Renewed

The Power Is Now Media Inc. 3739 6th Street Riverside, CA 92501 Ph: (800) 401-8994 | Fax: (800) 401-8994 info@thepowerisnow.com www.thepowerisnow.com

The PIN Magazine™ is owned and published electronically by The Power Is Now Media, Inc.

Copywrite 2022 The Power Is Now Media Inc. All rights reserved. “The PIN Magazine” and distinctive logo are trademarks owned by The Power Is Now Media, Inc.

“ThePINMagazine.com”, is a trademark of The Power Is Now Media, Inc.

“Magazine.thepowerisnow.com”, is a trademark of The Power Is Now Media, Inc. No part of this electronic magazine or website may be reproduced without the written consent of The Power Is Now Media, Inc.

Requests for permission should be directed to: info@thepowerisnow.com

Pg. 12. Maybe, Just Maybe… vacant downtown office spaces are what the nation needs to solve the housing crisis.

Pg. 14. A Look at the refinance activity, Mortgage Rates, and the outlook in Q3, 2022.

Pg. 16. Opinion: It’s 2022, can technology replace the human touch?

Pg. 20. How the Medical program is changing lives for low-income patients after years of waiting

Pg. 22. Regulation Nightmares! CFPB on the Hunt for Unlawful nursing home debt collection.

Pg. 8. How the Inflation Reduction Act could be a game changer for the clean energy industry.

Pg. 10. The Inflation Reduction Act wills help families steer through tough times, but what are its long-term impacts?

Pg. 25. Want to keep your VA Loan on track? Here is how. by Sharon Bartlett.

Pg. 29. How long does Appraisals take in Maryland, by Emerick Peace.

Pg. 35. A Look at Florida Housing Market What can we learn: Market stats, Prediction and what the market looks like in 2023, by Adriana Montes.

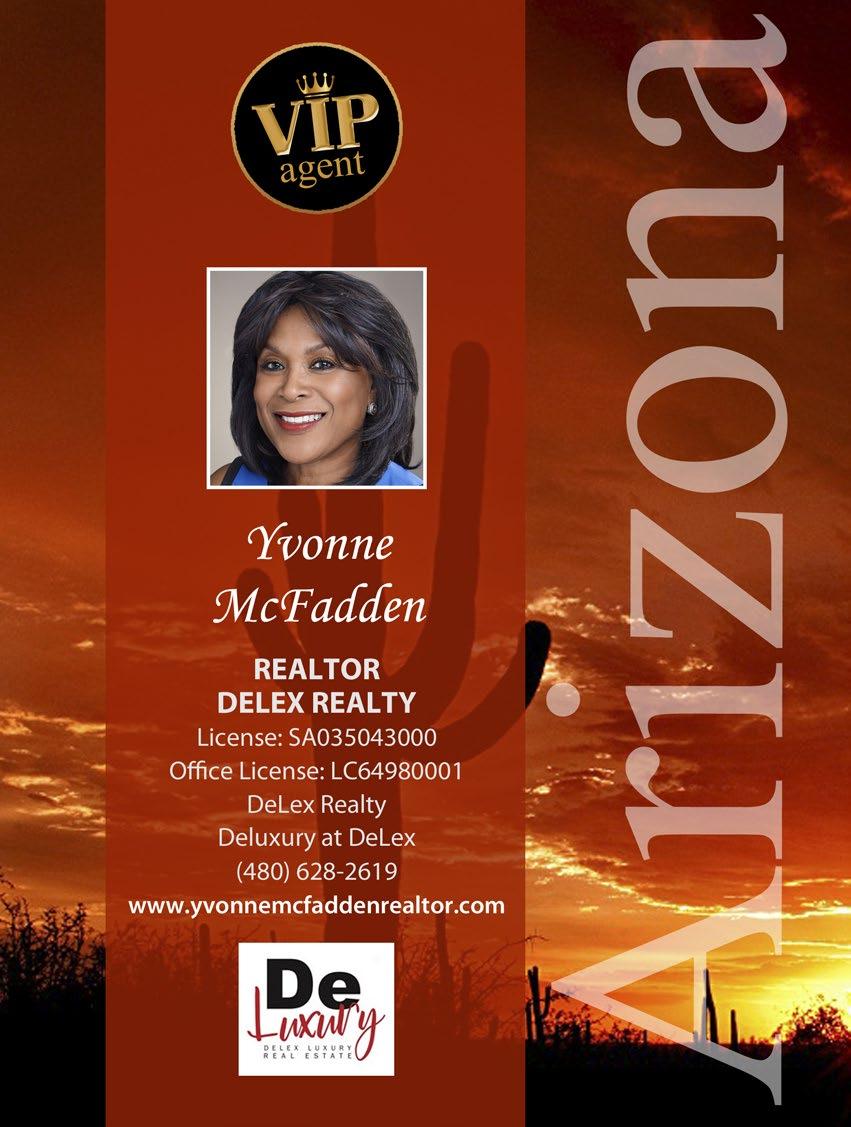

Pg. 39. 10 things you need to know before buying a home in Arizona, by Yvonne McFadden.

Pg. 43. How much will it cost you to move to or from Arizona?, by Tamra Lee.

Pg. 47. How much is too much when presenting your offer?, by Walter Huff.

Pg. 51. Home renovations that are likely to give you the best returns in Akron, Ohio, by Heith Mohler.

Pg. 55. How can realtors and brokers help if you’ve not been approved for a loan?, by Ruby Frazier.

Pg. 58. Renewed hope for r Civil Rights Institute and Fair Housing Council.

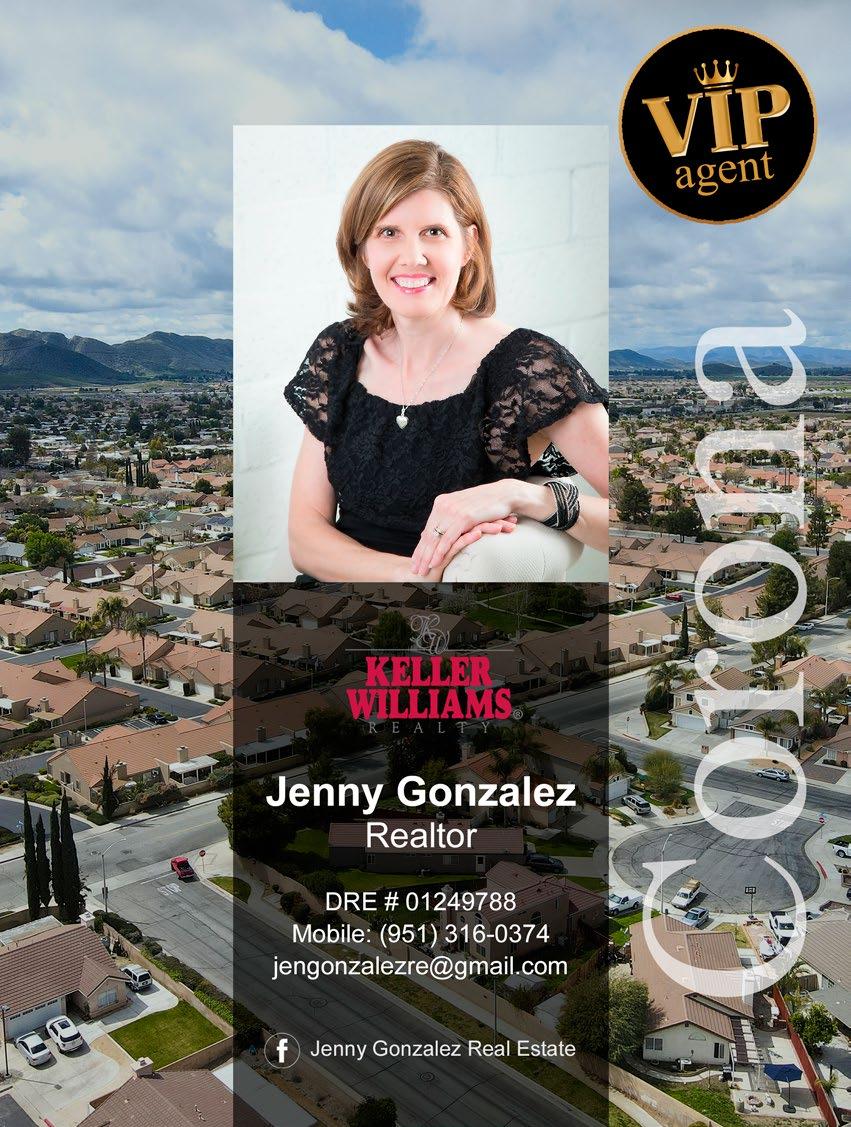

Pg. 65. How do you navigate a tax lien on a home when selling?, by Jenny Gonzalez.

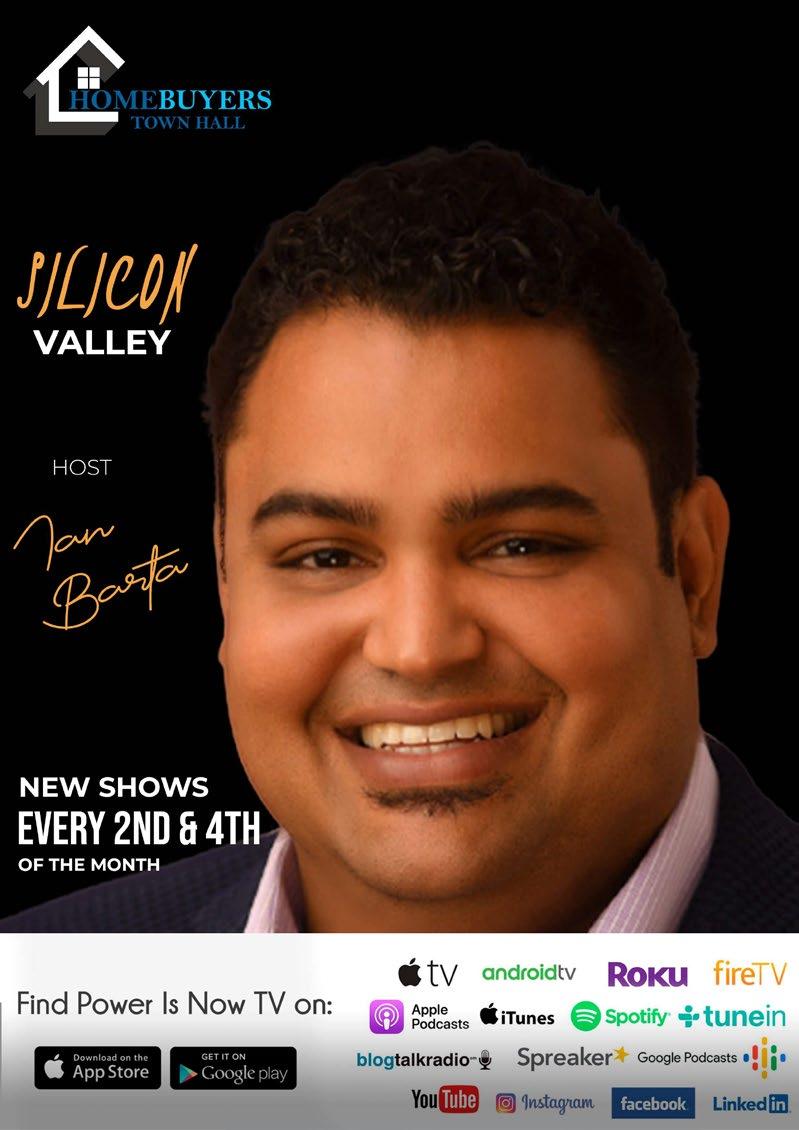

Pg. 69. The biggest mistakes that new Buyers make while House Hunting in Silicon Valley, by Ian Batra.

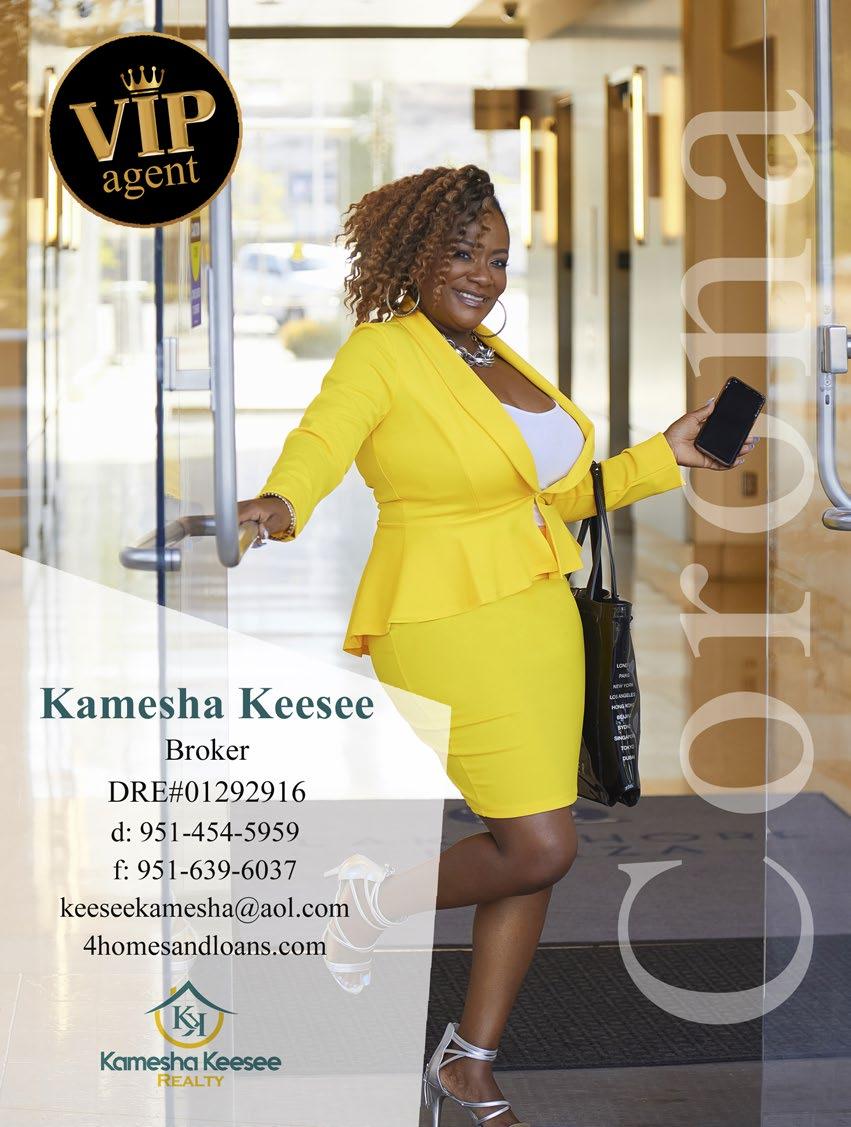

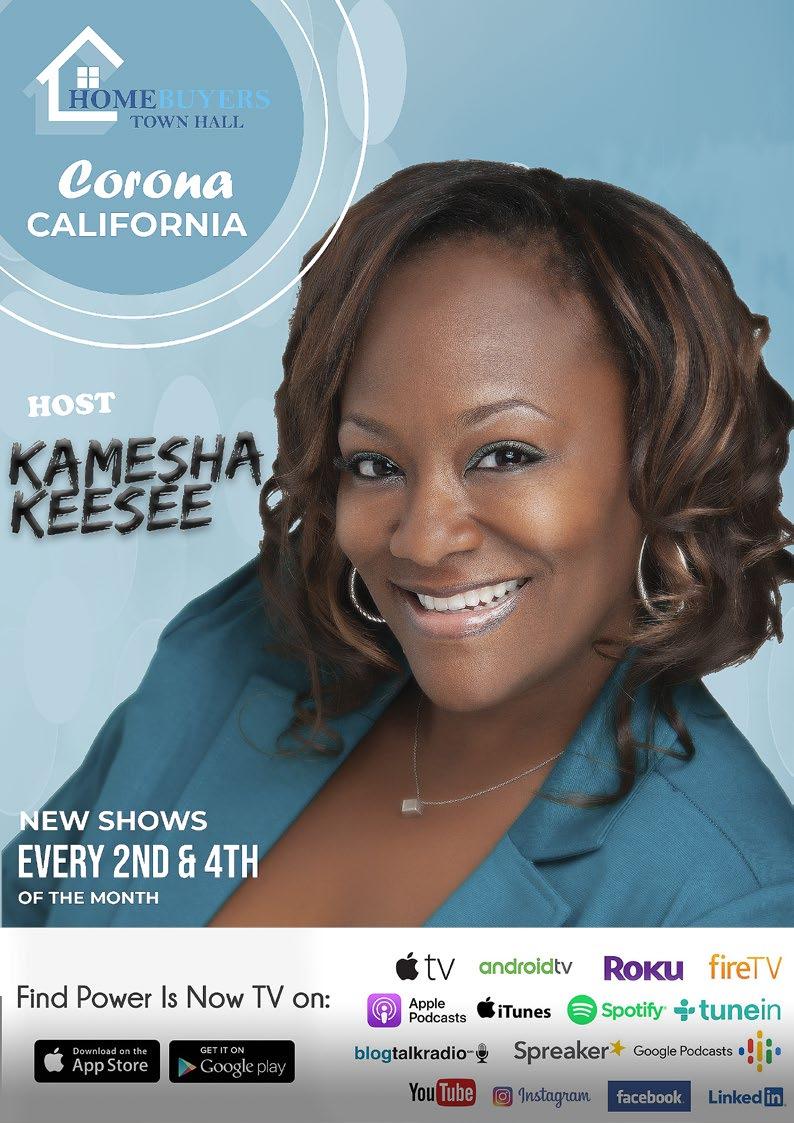

Pg. 73. Ready to become a homebuyer in Southern California?, by Kamesha Keesee.

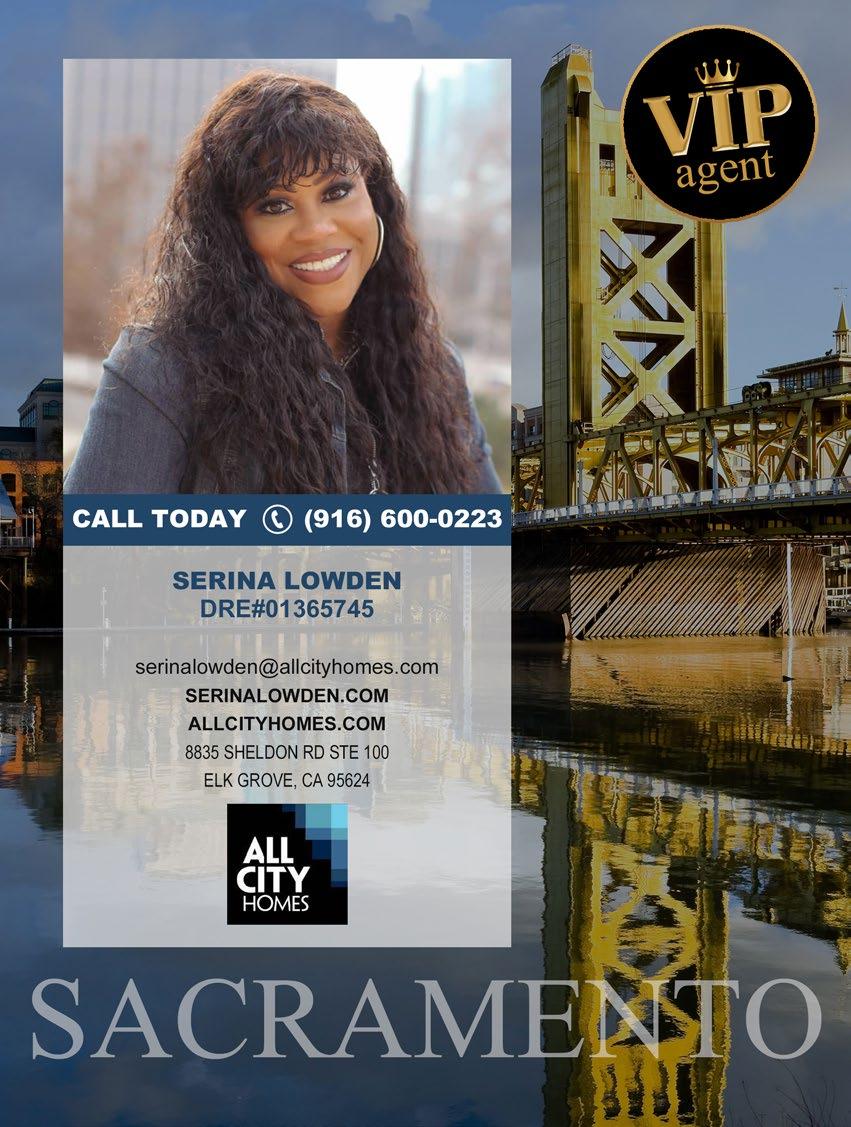

Pg. 77. Is writing a real estate offer letter worth it? How to write a winning Offer Letter, by Serina Lowden.

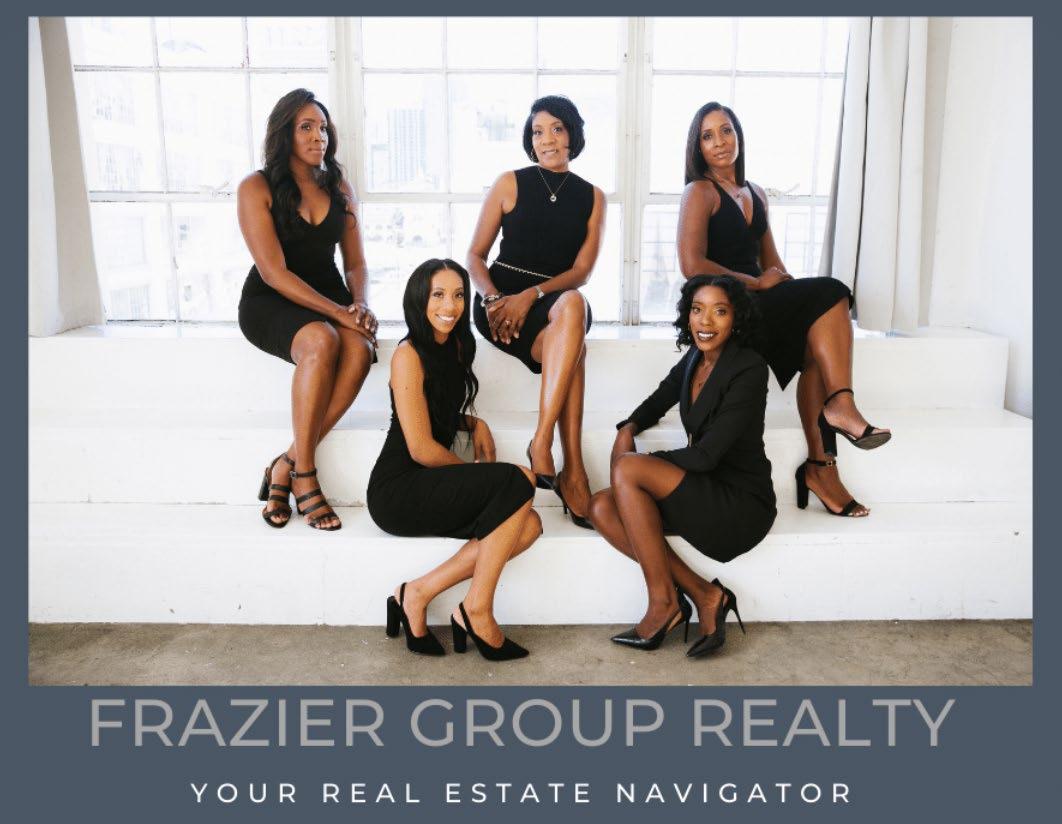

Pg. 81. What is a listing agreement and how will it affect your selling process, by Briana Frazier.

Pg. 87. Up your buyer’s game.How to buy a house even before it hits the market, by Francine Marsolek.

Pg. 91. Getting the Final Stage of Homeownership Right!, by Janet Petrozelle.

Pg. 95. Does it make sense hiring a real estate agent?, by John Costigan.

Pg. 99. Is it possible to negotiate Real Estate Agent Fees? 10 things you must know first, by Norman Green.

Pg. 103. This is how best to price your home in a sellers’ market, by Steven Rivkin.

Pg. 107. Want a Piece of SoCAL?Read this First!, by Decira Pimental.

Pg. 111. Ways to make banks say yes to your REO offer in California today! by Monica Hill.

Pg. 114. The City of Riverside Approves Homeless Action Plan to Deal With Rising Cases of Homelessness.

I want to remain optimistic heading into the fall season as I have throughout the year. In our last edition, I expressed that the third quarter was perhaps one of the toughest quarters I have experienced this far. But even that isn’t enough to shake me off the ground.

Yes, I want to remain optimistic and there are pointers I can already see that reaffirm my position. First, the sky high gas prices are falling consistently in many parts of the country and while for many people the current prices are still somewhat high, it is good enough reason for me to be hopeful about the coming year.

Secondly, I am pleased to announce that The Power Is Now team keeps growing. Jamar James, a name most familiar to the cryptocurrency industry is now a VIP Agent on our platform. I am excited because James brings a wealth of experience to you as a buyer, a seller or even as an investor on how you can incorporate crypto-currencies into your everyday life. Therefore this is a new and exciting frontier for all of us.

Additionally, I am excited to also announce that finally, the Civil Rights Institute has a new home in California which will open its doors towards the end of the month. I am pleased mostly because its a momentous event for us, and i mean us because i sit on the board of directors of the Fairhousing Council of Riverside i feel so proud seeing the remarkable progress and impact that the council has had ever since its founding in 1986, 18 years after the enactment of the Fair Housing Act, for which the council stands to scrutinize. As such, seeing this dream come to life is an honor for me.

In our magazine, we feature the Fair Housing Council of Riverside and the Civil rights Institute and we tell you a little about what these organizations do and what they stand for. We also go into brief details about the president of the FairHousing

Council of Riverside, Rose Mayes. Interestingly, last year in our October issue we also did a profile of The National Association of Advancement of Colored People (NAACP) and its president Derrick Johnson.

We also feature several articles that detail the topic of inflation including how inflation is affecting the clean energy industry, and how it is affecting the family unit. In addition, we also tell you why downtown vacant offices might be the answer we need to solve the housing crisis in our country. This is an issue you cannot miss for anything.

At this moment I would like to thank our readers,

listeners, and contributors for their continued support. We invite you to join us online for invaluable blog posts, engaging radio shows, and the latest issues of our magazines to enhance your learning in the field of real estate, finance, and success. You have the power to change your life, because The Power Is Now.

The Power Is Now Media, Inc.

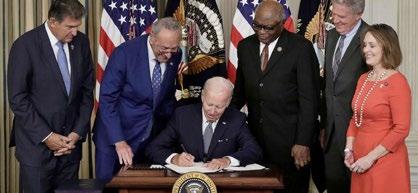

The Majority leader of the senate, Chuck Schumer, and Senator Joe Machin of West Virginia brought the inflation reduction act. It is a bill focusing on heavy investment in clean energy and solutions to climate change. Included in the act is channeling 370 billion dollars towards climate expenditure which, in return, will reduce 40% of carbon emissions by 2030. Strategies to be used towards achieving clean energy in the reduction act are as follows;

Tax credit for Americans to buy electric vehicles will reduce the energy usually released by vehicles powered by fuels that release carbon dioxide into the atmosphere. The U.S government will give such tax credits under two terms and conditions: for new electric cars, a tax credit will be at $7500, while used vehicles will receive $4000. The inflation reduction act encourages people to adapt to electric cars since they do not release any carbon wastes into the atmosphere.

The bill will not only take into consideration small vehicles, but it will also channel 3 billion dollars to all U.S postal service trucks ensuring they are all electric. Furthermore, $1 billion will be set towards heavy-duty electric vehicles, school buses, and garbage trucks. Similarly, $3 billion set aside will ensure U.S ports release zero emissions to the atmosphere in the fight to adopt clean energy.

The inflation reduction act will also consider home appliances by giving Americans a ten-year consumer tax credit. The bill will also dedicate $9 billion to ensure a discount plan for consumer home energy appliances and environmentfriendly retrofits. By so doing, energy for use at home will be efficient and run smoothly on clean energy by ensuring rooftop solar panels, electric HVAC, and heat pumps are available at more affordable prices.

In the bill, Senate majority leader Chuck

PHOTO FROMSchumer and Senator Joe Machin also included a tax credit that will benefit investors and manufacturers who incorporate clean technology. Examples of such companies are manufacturers of electric vehicles, solar panels, and wind turbines. A tax credit will be essential to them since it will make it easier and encourage them to continue using clean technology and make what they produce more affordable to consumers.

ensure that those who pollute the environment are taxed to fund sufficiently cleaning the environment. To protect and acquire the old-growth forests which serve as essential carbon sinks on the National Forest System land, the act will set aside $ 50 million.

The bill, as indicated, discourages the use of fossil fuels. Still, various provisions will be of merit to the fossil fuel development, such as necessitating charter sales for offshore drilling.

Environment America Washington Legislative office Executive director Lisa Frank in her statement raised the issue that Climate change and other severe environmental challenges are, in one way or another, a barrier to future generations. She encourages people to “create, build and invest,” but most importantly, she encourages people to take care of the natural environment to reduce the worsening heat waves, drought, and fire.

said, “As the saying goes, we do not inherit the Earth from our ancestors. We borrow it from our children.” He also indicated there is a need to rectify climatic change, which is worsening, and infusing the inflation reduction act will act as a game changer and enable the future generation to work in a suitable environment.

Although the bill is not merit, the tax credit will benefit Americans of all colors. It will be an actual game changer. Since the credits are determined to ensure all Americans shift to electricpowered vehicles, install solar panels in their homes, and buy cleaner, more healthy electric appliances that do not pollute the environment in our places of residence and the community.

Besides tax credits, the inflation reduction act is also concerned about methane emissions and includes a program to reduce its release into the atmosphere., there is a plan to

She continues by saying that achieving a “bright future” is still possible by encouraging renewable power and improving clean energy technologies. The inflation reduction act will take part in the journey of having a clean environment by ensuring the process runs smoothly and fast. It also will provide powerful tools to accelerate construction.

U.S PIRG Environment Campaign Director Matt Casale

By making environmental polluters bear the cost of cleaning up superfund sites, most Americans will avoid releasing hazardous wastes to the environment so that they are not taxed.

Lisa Frank also admits that the bill has several shortcomings in that it is a barrier to offshore wind expansion and consequently threatens sea life due to continued offshore drilling. It also does not protect the Arctic National Wildlife Refuge, which is often classified as America’s Serengeti, but the issues will be fixed.

The Inflation reduction act, passed by the National Congress and Signed by America’s President Joe Biden, will make huge investments toward climate change and improve health care. The shift to clean energy and low prescription drug costs will lead to a low cost of living for most Americans by having affordable, safe home energy, electric vehicles, affordable health, and prescription drugs. It will also have long-term impacts that will reform consumer morals and ensure that economy and politics are well aligned.

Asindicated earlier, families will be able to save due to the IRA act. For example, a family comprising four people can save up to $6,700 on health care and energy costs. On the other hand, young adults can save up to $7,700, and elderly couples can save the most money being $17,000.

The viability of saving through the IRA act will be evident when upgrading their home appliances, and incorporating energy-efficient appliances will lower the cost of living and reduce indoor air

pollution.

IRA also makes it possible to acquire tax credits for purchasing electric-powered vehicles. According to consumer reports, EVs save up to $2,600 in annual fuel costs. On the other hand, IRA makes it possible to have affordable health care by allowing health care facilities to bargain on medical prices and ensuring that drug firms do not hike prices more than inflation.

On a long-term basis, the Inflation reduction

act signed by U.S president Joe Biden will be active in several ways. The five most essential outcomes expected are such as;

The law enactment motivates middle-class and low-income people to purchase into a more clean and competitive economy.

For over four decades, the American community has been unsuccessful in strategizing climate proposals in a way that would benefit people of all classes. However, the 2022 IRA act embraces people of all races by giving provisions that will lower household costs of energy and shift energy use and utilization behaviors.

Tax credits on electric vehicles, renewable energy systems, and heat pumps will greatly merit millions of people legible for such distinctions. In the long run, consumers can save up to $1,800 on the energy bill per annum, according to Rewiring America.

Since world war two era, the U.S government has had friendly policies that encouraged the creation of the internet and telecommunications, among others. Inflation reduction encouraged Americans to invest heavily in environmentally friendly technologies or upgrade existing innovations by adapting to clean technology. IRA aims to enhance energy security, reduce carbon gases, incorporate clean technology in transport systems, deliver environmental justice, and support unprivileged communities.

The U.S government will also fund research and development so that 40% of greenhouse gases are reduced by 2030. It will directly participate by penalizing environment polluters and indirectly by having credits on wind technology and other energy programs.

During a Congress which included Senator Joseph Manchin, the IRA designed a law that favored new technologies over existing ones,

mainly in the fossil fuel sectors. As much as petroleum and chemical industries will take part in the journey towards an eco-friendly environment, new and emerging technologies will be favored more while steering competitiveness in the market.

The IRA aims to support the undeserved communities like the 2021 Bipartisan law by prioritizing wind technology and solar energy, significantly benefiting low-income people. IRA will further give construction efficiency refunds and allocate rural development to assist farmers in high-poverty areas. Such programs will encourage the creation of climate justice grants and focus more on improved air pollution monitoring.

Public policy is almost catching up with public opinion with the IRA act. It involves enforcing a pro-consumer and pro-business law that separates the public mind from business and political interests, which aims to preserve income and other inequalities.

The IRA act has left many business people stranded and unsure of which side to take, such as Mary Barra, the CEO of General Motors, who during Obama’s era accepted a bailout on bankruptcy and, During Donald Trump’s era, opposed her commitments. She further opposes the Inflation reduction act due to the corporate tax it entails and the also its environmental provisions.

The government has to be tactful and skillful in managing approved IRA funding over the next decade, ensuring it overcomes all possible challenges. Since IRA is centrally based on capital incentives over-regulation, it allows for successful future economic and political coalitions. New clean technology investments have led to job creation and wage increases among most people, stabilizing the nation to be more eco-friendly at cheaper living costs.

Currently, the U.S is facing a significant housing crisis since both rents and house prices are at or near record high levels. High inventories and the ever-increasing demand are various reasons leading to such instances.

It has also led to the realization that office spaces in prime land are empty and might not get back to full occupancy since most workers have settled on working remotely and thus will never return to their town offices. Workers in expensive cities and costly commute

areas will not get back to their offices and are comfortable working from home.

America is tossing on new norms after the Covid 19 pandemic. Realtors are unsure how to handle the unresolved issue of empty office spaces on prime land, especially in urban areas and the suburbs. Even as most workers return to the office for the first time after the Pandemic, most buildings are half empty, and their future is uncertain.

Some office buildings will

probably be converted to apartments, townhouses, condos, and other facilities. A shift towards converting empty offices to residential places will hugely add stock to the tight market. According to Brian Kropp, Vice President of Research in Human Resources at Gartner, “We’re not going to need as much office space as we have now,” Thus, it would benefit the city if they utilize that space in other ways.

In a survey conducted by Security Systems Company, Kastle office spaces are 43% occupied. Large companies

such as Twitter are downsizing their office spaces since it has allowed their workers to work entirely from home if they choose to. Other mega companies like Apple encourage workers to report to the office at least twice weekly.

Converting offices to homes is not new to Americans. It started in 2010 when the nation was facing significant impacts brought by The Great Recession, and since then, it is something that is being slowly incorporated.

According to the rentals site RentCafe, approximately 8000 units were converted to residential units from offices, particularly in Philadelphia and Washington D.C. 2022 looks forward to receiving 13000 units ready for residential use emphasizing primarily in Los Angeles and Cleveland cities. The act of converting office space to homes could be more rapid due to uncertainties witnessed after The Covid 19 pandemic.

Converting office space to residential units is quite challenging due to the immense work included, the lengthy timelines for the completion of projects, and many regulatory barriers. In most cases, office buildings with the most opportunity are

also the hardest to invest in and thus take longer to complete.

Companies such as financial and legal firms have ordered employees to return to their offices fully five days a week. However, employers also agree that not all employees will agree to return to the office fulltime, especially if it is possible to execute all functions remotely. For example, in New York City, most of its workers work from home, and only less than 40% of the workers return to the office.

In other Cities such as Texas, more than half of the employees had returned to their offices, especially in affordable areas such as Houston, Austin, and Dallas.

Most firms prepared well that about a quarter of their employees will continue to work from home while more than fifty percent of the workers will be hybrid, leaving only a small group of people who will fully return to their offices.

A lot of office space is going to be left unused. Instead of companies having them and catering for rent and other technical services monthly,

it is cheaper to downsize the excess space. So that they fulfill the real estate needs other than leaving such areas unoccupied for an unpredicted duration of time which could extend to over 20 years.

The most probable houses that will be converted to apartments and condos are houses constructed in the 1970 and 80s. Such buildings are considered those of EPC class C and are not modern to suit modern needs, such as indoor and outdoor space and a lot of light, among others. For instance, 550 luxury apartments in Philadelphia were converted from initial office buildings.

There is hope that most empty office spaces will be converted to residential homes encouraging a 24/7 life in most cities. The drive to utilize office towers is beneficial not only to developers but cities as well. As much as office townhouses will be converted to residential homes, there will still be enough space for office use. When workers need to collaborate and work together, young workers, who usually love meeting their colleagues in person, have enough room.

Aswitnessed, refinancing went considerably low compared to previous years. However, mortgage equity withdrawals continue to increase since most people use the second home loan, also known as home equity, to finance their housing.

During Q2 in 2022, cash withdrawals fell to 30%, leading to an increase in home equity lending of 30% quarter over quarter, the highest increase witnessed twelve years ago.

According to the flow of funds report, mortgage debt between May and July 2022 increased to 260 billion dollars. In the past years, mortgage debt declined due to homes sold on short sales and foreclosure wiping out the massive debt. Since part of the debt is used to add stock to the housing market, it cannot be classified as mortgage equity withdrawal.

During Q2 in 2022, mortgage debt was at 1.4 trillion dollars but was 48.9% lower than Q1 as a percentage of gross domestic products, and also slightly higher than during the housing bust. It, therefore, shows that homeowners have considerable home equity, which makes mortgage equity withdrawal, not a bother.

According to calculations carried out by the Fed’s flow of funds data, Net Equity Extraction was 169 billion dollars of the disposable personal income. Equity extraction in the last year increased as compared to previous years.

Mortgage rates are currently constantly moving, both higher and lower. In the last week, mortgage rates lowered slightly, although the new rates are still high shortly after delving into Q3 in 2022. Compared to Q2, specifically in June, mortgage rates were low, and one would have to trace back to 2008 to witness higher rates. Although various improvements were implemented, the impact was not felt because the stock market started to lose ground shortly after a scheduled auction of decade-old treasury notes.

Although a ten-year-old treasury is not associated directly with mortgage rates, it affects bonds that predict the mortgage. The two factors interact well depending on the day

involved since the stock market is differs on different days,

Bonds and rates are used interchangeably and are essential in Fed Fund’s policy. For instance, the approach is more likely to lend loans to a group of people who want the money acquiring mortgage bonds than to people who require a loan for investing in a ten-year treasury.

Fed funds rely heavily on a short life span spectrum which is crucial to all traders and thus the reason why they love dealing with a mortgage since they are more profitable in shorter periods.

Fed funds are also very strategic in tackling inflation. By raising the fund’s rate and making capital costs higher, the flow of credit to enterprises and end users lowers, pushing demand lower and pressuring the market prices.

Such factors are important as far as

mortgage rates are concerned since Fed considers such data when the amount is to be hiked for the Fed fund rate. Higher inflation rates than expected and robust data will lead the Fed Fund rate to hike prices, negatively impacting mortgage rates and making it almost impossible for people to acquire homes.

The high Feds rate predictions are highly dependent on the upward shift in the shorter term, such as mortgage rates. The above principle is inversely proportional to a ten-year treasury.

For the case of Q3, if inflation is going to happen, the Fed fund will thus increase the funding rate and thus lead to higher mortgage rates. Therefore, it indicates that house market prices might increase in the tight market with high demand exceeding supply which is why Q2 experienced decline in financing of homes and opting for equity loans due to the impacts of high inflation. The trend might proceed in Q3 if the issue is not resolved.

Summing up, mortgage rate, Treasury notes, and Fed fund policy work hand in hand directly or indirectly. As a witness in the year’s second quarter, high inflation rates negatively affected homeowners refinancing their homes, leading them to home equity loans resulting from the high living costs.

Mortgage debt increase is also vivid with over 200 billion dollars, the highest debt recorded since 2006. However, as the debt rates rise, the number of new houses continually increases, showing some hope of saving the high inventory levels.

Mortgage debt is taken as part of GDP percentage and prospected to be higher compared to Q1 by 48% and at the same time down 73.3% from the high levels experienced during the housing bust whereby the actual figure was 1.46 trillion dollars from the top.

Although there is a rise in the mortgage equity withdrawal, the percentage is minute as disposable personal income than during the housing bust. Most homeowners have enough equity and mainly rely on home equity lines for equity acquisition.

Everywhere you go these days, there’s the talk of automation and technology replacing the human touch and there is no doubt, technology is surely advancing at a very rapid rate. Focusing on the mortgage production, one thing is clearly evident, the process has become so centralized and very automated and even though the process is a little paper based. Major hallmarks that will soon be the face of this industry have come up changing the tone and shape of the industry.

Everything has become so easy, loan underwriting, using some electronic signatures as well as establishment of user-friendly “portal” which help the users to oversee their loan application and thus faster delivery and approval process which makes it become a mainstream in loan application and delivery. Loan approval has also become very easy and fast, thanks to the automated borrower-verification tools.

We may argue on this issue

but logically, technology has done so much for the economy and has changed the way businesses are run and conducted. But here is what Kermit Randa, CEO of PeopleAdmin has to say about technology and human touch;

“Even as we celebrate the contribution technology makes to helping educators do their job most effectively,” Randa says, “it is important to recognize there is one thing technology

will never replace: the value of the human element in helpings schools, students, and communities succeed …”

However, even if there is so much evolution in mortgage lending and all what goes in and out of this world in so far as technology is concerned, the overall user experience has not gotten better yet. Basically, there are so many challenges that are yet to be overcome. Financing a home for example for many people is still very confusing since most of the consumer or the borrowers are unable to get what they are looking for in terms of help in solving the many puzzles in their head.

some new ways to give their borrower counterparts a combination of technology and human expertise. Therefore, replacing human touch with technology is something that will have to take time.

This should be the time where mortgage experience for the consumer should be improved and given that the country has a very strong job growth rate as well as a stable home-sales, the purchase-loans volume is expected to increase in the current year and the year to come.

Back then when the housing market was doing fairly well, a few consumers were able to get approved mortgage online. It was in this phase the mortgage lenders were in complete dominance of the whole process which was neither automated nor efficient.

But with the technology, the industry has seen enormous changes and a number of innovations and with this improved technology, verification of borrower’s income and the assets are instantaneous. When searching for loans and their pricing, the process has become so easy and very fast, thanks to the new and improved technology.

Everything has become electronic for the improvement of the consumer experience, and what’s even fun, people can now sign disclosures electronically and also, ordering tax transcript from the IRS has become an electronic process.

Technology has done so much for a change in the way things are in so many sectors today but the same old taste of mortgage cannot be replaced, not that easily, reversing this trends will require the lenders to find

But we have to face one fact, even though that all these huge steps have been made for the benefit of the consumer, many of them have been motivated by the needs of the lenders to cut the costs and manage them.

Technology has also enabled the consumers to get access to greater and more informational systems about the mortgages than ever before. Most of the consumers have very little information about mortgages but with the access to the information, they become informed. In some ways, technology may have made the consumers not dependent on the human expertise which they largely depended on to make some of the crucial financial decisions of their lifetime.

With what technology have done and still continuous to do, many borrowers still fill out the forms manually meaning that incorporation of the technology to the process has not well been accepted or the coverage is still very low. Ironically, it turns out that most of the borrowers are interested in a good loan rather than technological touch in mortgage issuing process.

People are going for what not works, simply, their focus is on things that do not show results yet more and more mortgage lenders are putting more emphasis on social media and stuff, however, even though that is great, research from

Mckinsey proves that emails are more effective but as it is, more lenders cannot even respond to a single email within a day.

We all would agree that making the mortgage process faster and much more efficient remains to be at the peak of every lenders but as it is, most of the professionals want to take advantage of the prevailing strong housing market to make a boom in their business.

Online portals, a tool that has been on the rise and many lenders are realizing just how important this tool has been in reaching so many consumers out there. With these portals, consumers can now apply for loans and get approved in a much faster way. Actually, no loan officer is required to oversee the process.

But this tech has a problem, a major drawback and perhaps that may be the number one reason pushing people away from these improvements. If you are a borrower, and say you get stuck on the process, there is no one to help you or if you have a question, there is no one to assist you.

These portals are very important and have seen the success of many mortgage seekers. One thing you will realize is that automation creates consistency and can be applied as an effective tool in helping the loan advancer in seeing the loan advancement to the borrower through.

Can technology replace the human touch? I will surely say that it will depend. Somehow, if you look at what technology has done in the industry in so far as mortgage lending is concerned, there are huge strides that it has enabled and still much credit has been given to the changing technology and its impact. However, none of that would ever be possible without human engagement. The whole process needs human touch since humans are the source of the ideas while tech is just a facilitator of the tech. Therefore, even though automation has well been encouraged, overly, it cannot replace the human touch but we can still push for more and more digital mortgages and responsive tools and in doing so most borrowers should understand that many people are looking for the right mortgage rather than a fast one.

Medi-Cal is a medical program initiated in California and aims to help middle to low-income patients by partly costsharing medical costs. Medical is essential as it will help caregivers ease the high price of taking care of older relatives at critical times when people are struggling with jobs and also taking care of their younger ones. It will also reduce the burden on senior citizens who lack a stable income and cannot fully cater to assisted living expenses.

Two U.S residents, Chelsea Oruche and Kelsey McQuaid, face challenges in caring for their parents. In Chelsea’s case, her mother is seventy years of age, and taking care of her is pretty cumbersome since she has a young kid going to school, and at the same time, she is attending a law school. Due to her mother’s old age, she deserves better health care and attention, and Chelsea does not have the experience.

Kelsey McQuaid’s case is similar to Chelsea’s in that her mother, who is 67, also needs assistance, and her wife expects a child. Kelsey’s family finds it challenging to give their mother full-time care and attention, especially because she has Dementia and also needs a memory care program.

The above incidences are common among most American families. In the next decade, demographics show that more than a quarter of the people in California will be above 65 years of age and thus require special care and attention. Aided living and memory care facilities are expensive, ranging from about $5,000 to $7000 each month. The prices remain high even for people that receive more income and could be said to be living comfortably. Medi-Cal programs have been of help and a source of hope for caregivers and seniors. So far, it is active in 15 counties, Los Angeles and Sacramento.

There is high demand for the Medi-Cal program, and although it is expanding, many people will wait up to one year before they benefit from the plan and are put in an assisted living center. Some people who will benefit from the Medi-cal plan have been waiting since 2019, indicating that patience is necessary to be a beneficiary.

Recently collected data showed that over 6,000 people are registered under the MediCal assisted living programs while over 4500 people are waiting to be enrolled. Assisted living programs are helpful, especially for people with

special needs and physical disabilities. Demand and supply.

As indicated earlier, demand is high while supply is still insufficient to care for almost all families requiring special care and can no longer take care of themselves, especially the low-income seniors. Thus, there is a need to put up more facilities to reduce the number of people on the waitlist and make life easier for most people in the long run.

Needs for more facilities led California to seek permission from the federal government to add 7,000 spots for older citizens. Medi-Cal needed to seek consent since the state and federal governments fund them. Hopefully, by February 28, 2024, the waitlist will reduce by Medi-Cal admitting more people into their facilities.

The success of Medi-cal is also dependent on external factors such as the availability of beds and continued supply and demand. Medi-Cal aims to align assisted medical services, making them easily accessible for people of all classes. Medi-Cal is a program that partially pays for older seniors leaving them to cater for bed and board fees. Although the health program has existed for quite some time, most Californians are unaware of the initiative. According to advocates, need is more critical than waitlist numbers. They emphasize that most people should be knowledgeable about the program to understand

it better.Maura Gibney, a California Advocates for Nursing Home Reform director, classifies Medi- Cal as an opaque initiative since most Californians are unaware of its merits. The conclusion was based on the low outreach vivid among citizens.

Medi-Cal is primarily for seniors who require full-time attention but necessarily do not require it in a clinical facility for occupancy. More than 50% of older people and those with disabilities require full-time help and assistance in their daily activities. Roughly 20% need help with personal activities like eating, bathing, and even clothing, while 40% of the seniors also require this help but are not receiving any. Qualified people, such as those with disabilities, benefit from Medi-Cal assisted living.

Seniors already benefiting from Medi-Cal can be enrolled in assisted living facilities in two ways: either as a transfer from a nursing home (to enable the state to save more money) or after being discharged from the hospital. Such individuals are prioritized and do not have to get on the waitlist.

Other means that lead to people not being put on the waitlist are consulting the Adults Protective Service Agencies, which was practical and of great assistance to McQuaid and his family.

The Consumer Financial Protection Bureau is a financial office whose primary attention is channeled towards older Americans protecting their finances and enabling them to make sound decisions on matters regarding their capital as far as age is concerned. CFPB aims to address and safeguard older citizens from risk emerging from consumer protection and ensure consistent and effective enactment.

CFPB worked toward protecting older citizens and conducted a survey that put together the challenges nursing home residents and caregivers encounter, which in turn cause financial harm to consumers. A part of CFPB’s results was on home debt collection practices that home expert nurses carry out, lawful aid, and elderly law attorneys.

Collecting debt unlawfully affects family members and friends. There are over 40 million people who take care of older pals catering to their health and functional needs. Nearly one person in every six is responsible for an aged relative or a friend. In as much as the National Home Reformation Act does not allow non-residents to add personal responsibility for the resident’s care cost, it has become a common issue as a result passed by some nursing homes.

Consequently, such nursing homes have severe forms of punishment for friends and relatives with arrears. For instance, they can either sue such people in court, hire debt firms to collect payments, or worse, report debt to a firm that deals with credit reports so that their credit score is altered negatively. The rules are based on the “responsible act,” signed by the person assisting the resident with the admission process. Some of the negative results of the act are that it can lead to bankruptcy and foreclosure on homes of people responsible for older relatives in nursing homes.

The high cost of a nursing home will probably lead older people who need aid to run into debt. In most cases, the average price of a nursing home is slightly above $100,000, which has been so from 2004 to 2020. The costs are expected to rise further by 60% or 19% if the prices stabilize for inflation.

Due to demographic changes, people will likely need nursing home care in larger groups by the

year 2060. Especially people above 65 years require being in nursing homes for at most one year and a few months, which could extend up to two years. Statistics state that women, blacks, and lower-income people are more likely to have over two years of nursing home care.

Third-party family members taking care of their friends at a nursing home are sometimes in awkward positions where they have to choose between taking care of their family and ruining their financial life. Affected relatives raised the alarm about the issue, which led the Department of Health and Human Services Centers for Medicare to write letters to nursing homes urging them to follow the law.

NHRA has a law prohibiting nursing homes from asking third parties to take responsibility for people in nursing homes, but the practice continues. It is incredibly vivid when family members are invited to sign numerous contracts, which in one or another make them responsible for their older relatives. Such prohibitions apply to both residents and future residents irrespective of whether or not they qualify for Medicare and

Medicaid programs.

Some of the observations that CFPB found out were that some admission contracts make the third-party responsible for nursing home residents. These contracts may appeal to nonresident relatives since they are emotionally attached to their older family members. They may also appear to be internally contradicting where nursing homes in later stages include provisions that seem to make the third party personally responsible.

CFPB also found out that some nursing homes forcefully make third parties responsible for their older folks that do not submit a time and accurate application for Medicare. When residents do not make timely payments, non-resident friends and relatives are forcefully made to pay and, if not, threatened and harassed.

There are instances where such nursing homes sue the third party, especially those not well aware of the terms and conditions of the contract. Some non-resident friends and family who probably cannot afford a lawyer to represent them in court are wrongly judged, leading to foreclosures on their homes and bankruptcy.

Nursing homes are critical to older Americans, and the number of people needing such care is increasing yearly. However, costs of nursing homes are expensive since there is limited coverage which causes older people to deplete all their savings and accumulate debts.

Although NHRA, on the other hand, prohibits nursing homes from charging third parties for their relatives. However, the act continues by making the non-resident member sign numerous contracts during admission. Although the CFPB is against charging non-residents, there is a probability that unlawful debt collection practices may continue, especially in nursing homes.

AVAloan is a type of loan that is given to veterans and their surviving spouses by the U.S government. To keep the VA loan on track, it is important to carry out strategies such as;

Pre-approval is not a guarantee that an individual will receive a loan requested, and indiscipline with credit is incredibly a bad idea. An individual who is financially indisciplined if he or she is always on the high debt collectors and such scenarios can greatly jeopardize the possibility of getting a loan. As someone who intends to maintain a good credit card report, it is advisable to pay debts on time, and of course, one has a stable worth to rely on.

It is advisable not to make purchases that require a lot of money, such as buying a new car or new set of seats, especially when working on a credit score and before closing on a property. It is dangerous for a person to get major purchases and can be a reason for a mortgage lender to deny a prospective buyer a loan. A buyer can then make the purchases after closing but be aware that it will affect the debt to income ratio.

Major career changes lead to lower credit points if not well taken care of. Lenders have to the on the buyer’s employment status before the closing dates. Changing a job does not result in automatically being denied a loan. It

can be given, but the process will take longer. Regarding career, remember that VA loan is given to veterans who are out of the job due to some condition but not any form of financial discipline.

A VA loan, just like any other loan, requires those that are legible to have with them all financial documents needed, such as tax returns and pay stubs. It is also necessary to clearly indicate who you are as a buyer and why you need the loan and also assure them that you will pay the loan in time and clear it in the near future. Some of the documents that the mortgage lenders need are a VA disability award letter, pension award letter, and military retirement account statement, among others.

A borrower of a VA loan requires proof of eligibility. Clients of the award consult their mortgage lenders, who instantly check online and give the certificate to the individual in need of it. There are cases whereby not recorded online, making the process take a little is bit longer, normally a few weeks or even months. In such instances, the buyer will go to the mortgage lender, who will further guide the veteran on going about the whole issue. Clients should know that only military veteran is legible to have such certificates.

A loan officer normally collects documents and forwards them to the underwriter to review and approve them. It is normal for the underwriter

to ask for additional information which they find necessary. Loan borrowers should not be afraid of such incidences but answer as quickly as possible for a faster closing. Alongside the documents include additional personal information such as phone number and email address so that underwriters communicate easily with the loan borrowers. Responding to the questions asked faster fastens the process of loan approval.

For example, a mortgage lender may need a pay stub to approve a mortgage. For example, there was an instance where the mortgage lender asked for a letter from the mortgage borrower, which indicated that they had a longterm working relationship and also stated the amount of money paid to the borrower. Several other reasons lead one to apply for a VA loan, such as when two spouses want to separate. As a borrower, one must show a proof list of enlistment beyond one year and re-enlistment. A letter from the commanding officer and the alive and well certificate is also necessary.

Buying a house is the most common reason why one gets a VA loan. However, it is important to know that such loans restrict the property one is buying. That is, a VA loan cannot be applied on vacation or commercial property. The house must be a residential one. Veterans should also be aware that only VA-approved condominiums qualify for such types of loans. Thus when looking for a house in a condominium, they should also check the VA condo database to know if they are still on the right track.

During closing, one seeking a VA loan must complete the VAs minimum occupancy requirement, which is a document indicating that one is willing to occupy the home.

appraisal is an impartial valuation of a home by a certified real estate appraiser. It is usually among the last steps in completing the purchase of a home. Appraisals are mostly ordered by the mortgage lender to ensure that they are not lending more money than the value of the home. An appraisal also assures the buyer that they are not paying more than the home is worth. A home appraisal should not be confused with a home inspection. While home appraisals are usually to determine the market value of a home, home inspections, on the other hand, are to ascertain the condition and safety of the home. The appraisal can only be done once the home has been inspected.

The cost of a home appraisal ranges from $300 to $400 though this may vary due to a myriad of factors. On the day of the appraisal, the buyer typically is not present. The seller might be present but is more often than not represented

by their real estate agent. In fact, the only reason the agent is present is to answer questions the appraiser may have.

A home appraiser usually has to prepare a Uniform Residential Appraisal Report. This is a detailed report on virtually everything in and around the home. The report covers things such as measurements, pictures, the condition of the home, and comparable house sales to determine the value of the home. Measurements are not only physical in terms of distance but also determining the age of the home. Comparable sales are usually sales of houses within a short radius of the location of the home. The appraiser will use real estate software to see other sales. Features such as the location of the house, the number of bedrooms, heating and cooling systems, etc are also noted by the appraiser and included in the appraisal report.

One would hope that the appraisal report simply validates the predetermined value of the house and that the house inspection did not miss any crucial information that would significantly alter the home’s valuation. This outcome is usually pretty straightforward and one can go ahead and complete the purchase of the home.

Another outcome can be that the appraisal report determines the home to be worth more than the agreed upon price. Such an outcome is advantageous to the buyer as the house already has some equity from the start or has somehow appreciated in value. Finally, the appraisal report

may state that the home is overvalued. This is usually a complicated outcome as events can take one of many twists and turns. Firstly, the homeowner can ask for a review of the appraisal or even a whole new appraisal. The buyer can, however, use the lower value in the appraisal report to negotiate for a lower price. Finally, the buyer can simply choose to walk away and discontinue the purchase of the home.

The short answer is that there is not a fixed amount of time a home appraisal can take. There are various factors that may influence the length of time the process takes. That being

said, the on-site appraisal process averages between one hour to three hours, give or take. However, compiling the report and delivering it may be another week or two. Human factors such as an appraiser’s workload may also lengthen the time it takes to prepare and deliver the appraisal. The size of the house and compound may also play a factor as there could be more or less data to organize depending on the size of the home.

One can always keep tabs on the process by contacting the entity that ordered the appraisal. While this may keep one updated, contacting the appraiser may not necessarily shorten the wait period.

We’re Starting Over, Inc. a 501(c)(3) organization dedicated to supporting and uplifting people experiencing the effects of mass incarceration, systemic racism, housing insecurity, substance addiction, and mental health issues. We believe that people impacted by these issues are the ones closest to the solutions, which is why we are a Black led and criminal justice impacted organization engaged in this work. From experience, we’ve learned that housing is critical, but alone, it is not enough to support those exiting prisons or the streets. We not only provide transitional housing, but also include holistic services such as peer support, case management, employment, wellness, and re entry services. We also work to address the root causes of our houseguests’ difficult situations, leading grassroots organizing and policy initiatives in the Inland Empire region and statewide. Established in 2009, we’ve served over 1,400 men, women, and families in Riverside and Los Angeles Counties through the re entry and transition process.

We believe that the past does not define our future. We’re invested in creating safe and equitable opportunities for all members of our community, and especially those with past convictions. Housing opportunities are crucial for our community members and directly affect their ability to thrive.

Starting Over, Inc. is committed to reducing and eliminating the many barriers to life after incarceration. We have a deep commitment to identifying and implementing evidence based approaches to strong communities and families. We seek to creating program/project solutions where the need exists in our community. We do lots of things at Starting Over, Inc. but our primary goal is to address the immediate effects and root causes of incarceration, be it through housing, employment, legislation, or community organizing.

T t i l d ith i itiatives, access our services, or support our work through donations, you can or office@startingoverinc.org.

We currently operate eight homes in LA and Riverside Counties open to men, women, and children, with options for sober living or harm reduction housing All of our services are available to our houseguests, many of whom have been unable to obtain housing after being released due to their conviction histories

Our Case Management specialists provide support to our guests with obtaining necessary documents/identification and accessing insurance, education, healthcare, clothing, food, & more.

Our houseguests are not alone our support specialists, having experienced incarceration, addiction, and homelessness themselves understand our guests' needs and the barriers they face. We’re here to meet our guests wherever they are in their journeys and to support them moving forward through empowerment, support with recovery, referrals, and mentorship

Mass incarceration affects not just individuals, but families many of our community members and guests experience family separation at the hands of the child welfare system. The FREE Project is system impacted led and organizes parents and family members in a non judgemental space, advising on best practices and dependency court procedures We recently sponsored and passed statewide bill that eliminates major barriers to child placement and allows family members with criminal convictions unrelated to caring for children to be considered as placement options allowing for suitable family members with criminal convictions to step up in times of crisis

Through our Path to SEED program, we connect guests and community members with employment opportunities and provide training & support regarding obtaining and retaining employment, often a major hurdle for formerly incarcerated individuals

Our free clinics provide relief for expungements, wills/trusts, immigration, and more with the support of local legal organizations

In the past year, we’ve co sponsored and/or supported nearly a dozen statewide bills to reduce the scale of mass incarceration and its collateral consequences We’ve also worked locally to influence Riverside County to reduce criminal history look back periods from 7 years to 3 years in 2017 and to enable youth coming out of probation to be able to stay with their family members in subsidized housing

Our Participatory Defense organizing model (based on Silicon Valley De Bug) empowers family and community members in the courtroom to positively impact their loved one’s outcome and to bring them home. As fiscal sponsor and start up organization of Riverside All of Us or None (a chapter of a national initiative of formerly incarcerated people, family members, and allies advocating for the rights of the currently and formerly incarcerated people) we ensure that system impacted leadership remains at the center of the fight to keep our community together and address the social problems that incarceration purports to solve Our community outreach team also disseminates voter registration and public health information regarding COVID 19, and we organize food and clothing relief for community members in need.

The world has barely come out of the COVID pandemic and now the war in Ukraine is threatening to grow into a larger conflict that may see NATO get involved as well. Unfortunately, such events whether happening in Florida or thousands of miles on the other side of the globe still affect the housing market in Florida as well as other things. Predictions are made to inform decisions, especially huge investment decisions such as pertaining to the housing market. Hard as it may be to make predictions in such a volatile world, there are still a few things that may be worth considering in regards to the housing market, specifically, in Florida for 2023.

Florida home prices are tipped to go up 29.8%. Florida tops a list of states predicted to have increased home prices beating Arizona, North Carolina, Montana, and Tennessee to close out the top five. CoreLogic, Fannie Mae, Freddie Mac, and Zillow all predict that prices will rise slightly. This is mainly due to high demand with few houses available to meet this demand.

For the remainder of 2022, Zillow predicts prices will largely remain the same, rising in 2023 but may fall once the demand for houses is met. Whether this will happen remains to be seen. Furthermore, contrary

to the prediction of prices going up in 2023, some camps think that demand will go down and bring down housing prices with it. The fall in demand may be driven by rising mortgage rates.

Demand for housing in Florida is expected to keep rising in 2023. For example, in Tampa, the population is growing by 1.26% annually which may outpace supply. Furthermore, there is a lot of immigration into Florida from other states that will further drive up demand. Supply has been impacted in recent years due to the COVID pandemic and may not improve much with the looming global conflict as a result of the Russia-Ukraine War.

Seeing that prices will either continue to rise or remain high, it may be more economically sound to rent than to buy a home. As such, the rental market in Florida will continue to thrive, especially seeing that Florida expects more and more immigrants due to the low cost of living, job opportunities among other factors.

5. AIRBNB DEMAND WILL REMAIN HIGH Florida attracts a lot of tourists. With COVID and travel restrictions lifted, Florida can expect to see pre-pandemic tourist numbers. Consequently, demand for Airbnbs is set to remain high or even go up. This forms an interesting opportunity to invest.

It is expected that with the adoption of working remotely, more and more people will move away from Florida’s major cities into less populated areas with a slow-paced lifestyle. Florida’s west coast areas may benefit from this increase in population and demand for housing.

Tampa will see the highest year-on-year housing price increase. Orlando expected to maintain its trend as the most improved housing market in Florida. Where prices may go down, The Villages and Punta Gorda are likely to see the lowest decrease.

By Yvonne McFadden

By Yvonne McFadden

If you are already thinking of moving to Arizona, you probably already know about the state’s great weather, breathtaking landscapes such as The Grand Canyon, thriving economy, and relatively low cost of living. If you did not know all this, well, now you know. You can thank me later. That being said, purchasing a home can be a daunting task regardless of the state. Worry, not! I’ve got you covered. Here are 10 things you need to know before buying a home in Arizona:

Arizona has a lot to offer and there’s almost certainly something for everyone. Phoenix, the Valley of the Sun, is doubtless one of the first cities that come to mind. The city blends a vibrant city life with lots of escapes away from the hustle and bustle of the city. Scottsdale makes a case for itself by being America’s “most livable city.” Why? Just like Phoenix, it offers a balance between city life and activity with hiking trails and golf courses. Other places for one’s consideration include Tempe, Mesa, Gilbert, Tucson, and Flagstaff.

Every state has homebuyer assistance programs and Arizona is no different. As such, you should do some research on what programs are available to ensure you get all the help you can. Mortgages for first-time home buyers can be FHA, VA, or a USDA loan. A few programs in Arizona include Home Plus, Home in Five Advantage, Tucson Pima County Home Down Payment Assistance Program among others.

The importance of a good credit score cannot be overstated. This can be helpful while applying for a mortgage. A credit score of 620 and above is recommended. Anything lower than this may leave creditors with no choice but to deny you or charge a higher interest rate, both of which are not desirable outcomes.

Even when purchasing a home using a loan, one still needs to make a down payment. This is an upfront payment made toward

buying the home that is a percentage of the purchase price. There are down payment assistance programs one can take advantage of. Conversely, one can save up for one’s down payment. A down payment of at least 3% to 5% is common. However, this percentage does rise to around 20% to avoid paying private mortgage insurance.

Arizona is a competitive real estate market. Therefore, one needs every competitive edge one can get to improve their odds of owning a home with relative ease. In fact, in certain areas, you’ll need a pre-approval letter before you can start being shown houses. A mortgage pre-approval is an estimate of how much a lender can lend you based on factors such as your credit score and other financial metrics.

Imagine taking a trip to an exotic land but not using a tour guide to show you all the points of interest, hidden gems, and even areas to avoid. Your trip would be lackluster at best and most likely terrible. This analogy translates perfectly to home-buying. A real estate agent is your tour guide and in this case, Arizona is the exotic land. What you need is a seasoned agent to provide priceless advice and guidance on your homeownership journey. Real estate agents are obviously well informed on all the nuances of their real estate market, nuances very few people outside real estate agents are privy to. You would be wise to reach out to a real estate agent to be your guide on your road to homeownership.

Each state has its own popular home features. Such features are informed by factors such as weather and culture. In Arizona, pools are a surprising staple in a lot of homes. In fact, Arizona has the most swimming pools per capita in America. While swimming pools may be considered a luxury and not a necessity, air conditioning is definitely a must-have, especially in central and southern Arizona as temperatures can be quite high at times. Fire protection is another recommended feature to

look for when purchasing a home in Arizona. With high temperatures, one should consider fire protection measures, especially if the home is located close to a forest.

Apart from credit score, you should make sure you are financially sound across various metrics. For example, your debt to income (DTI) ratio should be healthy, so to speak. DTI is the ratio of your total debt to total income. Lenders prefer a DTI of less than 36% and are unlikely to approve your mortgage if your DTI is over 43%. That being said, other factors may play a role in determining what DTI ratio is “healthy” for different people.

When most people think of buying a home, raising the down payment and qualifying for a mortgage are usually top-of-mind. However, there are other costs associated with purchasing a home that may catch some people by surprise, especially first-time buyers. Closing costs in Arizona average between 1.05% and 1.4% of the home’s value and include costs such as mortgage origination fee, home appraisal fee, property taxes, home inspection fee, homeowners insurance, credit report fee, and realtor fee. To avoid unpleasant surprises, you should ensure you are familiar with all the costs associated with buying a home.

With the help of your real estate agent, it is now time to take a major leap and show your intent of buying a home. Making an offer is not always a straightforward process as some paperwork is involved as well as determining what a good offer is. The latter is crucial in ensuring that the seller takes your offer seriously and responds favorably to you. Once a favorable response comes your way, or even better, the seller accepts your offer, then it is just a matter of time before your purchase is complete.

By Tamra Lee Ulmer

By Tamra Lee Ulmer

One of the most googled recent phrases regarding either moving to or from Arizona is “moving costs from California to Arizona.” This, perhaps, is a testament to the growing appeal of living in Arizona. As such, as an Arizona resident and more so a real estate agent in the state, I will be sharing some insight on what it takes to move to the Grand Canyon State as well as moving costs out of the state. Firstly, why would anyone want to move to

Arizona? Well, the state has a relatively low cost of living and a booming economy. Taxes are relatively low. The cost of buying a home is also comparably low. By extension, rent is more affordable as well. Being the Grand Canyon State, Arizona is also known for having a variety of outdoor activities. The weather is also great. Urban centers are less congested compared to some of the other “popular” states.

That being said, one may also want to leave Arizona. While the assumption is one would only leave for unavoidable reasons like getting a job in another state, for example, the state also has a few disadvantages. One is that the summers are really hot and most of the disadvantages of living in Arizona seem to be related to the state’s high temperatures. Desert animals such as scorpions and rattlesnakes are native to the state. Water is limited making it difficult to pick up hobbies such as gardening.

So whether you are moving into or out of the state, there are a few things you need to consider as regards moving costs

Using a moving company is a convenient way to move from one place to another. However, it can also be expensive. According to movebuddha.com, based on a move size of a studio or one-bedroom apartment, using a moving company would set you back $1,174 to $3,213. This cost goes up as the move size increases. However, you can also use a moving container which brings down the cost to $1,026 to $2,039. Getting a rental truck and doing the move yourself further brings down the moving cost to between $846 and $1,197. This is based on the moving size of a studio or one-bedroom apartment and also based on moving from California to Arizona.

In Arizona, the summer serves as an offpeak season. Why? The high temperatures. Arizona summers can get so hot to a point of slowing down most activities. To counteract this, a lot of businesses offer discounts on their goods and services during the summer months. Therefore, if you can, try and move to Arizona during the summer, not only to get discounted moving rates but to also see the state at its presumably worst when it’s really hot. It can only get better.

When one moves to Arizona from another state, one has to replace one’s driving license with an Arizona driver’s license. The fee is however small with prices ranging from $10$25 depending on one’s age.

16-39:

40-44:

45-49:

50 and older:

Most moving companies come with free coverage for your stuff. The insurance comes into effect once you sign your bill of lading document which is a detailed list of all the stuff you are moving. However, this insurance offers coverage of only 60 cents per pound per item. In the event of damages, the insurance would hardly cover the cost of the damaged stuff. As such, it is advisable to have full value protection insurance so that your stuff is fully covered. This covers the cost of replacing everything on your bill of lading and usually costs about 1% of the total value of your stuff.

While we are looking at moving costs into or out of Arizona, it is interesting to note that you may also be charged for not moving. Moving companies each have their own cancellation policy. It is prudent to familiarize oneself with a moving company’s cancellation policy in the event one has to cancel one’s move.

Another similar cost is storage fees or delayed delivery fees. If your move is delayed for one reason or another, the moving company may have to store your belongings in a warehouse and thus charge storage fees.

By Walter Huff

By Walter Huff

The supply and demand dynamics have been out of sync for a while now, and with the supply being so small and the demand being great, the housing market for the past year has been very competitive. Price appreciation has gone through the roof, and multiple offers are made on the same property. In a market this competitive, it is easy to get outpriced. It is, therefore, crucial when making an offer that will topple the competition. One that will not offend the buyers and one that will not have you overpay on purchasing the home. It’s all about finding the right balance. That is easier said than done, so here’s a small useful for both the pandemic and post-pandemic guide to help you determine what to pay.

A real estate market is either a seller’s or buyer’s market. There is a slight chance of a balanced market, but most times, the market is either a seller’s or buyer’s market. In a buyer’s market, the inventory supply is greater than the demand. In this kind of market, the homebuyer has some negotiating power, seeing that people aren’t exactly lining up to buy the home. The home seller would be willing to accept a below-list price offer. Remember, the offer should be so low that the seller disregards you altogether.

In a seller’s market, the tables are turned. The seller has the power, so it is unlikely that the seller will go below the asking price. The market will be very competitive, with multiple

offers on a home, so go in gun blazing and offer the best offer. In this market, it is easy to get carried away in the bidding wars and end up overpaying on a property. Remain grounded; to do so, have a budget that dictates how much more you are willing to pay for a home. Agreed, a home may be perfect in your eyes, but with the closing costs and other unexpected fees, is the house really worth it?

It is a treat to work with a motivated buyer. To find one shouldn’t be difficult; this information is available on most real estate listings, and if not, your real estate agent should be able to find this information for you. The longer the time a house has spent on the market, the more negotiating power you have. The duration makes the seller motivated, and they would be open to a lower offer.

Conversely, don’t go making lowball offers to properties that have barely stayed on the market. These sellers are very unwilling to compromise on the price. If you are going to make an offer on such a property, offer the list price or over the list price-with limit, of course. Factor in your monthly mortgage payments and all other expenses; can you afford it?

If you have reviewed the market and the length of time homes are spending on the market, the next step will be to conduct a comparable analysis (comps) or a comparative market analysis (CMA). Your focus should be on homes sold within three months, within a half-mile and one-mile radius, and with the same square footage as your prospective home. You will carefully go through the list price and sale prices of these homes. With this information, you will be able to make a great offer and get your home at a fair price without overpaying!

The common denominator in all these factors is affordability. To know how much to offer on a home, you must know how much you can afford. That will save you and your realtor valuable time. Finding a suitable home needs work, so don’t be afraid to go looking for that motivated seller, don’t be lazy, analyze the market and finally do a comparative analysis. A limit is essential; you want to buy a home that you can afford in every regard. Therefore, have an informed price cut above which you can’t go beyond. All these tasks may seem tedious, but it should be a breeze with the right real estate agent.

PHOTOS FROM 123RF

PHOTOS FROM 123RF

This year hasn’t been the best for many people and while it cannot be compared to the past two years, we seem to be going into the thick of things especially after the fact that inflation rates are sky-high. Many people aren’t buying and for the past two years, fall has now become the favorite home shopping month, but I doubt there will be much activity this year following the rising cost of EVERYTHING. We are accustomed to dramatic increases in home prices and that’s nothing new especially in the west and east coasts. What I am really interested in is the cost of renovation. For those looking to renovate this fall to maximize their returns, Here are some tips for you; .

Set a budget and follow it purposefully. You may have a budget in mind, but sometimes you can’t afford that. If that’s the case, plan your renovation within your budget. When you work within your budget, you can ensure you will complete the renovation in no time without the need to overspend.

When your time is up for the work, then you need to consider if you’re going to recoup the money spent on the renovation. Most people do not consider this. While you need to spend the right amount of money, you also need to spend it in the right way. This is true for both construction materials and building tools. Make sure you invest in quality as you are not only about to invest in your home but also in yourself. This brings us to the issue of value. Most people don’t invest in quality as they are more concerned about what their house looks like than its longevity.

PHOTOS

A kitchen is the heart of your home, where family and friends gather. Investing in a new kitchen gives you the opportunity to add your personal touch. There are countless ways you can make your kitchen to your taste. You can opt for a luxury benchtop or marble top, remove cupboard doors and replace them with glass or white frames. If you don’t like the current layout of your kitchen, then do some demolition and create a layout of your dreams. You can install a granite countertop, introduce more cupboards to increase your storage space, and get an electric cooker. A well-designed kitchen is easy on the pocket and it doesn’t need to be a costly renovation. You can start by replacing old lights with energy-saving lights if you want to make your kitchen look more modern. The ROI for this is about 54%

Home remodeling projects like bathroom renovations have a big impact on your home’s value. Maybe you’re going to increase the size of your space to give it an updated look, and with the right design and selection of materials, it can mean big profits. The ROI for this is about 70%

Remodeling your basement is a must, especially

if you’re a homeowner that has a basement. If you don’t have one, that could be a huge mistake, as it makes the most sense to have a basement. A basement will give you room to store all of your items in one area. So if you have been considering a basement remodeling project, now is the time to consider it.

This is one of the most important rooms in a house as this is where most of the activities and entertaining take place. You may want to renovate your living room to improve its look so that you can welcome your guests into it. Some of the things you need to think about are the window blinds, ceiling fans, and especially the rug that you are going to buy for the room. You need to buy it in a fashion that is going to add to the charm of the room. The rug is going to define the look of your living room. Also, the chairs and walls are not to be left out. The ROI for this is around 61% to 72%.

Renovating your home can be the best thing you will ever do to your home. When you renovate your home, not only are you making it more attractive, but you can also get the maximum value for the house.

No one likes to be told “no.” Rejection hurts. And having your application for a loan declined is particularly devastating, because it throws your entire dream of homeownership into doubt. Still, just because one lender rejects your loan application doesn’t mean you’ll never be able to buy a home. So, if you didn’t get approved for a loan, it’s recommended that you talk to your realtor. Realtors can help you in ways you can’t imagine.

There are numerous apparent reasons why one may not get approved for a mortgage. Some of them include: low credit scores, high debt-toincome ratio, insufficient down payment, and a recent change in one’s financial situation such as loss of job.

Remember, when you get denied a loan due to low credit scores, it doesn’t certainly mean you have low credit reports. Sometimes there may be errors in your credit reports that led to a low credit score. A 2013 federal Trade Commission survey revealed that one in four Americans said that they spotted errors on their credit reports.

A realtor can help you to easily identify any errors on your credit reports. In case of any errors on your credit reports, it would take about 30 days or more to get them removed. However, there’s a way around this. If you let your lender take care of the legwork, it would take fewer days to get the error removed. And since realtors are very conversant on such issues, they can connect you with good lenders who can take over the process for you.

“Lenders are able to do what’s known as a rapid rescore, which can get errors removed within five to seven business days,” says Richard Redmond, mortgage broker at All California Mortgage in Larkspur and author of ‘Mortgages: The Insider’s Guide.’

When you get denied a loan because of your debt-to-income ratio, do not give up. That just means that your income from your incomegenerating streams isn’t high enough to settle your debts. However, you should remember that the debt-to-income ratio varies across different lenders.

“It’s very common to be turned down by one lender and then be able to get approved by several others,” says Redmond. “Different lenders have different debt-to-income requirements.”

This means that you can try another lender. But you can take your chances and approach any lender. To avoid wasting more time, this is where you need your realtor. Realtors are conversant with these lenders and they know their terms and conditions to go get approved for a mortgage. Therefore, a realtor is your best chance of getting to a lender who will accept your debt-to-income ratio.

When you don’t get preapproved for a loan for various reasons, do not give up since that’s not the end of it. Consult your realtor and they may know a thing or two on how to get around it.