ESG Spotlight on Middle East banks’ climate commitments and progress page 20 TECHNOLOGY

AcuityTec boosts payment security with adaptive fraud defence page 12

Cvent offers insight for making your events more accessible page 13

BOOK REVIEW 10 Tips to Help Compliance Officers SOAR! by Simone E Martin page 22

THIS

Staying ahead

The new playbook for scaling challenger banks page 6

Unicorn on the move MNT-Halan on its quest to empower the unbanked page 8

Coins, Cats and Clever Kids

Sunshine+Kittens offers a fresh take on financial education page 10

Improved financial inclusion

myTU on how fintech could boost integration of migrants in Europe page 14

Electric vehicles and payment anxiety Aevi on the hidden roadblock to EV adoption page 15 Dubai’s approach to virtual assets

Spotlight on VARA’s new digital marketing guidelines page 16

Money Fellows’ $100million move

CEO Ahmad Wadi discusses charting a course for international expansion and innovation

Driving open finance forward

The biggest challenges holding back adoption page 18

Friendship meets finance

Cino’s fresh approach to simplifying group payments for Gen Z page 21

BRINGING FINTECH TO THE WORLD

Editorial Enquiries editor@thefintechtimes.com

Editorial Director

Mark Walker

Editor in Chief

Claire Woffenden

Art Director Chris Swales

Features Editor Polly Jean Harrison

Marketing Karen Phiri

Business Development

Deepakk Chandiramani

Stephen McMaugh

Journalists Francis Bignell Tom Bleach

Published by

Rise London, 41 Luke Street, London EC2A 4DP, UK

Leading the digital banking charge

The race is on, and fintechs are surging forward.

Boston Consulting Group’s latest Global Payment Report, Fortune Favours the Bold, makes it clear – banks must evolve or risk being left behind.

Connect with us /fintech-times

This Newspaper was printed using environmental print technology, on 100% recycled paper.

Copyright: The Fintech Times 2024. Reproduction of the contents in any manner is not permitted without the publisher’s prior consent. ‘The Fintech Times’ and ‘Fintech Times’ are registered UK trademarks of Disrupts Media Limited.

With fintechs blazing a trail in the payments sector, banks now need to look beyond their comfort zones and aim to capture at least 50 per cent of new growth from areas outside their core business.

The report highlights the urgency for innovation, projecting that global payments revenue growth will halve by 2028, with annual growth rates dropping from nine per cent to just five per cent. North America and Europe, in particular, are set for the sharpest slowdowns, with projected growth of only three per cent each year.

The findings also show a shift in investor priorities: 33 per cent of the payments industry’s investor base is now value-focused, up from 26 per cent in 2021. As fintechs outpace traditional players, technological modernisation has become essential to keep up with the rapidly changing payments infrastructure.

In this issue, we spotlight how challenger banks are responding to these pressures. These digital-first

players are adapting through strategic partnerships, innovative technologies and a customer-centric approach, all essential for scaling sustainably.

From tackling new regulatory requirements to expanding their service offerings, we delve into the strategies helping challenger banks maintain their competitive edge.

We also explore the rise of open finance, which, while promising, has seen slower adoption than

From tackling new regulatory requirements to expanding their service offerings, we delve into the strategies helping challenger banks maintain their competitive edge expected. Aimed at fostering a more connected financial ecosystem by sharing a broader scope of financial data, open finance faces significant hurdles, such as privacy concerns and the need for robust regulatory frameworks. Our experts weigh in on what it will take for open

finance to reach its full potential and how the industry can overcome these barriers.

Additionally, we bring you an inside look at Sunshine+Kittens, the new kids’ money app blending gamified learning with financial literacy and reveal how MTN-Halan is on a mission to transform mobile money solutions across emerging markets.

We also delve into how myTu is using fintech to address the banking needs of migrants. By providing essential banking services tailored for individuals navigating new financial landscapes, myTu aims to bridge gaps in access to accounts, remittances and savings tools.

As we move into the final stretch of the year, it’s the perfect time for reflection and forward planning. Over the coming weeks, we will be taking stock of what’s been achieved and consider the road ahead.

We invite industry leaders and innovators to share their key takeaways from 2024 and their predictions for the fintech landscape in 2025.

Claire Woffenden,

editor in chief, The Fintech Times

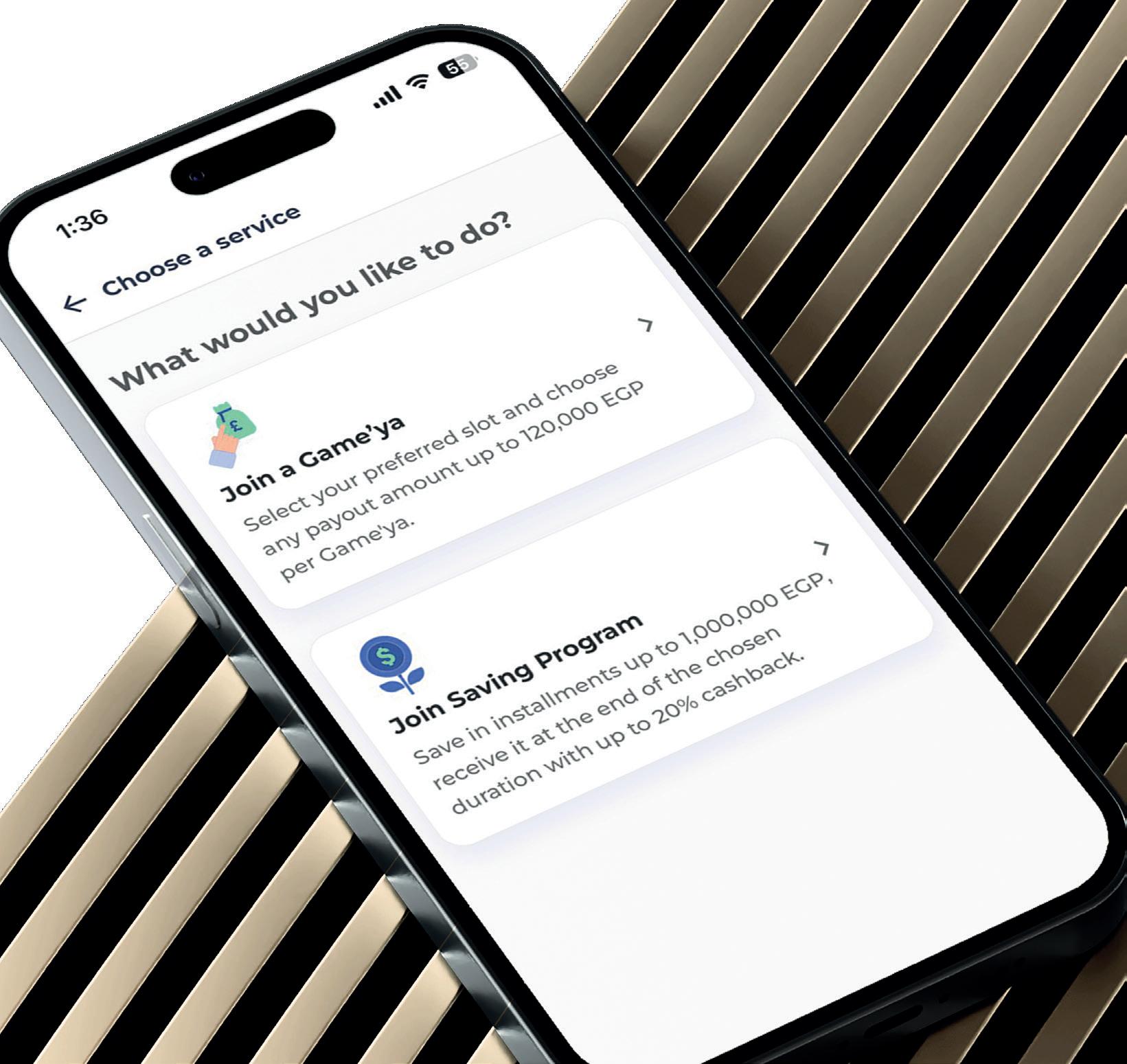

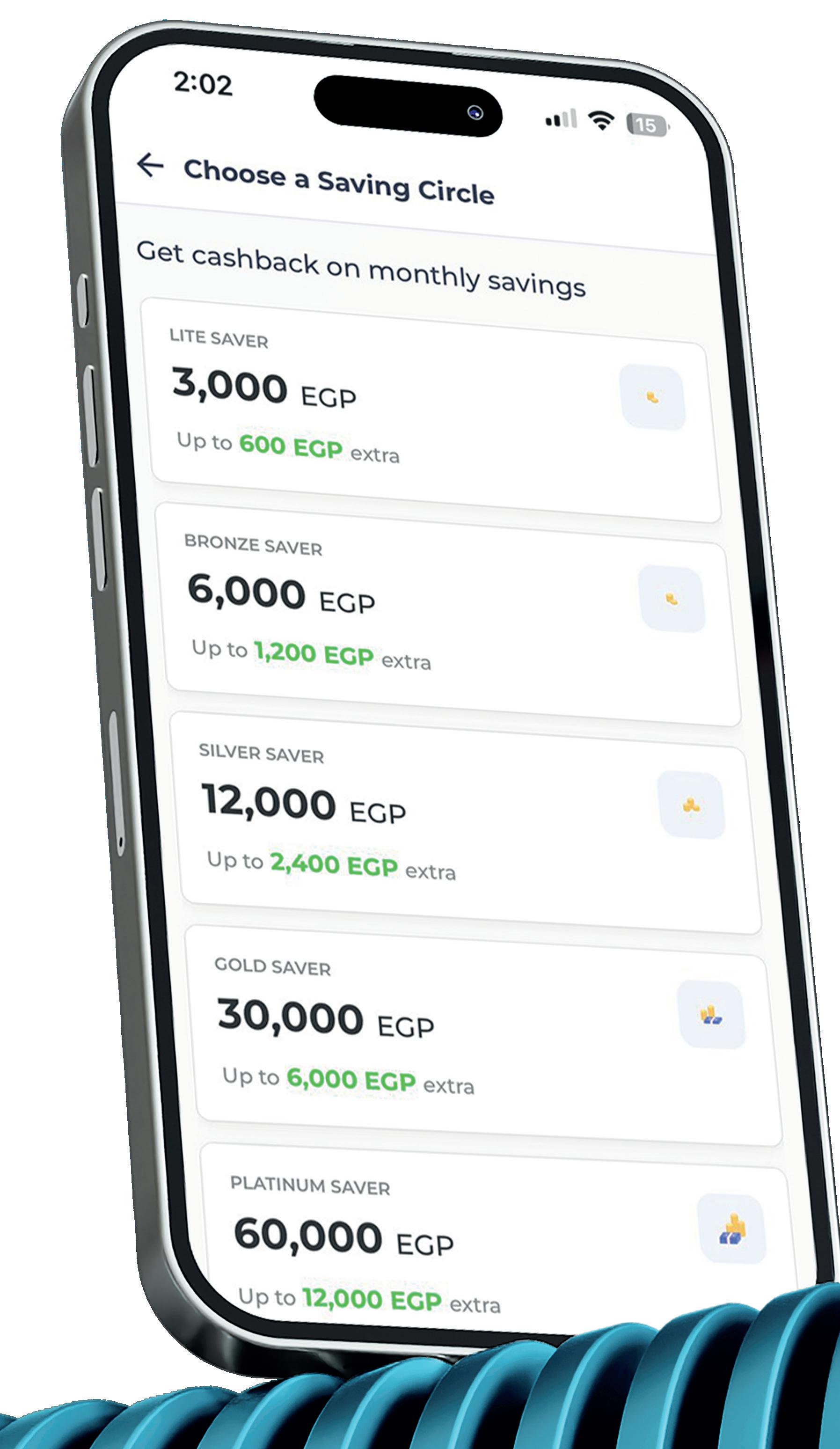

MONEY FELLOWS’ $100MILLION MOVE

Ahmad Wadi , CEO of Money Fellows discusses charting a course for international expansion and innovation

Money Fellows, the Egypt-based fintech, is preparing for a pivotal Series C funding round, targeting $80-100million to fuel its next phase of growth. Since its launch in 2017, the company has focused on bridging financial inclusion gaps through the digitisation of traditional savings and credit practices. With profitability now secured and new products in the pipeline, Money Fellows is poised to scale rapidly both within Egypt and in new international markets.

“As we look ahead to the coming year, I’m incredibly excited about the milestones we’re set to achieve. We have a prepaid card launch in the works, and we’re proud to be graduating from the Central Bank of Egypt’s regulatory sandbox, both of which are key steps in our growth,” says Ahmed Wadi (above), founder and CEO of Money Fellows.

FROM TRADITION TO DIGITAL TRANSFORMATION

Since its inception, Money Fellows has championed financial inclusion by digitising rotating savings and credit associations (ROSCAs). This traditional system, where participants contribute to a collective pot and receive the sum in turns, has been modernised by the fintech to offer better rates, accessibility and security.

By bringing this model online, Money Fellows offers more security, transparency, and convenience, especially to underbanked populations.

“We’re offering lending, saving, and planning at much better rates and incentives,” explains Wadi. The platform has modernised a long-trusted system, enabling users to seamlessly manage their finances while maintaining the collaborative spirit of traditional ROSCAs.

REGULATORY MILESTONE: ENTERING THE CBE SANDBOX

In 2023, Money Fellows entered the Central Bank of Egypt’s (CBE) Regulatory Sandbox, a critical step in testing and refining their digitised ROSCA model. As the first fintech to bring this model into the sandbox, the company has contributed to the development of regulations that will shape how similar fintech innovations are governed in the future. This milestone is key to ensuring that the ROSCA model operates within a secure and regulated environment, helping pave the way for other fintechs in Egypt.

Graduating from the sandbox marks a significant achievement for the company, positioning it for further growth while ensuring compliance with local regulations.

SERIES C: A STRATEGIC INFLECTION POINT

Money Fellows’ upcoming Series C funding will be crucial in driving its next phase of growth. The company has already raised over $45million in previous rounds, led by investors such as CommerzVentures, Middle East Venture Partners (MEVP), and Arzan Venture Capital. Now, the new $80-100million injection will enable Money Fellows to rapidly scale its operations, expand its

product range, and accelerate its international expansion.

“This round will enable us to scale rapidly and expand our diverse financial product offerings across both B2C and B2B segments,” Wadi says.

NEW PRODUCTS AND TECHNOLOGY

As part of its expansion, Money Fellows is set to launch a prepaid card in the fourth quarter of 2024. This card will provide users with a convenient and secure way to manage their funds, allowing flexible access to their savings and seamless everyday transactions. Notably, this will be the only prepaid card in the market that enables users to access funds and top up through their participation in Money Fellows’ circles, acting as a gateway to financial services without the need for a traditional bank account.

Looking further down the roadmap, Money Fellows is also planning to introduce an Investment Solution that will enable users to

regulatory sandbox also allows fintech firms to test new solutions in a controlled environment before fully rolling them out, ensuring compliance with regulatory standards. “Graduating from the sandbox ensures the fulfilment of one of our primary strategic milestones, vis-à-vis regulations,” Wadi explains.

EXPANSION PLANS: ENTERING NEW MARKETS

With Egypt serving as the company’s launchpad, Money Fellows is now setting its sights on regional and international markets. The upcoming Series C funding will play a crucial role in enabling the fintech to develop localised solutions tailored to the specific needs of each region it enters. “We’re focused on creating solutions that resonate with local markets,” says Wadi.

Among the markets being explored for expansion in 2025 are Saudi Arabia (KSA) and Morocco, both of which represent significant

GRADUATING FROM THE SANDBOX MARKS A SIGNIFICANT ACHIEVEMENT FOR THE COMPANY, POSITIONING IT FOR FURTHER GROWTH WHILE ENSURING COMPLIANCE WITH LOCAL REGULATIONS

diversify their savings into various portfolios. This future offering will provide tailored investment options, helping users grow their savings and achieve long-term financial goals. The company will also increase its investment in artificial intelligence (AI) and data analytics. These technologies will help Money Fellows enhance user experience, improve operational efficiency, and ensure robust security measures as it scales. “We will continue to invest in cutting-edge technology like AI and data analytics to improve the user experience while also focusing on security and regulatory compliance,” Wadi adds. Graduating from the Central Bank of Egypt’s

opportunities for Money Fellows to expand its financial inclusion model. This regional push will be complemented by strategic partnerships with local financial institutions and fintech platforms, allowing Money Fellows to integrate efficiently into these new cosystems.

The company’s goal is to broaden its impact by offering financial inclusion to a diverse range of users, adapting its services to meet various needs, whether for leisure or essential purposes. Positioned as an alternative financial solution, Money Fellows aims to cater to people from all walks of life. For example,

some users participate in Money Fellows’ circles to save for upcoming holidays or travel plans, showcasing the platform’s versatility.

By expanding its reach, Money Fellows seeks to establish a stronger foothold in the MENA region, helping more users access financial services tailored to their unique goals.

PROFITABILITY AND LONG-TERM SUSTAINABILITY

A key milestone for Money Fellows has been reaching business profitability. “We’ve recently reached the significant milestone of achieving business profitability – something we’ve long aimed for,” Wadi shares. This achievement enables the company to reinvest in its growth and focus on scaling its operations.

With profitability secured, the Series C funding will be directed toward further expansion and innovation. “Moving forward, any external capital we raise will be focused on fuelling our international expansion, driving us closer to becoming a global leader in the fintech space,” Wadi asserts.

Money Fellows’ growth strategy centres on product innovation, market expansion, and maintaining regulatory compliance. By reinvesting profits, the company is well-positioned to expand its offerings and customer base.

STRATEGIC PARTNERSHIPS AND ECOSYSTEM GROWTH

Part of Money Fellows’ expansion strategy involves fostering partnerships with financial institutions and fintech platforms in new regions. These partnerships will allow the company to quickly establish itself in emerging markets and access the regulatory and technological infrastructure necessary for growth.

“Partnerships will fuel the development of localised solutions tailored to new regions,” Wadi explains. By collaborating with local financial institutions, Money Fellows can offer products and services that are adapted to regional needs, while also ensuring compliance with local regulations. This ecosystem-driven approach will play a key role in the company’s ability to scale effectively.

LOOKING AHEAD

Money Fellows is entering an exciting new phase as it prepares for its Series C funding and international expansion.

“As we look ahead to the coming year, I’m incredibly excited about the milestones we’re set to achieve,” says Wadi. With a strong foundation in place, the fintech is ready to accelerate its growth, both in Egypt and globally.

Staying ahead: The new playbook for scaling challenger banks

From streamlining operations to enhancing customer experience, challenger banks are revising strategies to balance growth and competition.

Challenger banks have come a long way since their early days of disrupting the financial sector. Now, as they reach new levels of maturity, they face the challenge of scaling up without losing their competitive edge.

To understand how these banks are navigating this evolution, we spoke with industry experts who reveal the key strategic adjustments helping them stay ahead.

Nida Sattar, product director for payments at business challenger bank Allica Bank

“As more established challenger banks like Allica continue to grow, staying competitive means speed of execution is always top of mind. This means keeping laser focus on a few key areas: hiring the right talent, streamlining processes to avoid bottlenecks as we scale, and quite often, making quick decisions on forming strategic partnerships that help us meet our objectives faster. The industry and market move fast, and agility is key.

“One of the biggest advantages challenger banks have is their nimble architecture, which allows them to adapt quickly to market changes. They can use real-time data to respond to customer needs and new opportunities faster than

traditional banks. By staying nimble and teaming up with the right partners, players like Allica can build innovative products and solutions and ship these to market quicker, whilst growing.”

Benjamin Humphrey, CEO and founder of consumer insights and user research platform Dovetail “Challenger banks are stepping up by putting customer understanding at the heart of everything they do. They’re not just ticking boxes – they’re building products that people actually want, and that’s what gives them a real edge in such a competitive space. With AI and innovation in their toolkit, these banks are staying ahead of the curve. We’re seeing AI chatbots take on a bigger role, cutting down the need for phone calls and giving customers the quick answers they expect. Behind the scenes, AI is just as crucial – helping teams analyse feedback in real-time, spot trends, and share insights across the business so they can pivot fast on product and strategy.

“A recent survey from Plaid showed that 60 per cent of consumers believe AI will reshape financial services in the next five years. AI isn’t just a buzzword – it’s poised to help lower costs, sort out customer issues, give advice on budgeting, manage subscriptions, and deliver personalised financial guidance. It’s all about automation and personalisation – that’s where the future of finance is heading.”

George Donchenko, country manager at Viva Money, a digital lending platform operating in India “The main challenge

they face in closing the scaling gap is access to low-cost funding. To overcome this, they typically establish partnerships with commercial banks or acquire stakes in other institutions to gain access to retail and corporate deposits, which are significantly cheaper than

raising funds in the open market. In other areas, such as technology, customer experience, and customer service, these challengers are generally ahead of traditional commercial banks and therefore do not need to catch up with the more established institutions.”

Sarah Carver, head of retail banking, wealth and insurance at financial services business Delta Capita

“With a more challenging funding environment in recent years, there has been a growing emphasis on profitable scaling, with notable examples like Starling Bank and Revolut leading the way with sustainable pricing models while scaling. Additionally, we have seen a steady expansion in the breadth of services from challengers, whether through new product offerings or strategic partnerships.

“While profitability and a competitive service offering remain key, trust is becoming increasingly critical. There has been a rise in cyber and ransomware attacks on

“However, challengers have not forgotten their initial unique selling point – a laser focus on customer experience. They continue to invest in their mobile apps, with Monzo and Starling consistently topping the charts for customer satisfaction and intuitive app design.”

Tom Kiddle, co -founder of Palisade, a digital asset custodian backed by Ripple

“Established challenger banks are increasingly exploring the integration of blockchain/Web3 technology into their offerings to stay competitive and respond to the growing demand for digital assets. For example, challenger banks Revolut and N26 both offer cryptocurrency trading

products, challenger banks could make significant inroads in the near future. Web3 technology will serve as the invisible backend for many of these institutions, helping to optimise their stack – including reducing fees and improving settlement times. Fintechs not factoring in Web3 technology will become the ‘Blockbusters’ of the financial industry a few years from now.”

Serena Smith, chief client officer at i2c , which offers a card issuing, digital banking and payment processing platform

“Established challenger banks are continuously refining their strategies to scale while staying competitive in an evolving market.

challenger banks and the broader financial services industry. Although this may not become a direct customer differentiator, challenger banks have increasingly come under the scrutiny of the FCA, meaning regulatory compliance and security will remain essential as they grow.

and custody. We are also seeing the rise of new crypto products, such as crypto-backed loans, crypto-based credit cards and stablecoins pegged to fiat currencies.

“Although crypto-fintechs and major financial institutions currently dominate the market for these

themselves from traditional banks. i2c Inc. supports challenger banks in this endeavour by offering scalable payment processing solutions that adapt to evolving customer needs. As challengers grow, maintaining agility and customer-centricity remains key to their long-term success.”

Shilpa Doreswamy, sector director of retail banking solutions at GFT, a digital transformation specialist catering to financial institutions

“The lines are blurring between challenger banks and incumbent banks, with both entering the next phase of digital evolution. There are shared challenges as they vie for market share, customer acquisition, customer retention and revenue growth, in a market that is increasingly becoming more demanding and informed. The next phase of evolution for challenger banks will likely be to:

Challenger banks have come a long way since their early days of disrupting the financial sector. Now, as they reach new levels of maturity, they face the challenge of scaling up without losing their competitive edge

1

Build trust through purposedriven banking: There is an ever-increasing expectation from banks to be sensitive and conscious about communities, climate, and societal issues.

2Address whitespaces through vertical neobanks: Identifying whitespaces within customer demographics and becoming relevant to specific sub-segments in certain areas is gaining more traction.

3

They focus on expanding their product offerings, entering new markets, and leveraging partnerships with fintechs to enhance their service portfolio. Many are also investing in innovative technologies like AI and blockchain to differentiate

Profitably accelerating into the digital-first world: Digital-first banks such as Monzo, Starling and Revolut are beginning to see increasing revenues and profit realisation. As banks accelerate into the digital-first world, aspects such as Total Cost Ownership (TCO) and speed-to-market become critical, with a focus on profitability.”

UNICORN ON THE MOVE

Mounir Nakhla , Founder and CEO of MNT-Halan on its quest to empower the unbanked across the Middle East

MNT-Halan, recognised as Egypt’s first fintech unicorn, is extending its reach to unbanked and underbanked populations by integrating microlending, consumer finance, digital wallets, card services and payments within a single app.

Based in Cairo, the company’s approach centres on using its proprietary API First Core Banking platform to provide accessible financial services to underserved communities.

Now the seventh-largest financial institution in Egypt, MNT-Halan holds over 25 per cent of the country’s microfinance market. The company reports more than 1.8 million active users per quarter and has issued over $4.4billion in loans, growing its loan book to over $750million – surpassing the personal loan portfolios of the majority of Egyptian banks.

In recent months, MNT-Halan has pursued expansion into the Middle East. In March, it acquired Pakistan’s Advans microfinance bank, and in August, it took over Turkey’s largest nonbank microleasing company, Tam Finans.

These acquisitions follow a $157.5million fundraising round in July, supported by international investors like IFC and DPI. To date, the company has raised a total of over $722million, enabling it to expand its footprint and further develop its services.

We sat down with Mounir Nakhla, CEO of MNT-Halan, to delve deeper into the company’s rapid growth and plans for expanding financial access across the Middle East and Africa.

THE FINTECH TIMES: What inspired MNT-Halan to build a superapp?

MOUNIR NAKHLA: I’ve had a longstanding interest in providing financial services to people and the owners of small businesses that are financially underserved. I believe it is a great tool to empower and improve their lives. Since 2010, I have established multiple successful ventures to that end, but they were mostly brick and mortar businesses. After visiting Gojek in

Jakarta in 2017, I was determined to establish a tech company and launch similar services in Egypt. Soon afterwards, Ahmed Mohsen and I established Halan, mimicking our Indonesian counterpart. In 2019, we pivoted and aborted the ride hailing business and doubled down on becoming the region’s leading financial super app providing frictionless access to financial services, payments, a card, an investment platform as well an e-commerce platform, and a game. As a result, we dramatically improved our unit economics. This strategic shift wouldn’t have been possible had we not spent 18 months developing our proprietary core banking software. Today, we are emerging to become one of the largest financial institutions in Egypt and Turkey in terms of the number of customers. We have served more than seven million customers and together, we have disbursed north of $10billion. We have also launched our activities in Pakistan and the UAE and are exploring other regional and African markets.

we enable users to manage their financial lives more effectively. Our design ensures that we’re not just delivering convenience but also tailored solutions that reflect the specific needs of our diverse user base.

TFT: Following your recent expansions into Pakistan and Turkey, how do you assess which markets to enter next?

MN: We look for markets that have large financially underserved populations. In 2024, this is still quite common, giving us many options. In most countries, banks do not bother with small-ticket loans, and credit card penetration is low.

When assessing markets, we consider factors such as population size, GDP and growth, household debt-to-GDP ratios, small business loan and credit card penetration, unit economics, competitive landscape, and national tech infrastructure, including credit bureaus and e-KYC systems.

Our strategy is to grow through M&A since credit is a local business and licensing takes a long time.

Our ability to scale quickly through technology, paired with our on-the-ground presence in communities, ensures we reach underserved populations effectively. By fostering partnerships and utilising data-driven decision-making, we ensure sustainable growth and remain a step ahead of the market

TFT: How do you balance the needs of such a diverse, underserved user base?

MN: We keep our users at the centre of everything we do and develop products and services that best solve their problems. To do that effectively, we rely on data to guide our decisions. By segmenting and profiling our users, we gain a deep understanding of their behaviours and needs. Our technology continuously evolves based on insights drawn from this data, ensuring that we can address the unique challenges of our underserved user base.

By bundling micro-lending, payments, e-commerce, and consumer finance into one app,

TFT: How has your API First Core Banking software transformed the way you deliver financial services, and what’s its biggest advantage over traditional banks?

MN: Neuron, our proprietary API First Core Banking system, has revolutionised how we deliver financial services by providing a scalable, secure, and flexible backbone for all our digital products. Traditional banks rely on legacy systems that can be slow to adapt and costly to maintain, whereas Neuron allows for seamless integration of new services and rapid adjustments based on customer feedback. Its ability to manage millions of customers and multiple

currencies, combined with high availability, offers a frictionless experience, driving engagement and financial inclusion across Egypt and now into international markets.

TFT: With MNT-Halan’s rapid growth, what strategies are in place to stay ahead in Egypt’s competitive microfinance sector?

MN: There are tens of players and yet we maintain a market share that is north of 25%. Our strategy to keep this leadership position is to maintain a deep connection with our customers, we offer them other services that are important to them and give them a fantastic experience. We have realised that the more services our customers use with us the less likely they are to churn and therefore, contribute to the lifetime value.

Our ability to scale quickly through technology, paired with our on-the-ground presence in communities, ensures we reach underserved populations effectively. By fostering partnerships and utilising data-driven decision-making, we ensure sustainable growth and remain a step ahead of the market.

TFT: How are you planning to utilise your latest $157.5million fundraise, and how do international investors shape your vision? MN: This fundraise enabled us to close the acquisitions in Turkey and Pakistan, grow our GCC business and invest more in technology. It is also helping us to scale our operations in different markets. Our international investors have added tremendous value in evaluating our strategy and refining our business model. They often have very interesting insights through their experience in similar countries and companies.

TFT: What initiatives is MNT-Halan undertaking to drive financial literacy and long-term financial inclusion across the region? MN: We are deeply committed

to increasing financial literacy through both on-the-ground initiatives and digital education campaigns. Our team works directly with underserved communities to teach individuals how to manage finances, use digital wallets, and access loans responsibly. Additionally, through our partnerships with organisations like UN Women and DEG, we actively promote women’s economic empowerment, providing them with the financial tools and education to take control of their own and their families’ financial futures. Our efforts aim not just to provide access but to foster long-term financial independence.

Mounir Nakhla (right), founder and CEO of MNT-Halan with Ahmed Mohsen, chief technology officer (left)

COINS, CATS & CLEVER KIDS

Sunshine+Kittens, the latest kids’ finance app, has launched with a different take on financial education, blending learning and play with backing from major industry names

Aiming to bring a fresh perspective to youth finance, Sunshine+Kittens introduces children to money management through an interactive, game-like experience. While many financial tools for young users focus on practical basics, this app sets out to infuse these lessons with a playful twist.

The Fintech Times chats with Charles O’Neil (above), co-founder of the app, to uncover the vision, approach and partnerships

behind the app’s pounce into the world of youth finance.

BRIDGING A FINANCIAL LITERACY GAP

O’Neil’s journey to Sunshine+Kittens began with a simple observation: traditional financial education tools often miss the mark with kids. He recalls searching for a banking solution for his daughter, only to find options that felt uninspired.

“I was working for a large investment bank at the time, and I

knew finance can be a dry subject. Like most parents, I am aware of how important it is for kids to learn financial literacy. I also know that they aren’t learning it at school, to the point that most young adults would fail a simple financial literacy test. I looked at the high street banks and the incumbent brands that supposedly teach kids about money and all I could think was – how dull. These guys understand money… but don’t get kids,” he said. In response, O’Neil teamed up with long-time friend and creative partner

Paul Jason. They wanted to create a product that didn’t just teach financial basics, but did so in a way that children would naturally gravitate towards.

“We’d been toying with the idea of a fintech product for a while and had been lamenting the poor state of financial literacy tools,” O’Neil shares. “We share a similar worldview and belief that creativity can connect with people and change behaviour.”

Their combined experience in advertising and creative industries shaped the app’s unique, character-driven approach, while the name Sunshine+Kittens reflects this philosophy, combining two things O’Neil’s son had once described as his favourite: sunshine and kittens.

“The penny finally dropped when my son, aged six, made an ode to his babysitter, describing her as ‘the perfect blend of Sunshine and Kittens,’ he shares. This playful sentiment helped shape the app’s identity, aiming to make learning about money feel fun and natural.

GAMIFYING FINANCIAL LEARNING

Sunshine+Kittens, aimed at kids aged six to 18, is built around the idea of gamification, which uses game-like elements such as rewards and challenges to engage users. But the app aims to go beyond surface-level gamification.

O’Neil is quick to differentiate their approach from simpler tools on the market: “This isn’t black text on a white background with some multiple-choice questions at the end, then labelled as gamified. This is an immersive experience for both parents and kids to engage with, delivered with exceptional creativity.”

The app introduces financial concepts through tasks that feel like games, blending educational content with activities children find familiar and fun. The goal is to make concepts like saving, budgeting and spending as natural as playtime, offering a fresh take on how financial literacy can be delivered. With a user-centric ethos and creative design, the Sunshine+Kittens team combines talent from Disney, Star Wars and Universal. Co-founders O’Neil and Jason have been joined by big industry players such as renowned designer Jake Lunt Davies, the creator of the iconic BB8 Star Wars character, and David Arnold, one of the world’s top film composers.

TACKLING FINANCIAL HABITS

Sunshine+Kittens is launching at a time when young people are increasingly exposed to financial products without fully understanding their implications. O’Neil specifically calls out the rise of buy now, pay later (BNPL) services, which, while convenient, can lead to significant debt accumulation.

“Most of the concerns surrounding BNPL, and the debt issues this generation face, stem from the fact kids and young adults don’t realise the longer-term consequences of their actions. A couple of quick clicks and they start accumulating debts that they may be living under for years.”

The app aims to address these challenges by teaching kids about responsible spending and debt management in a format they’ll want to engage with. By integrating these lessons into everyday activities, Sunshine+Kittens hopes to give children the tools to navigate the complexities of personal finance as they grow.

“We need to educate young people on the dangers of these

“WE CAN’T SAY TOO MUCH AS WE’RE BUSY DEVELOPING, BUT LET’S JUST SAY – WE’RE DESIGNING THIS FOR KIDS, TO FIT INTO THEIR LIVES, USING VISUAL LANGUAGE AND TECHNOLOGY THEY ALREADY LOVE AND UNDERSTAND. IT

types of services. The difference between good debt and bad debt. But we can’t lecture them. We need to do it in a fun and joyous manner. To educate them in a way that they don’t feel like they are being ‘taught’. Otherwise, they will simply tune out.”

A STRONG SUPPORT SYSTEM

To bring this vision to life, Sunshine+Kittens has partnered with The PayFirm and SaaScada. These collaborations allow the app to leverage financial technology without needing to build everything in-house. The PayFirm provides a secure payments platform, while SaaScada offers data-driven insights that help the app personalise the user experience.

O’Neil highlights the benefits of these partnerships, explaining that they provide the necessary infrastructure to scale quickly and adapt as needed. “The Payfirm and SaaScada are next generation EMI and core banking platforms respectively. They offer us a turnkey solution to bring in the latest, relevant innovations in a plug’n’play manner. They give us the ability to bring our product to market quickly and then pivot when necessary.”

By integrating real-time transaction data, the app can offer personalised insights that

reflect each user’s habits, helping them learn in a way that feels intuitive.

MASTERCARD’S ROLE IN REACHING YOUNG AUDIENCES

Sunshine+Kittens has also garnered the interest of Mastercard, which has long supported initiatives in youth financial education. While Mastercard is featured as a key partner, details on their exact role have yet to be detailed, O’Neil comments: “Mastercard had been looking for a youth product for a while. When we approached them and showed them Sunshine+Kittens, they got very excited.”

LOOKING AHEAD

As Sunshine+Kittens prepares to launch, the team’s focus remains on delivering an app that blends learning with play in a way that resonates with children.

“Money is becoming increasingly digital and abstract, and the old mechanism for learning about it (i.e., cash) is disappearing. Without getting into specifics – as this is our secret sauce – we are taking the learning from mobile free-to-play games and from Web3.0 reward mechanisms and designing them into an educational experience.

“We can’t say too much as we’re busy developing, but let’s just say – we’re designing this for kids, to fit into their lives, using visual language and technology they already love and understand. It will be totally unlike anything else in the market.”

GET A HOLD OF YOUR FRAUD

Revolutionising payment security with adaptive fraud defence and perpetual KYC

As the global digital payments landscape expands, with projections to reach $16.59trillion by 2028 at a CAGR of 9.52 per cent, the need for robust fraud prevention has never been greater.

AcuityTec addresses these growing threats by providing advanced payment verifications and fraud prevention solutions. Leveraging KYC data and technologies like machine learning, real-time transactional monitoring, and perpetual KYC (pKYC), AcuityTec empowers businesses to stay ahead of emerging fraud schemes while ensuring secure, seamless transactions without compromising user experience.

NEXT-GEN KYC AND CREDIT CARD TRANSACTIONAL VERIFICATION

Central to AcuityTec’s innovative suite of products is CardTrust, a groundbreaking solution designed to simplify and enhance KYC verification at the point of card transactions. Built to reduce the friction and cost associated with traditional KYC processes, CardTrust leverages minimal customer data to verify transactions instantly. By cross-referencing the BIN (Bank Identification Number), the last four digits of the card, and a ZIP code with issuer bank records and customer KYC data, CardTrust ensures real-time verification with zero customer friction. In addition to validating the transaction, CardTrust runs comprehensive name, address and phone ID verification checks, significantly enhancing the security of each payment. Furthermore, it allows clients to customise the process by integrating additional KYC or authentication verifications from AcuityTec’s extensive data hub, tailoring the solution to meet specific business needs.

As Alfredo Solis, managing director of AcuityTec, explains: “CardTrust provides a real-time defence layer, leveraging bank issuer data and adaptive intelligence to mitigate fraud without disrupting payment flows.” This balance of speed and security is crucial in today’s fastpaced financial landscape.

ADAPTIVE FRAUD DEFENCE: REAL-TIME PROTECTION

AcuityTec’s Adaptive Fraud Defence system offers businesses powerful

real-time fraud prevention to combat fraudsters’ growing sophistication. By leveraging machine learning, the system constantly analyses transactional data, identifying suspicious behaviours and emerging fraud patterns. This proactive approach ensures businesses can prevent fraud before it escalates into chargebacks or losses.

The system builds detailed customer profiles based on historical data, payment methods, and behavioural trends. Any deviations trigger risk-based workflows, enabling automatic transaction pauses or additional verification requests. This dynamic approach ensures legitimate customers enjoy a seamless experience while potential fraud is intercepted.

AcuityTec’s adaptive fraud defence stands out for its unparalleled flexibility. Businesses can fine-tune workflows and configure risk rules to address regional regulations, customer profiles, industry sectors, and transaction behaviors. This modular approach ensures each deployment is optimised for security and operational efficiency, delivering a tailored solution that

adapts dynamically to unique fraud patterns and compliance needs.

Furthermore, businesses receive a comprehensive 360-degree view of transactions and customers with real-time monitoring with multiple data streams across every interaction point. The platform operates with continuous analysis of data and behaviours to detect and flag even the slightest anomalies and suspicious activity, enabling immediate response and mitigation. By leveraging advanced algorithms and machine learning, businesses gain deeper insights into fraud trends, allowing for proactive defence while building a more accurate and nuanced understanding of customer behaviour.

“Our platform customisation enables companies to fine-tune their risk management strategies, ensuring robust protection and seamless transaction flows across channels,” adds Solis.

PERPETUAL KYC: COMBAT AI-DRIVEN FRAUD

As regulatory landscapes shift and fraud techniques like deep fakes and AI-generated fraud evolve,

traditional KYC processes struggle to keep up in high-stakes payment environments. Perpetual KYC (pKYC) addresses these challenges by continuously verifying identities and updating customer profiles, ensuring businesses always have the most accurate data.

Periodic KYC reviews can leave gaps that expose businesses to fraud. AcuityTec’s solutions integrate pKYC, biometrics, authentication data, document verification, and machine learning, all powered by a risk engine with thousands of parameters and customisable thresholds.

“Our pKYC approach provides ongoing protection by continuously verifying customer KYC data, authentication data, document verification, and machine learning, all powered by a risk engine with thousands of parameters and customisable thresholds. From onboarding to transaction security and solutions like CardTrust, pKYC, ensures seamless identity proofing and fortifies businesses against emerging local and global fraud threats while staying agile with evolving regulations,” Solis adds.

SETTING THE BENCHMARK

AcuityTec is not merely responding to the evolving demands of fraud prevention; it’s defining the future of secure transactions. With the launch of CardTrust and the integration of advanced solutions like Adaptive Fraud Defence, Transactional Monitoring, and Perpetual KYC, AcuityTec equips payment operators with the cutting-edge tools necessary to outpace emerging threats. By streamlining fraud detection processes and automating critical KYC verifications, AcuityTec enables businesses to optimise operational efficiency without sacrificing security.

AcuityTec ensures that businesses remain resilient, agile, and prepared to meet the most complex fraud challenges head-on in an industry where performance, security, and compliance are non-negotiable. “Whether you’re looking to elevate your transactional monitoring or integrate advanced identity verification solutions, AcuityTec’s platform seamlessly scales with your business needs,” concludes Solis. www.acuitytec.com

Event technology specialist

Cvent offers insight and advice for making your events more accessible and inclusive for all

TRANSFORMING EVENTS THROUGH ACCESSIBILITY

Accessibility and inclusion have always been important, but with rising numbers of people living with a disability, it is now, more than ever, a fundamental part of your event planning.

Some 16 per cent of people worldwide have a disability, according to the World Health Organisation. Across the EU, this rises to one in four adults; in the UK, it’s around 24 per cent of the population (or 16 million people). If your events aren’t welcoming and accessible for everyone, you’re likely missing out on the opportunity to reach a much wider audience. That’s not only disabled people either; it’s also their family members and supportive friends who may refuse to come to your events unless all their needs are met.

WHAT IS AN ACCESSIBLE EVENT?

Creating an accessible event means designing it to be open to anyone regardless of their physical challenges or hidden disabilities (such as ADHD or Asperger Syndrome). Similarly, inclusion involves making everyone feel welcome in a diverse setting that supports equity for all those involved.

Keep in mind you’re legally obligated to make your events fully accessible. Disability is one of nine ‘protected characteristics’ defined by the 2010 Equality Act – making it illegal for any UK business to discriminate against persons with disabilities (PWDs).

Moreover, in June 2025, the European Accessibility Act will come into force, bringing in common rules on accessibility requirements across EU member states.

SO, HOW DO YOU PLAN MORE ACCESSIBLE

EVENTS?

First, create a culture of inclusion by ensuring everyone involved in the planning and execution of your events is given the same level of

awareness and empathy training. Then, consider each event element from the perspective of a PWD.

When sourcing venues, for example, consider both the accessibility within the venue and how your attendees may travel to your event. Then, work with your chosen venue to ensure additional measures can be added, and specific requests are supported.

When creating an event registration website, check that the platform used to design and host your site is accessible. A platform like Cvent’s Attendee Hub lets you know when colour combinations don’t meet accessibility guidelines to help you support attendees who may have visual impairments or be colour-vision deficient.

When designing your site, add alternative text to images and make it easier for those using assistive technologies, such as screen readers and braille displays, to navigate your event website and registration process.

Your registration page should also ask the right questions with checkboxes. These could include questions such as:

■ Do you require captions?

■ Do you require a sign language interpreter?

■ Will you be accompanied by a service animal or personal care assistant (PCA)?

■ Do you require wheelchair access?

By asking more detailed questions at the registration stage and contacting anyone who has requested certain requirements, you’ll create a positive first impression of your event and give yourself more planning time to incorporate additional accessible elements.

Next, consider the attendee journey.

For example, to accommodate visitors in wheelchairs, you’ll need to widen the aisles and add lower poseur tables. You’ll also need a dedicated wheelchair area in your conference hall or break-out rooms.

Some visitors with physical impairments may be accompanied by a PCA, who is there to assist the attendee. In this case, you’ll need to ensure that:

■ The PCA is given free entry

■ They’re always able to sit next to the person they’re looking after

■ You’ve factored them into catering numbers and room capacities

The same goes for service animals such as a guide dog for a visually impaired attendee. You’ll need to ensure that:

■ There’s a reserved space for them at the end of an aisle so that their dog can remain alongside

■ You provide facilities such as drinking water and somewhere for a dog to go to the toilet

■ Staff are made aware not to distract or fuss over a service animal

If your events aren’t welcoming and accessible for everyone, you’re likely missing out on the opportunity to reach a much wider audience

Quiet rooms and wellness spaces for anybody to take a break from the hustle and bustle of the show floor are also a great addition to your event. But if you have anxious or neurodivergent attendees, you may need to reconsider audio-visual elements such as strobe stage lighting so that it doesn’t trigger photosensitive epilepsy. Also, make

sure ice-breakers, breakout sessions, competitions, and other activities at your event are accessible or multi-sensory. Making your events accessible also extends to virtual formats. Here are some tips:

Ensure that online presentations meet certain colour contrast ratios to be accessible for the visually impaired or people with colour blindness.

■ Not everyone can see or interpret presentation slides. Ask presenters to explain visual content.

■ Attendees with a hearing impairment may require online presentations to show more detail, offer live captions or have someone in the chat who can answer their questions in real time.

The ROI (return on investment) of making your events more accessible is both reputational and compliance with the laws of the land.

If your organisation needs additional motivation, remember, in the UK, 40 per cent of households have at least one disabled person, which puts the value of the ‘purple pound’ at around £274billion, according to the charity Scope. Everyone can make accessibility improvements to their event programmes. Even if it’s something small, it could make a world of difference to someone’s experience of your offer. So, metaphorically, walk the floor of your event in the shoes of a person with a disability and embrace the help that technology can offer. Together, we can make all types of events a more accessible and inclusive environment for everyone to enjoy.

■ To learn more about making your meetings and events more accessible, visit cvent.com/en/ resource/event/big-book-of-eventaccessibility

Mike Fletcher

Of all the challenges facing Europe right now, migration is one of the most complex. Migration is a social, economic, and political phenomenon. The successful integration of migrants is not easy, but paramount –failure to integrate can have serious political consequences and hurt multiculturalism.

In addition, making migration work could help Europe overcome demographic and economic stagnation. Although social and economic integration take up most of the space in conversations around the integration of migrants, they often ignore financial inclusion. This is a mistake. It is difficult to find a job, rent a property or even acquire a smartphone without a bank account or some type of credit score. In this day and age, this shouldn’t be an issue. The world has seen fintech advance by leaps and bounds in the last years. Leveraging financial technology offers an opportunity for Europe to facilitate desperately needed financial inclusion measures. And, best of all, it’s something that can be fixed today.

THE STATE OF MIGRATION IN EUROPE

The last decade has seen the biggest movement of migrants globally since the end of the Second World War. According to the latest available international migrant stock data from the International Organisation for Migration, more than 40 million non-European international migrants lived in Europe in 2020. Accounting for people moving within Europe, the number rises to 87 million. The outbreak of war in Ukraine has only compounded that number. The numbers from Ukraine alone are in the millions. According to UNHCR, about 5.9 million refugees from Ukraine have moved to EU countries and now make up roughly one per cent of the EU population. In 2022 alone, some 9.93 million non-EU citizens were employed in the EU labour market, and they are pulling their weight. Non-citizens far outpace EU citizens in employment in essential sectors like accommodation, agriculture, construction and domestic work. Contrary to concerns that migrants are a financial burden on their host countries, they in fact help stave off looming labour shortages while boosting economies and tax revenue, which is crucial to overcoming the lasting post-Covid slumps. Take Poland, where 70 per cent of the nearly one million Ukrainians with temporary protection are employed. In 2023 these refugees paid between 18.2 and 22.5 billion PLN in taxes –equivalent to about $5billion. Even so, many migrants remain in the shadow economy. According to the European Commission, this is

HOW FINTECH COULD BOOST INTEGRATION OF MIGRANTS WITHIN EUROPE

Improved financial inclusion of migrants is essential for their integration – but steps still need to be taken

Korneu, co-founder and CEO of neobank myTU

directly tied to a number of factors: administrative delays in processing work permits, legal workload limitations and wage thresholds, and the extended gap in employment and added-on administrative burden that migration creates for individual workers. Compounded with financial exclusion, this becomes an untenable situation that forces migrants to find other ways to function economically.

WHAT’S STANDING IN THE WAY?

The banking sector is generally hesitant to service migrants. Whether illegal, legal refugees, or legal migrants, they are often viewed as a high-risk population, or as less interesting customers than local citizens. New migrants typically lack the documentation required for standard verification processes. They also often have uncertain residency status, may be somewhat financially illiterate or distrustful of financial institutions, and hindered by a language barrier. A common requirement for opening an account and accessing services is proof of a residential address using a utility bill. But migrants, particularly if they intend to rent, often won’t have a utility bill. This often puts migrants in a catch-22 situation: you need a bank account to rent a flat, but you need a flat to open a bank account. With the broad range of customer categories, neobanks have begun to lead the way in this area, especially compared to traditional financial

institutions. Less entrenched and risk-averse than these traditional financial institutions, neobanks are better suited to innovate and expand their offerings based on the needs and special circumstances of migrants (such as not having a credit score). If they stay on this trajectory, neobanks and other fintech companies could hold the key to making financial inclusion more accessible for migrants, so they can proceed to better integrate also economically and socially, accessing jobs, accommodation and more.

That’s not to say neobanks can fix this problem alone, especially for migrants in smaller countries where these banks are not always available. Inconsistent regulatory frameworks and policy variations create further hurdles for financial inclusion. In other words, continuing financial reform from the EU needs to meet neobanks and fintech institutions halfway.

NEW CIRCUMSTANCES

What does this migrant-friendly banking look like in practice? For starters, identity verification must go broader than names and addresses on utility bills. Some neobanks have taken the lead here, including more people in the financial system by employing various ways to confirm clients’ identities. These neobanks accept professional networks like LinkedIn and social media accounts

for partial verification. On the security side, they employ the latest technology to avoid fraud, such as blockchain and AI. And they can analyse behavioural biometrics like typing and navigation patterns. Many migrants are commerce owners or have skills suited for freelancing. Migrants need specialised banking services in order to start their own companies too. These services include multicurrency accounts, seamless digital identity verification, and low-cost international money transfers. Multi-language support, assistance with insurance, taxation and compliance, and virtual business addresses are also crucial. Additionally, access to peer-to-peer lending platforms, integration with freelance platforms, and blockchain technology for secure transactions as well as smart contracts for business agreements are necessary to support their unique circumstances. Collaboration is also key. Neobanks and digital financial services like Wamo.io and Wise have begun partnering with official e-residency programmes in countries like Estonia to offer business banking solutions, including accounts and invoicing tools, and even medical and travel insurance for e-residents. This collaboration goes beyond working with governments. Some neobanks have partnerships with freelancer platforms and marketplaces that cater to EU-based freelancers and contractors. Freelancers can link their N26 account directly to their Upwork profile, making it seamless to receive payments from clients globally. Qonto, a French neobank for small businesses and freelancers, has partnered with legal service platforms, such as Legalstart (France), Firma.de (Germany), Finutive (Spain), or lexdo.it (Italy), to offer comprehensive business registration and banking services.

If neobanks and fintechs are able to recognise the migrant opportunity and tap into it, we will have taken an important step to facilitate integration. We need solutions that let migrants rent a flat, open an account, and get paid for their work. Fintech-led solutions can make that happen.

About Raman Korneu Raman is CEO and co-founder of neobank myTU that is pioneering the use of cloud-only infrastructure and AI to make essential financial services easier to access, more secure and more cost-effective. www.mytu.co

Raman

ELECTRIC VEHICLES & PAYMENT ANXIETY

The hidden roadblock to EV adoption with Sarah Koch , director of marketing and communications at Aevi , a platform provider for in-person payment orchestration

As of recent projections the electric vehicle (EV) market is expected to gain a steady 6.63 per cent growth year-on-year across the world. These studies also suggest that by 2029 the EV market will reach a $1,084billion revenue in the US alone, and with over 26 million EVs on the roads globally as well as significant government push toward a green transition, we are witnessing a major shift in what powers our everyday mobility.

However, one critical issue has become increasingly noticeable: so-called ‘payment anxiety’.

WHAT IS EV ‘PAYMENT ANXIETY’?

Much like ‘range anxiety’, which is the fear of running out of charge without access to a charging station, EV drivers are now experiencing a new concern. Complicated in-person payment systems at charging stations have deterred drivers since the advent of electric vehicles, adding an additional layer of stress to an already complex transition.

As EV adoption grows, the need for a streamlined and more efficient payment system has never been more urgent. Let’s explore how complicated payment systems can impact EV drivers and how this, in turn, can affect the broader adoption

of electric vehicles.

Finally, we will see how these challenges can become a great opportunity to drive the EV market.

THE GLOBAL RISE OF EVS AND THE INFRASTRUCTURE TEST

When it comes to EV adoption, countries like Norway, China, and South Korea that are leading the charge, this in part is fuelled by conspicuous government incentives, technological advancements and public demand for sustainable transportation. What stands out is how these governments have not only incentivised EV adoption at the purchase stage, but how they’ve also invested heavily in the development of robust charging infrastructure.

For instance, Norway’s extensive and well-orchestrated public charging network is often considered as the gold standard in offering drivers a seamless experience. However, as more and more countries look to replicate this model and EV adoption moves to a mass market scale, other regions are clearly facing growing pains, particularly when it comes to payment systems at charging stations.

EV drivers worldwide frequently face unclear pricing and inconsistent payment options at charging stations, with many service stations requiring specific apps or RFID cards, while others only accept local payment methods. This fragmented approach leads to obvious frustration and a disjointed experience. As a result, many EV drivers are forced to manage multiple apps just to find the best bargains, contributing to widespread app fatigue. Potential

new adopters also cite confusion surrounding charging infrastructure as a major deterrent. Without much-needed standardisation, these challenges will only worsen, creating a significant barrier to wider EV adoption. What many current and potential EV drivers, particularly in Western markets, seek is the simplicity of paying with conventional payment cards.

PAYMENT SYSTEMS: A DARK HORSE IN THE EV REVOLUTION

Just as drivers need confidence in the availability of charging infrastructure, they likewise need assurance that paying for these services will be easy and straightforward.

We believe that the future of payments lies in simplicity and flexibility especially when it comes to the mobility space. This means creating payment systems that have this goal in mind and can work for everyone, whether that’s contactless cards, mobile wallets, or even the adoption of new dynamic pricing models based on real-time demand and energy usage.

EV DRIVERS WORLDWIDE FREQUENTLY FACE UNCLEAR PRICING AND INCONSISTENT PAYMENT OPTIONS AT CHARGING STATIONS

EV drivers should be provided with a charging experience that is as seamless as refuelling a car, and one important aspect can be achieved by optimising the EV infrastructure for the in-person payment process. This should also extend beyond payments; clear, dynamic pricing models need to be integrated to

inform drivers about real-time costs which are based on energy demand and the time of the day. It’s becoming more and more clear how without these features, consumers may hesitate to make the switch to electric, fearing unpredictable expenses and complex transactions.

POWERING THE FUTURE OF EV WITH SIMPLIFIED PAYMENTS

As the EV market continues to grow, so do the expectations of its users. While much attention has been given to expanding charging infrastructure and increasing battery range, the importance of a smooth and reliable payment experience cannot be overstated. Complicated in-person payments are a hidden obstacle to wider EV adoption, but they don’t have to be. By focusing on simplicity, transparency, and innovation in payment systems, we can alleviate EV payment anxiety and pave the way for a future where electric vehicles are the norm, not the exception. The EV market is experiencing a pivotal transformation, similar to the retail revolution of the early 2000s. Just as the rise of e-commerce depended on seamless and secure payment methods, the EV market now requires frictionless in-person payment solutions at charging points to support its growth. This shift is crucial for the mainstream adoption of electric vehicles, as simplifying payment experiences will play a key role in driving widespread EV use.

https://aevi.com

SPOTLIGHT ON VARA’S MARKETING REGULATIONS

A blueprint for the future of digital assets

The Dubai Virtual Assets Regulatory Authority’s (VARA) recent release of its 2024 Marketing Guidelines for Digital Assets marks a bold step forward in the global push for responsible regulation of the digital asset market. As countries and regulators grapple with the challenges of overseeing this rapidly evolving sector, Dubai’s approach stands out as a model for what effective oversight should look like – balanced, comprehensive, and forward-looking.

approach, introducing regulations in response to crises, VARA has taken a proactive stance. It has carefully studied the digital asset industry and laid out a comprehensive framework that addresses key issues such as misleading promotions, aggressive marketing tactics, and uninformed investment decisions. This strategy is not only about enforcing rules but also about fostering a safer, more transparent market where investors can have greater confidence.

1

Clear definition of marketing activities

VARA defines ‘marketing’ broadly, covering any form of advertisement, solicitation, offer, or promotion. This includes social media posts, blogs, influencer endorsements, sponsored content, events, and even educational materials that indirectly promote digital assets.

The regulation applies to all entities, whether domestic or foreign, licensed or unlicensed, if their marketing activities are targeted at the UAE.

2 Specific compliance requirements

4 Regulation of third-party marketing

If an entity uses a third-party marketing agency, the responsibility for compliance lies with both the entity and the agency. VARA requires marketing agencies to secure approvals from the entity and conduct due diligence before executing campaigns.

5 Record keeping requirements

At first glance, the extensive list of rules may seem daunting to industry players. The new regulations span everything from traditional advertisements to digital promotions, influencer partnerships, and even educational content related to virtual assets. But beyond the regulatory complexity lies an essential truth: without stringent measures to protect investors and guide market conduct, the credibility and sustainability of the entire digital asset sector are at risk.

The past few years have been a rollercoaster for digital assets. Cryptocurrencies and other virtual assets have seen meteoric rises and equally dramatic falls. This volatility, coupled with high-profile scandals and fraudulent schemes, has left many skeptical about the future of this sector. Yet, amid the chaos, Dubai has steadily positioned itself as a beacon of order and opportunity.

WHY DUBAI’S APPROACH IS DIFFERENT

While many regulators worldwide have adopted a reactionary

A critical component of the new regulations is the emphasis on transparency and clarity in all marketing and promotional activities. All communications – whether a tweet from a prominent influencer or a full-page newspaper ad – must now include clear disclaimers about the risks associated with digital assets.

Gone are the days when marketing gimmicks could lure unsuspecting investors with promises of guaranteed returns or exaggerated claims of safety and security.

This transparency is vital because it shifts the industry narrative away from hype and speculation toward a more realistic and measured view of digital asset investments. By requiring marketers to provide balanced information, VARA ensures that investors are equipped to make informed decisions, reducing the likelihood of panic-driven sell-offs or reckless speculation.

KEY HIGHLIGHTS OF VARA’S MARKETING REGULATIONS

To provide a deeper understanding, here are some of the most critical components of VARA’s 2024 Marketing Guidelines:

Risk disclosures: All promotional content must clearly communicate that virtual assets are volatile and investors can lose their entire investment. There must be no implication that returns are guaranteed or that investments are risk-free.

Prohibited practices: Marketing that uses urgency, exaggerated claims, or messages designed to create a fear of missing out (FOMO) is strictly prohibited.

Fairness and transparency: Marketing content must be fair, clear, and not misleading. This includes avoiding complex language or financial jargon that may confuse inexperienced investors.

3Restrictions on marketing of anonymity-enhanced cryptocurrencies (AECs)

VARA has outright banned the marketing of anonymity-enhanced cryptocurrencies within or targeting the UAE. This is a significant move to prevent the promotion of digital assets that lack transparency and traceability, which can pose significant risks for money laundering and other illicit activities.

All entities must keep records of their marketing activities for a minimum of eight years. These records should include details of content distribution and approvals, ensuring full transparency and accountability.

6 Event marketing rules

Firms not licensed by VARA can market at physical events in Dubai only if they refrain from onboarding UAE residents as clients. All event marketing materials must include disclaimers that the entity is not licensed to conduct VA Activities in Dubai.

7 Severe penalties for non-compliance

Penalties for violating the marketing guidelines can reach up to AED 10million per infraction, and repeat offenders may see fines doubled. This demonstrates VARA’s commitment to strict enforcement and underscores the need for entities to take compliance seriously.

SETTING A HIGHER BAR

Dubai’s regulations go further than simply policing local activities – they have implications for global players as well. Any entity, whether licensed by VARA or not, must comply with these guidelines if they are marketing or promoting digital

Loredana Matei, founder at Jensen Matthews PR

assets to UAE residents. This means that global digital asset firms looking to enter the Dubai market, or even those targeting Dubai-based investors, must align their marketing practices with these standards.

This move effectively sets a higher bar for global compliance. It tells the world that if you want to operate in Dubai’s digital asset market, you must uphold the same level of integrity and transparency expected of local firms. It’s a significant message that Dubai is not interested in being a regulatory haven, but rather a legitimate, well-regulated hub for digital finance. For companies, this means reassessing their promotional strategies. Influencer campaigns, for example, can no longer use urgency or fear of missing out tactics to push products. The overuse of ambiguous disclaimers buried in fine print is no longer acceptable. Every piece of marketing must be straightforward, fair, and not misleading. While this may seem burdensome, it will help filter out players who rely on unethical tactics and attract serious, long-term participants who are committed to building a credible industry.

A CATALYST FOR MARKET MATURITY

The impact of these regulations extends beyond marketing. By requiring that only licensed Virtual Asset Service Providers (VASPs) are permitted to promote their services, VARA is pushing firms to operate under a legitimate license and adhere to strict regulatory standards. This will not only reduce the number of bad actors but also contribute to the overall maturity of the digital asset market in Dubai. Furthermore, the enforcement of penalties – up to AED 10 million per violation – is a clear signal that

VARA is serious about compliance. Repeat offenders may find themselves hit with doubled fines, further deterring non-compliance. The message is clear: either play by the rules or face the consequences. These regulations also elevate Dubai’s standing on the global stage. In a time when the US Securities and Exchange Commission (SEC) and European regulators are wrestling with fragmented and sometimes unclear policies, VARA’s structured approach offers a blueprint that other jurisdictions could follow.

THE ROAD AHEAD

There’s no doubt that VARA’s new marketing guidelines will require some adjustment from firms. Marketing agencies will need to refine their strategies, legal teams will have to scrutinise every campaign for compliance, and influencers will have to exercise greater caution when endorsing digital asset products. The short-term impact may be challenging, but the long-term benefits far outweigh these initial hurdles.

For Dubai, these regulations are more than just rules – they are a statement of intent. The Emirate is not just vying to be a global hub for digital assets; it’s laying the groundwork to become a model jurisdiction for responsible and innovative financial services. If other regions are serious about creating a sustainable digital asset market, they would do well to take note of Dubai’s approach. In the end, a well-regulated market is not just good for investors, it’s good for everyone. It attracts better firms, boosts investor confidence, and fosters a healthier, more sustainable industry. Dubai’s new marketing regulations are a step in the right direction, and the rest of the world should be watching closely.

VARA INTRODUCES STRICTER MARKETING REGULATIONS FOR VIRTUAL ASSETS SECTOR IN DUBAI

Dubai-based regulator, the Virtual Assets Regulatory Authority (VARA), is updating its marketing regulations, as part of a move to strengthen the regulatory framework for Virtual Asset Service Providers (VASPs) operating in the region.

VARA Marketing Regulations for Virtual Assets and Related Activities 2024 aim to enhance the transparency of marketing practices within the virtual assets sector in Dubai.

The updated regulations place stronger emphasis on the accuracy of marketing communications, the avoidance of misleading information, and the protection of consumer interests. The new updates apply to all entities involved in marketing virtual assets or related activities.

Alongside these updates, VARA is also introducing a Marketing Guidance Document, providing actionable insights for VASPs engaging in marketing activities within the region. This document provides detailed instructions and best practices on how to conduct compliant marketing activities in Dubai, ensuring that VASPs can navigate the regulatory landscape with confidence.

The guidance covers a range of topics, including the appropriate use of language in marketing materials, disclosure equirements, as well as the ethical onsiderations that should underpin all marketing efforts.

“As the world’s first independent regulator for virtual assets, VARA is creating a regulatory environment that not only protects consumers but also supports the growth and innovation of the virtual assets sector,” explained Matthew White, CEO of VARA.

“Our updated marketing regulations and the newly issued guidance document reflect our commitment to maintaining Dubai’s position as a global leader in digital finance.

“We believe that by providing clear and actionable guidance, we can help VASPs deliver their services responsibly, while fostering greater trust and transparency in the market.”

VARA’s new regulations are set to come into effect on 1 October 2024. The news comes shortly after the Securities and Commodities Authority signed a cooperation agreement with Dubai’s VARA to bolster the UAE’s position as a leading global hub for virtual assets.

WHY OPEN FINANCE IS STILL WAITING TO TAKE OFF!

Open finance aims to give third-party providers access to a wider range of financial data, extending beyond just banking services. While it holds promise for more personalised products and improved financial inclusion, its adoption has been slower than expected. Several key challenges, including privacy concerns and a lack of strong advocacy, continue to stand in the way.

To explore the challenges preventing the widespread adoption of open finance, we reached out to industry leaders for their insights.

Advocacy gaps are holding back progress

One of the biggest gaps in the industry is the lack of clear advocacy for open finance, says

With open finance struggling to gain traction, experts discuss the biggest challenges holding it back, from data privacy concerns to regulatory gaps

Christopher G. Fox, PhD, founder of Ideas-Led Growth, a consultancy for financial companies. He argues that many financial institutions and non-banks are not being adequately persuaded of the benefits of open finance. “Too many providers take it on faith that open finance tools are worth adopting,” Fox says.

“They don’t have strong comms and marketing strategies that persuade top decision makers to consider or embrace open finance.” Without targeted advocacy, Fox believes open finance will remain “stuck in the realm of theory and buzzwords” rather than becoming a mainstream reality. “Providers need to invest in robust thought leadership

strategies that specifically address the needs of traditional banks or other enterprises.

Data privacy concerns remain a major barrier

Mark Geneste, chief revenue officer at SaaS cloud banking platform Mambu, points to data privacy as a key issue holding back the adoption of open finance. As cyber threats grow, many consumers are increasingly cautious about sharing financial data. “Many individuals are worried about the safety of their data, preventing the widespread adoption of open finance,” he says.

To address these concerns, Geneste suggests that financial institutions should partner with fintechs that comply with global data protection laws. This, he believes, will help restore consumer confidence. “By partnering with a true SaaS banking platform, fintechs can ensure their platforms are compliant with global regulatory standards,” he adds.

Geneste also notes that a lack of consumer awareness remains another significant obstacle. “With many consumers unaware of what open finance is or how it will benefit them, it is clear to see why adoption has stalled.” He points to Mambu research showing that 52 per cent of consumers are unfamiliar with open banking technologies, stressing the need for increased awareness campaigns to drive adoption.

Fragmented data limits open finance potential

The fragmented nature of financial data stands as a major obstacle to unlocking the full potential of open finance, according to Ezechi Britton, CEO of the Centre for Finance, Innovation and Technology (CFIT). He highlights how the lack of collaboration between data holders and financial service providers hampers both economic growth and consumer choice.

“Fragmentation proves a significant drag on economic growth and consumer choice,” Britton says, pointing to the inefficiencies that arise from disconnected data. Research conducted by CFIT’s coalition on open finance estimates that better access to personal financial data could deliver a £30.5billion boost to the UK economy.

To achieve this, Britton explains the importance of secure datasharing mechanisms. “The success of open finance hinges on secure and ready access to financial data, and widespread adoption relies heavily on building trust and confidence in consent and data security. A crucial part of our industry-wide coalition’s work on open finance was to develop a prototype authentication flow and consent hub, demonstrating how users could easily complete authentication with several organisations and understand what data they are sharing, for how long, with whom and how they can revoke their consent easily.”

Lack of understanding and data protection concerns

Christo Christodoulou, head of strategic partnerships, EMEA at global payments platform Airwallex, says the lack of awareness surrounding open finance – especially its benefits and implications – is a significant barrier to adoption. “Open finance is the next step up from open banking, but we need consumers, businesses, and banks fully onboard for it to succeed,” he says. Without a clear understanding of how open finance can enhance financial services, adoption will remain limited. Data protection concerns also weigh heavily on the minds of potential users. Many are reluctant to