their dependencies on specific countries, particularly those susceptible to political risk. The urgency to diversify supply chains has become paramount as companies seek to mitigate the impacts of disruptions stemming from military conflicts or diplomatic strife.

A notable example is the ongoing trade tensions between the United States and China, which have created uncertainty surrounding tariffs, export controls, and supply chain security. Consequently, many companies are actively working to minimize reliance on Chinese manufacturing by exploring alternative sourcing locations across Asia. This shift has led to adoption of regionalized production strategies, emphasizing the importance of manufacturing within specific regions to serve local markets, thereby reducing logistical complexities and enhancing supply chain resilience against unforeseen geopolitical events.

These factors have catalyzed a shift toward more regionalized and resilient supply chains, where businesses focus on producing goods closer to their customer bases or within the same region.

In Asia, the “China for China” concept has gained traction. Multinational companies establish production facilities within China to serve the domestic market rather than export from China to the rest of the world. This strategy helps businesses reduce risks associated with tariffs, trade restrictions, and geopolitical uncertainties while benefiting from China’s vast consumer market and production capabilities.

For Rainer Kern in 2022, the chief financial officer for China at Kärcher,

“This year has been a tough year. Lockdowns are difficult for any business. However, the Chinese market has developed in the last two years. We want to develop more local for local production. We will sooner or later export because certain trends that start here will also go into other markets, with a delay of three to five years.

Similarly, “Region for Region” sourcing strategies have emerged, emphasizing the production of goods within specific regions for consumption in those regions, such as manufacturing in Southeast Asia for Southeast Asian markets.

Industry Adaptability: Which Sectors are Better Suited for Regionalized Production?

The success of these regionalized sourcing strategies depends on the type of industry, the nature of the products, and the underlying production processes. Some industries are better suited for regionalized production and near-customer sourcing, while others may face inherent limitations.

• Automotive Industry: The automotive sector has increasingly embraced regionalized production due to its complex supply chains and high sensitivity to disruptions. Automakers have historically relied on just-in-time (JIT) manufacturing models that require parts to be delivered precisely when needed. During the pandemic, JIT models collapsed due to supply chain interruptions, leading to production delays and significant losses. Consequently, many automotive companies are shifting towards “Region for Region” strategies, establishing manufacturing hubs closer to key markets in Asia, Europe, and North America. This shift reduces the risks associated with long-distance shipping and trade barriers.

For instance, the rise of electric vehicle (EV) manufacturing in China is a prime example of localized production benefiting local consumers and international exports. Chinese automakers have built extensive supply chains within the country to support the growing demand for EVs, reducing dependence on imports. Similarly, Western automakers have sought to establish EV production lines in Asia, targeting local and regional markets.

• Consumer Electronics: The consumer electronics industry, traditionally reliant on global supply chains, is increasingly exploring regionalized production models. Companies like Apple and Samsung are diversifying their Asian production bases to mitigate risks associated with dependence on a single country. Vietnam, Indonesia, and Malaysia have emerged as alternative manufacturing hubs for consumer electronics as businesses seek to balance production between cost efficiency and risk mitigation. However, the high complexity of electronics manufacturing poses challenges for complete regionalization. The intricate supply chains for semiconductors, displays, and batteries make it difficult to source all necessary parts within a single region. While companies may relocate assembly lines closer to end markets, they may still need to rely on globally sourced components, limiting the full realization of regionalized production.

• Textile and Apparel Industry: The textile and apparel sector is well-positioned for near-customer sourcing and regionalized production due to its

relatively low technological complexity and laborintensive nature. Companies are increasingly relocating their production from China to countries like Bangladesh, Vietnam, and Indonesia to reduce costs and diversify their supply chains. The emergence of “nearshoring” strategies—where companies establish production facilities closer to key consumer markets—has become a popular trend in the industry. This allows brands to reduce lead times, lower transportation costs, and better respond to changing consumer demands.

One of the challenges the textile industry faces in fully embracing regionalization is the availability of skilled labor and infrastructure development in new production regions. Shifting production away from traditional hubs like China requires significant investment in human capital and logistics networks, which may limit the transition speed.

• Pharmaceutical and Medical Device Industry: The pandemic has also forced the pharmaceutical and medical device industries to rethink their sourcing strategies. The global shortages of critical medical supplies during the COVID-19 crisis exposed the vulnerability of relying on distant suppliers. As a result, there has been a push for localized production of essential medical products, such as personal protective equipment (PPE) and vaccines, in regions closer to end markets. However, pharmaceutical production is heavily regulated, requiring specialized knowledge, equipment, and raw materials that may only be readily available in some regions. For this industry, achieving fully localized supply chains is challenging, particularly for complex products such as biologics or advanced medical devices. Nonetheless, companies are focusing on building more resilient supply chains by establishing dualsourcing strategies and diversifying their supplier base across multiple Asian countries.

The Implications of Regionalized Supply Chains for Sustainability

Regionalized supply chains also offer significant implications for sustainability goals. As companies navigate the complexities of modern sourcing strategies, the drive towards environmental responsibility and sustainable practices is becoming increasingly intertwined with supply chain decisions.

According to Cloris Zhang, Senior Vice President of Integrated Supply Chain AMEA at Mondelez, “Sustainability roles contain different skills, including management of government and NGO relationships, understanding carbon emissions including definition of data with regards to collection and analysis to enable visibility and change management to work on people’s mindset.”

Regionalized production helps to significantly reduce the carbon footprint associated with transporting

goods over long distances. By manufacturing closer to end consumers, companies can minimize the emissions generated from shipping and logistics. This localized approach lessens the environmental impact and aligns with consumer expectations for eco-friendly practices. Many consumers today prefer brands that prioritize sustainability, making it crucial for businesses to demonstrate their commitment to reducing environmental harm.

Additionally, regional supply chains facilitate more efficient use of local resources. Companies can reduce waste and optimize production processes by sourcing materials and components from nearby suppliers. This proximity allows for more effective recycling and reuse of materials, further contributing to sustainability efforts. Moreover, localized supply chains can foster collaboration among businesses and suppliers to develop innovative solutions that promote sustainability across the value chain.

Challenges in Implementing Regionalized and Localized Sourcing Strategies

While regionalized production and near-customer sourcing offer significant benefits, they also present challenges that businesses must address.

Establishing new production facilities or relocating existing ones requires significant capital investment in infrastructure, technology, and workforce development. In many cases, emerging manufacturing hubs may need more infrastructure to support large-scale production, leading to delays and additional costs. For example, countries like Vietnam and Indonesia, while increasingly attractive as alternative production bases, may not yet have the same industrial sophistication and logistics networks as China.

Finding a skilled workforce is another challenge, particularly in industries that require advanced technical knowledge, such as electronics and pharmaceuticals. Companies must invest in training and education programs to build the necessary talent pool in new regions, which can take time and resources.

Even in a regionalized model, some industries may still require components from different parts of the world. Assembling complex products, such as automobiles or consumer electronics, often involves multiple tiers of suppliers spread across various countries. While companies can shift certain stages of production closer to their customers, they may still depend on global supply chains for critical components, making complete regionalization difficult.

Businesses must also navigate regulatory differences between regions, which can complicate sourcing strategies. Trade barriers, tariffs, and differing standards can hinder the smooth flow of goods between countries, especially in industries requiring strict regulations, such as pharmaceuticals or medical devices.

While regionalizing supply chains can mitigate some risks, geopolitical tensions and trade disputes remain challenging. Companies must carefully assess the political landscape in their operating regions, as instability or shifting government policies could disrupt production.

The Future of Sourcing in Asia: A Balanced Approach

As businesses strive to navigate the increasingly perilous global trade landscape, the urgency for adopting regionalized production, near-customer sourcing, and localized supply chains has never been more critical. These strategies are essential for enhancing supply chain resilience in the face of growing risks. However, it is important to recognize that they are not a universal solution applicable to all sectors.

Industries with intricate production processes and specialized components may require additional resources and support to embrace regionalized models fully. Consequently, many companies may adopt a hybrid approach combining regionalization with global sourcing, bolstering resilience while achieving cost efficiency.

like the SkillsFuture Series in Advanced Manufacturing, the government collaborates with industry leaders and educational institutions to equip its workforce with the skills for advanced manufacturing.

Building trust in supply chains

With the advent of IoT and blockchain technologies, companies can now track and monitor products from the manufacturing stage through to delivery. This transparency can minimize errors, reduce risks and guarantee compliance with international standards, particularly in the food and pharmaceutical industries.

For instance, Singapore’s the GrowHub Innovations Company has introduced a blockchain-powered food traceability platform aimed at increasing transparency within the agricultural ecosystem of the Asia-Pacific region.

GrowHub CEO Lester Chan said in an interview that consumers are becoming more informed about their food choices, including their ethical origins and environmental impact.

“Consumers today are savvier than ever before and keenly interested in the origins and ethical footprint of the food they consume. They want to make purchases that align with their values. This heightened consciousness has exposed the lack of transparency that has permeated the food industry,

Chan

said.

Meanwhile, Japan’s Mitsubishi Logistics has utilized blockchain technology to ensure clients can verify that products are maintained under appropriate conditions throughout the supply chain.

In collaboration with Takeda, they implemented the ML Chain data platform in January 2022, which visualized temperature control and location data for pharmaceutical products.

This initiative aimed to enhance quality control by sharing temperature and location information among various stakeholders in the distribution process while ensuring reliability through blockchain technology.

“We will continue to develop and expand the functionality of our data platform using blockchain and other cutting-edge technologies and will work together with Takeda and other companies to ensure a stable supply of pharmaceuticals while maintaining quality in pharmaceutical logistics,” senior manager executive officer Hitoshi Wakabayashi said.

This move shows the company’s aim to diversify its supply chain, even amid ongoing geopolitical tensions between Washington and Beijing. Such steps reflect a broader trend of companies using AI to navigate complex global supply chains.

Aside from diversification, tech giant IBM proposed that supply chain leaders using AI-driven workflows gain resilience that leads to increased revenue growth and profitability. This approach, called a “smarter” supply chain, relies on intelligent workflows fuelled by data-driven decisions. These workflows improve forecast accuracy by 20 to 30 percent and can make quick responses to disruptions, the report added.

IBM also proposed the five key trends, including dynamic computing, personalised customer experiences, self-learning operations, agile models and transparent & ethical networks. These elements are based on its AIdriven workflows to improve supply chain responsiveness and flexibility. Companies can build resilient and adaptable supply chains ready for expected changes and unforeseen challenges by harnessing AI, predictive analytics and automation.

Challenges

Implementing Industry 4.0 technologies is not without challenges. The initial investment can be high, and the learning curve is steep. In less developed parts of Asia, inadequate infrastructure can slow adoption. Cybersecurity also remains a concern, with interconnected systems hypothetically vulnerable to attacks.

For supply chains, the challenge lies in balancing the costs and benefits. Smaller companies may struggle, while large corporations might afford to overhaul their systems. And as companies digitize, they open themselves up to cybersecurity threats that can disrupt entire supply chains.

Industry 4.0 is reshaping trade and logistics across Asia, bringing speed in delivery time and transparency among better customer experience. However, its success hinges on overcoming challenges, from training a skilled workforce to addressing cybersecurity. As the Fourth Industrial Revolution unfolds, Asia’s supply chains are adapting and setting a new standard for the global economy.

V

TECHNOLOGY

Logistics, small and medium enterprises, and an unappealing outlook: Is there a solution?

BY ONROBOTS

It is a numbers game when it comes to skilled labor in Singapore. After falling to a historic low of 0.97 earlier in the year, Singapore’s dwindling fertility rate does not bode well for the future of the nation’s workforce. In fact, one in four citizens will be aged 65 and older come 2030, putting strain on the workforce and sectors that typically rely on physical labor.

The logistics sector is one example, and its physical nature means it is viewed less favorably compared to other trending sectors. This comes in spite of strong demand for industrial spaces due to supply chain adjustments amidst international corporations making Singapore their supply-chain hub, as logistics continues to paint an unappealing image for young Singaporeans entering the workforce.

While these international corporations still find enough talent to operate comfortably due to their global reputation, Small and Medium Enterprises (SMEs) within the sector find it particularly difficult to compete for incoming talent due to fewer resources and less-attractive compensation packages.

Logistical SMEs in Singapore must then turn to other solutions to both attract talent as well as meet operational demands in light of these challenges — which is where Industry 4.0 comes in.

Automation Adoption

Industry 4.0 holds the potential to alleviate these challenges for SMEs and create a vibrant logistics sector in Singapore. Through smart technology and the integration of new advancements, Industry 4.0 augments existing roles and supplements human tasks with the aid of automation.

In fact, organizations in Singapore are well aware of the benefits automation brings. Singapore ranks number two in robot adoption worldwide with a recorded density of 730 robots per 10,000 employees — one spot behind world-leading South Korea. Robotics adoption in Singapore has grown 27% annually since 2015, with the nation positioning itself with a proactive approach in adopting cutting-edge technology to boost productivity and operational efficiency. Automation is seen as a key solution to Singapore’s manpower woes, with 75% of organizations struggling to find and hire skilled talent in 2024.

The adoption of automated technology is addressing key challenges faced by the logistics SMEs ailing in manpower, which range from operational efficiency to talent attraction. For one, automation allows routine and time-intensive tasks to be streamlined, which allows for smoother workflows, faster decision-making, and improved accuracy in inventory and order management. This optimisation minimizes operational bottlenecks, enabling SMEs to handle larger volumes with ease and maintain competitive customer service standards - even during peak periods.

In the tight labor market where attracting talent in logistics is challenging, automation also makes these roles more appealing by reducing the physical strain of repetitive tasks such as lifting heavy loads for palletising. This paints a better picture for the industry, allowing it to create opportunities for employees to focus on problemsolving and tech-oriented skills rather than simply perform manual labor, which aligns with the country’s goal of building a future-ready workforce and a more attractive industry to enter.

In a study conducted by Zapier, 94% of workers say they perform repetitive, time consuming tasks in their role, and 90% of workers say that automation has improved lives around the workplace. Contrary to popular belief, automation does not replace the human worker. Instead, it acts as the productivity tool for businesses as they help them achieve performance objectives, increase quality, and provide a better working environment for employees.

Stacking Up Against the Competition

Adopting automation does sound like the solution for logistics SMEs in Singapore, but there are various speed bumps in this plan. Diving deeper into the landscape of organizations in Singapore, digitalisation among SMEs has improved over the years where technology adoption rates increased from 73.8% in 2018 to 94.3% in 2022, but significant gaps between them and the larger firms continue to linger.

According to the Infocomm Media Development Authority (IMDA), the technology adoption intensity of SMEs improved to 2.1 in 2022, but is still considerably lower than the 5.7 for their larger counterparts — highlighting the disparity even in the adoption of technology and automation apart from just competing for talent.

With that, operational efficiency and talent acquisition might continue to elude SMEs as they simply cannot stack up against international organizations. Only operating with receipts not exceeding S$100 million, SMEs also have employment of less than 200 workers. They must allocate sufficient resources to advanced technology without impacting their budget significantly.

SMEs often struggle with resource allocation for advanced technologies without notably impacting their budgets. While Industry 4.0 presents opportunities for creating a vibrant logistics sector, its implementation and the associated job roles can be challenging for SMEs to budget for and ultimately fill.

Supporting SMEs and their Automation Journey

Recognising the distinct challenges faced by SMEs in Singapore, OnRobot’s D:PLOY platform is designed with SMEs in mind, offering a streamlined approach to robotics automation that requires minimal engineering expertise.

The typical learning curve when deploying an automated solution within a business can be steep, with many moving parts needed to make the solution work. There are lots of back and forth, along with multiple parties needed to program the solution to the unique requirements of the SME. Compared to large corporations with more resources and in-house teams to aid automation adoption, some SMEs do not have manpower and engineering expertise to incorporate the solution.

D:PLOY is the first automatic development platform for collaborative robots (cobots) and industrial robots that enables the configuration of complete, off-theshelf robotic systems for high-mix applications — such as palletising and machine tending. It is designed to do fast, easy in-house workpiece changeovers with no programming, and can be put to work with same-day installation.

This allows SMEs to gain automated assistance as smaller players against big corporations. D:PLOY aims to empower SMEs to overcome the barriers to automation, as they gain significant advantages from the economies of scale of these standard systems, including lower cost and full price transparency, immediate availability, and the flexibility of easy, built-in redeployment for workpiece changeovers. James Taylor, chief commercial officer for OnRobot said: “With D:PLOY, we are taking the next logical step in simplifying the overall application rather than just focusing on individual components within the robot cell.”

“While robotics is the most logical solution, there are still barriers to deploying robotics as it can be a time-consuming and costly endeavor for SMEs, who often lack the capital, programming skills and scale to justify the investment.

Automating for Today

In closing, embracing entry-level automation solutions offers SMEs in Singapore’s logistics sector a viable path forward. By integrating accessible Industry 4.0 technologies, these businesses can increase operational efficiency, reduce dependency on physical labor, and make their workplaces more appealing to a younger workforce.

This shift not only addresses immediate labor challenges but also positions logistical SMEs as agile, innovative contributors within Singapore’s vibrant SME landscape, ensuring their resilience and continued competitiveness in a demanding market.

Logistics might not be a trendy industry to enter, but by breaking down automation barriers and improving its image, it just might be the next up. V

ABOUT

Headquartered in Odense, Denmark, and with offices spread across the globe, OnRobot is the world’s leading provider of hardware and software solutions for collaborative applications.

SUPPLY CHAIN AND MANUFACTURING

The holidays are here; What 2025’s Lunar New Year means for Asia’s dual role in global supply chains

BY MATTHEW PARRA

As the December festivities wind down, supply chains across Asia are shifting their focus to the next major peak season: Lunar New Year (LNY). Widely celebrated across the region, this festival isn’t just a time for family and culture - it’s

also a critical driver of consumer spending and a logistical marathon for businesses.

“It’s a seven-day celebration with 20 to 40 days of impact.” says TMC Vice President of Logistics David Bennett.

Asia’s unique dual role in the global chain becomes apparent during this time as both the world’s manufacturing hub and a key consumer market. While overseas businesses depend on the region’s factories to produce and ship goods, LNY also fuels a surge in local demand. This adds a layer of complexity to the season which affects production, logistics and retail operations worldwide.

Why the Lunar New Year is a game changer for supply chains

LNY brings a perfect storm of logistical challenges, amplified by Asia’s dual role as a global producer and consumer. This affects the global shipping landscape due to the sheer volume of factory closures and a sharp decline in production.