5 minute read

Unlocking Thailand’s carbon-free future with green hydrogen

Bratin Roy

Introduction

Advertisement

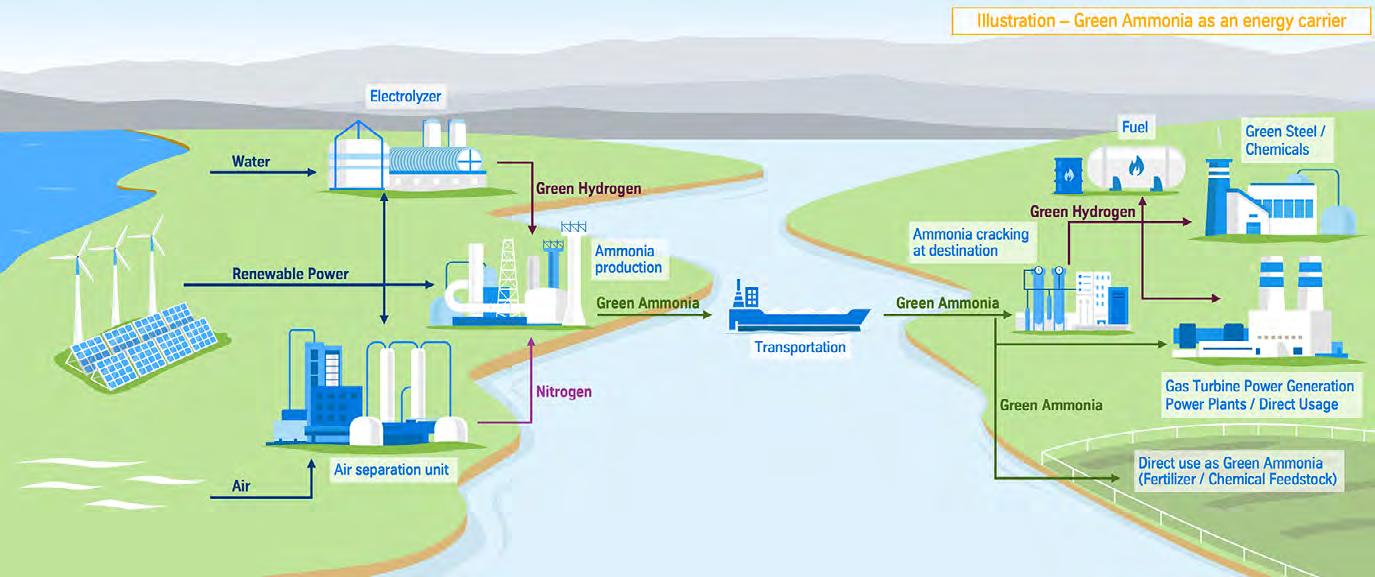

Hydrogen is set to play a central role in energy transformation as an energy storage medium and energy carrier. It will have a vital positioning as a key element to unlock a carbon-free future in global economy. There are different ways to produce hydrogen, which are typically referred to as green, blue, grey and sometimes turquoise, yellow and pink hydrogen.

When green hydrogen is produced, only renewable energy sources are used to provide the energy needed for hydrogen production, e.g., via electrolysis. Blue hydrogen is produced by splitting natural gas into hydrogen and CO 2 , for example, through steam methane reforming (SMR). The CO2 is not released into the atmosphere but is captured in the process and then stored in geological formation permanently. This process of carbon capture and storage (CCS) mitigates the environmental impact of CO2. It is important to note that grey hydrogen is produced, like blue hydrogen, from fossil fuels such as natural gas. However, carbon emissions are released into the atmosphere, making this way of hydrogen production less environmentally safe. Turquoise hydrogen is created through the pyrolysis of methane, which is split into solid carbon and hydrogen in a reactor. This process does not produce gaseous CO 2 as a by-product; if renewable energies power the reactor, it is considered CO 2 -emission neutral. Pink hydrogen is also made through electrolysis, with power coming from nuclear energy.

Potential For Expansion Of Green Hydrogen Usage And The Renewable Energy Industry In Thailand

Thailand has pledged to achieve net zero emissions by the year 2065, with green hydrogen playing an important role in reaching this target. Thailand intends to produce green hydrogen. Under the Alternative Energy Development Plan (AEDP), one of Thailand's five master plans related to energy development, hydrogen is included as part of the “Alternative Fuels” category with a set target goal of 10 kilotons of oil equivalent (KTOE) in total by 2036. For the green hydrogen, Thailand has a benefit of irradiation conditions that render solar power productive throughout the year. According to the International Energy Agency, given current baseload capacity,

Thailand’s grid could still accommodate significant additional deployment of variable renewable energy to generate electricity.

Thailand currently has an installed renewable energy capacity of more than 15 GW, and Thailand’s Energy Regulatory Commission started promoting power purchase agreements for up to 5.2GW across four types of renewable energy projects: 335 MW of biowaste; 1GW of solar with battery storage, 1.5GW from wind and 2.3GW of solar power without battery storage. It is aimed to have all the capacity that can be integrated into the production of green hydrogen installed by 2030. That green hydrogen can be used for several applications such as decarbonization of residential and commercial heating and cooling systems. In the mobility sector it can be used in hydrogen fuel cell vehicles, and hydrogen-based low carbon fuels can contribute to the decarbonization of the mobility sector as a feedstock to produce ammonia, methane and methanol.

Challenges

Major challenges today are the cost of production as green hydrogen is a capitalintensive process, as scaling up of electrolysis cells is quite expensive as well as the high levelized cost of infrastructure and transportation. In addition, there are also safety concerns due to flammability, buoyancy and ability to embrittle metals of the hydrogen. Another major hurdle faced by the industry today in developing a hydrogen economy is the is complex and wide-ranging supply chain challenge. It includes: (a) utilities, providing either raw materials or energy to enable hydrogen production, hydrogen manufacturing equipment and relevant supply chains; (b) transport, distribution and storage, including pipeline and vessel/vehicle transport; (c) fuel cell components and fuel cells; and (d) hydrogen carrier chemicals and materials. In addition, the lack of uniform standardization and international regulation synchronized with the absence of local requirement creates further uncertainty for investors, as the requirements of off-takers, especially from potential exporting countries, are still not very clear.

How To Overcome The Above Challenges

The current policy incentives mainly focus on the supply side. Developers and investors need a visible offtake pipeline for their product. Governments could provide this by introducing a green hydrogen consumption obligation (GHCO) mechanism for the production of fertilizer and other chemicals as well as petroleum refining, similar to the Renewable Purchase Obligations (RPO). Strong offtake agreements will make the projects bankable as well as uniform certification schemes (like CertifHy, CMS70) for certifying hydrogen for onboard off- takers.

In addition, hydrogen’s future depends on large-scale CO2 storage, which can be provided by geological formations (such as aquifers, and depleted oil and gas reservoirs) to handle demand and supply changes. Research and development efforts are needed to increase the efficiency of the electrolyzer system as well as the electrolyzer operating time, power density and stack size. With these improvements, material costs will be reduced and more flexible systems achieved that can accommodate an occasionally interrupted and fluctuating power supply. Further additional revenue sources can be explored in the carbon market. Carbon markets are a mechanism by which carbon mitigation actions can be certified and transferred to tradeable carbon credits. Three different types of carbon markets which can be used for green hydrogen projects are National Carbon Markets, Voluntary Carbon Markets (int.) and Compliance Carbon Markets (Art. 6, PA).

Bratin Roy Sr. Vice-President Industry Service I Sustainability

TÜV SÜD ASEAN, South Asia, Middle East and Africa Region (ASMEA)

Contact Details:

Rishab Dudhoria

Business Development Head – ASEAN Supply Chain Services and Sustainability

TÜV SÜD (Thailand) Limited +66 65 985 3011 rishab.d@tuvsud.com