Rising Tides & Rising Costs: How the Cost of Insurance Relates to Affordable Housing

Rising Tides & Rising Costs: How the Cost of Insurance

Relates to Affordable Housing

M. Martin Boyer, PhD & Franca Glazer, PhD – HEC Montreal

J. Brad Karl, PhD & Charles Nyce, PhD - FSU

Today’s Agenda

• Three-part presentation:

• Relationship between insurance & property values

• Our Project (Public Private Partnership)

• Ultimate Goal: Reduce Cost of Catastrophic Risk

• Public Private Partnership Part 1: Changing the Risk Profile

• Public Private Partnership Part 2: Optimizing Risk Financing

• Recommendations

“Affordabl e” Housing

• Factors reducing affordability

• Demand for housing (location, location, location)

• Construction costs

• Annual costs of homeownership

• Taxes

• Maintenance

• Insurance

• Florida has the highest homeowners insurance premiums in the US!

What is driving rising insurance prices? Exposure growth Inflation

Climate Change Cost of Capital

What can be done to reduce insurance costs in Florida?

Ultimate Goal:

Reduce the Cost of Catastrop hic Risk

• Project Outline:

• Justify the need for public private partnership

• Risk Reduction Proposal – Alter the catastrophic risk profile

• Optimize Risk Financing Proposal – Optimal Role of Government Financing & Optimal Structure of Government Funding

Why do we need a Public Private Partnership?

• Why private market is not enough?

• Cat Risk Exposure

• Information and Understanding: uncertainty in future loss prediction

• Adequate returns for investors

• Rate inaccuracy/inadequacy

• Affordability

• We already have one between private market and State of Florida, need all stakeholders at the table (including Federal Government) to ensure that changes do not cause market disruptions

• Long-term solutions must recognize that future losses may be beyond the capacity of voluntary markets and current public mechanisms, and may require a Federal backstop

Lower

Risk Exposure - Changing the Risk Profile

M. Martin Boyer, PhD

Charles M. Nyce, PhD

Cat Risk Profile

Risk Reducti on Proposal

• Traditional Risk Management Strategies include:

• Avoidance (move people out of Florida/away from coasts)

• Stop Risk Expansion (no new construction in FL)

• Slow Risk Growth (tougher building codes)

• Reduction (mitigate existing properties)**

• Resiliency (figure out a way to pay for, and bounce back from, losses that do occur)***

Mitigation – Public Private Partnership

Theory – invest in mitigation only up to (if) MB=MC

Unsophisticated: e.g. storm shutters, landscaping (things homeowners can do on their own)

Property Level:

There are a variety of types of mitigation:

Aggregate measures: neighborhood and more global efforts e.g. seawalls, aggregate landscaping to breakup wind fields

Sophisticated: roof shape, roof to wall connections, wall to foundation connections, secondary water barriers, complete envelope protection

Mitigation Problems

Piecemeal mitigation may not be very effective (building envelope)

• Significant costs borne in a single time period to protect building envelope

Upfront costs vs. long-term (uncertain) savings

• Discounts on homeowners insurance premiums are long-term savings

• Reduction in out-of-pocket catastrophe expenses are long-term uncertain savings

Myopic Risk Perception

Charity Hazard

Hold-ups by property owners

Externalities

Aggregate Mitigation

• Aggregate measures: e.g. seawalls, aggregate landscaping to breakup wind fields

• Benefit multiple properties and multiple generations

• Sponsor/effort should be government entity

• Financing duration should match the life of the mitigation feature

• Benefits:

• Reduce the severity of losses

• Reduce the tail of the loss distribution

• Shift the distribution to the left

• In our model:

• Government attachment point shifts

• Amount of loss distribution financed by government entity is reduced

• Result: Government has real incentive to invest in aggregate mitigation because it reduces its own future losses

At individual property level, mitigation does not have a significant impact on aggregate losses, so decision must make financial sense at that property level (MC/MB)

Property Level Mitigatio

Not great success at government incentivizing property owners to undertake sophisticated mitigation

My Safe Florida Homes Program – approx. 26,000 grants approved (not all taken), average size approx. $9,500.

Homeowner puts approx. $5000 out of pocket, average homeowners insurance premium reduction was just under $1,000. 6-year payback period.

How do we change the mitigation dynamic at the individual property level?

Property Level Mitigatio n (PLM)

Government entities offering less than actuarially fair premiums REDUCES mitigation incentives!

There are researchers today that promote mortgage lenders:

offering differential mortgage rates for mitigated vs. unmitigated home Lending for home + mitigation expenses

PLM: Changing the Dynamic –Mortgage Lenders

• Mortgage lenders are good at financing

• Why should they be involved in mitigation?

• Do we see differential mortgage defaults because of catastrophic losses? Maybe? Hawaii wildfires – yes, CA wildfires –no, Hurricane Ian .1% more in Ft. Myers , Hurricane Katrina – yes.

• Given that homeowners insurance is required to get mortgage, and the mortgagee clause, any catastrophic event covered by homeowners insurance policy should not see mortgage defaults

• No research on mitigated vs. unmitigated home mortgage performance

• Mortgage lenders have not been involved in sophisticated mitigation

PLM: Changing the Dynamic –

Property Insurers

• Property insurers bear approximately 60% of the catastrophic losses in US

• Property insurers understand sophisticated mitigation & have capital to support investment in it

• Vast change to the typical insurer/insured relationship

• Need to address the insured holdup on mitigation vs. length of insurance contract

• Create contract structures such that mitigation decision is based on longer time period

• 2 choices:

• shorter contracts with exit fee (switching costs need to be high to get multiyear benefit)

• Longer contracts (length would depend on lifecycle of mitigation features)

• Insurers understand risk mitigation technology and its existence/lack of cannot be observed freely

• Once a mitigation investment has been made, it cannot be undone

• The mitigation investment stays with the property, even if insured decides to switch insurers

• Insured enters into agreement with insurer to:

• Insure property

• Undertake mitigation efforts

• This agreement can be a long-term contract or series of short-term contracts

• Insurer funds mitigation efforts in time period #1

• Insured pays insurer reduced insurance premiums in time periods 1-XX

• Insured reimburses insurer for mitigation efforts on payment plan 1-XX

• Combined payment must be less than unmitigated insurance premiums for MC/MB calculations to hold

PLM: Changing the Dynamic –Property Insurers

• Significant Changes are Needed:

• Government certification/government guaranty of contract to avoid solvency concerns of insurers

• Differential regulatory oversight?

• Two capital funds (one to support underwriting, one to support mitigation investments)?

• Government incentives to mitigate switch focus to insurers vs property owners

Lowering the Cost of Capital –Optimizing Risk Financing

Franca Glenzer, PhD

J. Bradley Karl, PhD

Charles M. Nyce, PhD

What are private insurers really good at?

What do they bring to the table?

• Real Services

• Risk identification

• Risk pricing (underwriting)

• Claims adjusting

• Access to capital

• Internal & External

• $$ to pay the losses they choose to underwrite

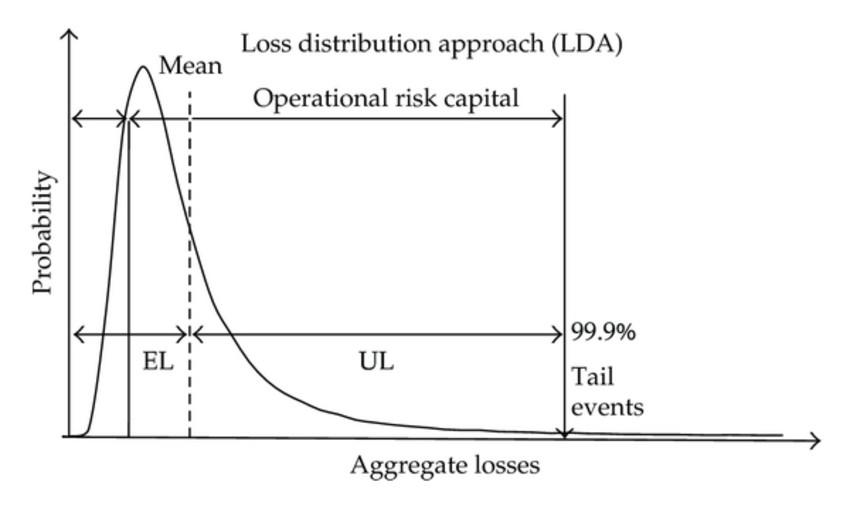

How Do Insurers Pay for Losses (traditionally)?

Insurers estimate losses they expect to pay

Some estimates made with high levels of certainty (e.g. auto, life, etc.)

Other estimates are less certain (e.g. catastrophic windstorm losses)

Premium charged today reflects:

Cost of paying for estimated future losses

Additional cushion for unexpected future losses

Costs of maintaining and administering the insurance pool

Investment earnings

Cat Risk Profile

Governments Insuring CatastrophesTheory

• Recall from earlier: What do insurers bring to the table:

• Private Insurers have advantages in underwriting, claims handling, real services, etc.

• Governments have better access to capital

• Boyer and Nyce (2013) show that:

• The cost of catastrophic insurance can be so high so that making the implicit government’s guarantee explicit can reduce overall costs

• Government intervention will have an impact on the price of insurance and on the wellbeing of insurers, reinsurers, and policyholders.

• If government intervention in the insurance market increases society’s welfare, then it would be at the highest possible levels of risk

Does PostLoss Funding Ever Make Sense?

Are there instances when it makes sense to finance a portion of tail risk after the loss-generating event occurs? e.g. pay for some portion of hurricane damage after the storm occurs

Is there a role for the government to facilitate post-loss financing mechanisms?

Our research focuses on these questions

Pre-loss vs post-loss financing

Putting it All Together – Our Theoretical Framework

• At this point, it does not appear that one is ALWAYS better than the other (Pareto Improving)

• Are Floridians ever better off utilizing post-loss financing?

• Maybe, it all comes down to the trade-offs

• The devil is in the details

• lower up-front premiums are better, but less fair underwriting, subsidies across risk classes and through time, reduced mitigation and location incentives and increased political risk are tough to outweigh

• Can we construct a model that enables us to weigh each of these trade-offs to determine WHEN post loss financing may make sense?

Putting it All Together – Our Theoretical Framework

• A government entity financing tail risk on a post-loss basis may be feasible

• We have a theoretical model that considers an individual’s utility if

• All losses are financed on a pre-loss basis, vs

• Some portion of losses are financed on a post-loss basis

• This theory will guide in making empirical estimates of

• The extent to which individuals would benefit from a post-loss financing option

• How post-loss financing could influence housing or income decisions

• The degree of risk that is financed on a post-loss basis

• We also plan to provide perspective on how a post-loss financing mechanism could be structured

Our

Theoretic al Model

The government determines (through the solvency level) the minimum assets an insurance company must hold

Government indemnifies policyholders when actual losses exceed insurer’s assets

Insurance “bail outs” are paid for by a tax on all households (Post-loss).

We compare welfare effects under different levels of regulatory stringency

Solvency

regulation and government intervention

Preliminar y results

The less the government intervenes, the more prevention effort is undertaken

There is a hump-shaped relationship between government involvement and individuals' well-being:

Some pre-loss financing increases well-being since it increases prevention incentives

There is an optimal degree of government intervention

After a certain point however, pre-loss financing makes premiums excessively expensive and individuals worse off

Recommendations

If we do this right, every stakeholder will be both happy and angry with our recommendations!

Three Areas of Recommendation

• Need for a Public/Private Partnership

• Mitigation - Changing the current & future risk profile (Aimed at Limiting Exposure Growth)

• Lowering the Cost of Capital (funding catastrophic exposure)

• Government Involvement in Insurance Markets

• How the Government Funds that involvement

• Strengthening Private Insurance Markets

• Primary

• Reinsurance

• Capital Market Solutions

All of our recommendations:

• Are aimed at reducing either exposure, cost of capital or BOTH!

• Are applicable to Federal Government, State/Local Government, and/or Private Market

Recommendations to Reduce Exposure:

1. Develop strategies to improve the affordability of mitigation

2. Expand and improve Florida Building Code to incorporate “Code plus” standards

3. Develop a uniform Hurricane Resistance Grading Schedule taking into account ALL relevant features

4. Establish a Community Rating System for wind (BCEGS) AND flood exposure

5. Pilot program for mortgage lenders and insurers to develop insurance/mortgage products that effectively promote mitigation

6. Require that all new construction building permits include proof of private market insurance coverage

7. Encourage not-for-profit organizations aimed at mitigation

8. Education programs to educate stakeholders in catastrophe prone areas on the risks and cost of location

9. Expand research funding into cost-effective mitigation, windstorm prediction, and interaction between windstorm and storm surge (Florida should be a mitigation hub!)

Recommendations to Reduce Cost of Capital:

1.Allow/encourage insurers to accumulate reserves over multiple years (Federal Tax Law)

2.Allow individuals to establish individual disaster preparation accounts for: mitigation, deductibles, or disaster recovery (Federal Tax Law)

3.Reposition the National Flood Insurance Program as a reinsurance program with flood covered by homeowners policy (Federal Program change)

4.Address insurance financing system inefficiencies (State level)

5.Address Cat Fund Operations (State level)

6.Address Citizens Operations (State level)

7.Address insurance affordability in a means tested program outside of the insurance mechanism (State level)

Recommendations to Reduce Cost of Capital:

8. Proactively explore alternative risk financing solutions

9. Adjust insurance regulation to allow more insurer flexibility in providing basic insurance coverage/options (e.g. ACV vs. Replacement Cost)

10.Enact proactive programs to attract investors to the Florida property insurance market (at all levels)

11.Incentivize insurance operations in Florida (at all levels)

12.Incentivize insurers to retain capital and grow balance sheets

13.Explore developing insurance solutions in free trade zones or reservations

14.Incentivize improvements in rating methodologies and solvency testing

15.Ensure that premium discount structures reflect true risk reduction and incentivize cost-effective mitigation

Recommendations to Reduce Exposure & Cost of Capital:

1.Promote risk-wise behavior

2.Tie Citizens policies to My Safe Florida Homes Program