4 minute read

Investing in times of global uncertainties

BY OLAF VAN DEN HEUVEL, CHIEF INVESTMENT OFFICER AT AEGON ASSET MANAGEMENT NL

The global economy has shifted into a lower gear in the past few quarters. Following a period of a strong and broad-based economic momentum, soft spots in the economy emerged in the second half of 2018 and continued into 2019. Growth decelerated across the board, with more pronounced weakness among countries and sectors where trade and manufacturing play an important role. The slower growth fits into a dynamic of high policy and political uncertainty, which weighs on global investment and confidence. Slower growth is also caused by ongoing trade tensions.

Advertisement

Not even a year ago, central banks around the world were tightening monetary policy. Most importantly, the Federal Reserve increased policy rates several times on the back of a solid economic paradigm in the United States, and it was expected that the tightening cycle would continue. Only months later – after several economic indicators disappointed and risk assets sold off in the final months of 2018 – central banks reversed course and started to ease policy to support the economy. Other good examples of the quickly changing conditions are the trade tensions and the Brexit process.

The Brexit path was rife with uncertainty and the political stance has fluctuated between a deal and a no-deal Brexit before eventually further extensions were agreed upon. Simultaneously, the sentiment of the trade talks between the US and China oscillated from friendly to hostile and back on numerous occasions. Meanwhile tariffs have been increased substantially and the overall impact of the ongoing uncertainty had a negative impact on the economic momentum over the course of this year.

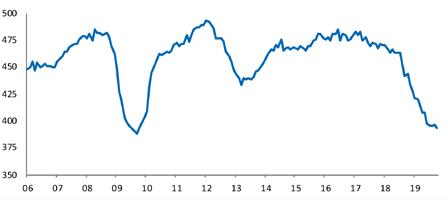

Global growth decelerated, with specific weak spots. The economic cooling in Germany is a telling example for the global economic activity. This is illustrated by two charts. Figure 1 shows the softening of the manufacturing PMI, indicating that the industrial sector is in a soft patch globally. Even though the services sector is more important for most developed countries, the weakening of the manufacturing sector did have an impact on the broader economy. In Germany, where the (automobiles) manufacturing sector is an important driver of the economy, the weakness was visible. Growth in the largest eurozone economy has declined to around 0%.

Figure 1: Global Manufacturing PMIs Two scenarios to identify attractive and robust assets

We argue that the path of the economy in the coming period remains dependent on the outcome of the highly uncertain binary events. As these fluid events might have a major impact on the economy, we decided to construct two scenarios – rather than one basis scenario – to account for the highly uncertain environment.

In our positive scenario, growth in the coming years remains close to the current level. This scenario is likely to materialize if the trade dispute is resolved, and if the recent weakness in the manufacturing sector does not persist. In the absence of adverse shocks, the cycle can continue in the coming years. Still, we foresee slower growth in comparison to previous years as capacity constraints in pockets of the economy have intensified. In this positive scenario we expect global monetary policy to remain accommodative – possibly in combination with a fiscal

impulse – to support growth in the near term. In this scenario fixed income investments have relatively low expected returns, with somewhat higher returns for higher risk categories within the fixed income space. Our return outlook for equities in the positive scenario is in the mid-single digits spectrum, roughly in line with historical averages.

In our negative scenario, we account for a growth slowdown in the near future. The loss of economic momentum could be driven by various factors, of which a further escalation of the trade dispute is among the most likely and impactful. The adverse effects of continuous trade uncertainty could disturb the economy via various channels, the confidence and investment channels in particular. Given the nature of these possible headwinds, we expect open economies to face more adverse effects in the near future.

Other factors that have the potential for the negative scenario to materialize, are related to Brexit, as well as a broadening of the manufacturing weakness, spilling over into the wider economy. In this scenario we expect labor market weakness, ending the strong employment trend that pushed the unemployment to current lows. We foresee a quick reaction from central banks, easing conditions further – where mainly the Federal Reserve is

Photo: Archive Aegon Asset Management

well positioned to counter the slowdown. This results in relatively low returns for most fixed income assets. The economic slowdown results in a revaluation of higher risk assets, causing negative returns for most equity categories.

Multi Asset Perspective: diversification, high yield and alternative fixed income categories

Given the two scenarios presented, we prefer assets that have the potential to do reasonably well in both a positive- and negative economic situation. We continue to believe that alternative fixed income categories remain

OLAF VAN DEN HEUVEL

attractive building blocks for investment portfolios. Specifically, our outlook on alternative fixed income assets, such as Dutch mortgages and European Asset Backed Securities remains positive. Also, high yield corporate bonds appear relatively attractive. This year’s analysis reveals that these asset classes are attractive on a risk adjusted basis, taking into account both our macroeconomic scenarios. Finally – as always – we emphasize the merits of well diversified portfolios. Actively managed and broadly diversified portfolios should be well positioned to navigate the likely volatile financial markets in the coming period. «

Figure 2: German car production

Disclaimer: The information in this article is for information purposes only and cannot be considered as personal advice. The value of your investment may fluctuate. Past performance is no guarantee of future results.