Will ESOPs Become the Norm?

Managing Corporate Cash

Preparing for the IPO Comeback

Managing Risk in Tax Season

Difficult Auditor-Client Interactions

Home Sale Strategies And More!

ILLINOIS CPA SOCIETY

550 W. Jackson Boulevard, Suite 900, Chicago, IL 60661 www.icpas.org

Publisher | President and CEO

Geoffrey Brown, CAE

Editor

Derrick Lilly

Assistant Editor

Amy Sanchez

Senior Creative Director

Gene Levitan

Copy Editor

Mari Watts

Photography

Derrick Lilly | iStock

Circulation

John McQuillan

ICPAS OFFICERS

Chairperson

Jonathan W. Hauser, CPA | KPMG LLP

Vice Chairperson

Deborah K. Rood, CPA, MST | CNA Insurance

Secretary

Brian J. Blaha, CPA | Wipfli LLP

Treasurer

Mark W. Wolfgram, CPA, MST | Bel Brands USA Inc.

Immediate Past Chairperson

Mary K. Fuller, CPA | Citrin Cooperman

ICPAS BOARD OF DIRECTORS

John C. Bird, CPA | RSM US LLP

Jennifer L. Cavanaugh, CPA | Grant Thornton LLP

Brian E. Daniell, CPA | West & Company LLC

Pedro A. Diaz de Leon, CPA, CFE, CIA | Cherry Bekaert Advisory LLC

Kimi L. Ellen, CPA | Benford Brown & Associates LLC

Lindy R. Ellis, CPA | Ernst & Young LLP

Jennifer L. Goettler, CPA, CFE | Sikich LLP

Monica N. Harrison, CPA | Tinuiti

Joshua Herbold, Ph.D., CPA | University of Illinois

Scott E. Hurwitz, CPA | Deloitte LLP (Retired)

Joshua D. Lance, CPA, CGMA | Lance CPA Group (Deceased)

Enrique Lopez, CPA | Lopez & Company CPAs Ltd.

Leilani N. Rodrigo, CPA, CGMA | Roth & Co. LLP

Richard C. Tarapchak, CPA | Verano Holdings Corp.

BACK ISSUES + REPRINTS

Back issues may be available. Articles may be reproduced with permission. Please send requests to lillyd@icpas.org.

ADVERTISING

Want to reach 21,700+ accounting and finance professionals? Advertising in Insight and with the Illinois CPA Society gives you access to Illinois’ largest financial community. Contact Mike Walker at mike@rwwcompany.com.

Insight is the magazine of the Illinois CPA Society. Statements or articles of opinion appearing in Insight are not necessarily the views of the Illinois CPA Society. The materials and information contained within Insight are offered as information only and not as practice, financial, accounting, legal or other professional advice. Readers are strongly encouraged to consult with an appropriate professional advisor before acting on the information contained in this publication. It is Insight’s policy not to knowingly accept advertising that discriminates on the basis of race, religion, sex, age or origin. The Illinois CPA Society reserves the right to reject paid advertising that does not meet Insight’s qualifications or that may detract from its professional and ethical standards. The Illinois CPA Society does not necessarily endorse the non-Society resources, services or products that may appear or be referenced within Insight, and makes no representation or warranties about the products or services they may provide or their accuracy or claims. The Illinois CPA Society does not guarantee delivery dates for Insight. The Society disclaims all warranties, express or implied, and assumes no responsibility whatsoever for damages incurred as a result of delays in delivering Insight. Insight (ISSN1053-8542) is published four times a year, in spring, summer, fall, and winter, by the Illinois CPA Society, 550 W. Jackson, Suite 900, Chicago, IL 60661, USA, 312.993.0407.

Copyright © 2023. No part of the contents may be reproduced by any means without the written consent of Insight. Send requests to the address above. Periodicals postage paid at Chicago, IL and at additional mailing offices. POSTMASTER: Send address changes to: Insight, Illinois CPA Society, 550 W. Jackson, Suite 900, Chicago, IL 60661, USA.

18

spotlights

4 CEO Outlook Advocacy: Looking Back to Move Forward

6 Capitol Report

Are You Ready for Beneficial Ownership Compliance Reporting?

46 In Play

Allan Koltin, CPA, CGMA, shares his advice for firms exploring growth via private equity.

48 Gen Next Paying It Forward: Inspiring the Next Generation of CPAs trends

8 Risk Management

Managing Risk in Tax Season and Beyond

10 Tax Planning

The Like-Kind Exchange Home Sale Strategy

12 Professional Issues

What the Future of Accounting Really Needs

14 Auditing

What Drives Difficult Auditor-Client Interactions?

16 Corporate Strategy & Finance Preparing for the IPO Comeback insights

30 Leadership Matters

2 Types of Goals You Need to Succeed in the New Year

32 Growth Perspectives

Deal or No Deal? My 2024 M&A Predictions

34 Evolving Accountant Assessing SAS 134-140: How Did It Go?

36 Financially Speaking

The State of Philanthropy: How CPAs Can Help Donors

38 Corporate Insider

What’s Old Is New Again in Corporate Finance

40 Tax Decoded

It’s Complicated: A Closer Look at Cannabis Sales and 280E

42 Ethics Engaged

The Ethics of Burnout

44 Practice Perspectives

In Succession Planning, What Constitutes Success?

inside Winter 2023

Managing Corporate Cash in an Uncertain Economy

Treasuring Stability:

22 Breaking the Partner Model Will Employee-Owned Firms Become the Norm? 26 Finding Your Balance Ahead of Another Busy Season

ceooutlook

Geoffrey Brown, CAE President and CEO, Illinois CPA Society

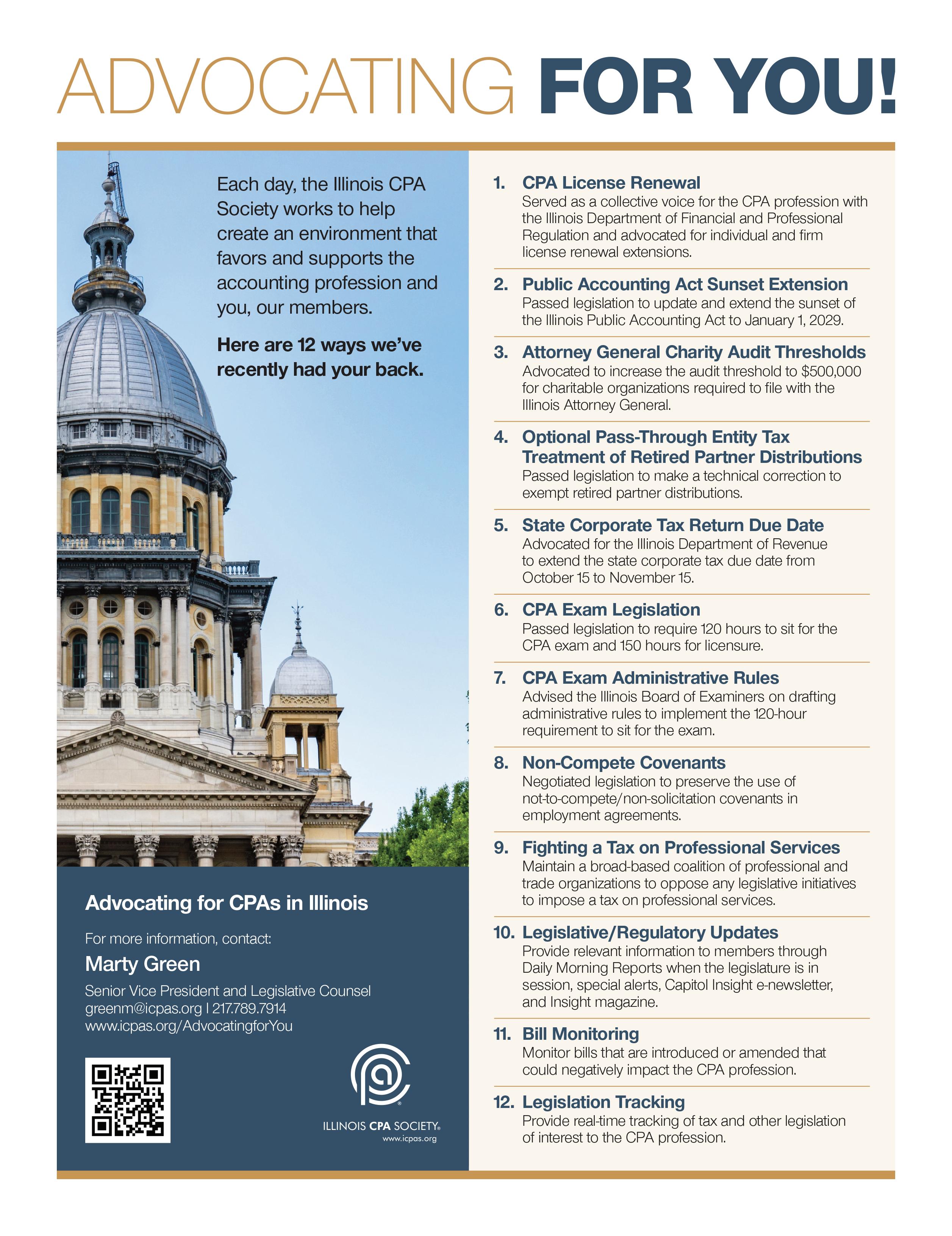

Advocacy: Looking Back to Move Forward

Our legislative successes in 2023 pave the way for important advocacy initiatives in the year ahead.

In a time of great turbulence and polarization, the advocacy efforts of professional organizations like ours are paramount. Among gridlocked legislative bodies, it’s imperative that we keep the lines of communication open and ensure our important advocacy agendas advance, as we have a duty to effectively represent the interests of our constituents and stakeholders before a variety of regulatory agencies. I can assure you that our entire Government Relations team and volunteers take their responsibilities very seriously.

Advocacy is one of our key pillars. We track a wide range of legislative, regulatory, and legal issues to identify policy matters potentially impacting CPAs and their firms, among others. We regularly engage federal and state policymakers to help ensure you have a say in the policies that impact the CPA profession and your business.

I’m proud to look back on 2023 and say that we met our legislative priorities. Our team worked diligently to see that the Illinois Public Accounting Act was successfully and meaningfully updated and extended through 2029 and that the charitable audit threshold was increased from $300,000 to $500,000. These important policy wins have paved the way for future efforts. Some of the issues that are front and center now include:

• Professional licensing processing delays and the Illinois Department of Financial and Professional Regulation’s plans for the upcoming CPA license renewal period.

• Local government audit backlogs.

• Compliance with the Corporate Transparency Act and new beneficial ownership information reporting requirements going into effect on Jan. 1, 2024.

While we work with stakeholders on these issues and advocate on your behalf, we also encourage you to get involved in the important issues that the CPA profession is facing. You can support our advocacy initiatives and policy efforts by getting engaged:

• Use your local legislative voice. When called upon, contact your legislators and regulators to amplify our messaging.

• Engage your local media. Media outlets often seek CPAs for their expertise and professional opinions on a wide variety of business and finance topics. Don’t be shy about engaging with media outlets in your area. Even sending a “letter to the editor” can be a surprisingly effective way of raising awareness of important issues and advancing our professional point of view within your local community and among your legislators and policymakers.

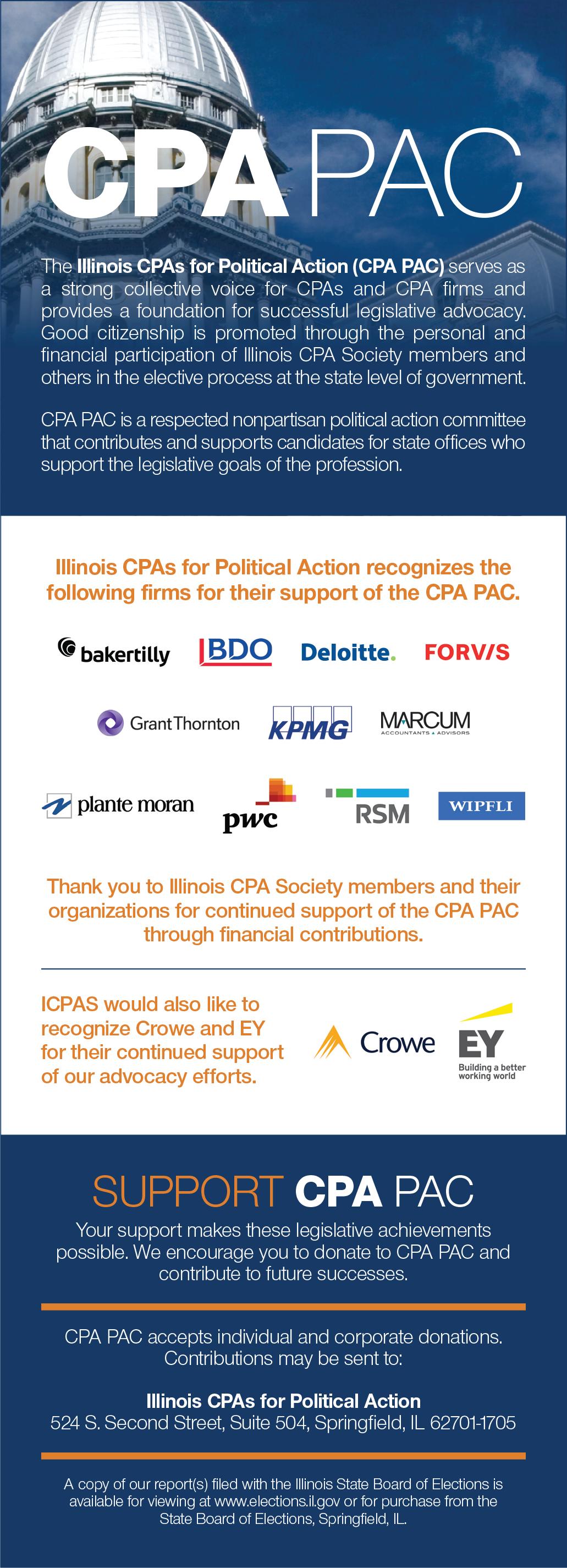

At the very least, stay knowledgeable of our advocacy efforts on your behalf by keeping up with our legislative updates, utilize our Advocacy Toolbox, and consider supporting the Illinois CPAs for Political Action Committee (CPA PAC). The CPA PAC is a wellrespected nonpartisan political action committee that supports candidates for state offices who support the legislative goals of the profession. The CPA PAC serves as a strong collective voice for CPAs and provides a foundation for successful legislative advocacy.

We represent not only you, our dedicated members, but also every current and prospective CPA throughout our state. Your involvement is integral to the success of our advocacy actions! I encourage you to stay aware, get engaged, and use your voice as a respected CPA in Illinois.

4 | www.icpas.org/insight

capitolreport

Martin Green, ESQ Senior Vice President and Legislative Counsel, Illinois CPA Society @GreenMarty

Are You Ready for Beneficial Ownership Compliance Reporting?

Small businesses, including CPA firms, will soon be required to report beneficial ownership information per the Corporate Transparency Act. Here’s what you need to know to prepare.

By now, you’ve likely seen a number of warnings on the upcoming beneficial ownership information (BOI) reporting requirements imposed by the Corporate Transparency Act (CTA). Beginning Jan. 1, 2024, the CTA will require small business entities in the United States and non-U.S. entities—including CPA firms—to report information about their beneficial owners (i.e., the persons who ultimately own or control the entities) to the U.S. Treasury Department’s Financial Crimes Enforcement Network (FinCEN).

Overall, the goal of the CTA and beneficial ownership reporting requirements is to combat “dirty money” issues, including tax evasion, money laundering, and other financial crimes. Though, I’d add that the name itself, “Corporate Transparency Act,” is somewhat deceiving in that the reporting requirements are far reaching for small businesses.

Of course, with the effective date fast approaching, now is the time to familiarize yourself with these reporting requirements. After all, being prepared to advise your clients or companies, and execute these required filings on their behalf, will be an essential service as their trusted and strategic advisor.

That said, here are some questions and answers you need to know:

1. What’s considered a reporting company? Generally, there are two types of reporting companies: domestic and foreign. A domestic reporting company is a corporation, limited liability company, or other entity created by filing with the secretary of state within the U.S. A foreign reporting company is a corporation, limited liability company, or other entity formed

under the law of a foreign jurisdiction and registered to do business in the U.S.

2. Are there exemptions? There are 23 types of entities exempt from reporting, many of which are already subject to substantial federal and state regulatory reporting and oversight. Generally, qualifying entities exceed $5 million in gross receipts and have 21 or more full-time employees. At first glance, it may appear that your accounting firm may be exempt from BOI reporting; however, exemptions only apply to firms registered with the Public Company Accounting Oversight Board as required by the Sarbanes-Oxley Act of 2022, and those with more than $5 million in gross receipts and 21 or more full-time employees.

3. What information needs to be reported? Entities required to meet the new reporting requirements are obligated to identify and report beneficial owners. Notably, beneficial owners are defined broadly in the CTA. If by chance a company is owned by another company, further inquiry will be necessary to identify the person owning the parent company. Overall, beneficial owners include those with substantial control, such as a person with indirect or direct ownership equal to or greater than 25% of the company, or a company applicant. For domestic entities, the company applicant is the person who directly files entity-creation documents with the secretary of state. For foreign entities, this would be the individual who first registers the entity to do business in any state.

Additionally, the company and beneficial owners and company applicants will have to respond to 50-plus questions, including

6 | www.icpas.org/insight

details about the reporting company, beneficial owners, and company applicants.

4. What are the penalties for not reporting? The final rule provides for both criminal and civil penalties for reporting violations. Civil penalties may include $500 for each day the violation continues. Criminal penalties may include up to $10,000 in fines and imprisonment of up to two years. My sense is the criminal process is reserved for willful misconduct and fraud.

Of course, entities must begin reporting BOI by Jan. 1, 2024, and must do so through FinCEN’s secure electronic filing system. All initial reports must be completed before Jan. 1, 2025, and any changes in previously reported information will require supplemental reporting within 30 days of those changes.

On Sept. 18, 2022, FinCEN released a guide to assist small entities in complying with the reporting requirements. The Illinois CPA Society (ICPAS) has posted this guidance and other resources on the Government Relations page of the ICPAS website.

With so much uncertainty surrounding these reporting requirements, ICPAS, along with the AICPA and other state CPA societies, have been working with their respective Congressional Delegation members to pass legislation extending the initial reporting deadlines. Additionally, ICPAS is part of a coalition of state CPA societies that signed onto an AICPA letter to FinCEN commenting on proposed agency regulations and asking for a delay in the BOI reporting implementation. As we continue to monitor this situation, we’ll of course provide any necessary updates to our members.

www.icpas.org/insight | Winter 2023 7

Managing Risk in Tax Season and Beyond

Now more than ever, CPA firms need to be proactive—not reactive—to potential risks associated with their client relationships. Consider these risk management tips as another tax season nears.

BY SUZANNE M. HOLL, CPA

• Deteriorating relations (e.g., not taking your advice, unresponsive, or acting in a way that suggests compromised integrity).

• Potential conflicts of interest.

ALTHOUGH the current tax year has shown signs of returning to more normalcy after the pandemic-induced chaos of recent years, CPA firms continue to face unique challenges and risks they shouldn’t ignore. In addition to trying to keep up with the increasing complexities of evolving tax laws and regulations (e.g., state passthrough entity taxes, K-2s/K-3s, etc.) and easing but ongoing challenges of working with the IRS and other taxing authorities, many firms are experiencing significant capacity challenges as they struggle to find and retain qualified talent to support and meet their clients’ service needs.

To mitigate these risks, firms need to prioritize performing the “right services” for the “right clients.” Here are three client-related questions to consider that may help you identify potential risks to your firm and position it for long-term success.

1. IS THE CLIENT STILL A GOOD FIT?

From a timing perspective, there’s no better time than now to review your client list to decide whether clients remain a good fit for your firm—and do so before and after every tax season. Disengaging from clients that don’t meet your firm’s needs will better position you going forward. Consider these red flags with clients:

• Difficult or uncooperative behavior (e.g., withholding critical information, argumentative, or disrespectful to firm members).

• Changes in a client’s business.

• Constantly questioning your fees or requesting a discount before services commence.

• Late, slow, or partial payments.

Pay particular attention to difficult or manipulative clients who are slow in accommodating your requests, don’t return your calls, or are unresponsive. When a client seems unwilling to provide you with the information needed to complete an engagement, assess the underlying cause: Is the problem merely sloppy recordkeeping or is the client deliberately delaying or withholding information? Be cautious in situations where it appears that documents are deliberately withheld or you’re urged by a client to proceed without appropriate or sufficient documentation.

Abrupt changes in a client’s behavior may be indicative of a failing business, financial problems, substance abuse, or other personal problems. Trying to uncover the source of the problem could be beneficial, but whatever you do, don’t ignore the warning signs of a deteriorating relationship. And always be on the lookout for potential conflicts of interest. It’s extremely important to examine potential or actual conflicts of interest from each party’s point of view.

Conflicts of interest have long been a major factor in professional liability claims against CPAs. Part of the problem is that if CPAs aren’t proactive and sensitive to their existence, potential conflicts of interest aren’t perceived before the incidents that trigger these claims. If potential conflicts are identified, you must assess whether

8 | www.icpas.org/insight RISK MANAGEMENT

you can objectively represent the parties involved, and if you determine you can, assess whether there are reasonable safeguards to eliminate or reduce the threat to an acceptable level.

2. IS THE ENGAGEMENT A GOOD FIT?

Firms who dabble in practice areas outside of their expertise have a much higher risk of having a claim. Learning the art of saying “no” to clients is an important, but often overlooked, risk mitigation tool. If clients seek your help with transactions or activities outside your comfort zone or skill set, you’ll be better served suggesting they seek the advice and counsel of professionals with expertise in those areas.

It’s important to recognize, embrace, and maintain your competencies. Frankly, this rule is fundamental to the profession, as the AICPA’s Code of Professional Conduct requires CPAs to only undertake professional services they can reasonably expect to complete with professional competence.

3. ARE YOU MANAGING CLIENT EXPECTATIONS?

Effective communication is a key factor in any CPA-client relationship, and when you work to stay informed and in control of managing client expectations, you help to safeguard your firm. To that end, good documentation is critical to successfully managing client expectations. Jurors (members of the public) generally consider CPAs to be experts in documentation, and falling short of that expectation may be viewed as negligent and perceived as performing below the standard of care. Consider these documentation tips:

• Utilize engagement letters. While these letters won’t immunize you from lawsuits, they can be your first line of defense if a client makes a claim against you. You likely already have executed engagement letters with your tax clients. However, to prevent engagement creep, memorialize the additional services by updating your letter or obtaining a signed addendum, clarifying the revised scope and limits.

• Always document significant meetings and communications. Follow up with written communications in circumstances including but not limited to:

- Change in engagement scope (may require a new engagement letter).

- Negative information (e.g., tax return is already late, client’s failure to timely provide information, or client is facing an audit).

- Judgment calls (e.g., aggressive tax positions taken by your predecessor).

- Client agreement to take significant action.

- Conversations regarding transactions, extensions, or estimated tax payments.

• Advise clients of opportunities and risks. Consider obtaining a tax representation letter or stand-alone certification letter to mitigate high-risk scenarios, such as:

- If your firm is preparing amended income tax returns to reflect employee retention credit (ERC) adjustments as required by the taxing authorities, and the firm isn’t responsible for assessing or opining on the client’s eligibility for the ERC, it’s recommended to have the client sign a tax representation letter in addition to having a signed engagement letter for such services. This added defensive documentation will help protect the firm if clients later allege that the firm should’ve opined regarding ERC eligibility, and/or if clients later allege the firm didn’t appropriately advise them of the potential risk given the extended statute of limitations afforded by the IRS

for assessments without a corresponding extension for taxpayers to pursue refunds on the income tax returns.

- For clients with known extensive digital asset transactions, it may be prudent to have them sign a tax representation letter or a stand-alone certification letter at the conclusion of the engagement addressing crypto asset implications. This additional defense provides evidence of the client’s understanding and acceptance of their responsibilities regarding digital asset transactions and the limitations of the services your firm provided.

- In addition to the above examples, there’s a new area of potential risk associated with the Corporate Transparency Act (CTA), which introduces a new and expansive reporting regime for entities deemed to be reporting companies. Therefore, CPA firms are strongly recommended to inform and advise their clients of the beneficial ownership reporting requirements under the CTA.

• Ensure written documentation is factual, professional, and without personal commentary or unsubstantiated opinions. Unprofessional or inappropriate comments can damage documentation integrity. Ask yourself whether your documentation would be helpful or harmful if presented at trial.

• Mind fees, billings, and collections. The challenging economy has brought fee issues to the forefront as some clients struggle to meet their financial commitments, including bills owed to their CPAs. Good communication with non-paying clients is important and may spur payment. At the very least, contemporaneously memorialized communications create a defensive documentation trail demonstrating that the client, by not responding to your communications, didn’t have a valid basis to claim your fees weren’t owed. When dissatisfied with work, clients normally respond to such communications by detailing their dissatisfaction.

• Strategically and respectfully disengage. Skillfully handled transitions can be mutually beneficial to firms and clients. However, care is needed when disengaging from engagements after they’ve begun. Disengaging too late and without sufficient cause may increase the likelihood a firm could face allegations of damages if the successor is unable to meet the deadline. Whether you decide to disengage with a specific client, type of business, or area of practice, it’s extremely important to terminate relationships professionally, formally, and in writing. At a minimum, your disengagement letter should always contain clear statements, a description of your work, and a list of any due dates or filings. When done effectively, disengagements are a good risk management tool for your firm, and knowing how to execute them skillfully and professionally will help you grow your practice and avoid potential liability exposure.

• Report potential claim situations early. Promptly report potential claims, including potential errors or omissions. Doing so protects your firm’s full policy limits.

Above all, it’s important to tread carefully when working with any client. Be sure to arm yourself with knowledge, know your limitations, and be willing and able to say “no” to some clients— your firm’s reputation and success depends on it.

Suzanne M. Holl, CPA, is senior vice president of Loss Prevention Services with CAMICO. With more than 30 years of experience in accounting, she draws on her Big Four public accounting and private industry background to provide CAMICO’s policyholders with information on a wide variety of loss prevention and accounting issues.

www.icpas.org/insight | Winter 2023 9

The Like-Kind Exchange Home Sale Strategy

As home values rise, tax structuring becomes more important in how your clients sell their homes.

BY DANIEL F. RAHILL, CPA/PFS, JD, LL.M., CGMA

SINCE the beginning of the COVID-19 pandemic, median home prices in the United States have skyrocketed, increasing by 41.6% from March 2020 to July 2023 as inventories have declined, according to the National Association of Realtors. The pandemicdriven shift to remote work, increasing demand for suburban and rural homes, and formerly low interest rates combined to accelerate demand and home values.

More recently, a significant rise in interest rates has limited the supply of homes for sale, as homeowners who had locked in low interest rate mortgages don’t want, or can’t afford, to give up those low rates to purchase a new home. The decreased inventory of homes for sale has further driven up values, and at this point, many homeowners have significant unrealized capital gains embedded in their homes well in excess of the home sale exclusion.

For taxpayers who find themselves in this situation, thoughtful tax planning is essential. One possible solution could be a like-kind exchange (Internal Revenue Code [IRC] Section 1031). Here’s how this home sale strategy can help your clients be more tax savvy while navigating today’s real estate market.

UNDERSTANDING THE TAX CONSEQUENCES

Capital gains tax should be a significant consideration when selling an appreciated home. It applies to the profit made from the sale and is categorized into two types: short-term capital gains and longterm capital gains. Short-term capital gains are applied to properties held for one year or less, while long-term capital gains apply to properties held for more than one year.

Short-term capital gains are taxed at ordinary income tax rates, which can be significantly higher compared to long-term capital gains. Long-term capital gains typically benefit from preferential tax rates of 0%, 15%, or 20%, depending on your client’s taxable income and filing status. Married filing jointly (MFJ) couples can qualify for

10 | www.icpas.org/insight

TAX PLANNING

the 0% capital gains tax rate if they have 2023 taxable income of less than $89,249. If they have taxable income of more than $89,250 but less than $553,849, they qualify for the 15% capital gains tax rate. If their taxable income is more than $553,849, they’ll qualify for the top 20% capital gains tax rate.

A taxpayer may also be subject to an additional 3.8% surtax on net investment income (NII) on a sale. NII includes capital gains, dividends, taxable interest, annuities, royalties, passive rents, and certain income from passive activities, and it increases the top tax rate to 23.8% on long-term capital gains. The NII tax, commonly referred to as the “Medicare surtax,” applies to MFJ couples with modified adjusted gross incomes (MAGIs) exceeding $250,000 and to single filers with MAGIs exceeding $200,000. These income thresholds aren’t indexed for inflation, so an increasing number of people are subject to the tax. If your client is in a high-tax state, the combined capital gains, NII, and state taxes could exceed 30% on the realized gain. For example, a $4 million gain could easily result in a tax bill of $1.2 million or more.

THE BUY AND HOLD STRATEGY

Perhaps the simplest, but least desirable, capital gains tax planning strategy is to hold an appreciated asset until death. When appreciated property transfers to an heir at death, its cost basis is adjusted (i.e., stepped-up) to fair market value at that time. Should the heir decide to immediately sell that asset after receiving it, there would be no capital gains tax associated with the sale because of the step-up in basis to fair market value. For your clients who want to hold on to their homes long term, this could be the best tax strategy.

THE HOME SALE EXCLUSION RULE

The Taxpayer Relief Act of 1997 repealed a longstanding rollover rule that allowed homeowners to defer recognition of capital gains from the sale of a principal residence. Instead, the replacement Home Sale Exclusion Rule permanently eliminates the tax on capital gains realized up to $500,000 for MFJ taxpayers and $250,000 for single taxpayers. For your clients to qualify, the property being sold must be their primary residence and they must have lived in it for at least two of the last five years before the sale.

THE LIKE-KIND EXCHANGE

A like-kind exchange (IRC Section 1031) allows the seller to defer capital gains taxes by reinvesting the proceeds from the sale of the real estate held for investment into a similar real estate investment property. To qualify, your client must meet several requirements.

For example:

• The exchange must be completed within 180 days of the sale of the relinquished property. Rental real estate is considered likekind property; real estate investors can exchange rental property for other rental property.

• To obtain fully tax-free treatment on the exchange, the replacement property must be identified within 45 days of the sale of the relinquished property, the cash proceeds from the exchange must be fully applied toward the acquisition of the replacement property, and the value of any debt on the relinquished property must be replaced with equal value on the replacement property.

• Both the relinquished property and the replacement property must be held for investment or used for productive use in the taxpayer’s trade or business. This is important to prove intent should the business purpose of the exchange be called into question.

CONVERSION OF A RENTAL TO A PRIMARY RESIDENCE

Converting a primary residence into a rental property doesn’t disqualify your clients from a like-kind exchange, but all the rules must be followed. Rev. Proc. 2008-16 provides a safe harbor for taxpayers who exchange their rental or investment property under IRC Section 1031. To qualify, your client must meet the following requirements:

• The relinquished dwelling unit must be owned by your client for at least 24 months immediately before the exchange.

• Within the 24-month qualifying use period, in each of the two 12month periods immediately before the exchange, your client must rent the dwelling unit to another person(s) at a fair rental rate for 14 days or more.

• The period of your client’s personal use of the dwelling unit must not exceed the greater of 14 days or 10% of the number of days during the 12-month period that the dwelling unit is rented at a fair rental rate.

• The replacement property must continue to be owned by your client for at least 24 months immediately after the exchange. Similar rules for rental and personal use (as noted above) will apply to the new property following the exchange.

If your client meets all Rev. Proc. 2008-16 safe harbor requirements, the IRS will not challenge the IRC Section 1031 transaction. This allows a taxpayer to defer the recognition of a capital gain on the exchange. The tax basis of the home exchanged would carry over to the new property.

CONVERSION OF A VACATION HOME TO A PRIMARY RESIDENCE

After the two-year requirement is met, your client can convert the investment property to a primary residence. However, upon later sale of the new residence, some of the gain could be ineligible for the home sale exclusion. The ineligible portion of the gain would be based on a ratio of the time that the home was a second residence or investment property to the total time that your client owned the property. The remaining gain would be eligible for the $250,000/$500,000 home sale exclusion.

Finally, IRC Section 1250 depreciation recapture rules could apply to a later sale if your client took depreciation deductions on the property while it was a rental. When depreciable real estate is held for more than a year and sold at a gain, previously deducted depreciation must be recaptured and taxed at a 25% top rate. Of course, if your client holds on to the home until death, these taxes would be avoided, and the property would receive a step-up in basis for the heirs.

Buying or selling a home is a stressful, complicated process— especially in an undesirable market. A like-kind exchange could be a valuable tax planning tool for a client looking to sell their home, but the rules are complex and must be adhered to. As qualified tax professionals, our strategic advice is paramount. If you can help your client plan four years in advance, the like-kind exchange strategy can be effective in deferring capital gains taxes when acquiring a new home.

Daniel F. Rahill, CPA/PFS, JD, LL.M., CGMA, is a wealth strategist and creative tax writer at Wintrust Wealth Management. He’s also a former chair of the Illinois CPA Society Board of Directors and is a current officer and board member of the American Academy of Attorney-CPAs.

www.icpas.org/insight | Winter 2023 11

What the Future of Accounting Really Needs

If the accounting profession is to remain relevant to future generations of workers, changes in work-life balance, diversity, and pay are needed now.

BY SETH FINEBERG

If we’re going to make accounting a more attractive career to pursue and stay in, I believe there are three things the profession needs to embrace.

1. A FLIP TO ‘LIFE-WORK’ BALANCE

I’VE said this in a multitude of ways, but I think it’s time to spell it all out: If the accounting profession is to thrive, let alone survive, some serious changes need to occur—and in fairly short order.

This is a profession I’ve observed, and thankfully gotten to know closely, for more than two decades. In that time, I witnessed a few major setbacks and milestones: the impact of the Sarbanes-Oxley Act of 2002, multiple recessions, and the more recent digitalization and automation of the profession, to name a few.

But nothing, in my view, has impacted the profession more than the global pandemic. Any hesitations about automation, cloud utilization, and remote work had to be dealt with head on, because it was the only way work could get done. Firms large and small—even those that felt they couldn’t ever work from home or utilize cloud or automation tools—were forced to reckon with their new reality, which was only compounded by what seemed like a never-ending tax season and a lack of acceptable guidance from the IRS about the employee retention credit and Paycheck Protection Program.

The result? For the first time since I began covering this profession, I saw accountants literally in tears with claims they officially wanted out of accounting altogether. A growing number are simply saying they’ve had enough. It’s understandable that the numbers of accountants entering the profession and still available to do the work are in decline.

The idea of work-life balance has been discussed for years. For professionals who are required to regularly earn continuing professional education credits to retain their credentials, on top of working likely anywhere from 60 to 80 hours per week during the multiple busy seasons throughout the year, balance is a bygone for anyone looking to get ahead. At some point, we have to say “enough.”

Therefore, I believe the concept of work-life balance has to be flipped to life-work balance, which prioritizes people’s time, sanity, and sense of purpose. I’m not suggesting the profession should accept that the needs of clients or companies be ignored, but a pathway to “balance” where both people’s and businesses’ wellbeing matter. This profession needs to set boundaries and stick to them. Let that be the norm.

Just consider the cyclical nature of what’s accepted (in an almost dystopian rite of passage) as “busy season.”

This cycle of abuse accountants endure year in and year out, to the point at which I’ve seen so many want to leave the profession because they simply can’t take it anymore, has to end.

It’s also time to say “enough” to the expectation that serving bad clients, extra hours, working weekends, and completing the majority of work during predetermined blocks of time is just the way it is. If these things don’t change, the profession will never be attractive to future generations of accountants.

12 | www.icpas.org/insight PROFESSIONAL ISSUES

2. A CONTINUED PUSH FOR DIVERSITY AND INCLUSION

Saying and doing uncomfortable things isn’t necessarily in the DNA of accountants. But, as is the theme of this article, accountants are humans and need to treat themselves—and others—as such. In order for this profession to progress and be one people want to come into, those of us in it now need to help foster a more diverse and inclusive work environment and community.

When I first began covering accounting more than 20 years ago, the number of women in leadership positions was a paltry few, as white males dominated those roles. Calls for this to change were heard and, while there’s still a long way to go to achieve true balance, today there are far more women leaders in the profession than ever before.

When it comes to people of color in leadership roles, that number is still a paltry few and doesn’t begin to reflect the demographics of our country. I believe this profession has to begin to reflect the society it serves if it’s going to be a welcome career choice.

This may be an uncomfortable conversation (for some) to have, particularly for those currently in leadership roles, but we must face the fact that our country has a deep history of not being inclusive or equitable. Allowing people to be their authentic selves at work has become as important as the life-work balance I mentioned above, if not more so.

Collectively, the profession has to do far better than it has and offer more than just lip service to become truly inclusive. People want to work in an environment where they’re seen and judged equally on their merits as professionals.

3. AN HONEST CONVERSATION ABOUT PAY

Finally, it’s time for the profession to have an honest conversation about compensation. Regardless of where you live, starting and even mid-level salaries for accountants simply aren’t high enough to justify one’s investment in education and professional development. Those well established in the profession know that a lucrative career may arise, but students and young professionals have a very hard time seeing when, or if, a payoff awaits. Just look at the starting salaries Robert Half’s 2024 Salary Guide estimates for the roles students and young professionals are commonly hired into:

• Associate, audit/assurance services: $49,000

• Tax associate: $52,750

• Senior associate, audit/assurance services: $57,750

• Senior tax associate: $67,250

If compensation doesn’t become more competitive with entry-level roles in comparable professions, the number of students pursuing accounting careers will certainly continue to decline.

I’ve seen time and again that the accounting profession can adapt and change when it needs to. Now is another time that it needs to. If this profession is to have a future, that change needs to be driven by those of you in the profession now. You all have the means to inspire change and help redefine what it means to be an accounting professional.

Seth Fineberg is an independent consultant to the accounting profession, working with firms and vendors that serve it. He’s been a journalist and editor for over 30 years, spending most of his career as an editor with Accounting Today and AccountingWEB.

www.icpas.org/insight | Winter 2023 13

What Drives Difficult Auditor-Client Interactions?

The relationship between an auditor and their clients is very complex and often met with conflict. Here, researchers explore these dynamics to identify areas for improvement.

BY JOSHUA HERBOLD, PH.D., CPA

WHEN I teach accounting courses, the students and I start off in what I call “Homeworkland.” In Homeworkland, the numbers work out nicely, all the characters behave ethically and rationally, predictions are accurate, the rules are clear, and there’s one—and only one—answer to every question. While visiting Homeworkland, we gloss over the intricacies of human motivation—not to mention the interaction of multiple humans and motivations—so that we can focus on learning the material in its most basic form. Pretty quickly, we leave Homeworkland and talk about the complicated and oftentimes messy “real world” because, of course, that’s where we actually live, and things get interesting here.

THE REAL WORLD

While audit regulation assumes that clients cooperate with and are helpful to auditors, experts warn that isn’t always the case.

Recent research from Christine Gimbar, Ph.D., MAcc, associate professor of accounting and management information systems at DePaul University, and her co-authors Melissa Carlisle, CPA, Ph.D., assistant professor at Case Western Reserve University, and J. Greg Jenkins, Ph.D., MS, professor at Auburn University, examines what happens when auditors leave Homeworkland and start working with real people. Discussing their research article, “Auditor-Client Interactions—An Exploration of Power Dynamics During Audit Evidence Collection,” Gimbar notes: “The relationship between the auditor, the audit client’s management, and investors is very complex. Management pays the auditor, but the auditor is working for investors, and the audits are mandated by U.S. Securities and Exchange Commission (SEC) regulations. So, there’s an issue because the auditor is supposed to be protecting the public interest, but when I was in practice, we’d always talk about having a client service role and working with the client to conduct the audit. That’s a really difficult dynamic to navigate.”

Gimbar and her co-authors began their exploration of this dynamic by interviewing staff auditors (associates and seniors) from Big Four

14 | www.icpas.org/insight AUDITING

and regional audit firms. The interviews were conducted on a semistructured basis; the same five pre-written questions were used to guide each interview, but the researchers interrupted the interviewees as little as possible to allow them to discuss any aspect of their audit experiences.

“Basically, what we're trying to look at is how interactions go between staff level auditors and their clients during audit evidence collection. How do they ask the client for information and data? How do they obtain those things? How do they encounter clients?” Gimbar says.

Interactions between staff auditors and clients are especially important today considering more complicated tasks are being driven down to lower levels of the audit team. According to the AICPA’s CPA Evolution webpage, “Procedures historically performed by newly licensed CPAs are being automated, offshored or performed by paraprofessionals. Now, entry-level CPAs are performing more procedures that require deeper critical thinking, problem-solving, and professional judgment, and responsibilities traditionally assigned to more experienced personnel are being pushed down to the staff level.”

AUDITOR-CLIENT INTERACTIONS: A SOCIAL MISMATCH

While conducting interviews, Gimbar and her co-authors uncovered an apparent “social mismatch” between staff auditors and their clients, with all auditors stating they had a negative experience. Here’s what they learned:

• Client personnel sometimes exert control over the audit through unfriendly and hostile behaviors.

• Interviewees often feel inexperienced and unprepared for client interactions.

• Addressing challenging audit issues can lead to difficult interactions.

While there are no studies that measure the proportion of audit clients that are unfriendly or hostile to the auditors, Gimbar says, “The one thing we can hang our hat on is, when we asked about negative or hostile client interactions, every single person could tell a story. Every staff auditor we interviewed had that experience.”

Notably, staff auditors often felt that client personnel didn’t understand the purpose of the audit or why the staff auditors were requesting particular pieces of information. Unfriendly clients also tended to show a misunderstanding of the audit methodology and sometimes even questioned the abilities of the auditors.

As one interviewee noted: “The controller didn’t directly say that we were dumb or anything, but she told us both that we don’t know anything, that we shouldn’t need to ask these questions every year, and, you know, she’s an expert in what she does, and we’re not qualified to do this.”

Other negative auditor experiences included interactions with unfriendly clients who:

• Were in a bad or temperamental mood.

• Required auditors to formally request meetings with client personnel (as opposed to informal conversations).

• Ignored or were slow to reply to information requests.

• Claimed requested documents had already been provided.

• Effectively forced auditors to conduct remote audits.

• Frequently moved the engagement team from one room to another.

Most interviewees also felt inexperienced and unprepared relative to their clients. These kinds of interactions clearly have the potential to impact audit results. One interviewee described it this way: “Let’s say you don’t mesh well with the controller, your main person getting you information and answering 80% of your questions for the audit. There’s no one else to go to. So, you’re kind of stuck.”

Additionally, while prior research has shown similar social mismatches between staff auditors and clients, Gimbar says the effect is likely to be worse now that more client engagements are being performed by newer CPAs: “We hear from firms who say, ‘We want to hire students who we can put in front of clients.’ They want to hire students that can interact with senior client personnel. But greater differences in experience, knowledge, and age lead to greater social mismatches in auditor-client interactions, and audit staff feel it.”

HOW DO STAFF AUDITORS RESPOND?

When responding to or dealing with unfriendly clients, Gimbar says staff auditors reported spending more time:

• Preparing for interactions.

• Getting help from other auditors on the engagement team.

• Explaining the relevant audit issue to client personnel.

• Ingratiating themselves to the client.

Interviewees also reported sometimes delaying client interactions or avoiding clients.

In the first two interviews they conducted, Gimbar and her coauthors noticed that both interviewees, while talking about avoiding clients, mentioned something that the researchers refer to as “ghost ticking.” In academic research, ghost ticking is more formally known as a “premature signoff,” which happens when auditors document having completed tasks without actually having performed those tasks.

In fact, nearly half of the interviewees said they had engaged in ghost ticking and one-third reported that they were aware of ghost ticking done by others.

“These behaviors absolutely can affect audit quality,” Gimbar warns. “Our project is one of the first few papers to document that ghost ticking happens. Not only is it happening, but staff auditors are willing to admit to it and tell us about it. They may think to themselves, ‘My work is low risk, what I’m doing isn’t all that important. Will this really change the audit opinion? Probably not.’ But that audit evidence is the foundation for everything else in the audit.”

Overall, Gimbar stresses interactions with unfriendly clients can be and need to be improved if we want to retain CPAs in the audit profession: “I’m a former auditor. I’m trying to improve auditors’ experiences and, in turn, attract people to the profession.”

Importantly, both auditors and clients have roles to play in improving their interactions. On the client side, they need to understand that auditors aren’t coming in to do an efficiency audit—these audits are required by the SEC. And on the auditor’s side? “There needs to be more coaching of staff auditors on difficult interactions,” Gimbar suggests. “That way, staff can be prepared for the worst but hope for the best.”

Joshua Herbold, Ph.D., CPA, is a teaching professor of accountancy and associate head in the Gies College of Business at the University of Illinois Urbana-Champaign and sits on the Illinois CPA Society Board of Directors.

www.icpas.org/insight | Winter 2023 15

CORPORATE STRATEGY & FINANCE

Preparing for the IPO Comeback

Will initial public offerings (IPOs) return big in 2024? Many experts are saying yes— here’s what CPAs and CFOs need to know now to prepare.

BY JEFF STIMPSON

AS both investors and issuers wait for market conditions to improve, the initial public offering (IPO) backlog continues to expand. As of Nov. 2, 2023, there’s only been a meager 133 IPOs so far this year, trailing 2022’s 181, according to the market observer site Stock Analysis. This is a dramatic decline from 2021’s massive 1,035 IPOs.

According to Kiplinger, looming IPOs to watch for in 2024 include online retailer Fanatics, tech companies Cerebras Systems and Waystar, and travel services company Navan, among others. Health care, fintech, artificial intelligence, and green energy companies are also expected to be among hot issues in the coming year.

In other words, all signs point to a more fervent offering revival in 2024. Here’s what CPAs and chief financial officers (CFOs) should do now to get their clients and companies ready for an IPO.

MIND THE IPO PREDICTIONS

During Deloitte’s recent “Path to Public Series: IPO Readiness Panel and Presentation,” experts predicted an uptick in equity activity to close out 2023, with even more activity in 2024, particularly in the first half of the year as companies look to get ahead of the United States presidential election in November. Jim Clayton, BDO’s private equity national co-leader in Philadelphia, notes that most surveys show an expected improvement in valuations by the second half of 2024. In fact, a recent poll by his firm showed that 80% of respondents believe an optimal IPO market will return in 2024.

But elections bring up more uncertainty, says Dean Quiambao, partner at Armanino in San Ramon, Calif. “Because of the uncertainty, I predict there will be a big concentration of companies going public in the second quarter of 2024,” he says. “Right now, you see companies dipping their toes and trying to assess the uncertainty—they’re trying to give themselves more runway for more profit and better numbers to tap the public market.”

“In days past, it was good enough for companies to say, ‘We have enough sizzle here, and we can sell the sizzle.’ What CFOs are now saying is once their companies reach profitability or have a very clear path to profitability, they’ll try to go public because a stall in the IPO market doesn’t last forever,” Quiambao says.

A tighter credit market is also driving companies to seek cash elsewhere. While some entities have been creative in debt and other financing, Gary Klintworth, senior managing director at CBIZ ARC Consulting LLC in San Francisco, notes that growth is difficult without funding or cash flow.

“Stripe, Instacart, ARM, and Klaviyo have been anticipated IPOs for several years, so these are exceptions. However, there’s an appetite for companies to tap the public markets for funding, even at lower valuations, in order to create some liquidity,” Klintworth says.

GET IPO READY

Clayton says companies thinking about IPOs shouldn’t wait long to start getting ready: “When looking back at the downturn in IPOs during the financial crisis, it’s important to mind that many companies waited, and in some cases waited too long, to start the IPO process and therefore weren’t ready when the market turned.”

16 | www.icpas.org/insight

Getting ready might involve a new way of documenting operations. Certain provisions of U.S. generally accepted accounting principles for public entities differ from those for non-public entities. For instance, public business entities are generally required to adopt new accounting standards before private companies, and a company undertaking an IPO must present financial statements that are consistent with public-entity accounting principles and must comply with the disclosure requirements for public entities for all periods presented.

Other topics where accounting principles or disclosures may apply to public entities but not to non-public entities include earnings per share, segment reporting, temporary equity classification of redeemable securities, certain income tax-related disclosures, and certain disclosures related to pensions and other postretirement benefits.

When it comes to getting IPO ready, it’s often best to get some help.

“Accounting firms can help companies evaluate their systems, processes, and people, as well as their overall financial, management, and IT controls,” Klintworth says. “In addition, being able to forecast accurately is an area where assistance is necessary. Having good advisors in place to assist in the heavy lifting and pre- and post-IPO staff augmentation, outsourcing, and co-sourcing is critical.”

Clayton says that accounting firms often start by assessing the current organization—its people, processes, technology, and recent audits—to understand what’s needed to get to an IPO: “Providing a client with a roadmap and plan from the start to IPO filing, as well as guidance for operating as a public company after the flip, is important.”

When helping clients through an IPO transaction, firms should keep their clients focused on the goal of long-term growth—not just nearterm profitability. The reality is, according to Deloitte, that planning should start anywhere from 18 to 36 months in advance of the anticipated IPO date. During this time, companies should work to:

• Develop a business model with sustainable growth potential.

• Assemble a strong team for the IPO journey and beyond.

• Build a solid business infrastructure and implement systems that facilitate financial planning and forecasting.

• Prepare for a smooth financial reporting close process and develop appropriate risk management practices.

• Allow adequate time to ramp up for the IPO.

“Prior experience with an IPO, especially for the CFO, is extremely beneficial, and it’s also a comfort to the investment bankers and attorneys involved in a deal,” Clayton adds.

Unfortunately, prior experience with an IPO isn’t common, says Guy Gross, Chicago-based SEC practice leader with RSM US LLP: “For most smaller IPOs, it’s a first-time experience for the company’s accounting personnel. In these cases, allowing the appropriate amount of prep time is invaluable to ensuring the process goes as smoothly as possible.”

Gross suggests this poses an opportunity for accounting firms to step up further as strategic advisors and ensure their clients not only engage with and bring in the appropriate consultants for a successful IPO process but also develop their internal teams to thrive throughout and after the IPO. Gross notes this could include forging relationships with investment bankers, Securities and

Exchange Commission (SEC) attorneys, and consultants who assist with IPO readiness. It could also include helping the client to develop internal control documentation and testing and learn how to prepare quarterly and annual SEC filings, among other matters.

Gross says firms should also work closely with the consultants to ensure their clients are doing everything necessary before they go public, including complying with all the SEC reporting requirements: “Closing the books and issuing financial statements in 45 days for a quarterly filing is very quick—likely much faster than the company performed these tasks as a private company. Some companies believe they have the bandwidth to prepare for the IPO and also do all of their daily activities. This can be a big mistake.”

Klintworth stresses that nobody is ever really ready to be a public company.

“Companies need to show that they can execute on their business plans, financial projections, and key metrics for two to three consecutive quarters prior to being in a great position to prove IPO readiness. Systems, processes, and people must also be in place in order to scale,” he says.

“When you think of the big picture, the goal isn’t to just go public,” Quiambao says. “The goal is to be a successful public company that’s ready and able to consistently grow its market value.”

Jeff Stimpson is a New York-based reporter and has covered tax for 20 years. His work has appeared in various business and general interest publications, including Accounting Today and Financial Advisor magazine.

www.icpas.org/insight | Winter 2023 17

Treasuring Stability

Managing Corporate Cash in an Uncertain Economy

Preserving cash, capitalizing on opportunities, and remaining flexible are key moves for any finance team during uncertain times. Here, six finance experts share added advice for managing treasuries today.

BY TERI SAYLOR

18 | www.icpas.org/insight

www.icpas.org/insight | Winter 2023 19

tAits core, effective treasury management plays an instrumental role within a company’s strategic plan, helping drive decisions across all financial areas, including capital planning, internal budgeting, overall growth planning, risk management, and relationships with customers and suppliers.

Of course, instability and uncertainty in the financial sector— whether due to stubborn inflation, rising interest rates, threats of a looming recession, global conflicts, lingering pandemic impacts, or other factors—have challenged traditional treasury management tactics in recent years.

Fortunately, companies are finding ways to adjust. In fact, recent studies suggest chief financial officers (CFOs) and chief executive officers (CEOs) in the United States are slowly becoming more optimistic about the economy again.

According to the AICPA & CIMA 3Q 2023 Business and Industry Economic Outlook Survey, 29% of respondents, including corporate decision makers, are optimistic about the economy, up from 14% in Q2. Further, 45% reported they’re optimistic about their own organizations. Additionally, respondents reported making higher projections for revenue and profits in the year ahead.

Yet, despite these positive responses, organizations of all sizes remain wary of the impacts of high inflation and interest rates, along with the state of the workforce (39% of survey respondents reported the need for additional employees).

As such, corporate finance leaders are turning to shrewd treasury management strategies to weather the current economic environment and be positioned to quickly react to opportunities that arise, like a strategic acquisition or purchasing incentive from a supplier.

“A properly managed treasury strategy should create flexibility to manage through various fluctuations in the economy,” says Anthony J. Gattuso, senior vice president and director of commercial banking at BMO Commercial Bank. “Regularly reviewing your treasury management goals—including with key partners—can help you tailor your strategy and stay on track in your efforts to moderate risk and improve predictability of your cash cycle.”

For Carla Tolomeo, assistant vice president at BMO Commercial Bank, treasury management today is about remaining nimble: “Companies that are nimble will fare better than those that are cumbersome and slow to take action.”

Double Down on Debt

For watchful companies, accelerating debt repayment has paved a pathway to stability.

Frank Cesario, CEO and director at Yunhong Green CTI Ltd., a manufacturer of film-based products, relied on forecasting strategies to pay down his company’s debt five years ago in anticipation of rising interest rates.

“Although we had experienced interest rates near zero for an extended period of time, we knew it wouldn’t last forever,” he says. “We determined we owed too much money and went through a dedicated process to bring that down.”

Today, he says his company’s debt load is about a quarter of what it used to be.

“Imagine how much more exposed we’d be to the recent rise in interest rates if we still had that debt load,” he notes.

Point being, as borrowing costs have climbed to highs not seen for decades, Cesario urges corporate finance leaders to be mindful of eliminating costly, and possibly crippling, debt as soon as possible. That could be done through a variety of strategies, whether through accelerated payments, raising capital, refinancing, or other moves relevant to the company’s financial position.

Notably, both Gattuso and Tolomeo agree that paying down debt to free up cash is key to enabling companies to remain flexible now.

Remember Cash Is King

“Cash is king, and cash flow is the lifeblood of any business,” Gattuso stresses. “An effective treasury management strategy can help unlock working capital capacity, reduce reliance on debt and exposure to related borrowing costs, and create flexibilities to manage through down cycles.”

Generally, for businesses in a well-capitalized cash position, Gattuso suggests balancing strategy around operating cash, reserve cash, and strategic cash that’s forward looking.

“In an environment with a relatively flat or inverted yield curve, businesses are largely keeping excess cash in short-term bank products, such as liquid money market accounts, which are producing attractive returns while maintaining more immediate access to cash,” he says.

Cesario advises taking an aggressive approach to maintaining liquidity for practical needs, like funding operational expenses (e.g., payroll, mortgages, and rent).

“You can only survive on borrowed funds for so long,” he stresses. “While debt can be a strategy for lengthening the runway to achieve

20 | www.icpas.org/insight

success, don’t assume you can keep borrowing indefinitely—I’m not aware of any business model that can make that work.”

However, managing working capital comes with its own risks, says Derek Sasveld, CFA, director of investment strategy and research at Busey Wealth Management, who advises finance executives to closely watch interest rates. He predicts the Fed may stop raising lending rates, which could begin lowering short-term investment rates in the early part of 2024.

“If you’ve become accustomed to earning 5.5% on your money market accounts, prepare for lower interest rates in 2024 and 2025,” Sasveld cautions. “To protect against that to some extent, maybe consider going out a little longer in terms of the maturity of the investment products you buy.”

Additionally, Sasveld urges caution when balancing the need for liquidity against the desire to earn the highest interest rates available.

“Weigh the return on investment when considering your cash management strategy. Working capital is supposed to be conservatively invested,” he says. “It’s one thing to paint around the edges to earn a little extra yield if you want to take some risk to do that. But if you're managing corporate cash for working capital, you need to play it safe and build in protections against potential negative market fluctuations.”

Seek Strategic Opportunities

In today’s fast-paced and fickle financial markets, even small fluctuations can make a significant impact on an organization’s bottom line. Implementing a robust treasury risk management framework that enables CFOs to assess and manage threats associated with cash and investments, such as interest rate

changes, currency fluctuations, and other market factors that impact a company’s financial position, is essential to ensuring long-term stability and staying poised to seize opportunities that come along.

“Companies should always be thinking about how to best position themselves to manage risk and take advantage of opportunities,” Gattuso says. “For the first time in many years, businesses have an opportunity to think more strategically about how they deploy their excess liquidity given the currently more rewarding interest rate environment.”

Peter Moirano, director of liquidity sales at BMO Commercial Bank, believes economic cycle changes create an environment ripe for opportunities. Currently, he’s seeing activity in the mergers and acquisitions market from corporations that have held cash in their strategic reserves earmarked for taking advantage of the changes in the current economic cycle.

“Companies that haven’t been well-managed during stressful times create opportunities for stronger corporations to acquire them,” Moirano says. “Those that have liquidity and are well-positioned to take advantage of these opportunities will benefit in the long term.”

Other disruptions, like supply chain backups, have also created opportunities for corporate leaders to strategically capture inventory.

“When there’s stress in the supply chain system, there’s a tendency for companies to try to overorder and for suppliers to try to overproduce. When things normalize, that buyer or producer may need to unload the excess inventory they’ve stored up, setting up great buying opportunities for other companies with liquidity that can take advantage of the situation,” Moirano says. “Simply, liquidity enables companies to be flexible, pivot, and move quickly.”

Listen to Learn

For Robert Chan, treasurer at Underwriter Laboratories LLC, having a strong foundation in treasury management is key to mitigating financial risk, managing liquidity, and enabling growth.

Chan advocates for companies of all sizes to have a dedicated treasurer on board instead of relying solely on their CFO or controller for treasury management.

“Treasury management should be a core component of every business, and it’s critical to at least have somebody on board with treasury experience to listen to,” he says. “You must make sure you have strong cash management—both on the receipts and disbursement sides—and safeguard your assets to ensure your fraud protections are in place.”

For organizations not quite large enough to afford a dedicated treasurer, Moirano suggests there’s insight to be gained from tapping into your network: “Building strong relationships with customers, suppliers, and peers, and keeping open lines of communication with them, offers plenty of learning opportunities.”

“These are the people who’ll be describing the challenges they’re facing and the opportunities they’re seeing and experiencing,” he says. “Many people haven’t had to deal with the situations we’re seeing now, so coming together and sharing perspectives and insights into the market provides invaluable advice for navigating this environment.”

Teri Saylor is a Raleigh, N.C.-based writer who covers a range of topics from business to lifestyles.

www.icpas.org/insight | Winter 2023 21

22 | www.icpas.org/insight

Breaking the Partner Model

Will Employee-Owned Firms Become the Norm?

As accounting firms struggle to find effective solutions to their talent acquisition and retention challenges, one creative restructuring practice has made its way into the profession—but will it last?

BY CARRIE STEMKE

www.icpas.org/insight | Winter 2023 23

he last decade has seen many changes to the accounting profession: the onset of the digital age, obstacles wrought by the pandemic, and rapidly changing client needs and expectations, just to name a few. Now, the industry is facing a particularly difficult set of challenges: fewer students are pursuing accounting degrees, young professionals no longer accept the profession’s promise of excessive work hours or the tedium of tax season, and long-established accountants are departing the profession at a rapid rate.

Accounting firms have struggled to find effective ways to handle the ballooning talent recruiting and retention issue. Recently, some firms, including BDO USA LLP, the sixth largest accounting and consulting firm in the United States, have decided to make drastic changes: They’ve abandoned their traditional partnership models and adopted employee stock ownership plans (ESOPs).

An ESOP is a benefits plan in which employees own part or all of the company they work for. Employers have the option of either replacing workers’ traditional 401(k)s with an ESOP or including it as an additional employee benefit on top of an already existing retirement plan (BDO opted for this latter choice).

Perhaps surprisingly, undergoing an ESOP transition doesn’t take an incredibly long time, making it a very viable option for accounting firms looking to make a talent retention change within a year.

“The normal timeline is four to 12 months,” says Aziz El-Tahch, managing director and ESOP and ERISA advisory practice co-leader of Stout, the company that acted as BDO’s financial advisor as they underwent the transition. “The first step is a feasibility analysis, where the key decision makers of the company really understand what the ESOP looks like financially from both the perspectives of corporate and individual shareholders. Once they see that, then we undertake an iterative process where we tweak the design of the transaction to meet certain corporate objectives. Once the board has a good sense of how much capital to raise, that’s when we start execution. Then, it’s a four- to six-month process.”

Why an ESOP?

Often, exploring an ESOP is triggered by either the retirement of a senior partner or by the lack of having someone in the company who could feasibly take over the business—or both. An ESOP can

be an incredibly useful succession planning tool, and many business owners opt for them in order to ensure that when they retire, the business stays with its employees rather than selling to an outsider who might come in and change the company culture.

Prioritizing culture and incentivizing talent with a great benefits package are two elements of effective talent retention, and both of these were top of mind for BDO’s senior partners when they were considering buyout offers from private equity (PE) firms.

“We realized so many benefits by transitioning to an ESOP that weren’t possible with a PE deal,” says Stephen Ferrara, chief operating officer of BDO. He notes that accounting firms often experience a loss of control, becoming beholden to the PE firm, which has oversight.

By undergoing the ESOP transition, Ferrara says every employee at BDO will continue to earn their salary, bonus, matching 401(k) contributions, and, on an annual basis, now receive a 10% ESOP contribution paid on their behalf by the firm.

“To me, the ESOP is a game changer,” he explains. “With it established, every employee has a wealth-building opportunity they haven’t had in the past. It makes every employee an owner without requiring them to make a huge investment. It ties employee benefits to firm performance, and we really think that’ll help with talent retention.”

Ferrara adds that the ESOP transition was a way to make working at BDO more appealing to recent college graduates: “With the ESOP, we hope to demonstrate to new graduates that they can have more ownership over their own destiny—a talent retention tool that’s worked well in other professions.”

A Viable Solution for the Profession?

The introduction of ESOPs in the accounting space begs this question: What will other firms do? Is this a viable talent retention and succession planning solution for an industry that’s been in a state of flux for years now?

Andy Kamphuis, CPA, a shareholder and managing director at Vrakas CPAs + Advisors, thinks so. He views BDO’s decision as not only a creative one, but also reflective of the many catalysts for change tugging the accounting profession in different directions. “There are many effective ways to respond to these changes that aren’t necessarily one-size-fits-all solutions,” he says.

From his experience of working at an accounting firm that serves the needs of many clients using ESOPs, Kamphuis finds these types of structures work well for companies where people are the primary value creators. “This factor alone makes CPA firms great candidates for utilizing ESOPs as a talent retention tactic,” Kamphuis says.

If you want a comparable, profession-wide success story, El-Tahch says to look at the engineering industry. “It’s extremely similar to accounting,” he notes. “The companies that have been most successful with ESOP transitions have highly engaged workforces, very good earnings in cash flow metrics, and generally are part of

24 | www.icpas.org/insight

growing industries—all of which apply to accounting. Both professions have educated workforces, and people are really important in terms of the value their labor creates. Decades ago, one or two well-known firms transitioned to ESOPs, then dozens and dozens of others followed.”

Just like engineering firms, El-Tahch expects accounting firms will take note of BDO’s transition and its first-mover advantage and start to explore this option at a greater frequency than they have in the past.

What Challenges Await Firms?

As accounting firms consider whether moving forward with an ESOP is right for them, it’ll be important for firm leaders to be aware of the challenges associated with the transition in order to position themselves for success. According to experts, there are a few major obstacles that company owners tend to face. The good news? They’re challenges that, by setting the right expectations and engaging in careful planning, can be avoided or overcome.

The first challenge: raising the capital. To successfully launch an ESOP, you’ll need to find a bank that’s experienced in this finance niche. Not all banks understand the structure and what’s involved in the transaction, experts caution. So, accounting firm leaders shouldn’t be surprised if they have to put extra time and effort into finding a bank that’s good at working with companies undergoing an ESOP transition—and they should expect that some lenders will simply be overwhelmed by the proposal and say no.

Additionally, firms can expect to deal with a lot more service providers when undergoing an ESOP transition. “This can be extremely surprising to companies that are previously used to it being just them, so to speak,” Kamphuis says. “All of a sudden, they have an ESOP advisor, they’re going through an auditor review for the first time because that’s required, and they have new benefit plans that might trigger new audit requirements—there’s more people looking at your stuff, and you’re paying more fees for the oversight.”

One other “surprise” to be aware of? Transitioning to an ESOP requires you to take on debt as a capital-raising function. For firms that haven’t been in debt, this can mean a shift in their mindset and in the way they do business. Of course, overcoming this challenge may require firm leaders to think about whether an ESOP is right for them.

El-Tahch encourages firms considering this transition to do a feasibility analysis. “Literally sketch out what an ESOP would look like for your firm. There are different ESOP structures you should think about—the one that worked for BDO may or may not work for your firm,” he stresses. “This is a flexible and customizable transaction, and until you sit down and do an analysis, it’ll be hard to know whether or not it makes sense for your firm.”

The good news in this regard: Doing a feasibility analysis isn’t extremely difficult, and nor does it require any detailed financial information that you don’t have readily available.

In addition to setting the right expectations about finding a lender and taking on debt, El-Tahch and other ESOP experts can’t stress enough the importance of surrounding yourself with the right transition team.

“It’s absolutely crucial to have good legal counsel; get someone who understands corporate transactions, tax law, and ESOP transactions. This is a specialized niche. Work with good advisors who understand how to structure and execute an ESOP transaction,” El-Tahch advises. “With an ESOP, there are a lot of parties involved. You’ll need an ESOP trustee and lender who’ll do their due diligence. You want to work with someone who’s done it before, who knows what they’re doing, and who can help you navigate this as efficiently as possible. Remember, you’ll be doing this transaction while you still have your day job.”

Of course, another challenge firms can expect is communicating the benefits of an ESOP to other senior partners and employees. “People need to understand the long-term value they’re creating in a way that drives their behavior,” El-Tahch says. “After all, the dividends the shareholder-employees will reap are now tied directly to the performance of the firm.”

While transitioning to an ESOP is a retirement plan that can bring big benefits when optimized properly, Ferrara says it’s particularly crucial to emphasize that it’s one that requires patience. Ferrara estimates it’ll take BDO until about mid-2024 for employees to receive their first ESOP statement. Of course, it’ll demonstrate the value in a powerful way (in financial terms that are on paper). However, it does mean that about a year will have elapsed since BDO completed the transition and when employees begin seeing the first dividends they’ll receive.

So, how can employers engage and educate employees to ensure success? El-Tahch frequently attends conferences where he talks about this very subject, and he has a couple of suggestions.

1. Overcommunicate. Establish communication committees led by individuals who people respect. “Have them teach their peers about the ESOP. Peer-to-peer education is a lot more effective sometimes than command-and-control, top-down management,” El-Tahch says.

2. Be transparent. El-Tahch stresses that companies who regularly share how they’re performing and establish a link between their sales, earnings, and stock price in a clear and intentional way will be more successful in helping employees understand what they should be doing to drive value.