9 minute read

How worldwide production is looking for 2021

Aquaculture

bounces back

A worldwide survey of producers reveals the post-2020 recovery is under way, but there are also winners and losers

BY ROBERT OUTRAM

THE Global Seafood Alliance (GSA) Conference – no� onally in Sea� le this year, but actually online – also saw the unveiling of the GSA’s global aquaculture produc� on surveys and forecast, covering fi nfi sh and shrimp.

Both surveys were produced by the GSA in associa� on with Rabobank, with addi� onal data from the United Na� ons Food and Agricultural Organisa� on (FAO) and analysts Kontali. Produc� on growth es� mate for 2020 and 2021, and forecasts for the coming year, were based on input from producers.

The results were presented by Gorjan Nikolik, Senior Analyst, Seafood, with Rabobank.

Shrimp shine in 2021

For the shrimp sector, it was a story of recovery from the slump in 2020, with further growth to come.

Nikolik said: “For La� n America as a whole, it’s been a booming year for shrimp produc� on.”

Mexico’s produc� on of vannamei shrimp declined slightly in 2020 compared with the previous year, but es� mates for 2021 suggest that, at just under 180,000 tonnes, the current year’s out will be 8% up year on year.

Brazil’s output is expected to be at least 65,000 tonnes or more according to the GOAL survey, with some es� mates predic� ng as much as 100,000 tonnes.

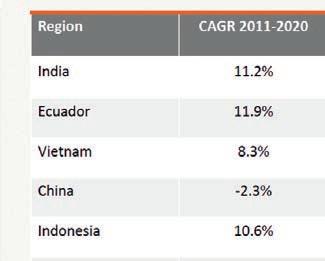

Ecuador remains a strong performer in the fi eld, with con� nued year-on-year growth of 5.1% even during 2020 and expected growth of 10.2% to reach just under 800,000 tonnes.

Indian produc� on contracted steeply by 12.5% in 2020. With 2021 output es� mated at around 700,000 tonnes, it is expected to take un� l 2023 to get back to the produc� on levels of 2019.

China’s fi gures are controversial, Nikolik said. Offi cially, shrimp produc� on in China passed 2 million tonnes in 2018, with just under 2.2 million in 2019.

Rabobank’s alterna� ve assessment, based on industry sources, suggests 2019 output was more like just over 500,000 tonnes, represen� ng a slight fall compared with 2018.

Applying industry expecta� ons to offi cial data, Rabobank suggests growth is resuming a� er a fairly fl at 2020, with 9.1% growth in 2021, or a total for the current year of more than 2,300 tonnes.

Vietnam is expected to record 13.6% growth for 2021, to around 760,000 tonnes, although growth next year is only predicted to be 0.9% and Rabobank feels offi cial fi gures may be overstated.

Indonesia’s fi gures are also disputed. Rabobank feels the offi cial fi gures for 2019, of over 900,000 tonnes, are over-op� mis� c and believes the real fi gure, based on industry sources, could be more like 380,000 tonnes.

Thailand, meanwhile, will see an es� mated 7.8% in growth for 2021, taking the country’s produc� on to just over 400,000 tonnes, while smaller producers such as the Philippines and Malaysia appear to be pre� y fl at in growth terms. In total, produc� on

This page from top: India and Ecuador: shrimp exports by volume and value, 2020; Shrimp; Expected shrimp produc� on growth by region – CAGR = compound annual growth rate Opposite from top: Farmed carp, China; Global fi nfi sh produc� on – sources Rabobank, FAP, GSA; Global salmon produc� on by region

in 2021 for south east Asia – not including China – is expected to be around 1.6 million tonnes.

Using an es� mate based on offi cial fi gures supplied to the UN Food and Agricultural Organisa� on up to 2019, global shrimp produc� on for 2021 will be around 7 million tonnes, up 8.9% on 2020, which had seen a fall of 2%.

Rabobank’s own es� mate – taking out overcounting for China, Indonesia and Vietnam – applies the same expected growth rate, but comes up with a global fi gure of just under 4.5 million tonnes.

In 2020, India was s� ll the world’s top shrimp exporter by value (US$4.48bn), but in volume terms Ecuador took the top spot, at 637,000 tonnes. For the year to date – up to July 2021 – Ecuador as leading on both counts (at US$3.09bn and 522,000 tonnes).

The GSA’s survey of producers suggest that further growth globally is expected for 2022, although producers are less op� mis� c about the impact of rising feed prices. In descending order, their top three concerns were market prices, disease preven� on and the cost of aquafeed.

A tale of two salmon na� ons

The Global Finfi sh Aquaculture Survey and Forecast found that 2021 was a very diff erent story for two of the leading Atlan� c salmon producers: Chile and Norway.

Norwegian farmers expect to record just over 10% growth, to around 1.5 million tonnes for 2021 a� er growth slowed to 2.7% in 2020. Another 4.6% in growth is expected for 2022. Nikolik observed, however, that thanks to environmental regula� ons, Norway is approaching the limits of its capacity for marine fi sh farming.

In Chile, es� mated produc� on for 2021 has actually slumped by just over 14% compared with 2020, taking produc� on to a li� le over 600,000 tonnes. One of the key factors for Chile has been biological issues, which have led to die-off s and culls of fi sh.

UK salmon producers expect to record a big increase for 2021, with around 210,000 tonnes compared with 2020’s es� mate of around 175,000 tonnes. In contrast, Canada’s produc� on, at around 140,00 tonnes, has been fl at and is expected to remain so.

The “others” in salmon farming – including Iceland, Australia, Ireland and the US – are becoming increasingly signifi cant, Nikolik said. With combined produc� on topping 160,000 tonnes, es� mated year-on-year growth for 2021 is 20% and growth is expected to con� nue at around 6% for the next two years.

Norway’s growth spurt and Chile’s misfortunes have cancelled each other out to create an expected steady growth curve for salmon produc� on between 5.2% and 4.4% over 2020 to 2022, slowing to 2.8% in 2023. Es� mated global produc� on for 2021 is around 2.8 million tonnes.

Other species

Atlan� c cod produc� on in Norway is experiencing a revival, the survey shows. From its high of around 22,500 tonnes in 2010, produc� on declined to just over 5,000 tonnes by 2019, but that is now growing and 2021’s es� mate is more like just under 10,000 tonnes, with further growth of more than 47% expected for 2022.

Meanwhile sea bass and sea bream produc� on – s� ll led by Greece and Turkey – appears to be recovering from the slumped levels of 2020, with an es� mated 3.8% increase taking the expected total for 2021 to just under 500,000 tonnes. This is s� ll marginally below the industry’s previous high in 2019, but 1.2% growth in 2022 and 4.2% in 2023 should see produc� on reach new peaks in those years.

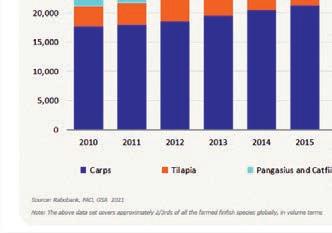

Tilapia is a mature sector for established producers such as China and Indonesia, but it is growing in Bangladesh, the Philippines, Vietnam, Egypt and La� n America.

The FAO es� mated that world � lapia produc� on was around 5.5 million tonnes in 2019. Since then, the GOAL survey es� mates, total produc� on has grown by 1.2% for 2021 and will see further growth of 2.5% in 2022 and 3.7% in 2023.

Produc� on of pangasius, a large ca� ish, is es� mated at 3 million tonnes for 2020, up 3.7%, with a further 6% increase year on year for 2021.

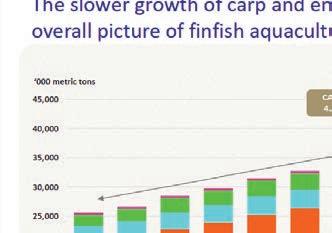

Growth in carp produc� on – a huge industry in which China is by far the biggest player – appears to be slowing. Es� mated produc� on for 2021 is just over 24 million tonnes and growth for next year is only expected to be 1.6%.

The big picture is that global fi nfi sh produc� on for 20121 is likely to be around 38 million tonnes, up 2.5% on the es� mated fi gure for 2020, which had seen growth of only 0.2% from 2019. The industry expects to see further growth of 2.7% in 2022. FF