THE ONLY FULL - SPECTRUM FINTECH MAR K ETPLACE BAN K Scott Sanborn , CEO of LendingClub discusses all... MASRIA DIGTIAL PAYMENTS: Comprehensive, streamlined payment solutions TECHNOLOGY: Route to IPO PERMANENT TSB: Irish market leading provider of retail and SME banking FINTECH FOUNDERS PEPPER MONEY ANZ: Australia's number one alternative lender BANKING: Attracting private equity investment FINSERV: Customer retention and loyalty finance programme October 2022 | fintechmagazine.com

Get tickets Sponsor opportunities SHAPING THE FUTURE OF BANKING, FINANCIAL SERVICES & PAYMENTS A BizClik Event: 3,000+ Participants 2 Days 2 Stages 70+ Speakers

Watch our 2021 Showreel

Join us at FinTech LIVE London

presentations, Q&A sessions to 1-2-1 networking, the 2-day hybrid show is an essential deep dive into issues impacting the future of each industry today.

Global giants and innovative startups will all find the perfect platform with direct access to an engaged and active audience. You can’t afford to miss this opportunity.

See

Sponsor opportunities

you on: 1st-2nd November 2022

EDITOR-IN-CHIEF JOANNA ENGLAND

EDITOR

ALEX CLERE

CHIEF CONTENT OFFICER

SCOTT BIRCH

PRODUCTION DIRECTORS GEORGIA ALLEN DANIELA KIANICKOVÁ

PRODUCTION MANAGERS

JANE ARNETA MARIA GONZALEZ CHARLIE KING

Never miss an issue! + Discover the latest news and insights about Global FinTech...

JOIN THE COMMUNITY

The FinTech Team

CREATIVE TEAM

OSCAR HATHAWAY SOPHIE-ANN PINNELL HECTOR PENROSE SAM HUBBARD

MIMI GUNN JUSTIN SMITH REBEKAH BIRLESON JORDAN WOOD DANILO CARDOSO CALLUM HOOD

CHIEF DESIGN OFFICER MATT JOHNSON

MARKETING MANAGER EVELYN HOWAT VIDEO PRODUCTION MANAGER KIERAN WAITE

DIGITAL VIDEO PRODUCERS MARTA EUGENIO ERNEST DE NEVE THOMAS EASTERFORD DREW HARDMAN|

JINGXI WANG JOSEPH HANNA

MEDIA SALES DIRECTOR BEN MALTBY

PROJECT DIRECTORS

JAKE MEGEARY MICHAEL BANYARD

JOE PALLISER

MANAGING DIRECTOR LEWIS VAUGHAN

CHIEF OPERATING OFFICER STACY NORMAN

CEO GLEN WHITE

THE ROUTE TO IPO IS PAVED WITH GOOD INTENTIONS

As we speed into Q4, it's easy to look back and only see the negatives. Fintech has had a tough ride. Investment is down. BNPL frontrunners have seen their valuations crash, and companies we expected to IPO themselves into the business history books, have stalled, bucked and shied away at the final hurdle.

It’s hardly surprising, though. Following a period of unnaturally fast expansion, the growing pains have finally caught up with them. The past almost three years has seen the world placed in highly unnatural circumstances that have led to giant changes. Now, the giddy ride is over and, as we return to normality, a sense of reality must prevail.

Innovation requires regulation. Booms inevitably – indeed, always – lead to a bust. And new markets must go through a period of painful maturation before they can safely say they’ve ‘made it’.

But, despite the challenges, all the signs are good; hard times breed resilience and stability in the long term.

These subjects and more are the focus of this month’s issue – and we have some fantastic insights for you to digest.

So, sit back, enjoy the magazine, and let us know your thoughts.

JOANNA ENGLAND joanna.england@bizclikmedia.com

“The giddy ride is over and, as we return to normality, a sense of reality must prevail”

fintechmagazine.com 5

© 2022 | ALL RIGHTS RESERVED FOREWORD

FINTECH MAGAZINE IS PUBLISHED BY

Our Regular Upfront Section: 12 Big Picture 14 The Brief 16 Timeline: How the cybersecurity industry began 18 Trailblazer: David Vélez 20 Five Minutes With: Kim Van Esbroeck LendingClub A transformative year: LendingClub’s digital marketplace bank 26 Banking Attracting private equity investment Vodafone Fiji Cultivating connections and enhancing underprivileged lives 50 58 CONTENTS

Financial Services Customer retention and loyalty programme finance Masria Digital Payments Enabling businesses to roll out their financial solutions Pepper Money ANZ How low-code composition has transformed lender Pepper Money 74 126 104 Permanent TSB Enjoying fruits of strategic supplier management Technology Route to IPO Top 10 Fintech founders 82 96 118 140 TOP 10 Payment Solutions Inflation bites: Consumer finance trends

From Open Banking to Open Finance for SMEs

Digital disruption in financial services is already a reality for retail customers but it hadn’t happened yet for SMEs and entrepreneurs, who were still seeing their needs and demands pretty much uncovered. SMEs across the globe are seeking beyondbanking ecosystems, integrating third-party services, that cover their needs in a single, easy-to-use service, allowing them to focus on their core activities.

Simplifying processes to achieve outstanding KPIs

With this landscape in mind, STEP, a global marketplace for financial products for SMEs with the mission of delivering a fullyfledged Customer-Centric digital solution, used CRIF Group’s solutions, among which Strands’ BFM and Engager, enriched by CRIF account aggregation, in order to deliver excellence in every product/service to SME and corporate customers.

Structuring a customized insight driven experience tailored to SMEs, using CRIF’s open banking capabilities and Strands’ advanced analytics, STEP was able to create a competitive advantage in a very simple way, by enabling:

• Account aggregation – first platform to offer it for free to SMEs on European scale

• Invoice reconciliation - retrieve invoices from third party providers such as Quickbooks and many others

• Strands BFM + Engager - for cash flow management and forecasting; business insights to trigger relevant information for a personalized experience.

• Third party products - integrated that allow SMEs to apply for an instant loan, discount their invoices, manage their international payments and FX transactions, acquire payments from customers, ask for an ESG rating, subsidized finance, insurances among others

The solution provided by Strands and CRIF has enabled STEP to achieve unbelievable results since its market launch in October 2021 with more than 4,000 SMEs having chosen the STEP platform in two countries (Italy and Spain) in order to always keep their financial position under control and seek for an innovative fully-fledged financial solution. This customer loyalty has led to a 22,6% cross selling ratio and a pipeline of more than 450 million euros loan and working capital operations already requested.

CRIF is a global company specializing in credit & business information systems, analytics, outsourcing and processing services, as well as advanced digital solutions for business development and open banking.

CRIF is currently the leading credit information banking group in continental Europe and a major player in the global market for integrated business & commercial information and credit & marketing management services. Through continuous innovation, the use of state-of-the-art technology and a strong information management culture, CRIF supports 10,500 banks and financial institutions, more than 600 insurance companies, 82,000 business clients and 1,000,000 consumers in more than 50 countries of 4 continents. For more information: www.crif.com

BIG PICTURE

10 October 2022

Soaring costs lead to anger and anguish Colombo, Sri Lanka

Rising food and fuel prices and spiralling inflation have prompted a ‘summer of discontent’. Anti-government protests have been seen in Ecuador, Panama and Sri Lanka (pictured). In the latter, protestors stormed the President’s House in Colombo and forced him to flee. In South Africa, thousands of people took part in rallies to decry rising fuel prices, high inflation and rampant unemployment. In the UK, rail workers, bus drivers and criminal barristers all walked out over pay and conditions. Fintech has already felt the pinch, but further inflation and a potential recession could plunge the sector into deeper financial trouble.

© Antan O/CC BY-SA 4.0

THE BRIEF

“PEOPLE ARE LOOKING FOR PAYMENT METHODS THAT OFFER THEM FINANCIAL FLEXIBILITY AND ALLOW THEM TO UTILISE THEIR PURCHASING POWER ON THEIR TERMS”

Keith SERDON

Chief Commercial Officer, Mollie

READ MORE

READ MORE

“IT IS SO IMPORTANT RIGHT NOW TO REFRAIN FROM MAKING ANY RASH DECISIONS THAT COULD LATER DAMAGE A PERSON'S FINANCIAL SECURITY”

Andrew MEGSON Executive Chairman, My Pension Expert

READ MORE

Saudi BNPL fintech Tamara closes US$100mn Series B

Saudi buy-now-pay-later (BNPL) fintech Tamara has raised US$100mn in a Series B funding round led by Sanabil Investments.

The Riyadh-based fintech, which was launched in September 2020, allows customers to spread the cost of a purchase over several interest-free instalments. It is fully Shariyah compliant and has enjoyed early success, despite the broader troubles facing the global BNPL sector. Tamara has seen tenfold year-onyear revenue growth, onboarding more than 3 million customers and over 4,000 partner merchants including IKEA, Adidas, Namshi plus a number of local SMEs.

The latest round also includes participation from Coatue, Shorooq Partners, Endeavor Catalyst and a follow-on investment by Checkout.com. Tamara says it will use the funding to expand its product offering across payments and shopping; expand to new markets; and strengthen the existing customer and merchant experience. CEO Abdulmajeed Alsukhan claims Tamara can help its partners realise a 40% rise in average order value.

“ALL COMPANIES WITH A VISION TO BECOME PUBLIC SHOULD ACT LIKE A PUBLIC COMPANY LONG BEFORE THEY ARE ONE”

Romi SAVOVA CEO, PensionBee

12 October 2022

BY THE NUMBERS

36% No – losses too likely

25%

Maybe – I’ll watch the markets

39% Yes –crypto is always volatile

REMITLY TO ACQUIRE ISRAELI COUNTERPART REWIRE Remitly, which provides remittances and financial

ROBINHOOD LAYS OFF 23% OF ITS WORKFORCE

Robinhood CEO Vlad Tenev has said "this is on me", after it laid off almost a quarter of staff. The move reflects a fall in customers.

‘CRYPTO WINTER’ HAS EFFECT ON INVESTMENT FRAUD

A new report indicates that the 'crypto winter' has had a knock-on effect on fraud. Scams have fallen by 65% over the past year, according to TradingPlatforms.com.

JAR

The Indian fintech has hit a valuation of around US$300mn after its latest funding round. Jar raised more than US$20mn in its Series B round, with existing backer Tiger Global leading the investment.

DIGIT INSURANCE

Indian insurtech unicorn Digit Insurance has gone ahead and filed for its IPO, bucking a trend of delayed public listings. It is said to be seeking at least US$440mn, having last been valued at US$3.5bn.

ADYEN

Shares in Dutch fintech Adyen fell by 11% after it missed expectations for net revenue for the first half of the year. Operating expenses rose nearly 50%, driven partly by the addition of 400 new employees.

STRIPE

Investment fund T. Rowe Price has marked down the value of its stake in Stripe, signalling an end to the company's lofty valuation. The move could mean that Stripe is worth closer to US$75bn than US$95bn.

O O D T I M E S B A D T I M E S

OCT22

WE ASKED YOU: WOULD YOU CONSIDER INVESTING IN CRYPTO OVER THE NEXT FEW MONTHS OR HAS THE PROLONGED SLUMP PUT YOU OFF?

G

fintechmagazine.com 13

TIMELINE

1970 s

THE BEGINNING OF CONNECTIVITY AND VIRUSES

The Advanced Research Projects Agency Network (ARPANET) became the first connectivity network developed prior to the internet itself.

Engineer Bob Thomas created a program that could move between the Tenex terminals on ARPANET, called Creeper. The code printed the message, “I’M THE CREEPER: CATCH ME IF YOU CAN.” across the network. Not at all prophetic…

How cybersecurity industry began

1979

THE FIRST HACKER WAS A TEENAGER

Kevin Mitnick was just 16 years old when he hacked The Ark – a massive system that was used for developing operating systems. It was located at the Digital Equipment Corporation – a major American company in the computer industry from the 1960s to the 1990s.

Mitnick was arrested and jailed over the incident, becoming the first of numerous cyber attackers to infiltrate commerce over the coming decades.

THE CYBERSECURITY INDUSTRY AND HAS BECOME A CRITICAL BUSINESSES, WITH FINANCIAL INSTITUTIONS OF CYBER FORTIFICATION

THE EARLY 80 s

CYBER ATTACKS BECOME ‘A THING’

With the advent of cyber attacks present, the 80s signalled the start of numerous problems for computer networks. High-profile attacks taking place in this decade included AT&T, the Los Alamos National Laboratory, and National CSS.

In 1983, terms were coined to describe the attacks, including “computer virus” and “Trojan Horse”, the latter in reference to the Greek Trojan War.

How the cybersecurity industry began

INDUSTRY BEGAN FIVE DECADES AGO

CRITICAL COMPONENT OF ALL ONLINE INSTITUTIONS AT THE FOREFRONT FORTIFICATION

2000 AND BEYOND

CYBER WARS AND POLITICAL INFILTRATION

From the early noughties to today, there has been a steady increase in cybercrime and the threat it poses to economic stability. Ransomware and Malware are used by organised criminals to infiltrate and extort data and funds from even the best fortified entities.

The cybersecurity industry globally is now worth an estimated US$140bn. No business is beyond attack, as the SolarWinds breach of 2021 proves, along with thousands of other recent incidents. Cyber infiltration is now considered a form of warfare.

1988

WORMS ARE CREATED

According to some reports, Robert T. Morris – a student studying at Cornell University – wanted to determine the size of the internet as a whole.

To do it, he built the first worm, which was to move through the network and infect UNIX systems. But an error in the design of the program caused it to infect each machine, one after the other. This led to networks that were clogged with information, leading to massive system crashes.

1990 s

ILOVEYOU

By the 90s, the internet had become a global concern and the cybersecurity industry grew with it. The decade saw the creation of Polymorphic virus risks and the first antivirus program. The goal was to increase ways to protect against risks.

As one hacker group developed after another, companies faced a lot of challenges to improve security to minimise hacking. The 90s also saw malicious viruses launched on a mass scale, as ILOVEYOU and Melissa infected millions of computers by targeting Microsoft Outlook.

fintechmagazine.com 15

The Brazilian Banker Billionaire

Born in Medellin, Colombia in 1982, David Vélez comes from a large, extended family of entrepreneurs. His father, who co-owned a button factory, had 11 siblings, all of whom ran their own businesses, providing the young Vélez with an environment that thrived on innovation and disruptive ideas.

But Medellín was also a crime capital where drug wars and the cartels reigned supreme. The family suffered greatly, and an early memory for Vélez was leaving a shopping centre with his family just moments before it was bombed. Later, one of his uncles was kidnapped. The two events resulted in Vélez’s parents uprooting the family to find a safer place to live.

A passion for finance and innovation

At the age of nine, the family moved to Costa Rica, where he flourished, proving to be a fine student – and discovered a passion for the financial markets. Vélez attended a local German-language prep school, graduating as valedictorian and winning admission to Stanford University. By 18, Vélez had moved to the US and started his degree at Stanford, studying Finance. Upon graduation, with a newlyminted MBA, he qualified as a financial engineer.

The time he spent in California saw him explore a range of potential careers in the technology industry – and he considered various startup ideas, as well as positions in Google and Amazon.

As the CEO and Co-founder of Nubank – South America’s largest and most successful challenger – David Vélez has a disruptive reputation

TRAILBLAZER

16 October 2022

fintechmagazine.com 17

But in 2012, Vélez returned to South America and relocated to São Paulo. He had secured himself a much-soughtafter position as a partner at Sequoia Capital. Then, aged 30, Vélez was hired to establish the VC in the emerging market powerhouse of Brazil. The location was perfect: a young, tech-hungry population, plenty of natural resources and home to the world’s seventh-largest economy.

The project looked exciting and full of promise – but, before it had even got off the ground, it was dropped due to the shortage of computer science engineers graduating in Brazil.

The event was a great disappointment to Vélez, whose entrepreneurial background meant he’d always hankered after launching a dynamic startup. But investors had been discouraged by the sheer lack of on-the-ground innovators coming out of the Brazilian education system.

Plans to donate his personal US$6bn fortune to philanthropic causes

Describing that time in an interview with Forbes, he said: “It was the day before my birthday, and it was a bit of a shock.

“You want to position yourself on the side of the market where there’s scarcity. In the US, there’s an oversupply of good entrepreneurs. Somebody with my experience and background is a commodity. In Latin America, there was significant scarcity.”

Going after the big banks

Following the disappointment, Vélez set his sights on the establishment, which consisted of several, giant incumbent banks that dominated Brazil’s financial industry. The system needed reform – and fast. High fees, poor service offerings and an aversion to technology within the legacy banks meant opportunity was ripe for the picking.

According to reports, the vast majority of Brazilian banks were appallingly un-customerfriendly, charging annual fees for even basic credit cards. They also charged monthly fees for all services, ranging from fraud protection to text-message alerts. Data shows that, even in 2019, fees made up nearly 40% of Brazilian banks’ revenue, compared with 15-20% for banks in other leading South American countries.

TRAILBLAZER

18 October 2022

Challenging the narrative

It was a brave move in a culture where organised crime and brutal business practices often result in personal harm. Vélez risked stirring up a wasps’ nest – but was determined to see his ideas pave the way for a new style of banking to come to fruition.

Nubank was duly launched in 2013 –and has since survived and thrived its way through myriad disasters, including recession, corruption scandals and the pandemic. Warnings from friends that he was putting himself in danger went unheeded. He was told the incumbent banking fraternity would never allow him to succeed – or, possibly, even live… with Vélez divulging to Forbes that one friend told him, “They’re going to kill you, they’re going to kidnap your kids”.

Success for Nubank

Now one of the world’s most valuable decacorns, Nubank has climbed from success to success. Though less than a decade old, it already boasts over 35 million customers. Much of the success can also be attributed to fellow founders, Cristina Junqueira and Edward Wible, who shared Vélez’s passion for change.

Less than a decade after its founding, Nubank has 45 million customers and is valued at $45bn. It is also backed by some of the world’s biggest investors, including Founders Fund, Tiger Global and Sequoia.

A family man

As well as being a keen philanthropist, Vélez has four children with his wife, Maria, the last of whom was born earlier this year.

A recent Bloomberg report also confirmed that the couple have pledged to give the vast majority of their personal US$6bn fortune to philanthropic causes.

“You want to position yourself on the side of the market where there’s scarcity. In the US, there’s an oversupply of good entrepreneurs”

Kim Van Esbroeck

Country Head for Belgium, Aion Bank

“ I am proud of the tenacity and flexibility of my team”

FIVE MINUTES WITH... 20 October 2022 5

Esbroeck

Kim Van Esbroeck is responsible for growing Aion’s business through commercial activities and business development, directly managing Aion Bank’s Belgian sales and partnerships teams, as well as its flagship branch in Brussels

Q. DESCRIBE YOUR JOURNEY INTO FINTECH. HOW DID YOU GET HERE?

» My career started in the payments industry. I held several different positions from test engineer to head of card marketing at Integri and Clear2Pay, then, at Belgian payment leader Bancontact, I was Chief Operations Officer, then was promoted to Chief Commercial Officer before being named CEO in January 2017.

In 2020, I was looking for a new challenge, and Aion Bank was entering the Belgian market with an entirely new banking concept – fully end-to-end digital, powered by the latest in cloud technology. I was drawn to the company’s mission to offer a better way of banking to people, and its technology is at the forefront of the industry. Looking back, I really didn’t do any career planning, but I followed my gut, and, if a train passed that I found interesting, I jumped on it.

Q. WHO WAS YOUR CHILDHOOD HERO AND WHY?

» I was a big Madonna fan when I was a teenager. Obviously, she’s an iconic performer, but I loved her attitude. She was defiant to carve her own path, no matter

who challenged or disagreed with her. She created a new template for what a pop star could do and say. Looking back at her career, I understand now that, as a woman in the 80s, she needed to adopt an f* you attitude to the male-dominated industry in order to get her voice heard. She is a true power lady!

Q. WHAT WAS THE LAST BOOK YOU READ - AND HOW LONG AGO DID YOU READ IT?

» Becoming by Michelle Obama. It’s actually not the last one I’ve read, but it made an impression on several levels –including how, at the end of the day, your personal and professional selves are one and the same. You bring your personal self to your job everyday; it is a major building block of your professionalism, achievements and drive for results, often weighing more in the balance than all the qualifications you have accumulated.

Q. WHAT'S THE BEST PIECE OF ADVICE YOU’VE EVER RECEIVED?

» The most amazing things lie outside of your comfort zone, so force yourself at any moment to step out.

fintechmagazine.com 21

Q. NAME ONE PIECE OF TECHNOLOGY YOU COULDN’T LIVE WITHOUT AND TELL US WHY

» I love the park-assist functionality in my car. The camera and sensors that have spatial awareness sounds like a simple technology because we use it everyday, but, very soon, that same tech will advance, so our cars will be able to park themselves!

Q. AION BANK IS MOVING FROM STRENGTH TO STRENGTH – DID YOU EVER THINK YOUR PLANS WOULD TAKE YOU TO THIS POINT WHEN YOU FIRST STARTED OUT?

» Anyone who has worked at a start-up knows that where you start is almost never where you finish. When I joined Aion, we were just about to launch our marketing efforts for our retail banking business. The big challenge was building a new brand in the middle of a pandemic and lockdown. Across the past two years, our business has grown and evolved, but the core of what we want to achieve has not changed - we want to democratise better banking for people, making it more accessible and fully digital.

Q. IS THERE A PERSONAL ACHIEVEMENT FROM THE PAST 12 MONTHS OF WHICH YOU ARE PARTICULARLY PROUD?

» I am proud of the tenacity and flexibility of my team. We went through a few shifts and pivots over the past two years – everything from strategy to tactics, to prospects, to marketing, to sales. This can be distracting, but my team kept pace and continues to deliver.

Q. DESCRIBE YOURSELF IN THREE WORDS

» Perfectionist and control freak with a never-give-up attitude

Q. WHAT INSPIRES YOU IN FINTECH TODAY?

» Fintech is constantly changing and disrupting business models. The exciting thing about the next generation of fintech is that Banking-as-a-Service is fuelling further innovation. With BaaS providing the underlying tech, licence, compliance and regulatory needs, fintechs can focus on what they do best – making people’s lives easier with completely new front-end solutions.

Q. WHAT'S NEXT FOR KIM VAN ESBROECK?

» We plan to further invest in our BaaS strategy. What sets us apart in BaaS is our

5 FIVE MINUTES WITH...

22 October 2022

combination of banking expertise and innovative technology. We offer one of the most comprehensive Retail and SME banking platforms powered via hundreds of open APIs. This platform is also a ‘360’ ecosystem that taps into fast-moving fintech innovation by integrating nearly 90 of the best fintechs. The growth of BaaS leverages strong tailwinds of Open Banking and modern cloud engineering.

Our ability to offer a technical solution alongside our ECB licence, regulatory and compliance expertise uniquely positions us to become one of the top European BaaS players in the next two or three years.

“I was a big Madonna fan when I was a teenager. Obviously, she’s an iconic performer, but I loved her attitude”

fintechmagazine.com 23

Build a Digital Future and Lasting Customer Success

Accelerate growth and create wholistic business value with pioneering technology-fuelled digital solutions tailored to the realities of your enterprise and the financial services industry. Inspire customer loyalty and success.

Tech ‘about evolution, not revolution’ - Coforge

Gautam Samanta, Coforge EVP and Global Head of Banking and Financial Services, stresses that digital transformation is all about delivering value.

Coforge is a global digital services and solutions provider, and helps its clients embrace emerging and new technologies to achieve real-world business impact.

The company’s proprietary platforms power critical business processes across a select number of sectors, and it has a presence in 21 countries, with 25 delivery centres across nine nations.

One of the sectors in which Coforge is a key player is banking and financial services (BFS), where it is helping its BFS clients on the digital transformation journey by making the road as straight and smooth as possible.

“Digital transformation is an evolutionary process, not a revolutionary one,” says Samanta. “So we do not see it as disruptive.”

He adds that having a clear vision of what digital transformation is - and isn’t - is what shapes the solutions that help Coforge’s clients achieve their goals.

“For us, digital transformation is not just a marketing phrase to wrap around software services. It is not about the technology.

It is about delivering business value for stakeholders, including shareholders, customers and employees.”

Samanta adds that Coforge’s approach is effective because its solutions also “absorb the realities of our customers’ enterprises” - the reality being that “the old and the new often coexist in business processes that can sometimes be decades old”.

“One of the things that differentiates us is that we are pragmatic in our approach to helping clients,” Samanta adds. “Yes, we transform with the new, but not at the expense of the old, which often has value.”

It helps, too, that Coforge has a deep understanding of what value looks like in BFS, because the company has chosen to focus its attention on this sector, as well as a small number of other verticals.

“We focus on very select industries, and have a deep understanding of the underlying processes of those industries, which provide us with a distinct perspective,” says Samanta.

Learn more ›

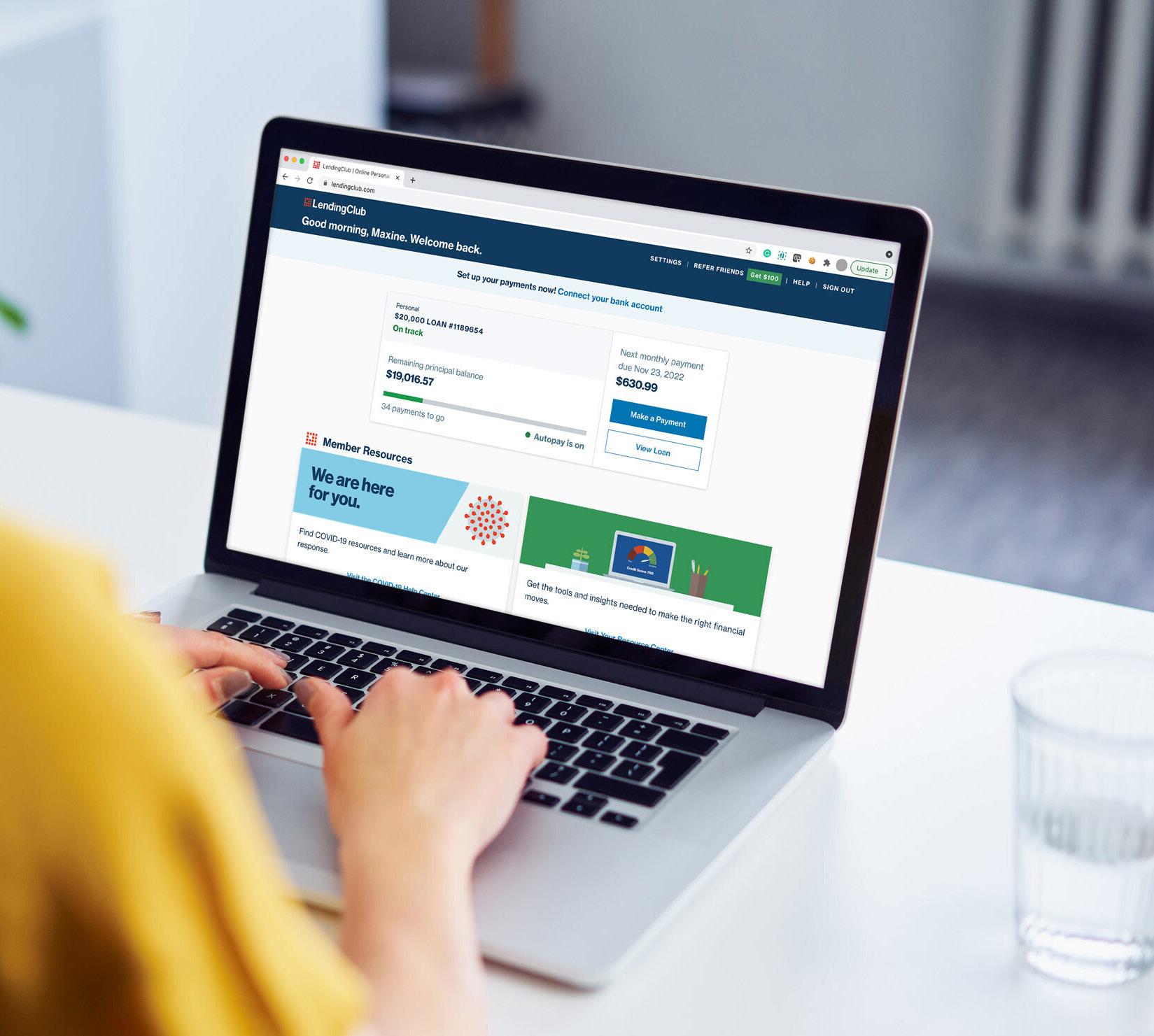

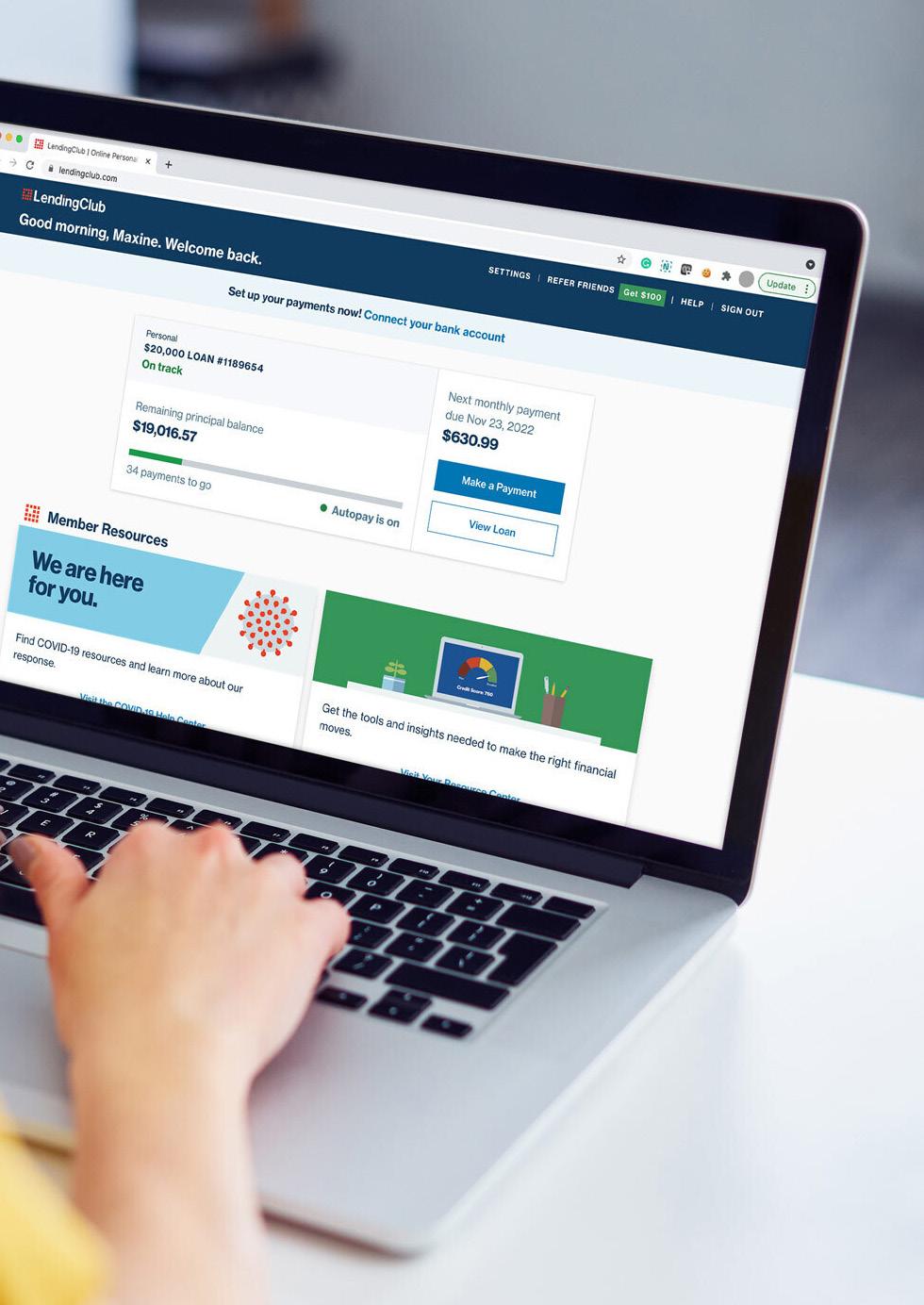

A Transformative Year: LendingClub’s Digital Marketplace Bank 26 October 2022

BY:

PRODUCED BY:

fintechmagazine.com 27

JAKE MEGEARY WRITTEN

JOANNA ENGLAND LENDINGCLUB

As customers look to make their money work better for them, LendingClub is disrupting traditional banking with a new approach

The financial health crisis is here. People are suffering amid a rising cost of living and debts are mounting as disposable incomes shrink to cover spiralling living costs. Saving money and lowering outgoings for millions of households, globally, is now a necessity.

Innovation in finance is driven by disruption, and one contender leading the charge began life as a technology company specialising in data but has now transformed into one of America’s fastest growing digital banks.

Strictly speaking, LendingClub defines itself as a technology/financial services company. Founded in 2006, innovation and marketplace disruption is embedded at its core, says Scott Sanborn, CEO, who joined the company in 2010. A passionate advocate of the work LendingClub does, Sanborn says its services have never been needed more than they are now, as consumers find themselves pushed to – and, in some cases, beyond – their financial limits.

Lower-cost financial options for borrowers

At its core, LendingClub offers lowercost lending services to borrowers than traditional banks. It’s able to do this because it acts as a broker pairing institutional investors with would-be borrowers.

28 October 2022 LENDINGCLUB

fintechmagazine.com 29

The AI Platform that Generates

Language to Motivate Every Individual to Engage and Act

Persado is the only Motivation AI platform that enables personalised communications at scale. Leading financial institutions including Ally Financial, JPMorgan Chase, and LendingClub rely on Persado to generate hyper-personalised communications. Persado’s top 30 customers have recognised over $1.5 billion in incremental revenue.

Learn more about Motivation AI at www.persado.com

Persado: Motivating customer engagement through AI

Persado’s Motivation AI platform enables personalised communications at scale, delivering incremental value to global brands

It’s one thing to know about your customers, quite another to utilise customer data to motivate and inspire them. Persado’s Motivation AI platform leverages a vast language knowledge base, advanced AI and machine learning (ML), and a decisioning engine, to deliver the precise message that motivates customers to engage and act. The result has been an impressive revenue lift and hundreds of millions of dollars in incremental value for some of the biggest companies in finance, retail, telecommunications, and other fields. Brands like JPMorgan Chase, Michaels, Gap, M&S, Dropbox, LendingClub, and Verizon rely on Persadoto generate hyperpersonalised communications.

Alex Olesen, head of Persado’s vertical strategy practice, says: “We underwrite every client partnership to project how much incremental revenue Persado can drive for our clients. We also build real-time performance reporting so our clients can see the actual uplift we are driving throughout the duration of the partnership.”

Persado is the only Motivation AI platform that enables personalised communications at scale. Digital communications present the largest opportunity to attract and build customer lifetime value. However, digital overload causes conversion rates to degrade quickly.

“It is typically not that an organisation’s offer or value proposition is unappealing, but that the brand needs to go the next step to motivate engagement and action,” Olesen says. “With the

Motivation AI platform, the top 30 Persado customers alone have recognised over US$1.5bn in incremental revenue.”

Marketers are tasked with driving growth and opening up channels of revenue. Few realise that inspiring and motivating customers to act contributes the majority of the conversion attribution. For example, Persado is working with LendingClub’s marketing department to help manage campaigns across all channels and banking products and develop optimised messaging across emails and marketing campaigns.

In 2021, LendingClub drove growth through marketing campaign enhancements enabled by Persado’s Motivation AI platform.

Learn More

LendingClub: Innovative banking for today’s customer

Customers can take advantage of an array of lending products from personal and business loans to auto refinancing and patient solutions.

The system is remarkably effective – and, says Sanborn, routinely cuts loan repayment interest charges significantly, because it puts the customer's interests first regarding their finance requirements.

He explains: “Imagine you’re going to buy a car from a dealership. Currently, in the majority of the sales, you are going to pay more for the finance than your risk would indicate. The dealer adds a markup. There's no cap on how big that markup can be. And they are not required to pass you to the lender that gives you the best deal. They may also be passing you to the lender that gives them the best fee break or rate or incentive. So, you spend all this time picking a car, negotiating the price, but you don't negotiate the cost of your financing. You drive off the lot paying more than you otherwise should.

“That’s where LendingClub comes in: using its technology platform, it can match borrowers with the best lending plans, making them vital savings in the process.”

SCOTT SANBORN CEO, LENDINGCLUB

Consumers now see banking as a thing you do, not a place you go, and they are increasingly saying that the strength of the mobile experience is what should be the driver of choice

32 October 2022 LENDINGCLUB

EXECUTIVE BIO

TITLE: CEO

LOCATION: SAN FRANCISCO, USA

Scott is the CEO of LendingClub, the only full-spectrum digital marketplace bank at scale, which has helped more than 4 million Americans save billions of dollars since it was founded in 2007.

Appointed CEO in 2016, he is responsible for leading 1,000+ employees to achieve the company’s vision to put members on a path to financial success, as the business evolves beyond its personal loan heritage to serve a broader set of customers’ needs by taking advantage of its technology and data-driven marketplace.

Scott joined LendingClub in 2010 and has been a driving force in the management and development of the organisation. With executive roles as Chief Marketing Officer, Chief Operations Officer, and President, he helped steer the company through a prolonged period of tripledigit growth running up to its 2014 IPO, the largest tech IPO that year. Prior to LendingClub, Scott held leadership positions as the Chief Revenue Officer for publicly-traded eHealth Insurance, President of RedEnvelope, Inc., and SVP at the Home Shopping Network.

He holds a BA from Tufts University.

SCOTT SANBORN

fintechmagazine.com 33

Experian Marketplace: giving financial power to consumers

Experian Marketplace is helping consumers to save money in tough times, thanks to its D2C business, its credit bureau and its partnership with LendingClub.

Within Experian’s direct-to-consumer (D2C) business, Experian Marketplace, it has assembled a network of lending partners who allow the company to serve offers to its broad consumer base. The core Marketplace mission centres around data, personalisation, and how they can be used to improve financial inclusion and restore financial power for consumers.

Marketplace uses its relationship with Experian’s credit bureau to prop up unparalleled advantages, including the ability to scale pre-approved programmes quickly. It also allows Experian to operate across multiple verticals including credit cards, personal loans and – since the acquisition of Gabi in November 2021 – digital insurance.

That variety ensures consumers receive the support they need to save money –something which is really important in light of current macroeconomic conditions.

“Currently, 76% of consumers will see a pre-approved offer,” says Rakesh Patel, SVP – Marketplace for Experian. “We want to take that to 100% of all consumers.”

Forging a fruitful partnership with LendingClub

Patel, who started life at Experian 15 years ago, knows there are parts of the credit ecosystem that are broken: “In the US, when you want to start a credit relationship, the easiest way is to apply and get declined. That’s not a consumer-friendly value proposition. Experian has tackled that by saying people no longer need to get declined for anything in order to start a credit relationship. They can come directly to Experian through Experian Go and start their credit relationship on a positive note.”

Experian has a longstanding relationship with LendingClub, which has allowed it to create unique experiences for consumers. Patel believes the partnership will transform how Experian engages with customers: “LendingClub and Experian Marketplace have a vested interest in putting consumers at the heart of everything we do. With our vision of financial empowerment for all, LendingClub gives us that ability to provide proactive engagement with our consumers around offers they may be pre-approved for.”

SCOTT SANBORN CEO, LENDINGCLUB

The amount of innovation happening everywhere, including in financial services… means that being effective requires constant examination of the landscape 36 October 2022 LENDINGCLUB

Sanborn says that, at a customer level, LendingClub makes significant monthly savings on outgoings. “On average, we're saving customers about $80 a month versus their car loan. Imagine – you drive the same car, pay it off in the same time frame, but have $80 more a month in your pocket.”

Expanding financial services through M&A Clearly, the formula is working. To date, the fintech has helped more than four million

customers and is the US market leader in one of the fastest-growing categories of lending: credit.

In 2021, LendingClub also bought into the banking sector through its acquisition of Radius Bank, where it obtained their bank charter. This event has seen the company expand significantly, transforming its identity within the fintech industry. So, is it a fintech, a digital bank, or something else entirely?

fintechmagazine.com 37

What’s next for financial marketing?

How should finance industry marketers respond to an uncertain economy? Marketing budgets may have been cut, but not expectations for results. Read Quad’s latest white paper, “The New Lending Landscape,“ for a comprehensive review of changing consumer behaviors and strategies that will help FI marketers succeed.

OUT

A marketing experience company FIND

“I would say we are a technology company… but we're a technology company with a banking charter, making us a fully-digital marketplace bank. We are something truly different. There are some direct-to-consumer banks, but we are becoming a digital marketplace bank at a time where there's a lot of change in consumer preference.”

Sanborn points out that, a decade or more ago, what drove customer preference for banking was the location of a bank branch. The landscape is now significantly different. “Consumers now see banking as a thing you do, not a place you go, and they are increasingly saying that the strength of the mobile experience is what should be the driver of choice. So, our transition to digital

banking is at a time when consumers are valuing the digital experience, and we can therefore provide a tremendous amount of value to our customers.”

The disruption of traditional lending LendingClub has a history of disruption within lending and Sanborn believes the disruption of traditional credit models has been long overdue because, fundamentally, it charges the customer far more than it should. “If you look at credit cards as an example, credit card companies separate their customers into two categories.

fintechmagazine.com 39 LENDINGCLUB

Revolvers – those are people who don't pay off the credit card balance; they have a loan. And then there's transactors – those are the people who use the card as a convenience mechanism and they pay it off every month. Those transactors are getting benefits. They're getting rewards, miles, cashback, and all of those things. The revolvers have to pay for that.

“So, you have one half of the customer base paying for the other half of the customer base. That's structural inefficiency. If you just looked at that customer and said, ‘Hey. What is the true cost of credit that you need?’, you'd find that it's lower. That's what we do with personal loans.”

Meeting customer needs

As well as taking a dynamic approach to lending, LendingClub is unusual in that its core business model increases financial inclusion by expanding access to lower cost credit. The company takes the approach that current customers and the system are ripe for a revamp. While LendingClub’s marketplace model enables it to seamlessly serve a broad range of customers, its core customer has a relatively high FICO score of around 700 and an annual income north of $100K. The team focuses on providing borrowers that are charged over the odds by lenders, such as women and minority groups, with a far better deal.

“Our customer is highly banked,” he says. “In fact, they're 100% banked. They're just not well-served. It's working out better for the banks than it is for them. What we are doing for them is providing a nationwide digital solution that disproportionately helps people who are living in areas where bank branches are closing, because more and more bank branches are closing every year.”

40 October 2022 LENDINGCLUB

LENDINGCLUB HAS SERVED MORE THAN FOUR MILLION CUSTOMERS AND IS THE MARKET LEADER IN ONE OF THE FASTEST-GROWING CATEGORIES OF LENDING: UNSECURED CREDIT.

fintechmagazine.com 41

TransUnion Celebrates

15+ Years of Partnership With LendingClub

From FinTech’s early days, TransUnion has proudly partnered with LendingClub — helping expand financial inclusion to millions of consumers through leading trended credit and alternative data. We celebrate LendingClub’s success and our collaboration which continues to deliver state-of-the-art innovation and growth.

We celebrate our 15+ year partnership with TransUnion. TransUnion has actively listened to our needs and proactively introduced new strategies and capabilities to help fuel our innovation and growth. We look forward to continuing this important partnership as TransUnion introduces innovative data and solutions that help us continue to serve the evolving needs of our members.

– Ronnie Momen, Chief Consumer Banking Officer, Lending Club

Click here to learn more © 2022 TransUnion LLC All Rights Reserved | 22-F116191

Sanborn points to the flurry of global bank branch closures and the fact that certain demographics are penalised by the current system using auto loans as an example, although it is true of all credit. “It's been long documented that women and minorities end up paying a higher price at the used car dealer for their financing than others. So, we're addressing some of those systemic inequities. But, primarily, we're making it easy to access low-cost credit that is structured in a responsible way.”

Becoming a digital marketplace bank has driven this process forwards. “We don't have to support bank branches, which is another structural inefficiency. We don't have any of that – and it creates savings in our

model. We also have the highly profitable marketplace and can pass those savings back to the consumer and still be highly profitable. The combinations of our bank, marketplace and large and loyal customer base is truly unique in banking.

The importance of digital partnerships LendingClub’s stratospheric success has been bolstered by the fintech’s robust network of partners. Currently, they are collaborating with a handful of partners including Persado, Experian, Narmi, TransUnion and Quad, all of which are providing essential services that aid LendingClub as it disrupts traditional banking.

fintechmagazine.com 43 LENDINGCLUB

44 October 2022

“The amount of innovation happening everywhere, including in financial services, means that being effective requires constant examination of the landscape to see where innovation is happening – and how you can harness it. Persado helps us unlock that with personalised language and content that's driving incremental activity, which is good for the company and – given the nature of our products – also good for the customer,” says Sanborn, who embraces the notion thata digital ecosystem serves the needs of an evolving environment.

“No one company can possibly do everything. There's so much happening in optical character recognition of documents,

SCOTT SANBORN CEO, LENDINGCLUB

SCOTT SANBORN CEO, LENDINGCLUB

fraud prevention and data aggregation using differentiated sources. Part of excellence is being able to have a finger on the pulse of where innovation is happening while also creating a culture, a structure, that can identify partners and implement with them to drive the business.”

Essentially, Persado offers a powerful platform that helps LendingClub pinpoint what is motivating customers so they can find the right product and put out the right message that is tailored to the right audience. “Persado enables us to be predictive in what we’re doing, to drive the right outcome,” he says.

Part of excellence is being able to have a finger on the pulse of where innovation is happening – and creating a culture, a structure, that can identify partners and implement with them to drive the business

fintechmagazine.com 45 LENDINGCLUB

LendingClub has been partnered with TransUnion – acting as LendingClub’s primary credit bureau – since it was founded. Recently, they also added Experian to the space where they are embarking on the next growth horizon focused on providing transparency, confidence and relevancy to the consumer.

Other partners include Narmi, a provider of digital banking technology, and Quad, which provides a postal marketing service

that is, Sanborn says, remarkably effective. “Some analogue marketing is still very important. People are often surprised by that, but it's a great consumer experience.”

A banking outlook for the future

As the fintech and all-digital banking continues to expand globally, there are no shortages of opportunity for companies offering disruptive services. LendingClub, since its acquisition of Radius Bank in

SCOTT SANBORN CEO, LENDINGCLUB

Our customer is highly banked. In fact, they’re 100% banked. They’re just not well-served. It’s working out better for the banks than it is for them

fintechmagazine.com 47 LENDINGCLUB

February of 2021, is now positioned perfectly for growth. At this point of post-acquisition, the digital marketplace bank has all its lending products in-house and is now issuing them through the bank. “We’re funding personal loans, auto loan refinance, and our purchase finance business through the bank,” says Sanborn.

“We also have launched high-yield savings accounts and CDs. That's gathering deposits to help fund the loans that we hold on our balance sheet. The next big frontier

SCOTT SANBORN CEO, LENDINGCLUB

It’s been long documented that women and minorities end up paying a higher price at the used car dealer for their financing than others

48 October 2022

will be working on a core set of banking experiences that are really targeted at our consumer.”

It’s a bright future – not only for LendingClub, but also for their customers, who are reaping the benefits of choice in a climate where controlling outgoings has never been more crucial to daily survival.

“Our core consumers are highly banked with a high income, usually of over 100,000. They have a high FICO score, between 700 and 710. But they're also high debt. We help them lower the cost of their

debt, manage their spending and help them find savings.”

He adds: “We’re moving towards a banking experience that makes it easy for people to spot where in their lives they could find additional savings. If they squirrel away those savings, they won't need to use their credit card if an emergency happens. That’s our core aim – and the big series of investments we'll be making next.”

fintechmagazine.com 49 LENDINGCLUB

ATTRACTING

INVESTMENT

EQUITY

BANKING 50 October 2022

ATTRACTING PRIVATE INVESTMENT

intech has enjoyed several boom years, raking in unprecedented amounts of capital and producing a high number of successful scale-ups. But with the economic winds seemingly turning, what will become of fintech and its ability to attract funds? We take a look at private equity (PE), asking what the current market prospects are and revealing what fintechs should know in order to attract the right investor.

What’s the difference between venture capital and

Many fintech founders will be familiar with venture capital. It’s one of the most popular ways for up-andcoming fintechs to secure finance, and because of the relative nascency of the fintech sector until now, it has garnered more attention than private equity. As the name suggests, venture capital is oriented towards smaller, younger startups. Venture capitalists invest in promising companies in return for a smaller stake in the business, in the hope that it will grow rapidly in a short time and

fintechmagazine.com 51

POWERING THE FINTECH REVOLUTION Our enterprise technology platform combines networking, edge cloud, collaboration, and security to protect, accelerate and modernize your financial applications. Let’s talk about our transformative technology services and strategies today. lumen.com/financial-services | 800-871-9244 © 2022 Lumen Technologies. All Rights Reserved. C M Y CM MY CY CMY K

By contrast, private equity is focused towards more mature businesses that have already enjoyed some success and growth. They may be businesses that are enduring some sort of financial difficulty that requires an activist investor or potential restructuring. PE firms tend to take a larger stake, and may take over a public company with a view to delisting it.

“The private equity stage is akin to moving from grammar school to college,” says John Clark, Managing Director at Royal Park Partners. “At this point, the company has demonstrated product market fit –congratulations! The investors at the next stage of a company’s evolution are likely coming out of Harvard Business School or McKinsey, so expect laser focus on the nuts and bolts of the business, such as metrics on customer acquisition cost (CAC), lifetime value (LTV), total addressable market (TAM), cash flow, profitability at a unit economic level and competitive landscape.

THE PRIVATE EQUITY STAGE IS AKIN TO MOVING FROM GRAMMAR SCHOOL TO COLLEGE”

JOHN CLARK MANAGING DIRECTOR, ROYAL PARK PARTNERS

“This group of investors isn’t looking for 10-times cash returns, but a more modest three-to-five times. They are therefore keen to convince you the valuation today is too high and cannot make any money unless they add structure to a deal (downside protection). The rationale is they make fewer but more concentrated investments and look to have a board seat and/or an observer seat as well.

“At this stage, the thinking is ‘how do we get you from US$10mn of revenues to US$40mn or US$50mn in three-tofive years?’ It becomes a tactical and strategy-driven process, focused on professionalising the organisation. This tends to be the biggest shock to founders as they transition from VC to growth/PE investors.”

“

fintechmagazine.com 53

What is the state of the current PE market?

A lot has been made of the current economic conditions, and whether they’re conducive to investment. It’s possible that the latest economic developments –high inflation and the spectre of a global

was invested in fintech by PE across 144 deals in 2021 – a new record that’s substantially above the prior record of US$5bn in 2018. Fintech’s relatively higher gross margin and cash flow profile make it attractive to PE. It’s also an extremely scalable sector – financial services touch everyone, everywhere.”

Private equity is still dwarfed by venture capital funding, though. VC investment

Fintech report, almost triple the US$46bn the year before. This heightened level of investment may reflect an industry coming of age, or it might indicate that new sub-

Anton Ruddenklau, Global Fintech Leader for KPMG, says: “We’re seeing an incredible amount of interest in all manner of fintech companies, with record funding in areas

BANKING

54 October 2022

such as the increased threat of cybercrime, demand for embedded financial services and the inefficiency of current core banking infrastructure”.

What do private equity firms look for in an investment?

“H1 2022 has seen a somewhat inevitable deceleration in the rate of private equity dealmaking across the board, though Europe has been more resilient,” Lawson continues. “Over the coming quarters, we may see a further reduction in new deals as rising rates, declining GDP, falling consumer confidence and the ongoing war in Ukraine impacts businesses.

fintechmagazine.com 55

56 October 2022

fintechmagazine.com 57

PRODUCED BY: STUART IRVING WRITTEN BY: JESS GIBSON

CULTIVATING CONNECTIONS AND ENHANCING UNDERPRIVILEGED LIVES

58 October 2022

fintechmagazine.com 59 VODAFONE FIJI

60 October 2022 VODAFONE FIJI

With its many islands hemmed by crystalline waters that wash onto white sand and greencarpeted mountains, Fiji is a vista of immense natural beauty.

The archipelago, made up of over 300 islands and 500 islets, was formed as a result of volcanic activity over 150 million years ago. The two main islands of Viti Levu and Vanua Levu – which contain almost 90% of Fiji’s total population between them –are the beating heart of the economy, with tourism accompanying minerals, sugar cane and fishing as one of its largest drivers, aiding Fiji in being one of the most developed economies in the Pacific.

Despite this, though, the reality of daily life on Fiji’s islands belies the image most of us possess; it is a developing nation, after all – one that’s still battling with the brutal blows inflicted by the COVID-19 pandemic on tourism and the economy. Pockets of rural Fijian communities still function day-to-day with just 2G or, if they’re lucky, 3G connectivity, lacking the infrastructure needed to enhance this further for the time being.

But this is where Vodafone Fiji steps in. The company, which is “the main telecommunications player in Fiji” (with 85% market share), is committed to “enriching people’s lives” and overcoming the obstacles currently plaguing the archipelago.

“When it comes to connectivity, we no longer treat it as a want, but as a basic need for customers now,” establishes Chief Technology Officer (CTO), Vikash Prasad, “especially in a developing country like Fiji, where there's lots of people who still live in these rural or maritime areas.”

Becoming the largest telco network in Fiji Parent company Vodafone is itself a global telecommunications company that dips its toes successfully in a wide array of industry sub-sectors, though it does so with a customercentric ethos that builds “strong customer affiliation and brand loyalty”. It is this approach to which Prasad attributes Vodafone Fiji’s success.

VIKASH PRASAD CHIEF TECHNOLOGY OFFICER, VODAFONE FIJI

“Vodafone Fiji is a dynamic and fast-paced business, operating in an essential industry,” Prasad states, highlighting the differentiating factors of the company. “Our vision is to be the most admired

“IT'S ALWAYS VITAL TO HAVE A GOOD PLAN IN PLACE. IF YOU HAVE A GOOD PLAN IN PLACE, YOU HAVE THE FIRST PART DONE”

At Vodafone Fiji, Vikash Prasad dedicates himself to the pursuit of technological advancement to provide digital equality and equity to those most in need

fintechmagazine.com 61 VODAFONE FIJI

Hear about the ways Vodafone Fiji is enriching Fijian lives

company in Fiji, and our mission is to enrich people’s lives.”

Prasad also credits the telco’s “exceptional frontline, customer care teams and business account managers” with helping it to stay on top of the competition and reach 95% of the Fijian population. “Apart from the traditional voice, data and SMS offerings, we offer the best ICT solutions in the region, such as Cloud, SDWAN, and many other innovative solutions that are tailor-made for many of our ICT customers.”

In addition to customer-centricity being a defining element of Vodafone Fiji’s success, its recent foray into the FinTech world is opening up new doors.

“We are also an emerging FinTech company, providing digital services in terms of financial and e-business at a national level,” says Prasad. “Being an incumbent, we have to be agile in all our operations, so it's all about creating value in our products and services.”

“WHEN IT COMES TO CONNECTIVITY, WE NO LONGER TREAT IT AS A WANT, BUT AS A BASIC NEED FOR CUSTOMERS NOW – ESPECIALLY IN A DEVELOPING COUNTRY LIKE FIJI, WHERE THERE ARE LOTS OF PEOPLE WHO STILL LIVE IN THESE RURAL OR MARITIME AREAS”

VIKASH PRASAD CHIEF TECHNOLOGY OFFICER, VODAFONE FIJI 62 October 2022 VODAFONE FIJI

This approach has enabled steady yearon-year growth for Vodafone Fiji, which the company hopes will continue as it sets out on its 5G journey, becomes more established in FinTech and finds innovative ways to ensure its customers receive the connectivity needed to boost its tourism-heavy economy.

Moulding attitudes for the future of telco innovation

Innovation is essential to the longevity of a business – as Prasad well knows. In the postCOVID age of rapid digital transformation and detailed data analysis, impacted by geopolitical and climate-related events, this is particularly true. But having a skilled team that thinks out of the box requires a change in management and strategy, which is often the product of company-wide cultural overhauls.

So, Vodafone Fiji has invested in its staff – via training, enabling work-from-home capabilities and providing leadership coaching – and employees have, in turn, ‘invested’ in the business, allowing innovation to flourish. “Our staff believe in our vision,” he says.

“One of the things we are also doing as part of our transformation revolves around our workforce – we’re focusing on increasing the capabilities of our people and investing in our talent pool. That means putting our staff through specialised training, and providing for and equipping them so that they strive for greatness in the new digital world,” Prasad states, going on to explain how his personal ethos is woven throughout this process to promote excellence.

“A life lesson that I live by is that we have to do things right the first time, and that what is right to do is not always easy. We need to put in the hard yards now so that we can reap the benefits of it in the future.”

Now, this doesn’t mean that Prasad’s team has no room to make mistakes; it means

VIKASH PRASAD

TITLE: CHIEF TECHNOLOGY OFFICER

Vikash Prasad is responsible for providing leadership direction and innovation ownership to drive overall technology strategy, operational excellence, and innovation for Vodafone Fiji. He is recognised for building strong technology platforms and delivering several network transformation initiatives for Vodafone.

Vikash leads a dynamic team responsible for continued network growth and adopting technology evolution, ensuring Vodafone delivers next generation network initiatives to create the most innovative and reliable networks in Fiji and across the Pacific. In his 19 years with Vodafone, Vikash has successfully driven a number of multi-million dollar mobile network projects. Vikash previously held the roles of Manager Access Networks, Engineer Network Services and Systems Support Analyst.

He holds a Masters in Business Administration (Technology) from the Australian Graduate School of Management at the University of New

BIO

EXECUTIVE

VODAFONE FIJI

Metric: a powerful platform for network optimisation

Multivision and Vodafone Fiji work together via Metric, an efficient and powerful platform, which enhances the critical role that partnerships play in achieving growth.

Multivision has been a key partner of Vodafone Fiji for almost four years now, with the two companies joining forces in 2019 when Vodafone Fiji subscribed to Metric, a SaaS offering owned, delivered, and remotely managed by Multivision. A company that also provides professional and strategic advice alongside bespoke IT solutions and co-sourcing of IT talents, Multivision has worked with a host of bigname businesses such as Siemens, Unitel, and Ice.net.

Since its inception in 2007, Multivision has based its work around one core philosophy: ‘Grow to make you grow’, which is threaded through each aspect of the company´s daily work.

With Metric and this fruitful partnership, Vodafone has been able to conduct

in-the-field quality audits of network performance. This has allowed Vodafone Fiji to continue its two-year 5G infrastructure build while ensuring that existing connections are stable and secure for even the most rurally isolated Fijians.

Vikash Prasad, Chief Technology Officer for Vodafone Fiji, describes this platform as “efficient and user-friendly, a powerful tool that allows us to have access to almost real-time information out in the field, all of which is web-based,” explains Prasad.

“In addition to monitoring daily network operations, when optimising networks, the platform allows us to efficiently provide automated solutions’ reporting. This information can then be shared with Vodafone Directors and easily related to network KPIs, reducing the need for multiple platforms and screens.”

Vikash Prasad is vocal when praising the Metric team for their “timely and responsive communication, the quality of their support, and their ability to solve a variety of issues, no matter the complexity.”

“Multivision promotes innovation and simplicity, and Metric is a powerful tool for us,” he adds.

that, by investing time in the planning, research, design or training aspects of a task or process, the final result itself will be right the first time. And this thread continues throughout everything Prasad oversees, particularly Vodafone Fiji’s digital transformation. “It's always vital to have a good plan in place. If you have a good plan in place, you have the first part done.”

A popular theme to many a business discussion over the last two years has been the unexpected boost that COVID-19 gave to digital transformation. In some cases, the pandemic merely spurred on a pre-existing idea or sped up the pace; in others, it created an urgent business need in order to survive.

VIKASH PRASAD CHIEF TECHNOLOGY OFFICER, VODAFONE FIJI

“During COVID, there was a surge in demand for data, and this would've been the same story for a lot of telcos around the world. That put a lot of stress on the network, and during that time, the boundaries of our mobile network services were being tested.”

Not only were Vodafone Fiji’s networks being tested in the short-term, but there were also long-term economic effects that created a need for digitisation. “For Fiji, tourism has always been one of the biggest economic drivers. So, when the borders closed down, the economy suffered.”

“DEVICE STRATEGY WILL PLAY A KEY ROLE, WITH ONE OF THE MAIN DRIVERS WHEN IT COMES TO DEVICES BEING AFFORDABILITY”

66 October 2022 VODAFONE FIJI

PARTNERING WITH MULTIVISION

MultiVision has been a partner of Vodafone Fiji’s for four years now. From this fruitful partnership, Vodafone has been able to undergo an in-the-field, quality audit of its network performance, subsequently acquiring the Metric platform for network optimisation. Prasad describes this platform as “efficient and userfriendly”, “a powerful tool” that collates “KPI data with other data” to allow for a correlation of issues.

Vodafone Fiji engineers have so far only worked with those at MultiVision via virtual means, often on other sides of the world – though this will no longer be the case soon. These meetings have allowed the fine-tuning and customisation of the platform, despite the time difference, with Prasad describing the MultiVision team of engineers as “timely and responsive” and providing “excellent support”.

fintechmagazine.com 67 VODAFONE FIJI

VIKASH PRASAD CHIEF TECHNOLOGY OFFICER, VODAFONE FIJI

This directly impacted the telco’s ability to put the necessary infrastructure in place to support citizens and tourists alike in the immediate wake of the pandemic. “But everything is changing now,” Prasad smiles. “Our customers want connectivity everywhere, so businesses are shifting priorities. One of the buzzwords right now is the cloud and having cloud platforms or migrating to cloud

platforms, but with that comes a lot of risks, as well. Cyber threats are one of the biggest challenges that we face right now.”

As such, Vodafone Fiji is investing not just in its team, but in expanding technological infrastructure across the whole of Fiji to develop the cloud, 5G connectivity and its FinTech arm.

The road to 5G is paved with good intentions Being a developing country situated on an archipelago means progress can be slow. Across Fiji, which is predominantly made up of rural or coastal locations, developing connectivity to wireless mobile networks is difficult – and that’s without considering regulatory requirements, different frequency spectrums, and affordability for all customers, which is why Prasad refers to 5G in that respect as “a double-edged sword”.

“A LIFE LESSON THAT I LIVE BY IS THAT WE HAVE TO DO THINGS RIGHT THE FIRST TIME, AND THAT WHAT IS RIGHT TO DO IS NOT ALWAYS EASY. WE NEED TO PUT IN THE HARD YARDS NOW SO THAT WE CAN REAP THE BENEFITS OF IT IN THE FUTURE”

fintechmagazine.com 69 VODAFONE FIJI

“VODAFONE FIJI IS A DYNAMIC AND FAST-PACED BUSINESS, OPERATING IN AN ESSENTIAL INDUSTRY”

VIKASH PRASAD CHIEF TECHNOLOGY OFFICER, VODAFONE FIJI

Prasad hopes that, by delivering connectivity to the entirety of Fiji, he can uplift the digitally ‘poor’ – those with basic or limited connectivity, hindering personal progress – ensuring digital equality and, most importantly, equity.

“A lot of focus for us is also about covering these areas, making use of the existing assets that we have, and trying to sweat them as much as possible so that we deliver the connectivity that people are after.”

Vodafone Fiji may be an estimated two years away from full 5G connectivity, but with Prasad at the helm developing and solidifying plans, as well as encouraging his team to think differently, the rollout is likely to be free of any kinks or issues.

70 October 2022 VODAFONE FIJI

IT TAKES TWO (OR MORE) TO MAKE A THING GO RIGHT

“We are always on the lookout for new partnerships. It’s no secret that to succeed, having trusted partners is a must –it’s no longer about operating in a silo.

For a telco & ICT provider like Vodafone Fiji, acquiring accreditation and certifications from world-class vertical companies such as Cisco, Oracle and Microsoft is key for us as we strategise to further enhance our position in the ICT sector

Simply put, collaboration with vertical industries is now the mainstay when it comes to delivering best-in-class valueadded services to our customers, resulting in new revenue streams.

Apart from partners such as ZTE, Cisco, Aviat Networks, we also work very closely with partners such as MultiVision, Ciena, umlaut, InfoBip and many others to deliver the best value not only for Vodafone, but for our customers as well.”

“Fiji is a developing country, so the average user may not spend up to a thousand dollars to get a 5G phone; a normal, basic phone would meet their requirements. And Fiji is also predominantly a prepaid market.

“So having the right device strategy, where we have a pool of low-end 5G devices that are prepaid, will really help.”

But another obstacle to overcome is the Fijian terrain itself, which prevents the telco from “using the traditional mobile towers or cell towers” across every area.

“We needed to think outside the box. And one of the very cost-effective solutions that we have deployed here is broadband satellite: it’s quick to deploy, easy to install, easy to operate, and can be done within days,” Prasad explains.

Shifting priorities and expanding verticals

Ultimately, the company’s approach is not to rush ahead, but instead to “wait, watch and then act”. This will help the team to build an “understanding of the 5G ecosystem and how it will bridge the current digital gaps”, as well as informing them of “any investments needed to fully grasp this”.

As established, affordability for all customers is key to both Vodafone Fiji and Prasad. You see, 5G infrastructure is all well and good, but the vast majority of the devices designed for such capabilities are high-end and, as such, have high-end prices attached.

“Device strategy will play a key role, with one of the main drivers when it comes to devices being affordability,” Prasad affirms.

In the face of globally-shifting priorities, it’s become necessary for businesses to expand their verticals, breaching into multi-cloud terrain as part of their digital transformation. For example, Vodafone Fiji has merged its private cloud with that of Oracle Cloud Infrastructure (OCI), Microsoft Azure and Amazon Web Services, which, in Prasad’s words, is “bringing the best of private and public clouds together with our expertise so that we offer our customers a unified cloud platform for all their needs”.

Arguably the biggest move for Vodafone Fiji in recent years is the development of its Mobile Money platform, which marks the company’s move into the FinTech space to complement the different industries within the local Fijian market and, therefore, the economy.

“Mobile Money is one of the greatest examples and pride of Vodafone Fiji,” Prasad enthuses. “M-PAiSA is an in-housedeveloped digital wallet platform that

fintechmagazine.com 71 VODAFONE FIJI

VIKASH PRASAD CHIEF TECHNOLOGY OFFICER, VODAFONE FIJI

provides a number of basic financial and digital payment services.

“Launched in 2010, M-PAiSA now processes over $200mn in monthly M-PAiSA transactions, making it a significant player in Fiji’s digital and cashless payment space.”

This bespoke digital wallet platform, M-PAiSA, has established itself as a market leader in the mobile and digital payment space, with “high brand equity” and “trust as a reliable and robust digital payment platform”.

Prasad details the effect this success has had in the years since M-PAiSA’s launch: “One of Fiji’s fastest growing economic drivers is inward International Remittance. Within a space of 12 months, M-PAiSA has gained a 25% market share of all inward remits into Fiji.

“We have taken an advantageous position by being the first to market with our innovative payment services using QR pay. Month-on-month, we see new merchants come onboard with us. Next on the horizon for Vodafone Fiji is to become a scheme

“FOR FIJI, TOURISM HAS ALWAYS BEEN ONE OF THE BIGGEST ECONOMIC DRIVERS. SO, WHEN THE BORDERS CLOSED DOWN, THE ECONOMY SUFFERED”

72 October 2022 VODAFONE FIJI

payment provider. This is a whole new ball game for Fiji as a nation.

“All-in-all, Vodafone is not only a CSP but offers services that can be offered by a FinTech organisation.” Exciting, indeed.

Digitalisation, data and virtualisation

The future outlook for Vodafone Fiji will feature “digitalisation, data and virtualisation” on a large scale, which, of course, includes the continuation of its mobile networks' rollout with focus on 5G and beyond, as well as the development of its FinTech arm. This means “evolving legacy platforms into world class systems that can be supported through cloud” and obtaining “deeper insights through collaboration in terms of analytics and forging partnerships” to allow for “detailed, real-time insights of customers’ pain points”.

At the very core of realising this aim of enabling connectivity in underprivileged rural

and coastal regions sits data and analytics –and in the modern world, data is king.

“When it comes to analytics, it’s a move to fresher, more dynamic ways of understanding our customers using crowdsourced data,” Prasad explains. “It’s no longer just about using data from your OSS & BSS platforms. Detailed insights from near realtime systems gives another level of clarity on what the pain points are exactly.” This means that, no matter where in Fiji someone resides – whether on the most remote islet or the centre of the capital, Suva – they aren’t held back by being digitally poor.

Providing digital equality and equity to those who are underprivileged is a noble endeavour, particularly when the aim is to do so carefully and steadily to make sure it lasts for the foreseeable future.

fintechmagazine.com 73 VODAFONE FIJI

Customer retention and loyalty programme finance

WRITTEN BY: JOANNA ENGLAND

WRITTEN BY: JOANNA ENGLAND

74 October 2022

As the lending environment is impacted by the global financial crisis, service providers are seeking new ways to retain customers

These days, most customers seeking loans are stuck between a rock and a hard place. The cost of living crisis has resulted in less disposable income and, in many cases, essential payments can only be managed with the help of understanding lenders.

However, lenders – fully aware of the plight of customers and rising interest rates – have rolled back many of their affordable products and services, leaving fewer credible options in the marketplace for loan-seeking consumers.

Even when sound agreements are met between banks and consumers, economic instability is a constant source of stress. In the UK alone, inflation is at its highest rate in 40 years – and energy price rises show no sign of slowing down. These elements place additional pressure on businesses and lenders, alike.

Furthermore, spending, as expected, has contracted and savings are also being depleted. So how can consumers protect their financial assets, maintain

their savings and still manage a healthy relationship with their financial services provider?

In an age of digitised, global finance, the humble Credit Union has one lending solution that could well preserve the pocket change of even the most financially challenged borrower – in the form of loyalty loans.

How do Loyalty Loans work?

According to the UK’s Wiltshire & Swindon Credit Union (WASCU), loyalty loans are a style of lending product that protects customers’ savings when they request finance for essential purchases or expenses. Rather than using their own cash to secure a transaction, the lender will provide up to five times the amount the saver has accrued, with the option to pay off the loan within a flexible time frame – and usually with lower interest rates than standard lenders.

“ It is so important right now to refrain from making any rash decisions that could later damage a person's financial security”

ANDREW MEGSON EXECUTIVE CHAIRMAN, MY PENSION EXPERT

fintechmagazine.com 75 FINANCIAL SERVICES

Easy multi-entity management and reporting Sage Intacct cloud finance software for financial services FINANCE THAT SCALES WITH YOU LEARN MORE

Considering the current financial climate, helping customers to maintain their assets while enabling flexible borrowing could well be a lifeline to protect consumer assets while giving them flexibility and spending power. The loans are also based on the amounts of cash the customer has saved on a regular basis, thus reducing risk for the lender while incentivising the customer to save more.

STEVE ZIMBERG DIRECTOR OF MARKETING, NORTH AMERICA, FINTECHOS

Steve Zimberg, Director of Marketing, North America at FintechOS, says market conditions will always fluctuate, and financial institutions must be agile enough to serve their customers and members in those moments of flux.

“Loyalty and savings loans are products that can certainly be useful to support customers/members seasonally or for emergency needs.”

In either scenario, he says that a financial institution's ability to move quickly and be of service to its members is critical. “Organisations with a High-Productivity Fintech Infrastructure (HPFI) can quickly pivot to meet the needs of local and economic market conditions, and rapidly configure and personalise loan products and journeys at scale.”

This can be a real boon for financial institutions of all sizes, especially for organisations that want to enter new areas of opportunity but may not have the resources to execute such a move or are tethered to a legacy banking core and cannot move quickly. “Having the right HPFI helps financial institutions stay relevant in all economic climates,” Zimberg says.

process

a single digital experience ensures that customers can compare

terms and make

decisions”

“ Financial institutions unifying their online and in-branch loan application

through

loan

informed

fintechmagazine.com 77 FINANCIAL SERVICES

FINANCIAL

Loyalty loans are also another option in a market where choice is critical to customer servicing. Zimberg points out that customers should explore and examine the terms of each type of loan and decide with their financial advisor the right option for their particular needs.

Conversely, financial institutions need to be prepared to pivot in different economic climates and offer personalised loans –of all types – that meet the needs of their customers/members. “Financial institutions unifying their online and in-branch loan application process through a single digital experience can ensure that customers compare loan terms and make informed decisions.

SERVICES

“

Borrowers will have to prepare themselves for the likelihood of increased repayments, such as higher mortgage rates”

RICHARD EAGLING PERSONAL FINANCE EXPERT, NERDWALLET