S u m m e r 2 0 1 1 THE MAGAZINE OF THE E x p l o r i n g t h e i s s u e s t h a t s h a p e t o d a y ’ s f i n a n c i a l w o r l d g i c p a s . o r g / i n s i g h t . h t m Solution For Ever y Challenge, a

Your complete Robert Half will help you find the optimal balance of temporary, project consulting and full-time financial resources to maximize productivity and profitability within your organization. As the world’s leader in specialized financial consulting and staffing services for more than 60 years, only Robert Half offers you this complete solution. Accountemps, Robert Half Finance & Accounting and Robert Half Management Resources are the leaders in specialized financial and accounting staffing for temporary, full-time and project placement, respectively Chicago • Oakbrook Terrace • Hoffman Estates • Northbrook Rosemont • Gurnee • Naperville • Tinley Park TEMPORARY / PROJECT / FULL - TIME 1.800.803.8367 accountemps.com 1.800.474.4253 roberthalf.com 1.888.400.7474 roberthalfmr.com © 2011 Robert Half. An Equal Opportunity Employer. 0806-0005

What do you see?

A partner who works as hard as you do.

You want to make your client’s vision a reality. So we make that our goal as well. Whether we provide treasury management, financing or simply act as a sounding board, we’ll help you be part of a success story. Because when your client succeeds, you succeed.

H a r r s ® i s a t r a d e n a m e u s e d b y H a r r i s N A a n d t s a f fi l i a t e s M e m b e r F D I C

harrisbank.com/redframe

PROUD DIAMOND SPONSOR OF THE ILLINOIS CPA SOCIETY.®

i n d e x

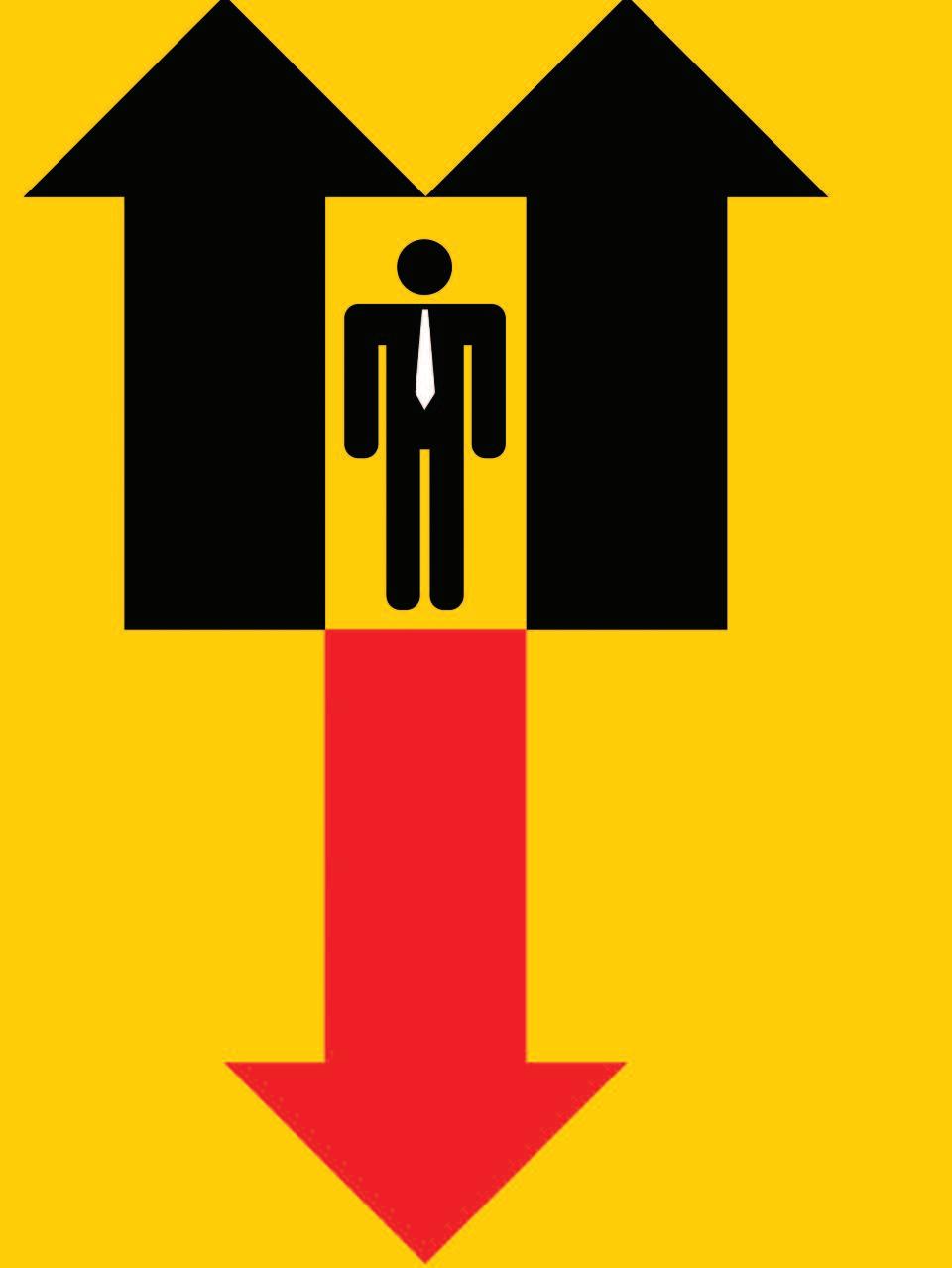

34 Strategizing in a Down Economy

B y C a r o l yn Ta n g K m et

There are many paths that lead to future growth, but choosing the right one takes some strategizing

38 M&A Movers & Shakers

B y C l a r e Fi t zg er a l d

Accounting firms are taking advantage of opportunities to drive growth, attract talent and plan for succession

42 Fraud Hit List

B y K r i st i n e B l en k h o r n Ro d r i g u ez

Today ’ s fraud danger zones and how to avoid them

12 Tax Insight When ‘Tax Exempt’ Isn’t

B y Kei t h St a a t s, JD

Being a charitable organization doesn’t always get you off the hook

14 Fraud Insight It’s a Family Affair

B y Brad Sargent, CPA/CFF, CFE, CFS, Cr FA , FABFA

What happens when a spouse, sister, uncle or parent steals from you?

16 Legislation Insight Spring to Action

B y Ma r t y Gr een , E sq

Momentum builds for state and federal CPA- supported legislation

18 Retirement Insight Golden Rules for Golden Years

B y Ma r k J Gi l b er t , C PA /PF S

How not to run out of assets when you need them most

20 Hiring Interview Revamp

B y C l a r e Fi t zg er a l d

Non-traditional interview techniques help firms assess potential hires

22 Client Retention Think Global

B y B r i d g et Mc C r ea

Your most important client is expanding overseas Now what?

24 Social Media Crowd Control

B y Sel en a C h a vi s

How to manage negative feedback in the social media age

26 Sustainability Top Barriers to Greening

B y Sh er yl N a n c e - N a sh

What ’ s holding companies back from embracing the sustainability dream?

30 Marketing Website Reconstruction

B y D er r i c k Li l l y

Haven’t touched your site since 1998? It ’ s high time for a redesign.

32 Young Money Five Ways to Save

B y D er r i c k Li l l y

regulars

You work hard for your money Now make it work hard for you

4 First Word

A message from the Illinois CPA Society ’ s President & CEO 6

2 INSIGHT icpas org/insight htm

S u m m e r 2 0 1 1 features c o l u m n

s departments

’s Message

Seen & Heard News bytes, sound advice and practical business tips 46 Classifieds/Advertiser Index 48 Time & Talent ICPAS volunteer program news

/ insight.htm

Chair

2011-2012 ICPAS Chair, Robert E Cameron, CPA 8

icpas.org

At Garelli Wong and Jackson Wabash, we help Chicago’s top firms and accounting departments. Our team unites employers with the right accounting and finance talent for direct hire, temporary and consulting assignments. We look and listen beyond the job description, to combine the right skills with the desired experience. To learn more about our dedication to finding the right fit, visit us on the web or call your local office. People are the key to your success. Let us help you find the right fit. Chicago Schaumburg Oakbrook Terrace 312.583.9264 847.397.9700 630.792.1660 WWW.GARELLIWONG.COM WWW.JACKSONWABASH.COM

FIRST W O R D

I N S I G H T S TA F F

Publisher/ICPAS President & CEO Elaine Weiss

Editor-in-Chief/Director of Publications Judy Giannetto

Creative Services Director Gene Levitan

Creative Services Manager Rosa Garcia

Publications Specialist Derrick Lilly

National Sales & Advertising Angie VanGorder

YGS Group, 3650 West Market Street, York, PA 17404

P: 800 501 9571 x176 F: 717 825 2171

E: angie vangorder@theygsgroup com

Circulation/Member Services Director Ron Jankowski

Editorial Offices: 550 W Jackson Blvd , Suite 900 Chicago, IL 60661

I C P A S O F F I C E R S

Chairperson, Robert E Cameron, CPA Cameron, Smith & Company PC

Vice Chairperson, James P Jones, CPA

Edward Don & Company

Secretary, William P Graf, CPA Deloitte & Touche LLP

Treasurer, Daniel F Rahill, CPA, JD KPMG LLP

Immediate Past Chairperson, Sara J Mikuta, CPA Leaders Bank

I C PA S B O A R D O F D I R E C T O R S

Ann M Bourne, CPA, Ernst & Young LLP

Edward J Hannon, CPA, JD, Freeborn & Peters LLP

John A Hepp, PhD, CPA, Grant Thornton LLP

Geralyn R Hurd, CPA, Crowe Horwath LLP

Paul V Inserra, CPA, McClure, Inserra & Co , Chtd

Leif J Jensen, CPA, Leif Jensen & Associates Ltd

Kathleen M Kedrowski, CPA, Navigant Consulting

Michael J Maffei, CPA, GATX Corp

Elizabeth A Murphy, PhD, CPA, DePaul University

Michael J Pierce, CPA, RSM McGladrey Inc

J Bradley Sargent, CPA, Sargent Consulting Group LLC

Edward H Stassen, CPA, Golden County Food Holdings Inc

Reva B Steinberg, CPA, BDO USA LLP – Retired Consultant

Thomas L. Zeller, PhD, CPA, Loyola University of Chicago

Even if you no longer have a connection to a school year calendar, chances are you still feel the mental shift that takes place in the late summer Our relaxed attitude is shaken up a bit as we start thinking about what the remainder of the year holds, and just like returning students, we’re curious about what lies ahead. If it’s learning and networking opportunities you’re looking for, ICPAS has a full line-up

First up is our year ’s biggest event our 31st Midwest Accounting & Finance Showcase scheduled on August 23 and 24 in Rosemont. Offering attendees the chance to earn up to 16 hours of CPE in two days for just $280, the Showcase remains an incredible value and time saver And, with free access to over 80 exhibitors, it doesn’t get any easier to learn about the new trends and technologies shaping our profession

This year ’s Showcase offers a blend of offerings from favorites like Dana “Rick” Richardson’s 18th Annual Tomorrow’s Technol ogi es and Albert Grasso’s Indi vi dual Tax Update, to new sessions covering cutting-edge topics like Ethi cs i n Troubl ed Ti mes and Consumi ng Content on Tabl ets, Smartphones and Netbooks If you’re looking to improve your s

Showcase is time well spent

Next is the CPA Day of Service. Last year, our first ever CPA Day of Service was hugely successful More than 900 participants from every segment of our membership generously volunteered their time to help others The CPA Day of Service is a great opportunity to show what we already know that CPAs give back Best of all, this event is extremely flexible, statewide, and offers volunteers the opportunity to give back in a way that is tailored to their needs, schedules and interests This year ’s CPA Day of Service will take place on Friday, September 23 For more information about registration, free t-shirts and volunteer ideas, visit www.icpas.org/CPADayofService.htm, or turn to page 48 of this issue.

Last, but certainly not least, keep an eye out for a Member Town Hall Forum near you This fall I, along with our new Chairperson Robert E Cameron, will host these statewide forums to connect with members and discuss the trends and challenges affecting the profession

All in all, the ICPAS is kind of like your alma mater; it connects you to something bigger than yourself No matter what you’ve been through personally, professionally or financially, the Society is a place to learn, network and grow Here, you’re part of something And as you change, so do we So if it’s been awhile, do join us again, or come for the first time to one of our many upcoming events

Hope to see you soon.

ICPAS Presi dent & CEO

INSIGHT is the official magazine of the Illinois CPA Society, 550 W Jackson, Suite 900, Chicago, IL 60661, USA Its purpose is to serve as the primary news and information vehicle for some 23,000 CPA members and professional affiliates Statements or articles of opinion appearing in INSIGHT are not necessarily the views of the Illinois CPA Society The materials and information contained within INSIGHT are offered as information only and not as practice, financial, accounting, legal or other professional advice Readers are strongly encouraged to consult with an appropriate professional advisor before acting on the information contained in this publication It is INSIGHT’s policy not to knowingly accept advertising that discriminates on the basis of race, religion, sex, age or origin The Illinois CPA Society reserves the right to reject paid advertising that does not meet INSIGHT’s qualifications or that may detract from its professional and ethical standards The Illinois CPA Society does not necessarily endorse the non-Society resources, services or products that may appear or be referenced within INSIGHT, and makes no representation or warranties about the products or services they may provide or their accuracy or claims The Illinois CPA Society does not guarantee delivery dates for INSIGHT The Society disclaims all warranties, express or implied, and assumes no responsibility whatsoever for damages incurred as a result of delays in delivering INSIGHT INSIGHT (ISSN-1053-8542) is published four times a year, in Spring, Summer, Fall, Winter, by the Illinois CPA Society, 550 W

for non-members: $30 US, $40 Canada and international addresses, $42 Mexico Copyright

Suite 900, Chicago,

Subscription

© 2011

the

be reproduced by any means without the written consent of INSIGHT Permission requests may be sent to: Publications Specialist, at the address above Periodicals postage paid at Chicago, IL and at additional mailing offices POSTMASTER: Send address changes to: INSIGHT, Illinois CPA Society, 550 W Jackson, Suite 900, Chicago, IL

USA

Jackson,

IL 60661, USA , 312 993 0393 or 800 993 0393, fax: 312 993 0307

rates

No part of

contents may

60661,

k

l l s , e x p a n d y o u r k n o w l e d g e , g r o w y o u r b u s i n e s s , o r b u i l d y o u r c o n t a c t s b a s e , t h e

i

A M E S S A G E F R O M T H E I C PA S P R E S I D E N T & C E O El ai ne W ei ss

4 INSIGHT icpas org/insight htm

We’re here to help you... Don’t forget to renew your membership today! Renew online at www.icpas.org. Questions: Please contact Member Services at 800.993.0393. MANAGE the BUSINESS MAKECONNECTIONS STAYINFORMED

CHAIR’S MESSAGE

From the age of five, I knew that I wanted to follow in my father ’s footsteps to one day become a respected member of my local business community to one day be a CPA Today, I feel lucky and proud to be a member of this profession, and I love being able to use my talents to help others accomplish their goals As the newly appointed chair of the Illinois CPA Society, I hope to use those same talents to serve Society members and enhance our profession

As rewarding as being a CPA is, we all know it also has its challenges. Two years ago, the Society surveyed its members to get a reading on the “Pulse of the Profession,” and to reveal those issues that kept our members up at night Last year, we began to dig deeper by holding a series of small group discussions for small-practice owners. These discussions provided valuable insights into the needs of this particular member segment

Current Position

Principal, Cameron Smith & Company PC

CPA Certified

1986

ICPAS Service Society member since 1986

ICPAS Board Service

Vice Chairperson (2010-11); Treasurer (200910) and Director (2007-08)

Current Committee Service

Executive Committee (2010-11), Information Services Task Force (2010-11), Lifetime Achievement Award Task Force (2010-11), Nominating Committee (2010-11), Peer Review Report Acceptance (1995-2011), Small Practice Management Advisory (2008-10), Small Practice Advisory Task Force (2010-11) and Strategic Planning (2007-11)

Former Committee Service

Agribusiness (2007-09), Audit (2009-10), Finance Committee (2008-10), Finance and Treasury Committee (2009-10), Government Report Review (2007-08), Peer Review Rules Implementation (2008-09), and MAP Small Practice (2000-03)

Education BS – Illinois State University, 1984

Professional & Community Service

Current treasurer, New Berlin Community Unit School District (14 years) Member of the Springfield YMCA Recreation Committee (6 years) Member of the Springfield YMCA Referee Committee (2 years) Former board member of the New Berlin Community Unit School District (8 years) Former president of the New Berlin Community Club Former youth soccer coach (15+ years) Former Boy Scout leader (5 years)

Areas of Expertise Accounting, auditing and peer review

Why are we doing this? Because the Society is committed to enhancing its relevance and value to its members, and, during my term, I would like to see us continue to make progress in this area This may mean better communicating what we already do for our members, offering new products or services, or revamping existing products and services to meet the changing needs of our various member segments

Hopefully, you have begun to note these changes, but know that we’re not yet done This year we plan to extend our small group discussions across other key member segments, including industry & business and young professionals. There are other ways to give us feedback, however. As we move forward, I would like to see higher response rates and participation in our member surveys, CPE evaluations, member forum meetings, Member Town Hall Forums, chapters, committees and ICPAS LinkedIn so that we can better hear our members’ suggestions and concerns Nothing initiates change better than honest and constructive feedback

In addition, two regulatory issues will be top-of-mind for me during my tenure as chair: M a n d a t o r y

m e n t a t i o n o f a s i n g l e - t i e r l i c e n s i n g s y s t e m i n t h e State of Illinois. I fully expect some bumps along the road and a number of questions from our members as the year progresses Still, I would like to see us well on our way to successful implementation by the end of my term

Finally, I would like to see the number of members we have involved in volunteer Society service continue to grow. It’s no secret that our profession is changing; today, it’s more important than ever for each of us to have a voice Personally, I didn’t begin to learn of the Society’s benefits and didn’t have a voice in the workings of our Society and profession until I began to volunteer for Society service. As such, I encourage others to follow in my footsteps, to volunteer and begin enjoying those same rewards There are times when it’s not easy Heck, there are even times when it’s not enjoyable However, there is never a time when I don’t appreciate the benefits volunteer service gives to the profession.

Robert E Cameron, CPA ICPAS Chai r

d i

p l

p e e r r e v i e w a n

m

e

2 0 1 1 - 2 0 1 2 I C PA S C H A I R R O B E R T E C A M E R O N, C PA

About Robert E Cameron, CPA

6 INSIGHT icpas org/insight htm

1 Alliant vehicle loan rates as of 06/01/2011. 2 Illinois bank average vehicle loan rates of 5.21% APR (new, 72 month term) and 5.26% APR (used, 60 month term) sourced from the National Association of Federal Credit Unions in cooperation with Datatrac Corp. as of 06/01/2011. 3 Alliant vehicle loan rates as of 06/01/2011. Loan approval, APR and downpayment required based on payment method, creditworthiness, collateral and ability to repay. Rates include automatic payment option. Rates are 0.4% higher without automatic payment. Rates, terms and conditions are subject to change and can vary based on age of vehicle. APR = Annual Percentage Rate. Add 1% for over 72 month term. Rates are offered on vehicle loans new to Alliant and are not applicable to current Alliant vehicle loans. Payment Example: For a loan period of 72 months and an APR of 2.95% (New), your monthly payment per $1,000 would be $15.18. For a loan period of 60 months and an APR of 3.25% (Used), your monthly payment per $1,000 would be $15.31. 4 Comparison of Alliant’s new and used vehicle loan rates as of 06/01/2011, of 2.95% APR (new) and 3.25% APR (used) vs. the Illinois bank average vehicle loan rates of 5.21% APR (new, 72 month term) and 5.26% APR (used,

60 month term) sourced from the National Association of Federal Credit Unions in cooperation with Datatrac Corp. as of 06/01/2011. 5 You must be or become a member of Alliant Credit Union to apply. Applicant must meet eligibility requirements for Alliant membership. Visit www.alliantcreditunion.org for details regarding Alliant membership eligibility. ©2011 Alliant Credit Union. All Rights Reserved. SEG359-R06/11 Your savings federally insured to at least $250,000 and backed by the full faith and credit of the United States Government National Credit Union Administration, a U.S. Government Agency Sign up today for The Alliant Advantage at www.alliantcreditunion.org/ilcpa The Alliant Advantage! As an Illinois CPA Society member, you’re eligible for... Better than bank rates on loans Get a great rate on your auto loan with Alliant. Apply now5: www.alliantcreditunion.org/ilcpa With our quick loan approvals, you’ll have money available when you need it. You’ll enjoy flexible repayment terms and much more, too. new car used car Illinois Bank Average Loan Rate Alliant Credit Union1 2.95%APR 3 3.25%APR 3 5.21 % APR 2 5.26%APR 2 2 2 WITH A LOAN FROM ALLIANT 4 Depending on loan type. SAVE UP TO 43%

SEEN H E A R D

41%

Are You a Great Leader?

ManpowerGroup has identified three crucial “R”s of great leadership

How do you stack up?

Reliable: Employees want trusted leaders who can be counted on for consistency

Responsible: Great leaders avoid excuses and demonstrate backbone

Resourceful: Strong leaders are creative in numerous aspects of the job new products or services, communications, problem- solving, budgeting, etc

For more on the three Rs, visit manpower com

CFO Views on US Deficit & Inflation

Sixty-four percent of the nation’s CFOs and senior comptrollers say the best way to reduce the US federal deficit is to reduce spending, while 35 percent say there should be equal measures of reduced spending and increased taxes, according to a national biannual survey conducted by Grant Thornton LLP [GT com] The newly enacted national health care law is one primary concern, with 49 percent of respondents saying it will increase the pricing of their goods, 40 percent saying it will decrease their company ’ s growth and 37 percent saying it will decrease their hiring. Other areas of concern in terms of pricing pressure are employee benefits (75 percent), raw materials (47 percent) and energy (45 percent)

LinkedIn Errors to Avoid

LinkedIn can take your networking to the next level with little effort, says CBS’s Moneywatch com, but most people aren’t using the site to its full potential Here are four common mistakes

A Vague Headline: Many people naturally leave their current title as their headline, but this doesn’t describe what you actually do Instead, develop a headline that describes your expertise and professional focus

FEATURED APP: Expensify

For all the road warriors out there, forget the days of trying to keep track of your paper receipts Thanks to the Expensify app, which is available for iPhone, iPad, Android, BlackBerry and Palm devices, you can import expense data straight from your credit card, email receipts, track all business-critical expenses, create spreadsheets and PDF expense reports, and even export data to QuickBooks

This app has everything you need to take the expense out of expense reporting Expensify is free to individuals and consultants, and has a scalable subscription plan for companies Visit Expensify com for more information

Maintaining a Passive Profile: Filling out your profile is just the beginning Professionals need to regularly identify and reach out to potential contacts and use status updates to stay visible

Not Trying the Tools: LinkedIn has a variety of tools to expand your network Try joining a LinkedIn Group to make new connections, and don’t forget to upload your mobile contacts list to see if people you already know are on LinkedIn

Networking Only When in Need: Network on LinkedIn like you would in real life Try to give more than you receive, especially when it comes to recommendations It ’ s always polite to give one before requesting one 8

N E W S B Y T E S , S O U N D A D V I C E A N D P R A C T I C A L B U S I N E S S T I P S

&

1 2 3. 4 8 INSIGHT icpas org/insight htm

employers who have used more independent contractors than full-time employees in the past two years Source: Right Management

$17.5 trillion

Total retirement assets held by Americans in Q4 2010, up 9 1 percent for the year.

Source: Investment Company institute

Recession Generation’s College Regrets

Seventy-one percent of recent college grads would have done something differently while in college to better prepare for the job market, according to a survey from Adecco Staffing US [adeccousa com] Generation R grads (young professionals who graduated between 2006 and 2010) indicated a desire to have started their job search earlier (26 percent), spent more time networking (29 percent), and/or applied for more jobs (26 percent) prior to graduation. The survey further found that 43 percent of Generation R grads are currently working at a job that does not require a four-year degree

Innovation

in the Spotlight

Developing new products and services is as important to CEOs as growing existing market share, says PricewaterhouseCoopers’ [PwC] 2011 Global CEO Survey Specifically, the survey found that innovation and increasing existing business outstrips all other means of expansion, including moving into new markets, mergers and acquisitions, joint ventures and other alliances

Overall, 78 percent of the CEOs surveyed believe innovation will generate “significant ” new revenue and cost-reduction opportunities over the next three years What ’ s more, CEOs rethinking their approach to innovation are increasingly seeking to collaborate with outside partners and markets

According to PwC, CEOs and other executives can drive innovation by creating a culture that is open to new ideas and systematic in the development of those ideas PwC has identified four phases of innovation, namely:

Discovery: Identify and source ideas and problems from employees, customers, suppliers, partners and others as the basis for future innovation

Incubation: Refine, develop and test ideas to see if they make business sense

Acceleration: Establish pilot programs to test commercial feasibility

Scale: Integrate the innovation into the company, commercialization and mass marketing

Visit pwc com for more

INSIGHT Wins Industry Awards

The Illinois CPA Society ’ s INSIGHT Magazine has won two prestigious media industry awards: The 2011 Magnum Opus Bronze Award for Best Association Publication and Graphic Design USA’s American Inhouse Design Awards Certificate of Excellence for Publication Design

The highly regarded Magnum Opus Awards recognize exemplary work in the area of custom media Year after year, the awards garner entries from big name, big budget organizations, including the Sara Lee Corporation, The Walt Disney Company, Wells Fargo and United Airlines, to name a few Graphic Design USA’s American Inhouse Design Awards is a premier showcase for outstanding work by inhouse designers in the United States; only 15 percent of more than 4,000 entries are recognized with a Certificate of Excellence

Visit www.icpas.org/insight.htm and click on the “About INSIGHT” link for a complete list of INSIGHT awards

SEEN& HEARD

10 INSIGHT icpas org/insight htm

CPA Society’s Young Professionals Group invites you to...

CPAs… Work hard. Network harder. It’s summer! Time to step away from your cubicle and indulge in a memorable wine and chocolate tasting experience. Have some fun and give back at the same time. Help make the dream of becoming a CPA come true for deserving students hoping to follow in your footsteps. Get a group together, bring a friend, or come solo and toast to a good cause with other young accounting professionals.

Thursday, August 11, 2011 | 6:30PM - 8:30PM

Deloitte*

111 S. Wacker Drive, 15th Flr., Chicago, IL 60606

*The event location was generously provided by Deloitte LLP.

Event Price: $45 per person

To register, please call 312.993.0407, option 4, event code: S571

Proceeds of the event will benefit the CPA Endowment Fund of Illinois. The mission of the Fund is to Pave the Way for Tomorrow’s CPAs through scholarships and other programs. For more information or to make a donation, please visit www.icpas.org/Endowment.htm.

The Illinois

The Illinois

When ‘Tax Exempt’ Isn’t

Being a charitable organization doesn’t always get you off the hook

Keith Staats, JD is a senior manager of Grant Thornton’s State and Local Tax practice, based in Chicago Keith previously served as general counsel of the Illinois Department of Revenue, where he was involved in the development of tax policy, the evaluation and review of tax-related legislation and the overview of tax-related litigation.

Section 501(a) of the Internal Revenue Code (the “IRC”), generally exempts charitable organizations from federal income taxation. Charitable organizations exempted pursuant to IRC Section 501(c)(3) are the most common type of federal income tax exempt organization Because most states, including Illinois, use federal taxable income as the starting point to determine income subject to state income taxation, IRC Section 501(c)(3) organizations are also generally exempt from state income taxes

It’s a common misconception, however, that organizations exempted from federal income taxation are automatically exempt from all state and federal taxes In fact, IRC 501(c)(3) organizations and other organizations exempted under IRC Section 501(a) may be exempted from some state and local taxes, but must comply with various application and reporting requirements in order to obtain and maintain eligible tax exempt status under state and local law

What’s more, such organizations are not even exempt from all federal income taxes; unrelated business income (income from a trade or business that isn’t substantially related to the exempt purposes of the organization) remains taxable Most states require reporting of such income, and the federally taxed income of these organizations is subject to state income tax in most states

Sales & Use Taxes

Some states grant IRC Section 501(c)(3) organizations automatic exemption from paying sales and use taxes, but many states, like Illinois, have additional, stricter requirements for exemption, and require a separate application for state sales and use tax exemption

What’s more, with certain exceptions, Illinois does not exempt a charitable organization from charging and collecting sales tax on its retail sales In order to be exempt from Illinois state and local sales taxes on purchases, an organization must file an application for exemption with the Illinois Department of Revenue (the “Department”), and must fall within one of the exempt categories under Illinois law Exclusively charitable, religious, governmental bodies and schools are the major exemption categories.

Also, the organization must demonstrate that it is “exclusively charitable” as defined by regulations and the courts. Religious organizations, governmental bodies and schools must demonstrate compliance with the statutory definitions of those categories

Once exempt status is granted, the organization receives a sales tax exemption identification number (an “E number”) that is effective for five years from the date of approval The E number must be presented when an organization makes purchases, and may not be used to retroactively exempt purchases made prior to the approval.

In addition, an exempt entity may not make purchases tax free for the use of a related, but non-exempt organization, and with certain limited exceptions, it is not proper to purchase items for resale with an E number

TAX INSIGHT

12 INSIGHT icpas org/insight htm

As a general rule, an organization’s sale of tangible personal property remains subject to tax However, there are three exceptions under Section 130 2005(a)(1) of the Department’s rules: First, some of the sales an organization makes to its members are exempt, such as sales of uniforms by a scout organization to its members or sales of Bibles by a church to its members However, a school’s sale of books and supplies to its students is taxable Second, sales by charitable organizations that are non-competitive with normal business establishments are exempt, including “infrequent” sales of cookies, doughnuts, candy or calendars Again, however, the sales of items such as hats and greeting cards, etc , are taxable, since these sales are deemed to compete with normal businesses Third, “occasional dinners and similar activities” are exempt from sales taxes This exemption includes occasional dinners, ice cream socials, carnivals, and rummage sales, no matter whether the items sold are purchased by the organization or donated to it The Department’s rules state that the “occasional dinners” exemption is limited to twice a year.

Property Taxes

In order for Illinois-based IRC Section 501(c)(3) organizations to be exempt from property taxes, they must apply for an exemption with the local taxing authorities and obtain an exemption issued by the Department Under the Illinois Property Tax Code, the applicant must show that the property is held in exempt ownership and is used for an exempt purpose.

The application must be obtained from, and filed with, the Board of Review in the county in which the property is located. The local Board then evaluates the application and makes a recommendation to the Department, which makes a final determination. In the event the application is denied, the applicant may protest the Department’s determination and seek an administrative hearing and judicial review.

Like sales tax exemption requests, an applicant’s IRC Section 501(c)(3) status does not guarantee a property tax exemption. A charitable organization must demonstrate that it is “exclusively charitable” as defined by the Illinois Constitution and Property Tax Code

The definition of the term has been further refined by the courts, most recently by the Illinois Supreme Court in Provena Covenant Medi cal Center v The Department of Revenue, 236 Il l 2d 925 (2010) The standards for establishing that an organization is “exclusively charitable” are much stricter than the federal standards for granting IRC Section 501(c)(3) status

Withholding & Employment Taxes

Generally, federal tax exempt organizations that have employees remain subject to state requirements for the filing of returns and payment of unemployment taxes, although state laws may provide IRC Section 501(c)(3) organizations with alternative methods of calculating the amount of unemployment taxes In Illinois, the Department of Employment Security is the agency responsible for administering these taxes

What’s more, qualifying organizations are required to withhold Illinois income taxes from employee wages, and are responsible for filing the appropriate returns and making payments to the Illinois Department of Revenue

In a nutshell, tax-exempt charitable organizations are not necessarily exempt from all taxes, which means that a solid grasp on business taxes and federal, state and local registration and filing requirements is mission-critical

The Holmes Group 1-800-397-0249 www.AccountingPracticeSales.com trent@accountingpracticesales.com Go with the biggest in the industry. Our biggest concern is you. Our broker’s wealth of experience culminates to make sure your comfort level is met, your questions are answered and everything is being done to sell your firm. Give us a call today so that we may go to work for you and produce the results you desire. Work For You. ll t done answe ions are st , your que met o make s t culminate rn we conce stbigge estgbig Go hingveryt d and e re l is leve comfort h of alt s de result the we may hat oday t us a call t Give o se ent@accountingpracticesales.com .AccountingPracticeSales.com tr www sire u r yo rk fo wo to go careercenter A benefit of your Illinois CPA Society Membership Job Listings | Resume Postings Career Coaches* | Career Resources Check out the Career Center today at www.icpas.org *fee-based service help keep your career on track icpas org / insight htm | SUMMER 2011 13

It’s a Family Affair

What happens when a spouse, sister, uncle or parent steals from you?

Brad Sargent, CPA/CFF, CFE, CFS, Cr.FA, FABFA

is the managing member of The Sargent Consulting Group, LLC, which specializes in forensic accounting and financial investigations Brad is a frequent lecturer on forensics and fraud, and is chair emeritus of the American Board of Forensic Accounting He also serves on the Board of Directors of the Illinois CPA Society, and has been a member of the Society since 2002

Fraud is defined as the knowing, intentional misrepresentation of a material fact, justifiably relied upon and resulting in damage. For forensic accountants, the materiality of both the misrepresentation and the resulting damages is critical. Our job is to evaluate and quantify the economic impact of fraudulent actions But good forensic accounting goes beyond the numbers to look for patterns and circumstances that help identify intent

M o t i v a t i o n a n d r a t i o n a l e a r e k e y components in any forensic investigat i o n . W h y w o u l d s o m e o n e i n t e n t i o na l l y d e c e i v e o t h e r s ? F i n a n c i a l g a i n , economic duress, ego gratification and self-righteousness are common themes we see in business situations. However, w h a t i f t h e b u s i n e s s i n v o l v e s f a m i l y members? Do the same rules apply?

W h e n o u r w o r k c r o s s e s i n t o t h e unique area of family law, thick forensic skin is a prerequisite

F a m i l y t h e w o r d c o n j u r e s u p a wide variety of thoughts for us all We live in an era when “non-traditional” is t h e n o r m f o r m o s t t h i n g s , i n c l u d i n g family Regardless of the circumstances, our deepest emotions are tied to the ones who brought us into this world, the ones we grew up with and the ones we fell in love with, married and started families with

Blood being thicker than water, we trust our family members more than any others Many people enter into business relations with family predicated on this trust. A family owned and operated business is still a part of the American Dream

For purposes of this column, I’ll focus on two distinct family law practice areas: Divorce and trusts and estates

Divorce now impacts more than 50 percent of American families. When marriages dissolve and substantial assets need to be divided, people can rationalize actions that they would never consider under normal circumstances

Thomas T Field, Esq , partner at the law firm of Beermann Swerdlove LLP, focuses on matrimonial issues. Field, who was just named a “Top 40 Illinois Attorney under 40,” offers this scenario on a recent case: A spouse employed alleged mental illness as a front for a sudden loss of employment, which was preceded and followed by covert extramarital affairs with

FRAUD INSIGHT

14 INSIGHT icpas org/insight htm

multiple people The spouse misappropriated hundreds of thousands of dollars from family accounts and fled the United States. The individual in question left a seven-figure salary, and the non-wage earning spouse and three minor children behind to fend for themselves Having returned to the country after a judgment was rendered, the spouse is now working several states away. We will be tracking this individual down to start wage garnishment.

Think about this story; possibly faking a mental illness to avoid working and supporting a spouse and children Then withdrawing hundreds of thousands of dollars from accounts and fleeing the country. How do you reconcile these actions with an album of wedding photos showing the happy couple? These breaches of trust result in damage that goes far beyond matters of economics

Estate and trust disputes can contain acts and allegations that are just as sensational. When a parent passes away and control of their assets is designated to one family member, the others rightfully presume trustworthiness Certainly the decedent made that presumption. But, what if the controlling party diverts assets from the intended beneficiaries for their own gain? This is fraud of biblical proportions Anecdotally, I worked a case involving the eldest offspring acting as trustee, funneling millions of dollars away from

their siblings to set up a business that competed directly with the family business.

Ray J Koenig III, Esq , a member of Clark Hill’s Litigation Pract

s t a t e L i t i g a t i o n Koenig explains that, “The commitment of fraud by one family member against others has both immediate and long-term effects

M o r e i m m e d i a t e l y, e x p e n s i v e a n d t i m e - c o n s u m i n g l i t i g a t i o n e n s u e s L o n g - t e r m , t h e t r u s t i m p l i c i t a m o n g f a m i l y m e m b e r s i s destroyed, resulting in a shattered family.”

Human behavior can be outrageous when our deepest emotions (love, in particular) factor in. I have witnessed successful, sophisticated business people throw common sense out of the window d u r i n g f a m i l y d i s p u t e s . T h e s e n s e o f b e t r a y a l a n d t h e e n s u i n g d e s i r e f o r r e v e n g e c a n l e a v e t h e m o s t s e a s o n e d a t t o r n e y s a n d forensic accountants shaking their heads in dismay

However, as an accountant first and foremost, I take solace (and refuge) in the black-and-white world of financial records The data (at least third-party independent data) doesn’t lie, cheat or swindle and my job is to provide the facts As accountants, we can serve our clients at their moments of greatest need.

“I refuse to go back to the way we did SEC reporting before adopting WebFilings.” — David Garrison, Executive Vice President and Chief Financial Officer, Arrhythmia Research Technology, Inc. To read and hear more customer testimonials, visit webfilings.com/customers/testimonials Streamline the Process. Ensure Accuracy, Take Control. Reduce Overhead, Save Days. e: info@webfilings.com w: webfilings.com p: 888-275-3125 A revolution in SEC Reporting is here.™

i c e G r o u p i n C h i c a g o , f o c u s e s o n Tr u s t a n d E

“Blood being thicker than water, we trust our family members more than any others. Many people enter into business relations with family predicated on this trust.

icpas org / insight htm SUMMER 2011 15

A family owned and operated business is still a part of the American Dream.”

Spring to Action

Momentum builds for state and federal CPA- supported legislation

Marty Green, Esq is the Illinois CPA Society ’ s VP of Government Relations He previously served as executive assistant attorney general for Illinois Attorneys General Lisa Madigan and Jim Ryan, and as director of the Governor's Office of Citizens Assistance and assistant to the Governor for Public Affairs, both under Governor James Edgar A graduate of Western Illinois University and Saint Louis University Law School, Marty is a practicing lawyer and member of the Illinois Bar

I’m happy to report that CPAs scored several victories during the Spring Session of the Illinois Gene r a l A s s e m b l y a n d C o n g r e s s . B o t h t h e I l l i n o i s House and Senate overwhelmingly passed legislation (House Bill 1277) initiated by the Illinois CPA Society to amend the Illinois Open Meetings Act House Bill 1277 provides an exception to the Act that permits narrow discussions to take place in a closed-meeting setting between auditors and gove r n m e n t a l a u d i t a n d f i n a n c e c o m m i t t e e s i n t h e areas of internal control weaknesses, identification of potential fraud risk areas, known or suspected frauds and fraud interviews

The Society worked closely with the Illinois Press Association and the Illinois Attorney General, as well as other supportive stakeholders such as the Illinois County Auditors Association and the State Internal Audit Advisory Board, to alleviate opposition to an additional exception to the Act This legislation adheres to the tenants of government transparency and fidelity to audit principles, and it is anticipated that Governor Quinn will sign it into law

While the potential for taxing accounting, financial and other services is always tempting in order to gather additional revenues, legislators showed little appetite for this. Illinois currently taxes 17 diff e r e n t s e r v i c e a r e a s c o m p a r e d t o a m u c h h i g h e r ratio of service taxes in neighboring states

Additionally, throughout the Spring Session the Society’s Government Relations Office informally responded to technical inquiries from legislators and their staffs concerning pending legislation The fact that legislators turned to the Society for objective technical responses to help to formulate their positions exemplifies the excellence and integrity of both the Society and the CPA profession.

On the federal level, CPAs scored another success with the repeal of the onerous 1099 MISC reporting requirements The S o c i e t y w o r k

sional Delegation in collaboration with the AICPA to illustrate the tremendous burdens the requirements put on small businesses

We have also seen initial success in undoing the patenting of tax s

(S.23) and the House Judiciary Committee’s passage of the Com-

LEGISLATION INSIGHT

t

m e m

e

f t h e I l l i n o i s C o n g r e s -

e d c l o s e l y w i

h

b

r s o

a t e g i e s w i t h t h e S e n a t e

p a s s a g e

f t h e P a t e n t R e f o r m B i l

t r

’s

o

l

16 INSIGHT icpas org/insight htm

p r e h e n s i v e P a t e n t R e f o r m B i l l ( H R 1 2 4 5 ) , w h i c h i n c l u d e s a p r o v i s i o n t h a t p r o h i b i t s patents on tax planning methods.

As part of the AICPA Spring Council Meeting in Washington, D C , senior leaders of the Society met with members of the Illinois Congressional Delegation to discuss patenting of tax planning methods and other federal issues of interest to the profession

Overall, CPAs have some significant wins in the legislative arena due in large part to the reputation and high regard of the profession. There are of course potential challenges ahead, but we are well-positioned to address those challenges We will continue working to keep the momentum moving in the right direction.

On another note, by now you should have received information titled Pathway to CPA L i censure from the Society This document outlines the framework that the Board of Directors has adopted for the future of CPA licensure as part of the anticipated legislative updates to the Illinois Public Accounting Act

This framework will continue Illinois’ transition to a one-tiered, license-only state consistent with the Uniform Accountancy Act and 45 other states After July 1, 2012, the Licensed CPA title will be the only option for newly certified CPAs.

What was traditionally known as licensed services will be expanded to accountancy activities for CPAs to encompass tax, financial, and management consulting services, and accounting services provided to clients or an employer, or the teaching of any of these areas at the college or university level by CPAs

B r o a d e r r e c o g n i t i o n o f c o n t i n u i n g p r o f e ssional education will be sought for both formal and informal credit hours that contribute t o t h e p r o f e s s i o n a l c o m p e t e n c i e s o f t h e licensee A CPA (inactive) option will be availa b l e f o r l i c e n s e e s w h o a r e n o t e n g a g e d i n accountancy activities.

As of June 30, 2011, the Registered CPA title will no longer be available for new applications However, all active Registered CPAs as of June 30, 2011 can continue to renew this title for life.

Member input on this framework is an important part of the Board’s processes in updating the Public Accounting Act I encourage you to visit the Government Relations section of www icpas org for additional background information and to submit your comments on improvements to the Act or overlooked areas in the framework outlined above.

upcoming events

corporate finance professionals

executive education

Astute Cash Flow Management

August 10, 2011 | Chicago, IL

technical workshop

Fair Value Accounting: A Critical New Skill for CPAs

August 11, 2011 | Chicago, IL technical workshop

International vs. US Accounting: What in the World is the Difference?

August 12, 2011 | Chicago, IL

special event

Midwest Accounting and Finance Showcase

August 23-24, 2011 | Rosemont, IL

technical workshop

Critical Skills for Creating Great Budgets: Maximizing Profits, People and Power

September 2, 2011 | Chicago, IL

technical workshop

FASB Review for Industry: Targeting Recent GAAP Issues

September 8, 2011 | Chicago, IL

executive education

Capital Investments

September 14, 2011 | Chicago, IL

technical workshop

Forensic Accounting: Fraudulent Reporting and Concealed Assets

September 19, 2011 | Chicago, IL

technical workshop

Surviving and Growing

Your Company in Difficult

Times: Essential Skills for the Finance Team

September 20, 2011 | Chicago, IL

conference

Midwest Financial Reporting Symposium

September 30, 2011 | Rosemont, IL

making your life easier | www.CCFLinfo.org

The Illinois CPA Society’s

icpas org / insight htm | SUMMER 2011 17

Golden Rules for Golden Years

How not to run out of assets when you need them most.

Mark J Gilbert, CPA/PFS is a principal in the financial advisory firm of Reason Financial Advisors, Inc His 25-plus years of finance and accounting experience includes 13 years in personal financial planning. An ICPAS member since 1982, Mark currently serves in the Society ’ s IA/PFP Member Forum Group and on its Committee on Structure and Volunteerism

In my last column, I suggested how to advise retirement fund accumulators in their 30s to 50s In this issue, I’ll cover the intricacies of advising clients who are only 3 to 10 years away from retirement clients I’ll call “serious retirement thinkers.”

First and foremost, knowledge is power To understand your clients’ financial readiness for retirement, a retirement plan that includes cash-flow projections is a must You, or a competent personal financial planner, can develop this plan. You can then assess whether your client’s present financial resources (including anticipated future savings and investments) are likely to meet their anticipated future needs.

The retirement plan should account for a number of client

means of this planning process, your clients will get a much clearer picture of whether their Plan A is on track, or whether a Plan B is needed

This customized retirement plan also should account for existing assets, income sources, any unique aspects of your client’s financial situation, and projected investment returns and inflation rates. With this information in hand, you can help your client understand the pros and cons of accelerating payouts or delaying benefits as their retirement date nears

Having a retirement plan is one thing; putting it into action is quite another. These six steps give you a guideline for how to make the most of retirement plan findings

1. Commit to changes

Sometimes, actually making any recommended changes is the hardest part of the financial planning process since inertia is always the easiest course The reality is, however, that your serious retirement thinkers don’t have the luxury of time to mull things over

2.

Make retirement a priority

Some serious retirement thinkers are still supporting their adult children financially In order to meet retirement goals, however, they may need to rethink this especially if their plan reveals the need to accelerate retirement savings and investing

3. Understand the deals

Age comes with its privileges. Workers 50 years and older can make annual catch-up 401(k) and IRA contributions, which raise annual contribution limits from $16,000 to $22,000 and from $5,000 to $6,000, respectively Encourage your clients to utilize these favorable tax provisions.

RETIREMENT

INSIGHT

g o a l s , i n c l u d i n g t h e n e e d t o m a i n t a i n q u a l i t y o f l i f e , p a y o f f m o r t g a g e s , p a y f o r t r a v e l a n d n e w p u rc h a s e s , a n d s o o n . B y

18 INSIGHT icpas org/insight htm

4. Get the right coverage

Insurance needs change with age Term life to protect the primary breadwinner ’s income while children are young may no longer be needed Permanent products may provide lifetime income benefits, and long-term care insurance may become more important. Make sure your clients evaluate their insurance needs and have the appropriate policies in place

5. Enhance asset value

P e r h a p s y o u r s e r i o u s r e t i r e m e n t t h i n k e r i s a b u s i n e s s o w n e r N o w ’s t h e t i m e t o s e r i o u s l y consider alternatives for the business, such as a n i n t r a - f a m i l y s a l e o r g i f t t o c h i l d r e n , a n inside sale to the management team, an outs i d e s a l e t o a t h i r d p a r t y, o r a s i m p l e w i n d down of operations If value is to be improved, an owner may need time to develop and market new products and services, make a strategic acquisition, or put into place an effective c o m p e n s a t i o n p r o g r a m t h a t a l l o w s t h e k e y employees to purchase the business.

O r, m a y b e y o u r c l i e n t w a n t s t o d o w n s i z e their living arrangement and sell their home It’s just as important to plan the repairs and maintenance needed to bring top dollar for the property Encourage your client to take the necessary time to plan for these types of transitions

6. Invest appropriately

Part of the knowledge gained from the retirement planning process involves how the client s h o u l d m o d i f y i n v e s t m e n t s t r a t e g i e s A t t h i s stage of life, clients should be thinking about r e d u c i n g v o l a t i l i t y b y i n v e s t i n g l e s s a g g r e ss i v e l y W h y ? B e c a u s e s u b s t a n t i a l p o r t f o l i o l o s s e s a r e d i f f i c u l t e n o u g h t o r e c o v e r a t a n y time, and it becomes all the more difficult in retirement when funds are being counted on to support one’s quality of life

Of course, a conservatively invested portf o l i o c a n b e e x p e c t e d t o p r o d u c e l o w e r returns Even if those lower returns are insuff i c i e n t , I ’ v e f o u n d t h a t m o s t o f t h e t i m e t h e answer is not to take on more investment risk, but ra the r to c ut ba c k on life sty le e x pe nse s, delay retirement, save more or a combination of all three

September

23, 2011 A

icpas org / insight htm | SUMMER 2011 19

Good Day for Doing Good Be part of the Illinois CPA Society’s second annual CPA Day of Service. It’s as easy as 1-2-3: Choose a community organization or charity to help. Register your volunteer activity plans at www.icpas.org/CPADayofService.htm. Receive a free CPA Day of Service t-shirt (while supplies last, free to ICPAS members). Volunteer as an individual, or get a group together and volunteer as a team.

can choose

Serious retirement thinkers are faced with an almost endless resource of information Most of them need the help of a CPA to distill that information and to make sense of it I encoura g e y o u t o s t e p u p a n d t a k e o n t h a t r o l e b y starting the conversation with your clients It will reaffirm their trust in you volunteer activity you like. See our website www.icpas.org/CPADayofService.htm for ideas.

You

ANY

CPAs for the Public Interest (CPAsPI), the community service arm of the Illinois CPA Society, links the expertise of CPAs and finance professionals with Illinois not-for-profit organizations and community needs. 1 2 3

Questions? Please contact Jill Wiles Wolf, Public Service Manager at wilesj@icpas.org or 800.993.0407, ext. 277.

Day of Service

Inter view Revamp

Non-traditional interview techniques help firms assess potential hires.

By Clare Fitzgerald

By Clare Fitzgerald

The tried-and-true traditional interview process may be adequate to find and secure a warm body to fill that vacant spot in your office, but companies hunting for a true cultural fit are increasingly turning to creative strategies often within informal settings.

events, scouring social networks, opening their office doors and implementing a wide range of programs to find and evaluate the most promising potential hires

“Technology has given companies the opportunity to reach so many more people today,” says Genevieve Roberts, partner at the Titan Group human resources consultancy “Now companies can use specialty job sites and social networking tools like Twitter and Facebook to get their opening in front of many more people.”

David Ryan, a human resources executive and officer in the Illinois State Council of the Society for Human Resource Management, notes that companies are going beyond postings on traditional job boards like CareerBuilder or Monster, and are

“You can often see even more about a person’s background on LinkedIn than in a resume,” he explains A

grams Set up like speed dating, large numbers of interviews can be conducted over short time spans, with candidates getting only a few minutes to explain why they should be hired.

For firms seeking a more targeted approach, Roberts suggests implementing strong employee referral programs. “Your people can be your best advocates,” she says “Top performers tend to know other strong candidates and can identify people who are a strong personality and cultural fit as well ”

Chicago-based accounting and consulting firm Grant Thornton LLP offers rewards for employees who refer a successful hire

“We really encourage people to know their networks,” says Nina G u t h r i e , t h e f i r m ’s n a t i o n a l d i r e c t o r o f u n i v e r s i t y r e c r u i t i n g .

When searching for an experienced hire, Guthrie says the firm taps into employee networks, often asking senior staff to name the top five people with whom they would want to work “We’ll then target those prospects to try to bring them onboard,” she explains.

Whatever sourcing channel you use, the selection process is all important Testing grounds, however, need not be so formal or costly. Creative strategies to test potential new hires include:

Online assessment tools

If administered correctly, these tools can help companies get to grips with the inner workings of the people on their candidate short list. “Assessment tools can really help you get an idea of a person’s strengths and weaknesses and identify areas where you’ll need to dig deeper in the actual interview,” says Roberts.

“You can gain a greater sense of candidates’ tendencies, like whether they are introverted or extroverted, or what gives them a sense of fulfillment, and then evaluate if their profile matches your company culture,” Ryan adds

Assessment tools alone won’t give you the whole picture, however. “Use them only to gain more data about a person,” says Roberts “The more data you have, the better your chances of making a good hiring decision ”

F o c u s e d a b o v e a l l o n g e t t i n g t o k n o w t h e c a n d i d a t e , c o m p a n i e s a r e o rg a n i z i n g s o c i a l

n o w e x p l o r i n g p r o f e s s i o n a l n e t w o r k i n g s i t e s l i k e L i n k e d I n

t

n o t h e r t r e n d i n

h e h i r i n g a r e n a : S p e e d n e t w o r k i n g p r o

H I R I N G

20 INSIGHT icpas org/insight htm

Informal social events

“Whether it’s a lunch or dinner or opportunity for the team to sit down with candidates, informal gatherings help companies evaluate the intangibles like how they engage in conversations and how they would represent the firm in social settings,” says Roberts

Chicago-based accounting firm McGladrey hosts dinners and networking programs the night before campus interviews to get t o k n o w a n d e v a l u a t e s t u d e n t s o n a m o r e i n f o r m a l l e v e l “We’re looking at communication and interpersonal skills,” says Paul Nickel, recruiting manager “For example, we’re looking to see how they might interact with a client ”

“We’re courting students from the time they are sophomores in college, so we’re working to develop a relationship very early on,” explains Guthrie, noting that Grant Thornton builds relationships in a variety of ways, such as speaking in accounting classes, holding informational sessions on campus and pairing students with partners who can encourage their interest in accounting and share “day-in-the-life” stories from the frontlines

Some firms go so far as to organize full-on excursions such as a trip to a baseball game or skiing both to promote the image of “this is a fun and fulfilling place to work,” and to evaluate candidates’ social skills.

“That’s what really separates the good from the great,” says Guthrie “You can really see the levels of conversation, evaluate their interest in the types of clients we serve and get a sense of their true aspirations “We’re looking for students who have that X factor,” she adds, “candidates who not only have outstanding business acumen but also want very challenging work ”

Community and volunteer activities

“Whether it’s building a house or planting a tree, there’s so much you can learn about a person when you’re in jeans and a t-shirt and working on a project like that,” says Guthrie. “People can really open up and relax ”

Community and volunteer activities offer the opportunity for a meeting of minds. The fact that, say, a candidate is a member of H a b i t a t f o r H u m a n i t y, a n d y o u r f i r m a l r e a d y c h a m p i o n s t h a t charity, gives you a clear indication that this candidate will be a good cultural fit. Shared values are a must.

From the candidate’s point of view, the fact that your firm takes the time to volunteer for a cause or for the betterment of the community gives you automatic cool points More and more, professionals want to feel that the work they do matters And they want to work for organizations that put social responsibility at the forefront of their goals

As Guthrie explains, “We want to get to know the person and give the person the opportunity to really know our firm It’s much more effective to spend time and money on the front end to do that than to hire the wrong fit.”

Case Studies

When it comes to higher-level positions, Roberts suggests case studies as a great testing tool. “Whether you ask them to give a presentation, react to a client scenario, or solve a customer problem, case studies provide an opportunity to see how candidates would respond in a real-life situation,” she says “If you need to ascertain how well a person can think on his feet or critically analyze a situation, case studies can be helpful.”

These dynamic, interactive and often informal testing grounds take some of the guesswork out of recruiting, and help to present a much more rounded picture of hiring hopefuls

Succession Planning Services

for Illinois CPA Society members

The Illinois CPA Society, in conjunction with Accounting Transition Advisors, is here to help with Project MATS (Merger, Acquisition, Transition and Succession).

Project MATS is an on-demand service providing content, advice, consultation, information, case studies and succession services at no cost for members.

This new service is dedicated to helping you...

• evaluate your practice value

• understand the latest succession and merger trends

• develop a basic plan for growth or succession

• enhance your potential to realize a financial reward

Learn more and get advice from the experts at Accounting Transition Advisors today.

Visit www.icpas.org/practicemanagement or call Michele Haryasz at 800.993.0407, ext. 287.

An independent

Visit the ICPAS Booth on Tuesday, August 23, 2011 at the Midwest Accounting and Finance Showcase to talk live with succession planning expert Lon Goforth. icpas org / insight htm | SUMMER 2011 21

Merger, acquisition, transition and succession – big issues that keep practitioners up at night.

consulting organization performing merger, acquisition, transition and succession services exclusively within the tax and accounting profession.

Think Global

Your most important client is expanding overseas. Now what?

By Bridget McCrea

International business is on the rise, and many of your clients are leading the charge. Global trade grew by 13.5 percent in 2010, according to the World Trade Organization, marking the fastest ever expansion in global commerce. That’s great news f o r a c c o u n t i n g a n d f i n a n c e p r o s w i t h i n t e r n a t i o n a l b u s i n e s s experience, and serves as a warning for those without it

“Chicago’s high number of manufacturing companies has led to a lot of international expansion in the past 25 or so years,” says Antony Nettleton, audit practice leader and International Business Center director for Grant Thornton LLP, in Chicago Nettleton states that, “We’ve seen a lot of local manufacturing firms move production into countries like Mexico and China, where the cost of labor drove lower production costs.”

In addition, as the US economy and market demand have matured, there has been an increasing focus on international

Six Steps to Global Client Success

One: R e a c h o u t t o f i r m s / c o l l e a g u e s i n t h o s e countries into which your clients are seeking to expand

Two: Work with the local investment resources m o s t c o u n t r i e s h a v e h e r e i n t h e U S A . T h e i r j o b i s t o h e l p y o u r c l i e n t s s e t u p o p e r a t i o n s i n t h e i r c o u n t r y a n d t h e i r services are free

Three: Visit the countries with your clients Travel extensively and maintain an enquiring, open mind

Four: Join a network of international firms The statutory rules in each country differ widely, and in order to help domestic clients expand, you need to be able to help your client connect with the right advisors overseas.

Five: Learn the US tax rules related to foreign c o r p o r a t i o n s s o t h a t y o u c a n a d v i s e clients on how to set up the foreign entity related to the domestic filings

Six: M a n y c o u n t r i e s a r e m i g r a t i n g t o I F R S, which means you need to understand this b a s i s o f a c c o u n t i n g a n d t h e s i g n i f i c a n t differences between IFRS and US GAAP.

In response, Chicago-based firms like Grant Thornton have established international networks that can step up to the plate and help the client make the best possible accounting decisions when dealing with the complexities of international expansion.

“If one of our clients goes into Vietnam to do business, we have someone there on the ground ready to help set up operations, and to deal with taxes, systems and controls,” says Nettleton. “The more companies venture overseas, the more complex things become ”

An obvious area of concern is foreign forms of accounting such as International Financial Reporting Standards (IFRS) Accustomed to Generally Accepted Accounting Standards, domestic companies expanding overseas are relying on their CPAs to help them decipher IFRS and to manage value-added taxes, social taxes and other nuances that they don’t necessarily have to deal with domestically

C u l t u r a l d i f f e r e n c e s a l s o c o m e i n t o p l a y, N e t t l e t o n p o i n t s o u t , a s d o b a s i c accounting considerations such as how quickly invoices are paid. In Italy, for example, it’s not uncommon for a vendor to be paid within 120 days, versus the 30 to 60 days that American firms are used to.

“These nuances can really surprise your clients, so it’s up to you to be able to educate them on these issues,” says Nettleton “And while the CPA doesn’t necessarily have to know everything about every country, it’s important that he or she understands that going into a foreign country is significantly different than building a new plant in Arkansas ”

L o c a l l a w s a n d c u s t o m s c a n s i g n i f i c a n t l y a f f e c t U S a c c o u n t i n g f i r m s a s t h e y spread their wings overseas, explains Kevin Wydra, CPA, audit partner with Crowe Horwath LLP in Oakbrook, Ill. and chairman of the Illinois CPA Society’s Audit and Assurance Services Committee. Having extensive experience working with US companies with overseas presences, Wydra says organizational structure is an important first consideration for clients who have to balance their US operations with the

C L I E N T R E T E N T I O N

m a r k e t s t o g r o w t h e t o p l i n e C o m p a n i e s h a v e t h e r e f o r e d e v e l o p e d o p e r a t i o n s i n t a x - f r i e n d l y c o u n t r i e s l i k e I r e l a n d and the Netherlands

22 INSIGHT icpas org/insight htm

local laws and customs prevalent in the target country. Many of those countries require statutory audits and compliance with other local accounting requirements, both of which are typically handled by local firms and require special attention to detail.

From the audit perspective, Wydra says he focuses closely on w h e t h e r t h e s e r v i c e s r e n d e r e d b y h i s c o m p a n y a n d i t s f o r e i g n a f f i l i a t e n e t w o r k a r e c o m p l i a n t w i t h U S i n d e p e n d e n t r e q u i r ements. Recently, for example, a client wanting to set up shop in Singapore ran into issues when the local affiliate was willing to p r o v i d e b o t h b o o k k e e p i n g a n d a u d i t s e r v i c e s . W h i l e t h i s w a s a l l o w e d u n d e r t h e l o c a l s t a n d a r d s , t h i s i s n ’ t c o m p l i a n t w i t h AICPA independence standards.

That scenario alone proves the importance of a CPA’s ability to understand the accounting services being rendered, and to ensure c l i e n t s a r e i n c o m p l i a n c e w i t h d o m e s t i c a n d / o r i n t e r n a t i o n a l requirements, says Wydra

But by mastering the ropes of international business, accounti n g f i r m s o f a l l s i z e s c a n e s t a b l i s h t h e m s e l v e s a s a “ g o - t o ” r e s o u rc e f o r c l i e n t s t h a t c a n ’t p o s s i b l y h a n d l e t h e i r e x p a n s i o n overseas on their own

“When you can position yourself to be able to handle large, m u l t i n a t i o n a l c o r p o r a t i o n s w o r l d w i d e , y o u m a k e y o u r s e l f t h a t much more valuable in today’s increasingly global business envir o n m e n t , ” s a y s Wy d r a “ I t a l l o w s y o u t o c o n t i n u e t h a t t r u s t e d advisor relationship that you established domestically, and build on it globally ”

“To truly become global in knowledge and experience and to be able to address clients’ needs as they arise accountants will h a v e t o e d u c a t e t h e m s e l v e s o n t h e p r o c e s s e s , s t a n d a r d s a n d requirements that are being used in the target countries,” says Dan Rahill, CPA, Illinois CPA Society treasurer and a tax partner with KPMG LLP in Chicago Rahill suggests accountants do the necessary self-study and research to get up to speed on how business, audits and taxation are handled in the most popular regions their clients are exploring

Of course, nothing beats early preparation and hands-on exper i e n c e “ S h o r t - o r l o n g - t e r m f o r e i g n a s s i g n m e n t s e a r l y i n a n accountant’s career provide great experience and clearly gives them an advantage among their peers,” says Rahill. “Requesting assignment to a foreign-owned multinational client will provide a professional with some great technical experience, including possible exposure to IFRS.”

F o r m a n y d o m e s t i c f i r m s , h o w e v e r, p a r t n e r i n g w i t h f o r e i g n firms that know their local turf best is the most effective option.

“To most effectively deal in the middle market and with largec a p i t a l c o m p a n i e s , d o m e s t i c a c c o u n t i n g f i r m s w i l l h a v e t o develop a global network of service providers that they can tap into,” says Rahill. As he explains, these resources will be invaluable when it comes down to dealing with “audits to cash management to business structure, and everything in between ”

Racking up some frequent flyer miles will also take your quality of service to new heights “Don’t assume that everything is just like it is here, in the United States,” says Nettleton “If your clients are doing business in other countries, you really need to visit those places in person to get a feel for how business is conducted there Too many accountants do their work from their offices in Illinois, with no appreciation whatsoever of what it’s like in the countries where their clients are operating ”

/.%"8 &03&-#&1 9 *2,& *.".$*", .23*343*/.2

1*%"8 &03&-#&1 9 /2&-/.3 *%6&23 *.".$*", &0/13*.( 8-0/2*4&%.&2%"8 $3/#&1 9 /2&-/.3 "7 1"$3*3*/.&1 8-0/2*4-

)412%"8 $3/#&1 9 "+#1//+ &11"$& /.2314$3*/. .%4231*&2

4&2%"8 /5&-#&1 9 /$"3*/. "7

&%.&2%"8 /5&-#&1 9 /2&-/.3 /3 '/1 1/'*3 ",' "8

)412%"8 /5&-#&1 9 /2&-/.3 /3 '/1 1/'*3 4,, "8

&%.&2%"8 /5&-#&1 9 )*$"(/ 1"4%

1*%"8 /5&-#&1 9 /2&-/.3 &",3)$"1& /-0,*".$& ".% 1"4% ",' "8

&%.&2%"8 &$&-#&1 9 /2&-/.3 -0,/8&& &.&'*32 ",' "8

)412%"8 &$&-#&1 9 01*.('*&,% /3 '/1 1/'*3

4&2%"8 &$&-#&1 9 01*.('*&,% &%.&2%"8 &$&-#&1 9 /2&-/.3 $$/4.3*.( 4%*3*.(

/1 3)& -/23 $411&.3 *.'/1-"3*/. /1 3/ 1&(*23&1

5*2*3 666 *$0"2 /1( /1 $",,

"

1 + ! / 4 1 " , & . % " 1

",, *.3&1 /.'&1&.$&2

icpas org / insight htm | SUMMER 2011 23

Crowd Control

How to manage negative feedback in the social media age

By Selena Chavis

Do you know what customers are saying about you and where they’re saying it? In the age of social media, many companies have learned the hard way that bad press can spread like wildfire.

And whether or not the negative feedback is deserved, experts caution that you have to be prepared to respond quickly and appropriately to turn a potentially volatile situation into an opportunity

“They may or may not be right,” says Mana Ionescu, president at LightspanDigital.com, a Chicago-based digital marketing firm specializing in social media and email marketing “You may have to look at it as an opportunity to educate the public It could be a great branding opportunity in that it may show you a side of your brand that needs attention.”

Negative responses tend to fall within three categories: 1) those that are blatantly malicious in nature; 2) those that may be misguided; and 3) those that have been earned or warranted.

In the case of “blatantly malicious” comments, the most appropriate response may be no response at all “Sometimes the person venting looks so bad that it makes sense not to respond,” says Ellen Hattenbach, a business development executive at Frost, Ruttenberg & Rothblatt, P C , a large CPA and business advisory firm based in Deerfield, Ill. “Sometimes, no matter what you do, it’s not going to make a big differe n c e , ” I o n e s c u a d d s , p o i n t i n g o u t t h a t i f y o u d o c h o o s e t o r e s p o n d , o p t f o r n e u t r a l i t y s o t h a t y o u don’t feed the fire

In the second instance, experts suggest that companies evaluate the opportunity the misguided negativity presents “Negative feedback is a gift it’s an opportunity to make a change,” says Sima Dahl, a Chicago-based consultant in the marketing, branding and social media space to B2B owners. It’s an opportunity for one-to-one interaction that can potentially earn you a new customer She suggests empathizing expressing regret that a customer is feeling mist r e a t e d o r f a c i n g d i f f i c u l t y a n d t h e n m o v i n g t h e conversation to a more private channel where the feedback “can include more than 140 characters” per response.

In the third instance, where the negative feedback is valid, Ionescu suggests that companies “acknowle d g e t h e m i s t a k e ” a n d “ d o n ’t g e t i n t o t h e b l a m e game ” A company that comes across as humble and willing to rectify a situation will be perceived in a much more positive light than a defensive one

She references a recent social media disaster at Nestle that many claim as a textbook case of how not to handle negative attention. In a nutshell, the company came under fire across many social media networks when it responded defensively to a Greenpeace campaign against the company’s use of palm oil Greenpeace members populated the Nestle Facebook fan page with wall posts, while also changing their profile pictures to altered versions of the Nestle logo. The perceived caustic tone of the Nestle Facebook page moderator only added fuel to the fire

S O C I A L M E D I A

24 INSIGHT icpas org/insight htm

“That could have been so easily avoided if they had just killed them with kindness,” Ionescu suggests, adding that while most accounting and finance firms won’t face attacks on this scale, it’s important to understand the nuances of social media interaction And even more importantly, firms need to have a solid crisis plan of action in place

Dahl feels that many accounting firms are treading cautiously for fear of making costly mistakes. “This concept of trying to think through every scenario before we try social media is a fallacy Social media success is reserved for brands that ‘do’,” she explains.

Frost, Ruttenberg & Rothblatt, P C for one h a s e s t a b l i s h e d a s o c i a l m e d i a p r e s e n c e through its Facebook page, using video and other tools to introduce the public to its staff “If you were looking for an accounting firm, and you went to our site, you would get a flav o r f o r o u r s t a f f a s p e o p l e , ” n o t e s A l a n Dordek, director of marketing and business development at the firm

O n e o f t h e u n i q u e o p p o r t u n i t i e s t h a t social media provides professional services e n t i t i e s i s t h e m e a n s t o c o n n e c t w i t h t h e public on a much more personal level “So m u c h o f t h e w a y f i n a n c i a l s e r v i c e s a n d a c c o u n t i n g f i r m s g o t o m a r k e t i s t h r o u g h referrals,” says Dahl, adding that the public is much more likely to connect with individuals than with a firm “That’s a really unique opportunity for social marketing ”

However, there are risks, particularly if your social media initiatives aren’t monitored From free tools to complex enterprise systems, business entities should make room in business operations for tools that will enable them to monitor and immediately respond to negative feedback “If a complaint comes through Twitter, we have to respond within an hour,” says Ionescu, pointing out that the larger the brand, the shorter the timeframe for response strategies “Our stats suggest that if it gets beyond an hour, you tend to lose the customer or control of the message.”

Negative messages or comments on blogs don’t require quite as immediate a response, but marketing experts still suggest at least a 24-hour turnaround

G o o g l e A l e r t s , a f r e e t o o l r e c o m m e n d e d by Ionescu for individuals and small companies, provides notifications when your name is mentioned on the Internet “There’s a tiny d e l a y w i t h G o o g l e A l e r t s . T h e y d o n ’t p i c k up everything, but it’s a good no-cost tool,” she explains

Frost, Ruttenberg & Rothblatt, P.C. currently uses this tool, in addition to having established a committee of partners that meet on a

regular basis to discuss opportunities and issues related to social m e d i a . “ O u r p a r t n e r s h a v e r e a l l y e m b r a c e d m e d i a a n d s o c i a l media,” says Hattenbach. While they believe the opportunities outweigh the risk, they have still established internal policies that cover areas such as how to handle negative feedback. “Our partners are really leading this effort,” she says.