THE RETIREMENT ISSUE

1 27 JANUARY 2023

FOR YEARS, Deon Kleynhans* begged his elderly parents to sell their large, four-bedroom family home and buy a smaller property that would be easy to maintain and give them a decent amount of money to enjoy their retirement.

But every time he made the plea, they dug their heels in and shut him down, saying that they wanted to leave it to their three children.

Eventually, the 45-year-old gave up the fight, but found it hard to watch his parents barely scrape by each month, all for the sake of giving him and his siblings a house to inherit.

“My parents worked hard their whole lives to give us everything we needed, and they deserved to enjoy their retirement. I did not want anything from them. Not property, furniture or money. I am an adult, responsible for my own future. They did not need to still be making sacrifices for me.”

Years later, his parents finally made the difficult decision to sell the house – although by then, they were left with little choice as

the rising cost of living, electricity and medical aid devoured their monthly pensions. They will soon be moving to a retirement village, and they have quite a bit of money left to enjoy their golden years.

Changing priorities

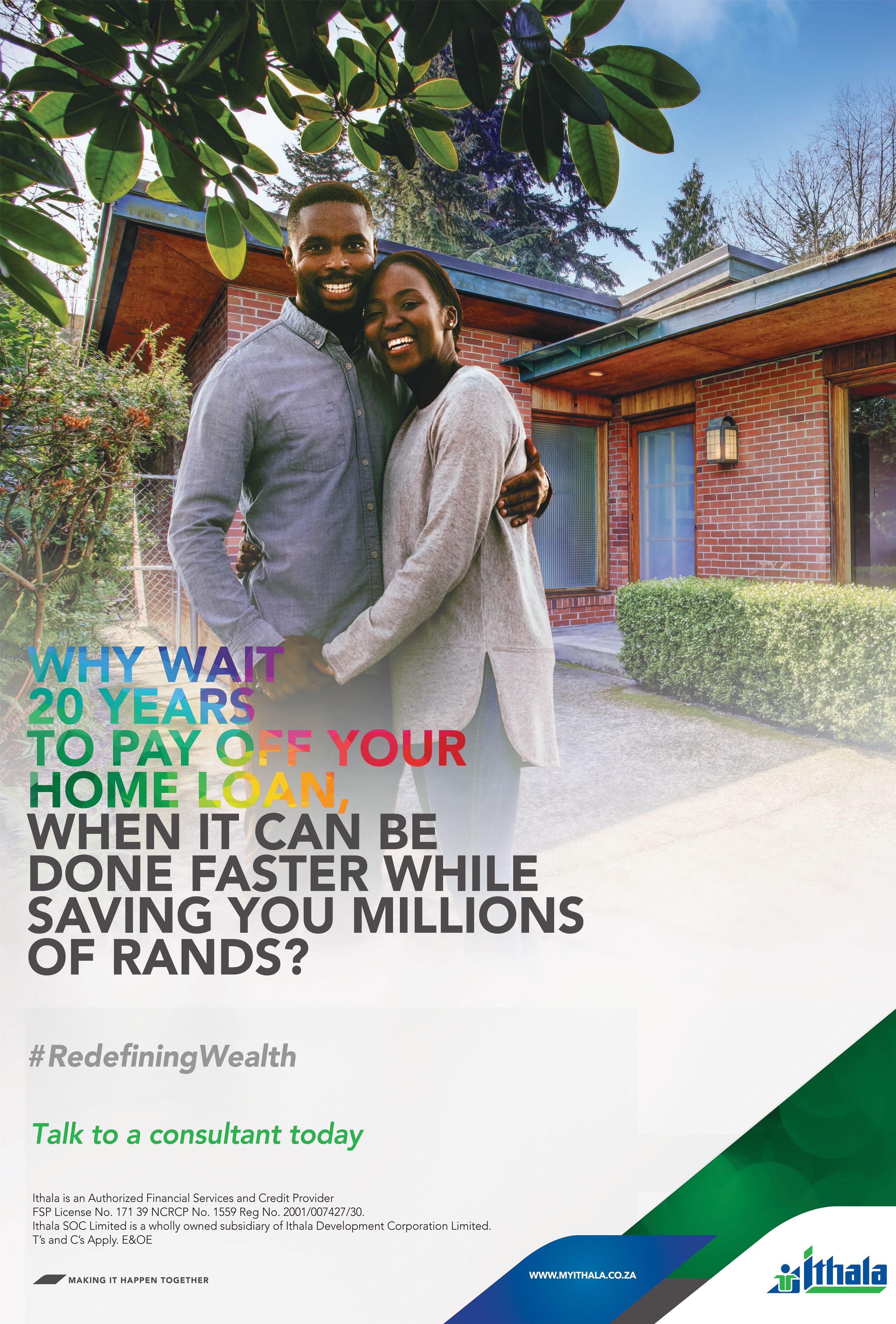

While it has almost always been the norm for homeowners to bequeath their properties to their adult children when they pass away, it seems the trend is shifting, with more retirees selling in order to downscale and enjoy a better quality of life.

Likewise, more adult children are in support of this, choosing to have their parents enjoy their retirement years and hard-earned money rather than remaining in their homes just so they can pass them on.

The dream for many retirees these days is to move into a modern retirement development that offers community, activities, friendship, health care and security, but most of them cannot afford to buy a home in such a village.

The alternative, therefore, is to purchase a life right, which is far more affordable and offers them a

unit in such a development for the rest of their lives, although ownership remains with the developer.

When they pass away, the developer also retains the capital growth on the purchase price. A portion of the original purchase price, which differs throughout developments and agreements, is returned to the estate of the deceased. This means that there is no physical property to bequeath.

However, heirs can feel secure that their parents were able to enjoy their retirement years at a significantly reduced price.

For some, this is enough. But others want a property to be left to them, regardless of the lives their parents will lead.

Mariska Auret, a director at Rabie, says there is “a lot of concern” from retirees who feel they have to leave something to their heirs, especially when they have little or no other assets.

However, where a retiree has other assets, whether they are immovable, such as property, policies or a share portfolio, it seems easier for them to make a lifestyle choice that serves them,

rather than being concerned about their heirs.

“Unfortunately, there are always instances where heirs dissuade their parents, for their own gain. In our experience, the benefits of life rights, once understood, outweigh the need to leave something behind, and simultaneously, more heirs are realising the tremendous positive impact that living in a life right estate has on their parent/s.”

Over the past few years, says Phil Barker, a consultant to Renishaw Property Developments, heirs and retirees have, together, seen that fewer people have the financial means to bequeath a property.

“We are seeing more and more heirs recognising the need for their parents to continue to live the lifestyle that they are used to and have enjoyed.”

Gus van der Spek of Aview Properties agrees. He says the lack of capital growth that people are facing with life rights is “a small price to pay for the safety, security and well-being of their parents”.

“Our experience is that the majority of individuals in the children’s generation are more interested in standing on their own two feet, and are just happy that mom and dad are safe, cared for and happy.

“The financial side of things is regarded as part of retirement living, and I think this will most definitely be the trend as life rights become more widespread.”

He explains that life rights generally provide a range of services that are not just lifestyle-based and include essentials such as medical care and food.

“In addition, the social element of retirement living is very important, so there are a number of benefits people get from living in retirement developments.”

As life expectancies continue to increase, Barker says retirees have to ensure, as best they can, that their retirement savings will last.

“Life rights and the sectional title equivalents are ways of assisting this process. Our

experience is that the children of retirees are recognising this and supporting their ageing parents in making this type of difficult decision.”

He emphasises that times are changing, and that, in the end, it all boils down to affordability.

“People are living longer and medical costs escalate as one ages. Life savings to fund one’s longer life must inevitably include the family home.”

Ultimately, Van der Spek encourages retirees to choose where they are going to be happy. After all, they have worked hard to set themselves up for a comfortable retirement.

“I would urge them to see an investment like this as a repayment for life’s work. They have earned the time to settle down and enjoy these golden years in the way they feel is best, and that ultimately should be the focus of the decision.”

A life right, explains Auret, benefits retirees by offering them a tailor-made lifestyle.

“It is therefore an investment that outweighs any financial interest or gain that an heir might receive (which is not guaranteed in any event). The heir will still benefit financially, as they will receive the original capital back, depending in which development they purchase, as developers have varying terms and conditions.”

She says legislation protects the occupier (retiree), which means that they have a home for life – “a tremendous benefit”.

“Above that, there are so many things that are looked after on behalf of the occupier – 24/7 security, maintenance, landscaping, as well as the benefits of enjoying amenities such a clubhouse, a nurse on duty and so on.

“Retirees and their families therefore need to carefully consider what is in the best interest of the retiree. It’s about giving him or her the opportunity to enjoy a care-free retirement and not have the stress of things like safety, mowing the lawn or fixing the roof.”

* Name changed

While it has mostly been the norm for parents to bequeath their property when they pass away, the trend is shifting

BY BONNY FOURIE bronwyn.fourie@inl.co.za

TODAY’S retirees are remaining active until well into their golden years and, as such, are demanding more from retirement accommodation.

Health-care offerings that suit independent residents through to those in frail care, as well as lifestyle and sporting facilities, are therefore among the priorities for retirement property developers. Such accommodation in the coastal areas of the Western Cape and KZN are particularly sought after.

For those wishing to retire, or more often semi-retire, Jonathan Acutt, the managing director of Acutts Real Estate, says the idea of moving to the coast as a lifestyle choice has become more predominant, especially as younger families seek opportunities overseas.

Acutt says there are three major considerations for those looking to semigrate to the coast:

1. Safety

“Safety and security are high on the priority list. This is why community scheme living, especially for retirees or semiretirees, is becoming more popular. These come with safety features such as 24-hour security, perimeter fencing, CCTV cameras, and access control for complete peace of mind.”

2. Social activities

Further to this, Acutt says there needs to be a strong focus on social activities and interactions with neighbours and communities. The social distancing during the pandemic highlighted the value of social interaction and

FIND US HERE:

@iolproperty @iolproperty @iolproperty.co.za

community engagements.

“That’s why it’s worth considering the availability of a community centre and social or sporting activities such as game nights, organised hikes, environmental groups, and markets. Estates that emphasise sustainable communities, where the communities are putting more in than they’re taking out, is important.”

3. Self-sustainability and sustainability

In a world where the supply of basic services, such as electricity and water, is an issue, he also sees a great emphasis on communities that are sustainable and self-providing.

“Retirees should look for elements like solar power, water storage and designs that maximise natural lighting and breezes. Beyond this, sustainable living, in itself, is a must. Living within a natural environment, supporting the natural environment, is a simply a better, healthier way to live.”

Echoing this, Reece Daniel, the developer of Serenity Hills in Margate, says people are looking for retirement homes where they can enjoy active, outdoor lifestyles. This has negated a need for priority shifts.

In addition to the above, Serenity Hills offers guidelines for those starting the hunt for a retirement home:

✦ Natural spaces.

✦ Pet-friendly accommodation.

✦ Value for money.

✦ Health care.

✦ Children’s facilities.

✦ Community.

For many retirees, however,

the idea of moving into a retirement village can be daunting, especially if they would rather not label themselves as in need of specialised elderly living. Weighing up the pros and cons is personal, and circumstances vary from person to person, experts say.

You might, for example, be a single older person with no children, married and with adult children who have left the nest, married, looking after grandchildren or supporting your adult children.

Whatever the case, many people get to a point where they’re quietly thinking about whether they should, or could, move into a retirement village. And one of the most important things to wrap their heads around is the sort of property contract they should enter into.

There are three possibilities offered in retirement villages – life rights, freehold and sectional title.

Life rights essentially means that once you pass away and your unit is resold, your estate gets back the amount you paid for the property, minus some costs, but not any profit made on the sale.

However, it does come with benefits.

Furthermore, most retirement complexes no longer offer outright ownership, says Jason Appel, the financial planner at Chartered Wealth Solutions.

“Internationally, it’s mostly life rights, but we’re still getting used to it here.”

Life rights options are more budget friendly than ownership. Levies also cover care of the garden, a swimming pool – if there is one – and all communal areas.

In the example he looked at for his parents, Appel says buying a life rights property was R500 000 less than buying it outright.

“The saving of R500 000 on capital outlay should, of course, be invested.”

If the extra income is not needed monthly, it will compound in the investment portfolio.

He adds that the saving on monthly levies/rates and taxes would, of course, also result in needing less monthly income out of your investments.

“A reduction in expense of R3 000 a month would add five to six years to the longevity of the client’s assets. The best way to improve the longevity of a retired person’s plan is to reduce their expenses, and a little goes a long way.”

If you go for life rights, you forgo the capital appreciation in the property’s value.

“This growth is hard to estimate as residential property valuations vary quite drastically. I would suggest that people consult their financial planners before making the decision.”

One of the main benefits of life rights, he explains, is that if you live to a really old age, and you run out of money, the village will not throw you out. Rather, the cost of your continued care is deducted from the capital amount you paid upfront.

Appel says people sometimes avoid life rights because the feeling is that their heirs will lose out on the initial investment.

However, personally, he would rather know his parents were being well cared for and there was no risk of him having to put in extra money down

the line.

“It really helps me knowing that’s taken care of.”

From a purely numbers point of view, it’s better to invest in a retirement village earlier rather than later.

“A person buying in at age 50 or 72 gets the same value over time, so the younger person will ultimately get a better deal. However, most people are not ready to even talk about it in their fifties.”

An added consideration though, is that most places have a waiting list.

The other two contracts explained:

✦ Freehold

Rob Jones, the managing director of Shire Retirement Properties, says the option means you own the land and building. It is your responsibility and you pay rates and taxes as there is a registered title deed in your name.

“You can leave it to your heirs and any gains in value would be for you. There may be some exit levy to pay to the complex, but it differs from place to place.”

✦ Sectional title

Here, you own a portion of the building, for example, an apartment or townhouse.

“You will have a title deed and you can leave it to your estate. You are responsible for internal maintenance, while the body corporate takes responsibility for outside maintenance as a general rule. You pay for that in your levies, of course.

“There may be some exit levy to pay to the complex, but it differs from place to place,” Jones says.

DISCLAIMER: The publisher and editor of this magazine give no warranties, guarantees or assurances and make no representations regarding any goods or services advertised within this edition. Copyright ANA Publishing. All rights reserved. No portion of this publication may be reproduced in any form without prior written consent from ANA Publishing. The publishers are not responsible for any unsolicited material.

Publisher Vasantha Angamuthu vasantha@africannewsagency.com Executive editor Vivian Warby vivian.warby@inl.co.za

Features Writer Bonny Fourie bronwyn.fourie@inl.co.za Design Kim Stone kim.stone@inl.co.za

Experts advise those who wish to retire or semi-retire on what to keep front of mind, and explain the various ownership options available

WIDENHAM RETIREMENT Village joins Margate, Ramsgate and Umdoni Retirement Villages as the new village in the Hibiscus Retirement Villages stable.

The development is set on 100 hectares of conservation area overlooking the sea, between the villages of Umkomaas and Widenham, 40km south of Durban and 9km north of Scottburgh.

Widenham Retirement Village has plenty to offer retired people. Two bowling greens, a swimming pool, a community centre, activity rooms, a gym, a library, a bar and club house facilities are administered by the residents, for the residents.

We have more than 25 activity groups, among them aqua aerobics, bridge and card clubs, fitness groups, garden club, walking groups and birding club. The Widenham Retirement Village Bowling Club is affiliated to the Kingfisher Bowling Association.

We have a nursing clinic, with sisters on duty, and a frail-care facility in the planning stages.

The village also has more than 8km of walkways throughout the wetland and around the perimeter fence. The property has electric fencing, security cameras, gate control and patrolling guards. At night, we have patrol dogs on the fence line.

We have two large water tanks and were able to keep our residents supplied with water over the past outage. Should it be necessary, we have access to borehole water as well.

Our wetlands are conservation areas and we are constantly monitoring them for alien plants which we remove. We have duiker, bushbuck, otter, mongoose and a plethora of birds in the wetlands.

Phases 1, 2 and 3 are complete and Phase 4 is 95% complete. A total of 345 cottages are occupied by more than 550 residents. Phase 5 has 60 sites from which to choose. Once you have chosen your site and decided on a two- or three-bedroom unit, we will begin building it for you.

All our Retirement Villages are sold on the life right basis. Peace of mind in your retirement is what you deserve – retire once, move once.

To visit us and experience our village and hospitality first hand, contact Caylin at 066 306 0669 or Jenette at 066 306 0612 from Monday to Friday during office hours.

DON’T expect an immediate inheritance if you are named an heir.

Receiving an inheritance or being named an heir means that someone, not necessarily a family member, thought of you while drawing up their last will and testament.

Being named in someone’s will or knowing you will be inheriting an asset can lead to excitement and anticipation, especially if you don’t know what you are inheriting.

While many people will be expecting to receive their inheritance immediately, in reality, it could take some time before you get what you are due to inherit.

Hilary Dudley, the managing director of Citadel Fiduciary, and Willie Fourie, the head of fiduciary services at PSG Wealth, explain wealth inheritance and how you can take care of the assets you have received.

Receiving an inheritance or being named an heir means that someone, not necessarily a family member, thought of you while drawing up their last will and testament.

“This person decided to bequeath an asset to you and, once the estate is finalised, this asset is then transferred to you,” Fourie said.

Dudley said nothing specific happened after a will had been drawn up and named you an heir, unless the person whose name the will was drafted in wanted to inform the people that they had been nominated.

Fourie said the mere nomination as an heir in a will did not mean that the named heir became entitled to the asset at that point.

“The will and bequest comes into operation only after the death of the testator and only once the will has been accepted by the Master of the High Court as the will of the deceased,” Fourie said.

After the death of a person,

informing heirs of their inheritance is not as dramatic as the formal reading of the will that is seen in movies.

“The executor nominated in the will normally informs the heirs that they are named in the deceased’s will and might share with them a copy of the will by email,” said Dudley.

Fourie said that once an heir had been informed of their inheritance, the executor may distribute the assets in the deceased estate only after the liquidation and distribution account has been:

✦ Approved by the Master of the High Court.

✦ Published in the Government Gazette and a newspaper in the area where the deceased was resident before death.

✦ No objections to the account had been lodged with the Master of the High Court.

Once all those things have taken place, the executor of the will can transfer the assets to the heir.

Dudley said it was important to note that there were laws and regulations in South Africa regarding inheritance, among them:

✦ The Wills Act that governed the formalities around the drafting and execution of wills.

✦ The Intestate Succession Act which dictated which family members would receive an inheritance in cases where the deceased did not leave a will.

✦ The Administration of Estates Act which set out how the deceased estate was administered. That includes the operation of the office of the Master of the High Court, the appointment of the executor and the executor’s duties.

✦ The Estate Duty Act that set out under what circumstances and how the estate duty would be levied on a deceased estate.

“There are various other laws, such as the Income Tax Act, that will also be applicable to the administration of a deceased estate,” Dudley said.

There are differences between a child and an adult being named an heir.

If a child is named in a deceased’s will and the will does not have provision for a trust, or if the deceased died without a will, the minor’s inheritance must be paid to the Guardian’s Fund which is administered by the Master of the High Court, a division of the Department of Justice.

“The child’s money in the Guardian’s Fund is invested with the Public Investment Commission. The child’s guardian can claim maintenance for the child whose money is held in the fund,” Dudley said.

Fourie said: “Normally a properly drafted will makes provision for a testamentary trust to be created for the benefit of the minor. This testamentary trust is then managed by the nominated trustees until the beneficiary of the estate reaches majority age, that is, 18 years old.”

With regard to adults, the inheritance can be transferred to them if the will contains certain restrictions on the transfer or provides for the management thereof in a trust.

As a final piece of advice, Dudley said: “In my experience, it is best to discuss these issues with your family as part of your estate planning process.

“Having an idea of what will happen after your death and your estate planning process will give your family certainty and peace of mind at a time when they are saddened and distressed.”

Fourie said an inheritance could make a real difference in the life of an heir by allowing them to pay their debts, supplement their retirement income or pay for a child’s education, so they need to get advice from a qualified investment adviser.

“If there is something left of this inheritance at the end of your life, pay it forward. There are charitable institutions that are in dire need of funding.”

& Full Bathroom *Parking Bay Close to Dean Street Shops, Restaurant and Jammie Shuttle Stop

Spacious North-Facing Two Bedroomed Apartment with Lounge and Balcony with Mountain Views. Bathroom with Shower over Bath. Fitted Kitchen. *Garage. *Walk to Shopping Centres, Restaurants, UCT and Transport.

CONTACT: RHONDA C: 082 448 7795 T: 021 685 2212 E: RRPSALES@MWEB.CO.ZA / WWW.RHONDARAADPROPERTIES.CO.ZA

This magnificent home sits high on our beautiful mountain at the edge of National Parks land and has uninterrupted views across False Bay towards Simon’s Town, the Hottentots Holland Mountains of Somerset West/Stellenbosh and South to Rooi Els as far as the eye can see.

Once you enter you almost have the feeling of being on board ship with every room boasting breathtaking views from every corner of the property.

PROPERTY DESCRIPTION:

TOP LEVEL: 1:

3 Garages with direct access double glazing, sliding doors and Euro style open in/tilt windows and doors for easy cleaning with lounge and dining view preserving Luxaflex Blinds. Fantastic entertainers kitchen with views, Luxaflex Blinds, open in/tilt windows, easy access drawer and cupboard systems. Energy saving instant water heaters for kitchen and bathrooms. 3 phase energy supply to enable load balancing and instant water heating. Beautifully appointed entrance, secure and side garden patio, lounge and dining areas with large balcony, 3 x 316 plate stainless steel pillars clad in ALU support sea facing beam. Low maintenance Rhein Zinc Eave cladding and gutter on main roof. Warranties on main and new garage roofing. Stainless steel recessed gutter on main roof feeds 2 x 6000 litre tanks in large level 3 store room, programmable water system.

LEVEL 2.

2 Bedrooms both with beautiful en suites, common balcony access and fabulous views. Ample cupboards. Carpeted bedroom areas..

LEVEL 3.

This level is office space with a separate bathroom at the moment but can be turned into an apartment with its own entrance or alternately another 2 bedrooms. Inside ALU American Shutters for security and comfort.

ASKING PRICE R7.25 MILLION

Bidding opens 7th Feb 2023 At 12h00 & closes from* 12h00 on 8th Feb 2023 https://bidlive.maskell.co.za

Duly instructed by the Liquidators of Oakbranch Trading (Pty) Ltd, Master's Ref.: D89/2022

Erf 9211 Pietermaritzburg in extent of 461m² : 3 Dassie Lane, VCCE Park Village

The property comprises a double storey 3 bedroom, 3 bathroom (all en suite) residence with an open plan lounge, kitchen / scullery & dining room, domestic accommodation, guest bathroom, double garage, laundry room

DOGON GROUP PROPERTIES

Atlantic Seaboard Office 021 433 2580

thekings@dogongroup.com

www.dogongroup.com

RHONDA RAAD PROPERTIES

Cape Town Office 082 448 7795

Email: rrpsales@mweb.co.za

www.rhondaraadproperties.co.za

SHELLEY RESIDENTIAL

KZN

Office 082 412 4463

Email: hello@shelley.co.za

www.shelley.co.za

DOGON GROUP RENTALS

Sea Point Office 021 433 2580

enquiries@dogongroup.com

www.dogongroup.com

DOGON GROUP PROPERTIES

Southern Suburbs, Claremont Office 021 671 0258

southernsuburbs@dogongroup.com www.dogongroup.com

CAPE WINELANDS

Nicho 072 601 1772

Hannes 066 476 1890

sales@aandewijnlanden.co.za

viognier.aandewijnlanden.co.za

SERENITY HILLS ECO ESTATE

KZN, South Coast Office 073 142 8292

Email: home@serenityhills.co.za

www.serenityhills.co.za

PETER MASKELL AUCTIONEERS

KZN

Office: 033 397 1190

Email: info@maskell.co.za

www.bidlive.maskell.co.za

BALWIN PROPERTIES

Ballito Office 084 788 1020

Email: michelle@balwin.co.za

www.balwin.co.za

DOGON GROUP PROPERTIES

Western Seaboard

Office: 021 556 5600 or 021 433 2580 enquiries@dogongroup.com www.dogongroup.com

VAN’S AUCTIONEERS

Gauteng Office 086 111 8267

www.vansauctions.co.za

www.iolproperty.co.za

WIDENHAM RETIREMENT

VILLAGE South Coast, KZN 066 306 0669 / 066 306 0612

www.hibiscusrv.co.za

www.widenhamretirementvillage.co.za