FINTECH THROUGH DIVERSITY

DISRUPTING

Q4: CONNECTING INVESTORS AND COMPANIES THROUGH TECHNOLOGY

WOMEN IN FINTECH Learn about a new path for private and public companies seeking to generate liquidity IPO FEATURING:

2023 fintechmagazine.com

ASSESSING THE PROGRESS OF OPEN BANKING

THE ROADMAP TO

March

bizclikmedia.com

Ways to Work With us

We produce Digital Content for Digital People across 20+ Global Brands, reaching over 15M Executives

Digital Magazines

Websites

Newsletters

Industry Data & Demand Generation

Webinars: Creation & Promotion

White Papers & Research Reports

Lists: Top 10s & Top 100s

Events: Virtual & In-Person

Work with us

The FinTech Team JOIN THE COMMUNITY Never miss an issue! + Discover the latest news and insights about Global FinTech... EDITOR-IN-CHIEF JOANNA ENGLAND EDITOR ALEX CLERE CHIEF CONTENT OFFICER SCOTT BIRCH MANAGING EDITOR NEIL PERRY PROOFREADER JESS GIBSON CHIEF DESIGN OFFICER MATT JOHNSON HEAD OF DESIGN ANDY WOOLLACOTT LEAD DESIGNER SAM HUBBARD FEATURE DESIGNERS SAM HUBBARD REBEKAH BIRLESON MIMI GUNN SOPHIE-ANN PINNELL HECTOR PENROSE JUSTIN SMITH ADVERT DESIGNERS JORDAN WOOD DANILO CARDOSO CALLUM HOOD VIDEO PRODUCTION MANAGER KIERAN WAITE SENIOR VIDEOGRAPHER HUDSON MELDRUM DIGITAL VIDEO PRODUCERS MARTA EUGENIO ERNEST DE NEVE THOMAS EASTERFORD DREW HARDMAN JOSEPH HANA SALLY MOUSTA JINGXI ANG PRODUCTION DIRECTORS GEORGIA ALLEN DANIELA KIANICKOVÁ PRODUCTION MANAGERS JANE ARNETA MARIA GONZALEZ CHARLIE KING YEVHENIIA SUBBOTINA MARKETING MANAGER EVELYN HOWAT PROJECT DIRECTORS JAKE MEGEARY JACK MITCHELL MEDIA SALES DIRECTORS MIKE SADR MANAGING DIRECTOR LEWIS VAUGHAN CEO GLEN WHITE

FEMININE FINANCE

Women are becoming a force to be reckoned with in the fintech space

This month we celebrate International Women’s Day and all that entails. In the fintech space, that means applauding all the brilliant and innovative women who have climbed the ranks in the financial industry and become leaders of their fields. From startups to giant corporations, and to groundbreaking digital banks, there’s no denying that women are bringing a unique perspective to the financial space, and with it, heaps of innovation.

This month, we’ve also explored BNPL and the institutional adoption of crypto - an unfolding drama coming to an ewallet near you. And of course, we have some amazing interviews and deep dives into the leading sectors to keep you abreast of all trends and events.

Happy March - we hope you enjoy the issue!

JOANNA ENGLAND joanna.england@bizclikmedia.com

fintechmagazine.com 5

diversity in the candidate pool has been proven to result in increased diversity in companies, which is what we’re slowly seeing happen”

© 2023 | ALL RIGHTS RESERVED FOREWORD

FINTECH MAGAZINE IS PUBLISHED BY

UP FRONT

000 130 18 12 22

CONTENTS

12 BIG PICTURE World Economic Forum Annual Meeting 2023 14 THE BRIEF Improving diversity by focusing on staff retention 16 TIMELINE The semantic web and the future of Web 3.0 18 TRAILBLAZER Guillaume Pousaz 22 FIVE MINS WITH Linoy Kidd — leading in banking and building schools

fintechmagazine.com 7 46 74 96 120 MARCH 2 023 FEATURES 46 OPEN BANKING Assessing the progress of open banking 74 PAYMENTS Shaping the shopper experience through BNPL 96 CRYPTOCURRENCY Seasons change: emerging from the crypto winter 120 DIVERSITY Disrupting fintech through diversity 130 TOP 1 0 Women to watch in fintech for 2023

Watch our 2022 Showreel A BizClik Event 3RD MAY 2023 VIRTUAL CONFERENCE Join the Virtual Event Disrupting Fintech SPONSORSHIP GET YOUR PASS

COMPANY REPORTS

30 MORGAN STANLEY AT WORK

The path to liquidity: Exploring strategies for private companies

52 BELL Evolving towards the finance of the future through data and analytics

82 Q4 Connecting investors and companies through technology

104 FIDELITY INTERNATIONAL

fintechmagazine.com 9 30 104 52 82 MARCH 2 023

How Fidelity brings digital assets to institutional clients

Segmentation has never been this rewarding

Stop ransomware in its tracks.

Boost security performance with Akamai Guardicore Segmentation.

Learn more

Akamai prioritises the future demands of cyber customers

Steve Winterfeld of Akamai discusses the company’s university-based founding and how it merged into a leading multibillion-dollar cybersecurity firm

Akamai was founded following a competition at the Massachusetts Institute of Technology (MIT), entered by its co-Founder and CEO Frank Thomson Leighton—Dr Tom Leighton. Since that time, the organisation has expanded massively, and in the words of Steve Winterfeld , Advisory CISO at Akamai, the company “continues to solve hard problems.”

The cybersecurity company plays a critical role for corporations as it focuses on the future, to determine whether threat motivation will change and how to best combat ransomware attacks, state-sponsored DDoS attacks, and ransomware that could turn into wiperware.

“Those are real concerns, and we’re keeping an eye out for those. And so we have probably 15 security capabilities backed up by services, responding to customers’ needs and rapidly growing on the edge compute and cloud side.”

“We started out with a web application, or as it is more commonly called now, web application and API protection, and expanded into protecting the infrastructure against DDoS to include the DNS infrastructure and recently added internal infrastructure protection and visibility through micro-segmentation,” explains Winterfeld.

Responding to the cybersecurity needs of the customer

As an established cybersecurity organisation, Akamai can now focus on what customers need.

Winterfeld explains that, in response to its clients’ feedback, the company has been acquiring the necessary assets and tools to fulfil those needs with the recent purchase of Guardicore. Guardicore’s leading microsegmentation products will be added to Akamai’s comprehensive portfolio of Zero Trust solutions to protect enterprises from damage caused by breaches like ransomware, while safeguarding the critical assets at the core of the network.

“We bought Linode, which is a cloud provider. And so now we have an integrated platform to build and perform on as well as secure.”

A prime example of Akamai’s ability to meet customer demands, particularly in high-risk environments, is its partnership with First Bank, which is “very concerned about its real-time visibility into its network. We’re partnering with them on a software-based microsegmentation, where they’re able to see those data flows and create segments.”

BIG PICTURE

Image credit: © WEF/Faruk Pinjo

Image credit: © WEF/Faruk Pinjo

World Economic Forum

Annual Meeting 2023

Davos, Switzerland

Klaus Schwab, Founder and Executive Chairman of the World Economic Forum (WEF), speaks at the beginning of its annual meeting in Davos in January. Amid ongoing political and economic uncertainty, there was a lot to discuss in Switzerland. Ukraine urged Western leaders to provide more military equipment in the fight against Russia; UN Secretary General Antonio Guterres warned that the world was “flirting with climate disaster”; and the whole event took place against the backdrop of a Europe-wide corruption scandal that has so far implicated a number of MEPs.

fintechmagazine.com 13

THE BRIEF

“We’ll see mainstream crypto investors voting with their wallets and favouring platforms (and jurisdictions) that are embracing, rather than trying to escape, regulation”

READ MORE

“For younger people seeking meaning in their careers, it’s particularly important to highlight the significant initiatives of female leaders in the tech sector”

Krista Griggs

Head of Financial Services & Insurance Fujitsu

READ MORE

BY THE NUMBERS

Will the FTX fallout affect long-term confidence in crypto?

71% N0 29%

YES

EU consortium delivers controversial digital ID wallets

The EU has announced a multicountry consortium to lead the delivery of a cross-border payments pilot programme –including the launch of a controversial digital ID wallet.

READ MORE

Micheal Ramsbacker CPO Trulioo

14 March 2023

Improving diversity by focusing on staff retention

Improving staff retention is an important first step in tackling the tech sector’s diversity problem, according to the authors of a new research report, published by Wiley.

Nearly two-thirds (64%) of businesses admit to struggling to retain employees from underrepresented backgrounds, according to the research. This is in spite of a majority (65%) of respondents believing that they work hard to foster an inclusive corporate culture.

More than a quarter (27%) of tech workers aged between 18 and 24 say they have left a role because they didn’t feel a sense of belonging, while over a fifth (22%) say they had previously experienced biased treatment from managers. The research indicates that failing to create a truly inclusive and welcoming environment contributes directly to poor retention rates on tech teams.

BUTTER

The Silicon Valley fintech, which helps online subscription businesses to reduce “accidental churn” within payment processing, has raised US$22mn in Series A funding led by Norwest Venture Partners.

40SEAS

The Israeli fintech platform for cross-border trade financing has emerged from stealth, raising US$11mn in seed funding from Team8 and securing a US$100mn credit facility from ZIM Integrated Shipping Services.

PADDLE

The UK payments fintech announced it would be cutting around 8% of its workforce as tech industry layoffs continue into 2023. Founder and CEO Christian Owens said it was a response to rising inflation.

CLEARCO

The troubled lending firm, which has undergone a significant downsizing in the past year, has announced the departure of CEO Michele Romanow – the second chief executive to leave the company in the past 12 months.

W A Y U P S

MAR23

W A Y D O W N S

fintechmagazine.com 15

THE SEMANTIC THE FUTURE 2006 2014 2015

As the internet prepares to make way for the development of Web 3.0, we take a look at the innovation timeline

THE SEMANTIC THE FUTURE OF 2006 2014 2015

The beginning of it all

The term Web3 points to the third generation version of the internet. Web1 was the dial-in of the 90s. Web2 refers to the technologically revamped version of Web1, after it was replatformed on Javascript, HTML5 and CSS3. In 2006, Tim Berners-Lee, the British scientist who developed the original internet, first proposed the concept of Web3 when he spoke about the Semantic web as a component of Web 3.0 – the third generation internet.

The advancement of blockchain technology

But Web3 didn’t really materialise until 2014. The term was phrased by the cryptocurrency Polkadot founder and Ethereum co-founder, Gavin Wood,, who is also the founder of blockchain infrastructure company Parity Technologies. He put his vision of the internet’s future forward as blockchain began to develop and its potential to provide a wholly decentralised online ecosystem was realised.

Facebook dabbles in Meta

Facebook’s role in metaverse history began in 2014, when the company bought the virtual reality hardware/platform Oculus. Prior to this, the very first virtual spaces existed within the gaming sphere as early as 2006, with games like Second Life, followed by Minecraft and the still very popular Roblox. Facebook’s Meta is, however, a very different beast from its gaming predecessors.

TIMELINE

16 March 2023

SEMANTIC WEB AND OF WEB 3.0

SEMANTIC WEB AND FUTURE OF WEB 3.0 2020 2023 2030

2020 2023 2030

New normal and the metaverse

Once COVID-19 hit and governments around the world forced their citizens into lockdowns, life online suddenly became the experience of the majority. The pandemic saw reliance on online transactions and shopping soar. Furthermore, leading banks, fintechs, entertainment companies, retailers and tech giants all staked a claim in Meta. This has since prompted other companies to launch their own online metaverse equivalents, all built on Web3 technologies.

Peer-to-peer interaction

Today, Web3 technology enables the creation of decentralised networks and platforms that allow peerto-peer transactions as well as interactions without the need for intermediaries. This can lead to a more equitable distribution of power and resources.

Web3 business innovations are considered the solutions to several key challenges that users face with Web2, such as data breaches, compromised online security and privacy.

Augmented reality to become…reality?

Could we be heading to a future that sees the majority of our interpersonal human interactions take place online? Some experts absolutely think it's possible.

According to Melanie Subin, a Director at The Future Today Institute in New York City, by 2030, “a large proportion of people will be in the metaverse in some way”. She says some will simply use it “only to fulfil work or educational obligations”, while others “will live the majority of their waking hours 'jacked in'.”

fintechmagazine.com 17

GUILLAUME POUSAZ

As the high-flying CEO and Founder of Checkout.com, Dubai-based Guillaume Pousaz is the Swiss billionaire with an estimated net worth of US$20bn

As the high-flying CEO and founder of Checkout.com, Dubai-based Guillaume Pousaz is the Swiss billionaire with an estimated net worth of US$20bn

Born in 1981 in Geneva, Switzerland, Guillaume Pousaz studied mathematical engineering at the Ecole Fédérale Polytechnique De Lausanne, before enrolling on a bachelor's degree in economics at HEC Lausanne, with a view to entering the world of investment banking.

As a youngster and student, he was always interested in the creative side of life, and was fascinated by street art – a passion that has resulted in his Checkout.com offices being decked in unique design works that mix logic with art.

However, in 2005, his decision to enter banking was halted when his father was diagnosed with cancer. He left his university course and, according to reports, moved to California to become a surfer ‘for a while’.

Entry into finance

Although the surfing life appealed to his bohemian outlook, Pousaz soon began to think about a career in finance once again.

While in California in 2006, he began working for the finance company IPC, which seemed a good compromise as it had offices close to the beach.

The role at IPC introduced Pousaz to the payments industry – and highlighted how the world of online shopping was transforming the retail and consumer experience. Pousaz was so inspired by the payments space that, by 2007, he had launched his first startup company – a fintech called NetMerchant that facilitated payments from US and European companies needing to make payments in foreign currencies.

He ran NetMerchant until 2009 and then diversified again, buying the Mauritiusbased fintech SMS Pay for US$300,000. He also launched his second startup, Opus Payments, in 2009 – another payments processing fintech – only this time, his target marketplace was Asia. Opus Payments was based in Singapore and managed payments from Hong Kong businesses to process their international transactions from global buyers.

The launch of Checkout.com

By now, it was clear that Pousaz had found his groove. He liked payments, he was good

TRAILBLAZER

18 March 2023

THE WEALTHIEST MAN IN SWITZERLAND

TRAILBLAZER

“BE ALL IN, ALL THE TIME. YOU OWE IT TO THE COMPANY, TO THE OTHER FOUNDERS, AND YOURSELF”

at it, he understood the power of the internet, and its potential for customers. But, he had encountered issues during his first startup years. In fact, one drawback was the issue of payments processing on a global scale, for both shops and shoppers.

He solved the issue by launching his third startup, Checkout.com, in 2012. The ease of use and frictionless experience the fintech offered its customers made it an instant hit with online retailers. By 2019, Checkout.com was one of the world's most successful fintech stories.

Pousaz and his leadership team even raised US$230mn in funding that year – which ended up being the largest Series A funding round ever for a European fintech company.

Pandemic accelerated growth for Checkout.com

Of course, the rest is history. COVID-19 did its worst, resulting in the world being plunged into lockdowns, online payments companies reaped the rewards, and Checkout.com was no exception. In fact, by January 2021, the company had launched its next funding round, raising a further US$450mn at a valuation of US$15bn. Forbes then estimated Pousaz's net worth to be US$9bn. During 2020, Checkout.com released a report saying its payments processing volume had tripled in that year alone.

What’s next for Pousaz?

Well, so far, he seems keen to stick with Checkout. com. Now married and a father of three, he spends his time commuting between Dubai and London, telling Forbes that he travels on the red-eye from Dubai to London every Sunday night, so that he can work his four-day, 80-hour week in the London office, before heading back to his family in the UAE on a Friday morning.

By anyone’s measure, it’s a brutal work pattern, but one that Pousaz seems to thrive on. And, with Saturdays dedicated to his kids, he tries not to allow himself to be distracted. “I get 800 emails a day at this point,” he said.

fintechmagazine.com 21

FIVE MINUTES WITH...

LINOY

KIDD

LEADING IN BANKING AND BUILDING SCHOOLS

Linoy Kidd, CIO of HSBC, shares the inspirational story of how she climbed the corporate ladder while raising money to build schools for children

Q. DESCRIBE YOUR JOURNEY INTO BANKING. HOW DID YOU GET HERE?

» I did my undergraduate degree in IT, which has a direct correlation to the job that I do now. I did a summer internship at a Dutch bank called ABN AMRO and the people were so helpful. After that position, I went into telecommunications to try a new industry, but I really preferred banking. As you can imagine, some incredible brains work in the bank; they have to understand so many intricacies including algorithms and underpinning formulas. That, and I really liked the fast pace of the job and how smart the people are.

For me, working with the business in partnership is the most rewarding part of my job. I joined HSBC 17 years ago and started in foreign exchange options as a support analyst, then worked my way to team leader. I moved on to Manager and then CIO in Mexico, before becoming CIO in MENAT for MSS (Markets Security Services).

As soon as I became a leader of men/ women I knew this was my calling in life. I love being a leader and managing people. I really feel it is a privilege to manage people and to try and get the best out of them to work and output for the business.

Q. WHO WAS YOUR CHILDHOOD HERO AND WHY?

» I grew up in the 80s, when Band-Aid was a big event on television. I knew that I wanted to emulate those that help others and to action change in the world in whatever small way I could. Martin Luther King sacrificed himself for the greater good to change the face of the world forever. I always quote him: “I have a dream where all children can play together no matter their race... not everyone can be famous but everyone can be great because greatness is determined by service.”

My grandmother was also a big influence. She could not read or write and would beg her grandkids to teach her. She was Kurdish from Iraq and was just never taught to

fintechmagazine.com 23

FIVE MINUTES WITH...

read. Because of my education, I was able to get a role here at HSBC. Fastforward three years and my daughter has just graduated with a double major with distinction in STEM. Because of this, combined with a deep understanding of what education can bring, I set up the #Infusion100 movement four years ago. With colleagues from HSBC, we have built seven schools: five in Africa; one in Haiti after the earthquake there; and one in Nicaragua. These schools have educated over 1,000 students so far, and continue to do so.

We encourage them to learn and then make a choice for how they want to live. Education gives choice; education gives freedom.

With Infusion100, I want to show women around the world that there is no glass ceiling. That we can punch through it and that anything is possible, no matter your past or who or what you are.

Q . WHAT'S THE BEST PIECE OF ADVICE YOU’VE EVER RECEIVED?

» I had a manager in Hong Kong who told me that it is the ‘think outside of the box’ ideas that make the difference. At Google, they have the 10% principle: carve out 10% of your work week to try and innovate, to do something new that is not part of your day's work. Google Maps came from this 10%, so its impact can be wide ranging.

Q. NAME ONE PIECE OF TECHNOLOGY YOU COULDN’T LIVE WITHOUT AND TELL US WHY (EXCLUDING YOUR MOBILE PHONE)

» I am a sports fanatic; I go boxing every day after work. Every year, we walk over 100km for charity so I can’t live without my Garmin. I wake up and check it, and I go to sleep checking it. It basically shows me everything, including calories burnt, steps, stairs, heart rate (so I know when I am getting too stressed), and sleep – and no, I don’t sleep enough.

Q. WHO DO YOU LOOK UP TO IN TERMS OF LEADERSHIP AND MENTORSHIP?

» I really look to leaders that lead from the front. I built a school in Nicaragua and, like the chief of that village, I try to emulate the way that he leads his village and his tribe. He knew every mother, child, and baby by name. He greeted them with a smile on his face. He was humble and not only that, but every day at the school work site, he was there early and gave 200%. He was strong and he led the way. He had built every house in the village by hand.

On the last night, we had an arm wrestle with all the village leaders and us. He beat everyone. He laughed it off; I wanted to emulate this type of leadership, to treat everyone equally, whether they are the CEO or a graduate. Everyone has a place in the world, everyone.

DESCRIBE YOURSELF IN THREE WORDS DETERMINED STRONG STUBBORN

Q. IS THERE A PERSONAL ACHIEVEMENT FROM THE PAST 12 MONTHS OF WHICH YOU ARE PARTICULARLY PROUD?

» I gave birth to a son during the pandemic; it was brutal as no one was allowed to be in the delivery room with me. I had to have an emergency C-section because the baby went into distress, and I got a double infection that I couldn’t fight while in labour. I signed my life away on that table and they came over with a waiver form saying if I die, I am liable for my own life. At that moment, I felt totally alone. I experienced some PTSD and depression after that, but then I started boxing again. I got my life in order, and now I want to show women you can have it all; that whatever you live through that doesn’t kill you, makes you stronger. During my maternity leave, I went to Ghana and built the sixth school. I dug it with my new baby because I wanted to show people that it's possible to do anything as a woman – even five months after the surgery. Give birth, bring up a baby and build a school. No one wanted to go on this school build, and it was very risky because it was in the middle of COVID-19. But we went and we built anyway because that is our calling as the Infusion100 team: to build a school a year until we die.

Q. WHAT INSPIRES YOU IN BANKING AND FINTECH TODAY?

» IT underpins the business; you cannot have one without the other. It is our job to take out the blockers and enable the business to do their job as seamlessly as possible.

So it’s amazing to be pivotal to the underlying strategy. Pivoting to the

cloud has been instrumental to be more agile and using the agile methodology to revolutionise the way IT works.

Q. WHAT’S NEXT FOR LINOY KIDD?

» At work, I am very happy with the level I have achieved. I worked hard to get where I am today, and I will look to grow within these shoes for many more years to come.

I’m always thinking of new ways to revolutionise the human experience within IT and banking, bringing networks upon networks of people together to show what can be achieved in a small space of time.

In terms of the charity, we will hit nine years next year. I want to build nine schools in nine years, then keep going and going with that to set up out of school education for those less fortunate and who do not have access to education. I want to think of ways to be a better leader to improve myself day on day, to help those around me and to change their lives in whatever small way I can, to keep on working on giving people the toolkit to step out of poverty, to give them the same viewpoint on life that anything is possible when you bring people together.

FIVE MINUTES WITH...

26 March 2023

The effortless power of one platform

Give any part of your business an instant digital upgrade

The Backbase Engagement Banking Platform is the evolution of digital banking.

Built for fast implementation and ease-of-use, the platform allows financial institutions to rapidly deploy digital solutions that delight customers and empower employees.

With the power of one platform, you can:

Engage your customers

Create tailored customer journeys from account signup to product up-sell

Empower your employees

A 360° view of your customer helps you deliver personalized and instant service

Ready to get the full picture?

Talk to our specialists

Leverage a composable architecture

Select best-of-breeds partners for your perfect end-to-end solution

Reduces overhead and drive greater innovation with our cloud model.

The Backbase Engagement Banking Platform

Start small, grow big Future-proof digital solutions can be customized to your needs now, then scaled later.

This advertisement can only scratch the surface of what the Backbase Engagement Banking Platform can do for your business, employees and customers.

Ready to get the full picture?

Function as an agile workforce to fast-track consumer innovation

Tap into the cloud

Get the agile advantage

Talk to our specialists

30 March 2023

AT WORK

MORGAN STANLEY

WRITTEN BY: JOANNA ENGLAND

PRODUCED BY: BEN MALTBY

THE PATH TO LIQUIDITY: EXPLORING STRATEGIES FOR PRIVATE COMPANIES

Morgan Stanley at Work is helping to create a new roadmap for private and public companies seeking to generate liquidity

The route to IPO is a complicated one – especially given the current climate, as the economy slows and companies are under increasing pressure to scale while maintaining more modest financial constraints than they were previously afforded.

When a private company seeks to go public, it usually means one of three things: firstly, a company is seeking to raise capital; secondly, its board is planning to provide liquidity for investors and employees; and, finally, there’s a desire to raise brand awareness and strengthen market position in the eyes of potential customers.

The route to an IPO has often been seen as a key milestone in a company’s development in the global marketplace.

But in recent years – helped along by some regulatory changes and market factors – many companies are choosing to delay their route to the public markets and instead work on accessing capital through venture capital and growth equity investors to maintain their private company status.

Capital in private and public markets

According to Kevin Swan, Co-Head of Global Private Markets for Morgan Stanley at Work, these days the average time for a startup company, from launch to make the move to go public, is now over 12 years.

Swan, who studied as an engineer specialising in mechatronics – a

multidisciplinary field that exists at the intersection of mechanical, electrical and computer engineering – got swept into the financial world through his early career experiences in startup companies. The path led him into venture capital and later to a company called Solium Capital, which was then acquired by Morgan Stanley in 2019.

Swan’s background has been instrumental in his understanding of the various reasons underscoring certain companies’ decision to choose an IPO route or remain as private entities.

The delay in going public, he explains, is mainly due to changes in the regulatory

32 March 2023 MORGAN STANLEY AT WORK

environment in addition to the flow of capital from public to private markets. This has resulted in private companies being able to raise significant capital without having to go public.

“Over the past decade, we’ve seen increasing amounts of capital flow into the private markets, and we’ve encountered several other factors that have led to this dynamic situation, where companies are now staying private for much, much longer.”

“Now, the average time to enter the public market for a venture-backed tech startup is much longer and these companies are valued in the billions, many in the tens of billions.

Furthermore, some are able to raise enough private capital to not even necessarily need to pursue an IPO and rather enter the public markets through a direct listing.”

Even though it may take a company several years to reach the point where pursuing the public markets is a possibility, preparing for that process requires careful planning. Alternatively, while a company may wish to remain private, it may need to address its equity structure and liquidity strategy to ensure it remains an attractive option for its investors and employees as well as navigate the current economic climate.

fintechmagazine.com 33

Morgan Stanley at Work reshaping private markets liquidity

Although IPOs are generally considered the ultimate liquidity event, private capital markets are continuing to gain momentum in terms of investment interest. As a result, many companies are able to generate the funds required to provide employees with some liquidity on their equity packages, without going public.

These types of events, however – and the management of successful equity programmes – require considerable groundwork to be viable.

And that’s where Morgan Stanley at Work comes in: a division of Morgan Stanley that is focused entirely on private and public company share plan administration solutions that empower companies in providing employees workplace financial benefits.

Their offering covers equity management, retirement solutions and financial wellness. For private companies wanting to maximize the benefit of their equity programmes, Morgan Stanley at Work offers a number of liquidity solutions.

Morgan Stanley’s day-to-day operations primarily consist of investment banking and financial services, so offering solutions that aid in the path to the public markets beyond raising capital has been a natural progression. As a global corporation, it is uniquely positioned to provide an equity management system for the private market that can facilitate recordkeeping, transactions, and money movement.

“If you're a public company, that infrastructure already exists in the form of transfer agents and clearing brokers, where you can easily buy and sell stocks in a public

34 March 2023

company online or through your financial advisor,” Swan says.

However, in the private marketplace, this can be more of a challenge, as historically speaking, there’s never been a highly sophisticated infrastructure to provide easy liquidity solutions. Morgan Stanley at Work is taking a progressive approach to solving that challenge by building a trading infrastructure and transaction execution framework that caters to private markets and is designed with an issuer perspective.

Specific protocols for private companies

Unsurprisingly, the private markets don't operate in the same way as public markets. Regulation is quite different, and the private investor community often has different objectives and time horizons than public investors. Morgan Stanley at Work offers

KEVIN SWAN

TITLE: CO-HEAD OF GLOBAL PRIVATE MARKETS

INDUSTRY: FINANCIAL SERVICES

LOCATION: ALBERTA, CANADA

Kevin Swan is a Managing Director of Morgan Stanley in Wealth Management. He is Co-Head of Global Private Markets for Morgan Stanley At Work which delivers equity management, liquidity, and workplace solutions to private companies. He joined Morgan Stanley through the acquisition of Solium Capital where he served as the VP of Corporate Development.

EXECUTIVE BIO

Prior to joining Morgan Stanley, Kevin held roles in product management and corporate development, was a Partner at venture capital firm Inovia Capital, and served as a board member at several venture backed technology startups. Kevin has a B.Sc. from the University of Alberta and a M.S. from Stanford University where he studied mechatronics and control systems.

KEVIN SWAN

CO-HEAD OF GLOBAL PRIVATE MARKETS, MORGAN STANLEY AT WORK

MORGAN STANLEY AT WORK

“Historically speaking, there’s never been a highly sophisticated infrastructure to provide easy liquidity solutions in the private marketplace and Morgan Stanley at Work is taking a progressive approach to solving that challenge”

Shareworks – an equity management platform utilized by private companies to manage their cap tables, employee stock plan and liquidity programmes. They have also launched a private market transaction desk that can help execute block sales and other forms of secondary transactions, giving shareholders access to liquidity and clients access to investment opportunities.

“We have the equity management platform and transactional capabilities to be able to support companies and shareholders,” Swan explains. “We also have an attractive investor client base for participation in liquidity events and secondary transactions.”

According to Swan, high-growth venturebacked companies control their cap tables, as ownership structures and the different legalities provide them the authority to

decide who can be an investor –and who can't.

“The big takeaway is that these companies have a definitive say in terms of who can actually own their shares. So they want highquality, reputable, long term investors on their cap table.”

Morgan Stanley at Work is fortunate to work with some of the best companies in the world, due to the full suite of wealth management and financial wellness offerings. These services empower companies to extend benefits to their employees, at the same time as engaging directly with both employees and investors.

“A lot of times, for employees in these startups, it's the first time that they've obtained any wealth. And whether that's a modest amount or generational wealth–which isn't uncommon at some of these

36 March 2023

startup companies – we have solutions and a large population of top financial advisors to support these employees on their financial journey.”

Managing the public versus private pathway

Sam Adams is the Executive Director of Private to Public Strategy for Morgan Stanley at Work. A veteran of the ‘route to IPO’ journey prior to joining Morgan Stanley, she managed a number of prominent IPO projects, which helped her to decide that managing share plan administration programmes and supporting companies through the process was the perfect use of her acquired skills.

“We have several private clients who have no intentions of ever going public and we're starting to see a larger trend in new clients who want to establish stock plans with regular liquidity activity already preprogrammed in,” explains Adams.

“This is because it gives them the flexibility to allow people to take some of the value that they've helped create in the company off the table through the shares they've earned as an employee, while not putting so much pressure on the overall company to have to make a decision of whether or not to go public within a certain time period.”

As someone who has witnessed firsthand the complicated process of the path to IPO, Adams is passionate about her role and says companies that manage their equity programmes well not only benefit themselves but in turn, also change the lives of their loyal employees.

“One of my personal missions in life is to make sure that capturing that opportunity doesn't get lost on other people. It really can be a life-changing thing, and Morgan Stanley at Work can not only help the company have the underlying infrastructure to make those

SAM ADAMS

TITLE: EXECUTIVE DIRECTOR, PRIVATE TO PUBLIC STRATEGY

INDUSTRY: FINANCIAL SERVICES

LOCATION: CALIFORNIA, US

Sam Adams is currently an Executive Director at Morgan Stanley at Work leading a specialized team focused on helping private companies transition their stock plans into the public market.

Prior to this role Sam lead the global equity team at DoorDash through building a best-in-class equity infrastructure to operate as a growing public company and a tremendously successful IPO in 2020. She also led MuleSoft’s global equity team through an IPO in 2017 and subsequent acquisition by Salesforce in 2018.

EXECUTIVE BIO

Additionally, she designed MuleSoft’s Total Rewards and Mobility practices, including global compensation programs, ESPP, and employee benefit packages. Sam was also a key member on the Trulia legal team managing all things stock and corporate compliance through their IPO in 2012 and subsequent acquisition by Zillow in 2015. Sam received a BA in Sociology from UCLA in 2004 and the CEP designation in 2015.

MORGAN STANLEY AT WORK

SAM ADAMS OF MORGAN STANLEY AT WORK DESCRIBES HER IPO STRATEGY JOURNEY

As the Executive Director, Private to Public Strategy for Morgan Stanley at Work, Sam Adams is passionate about managing IPO and private equity paths for companies

Playing a major role in the IPO and private equity programmes of some of the world’s largest companies was not originally in the career plan for Sam Adams. The Los Angeles native initially had ambitions to enter the interior design industry, as her family owned a textile cleaning and restoration business. “I felt it was part of my DNA,” she says.

But fate had other plans. After a post-college move to San Francisco, following the 2008 financial crash, Adams ended up working for a small start-up company that inadvertently put her on the path of being an equity owner and guiding companies and employees through large liquidity events.

From there, Adams moved to another start-up company, which involved her in the IPO process, and gave her the opportunity to be mentored. This led to further roles at MuleSoft and DoorDash – always operating in-house equity functions with a penchant for the private to public transition process.

She joined Morgan Stanley at Work because it offers her the opportunity to employ her skills and knowledge without having to move on from companies once the IPO process has been completed.

“I'm a single mom and I've had to learn all these things on my own, and I take it really personally that, through my work, I can help other people who are probably in the exact same position that I was in 10 years ago.”

She adds: “It's great to be able to recognise the value potential in a growing company. It's also important to have a high amount of responsibility and gratitude for those things, too. That really gets me up in the morning because I know that the work we do ends up creating an experience for an end user that we probably never talk to.”

DID YOU KNOW...

SAM ADAMS EXECUTIVE DIRECTOR, PRIVATE TO PUBLIC STRATEGY, MORGAN STANLEY AT WORK

38 March 2023 MORGAN STANLEY AT WORK

“Trust and reputation are a really big deal. Typically, when a company decides to embark on the path to IPO, they may only give themselves three months to manage the entire process”

transactions happen, but on the participant side, ensure that people have the right resources to take advantage of what that opportunity brings to the table.”

A developing trend in private capital markets

A good equity programme not only rewards employees but also creates a deeper investment culture within the organisation. If an employee can see the value of their shares rising as the company grows, it can incentivise them to work towards the company’s common goals. Equally, companies today may have to take into account lifestyle choices. Employees might have certain expectations in mind when they consider equity programmes at the job-offer level. Today, as companies take longer to reach the IPO stage, they also have simultaneous

opportunity to scale and grow. This means they have to offer competitive equity stake value or risk losing out to the competition. The war for talent as we’ve known it for the last 10 years is beginning to slow, evidenced by the volume of layoffs, particularly in the technology sector. However, down markets may breed innovation because with mass layoffs comes a surplus of talented people that find themselves without work, have potentially realized some significant value from previous roles and are ready to solve new problems. Similar to companies that emerged in the aftermath of the 2008 financial crisis, Morgan Stanley at Work believes there will be a new period of innovation out of the current downturn as well.

Swan says: “One of the big drivers in the evolving approach private companies take

fintechmagazine.com 39

towards liquidity over the last decade was the war for talent. Private companies have become much larger, but the draw for startups to attract employees was always in the equity. You knew that you were taking a job where you were going to be fairly underpaid from a market perspective in your base salary. However, you're going to have the upside of equity, which could create an asymmetrical outcome, financially, for yourself.”

But what happens if these companies stay private for longer? “Now, we have companies that are worth billions – even tens of billions of dollars and they're financially sound –and they’ve raised a tonne of capital. But as valuations increase, you obviously don't have quite the same upside in any new equity you

receive as you did when you were a small startup worth a few million dollars,” Swan says.

He goes on to explain that a shift has occurred, where these companies have to start paying more competitively on base salaries. But, they may also have to be competitive on the equity front. And very often in these cases, private companies are competing with large public companies.

“So, if I'm a senior engineer looking at joining one of these late-stage private companies and I've got an offer from them and I've got an offer from one of the world’s leading public tech companies – they may be very similar in terms of the base salary, and even the value of the equity I'm getting. But one big difference is that in a public

40 March 2023

company, when your equity vests, you can immediately sell it on the public markets. You have access to a liquid market.”

At a private company, the options are more limited. Swan establishes that this is where Morgan Stanley at Work comes in, following a growing number of private companies that have started becoming more proactive in providing liquidity to compete with public companies. Just over the past three years, it's a much more commonplace approach for large companies to take.

Offering access to value through private equity programmes

Current financial instability is another reason for employees to demand greater value and

security from their companies, says Adams, highlighting that the need for better equity packages has probably never been greater.

“In terms of what's happening economically, I think liquidity is even more important because people don't have access to as much capital. Credit is far more expensive; inflation means that your money doesn't go nearly as far as it did a couple of years ago.”

“But people still have real needs to manage their lifestyles, and that can look like buying a home or paying for education for children. Your day-to-day life in this environment now means that it's harder to meet those same financial obligations. And so, if you have equity and you have all this value sitting on the side lines, people want

fintechmagazine.com 41 MORGAN STANLEY AT WORK

access to it. They need access to it now, probably more than they have in the last 5 to 10 years.”

Private market liquidity and the investment community in a downturn

Questions, however, remain. How do private companies fit into all this, particularly at a time when investment is activity low? And how can they generate enough capital to remain as competitive as their public counterparts?

Adams says it all comes down to arranging the right types of liquidity events and setting up a strong framework.

“As an employee, you've been helping generate value over the period that you've been employed, and you've seen prices go up. Now, we're starting to see company valuations level out or go back down. But investors still believe in these businesses. Some of the economic factors at play here are not necessarily because these businesses aren't good businesses worth investing in.”

She points out that the tough climate doesn’t mean investing opportunities won’t happen; rather, in some ways, the opportunities are greater. “It's an interesting opportunity for investors who have probably

been sitting on the side lines when valuations were higher and saying, ‘That price point feels too high for me to start to get involved’, and take positions in companies that they truly believe in at a price that seems a little bit more reasonable and sound, and start to be able to play the long game.”

Private market liquidity can be beneficial

Not going public but enabling employees to gain value from their stocks can result in gains all around, without the demands of going public. For example, if a group of two or three investors is looking to take a position and a group of 100 employees is ready to sell to them, it reduces the number of shareholders on the company’s cap table.

“This can potentially be really beneficial to all parties,” Adams states.

She points out that the benefit of gaining liquidity works on two levels for companies. Firstly, by letting them sell directly to an investor, they are allowing liquidity for employees without dilution. The process also provides an opportunity to clean up the cap table, the records of stock ownership, and reduce the number of actual shareholders.

One downside, however, is that the process may force companies and individual shareholders to come to terms with the delta in current valuations versus where they were a year ago. The gap in valuations from a company’s last fundraising round and what investors are willing to pay today is widening in private secondary markets.

“Something that we think our clients are still coming to terms with is taking the hit on price now and knowing that, if this is a good business, it will outlast the market conditions that exist today,” she says.

KEVIN SWAN

CO-HEAD OF GLOBAL PRIVATE MARKETS, MORGAN STANLEY AT WORK

42 March 2023 MORGAN STANLEY AT WORK

“We’ve seen increasing amounts of capital flow into the private markets… companies are now staying private much, much longer”

Investing in Private Companies

From a venture capitalist perspective, the situation can be complicated. They want to maximize the valuations in their existing portfolio companies while entering new ones at what they deem as fair valuations. VCs carry out their own valuation models on what future valuations of certain companies will look like, generally built on revenue multiples, growth rates and unit economics. But, there is also an element of volatility in share prices, depending on competitive dynamics and the market’s climate.

Added to that is the current, ongoing economic downturn – though this will almost certainly self-correct at some point, with Swan explaining that “the venture capital market is very cyclical”.

“Even compared to other financial markets, it has the highest highs and the lowest lows

when it comes to valuations. For example, just over a year ago, secondary investors would pay a premium on the last round that a company raised.

“Now, we're in a different macro environment and talking about the discounts on the round an investor would pay. What's interesting or unique is that it's been so long since we've had one of these downturns. The market has been relatively stable for a decade. So there's a whole generation of people operating in this market that have never experienced a recession.

Also, 10 years ago, we didn't have these massive private companies, liquid secondary markets, and large amounts of private capital available; it's uncharted territory for everyone. But, like any market, it'll figure itself out in the long-term.”

fintechmagazine.com 43 MORGAN STANLEY AT WORK

The future for Morgan Stanley at Work

Due to Morgan Stanley at Work offering a unique service via the provision of a clear and managed path through both IPO offerings and private liquidity services, the future's looking bright. Adams explains that, very often, these processes are messy and rushed. But when a dedicated team can guide a company through the regulatory and transactional minefield, it can be an invaluable service.

Furthermore, many companies are now turning to the service because they want to be ready and prepared in the event of an IPO. Equally, though, they would like the support of an expert team when it comes to managing their private equity programmes, too.

“If you're a corporate company and you're issuing equity to raise money or leveraging stock as part of your compensation programme then it's really important to continually connect the dots between your investor community, your board of directors, and your employee base,” she says.

Adams stresses the importance of understanding the needs of different groups and elements that are going to propel the business and provide liquidity for people while still potentially scaling to be a public company, “whether or not that ends up being the final result”.

“Sometimes it's M&A; sometimes it's staying private; and sometimes it's going through an IPO process,” Adams outlines. “For us, I think the next 12 to 18 months are really focused on making all of that easier for corporate clients. If it's easier for them, then it should be a better experience for their investors and their employees.

And working with a brand like Morgan Stanley at Work for such heavyweight decisions also has its merits.”

“Trust and reputation are a really big deal. Typically, when a company decides to embark on the path to IPO, they may only give themselves three months to manage the entire process. It can be messy and disorganised, because there are just so many bases that need to be covered. And then, once they reach the IPO, all that must be managed on the other side of the event, too. It’s not a process that suddenly ends when the company is public.”

In relation to this point, Adams notes that companies thinking about their route to IPO may begin preparations a good 12-months in advance to give themselves time to organise everything. She also says that many companies are using Morgan Stanley at Work to get their financial ducks in a row, so that if they do make a last-minute decision to go public, they can do so at short notice and be in their best shape.

“It alleviates a bunch of the pressures that companies start to feel as they approach a large liquidity transaction, like a tender offer or IPO, because they have trusted partners within the Morgan Stanley at Work umbrella. You can help give people resources to make good smart decisions.”

SAM ADAMS EXECUTIVE DIRECTOR, PRIVATE TO PUBLIC STRATEGY, MORGAN STANLEY AT WORK

44 March 2023 MORGAN STANLEY AT WORK

“IPOs can be messy and disorganised, because there are just so many bases that need to be covered”

Disclosure

This following article is a paid advertisement by Morgan Stanley at Work and does not necessarily represent the views and opinions held by the staff and management of FinTech magazine.

©2023 Morgan Stanley Smith Barney LLC. Member SIPC. CRC 5429284 1/2023

ASSESSING THE PROGRESS OF OPEN BANKING

ASSESSING THE PROGRESS OF OPEN BANKING 46 March 2023

Open banking has come a long way in just five years, establishing itself as a key driver of innovation within finance. But do consumers know what it means?

WRITTEN BY: ALEX CLERE

Open banking refers to the concept of consumers granting third-party app developers access to their transactional information, usually from their bank, directly through an API. This then allows the fintech ecosystem to build out more value, creating tools that support those customers through their daily lives and bring meaningful insights to their banking data.

Open banking has been around as a concept for several decades, but it has only come to life in practice in the last couple of years. In fact, it may have reached mainstream status at just the right time. According to Constanza Castro Feijoo, Stakeholder Engagement Manager at the Open Banking Implementation Entity (OBIE), open banking in the UK – one of the pioneering markets for it – has only been around since 2018 and it took two years to get the standard live.

Like most things in fintech, it began relatively slowly. After 1mn people had started using open banking in their daily lives, it took a year until the industry reached the 2mn people mark. Yet it took only 3 months for open banking to accumulate its latest million customers, going from 5mn to 6mn users. Today, there are 6.6mn users of open banking technologies in the UK, with 90% of banks adopting the standard and

offering this service to their customers. Over 250 fintechs have joined the open banking ecosystem and there are regularly 1bn API calls a month involved in facilitating the technology, Castro Feijoo says.

Part of the reason for this success is that regulators and government agencies have got on board with open banking early, recognising its potential to completely reshape the banking landscape. In the UK, open banking was initially mandated to the nine banks who, together, offer 85% of all business and personal current accounts – but of course, since those days, the sector has surpassed all regulatory minima. According to Grand View Research, the size of the global open banking market is expected to grow to over USD$135bn by 2030.

Open banking is still learning, still tweaking “We’re still learning and we’re finding things we need to improve as we go,” says Nicole Green, VP Product Strategy and Operations at Yapily, summing up the current juncture that open banking finds itself at. “That’s where we are as an industry – we’re a teenager maybe, if we wanted to age ourselves. We’re going through that awkward stage.”

“OPEN BANKING IS STILL LEARNING AND WE’RE FINDING THINGS WE NEED TO IMPROVE AS WE GO”

fintechmagazine.com 47 BANKING

NICOLE GREEN VP PRODUCT STRATEGY AND OPERATIONS, YAPILY

KYC AND AML SOLUTIONS FOR FINTECHS

Harness the power of data and leading-edge technology to turn existing know your customer (KYC) and anti-money laundering (AML) compliance challenges into opportunities

DISC OV ER MOR E An LSEG Business

Broad adoption and rapid acceleration inevitably mean challenges along the way: Green acknowledges that, with open banking being so dynamic and constantly evolving, there are bound to be pitfalls and obstacles. But when done correctly, open banking has the power to improve the banking relationship from three different sides.

Green thinks of the beneficiaries of open banking as three distinct groups. There’s the fintech players within the ecosystem itself, who bring new open banking solutions to market and have created whole

businesses based on this new approach. Then there’s the businesses who are able to consume these products and create more personalised financial products for customers – like affordability or credit assessments that can improve financial inclusivity, or payment products that can eliminate chargebacks and reduce the cost. The final, and perhaps most important, group is the customers themselves: they get the benefits of all of these products, which can potentially have meaningful impacts on their financial security.

“

OPEN BANKING IS MAYBE A TEENAGER, IF WE WANTED TO AGE OURSELVES. WE’RE GOING THROUGH THAT AWKWARD STAGE”

fintechmagazine.com 49 BANKING

NICOLE GREEN VP PRODUCT STRATEGY AND OPERATIONS, YAPILY

Yapily published a report towards the end of last year that cited the cost-of-living crisis, driven by high inflation and interest rates and rising energy costs, as a major source of concern for 95% of people. This is an area where open banking could have a really positive impact on consumers’ lives. According to the report, around twothirds of respondents had started using new financial tools for the first time to help them budget, manage their bills or check their credit score.

Do people need to understand the term ‘open banking’?

Despite these promising signals for adoption, Yapily’s survey also raises a potentially

detrimental side-effect of open banking’s meteoric rise to success. It found that 52% of ordinary consumers have not heard of the term ‘open banking’, despite an increasing number of people enjoying financial tools that rely on it. So is it important that consumers are educated about open banking and understand what’s involved ‘under the hood’, so to speak?

Rolands Mesters, CEO and Co-Founder at Nordigen, believes that it’s important for consumers to understand that open banking is a trustworthy technology. “The early adopters need to be sure that nothing funky is going to happen with their most precious assets,” he says. But this doesn’t mean they have to call it the same thing that industry

50 March 2023

calls it. After all, few people understand the wires and the signals that happen behind an ATM, but they know what it’s for – and, crucially, they know how to use it.

“The further we go into adoption, the less open banking as a name is going to matter,” Mesters explains. “Today, for example, when we’re making payments, we’re not really thinking about what sort of payments there are. We tend not to wonder whether paying with your phone on a counter is a card payment or not. It is and it isn’t. Open banking hopefully gets to that scale, and the faster it gets to that scale the better. At that scale, it really doesn’t matter how many people know what open banking means and what it is.”

“THE FURTHER WE GO INTO ADOPTION, THE LESS OPEN BANKING AS A NAME IS GOING TO MATTER”

fintechmagazine.com 51 BANKING

ROLANDS MESTERS CEO AND CO-FOUNDER, NORDIGEN

52 March 2023

THIS DOCUMENT HAS BEEN PREPARED BY BIZCLIK MEDIA GROUP fintechmagazine.com 53 WRITTEN BY: İLKHAN ÖZSEVIM PRODUCED BY: CRAIG KILLINGBACK BELL FINANCE

EVOLVING TOWARDS THE FINANCE OF THE FUTURE THROUGH DATA AND ANALYTICS

54 March 2023

Nantes Kirsten, Director of Financial Analytics CoE, and Matthew MacEwen, VP of Finance Transformation, detail Finance’s change catalysts via data and analytics

Bell is Canada’s largest communications company, providing advanced broadband wireless, TV, Internet, media and business communication services throughout the country. Their purpose is to advance how Canadians connect with each other and the world, enabled by a strategy that builds on their competitive strengths and embraces the new opportunities of the integrated digital future.

Founded in Montréal in 1880, Bell has a long history of connecting Canadians to the people and things that matter. From their earliest days, starting with the telephone, Bell continues to bring generations of Canadians together with the latest technology. Today, Bell is delivering the future to customers with an unmatched infrastructure investment in the best broadband fibre and wireless technologies, including the growing 5G network.

Through Bell for Better, they are investing to create “a better today and a better tomorrow”, by supporting the social and economic prosperity of their communities with a commitment to the highest environmental, social and governance (ESG) standards. This includes the Bell Let’s Talk initiative, which promotes Canadian mental health with national awareness and anti-stigma campaigns like Bell Let’s Talk Day, and significant Bell funding of community care and access, research and workplace leadership initiatives throughout the country.

fintechmagazine.com 55 BELL FINANCE

Transformations through Data and Analytics

Beginning their finance transformation journey back in 2019 – Bell Finance saw the potential emerging technologies have to fundamentally transform the way that they work and the services that they provide, discerning that data and analytics (D&A) is core to what they do as a finance function. So fundamental, in fact, that they consider D&A and technology adoption to be a cornerstone of their entire transformation, if not the chief driving force behind it.

If you stop to consider what a finance department or an accounting function actually is, you’ll quickly realise that it begins and ends with data and information – and the packaging up of that information to either produce new insights on performance, help develop business forecasts, or to ultimately provide strategic recommendations and services to the organisation as a whole.

“It's really about being able to develop a leading edge practice by moving away

from a traditionally federated approach, to instead managing data and analytics by channelling it into a centralised team and a centralised system,” says Matthew MacEwen, VP of Finance, and lead of Finance Transformation initiative at Bell, including the Finance Data and Analytics work stream. “This has really helped our finance function to accelerate its transformation and to have a specific focus, ensuring our entire finance community has access to all of the data that they need in order to carry out their day-to-day jobs, and help drive automation of manual processes.”

In 2019, MacEwen was asked by the CFO to help lead their finance transformation initiative, and to help develop their future state roadmap. At that time, the company had started centralising their CoE and MacEwen was – and still is – the leader of that group. In his D&A role, he leads finance transformation, as well as supporting

56 March 2023 BELL FINANCE

EXECUTIVE BIO

Nantes Kirsten

TITLE: DIRECTOR OF FINANCIAL ANALYTICS COE

INDUSTRY: FINANCE

LOCATION: CANADA

Nantes Kirsten leads the Financial Analytics Centre of Excellence (CoE) at Bell, a specialist team of financial data, strategy and automation experts developing solutions that drive efficiency and are enabling transformation within Bell’s Finance organisation. Kirsten’s involvement at Bell started as a management consultant supporting the formulation of the vision and roadmap for Bell Finance’s D&A transformation program.

Before joining Bell, Kirsten held various hands-on and leadership roles within risk and finance divisions, across Telecommunications, Financial Services and Retail industries.

“It's really important that the entire Centre of Excellence is engaged in the transformational vision, and that all those involved share the same beliefs”

BELL FINANCE

NANTES KIRSTEN DIRECTOR OF FINANCIAL ANALYTICS COE, BELL

KPMG in Canada helps telecommunication companies gain a competitive advantage

The sector is undergoing transformation at a rapid pace driven by changing consumer behaviours and new technologies.

Our team offers a forward-looking portfolio of Audit, Tax, Risk, Financial and Strategic Advisory services backed by a global network of skilled industry professionals positioned to help clients anticipate and exceed evolving expectations.

Learn more

KPMG in Canada joins forces with Bell to drive finance transformation

Dan Krausz on how KPMG is one of Bell’s strategic advisors on its finance transformation journey, operating as an integrated team to realize value

As Partner and Telecommunications Sector

Lead at KPMG in Canada, Dan Krausz has played a key role on Bell’s finance transformation journey over the past few years.

Rapid technology innovation in telecommunications

To be successful in the face of huge industry transformation, Krausz explains that one thing is vital: “Telecommunication organizations need access to more data, more frequently, that is well governed. Data is at the core of what finance does, so being able to make informed decisions, fast, is something that finance needs to drive.”

Business-led and technology-enabled finance transformation

By working with Bell on their finance transformation project from the beginning, KPMG has helped shape the related vision and strategy.

“We started out by helping Bell determine what they wanted to achieve and then translated that into a practical roadmap for implementation,” explains Krausz.

An integral aspect of KPMG’s involvement in the transformation is the combined approach of delivering technology outcomes while bringing a business lens to the table, taking a use case approach.

He adds: “There have been several workstreams that we have been involved in. One that I’m most proud of is intelligent forecasting – we were able to develop AI models which use both internal and external data sources to produce forecasts. These not only improved forecast accuracy, but they also continue to learn and become more accurate over time, and drive efficiency into a process which was previously manual in nature. Another use case was for analytical process automation – significantly reducing the number of manual journal entries as part of the financial close process. This also provided additional granularity from a management reporting perspective given the details were maintained in the data warehouse.”

“A common theme throughout this project with Bell has been our collaboration, working shoulder to shoulder to not only deliver transformation outcomes, but to support the enhancement of Bell’s capabilities, helping to ensure that the teams are well equipped to leverage new technologies,” concludes Krausz.

EXECUTIVE BIO

Matthew MacEwen

TITLE: VICE PRESIDENT OF FINANCE TRANSFORMATION

INDUSTRY: FINANCE

LOCATION: CANADA

Matthew MacEwen is the Vice President of Finance, Customer Experience and Corporate Planning, Transformation and Finance Analytics at Bell Canada. In addition to supporting various Business Units in achieving their strategic, operational and financial objectives, Matthew is responsible for executing Bell Canada’s digital transformation for the Finance function. This includes advancing the function’s capabilities with the development and

MATTHEW

MATTHEW

some of their finance operation’s business, including business units from a more financial planning and analysis (FP&A) perspective.

The emerging technologies in question –and central to Bell Finance’s transformation – are, of course, artificial intelligence (AI), the application of machine learning (ML) and predictive analytics within finance processes. These technologies have the potential to provide many organisational benefits, such as providing useful insights to minimise unpredictability, creating sophisticated forecasting capabilities and automating traditionally time-consuming and inefficient processes.

For a finance department, the fiscal knock-on effects of such technologies are able to free up resources that can have a sweeping effect throughout the entire structure of an organisation. This is exactly what Bell finance has set out to do – and they are already seeing the impact of such systems.

Another aspect of this transformation concerns not only technology and data, but also Bell Finance building new capabilities within the actual function, as well as the critical upskilling of their workforce so

MACEWEN VICE PRESIDENT OF FINANCE TRANSFORMATION, BELL

fintechmagazine.com 61 BELL FINANCE

“One of the things that we learned was to take a more agile approach and to work on smaller developments that we iterate on – and then to build out from there – versus trying to do more big-bang developments from the outset”

Assess Your Analytics Maturity

Learn more

that they are able to leverage these new technologies and provide services in more sophisticated forms. The dynamic balance between the transformation of processes and that of people is a delicate and everpresent one. These are not just changes that take their aim at possibilities with the potential to transpire weeks and months into the future, but incremental shifts that have a fundamental effect on the dayto-day workings within the organisation itself, with the potential to transform organisational processes as a whole. The Finance organisation therefore realises that

this transformation starts with people and people engagement.

“It's really important that the entire CoE engages in the transformational vision, and that all those involved share the same beliefs,” establishes Nantes Kirsten, Director of Financial Analytics & AI, Centre of Excellence.

“I realised early on in my career, as a quantitative risk-management consultant –that I enjoyed data science and the ability to translate data into actionable decisions and insights, and that's when I decided to move into telecommunications where there's an abundance of data and untapped insights.

64 March 2023

At Bell, as the Director of Finance and Analytics at the CoE, we are trying to help use data to enable transformation and drive better insights – and there are so many others in the team that share this alignment between what we enjoy and the work we get to do,” he says.

The Financial Analytics CoE is focused on the finance 2025 transformation program data and analytics delivery, seeking to complete its transformation in the next few years; a transformation that will reshape Bell Finance from the bottom up and inevitably evolve the organisation closer to the Finance of the Future.

“I lead the financial data development team,” explains Kirsten, “alongside the solutions development teams that focus on visualisation, reporting automation, and financial data science initiatives like intelligent forecasting; we're currently focused on using the data and technology work-stream within finance 2025 to enable the transformation.”

Asked about the genesis of such a program, MacEwen says: “A program like this starts with leadership support and commitment. We had crucial and very strong support from our senior leadership

MATTHEW MACEWEN VICE PRESIDENT OF FINANCE TRANSFORMATION, BELL

“Beginning with leadership sponsorship, one of the first things we did in the early phases was to focus on people, and to find those within their finance function who had leading-edge skills in some of these technologies and to bring them together, and that really formed the nucleus of our centre of excellence”

fintechmagazine.com 65 BELL FINANCE

team, starting with our CFO all the way through to the actual investment in the Program as well as in bringing people together to provide a different way of working for our finance function.”

Beginning with leadership sponsorship, one of the first things they did in the early phases was to focus on people and to find those within their finance function in possession of leading edge skills in some of these technologies and to bring them together, “and that really formed the nucleus of our centre of excellence”.

“As we gathered those folks, along with some of the work that they were doing, into a single team, we started to build a team vision – and to create a roadmap that we then started to execute as a part of our longer-term strategy.”

The Centre of Excellence’s core capabilities

The CoE acts as the brain as well as the executive centre of the finance transformation’s nervous system at Bell, and there are core capabilities and skills that determine how effective it is in bringing about this transformation.

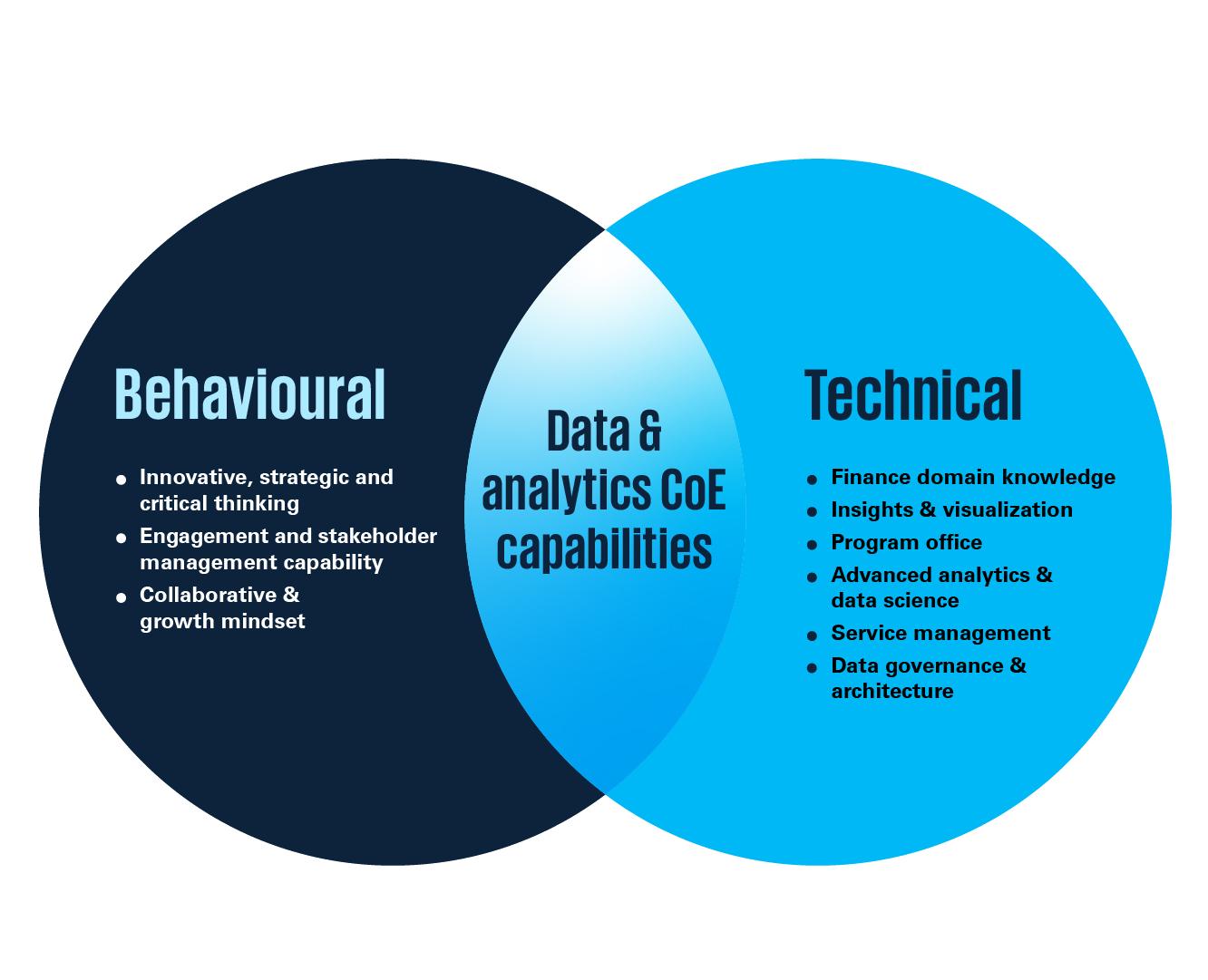

Kirsten proposes that they are categorised broadly in two areas: “There are behavioural capabilities and technical capabilities that are required.”

“On the behavioural side, for any centre of excellence, you need to have an innovative, strategic and critical thinking cap on. It ensures that we keep driving our transformation mandate, but also helps keep our lives interesting. Also on the behavioural side is solid engagement and stakeholder management capability. It's critical that we have a strong stakeholder engagement capability in the CoE so that we continue to keep our finance partners involved, engaged, testing and adopting

the solution, and of course, collaboration is absolutely key.”

“On the technical side (and I don't think this will come as a surprise), you need to have an intimate understanding of the finance organisation. As we're a finance CoE, this is different from what you would see in other enterprises – typically as a Centre of Excellence with an analytics focus. You naturally need the technical Data mining / Wrangling and Visualisation competence, but the solution development is crisper with a good foundational finance understanding.“

66 March 2023 BELL FINANCE

“Finally, it’s important that we are technology agnostic. We should be able to pick up a technology, learn how to code in it, use it, and to make sure that our solutions can be developed in any technology, any coding language and focus more on driving value through the use case, not leading with technology.”

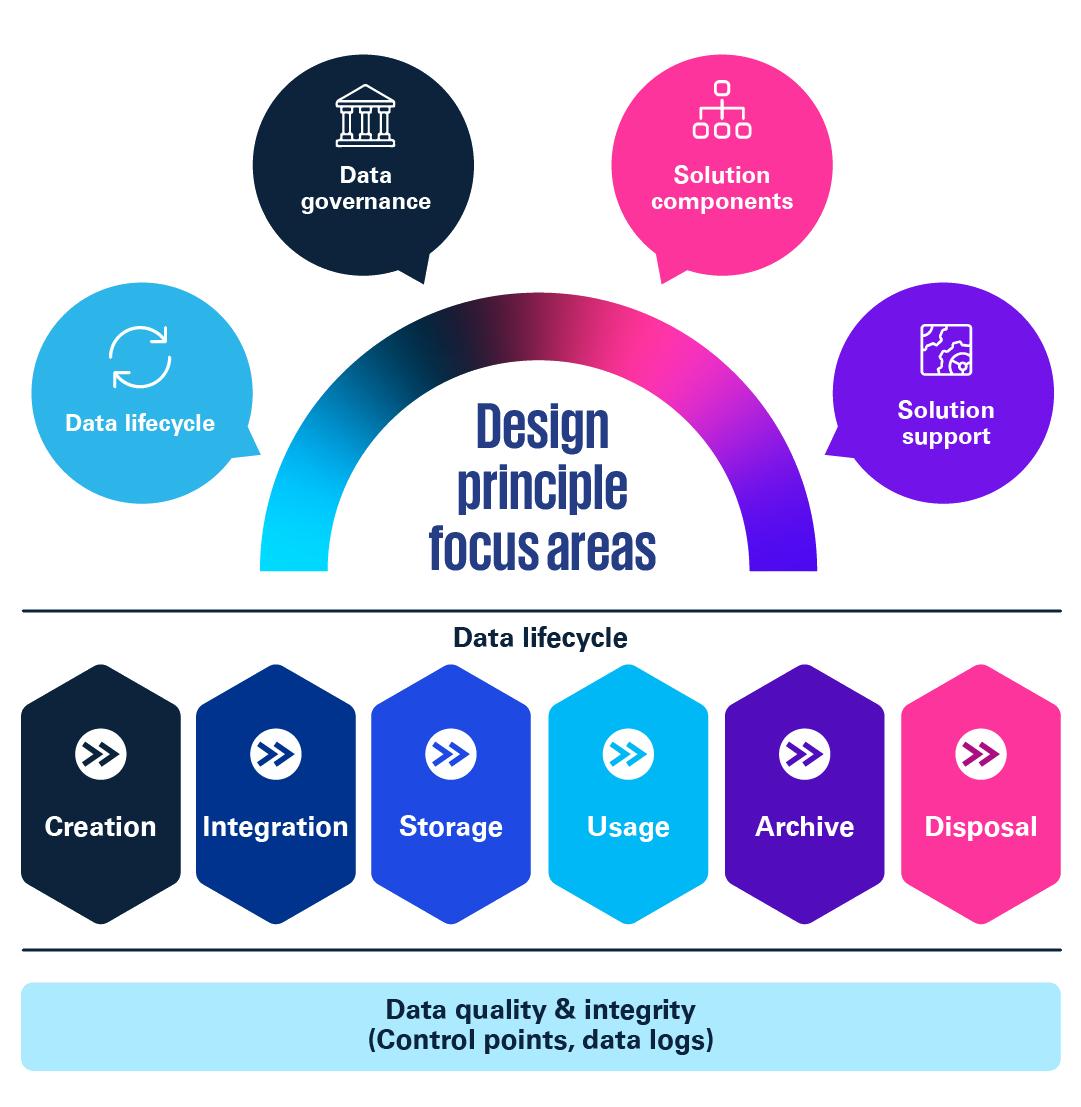

The central data design and architecture principles for the Centre of Excellence In terms of core data design and architecture principles, the Bell Finance CoE began

NANTES KIRSTEN DIRECTOR OF FINANCIAL ANALYTICS COE, BELL

“Pick an impactful use case and find the data that unlocks it”

fintechmagazine.com 67

the transformation journey with a keen understanding that the solution component (that is, the use case) was going to be the driving force at the helm.

“Pick an impactful use case and find the data that unlocks it,” says Kirsten. “And that's one of the principles to which we adhere: find something that’s tangible to our clients and that adds value and then make sure we have centralised data that reconciles with upstream accounting systems that can enable development and automation of that use case.”

The other core aspect that they wanted to retain while reaching their transformation goal was “to develop principles that give us a blueprint, to be able to repeat what we've done”.

The use case would then lead to repeatable principles and processes, (“recipes”) for the Data Development Lifecycle, and then to solid Data Governance around the solutions and lifecycle.

So, in terms of the data lifecycle, Bell Finance wants to make sure that they have core principles in place to answer the data lifecycle questions, for example how they gather requirements, how they develop and how they engage and train their finance users.

“‘How do we start experimenting and have those data lifecycle components at the core of our CoE initiatives?’ – these were all part and parcel of the principles that we needed to put in place. Then there are support considerations, such as the finance support for the end-users, so we needed to make

68 March 2023 BELL FINANCE

sure that we had a process in place for them to ask someone for help. We need our CoE as their first-line of support.

“At the core of all of this is easily accessible, curated and centralised data.” For such a transformation, then, the Centre of Excellence was necessary. This Centre of Excellence then had to be formed with systems in place that would sustain it –so that it could then go about forming the transformational process that would feedback into its own operations, like an organisational form of M.C Escher’s ‘drawing hands’.

Essentially, the point is that the systems in place are open-ended and ever-adaptive to change – a necessary requirement for an effective transformation to take place. But,

of course, such a program is no easy feat, to say the least. As part of the CoE, both MacEwen and Kirsten acknowledge that, early on, one of the challenges that arose stemmed from attempting to tackle too much at once and “biting off more than we could chew”, which they both emphasise.

MacEwen says: “One of the things that we learned was to take a more agile approach and to work on smaller developments that we iterate on – and then to build out from there – versus trying to do more big-bang developments from the outset.”

Kirsten adds: “And you should never underestimate the amount of time testing and training of users will take. The endusers sitting in the finance organisation are so critical to adoption,” – (the crucial user-

fintechmagazine.com 69 BELL FINANCE

Bell for Better—Monika

adoption aspect of the transformation)

– “so you want to make sure that they're bought in and brought in from an early stage and that you allow sufficient time in your program plan for that piece.”

He also underlines that finding the right people – those that are passionate about finance, data and analytics, but also about the vision and practicalities of organisational transformation – is key and that, with such a transformation, “it’s critical to choose the right technology and advisors (internally as well as externally) to ensure that your vision is in-line with best practices in the industry and with best in class companies are doing so that, from a solution development and technology point of view, you're not finding yourself on an island.”

The partner ecosystem

Beyond senior support and the obvious financial investment needed in bringing about such a transformation, partners are invariably vital to such a process.

For their finance transformation, a blend of a strategic-advisory type of partner, as well as technology partners were needed.