The UK's leading conference for SMEs, fast-track start-ups and high growth business owners

Elite Business Live is a one-of-a-kind annual event that is unduly dedicated to business growth. Spanning two full days, this event is packed with high calibre speakers, interactive breakout sessions and unmatched networking opportunities.

HIGH PROFILE SPEAKERS

PANEL DISCUSSIONS

INTERACTIVE BREAKOUT SESSIONS

VIP NETWORKING

Studio audience tickets for sale or register to watch live for free online.

CLICK HERE TO REGISTER

Phil Hobden Silverfin & Accounting Tech writer/podcaster

WELCOME

Navigating Accountancy in the Digital Age

WELCOME TO

“Navigating Accountancy in the Digital Age” a comprehensive digital guide designed to equip you with the knowledge and tools necessary to thrive in the ever-evolving landscape of accountancy. Whether your practice is just starting out, scaling comfortably, or preparing for an exit, the challenges of servicing your clients and practice remain even as the role of accountants continues to grow and be redefined.

For almost ten years, I have been working with accountants to implement new technology, create new and profitable

service lines, and transform their practices to better suit the needs of the clients they serve. During that time, one thing has remained constant: standing still is not an option.

Automation, artificial intelligence and digital platforms are no longer futuristic concepts — they are here and creating many opportunities such as enhanced efficiency, accuracy, and strategic insight. However, the technical transformation also comes with significant challenges that must be navigated with care and foresight.

In this guide, we delve into the critical areas shaping

the profession: integrating cutting-edge technologies, adapting to evolving regulatory requirements, fortifying cybersecurity and addressing the ever-present issues of talent acquisition and retention. In a world where a proactive approach to learning and adaptation is required to stay ahead of trends and ensure your practice is at the forefront of change, we aim to provide you with actionable insights and practical advice.

Technology is not just changing how accountants work; it is transforming what is possible within the profession. With AI and machine learning, tasks that once took hours can now be completed in minutes. This transformation is already well underway, with leading firms such as Gravita and Larking Gowen using AI-enhanced data to improve accuracy, and tools like Silverfin Assistant spotting anomalies, improving compliance, and even training junior staff — all of which, alongside advancing automation, translate into better quality service.

Cybersecurity has become a paramount concern as digital threats evolve in sophistication. Talent acquisition and retention remain significant challenges not least as Universities struggle to reflect the job accountants now perform..So, whether you are a seasoned professional or new to the field, this guide will help you understand and master the dynamics of digital accountancy. Embrace the journey ahead, as we explore how to transform potential obstacles into stepping stones for success. Let this guide be your roadmap to navigating the complexities and harnessing the opportunities that lie ahead in the world of digital accountancy.

Swoop

Swoop offered a superb service overall. We were assigned a dedicated Accounts Manager by Swoop who got our loan approved in 5 days and the money was in our account shortly afterwards.

ADNAN N, SMALL BUSINESS OWNER

CONTROL THE CONTROLLABLES

The ongoing surge in corporate insolvencies is a significant cause for concern among UK businesses, and this trend is expected to persist into 2024, echoing the relentless pace witnessed in 2023

2023 STATISTICS

REVEAL a staggering 17% year-on-year increase from 2022 to 2023 and maybe even more concerning marking a substantial 33% spike compared to the pre-pandemic era. In the final statistics release of last year, the Insolvency Service confirmed 2,466 registered company insolvencies in November 2023, a number 21% higher than the previous November and 7% higher than the figures in October 2023. A recent report from accounting giant PwC predicts a ‘significant’ rise in business’ collapsing in 2024, with the hotels and catering, manufacturing, and transport and storage sectors likely to be the hardest hit.

The implications of insolvencies are profound. The current wave of corporate insolvencies serves as a resounding warning, particularly for those with unpaid invoices awaiting resolution. Even if a company believes it stands resilient against insolvency, the stark reality is that its customers may not be as fortunate.

In this volatile environment, the pronounced 59% increase in Creditors’ Voluntary Liquidations (CVLs) compared to pre-pandemic levels suggests that businesses are operating in a tough and unpredictable landscape. The delicate nature of the credit cycle is underscored, emphasising how a disruption in this chain can send shockwaves across entire industries.

Consider this scenario: if a customer with a substantial order fails to fulfil their payment obligations, would your business have the financial capacity to settle all outstanding invoices promptly? This underscores the critical importance of businesses remaining vigilant and implementing effective credit control processes. In such uncertain times, proactively managing outstanding invoices can be the key to navigating the precarious economic landscape and ensuring the stability of your enterprise.

It’s time to consider what you CAN control, and often that starts with your own credit control. Consider the following:

• Be on top of your payment cycles.

• Understand your customers –credit checks and monitoring are key.

• Regularly review credit limits for your clients. Are they too high or sometimes even too low?

• New sales & clients are good, but how much have you sat unrealised on your ledger?

• Be proactive in chasing payments – when your invoices aren’t paid on time, you must be proactive.

• Have a backup plan for a gap in your cash flow – what finance options could help bridge short-term gaps?

• If all else fails, consider when you need to look at Commercial Debt Recovery. And remember, the older the debt, the harder and more expensive it is to recover.

It’s time for UK businesses to become more proactive in shoring up their own ledgers to ensure they can continue to grow when others around them may be struggling.

Five big challenges facing UK accountants in the next 12 months

As we blast past the halfway point of 2024, it’s clear much has changed for the wider accounting profession in the UK

RAPID TECHNOLOGICAL ADVANCEMENTS,

evolving regulatory landscapes, and economic uncertainties make standing still not an option for any practice wanting to thrive or even survive. Here are five key challenges that accountants need to master:

Integrating automation and AI

The digital revolution is reshaping the accounting industry. The integration of automation and artificial intelligence (AI) is no longer a futuristic concept but a reality giving the firms getting it right points of differentiation including accuracy, speed and advisory content. Every industry conference this year had AI as the leading topic both on and off stage! These technologies streamline routine tasks, allowing accountants to focus on more strategic activities. However, the shift does require a notable investment in both technology and upskilling staff, so planning and getting started are key.

Accountants need to become adept at using the digital tools and platforms at their disposal. Industry expert Will Farnell still thinks that less than 20% of firms are truly digital practices (see his book ‘The

Human Firm’). Moving away from legacy software such as traditional desktop software and Excel spreadsheets is a critical part of this transformation: it’s not just a technical upgrade, but a cultural shift within firms.

Navigating regulatory changes and compliance

The regulatory environment is in constant flux. The postBrexit landscape continues to introduce new rules that accountants need to navigate meticulously and no doubt a change in Government following the recent election will impact initiatives like Making Tax Digital (MTD). Moreover, the increasing focus on environmental, social, and governance (ESG) and even carbon accounting requires accountants to develop new competencies in sustainability accounting. Compliance with evolving anti-money laundering

(AML) regulations adds another layer of complexity and answering the question of how do we stay up-to-date and compliant while controlling the costs passed on to clients is no easy feat.

Mitigating cybersecurity threats

With the increasing use of digital platforms and sophistication of attacks, cybersecurity is a top priority. As custodians of highly sensitive financial information, accounting firms can become targets for cybercriminals. So, ensuring robust data protection is not just about regulatory compliance, but also about safeguarding firms’ reputations. It’s an area that still seems oddly neglected with many firms choosing to hold onto client data rather than pass it and the responsibility for its safety to technical specialists.

Tackling talent acquisition, retention, and upskilling

The accounting profession faces a significant skills shortage, and attracting and retaining top talent is proving increasingly challenging. Younger generations of accountants have different career expectations, value work-life balance more and expect continuous learning opportunities without repetitive and frustrating tasks. The capacity crunch is real in accounting and, whilst technology can help, it’s still down to firms to create the right environment and reflect these changing expectations to remain attractive to candidates.

Every industry conference this year had AI as the leading topic

Smaller accountancy firms, where culture and flexibility are easier to control, are attracting waitlists of candidates (Strive-X is a great example of this).

With 86% of accountants wanting their employers to provide more training on the use of accounting technologies (ACCA Global talent trends survey 2023) investing in professional development and upskilling is crucial. Firms must also look beyond the usual regulatory training to engage and retain staff. Building a culture that supports growth and learning also helps firms stay competitive and aligned to customers’ priorities.

Navigating economic uncertainty

Economic fluctuations including inflation, changes in interest rates, geopolitical events, elections, and the continuing impact of Brexit and Covid are all significantly impacting businesses their financial priorities and performance. Accountants play a crucial role in helping clients navigate these forces providing strategic advice on risk management and identifying opportunities in volatile markets.

This requires accountants to be agile and well-informed (which requires time and headspace that no doubt technology plays a role in creating) in order to provide clients with the guidance needed to adapt to evolving economic landscape. Mastering this further stretch of accountant towards trusted advisor will set successful firms apart but is not for the faint hearted.

Beyond 2025

We don’t have a crystal ball but adapting to digital transformation, staying compliant with regulatory changes, safeguarding against cybersecurity threats, attracting and retaining talent, and navigating economic uncertainties are going to remain important. If anything, the challenges in these five areas are likely to steadily grow.

However, recognising and starting to tackle these challenges offers accountants the chance to enhance their value proposition and solidify themselves as indispensable strategic advisors to clients, in what continues to be an unpredictable and demanding financial landscape.

The thirst for best of breed technology is great

So, why are there no clear winners in tech firms usage?

IF YOU NEEDED a marker on the transition the accounting profession is undertaking then this is it – 93.5% of mid size accountancies are following a best of breed approach to adopting new technology. That’s according to research Phil Hobden, Head of Strategy & Growth, Know-it conducted in the last few weeks with senior leaders charged with overseeing technology and operations at 31 UK accounting firms.

Representing a mix of tier 1 and 2, with a sprinkling of smaller firms, these practices highlight the intricate technology stacks ambitious firms are managing.

Hobden asked the accountants responding to the research to share which technology they selected for core functions within their firms. It was designed to understand if the adoption of sector specific tools is aligned to the attention they are currently getting.

Starting with practice management software, Karbon is a favourite, though there is plenty of variation in this category with around five other tools named. The majority, though, still use the tools embedded in compliance software. One had even built their own in-house tool.

There’s a similar story with electronic signature tools. 16.1% favour Adobe, whilst 22% prefer to use Docusign. Otherwise,

firms are using the tools embedded in core practice technology.

When it comes to communication platforms, favoured collaboration tools are Teams (58%) and Slack (22%). The pandemic will no doubt have accelerated adoption. However, it’s clear firms are not going back to how things were before, suggesting that productivity gains are apparent and there’s a more organised move to remote working and/or cross team collaboration.

Fathom and Syft have gained traction for providing industry insight, reporting and forecasting capability outside of what the core technology firms are using. It’s an interesting glimpse into how important understanding the macro picture is to midsize firms, and provides more colour to the view that technically-savvy firms have an appetite for growth.

Even so, there are some areas that are lacking. For instance, document management is far from straightforward. In fact (and

rather ironically), you could argue it’s messy.

The majority have switched to the cloud, with Google Drive, Microsoft OneDrive, Share Drive and DropBox all in the mix. Around a quarter are using the solutions embedded in their compliance system.

What does this tell us? Mainly that every firm is different and will develop its technology strategy at its own pace. But, to my mind, there’s real choice in the market. Working with partners to take advantage of that choice, can and will open up huge opportunities to make incremental gains in so many facets of a business – from fewer errors in complex compliance work, through AI assisted training for new accountants, to more efficient ways to

collaborate.

So it seems surprising that the numbers show that there’s also an oxymoron in play. Every firm questioned on its approach to sourcing technology said they followed a best of breed approach.

Yet, many are using tools that sit within existing software suites, largely because they are covered by a license.

As some admitted, despite being resoundingly clear on a progressive strategy, they have some way to go to reach their utopia. However, with the right partners, they generally agreed they are making steps in the right direction.

This is an interesting insight. One that shows how firms are considering culture, cash and energy for change. If there are bigger efficiency and profitability gains to be made elsewhere, there’s no reason to put document management to the top of the technology change list.

But it doesn’t mean it won’t be on the change list in the future. There will be a point when every tool needs to be assessed on its merits of boosting productivity and releasing capacity for more innovation in client service models. As technology evolves and competition intensifies, it looks as though the willingness to

move with the times, when the opportunities arise, will drive wider adoption of best of breed. Based on these results and hypotheses, Hobden had a couple of conversations that brought to light some other theories. Some firms are grappling with legacy and large stacks, so the perceived costs and upheaval involved in transitioning to best of breed can’t be justified, or certainly can’t be justified right now. While, in a handful of cases they are still trying to find the killer app that works for their business. And, as the saying goes, they’re in a position of ‘it ain’t broke, don’t fix it’.

It demonstrates the tricky conundrum leaders face. Many know there’s a direct impact on ways of working – more efficiency and true collaboration – and they understand that a reliance on legacy technology is impacting the ‘cost to serve’. But, as was noted in the conversations Hobden had, often it’s not the tech that is the stumbler, but finding a provider that understands the demands on their business.

What we have taken away from these responses is that best of breed as an approach has won the hearts and minds of accountants – the benefits case is clear. However, most firms have not implemented as much of this strategy as might be expected. As such, efficiency gains are missed, true collaboration can’t be assumed for staff or clients and a reliance on legacy technology still impacts cost to serve. So, firms that do prioritise best of breed projects can still achieve a competitive advantage and with the right strategic technology partners unlock significant improvements – nevermind the potential of AI – using these to optimise and automate in such a way as to improve staff and client satisfaction, while creating insights and capacity for additional advisory revenue.

Unlock the True Value of Your Business

A business valuation is the cornerstone of business success. Without a clear understanding of your company’s value, navigating the complexities of succession and growth planning becomes a challenging task.

Whether you’re thinking of selling your business or seeking insights into your financial trajectory, BusinessesForSale.com’s quick valuation tool will help you understand the worth of your business.

Get an estimated business valuation in under 5 minutes, for free.

You’re not as AML compliant as you think

Earlier this year we surveyed over 200 accounting and bookkeeping firms of all sizes from across the UK, and uncovered how they are currently thinking about, and managing their AML compliance

UNSURPRISINGLY, our research revealed some common themes. The most common ‘gaps’ are those consistently highlighted by the Institute of Chartered Accountants England & Wales (ICAEW) and HMRC in their AML supervisory reports.

For example, the three most common findings highlighted in the most recent ICAEW supervisory report are:

• Not updating client due diligence on a regular basis

• Carrying out risk assessments on clients

• Not applying a consistent approach to due diligence

Firmcheck’s ‘2024 Landscape Of AML Compliance’ report found that 30% of firms don’t have a standard client risk assessment, and 28% are without a firmwide risk assessment – one of

the most important components of your AML compliance.

The complete juxtaposition of these findings is that of the firms we surveyed, an overwhelming majority (91%) recognised AML compliance as an important part of their firm operations, and 90% of firms said they were confident in their AML compliance measures, despite sharing insights into their processes that documented clear gaps.

Improving your AML compliance

The topsy-turvy nature of these findings is no surprise, though. The Money Laundering Regulations evolved from simply requiring you to get a copy of someone’s ID and store it— job done. Unfortunately, the regulations have been amended over the years to be more robust in the face of financial crime.

Even today though, AML processes are still commonly following that pattern from over 20 years ago, with the most common answers in our research focused on gathering basic information about customers, checking and verifying their IDs, and updating their details/ID documents if something expires – very little attention is given to the due diligence and risk assessment components, which is the most critical part of your AML process.

Leveraging software was one way we saw firms closing those common compliance gaps:

• Adopting AML compliance software meant firms are 2x more likely to have a standardised means of conducting due diligence, and managing risk assessments

• Ongoing monitoring and AML management is 3.2x more likely to happen when using software to manage AML processes.

The other observation we’ve noted during our conversations with accountants and bookkeepers is that they are sometimes unaware, or find making sense of legislation and their professional supervisory bodies guidance challenging. As a result, actually plugging those gaps or knowing if you’re doing a ‘good enough’ job is hard to establish. That’s why we’ve created a concise, 7-step health check that can give you an indication of how AML compliant you’re in just 45 seconds.

You can complete your free AML health check below, and get personalised AML tips if you’d like to make some progress with your current AML processes.

Complete your free AML health check

Phil Hobden UK Product Lead, Silverfin

AI: How AI and Automation will drive efficiencies for accountants

By 2034 AI will contribute to boosting productivity in firms by 40%. For accountants the gains are significant

AI TOOLS WILL help with the heavy lifting accountants must do by automating repetitive tasks, learning to spot anomalies and reducing errors whilst also improving compliance. Given the current capacity crunch facing the sector, it’s exciting that employees can be freed from cumbersome tasks creating bandwidth for more profitable and higher-margin client work.

Where do you start?

An AI strategy should consider people and culture, process and workflows, stakeholder/ client management, data and risk management, technology partnerships, and metrics.

Are you ready? People and process come first Everyone in the organisation needs to know that this is not about replacing humans. It’s about making their job easier, less stressful and more fulfilling. It’s about building a company that is profitable and thrives. It’s a good idea to appoint champions across the

organisation to help land this critical point. They can help teams review the workflows and processes that are cumbersome or broken and identify how AI can be used to automate and optimise them.

Stakeholder mapping and prioritisation

Think about who needs to be involved - internally and externally - and use it to prioritise the areas where AI can make the most gains quickly. Quick wins will also help enthuse the team.

Data

and risk management

With a priority list, you can assess the data that’s involved and ensure it is ready, organised in the right format and stored securely. AI, combined with cloud technology, can help with the task of structuring and bringing together the data silos you have. Always seek the advice of experienced accounting AI and cloud specialists who understand how data can be seamlessly moved into operational workflows. It’s a complex task that needs to meet security

and privacy standards, without compromising the integrity of your business.

Read more: How to create an AI policy for your accounting firm

Measure success

Profit and margin are obvious measures, but team capacity and the accuracy / quality of their work, as well as customer / employee satisfaction are also valid. If you can attract more clients and better quality job candidates, then it’s a big win for the strategy.

Partner for a winning plan

Experts like Silverfin, have worked with accountancy practices globally and have plenty of technical experience to draw upon. But, don’t select a partner just on technology prowess. Think about how you can tap into their knowledge of building cultures that value AI. It’s the difference between delivering a good strategy and a great one.

Take a finance health check

How healthy are your finance processes? Are you being overwhelmed by mundane, manual processes that are holding you and your team back from achieving the growth and progress you need to?

IT’S TIME YOU checked in on the health of your accounting processes. You could save yourself time, money and a lot of stress by switching to a more efficient system.

What to look for

There are some classic tell-tale signs that you are beginning to outgrow the accounting software your company used when it first started out. And these challenges

will continue to grow as your business expands.

• Inefficient processes: A buildup of manual, repetitive tasks like data entry and chasing for updates

• Stressful month-end: Taking over ten days to close books, causing overwork and frustration

• Consolidation issues: Multiple spreadsheets spanning different departments, prone to errors and causing delays

• Multi-currency transactions: Losing money due to manually monitoring and trying to stay on top of fluctuating exchange rates

• Drawn-out approvals: Timeconsuming emails chasing for expenses and invoices to be signed off

• Reporting headaches: Building reports from scratch in Excel due to inflexible systems.

Take our short survey to help us understand exactly what issues you are struggling with regarding your accounting software, and what features you think you’d benefit from.

Your opinions will help us make sure we deliver the best solutions to help you perform better as a business and get your finances back to fighting fitness.

Take your finance health check

Empower your business to soar

Power your growth

GETTING PAID

How to ensure you and your clients get paid for the work they do

IN THE WORLD of business, particularly in the service industry, one of the most critical aspects of maintaining a healthy operation is ensuring that both you and your clients are paid for the work performed.

Timely and fair compensation is not just a matter of financial stability; it’s a cornerstone of professional integrity and trust. Here’s how you can establish robust systems and practices to ensure consistent cashflow, know your customer and ultimately get paid on time.

1. Know Your Customer

Knowing your customer (KYC) is fundamental to the success and sustainability of any business. KYC is not just about gathering data; it’s about using that data to build relationships, enhance products and services, optimize marketing and sales strategies, ensure compliance, and drive strategic decisions. Here are some of the best ways to really get to know your customer:

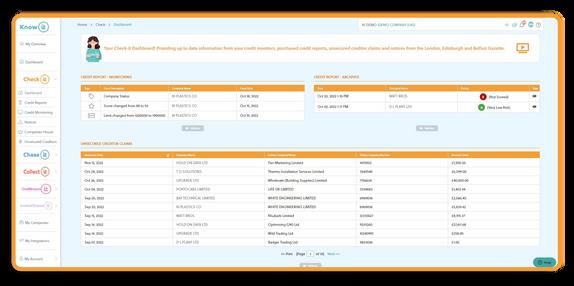

• Credit Checking: Helps assess a customer’s ability to pay their debts. This information

is crucial for making informed decisions about extending credit or terms of payment.

• Credit Monitoring: It’s normal for things to change after the initial credit check. Therefore, it’s important to keep track of your customers credit file which might highlight potential red flags. By continuously monitoring the credit health of customers, businesses can protect themselves from financial instability and foster long-term success.

• Gazette Notices: By monitoring notices related to insolvency, legal disputes, and financial difficulties, businesses can better assess the creditworthiness of their customers, making informed decisions about extending credit or adjusting payment terms.

• Companies House: Companies

House provides a publicly accessible database where information about companies, such as financial statements, directors, shareholders, and registered office addresses, is available. This transparency helps in building trust and accountability.

• Supply Chain Monitoring: Gain insight into which of your customers have suffered financial losses due to their own customers going into liquidation or administration. This data isn’t provided on standard business credit reports and allows you to anticipate a potential cashflow catastrophe before it’s too late.

Carrying out these checks on your customer is a great way to make more informed credit decisions on your customer which could be the difference between getting paid or not.

2.

Clear Contractual Agreements

The foundation of getting paid starts with a well-drafted contract. A contract should clearly outline the scope of work, payment terms, deadlines, and consequences for late payments. Here are key elements to include:

• Scope of Work: Define what services will be provided.

• Payment Terms: Specify the payment schedule (e.g., upfront payment, milestones, upon completion).

• Deadlines: Set clear deadlines for when payments are due.

• Late Payment Penalties: Outline penalties for late payments, such as interest charges.

A detailed contract leaves little room for misunderstandings and sets the stage for professional accountability.

3. Transparent Communication

Open and ongoing communication is vital. Regular updates on project progress and clear invoicing can prevent misunderstandings about the status of work and the reasons for charges.

• Regular Updates: Keep clients informed about project milestones and any changes in scope.

• Clear Invoices: Provide detailed invoices that break down the work performed and the corresponding costs.

Transparency builds trust and reassures clients that they are receiving value for their money.

4. Efficient Invoicing System

An efficient invoicing system is critical to ensuring you get paid on time. Here are some best practices:

• Timely Invoicing: Send invoices

promptly upon reaching agreed milestones or project completion.

• Automated Systems: Use invoicing software to automate reminders and follow-ups.

• Multiple Payment Options: Offer various payment methods to make it easier for clients to pay.

Efficiency in invoicing reduces administrative burden and speeds up the payment process.

5. Client Education

Educating clients about your payment processes and expectations from the outset can prevent future payment issues. Provide them with a clear understanding of:

• Payment Terms: Explain when and how they are expected to pay.

• Invoicing Process: Walk them through your invoicing system.

• Penalties for Late Payments: Make them aware of any penalties for late payments upfront.

An informed client is more likely to comply with payment terms.

6. Proactive Follow-ups

Follow-ups are essential when payments are delayed. A structured follow-up process can include:

• Gentle Reminders: Send reminders a few days before the payment is due.

• Firm Follow-ups: Follow up immediately if a payment is missed.

• Escalation Procedures: Have a clear process for escalating issues, such as involving a collections agency or taking legal action if necessary.

Proactive follow-ups demonstrate your commitment to being paid for your work.

7. Building Strong Relationships

A strong, positive relationship with your clients can also facilitate timely payments. Building such relationships involves:

• Delivering Quality Work: Consistently deliver highquality work that meets or exceeds client expectations.

• Professionalism: Maintain a professional demeanour in all interactions.

• Responsiveness: Be responsive to client needs and concerns.

Strong relationships foster mutual respect and a higher likelihood of prompt payments.

8. Risk Management

Sometimes, despite best efforts, clients may delay or fail to make payments. Risk management strategies can include:

• Credit Checks: Perform credit checks on new clients.

• Advance Payments: Request advance payments or deposits.

• Payment Milestones: Break projects into smaller, manageable milestones with payments tied to each.

These strategies can help mitigate the risk of non-payment.

Conclusion

Ensuring timely payment for the work you and your clients requires a multi-faceted approach that combines clear contractual agreements, transparent communication, efficient invoicing, client education, proactive followups, relationship building, risk management and knowing your customer. By implementing these strategies, you can create a reliable payment process that supports the financial health of your business and fosters trust with your clients. In the UK context, where late payments are a significant issue, these practices are especially crucial. Remember, the goal is not just to get paid, but to establish a professional environment where payment is a seamless and expected part of the business relationship.

UK Payment Landscape: Key Statistics

Understanding the UK payment landscape can provide context for the importance of these practices:

• Late Payments: According to the Federation of Small Businesses (FSB), 62% of small businesses in the UK experience late payments, with an average delay of 23 days beyond agreed terms.

• Cost of Late Payments: Late payments cost UK small businesses £2.5 billion each year, impacting cash flow and business operations.

• Government Initiatives: The UK Government has implemented measures such as the Prompt Payment Code, encouraging large businesses to pay small suppliers promptly. Despite this, compliance remains an issue, with only 27% of large companies consistently meeting the code’s requirements.

• Digital Invoicing: A report by QuickBooks indicates that businesses using digital invoicing and payment solutions see a reduction in late payments by up to 15%.

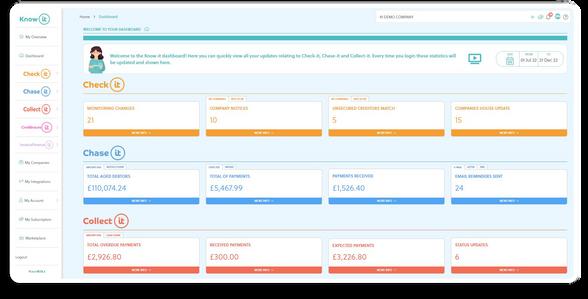

Automate Your Credit Control Process!

50,000 small businesses close every year due to late payments - don’t let this be you! With Know-it you can:

Credit check & monitor businesses

Automate payment chasing via email, letter and SMS

Collect unpaid invoices in the click of a button and get paid! Know-it seamlessly connects with leading accountancy packages

Start your free 30 day t i l t d and get one free credi p

Accountex Summit Manchester opens free registration

On 17 September, thousands of attendees are expected to return to Manchester Central for the sixth edition of Accountex Summit Manchester

“LAST YEAR’S SHOW was a huge success, we welcomed a 35% increase in attendees!” said Accountex Portfolio Director, Caroline Hobden. “This year we’re excited to deliver an even better show with new exhibitors, speakers and features.”

‘You will leave feeling empowered’

The show will feature a lineup of more than 120 software and service providers, including big names such as FreeAgent, Intuit Quickbooks, IRIS, Sage, Wolters Kluwer, and Xero. Attendees will have the chance to meet the teams, experience tailored demonstrations and discover invaluable insights.

“For the past three years, I

have attended Accountex, and every year I discover a new software solution to enhance my business. This enables me to save time and increase my capacity to serve more clients.” Commented visitor, Mandy Crossley, Director/Accountant for MC Accounting & Business Solutions.

‘The quality of the speakers is exceptional. For me it’s a ‘can’t miss event’’

The CPD accredited seminar programme boasts 60+ industry-leading speakers, covering a wide range of topics, including AI, diversity and mental health. With sessions held across four theatres, attendees will gain access to thought leaders and experts

shaping the future of the profession.

Visitor Rebecca Holloway, Associate Director at Harold Sharp Limited commented, “If you want to see all the best speakers from the accounting industry, this is the place to be. There is just so much great content all in one day, you can’t afford to miss it.”

‘Accountex Summit Manchester is a one stop shop!’

In addition to the education programme and exhibitors, attendees can look forward to a post-show drinks event for networking and unwinding after a busy day.

Accountex Summit Manchester is taking place at Manchester Central on 17 September 2024.

For further information and to book your free ticket, click below. Use priority code ASM216 when booking your ticket.

Book your FREE Accountex Summit Manchester ticket

NAVIGATING UNCERTAINTY

Economic outcomes and impacts on SMEs and accountants

THE UK ECONOMY, much like its global counterparts, stands at a crossroads. While market optimism hints at a soft landing, the unpredictable nature of economic forces necessitates a cautious yet prepared approach.

Founder of Capitalise, a credit score and funding platform for SMEs, Paul Surtees explains the intricate dynamics that businesses face today. “I aim to shed light on the potential economic scenarios and their implications for SMEs and accountants, offering insights to navigate this complex landscape.”

The

Market’s Soft Landing

Recent forecasts suggest a soft landing for both the UK and US economies, characterised by the S&P and FTSE breaking new highs. This optimism is further fueled by large corporations securing lowcost funds, indicating stable economic conditions. While this is a welcome outlook, it differs somewhat from SME indicators such as the Xero Small Business Index (XSBI) that paint a more challenging outlook for business owners. It is therefore

essential to prepare for a range of potential outcomes rather than relying solely on base case forecasts.

Potential Economic Scenarios

Strong growth with moderate inflation:

• Implications: Businesses may experience increased consumer demand, necessitating expansion and scaling operations. For accountants, this translates to a higher volume of transactions and the need for efficient financial management tools.

• Action Points: Invest in forecasting software and robust credit control mechanisms to predict the likely impact of a growing business and handle the cashflow.

Stagflation (3-4% Inflation, 5% Interest Rates, No Business Growth):

• Implications: Stagnant economic growth coupled with rising inflation and interest rates can squeeze profit margins, leading to tightened cash flows.

• Action Points: Implement stringent cost control measures

and explore diversified revenue streams. Accountants should focus on detailed strategic business and financial planning to help clients navigate this challenging period.

Economic Recession:

• Implications: A recession could lead to reduced consumer spending, increased unemployment, and financial stress across sectors.

• Action Points: Strengthen cash reserves and prepare for potential cost-cutting. Accountants should advise on liquidity management and debt restructuring options to ensure business continuity.

Geopolitical and Economic Uncertainties

The unpredictable nature of geopolitical events continues to pose significant risks. The ongoing war in Ukraine, potential oil sanctions, and

instability in the Middle East are factors that could disrupt supply chains and drive up costs. For instance, rising energy prices could impact operational costs, while food inflation could affect sectors like hospitality and retail.

Persistent Inflationary Pressures

Despite a welcome decline in inflation, mid-term pressures remain. The Bank of England anticipates a few positive increases in inflation this year related to how inflation is indexed, but more persistent factors such as fiscal spending, re-militarization, and global trade restructuring pose larger risks. Persistent inflation can stress real estate, particularly commercial real estate (CRE), and subsequently, banks. The mini-banking crisis which started in the US in 2023 serves as a stark reminder of these vulnerabilities.

Impact on SMEs and Accountants

• Credit Control, Risk and Cash Flow Management: With economic volatility, maintaining robust credit control is crucial. Understanding your clients’ credit risk is critical to credit control. Once risk managed, SMEs should ensure timely payments and manage receivables efficiently.

Accountants can play a pivotal role by providing insights into cash flow management and leveraging digital tools to streamline processes.

• Embracing Technology: In the face of uncertainty, embracing technology is not just advantageous but essential. AI and automation can enhance productivity, reduce errors, and provide real-time financial insights. Accountants can stay ahead by continuously integrating new technologies

into their practice. The conversations currently are cautious, but optimistic, in the community.

• Scenario Planning and Risk Management: Preparing for various economic scenarios involves thorough risk assessment and contingency planning. SMEs should engage in scenario planning to understand potential impacts and develop strategies accordingly. Accountants can guide this process by offering analytical insights and strategic advice around funding for the business.

While the hope for a soft landing is valid, the need for vigilance and preparedness cannot be overstated. By understanding and preparing for a range of economic outcomes, and if necessary the associated different financial projections those may deliver, SMEs and accountants can navigate uncertainties more effectively. Embracing technology, maintaining robust financial management practices, and staying informed about geopolitical and economic developments will be crucial in the journey ahead.

As we move forward, let’s keep our focus on adaptability and resilience. The future remains unpredictable, but with strategic planning and proactive measures, we can steer through the uncertainties and emerge stronger.

Sign up for business credit scores and access to funding below

HOW TO AVOID LATE PAYMENTS

What can SMEs do to tackle the issue of late payments?

THE IMPACT OF late payments can be drastic on small businesses. Late payments are detrimental because they disrupt financial stability, incur additional costs, hinder growth potential, strain relationships and can have a lasting impact. But how do we avoid late payments? And, if we can’t avoid them, how do we mitigate the impacts?

Alex Von Schirmeister, Managing Director of Xero UK and EMEA took to the stage at this year’s Elite Business Live event along with an insightful panel including Andrea Reynolds, Founder & CEO of Swoop, Emmanuel Asuquo, financial advisor and TV personality, Liz Barclay, Small Business Commissioner and Richard Bearman, Managing Director of the British Business Bank. The panel spoke about the challenges of late payments, and the impacts it can have on the productivity and financial stability of a business.

Liz Barclay discussed how late payments affect not only the productivity of small businesses but also business owners’ mental health. Late payments can take a business owner’s time and attention away from dayto-day operations, hence, lose focus of other tasks at hand. “If you’re spending three and a half hours a week chasing unpaid invoices, you don’t know if you can recruit, if you can invest, and whether you can grow the business, so your productivity is down,” Liz said. “You’re worrying about whether you’re

going to have the money to pay the wages, and that keeps you awake at night.

Throughout my career, I’ve been either a freelancer or ran my own business. And so, I know what that feels like. If you are awake worrying, that affects your mental health. So, it’s not just the economy we’re talking about here. This is lives we’re talking about and it’s the lives of small business owners.” Late payments affect the trajectory and forward planning. If you do not know when the cash is coming in, it gets difficult to allocate finances into different areas of your business.

“Late payments make a huge difference,” she added. “If you know when the payments are going to hit the bank account, you can do an awful lot more with your business.

The government wants growth, they want to increase productivity. This is the place to start.”

Emmanuel highlighted the importance of open conversations between self-employed individuals and their clients regarding payment expectations and consequences. He spoke about the uncertainties self-employed individuals face, and how late payments can affect their mental health and family planning. Late payments can put extra pressure on other parts of your business, leaving you unable to pay staff wages, for example. “Once you become self-employed, you can’t guarantee that you’re going to get paid once a month,” Emmanuel explained. “I speak to business owners who maybe have a good year, but because the money has taken so long to come in due to late payments, they don’t get to experience the money that they’re making. When you become self-employed, mortgage planning can be very difficult. There is even more pressure when you’re not only paying yourself but paying other staff. You must put them before yourself and if they don’t get paid on time you can lose good talent.”

Alex highlighted how technology and digitalisation can help small businesses with invoicing and payment processes, while emphasising the need for a culture shift towards timely payments. “There’s no question that technology will do several things to mitigate late payments,” he told the audience. “Technology can help you be on top of your numbers and adding visibility is critical. Technology can also help make your invoicing process more efficient so that you know when the money is coming in. I think the challenge here is the culture around late

payments, of not caring about paying on time. There is a culture of larger companies either not realising this is a problem, or worse, not caring about the consequences of late payments. There’s a complete lack of awareness and intimacy of the impacts late payments have on SMEs. But also let’s be honest, we should call it unapproved debt. Many larger companies are purposeful living and then economically drawing a benefit from paying late and that should be unacceptable.”

Andrea Reynolds spoke about the challenges she faced with late payments from suppliers and the awkwardness of constantly chasing late payments, especially if you’re trying to build and maintain relationships. Sending automatic payment reminder emails or using a third person as a reason you’re chasing up for a payment, could be ways to get the payment process sped up –while still maintaining a good relationship with your suppliers. Using technology, such as automated accounting software, can also be a fool-proof way to automate the payment processes while taking your mind off the tedious task of chasing up on

your customers. “You’re trying to put your best face forward when you’re dealing with customers to show you’re a strong financially viable business, and then chasing invoices might come across the wrong way,” Andrea said. “Setting up automated reminders in your accounting software, for example, can take a little bit of the psychological edge away from you personally chasing this business.”

“From my experience, the larger businesses are the hardest to get to pay on time,” Andrea added. “But I think there’s more work and more pressure we need to be putting on those organisations because they come up with excuses and say it is due to their system or procurement policy. I think there’s a lot of improvement to be done there. To anyone afraid of that first step of chasing invoices, use technology so there are no excuses. There’s no excuse if you’re receiving an automated reminder. And it’s not you as a business owner personally chasing. The other trick that we all use is the good cop, the bad cop – having the scary finance person ‘chasing’ the supplier for the payment. You can continue

that relationship with the supplier and claim your finance team is chasing you on the payment. I think those types of tips genuinely work.”

Richard Bearman talked about the culture of late payments and encouraged SMEs to use financial products to maintain cash flow when facing late payments. “We see many businesses coming to us for help because they’ve just got this cash flow issue of late payments. There’s a culture issue with this, and a lot of the businesses facing the impacts of late payments are small to medium-sized businesses. I can remember a very specific example of an entrepreneur who was saying he was just getting evermore frustrated about late payments. And then he realised that the projects he supplied were crucial to the customer. From then on, he said he would not deliver until he had been paid. Even though that’s an extreme example, I think that’s what the testing of power is. And then the other end of the spectrum using the financial services products, there are digital products that can minimise the impact of late payments and protect your business.”

Richard also suggested using asset-based finance to keep trading despite late payments, with opportunity cost as a consideration. “If you’ve got good credit, think about the finances and opportunity cost, and then raise money against those assets, lease the money and keep trading,” Richard said. “It doesn’t stop the late payments but at least it is paid and allows you to keep trading, and yes of course it comes at a cost but consider whether it’s an opportunity cost.”

Could AI help solve the plight of late payments?

ARTIFICIAL INTELLIGENCE

CAN achieve some amazing feats, but few are likely to give SMEs more satisfaction than getting paid on time.

Late payments are a major pain, both for the suppliers who need to chase up their cash and for the late payers themselves, who risk damaging their reputations and business operations.

According to the UK government’s most recent figures, large businesses pay a quarter of their invoices late. On average, SMEs are owed £22,000 each. Remedying this could boost the economy by an estimated £2.5 billion a year.

“The impact is pretty vast, considering that 99% of businesses are SMEs,” says Angus Milledge, EMEA SMB Director at spend software specialists, SAP Concur.

All too often, a firm will use outdated accounts payable (AP) processes. “So, when they receive a supplier invoice, the only way to capture it is manually,” he says.

The ideal solution is to automate AP tasks, like manual data entry. A typical invoice contains an average of 70 data points, he explains, “and if you introduce AI or machine learning, the system accurately scrapes data from the invoice and puts it in your finance system. That is a huge saving in terms of productivity.

“The beautiful thing about AI is that it’s constantly learning, so the more supplier invoices that are processed, the smarter your solution becomes.

Everyone loses out when companies settle invoices late. But with the help of AI, the days of processing them by hand may be numbered

“In a manual world you’ll often have a really astute and productive finance team, but the biggest bottleneck is usually the approvers. It’s not really their day job to sit approving invoices – they’ve got other things to worry about, and that’s the Achilles’ heel in the whole process.”

Milledge acknowledges that the prospect of radically changing a traditional business’s AP processes can be daunting. “But eventually, most hit a critical point where the decision is to invest in additional headcount to support the volumes of a growing business, or in technology incorporating AI to make that a more seamless and faster process.”

The benefits of implementing an automated supplier invoice management solution are manifold. An independent study

in seven countries by consultants

Analysys Mason found that in SMEs and firms with fewer than 2,000 employees, increased efficiency alone saved finance teams 134 hours a week and an average of £11 (€13) per invoice.

Embracing automation means that these teams can route invoices swiftly to reviewers so they aren’t stuck or lost on email or paper. Where a purchase order system is in operation, the same technology automatically checks and validates invoice data. Digitally centralising the information prevents the kind of duplicate payments that can occur when some invoices are submitted on paper and others are sent by email. The system also flags up fraudulent invoices, which have proliferated postlockdown as chancers try to take advantage of manual processes. About 17% of invoices contain errors. The benefits of an automated AP system is that they generate reports on spending data and trends, giving crucial insights to senior managers. What’s more, by timing payments to optimal effect, they enable the business to manage its cashflow and capital better.

Analysys Mason’s study found that companies using Concur Invoice saw a positive return on investment within seven months and saved an average of £31,000 annually. Having automated their invoice management processes, firms also saw late payments drop by 24% and misplaced supplier invoices fall by 22%.

The issue has taken on a new urgency in recent months as the government, in its own words, “takes action to back small businesses and tackle late payments”.

From 2018 to 2022, the number of late payments fell slightly, from 31% to 26%. In late 2023, the Department for Business and Trade announced tougher measures to deal with the problem, building on its

Reporting on Payment Practices and Performance Regulations.

Initiatives include strengthening the Prompt Payment Code, broadening the powers of the Small Business Commissioner and taking forward legislation to extend payment performance reporting obligations.

“I think the government’s looking at it through a new lens to make sure that it’s enforced better, and there are penalties to make sure that the smaller businesses are able to grow, invest and receive their money in time,” says Milledge.

One significant development came in the Chancellor’s 2023 Autumn Statement, which tightened payment time requirements for firms bidding for large government contracts.

“From April 2024,” said Jeremy Hunt MP, “firms bidding for government contracts over £5 million will have to demonstrate they pay their own invoices within an average of 55 days, tightening to 45 days in April 2025, and to 30 days in the coming years.”

For AI, the government’s intervention looks like a gamechanger.

“It’s going to become necessary to stick to agreed payment terms with suppliers,” he notes. “It’s not just a case of ‘it’s nice that we pay the majority of our invoices on time’ – it’s going to become a requirement of running an effective business.

“From my perspective, it’s not just a case of companies reaching a point where they have to decide whether to invest in additional human resources or in technology.

“In order to source products and services from businesses, do they want to be considered as prompt payers? And will they ever be in a position to tender for government business?

“It seems like it’s going to be a requirement to do business going forward, and that’s good news for business and the economy.”

Celebrating Britain’s Top Performing SME Businesses

Are you a Top SME?

How would you like to pitch your business to battle against the best in Britain?

Well here’s your chance to become known as one of the UK’s best and brightest recognised SME.

Keep up-to-date with updates on the EB100 Awards and also the latest business news, reviews and exclusive insight into the SME community.

We were thrilled to be ranked #3 and was an amazing achievement that we were able to take home the diversity and inclusion award on the night. It was an overall great evening that the team enjoyed thoroughly, Thank you!”