3 minute read

Wool industry faces yet another battle

from Wool2Yarn Global

by Ely Torres

By Yang Xiaoxiong, chairwoman of Nanjing Wool Market

The COVID-19 outbreak in 2020 changed people’s lives. After a difficult fight against the pandemic, many industries in China are slowly recovering. Even shopping malls and catering services are starting to open. Yet one industry, struggling to get back to work, has been dealt another fatal blow. This is the textile and garment industry with the largest proportion of exports. As the outbreak abroad spirals out of control, the biggest concern is the decline in orders, either already cancelled or on the way to cancellation. We are facing an unprecedented predicament and crisis, which is the most incisively and vividly manifested in the current situation of textile industry in 2020.

Advertisement

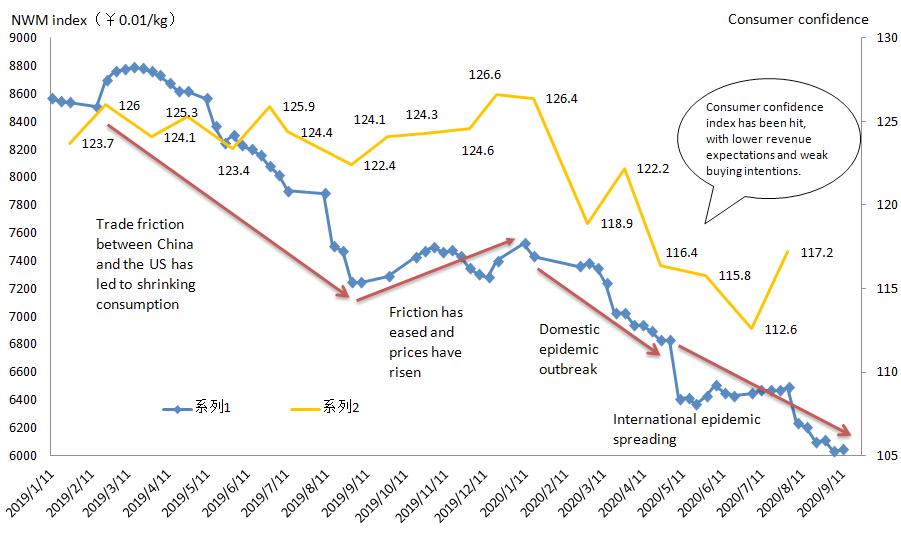

As of September 11, 2020, NWM Comprehensive price index closed at 6043 cents/kg, down 33.5% from its 2018 peak, but still higher than the 2008/09 lowest of 4,014 cents/kg. The main reason is that the market price surged to a new record from 2015 to 2018, and a large amount of high-priced inventory accumulated. Even if the market plummets, it is still hard to fall below the minimum price.

Others are comparing declines to those seen during the 2008 financial crisis and ready to stock up. Although during the economic crisis in 2008 the prices fell, all industrial chains and terminal consumption were basically in normal operation, as the roadblock was removed, so the market recovered soon after financial order was restored. All industrial chains have been damaged to varying degrees, after being hit by the pandemic this

Nanjing Wool Market composite price index and consumer confidence index (January 2019 to September 2020)

year. In particular, the situation is still grim in some foreign countries and regions, where production and life are still stagnant. The economy is far from normal. Prices fell and rebounded quickly in 2008, while it will be a long time before prices recover sustainably this year. The whole market liquidity is impeded.

As external demand is blocked, the strategy has to be changed to “domestic sales”. In order to stimulate the internal circulation economy, the domestic garment market has taken the role of Noah’s Ark. But this time, under the dual effects of the pandemic at home and the decline in overseas markets, we need to be prepared for more pressure. After all, we did “take a break” for a long time in early 2020, leading to job losses, wage cuts, and bankruptcies. Consumers have far less extra income to spend than they used to. Coupled with the pressure of car loans and mortgages, the so-called “retaliatory” consumption did not occur. Moreover, wool is a luxury fiber, not a necessity, so the impact on the wool industry is even more severe.

Of course, there are opportunities in times of crisis. With many of the world’s vaccines already in phase III clinical trials, the pandemic will sooner or later be contained. In the post-pandemic period, every country and region will restore economic systems as soon as possible and increase financial and policy support. There are also signs that the industry is moving in a better direction. According to the customs data from January to July 2020, domestic exports of wool textile raw materials and products totaled US$4.67 billion, which decreased 31.3%. Exports overall situation is still grim, but that was up 1.9% from the first half of the year, a narrowing of the decline for the first time this year. Each link within the wool industry does its best to destock this year. The lower price of raw materials will also arouse the interest in developing products, making products more competitive. Once the global pandemic is under control, market demand will gradually pick up. There are only broken enterprises, not collapsed industries. We believe that the wool industry can be revitalized under a new development paradigm with domestic circulation as the mainstay and domestic and international circulations reinforcing each other.