The Colorado Association of REALTORS® (CAR) assumes no responsibility for return of unsolicited manuscripts, photographs or art. The acceptance of advertising by the Colorado REALTOR® does not indicate approval or endorsement of the advertiser or their product by CAR. CAR makes no warranties and assumes no responsibility for the accuracy or completeness of the information contained herein. The opinions expressed in articles are not necessarily the opinions of CAR.

This is a copyrighted issue. Permission to reprint or quote any material from this issue is hereby granted provided the Colorado REALTOR ® is given proper credit in all articles or commentaries, and the Colorado Association of REALTORS® is given proper credit with two copies of any reprints.

The term “REALTOR ®” is a national registered trademark for members of the National Association of REALTORS® The term denotes both business competence and a pledge to observe and abide by a strict Code of Ethics. To reach a CAR director who represents you, call your local association/board.

FROM THE CEO

Empowering Success: Harnessing the Strength of REALTOR® Associations

As we look forward to another year, I want to take a moment to express my sincere appreciation for your unwavering commitment as a Colorado REALTOR®! This year has certainly thrown us some curveballs - from shifting market dynamics to the headscratching NAR settlement, and everything in between, including discussions around our Association’s significance and the evolving needs of our clients. But let’s remember, your membership at the local, state, and national associations has been key in navigating these challenges and opening doors to a wealth of resources that can supercharge you career and success.

At the grassroots level, your local associations are where the real magic happens. Here, REALTORS® can tap into a vibrant network of fellow professionals who are in the trenches just like you. Local associations provide vital resources, specialized training, and development opportunities that are tailored specifically to the nuances of the Colorado market. Whether it’s honing your skills on the latest industry trends or attending events that foster genuine connections, these local networks are crucial for your growth. Plus, you’ll often gain access to real-time market data and insights that are absolutely essential for making informed decisions and giving your clients the best advice possible.

Then we’ve got the Colorado Association of REALTORS® (CAR), which amps up those benefits even further. CAR is your advocate on the legislative front, fighting for changes that impact our industry right here in Colorado. We work tirelessly to ensure that your voice is heard in important legislative and regulatory policy discussions, affirming the critical role that REALTORS® play in shaping the future of our communities. With ongoing education, professional development, and market trends programs, CAR equips you with the tools needed to navigate the complexities of our evolving market. If you’ve ever used the CAR Legal Hotline or Professional Standards program, you know this support not only empowers you to excel in your business but also enhances your ability to serve your clients with confidence and expertise.

Tyrone Adams CEO of the Colorado Association of REALTORS®

Moreover, let's not overlook the National Association of REALTORS® (NAR), which provides a broader platform for advocacy and networking. Through NAR, you gain access to a treasure trove of resources, including cutting-edge technology, marketing tools, and invaluable research that can elevate your practice on a national scale. Their commitment to maintaining high ethical standards and professionalism in real estate helps to strengthen our industry as a whole.

As we look forward, I urge you all to take full advantage of the benefits offered at every level of our REALTOR® associations. Get involved with your local leadership, dive into CAR's initiatives, and make the most of what NAR has to offer. Your active participation is what builds a vibrant and resilient real estate community.

In conclusion, while we may face unpredictable challenges in the year to come, remember that together we are more than capable of navigating them. Your commitment, collaboration, and proactive engagement are what will not only drive your success but will also enhance the reputation and effectiveness of our profession across Colorado. Thank you for being a member and you for all that you do. Have a safe and joyous holiday season, and let’s make this next year our most successful yet!

2024 November Elections Update

Of our 59 endorsed bipartisan candidates for the state legislature this November, 58 were winning or have won their respective races as of November 13th, the last day for voters to “cure” their ballots if there were any discrepancies (missing signature, ID verification, etc.). That’s a 98% success rate.

If the current results hold, the following will be General Assembly composition for the next two legislative sessions starting on January 8th, 2025:

Colorado Senate: 23 Democrats – 12 Republicans

All 14 CAR endorsed Senate candidates won their respective races. This list includes 8 Democrats and 6 Republicans. Notable:

• Endorsed candidate Scott Bright (R) flipped SD 13 seat.

Colorado House: 43 Democrats – 22 Republicans

44 of 45 CAR endorsed House candidates won/winning their respective races. This list includes 25 Democrats and 20 Republicans. Notable:

• Endorsed candidate Rebecca Keltie (R) leading her race by 21 votes to flip HD 16.

• Endorsed candidate Dan Woog (R) flipped HD 19 by more than 200 votes.

• Endorsed candidate Ryan Gonzalez (R) flipped HD 50 by over 500 votes.

Democrats will continue with significant majorities in both chambers, but they will not have a super majority in either chamber. Democrats and Republicans in both the House and Senate recently had their caucus elections to elect new leadership for the 2025 legislative session:

SENATE

• President - and REALTOR® Champion Sen. James Coleman (D), succeeds termlimited Steve Fenberg.

• President Pro Tem – Sen. Dafna Michelson Jenet (D) succeeding Sen. Coleman

• Majority Leader - Sen. Robert Rodriguez (D) reelected.

• Asst Majority Leader – Sen. Lisa Cutter (D) succeeds Sen. Faith Winter who did not seek reelection.

• Minority Leader – Sen. Paul Lundeen (R) reelected.

• Asst Minority Leader – Sen. Cleave Simpson (R) succeeds term-limited Bob Gardner.

• Majority Leader – and REALTOR® Champion Rep. Monica Duran (D) reelected.

Brian Tanner

Vice President of Public Policy for the Colorado Association of REALTORS®

Government Affairs

• Asst Majority Leader – Rep. Jennifer Bacon (D) reelected.

• Minority Leader – and REALTOR® Champion Rep. Rose Pugliese (R) reelected.

• Asst Minority Leader – Rep. Ty Winter (R) reelected.

With leadership in place, we look forward to seeing the legislative committee assignments for legislators in the 2025 session.

ELECTIONS POSTMORTEM

As elections continue to remain highly partisan and personal for so many, it’s important we reshare our internal process for endorsements, which we originally shared via email on September 10th.

CAR’s Political Action Committee (CARPAC) is the official body for evaluating and endorsing legislative candidates. It is comprised of 19 REALTORS® from around the state. They evaluate incumbents as to who should be endorsed as a Friendly Incumbent or not. For races without a Friendly Incumbent, each candidate is vetted in a process requiring them to complete a candidate questionnaire and a candidate interview with REALTORS® who serve on CARPAC, the Legislative Policy Committee (LPC), CAR’s Leadership Council, and some local members. These interview panels recommend a position (endorsement, no endorsement) for the full 19-member CARPAC to review and consider for official action.

We understand more than 26,000 Colorado REALTORS® run the entire political gamut and that CAR’s endorsed candidates will not align with every member’s partisan leaning. We also understand that candidates have positions on other issues that may run counter to members’ personal views or beliefs. CAR evaluates and endorses candidates based on how they impact housing, property rights, and the real estate market. We also consider the political composition of the district they serve. If other policy issues drive voting decisions, we fully support and encourage every member in making decisions that best align with those personal values knowing they may fall outside our political sphere.

Some have asked us to not endorse in elections. We truly believe sitting on the sidelines for candidate endorsements would be a disservice to REALTORS® and our associations. By endorsing candidates and engaging in elections, we can lift our issues – housing, property rights, and real estate – to the forefront for all candidates, and

encourage elected officials to explore legislation related to these issues. It’s a true statement that “if real estate is your profession, then politics is your business” and supporting candidates to help them win their respective races sets our association up for better success in future legislative sessions.

Our Mission Statement reads “The Colorado Association of REALTORS® empowers members as industry and community leaders with knowledge, ethics, professionalism, and is the collective voice for housing and property rights.” Our 2024 endorsements reflect this.

We may not always be aligned on every issue, but our 2024 endorsed candidates have communicated an aligned approach and shared values with our association and a commitment to solving our housing crisis while protecting private property rights.

2024 LEGISLATORS OF THE YEAR

At our October Leadership Symposium (formerly Fall Forum), CAR was able to present awards for our 2024 Legislators of the Year to:

• Sen. James Coleman (D – SD 33) Denver

• Sen. Barbara Kirkmeyer (R – SD 23) Weld, Larimer counties

• Rep. Shannon Bird (D – HD 29) Adams, Jefferson counties

• Rep. Lisa Frizell (R – HD 45) Douglas County

This year’s honorees were recognized for their respective pro-housing positions and votes on a wide range of bills along with their commitment to consistently reach out for REALTORS®’ feedback and positions on legislation. While their votes on legislation often aligned with our positions, just as important was their asking REALTORS® how to improve bills and their willingness to carry amendments to that effect.

REALTORS® Political Action Committee (RPAC)

Our election success starts and ends with RPAC. The individual, voluntary contributions made by REALTORS® to RPAC were used to help elect bipartisan candidates who understand and support our interests. CARPAC explored and approved disbursements totaling more than $214,000 to over 60 local and state political candidates or current legislators. CARPAC also approved disbursements for Independent Expenditure (IE) campaigns focused on specific races to make a difference, which it did. These IE efforts allow us to control messaging since they are entirely independent of any candidate and focus solely on positive support of candidates who stand with us on housing, property rights and real estate issues. In several races decided by a few thousand, a few hundred or even 21 votes, we contacted tens of thousands of voters (the general public) to share how our endorsed candidates were the best on issues impacting REALTORS® and consumers.

There is still time to make an RPAC investment for 2024 to set us up for success in 2025! Become a major investor or even start with a Fair Share investor at $25. We have one last fun RPAC activity for you! The 2024 RPAC year closes on December 5th and we are giving away a $500 Amazon gift card.

How to enter to win the $500 Amazon gift card:

1. Purchase one or more raffle tickets to be eligible

• 1 ticket = $25

• 1 ticket = 1 entry

2. Click here to purchase

CONGRATULATIONS to the Local Associations below who have hit Triple Crown in 2024 and there’s still time for more associations to join them by December 5th! To hit the RPAC Triple Crown, the local must hit their Overall Raised Goal, Reach 37% participation, and hit their Major Investor goal!

*List is current as of 11/13/24*

• Mountain Metro

• Durango

• Glenwood Springs

• Grand County

• Gunnison Crested Butte

• Telluride

• Vail

• Estes Valley

• Four Corners

• Royal Gorge

PHOTOS FROM RPAC LUNCH IN OCTOBER

PHOTO HIGHLIGHTS FROM

2024 CAR LEADERSHIP SYMPOSIUM

The Federal Reserve Cuts Rates and Mortgage Interest Rates Increase; Why?

By Mathew Schulz, CVLS, CML President, Residential Loan Programs, Firelight Mortgage Consultants CAR Foundation Board Member

Happy Holidays all. If you are a regular reader of my contributions, you will know that I am smack in the middle of my favorite time of year - fall! As I write this, Navy is 6-0 facing Notre Dame (yeesh – fingers crossed), Army is also undefeated leading up to an amazing show down of the Armed Forces in contention for the Commander-InChief’s Cup. I will have embarrassed myself dressing up as Prince Charming opposite my six-year-old daughter dressing up as Mal from the Descendants - don’t judge, I made that costume as conservative as possible for her - for Halloween, and oh yeah, I moved inside a bottle of Ketal One Vodka since mortgage rates sharply increased after the September Federal Reserve rate cut.

This move has puzzled the average consumer as they falsely believe that the Federal Reserve controls mortgage rates, as the media and marketers would have the public believe. If you have read previous articles of mine, you likely remember my being a broken record about how mortgage interest rates are derived from mortgagebacked securities and not the Federal Reserve. The Federal Reserve controls the Federal Funds Rate and the Federal Prime Rate, but NOT mortgage rates. I figured this was a

perfect time for a refresher and further commentary.

Please forgive me off the bat as I will be oversimplifying certain aspects of investing and investing terms. So, what are mortgage-backed securities? I am so glad you asked. A mortgage-backed security is when a bank or lending institution sells a group of loans from one institution to another. For our simplified purpose, think of when you have had a mortgage sold or transferred from one bank to another. The first bank is “pooling” together 1,000, 5,000, 10,000 etc. Fannie Mae 30 Year Fixed Mortgages, or VA 15 Year Fixed Mortgages, and selling them from the first bank to another bank or servicing institution. These pools of loans are bought and sold as mortgage-backed security bonds.

If we want to oversimplify investing, we can think of two investing tools or instruments: stocks and bonds. If you own a stock, you don’t own anything tangible, you have a sheet of paper that says you own one billionth of IBM, and if IBM makes money, you make money; if they lose money, you lose money. It is not secured by anything and therefore has higher risk, and with that higher risk comes the potential for higher highs or lower lows. On continued on next page

the other hand, a bond is an investment instrument that is secured or guaranteed by something. A government bond that grandma used to give you was guaranteed to pay out based on the full faith and credit of the Federal Government. Mortgage bonds are pools of mortgages that are bought and sold as bonds because if a consumer doesn’t pay their mortgage, the bank will foreclose on the property, sell it, and get their money back that way. Therefore, these mortgages are secured by the homes or real estate they are written on. Based on these instruments being secured - or safer - bonds will traditionally not pay out as aggressively as stocks.

Traditionally, but not always, these two markets (the stock and bond markets) will perform opposite of each other. If the stock market is doing well, investors, and I am talking big investors, hedge fund managers, and retirement portfolio managers - not people like you and I - will pull their money out of lower performing bonds and put that money to work in the stock market. On the other hand, if the stock market is doing poorly, investors will put their money into the “safe haven” of the bond market. This is why it is very common to see falling mortgage rates at a time of poor economic growth or hardship and rising rates at a time of strong economic growth. Again, not always, but as a generalization.

most economists believe this was the right thing to do. However, when you print money like this and people are not technically “earning” it, you are bound to see inflation, and boy, did we. It was not long ago that we were paying $8 for a dozen eggs, $5 gallon of milk, everything seemed to be very costly at a time that we were just getting back to work and gaining a sense of normalcy. This hyperinflation was the kicker to reverse the market. Think of bonds that in general don’t make much money in the first place. When inflation is bad, i.e., the value of the dollar decreasing, bonds are technically making even less money. Bond investors absolutely hate this. Their investments are decreasing in value.

Ironically, this is one of the times that marketers would’ve been better off speaking the truth:

The period around COVID is a great case study. Directly at the onset of COVID, mortgage rates fell, and for two years, we experienced the lowest mortgage interest rates in history. There are several factors around this, but one big factor is that investors, both home and abroad, were scared to death. People were not working - they were getting furloughed, or worse, laid off or let go. People were getting ill, hospitals were at capacity, people were passing away at alarming rates. This caused global panic in economic markets. So, what do investors want to do? They want to dump their money into the “safe haven” of bond markets. Again, this is a simplification, but true. With this surge in bond investing came the record low rates that we saw.

“Although Federal Reserve to cut rates, economists believe mortgage rates will increase, lock in now”.

Now let’s look at the Federal Reserve’s rate cut in September and the subsequent mortgage rate increase immediately following. The media and marketers would have the public fooled into believing that mortgage rates are going to keep falling as the Federal Reserve is cutting rates. First, think of the source. As a media outlet, your job is to get viewers and clicks. Which headline do you think will get more views: “Federal Reserve to cut rates, mortgage rates to fall further” or, “With Federal Reserve rate cuts, mortgage rates to stabilize or increase”. People want to read what they want to be true. Ironically, this is one of the times that marketers would’ve been better off speaking the truth: “Although Federal Reserve to cut rates, economists believe mortgage rates will increase, lock in now”. So many times, I listen to mortgage ads on the radio or online and I want to scream at the mistruths they are claiming, all to get the phone to ring and the internet inquiries to come in.

Fast forward two years to the beginning of 2022. The world was beginning to get back to a semi-version of normal. For the past two years, our government had been printing money to prevent both a national and global economic collapse. While this would prove to be painful,

Now that we have questioned our sources of information, let’s examine why this happened. First, if you recall the time leading up to the actual rate cut, the headlines were all about the upcoming Fed meeting and their imminent rate cut, the only question was, would it be .25% or .50%. Those same economic factors that were leading up to the Fed cutting their rates are the same economic factors that would cause mortgage rates to go down, and down they went. Rates fell for close to two months in advance of the actual rate cut. I had locked a 5.375% 30 Year Fixed Conventional Loan with only .25% in discount three days prior to the cut. The lowest I have done since 2021.

continued on next page

So again, why did mortgage rates rise after a Fed rate cut?

This is where it is important to look at WHY the Fed is doing what they are doing and not just their actions. When reading the Federal Reserve’s remarks following the meeting, the following were their main concerns: First, inflation. Again, inflation is the enemy of bonds and although the Fed noted that inflation was improving, it was still not where they wanted it to be. Next, oil prices. We have seen a lot of volatility in the oil markets recently, with oil prices sharply increasing in the days and weeks leading up the Fed’s decision, this is another indication of inflation not being where it should be. Lastly, there hadn’t been a lot of buying demand of US debt leading up to the Fed’s decision, meaning, not a lot of demand to be purchasing these mortgage-backed securities that I am such a broken record about. It is because of the Fed’s commentary after their meeting that we saw rising rates even though they chose to cut their own rates.

So, let’s try to summarize this long diatribe of boring information. We know that the Federal Reserve does not control mortgage interest rates and that mortgage interest rates are derived from the buying and selling of mortgagebacked securities. In general, but not always, these mortgagebacked securities that are sold as bonds will perform opposite of the stock market. Therefore, with good economic news that benefits the stock market, our mortgage-backed securities bond market will often suffer, causing mortgage rates to

suffer. Leading up to the September Federal Reserve’s decision to cut rates, it was very public that this was about to happen based on improving inflation and multiple Fed Chairmen and Chairwomen publicly speaking about the likely Fed moves. Then, BOOM, the Fed cuts rates and publishes their comments behind their cuts and scares bond investors again. With inflation still being a concern, oil volatility due to increased tensions in the Middle East (we haven’t even gone there), there are enough outstanding economic factors remaining to ensure that mortgage bond investors are not in the clear by any means. And therefore, ultimately, this is how I ended up in the shortest mortgage refinance boom in my 22-year career. If that is clear as mud and you would like further commentary on this topic, feel free to reach out to me anytime.

Stay tuned for next quarter’s article on how to polish up your resume and the positives of collecting trash on the side of the highway.

Mathew Schulz, CML, is the President of Firelight Mortgage Consultants in Greenwood Village, Colo., a mortgage company that he has owned for 15 years. He is also a board member of the CAR Foundation. You can reach him at mschulz@FirelightMortgage.com.

How Can Two Appraisers Value the Same Property Differently?

By: Melanie J. McLane, ABR, RAA

A variety of factors—including timing, purpose of the valuation and comparable sales used—can lead to disparities.

One of the most frustrating things for consumers, agents, and even appraisers involved in a real estate transaction is seeing disparate results in two or more appraisals of a property. Dig beneath the surface and you’ll often find good reasons for the differences. Here are factors to consider as you try to understand the two different opinions of value.

ESTIMATED VALUE ISN’T ALWAYS MARKET VALUE

First, check the date of the appraisals. Appraisals typically have a short shelf life. In a volatile market, one that’s more than six months old will be hopelessly out of date. Even a more recent appraisal may become outdated because of a sudden economic shift, natural disaster, or other occurrence. So, if a property owner supplies you with a pre-sale appraisal, check the date. The date that really matters is the effective date of the appraisal, which may not be the same date the appraiser inspected the property. In the case of an estate appraisal, for example, the effective date is generally the date of the owner’s death, which could be several months, or even years, before the inspection.

Second, check the intended use, intended user and type, and definition of value. Appraisers must identify all three as part of their scope of work. If the intended use is “for insurance purposes” and the definition of value is “replacement cost of improvements,” then that appraisal is not valid for establishing an asking price to sell the property. Some of the other types of value that appraisers may be asked to estimate, to name a few, include:

• Value in use (the value of the property based on its current use)

• Retrospective value (the value of a point in the past, such as before a divorcing couple separated)

• Value of a partial interest

• Liquidation value

None of these are the same as current market value.

Third, consider the highest and best use. You are likely familiar with this concept, which requires an appraiser to determine the one use of the property that is physically possible, legally permissible, financially (economically) feasible, and maximally productive. Here’s an example: An agent lists a small mobile home park. He assumes the highest and best use would be to subdivide it into three building lots. An agent, who is also an appraiser, brings the buyer. At the closing, the listing agent says, “So, you’ll get rid of those trailers and sell the lots, right?” [A subdivision had been approved.] The buyer says, “No, my agent and I analyzed the income and the return from the mobile home lot rentals, and it’s more profitable to simply keep it the way it is.”

RECONCILING DIFFERENCES OF OPINION

If the lender has reason to believe the appraisal work contains errors or the opinion reflects bias, the lender could request a reconsideration of value (ROV) by the appraiser. That’s a step we could see more frequently in the future as the result of a rule issued in late July by federal regulators— Comptroller of the Currency, Federal Reserve, Federal Deposit Insurance Corp., National Credit Union Administration, and Consumer Financial Protection Bureau. The new rule outlines how lenders can incorporate ROVs into their processes and offers sample policies and procedures to identify, address, and mitigate the risk of discrimination.

But there’s also a scenario in which you could encounter two current appraisals with different valuations, even though the definition of value, intended user and intended use are the same.

Say a property is under contract for $550,000, and the appraiser’s opinion of value comes in at $500,000. If the parties won’t renegotiate the price, the contract most often falls through. Subsequently, the property goes under contract with a new buyer, again for $550,000. The lender obtains a new appraisal, and the opinion of value comes in at $560,000. The first appraisal was 9% below the contract price, while the second appraisal is roughly 2% above the contract price.

WHY MIGHT THAT OCCUR?

A review appraiser would look at a range of factors.

First would be comparable selection. Did each of the appraisers select and use comparable sales that have, per Fannie Mae’s requirement, “similar physical and legal characteristics when compared to the subject property”? Were any potential comparable sales overlooked? Did the appraiser comment on sales that were not used because the appraiser had information about those sales that made them less reliable than other sales? An example might be any of these: a non-arm’slength transaction, a transaction in which a stigma affected the property’s resale value, or a transaction in which condition issues affected the value but didn’t show up in exterior images.

Second, the review appraiser would look at how the comparable sales were adjusted. Adjustments are changes made to the value of a comparable property to account for differences between it and the subject property. Are the adjustments defensible? Let’s say an appraiser adjusts a comparable property down $4,000 because it has two-and-a-half baths but the subject property has only two. The reviewer will look to ensure the adjustment was based on the market reaction—the difference a typical buyer in the that market has paid for a home with an extra half bath, all other things being equal—rather than on the cost of adding one. Did the appraiser inadvertently “double dip,” i.e., adjust twice for the same issue? I’ve seen an example in which an appraiser adjusted in two places for a home having only two bedrooms—once when noting the bedroom count and once when spelling out “functional flaws.”

Were the adjustments consistent, and, if not, was there an explanation for why they were not? Let’s say the appraiser adjusted for additional acreage on the property and used an adjustment of $6,000 per acre on one comparable sale but only $2,000 per acre on another. To understand the inconsistency, the review appraiser will look for an explanation in the comments, e.g., “The acreage adjustment for comparable sale 2 is different from that for comparable sale 1 because the additional acreage for sale 1 is flat and useable, but the topography of sale 2 is a steep bank both in front of and behind the house, reducing the useable space.”

Finally, the review appraiser will pay attention to how the appraiser reconciled market data. For each comparable sale used in an appraisal, the appraiser notes gross adjustments and net adjustments and calculates them as a percentage of the comparable sales price. Gross adjustments are all adjustments added together, regardless of whether they are negative or positive; net adjustments factor in whether an adjustment is negative or positive. So, if an appraiser adjusts a sale –$5,000 for an out-of-date kitchen but +$2,000 for having more usable land, the gross adjustment would be $7,000 but the net adjustment would be -$3,000. If the comparable sale price was $100,000, the gross adjustment percentage would be 7% and the net adjustment percentage would be –3%. Lower gross and net adjustments could indicate that the comparable sale is more similar to the subject property; however, they could also indicate that the sale was under adjusted.

The appraiser’s reconciled value must be somewhere in the range of the adjusted comparable sales—it can’t be lower than the lowest adjusted price, or higher than the highest adjusted price. The appraiser should explain how and why they reconciled to their final value. So, the next time you’re scratching your head about how two appraisal reports on the same property can result in different estimates of value, think about the detailed nature of appraisals, and do a little digging. You’re likely to find the answer in the reports themselves.

Melanie J. McLane, ABR, RAA, is broker of record for Jackson Real Estate in Jersey Shore, Penn., and a Pennsylvania certified residential appraiser. Article originally published by REALTOR® Magazine, a publication of the National Association of REALTORS®. Republished with permission from the National Association of REALTORS®.

Silver Certif ication: Simplifying and Elevating the Moving Experience for Seniors

Reaching retirement age is a significant milestone. However, many seniors face physical limitations that affect their daily activities. Relocating to a new home or retirement community without assistance can be challenging and potentially hazardous. Fortunately, Exodus Moving & Storage is among the few companies to hold this prestigious certification and will help with the heavy lifting.

WHAT IS SILVER CERTIFICATION?

Silver Certification is a distinguished qualification resulting from an intensive training program developed by the National Association of Senior Move Management Specialists (NASMMS), in partnership with Wheaton Worldwide Moving Van Line. This program encompasses various aspects critical to serving older adults, including understanding family dynamics, cultural differences, emotional and physical awareness, empathy, and effective communication with third parties. Exodus Moving & Storage takes pride in crew members who diligently complete this training over a four-week period. Each Silver Certified move is led by a certified crew member to ensure the highest standards are maintained. Additionally, the team goes the extra mile by engaging with retirement community administrators to identify and address specific challenges faced by new residents. One notable improvement that has been implemented is ensuring all cords remain attached to their respective devices during moves, alleviating a common frustration for seniors and staff alike.

THE VALUE OF SILVER CERTIFICATION

company like Exodus Moving & Storage, which holds Silver Certification, ensures they receive the utmost care and professionalism. Certification signifies that the Exodus Moving & Storage team is well-equipped to manage the unique challenges associated with moving older adults, providing peace of mind for both you and your clients.

SERVICES OFFERED BY EXODUS MOVING & STORAGE:

1. Full-Service Assistance: Comprehensive support from packing and unpacking to handling heavy items, ensuring a smooth transition to a new living space.

Silver Certification is crucial because moving can be particularly challenging for seniors, involving both physical and emotional strains. Older adults often possess more belongings, many of which carry significant sentimental value. The process of packing, downsizing, and relocating heavy items requires not only physical effort but also emotional sensitivity. Through Silver Certification, Exodus Moving & Storage demonstrates a profound understanding of these complexities. Training ensures that the team can handle the emotional and physical challenges that come with moving later in life, making the relocation experience as seamless and stress-free as possible for clients. Your clients rely on your expertise and trust your recommendations. Referring them to a moving

2. Tailored Solutions: Personalized moving solutions for various scenarios, whether transitioning to a local retirement community, downsizing, or moving across the country.

3. Emotional Consideration: Respecting and handling the emotional weight of moving cherished belongings and memories with care and empathy.

BACKGROUND: EXODUS MOVING & STORAGE

Founded in 1996, Exodus Moving & Storage is a family-owned, locally operated, Community Involved company with national connections. Located in the heart of Colorado, we are committed to our community and have supported numerous local organizations, including those aiding youth, military families, and the unhoused. Our dedication to promoting local art further underscores our commitment to enriching the community we serve.

By achieving Silver Certification, Exodus Moving & Storage underscores our ability to assist older adults effectively. Our emphasis on empathy, professionalism, and dedication to making moves stress-free makes us a trusted partner for seniors embarking on the next chapter of their lives.

For more information on how we can assist you and your clients, please visit our website, or contact us directly. Exodusmoving.com 970-484-1488.

WILLIAMS UNDERWRITING GROUP

2025 INDEPENDENT CARRIER REAL ESTATE ERRORS AND OMISSIONS PROGRAM

KEY POLICY FEATURES:

• Choice of Limits of Liability for both individual and firm licenses of $100,000/$300,000, $250,000/$750,000 or $500,000/$1,000,000.

• Deductible is $1,000 each Claim. Each licensee pays this deductible. There is no deductible for claim expenses. Only one deductible applies if a claim involves multiple licensees with the same firm.

If you do not renew your insurance on time, the Colorado Real Estate Commission may place your license on inactive status. Payment must be received by WUG no later than December 20, 2024, to assure your insurance certification to the Colorado Real Estate Commission before their deadline.

Neither WUG nor the insurance company will be responsible for any delay in the issuance of a license or Certificate of Coverage where forms are received after December 20, 2024. All premiums are fully earned at the inception of the policy period (No Refunds).

Licensees who do not obtain insurance by January 31, 2025, will lose any previous established retroactive date (i.e., “prior acts” coverage). Your new retroactive date will be the 1st of the month in which your payment is received, coinciding with your effective date.

Williams Underwriting Group (WUG), A Division of Accretive Specialty Insurance Solutions, LLC is pleased to announce that we will continue to provide real estate errors & omissions coverage in 2025 for Colorado licensees and Firms. For the past twenty-six years WUG has understood the importance of providing quality claims-made E&O coverage to Colorado real estate licensees. Our policy will continue to be underwritten by Continental Casualty Company, a CNA insurance company (rated “A” by A.M. Best). WUG continues to be the exclusive real estate errors & omissions insurance provider for the Colorado Association of REALTORS® (CAR) with additional benefits for CAR members. www.wugieo.com/colorado-resources/colorado/

• Lock Box Property Damage Limit of $100,000 per claim / $300,000 aggregate. There is no deductible for Lock Box coverage.

• Discrimination/Fair Housing Limit of $25,000 per claim / $25,000 aggregate (damages)

• Escrow/Earnest Money Sublimit of $10,000 per claim and $25,000 aggregate (damages)

• Defense Outside Limits There is NO LIMIT on the amount of defense costs the carrier will pay in connection with claims covered under the basic policy.

• Property Management Services, as defined in the policy, are automatically included. Coverage does not extend to unlicensed employees who perform Property Management Services.

• And more! Learn more here

MARKET TRENDS

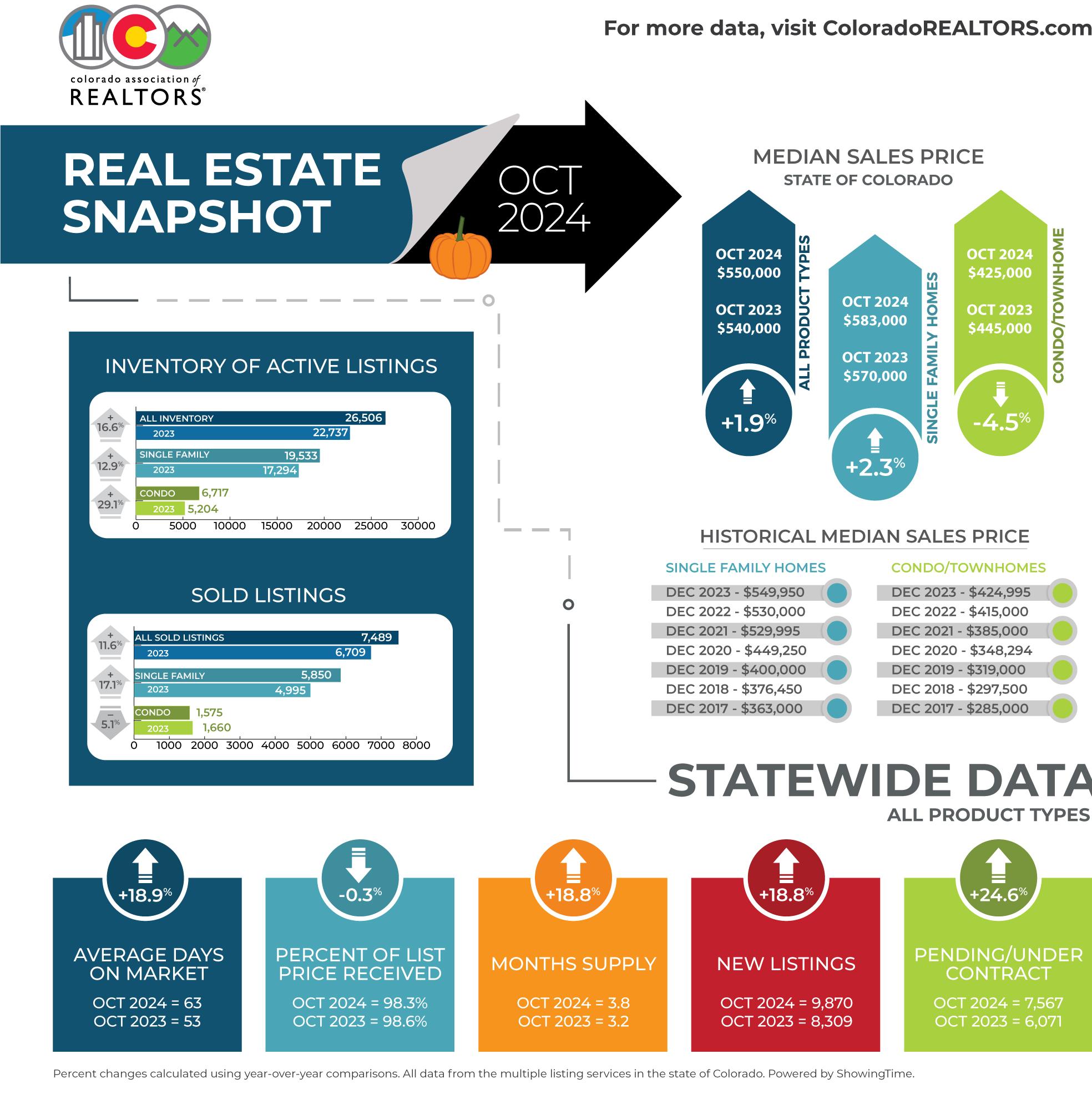

Subdued Home Buyers and Sellers Push Inventory Higher Across the State as the Waiting Game Continues

INVENTORY OF ACTIVE STATEWIDE = 26,506

Parties on both sides of the housing transaction continued their waiting game going into the early November election, keeping a close eye on not just the results of the presidential election, but speculation about further interest rate reductions, the economy, and geo-political factors as well. These elements all contributed to a very cautious pool of homebuyers and helped push inventory higher in markets statewide, according to the latest Market Trends Housing Report from the Colorado Association of REALTORS® (CAR) and analysis from the Association’s spokespersons across Colorado.

“While Denver has consistently been characterized as a seller’s market throughout recent years, current trends indicate a moderate shift toward a buyer’s market this winter season,” said Denver-area REALTOR® Cooper Thayer. “With 3 months of single-family inventory and over 5 months of townhouse/ condo inventory on the market, we’re seeing a changing negotiation dynamic in our transactions. Average time on market rose to 42 days last month in the City and County of Denver, its highest level since February, and around 80% higher than the typical October figure over the past 3 years. This has provided buyers with more leverage and more time than usual, a great position to be in a negotiation.

Despite the potential buyer advantages, their behavior continues to be governed by caution.

“Buyer demand continues to be subdued, leading many sellers to reduce their prices in an effort to attract interest,” said Boulder/Broomfield-area REALTOR® Kelly Moye. “While there were initial hopes that market activity would pick up after the election, it's still too early to draw any conclusions, as the anticipated surge in buyer engagement has yet to materialize. While some buyers are taking advantage of the situation,

others continue to wait. Most REALTORS® anticipate a busy first quarter of 2025 when this pent-up demand will finally absorb the inventory and our market will be more robust.”

Inventory of active listings is up 14% year-over-year in the seven-county Denver metro area, and up 16.6% statewide. At 3.5 months’ supply of inventory in the Denver-metro area and 3.8 months statewide, the supply continues to hover at levels not seen in more than a decade.

“An enormous number of buyers (and sellers) are just waiting in the wings during this high-interest rate phase in our economy,” said Fort Collins-area REALTOR® Chris Hardy. “Pentup housing demand is like holding your thumb over the end of a water hose,” Your thumb (high interest rates) is stopping the natural flow of the water (real estate sales), but the pressure builds up behind your thumb until the water starts to squirt out the sides. This is what we’re seeing in the real estate market right now.”

The pent-up demand and inventory increase are having little to no effect on median pricing.

Arapahoe County has a median price of $599,000 with almost 1,300 single-family residential homes on the market. Aurora has a median price of $529,000 and 1,053 homes currently on the market. While the number of sold properties are up, the number of days on the market are also up. This is good news for buyers who may have a little more time to make a decision, and more inventory to choose from with prices remaining very close to pricing from this time last year.

“It seems that the townhome/condo market is offering buyers great choices and seemingly significant price reductions over this time last year. A home for the holidays is a great opportunity for buyers right now with the option to possibly sleep on the choices. This is an option that buyers simply have not had for several years,” said Aurora REALTOR® Sunny Banka.

Looking at the statewide market, sold and pending/under contract homes were up significantly from a year prior and despite the volume of active inventory, it was not enough to keep year-over-year median pricing from ticking up in the single-family home category.

LOCAL MARKET SUMMARIES

Taking a more in-depth look at some of the state’s local market data and conditions, the Colorado Association of REALTORS® Market Trends spokespersons provided the following assessments:

AURORA

“There’s some good news for Aurora-area buyers as they welcome more housing inventory and choices not seen in perhaps more than a decade. Inventory in most Aurora, Adams County, Arapahoe County and Centennial zip codes is up. Sold inventory is also up, which indicates that buyers are absorbing much of the additional inventory. Sold prices are relatively flat with most Aurora Zip Codes seeing only a 2-3% increase over this time in 2023. Adams County is at a median price of $530,000 with approximately 1,300 homes on the market.

BOULDER/BROOMFIELD COUNTIES

“In Boulder and Broomfield counties, the current real estate market is characterized by a 14% increase in active listings with homes sitting on the market for an average of 55 days. Despite more inventory, home prices remain relatively flat compared to this time last year, with the average sales-priceto-list- price ratio holding steady at 98%. Buyer demand continues to be subdued, leading many sellers to reduce their prices in an effort to attract interest. While there were initial hopes that market activity would pick up after the election, it’s still too early to draw any conclusions, as the anticipated surge in buyer engagement has yet to materialize.

“The expected interest rate reduction never came, and the election caused ‘buyer anxiety’ which slowed the market and created a sluggish real estate environment. Areas of opportunity seem to be in the attached dwelling market where there are 20% more new listings in Boulder County, and a whopping 33% more listings in Broomfield. Buyers hoping to purchase a townhome or condo have options and motivated sellers are offering their listings at affordable prices. While some buyers are taking advantage of the situation, others continue to wait. Most REALTORS® anticipate a busy first quarter of 2025 when this pent-up demand will finally absorb the inventory and our market will be more robust,” said Boulder/Broomfieldarea REALTOR® Kelly Moye.

continued on next page

COLORADO SPRINGS

“Have we seen the first break in trend that may bring some reprieve to buyers? Maybe, maybe not. The good news is we sold 21.4% more listings year-over-year, but we were also up 30% on active listings across the Pikes Peak Region. The median price fell year over year for all properties. Although it is just one month, and it only fell 2.4%, could this be the start of the reprieve some buyers are waiting for? With days on market continuing to stack up, and price drops hitting the market daily, it will be a trend to watch as we work through the next few months. Nationwide though, median price rose 3% from a year ago.

“Many thought that the election was holding buyers and sellers up. Although I don’t personally believe this was true. The economy is hard, prices are high, and buyers are very cautious. The data coming out in October showed why there is apprehension in the economy. Only 15% of small firms planned on hiring over the next 3 months. The share of small business owners saying it was hard to fill jobs also fell to 34% - the lowest since 2021. Mortgage rates stayed elevated, and after the election results were made final, rose further. U.S. consumers saw a 14% chance of missing a debt payment in the next 3 months, the highest since 2020. Americans earning less than $50,000 a year saw a 20% chance of delinquency. And for those making over $100,000, they saw an 8.4% chance, which was the highest since 2014. Debt is breaking the backs of the consumer, businesses, and the country. We could drop a long list of retail and restaurant chains that are either closing stores or admitting they have seen major consumer weakness.

“Looking into the future, the Federal Reserve dropped rates .25% again in November. I don’t think this will change much, but it should be noted for our report. We must continue to keep an eye on the commercial mortgage-backed securities market. The delinquencies there are continuing to rise. Unless we can figure out our debt issue, the rest seems futile. And let’s not forget, foreclosure moratoriums are on track to end at the end of the year. Can a new sitting president curtail all of this? I know many are hopeful. But the economy is a massive machine that is not easy to turn. Does housing avoid the rise in delinquencies that other parts of the economy are already seeing? Usually not. It will be an epic year ahead to watch and cover the housing market and economy,” said Colorado

Springs-area REALTOR® Patrick Muldoon.

“In the Colorado Springs housing market, the incremental increase in supply has raised the supply level to 3.4 months; in October 2021 and 2022, it was 0.6 and 0.5 months, respectively. This elevated level of supply is highly desirable because, in a normally balanced market, the supply level is between 4 and 6 months. Buyers currently have excellent opportunities due to high inventory levels, motivated sellers, and dropping interest rates.

“On the other hand, the election made it abundantly clear that the economy and affordability remain a hugely significant challenge for the American people. The highly unpredictable election introduced a significant level of caution among buyers and sellers, with many stepping aside, waiting for the outcome. The president-elect, during his campaign, made weighty comments about the need to improve housing affordability and supply. However, significant concerns among economists, home buyers, and sellers remain about potential impacts on housing affordability due to the president-elect's anticipated proposal for higher tariffs on imports, which usually lead to increased consumer prices and inflation. Regrettably, this can radically fuel the wait-and-see posture among home buyers,” said Colorado Springs-area REALTOR® Jay Gupta.

Active Listings – Supply: In October 2024, the number of single-family/patio homes for sale in the Colorado Springs area was 3,394, representing a tiny 0.1% increase monthover-month and a whopping 35.5% increase year-over-year, and the highest level of inventory in September since October 2015. Overall months’ supply of active listings was at a healthy level of 3.4 months. For homes priced under $400,000, supply was 2.9 months; homes between $400,000 and $600,000 at 3.0 months, homes priced between $600,000 and $1 million at 4.1 months, and 6.5 months for homes priced over $1 million.

Sales – Demand: There were 998 sales of single-family/patio homes in October 2024, compared to 933 in the previous month and 851 in October last year, representing an increase of 7.0% month-over-month and a healthy 17.3% year-over-year. The monthly sales volume was up 11.5% month-over-month and 17.4% year-over-year. The year-to-date sales volume was down 3.1% compared to last year. However, looking back 10 years to October 2014, the monthly and year-to-date sales

continued on next page

volumes are up 123.1% and 122.8%, respectively.

Days on the Market: The average number of days on the market in October 2024 was 44, the same as last month and 45 days in October last year.

Price Reductions: In October, 44.2% of active listings in El Paso County and 30.7% in Teller County had price reductions.

Sales by Price Range: Last month, 26.3% of the homes sold were priced under $400,000, 45.9% between $400,000 and $600,000, 22.2% between $600,000 and $1 million, and 5.6% over $1 million. Year-over-year in October 2024, there was an 18.5.0% increase in the sale of single-family homes priced under $400,000, a 14.2% increase in homes priced between $400,000 and $600,000, a 23.3% increase in homes priced between $600,000 and $1 million, and a 9.8% increase in homes priced over $1 million

Average & Median Sales Prices: Last month, the average sales price of single-family/patio homes was $557,741 compared to $535,023 in the previous month and $556,964 in October last year, representing a 4.2% increase month-overmonth and only 0.1% year-over-year. The median sales price dropped to $475,000 from $485,000 in the previous month and last October, indicating a decline of 2.1% both monthover-month and year-over-year. In October 2024, the average prices reached a record high level compared to any October previously.

CRESTED BUTTE/GUNNISON

“The real estate market in the Gunnison – Crested Butte area has been kind of a rollercoaster. We started the year a bit busier than 2023 and then things really slowed down as we headed into the summer. This is typically our busiest time of year, so it was concerning when July brought lots of visitors to town, but not much real estate activity. Things started to pick up again in late August and the showing and contract activity has continued into our off-season. Overall, the year is on track to have the same number of sales as 2023, but there is more under contract so we may end up slightly ahead.

“Our inventory is up slightly overall, but not substantially. On average, prices continue to remain steady. In some specific

areas and property types, average sales prices are down as much as 2-4% and some are up as much as 10%. Remember that average prices are just that and because we don’t have huge numbers of sales, it will be important to look at sales in the last year when determining the value of your property and to be as targeted as possible when making calculations.

“Many sellers have taken their properties off the market for a couple of months to get a fresh start when ski season starts. As we prepare for 2025 and the coming winter, it is likely that more properties will come up for sale and that buyers will continue to look to the area as a special Colorado ski town where they want to spend time. A “wait and see” strategy could likely mean paying more and having more competition when you make an offer – especially for properties that are priced correctly. Real estate in the area continues to be a good investment, but more importantly, this area continues to be a place where life is good and people want to be,” said Crested Butte -area REALTOR® Molly Eldridge.

DENVER COUNTY

“While Denver has consistently been characterized as a seller’s market throughout recent years, current trends indicate a moderate shift toward a buyer’s market this winter season. With 3 months of single-family inventory and over 5 months of townhouse/condo inventory on the market, we’re seeing a changing negotiation dynamic in our transactions. Average time on market rose to 42 days last month in the City and County of Denver, its highest level since February, and around 80% higher than the typical October figure over the past 3 years. This has provided buyers with more leverage and more time than usual, a great position to be in a negotiation.

“While pricing has remained steady in the single-family market, the townhouse/condo market has been particularly impacted by high levels of inventory. Median sales prices came in at just $400,500 for the month of October, a 12% decline from last year. For comparison, single-family median sales prices are up from last year by about 2.3%, at $675,000 for the month. But prices alone don’t tell the whole story. Over 55% of closed transactions in Denver in October logged seller concessions, with an average concession amount of $8,760. This means, on average, net pricing has actually decreased by

around $4,000 per transaction on average beyond the posted decrease in sales price.

“We’ve seen buyers taking advantage of this more favorable environment, utilizing the competition between sellers to seek out better deals. The average list-to-close price ratio in Denver last month was just 98.2%, meaning on average, buyers were able to close on their homes for 1.8% below asking price. With election uncertainty now behind us, it looks like we may be setting the stage for a busy spring. However, interest rates, insurance premiums, and HOA costs are still challenges for buyers to overcome, and spring activity will likely be contingent upon some relief in those areas,” said Denver County-area REALTOR® Cooper Thayer.

DOUGLAS COUNTY

“Even in this challenging market, Douglas County continues to prove its exceptional desirability, posting near-record sales prices last month. Median close prices in October rose 5.1% month-over-month to $725,000 – just shy of the alltime monthly record of $731,000 experienced in April 2022. Despite the number of sales remaining at relatively normal levels, overall transaction volume exceeded $400 million last month, the first time October sales reached that level since 2021.

“Patience has proven to be the key in this market, with over 3 months of inventory for sale and affordability challenges creating hurdles for new homeowners. Listings in Douglas County spent an average of 50 days on the market in October, marking a roughly 100% slowdown from the summer season. Slow isn’t bad, though, and we have found certain adjustments in strategy to keep clients successful in this environment. One piece of advice to sellers is to emphasize differentiating your listing from the abundance of supply on the market.

“Today’s homebuyers have much more time to make decisions and negotiate and are spending a higher percentage of their income on housing costs, driving them to be much more costconscious. The most successful listings today are those that are more unique and/or put in more preparation work than comparable properties on the market. Sellers should focus not only on addressing potential areas of concern before listing, but also consider going ‘above and beyond’ to make their listing stand out more,” said Douglas County-area REALTOR® Cooper Thayer.

DURANGO/LA PLATA COUNTY

“October started out with a flurry of closings, but by the end of the month, winter weather had arrived and with it, we saw quite a few active listings withdraw for the season. This was especially pronounced in our rural areas. Even with homes withdrawing from the market, looking at our numbers, La Plata County has quite a bit more home inventory than last year at this time. Purgatory and Vallecito resort areas are firmly in the buyer’s market category with at least 7 months of inventory. In-town, Durango clearly remains a seller’s market hovering around a 3-month supply, and it is also the only area with any significant median increase in 2024.

“As we see in every presidential election cycle, some buyers with discretionary income will hold off on home purchases until the election has been decided. We expect these buyers to return to purchase soon.

“The only thing you can count on about the La Plata County real estate market is the quiet time between Thanksgiving until after the first of the year, and we are now headed into that season for home sales outside of our resort market. That resort market exception is where we look forward to a busy winter season with Purgatory opening weeks before we usually have significant snowfall. Our visitors will soon be on their way for holiday shopping of homes, hopefully boosting our sales up north which had a less than stellar summer season.

“Of note this past month is the affordable inventory coming on market, with new deed restricted subdivisions and dozens of move-in ready homes in Bayfield and Ignacio that are easing a fraction of the housing strain of our working community,” said Durango-area REALTOR® Heather Erb.

FORT COLLINS

“’Simba! You are more than what you have become!’ These words of warning came from the late great James Earl Jones voicing the character of Simba’s father, Mufasa, in Disney’s Lion King. This warning applies to our current housing market as we stand on a precipice overlooking a host of frothy economic data following the conclusion of the long-awaited presidential election.

“Let’s start with the economy since that’s the primary driver of what determines mortgage interest rates. Broadly speaking,

the U.S. economy is on solid footing with inflation hovering near the Federal Reserve’s target rate of 2%. The unemployment rate for October is just over 4% - a level that indicates a bit of balance between jobs available and job seekers (the Fed doesn’t like an overly hot job market). Consumer spending remains robust. All of these indicators led the Fed to reduce their rate by .25% at their most recent meeting. One might think that with all this rosiness, mortgage interest rates would also participate in this economic-feel-good-vibe. Sadly, no.

“Wall Street investors had already priced in the quarter point reduction weeks ahead of the recent Fed meeting, so those who closed on homes in early October and had locked down their rate in late September received the lion’s share of lower mortgage rates. At the time of this writing, the stock market has rallied based on the election being over but major investors have flocked to the bond market in anticipation of the next presidential administration’s proposed economic policy which is perceived to be inflationary, causing the government to likely need more money to pay its bills. This is pushing the yield of 10-year treasury notes higher, which in turn, drives up the cost of 30-year mortgage interest rates.

“What does this have to do with our market being more than what it has become? If you consider that a humongous number of buyers (and sellers) are just waiting in the wings during this high interest rate phase in our economy, pentup housing demand is like holding your thumb over the end of a trickling water hose. Your thumb (high interest rates) is stopping the natural flow of the water (real estate sales), but the pressure builds up behind your thumb until the water starts to squirt out the sides. This is what we’re seeing in the real estate market right now. Some buyers are willing to accept a higher interest rate now because they know they might have a more competitive opportunity to get a house they want without having to compete as aggressively as they would when the thumb comes off the end of the hose and all the buyers are in the market looking for homes at the same time.

“This is why we are seeing such paradoxical numbers in the sales data right now. Sales in Fort Collins were up 29% yearover-year – but that is to be expected since it was this time last year that we saw the severest drop off in sales due to the previous year’s spike in interest rates. In September 2024, when interest rates started to drop into the mid to low 6% range,

buyers jumped in quickly. Sellers saw this as an opportunity and decided to put their houses on the market so they could take advantage of the lower rates for their replacement property purchase (listings are up nearly 9% year over year). That’s also apparently why the median sale price has crept up to $628,850 year over year. Year-to-date, the median price is up just 2.2%.

“Combine those numbers with a clear economic demographic shift and you’ll see the bulk of houses being sold right now are to home buyers less sensitive to interest rate fluctuation. The vast majority of homes being sold in our area right now are in the $500,00 to $1 million range and the year-over-year sales numbers in that price band are all in positive territory. This tells us that the majority of buyers in the market right now are those buyers who have the wherewithal to withstand higher interest rates from money they have in other investments, money they have cashed in on the increase in value of their existing homes, or the money they have enjoyed since the post-pandemic bump up in wages.

“Time can only tell how long the high interest rate thumb will remain over the housing sales hose. But when interest rates come down into the low 6% range, as some economists are predicting for 2025, prepare for our market to be more than what is has become,” said Fort Collins-area REALTOR® Chris Hardy.

GLENWOOD SPRINGS/GARFIELD COUNTY

“Fall In the Roaring Fork and Colorado River valleys did not bring a substantial change in new listings over last October. In the single-family sector, new listings were down 10%, with 58 new homes entering the market compared with 65 in 2023. Pending sales remain steady with 59 homes under contract versus 55 last October. Days on market did see a substantial adjustment from 92 days last October to 69 days this October. The most significant change in the market came to our buyers in the trenches and median home price. The median home price in October 2023 was $590,000. This October, we saw an increase of 23.5% for a median sales price of $728,400. The month of October ended with 181 active single-family homes on the market which equates to a 3.4-month supply.

“The multifamily sector saw similar lack of excitement with 20 new listings coming on in October compared to 16 in 2023. There were 20 multifamily units under contract at the end of October, compared to 13 at the end of last October. Days on market did increase from 51 to 70, there were 47 active listings at the end of the month versus the 43 the market saw in October of 2023. This keeps our month's supply steady in multifamily with 2.9 months’ supply this year versus 2.6 last October. The big change in the multifamily sector was a softening of the median sales price which fell 17.6%. October 2024 saw the median sales price of the condo townhouse market settling in at $515,000, a $115,000 reduction from 2023.

“With the long-awaited election past us, REALTORS® on the street are looking towards the future and the hope of interest rate changes helping to bring new product to buyers anxiously waiting,” asked Glenwood Springs-area REALTOR® Erin Bassett.

GRAND JUNCTION/MESA COUNTY

“Compared to this time last year, we are making a little headway, but not by much. Active listings have increased giving buyers more choice, but affordability remains the challenge. The greatest number of available listings are in the $400,000-$600,000 range however, with no improvement in the interest rates, buyers are still forced to sit on the sidelines.

“Our median price in October was just under $400,000 and the more affordable condo/townhomes are in short supply. Although active listings grew slowing, October was the lowest month since last February,” said Grand Junction-area REALTOR® Ann Hayes.

PAGOSA SPRINGS

“Month-over month increases for the Pagosa Springs market included inventory (+21% at 222 homes),

median sales price (+4.6 % at $527,500), average sales price (+23% at $850,543), and the number of days homes were on the market before being sold (+51.9% at 120 days). Year-overyear increases included new listings (+6.3% at 578 homes), median sales price (+9.2% at $599,000), average sales price (+15.4% at $771,356), and the number of days homes were on

the market before being sold (+28.2% at 123 days).

Year-to-Date Average Home Price $771,356

Year-to-Date Median Sales Price $599,000

Actives Homes & Condos on Market 222

“Relative to 2024, brave sellers placing homes on the market have received a gain from October 2023. Unseasonally high temperatures and a large increase in pricing (compared to 2023 pricing) likely increased October listings. High interest rates, higher home prices, together creating high monthly mortgages, and a 7-month supply of home inventory are keeping homes on the market longer. Sellers are adapting to the consequence with patience in selling and listing earlier than anticipated to meet their goals. Currently there are 222 homes and condos on the market for sale. About half of the inventory (109 homes) is priced at $600,000 and up.

“Land inventory is decreasing as properties are placed under contract and winter inventory diminishes. Prices for 2025 land prices are positioned to be higher than 2024 prices as recent land assessments have escalated. November and December sales will likely reveal the true 2024 real estate picture for Pagosa Springs, especially with early winter snowstorms bringing more snow than normal for fall,” said Pagosa Springsarea REALTOR® Wen Saunders.

PUEBLO

“Pueblo’s real estate market showed some positive numbers in October with new listings up 30.2% compared to 2023 and up 4.3% for the year and active listings jumped 24.9% to 892. That activity has pushed the months’ supply of homes up 39.5% to 5.3 months and sits on the cusp of a balanced market.

Pending sales were up 10% compared to October 2023 and sold listings rose 9.45% compared to October 2023, although we remain down 11% year to date. Our median price is up 3.2% year to date at $319,900.

“The percentage of list price received ticked up 0.7% and sits at 98.4% while the average days on market fell in October to 77 days, down 12.5%.

“With the election behind us, the market should get a little boost and NAR economists are predicting interest rates will

stay in the 5.5% to 6.5% range in 2025,” said Pueblo-area REALTOR® David Anderson.

STEAMBOAT SPRINGS/ROUTT COUNTY

“The Steamboat Springs real estate market demonstrated growth in the single-family home segment for listings. Yearto-date, new listings have increased 25.7%, while the median sales price rose 28.1% to $2,249,000. The townhome and condo market has seen similar upward trends with median sales price reaching $846,00 - a 22.3% year-over-year increase. Even with increased listings, inventory remains limited, which has contributed to rising prices across property types, despite the slight increase in days on market for single-family homes.

“In the outlying areas, market conditions vary. In Clark, where inventory remains low, sale prices have been higher while sustaining a longer time on market. The Hayden market has seen a few more new listings with stable price growth. Hayden appeals to buyers looking for a rural lifestyle and more accessible price points compared to Steamboat. Oak Creek, however, has experienced a decline in both median and average sales prices, as well as a 33.3% reduction in sold listings, largely due to 26.5% fewer listings. Days on market for this south Routt area sits at 91 compared to 61 last year. These communities offer diverse housing options for those drawn to the Steamboat area but seeking alternatives outside the main resort hub,” said Steamboat Springs-area REALTOR® Marci Valicenti.

SUMMIT, PARK, AND LAKE COUNTIES

“Inventory is up 30%, median prices are down 13%, and the numbers of sales are up 18%. With the various factors keeping prices high over the last few months, it is the sellers who are negotiating and dropping their prices to get their places sold before the snow flies.

“Single-family homes in Summit and Park counties had a median sale price of $1,025,000 and the average was $1,756,498. While the median price was down the average price was up showing that higher end homes are also moving.

Average price of a Single-Family Home sold this October: Summit County $2,425,969 37 sold Park County $ 716,546 37 sold Lake County $ 765,000 1 sold Average price of a Multi-Family Home sold this October: Summit County $ 897,023 71 sold

“Among the 651 active residential listings in Summit, Park and Lake counties, the most affordable listing is a single-family home in Park County priced at $178,000, while the most expensive is a luxurious single-family home in Breckenridge, listed at nearly $19 million.

“October’s 174 sales in Summit, Park and Lake counties saw a wide price range as well, with the lowest a home in Park County for $120,000 and the highest was a single-family home in Breckenridge for $8.8 million. Forty-one percent of the transactions had a sales price exceeding $1 million and 34% of sales were cash. These numbers exclude deed restricted, affordable housing, land and commercial,” said Summit-area REALTOR® Dana Cottrell.

TELLURIDE

“Telluride and the greater San Miguel County year-to-date transactions sit at 394, down 28% compared to the same period in 2023. However, total dollar volume through October is $871.2 million, up 17% compared to 2023 for the same period of time. The town of Mountain Village continues to drive the dollar volume of sales with $220.8 million with price per square foot falling 8%. The town of Telluride had a dollar volume of $131.3 million, with prices per square foot increasing 43% so far this year.

“An interesting observation is the amount of marketing by long time successful real estate brokers as listings sit at an all-time low and the number of agents in our market slightly increasing. I don’t see this situation changing in the near future or even for several more years. New inventory takes two to three years to build in this market and percentage of motivated sellers is still low,” said Telluride-area REALTOR® George Harvey.

“October is the shoulder season between summer and ski season which traditionally is stable on activity. However, this year, between the election and macro-economic issues, there have been some significant swings in the market. New listings are stable at plus 2% and total inventory is positive 3.7%. Months’ supply of inventory is down 2% to 4.8 months, which is still below the 6 months considered a stable market. Closed unit sales are down 14.6% however, pending sales are contributory as they are positive 39.5%, a big jump from a typical month.

“October had some interesting activity when we go into a bit more depth in analysis. As previously mentioned, transactions were down 14.6% compared to October 2023. However, dollar sales were up 43% versus last year. The variance is the most significant swing for any month this year, or in recent memory. The opening price niche represented 31% of units and 10% of dollar volume in 2023 versus 37% of units and 8% of dollars on 2024. The top price niche is the catalyst for the swing with 6% of transactions and 19% of dollars in 2023 compared to 18% of transactions and 56% of dollars in 2024. This swing was driven by a handful of transactions at the very top end of the market. We have never experienced a swing this significant in the past.

“If the post-election stock market is an indicator of the potential impact on our ski season market, the next few months could be interesting. At this point everything is speculative, and inventory will be the key to the future market,” said Vail-area REALTOR® Mike Budd.

The Colorado Association of REALTORS® Monthly Market Statistical Reports are prepared by Showing Time, a leading showing software and market stats service provider to the residential real estate industry and are based upon data provided by Multiple Listing Services (MLS) in Colorado. The October 2024 reports represent all MLS-listed residential real estate transactions in the state. The metrics do not include “For Sale by Owner” transactions or all new construction. CAR’s Housing Affordability Index, a measure of how affordable a region’s housing is to its consumers, is based on interest rates, median sales prices and median income by county.

The complete reports cited in this press release, as well as county reports are available online at: http://www.coloradorealtors. com/market-trends/

LEADERSHIP SPOTLIGHT

Andrea Warner

Andrea Warner, Broker/Owner Colorado Peak

Real Estate, Inc

Southeast District Vice President

What was your first job? Hardees

How long have you been a REALTOR® and how did you get your start? Since 2009, my ex was military and when we moved to Colorado a lot of our military friends were moving here also. I was helping them find homes by driving around, and I wanted a career that gave me the flexibility to be with my children and be present at all their events, so my ex encouraged me to look into it because I loved the search for homes and loved walking through them with our friends.

What do you love most about being a REALTOR®? I love that we hold ourselves to a higher standard and that we hold each other to that code. I love that we stand up for property rights and the American dream of homeownership. We believe in the REALTOR® brand and what it stands for and I take great pride in that. I also enjoy being able to give back to my industry.

Tell us briefly about one of your most memorable listings. It was my first property that I managed, and it was my first year being able to do property management.

This couple was military retirees and actually lived back in North Carolina where I am from. They trusted their home was being taken care of, but it wasn’t. It was very sad. I managed their property for 5 years and dealt with 2 floods back-to-back and insurance wouldn’t cover it. I helped them find funding that helped pay for the damage. They needed to sell the home for the funds for a family tragedy and it was a hard listing and closing. When we finally closed, we both cried because it was the end of our business relationship. This working relationship is what enhanced the reason why I wanted to be a REALTOR®helping those who need help maneuvering through the most important investment in their lives. We are still friends on Facebook to this day.

What is one thing you recently learned or are learning? People will respond better to you if you stop and listen to them. People just want to know they are being heard. I am learning that I can’t fix everything for them but knowing that they have someone who takes the time and listen is what helps the most. Also, it helps for us not to respond out of haste, stop and listen and ask questions. I think that is what also makes a great leader.

What’s your favorite comfort media? That is a hard one because I have two. I am a big romance novel reader. I find it is the only thing at shuts my mind off so I can relax. Plus, I love live music. Just sitting there and listing to performers do what they love inspires me and just putting a vinyl on my turntable to zone out is the best.

What three words would your friends use to describe you? Passionate, giving, PITA (haha).

AE SPOTLIGHT Tiffany James

CEO of the Fort Collins Board of REALTORS®

How long have you been an AE and how did you get your start? I've been an AE since March 2024. I started my career in REALTOR® association management at the Las Vegas Association of REALTORS®. I began in government affairs and eventually became Communications Director. I earned my REALTOR® Certified Executive designation nine years ago and that's where I discovered my passion for association management.

What do you love most about the job? I love the daily opportunity to be creative. This role is a blend of administrative tasks, creative program development, organization, motivation, journalism, and leadership. I also enjoy working with an inspiring group of entrepreneurial members.

What is a challenge your board/association is facing in the next few years or currently? The industry is undergoing significant changes. The new practice changes have been both a challenge and an opportunity. Lawsuits affecting organized real estate are also challenging, but I believe this adversity will force leadership to rethink the status quo and innovate to better support our members. Challenges often drive positive change and improvement.

Is there something your board/association does regularly to give back to the community? Our community outreach committee is very active. Every month, they organize community service projects. Annually, we host a bowla-thon at Chipper's Lanes, a local bowling alley. Teams of six bowl for a good cause, and the event includes raffles and fundraising. Last year, we raised over $18,000 to support a member whose wife was diagnosed with cancer. This event brings our community together and has been a tradition for over 33 years.

What would your members be most surprised by about your job?

My members might be surprised by the wide range of skills needed to be a successful AE. While some core competencies are universal, the specific skills required can vary greatly depending on the size and needs of the association. For instance, a smaller association may benefit from a multi-talented AE who can wear many hats, while a larger association might prioritize specialized skills in areas like marketing or government affairs.

Which talent would you most like to have? I'd love to be able to read quickly to consume books.

What is your favorite tv (or streaming) show to watch?

I love The Voice. It’s inspiring.

Motto or piece of advice you try to live by?