MORTGAGEE LETTER 2024-14

The provisions of this ML are effective as of July 10, 2024

This Mortgagee Letter (ML) updates the Federal Housing Administration (FHA) Defect Taxonomy to clarify that fraud or material misrepresentation involving a sponsored ThirdParty Originator (TPO) is a Tier 1 severity defect.

All updates will be incorporated into a forthcoming update of the HUD Handbook 4000.1, FHA Single Family Housing Policy Handbook (Handbook 4000.1).

Affected Programs

The provisions of this ML apply to all FHA Title II Single Family mortgage programs.

Background

The FHA Defect Taxonomy (Handbook 4000.1, Appendix 8.0) is FHA’s quality assurance framework for Title II loan reviews. It provides a consistent method for identifying defects at the loan level, useful data and feedback through structured categorization of defects, and balance between FHA’s statutory obligation to mitigate risk to the Mutual Mortgage Insurance Fund (MMIF) and quality assurance business processes.

The Fraud or Misrepresentation section of the FHA Defect Taxonomy currently states that Findings of fraud or materially misrepresented information can fall into one of two severity tiers:

• Tier 1 (indicating that the Mortgagee knew or should have known),or

• Tier 4 (indicating that the Mortgagee did not know and could not have known).

It further states that FHA determines if the Mortgagee knew or should have known based on whether:

• An employee of the Mortgagee was involved, and/or • Red flags in the loan file that should have been questioned by the underwriting Mortgagee.

Mortgagees are responsible for the actions of their sponsored TPOs under 24 CFR § 202.8(a)(3) and Handbook 4000.1 Section I.A.5.a.v. To better align the Defect Taxonomy with these existing requirements and mitigate risk to the MMIF, FHA is updating the Defect Taxonomy to include fraud or material misrepresentation involving a sponsored TPO as one of the “knew or should have known” conditions used by FHA to determine whether a Tier 1 severity classification is appropriate.

Based on this update, FHA will seek life-of-loan indemnification from Mortgagees when there is evidence of fraud or material misrepresentation involving a sponsored TPO, regardless of whether FHA identifies specific red flags that should have been questioned at underwriting.

Summary of Changes

This ML:

• updates Handbook 4000.1 Appendix 8.0 – FHA Defect Taxonomy section IV Fraud or Misrepresentation.

Vincent M. Valvo CEO, PUBLISHER, EDITOR-IN-CHIEF

Beverly Bolnick ASSOCIATE PUBLISHER

Ryan Kingsley EDITOR

Katie Jensen, Sarah Wolak, Erica Drzewiecki STAFF WRITERS

Alison Valvo

DIRECTOR OF STRATEGIC GROWTH

Julie Carmichael PROJECT MANAGER

Meghan Hogan DESIGN MANAGER

Christopher Wallace, Stacy Murray GRAPHIC DESIGN MANAGERS

Navindra Persaud DIRECTOR OF EVENTS

William Valvo UX DESIGN DIRECTOR

Andrew Berman

HEAD OF CUSTOMER OUTREACH AND ENGAGEMENT

Matthew Mullins, Krystina Coffey MULTIMEDIA SPECIALIST

Melissa Pianin

MARKETING & EVENTS ASSOCIATE

Kristie Woods-Lindig ONLINE ENGAGEMENT SPECIALIST

Nicole Coughlin

ADVERTISING ASSOCIATE

If you would like additional copies of Mortgage Banker Magazine call (860)719-1991 or email info@ambizmedia.com Submit your news to editors@ambizmedia.com, www.ambizmedia.com © 2024 American Business Media LLC. All rights reserved. Mortgage Banker Magazine is a trademark of American Business Media LLC. No part of this publication may be reproduced in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission from the publisher.

Advertising, editorial and production inquiries should be directed to: American Business Media LLC, 88 Hopmeadow St., Simsbury, CT 06089, Phone: (860) 719-1991, info@ambizmedia.com

32

CMG Financial pursues "market differentiator"— and a paradigm shift—in building a de novo, in-house servicing >>

CMG Financial's

Paul Akinmade, Chief Strategy Officer; Courtney Thompson, EVP Head of Servicing and Christopher George, President & Chief Executive Officer

PARTNERSHIP MATTERS MORE THAN EVER TO REAL ESTATE AGENTS WITH FEWER REFERRALS TO OFFER

BY ROB CHRISMAN , CONTRIBUTING WRITER

MORTGAGE BANKER MAGAZINE

WRob Chrisman has been in mortgage banking since 1985 and publishes a widely read daily market commentary on current mortgage events.

has a house on the market at this time of year, with the summer here, and with conditions the way they are, you can bet they are a real seller — and probably happy to negotiate with you!”

here can loan officers (LOs) find the elusive purchase borrower? Many lenders have originators who are looking for leads in unconventional places. LOs are making the rounds at remodeling shows, for example. Builders focused on that business often know of someone in need of financing before anyone else.

There are LOs teaching classes at local community colleges and high schools to put their name in front of future home buyers. Originators are contacting human resources staff at local companies, who know of employees and recent hires searching for homes.

Some originators are focusing on the future market, since buyers need to think long term. “Don’t bail out because rates are high now because, of course, it won’t last forever,” they tell prospective buyers. “You can probably find a house now at a lower price than you will be able to a year or 18 months from now. If someone

Rates will fall eventually. Predicting when and by how much is notoriously difficult. When rates do fall, your previous clients can refinance at a lower rate. When their payments go down, and possibly substantially, it’s like getting a raise! However, falling rates mean there will probably be another purchasing frenzy and prices will get bid up. If someone buys a home now they will already be in the house when that happens and able to reduce their payment with a refinance.

Real estate agents want to treat loan officers as partners. They need a loan officer with good follow-up skills and with a system in place. Tell the agent how you keep in contact with the leads they give you. How often do you contact them? Do you handle leads differently during the process of securing a loan? Loan officers want to receive every lead their agent partner gets.

But, the shortage of sales means referrals and leads are precious

Real estate agents don’t want originators that are merely transactional. They want someone who sits down with clients and educates them on the best products for their situation, returns calls, and communicates throughout the transaction, keeping the agent updated all the while. Having the best rate is not always a path to sure success.

> ROB CHRISMAN

now for agents. Often, a real estate agent will not give a new originator a hot lead; there is too much to risk. Expect the opposite to happen, actually. The agent will work with a lead that you provide.

Real estate agents don’t want originators that are merely transactional. They want someone who sits down with clients and educates them on the best products for their situation, returns calls, and communicates throughout the transaction, keeping the agent updated all the while

Having the best rate is not always a path to sure success because real estate agents like information. Knowing that, for example, call a new agent and tell them how you are navigating the home insurance situation that we are experiencing. Reinforce that pitch with success stories. Have five to ten insurers that the agent doesn’t know about and share their info.

Be realistic about interest rates, especially buy-down rates. How can it help clients? Sure, there are savings up front. But, what happens in three years? Be able to answer that question

with authority. Share examples of monthly costs. Sit down and educate the agent. Ask them, “What price range do you normally work within?”

Providing a sheet for agents to have at their open houses, detailing various options, gets loan officer’s names in front of prospective buyers, too. Educate agents on how they determine that a buyer may be eligible for certain types of financing. Teacher loans? Doctor loans? VA loans? Explain the differences between owner-occupied and investor products. Open the agent’s eyes to new products. Be pragmatic, informative, educational (but not pedantic), and a collaborator.

Business has been slow, and with rates where they are, we can expect business to stay slow. Taking time to “recharge your batteries” is a good opportunity for lenders and originators to train themselves on new and existing products, familiarize themselves with their company’s software, rendezvous with former clients, and continue to improve as subject matter experts for the future.

Creating a space for the next generation in NMLS education.

Introducing Maximum Acceleration, your new premier provider of continuing education.

We’re not just bringing you a lecture. We’re bringing you the fuel to spark your competitive fire, the plan to win the game on the merits, the confidence to know the rules and master them.

We’re Maximum Acceleration, and we’re where loan originators go to put their career in high gear.

— LaDonna Lockard, CEO

WAREHOUSE LENDING COULD DRY UP IF CAPITAL REQUIREMENTS BECOME TOO BURDENSOME

BY BOB NIEMI , CONTRIBUTING WRITER MORTGAGE BANKER MAGAZINE

Imagine reading a blog post about Basel III that says it could be the endgame for mortgages, pushing large banks even further away from the market. You ask around, call some friends, but no one seems to understand the nuance. Well, except your know-it-all mortgage friend who thinks you said “basil,” that spice he loves on margherita pizza. You shake your head and look for more reliable information on what Basel III really entails.

“Basel” refers to the city on the Rhine River — and is pronounced “BAH-zәl,” unlike the spice. The Basel Committee on Banking Supervision meets in Basel, Switzerland, and has roots dating back to 1974. The first Basel Accord, released in 1988, established minimum capital requirements to internationally active banks.

Basel II was released in 2004, revising Basel I capital frameworks by introducing more risk-sensitive capital requirements and enhancing risk management practices.

Basel II was criticized for its complexity and for potentially underestimating risks during the financial crisis, leading to a revision in 2009 in response to the global financial crisis of 2008. Basel III was subsequently introduced with new

efforts to increase the resiliency of banks by strengthening capital requirements. The gold-plating additions force banks to deal with stricter definitions of capital and higher minimum capital ratios.

The impact will require banks to hold more capital based on new standards for assets like small business lending and consumer mortgages. Capital can be used for business, investment, or simply held to meet these increased requirements. Reserves must be liquid to meet these needs. To implement Basel III, the Federal Banking Agencies proposed an interagency Notice of Proposed Rulemaking which was anticipated to impose up to a 20% increase in the capital requirements for larger institutions.

Let’s do a level set and review what “capital” means in this context.

We know “capital” is the value of a business, including working capital and more liquid assets like money held in banks and longer-term investments and real estate holdings. Think of liquid capital as the assets a business uses to pay salaries and expenses tied to day-to-day operations. Longer-term investments help businesses “grow money” beyond

regular business bank accounts. There are other types of capital that cannot be easily spent, such as goodwill, brand value, and intellectual property.

The capital banks hold is not only used for running operations, but to protect shareholders and depositors as well, like a safety net. A bank’s assets typically include cash, securities, and loans made to consumers, businesses, other banks, and governments. Banks use cash and other liquid assets in day-to-day operations. Longer-term investments like consumer, small business, and mortgage loans made to customers cannot be easily spent. However, mortgage servicing rights (MSRs) are more liquid assets for investment than holding whole-loan portfolio products. A portfolio loan can return more on the investment, but the asset repays over a longer period over time. An MSR could be sold for cash,

but generally not overnight.

These different assets (creators of capital) have different risk characteristics to which the Basel accords assign different risk weights. Those risk weights indicate the risk certain investments are for the bank to hold. Credit risk from small business lending, consumer loans, and mortgages must be reconciled by the bank with capital reserves should those loans default. Not all loans repay on the same schedule, either, or have the same underlying guarantees.

Mortgage assets with higher risk carry a higher risk weight compared to that of a U.S. government bond, which has a zerorisk weight. A mortgage borrower may default, but the government won’t.

Banks finance investments and lending activities with capital, such as customer deposits, and debt. Banks do their own borrowing. While all businesses need

Combined with rising housing costs, delayed rate relief, and nationwide housing shortages, these efforts will only exacerbate the challenges lenders face today.

BOB

NIEMI DIRECTOR OF GOVERNMENT AFFAIRS

WEINER BRODSKY KIDER

reserves for unforeseen events, banks must hold money in reserve to make sure they can manage unexpected problems and maintain business continuity. The increased reserves can help the bank absorb losses to reduce the likelihood of a bank failure. In today’s digital banking world, challenges can materialize faster because consumers can empty their accounts almost instantaneously.

This increases the need for sound risk management practices and additional capital reserves.

The risk weighing impacts under Basel III are based on their perceived riskiness. Longer term mortgages and mortgages with higher loan-to-value ratios and lower borrower creditworthiness carry higher risk weights. Basel III applies a risk weight applied to MSRs of 250%, which dramatically reduces the incentive to hold servicing rights on a bank’s balance sheet. To hold an MSR worth $100, for example, banks would need $250 in reserve.

Is this sound, or an additional incentive for banks to focus on lower-risk assets and move further away from mortgages? Possibly both. The increased risk weight for MSRs alone will impact first-time homebuyers as they find it harder to obtain loans with smaller down payments as banks implement these requirements. Smaller down payments mean higher loanto-value ratios, riskier assets for banks, and higher capital requirements.

Basel III also increases capital requirements to offset banks’ risk from warehouse lines extended to independent

mortgage bankers. Warehouse lenders are a critical component of the mortgage finance industry as they provide shortterm financing for independent mortgage bankers to fund loans, which are then repaid when the loans are sold in the secondary market. These increased capital requirements and risk weighting will reduce a bank’s willingness (or ability) to engage in warehouse lending.

This could increase costs for existing warehouse lenders, reducing credit availability in the mortgage market.

It is important to recognize, however, that Basel III would only apply to the fewer than forty banks that hold over $100 billion in assets. These large financial institutions have been pulling away from the mortgage market since Basel II, due to the increased capital requirements, regulatory burdens, and profitability challenges from evolving markets. Nevertheless, banks continue to be systemically important to the independent mortgage bankers and servicers, as well as their business partners, and this attempt to strengthen the global banking system could create a fundamental shift in how mid-sized and U.S.-based regional banks operate.

But, Basel III could also reshape the dynamics of U.S. mortgage lending, making it more like Europe, where thirty-year mortgages are unheard of. Combined with rising housing costs, delayed rate relief, and nationwide housing shortages, these efforts will only exacerbate the challenges lenders face today. While the proposed rule has been tabled for further review, when the next iteration comes around, educate your friend over pizza.

Recent data reveals that climate is influencing migration patterns in the United States, but in unexpected ways. Many Americans are moving to areas increasingly threatened by climate risks such as wildfires, flooding, and extreme heat. According to a 2023 Redfin report, high-fire-risk counties saw a net gain of 63,365

Texas is at the forefront of this trend, with 36.1% of new residents moving to its fire-prone counties, a significant rise from 28.7% in 2022. Despite its reputation for wildfires, Texas continues to be a top destination for newcomers. In contrast, California’s high-fire-risk counties experienced a net outflow of 6,937 people, reflecting growing awareness and concern about fire risks in the Golden State. Factors like escalating home prices and wildfire damage are contributing to this shift.

6,937

Florida remains a major draw for those moving to high-floodrisk areas, with 53.5% of the national net inflow heading there. However, this percentage has slightly declined from last year, indicating a growing awareness of flood hazards. Miami-Dade County, despite being a significant flood risk zone, saw a notable net outflow of over 47,000 people. This exodus is driven not only by climate concerns but also by rising housing costs and insurance premiums. The median home price in Miami has surged nearly 75% since 2019. As a result, nearly two-thirds (64.7%) of homes listed in June lingered on the market for at least 30 days without finding a buyer, up from 59.6% last year. According to Redfin, June’s numbers mark the most significant annual rise in a year and the highest level

6,937

MIGRATING COUNTIES

36.1%

TX NEW RESIDENTS MIGRATING TO FIRE-RISK COUNTIES

June also marked the fourth consecutive month of rising home listings lingering on the market, leading to a growing accumulation of unsold inventory. This trend is largely due to buyers hesitating in the face of record-high home prices and elevated mortgage rates.

like Tampa (70%), Fort Lauderdale (77%), Jacksonville (70%), and Orlando (69%) are all seeing significant upticks in stale listings.

53.5%

FL NEW RESIDENTS MIGRATING TO FLOOD-RISK COUNTIES

Tune in to new epiosdes of Mortgage Meteorology every Thursday on The Interest for June since 2020.

Texas and Florida are experiencing the most intense impacts of this market slowdown. In Dallas, 63% of listings in June sat on the market for at least 30 days, a sharp increase from 52% last year. In Florida, cities

The increase in unsold inventory in these states is partly due to a surge in new home construction, adding to the supply when demand is cooling due to high housing costs, including rising insurance and HOA prices.

47,000

RESIDENTS MIGRATING OUT OF MIAMI-DADE COUNTY

Nationwide, over 40% of homes were on the market for at least 60 days in June, slightly higher than last year’s 38.4%. Despite the seemingly small shift, this marks the hottest annual increase in nearly a year and the third straight month of rising long-term listings.

Redfin suggests that unless there is a significant shift in mortgage rates or pricing strategies, the broader market may continue to experience this cooling trend.

Watch it on

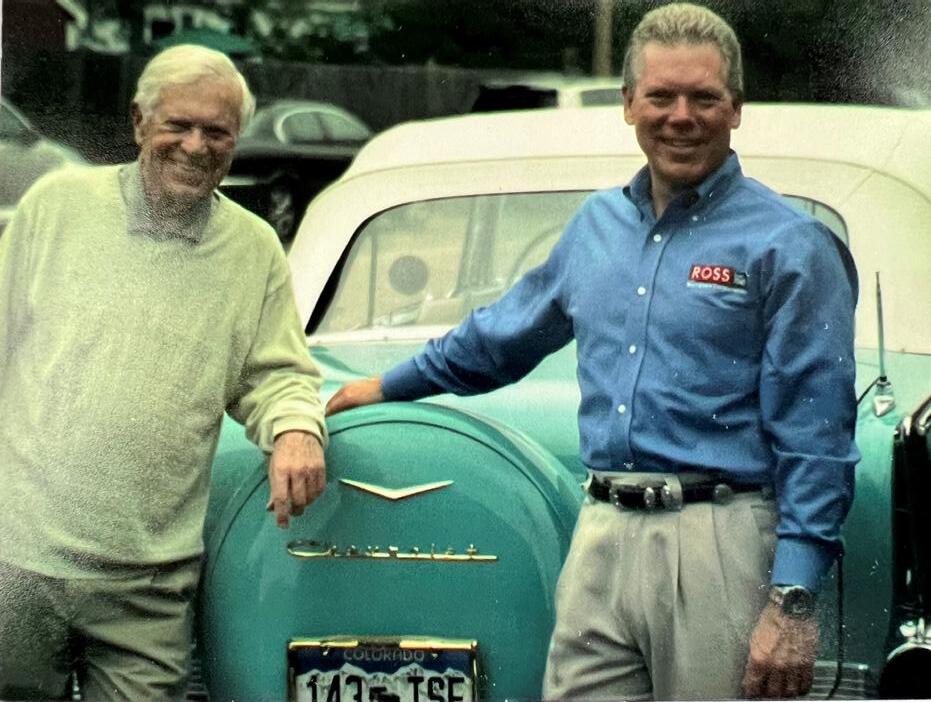

Ross Mortgage Corporation (RMC) wasn’t always “Ross Mortgage Corporation.”

The company was founded

75 years ago as Advanced Mortgage, the lending arm of a construction company that current CEO Tim Ross’s father began working for after graduating law school. The year Advanced Mortgage was founded, 1949, British astronomer Fred Hoyle termed the phrase “Big Bang” to explain the origins of the universe, the National Basketball Association (NBA) was formed, and the Soviet Union tested its first atomic weapon.

Ross followed his father into the industry after he graduated college, and the legacy independent mortgage bank’s (IMB) name changed around that time. Four decades later, Ross says he’s seen just about everything that the market — and borrowers — have to offer. Building a legacy means maintaining a legacy, and that first principle for Ross is interest-rate blind.

“How it is that we built the business over the

BY RYAN KINGSLEY , EDITOR , MORTGAGE BANKER MAGAZINE

years has a great deal to do with how it is that we serve the customer,” Ross says. “A major tenet of our organization is the delivery of the product and service to the customer in a way that delights them.” Headquartered in Troy, Mich., RMC’s mortgage neighbors — United Wholesale Mortgage (UWM) and Rocket Mortgage — may always have the edge on lower rates. But, Ross’s legacy of “delighting” customers has hung in over the past two years of margin compression and decades-low origination volume.

In a wide-ranging interview with Mortgage Banker Magazine, Ross discussed the importance of Ross Mortgage Corporation (RMC) reaching its 75-year anniversary, the ways in which the company has adapted during two challenging years in the industry, and the strategies that RMC is developing in order to stay competitive and carry its lending legacy into the future — a future that will not include Tim Ross at the helm of the company for very much longer, he said.

That conversation, which has been edited and condensed for concision and clarity, follows.

“This has been particularly tough,” Ross told Mortgage Banker. “The length of this down cycle is different. There has been a great deal of merger and acquisition and exit from the business. We’ve experienced that in the past, but I think this has been a bit unusual as people did choose to head for the exits. We had to make some very difficult and serious decisions about remaining in place and continuing the legacy, if you will, and remaining in business.”

TIM ROSS, CEO ROSS MORTGAGE CORPORATION

Q: At what point did you have to answer that question, tie the bow at 75 years or keep going? Was that really on the table?

“Absolutely. It has to be on the table because there is an opportunity to preserve the core. While the legacy is critically important, you have to make a good business and personal decision at the same time, as to whether or not it makes sense for us to continue. There

is no question that we did have to take a look at the brutal facts of where we stand and what we need to do and what we need to accomplish in order to continue to make sense of the enterprise. We laid out those plans. We knew where the ripcord was.”

Q: When were you making that decision? The third or fourth quarter of last year?

“Particularly as we went through the third and fourth quarter last year. Certainly rolling up under another company is an option. Merging with somebody else is an option. A quiet shutdown is an option. All of those things were on the table, and while we never got serious about any one of those in terms of engaging with others, as far as taking one of those options, they were all considered. Because we’ve been around for a long time, there’s an opportunity for us to talk to a lot of people, too, to be able to engage in a conversation about what you’re doing, what

we’re doing, what could make sense going forward. Those did take place. Fortunately, as we entered into 2024 and got through the first quarter and found profitability, the spring market buoyed us and most everybody else even though there weren’t many fundamental changes in the market.”

Q:

This contraction in the market really doesn’t favor the midsize companies who lack the scale to withstand any storm. Smaller companies that are more nimble, it’s a bit easier for them to adapt to a challenging market. You originated somewhere around $500 million in 2020, on that smaller end. Would you agree that we’re seeing the middle tier of lenders at the most risk, and smaller IMBs having more of an advantage in the market?

“I believe so. When you get to the middle tier, you have a number of masters that you must answer to. Something that’s been said here over the years, and particularly based on certain business conditions that we’ve experienced because of our size, we’re able to make business decisions ‘leaning up against a doorframe with a cup of coffee in our hand.’ It does not take a huge response from investors and directors and so on for us to be able to make that change.”

Q: What kind of business decision, for example?

“One of the things that we did do when most of the large investors exited wholesale was to do the same. We were too small to really compete in that arena and concerned about regulatory change, so we became a real monoline lender for these last many years doing just strictly retail. All of our business interest and investment has been in building and maintaining the retail production network

today. I think things are a little bit different, and the opportunity for us to consider a return to the wholesale and TPO market is one where we think that we have something to offer where we can niche that business. We would not want to go head-to-head with United Wholesale, but I think that based on who we are, possessing expertise particularly in government lending, is something that this emerging broker community would embrace.”

Q: Can you say a little bit more about what you mean by “niching” that TPO business?

“One expression that people here have heard me say over many years is, ‘Complexity is our friend.’ The more complex it is, the more difficult it is, the more regulation that’s required really suits a company like Ross. We’re very good rule followers. We’ve been doing this for many, many years and our ability to be able to take those products — FHA, VA, USDA, where there is more expertise required, a little more hand-holding and regulation — that we can deliver a level of service to the broker that would encourage them to wish to do business with us. That relationship at the end of the day is critically important to us, our ability to be able to form relationships with our referral sources, whether they be traditional like the real estate community, certainly our borrowers, but also members of the mortgage brokerage community, is something that we take great pride in. They’re critically important to us, and that when we do develop relationships with people they’re deep relationships and supportive of one another.”

Q: Existing home sales through this spring were lower than they were in the spring of 2023. You said RMC found profitability in the first quarter. The MBA released its first quarter performance report showing

overnight. We’ve

There is no question that we did have to take a look at the brutal facts of where we stand and what we need to do and what we need to accomplish in order to continue to make sense of the enterprise. We laid out those plans. We knew where the ripcord was.

TIM ROSS

market is something that has served us well and is serving us today. In the first part of this year, however, you can’t ignore the refi opportunity. We are lagging behind industry averages in terms of our percentage of refinance activity.”

Why is that the case?

“The message to our sales group, to our client base, is that we are here to serve them, that we will do anything that makes sense. But, the fact of the matter is, to the sales group, some of your clients are refinancing and they’re not refinancing with

Q:

dollars a month on the purchase side.”

The FHFA published research in March projecting the lost sales we’re likely to see in years to come due to the lock-in effect. There’s a compounding effect — every lost sale this year is a lost refinance or a lost sale in the following years. How much are you thinking about needing to adapt your business model to the reality that there will be a large cohort of homeowners who hold onto those low mortgages, and thus fewer loans?

“There’s really a couple of things that come to this conversation. One would be a consideration to return to another business line that we had operated effectively in the past, and to return to that is just one of the ways that we supplement the retail volume through an expansion and return to the TPO market. That would be one of the ways that we begin to address the continuing challenge of business volume. The other would be to recognize that while some may be unwilling to leave their present residence, there is an opportunity for us to do two different things. One would be the refinance opportunity. People will ultimately trade in some of these low-interest-rate mortgages if they find themselves over-extended. The other is to continue to focus on something that we’ve also done well over time, and that’s renovation lending. We do have some area of specialization where renovation lending is

concerned. People can stay in their existing residence and just improve it in order to be able to make it more livable for them.”

There are other shifts underway in the industry, as well. Everything’s becoming more technology focused. The number of sales continues to fall as loan sizes keep growing. The environmental impacts of climate change on the housing market. What a home costs and how much it costs to insure that home will likely only get more expensive. How does Ross get from 75 years to a hundred years, adapting to all of these trends?

“It’s a fair question and one that I don’t know that I can answer specifically. We’ve got the opportunity to identify where real advantage takes place in order to keep our costs under

control because at the end of the day it’s really the only thing I can control. I don’t have control over many of the things that you’re mentioning. The only thing I have absolute control over is how much I spend in order to be able to close a mortgage loan. The more I can incorporate the technology into the process, the more opportunity for me to continue to deploy our best and brightest to their highest and best use — trying to eliminate as much of that ‘stare and compare’ as I can because the technology should be able to do more and more for us going forward.”

Q: Do you service your own loans?

“We do not. We were a servicer to a point, but then as the servicing income was built into the price of the loan we elected to exit mortgage loan servicing, and we’ve been essentially a correspondent with the biggest servicers for several years now. That would

be another thing that would be back on the table. It's a conversation that takes place, and whether or not there is space for small companies to be servicers again. Some of our competitors are. I wish I had been a servicer over the last two years because that is an income stream that would have supplemented some of the losses on the origination side, and did for many.

Q:

For the 100-year anniversary, do you still see yourself at the helm should 2049 come to pass for Ross Mortgage Corporation?

“I do not see myself at the helm. We’ve built a management team here that has been groomed to take the company forward into the foreseeable future. I have one relation who is in the business today who has an equity interest in the business. That is my sister. She’s been our CFO for some time, and my son

works for us today, too, in the Chicago market area. There are Rosses sprinkled through the organization, even though the senior leadership team are not related, but have been here many years.”

Q:

So, would RMC stay in the family? Is it in the family today, ownership-wise?

“It is. It is in the family today, for sure. I think that in order for RMC to be able to get to the next 25 years, it’s probably likely that some of that would be transferred to other than family members as they would both earn and deserve an equity interest in the business they’ve helped to build.”

Q: With interest rates holding higher for longer in 2024 and 2025 shaping up to be a challenging year of elevated borrowing costs as well, what keeps you up at night?

“There’s just certain aspects of the business that are absolutely finite in terms of what I said earlier. The only thing that I can control is how much it costs to be able to produce the loan. What I need to be able to do is to maintain a level of production and maintain our margin in order to be able to cover our cost to produce. That’s maybe back to sort of the legacy aspect of this, knowing that based

on current reserves and the fact that we know precisely where we need to be in order to be able to cover our costs and make a little bit of money. Any significant decline in our overall production below that level is something that keeps me up at night. We’ve got a great and stable field force, but they need to be cared for, nurtured, and supported in order for them to stay with us. Today, there’s not a great deal of movement in the business, but things like mergers and acquisitions tend to rock that boat. People who would never have left their existing circumstances because they’ve been well supported and they know their systems and their people and so on, all of a sudden wind up with new management, and they don’t like it.

Q: To be fair, people might say, ‘Shoot, it’s all the same management. We’re out because nothing ever gets freshened up.’ As you’ve gone through this downturn, have you lost some of that field team who you’re trying to nurture and support and take care of?

‘Complexity is our friend.’

“We’ve had some attrition, but it’s been very modest, just maybe a couple people. That’s been it. We’ve been fortunate. We’ve added people and some of the more recent additions are making a significant contribution. Net, we’re well ahead.”

Q:

You decided not to pull the company’s ripcord. Are you pulling your own ripcord soon?

“Oh, I think, yes. I’d like to think that I would continue to be involved, from a strategic point of view, but without any day-to-day responsibility. You know, keep an office for me, give me a place to hang my hat. But again, the people that are running the business today are doing a great job, and they’re making good decisions. They’re making tough decisions at times. So yeah, I see myself continuing to be involved from a strategic point of view, but not on the day to day.”

The more complex it is, the more difficult it is, the more regulation that’s required really suits a company like Ross ... We can deliver a level of service to the broker that would encourage them to wish to do business with us.

Tim Pascarella, President of Ross Mortgage

A warm welcome to you! I’m Kelly Hendricks, the Managing Editor of Mortgage Women Magazine and Senior Vice President of Delmar Mortgage, and it brings me great joy to extend this invitation to you. Throughout my career in the mortgage industry, I’ve been fortunate to have leaders and mentors who played pivotal roles in shaping my journey. I am thrilled to introduce a transformative initiative – the Mortgage Women Leadership Council, created by Mortgage Women Magazine.

In my role, I’ve experienced the challenges that women face in leadership within the mortgage sector. These challenges led to a profound realization — the need for a dynamic network to empower women in our industry. This realization is the driving force behind the creation of the Mortgage Women Leadership Council. I believe in the power of collective support, and I am excited about the opportunity to share and benefit from each other’s experiences.

Our mission is clear: to promote and empower women’s leadership in the mortgage sector. The council aims to create a supportive environment for professional growth, mentorship, and networking. Joining the

council comes with various benefits, including networking opportunities and access to industry-specific professional development resources. We understand the unique challenges women face in mortgage leadership and have tailored mentorship and support systems to address them.

I invite you to join this movement to empower women in the mortgage industry. The Mortgage Women Leadership Council is committed to fostering a welcoming and supportive environment. Your involvement will not only contribute to your personal and professional growth but also play a crucial role in advancing women’s leadership in our industry. To join or get involved, simply click here to apply.

Thank you for considering this invitation to join the Mortgage Women Leadership Council. For further inquiries about the council and details on how to join, please contact Beverly Bolnick at bbolnick@ambizmedia.com. Let’s work together to advance women’s leadership in the mortgage industry — because collective action brings about meaningful change.

Kelly Hendricks Managing Editor, Mortgage Women Magazine

Access to a Powerful Platform: Amplify your voice and influence through Mortgage Women Magazine, exclusive sponsored programs, email newsletters, and impactful events.

Editorial Opportunities: Showcase your expertise and insights through editorial features in Mortgage Women Magazine, gaining visibility and recognition among industry peers.

Awards and Recognition: Receive well-deserved recognition through our award programs, celebrating your achievements and contributions to the mortgage industry.

Community Support: Become part of a dedicated community committed to celebrating and driving meaningful progress in the mortgage sector. Connect with likeminded women leaders, share experiences, and foster collaborative initiatives.

Mortgage Women Magazine: Enjoy your complimentary digital subscription to Mortgage Women Magazine, the premier publication for women in mortgage. Read advice, learn about industry updates, and take in the inspiring stories of your peers.

Join us and be a driving force in creating a more inclusive and thriving mortgage industry. Together, as a united community, we believe we can make real change.

Enjoy 1 year of your individual membership free! Use code MWM2024

Become a member today. mwlcouncil.com

BY PREETAM PUROHIT , CONTRIBUTING WRITER, MORTGAGE BANKER MAGAZINE

It has been tough going for Americans trying to buy homes over the past couple of years – especially lower- and median-income households. Nationally, median home sales prices have increased from roughly $260,000 at the beginning of Covid-19 pandemic to more than $400,000, according to National Association of Realtors (NAR) data. Concurrently, interest rates increased from roughly 4% pre-pandemic to the current level of 7%, or slightly lower. (See Chart 1)

Under these conditions, affordable mortgages are rightly earning a lot of attention. Affordability has been a key challenge for homeowners, especially first-time homebuyers struggling to afford the housing market’s high cost of entry because of the double whammy of home price appreciation and higher interest rates. (See Chart 2)

Assuming a mortgage payment ratio of 36% of the borrower’s gross monthly income leaves $2,760 for principal and interest, assume the monthly cost of tax and insurance is $600. At the current interest rate of 7%, the median income borrower in Rhode

Island, for example, where Embrace Home Loans is headquartered, is only able to afford a loan of $390,000, which would require either significant down payment or a lowerpriced home. Low inventory levels mean the competition for lower-priced homes is extra high, making it even more challenging for a borrower to win that deal. Likely there’s a bidding war. (See Chart 3, following page)

Lenders play an important role in sustaining healthy communities and expanding access to affordable mortgages — it is important for communities to have their elected officers, teachers, and municipal employees living in the same communities. But, lenders often must educate borrowers about the existence of affordable mortgages.

It’s easy for prospective homebuyers to see home prices and interest rates rising at the same time and automatically remove themselves from the home-buying conversation. Lenders who do not understand affordable mortgages cannot educate borrowers in their community about the opportunities for homeownership just waiting for them — and lenders — to take advantage of.

CHART 1: US NAR EXISTING HOME SALES MEDIAN PRICE

SOURCE: BLOOMBERG, NATIONAL ASSOCIATION OF REALTORS

CHART 2: 30-YEAR CONFORMING MORTGAGE RATE

SOURCE: BLOOMBERG, OPTIMAL BLUE

SOURCE: EMBRACE HOME LOANS

While depository banks come under the umbrella of the Community Reinvestment Act (CRA), enacted in 1977, which requires them to meet the needs of all the borrowers in their communities, including low- and moderateincome households, independent mortgage banks (IMBs) are exempt from CRA. Some state-level CRA laws exist, and a recently passed law in Illinois does assess IMBs under a CRAlike framework. Absent such state-level laws, IMBs are indirectly encouraged by regulators to make mortgages affordable and assess borrower profiles to ensure that all segments of the community are well represented in their loans.

Federal Housing Agency (FHA) and Veteran Affairs (VA) loans were the original affordabilityoriented programs made available to borrowers with low credit scores and high loan-to-value and/or debt-to-income ratios. Fannie Mae and Freddie Mac provide affordability-oriented programs, too, through their Home Ready and Home Possible products, respectively. The

availability of Home Ready and Home Possible mortgages to borrowers depend on income limits determined by the geographic location of the property.

There are also affordable programs available at state and county levels, usually provided by a state’s housing finance agencies. Borrowers need to research these programs more thoroughly as every state or country has a unique program only available through a handful of lenders. Lenders who provide access to these programs must be approved by housing agencies since the programs are specialized and borrowers have to be underwritten to specific requirements.

Most affordable mortgage programs determine borrower eligibility using an income limit of under 80% of the area’s average median income (AMI), depending on the family size.

In Rhode Island, the state housing agency RI Housing has an income limit of $112k for a family of four to access affordable mortgage programs. A borrower that qualifies would benefit from access to lower interest rates, lower down payment requirements, and down payment

assistance (DPA) programs.

Such programs expand access to homeownership, especially among first-time homebuyers.

DPA programs provide assistance to borrowers unable to reach certain money-down minimums, with limits depending on the income thresholds and geographic locations. Some DPA programs, however, charge higher interest than rates for first mortgages.

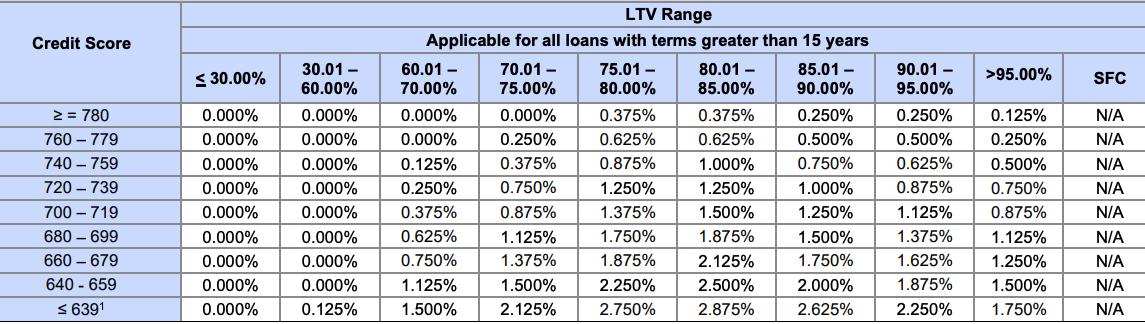

Loans for borrowers with income less than 50% of the AMI are called Very Low Income Purchase (VLIP) loans and those between 50% to 80% of AMI are called Low Income Purchase (LIP) loans. These income limits allow lenders to qualify the borrowers without any LLPAs with the GSEs providing substantial savings to the borrower relative to a conforming loan.

As seen in the table, these adjustments can provide significant savings, especially for borrowers with credit scores below 700, by providing significant reductions in their mortgage rates. The economics of these loans make homes affordable for borrowers and the production of these loans profitable for

lenders because these products are part of the community-building goals of the GSEs. Lenders receive a “pay up” when selling these loans, and are therefore able to provide the borrower with some lender concessions, like underwriting fee waivers.

The most effective programs involve income limits based on AMI, but there can also be conditions for financing such as a requirement to live at the property for an extended period of time or penalties for refinancing the loan or selling the property too soon. Not only do loan officers need to know these nuances, but borrowers need to understand this fine print, too.

Grants available from foundations trying to make a cultural shift within the lending community to be more accepting of the DPA and CRA products — trying to satisfy corporate social responsibility (CSR) goals rather than just satisfying regulation — can also be sources

SOURCE: FANNIE MAE

of affordable mortgages. Lenders who link borrowers to these foundations help diversify borrower pools, as required by regulators like the Consumer Financial Protection Bureau (CFPB).

Lenders’ profitability associated with the bond loans can be a challenge since there is a cap by housing agencies on the margins that lenders are allowed to charge the borrowers. Instead, profitability from these products often arrives indirectly — these loans act as a mechanism for lenders to fill their pipeline and to be able to attract high-producing loan officers.

“Once a loan officer is able to help an agent partner access these loans with a member of the community, the connection is instant and relationship value is immense,” says Nick LaClair, head of pricing at Embrace Home Loans. “The LO is able to establish trust with that agent who then provides referrals in the form of buyers purchasing homes.”

delinquencies underwriting these loans, favorable prepayment characteristics offset some of the negative value.

Lower loan balances mean rates would need to move significantly for the monthly savings to cover the closing costs on a refinance. Meanwhile, lower credit scores impact borrowers’ ability to qualify for a refinance, while the terms of affordable mortgages often require borrowers to hold the mortgage for a certain number of years before refinancing.

“Once a loan officer is able to help an agent partner access these loans with a member of the community, the connection is instant and relationship value is immense...”

NICK LACLAIR HEAD OF PRICING EMBRACE HOME LOANS

The low (or negative) profit margin on producing an affordable mortgage becomes a net positive for the lender and the community. Borrowers access homeownership and lenders access referral networks. “It is a win-win situation for both the LO and the agent, too,” LaClair adds.

While there is an inherent risk of higher

This guarantees cash flow to investors, as well as lenders who service their own loans.

A knock-on benefit of offering these programs is building a more informed home ownership community where you lend. While every affordable mortgage program has its own charter, many have a compulsory education class that borrowers must take to access the financing. The home buyer’s education ultimately provides borrowers with a clearer understanding of their financial situation and sets them up for a successful homeownership.

Preetam Purohit, CFA, CQF, FRM, is currently the head of hedging and analytics at Embrace Home Loans.

WHERE IDEAS GO HEAD TO HEAD

BY RYAN KINGSLEY , EDITOR , MORTGAGE BANKER MAGAZINE

CCourtney Thompson likes to talk with her hands. To watch her piece together the many moving parts of mortgage servicing is to imagine her knitting an invisible sweater, or topping an invisible pizza — not nerding out on the history of a regulatory system organized around paper.

“We don’t open mail. We don’t answer our phones,” she scoffs, lamenting the fact that in 2024, the nucleus of mortgage servicing law is still the U.S. Postal Service. “All of these rules and regulations that are designed around protecting consumers actually operate as hurdles to connecting with them.” For years, legacy regulations constrained by legacy technologies have stymied innovation in mortgage servicing, hurting homeowners, most of all.

“That’s why I stay, by the way,” adds the executive vice president and head of servicing at San Ramon, Calif.-based CMG Financial. “Because it’s a nasty business.”

Technology developed in the 1960s and 1970s remains the infrastructural core of servicing platforms in widespread use today. Designed around processes for taking and making payments and aggregating information for reporting to investors, borrowers not only took the back seat of these processes — they were left at the curb. The industry has still not solved for human connectivity after a loan closes, stunting industry growth while posing systemic risks.

Seth Sprague says the industry now is spending a lot of time “focusing its efforts to try to keep borrowers engaged.” As director of mortgage banking consulting services for Richey May, the mortgage industryspecific tax audit and advising firm, Sprague has observed how innovation in servicing has lagged innovation in other aspects of the mortgage process. “It’s that disengaged borrower that really leaves a lot of losses for everybody.”

Engagement and empowerment aren’t exactly the same, though. Can servicing transcend making and taking payments, revising a loan balance, and dealing with crises? Should it, even?

“I’m the proverbial guy that flunked his way out of high school and didn’t go to college and started as a loan officer and worked his way up,” says Chris George, founder, CEO, and private owner of CMG, who over the past year has invested in building a de novo, inhouse servicing platform that centers rather than marginalizes the borrower experience. He aims to inside-out the commoditization of collecting payments by reinvigorating the borrower-servicer relationship.

It’s difficult work, pioneering work, and expensive work — very expensive work. George won’t divulge the expense. That’s also beside the point. “We’re pretty close to getting there,” he confirms. “We see this as a pivotal point in our company’s legacy.”

In 2019, CMG originated roughly $6.5 billion in loan volume. Production swelled to nearly $14 billion in 2021, before receding to $9.5 billion in 2022. In

2023, the worst year of existing home sales since George founded CMG in 1993, the company boosted 2022’s production by 45%,

“There’s a tipping point where these things can’t be supported anymore. These ecosystems that are running the American financial system, to replace them is essentially replacing your operation, which is why it’s that expensive and that hard.”

Courtney

Thompson

Executive Vice President, Head of Servicing CMG Financial

closing nearly $14 billion worth of mortgages once again. Through the first half of 2024, CMG was on track to match or surpass last year’s production.

While CMG has never serviced its own assets, now it can do so profitably due to its growing market share. George’s freedom as a private owner to make investments in servicing innovation “could be a market differentiator really from a servicing perspective,” says Thompson. More so, George has spent big on CMG’s freedom to control its destiny — and its borrowers' destinies.

Experts say it requires 200,000-300,000 units to make any money on in-house servicing. “You really need to understand what you’re getting into, and it does take cash,” says Sprague. “Servicing isn’t a hobby.”

“When you look at technical innovation, we’re kind of on a growth of our maturity curve,” says Paul Akinmade, the company’s chief strategy officer, who entered the industry in 2004 as an originator. “You look at the G-Rates, the Freedoms, the loanDepots, the Quickens of the world, they’re established. The challenge with that is they’ve already built their battleships.”

So, CMG assessed the shortcomings of others’ “battleships” and decided to build something novel — an engine that unifies the application, origination, and servicing experience for borrowers and their loan officers. “If I see something that they’re doing at one company and somebody else is doing at another company,” he continues, “I can detect the imagination of all the best practices that are being done in the industry and consolidate them.”

An 18-month project, the platform should have loans flowing through it by early 2025, pending approvals from regulators. While CMG does not have plans to become a major player in the sub-servicing market, Thompson acknowledges that the company

could sub-service for a similarly situated partner that sees the value of their platform and economic model.

Ultimately, allowing borrowers to be more nimble in the market enables CMG to be more nimble, too. By reorienting servicing operations around the customer journey, not just a payment schedule, CMG hopes to make the back office of servicing the new front office for originating. Industry-wide loan production in 2024 has mirrored 2023, which serves the interests of CMG, helping them capture market share.

“We’ve been waiting for this market,” George says. “I’ve been waiting for rates to go up.” The difficulty of the endeavor makes it worthwhile. He continues, “The challenge of doing hard work is what we’re all about with this process because we think that’s an interesting barrier of entry for all the rest of the competition. It gives us a definitive, distinctive advantage.”

Innovating in a highly regulated industry is capital intensive, making return on investment (ROI) the usual guiding principle for such investments. CMG is different, however. While ROI is eagerly anticipated, George has loans on his books with notes in the low twos and high ones from COVID-era originations.

“I don’t think those loans are ever paying off,” says George, whose four sons work at the company. “You want to keep that thing until payment 360.” That’s a 30-year relationship. “One of my boys is going to be accepting the last payment for a loan that I made back in 2020, 2021.”

The additional business a satisfied borrower provides through future referrals is typically unquantifiable. It is similarly difficult to quantify how much future business is lost

“It is a substantially different way to look at loan servicing today, that really is putting the word ‘service’ back into loan servicing and the ability for borrowers to be able to see the added value of why they selected a particular company to do their mortgage.”

Chris George, Founder, CEO, and Private Owner, CMG Financial

from a dissatisfied borrower. The return on CMG’s investment, which includes rewiring much of the company’s operations, has no specific timeline, as opening a new branch location might.

Rather, the “intangible returns that the service of servicing brings to us” would be worth an eight-year wait if it takes that long to break even. The investment in a de novo servicing platform will result in winning and retaining more customers, George believes, while preparing the company for future demographic and technological shifts in the industry.

“Pioneers get shot and settlers get rich,” he quips. “I kind of like to think that we’re pioneering products and we’re not dying along the way. We’re bringing to light ideas that we think are good for the consumer.” Those ideas are similarly beneficial for CMG, which has grown market share in an elevated-rate environment. George attributes that down-market success to the idea that “every single person’s hand on the wheel is to serve the customer.”

Instead of forcing consumers to stoop to the servicing industry’s limited capacity, CMG would rise to the rapidly evolving expectations of consumers, who would prefer to spend more effort understanding the transaction and less effort searching for the components of the transaction.

“The consumer today is actively concerned about how their loan is serviced and how well they are treated in that process,” George

explains, “and want the kind of connectivity and the kind of access that they had when they were being taken care of during the origination process.”

Where the closing and selling of a loan would typically end the relationship between borrowers and loan officers, CMG’s new platform makes a borrower’s loan officer their primary point of contact through the servicing of the loan. “The idea is that we want you to be able to communicate with the person that you built trust with, and we want you to be able to do these things without having to talk to a completely different stranger,” he reasons.

The core of this platform is a homeowner marketplace that pools data currently held across disparate systems to situate borrowers mortgages within a more nuanced accounting of their financial lives. A borrower can access the homeowner marketplace to check the status of a loan, the value of their home, or changes in rates. Maybe that borrower wants to replace expensive appliances, build an addition, shop insurance or utility rates, or buy a second home.

Myriad touchpoints in one location provide visibility, convenience, and optionality, empowering borrowers to take ownership of their home loans — not just pay their bills before the due date. Homeownership is the cornerstone of average consumers’ ability to generate long-term wealth. Monthly mortgage payments are most consumers’

largest expense, affecting the food they feed their children, if they vacation, even from which streaming services they need to unsubscribe.

Bringing borrowers into the lived life of their mortgage should be table stakes in 2024, especially as affordability wanes and the average age of first-time homebuyers increases. According to the National Association of Realtors (NAR), the median age of a first-time homebuyer in 2023 was 35, up from 31 in 2013 and 29 in 1981. For many of these buyers, a mortgage fits into a financial strategy already in place, rather than serving as the first step.

George asserts, “It is a substantially different way to look at loan servicing today, that really is putting the word ‘service’ back into loan servicing and the ability for borrowers to be able to see the added value of why they selected a particular company to do their mortgage.”

Most regulations in mortgage servicing are designed around the technologies available to facilitate compliance. Because laws are generally static, but technology constantly evolves, and by evolving reshapes consumer demands, regulations fail to evolve with emerging technologies and shifting demand, poisoning the well of innovation with cost and compliance burdens.

The complicated nature of these laws requires companies to juggle federal, state, and investor-insurer rules and regulations simultaneously. “There’s localized treatment of things that should in 2024 probably have a federal standard,” Thompson says. Yet, much of what binds servicers to some kind of standardization and transparency didn’t

even exist until a decade ago.

Michael Waldron, founding partner of Gate House Compliance, a mortgage advisory firm, and president of Compliability Solutions, says the servicing industry has improved its focus on customers since the passage of the Dodd-Frank Act in 2014 — data is used more strategically, for instance, by contacting borrowers at preferred times and in preferred languages. However, he acknowledges that reliance on outdated

technology hinders the progress servicers can make toward modernization.

“Regardless of how good the technologies are, we still have an industry that is laden with disparate systems,” says Waldron, who previously led the integration of a speciality servicing platform when he worked at Mr. Cooper Group. “That’s an issue that the industry has been fully aware of, and quite frankly, very focused on, particularly in the last five to seven years.”

The patchwork of technologies and regulations created in the years following the 2007-2008 mortgage crisis is fragmented and arcane. New avenues for loss mitigation arose from the Dodd-Frank Act, along with RESPA regulations. But, compliance with new regulations required servicers to develop new capabilities grounded in technology more than half-a-century old.

The idea of adding effective customer service is laughable, says Thompson. “That

Technology developed in the 1960s and 1970s remains the infrastructural core of servicing platforms in widespread use today. “We’re rejecting the use of the financial core as the cornerstone of our ecosystem, having data be our cornerstone because it’s 2024,” Thompson says.

type of customer service in the context of servicing does not exist, and there’s a lot of reasons for that,” she explains, “including the fact that servicing is running on 60-yearold infrastructure.”

In the aftermath of the mortgage crisis, Thompson was one of 16 independent consultants selected by the Office of the Comptroller of the Currency (OCC) and the Federal Reserve Board (FRB) to manage one of the legal teams conducting reviews of the deficient servicing and foreclosure practices of 14 mortgage servicers subject to the OCC and FRB’s Independent Foreclosure Review. This effort became a referendum on the future of mortgage servicing laws.

After her work with regulators, Thompson led Flagstar Bank’s default mortgage operations team for nearly a decade, heading up its mortgage-specific fintech accelerator program, too. In 2021, she launched Consigliera, a servicing-oriented organization connecting financial institutions and the fintech community. The depth and breadth of Thompson’s expertise in high-risk solution management, operations, innovation, and development is difficult to overstate.

Such experiences, though, have shaped her understanding that legacy technology impedes the modernization of legacy regulations, impeding innovation in a vicious cycle that harms people — and not just borrowers, but whoever’s on the receiving end of an irritated borrower’s phone rant.

“It’s the root cause of why the servicing industry sucks so bad,” Thompson insists. “These are blue-collar jobs. We pay people $55,000 a year to support their family and work in operations, which is a gajillion hours a week, with 60-year-old technology, and we ask them, ‘Why can’t you do it faster?’”

In her role as a quasi-regulator with the Independent Foreclosure Review, Thompson used to be that person demanding new tricks from an old dog — soundness from a tech stack pieced together with spit and glue.

“‘What the hell’s wrong with you servicers? Why can’t you do this? Why can’t you do that?’” she recounts. “The reason why I stay in this industry is because of the people, and I mean the people that don’t understand the asset that is homeownership, and all these people on the inside — and maybe more so them — that are fighting to help those consumers.”

Despite improvements, experts agree that the industry needs to take big steps forward. This happens with “the help and partnership of the regulatory community to allow for the advancements of technology to service the customers in the manner in which they want to be serviced, and to still do so compliantly,” Waldron believes.

As artificial intelligence (AI) rapidly advances and the impacts of escalating climate change wreak havoc on communities across the U.S., the servicing industry is trying to catch up at a time when it should be trying to get ahead. The industry can manage 2-4% delinquency rates, but high delinquency rates during the Great Recession were a warning sign, as were the rates caused by catastrophic natural disasters in 2017 and 2018 and the COVID-19 pandemic.

While the infrastructure to handle such events exists, the servicing industry’s ability to improve borrower engagement directly affects its success in mitigating losses when such events occur.

“If a massive tornado rips through the entire country and hits a bunch of big cities, we got a

Imagine a human hand. With legacy servicing platforms, the core financial technology — the part that takes and makes payments — is the palm. Technologies for processes like foreclosure, bankruptcy, invoice management, and customer communications attach to that palm like fingers. Removing the financial core would detach those pieces and cause the system to collapse.

lot of problems,” says Richey Mae’s Sprague. “I’m not sure that’s something we could ever plan for. But, we got through COVID. I kind of give the servicing industry a lot of credit for being able to do well by the borrowers, do well by the bond holders.”

As founding technologies grow increasingly outdated and the patches for adding new functionalities become more tenuous, the threshold at which a massive delinquency event could overwhelm the system drops. The crux of this dilemma is what Thompson calls the “infrastructure problem,” a data sharingcapacity failure compounded by the systems it supports.

Meanwhile, much consolidation has occurred in the servicing industry over the past few years. In late July, Mr. Cooper Group announced plans to purchase the servicing operations of Flagstar Bank, one of the largest residential mortgage servicers in the U.S. Expected to close in the fourth quarter of 2024, that transaction would boost Mr. Cooper’s servicing portfolio to more than $1.5 trillion, exceeding 12% of the $12.44 trillion of outstanding U.S. residential mortgage debt. Climate change presents a looming systemic risk to the entire housing system. The escalating impacts of extreme weather have already severely disrupted the affordability and availability of homeowners insurance in major housing markets like California and Florida. Mortgage servicers are and will

continue to be the front line of that crisis, directly engaging with affected borrowers.

“When that reaches critical mass, the ecosystem will be tested,” Thompson warns. “There’s a tipping point where these things can’t be supported anymore. These ecosystems that are running the American financial system, to replace them is essentially replacing your operation, which is why it’s that expensive and that hard.” To solve a small piece of the infrastructure problem is only to fragment the system further. The whole thing needs rethinking.

Imagine a human hand. With legacy servicing platforms, the core financial technology — the part that takes and makes payments — is the palm. Technologies for processes like foreclosure, bankruptcy, invoice management, and customer communications all attach to that palm, like fingers. Removing the financial core would isolate those pieces, causing the system to collapse.

Legacy systems can only be retrofitted, which becomes financially and technologically prohibitive. A longstanding reliance on the financial core has weakened the entire industry’s resilience to system shocks.

But, technology companies’ ability to innovate is always tied to the client willing to pay for the innovation sought. “The price is too big unless you are one of the biggest guys,” Thompson adds. “The macro economics of innovation in servicing is one of

the core reasons why I decided to go back to the operations side.” Building a de novo platform while bringing servicing in-house thrusts CMG into the future

Not too long ago, what kept Akinmade awake at night was fear that an Amazon-type company would decide to try mortgages. “The reason for it is our technology is so fragmented and so legacy and so archaic that we are poised to be disrupted.” Four years ago, he took over CMG’s technology strategy and began building an engineering arm with the aim of unifying the disparate aspects of the borrower journey: pre-application, application to funding, and servicing.

“It’s really, really critical to understand the data and technology infrastructure in servicing to understand why servicers are often so limited in terms of how they can connect with people,” Thompson says. “I will dance on the infrastructure problem until I solve it or I’m not in the industry anymore because I quit, and just say, ‘I give up! You people! We can’t fix this problem!’”

When a mortgage bank wants to bring servicing in-house, three-ish options exist. Option one is acquiring another lender that self-services and retrofitting the system. Option two is buying a suite of products offered by one of the two dominant providers in the

marketplace, Black Knight and Sagent, then filling in the gaps with other providers. Costs for these options are increasingly inflated as the founding technologies grow outdated.

A mortgage bank’s third option for bringing servicing in-house is building something novel. George hired Thompson and her team to build a bespoke servicing platform for a customer of one. Addressing “the infrastructure problem” meant re-orienting the relationship between CMG and its customers. Solving for “human connectivity” meant embedding, not affixing, borrowers.

Imagine another human hand. For the palm, Thompson’s team has developed a data warehouse — a data layer that translates into a single integrated location from the beginning of the servicing operation. Instead of 40 touchpoints, CMG’s platform integrates five or six primary technologies through the data layer, which acts like a switchboard for the end-to-end system.

“We’re rejecting the use of the financial core as the cornerstone of our ecosystem, having data be our cornerstone because it’s 2024,” Thompson says. Not tying CMG’s entire servicing operation to the financial core makes the platform more pliable, seamless. It’s databasedriven, and being so, ouroborates the head and tail of origination and servicing, the mortgage life cycle.

“When you look at technical innovation, we’re kind of on a growth of our maturity curve,” says Akinmade, who took control of CMG’s technology strategy four years ago and began building an engineering arm to unify disparate aspects of the borrower journey.

What Thompson’s team is building may be for a client of one, but not an industry of one.

“We’re not even trying to customize things with the providers we’re working with,” she explains.

“We’re sincerely hopeful that those providers we’re working with can re-commoditize what we’re building with them so that somebody else can use it, too. That’s the only way to orchestrate change in these types of industries.”

Say a worried borrower with $30,000 of revolving debt, a 720 FICO score, and a gigantic, looming tax payment, calls in to discuss an escrow assessment. That revolving debt typically would be invisible to the borrower’s point of contact. The option of a HELOC to reconcile the revolving debt and escrow shortfall becomes readily apparent, instead of a lump sum payment that the borrower can’t afford or an increase in principal and interest for the next 12 months.

In this scenario, CMG can solve a problem for the borrower before it becomes a problem,

monetize a transaction that can fund the technology, and create a better customer experience, without a net gain on cost — and even with potential net reductions on cost. From a business standpoint, that ought to fund a white glove, concierge servicing experience.

Thompson is unaware of any other large financial services companies that have a “modern gooey center that is completely driven off of data.” Some are getting close, thugh. “The reason we’re doing that is because we want to give ourselves the best chance to survive,” she says. When better technology comes along, they can “flip out” that data core of the ecosystem.

“You’re going to get smacked in the face with branches,” added Akinmade, likening their task to navigating through a jungle. “You got a dull machete. You got to walk for miles. It’s not forgiving. It’s not for the faint of heart and you’re going to get sick along the way. But, if you get to the end, you will have charted a new path.”

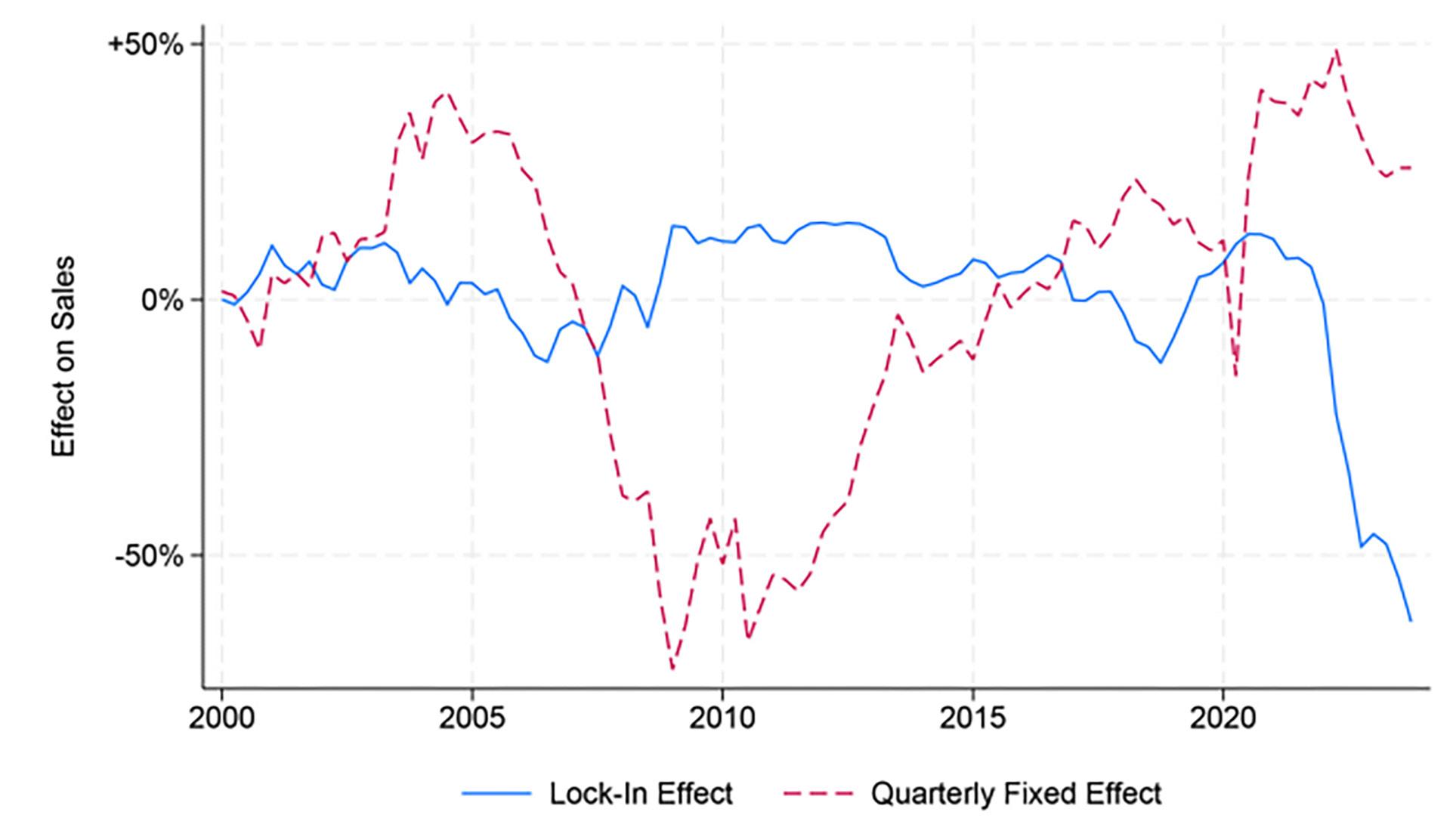

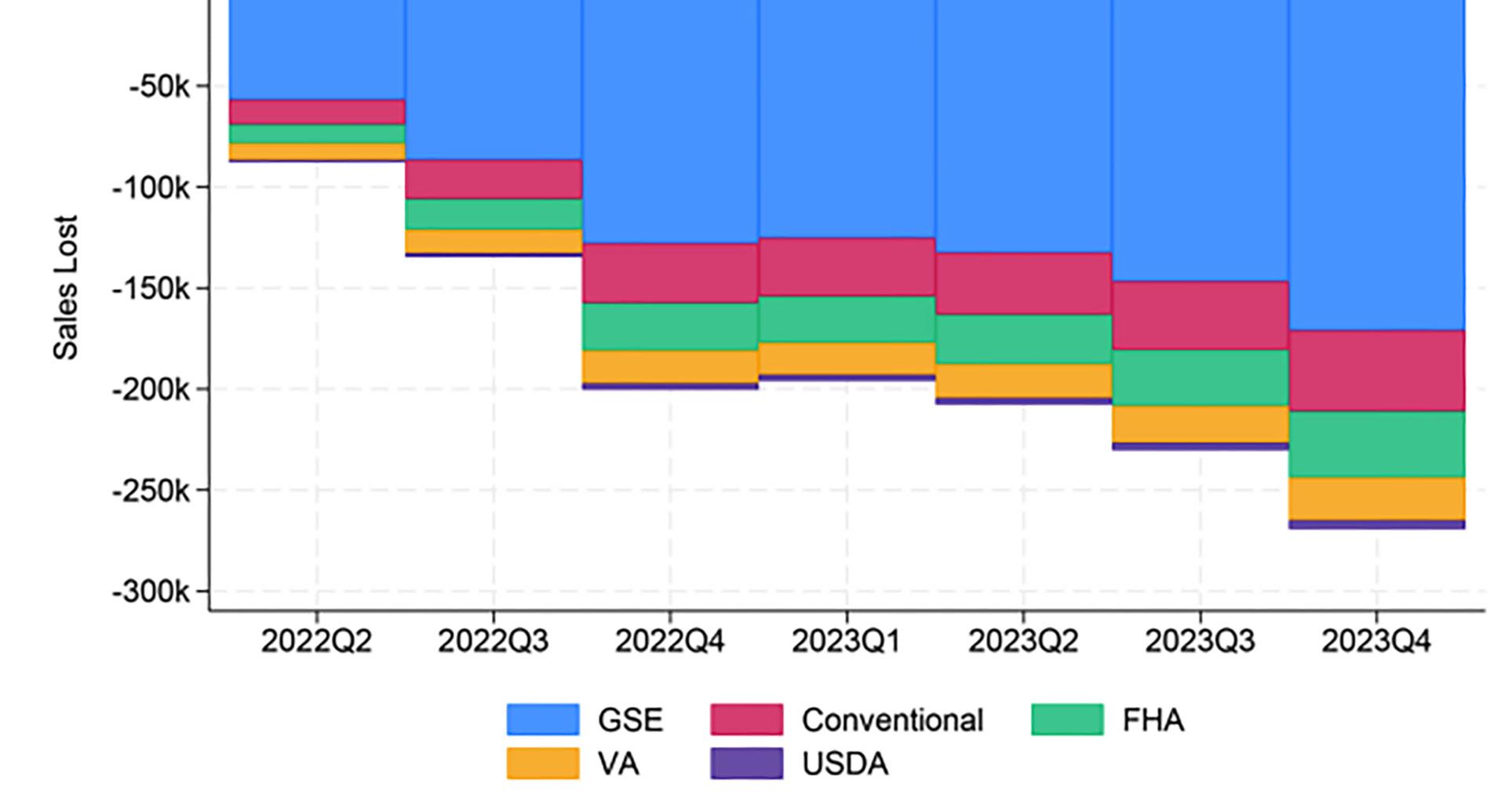

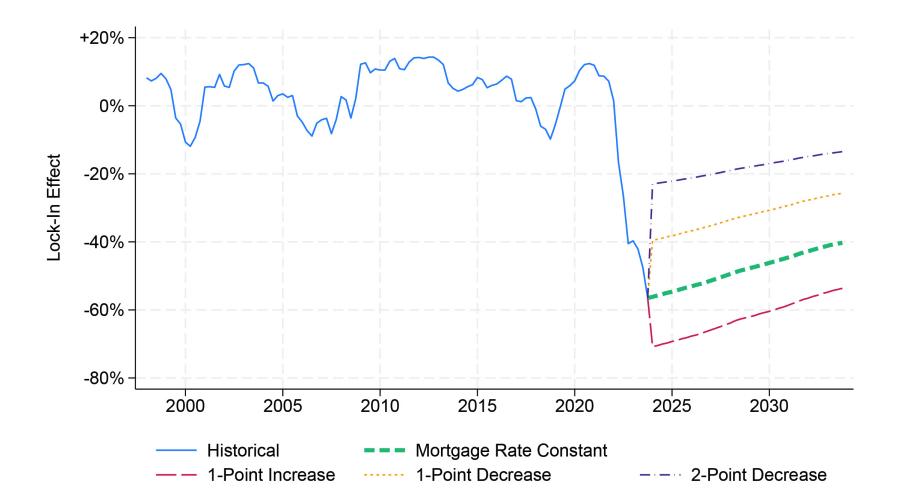

Business lost to ‘lock-in effects’ will compound for years, warns a team of FHFA economists

BY RYAN KINGSLEY , EDITOR , MORTGAGE BANKER MAGAZINE

You could see a lot in the popular press discussion about this phenomenon,” says Jonah Coste, explaining the exigence of his team’s efforts to measure the impact of roughly three-quarters of U.S. homeowners clinging to mortgages under 5%, hamstringing home sales and exacerbating inventory shortages. “It was always hypothesized and not really quantified.”

That is, until recently. At the end of the first quarter of 2024, a team of Federal Housing Finance Administration (FHFA) economists published research detailing their expectations for long-term “lock-in effects” stemming from a rapid increase in mortgage rates after millions of ultra-low mortgages were originated in 2020 and 2021.

In an interview with Mortgage Banker Magazine, edited and condensed below for concision and clarity, Coste and his colleagues discussed the implications of their findings, the knock-on effects likely to impact the broader economy, opportunities for mitigating lock-in effects, and the need for industry input in addressing this issue.

Jonah Coste is an economist at the FHFA and spear-headed the team’s research. Dr. Michael Seiler is a full-time professor at the College of William and Mary in Williamsburg, Va., and a visiting scholar at the FHFA. Will Doerner is a supervisory economist in the FHFA’s Division of Research and Statistics. Ross Batzer, a senior FHFA economist and the fourth member of the team, was unavailable at the time of the interview.

Q:What was the central question that you set out to answer with this research?

JONAH COSTE: The first was just quantifying the exposure to lock-in. As of the end of last year, the average active mortgage was 3.2 percentage points lower than what they could get on the same mortgage at that time in the fourth quarter. You can also look at it in a dollar amount. It’d be about $500/month, and additional payments if they had to remortgage, which is about 40% higher principal and interest payments. Or, you can look at the total present value of those increased payments, which is about $60,000 for the average mortgage holder.

The second was asking, how sensitive is the average on average, and then various different groups to being locked in, in terms of their propensity to sell their home? About every percentage point of lock-in reduces your likelihood to sell by about 18.1%. People in more expensive homes are more sensitive than those in less expensive homes. After controlling for affluence across the expensiveness of your

house and income and credit score, et cetera, non-white borrowers — Asian, Hispanic, and Black borrowers — are all more sensitive than white borrowers. For those three non-white groups, it’s about 22%, versus like 16% for white borrowers.

The third point was, can we get an aggregate effect? That’s just applying those sensitivities to the path that mortgage rates have taken and the path of the stock of existing mortgages, and we find that 1.3 million sales have probably been lost due to this since rates started ticking up in 2022. That’s getting added to every quarter now, 200,000 to 250,000 each quarter.

The final point is that the supply reduction due to this lock-in effect is dominating the direct effect of interest rates on home prices. Since we’re coming off such low rates, the increased rates are not only reducing demand, but they’re creating this lock-in which is decreasing supply. At least in the short run, we’ve shown that the supply effect can dominate. The best we can tell is it’s something like a 5% or 6% increase in prices due to the supply reduction compared to only

about a 3% direct-effect decrease in prices due to the higher interest rates, that demand effect.

Q:Were there certain loan types or loan products that the lock-in effect becomes more pronounced with?

You’re talking about the higher-priced homes, can you attach that to conventional or FHA borrowers being more or less sensitive to the lock-in effects?

JONAH COSTE: We don’t see a lot of heterogeneity across things like loan attributes. Now, we do see very different baseline rates of sales across these things. A home with a 15-year mortgage has a higher baseline propensity to sell than someone who would buy it with a 30-year mortgage. But, both of them decreased by about 18% for each percent of lock-in. The heterogeneity we really see is more on borrower attributes, and like I said, affluence is a big one, and it seems that of the measures of affluence, it really seems that home value is the biggest driver there. You see it show up a little bit with credit scores and with income measures, but the effect is largest

on home value. And then the second thing is race, where after accounting for those measures of affluence, the non-white groups seem to be much more sensitive than the white group.

WILL DOERNER:

If you break it down by loan type, like what you’re asking, we’re still getting a really strong effect across all of those segments. It’s not something that disappears if you don’t focus on Fannie-Freddie loans if you focus on other loan types. It’s not something that disappears if you focus on borrower incomes and different kinds of affluence of borrowers or their ages or how much DTI or how much down payment they’re putting in — across all of those categories you’re going to get well over 10% effects. When Jonah was talking about that 18% effect, most of the cuts that we have are above 15%. That’s why we think this is such an important paper to bring up because we can get at this nationwide, not just with Fannie and Freddie loans, but with loans across the country and talk about how different segments are impacted differently.

ELIMINATING AGGREGATE EFFECTS OF LOCK-IN

MODELED EFFECTS OVER TIME

SALES LOST TO LOCK-IN BY QUARTER

JONAH COSTE: