FRIDAY MARCH 7, 2025

9:00 AM - 5:30 PM

FRIDAY MARCH 7, 2025

9:00 AM - 5:30 PM

Chair-Elect

Nusenda Credit Union

Secretary

U.S. Department of Justice

Monique Fragua Indian Pueblo Cultural Center

Jason Galloway UNM Health Sciences Center

Dr. Meriah Heredia Griego

José Viramontes,

Dr. Abinash Achrekar

UNM Health Sciences Center

Harold Lavender CNM Ingenuity

Paul Mondragón Bank of America New Mexico

Bob Bowmania Productions

Singleton Schreiber

Independent Venture Capital & Private Equity Professional

Sanjay Engineer

FBT Architects

Katie Esquibel

Sandia National Laboratories

Junior League of Albuquerque

TIME

9:00 AM Opening Remarks

9:10 – 10:10 AM

10:15 – 11:15 AM

Planning Through Uncertainty

Albuquerque Community Foundation

11:20 AM – 12:20 PM

Flexible Uses of Life Insurance in Estate Planning

Equitable Estate Planning through a Trauma-Informed Lens

12:20 – 1:10 PM Lunch

Ken Leach Roybal-Mack & Cordova, PC

Brad Justice Justice Financial

Sarah K. Jaeger Weems Hazen Law

Disability Planning Unpacked: Focus on Special Needs Planning Tools

1:10 – 2:10 PM Feliz Martone Martone Law

2:15 – 3:15 PM

Ethical Issues in Estate and Trust Administration

3:15 – 3:25 PM NM-New

Stella Edens Pederson Heritage Trust

3:25 – 4:25 PM

Victor Ortiz NM-New

ABCs of Estate Planning with Retirement Accounts

Sara Traub Traub Law NM

4:30 – 5:30 PM How Do I Effectively Communicate with a Client or Beneficiary? What If I Have to Give Them “Unpleasant News”

5:30 PM Closing

John Attwood Cardinal Trust

KENNETH C. LEACH completed his education through the University of New Mexico with his B.A. in History in 1972, and his JD in Law in 1975. He was then admitted to the bar by the New Mexico and U.S. District Court in 1975. He is a Fellow of the American College of Trust and Estate Counsel (ACTEC), and has been listed on Martindale-Hubbell’s Bar Register of Preeminent Lawyers.

He is a member of the University of New Mexico Law School Alumni Association, the Albuquerque Bar Association, the New Mexico Estate Planning Council and Southern New Mexico Estate Council. He is a Trustee for New Mexico Community Trust and a former Albuquerque Community Foundation Trustee. Kenneth previously served on the New Mexico Board of Legal Specialization, An Agency of the Supreme Court of New Mexico Estate Planning, Trusts & Probate Law Specialty Committee. He is presently serving on the San Juan College Foundation Board and served as President from 2019-2022. Mr. Leach served on the University of New Mexico Foundation Board (from 1995-2003), and as the Chairman of the Gift Acceptance Committee for the UNM Foundation.

Kenneth has been listed in the prestigious “The Best Lawyers in America” publication in the Trust & Estates section for 26 consecutive years (1996-2022). He was the Community Foundation of Southern New Mexico advisor for the year of 2013, and he received the Excellence in Charitable Gift Planning Award for 2006 by the Albuquerque Community Foundation.

BRAD JUSTICE was born and raised in Orange County, California. After graduating with a double major in Business Administration and Portuguese in 2004, Brad was recruited by GE Consumer Finance to move to Albuquerque, New Mexico. Shortly thereafter, he transitioned into financial planning and earned a masters degree in financial services. He is the owner of a 9-person financial planning firm, Justice Financial, a private client group affiliate with the Northwestern Mutual Wealth Management Company. Brad has achieved prestigious industry milestones and excelled in multiple leadership roles. He has been recognized by Forbes as a best-in-state wealth advisor.

Today Brad focuses primarily on working with clients in the retirement income space, professionals, and business owners. He holds securities registrations in Series 6, 7, 26, and 63 in addition to the following designations: CERTIFIED FINANCIAL PLANNER™ Professional, Masters of Science in Financial Services (MSFS), Retirement Income Certified Professional (RICP®), Certified Life Underwriter (CLU®), Chartered Financial Consultant (ChFC®), Certified Advisor of Senior Living (CASL®) and Wealth Management Certified Professional (WMCP®).

Brad is married to Lisa, and they have four wonderful children, one dog, and more than 20 box turtles that live in their backyard. They love playing board games, swimming in the pool, traveling together, and anything that involves family.

His claim to fame is being an extra in the 1994 movie “The Mighty Ducks 2”.

STELLA EDENS PEDERSON became a licensed attorney in 1995 and is presently licensed in the states of Washington and New Mexico. Her career spans a broad variety of legal practice areas, including corporate law, real estate, estate planning and probate and trust administration.

Additionally, she worked in the oldest bank in Washington State, giving her experience in investment management and financial planning. She has been active in organizations supporting legal aid, women owned businesses and mentoring. She is active in the Santa Fe Estate Planning Council and a member of the 2024 class of Leadership Santa Fe.

Pederson’s passion for mentoring underscores Heritage Trust's commitment to fostering leadership from within. Her vision for the future includes both maintaining Heritage Trust’s position as a trusted partner for families and their advisors, and expanding the company’s reach and enhancing its service offerings to better serve the diverse needs of clients.

An empty nester, Stella moved with her husband and three dogs to Santa Fe in 2022. They enjoy the outdoors and the opportunities for live music in small venues that are abundant in Northern New Mexico.

VP, Trust Officer, Business Development

JOHN ATTWOOD SR. has worked in the fields of social and financial services for more than 20 years. A National Certified Guardian since 2006, he is a graduate of Oklahoma Wesleyan University, the American Bankers Association, and Graduate Trust School. In his position, John is responsible for the business development and administration of Trusts, Conservatorships and Estates. This includes experience with support, special needs, personal injury and complex, multimillion dollar trust accounts.

John enjoys establishing and maintaining relationships with clients, estate planning attorneys and trial lawyers. Cardinal Trust does not offer in-house investment advice; therefore, we collaborate with the clients’ preferred investment advisor to manage the trust investment assets. John is not ashamed to consider himself an “old school” trust officer. He is enthusiastic about client service.

He has worked as a medical decision-maker (National Certified Guardian since 2006) for those with disabilities, and as a corporate trust officer with banks and trust companies, where he specialized in administering personal injury settlements, special needs trusts and conservatorships to enhance the lives of the elderly and injured, including quadriplegic, paraplegic, traumatic brain injured and those challenged with mental illness over the full scale of the spectrum. John has worked with several New Mexico Trial Lawyers, Guardians ad Litem and been a guest speaker/sponsor at the New Mexico Trial Lawyers Board Retreats.

John asks each new client or family decision maker, “How can I utilize the trust assets to enhance the quality of life of my client?” He brings this passion to each person he serves.John serves as Treasurer for The Arc of New Mexico, Vice-President for the New Mexico Estate Planning Council, and board member for the Parker Center for Family Business (UNM Anderson Business School). He is a proud grandfather of a sweet set of five-year-old twins and three additional, very bright grandchildren. In his free time, he loves to fish for trout in Northern New Mexico and Southern Colorado.

Born and raised in Albuquerque, SARAH K. JAEGER understands the vibrance of our state’s communities and cares deeply about improving the wellbeing of New Mexican children and families so future generations can thrive. As an associate attorney at Weems Hazen Law, Sarah represents, and counsels injured New Mexicans through a trauma-informed lens. Sarah is proud to specialize in litigation on behalf of injured minors and survivors of sexual violence.

Sarah received her J.D. from the University of New Mexico School of Law and holds a B.A. in Human Development, Cultural Anthropology, Public Policy, and Dance from Connecticut College. She began her legal career at Peifer, Hanson, Mullins & Baker P.A., where she practiced in areas including appellate law, commercial litigation, and employment law, and worked as a Policy Analyst at New Mexico Voices for Children prior to attending law school. Outside her practice, Sarah is an avid dancer, choreographer, and tap teacher. She is a member, director, and teacher for the Alley Kats Tap Companies and a member of BreakingEven and can frequently be found performing in or choreographing for local shows around town.

FELIZ MARTONE is a highly experienced legal professional with a distinguished career spanning over 18 years in law. Her expertise is in the specialized areas of estate planning and disability law, making her a sought-after advocate for clients seeking comprehensive legal guidance. With a passion for estate planning education and community outreach,

Feliz ensures her clients’ life and wealth are handled according to their wishes. She has developed a reputation for providing compassionate, yet expert legal services, assisting families in planning for their future and securing their well-being.

SARA TRAUB is a three-time graduate of the University of New Mexico with degrees in University Studies, Business Administration and Law. Sara is a licensed CPA and attorney admitted to practice in New Mexico and United States Tax Court.

Sara is actively involved in the State Bar of New Mexico as a long-time member and past director of the Real Property, Trust & Estate and Elder Law Sections, and recently joined the Access to Justice Fund Grant Commission. Sara also serves on committees for the New Mexico Society of CPAs. Sara has been actively involved with the Albuquerque Community Foundation for over a decade, initially participating in the Future Fund and recently completing a 3-year term as a Trustee on the organization’s Board of Trustees. In her free time, she enjoys hiking, river rafting, and spending time with family and friends.

SESSION 1 9:10 AM

Ken Leach, Attorney Roybal-Mack & Cordova, PC

The presentation will be on planning during the uncertainty in view of a new administration in Washington, possible changes in tax law and policy and the issues that estate planners need to be aware of when planning during these uncertain times.

SESSION 2 10:15 AM

Brad Justice, Wealth Management Advisor Justice Financial

Life insurance can be a tool to maximize flexibility in estate planning when designed properly, especially in a time with pending changes in exemption limits. This session will revisit the different types of life insurance policies and how they can be strategically placed in an estate plan. It will conclude with a few current financial planning topics with broad applications for clients.

Sarah K. Jaeger, Weems Hazen Law

This presentation will focus on strategies and tools that attorneys and law firms can use when providing estate planning services to diverse populations. Key topics of discussion will include (1) the ways in which bringing a trauma-informed lens into estate planning can create better access to justice; and (2) key considerations when working with LGBTQIA individuals, multicultural families, and survivors of abuse and/or violence.

SESSION 4 1:10 PM

Feliz Martone, Managing Attorney

Martone Law

This presentation will explore key legal and financial strategies to secure the future of individuals with disabilities. This presentation will cover essential tools such as ABLE accounts, Special Needs Trusts, and Social Security disability benefits, ensuring long-term protection and financial stability. Attendees will gain practical insights to navigate complex planning with confidence.

SESSION 5 2:15 PM

Stella Edens Pederson, President Heritage Trust

SESSION 6 3:25 PM

Steering through the stormy seas of final administration: How lay and professional fiduciaries can get into tricky situations and how to avoid crashing on the shore.

Sara Traub, Founder Traub Law NM, PC

SESSION 7 4:30 PM

This presentation explores the veritable alphabet soup of current estate planning with retirement accounts, including the SECURE Act, RMDs, QCDs, and more.

John Attwood, VP, Trust Officer, Business Development Cardinal Trust

We all have clients that have a basic understanding of the role we play in their lives. As the role varies from investment advisor to CPA, to Estate Planning Attorney to Trust Officer, our method of communication varies. How do we “effectively” communicate and maximize the impact of our expertise with our client or beneficiary? It’s easy to communicate “good news” but what if we face a downturn in the market or our client has a significant tax liability or the expectations of our estate planning client or beneficiary is well beyond what is reasonable? Let’s learn from each other: communication skills, best practice and creative methods to transfer concepts relevant to our clients.

Albuquerque Community Foundation is looking for community members to serve on the Foundation’s scholarship and grant review panels.

Interested in serving on a panel? Scan the respective QR code to learn more and complete the sign-up form.

The American Heart Association Professional Advisor Network supports advisors with estate and philanthropic solutions helping you offer your clients meaningful options to reach their unique personal and financial goals. Our network is designed to increase your knowledge of both charitable giving and the latest tax legislation while assisting us with our mission to save more lives from heart disease and stroke.

Personal assistance from a nationwide team of estate and gift planning professionals

Free planning tools, gift calculators, tax guides, and more

Continuing education and networking opportunities

“The American Heart Association’s Professional Advisor Network provides valuable resources that support my planning process and aids in preparation for meaningful legacy conversations with clients. In addition to the American Heart Association’s commitment to providing top-tier educational resources, I appreciate the network’s ability to connect individuals whose personal and professional values are aligned, providing us opportunities to collaborate with other subject matter specialists across the country to advance each other’s careers.”

» Estate Settlement and Distributing Trusts.

» Special Needs and General Support Trust Administration.

» Serve as Financial Agent Under Power of Attorney.

» Charitable Trust Administration.

SESSION 1 9:10 AM

Presented By Kenneth C. Leach

Roybal Mack & Cordova, P.C.

The 2017 Tax Act –a Republican bill

•Passed House by a Vote of 227-203 (with no Democrats voting for it!)

•Passed Senate by a Vote of 51 to 48 (strict party line vote)

•President Trump signed the 2017 tax Act on December 22, 2017

•Most Provisions were effective after December 31, 2017

•Most Provisions regarding individuals are effective for 8 years and sunset on December 31, 2025

•Under the 2017 Tax Act, the basic exclusion amount was increased from $5 million to $10 million for estates of decedents dying and gifts and generation skipping transfers made after 2017 and before 2026.

•The $10 million amount is indexed for inflation occurring after 2011 which means the exemption for 2025 is $13,990,000 per person (married couples now have $27,980,000 dollars of exemption.)

• Exemptions sunset on December 31, 2025

• IRS green book and various other federal legislation proposals include provisions which would impact planning:

• (i) prohibit the tax-free exchange of assets between a grantor and a GRAT and imposing a 10-year minimum GRAT term and minimum remainder requirements (the greater of 25% of the transferred assets or $500,000)

• (ii) limit the effectiveness of GST exemption allocations to 90 years

(iii) severely limit the use of "Crummey" powersby limiting the ability to use annual gift tax exclusions to transfers to individuals or to IRC Section 2503(c) trusts

(iv) limit the gift tax annual exclusion to $50,000 in the aggregate.

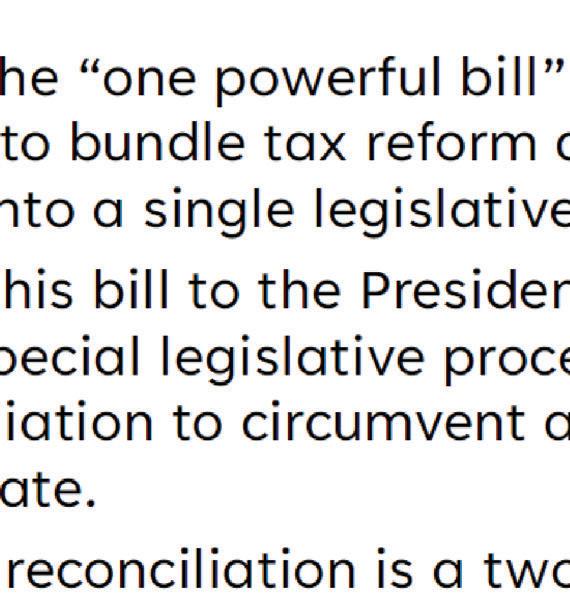

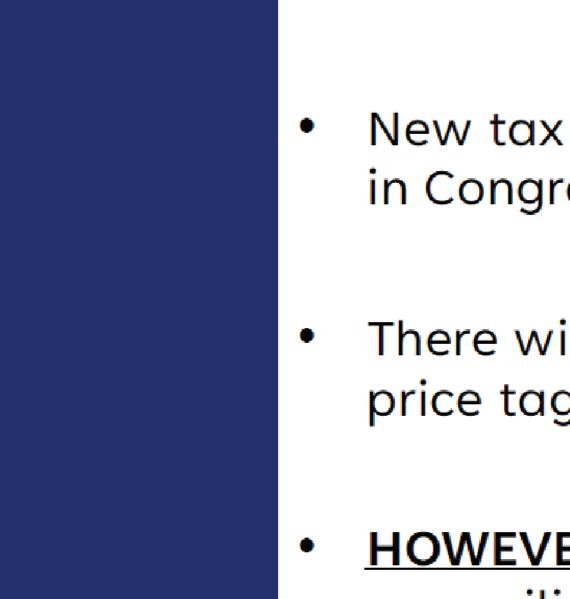

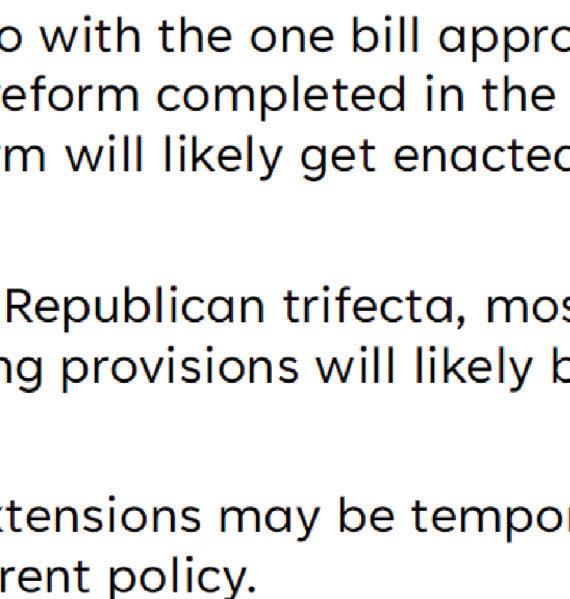

• Estate Planners need to construct plans that are flexible enough to take into account the possible sunset of the 2017 Act; but also to take into account the likely extension of the 2017 Act

•A “Clayton QTIP” trust is a trust for which a QTIP election at the death of the first spouse to die can either be made or not made, but if a QTIP election is not made any non-elected property passes to a separate trust (usually a traditional credit shelter-type trust for the benefit of the surviving spouse and descendants)

• Income not forced to be distributed to surviving spouse. This allows for income tax planning by sprinkling income and principal among the surviving spouse and other descendants. The surviving spouse is only required to have a mandatory income interest in the property with respect to which a QTIP election is made.

•Spousal power of appointment. The surviving spouse may have a limited power of appointment exercisable at death over the assets of the trust usually limited to and among the descendants of the first of the married couple to die. This allows flexibility in dealing with future events.

•Post Mortem Flexibility. An executor generally has up to fifteen (15) months (Nine (9) months plus an automatic 6month extension for the Form 706) after the decedent’s death to assess the current situation and determine whether or not and to what extent a QTIP election should be made.

• Example 1. An executor may elect portability and may make a QTIP election with respect to 100% of potential QTIP property thereby facilitating use of the predeceased spouse’s GST exemption by means of the “reverse QTIP election” under IRC §2652(a)(3) plus a full basis step up as to the QTIP property at the death of the surviving spouse.

•In two recent and unanimous opinions, the Tax Court held that a surviving spouse does not make a gift under IRC § 2519 upon the termination of two marital trusts holding “qualified terminable interest property” (“QTIP”) because the surviving spouse received all of the trust assets upon termination. Estate of Anenberg v. Commissioner, 162 T.C. No. 9 (May 20, 2024); McDougall v. Commissioner, 163 T.C. No. 5 (September 17, 2024).

•The court in both Anenberg and McDougall also held that the surviving spouse’s subsequent installment sale of the assets formerly held in the marital trusts likewise does not trigger a deemed gift under IRC § 2519.

•In McDougall, the court held that the terminating distribution to the surviving spouse is a gift by the remainder beneficiaries of their vested remainder interests in the trust

BecausethechildrenofthesurvivingspouseinMcDougall participatedintheterminationoftheQTIPTrustanddistribution totheirfather,Bruce,Thecourtheld:

“LindaandPeterplainlymadegratuitoustransfers.Beforethe implementationoftheNonjudicialAgreement,theyheldvaluable rights,i.e.,theremainderinterestsintheQTIP.Afterthe implementationofthatagreement,whichrequiredtheirconsent, LindaandPeterhadgivenupthosevaluablerightsbyagreeing thatalloftheResiduaryTrustassetswouldbetransferredto Bruce.Andtheyreceivednothinginreturn.Bygivinguptheir remainderinterestinreturnforreceivingnothing,Lindaand Peterengagedingratuitous transfersandtheTaxCourt concludedthattheyarethereforesubjecttogifttaxunderIRC §§ 2501and2511.”

•In drafting QTIP trusts to leave the flexibility of getting trust assets to the spousebeneficiary, consider giving a third party a power of appointment to appoint assets to the spouse.

• Reg. §25.2519-1(e) (“[t]he exercise … of a power to appoint [QTIP] to the donee spouse is not treated as a disposition under section 2519, even though the donee spouse subsequently disposes of the appointed property”).

Continued

•If an existing trust does not include a power of appointment, consider if the trust could be decanted to a trust that would add a power of appointment. If such decanting is within the proper exercise of the trustee’s discretion, the children should not be treated as making a gift because of the decanting.

•Givingthespouse(orsomeoneelse)a powerofappointmenttoappointthe remainderatthespouse’sdeathprovides an argumentforminimizingthegift amount byanyparticularbeneficiary resulting fromthebeneficiary’sconsent to anearlyterminationoftheQTIPtrust.

•Predeceased spouse’s residuary estate passes outright to the surviving spouse (i.e. simple will instead of to a QTIP trust where QTIP election could be made).

•If and to the extent the surviving spouse makes a qualified disclaimer any disclaimed property would pass to a credit shelter-type trust for the benefit of the surviving spouse and descendants.

•the spouse should not have a power of appointment over the assets in the trust to which disclaimed property is added as the disclaimer would not be qualified disclaimer under IRC §2518.

•qualified disclaimer must be made within nine (9) months of the date of death of the spouse who is the first to die (IRC § 2518(b)).

• Comparison to Clayton QTIP.

Fifteen (15) month time frame for a QTIP election if a Clayton QTIP is used instead of a Disclaimer Trust so Clayton QTIP would give more flexibility.

•The surviving spouse may not disclaim any property which the spouse has previously accepted benefits. IRC §2518(b); Treas. Reg. §25.2518-2(d)(1)

• This is one of the real dangers in using disclaimer trust planning.

• Make Gifts before the exemption sunsets.

• By doing this client will use a gift and estate tax exemption that the client may not have in the future!

• Keep in mind that the exemption still may sunset on December 31, 2025!

Estate tax benefits. If clients leave their estate outright to children by gift or bequest, property may be subjected to federal estate tax upon death of children. Trusts for children could be structured so that:

1. Child receives income.

2. Child receives principal under a HEMS standard.

3. Child can be the trustee of the trust and can direct investment of trust assets for income or principal growth as your child may decide is in child’s best interest.

4. Child is granted a limited power of appointment so child can at death appoint and direct the trust assets to anyone chosen by child except to that child, the estate of that child, the creditors of that child or the creditors of his or her estate. The class of beneficiaries to whom child can appoint property of the trust can be more limited if desired.

Consider providing for trusts that will not be included in estates of children

•None of the powers listed above either alone or cumulatively will cause the assets of a trust established for the benefit of a child to be included in his or her estate for federal estate tax purposes.

•The limited power of appointment will allow the child to appoint the property outright or in trust to descendants.

•If an irrevocable trust for a beneficiary is not included in the estate of the beneficiary at death, then the assets in the trust will not receive a basis step up for income tax purposes

• If the basic estate tax exemption remains high, the assets of the trust could be included in the estate of the beneficiary without negative estate tax ramifications

•Because of the current high applicable exclusion amounts, clients generally do not anticipate having estate tax issues and tend to believe that their children and grandchildren will also not have transfer tax issues.

• irrevocable trusts should still be considered for clients’ children and more remote descendants for asset protection

•Using formula general power of appointment (“GPOA”), the trust can be designed for a clients’ descendants in a manner that will cause the value of the assets in such trusts to be included in their respective gross estates just up to the point beyond which estate tax would be incurred!

•IRC §2041(b)(1) defines a GPOA as a power which is exercisable in favor of the decedent, the estate of the decedent, the creditors of the decedent or the creditors of the estate of the decedent.

• Property subject to a GPOA, whether or not exercised, will be deemed to have been acquired from the decedent and will, therefore, qualify for the step-up in basis. Treas. Reg. §§1.1014-2(a)(4), (b)(2).

•Exercise of the GPOA may be subject to a precedent of giving of notice and to take effect only on the expiration of a stated period after its exercise, IRC § 2041(a)(2)

•Structure power so it is exercisable only to the extent holding such power would not, by itself cause imposition of any estate tax.

•Order the GPOA to be applicable:

i.First, to those trust assets having the lowest basis

ii.Cascade to each next lowest basis asset until holding the power would no longer cause any imposition of estate tax

•Trust could provide that an independent trustee or a trust protector may grant a GPOA (perhaps, a formula GPOA) to a beneficiary after considering the income and transfer tax consequences

• Advantage. May provide more flexibility than having the trust instrument itself confer the general power of appointment.

• Disadvantage. Will an independent trustee have the willingness and sophistication to grant a general power of appointment to a beneficiary and will the independent trustee given this power even be in existence when needed?

will not be subject to

•The estate, gift and GST tax exemption of $13,990,000 in 2025 will allow clients to set up trusts for their children that will be GST exempt and can place up to 13,990,000 ($27,980,000 for married couples) in these trusts which will then be insulated from estate tax and the GST tax.

•This should be considered before the increased exemptions sunset on December 31, 2025

•A grantor trust is a trust for income tax purposes that the grantor has retained one or more powers under IRC §§ 671 through 679.

•Under IRC §675(4) and Reg §1.675-1(d), the power to substitute assets of equivalent value by the Trustor vested in a Trustee who is a nonadverse person makes the trust a grantor trust for federal income tax purposes and does not cause the trust to be included in the estate of the grantor under IRC § 2038. Estate of Anders Jordahl, 65 TC 92

•The power of a nonadverse party to authorize making a loan to the grantor with adequate interest; but without adequate security will make the trust a grantor trust under IRC § 675(2)

•When an irrevocable trust is established someone is going to have to pay the income tax on income received by the trust which is either: –The Grantor –The Trust –Or the beneficiaries.

(Reason #1)

•Grantor is making a gift tax free and gift tax exemption free gift of the amount of the income tax to the beneficiary.

Reason #2

•Installment sales may be made income tax free between the grantor and a trust that is a grantor trust for income tax purposes. Rev Rul 85-13

•If the trust is a grantor trust and the terms and provisions of the trust need to be modified, you can distribute the assets or decant into another grantor trust with no income tax consequences.

• Wait a second! What about the proposals to include a grantor trust in the estate of the grantor and to gift tax distributions to persons other than the grantor and spouse of grantor!!! Do we really want to take this risk and design the irrevocable trust as a grantor trust?

•Grantor trust status needs to be able to be toggled on or off.

–Toggle off by grantor releasing power that makes the trust a grantor trust.

–Toggle on by giving a trust protector or independent trustee the power to re-grant the power that makes the trust a grantor trust.

•Trustee may be given a power in the discretion of the trustee to reimburse the grantor for income taxes paid.

•2016 Amendment to New Mexico Uniform Statutory Rule Against Perpetuities effectively removes restrictions on establishing dynasty trusts in New Mexico.

•This was a dramatic change in trust law in the state of New Mexico, as instead of being able to have a dynasty trust run for perhaps a couple of generations with the general rule of § 45-2-901 NMSA no longer being applicable to “property interests held in trust”, a dynasty trust may now be designed so that the trust corpus may stay in trust forever.

•For real property held in trust, at the end of three hundred sixty-five (365) years from the later of the date on which an interest in real property is added to or purchased by a trust or the date that the trust became irrevocable.

•This provision puts New Mexico on par with states like South Dakota which has long used its repeal of the Rule Against Perpetuities to attract to South Dakota the trust business of clients who want to be able to have a dynasty trust protected from creditors, divorce and transfer tax.

Non-tax advantages of leaving property in trust for children and other family members

•Protection from Divorce

•Creditor Protection.

•Same level of protection whether or not the beneficiary is the trustee or a third party is the trustee.

•See 46A-5-504E NMSA

•Exceptions:

1.Child support and spousal support –46A-5503 NMSA.

2.Judgment creditor providing services for protection of beneficiary’s interest in the trust.

3.A claim of the state of NM or United States to extent a NM statute or federal law so provides.

•Disadvantages of leaving child’s share in trust instead of outright:

i.Child must file federal income tax return for trust each year;

ii.Trust must be drafted so that trust does not pay higher income tax, capital gains tax or 3.8% Medicare tax on “net investment income”.

iii.Complexity of bequest in trust vs simplicity of outright distribution.

•What if a client makes large lifetime taxable gifts while the increased basic exclusion amount under the 2017 Tax Act was in effect dies after the sunset of the 2017 Tax Act?

•Will the decedent be treated on his or her federal estate tax return as having made taxable gifts because the increased basic exclusion amount for estate tax purposes had been eliminated as of the date of death of the decedent?

•Final regulations have been issued that would prevent clawback of the increased basic exclusion amount with respect to taxable gifts made before 2026. T.D. 9884, 84 Fed. Reg. 64995 (Nov. 26, 2019).

•In REG 118913-21, 87 Fed.Reg. 24918 (Apr. 27, 2022), the IRS and Treasury proposed regulations that would permit a clawback of the doubled basic exclusion amount in effect until January 1, 2026, for gifts made before that date if the value of the gift is included in the deceased donor's gross estate.

•If a donor retains the title, benefit, or control over the transfer in a manner that will ultimately cause it to be included in his or her gross estate, then the available basic exclusion amount for ultimate calculation of the donor's estate taxes is determined by the basic exclusion amount rules in effect on the date of death (not on date of gift).

•Many clients are not comfortable making large gifts into trusts for children and other descendants because:

– Do not know how much will need for the rest of their life;

– Turn children into “trust babies” and disincentivize children from reaching potential.

– Fear of nature or extent of future changes in future tax legislation.

•What is a SLAT?

–One spouse establishes an irrevocable trust for the benefit of the other spouse and perhaps also other family members.

–The beneficiary spouse continues to have access to the assets in trust for the beneficiary spouse’s benefit and the grantor spouse also has access through the distributions to the beneficiary spouse (as long as they are married!)

•Beneficiary spouse may be distributed the income and may have access to principal for health, education, support and maintenance.

•An independent person could be granted a limited power of appointment to appoint trust principal at the death of the beneficiary spouse to and among a class of persons that could include the grantor spouse.

•If the estate tax exemptions are not reduced, clients may have some “buyer’s remorse” and may want to be able “reverse” the gifting to the SLAT.

–Disclaimer by beneficiary spouse and assets go back to the grantor spouse.

–Lifetime QTIP Trust –If make the QTIP election then for tax purposes the gift will not have been made.

•All income to beneficiary spouse no less often than annually.

•Principal can only be invaded for the benefit of the beneficiary spouse during his or her lifetime.

•If want to go ahead with the gift then no QTIP election is made, if because of future legislation want to opt out of it being a gift, QTIP election is timely made (by 10/15/25)

•Keep in mind that a partial QTIP election could also be made which could reduce the gift tax to zero in the event the IRS disagrees with the valuation of the assets gifted into the QTIP.

•However, unlike using a trust where assets could be disclaimed back to the grantor spouse the assets will not revert to the grantor spouse.

•Use a Wandry formula -In the 2012 Tax court case of Wandry v Commissioner, TC Memo 2012-88, The Tax Court approved an adjustment formula clause triggered by post-audit revaluation under which units are reallocated so that value of number of units to each donee equaled the gift tax exclusion dollar amount specified in transfer documents.

•Use a gift over to a GRAT, charity or outright to spouse.

•Under IRC § 677(a)(1) the grantor will be income taxed on the income from a trust, if the income, without the approval or consent of an “adverse party” or in the discretion of the grantor or a “nonadverse party” or both, may be distributed to the grantor spouse or the beneficiary spouse.

•Unless a child or other family members who are remainder beneficiaries and are therefore “adverse” must consent to distributions to the beneficiary spouse, the SLAT will be a grantor trust.

•As long as the grantor spouse is living, the grantor spouse has a duty to “support” the beneficiary spouse. If the trust assets may be used to fulfill the “legal obligations” of the grantor spouse, then SLAT will be included in the grantor spouse’s estate for estate tax purposes. See Reg 20.20361(b)(2).

•While grantor spouse is living only an Independent Trustee should have the power to make distributions for the beneficiary spouse’s “support”.

•Beneficiary spouse can serve as trustee as long as the power to make distributions for “support” are vested in another trustee preferably an “Independent Trustee”.

•If Beneficiary spouse’s power to receive principal is not limited to a HEMS standard, there will be estate inclusion upon death of beneficiary spouse.

•Beneficiary spouse should have right to remove the Trustee and appoint an Independent Trustee.

•Beneficiary spouse may be distributed all of the income, a fixed dollar amount or a unitrust amount.

• Note: if the SLAT is designed as a QTIP all of the income must be distributed to the beneficiary spouse.

•After death of grantor spouse, trust could be drafted to provide liberally for support.

•What clients truly want is the “I love you” will so that both spouses and the surviving spouse have use of all the assets until the death of the surviving spouse.

• Therefore, clients want to set up SLATs for each other!

•SLATs with identical terms and trustees, with similar assets which are established at or about the same time, could be attacked by the IRS using the reciprocal trust doctrine.

•The Reciprocal Trust Doctrine was set forth in Grace vs. United States, 23 AFTR 2d 69-1954 395 US 316 23 L Ed 2d 332 69-1 USTC ¶12609 1969-2 CB 173 (1969). See also IRC § 2036(a)(1).

•Basically, if A sets up a trust for B and B sets up a trust for A and each end up economically in the same position, then each trust is treated as a self-settled trust.

•Prepare a marital agreement giving entirely different property (not undivided ½ interests) to each spouse as that spouse’s separate property.

–One spouse gets the brokerage account

–Other spouse gets the real estate.

–Do not make gifts of the same value.

–Make trusts beneficiaries different –one trust for grandchildren, other trust for children or charities.

•One trust has power of appointment and not the other trust or if both have powers of appointment vary the class to whom assets can be appointed

•Appoint different trustees and successor trustees.

•wait for some period of time between the first SLAT and the date that the second SLAT is established by the other. There is no exact period of time that is “safe”.

•In general, the longer the period of time between the establishment of each SLAT, the less likely that the SLATs will be seen as “interrelated”.

•Divorce

•Beneficiary spouse dies first and assets all go to the children (consider insuring against this risk).

•SLATs need to be fully and carefully explained to clients.

• Do Not Ignore GST Tax; Allocation of Increased GST Exemption Amount.

•Without proper allocation of the GST exemption irrevocable trusts created by clients may be subject to the GST tax at the death of the non-skip person beneficiary unless the trust assets are included in the beneficiary’s gross estate.

•IRAs, 401(k) plans and other pre-tax assets (collectively “pre-tax plans”) are included in estate at full fair market value and withdrawals from pre-tax plans will be subject to income tax as taken.

•Assuming a combined state and federal income tax on the distributions from the pre-tax plans of 40%, this means that these are ideal assets to fund to charity without using other assets that would go fully to family members.

• Charity will receive 100% of the pre-tax plan assets. The charity can be a donor advised fund at a community foundation or a family foundation

•A family foundation is a private foundation which is a qualified 501(c)(3) organization which can be the recipient of charitable gifts during lifetime and charitable bequests at death.

•Any portion of a clients estate gifted during life or left to a qualified 501(c)3 family foundation at death would be deductible for federal income, gift and estate tax purposes.

•This not only saves taxes; but it keeps the money in control of the family as family members can serve on the board of directors of the family foundation.

• A donor advised fund (DAF) at a community foundation is a qualified 501(c)(3) organization which can be the recipient of charitable gifts during lifetime and charitable bequests at death.

• Any portion of a clients estate gifted during life or left to a qualified 501(c)(3) DAF at death would be deductible for federal income, gift and estate tax purposes.

• This not only saves taxes; but it keeps the money in control of the family as family members can serve as the family advisors on distributions made by the DAF

Recommendation: Gift LLC interests at a discount during lifetime

• Gifting minority interests to children or to trusts for children at a discount allows leverage of the annual exclusion and lifetime gift tax exemption using a Wandry formula gift.

•In the 2012 Tax court case of Wandry v Commissioner, TC Memo 2012-88, the taxpayers gifted membership units in a family LLC to their children and grandchildren. The Tax Court approved an adjustment formula clause triggered by post-audit revaluation under which units are reallocated so that value of number of units to each donee equaled the gift tax exclusion dollar amount specified in transfer documents. A Wandry type formula gift should be used to prevent gift tax from being incurred when the valuation of the family entity could be adjusted on audit by the IRS.

Recommendation: Gift LLC interests at a discount during lifetime

•Gifts of interests in LLC or other business assets can be used to create minority interests in assets of client at death.

• Example: 2% gift to children or trusts for children, could create a 49% interest in each spouse.

•A client with a taxable estate should not be the owner of any life insurance policy as this will just increase the size of the estate of the client by the death benefit paid on the life insurance and the estate tax due.

•life insurance placed in an ILIT should be considered to pay the estate tax liability .

•This is especially important when so much of the estate is illiquid (i.e. real estate, LLCs and other business entities).

•The primary purpose of a life insurance trust is to:

(i) shelter the proceeds of life insurance upon the life of both spouses from federal estate taxation and

(ii) provide liquidity for the payment of the estate tax and other debts of the estate without increasing the estate tax due because properly structured the life insurance proceeds in the life insurance trust are excluded from the estates of both spouses.

• Term

• Level (1, 5, 10, 20, and 30 years)

• Annually increasing (generally expires by age 80)

• Often an employee benefit

• Permanent

• Whole life

• Universal life

• Variable life

Permanent Insurance Example (for a Couple)

The data on the three preceding slides is hypothetical for illustration purposes only. The data is not intended to imply or assure the performance of any life insurance policy.

The illustrated benefits and values are not guaranteed. The assumptions on which they are based are subject to change by Northwestern Mutual.

Actual results may be more or less favorable than as shown in this illustration.

Illustrated values include interest crediting rates (see Important Information, Policy Summary) and Policy Charges based on the Company's current claim, expense and investment experience (2024 non-guaranteed charges and credits). Policy Charges are subject to change, but may not exceed the guaranteed charges.

• Death benefit

• Accumulated value

• Ownership considerations

• Modified Endowment Contracts (MEC)

• ILIT

• Estate taxes for closely held businesses or illiquid estates

• Special needs beneficiaries

• Business buyouts

• Roth IRA conversions for spouses

• Legacy planning and charitable giving

• Estate equalization among children, second marriages and family members

• Considerations when selecting a life insurance plan:

• Short term problem or long-term problem

• Credit strength of the carrier

• Flexibility of premium structure

• Short term, intermediate term, and long-term plan for cashflow

• First year administration market volatility

• Interest rates

• Tariffs

• Secure 2.0

Brad Justice uses Justice Financial as a marketing name for doing business as representatives of Northwestern Mutual. Justice Financial is not a registered investment adviser, broker-dealer, insurance agency or federal savings bank. Northwestern Mutual is the marketing name for The Northwestern Mutual Life Insurance Company (NM) and its subsidiaries, Northwestern Mutual Investment Services, LLC (NMIS) (Investment Brokerage Services), a registered investment adviser, broker-dealer, and member of FINRA and SIPC; and Northwestern Mutual Wealth Management Company® (NMWMC) (Investment Advisory Services), a federal savings bank. NM and its subsidiaries are in Milwaukee, WI. Brad Justice & Darci Severson are Insurance Agents of NM, Brad Justice & Darci Severson are Registered Representatives of NMIS, Brad Justice & Darci Severson are Advisors of NMWMC.

Northwestern Mutual Private Client Group is a select group of Northwestern Mutual advisors and representatives. Northwestern Mutual Private Client Group is not a registered investment adviser, broker-dealer, insurance agency, federal savings bank or other legal entity. Not all Northwestern Mutual representatives are advisors. Only those representatives with “Advisor” in their ti tle or who otherwise disclose their status as an advisor of Northwestern Mutual Wealth Management Company (NMWMC) are credentialed as NMWMC representatives to provide advisory services.

SESSION 3 11:20 AM

Social Security Disability Legislative

As of December 2024, over 8.7 million individuals received SSDI benefits, including disabled workers, disabled widow(er)s, and disabled adult children.

In January 2025, approximately 4.9 million people received SSI benefits exclusively, with an additional 2.5 million receiving both SSI and Social Security benefits.

Approximately y one e in n four r of f today's s 20year - olds s will l experience e a disability y before e reaching g retirement t age. .

Long - Term m Disability: : Estimates s indicate e that t one e in n seven n individuals s will l suffer r a long - term m disability y lasting g five e years s or r more e before e age e 65. .

Age e Distribution: :

About t 72% % of f Social l Security y disabled d workers s are e between n the e ages s of f 50 0 and d 66, , while e approximately y 28% % are e under r age e 50

Gender r Distribution: :

Women n constitute e a significant t portion n of f SSDI I beneficiaries, , with h many y receiving g benefits s based d on n their r own n earnings s or r as s dependents

The e Social l Security y Administration n (SSA) ) defines s disability y as s the e inability y to o engage e in n substantial l gainful l activity y (SGA) ) due e to o a medically y determinable e physical l or r mental l impairment t that:

Lasts s or r is s expected d to o last t at t least t 12 2 months s or r result t in n death.

Prevents s the e individual l from m performing g past t work k and d any y other r type e of f substantial l gainful l work k that t exists s in n the e national l economy.

This s definition n is s used d for r both h Social l Security y Disability y Insurance e (SSDI) ) and d Supplemental l Security y Income e (SSI) ) programs. . The e SSA A does s not t provide e benefits s for r partial l or r short - term m disabilities.

A child d is s considered d disabled d if:

They y have e a medically y determinable e physical l or r mental l impairment t (or r combination n of f impairments)

The e impairment t results s in n marked d and d severe e functional l limitations s that t significantly y restrict t the e child’s s ability y to o perform m daily y activities s compared d to o other r children n of f the e same e age.

The e condition n must t have e lasted d or r be e expected d to o last t for r at t least t 12 2 continuous s months s or r result t in n death.

President Barack Obama signed the ABLE Act in 2014. The law allows eligible individuals with disabilities to have a taxadvantaged savings account, modeled after 529 college plan accounts. Account funds can be used for a range of qualified expenses related to the disability of the individual. To be eligible for an ABLE Account an individual must have developed their disability before the age of 26. In 2026 the expansion will cover individuals to age 46.

The ABLE National Resource Center is a privatelyowned website and is not affiliated with the U.S. federal government It provides a wealth of targeted resources and best practice guidance to support the use of ABLE accounts, its staff does not provide case management on Social Security benefits or advice about investing in specific ABLE programs.

New Mexico has partnered with STABLE Account, a national ABLE plan, to make STABLE accounts available to residents of New Mexico.

New Mexico HB61 established the rules for ABLE New Mexico

STABLE Account partners with Vestwell, the program manager, to provide a simple and intuitive platform that helps people to manage their account and achieve their financial goals.

Easy Account Setup:

•OOpen an account online in about 10 minutes with basic beneficiary and funding details.

•IInitial deposit of $25; subsequent contributions as low as $1.

Choose from five portfolios:

•GGrowth: Higher risk, potential for higher returns.

•MModerate Growth: Balanced mix of stocks and bonds.

•CConservative Growth: Lower risk, lower returns

•IIncome: Focus on current income with low risk

• BankSafe: FDIC - insured, principal protection

Simple Contributions & Funding:

•AAdd money easily via one - time or recurring contributions, direct deposits, gifting, and more

•SSupports reaching up to $19,000 in yearly contributions.

•TThe first $100,000 saved in an ABLE account isn't counted as an asset by the SSI program

Transparent Fees & Account Usage:

•LLow monthly fee ($2.25/month) plus a small asset - based fee (0.19%0 33%)

•MMinimum online transfer of $5 to a linked bank account Performance & Support:

•MMonitor investment performance online.

•CComprehensive support available via phone, live chat, and FAQs.

E Act t of f 2024 4

This s bill l makes s permanent t three e tax x provisions s relating g to o ABLE E Accounts s established d to o assist t disabled d individuals, , specifically y provisions s allowing g increased d contributions s to o such h accounts, , the e allowance e of f a retirement t savings s contribution n tax x credit t up p to o $1,000, , and d allowing g a tax - free e rollover r from m a qualified d tuition n (529 9 plan) ) to o an n ABLE E account

“Today y is s a monumental l day, , with h the e critically y important t ENABLE E Act t passing g the e Senate When n I originally y entered d public c service, , it t was s to o fight t for r people e like e my y son n Stephen, , who o was s born n with h a rare e genetic c disease, , has s epilepsy, , is s on n the e autism m spectrum, , and d is s non - verbal. . This s legislation n is s the e perfect t example e of f what t I entered d public c service e to o do. . The e ENABLE E Act t helps s make e life e better r for r those e with h disabilities s by y allowing g them m and d their r families s to o continue e saving g and d investing g through h tax - free e savings s accounts This s legislation n empowers s those e individuals s to o secure e employment t and d actively y participate e in n society. . I am m thankful l for r the e support t of f my y colleagues s in n helping g to o ensure e the e passage e of f this s critically y important t legislation,” ” said d Senator r Eric c Schmitt t (R - MO)

For r 2025, , the e "ABLE E to o Work" " contribution n limit t is s $15,060 0 which h allows s eligible e working g individuals s with h disabilities s to o contribute e an n additional l amount t on n top p of f the e

standard d $19,000 0 annual l ABLE E account t contribution n limit, , provided d they y do o not t participate e in n an n employersponsored d retirement t plan n such h as s a 401(k). .

ABLE E and d Social l Security y Disability y Coordination

Case Study: Crystal is a young woman with cerebral palsy who qualifies for SSDI and recently started part-time work. Her parents established an ABLE account fo her to save for qualified expenses.

Challenges: Crystal wants to save more from her earnings without losing her SSDI benefits.

Solution: Through the ABLE to Work provision, Crystal is able to contribute additional funds to her ABLE account beyond the standard limit. She uses these funds for medical expenses, assistive technology, and transportation.

Tax credit of up to $1,000 for individuals and $2,000 for married couples. The credit can increase a taxpayer’s refund or reduce the tax owed but is affected by other deductions and credits. A taxpayer is eligible for the credit if they’re:

• Age 18 or older,

• Not claimed as a dependent on another person’s return, and

• Not a full-time student.

Furthermore, the Saver’s Credit can be claimed by:

• Married couples filing jointly with adjusted gross incomes up to $76,500.

• Heads of household with adjusted gross incomes up to $57,375.

• Married individuals filing separately and singles with adjusted gross incomes up to $38,250.

• Qualified surviving spouse filers.

CaseStudy:Johnisa30-yearoldwithadisability, whoworkspart-timeandearnsanannualincomeof $20,000. JohnopensanABLEaccounttosavefor disability-relatedexpenses,andoverthecourseof 2024,hecontributes$2,000tohisABLEaccount.

Eligibility:BecauseJohn’sincomeisbelowthe incomethresholdforsinglefilers,hequalifiesforthe ABLESaver’sCreditatthe50%rate.

Credit:Johnreceivesa$1,000taxcreditwhenhefileshistaxreturn,whichreduces theamountoftaxesheowestothefederalgovernment.Ifhistaxliabilityislessthan $1,000,thecreditwillbringhistaxbilldowntozero,buthewon’treceivearefundfor thedifferenceduetothenon-refundablenatureofthecredit.

A 529 to ABLE rollover allows funds from a 529 college savings plan to be transferred to an ABLE account. This can be done without penalty or tax.

The ABLE account must be for the same beneficiary as the 529 account, or for a member of the same family.

The rollover counts toward the annual contribution limit for the ABLE account.

Case Study: John and Marie had saved in a 529 education plan for their son, Ben, who was later diagnosed with autism and was unlikely to pursue higher education. With the passage of the ENABLE Act, they were able to transfer the funds into an ABLE account for Ben, providing for his long-term care and essential expenses.

The Act was signed into law by President Joe Biden on January 5, 2025.

The Act ends the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). These provisions reduced or eliminated the Social Security benefits of over 3.2 million people who receive a pension based on work that was not covered by Social Security (a "non-covered pension") because they did not pay Social Security taxes.

This law increases Social Security benefits for certain types of workers, including some:

• teachers, firefighters, and police officers in many states;

• federal employees covered by the Civil Service Retirement System; and

• people whose work had been covered by a foreign social security system.

Case e Study: Mark, a 62-year-old public school teacher, served 25 years in a noncovered pension system.

Later, he supplemented his income with a part-time job that contributed to Social Security.

Due to the Windfall Elimination Provision (WEP), Mark’s Social Security benefits were significantly reduced—even though he had worked in both covered and non-covered employment.

This reduction created a financial gap in his expected retirement income. With the reforms, Mark’s work history is treated more equitably, potentially increasing his Social Security benefit.

Resulting g Improvement:

A fairer benefit calculation helps ensure Mark receives retirement income that more accurately reflects his lifetime contributions.

Key y Takeaway:

The Social Security Fairness Act is designed to correct longstanding inequities for workers like Mark who split their careers between non-covered and covered employment—improving financial security in retirement.

ABLE Accounts: ideal for smaller, more accessible funds.

Special Needs Trusts: better for managing larger assets over the long term.

Combine ABLE accounts and SNTs for maximum flexibility and protection of assets.

https://www.ssa.gov/disability

Social Security released their SSDI and SSI disability claims allowance rates for the initial and reconsideration adjudicative levels for fiscal year 2024 broken down by nation, region, and state. Nationwide there was a slight decrease in the initial claim allowance rate when compared to last year (0.3%) and a slight increase in the reconsideration claim allowance rate (0.6%).

SSDI:

•BBased on individual’s work history and earnings.

•RRecipients typically qualify for Medicare after 24 months of receiving SSDI benefits.

•NNo asset limits.

SSI:

•AAvailable to individuals with limited income and resources.

•RRecipients qualify for Medicaid, and must meet strict asset and income limits to maintain eligibility.

MonthlyPayments:SSDIrecipientsreceivemonthlypaymentsbasedontheir averagelifetimeearnings.Paymentsvarybuttypicallyrangebetween$800and $1,800permonth,withtheaveragebenefitin2025around$1,976permonth.

RetroactiveBenefits:IftheSSAdeterminesthatthedisabilitybeganbeforethe applicationdate,theapplicantmayreceiveretroactivebenefitsforupto12months.

Cost-of-LivingAdjustments(COLA):SSDI benefitsareadjustedannuallytokeepup withinflation.For2025,SSDIrecipientswill receivea2.5%increasethroughtheCOLA.

In2025,themaximummonthlySupplementalSecurityIncome(SSI)paymentis$967foran eligibleindividualand$1,450foraneligiblecouple.Theamountyoureceivemaybelower basedonyourincomeandotherfactors.

SSIpaymentsarereducedbyanyincometherecipientreceives,includingwagesorin-kind support,butsometypesofincomeareexcludedfromthiscalculation.

UnlikeSSDI,SSIdoesnotprovideretroactivebenefitsforperiodspriortotheapplication date.Benefitsbeginthemonthaftertheapplicationissubmittedandeligibilityis established.

LikeSSDI,SSIbenefitsaresubjecttoannualCOLAtokeeppacewithinflation.For2025, SSIrecipientswillseea2.5%increaseintheirbenefitsaspartoftheannualCOLA adjustment.

To qualify for SSDI in 2025, you'll generally need 40 work credits, including 20 in the last 10 years before your disability began. However, the exact number of credits depends on your age when you became disabled.

• You can earn one work credit for every $1,810 in wages or self-employment income.

• You can earn up to four work credits per year.

• You must have held a job that Social Security covers, meaning you pay into Social Security.

• Individuals under 24 may qualify with six credits earned in the three years before the disability.

Case Study: Paul, a 50-year-old factory worker, suffers a back injury that renders him unable to work. He applies for SSDI after missing several months of work. Paul had worked steadily since age 20, earning more than enough credits to qualify for SSDI.

Challenges: Although Paul qualifies for SSDI based on his work credits, he is concerned about how his savings might affect his eligibility.

Solution: His financial advisor reassures him that because SSDI is based on work credits, his savings will not disqualify him. Paul’s SSDI payments begin after the fivemonth waiting period, providing him with the financial stability he needs while he recovers from his injury.

SSDI recipients do not face the same asset and income restrictions that apply to SSI recipients. Planners can manage SSDI beneficiaries’ assets with more flexibility without worrying about strict income caps.

SSDI recipients automatically qualify for Medicaid after 24 months of receiving SSDI benefits. This is an important consideration for clients who are concerned about healthcare costs.

Note: Some SSDI recipients also qualify for Medicaid to pay for their Medicare premium. An SNT would be needed to protect their eligibility for Medicaid in this scenario.

Income and asset limits:

$2,000 for individuals

$3,000 for married couples

This has not changed for 36 years!

Introduction: This bipartisan bill was introduced in the Senate on September 12, 2023, by Senators Sherrod Brown (D - OH) and Bill Cassidy (RLA).

Provisions: The legislation proposes increasing the SSI asset limits from $2,000 to $10,000 for individuals and from $3,000 to $20,000 for married couples, with adjustments for inflation.

Current Status: After its introduction, the bill was referred to the Senate Committee on Finance As of this date, it has not advanced beyond the committee stage.

Introduction: Representative Raúl M Grijalva (D - AZ) introduced this bill in the House on January 30, 2024

Provisions: The act aims to modernize SSI by: Increasing Benefit Rates: Raising benefits to at least 100% of the Federal Poverty Level.

Updating Resource Limits: Setting asset limits at $10,000 for individuals and $20,000 for couples, with inflation adjustments. Eliminating Benefit Reductions: Removing penalties for in - kind support and maintenance

Current Status: The bill was referred to the House Committee on Ways and Means and subsequently to the Subcommittee on Work and Welfare on December 17, 2024. No further action has been reported.

The bill proposes:

•EElimination of the 5 - month waiting period for SSDI benefits

•EElimination of the 24 - month waiting period for Medicare eligibility Status:

•IIntroduced on February 9, 2023, by Representative Lloyd Doggett (D - TX), referred to the House Committee on Ways and Means and the Committee on Energy and Commerce. On February 17, 2023, it was further referred to the Subcommittee on Health. As of this date, no further action has been reported.

•IIntroduced on February 9, 2023, by Senator Bob Casey (D - PA), the bill was read twice and referred to the Senate Committee on Finance No subsequent actions have been recorded In December 2024, Senators Debbie Stabenow (D - MI) and Susan Collins (R - ME) introduced the We Can’t Wait Act, which also addresses the elimination of the five - month waiting period for SSDI benefits

Case Study: David was approved for SSDI after a serious car accident left him disabled. However, the five-month waiting period created a financial hardship for him and his family. The Stop the Wait Act or We Can’t Wait Act would have allowed him to access benefits immediately, alleviating the financial burden of his disability.

As of September 30, 2024, food is no longer counted as in - kind support and maintenance (ISM) for SSI. Trustees can now provide food assistance without affecting SSI eligibility

Case Study: Lisa’s family recently set up a special needs trust for her, but they were concerned about how food assistance would impact her SSI benefits under the old rules.

Challenges: Previously, any food purchased by the special needs trust would have counted as in-kind support and maintenance (ISM), reducing Lisa’s SSI benefits.

Solution: With the SSA’s new rule, effective September 30, 2024, food is no longer counted as ISM, allowing Lisa’s trustee to use SNT funds for her groceries without affecting her SSI payments.

SSA revised the definition of past relevant work (PRW) by reducing the relevant work period from 15 to 5 years Additionally, the SSA will not consider past work that started and stopped in fewer than 30 calendar days to be PRW. These changes will reduce the burden on individuals applying for disability by allowing them to focus on the most current and relevant information about their past work. The changes will also better reflect the current evidence about worker skill decay and job responsibilities, reduce processing times, and improve customer service.

Effective on June 8, 2024.

• Martin O’Malley served as Commissioner of SSA from December 2023 to January 2025. A lifelong public servant, Mr. O’Malley was Assistant State Attorney for Baltimore, member of Baltimore City Council, Mayor of Baltimore, and then Governor of Maryland. His mission was to improve customer service amidst the reality of a 27year low in staffing.

• Michelle King, was appointed acting Commissioner of the SSA in January 2025, having worked 30 years in the agency, resigned February 17, 2025 after she refused to provide DOGE staffers access to sensitive information at the SSA.

• Lee Dudek, who had previously led SSA’s anti-fraud office, has been appointed as Acting Commissioner of SSA pending the Senate confirmation of Frank Bisignano, president and CEO of Fiserv to run the office full time.

• Mr. Bisignano has no previous experience in the SSA or in public service. Fiserv is a global financial technology company that offers services and solutions for payments, banking, and commerce.

•NNational Organization of Social Security Claimant’s Representatives (NOSSCR): NOSSCR.org.

The mission of NOSSCR is to advocate for improvements in Social Security disability programs and to ensure that individuals with disabilities applying for Social Security Disability and SSI benefits have access to highly qualified representation and receive fair decisions

•FFollow NOSSCR CEO David Camp’s LinkedIn Profile

•CCharles T Hall, Social Security News Blog: socsecnews blogspot com

•NNational Association of Disability Representatives (NADR): NADR org

•CContact Legislators: Write letters, make phone calls, and schedule meetings with congressional representatives and senators.

•JJoin Advocacy Campaigns: Partner with organizations such as the National Disability Rights Network (NDRN), and AARP (AARP is the nation's largest nonprofit, nonpartisan organization dedicated to empowering Americans 50 and older to choose how they live as they age).

•SSubmit Public Comments: Participate in public comment periods for proposed SSA regulations

•SShare Personal Stories: Highlight real - life examples of how current Social Security policies affect individuals with disabilities, emphasizing the need for change.

Dear [Representative/Senator Name],

I am writing to urge you to support legislation that improves financial security and access to benefits for people with disabilities. Specifically, I encourage you to advocate for the passage of the legislation such as the SSI Savings Penalty Elimination Act, the SSI Restoration Act, and the Stop the Wait Act These bills will modernize outdated asset limits, eliminate unnecessary waiting periods, and reduce financial hardship for millions of individuals People with disabilities should not be forced into poverty to qualify for essential benefits By supporting these initiatives, you can help promote economic independence and improve the quality of life for those who rely on SSDI and SSI Please prioritize these important measures and ensure that Social Security programs are fair, accessible, and sustainable for future generations

Thank you for your leadership and commitment to supporting individuals with disabilities

Sincerely,

[Your Name]

[Your Title/Organization]

[Your Contact Information]

What questions do you have about how to incorporate these changes into your current planning strategies?

Are there any client situations you’re dealing with where these updates could make a difference?

SESSION 5 2:15 PM

•1. Fiduciary Obligations of Personal Representative and Trustee

•2. Breaches of those duties

•3. Attorney Client Issues

Fiduciary Obligations of Personal Representative and Trustee

Fiduciary Obligations of Personal Representative and Trustee

INVENTORY

PAY ALL LEGITIMATE DEBTS

Fiduciary Obligations of Personal Representative and Trustee

ASSET PROTECTION

•Duty of Care

FULL DISCLOSURE AND ACCOUNTABILITY

REQUIRES:

A DUTY: An actual fiduciary relationship

BREACH: failure to meet a fiduciary obligation

HARM: actual damage as a result of the failure.

Unreasonable Delay in Distribtutions

“As advisor, a lawyer provides a client with an informed understanding of the client’s legal rights and obligations and explains their practical implications. As advocate, a lawyer zealously asserts the client’s position under the rules of the adversary system. As negotiator, a lawyer seeks a result advantageous to the client but consistent with requirements of honest dealings with others. As an evaluator, a lawyer acts by examining a client’s legal affairs and reporting about them to the client or to others.”

The core obligations of attorney-client representation require an attorney to provide competent (16-101) and diligent (16-103, 16-104) representation, maintain client confidentiality (16-106), avoid conflicts of interest with present (16-107-108) and past clients (16-109) and to charge a reasonable fee (16-105)

•1. Who is the client?

•2. Conflicts of Interest

•Fiduciary vis a vis the estate?

•Between Co-Fiduciaries?

•Between beneficiaries?

•Between the attorney and the estate?

•3. Attorney Client Privilege

•4. Privity and Malpractice

•5. Termination of the Attorney-Client Relationship

–Withdraw from the legal action

–Send closing letter

SESSION 6 3:25 PM

March 7, 2025

Alphabet t Soup p of f Retirement t Accounts

• IRA

• RMD

• RBD

• QCD

• PPA

• PATH

• DB

• SECURE

• EDB

• CGA

Let’s play “Spot the Acronym”…

Once e Upon n a Time, , before e 2020…

• Tax Deferral for IRAs (Individual Retirement Accounts)

• Section 401 of the Tax Code and Regs

• Basic Idea

• Earn now,

• Save for later,

• Tax later

• How much later?

• At least after age 59 ½

• But not forever!

Enter r RMDs

• RMD: Required Minimum Distributions

• Mandatory Taxable Distribution

• Annually

• After RBD: Required Beginning Date

• Based on Life-Expectancy Tables

• Continues for beneficiary after participant’s death

What t if f you u don’t t need d the e money… and d you u like e to o give e money y to o charity?

• QCD: Qualified Charitable Deduction

• Distributions from an IRA directly to qualified charities (not DAFs, Private Foundations, or supporting orgs)

• Not included in income at all

• Better than a charitable deduction limited to % of AGI

• Part of the 2006 PPA (Pension Protection Act)

• Extended indefinitely by the 2015 PATH Act (Protectiong Americans from Tax Hikes Act)

• Up to $108,000 per year (in 2025), adjusted for inflation

• Must be 70½

What t happens s when n a participant t dies?

• Had they reached their RBD?

• Did they have a Designated Beneficiary (DB)?

• Is the beneficiary their spouse?

• Is the beneficiary a trust?

• Is the beneficiary a charity?

• Is the beneficiary their estate? Why, you ask?

RMDs s Stretched d Over r a Measuring g Life, , or r not

• Depends on:

• Whether the participant had reached their RBD

• What kind of beneficiary you are:

• Spouses have the best options

• Estates have the worst treatment

• Trusts have to meet specific requirements

• Charities don’t pay the income tax, but have to get their piece and go away asap!

• All other individual beneficiaries, well, that’s changed…

• Setting Every Community Up for Retirement Enhancement

• Passed December 17, 2019, Effective January 1, 2020

Tacks on a new section (H) to UTC 401(a)(9)

Intended to encourage more retirement savings and for more employers to offer retirement plans

• Extended RBD to 72

• Eliminated cap for contributing beyond age 70½

• BUT, accelerated tax by eliminating stretch distribution for inherited IRAS in favor of 10-year rule, except for EDBs

• 10-year rule says full distribution within 10 years

• Applies to accounts of participants dying after 2019

• What about RMDs? Hold that thought.

• Eligible Designated Beneficiaries Spouse

Designated Beneficiary not more than 10 years younger than the participant

• Designated Beneficiary who is disabled or chronically ill

• Designated Beneficiary who is a minor child of the participant, until age 21, then 10-year rule kicks in

• (Or see-through trusts for any of the above)

• Issued February, 2022

• Correction published March 14, 2022

• Intended to clarify SECURE

• RMDs still need to be made, wait what!?

• Code Section 401(a)(9)(B)(i) still stands

• Death after RBD –distribution at least as rapidly as

• Through life of participant and DB

• No RMD for 2020, no excise tax for missing 2021 RMD

• Good faith interpretation

• Passed December 29, 2022

• Intended to clarify SECURE, and more

Extended RBD to 73 for participants turning 72 after 2022

Extended RBD to 75 in 2033 for participants turning 74 after 2032

• SNTs can have charities as remainder beneficiaries, just not DAFs and Private Foundations

• Change to disability onset age for ABLE accounts from 26 to 46 starting in 2026

• After 2023, 529 plans can be rolled over to a Roth IRA

• One-time $50k QCD to a CGA, CRUT or CRAT

Excuse me while we take this commercial break…

• One-time QCD up to $54,000 (in 2025)

• Split-interest contract with a single charity

• Income stream to donor, remainder to charity

• Charity administers it and sets the payout rate

Now where were we?

Notices s 2022-53, , 2023-54 4 and d 2024-35

• Further clarifiction

• Further waiver of excise tax on missed RMDs in 2022, 2023 and 2024

• Further postponement of final RMD regulations to 2025

• No RMDs for inherited Roth IRAs because participant had no RBD, just 10-year rule, or longer if EDB

• Issued July 2024, Effective September 2024

• Confirms that RMDs continue for inherited accounts where participant died after RBD

• No make ups, recalculations or extension for missed distributions pre-2025

• For DBs who are not EDBs, full distribution by end of 10th year after year of death, whether participant died before RBD or not

• For minor EDBs, minority ends at age 21, then 10-year rule kicks in

Defintion of child expanded to include stepchild, adopted child and eligible foster child

Trust for multiple children, 10-year rule kicks in after the youngest child turns 21

• Once an EDB dies, 10-year rule applies thereafter.

• Stretch still applicable to pre-2020 inherited IRAS, but 10year rule kicks in once that beneficiary dies.

, Traditional l IRAs

Death h

Before e

Required d

Beginning g

Date

Death h After r

Required d

Beginning g

Date

1) No o Required d Minimum m Distributions s (RMDs)

2) Fully y distribute e by y end d of f 5th h year r after r the e year r of f participant’s s death 10 0 years s if f a designated d beneficiary, , stretch h if f bene e is s an n Eligible e Designated d Beneficiary y (EDB)

Roth h IRAs

1) No o RMD

2) Fully y distributed d by y end d of f 5th h year r after r the e year r of f participant's s death, , or r 10 0 years s if f a designated d beneficiary, , stretch h for r EDBs

1) RMDs s every y year r after r the e year r of f participant's s death h or r death h of f EDB; ; AND 2) Fully y distributed d by y end d of f 10th h year r after r the e year r of f participant's s death, , unless s EDB, , or r within n 10 0 years s of f death h of f EDB N/A

PM

“EFFECTIVE

BY John Attwood, NCG Sr. Vice-President, Trust Officer

Business Development

March 7, 2025

New Mexico Estate Planning Conference

What is “Effective Communication with Our Client?”

Oral…Written…Non-Verbal

• We all have clients that have a basic understanding of the role we play in their lives. As the role varies from investment advisor to CPA, to Estate Planning Attorney to Trust Officer, our method of communication varies.

• How do we “effectively” communicate and maximize the impact of our expertise with our client or beneficiary?

• It’s easy to communicate “good news” but what if we face a downturn in the market or our client has a significant tax liability or the expectations of our estate planning client or beneficiar y is well beyond what is reasonable?

• Let’s learn from each other: communication skills, best practice and creative methods to transfer concepts relevant to our clients.

“ Trustworthy ” via Amazon or Barnes and Noble by: Hartley Goldstone and Kathy Wiseman

Concise Language –what’s unnecessary?

Appropriate Tone –monotone, raising your voice?

What’s the Audience Perspective-How do you “read” your client?

Concise Language (oral or written)

• Concise Language –Emails, Phone Calls, Voicemail, Cards

• Tone –Montone, Fast, Slow, “Millennial-Speak”?

• NV-How do you “read” your client and them you?

•Section 46A-8-801-Duty to administer trust: In good faith, according to the terms & purposes, and the interests of the beneficiaries and in accordance with the NM UTC.

•Section 46A-8-802 -Duty of loyalty: Administer solely in the interests of the beneficiaries

•Section 46A-8-803 –Impartiality: if two or more beneficiaries, trustee shall act impartially in investing, managing, and distributing the trust property, giving due regard to the beneficiaries’ respective interests.

•Section 46A-8-804 -Prudent administration: administer the trust as a prudent person would, by considering the purposes, terms, distributional requirements and other circumstances. Exercise reasonable care, skill and caution.

•Section 46A-8-805 -Costs of administration: Costs that are “Reasonable”, Consider purpose of the trust and skills of the trustee (Market survey with colleagues?)

•Section 46A-8-807 -Delegation by trustee: Reasonable care, skill and caution in…

1.Selecting an agent (CPA, Investment Advisor, Real Estate Agent, Private Investigator, Appraiser, etc.)

2.Establish the scope of work (engagementletter or contract)

3.Review the performance periodically (reports, review tax returns, etc.)

•Section 46A-8-809 -Control and protection of trust property: Reasonable steps to take control and protect trust property (real estate, TPP, investment portfolio)

•Section 46A-8-810 -Recordkeeping and identification of trust property: Inventory, accounting system for P&I, bifurcate trust assets from your own

•Section 46A-8-811 -Enforcement and defense of claims: How far back do you go?

“Blended Families…all the stuff”