African Leadership Magazine September 2024 Edition

Magazine

...A Publication of The African Leadership Organization

Ken Giami

Founder & Executive Chairman

King Richard Igimoh

Group editor

King.richards@africanleadership.co.uk

Staff Writers

Blossom Ukoha

Blessing Ernest

Country Representatives

Muna Jallow

The Gambia & Senegal

Meresia Aloo

Kenya

Janet Abena Quainoo Ghana

Editorial Board

Peter Burdin

London UK - Chair

Nwandi Lawson

Atlanta USA - Member

Simon Kolawole

Lagos Nigeria - Member

Peter Ndoro

SABC Editor Johannesburg - Member

Frenny Jowi

Nairobi Kenya- Member

Brig. Gen. SK Usman Rtd

Abuja Nigeria - Member

David Morgan

Washington DC USA- Member

Creatives & Graphics

John Mutum

Ayeni Victor Adegbola

Adeiza Okatenwu

Jehoshaphat Ogujiuba

CORPORATE HEADQUARTERS

Portsmouth Technopole, Kingston Crescent, Portsmouth PO2 8FA, United Kingdom

T: +44 23 9265 8276

Fax: +44 023 9265 8201

E: info@africanleadership.com

....Identifying, Celebrating & Enabling Excellence in Africa

www.africanleadershipmagazine.co.uk

Furo Giami

Chief Operating Officer / Executive Director

Sasha Caton Manager, UK & European Operations

Ehis Ayere

Group Head, Sales & Business Development

Ngozi Nwokolo

Executive Assistant to the Chairman

Samuel M. Elaikwu

Manager, Sales & Business Development

Happy Bension Director of Operations, North America

Christy Ebong Head, Research & Admin - North America

Stanley Emeruem

Business Development Manager

Kembet Bolton

Business Development Manager

Oluwatoyin Oyekanmi

Head, South African Bureau

Benard Adeka Head, Nigeria SS/SE

Simon Ugwu

Group Head of Events

Digital Media Team

Abayomi Israel Alalade

Deborah Olajuwon

Gaawa Barivule God’slove

AFRICAN & REGIONAL REPRESENTATIVE OFFICES

Abuja ■ Accra ■ Atlanta ■ Banjul

■ Bujumbura ■ Freetown ■ Johannesburg ■ London ■ Monrovia

■ Nairobi ■ Washington DC

ISSN 2006 - 9332

While great care has been taken in the receipt and handling of materials, production and accuracy of content in the magazine, the publisher will not take responsibility for views expressed by the writer

JOIN THE CONVERSATION

www.africanleadershipmagazine.co.uk

FOLLOW US ON SOCIAL MEDIA

Facebook: African Leadership Magazine

X: @AfricanLM

Instagram: @Africanleadershipmag

Linkedin: African Leadership Magazine

Youtube: African Leadership Magazine

FROM THE PUBLISHER’S Desk

Dr. Ken Giami

Founder, African Leadership Magazine UK

It’s Africa’s Time: A Journey of Progress and Promise

I woke up this morning reflecting upon and nodding to the rhythm of Shakira’s FIFA 2010 World Cup (TM) song, ‘This Time for Africa,’ and was filled with awe at how much progress Africa and Africans have made globally. As I thought about Africa’s journey from the days when a major international publication referred to her as the ‘hopeless continent’, I couldn’t agree more that this was Africa’s century, Africa’s time!

The African continent brims with potential and progress. Often called the cradle of humanity, Africa is emerging as a beacon of innovation, resilience, and growth. The hope for humanity’s food security and the future of tomorrow’s global workforce lies in today’s youthful Africa. Little wonder there is an ongoing rush to engage the continent -both from the good, bad and ugly. This is truly Africa’s time, and the world is taking notice.

This refreshing narrative can be seen in many ways; however, I shall focus on only the following areas:

A Rebound in Economic Growth

Africa’s economic landscape is transforming at an unprecedented pace. According to the African

Economic Outlook, the rebound in Africa’s average growth includes a rise to 3.7% in 2024 and 4.3% in 2025, exceeding the projected global average of 3.2%. Of this figure, 17 African economies are projected to grow by more than 5 percent in 2024. This story has been consistent, with Africa accounting for 6 of the 10 fastest-growing economies over most of the last 15 years.

“Africa is no longer the sleeping giant. It is awake, and it is on the move,” said Akinwumi Adesina, President of the African Development Bank. His words resonate with the palpable energy and ambition that permeate the continent.

Technological Innovation and Entrepreneurship

Africa is also becoming a hub for technological innovation. The rise of tech hubs in cities like Nairobi, Lagos, and Cape Town has earned Africa the moniker “Silicon Savannah.” In 2020, African tech startups raised over $1.4 billion in funding and almost $800 million in the first half of 2024 alone, a testament to the continent’s burgeoning tech ecosystem.

One inspiring story is that of Flutterwave, a Nigerian fintech

company that has revolutionized online payments across Africa. Founded in 2016, Flutterwave has facilitated over 140 million transactions worth over $9 billion. Its success story is a beacon of hope for aspiring African entrepreneurs.

Education and Empowerment

Education is the cornerstone of Africa’s progress. The continent has seen a significant increase in school enrollment rates, with UNESCO reporting that primary school enrollment in Sub-Saharan Africa reached 80% in 2018 and is growing year on year. Moreover, initiatives like the African Union’s Agenda 2063 aim to transform Africa into a global powerhouse through education and skill development.

Dr. Ngozi Okonjo-Iweala, the first African and first woman to lead the World Trade Organization, and that of Dr Tedros Gebreyesus of the World Health Organization exemplify the power of education and empowerment as Africans continue to occupy strategic positions globally and contribute to solving some of humanity’s biggest challenges. Their successes, and especially those of the African diaspora, are a testament to the boundless potential

that education unlocks. This is without prejudice to the extraordinary work still required in the education sector across the continent.

Cultural Renaissance

Africa’s cultural influence is also making waves globally. The continent’s rich heritage, music, art, and fashion captivate audiences worldwide, driving Africa’s global soft power. The global success of artists like Burna Boy and Wizkid, who have brought Afrobeat to the international stage, highlights Africa’s cultural renaissance.

In the words of Nelson Mandela, “The cultural heritage of Africa is the most precious treasure we have.” This treasure is now being shared with the world, enriching global culture and fostering a deeper appreciation for Africa’s diverse traditions. It is Africa’s time and African rhythms are danced to in malls, and stadiums from India to Brazil and worldwide.

In the Climate space, Africa’s forests may be humanity’s hope in addressing global environmental challenges. Wangari Maathai, the first African woman to win the Nobel Peace Prize, once said, “It’s the little things citizens do. That’s what will make the difference. My little thing is planting trees.” Her legacy lives on through the millions of trees planted across Africa, symbolizing hope and resilience.

The continent is rising, driven by the indomitable spirit of its people, the richness of its culture, and the promise of its future. As Africa continues to make strides in economic growth, technological innovation, education, cultural influence, and environmental stewardship, it is clear that the world must pay attention.

In the words of Kwame Nkrumah, “We face neither East nor West; we face forward.” Africa is moving forward, and its journey is one of inspiration, progress, and boundless potential. This is Africa’s time, and the world is watching in awe.

Africa’s economic landscape is transforming at an unprecedented pace. According to the African Economic Outlook, the rebound in Africa’s average growth includes a rise to 3.7% in 2024 and 4.3% in 2025, exceeding the projected global average of 3.2%. President of the African Development Bank, Dr Akinwumi Adesina; Deputy President of South Africa HE David

Mabuza; and Dr Ken Giami, Chairman of African Leadership UK at an ALM event in Johannesburg

The Power of the African Diaspora: African-American Businesses in Africa

Key Voices Shaping Africa’s Business and Economic Landscape 82

Green Ports and Trade Connectivity: A Conversation with Akif Ali Khamis, Zanzibar Ports Corporation (ZPC) 74

BOLD REFORMS, IMPACTFUL LEADERSHIP, AND SOUTH SUDAN’S ECONOMIC RESURGENCE

In this exclusive interview, we sit down with Dr. James Alic Garang, the Governor of the Bank of South Sudan. His professional journey is a remarkable tale of resilience and dedication, reflecting the tumultuous history of South Sudan itself. Born in the village of Northern Bahr el-Ghazal during a time when exact birth years were often estimated based on significant historical events, Dr. Garang’s path has been anything but conventional. From the perilous trek to Ethiopia as one of the Lost Boys of Sudan to completing his education in refugee camps and eventually earning his degrees in the United States, his experiences have profoundly shaped his strategic vision for the Bank of South Sudan. Returning to his homeland in 2011, Dr. Garang has been deeply involved in economic and financial sector development, contributing his expertise to various national and international institutions. His tenure at the World Bank in Dubai and later at the International Monetary Fund in Washington has provided him with invaluable insights into global financial policies, which he now leverages to drive economic stability and development in South Sudan. Dr. Garang’s leadership at the Bank of South Sudan is characterised by a commitment to transparency, accountability, and modernization, with a particular focus on establishing an efficient national payment system, enhancing staff welfare, and expanding financial services across the nation. Through these efforts, he aims to transform the Bank into a cornerstone of economic stability and growth, fostering a brighter future for South Sudan

Excerpt

Please tell us about your professional journey that led you to become the Governor of the Bank of South Sudan. How have your experiences shaped your strategic vision for the bank?

I am James Alic Garang from Northern Bahr el-Ghazal, South Sudan. My exact birth year is uncertain, as I was born in a village before the era of hospitals. My mother estimated my birth year based on significant events, such as the signing of the 1972 peace agreement between Sudan and South Sudan rebels. In 1987, I moved from my home to Ethiopia, walking for three months. Along with about 20,000 young boys known as the Lost Boys of Sudan, I received education and training there until we were forced to return to South Sudan in 1991. We then relocated to the Kakuma refugee camp in Kenya, where I completed high school.

In 2001, I arrived in Salt Lake City, Utah, as part of an American government initiative. I attended college, graduating in 2005, the same year South Sudan gained autonomous status. In 2006, I visited my family in South Sudan after 19 years. I then pursued a graduate programme at the University of Massachusetts, Amherst, and interned with the African Development Bank in 2009-2010, which greatly influenced my economic and development perspectives.

One of our biggest projects is the national payment system, supported by the African Development Fund and the East African Community. This system enables real-time settlements and incorporates a national switch for monitoring capital flows

Our vision is guided by transparency, accountability, and independence, ensuring greater transparency in operations and accountability to Parliament and the presidenc

Returning to South Sudan in 2011, I worked on research related to SMEs and financial sector development. In 2013, I joined the World Bank in Dubai, gaining valuable insights into global financial policies. These experiences shaped my strategic vision for the Bank of South Sudan, focusing on economic development and stability.

In 2014, despite the conflict, I returned home and joined Upper Nile University as an assistant professor, eventually becoming the Deputy Dean of the College of Economics and Social Studies. I also conducted research and advised the government.

Later, I worked for the IMF in Washington, advising on policies for 23 countries. This role allowed me to meet influential individuals and further refine my vision for economic stability.

My journey from a young child leaving home to a soldier, refugee, and then an economist has been shaped by the kindness and support of many people. These experiences have informed my vision for the Bank of South Sudan, emphasising transparency, accountability, and independence.

What is your strategic vision for positioning the Bank of South Sudan as a cornerstone of economic stability and development? How are you aligning the bank’s mission and operations to achieve this vision?

The vision of the Bank of South Sudan is to advance and expand financial services, transforming it into a modern central bank. This involves three critical elements:

1. National Payment System: We aim to establish an efficient national payment system to reduce reliance on cash transactions and promote digital financial services. This requires educating the public to embrace digital money.

2. Staff Welfare: We prioritise the

welfare of our staff by providing comprehensive training, benefits, and a conducive working environment. This enhances productivity and loyalty, driving the bank’s success.

3. Expanding Financial Services: We are committed to extending financial services to all states, bringing government services to local communities. The 2018 peace agreement has allowed us to open branches in various states, fostering private sector growth.

Our vision is guided by transparency, accountability, and independence, ensuring greater transparency in operations and accountability to Parliament and the presidency.

How would you describe your leadership style?

My leadership style is participatory and consultative, rooted in inclusivity, fairness, and diversity. I believe in bringing everyone on board to harness diverse perspectives and expertise. This approach reduces the risk of errors and ensures more effective decisionmaking.

I emphasise fairness and diversity in gender, regional representation, and opinions. No committee at the Bank of South Sudan is formed without female representation, and regional diversity is equally important. I value the unique contributions of each team member, fostering a sense of belonging and commitment to our collective goals.

How do you ensure that your team follows the vision or idea you are trying to implement, especially when it involves significant changes from previous practices?

Change management involves informing the team about the new vision, gathering their views, and addressing resistance individually or collectively. Ensuring everyone has a role in different

aspects of the organisation promotes a sense of value and involvement.

Establishing a hierarchy where certain directives must be followed is crucial. Addressing non-compliance by emphasising the necessity of participation and finding ways to work around resistance ensures the realisation of the vision.

Can you discuss some of the key reforms you’ve implemented and their impact on the country’s banking system?

One of our biggest projects is the national payment system, supported by the African Development Fund and the East African Community. This system enables real-time settlements and incorporates a national switch for monitoring capital flows. We have signed an MOU with the Ministry of Finance to avoid monetizing deficits, limiting central bank lending to the government.

Improving communication with stakeholders has been a priority, enhancing transparency and accountability. These reforms are designed to modernise our banking system and strengthen our economy.

What role do you see the bank playing in promoting financial inclusion?

We encourage commercial banks to establish branches in various states and take further steps towards financial inclusion. Despite challenges like low borrower incomes and weak enforcement of contracts, we remain committed to enhancing financial inclusion.

What was your approach to addressing inflation challenges?

Inflation has been driven by internal conflicts and external shocks like the COVID-19 pandemic. We have implemented measures to support supply-side policies, particularly through government investments in agriculture. Managing liquidity and limiting excessive cash withdrawals have been crucial steps in mitigating inflationary pressures.

Could you elaborate on your intervention approach to addressing forex and exchange rate volatility?

We have introduced a term deposit scheme and a reference rate for banks to use as a benchmark. Restructuring the informal currency market and addressing the scarcity of US dollars

One of our biggest projects is the national payment system, supported by the African Development Fund and the East African Community. This system enables real-time settlements and incorporates a national switch for monitoring capital flows

have been key initiatives. Ensuring compliance with regulations and promoting transparency in currency trading are ongoing efforts.

In summary, we are actively implementing measures to stabilise exchange rates, promote transparency, and ensure financial regulations are upheld for the benefit of our economy and its stakeholders.

Based on what you’ve said so far, it seems creating financial literacy awareness against inflation and currency management is crucial. What steps are you taking to create such programmes?

Current Initiatives: Currently, we haven’t undertaken extensive initiatives in financial literacy, but we recognise its importance. Drawing from Kenya’s experience between 2005 and 2008, Equity Bank invested significantly in financial literacy programmes, focusing on educating people, especially women, on effective business management, accessing loans, and expanding enterprises. The success of these efforts has demonstrated the positive impact of financial literacy on economic empowerment.

Recent Efforts: Inspired by these insights, the Bank of South Sudan hosted a national economic conference last year to gather public views on our country’s challenges and potential solutions. Following these discussions, it was recommended that we take proactive steps in public awareness and education. In March, we organised our first public awareness conference at the Radisson Blu Hotel, where we outlined the bank’s mandates, operational guidelines, and future plans. The response was positive, with many participants appreciating our efforts.

Future Plans: We are committed to expanding our public awareness initiatives and enhancing financial literacy across South Sudan. We recognise there is much more to be done and are eager to learn from best practices to tailor programmes that will effectively address financial management challenges in our country.

Dr. Alic, I’d like to look at economic growth, resilience, and sustainability in the country. Given the country’s reliance on oil, what are the strategic policies going forward to diversify the economy? What sectors are you focusing on?

We are committed to expanding our public awareness initiatives and enhancing financial literacy across South Sudan. We recognise there is much more to be done and are eager to learn from best practices to tailor programmes that will effectively address financial management challenges in our country

Looking ahead, while there’s a global push towards net zero emissions by 2030, South Sudan remains focused on harnessing its natural resources, including oil and agriculture. Agriculture, with its competitive advantage and the Nile River’s potential for irrigation, holds promise

Current Economic Strategies: Economic growth encompasses various sectors, both governmental and private, amid challenges in the oil sector. This year’s growth projections may be modest due to oil production disruptions. However, several initiatives are underway to expand other sectors. The government is actively promoting agriculture despite challenges like seed and equipment shortages. Agriculture is critical for sustainable growth and development.

Sectoral Focus: Policies are being developed, particularly in gold mining, chaired by the Ministry of Mining. Efforts include studying successful models from countries like Tanzania for a gold purchase programme and regulating artisanal production to curb smuggling. Additionally, improving the national payment system infrastructure is underway to support service efficiency and economic transactions. Key sectors targeted for growth include agriculture, mining (gold), and services, with a focus on enhancing payment system services to facilitate economic activities and improve efficiency.

Acknowledged Challenges: Challenges such as oil dependency and infrastructure/resource shortages are acknowledged, with ongoing efforts to address them through effective policy implementation.

Historically, South Sudan has heavily relied on oil for government revenue. What would be an ideal percentage for this reliance to drop down to?

Current Revenue Structure: Oil used to constitute 98% of government revenue, but due to decreased production, this reliance has dropped, making it challenging to meet financial obligations.

Future Projections: Looking ahead, while there’s a global push towards net zero emissions by 2030, South Sudan remains focused on harnessing its natural resources, including oil and agriculture. Agriculture, with its competitive advantage and the Nile River’s potential for irrigation, holds promise. Achieving a 50/50 balance between oil and other sectors over time seems reasonable. Oil remains crucial for jumpstarting the economy, echoing Ha Joon Chang’s perspective on gradual economic diversification. Dependence solely on oil is unreliable, and diversification is essential for sustainable growth.

Dr. Alic, when we look at attracting investors to South Sudan, what policies and initiatives have you implemented to create a conducive environment for them, whether through legal frameworks or other policies?

We are part of the East African Community (EAC) and are embracing policies to harmonise with the region. This includes policy harmonisation and improving payment systems, similar to the East Africa payment system

Investment Environment: Currently, this is an area where we’ve made limited progress. The government has established a one-stop shop for investment, consolidating functions previously handled by the Revenue Authority and Ministry of Trade into the Ministry of Investment after the peace agreement.

Legal Protections: We have robust laws in place to protect and facilitate investments, although significant inflows have yet to materialise due to lingering public sentiment and investor confidence issues. Ensuring capital mobility is crucial. Investors in South Sudan enjoy unrestricted repatriation of profits, unlike in other regions with capital controls. This freedom serves as a strong incentive across sectors like gold mining, agriculture, timber, and livestock.

Ongoing Challenges: Despite challenges, South Sudan remains open for business, aiming to dispel misconceptions and attract investors with clear legal protections and operational freedom.

What is being done to enhance regional cooperation in financial and economic matters, both within East Africa and internationally?

Regional Integration: We are part of the East African Community (EAC) and are embracing policies to harmonise with the region. This includes policy harmonisation and improving payment systems, similar to the East Africa payment system.

Cooperation Goals: We are focused on cooperating with others to deliver on convergence criteria. There are four of them, intended to be achieved at a certain point in the future, allowing all regional members to agree on having a single currency. One area where we cooperate extensively is ensuring inflation is stabilised around 8%. Few countries have met this, but South

Sudan, due to ongoing conflict, hasn’t achieved this criterion.

Economic Growth Targets: Additionally, economic growth of 4% per annum is a target. Countries like Tanzania and Kenya have achieved this, but South Sudan has struggled due to conflict. Uniform growth across the region is desired.

National Debt Management: We would also like to see national debt as a percentage of GDP lowered. South Sudan has met one criterion: although we have small loans here and there, they are not significant. The reason why we’re not attracting larger investments is due to perceptions about risk.

International Cooperation: We have an obligation to coordinate within major international financial institutions like the African Development Bank, World Bank, and IMF. Currently, due to our risk rating, we are not receiving substantial investments but are prepared for engagement with the World Bank and IMF for long-term development.

Africa, with over 400 million young people aged between 15 and 35 years, has the youngest population in the world, presenting both challenges and opportunities for the continent. Are there policies or measures that the Bank of South Sudan is implementing to support youth empowerment and entrepreneurship in the country?

Youth Employment Initiatives: As the central bank, we do not directly implement youth empowerment policies. However, the Bank of South Sudan is committed to supporting employment opportunities through competitive hiring practices. We have established a rigorous employment process where youth and other applicants undergo written and oral interviews to ensure merit-based selection.

National Engagement: Additionally, at the national level, the Ministry of Youth and Sport is actively engaging young people in sports initiatives, promoting national unity and pride. We are aligning our efforts with these initiatives to enhance youth engagement beyond ethnic or tribal boundaries.

Corporate Social Responsibility: Furthermore, the Bank of South Sudan is exploring avenues for corporate social responsibility that could benefit youth empowerment initiatives. We remain open to suggestions and collaborations that can further support youth entrepreneurship and empowerment in our country.

Dr. Alic, with the influx of refugees due to the Sudanese conflict, what opportunities and challenges do you foresee for the South Sudanese economy in the coming year with all the challenges that you are working with? How is the bank preparing to support the economic growth instability in this particular context?

Challenges and Opportunities: There are two clear examples: one of the challenges and one of the benefits that refugees coming in from Sudan and our returning South Sudanese who were in the North are bringing. From the positive side, they are coming in with improved services. For instance, medical doctors and surgeons who were specialists in Khartoum have come to South Sudan. Right now, in some residential areas like Kololo in Juba, we have many medical specialists from Sudan providing services that were not available before. This influx is a significant benefit that the conflict in Sudan has brought to South Sudan.

Supporting the Economy: We are working to improve payment systems so that patients can use credit and debit cards instead of cash at hospitals. At the Bank of South Sudan, we provide insurance to our staff, though it has limits on coverage, especially for certain incurable diseases. Through improved payment methods, we are indirectly supporting these services.

Humanitarian Efforts: Many refugees arrive at the border with nothing to eat and

no shelter. Providing them with food has become challenging. We have called upon the international community and humanitarian agencies to support these efforts. Currently, in border states, we have refugee camps where those who have arrived and not yet settled in their home states are being supported.

Integration into Local Economy: Once they settle in their respective states, we hope they will integrate into the local economy. Some have returned to their home states after decades away and are rediscovering their properties and engaging in local production. Agriculture has been highlighted as crucial for our economy, and some refugees are already taking this opportunity seriously.

Nine months into your tenure, approaching one year in office, what would you say is your most notable achievement?

Key Achievements: There are several accomplishments, but I’ll highlight three. Firstly, we’ve significantly expanded financial services into the states, a milestone previously unprecedented. Under my leadership, the bank successfully achieved this, marking it as a major achievement.

Project Completion: Secondly, I’ve dedicated considerable effort to completing long-standing bank projects. Some of these initiatives were at a standstill before my tenure. With renewed focus and support, we’ve seen these projects through to completion. For instance, the construction of our headquarters was initiated before my arrival but was in a critical stage. I personally oversaw its progress, visiting the site daily for four months, ensuring contractors met deadlines, and addressing any challenges promptly. This effort has transformed our headquarters into a landmark structure in Juba, setting a new standard for the financial sector in South Sudan.

Staff Development: Lastly, we’ve made substantial investments in our staff. Enhancing their skills and capabilities has been a priority, and I’m proud of the progress we’ve made in developing our team. Their dedication and professionalism have been recognised not only locally but also within the broader banking community.

South Sudan’s accession to Micro-Economic and Finance Management Institute

By Chance Baniko

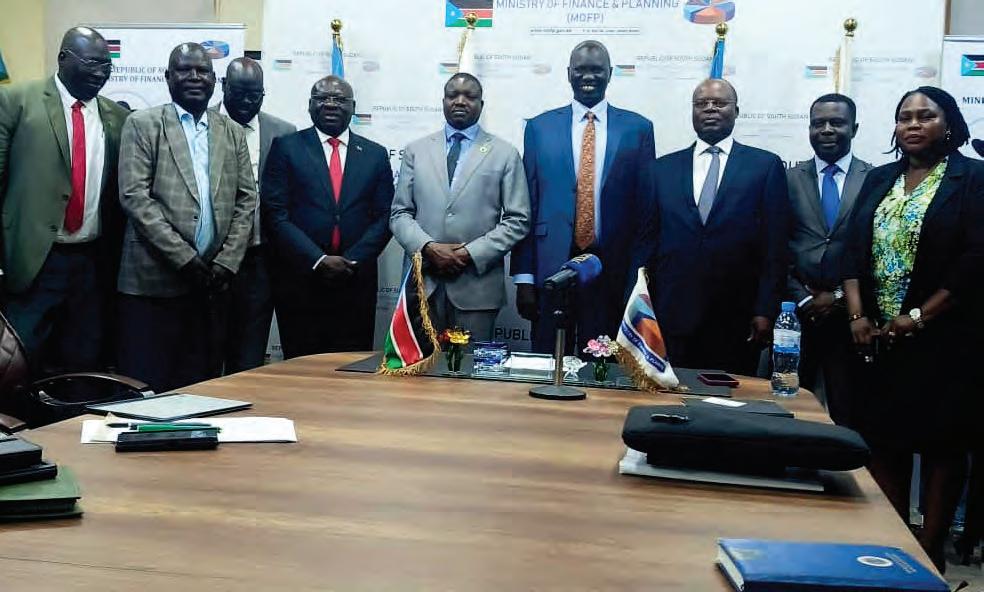

The Ministry of Finance and the Bank of South Sudan (BoSS) have signed an MOU at the ministry with Macroeconomic and Financial Management Institute (MEFMI) on the accession of South Sudan as 15th member to the block

The Ministry of Finance and the Bank of South Sudan (BoSS) have signed an MOU at the ministry with Macroeconomic and Financial Management Institute (MEFMI) on the accession of South Sudan as 15th member to the block. Speaking during the ceremony, BoSS Governor Hon. Dr. James Alic said that the engagement between the government and the facility started way back in 2012 in Morocco. The country stands to benefit from the institute in areas of debt recording, debt management amongst others.

BoSS governor said, “We shall do our best to catch up with the rest of the countries in the region. We are no more babies anymore.” The governor expressed optimism to the forth coming meeting and said as a country “we need to have access to the market and develop bond market and financial markets amongst others.”

The institute promised to train 13 cohorts who will become experts at home and in the region. On the other hand, the Executive Secretary of MEFMI

Louis Kesekende said his organization is thrilled to receive South Sudan as its 15th member, pointing out that he will work with the government of South Sudan on areas of capacity development to train cadres for the country.

We have foundational and intermediate trainings as well as advance trainings for the benefit of all member countries

“We have in country conferences as well as regional South Sudan’s accession to Micro-Economic and Finance Management Institute 7 BoSS Governor at the center, Hon. Dr. James Alic, Deputy Minister of Finance Hon. Agok Makur with Dr. Louis Kasekende Executive Secretary of MEFMI and other officials conferences and we are ready to respond to your needs. We have foundational and intermediate trainings as well as advance trainings for the benefit of all member countries.”

Closing the occasion, the Deputy Minister of Finance and Planning Hon. Agok Magur expressed his appreciation for the signing of the MOU and said that the government stands ready to fulfil its obligations. He pledged to pay the membership fee. Earlier in the meeting

held at BoSS premises Doctor Louis Austin Kasekende met and thanked Hon. Dr. James Alic for the warm welcome and the hospitality accorded to them by the bank since they arrived in Juba. He said the main objective of the visit was to strengthen and operational the relationship between South Sudan and MEFMI.

He then touched on South Sudan membership to the block and said that it was approved in the last Board meeting of MEFMI. While the country has already paid its capital contribution, the membership fee remains unpaid. In this connection, he also encouraged the country to pay the membership fee as soon as possible to enable a speedy capitalization as South Sudan, which still lags.

He highlighted that South Sudan needs to nominate their representative to the Board of Governors of MEMFI, either from the Bank or the Ministry of Finance and Planning.

Central Bank of South Sudan celebrates International Women’s Day

By Joseph Chol

Dr. James Alic Garang, Governor of the Bank of South Sudan, urged everyone to support initiatives that empower women and foster selfreliance

The Central Bank of South Sudan joined the global celebration of International Women’s Day 8th March 2024 by recognizing its outstanding female staff. The bank’s leadership acknowledged their tireless commitment, dedication, and passion for their work and their country. The event, held under the theme “Invest in Women: Accelerate Progress,” highlighted the importance of empowering women.

In his address, Dr. James Alic Garang, Governor of the Bank of South Sudan, urged everyone to support initiatives that empower women and foster selfreliance.

“Barriers must be removed to allow their steady progress,” he added. He said that

the BoSS has already broken the glass ceiling, referring to the appointment of Deputy Governor for Administration and Finance, Hon. Nyiel Gordon. He added that the Bank has four women directors, five women deputy directors, and nine women in grade one, and more to follow.

The BoSS Governor commended the ceremony’s organizers, urging them to extend it far and beyond. Replying to a query made earlier by a female staff on why women are not included in committees, the BoSS governor, said there must be a woman or two in each committee. He noted, “When we move to the new headquarters, we will explore ways on how to set up a childcare centre.”

Mayoress of Juba City, Flora Gabriel who attended the meeting said, “It is a great day to attend this magnificent event. Thank you for invitation.” She emphasized that women must be committed, determined, and focused on education. “Let’s respect men, because without them, we cannot form a family,”

On his part, 1st Deputy Governor, BoSS, Hon. Samuel Yanga Mikaya, hailed women on their special day, pointing out that they play greater roles in their societies as they currently occupy the very jobs, which were seen in the past as exclusive men’s territory. Commenting humorously on request

Let’s be a catalyst for change. Let’s create an environment where women can excel without unfairness. With the leadership of Alic, women would be further empowered. Let’s renew our commitment on gender equality.

to set up childcare at the bank, he enquired, “Where are the children? I can only see a single woman pregnant in today’s event.”

Deputy Governor, Hon. Nyiel Gordon Kuol, said., “Today is a remarkable day to celebrate women’s achievements. It’s a day to reflect on achievements and address challenges. While saluting BoSS women staff on this glorious day, she congratulated the First Lady, Hon. Ayen Mayardit, and H.E President of the Republic of South Sudan, Lt. General Salva Kiir Mayardit for bridging the gender gap.

Aiming at BoSS male staff, Hon. Gordon, said, “All of you are sons of

women. So, let’s work together to achieve inclusiveness.” She continued, “Let’s be a catalyst for change. Let’s create an environment where women can excel without unfairness. With the leadership of Alic, women would be further empowered. Let’s renew our commitment on gender equality.” The Director General for Administration and Finance, David Manyuon Nak, hailed women on their special day, referring to their perseverance and self-denial. He urged them to exert more efforts to address challenges. Following the speeches, different dances were performed on tunes of various traditional melodies.

USA honours

Dr James Alic Garang

By Joseph Chol

Since assuming his position in October 2023, Dr. Alic has spearheaded a transforming modernization plan for the Bank of South Sudan.

The Governor of the Bank of South Sudan, Hon. Dr. James Alic Garang, has recently been recognized for his leadership and dedication to improving the nation’s economy. These accolades come from both the United States and Africa, highlighting the international impact of Dr. Alic’s efforts.

Since assuming his position in October 2023, Dr. Alic has spearheaded a transforming modernization plan for the Bank of South Sudan. This plan focuses on:

1. Enhanced transparency, increasing openness and accountability within the bank’s operations to build public trust.

2. Improving efficiency and restructuring the bank to better deliver on its mandate and exercise stronger oversight of the financial sector.

3. Staff investment through implementing new staff benefits and policies to boost morale and improve overall performance.

These efforts are not going unnoticed by the international community.

News recently emerged of Dr. Alic receiving recognition and congratulations from the South Carolina House of Representatives during a visit to the state. Specific details about the nature of the recognition are pending,

Dr. Alic’s initial months in office have been marked by substantial progress. His unwavering focus on modernization, transparency, and staff wellbeing positions the Bank of South Sudan to play a more prominent role in guiding the nation’s economic development

but it signifies the growing international recognition of Dr. Alic’s leadership.

Furthermore, Dr. Alic was awarded a certificate of commendation by the African Leadership Organization. This prestigious continental body’s recognition underscores the positive impact Dr. Alic’s endeavours are having across Africa.

These recognitions add to Dr. Alic’s growing list of achievements, including the “extraordinary effort” prize awarded by the US House of Representatives in Washington D.C. and the proposal

within South Sudan to name a road after him.

Dr. Alic’s initial months in office have been marked by substantial progress. His unwavering focus on modernization, transparency, and staff well-being positions the Bank of South Sudan to play a more prominent role in guiding the nation’s economic development.

International observers will continue to follow Dr. Alic’s leadership with keen interest as he shapes South Sudan’s economic trajectory.

Unlocking South Sudan’s Economic potential through partnership

By Hon. Dr. James Alic

What

the world does not know is that South Sudan boasts a wealth of natural resources beyond oil. Fertile land, vast water reserves from the Nile, and abundant mineral deposits offer a diversified base for investment, to mention but a few

South Sudan, the world’s youngest nation, possesses immense potential for diversification, economic growth, and shared prosperity.

While oil has been the mainstay of the economy since independence from Sudan on July 9, 2011, the government’s focus on augmenting broader local production, particularly in the agriculture sector, presents exciting opportunities for investors. The latter singular interest also stands to foster a more resilient future for South Sudan and the region.

What the world does not know is that South Sudan boasts a wealth of natural resources beyond oil. Fertile

land, vast water reserves from the Nile, and abundant mineral deposits offer a diversified base for investment, to mention but a few.

The agricultural sector holds immense promise. With fertile plains and a long growing season, South Sudan has, indeed, the potential to still become a breadbasket for the region and beyond.

Investment in modern farming techniques, irrigation infrastructure, and storage facilities can unlock this potential, ensuring food security not only for our people but also, as already stated, for the region and continent while creating jobs for millions of people.

South Sudan is a country moving towards a positive frontier. To make this point clearer and as the Governor of the Bank of South Sudan, I had the privilege of hosting the EAC Monetary Affairs Committee meetings from April 29-May 3, 2024

However, South Sudan cannot achieve its growth potential in isolation. If anything, it needs to integrate with the global economy while strengthening collective action, especially the regional and international financial system. This conviction informed our decision to join the East African Community (EAC) in 2016, and the country is now realising some dividends.

While we have made considerable progress, I will admit that it has not been an easy journey. However, I can confidently say that South Sudan is no longer a ‘baby’ but a fully matured adult, just like others in the region, and is contributing to collective action in many respects.

South Sudan is a country moving towards a positive frontier. To make this point clearer and as the Governor of the Bank of South Sudan, I had the privilege of hosting the EAC Monetary Affairs Committee meetings from April 29-May 3, 2024.

Throughout the week-long meetings, the Bank of South Sudan had the opportunity to highlight to our EAC colleagues the immense potential that remains untapped in our country.

In a similar vein, I also noted that the banking sector remains a major reserve for investment from our regional brothers and sisters. Huge opportunities for varied investments exist in the banking sector.

Going forward, we promise to sustain a positive investment climate as we seek to attract both regional and global investors to South Sudan.

South Sudan stands at a crossroads. Yet, by harnessing its natural resources, fostering a stable environment, and investing in its people, the country can unlock its true growth potential.

From our experience, the journey will be exacting, but the rewards – a prosperous and diversified South Sudan – are well worth the efforts.

We expect investors to conduct their due diligence and manifest in longterm strategies. Collaboration with the government and local communities is essential to reap investment opportunities, and by extension, support the UN Sustainable Development Goals and South Sudan Development Plan.

Unveiling Fiscal and Monetary Policy Reforms Towards Economic Transformation Agenda

By Hon. Dr. James Alic

His unwavering focus on modernization, transparency, and staff wellbeing positions the Bank of South Sudan to play a more

It is my distinct honour and privilege to warmly welcome you to this joint press conference organized by the Ministry of Finance and Planning and the Bank of South Sudan under “Unveiling Fiscal and Monetary Policy Reforms Towards Economic Transformation Agenda.”

Today represents a watershed moment for economic and financial reforms in our country, emphasizing that the banking industry is one of the key pillars essential to the realization of the above reform agenda.

Permit me, fellow citizens, to rather digress and reflect on the evolution of modern central banking which succeeded the traditional central

banking associated with “gold standard” and Hume’s “rules of the game.”1 After transiting to the classical type, the major objectives of central banking have been to preserve financial stability, including currency convertibility into specie with a new attention to their supervisory role.

The control over the money supply was dominated by the convertibility target: “the monetary functions of the central bank were largely grafted onto the supervisory functions, and not the reversed.”

The bank core objective shifted to maintaining “price stability,” with the advent of modern central banking. It is the general style of monetary policy

that makes the main difference between traditional and modern central banking. The latter is more precisely antiinflation, largely oriented with a lower degree of goal independence and a higher instrument independence.

Distinguished guests, ladies, and gentlemen, through the prisms of the current developments, the financial system stability remains central to the development agenda of the country. Historically, central banks used the lender of last resort function as the principal tool to ensure financial stability.

Today, financial stability goes beyond the lender of last resort function. Indeed, financial stability and monetary policy are complementary since without financial stability, monetary policy impulses to the economy cannot be transmitted to the real economy. Therefore, financial stability is critical to achieving macroeconomic Price stability and full employment. The Bank of South Sudan modernization reform agenda, considering the above, is anchored on four pillars that are interdependent and multifaceted.

They revolve around the vision towards economic transformation agenda and strengthening the central bank mandate to achieve price stability. The pillars are sequenced are follows:

Pillar 1: Strategies to strengthen monetary policy framework to ensure price stability

Pillar 2: Corporate governance

Pillar 3: Transparency and Accountability

Pillar 4: Exercising central bank autonomy and independence.

Distinguished guests, ladies, and gentlemen, under the first pillar, the Bank of South Sudan plans to

pursue a strong monetary policy framework. This calls for a strategic approach to working with the key stakeholders in the economy to foster healthy competition and resource allocation; to pursue activities that lead to high productivity and economic growth; to reduce distortions in foreign exchange markets and make prudent investment decisions; and to ensure a sound and more efficient financial system.

Broadly, there exist multiple objectives leading to realization of this pillar, with the following featuring prominently:

• Ensuring that banks develop, adopt, and implement plans to promote financial inclusion and digitalization of financial services through harnessing innovation and technology. Here, we will use moral suasion, especially encouraging commercial banks to expand access frontier to the bottom of the pyramid.

• Working towards maintaining macroeconomic stability to tame inflation and anchor inflation expectations, while curbing currency exchange rate depreciation.

• Providing the conducive policy environment to transit from the current reserve monetary policy framework to price-based monetary policy framework, as required by EAC protocol. We hasten to add that this is part of convergence criteria and harmonization of monetary policies among EAC member States.

• Ensuring exchange rate stability, the bank will formalize the foreign exchange market by encouraging the informal currency traders to join the foreign-exchange market. This will be implemented through coordination with relevant authorities as these informal

outlets get regulated and officially licensed to transact in the foreign exchange market.

This will enhance data collection and streamline foreign exchange operations in the country, leaving little room for currency speculators and market indiscipline.

The concerned department will be directed to formulate a policy direction that will culminate in eliminating informal foreign exchange dealers. Going forward, the law enforcement agencies will discharge their immediate responsibilities to tame any noncompliance practices, including by ensuring that no one sells dollars in the open, or under trees without an appropriate license to engage in FX trading or before creating lawful “FX windows.”

• Implementing the National Payment System remains critical and sits at the centre of this strategy. We continue to work closely with our regional and international partners to:

i. Support a payments system that meets the diverse needs of customers

ii. Enhance the safety, affordability, and security of the payments system by adopting relevant industry and global standards

iii. Support an ecosystem anchored on collaboration that produces customercentric and world-leading innovations

iv. Create a supportive policy, legal and regulatory framework

Supporting economic development and agriculture remains imperative. It is in the public domain that recent global headwinds, rising interest

The Bank together with Ministry of Finance will coordinate policies, seeking to promote financial and macroeconomic stability as well as fostering foreign direct investment and mobilizing diaspora remittances

rates in the advanced economies, post COVID-19 era and the Russian-Ukraine war have disrupted the global supply chain and left a big scar on the global economy.

Consequently, many countries suffered losses in terms of economic growth and employment. There is no doubt that South Sudan’s economy remains vulnerable given that its performance relies mainly on growth in a few sectors, led by the oil sector and services.

The Bank together with Ministry of Finance will coordinate policies, seeking to promote financial and macroeconomic stability as well as fostering foreign direct investment and mobilizing diaspora remittances. Further, the Bank supports the government plans to diversify South Sudan’s economy, while reducing vulnerabilities to external risks. The Bank also encourages the establishment of agriculture credit facilities to support lending and extending credit to this crucial sector, which is a top priority policy in spearheading this reform agenda. By providing an enabling environment and legal framework, the Bank will sensitize the banking sector and other microfinance institutions to prioritize lending to enterprises engaging in agro-business and food processing. The modalities of such interventions will be discussed elaborately with the key stakeholders and the Ministry of Finance.

The Bank will undertake a formal review of its approach to foreign exchange reserve management. The outcome of the review would be guided by multiples principles to establish a rigorously defined operational framework for managing risk and return. Hence, the Bank will review the current investment guidelines to ensure asset allocation is critical for gen-erating returns and managing portfolios.

In coordination with the fiscal authorities, the Bank will work towards

shifting implementation of Treasury Single Account (TSA) memorandum of understanding. This will set the stage to decouple the use of foreign currency in most payments undertaken by spending agencies of the government and help us rebuild foreign exchange reserves. This deliberate rebuilding of reserves has positive implications on the domestic currency, the SSP and balance of payments. Distinguished guests, ladies, and gentlemen, under the second pillar, and to ensure sound and effective decision-making, the Bank will institute robust governance arrangements. To this end, the importance of effective governance arrangements for central banks cannot be overemphasized.

Through this Modernization Strategy document, effective Board oversight will play a critical role in ensuring sound governance. As defined, the Board is the decision-making body through which oversight function is exercised. This ensures that the bank is well managed and aligned with international best practices.

The Board oversight function is the “last line of defence” in the broader internal governance structure of the Bank. Robust board oversight is critical to several policy decisions, including

1. holding the central bank’s internal decision-making accountable and 2. ensuring that overall management is appropriate, compliant with legal requirements, and financially and operationally sound.

Distinguished guests, ladies, and gentlemen, under the third pillar central, central banks are formally accountable to the delegating authority, including legislative or executive branch of government and the public depending on the constitutional delegation of responsibilities. Through this document, we envisage several formal mechanisms through which the Bank of South Sudan is held accountable for its

activities, namely:

1. Monitoring by the legislature; through the existing legal provisions for the exchange of information, often in the form of regular meetings or consultations, with the Ministry of Finance and other government agencies, including the National Assembly.

2. Publication of regular central bank reports; the Bank of South Sudan is required to submit a written report (audited financial statements) to the legislature and the Ministry of Finance each year as stipulated in the Bank of South Sudan Act, 2011 (amended, 2023).

3. Ensuring transparency and disclosure requirements; in discharging of our duties, we shall clearly communicate that transparency requirements do not interfere with the achievement of the central bank’s functions and objectives.

Whenever confidentiality is desirable, selective disclosure, such as testimony in a closed session of a legislative committees would be preferred.

Distinguished guests, ladies, and gentlemen, under the fourth pillar, and for the Bank of South Sudan to be effective, we shall work towards achieving and enjoying a high level of autonomy vis-a-vis both political institutions and private economic interests. This is the trend world over.

The autonomy of the Bank of South Sudan will be commonly analysed through the lens of four related but distinct concepts:

1. Institutional autonomy, indicating that the Bank should not be influenced by the state or private third parties in its decision-making in the context of the performance of its functions;

2. Functional autonomy, which is directed to the capability of central

bank to im-plement its functions without direct governmental interference;

3. Personal autonomy, which ensures that key decision makers of the central bank, Governor and members of Executive Boards, Monetary Policy Committees and Oversight Boards are autonomous from political and private economic and social interests; and

4. Financial autonomy entails the capability of the bank to pursue its mandate by way of the financial means required to do so.

It is important to reiterate that the leadership understands the enormity and the inher-ent challenges facing this policy direction. Many central banks across the globe still grapple with issues related to autonomy and independence and South Sudan is not an exception. We believe, however, in setting the stage for such conversations to take shape and form, allowing the posterity to build on these key building blocks which represent an essential component for a modern central bank.

At the Bank management level, we shall ensure diversity and competence merits-based recruitment which incorporates the elements defined in the developed human resource competence framework:

1. Appreciating talent management, retention in diversity, and aligning current workforce and talent strategies to future business priorities,

2. Developing on the job training and succession plans

3. Assessing current capabilities, both across the organization and within the HR function and identifying key skills and capabilities required for the future.

At the Bank management level, we shall ensure diversity and competence merits-based recruitment which incorporates the elements defined in the developed human resource competence framework

Dr. James Alic Garang’s Speech at the 2024 Africa Summit in London

By Hon. Dr. James Alic

It is an honor and a privilege to stand before you today at the African Leadership Summit 2024 here in London. I am deeply humbled to be part of this important gathering and the conversation about Africa’s future. Despite prevailing challenges, Africa remains poised for a remarkable transformation that could change the global economic landscape.

Indeed, William Shakespeare is right when he said: “The golden age is before us, not behind us.” One of the key drivers of the expected transformation

stems from the continent’s fast-growing population. According to UN reports, Africa is projected to be home to 2 billion people by 2050, making it the most populous continent on earth. This demographic trend presents a unique opportunity for the continent to harness the power of its youthful population and drive economic growth through innovation, entrepreneurship, and increased productivity.

South Sudan, like other countries, has and continues to face a series of challenges that have significantly

Despite prevailing challenges, Africa remains poised for a remarkable transformation that could change the global economic landscape

South Sudan holds immense potential across many sectors. Spearheaded by the Bank of South Sudan, the banking sector has been playing a crucial role in supporting the economy and bolstering recovery

hampered its economic growth. It has been affected by multiple economic shocks, including fluctuating oil prices, disruptions, and the global economic downturn induced by the COVID-19 pandemic and its detrimental effects. These factors have led to a sharp decline in economic output, currency depreciation, and limited access to basic services for the population.

South Sudan, however, holds immense potential across many sectors. Spearheaded by the Bank of South Sudan, the banking sector has been playing a crucial role in supporting the economy and bolstering recovery. The Bank of South Sudan, together with stakeholders in the country, has been implementing various strategies to improve financial sector stability and attract investment. Some of the key initiatives include:

1. Enhancing financial regulations: The financial sector is working closely with regulatory authorities to strengthen financial regulations and improve transparency in the banking sector. This is crucial for

building trust among investors and ensuring the stability of the financial system.

2. Expanding financial inclusion: The Bank has expanded its branch network to extend financial services to underserved populations, including rural communities and small businesses. Commercial banks are also expanding their operations. By providing access to credit and other financial services, banks are supporting economic growth and empowering households to improve their livelihoods.

3. Promoting investment: Financial institutions are actively working to promote investment in key sectors of the economy, including agriculture, fishing, infrastructure, mining, and manufacturing. By providing financial support and advisory services to investors, banks are stimulating economic activity, creating employment, and boosting revenues.

4. Improving risk management: Banks are enhancing their risk management practices, thereby

mitigating the impact of external shocks on their operations. By diversifying their asset portfolios and adopting best practices in risk assessment, banks can better withstand economic uncertainties and safeguard the interests of their customers.

5. Embracing technology: Banks and mobile money operators, including m-Gurush, MoMo, and NilePay, are increasingly leveraging technology in South Sudan to enhance service delivery and reach a wider customer base. Digital banking solutions, mobile payment platforms, and online banking services continue to improve efficiency, convenience, and security for customers.

In striving to achieve its core mandate, the leadership of the Bank of South Sudan has anchored its policy direction on three main pillars of running a modern central bank—ensuring greater transparency, supporting accountability, and exercising independence.

Broadly, the Bank is implementing a prudent and data-driven monetary policy to ensure price stability, safeguard

financial stability, and rebuild policy credibility. It now focuses on:

• Strengthening the monetary policy framework and anchoring inflation expectations

• Rebuilding gross international reserves, including the plan to add a gold portfolio

• Collaborating with fiscal authorities to realign incentives and harmonize policies

• Expanding the branch network, fostering financial inclusion, and improving staff welfare

• Aligning with the EAC’s roadmap for establishing a monetary union.

Relatedly, we greatly appreciate H. E. President Salva Kiir Mayardit and the Unity Government for continuing to advocate and support our policy positions to stabilize the economy and ensure shared prosperity. Several ongoing initiatives and policies are paving the way for increased investment with significant outlays geared towards various sectors, including agriculture and ICT. For example, Elon Musk’s Starlink has recently been granted a license to operate in South Sudan,

In striving to achieve its core mandate, the leadership of the Bank of South Sudan has anchored its policy direction on three main pillars of running a modern central bank— ensuring greater transparency, supporting accountability, and exercising independence

South Sudan contributes to strengthening regional and international cooperation. In this context, it continues to deepen relations with the EAC, World Bank, IMF, and other major institutions. Collectively, they have invested significantly in development initiatives, food security, infrastructure, and economic stabilization measures

and a recent survey confirmed South Sudan as boasting the world’s largest land mammal migration, dubbed the 6-million-strong Great Nile Migration. The country is also investing in and promoting tourism, harnessing its potential in solar energy, and attracting investment in the real estate and mining sectors, with positive implications for growth and job creation.

South Sudan contributes to strengthening regional and international cooperation. In this context, it continues to deepen relations with the EAC, World Bank, IMF, and other major institutions. Collectively, they have invested significantly in development initiatives, food security, infrastructure, and economic stabilization measures.

To build a track record of prudent macroeconomic policies, South Sudan has undergone a 9-month StaffMonitored Program, and Program Monitoring with Board Involvement, which greatly supported the foreign exchange market and economic reforms. The country is now working to secure the Extended Credit Facility program, which will allow South Sudan to implement an economic program that can drive progress toward a stable and

sustainable macroeconomic position consistent with strong and durable poverty reduction and growth.

Please allow me to reiterate that at the heart of our economic agenda is the empowerment of youth and the promotion of entrepreneurship. By investing in education, skills development, and Small and Mediumsized Enterprises, we can unlock the full potential of our nation and deliver inclusive growth. Through partnerships with local and international stakeholders, we aim to create a vibrant ecosystem that nurtures innovation and creativity.

To conclude, I call upon all leaders gathered here today to join hands in shaping a brighter future for Africa and the world. Let us work together to harness the potential of our youth, embrace innovation, and build resilient economies that lift all boats. Let us also shun negative perceptions about African countries and reverse such narratives. Going forward, the Bank of South Sudan stands ready to play its part in this collective endeavor, while looking forward to forging new partnerships and welcoming you to South Sudan to explore a plethora of investment opportunities.

South Sudan’s Financial Sector Reforms:

In a nation marked by resilience and transformation, the Bank of South Sudan stands at the forefront of economic resurgence. We had an exclusive interview with Mrs. Grace Araba Gordon, the Director of Financial Markets at the Bank of South Sudan. With an impressive 18-year tenure at the Bank, Mrs. Gordon has been instrumental in implementing bold reforms and innovative policies that have significantly impacted the financial landscape of South Sudan. Her leadership and vision are crucial in steering the nation towards economic stability and growth, making her insights invaluable for understanding the complexities and triumphs of South Sudan’s financial markets.

In this candid conversation, Mrs. Gordon explores her remarkable career journey, starting from her early days in the back-office division to her current pivotal role. She highlights the strategic reforms introduced under the leadership of Governor Dr. Garang, which have fortified the monetary policy framework and enhanced market confidence. From the introduction of a term deposit facility to the deployment of advanced trading platforms, Mrs. Gordon discusses the transformative policies driving South Sudan’s economic resurgence. This dialogue explores the profound impact of these initiatives and offers a deeper understanding of the future trajectory of South Sudan’s financial markets through the eyes of a visionary leader.

Excerpt

Can you introduce yourself and describe the career journey that led you to your current role as Director for Financial Markets at the Bank of South Sudan?

I joined the Bank of South Sudan in 2006 as an official in the back-office division of the financial markets department, handling settlement and trade finance (letters of credit and guarantees). Subsequently, I became the head of the settlement division. My experience with the Bank of South Sudan spans 18 years.

As acting Deputy Director for the Financial Markets Department in 2020 for a period of two years, I was promoted to the position of Director of Financial Markets in 2023. During this period, my team managed to introduce several reforms, including the introduction of a term deposit facility and an FX trading platform, Refinitiv, for electronic FX and TDF auctions, which will be operational in a few weeks. We have also strengthened liquidity management and forecasting frameworks as we continue to develop strategies to boost foreign exchange reserves.

From your perspective as Director of Financial Markets, what are some of the key reforms and policies implemented under Dr. Garang’s leadership that have significantly impacted the financial markets and the broader economy of South Sudan?

The continuous implementation of the term deposit facility under the leadership of Hon. Dr. Alic has strengthened our monetary policy framework. This facility has allowed market participants to

Mrs. Gordon has been instrumental in implementing bold reforms and innovative policies that have significantly impacted the financial landscape of South Sudan. Her leadership and vision are crucial in steering the nation towards economic stability and growth, making her insights invaluable for understanding the complexities and triumphs of South Sudan’s financial markets

invest more funds and liquidity with the Bank of South Sudan. We have also used the facility to manage excess liquidity, alleviate pressure on the domestic currency, and stabilise the macroeconomic environment.

Another policy was the reorganisation of the informal foreign exchange market to discourage rent-seeking behaviour and streamline FX operations.

We strengthened monetary policy by adopting an inflationtargeting regime to replace monetary aggregates and implementing a modern liquidity forecasting framework to enforce compliance with statutory reserve requirements. Liquidity forecasting aims to stabilise the exchange rate and foster confidence, promoting long-term economic growth.

We have also increased our engagement with the industry by introducing Central Bank Bills to expand the range of instruments available to absorb excess liquidity from the market. This same platform will be used to deepen the interbank market and government securities.

Increased market oversight through the adoption of Refinitiv allows us to receive daily returns on all foreign exchange and money market transactions from financial institutions, strengthening our supervisory role and maintaining market discipline.

The communication strategy under the leadership of Hon. Dr. Alic involves frequent communication with stakeholders and the public to enhance policy effectiveness, create complementary news to policy actions, and reduce policy uncertainties.

The formation of a Monetary Policy Operations Committee (MPOC) oversees the implementation of policy decisions made by the Monetary Policy Committee (MPC).

The Bank of South Sudan also promotes financial inclusion, bringing financial services and products closer to people across the country. Under the leadership of Hon. Dr. Alic, we have opened more branches where regulatory gaps were identified.

What initiatives have been undertaken recently, especially under Dr. Garang’s leadership, to improve the issuance process of Treasury bills and bonds? How have these initiatives impacted investor confidence and market participation?

In light of various headwinds and multiple shocks, we have diversified our monetary policy instruments by placing more emphasis on term deposits and other instruments. The Bank of South Sudan first introduced money market instruments in 2016, issuing Treasury bills on behalf of the government. We also invested in the necessary infrastructure to support such operations. A robust CSD and T-bills auction analysis system was introduced shortly afterward. This policy direction yielded significant results, allowing the government to borrow from the banking sector and contributing to a stable exchange rate regime, thereby moderating inflationary pressures.

What innovative policies or regulatory reforms are being introduced to enhance the efficiency and stability of financial markets dealing with Treasury bills, bonds, and gold reserves?

To deepen our monetary policy framework, we intend to introduce other important tools, such as central bank bills. This policy direction will be discussed with the Ministry of Finance to realign and harmonise monetary policy instruments and create a conducive environment for a stable exchange rate regime and effective intervention methods. The act allows the Central Bank to run discount windows as facilities of last resort, providing temporary liquidity to the industry and supporting monetary policy transmission. However, the dynamics of financial markets require us to go the extra mile, supporting monetary operations through prudent regulations and policy coordination. Enforcing compliance with reserve requirements enhances the Bank of South Sudan’s ability to control money growth and fulfil its responsibility for maintaining stable monetary conditions.

Under Dr. Garang’s leadership, what efforts have been made to enhance investor confidence in South Sudan’s financial markets and the banking sector generally? What strategies or initiatives have been effective in improving transparency and accountability in transactions involving Treasury bills and bonds?

South Sudan is in the early stages of deepening its financial markets, and we have not yet developed legal frameworks for capital markets. However, efforts are being made to first strengthen money market instruments by enhancing the regulatory framework for the secondary market and developing a sophisticated marketplace in collaboration with advanced capital markets within the region and across the continent. It is important to emphasise that our money

market operations are transparent and open to scrutiny. We have adopted and installed modern infrastructure for payment and settlement systems that share data and information with market participants. Additionally, we have a robust feedback and monitoring mechanism capable of analysing outcomes and rectifying system errors when they occur.

The banking sector in South Sudan is sound, with a wide array of international banks. Could you share examples of successful risk management strategies implemented in the context of financial markets dealing with Treasury bills, bonds, and gold reserves? How have these strategies mitigated risks and ensured market resilience?

The Bank of South Sudan is considering introducing central bank lending facilities for banks on an overnight basis. The discount windows shall be run as facilities of last resort, providing temporary liquidity to banks and supporting monetary policy transmission. Pricing of the facility is recommended to be punitive, a margin above the policy rate.

How have global financial trends and regulatory developments influenced your approach to managing financial markets involving Treasury bills, bonds, and gold reserves? How have you adapted to these global influences?

We aim to boost foreign exchange reserves via gold purchases. Reserves act as a financial cushion, providing stability and confidence in a country’s economy and influencing monetary policy, including foreign exchange rates.

How would you describe Dr. Garang’s leadership style and impact as Governor of the Bank of South Sudan? How has his leadership influenced your work and the overall performance of the financial markets?

Hon. Dr. Alic is a charismatic and transparent leader who has demonstrated a keen interest in financial inclusion. His leadership brought about inclusive participation and the sharing of ideas across the sector. He has shown a desire to support the restructuring of the Central Bank to ensure it effectively delivers on its mandate. We have witnessed an improvement in staff welfare, including measures to improve working conditions, better healthcare, and opportunities for professional development and growth. He has also strengthened collaboration with international financial institutions.

What is your vision for the future of South Sudan’s financial markets under Dr. Garang’s leadership? What key initiatives or reforms do you foresee to further strengthen the financial markets and the resilience of the country’s economy?

We envision vibrant financial markets under the leadership of Hon. Dr. Alic. This includes the introduction of an interbank market for SSP to support monetary policy transmission, a deeper government securities market, a stable exchange rate and interest rate environment, and increased foreign exchange reserves. Hon. Dr. Alic’s extensive international exposure, having worked with multiple international financial institutions, provides an additional advantage, fostering a holistic view on matters of finance and the economy.

The continuous implementation of the term deposit facility under the leadership of Hon. Dr. Alic has strengthened our monetary policy framework. This facility has allowed market participants to invest more funds and liquidity with the Bank of South Sudan. We have also used the facility to manage excess liquidity, alleviate pressure on the domestic currency, and stabilise the macroeconomic environment

DRIVING FINANCIAL STABILITY: Insights from Chan Andrea

In this exclusive interview with Mr. Chan Andrea, the Director General of Banking Supervision at the Bank of South Sudan with a career spanning eighteen years in various capacities within the bank, Mr. Andrea has been at the forefront of significant financial reforms and modernization efforts. Joining the Bank of South Sudan (a branch of Sudan Bank) in 2006, he began his journey in the investment and foreign exchange departments before moving on to pivotal roles, including Executive Director to the Governor and head of the Financial Markets Department. His leadership in launching government securities like Treasury bills marked a critical step in easing fiscal pressures. In 2022, he took on the role of Director of Banking Supervision, where he now oversees policies and advises the bank’s senior management.

Under the current leadership of Governor Dr. James Alic, Mr. Andrea has been instrumental in driving forward key financial reforms aimed at modernising the banking sector in South Sudan. Among these initiatives is the overhaul of the payment infrastructure, transitioning from paper-based transactions to a modern automated system, with the support of the East African Community and the African Development Bank. The completion of the new central bank headquarters stands as a testament to these transformative efforts. As South Sudan navigates the challenges of regional instability and economic dependence on oil, Mr. Andrea emphasises the importance of diversifying into agriculture and mineral investments. His insights into the future of South Sudan’s financial landscape reveal a vision for a cashless society and enhanced financial inclusion through innovative technologies like mobile money services. This dialogue explores the journey, achievements, and future aspirations of one of South Sudan’s key financial leaders.

Excerpt

Mr. Chan, it’s an absolute pleasure to be here today. And I wanted to start by just asking you to introduce yourself and share the journey and experiences that have led you to your current role as Director General for Banking Supervision.