LOVE AND LOANS HOW LOVE AND LEGACY DRIVE LUND MORTGAGE

POUR DECISIONS

TURNING DOWN DRINKS AND TURNING UP SUCCESS

GOING SMALL TO GO BIG

THE BOUTIQUE APPROACH TO MORTGAGE LENDING

LOVE AND LOANS HOW LOVE AND LEGACY DRIVE LUND MORTGAGE

POUR DECISIONS

TURNING DOWN DRINKS AND TURNING UP SUCCESS

GOING SMALL TO GO BIG

THE BOUTIQUE APPROACH TO MORTGAGE LENDING

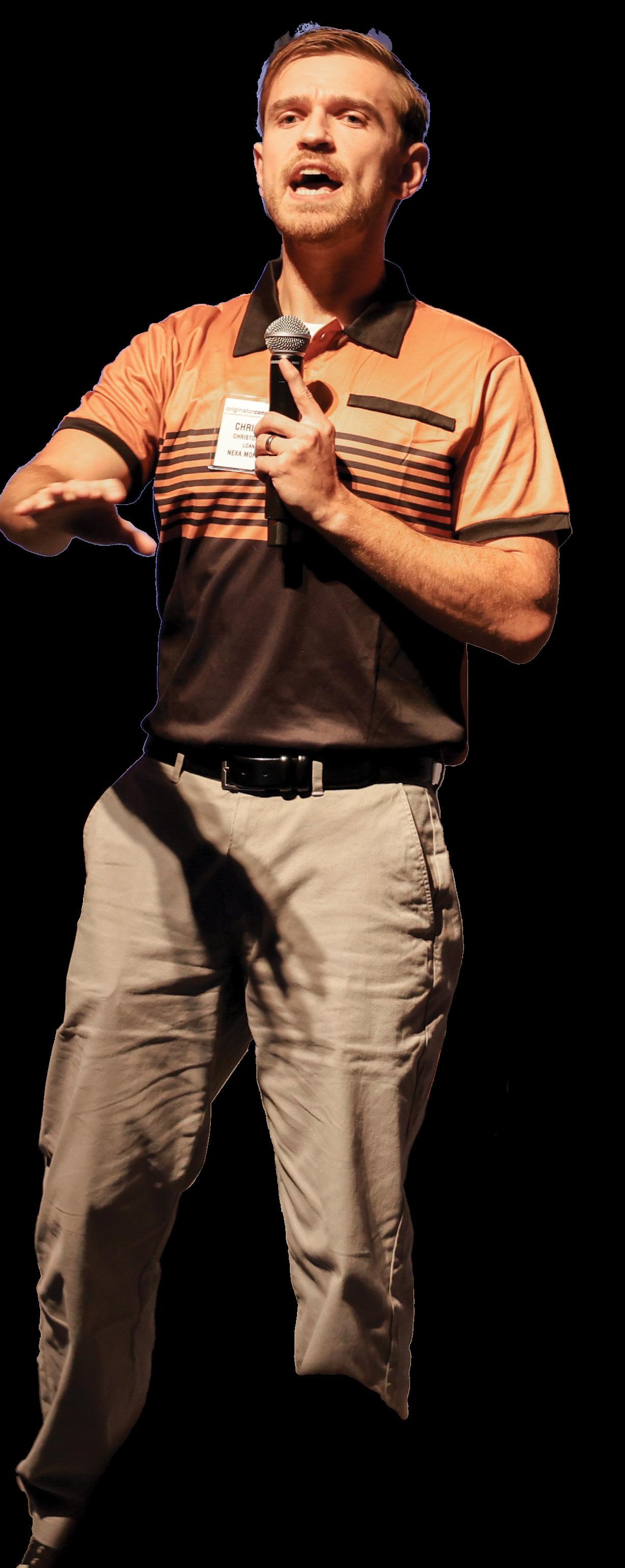

With a heart for heroes, CHRIS SHANK’S commitment to veterans fuels his new career path

LOVE AND LOANS HOW LOVE AND LEGACY DRIVE LUND MORTGAGE

POUR DECISIONS

TURNING DOWN DRINKS AND TURNING UP SUCCESS

GOING SMALL TO GO BIG

THE BOUTIQUE APPROACH TO MORTGAGE LENDING

With a heart for heroes, CHRIS SHANK’S commitment to veterans fuels his new career path

Just six months in, Chris Shank, a disabled veteran turned loan officer, whose commitment to giving back is making a monumental impact on the mortgage industry. From an emotional pledge of $1,000 at the Originator Connect conference to his passion for empowering fellow veterans, Shank’s journey is a testament to resilience and purpose. Explore his inspiring journey from military service to mortgage lending and how he’s making a meaningful impact along the way.

46 TYING THE KNOT AND CLOSING THE DEAL

Matt Oliver and Lisa Lund transformed a challenging industry landscape into a thriving mortgage business. From their serendipitous meeting at the Phoenix Open to weathering financial storms hand-in-hand, explore how their love story and professional journey shape their client-first philosophy and the enduring legacy they aim to create.

Tuning Out Market Mayhem

With interest rates and housing trends in constant flux, it’s easy to get lost in the data storm. Here’s why the best strategy might just be staying grounded, focused — and unfazed by the noise.

8 Transforming Challenges into Checkmarks

As the commission game shifts, those who adapt and educate find a new path to prosperity.

12 Bringing New Moves To Mortgage

Expand your professional toolkit by adopting tech, marketing, and leadership strategies from beyond mortgage. 16

Cutting Through The Cost Barrier

How strategic insurance and tax toves are keeping borrowers in their homes.

People on the Move

See who the movers and shakers are in the mortgage industry. 22

Your First Million Dollars: The Write Way Forward

How reading fuels personal growth. 26

Benchmarks And Best Practices: From Stress Test To Success Quest

Take a moment to reflect on this year’s successes and explore strategies to tackle stress as we look toward a stronger 2025.

Small Scale, Big Impact

Where big lenders push for volume, boutique firms focus on custom fits and borrower relationships. 36

Sober Success

Sobriety as a strategy: How clear thinking leads to better business decisions.

Directory 78 Facebook Thoughts: You Spin Me Right Round, Baby (At 3 A.M.)

62

Best Military Lenders 2024

These lenders go beyond the bottom line, honoring our heroes by helping them find homes. Celebrate those who make serving military families their greatest achievement.

66

Best Military Originators 2024

These originators make it their mission to serve military members and veterans. Read how their dedication turns finding homes for heroes into a meaningful calling.

70

Most Loved Employers 2024

Mortgage companies put to the test by their own teams. Discover who earned top marks for culture, benefits, and community impact — voted Most Loved by their employees.

Vincent M. Valvo CEO, PUBLISHER, EDITOR-IN-CHIEF

Beverly Bolnick ASSOCIATE PUBLISHER

Erica Drzewiecki, Katie Jensen, Ryan Kingsley STAFF WRITERS

Dave Hershman, Erica LaCentra, Harvey Mackay, Lew Sichelman, Mary Kay Scully CONTRIBUTING WRITERS

Alison Valvo DIRECTOR OF STRATEGIC GROWTH

Julie Carmichael PROJECT MANAGER

Melissa Pianin MARKETING & EVENTS ASSOCIATE

Navindra Persaud DIRECTOR OF EVENTS

Meghan Hogan DESIGN MANAGER

Stacy Murray, Christopher Wallace GRAPHIC DESIGN MANAGERS

William Valvo UX DESIGN DIRECTOR

Krystina Coffey, Matthew Mullins MULTIMEDIA SPECIALIST

Andrew Berman HEAD OF CUSTOMER OUTREACH AND ENGAGEMENT

Kristie Woods-Lindig ONLINE ENGAGEMENT SPECIALIST

Joel Berman FOUNDING PUBLISHER

Interest rates are going up. Nope, interest rates are going down. Home sales are declining, except in areas where they’re increasing. The rental market is strong, making mortgages attractive, just not where the rental market is softening, making apartments a better alternative to houses.

It’s all noise. And frankly, maybe the best idea is to just tune it all out.

As a news organization, we’re inundated daily with surveys, data reports, analyses, predictions, commentary, and prognostications about the state of the mortgage industry. Here’s the rub: almost all of it is right, but almost all of it is also wrong. It all depends on where and when and what’s coming. A market could surge for a few months, only to be faced with some disappointing news, and then it’s on a backward slide. Pretty much every originator already knows that interest rates this morning are no guarantee of interest rates this afternoon.

We’re not advocating paying no heed to actionable information. But being drowned in a deluge of data does no good, either. The rational course of action is to listen to enough knowledgeable sources to understand the general drift of the market. Then make plans that capitalize on your own unique skills and talents.

Has this been a bad market? For many, of course it has. But our pages have been filled with stories of originators and broker shops that have hit records this year. Those folks tuned out the noise. They didn’t get distracted or depressed by information they didn’t like. They looked at the market with as much clarity as possible, then they put their plans into motion. Purchases coming up short? Home equity and renovation loans to the rescue. Millennials locked out of the market? Time to build boomer business by figuring out the rules of reverse mortgages. Trigger leads not working? Divorce filings and new business formations can build a new database.

Our cover story this month is about a guy who hasn’t done much yet. His name is Chris Shank, and we met him at the Originator Connect conference in Las Vegas in August. Chris decided to get into the mortgage origination game this year, of all years. But he made a mark at the event by literally getting on stage in front of everyone and telling them how much he loved being an originator. Enough with the Eeyore faces, he all but said. Come at this like a winner — clients love to work with winners! Keep your attitude positive, put a smile on your face, make every connection you can, and be smart about the products you offer. Business will build.

But first, tune out the noise.

VINCENT M. VALVO Publisher, Editor-in-Chief

Submit your news to: editors@ambizmedia.com

If you would like additional copies of National Mortgage Professional, call (860) 719-1991 or email subscriptions@ambizmedia.com www.ambizmedia.com

EBY DAVE HERSHMAN, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

very change brings challenges, but it also brings opportunities. Those who are willing to change and take advantage of the opportunities will be those who not only survive, but also prosper. It reminds me of the tremendous blow to the markets during the Great Recession of 2008. So many loan officers and real estate agents left the industry. But some agents decided to specialize in short-sales and foreclosures. And after a while, rates moved down enough that refinances started to take off. Of course, with refinances again in vogue, many loan officers tried to come back in the industry — we called them rebound loan officers. Similarly, those who were foreclosed upon also came back into the market years later to purchase again (rebound buyers).

So, what are the opportunities this new “commission regimen” could bring our way?

• Education. I don’t care how much on-line information is out there, the average consumer tends to be fairly clueless about the real estate and mortgage process. And many real estate agents are certainly in need of education as well. Now we have just made the process more complicated. Before it

was easy — the seller paid the commission (though the buyer really pays it). Now we have added another option.

Loan officers who are successful give their prospects more options and then they educate them on these alternatives. That is what separates a salesman from a trusted advisor. More options demonstrate that the process is more complex than just shopping for a rate on a 30-year fixed mortgage. Thus, this is an opportunity to present more options and further educate the consumer and the agent on the paths they might take.

• Timing. In the mortgage business, any top producer can tell you that the earlier you get in front of a prospect the better. If you talk to them before they even start house shopping, you can develop a relationship and add value to their lives. That value might include helping them with their credit, making sure they are looking within the right housing price range or even introducing them to a real estate agent or another vendor partner.

Well, the option we just added to the equation makes it even more imperative for the agent to refer the prospect to you before they look at houses. The agent needs to know

Those who are willing to change and take advantage of the opportunities will be those who not only survive, but also prosper.

whether the buyer definitely will need to request that the seller pay the full commission which is due. That is too big an issue to leave to the last second.

Thus, your education needs to start with the agents because this change is new to them, and they need your help more than ever in this regard.

As I have said: every change begets opportunities. Some will look at this change and head for the hills. Others will assess the situation and find out

how other successful industry players are reacting. This change will not mean an end to the industry by any

means. People will still need the guidance of an agent to help them find the right home and negotiate the process. And with a shortage of homes in America, there will be plenty of demand. ■

Dave Hershman is the top author in this industry with six books published as well as the founder of the OriginationPro Marketing System and the OriginationPro’s on-line comprehensive mortgage school. His site is www.OriginationPro.com and he can be reached at

dave@hershmangroup.com

AREA OF FOCUS: Nationwide Real Estate Valuations Management — An Appraisal Management Company

DESCRIPTION OF PRODUCTS OR SERVICES: Licensed in all 50 states, plus D.C., PCV Murcor provides nationwide appraisal management and valuation advisory for residential and commercial real estate. With a foundation built on 43 years of experience, PCV Murcor brings a deep understanding of our clients’ goals that complements appraisal modernization. Our use of state-of-the-art AI technology ensures precision and efficiency in every aspect of our service. Experience innovationpowered recision and time-tested excellence with unparalleled service and cutting-edge products.

pcvmurcor.com sales@pcvmurcor.com (855) 819-2828

visit expotrac.com or scan this code

Find the full AMC list on page 77

Registration management

Simplify & speed up check-in

Track attendance

Unlimited attendees

Priced for your specific needs

Up to 15 custom fields

Create custom badges

Cloud-based software

Personalized support

producers.

ExpoTrac was developed and tested by event producers, creating a tailored product that does exactly what it needs to: check people in quickly, and make it easy to manage. We traveled the country, using ExpoTrac at more than 60 of our own events so that we could design a system that not only works for us, but that we know will work for you, too.

No more hauling around large trays of name badges. No more hiding badges that haven’t been claimed. No more cumbersome lastminute changes to someone’s title, company or name. Our cloud-based system makes it all easy, simple and fast. And even better, you can run this system with one small printer and one laptop — and then add more users instantaneously as demand picks up at various times of the day.

There is simply no other faster, simpler, agile and economical badge printing system on the market today. We stand behind it, because we use it every day.

TBY ERICA LACENTRA, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

he mortgage industry can be a very nuanced space to grow your career. It is imperative for mortgage professionals to constantly seek continuing education efforts to stay up to date on changes and trends in the industry and new regulations that could have a direct or indirect impact on their business. While there seems to be no shortage of educational resources and events geared towards the mortgage industry, depending on your role in this space, there may come a point where you feel that the mortgage industry may be failing to provide you with certain resources or areas of education. When you feel like you aren’t quite on the cutting edge, it may be time to look to other industries to boost your knowledge. So, in what areas of your professional development should you seek insight from other industries?

Technology in the mortgage industry has come a long way over the years. So many softwares and systems have incorporated AI and other automation tools into their platforms

to allow companies to operate more efficiently. However, compared to many other industries, the mortgage industry’s technology is only scratching the surface. Looking at industries like telecommunications, manufacturing, and healthcare and the advancements they are making can be eye-opening and hint towards the future of mortgage technology innovation.

While you may think that certain technologies may not ever have an application in mortgage and it can be hard to wrap your head around how that tech could be integrated into our space, at a basic level, it can help to see how comparable industries are leveraging things like AI and automation to improve their businesses. Seeing how the banking and insurance industries, to name a few, are leveraging technology in their underwriting, compliance, and more can be a great source of inspiration for how you can incorporate similar tech into your workflow.

I will be the first person to admit that when it comes to

marketing in the mortgage industry, our space is probably at least three years behind other industries when it comes to marketing innovation. As a marketing professional in this space, it can be frustrating at times to see other industries’ marketing advancements as the mortgage space slowly plays the game of catch-up. While there are many mortgage companies at the top of their marketing game, and they can be great sources of inspiration for your efforts, I think even their marketing teams would argue there is more work to be done to bring mortgage marketing techniques up to the levels you see in other sectors.

Doing research into how other industries are pioneering the way in social media marketing, con-

tent marketing, digital marketing, marketing automation, and more can really help to fill any deficiencies you are seeing in your marketing strategies. Also, attending content and marketing-centric events can be hugely beneficial because these events typically cover use cases and marketing strategies across numerous other industries. At a core level, marketing typically is either B2B or B2C so while the audiences may be different, certain techniques can be universally applicable. Being able to see the possibilities in one setting and discussing with marketing professionals from other sectors how their techniques could

apply to your own strategy could help take your marketing to the next level and well beyond the likes of your competitors in the mortgage space.

One of the final areas where it can often be beneficial to seek guidance outside of just the mortgage industry is leadership training and development. While the mortgage industry has no shortage of tremendous leaders, there is no one right style of leadership. Seeking inspiration from leaders in other industries can help you find the best way to develop your own path.

top that can provide insight into all of the steps they took to get there and how you can apply that to your career. Some books to start with include “Principles” by Ray Dalio, the CIO of Bridgewater Associates, “Grinding it Out” by Ray Kroc, known for making McDonald’s what it is today, and “The Cobbler”, by Steve Madden, American fashion designer and founder of Steve Madden, Ltd. All of these individuals have had success in

are at the top of their games.

When it comes to marketing in the mortgage industry, our space is probably at least three years behind other industries when it comes to marketing innovation.

One of the easiest places to start is doing research into which professional leaders inspire you or mirror a leadership style that you would like to emulate and see if they have books or educational content that you can dig into. Many influential executives have incredible biographies or autobiographies about their rise to the

very different industries so it can be fascinating to learn about commonalities and differences in their strategies and leadership styles.

You may also want to consider joining a leadership mastermind group that can connect you with other like-minded individuals from numerous other industries. Building your network, collaborating, and commiserating with other leaders can help you identify what you are doing well and where you can implement the best practices of others who

The mortgage industry has its own strengths and can certainly provide industry professionals with robust educational resources to ensure they remain up to date on trends in the space. However, there is nothing wrong with seeking information and insight from other industries that may excel in the areas that the mortgage space is lacking. The most important thing is to take back the knowledge you’ve gleaned from other industries and not only apply it in your own professional life but also share it with your colleagues. This forward-thinking will not only help you improve your own career but also help propel the industry forward.■

Erica LaCentra is chief marketing officer for RCN Capital.

Borrowers underwater with taxes and insurance can be a default risk. Helping them is critical.

EBY LEW SICHELMAN, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

very third call Craig Eagleson answers these days is from a befuddled lender or loan servicer who asks essentially the same question: “Can you help me lower my client’s debt-to-income ratio” so they can qualify for financing or rescue him from falling into foreclosure.

Fortunately, Eagleson, who heads Incenter Insurance Solutions, often can help. And so can Alison Tulio, who runs Incenter Tax Solutions. Their companies are two members of the Incenter Lenders Services family of firms that help lenders maximize their operational performance and find new growth paths.

(A third Incenter company, CampusDoor, provides third-party, back-end private student loan solutions, including both origination and refinancing, so lenders can consolidate multiple loans into one and help qualify more borrowers. But that’s a story for a different month.)

With double-digit increases in both homeowners’ insurance and property taxes stymying many a would-be homeowner as well as pushing bunches of current owners into default, what these two executives and their staffs do has risen in

importance, thrusting them to the top of the heap when it comes to solving lenders and servicers problems.

This isn’t meant to be a commercial for the Incenter affiliates. There are plenty of other firms, both national and local, which do the same. And consumers can do most of the legwork on their own to trim their insurance premiums and lower their property tax. But the services Eagleson and Tulio provide have become invaluable, especially in light of the difficulties many buyers are having in qualifying for financing so they are worth a closer look.

Incenter Insurance is basically a national insurance broker that’s licensed in all 50 states. On the personal insurance side, the company deals with nearly two dozen carriers; on the commercial side, 33. It deals directly with consumers, offering complimentary reviews of their current or — and this is important to people trying to buy a house — potential policies in hopes of identifying less expensive options.

Estimates vary, but experts say that anywhere from 30 percent to 60 percent of all property is over-assessed.

Lenders and servicers use the company’s services, too. And they can also “White Label” an embedded link into their platforms that enables borrowers to click through to Incenter Insurance’s site, where they can quickly search for policy alternatives on their own. Borrowers are not charged anything, but the hope, of course, is that they will allow Incenter to place their coverage.

It works something like this: During a one-on-one consult, agents take all the pertinent information to help determine the appropriate coverage, not just for cost but also for exposure to risk. Armed with that, the agents then shop for quotes. “We don’t try to shortchange it,” says Eagleson. “We build policies based on the best value. Our job is to find the best fit. If we can save the client money, great. But if not, we explain why the (more expensive) policy offers the better coverage.”

Incenter Tax works essentially the same way in that it offers consumers the opportunity to lower their property tax stipends, again at no cost. If,

after reviewing the latest assessment, the company determines there is a reason to appeal, it offers to handle the process on the property owner’s behalf for a one-time contingency fee.

The company works through 10,000 appraisers and attorneys nationwide who review the client’s assessment. If the company wins the appeal — and it boasts a 93 percent success rate vs. the 60 percent rate among consumers who handle the process on their own — it takes half of his first year’s savings. But every year thereafter, the savings will be all his, at least until the property is reassessed.

The company works directly with consumers. And like Incenter Insurance, its platform can be private-labeled on lenders’ and servicers’ platforms, where consumers can be just one extra click away. Obviously, property taxes are based, in part, on the most recent sales price. Consequently, there is little a buyer can do to lower the tariff until he takes occupancy. So Incenter Tax won’t be much help in qualifying buyers for loans. But it can be a big help to owners of all ilk, including those facing financial difficulty.

CEO Tulio tells me it trims its residential clients’ tax bills by about $4,600, on average.

Okay, that’s the plug. Now let’s get down and dirty with information to help your clients cut their insurance costs and property taxes all by their own selves:

• Property taxes — Estimates vary, but experts say that anywhere from 30 percent to 60 percent of all property is over-assessed. Better yet, as long as homeowners follow the rules regarding deadlines and other requirements — every jurisdiction has its own criteria — the appeals process is relatively simple.

Borrowers should start by doing the math. Multiply the tax rate — say $1.50 per $100 of assessed value — times the home’s assessed value. So if the place is valued at $300,000, the tax should be $1.50 times 3,000 or $4,500. If the arithmetic is incorrect, the tax man will have no choice but to recompute.

Next, they should look for errors in the assessor’s description of the property. Your client may be down for four bedrooms when he has only three or one acre when he has only half that. Any discrepancy in his favor will likely lead to a lower assessment.

Another way to trim insurance costs is by raising the deductible to an amount the insured can comfortably afford should he have to file a claim.

The higher the deductible, the more the savings.

Tell him to ask for a copy of his assessment record, aka work-

sheet or appraisal card. Every property has one and everyone has a right to see theirs. The record will list everything the assessor believes contributes to value: location, size, amenities, and so forth. Mistakes are not uncommon and it’s the borrower’s job to make certain everything is correct.

Next, he needs to gather ammunition to prove the property has been assessed unfairly. Like properties should carry like assessments, so he wants to make sure the house is assigned the same value as similar properties in the area.

Here, owners will need to find out what properties the assessor used for his comparisons. Then, they need to check them out to see how they differ. One might have a two-car garage, for example, and their place has only a carport. Or one might be all brick while theirs is of wood-frame construction clad in aluminum siding.

Another option is to have the property appraised by a professional to see how it stacks up to the assessor’s comparables or five to 10 others that are identical to theirs or nearly so — same model, lot size, improvements, upgrades, and finishes. Then look for any and all differences that make their house less desirable.

• Homeowners Insurance — First and foremost, borrowers need to shop ‘til they drop — every year, the experts recommend — and narrow their choices to the best three based on their price ranges, the breadth of their coverage, the quality of their services, and their financial stability. Once they get to that point, they should ask for specific price quotes. But they must be certain they are com-

paring apples to apples, with the same coverages and deductibles.

When they are placing a value on a property, owners should make sure they don’t include the value of the ground it is sitting on. The land a house is on is not at risk.

When they are placing a value on a property, owners should make sure they don’t include the value of the ground it is sitting on.

The land a house is on is not at risk.

Another way to trim insurance costs is by raising the deductible to an amount the insured can comfortably afford should he have to file a claim. If the owner can jump his deductible from $500 to $1,000, for example, he can trim his premium by as much as 25 percent. The higher the deductible, the more the savings.

Borrowers should also consider bundling their homeowners’ policies with their automobile and other coverages with the same carrier. If they have two or more policies, they might be able to cut their premiums anywhere from 5 percent to 15 percent. But they should make sure the combined price is lower than separate policies with different carriers.

Another tip: Owners should ask their insurers what they can do to make their houses more resistant to natural disasters. Adding storm shutters or reinforcing a roof also may be able to save some money.

They should also ask about discounts

for smoke detectors, burglar alarm systems, and dead-bolt locks. Some companies offer discounts of up to 20 percent. Price reductions also may be available if the insured is retired. If someone is at least 55 and no longer working, as much as a 10 percent discount is available through some companies.

Establishing and maintaining a good credit record can cut costs as well. Insurers almost universally use credit scores to price their policies. So advise your borrowers to pay on time, not to use more than 30 percent of their credit limits, and otherwise keep their financial noses as clean as possible.■

Lew Sichelman is a contributing writer to National Mortgage Professional magazine. He has been covering the housing and mortgage sectors for 52 years. His syndicated column appears in major newspapers throughout the country.

> Pennymac announced that William Chang will step down from his roles as Senior Managing Director and Chief Capital Markets Officer at PFSI, and Senior Managing Director and Chief Investment Officer.

> CRM platform Aidium recently appointed Tony Farnsworth as vice president of sales. Farnsworth is set to spearhead Aidium’s sales strategy.

> Former Venmo executive Papanii Okai was named as Rocket Companies’ Executive Vice President (EVP) of Product Engineering.

> Assurance Financial tapped Jim Clapp for the newly created role of Chief Lending Officer (CLO). Clapp is slated to lead Assurance Financial’s lending strategy.

// YOUR FIRST MILLION DOLLARS

Our lives basically change in three ways; through the people we meet, the places we travel, and the books we read.

I made that statement many years ago, and I still believe it today.

Television, computers, the Internet and even radio were supposed to be the

> Ken Wingert has joined the National Association of Home Builders as Chief Advocacy Officer.

BY HARVEY MCKAY, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

replacement for conventional books when each first became popular. But more books than ever are being published, and more copies are being sold.

In fact, a whiz-kid remarked smugly to his professor, “The book will soon be completely replaced by the Internet.” “Really?” the professor said. “Then

> Lisa J. Haynes is officially retired after a 10-year tenure at the Mortgage Bankers Association, the former Senior Vice President, Chief Financial Officer, and Chief Diversity and Inclusion Officer confirmed.

where will you get a book on how to fix your computer?”

Inscribed on the Thomas Jefferson Building at the Library of Congress are the first eight words of this quotation by Henry David Thoreau: “Books are the treasured wealth of the world and the fit inheritance of generations and

> Katie Johnson is stepping down as chief legal officer for the National Association of Realtors (NAR0. Johnson also served as NAR’s chief membership experience officer since March 2023.

> Acrisure has appointed Robin Benoit as its Chief People Officer. Benoit has served in this role in an interim capacity since March 2024.

nations. Their authors are a natural and irresistible aristocracy in every society, and, more than kings or emperors, exert an influence on mankind.”

National Book Month is held each October. The month-long celebration focuses on the importance of reading, writing, and literature.

Norman Cousins was one of America’s most famous editors. He ended his career teaching medical students, when he wrote this about books: “There is a simple non-medical technique for in-

creasing longevity. This system goes by the name of ‘book.’ Through it, man can live hundreds of lifetimes in one. What is more, he may enjoy fabulous options. He can live in any age of his choosing. He can take possession of an experience. He can live inside the mind of any man who has recorded an interesting thought, any man who has opened up new slices of knowledge, any man who has engaged in depths of feeling or awareness beyond the scope of most mortals. This is what good books are all about.”

When it comes to personal growth, books are a treasure trove of knowledge, insights and wisdom that can

> Wells Fargo & Company named Elena M. Gallo as Government Banking Division Executive. Gallo succeeds Mara Holley, who is retiring after leading Government Banking since 2015.

> Sridhar Sharma will assume the role of Executive Vice President and Chief Innovation and Digital Officer at Mr. Cooper. Sharma led Mr. Cooper’s development of Pyro AI.

> Mr. Cooper welcomed new Senior Vice President and Chief Technology Officer Jeff Carroll to oversee its core technology infrastructure operations.

HAVE A NEW HIRE OR PROMOTION TO SHARE?

Submit the information to editors@ambizmedia.com for possible publication. Announcements should include a headshot.

By learning from the experiences and advice of others, you can develop a toolkit of techniques for navigating obstacles in your own life.

help shape our perspectives, improve our skills, and inspire us to become better versions of ourselves.

Here is why reading is so crucial for personal development:

Expands your perspective. Books open you up to new cultures, philosophies and ways of thinking. By exposing yourself to a broad range of topics and authors, you can challenge your preconceptions and gain a more nuanced understanding of the world.

Enhances self-reflection. Reading about characters, situations, or ideas can prompt you to reflect on your own life, values, and behaviors. This self-reflection is a key component of personal growth, as it can lead to greater self-awareness and a clear sense of your goals and priorities.

Improves problem-solving skills. Many books, especially those focused on personal development, provide strategies for dealing with challenges. By learning from the experiences and advice of others, you can develop a toolkit of techniques for navigating obstacles in your own life.

Boosts creativity. Reading stimulates the imagination, encouraging you to think creatively and explore new possibilities. This can be particularly valuable in personal development, as it enables you to envision and pursue goals that you might not have considered otherwise.

Builds knowledge. At the most basic level, reading is a powerful way to acquire knowledge. Whether you’re learning about psychology, health, productivity, or any other topic related to personal growth, books can provide you with the information you need to make informed decisions about your life.

Enhances communication skills. Reading regularly can also improve your vocabulary and comprehension, which in turn can enhance your communication skills. Being able to articulate your thoughts clearly and persuasively is a valuable asset in both personal and professional growth.

In my own life, I’ve found that reading has been instrumental in shaping my understanding of business, leadership,

and human behavior. Books like Dale Carnegie’s “How to Win Friends and Influence People” and Stephen Covey’s “The 7 Habits of Highly Effective People” have not only informed my professional practices but have also influenced my approach to personal relationships and self-improvement.

As the author of seven New York Times bestsellers, I unashamedly promote the value of books — largely because of the effect that books have had on my life and career. I could never personally see or hear all the authors who have influenced me, but their written works fill my bookshelves and hard drive. And I can revisit them at my convenience.

Truly, books are a gift that keep on giving.

Mackay’s Moral: Leaders are readers. If you want to continue to grow and develop, make reading a non-negotiable part of your daily routine. n

Harvey Mackay is a seven-time New York Times best-selling author with 15 books.

Creating a space for the next generation in NMLS education.

Introducing Maximum Acceleration, your new premier provider of continuing education.

We’re not just bringing you a lecture. We’re bringing you the fuel to spark your competitive fire, the plan to win the game on the merits, the confidence to know the rules and master them.

We’re Maximum Acceleration, and we’re where loan originators go to put their career in high gear.

— LaDonna Lockard, CEO

So, the year didn’t exactly go how you wanted. Rest assured, nearly everyone is feeling that way.

Mortgage rates are still higher than projected, inventory is still a challenge, the gap in affordability is widening, and borrowers are still waiting for some sort of relief from these difficult conditions. At this point, it’s easy to lose hope, but it’s important to remember that despite the challenges of this year, you surely had successes too.

Take a moment to look in the rearview mirror and see where you’ve come from and how you’ve succeeded — you’ve likely accomplished more than you think. Taking this inventory is an important step in managing the stress this year has caused.

BY MARY KAY SCULLY, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Let’s dig deeper into why this year has been stressful and examine tactics for managing stress and how to set yourself up for a more successful 2025.

It’s stressful for everyone right now, no matter what industry you’re in. However, salespeople have been hit particularly hard. In a survey of sales professionals across industries, 67% of sales reps reported that they don’t expect to meet their quota this year, and 53% of sales professionals say it’s harder to sell than a year ago.

It’s a stressful time for borrowers too, especially with less-than-optimal conditions for one of the most important

financial decisions you can make in your lifetime. Borrowers want to make sure they are getting good rates and good prices so that their home is a sustainable investment. If your borrower is cranky on the phone, don’t take it personally. They’ve been tasked with making an important life decision in an incredibly challenging market.

Lenders are feeling the pain of the market as well. With less loan volume, margins get smaller and smaller and everyone has to do more with less.

So how do you effectively manage stress during a time like this? There are a lot of factors outside your con-

trol — the state of the market, the results of the election, and the busyness that comes with the holidays, to name a few.

Regardless of the stressors you may be experiencing, it’s important not to let them take a toll on your mental health. It can be easy to let the negativity in the news and even in your own office get to you. The silver lining is, no matter how the business looks right now, it will not be that way forever. One thing you can always count on is the consistency of change in the mortgage industry. So, what can you do?

Change your mindset. Instead of looking at what’s going wrong, spend your time examining what is going right.

To remedy the stress and uncertainty of whatever situation you find yourself in, it’s good to start by focusing on the positive, including what you have accomplished. How many transactions did you complete this year? What type of transactions did you make? Do you have any repeat borrowers or any new borrowers? Did you establish any new relationships? When you start to take inventory, you will likely find that you did more business or made more progress toward your goals than you think you did.

Regardless of how it feels, it won’t always be like this. The mortgage industry is resilient, and it always bounces back. In the meantime, take advantage of the slower times to focus on improving your knowledge of the industry. What is something you’ve always wanted to learn more about, but haven’t had the time to? Now is your chance to take the time to learn and grow.

Look into new ways to expand your reach. What is a new loan product that is gaining popularity or what is a new segment of borrowers you could work on gaining traction with?

You can also take this time to educate potential buyers on the benefits of owning a home when it comes to building wealth. While many borrowers you talk to may not be ready in this current market, you have a prime opportunity to build relationships and prep them for whenever the market decides to take a more favorable turn.

As the new year is on the horizon, get started as soon as possible to stay ahead of this consistently changing industry. As Marcus Aurelius said, “If you are distressed by anything external, the pain is not due to the thing itself but to your own estimate of it; and this you have the power to revoke at any moment.” So, no matter what 2025 throws at you, approach it with a new mindset. Being able to effectively manage stress is a skill you not only need in the difficult time, but in the good times, too. There will always be stressors, but how you respond to them makes all the difference for you and for your business.■

Mary Kay Scully is the Director of Customer Education at Enact, leading the development of the company’s customer education curriculum.

The mortgage industry is going through a significant change. For mortgage origination professionals, it’s a struggle to keep on top of all the changes, and to keep your sales strategies and marketing initiatives at their peak. You need to keep your pipeline filled, and you need the tools and directions to stay profitable, efficient, and effective. We’ve brought together the best in the business to create a top tier event specifically designed for mortgage origination pros.

The boutique approach, albeit not as profitable as big box lenders, offers a personable approach to lending that some argue is a dying art

BY SARAH WOLAK, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

In today’s fast-paced, automated world, where generic solutions are often marketed as universally applicable and customer service is increasingly outsourced to automated systems like online chatbots, the personalized approach of boutique mortgage lenders can easily be overshadowed. Unlike large-scale lenders like United Wholesale Mortgage (UWM) and Rocket Mortgage, whose brand recognition and streamlined processes make them appear more accessible and dependable, boutique mortgage lenders operate differently.

These specialized firms focus on providing tailored services and customized loan products, often catering to a specific type of buyer or niche market. Unlike their larger counterparts, boutique lenders prioritize the individual needs and goals of each borrower, offering a more personalized experience. This might include taking the time to understand a client’s financial situation, offering flexible loan terms, or providing guidance throughout the entire mortgage process.

However, this hand-holding approach can sometimes be overlooked in favor of the perceived convenience and reliability of big-box lenders, which may offer more standardized products and faster turnaround times. The boutique experience is not about volume or handling high-value transactions; it’s about ensuring that each borrower receives the attention and support needed to make informed decisions that align with their unique financial goals.

While boutique mortgage companies do exist, their presence is limited, and there

isn’t a widespread industry movement toward adopting this model. The allure of a boutique approach may appeal to some, but it hasn’t gained significant traction across the broader market.

Mike Cush, a freelance mortgage consultant, former vice president, and COO of Union Plus Mortgage Company, shared his perspective on why boutique models may not always succeed.

“Most U.S. banks don’t differentiate on mortgage lending as it is only a piece of the overall offering. Most IMBs (Independent Mortgage Banks) are started by or run by someone who was once a loan officer, and they grow by recruiting additional loan officers to capture leads. They don’t typically have a strong customer-facing value proposition because their success or failure depends largely on the performance of the loan officers they hire,” Cush explained. “In contrast, servicers take a different approach as their primary focus is on managing the asset. Since servicing is a low-margin business, they can’t afford to differentiate based on service delivery, resulting in a lack of brand loyalty.”

unique value proposition in a market where success is often determined by the performance of individual loan officers. This contrasts sharply with servicers, who, despite their operational differences, also struggle with creating brand loyalty due to the inherent limitations of their business model. As a result, the boutique model remains an intriguing but largely unadopted approach in the mortgage industry, with systemic factors favoring more traditional structures.

Amato said she chose to build her business up and brand it as boutique because it suits how she likes to do business.

“Purchasing a home is the largest investment of a lifetime. Some people do not want in-person. They do not want boutique. They want to just upload their documents, and that’s fine. I’m a people person. I like to connect on all levels with their needs, and also just emotionally,” she explained. “It’s a big decision, and there [are] a lot of questions that most people purchasing a home have.”

Cush’s perspective highlights a critical challenge faced by boutique mortgage firms: the difficulty of establishing a

Irene Amato of A.S.A.P Mortgage Corp. runs a bona fide boutique brokerage that’s proven to be a profitable business model for her business goals. A.S.A.P’s website boasts a specialties section — a value proposition to its customers — that boasts multilingual licensed loan originators who speak Albanian, Farsi, Hebrew, Mandarin, and Spanish, as well as specializations such as umbo loans, refinance loans, debt consolidation, FHA home loans, VA loans, USDA, 203k renovation loans, construction loans, and first-time home buyer loans. The company also holds a certification as a Military Housing specialist with the USA Cares program.

In the loan process, communication is key, especially for first-time buyers. Amato wrote a book called “Home at Last!” as a guide for all borrowers going through the home buying process, focusing on advice for buyers who might need an individualized approach, including single purchasers, self-employed, post-bankruptcy, and veterans.

The catered approach shouldn’t just apply to the mortgage business, Amato argues. “If I’m hiring a plumber, an architect, anything I’m doing, I want to be able to feel comfortable and have an advocate, not just a company,” she said. “I feel like when you go to a mortgage company to apply for a mortgage with a large lender or these companies that are mass production where they’re doing volume that is ridiculous, you have to lose something. I spoke to someone who said, ‘Oh, we do massive volume and we talk to every single client.’ There’s not enough time physically in the day to do that.”

Amato compared the big box lending style to fast fashion. “You’re not going to get the same service going to a Saks Fifth Avenue to purchase a dress that

you would if you went to a personalized dressmaker,” she quipped.

The specialties don’t end with residential loans. Monica Lubin, a Nashville-based real estate investor, broker, and private money lender for Keep Leading Spirit, a dba of Genovations Realty that specializes in buying and

selling homes. Run by Lubin and her husband, Kevin Lubin, the duo specializes in getting new investors into the ring. Both Monica and Kevin are new to the lending industry — about three months in — but have been fixing and flipping houses for over a year in Tennessee.

Lubin highlights her primary clientele as individuals with lower credit scores. “I think the majority of my clientele is people who have anywhere from 500 through 620 credit scores,” Monica admits. “Of course, I can go a little bit lower to 400, but I usually, when it is

400, connect them with credit repair resources and professionals.”

She emphasizes that working with less experienced borrowers and those with lower credit scores represents a longer-term investment compared to more seasoned clients. It also requires more detailed attention and management throughout the transaction.

lationship with our clients where we’re like, ‘Okay, how’s your day going?’ And just being encouraging. I have clients [who] always reach out and they’re like, ‘Hey, Monica, can you give me extra support today? I’m feeling a little bit discouraged.’ Investments are hard,” Monica said. This supportive approach underscores the company’s commitment to not just financial

“If I’m hiring a plumber, an architect, anything I’m doing, I want to be able to feel comfortable and have an advocate, not just a company.”

> Irene Amato, CEO, A.S.A.P Mortgage Corp.

“For my client to qualify for, let’s say, a DSCR loan, [they] have to have preferably a 700 credit score if they want to get 75% cashback. I would go the extra mile to make sure that we can work something out to get that 75% cashback,” she said. In a recent transaction, Monica and Kevin were able to secure 100% financing for a client in Delaware, with Kevin stepping in as a joint venture partner.

Additionally, Keep Leading Spirit operates from a Christian-based ethos, which Monica says influences their client interactions. “We do have that re-

transactions but also personal connections and encouragement throughout the investment journey.

Despite the dominance of large-scale lenders, boutique mortgage companies like A.S.A.P Mortgage Corp. and Keep Leading Spirit demonstrate that personalized, tailored service still has a place in the industry. While large lenders offer efficiency, boutique firms provide a more human touch, appealing to clients who value connection over convenience. Though niche, this approach offers a compelling alternative in a fast-paced industry. n

Do you have what it takes to be the best?

The New England Mortgage Expo returns to t Mohegan Sun Resort & Casino this January! 2,000 attendees, you won’t want to miss this oppo to be a part of New England’s largest and m mortgage event — the largest regional mortgage show in the nation. Join your peers for an exiti networking, product showcases, educational sessions motivational speakers, and so much more!

Originators attend for FREE using code MW

When there’s nothing to take the edge off, you have an edge

BY ERICA DRZEWIECKI, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

When he launched his mortgage career at age 19, Tony Blodgett wasn’t even old enough to order a beer.

“I was invited to get drinks after work and I’m like, I can’t even go to the bar,” recalled Blodgett, 47, now Executive Vice President of National Sales at New American Funding.

Less than a year later, while attending his first mortgage conference, Blodgett quickly noticed how the line between business and pleasure blurred together when industry professionals got together to talk shop.

Business deals have long been sealed over cocktails; closings commemorated with a special bottle. Meeting timelines in a high-stakes environment invites indulging oneself and taking a load off at the end of the day. And schmoozing during the height of the holiday season usually involves a cocktail or two.

But Blodgett, like an increasing number of other business professionals, does without the imbibing these days.

“After the conference, everyone was down at the pool and hot tub drinking, and some of the top producers in the industry were fighting over who got to pay the tab,” Blodgett remembered. “With sales professions in general, I feel like there’s this culture around drinking. A big part of getting business is going to events. Alcohol offers that social lubrication that makes networking easier for a lot of people.”

“Man, I wake up with so much more energy,” Blodgett says. “I’m so much clearer in my mind. I can go to networking events and not worry, did I have too many cocktails to where I shouldn’t be driving home? Do I gotta get an Uber, things like that. This just no longer becomes an issue … There were times [when] I look back at events I was at, and [I was] like, man, did I have too many drinks? Did I leave there feeling like I had represented myself the best way that I could? I think the answer is clearly no to those.”

Blodgett’s journey to sobriety began when he decided to do ‘Sober October’ in 2019 after listening to a podcast discussion between comedian Nikki Glaser and podcaster Joe Rogan on the topic.

“I had talked to one of my business coaches, someone in the mortgage industry who recommended that I maybe try taking a break once a

year, and so I kind of landed on the sober October thing,” he added.

Glaser, who had already embraced sobriety, mentioned she was inspired by a book, Allen Carr’s Easy Way To Control Alcohol. Blodgett found he could relate, recalling his departure from cigarettes years earlier, aided by Carr’s Easy Way To Stop Smoking. He downloaded the other book upon Glaser’s review.

“This was probably around the middle of October. I had not been drinking for a week or two and I still had the whole month to go. It’s a pretty short book so I listened to it in just a few days. And honestly, when I got done, I didn’t really think much about how it would impact my decision to drink in the future.”

But Blodgett reached the end of October. While at a friend’s house with his kids going trick or treating, a friend asked, “Hey, you want a beer?”

Blodgett declined, and his friend said “Tony, it’s October 31st. You’re there. It’s okay.”

But Blodgett just didn’t feel like it, and that was that.

“I just felt so good during those 30 days. I didn’t feel like I needed to reintroduce alcohol into my routine,” he reasoned.

Then came the holidays, and all the gatherings. Blodgett abstained, and people noticed.

“Honestly, it felt very awkward to me. I found myself ordering a non-alcoholic beer or a club soda with a lime in a short glass,” he said. “People who knew I wasn’t drinking were like, ‘What happened? Why’d you quit? Are you gonna quit forever?’ Nothing had happened, I

just had made that decision.”

As the new year rolled in, Blodgett decided to stay sober for 2020, and it paid off, especially when the COVID-19 pandemic brought the housing finance industry to a crossroads.

“A lot of people actually accelerated their drinking during COVID. I was at my sharpest. I really feel like it gave me an advantage during a really challenging time,” Blodgett recalled.

Rates were all over the place, uncertainty loomed; then things started really ramping up for the mortgage industry.

“It got really busy and I was able to really be on point to manage that,” he said.

When New Year’s Eve 2020 came upon him, Blodgett poured himself a bourbon.

“I just didn’t want there to be some weird situation where I wasn’t in control of my decision to drink. I wanted to feel like I was in control of it. So that started off just fine. I said, hey, I broke the

“People are like, ‘You’re so young. Do you think you’ll ever drink again?’ There’s no way to answer that other than, ‘one day at a time. I’m just not going to drink today.’ ”

> Eric Braun, Chief Growth Officer, Interstate Home Loan Center

seal, now I can casually drink. But I’ll be honest with you … within a few weeks, I was back to my normal drinking habits.”

This continued until April 2023, when Blodgett decided to do 75 Hard, a 75-day transformation challenge started by Andy Frisella, podcaster, entrepreneur, and CEO of the supplement company 1st Phorm. The challenge required several different commitments, one of which was abstaining from alcohol.

He was never “a problem drinker,” Blodgett asserted, but the time off had made him realize a personal potential that was once invisible.

“There’s no way that I was performing at my highest and best all the time because that only happens — in my opinion — when you’re completely clear-minded and not taking any alcohol.”

He revisited the book that helped him quit originally, then dropped drinking when his 75-day challenge began on May 1, 2023, and has been sober ever since.

“You know, it’s been a year and a few months, but this time for me it’s different because I don’t feel awkward when people ask me about it,” he said. “After seeing how I felt for those 15 months and how I felt for the two years afterward when I chose to indulge in drinking again, I’ve made a very conscious decision that for me, abstaining from alcohol 100% is not a difficult thing to do. It fits in very well with my lifestyle.”

Blodgett recommends the book he read to others who find themselves on a similar journey.

“I’m certainly not the only person in the mortgage industry who’s choosing to give up alcohol. Matter of fact, I know quite a few of them at this point because you tend to recognize those people when you go to these events and they are highly successful individuals. Look at most CEOs, people that are really achieving at a high level. I think it’s next to impossible to reach the real pinnacle of your own success if you’re setting yourself up to be foggy when you wake up in the mornings. You have to look at the

positives of what you’re going to receive from it, and maybe that will help propel you through this thought of missing out on something.”

Tim Davis, chief growth officer at Canopy Mortgage and CEO of The Originator’s Guide, is one of those high-achieving executives.

“Prior to me joining the mortgage business, during college, we drank and partied way too much,” Davis told NMP. “One night we ended up locking one of our roommates in the trunk of a car, and we didn’t find him until the middle of the next day. I just said, ‘That’s it’ and I haven’t had a drop to drink since.”

At that time, the 53-year-old Nashville resident and Dallas native was studying the arts. He has been sober since about age 20.

“I never met anyone in my life who said this statement: ‘My life improved and got so much better since I started drinking.’ Anytime you don’t taint yourself with any kind of alcohol or drugs you’re going to live a healthier life; absolutely it translates into business and personal success,” Davis observed.

If you run into Davis at a mortgage conference, his drink of choice is a Diet Coke.

He and Blodgett are both accustomed to being around family, friends, and colleagues who drink alcohol, and it’s not a big deal to them.

“I don’t judge. I have beer in my fridge right now. I have a wine fridge full of wine,” Blodgett said. “It’s never been a thing where I feel compelled to drink

if it’s around.”

He still goes to all the same happy hours and networking events, but it is more apparent to him when someone else has had a bit too much.

“I think everybody has this point where they cross over from it just slightly reducing their inhibitions to turning them into someone who maybe loses their filter, talks about things that maybe shouldn’t be talked about, or just gets to a place of inebriation and probably shouldn’t be in a business setting at those times. My tolerance for that is probably lower than it was when I was right there with them having a few drinks.”

The libations are handcrafted and plentiful during events like Beer & Real Estate and Wine & Real Estate, hosted by Chief Growth Officer at Interstate Home Loan Center, Eric Braun.

The 29-yearold resident of Brooklyn, NY brings together real estate

“I never met anyone in my life who said this statement: ‘My life improved and got so much better since I started drinking.’ ”

> Tim Davis, chief growth officer, Canopy Mortgage and CEO, The Originator’s Guide

agents, loan officers and other housing finance professionals over food and drink during several yearly events.

“The last brewery event that we had, there were over 500 people and most were drinking,” Braun says.

One person that wasn’t? Him.

“I’ve actually never had a legal drink, I like to say. I’ve had plenty of illegal ones, but I got sober when I was 20 years old,” Braun said. “It’ll be nine years since I’ve had any mind-or mood-altering substances, God willing, August 22.”

Braun speaks to teens at his old high school each year about his sober journey.

“I went from struggling emotionally, spiritually, physically due to addiction and everything that comes with it, to coming out the other side, being of service and not only in the capacity of helping hopefully other struggling addicts and alcoholics but also service to our clients and everybody on our team,” he said.

Braun’s approach with being sober is to take each day one at a time.

“People are like, ‘You’re so young. Do you think you’ll ever drink again?’ There’s no way to answer that other than, ‘One day at a time. I’m just not going to drink today.’”

He was taught that mentality, along with the fact that it’s smart to stay away from situations where one might be tempted early on in their journey.

“Being a person like myself, to not desire alcohol or substances is like a miracle,” Braun explained. “But I believe addiction is a disease, and I have to respect my disease. There’s a saying that if you go to the barber shop every day eventually you’ll get a haircut. I think that’s 100% true.”

Braun did the work, put himself in positive environments, and transcended the grip of drugs and alcohol. Now, he says, he isn’t even tempted when out with friends. This also appears to be true in a video of him on Facebook, where he can be seen

walking across a vineyard with a glass of wine to promote this year’s Wine-RE event.

“I think after you’ve had a spiritual experience like I’ve had and you have a foundation, then sobriety should be free. If you are hiding and still operating that way, then you’re not quite free yet. Nowadays I go out to these places and I don’t even realize people are drinking. Like it’s completely removed from my world.”

Without a doubt, the mortgage industry is a high-stress one at times. Fluctuating rates, losing out on deals, squashing homeownership dreams, and the potential for all this and more are out there waiting for one misstep.

“There’s a lot of pressure,” Blodgett admitted. “When it’s busy in our industry, people definitely get overworked and really have to put in the extra time and hours.”

Drinking to “take the edge off” and be more sociable at networking events and conferences can be avoided with simple preparation, according to Blodgett.

“I think I would just remind people that you are who you are regardless of the alcohol,” he said. “It might make you a little more willing to go up and talk to someone that you might otherwise not talk to; you might be more willing to ask for business; it tends to lower your inhibitions a little bit. But I think that could be accomplished through training, scripting, and being mentally prepared on what you want to accomplish at a networking event.”

A goal might be to introduce oneself to five strangers. Think of an introduc-

tion and how to make the other person feel comfortable enough to exchange business cards.

“Maybe do a bit more preparation,” Blodgett added. “When you go to a networking event make sure that you get out of it what you want. You can absolutely accomplish that through mindset, training, and preparedness, without having to rely on alcohol to give you that courage.”

Being an addict is just that, according to Braun. It has nothing to do with your profession.

“Listen, our industry is stressful,” he says. “There’s a lot of pressure on us from all parties, almost on all transactions, it seems, especially right now. But we can’t use the excuse of, ‘how can I ever do this sober? How can I deal with borrowers and Realtors and everybody without having a drink at night? Everybody does it. It’s accepted.’ Those are all just justifications to the fact that you think you have a problem.”

“A lot of people actually accelerated their drinking during COVID. [Because I didn’t] I was at my sharpest. I really feel like it gave me an advantage during a really challenging time.”

> Tony Blodgett, EVP, National Sales, New American Funding

Braun began his mortgage career as a telemarketer and worked his way through the ranks. Now he manages a division of about 50 people, in addition to being a loan officer and working on recruitment and marketing initiatives.

“If you look closely enough, you’ll find that there’s a lot of people there that aren’t drinking or they may just have one drink,” he says of industry events these days. “I think it’s important to differentiate between somebody who drinks and somebody who has a problem. I’m an addict, so I can’t drink or do substances successfully. There are plenty of people who can and accepting that early on in my sobriety journey was one of the keys to me achieving long-term sobriety. I admitted I was powerless and my life had become unmanageable. I had to adopt that belief early on so that I can see things a little bit clearer and navigate those environments.”

Braun encourages other mortgage professionals who think they might have a substance abuse problem to be honest with themselves and find a mentor who can help them work through it.

Even as they live sober and lead successful careers in mortgage, these pros aren’t without any vices.

“I’m definitely not a monk by any means,” Braun says. “I don’t ever want to portray that image where I’m super-disciplined, wake up at 4:30 a.m., do meditation … that’s not me at all. I fall short a lot and I have other vices that are just not as detrimental in the short term, I would say, as drugs and alcohol.”

Talk to his friends, family, and girlfriends, and they would say that he loves working — maybe a little too much sometimes. But because of his past experiences with addiction, he knows when to reign it in and take a step back.

“When I’m stressed, I like to work. When I’m happy, I like to work,” Braun says. “There are points throughout my week or every few months where I have to try to get back some level of balance.” n

A warm welcome to you! I’m Kelly Hendricks, the Managing Editor of Mortgage Women Magazine and Senior Vice President of Delmar Mortgage, and it brings me great joy to extend this invitation to you. Throughout my career in the mortgage industry, I’ve been fortunate to have leaders and mentors who played pivotal roles in shaping my journey. I am thrilled to introduce a transformative initiative – the Mortgage Women Leadership Council, created by Mortgage Women Magazine.

In my role, I’ve experienced the challenges that women face in leadership within the mortgage sector. These challenges led to a profound realization — the need for a dynamic network to empower women in our industry. This realization is the driving force behind the creation of the Mortgage Women Leadership Council. I believe in the power of collective support, and I am excited about the opportunity to share and benefit from each other’s experiences.

Our mission is clear: to promote and empower women’s leadership in the mortgage sector. The council aims to create a supportive environment for professional growth, mentorship, and networking. Joining the

council comes with various benefits, including networking opportunities and access to industry-specific professional development resources. We understand the unique challenges women face in mortgage leadership and have tailored mentorship and support systems to address them.

I invite you to join this movement to empower women in the mortgage industry. The Mortgage Women Leadership Council is committed to fostering a welcoming and supportive environment. Your involvement will not only contribute to your personal and professional growth but also play a crucial role in advancing women’s leadership in our industry. To join or get involved, simply click here to apply.

Thank you for considering this invitation to join the Mortgage Women Leadership Council. For further inquiries about the council and details on how to join, please contact Beverly Bolnick at bbolnick@ambizmedia.com. Let’s work together to advance women’s leadership in the mortgage industry — because collective action brings about meaningful change.

Kelly Hendricks Managing Editor, Mortgage Women Magazine

As a valued member, enjoy these benefits:

Access to a Powerful Platform: Amplify your voice and influence through Mortgage Women Magazine, exclusive sponsored programs, email newsletters, and impactful events.

Editorial Opportunities: Showcase your expertise and insights through editorial features in Mortgage Women Magazine, gaining visibility and recognition among industry peers.

Awards and Recognition: Receive well-deserved recognition through our award programs, celebrating your achievements and contributions to the mortgage industry.

Community Support: Become part of a dedicated community committed to celebrating and driving meaningful progress in the mortgage sector. Connect with likeminded women leaders, share experiences, and foster collaborative initiatives.

Mortgage Women Magazine: Enjoy your complimentary digital subscription to Mortgage Women Magazine, the premier publication for women in mortgage. Read advice, learn about industry updates, and take in the inspiring stories of your peers.

Become a member today.

Join us and be a driving force in creating a more inclusive and thriving mortgage industry. Together, as a united community, we believe we can make real change.

Enjoy 1 year of your individual membership free! Use code MWM2024

mwlcouncil.com

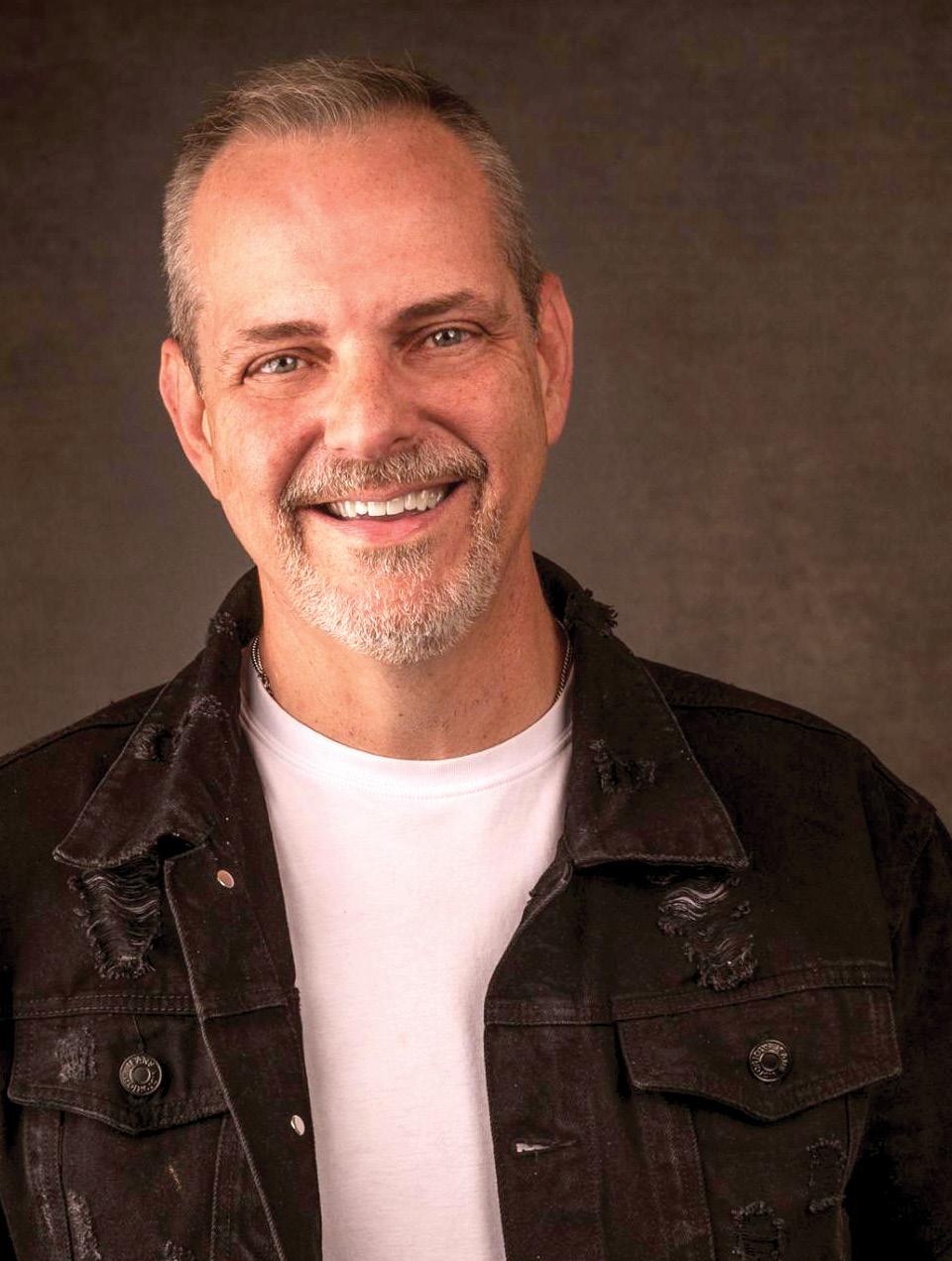

> Matt Oliver and Lisa Lund — she brings precision to operations while he focuses on client care, making them a blend of strategy and service. As a couple and business partners, Matt and Lisa carry forward a legacy of integrity, showing that a strong partnership can be the foundation for lasting client relationships.

BY ERICA DRZEWIECKI, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Matt Oliver joined Lund Mortgage in 2007 and married Lisa Lund in 2008. Albeit ironic that the global financial crisis was occurring mid-hire and mid-nuptials, the company — and the couple — stand solid to this day.

It was in 2005 during Arizona’s Phoenix Open (now the Waste Management Open) that Oliver and Lund first met.

“It was 19 years ago on a Saturday. We just had it here this past weekend,” she says. “I was there with a wholesale lender and he was there with his friends.”

Oliver was working for Chase Bank at the time, taking loan applications retail. Lund had been with her dad Stan Lund’s company about as long as she can remember, or at least since she asked for a 10key calculator around her eighth birthday.

“He asked me what I did and I told him I was a mortgage broker,” she recalls of the first conversation she ever had with the man who would become her husband, the father of their children, and today, senior loan consultant at Lund Mortgage, which she now brokers and owns.

Oliver jokingly asked Lund that fateful day why

anybody would go to a broker (instead of a bank) for a loan. “So I clearly explained it to him, and in 2007, I stole him over to the wholesale side.”

The mortgage business went into crisis mode about a year later and for the first time in his career, Oliver witnessed a mass meltdown of loan officers across the industry.

“I just kept saying to myself at that point, I don’t ever want to be in that position,” he recalls.

So when the market was hot from 2019 to 2021 Oliver didn’t roll in the riches. He buckled down with eyes on the horizon in preparation for the market downturn, which inevitably came.

“It was like shooting fish in a barrel to do loans in 2020 and 2021, but it wasn’t going to last forever. We’ve always kind of taken it as a good omen to remember the clients we’ve dealt with and come back to work with them. I think that’s why this past year was a little bit better because we did have a lot of returning clients come back to us.”

Oliver had more refinance volume and refi transactions than any other one of NMP’s Leading LOs of 2024, featured in the magazine’s April issue. His total refi volume for 2023, as printed, was $31,236,943 for 184 units. He also had $39,630,242 in purchase

We want to be your lifetime mortgage consultant. We’re going to look out for you.

If rates drop or if we feel that we could put your family in a better situation down the road, we’re always going to be here for you.

“ to you. we we going

> Lisa Lund, owner, Lund Mortgage

Lund, owner,

volume among 102 units, bringing his total loan volume for the year to $70,867,185, or 286 units.

He refers to Lund, his wife, as “a jack of all trades in this industry” and “a genius underwriter.”

The late Stan Lund, who passed away in 2014, started working in mortgage around 1981, for a home thrift and loan bank. When his daughter started her own business in 2009, he served as a key consultant right up until his passing.

“I feel that I was born into this business,” Lund says. “Ever since I was little, my dad would do ‘take your daughter to work day’ and I fell in love with the business from then on.”

She always liked math and seeing how her dad and his staff helped people get into homes.

In high school Lund started working at the shop, stacking files and helping with audits. She worked her way up from receptionist, to junior processor, processor, manager, and loan officer before taking over the business.

But Lund credits her father with ingraining the company ethos in all he touched.

“My dad left a great legacy and so many things to learn from,” she says. “In fact, when I was at the golf tournament this weekend, I ran into a client who remembered how my father came to his living room and sat down with him for his very first refinance and explained everything.”

That approach is one that she and her team hold paramount to this day.

“My dad taught me the old school mentality of what it means to work with clients and not just treat them as a number and to care about them,” Lund explains. “We brought the technology and the willingness to learn the technology part of it, but he brought so many good things that we carry on to this day about putting the client first and really understanding their needs. He really taught us to sit down, analyze everything and look at everyone’s individual situation separately. To say, we’re not here just to close this transaction for you. We want to be your lifetime mortgage consultant. We’re going to look out for you. If rates drop or if we feel that we could put your family in a better situation down the road, we’re always going to be here for you.”

>

“This philosophy translates into lots of refinance transactions at the company, and in Oliver’s portfolio.

“The database is probably the most valuable tool that any loan officer could have in this profession,” he says. “If you’re not keeping track of your

But in cases where a refi won’t do a client any good, Oliver will be the first to let them know.

“We pride ourselves on giving sound advice,” he says. “At the end of the day, it just comes back to if you’re doing what’s best for the client at all times, and if they can feel that, if they can understand

> Lisa Lund, on how she and her husband each contribute to their company’s success.

past clients and you’re not touching base with them and you’re not sending birthday cards or anything else, it’s worthless in my opinion. It’s worthless to not be doing that.”

While some mortgage companies play strictly for one team or the other, Lund prides itself on being both a purchase and a refi shop.

“I think it’s crazy to be fully committed to just one channel. We’ve definitely been more refinance dominant than purchase dominant, but we never took the purchase sector out of our business model,” Oliver says. “I think being proficient in both purchases and refinances, you should be able to retain those clients if you’re always doing what’s best for them. In today’s world, it seems like a lot of loan officers want to create these efficiencies with technology and be able to just talk to the client for three to five minutes and have their processor handle everything from then on out. To me, that’s bad business.Those people aren’t going to remember who you are in the transaction. There’s no reason for them to come back to you.”

that that’s what you’re doing for them, they’re always going to trust your advice in the future.”

Preserving the family legacy is important to Lund, whose oldest son is now working right alongside her.

“Our main goal is making sure our clients are satisfied,” she says. “So they’re going to come back to us. They’re going to send their children to us. They’re going to send their family members, their coworkers to us.”

That drove her decision to get licensed in other states outside of Arizona.

“We really branded ourselves in Arizona where everyone knows who we are. We decided last year to start getting licensed in other states, which is something I never thought we would do. But we saw a need for it when our current clients were reaching out, saying ‘hey, I have a family member here. We’re moving here.’ ”

Tackling challenges like this one are what keep Lund and her team growing every day.

“Like anything else, there’s always challenges, but I absolutely love it,” she says. “One of the things I like to say is that everyone excels in their own space and what they’re good at. So learn to work together instead of against each other. Matt is wonderful on the phones. He’s great at talking to the clients, helping them understand, and I am more the operational, detailed brain of it, hence the underwriting. I like to solve the problems and he likes to bring them to me.”

As a married couple who work together, Oliver and Lund have accumulated some good stories over the years.

“I did write him up one time and everyone thought that was funny because he is my husband,” she recalls. “Just navigating through this industry together and all the times, having the common goals and understanding to stay in each other’s own lane, but really supporting each other, I think has been a big thing for us. Not trying to overstep on the other person, but understanding what their strengths are and really pushing that forward.”

Oliver is a big Kansas City Chiefs fan, so football is often a conversation starter or bridge out in the field.