Indexed products are leading the way in the life insurance and annuity space. But critics continue to complain about misleading illustrations and complex products. Where do we go from here?

PAGE 12

An incredible ride with Integrity Marketing Group’s Bryan A. Adams

PAGE 6

The role of life insurance in estate and gift tax exemptions

PAGE 24 The ‘perfect storm’ driving annuity sales momentum

PAGE 28

What the end of the Chevron deference could mean for insurers

PAGE 38

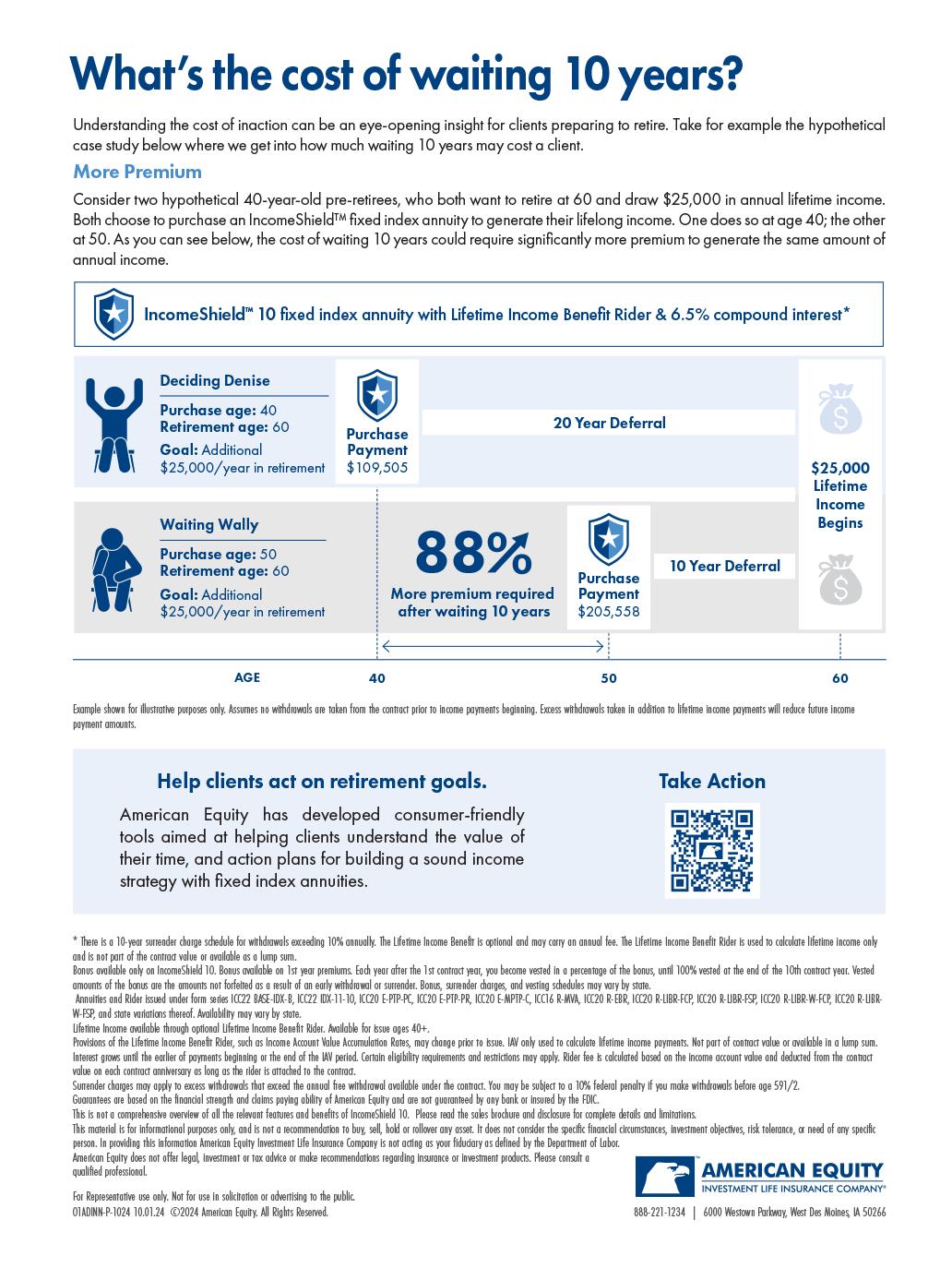

Are your clients ready to take action ?

See how much 1 0 years of inaction could cost your clients – page 5

Protect Retirement Financial Security with this Fixed Index Annuity

™

10% Premium Bonus¹ available on the IncomeShield 10 Money cannot be lost due to index volatility

Guaranteed income payments that cannot be outlived² Guaranteed Roll-up Income Account Value Rate Options

Annuities and Rider issued under form series ICC22 BASE-IDX, ICC22 BASE-IDX-B, ICC22 IDX-10-7, ICC22 IDX-11-10, ICC20 E-PTP-PC, ICC20 E-PTP-PR, ICC20 E-MPTP-C, ICC16 R-MVA, ICC20 R-LIBR-FCP, ICC20 R-LIBR-FSP, ICC20 R-LIBR-W-FCP, ICC20 R-LIBR-W-FSP, ICC20 R-EBR and state variations thereof. Availability may vary by state.

¹ Bonus only available on IncomeShield 10 (IncomeShield 9 in CA). Bonus available on 1st year premiums. Each year after the 1st contract year, you become vested in a percentage of the bonus, until 100% vested at the end of the 10th (9th contract year in CA). Vested amounts of the bonus are the amounts not forfeited as a result of an early withdrawal or surrender. Bonus, surrender charges, and vesting schedules may vary by state. See brochure and disclosure for details.

² Lifetime Income available through optional Lifetime Income Benefit Rider. Available for issue ages 40+. The minimum payout age is 50.

6000 Westown Parkway West Des Moines, IA 50266 www.american-equity.com

Help clients navigate the ups and downs of market volatility as you guide their ride to retirement.

Annuities from our Shield® Level Annuities Product Suite can help.

IN THIS ISSUE

INTERVIEW

6 An incredible ride

Bryan A. Adams founded Integrity Marketing Group, the nation’s leading independent distributor of life and health insurance products. He tells Publisher Paul Feldman about his company’s journey and its goal of providing holistic solutions to all Americans.

IN THE FIELD

18 From office helper to president

By Ayo Mseka

Before Elizabeth

Dipp Metzger became New York Life’s highest-producing Latina advisor, she was a young mother helping her husband sell insurance.

FEATURE

Indexing the Market

By John Hilton

Indexed products are gaining in popularity but critics complain about their complexity.

24 The role of life insurance in estate and gift tax exemptions

By James G. Blasé

Life insurance can be an alternative to grandfathering the large federal estate and gift tax exemptions.

ANNUITY

28 The ‘perfect storm’ driving annuity sales momentum

By Susan Rupe

Interest rates, market volatility and a growing demographic are fueling annuity interest.

INSURANCE & FINANCIAL MEDIA NE TWORK

HEALTH/BENEFITS

32 What Medicare clients are asking during open enrollment

By Susan Rupe

Provider networks, out-of-pocket drug costs and the future of Medicare Advantage are on clients’ minds, advisors say.

ADVISORNEWS

36 Emotional intelligence is a soughtafter skill for advisor By Ayo Mseka

Clients and prospects want advisors to understand their needs and relieve their stress.

IN THE KNOW

38 What the end of the Chevron deference could mean for insurers By Doug Bailey

The Supreme Court decision has implications for health and property/ casualty insurers.

The evolution of indexed products

The S&P Annual Survey of Assets last year revealed $11 trillion indexed to the S&P 500. The rapid growth of new indexed products in recent years reflects how these products have transformed the industry, offering the dual advantage of potential market-linked growth and downside protection.

Indexed products, especially indexed universal life insurance and fixed indexed annuities, have evolved significantly. These products give clients the opportunity to earn interest based on the performance of a specific index, while protecting their principal from market losses. This innovation addresses the increasing demand for retirement solutions that offer growth potential and security.

Traditionally, indexed products were linked primarily to well-known benchmarks like the S&P 500. While this index remains popular due to its historical performance and familiarity, the landscape of indexed products has expanded dramatically, offering a variety of options that cater to diverse client needs and risk tolerances.

Basic indexes

S&P 500 Index: The cornerstone of indexed products, it basically represents overall market performance, encompassing 500 of the largest U.S. companies. For clients seeking simplicity and reliable historical data, the S&P 500 is a logical choice.

Dow Jones Industrial Average: Another traditional option, the DJIA includes 30 prominent U.S. companies across various industries. While it

provides a snapshot of the market, its narrower focus compared to the S&P 500 might be more suited to clients interested in a more industrial- and blue-chiporiented index.

Russell 2000: This index tracks 2,000 small-cap companies, offering higher growth potential but with increased volatility. For clients with a higher risk tolerance and a focus on capitalizing on smaller, emerging companies, the Russell 2000 may be a good fit.

Innovative indexes

Innovation in indexed products has given rise to more sophisticated and exotic indexes, enhancing the appeal of FIAs and IULs by catering to various investment strategies and preferences.

MSCI Emerging Markets Index: This index includes equities from emerging economies, providing exposure to markets with high growth potential. It’s an excellent choice for clients looking to diversify their portfolios internationally while still benefiting from the security features of indexed products.

NASDAQ-100: Focusing on 100 of the largest nonfinancial companies listed on the NASDAQ stock exchange, this index is tech-heavy, appealing to clients bullish on technology and innovation sectors. The NASDAQ-100 offers higher potential returns, aligning with clients seeking growth opportunities in the technology-driven segments of the market.

Global multi-asset indexes: These indexes combine various asset classes, including equities, bonds, commodities and currencies, offering a diversified approach within a single product. This innovation

allows clients to benefit from a balanced risk-return profile, catering to those who seek a holistic investment strategy. Risk control indexes: These indexes dynamically adjust their exposure to different asset classes based on market conditions, aiming to maintain a predefined risk level. They appeal to clients who prioritize risk management and stability, offering a smoother ride through volatile market conditions.

Exotic indexes

The more exotic indexes may be of interest to clients with specific interests or higher risk tolerances.

Volatility control indexes: These indexes aim to mitigate the impact of market volatility by adjusting the allocation between equity and fixed-income components. They are designed to provide steadier returns, making them suitable for clients looking to navigate turbulent markets with confidence.

Thematic indexes: These indexes focus on specific sectors or trends, such as technology, health care, or clean energy. They offer clients the opportunity to invest in areas they believe will outperform in the future.

ESG indexes: As awareness of sustainable investing grows, environmental, social and governance indexes have become increasingly popular. These indexes focus on companies with strong environmental, social and governance practices. Clients committed to responsible investing will find ESG indexes aligned with their values and financial goals.

Custom hybrid indexes: Some products now allow for customized indexes that blend multiple strategies or sectors, tailored to individual client preferences and risk profiles. These offer a bespoke investment experience.

Innovation in indexed products has significantly broadened the options available to clients. The diversity and sophistication of indexed products provide advisors and their clients with an ever-growing choice of strategic approaches to enhance growth opportunities while safeguarding investments. And there is no end in sight for this explosive trend.

John Forcucci Editor-in-chief

Insurers warned of risks from ‘silent AI’

As use of artificial intelligence in the insurance industry expands, global consulting firm Alpha FMC has cautioned insurers to be aware of unforeseen risks that can lead to significant financial losses — a concept they refer to as “silent AI.”

Insurers in the United States are facing increasing pressure to adopt AI, due to growing competition and client demand, while simultaneously lacking standardized regulation that would enable them to uniformly navigate AI usage. However, insurers have no empirical data or theoretical models that estimate the frequency of potential losses. Additionally, most of the related legal cases have revolved around copyright infringement rather than unforeseen risks.

Silent AI refers to potential risks in traditional property and liability insurance policies that are associated with the use of artificial intelligence but are neither explicitly included nor excluded.

For example, it can apply to an insurance policy that did not take AI-related risks into account when it was issued. Those risks could be considered “silent” because they were not specifically addressed, and the policy could unintentionally cover them because of an overly broad definition and/or the absence of specific exclusions.

MORE OLDER WORKERS FILLING THE LABOR POOL

If you think you’re seeing more older workers in the office or in the shop, you’re not imagining things — new research shows the prime working age population (25-64 years old) has significantly fallen and is being filled by older workers. At the same time, the labor force participation rate of those ages 65 or older has not reached its prepandemic level, while that of the prime working age population has reached that level.

The report, “Trends in Labor Force Participation and Employment of Americans Ages 16 or Older,” examines the U.S. civilian labor force through December 2023, using data from the U.S. Census Bureau’s Current Population Survey.

When analyzing the U.S. population ages 16 or older by age and gender, females ages 65 or older made up the largest proportion by a sizable margin. However, males of the same ages tended to make up a comparatively larger share of the labor force than females, with the labor force gaps being smallest among the youngest and oldest age ranges.

JOB SEARCHING REACHES

HIGHEST LEVEL IN A DECADE

While the prime working age labor pool shrinks, more Americans are searching for new jobs — the highest rate in a decade, according to the New York Federal Reserve. The Fed survey found 28.4% of respondents were looking for a job — the highest reading since March 2014 and up from 19.4% a year ago. That includes both individuals already out of a job and ones currently employed but seeking new roles.

Job insecurity also reached a record high, the new survey found: The percentage of those expecting to become unemployed rose to 4.4%, up from 3.9% a year ago and the highest level ever recorded for the survey, which goes back to 2014.

How much unemployment or slowdown in growth should we be willing to accept to shorten the length of time that inflation is too high?”

— Kristin Forbes, an economist at Massachusetts Institute of Technology

The increase in job searchers was most pronounced among respondents older than 45, those without a college degree and those with an annual household income less than $60,000.

HAIL CREATING HAVOC FOR INSURERS

What caused the highest weather damage costs in the U.S. so far this year? It’s not hurricanes, floods or tornadoes — it’s hail, and researchers believe hail will wreak even more havoc because of climate change.

Research suggests that climate change will cause large hailstones to become more common. Next year, scientists plan the first U.S. field study of hail since the 1970s, in which they will chase hailstorms the way some do tornadoes.

Gallagher Re, a global reinsurance firm, said thunderstorms have been responsible for about $61 billion in economic losses. Hail was likely responsible for between $31 billion and $49 billion of that total. In the same period, tropical storms and flooding together have accounted for $14 billion in losses.

Bryan Adams’ path took him from funeral homes and folding shirts to heading an industry juggernaut, Integrity Marketing Group.

Integrity Marketing Group may not have started in 2006 had it not been for Bryan Adams’ job folding shirts in a shopping mall clothing store while in college.

“One day, I was standing there and saw a sharply dressed guy — I’ll never forget him — gray suit, red tie, white shirt. He looked like a million bucks. And he’s just the friendliest guy in the world. He said to me, ‘You seem pretty good with people, you ought to come work for me.’ And I asked, ‘What do you do?’ And he answered, ‘I sell life insurance.’”

“If that guy, Gary, hadn’t asked me to do that, I don’t know where my life would be today,” Adams said.

Today Integrity Marketing Group is the nation’s leading independent distributor of life and health insurance products, and recently launched Integrity Wealth, now valued at about $50 billion.

In this interview with InsuranceNewsNet

Publisher Paul Feldman, Adams describes how Integrity has “partnered” with many firms and agencies, acquiring new talent and skills as it has built both capabilities and value, and, in the process, created an industry leader.

Paul Feldman: Tell us a little bit about yourself, and how you got into the industry.

Bryan Adams: I grew up in a small town of about 1,800 people in West Texas. My mom and dad owned three funeral homes. There’s nothing like growing up in the 1970s and ’80s with the last name of Adams and your family owns funeral homes. My sister and I worked at the funeral homes ever since we could open the door, literally — we would welcome people in. And I was washing cars, mowing lawns, cleaning caskets, all of that.I ended up spending a lot of time with people within the investment part of the company I was with. I spent time with people in corporate finance, actuarial people, as well as distribution and marketing people. I connected with and enjoyed working with people within marketing and distribution because it was all about business development and how you can leverage technology for the betterment of your business.

For my dad, it was a calling to serve people. For my mom, it was much more

of, “OK, well, let’s make sure we take care of not only everybody else’s family but our family, too.” My mom and dad worked all the time. There were a lot of times we didn’t have dinner together because there were visitations, etc.

Sometimes my mom and dad would say, “I can’t believe that family didn’t have any plans in place.” I remember those conversations. I was probably 9 years old when my parents were talking about a family in town who had done pretty well, but their loved one passed away, and they couldn’t pay for the funeral.

and straighter than most people, because I folded so many pants and shirts in that job.

One day, I was standing there and a sharply dressed guy — I’ll never forget him — gray suit, red tie, white shirt. He looked like a million bucks. And he’s just the friendliest guy in the world. He said to me, “You seem pretty good with people, you ought to come work for me.” And I asked, “What do you do?” And he answered, “I sell life insurance.” And I said, “Man, listen, I grew up in a funeral home, and I’ve been wondering this my whole

And my dad said, “Don’t worry about it, we’ll figure this out.” My mom was like, “OK, again, we need to provide for our family, so how are they going to pay for it?” And there would be this natural tension between the two of them.

I remember at an early age I asked, “Why don’t more people plan for this if they know it’s going to happen? It’s inevitable that we’re all going to pass away.” And my dad said — I think he quoted Winston Churchill — “Because Americans are the only society on earth that believes that death is optional.” And you would see families who had life insurance and how much easier it was for them — the relief in those families was evident.

Later, when I was in college at Texas Tech, I was working in the mall in retail. I was the guy who was folding the shirts. You would come in, look around, and you’d kind of mess them up, and I’d be like, “Oh, my God, I’ve got to fold them again.” To this day, I can fold a shirt faster

life. Why don’t more people own life insurance?” And he said, “Well, that’s what we do, we give people peace of mind.” So I went to work with him.

Back in those days, you were walking door to door and trying to get in to tell people about what we were offering. But I had this passion. I could say, “Look, I grew up seeing the issues when someone didn’t have life insurance, and I can help you with this.” I had some early success with that. After college, I went to work for the investment group that owned those insurance companies. The rest is history. It has been my passion to help people.

Feldman: How did you start Integrity? Where did it all begin?

Adams: I started this out of my house. I started with my dog — he’s no longer with us — literally under my desk. I worked out of my house for a long time. When I got married, I had six people

Bryan Adams, his family and Integrity Marketing Group give back to the community in many ways, including a holiday toy drive.

working in cubicles in the house. My wife and I dated for a couple of years, so she was accustomed to the situation. She was cool for about the first year, and then she said, “OK, I think it’s about time for you to get an office.” It has been an incredible ride. I pinch myself every day.

Now, we’re serving people holistically. There’s a huge need for people to be served holistically with their life, health

advisement. We think that there’s a way for us to help them plan for the good days ahead in their retirement.

As you get older, there are two main concerns that people have: their health and their wealth. Your health may determine where you might rank those two. If you’re older and you’re healthy, then you tend to be focused on how to maintain your wealth. If, all of a sudden, you have

and wealth needs. That’s really the genesis of how we started Integrity. It was those early days understanding that people need what we do. We’re in one of the most noble professions in the world. We serve people in their most important times. And everybody wins. The carrier wins, agents win, agencies win — ultimately the consumer must win, first and foremost. It’s a virtuous business, a noble profession and I’m proud to be part of it.

Feldman: Integrity is one of the largest distributors in the United States. Tell us about your distribution and how you cover other markets, because it’s not just life insurance, health insurance and annuities. Now you also have Integrity Wealth.

Adams: We’re passionate about the wealth business today. We believe that most Americans don’t have great access to wealth advisement. I think a lot of the bigger banks and institutions want to focus on the ultrahigh net worth. But most of our clients — the everyday people, like my family — don’t get great service in wealth

a health issue that pops up, then it’s, “OK, gosh, do I have the right health insurance product? And how am I going to move on from this event to make sure that I live a long and healthy life?”

Also, people inherently want to leave a legacy and be remembered long after they’re gone. We’re able to do that with life insurance. Life insurance is one of the greatest tools to help people leave a legacy, whether that’s planning for your final expenses or for estate planning — or everything in between. We have so many incredible resources and products, and incredible carrier partners that we work with on providing those.

A lot of our businesses had been involved in the wealth management business with their own broker-dealer or registered investment advisor. We decided to bring those broker-dealers and RIAs together under one roof with Integrity Wealth. That enables us to leverage all those different capabilities — so that everybody has the best-in-class technology, service, custodians and resources; and so that we can make sure that we’re giving everyday Americans the best world-class

wealth management resources. We’re able to give them those resources that you would get at any large institution or big bank. Now, we’re able to meet them and give them even better coverage on their wealth side as well. We have decades of experience through our partners. We’re excited because now we’re able to leverage all those different capabilities, and our size and scale, to give people more options and ultimately serve them better.

Feldman: How do you see wealth management evolving? How has it evolved in recent years?

Adams: We’re incredibly excited. In fact, we just brought in a new president for Integrity Wealth, Craig Walling. He has tremendous experience in the industry and has done some amazing things, including heading UBS Private Wealth. One of the things we wanted to do is holistically serve people with their life, health and wealth, and do that by using a lot of our technological resources. Two and a half years ago, we had zero wealth assets; today, in aggregate, we have almost $50 billion of assets that we’re helping people with. We think that we’re just beginning that journey. It’s a big opportunity for us to meet people where they are. With the millions of customers that we’re already serving, and the hundreds of thousands of agents that we help on a dayto-day basis, we think that there’s a big need for us to be able to serve our agents. We’re looking at opportunities to help them get dual registered and get licensed in the wealth space, if they choose. We have world-class resources to be able to do that. In addition, we think that there’s an incredible opportunity for us to leverage our platform to bring in other wealth managers, to be able to leverage our technology, our resources. We want to meet customers wherever they are. We’re just getting started on that, and that’s a big part of where we’re going from here.

Feldman: I know you’re working to bring new people to the industry. Most organizations only want to work with somebody who’s already in the business, and those people just go from marketing organization to marketing organization.

Integrity Marketing Group employees clean up a playground in Fort Wayne, Ind.

Do your clients long for the lifetime income their parents got from a pension plan? The ApexAdvantage fixed index annuity provides the guaranteed income* they’re seeking—along with unmatched flexibility and control:

IMMEDIATE INCOME—Turn on competitive income payouts in as soon as 30 days.

TRUE INCOME DOUBLER—Receive double payouts for impairment in 2 of 6 ADLs:

• No confinement required.

• No medical underwriting.

• No fortune telling: Select joint or single lives and increasing or level payouts when income starts, not at issue.

LIFE INSURANCE FUNDING—Leverage direct-to-third-party-payouts to fund life insurance or leave more to charity!

Learn more about this exciting FIA from “A” rated** Ameritas Life Insurance Corp.

In approved states, ApexAdvantage Index Annuity (Form ICC22 2707 with ICC22 2707-SCH or 2707 with 2707-SCH) and riders are issued by Ameritas Life Insurance Corp. (Ameritas) located at 5900 O Street, Lincoln, NE 68510. Products are designed in conjunction with Ameritas and exclusively marketed by Legacy Marketing Group® Ameritas and Legacy Marketing Group are separate, independent entities. ApexAdvantage Index Annuities are modified single premium deferred annuities that offer a fixed interest option and index interest options. The index options are not securities. Keep in mind, your clients are not participating in the market or investing in any stock or bond. Policies, index strategies, and riders may vary and may not be available in all states. Optional features and riders may have limitations, restrictions, and additional charges. Product guarantees are based on the claims-paying ability of Ameritas Life Insurance Corp. Refer to brochures for additional details. ApexAdvantage is a registered service mark, and FutureNow Rider is a service mark, of Legacy Marketing Group. Ameritas® is a registered service mark of Ameritas Life Insurance Corp.

* A Guaranteed Lifetime Withdrawal Benefit is available for a current annual charge of 1.25% for the FutureNow Rider and 1.35% for the FutureNow Rider With Booster, multiplied by the premium accumulation value during the accumulation phase and by the benefit base during the withdrawal phase. ** A (Excellent) for insurer financial strength. This is the third highest of AM Best’s 13 ratings. Rating as of 5/4/2023. Ameritas Mutual Holding Company’s ratings include Ameritas Life Insurance Corp.

Adams: Most people think that this is a male-dominated industry, and I think it has been for a long time. One of the things I can say about Integrity, more than half of my executive team are female and diverse. If you look at our workforce, 63% of our employees are female — more than half of our customers are female. If you look at our agent base — we have the largest agent base in the country — 46% are female, which is incredible, and 40% of them are from minority communities. We’re meeting people where they need to be met in their communities; we’re incredibly passionate about that, and I think we’re truly changing the industry in so many ways for the better.

We want to serve all Americans. I mean, I’ve gone through this with my mom and dad. My dad’s gone through some health issues recently. As we’re going through it, my dad is being taken care of with incredible Medicare products that we created. He has great long-term care insurance. He’s not in a nursing home, but in case he ever is, he had the foresight to buy that policy 25 years ago. He has great life insurance coverage through our organization, he has annuity products for his wealth management and he also has wealth management products. As I’m looking at this from my mom and dad’s situation, as the one who manages a lot of that for them, well, that’s another reason I look at it and say, “There must be holistic planning.”

As these things happen, I need to explain it to my mom. Sitting down with my mom, who is one of the smartest people I’ve ever met, she’ll ask me — because these are complex situations — “Are we going to be OK?” And I say, “Well, let me break this down for you.” And it’s something I’m incredibly passionate about, because we want to make sure that everybody’s taken care of and everybody’s invited into this process, because everybody’s going to be impacted. Whether it’s your health insurance, your life insurance or your wealth management, everybody’s impacted.

We just need to make it simpler, easier to understand, and, ultimately, more human. So people know they’re being seen and understood and we’re not just selling some product to sell a product. These are products that they’re going to need at

some point, and I’m living through this with my parents today.

Feldman: Mergers and acquisitions have been an important driver for Integrity. How do you see that playing out in the future?

Adams: We never acquired companies just to acquire companies. We are very strategic at partnering with people. And we don’t call it “M&A” or “acquiring,” we call it “partnering.” It’s how I started Integrity in the beginning with this idea, in 2006, and my two co-founders and I

We tell employees, “Whatever your title is, it should also be owner, and here is your ownership.”

came up with this concept. We thought if we all keep on beating each other up and trying to fight for every last nickel and dime, it’s going to be a race to the bottom. But if we all come together, the rising tide will raise all boats. I fundamentally believe that. That’s where we created Integrity, with this idea that let’s all work together and serve more people and leverage our scale and size.

We didn’t do that with the idea of acquiring businesses; that kind of happened later as people started needing succession planning, etc. But what we found is that if you find people that have the best distribution, you have the best resources, you have the best products and services in the best geography. By coming together, we can serve people holistically, and we can do that anywhere in the U.S. So, it has been an important part of our being able to bring in new capabilities in data and market research, like we’ve done with some of our businesses, marketing advertising with Thomas Arts, with some of the technology businesses we’ve partnered with. Product development, like Nexus, which is an incredible product

development business — Ron Schertz is one of the most incredible leaders.

Mike White innovated the Medicare space with AIMC and developed a lot of Medicare supplement products. Tim Ash has really perfected the institutional service of clients and organizations with Ash Brokerage. I mean, we brought in so many incredible partners with the idea that one plus one equals a lot more than two. And it has been a lot of fun, as we’ve been able to say, “OK, let’s look at what you are great at, what you’re world-class at, and let’s share those capabilities. Then go out and serve more people with this kind of focus on our core values of Integrity, of family, of service and respect and partnership.”

Feldman: What is one thing about Integrity that you are most proud of?

Adams: I think one of the things I’m most proud of is that we’re an employee-owned company. In 2019, we became employee owned. We decided to give some of our shares to every single employee. Every employee at Integrity — regardless of whether you’re a janitor or you’re an executive — is a shareholder in this company. Our employees and our partners are the majority owners of our company today. It’s something I’m prouder of than anything else that we’ve done.

It comes back to this philosophy that we’re a service company. I fundamentally believe that, as an owner, you will serve people better than as just an employee. We tell employees, “Whatever your title is, it should also be owner, and here is your ownership.”

Our employees on average have seven times the amount of employee ownership as they do in their 401(k) plan. We gave them the stock; we don’t charge anybody for it. They didn’t have to get an employer match, or all that type of stuff. We said, “We want you to be an owner of this company. And it should change everything. It should change the way you come to work, it should change the way you interact with your co-workers, the way that you innovate this industry, and, ultimately, how you serve the agents and their clients as an owner of the business.” I think it’s one of those things that will help us continue to differentiate Integrity, long term, in being able to serve people better.

to

And 10% Free Withdrawals FOR AGENT USE ONLY. NOT INTENDED FOR THE GENERAL PUBLIC.

The Evolve Income Value has no cash value and cannot be withdrawn as a lump sum and is not part of the death benefit. SILAC® is licensed as SILAC Life Insurance Company in the state of California, license #6244-8. Withdrawal charges, bonus recovery and market value adjustment may apply to withdrawals made during the withdrawal charge period. Interest credit amount is not indicative of future performance. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. See Certificate of Disclosure for more details. This is a product of the insurance industry and not guaranteed by a bank, nor insured by FDIC or NCUA/NCUSIF. Product availability may vary by state. In Idaho, policy form is ELCFIA-ID. Not a deposit. Not insured by a federal government agency. Restrictions apply. May only be offered by a

Indexed products are leading the way in the life insurance and annuity space. But critics continue to complain about misleading illustrations and complex products.

Where do we go from here?

BY JOHN HILTON

Americans love the idea of participating in the stock market, especially when they’re not risking any losses.

That is a true winwin, and is the concept driving indexed products to spectacular sales of both annuities and life insurance.

On the annuity side, insurers who viewed indexed trends skeptically are rushing products out to join the sales frenzy. Indexed annuity sales totaled $59.3 billion through the first half of 2024. By comparison, $55.5 billion worth of indexed annuities were sold for the entire year in 2020.

Indexed annuity sales are on pace to rise 20% over last year’s record-breaking numbers.

Life insurance is a little different story. Whole life remains the dominant product, although in a sales decline, and term life remains a source of quick, direct-to-consumer sales. But Sheryl Moore, CEO of Wink Inc. and Moore Market Intelligence, is projecting record sales of indexed life insurance.

“Right now, the rates are absolutely fantastic,” Moore said in late August. “You have to remember that we’re coming off of a historically low interest-rate environment and everybody’s kind of high on these caps and participation rates because they’re so attractive. It’s a lot easier sale than it typically has been in a long time.”

John Foard is a certified financial planner and co-founder of Crown Advisors in Mooresville, N.C. He does not recommend indexed products for every client. With no downside, they are a good fit, though, for those who shy away from risk, Foard said.

“It is the fastest-growing segment of the life insurance market,” Moore said earlier this year.

Beyond sales numbers, the indexed universal life insurance market continues to attract big-case sales as well as critics from across the industry.

Those criticisms are among many threats to the indexed sales phenomenon. The industry has no control over some challenges, such as an interest rate cut from the Federal Reserve, an action expected to take place after this issue went to press.

“The market is expecting multiple rate cuts from the Fed this year,” said Michael Normyle, U.S. economist for Nasdaq, during a recent webinar. “Close to three cuts is what markets are pricing currently.”

to not replace it with a product that has a cap of 9%.”

Insurers meeting the need

The indexed market is not lacking for products as insurers engineer new indexes and new products to meet the need. Four new accumulation-oriented IUL products hit the market within a few weeks in August.

But for many others, an indexed annuity or IUL product is the right answer in the present economy. Interest rate spikes, especially in indexed annuities, whenever there is market volatility, Foard explained. People remember the market wipeout in 2008-09, and even Black Friday in October 1987.

“You could argue the decision to implement an indexed product, such as an annuity, to protect one’s assets after a major market correction or bear market is the result of fear or emotion,” Foard said. “Nonetheless, when an individual or family sees a major portion of their life’s savings wiped out in a fraction of the time it took to accumulate it, it creates fear of the unknown.”

The Federal Reserve adjusts the federal funds target rate range in response to changes in the economy. Manipulating rates helps the Fed satisfy a dual mandate to keep prices stable and maximize employment.

After a long period of near-zero rates, the Fed got busy in early 2022. Over a 16-month period, Fed Chair Jerome Powell announced 11 rate hikes taking the fed funds rate from 0.25% to 0.50% to 5.25% to 5.50%.

On the annuity side, insurers are realizing that structured annuities — also known as registered indexed-linked annuities — are not just a passing fad. Many companies that were big in the variable annuity space have pivoted to structured annuities.

Jackson Financial is one example. Once the No. 1 seller of variable annuities, the company endured a financial downturn along with the product line. Jackson engineered a comeback on its Market Link Pro RILA suite, introduced in late 2021. RILAs were introduced in 2010 by AXA Equitable Life Insurance Co., now known as Equitable, but it took some time for RILAs to catch on. RILAs hit $2 billion in sales by 2014, the year that Allianz, CUNA and MetLife introduced RILA products.

During the first half of 2024, LIMRA lists 19 sellers of indexed-linked annuities, accounting for nearly $31 billion in halfyear sales.

“I think that we’re going to continue to see more players enter the structured annuity space, even insurance companies that don’t have variable annuities,” Moore said. “When Athene hopped in there, that was a surprise. When F&G hopped in there, that was a surprise. Because these were companies that didn’t have VAs.

“So, I think we’re going to continue to see new players hop in, and I don’t see the growth slowing down anytime soon.”

American Equity’s IncomeShield 10 was the No. 1 selling indexed annuity, for all channels combined, during the second quarter, Wink reported.

The time is (economically) right

Indexed products sit squarely in the sweet spot amid an equities market that is robust but also prone to turbulence and uncertainty, a massive market of retirees and near-retirees, and rising interest rates.

One by-product of the rising-rate environment is an eagerness to exchange annuities for better yields.

“There has been a ton of replacement activity in the annuity market,” Moore said. “There are S&P 500 caps out there of 3.5%, and it almost seems like a crime

“They’re hitting the top of the spreadsheets for income. So, that’s really what our industry has come down to when we’re talking independent insurance agents,” Moore said. “American Equity has just been killing it. They’ve been at the top of the spreadsheets for some time. Their pricing is attractive.”

Moore

Normyle

Foard

How informed are consumers?

While strong sales are good news for agents, insurers and everyone in between, the critics of indexed products are not going away. “Zero is our hero” is a marketing slogan used to promote indexed annuities and remind consumers that they won’t lose money with the zero floor.

That concept works well in a mediocre or down market. But the Dow Jones Industrial Average has more than doubled from its pandemic low of 19,200 and rose about 10% in the first nine months of 2024.

The caps and participation rates on most indexed products limit growth. Typically, annual caps on indexed annuities range between 4% and 8%, although the exact cap can depend on the insurer, the type of index and the specific product.

Likewise, once funds are committed to an indexed product, they cannot be retrieved without paying a surrender penalty. Consumers need to know what they are getting into, Foard said.

“You are committing your funds to that insurance company’s specific product for a minimum specified amount of time, such as seven to 12 years, depending,” he explained. “This means you are unable to leave that product or company for the stated number of years without incurring a penalty to do so, and the penalties can be rather steep — especially in the earlier years.”

Indexed products are often confusing even for financial professionals, said Michael Collins, financial advisor and founder and CEO of WinCap Financial.

return, and I’m just like, ‘Yeah, that’s not guaranteed, but that’s just insane,’” Moore said. “Nobody should buy an indexed annuity thinking they should get 15% every year, but it’s happening.”

there’s a gap between what I’m hearing from consumer representatives and insurance companies that’s more significant than what I would otherwise expect, and I can’t quite figure out why,”

Nobody should buy an indexed annuity thinking they should get 15% every year, but it’s happening.

— Sheryl Moore

The issue with illustrations is the same for both indexed life insurance and annuities — unrealistic projections — but is playing out differently.

On the annuity side, the National Association of Insurance Commissioners adopted the Annuity Disclosure Model Regulation in 2012. Section six covers illustrations for fixed and fixed-indexed annuities with nonguaranteed elements.

However, only 10 states have adopted the specific section dealing with annuity illustrations.

said Michael Humphreys, Pennsylvania insurance commissioner. “I’d like us to be comparing illustrations with the same basic premise so we can all agree on whether they pass or fail, but we’re not there.”

IUL in court

Problems with IUL illustrations are being fought in court more so than in front of regulators. IUL is often part of complex premium financing deals with large amounts of money at stake. Several of these deals have gone bad and led to lawsuits.

“Clients that I would not recommend indexed products to include individuals who are seeking immediate growth or guaranteed returns on their investments, as well as those who have a low risk tolerance and are not comfortable with potential market fluctuations,” Collins added.

Illustrated concerns

The confusion that comes with indexed products is rarely helped by accompanying illustrations, critics say. Rather than helping clients understand, or at least showing them a realistic expectation, illustrations often do neither.

“I have some products that are illustrating a linear 15% guaranteed annual

“Greater adoption across more states would ensure more consistency in how carriers approach annuity illustrations, providing a uniform standard that benefits both consumers and the industry,” said Mike Considine, executive vice president and head of U.S. government and regulatory relations for Athene.

Considine and Adam Politzer, chief product officer for Athene, joined a Life Insurance and Annuities Committee meeting to talk about annuity illustrations during the NAIC summer meeting in August.

“I feel like with illustrations,

In other situations, internal costs can cause an IUL account’s value to drop substantially. That puts a policy at risk of lapsing, and the policyholder is on the hook for higher premiums—sometimes significantly higher premiums—just to keep the policy intact.

The common thread with IUL lawsuits nationwide is the illustration presented to buyers.

Actuarial Guideline 49 was adopted in 2015 to address IUL products created after the original 1997 illustration model was adopted. Insurers quickly got around it by offering IUL products with multipliers and bonuses.

Collins

Considine

Politzer

You can’t predict what’s ahead. But now you can plan for it with an income solution that offers the resilience, adaptability and growth potential clients need today. Protective® Aspirations Variable Annuity is designed to deliver strong guaranteed income, more control over investment strategy, and more flexibility for life’s twists and turns. Because retirement is dynamic. Your clients’ income solution should be, too. Learn more at protective.com/aspirations-va.

That led to AG 49-A in 2020 and, eventually, AG 49-B. Regulators referred to the latter update as “a quick fix” when adopted in 2023.

Moore called on the NAIC to reopen and amend model regulation 582, which covers life insurance illustrations. Regulators are not eager to take on that fight, with some predicting it will take three years minimum to complete.

“I’m seeing way more lawsuits on indexed life than I do on indexed annuities,”

avoid any perception of a direct investment in the stock market.

Awareness of all fixed products grew following the Great Recession of 2008-09. Millions of near retirees were crippled financially when retirement accounts lost a huge chunk in the market collapse. “Flight to safety” entered the retirement planning lexicon as new indexed products offered the opportunity to participate in market gains without ever losing valuable retirement dollars.

I do think there will be more lawsuits related to indexed annuity illustrations. I just think we haven’t had a market environment where people are getting enough zeros that they’re saying, “Hey, this isn’t what I signed up for. Let me talk to an attorney.”

— Sheryl Moore

Moore said. “But I do think there will be more lawsuits related to indexed annuity illustrations. I just think we haven’t had a market environment where people are getting enough zeros that they’re saying, ‘Hey, this isn’t what I signed up for. Let me talk to an attorney.’”

Everybody gets an index

Equity indexed annuities first appeared in 1995 as an innovative product design that gave consumers a path to earn interest based on the performance of a stock market index, most commonly the S&P 500, without any downside risk.

By 2006, the industry realized the word “equity” was too confusing. Products were renamed “fixed indexed annuities” to help

Then came the proprietary indexes. Moore counts roughly 160 different indexes now, many with grandiose names such as the JP Morgan Mozaic II index.

One issue is the lack of history with many of these proprietary indexes. A traditional index like the S&P 500 has decades of history to provide consumers with thorough illustrations based on historical performance. Newer indexes don’t have that.

“It’s been a bull run over the last 10 to 20 years,” Politzer said. “As a result, any reliance on that period of data is going to show a somewhat optimistic forecast of the contract. It’s just the nature of how the math is completed. We’ve actually added an extra disclosure to our

illustration as a result.”

Politzer conceded that some illustrations showed unreasonably high results and said Athene pulled “a couple because we weren’t comfortable putting them in front of customers.”

Then there are the “hybrid” indexes, a combination of multiple indexed asset classes or securities, often with a volatilityoverlay mechanism to stabilize returns.

Illustrations might not be as big of a factor as in the past, Moore said, because many agents are “flocking to the triedand-true” indexes such as the S&P 500.

“The conversations I’m having with agents … I’m getting feedback where they’re saying ‘I don’t trust hybrid indexes,’ or ‘My clients did not fare very well with their indexed hybrid allocation last year, and so I’m burned out on them,’” she said.

Volatility still present

The overall economy remains far from a comfortable, confident position, analysts from Nasdaq said during a recent webinar on economic trends and index innovation hosted by the National Association for Fixed Annuities.

While the Fed can exert influence through multiple rate cuts this year, there remains concern about the labor market balance and potential recession risks, said Normyle, joined by Mark Marex, senior director in index research and development for Nasdaq.

The COVID-19 pandemic highlighted the need for downside protection and diversification in a portfolio, Normyle said. Insurers can provide that through indexed products.

“The biggest thing that we continue to see and hear from clients is that investors want more choice,” Normyle said. “They don’t want to only be presented a menu of S&P 500 [volatility] control products that are fixed annuities. They want to be able to do RILAs. They want to be able to do something more exciting in the equity sleeve.”

InsuranceNewsNet

Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at john. hilton@innfeedback.com. Follow him on X @INNJohnH.

REDEFINING PROTECTION, INSPIRING TRUST

IT’S TIME FOR YOU TO STAND OUT AND OFFER THE

LifeShield isn’t just another name in Medicare Supplement Insurance—we’re built on a foundation of stability, choice, and service.

For nearly 50 years, LifeShield has been synonymous with reliability and innovation. Your clients and your business will thrive with LifeShield.

• Unmatched Flexibility: Give your clients the freedom to choose plans that fit their unique needs.

• Competitive Rates: Offer your clients competitive rates they can count on.

STEP UP AND STAND OUT.

• Boundless Choice: Let your clients go beyond the network. They can see any Medicare-approved provider—unrestricted and uncompromising.

• Outstanding Service: When you and your clients need support, you can rely on us for personal service.

LifeShield offers more than just insurance—we redefine coverage and elevate support to a new level. Empower your clients to live the life they choose. Transform your practice with LifeShield and make an impact that lasts.

Visit www.lifeshieldcombo.com.

Before she became New York Life’s highest-producing Latina advisor, Elizabeth Dipp Metzger was a young mother helping her husband sell insurance.

By Ayo Mseka

Before Elizabeth Dipp Metzger became a financial professional, she would spend her days helping her husband, Brian, sell insurance from his downtown office in El Paso, Texas, with their young children in tow.

Today, Metzger is president and founder of Crown Wealth Strategies, a comprehensive wealth solutions firm where she and her husband work together to bring harmony to their clients’ finances and their families so that they can enjoy their success and have peace about the future. She is New York Life’s highestproducing Latina advisor.

A day at the office

As a financial professional, Metzger provides her clients with an integrated financial and insurance strategy focused on maximizing value for her clients. She primarily supports families, business owners and the affluent market in planning for retirement, as well as doing college, estate and business planning. She focuses on working with physicians, professionals and business owners in the affluent market.

Each day Metzger spends with these clients is “100% different,” she said as she described her typical day at the office. “And that’s what makes it so fun to do,” she said. “I love the flexibility of my career and the ability to work with various people from all walks of life.”

Some of the other enjoyable aspects of her job are the relationships she has been able to build along the way with her clients and her ability to use her knowledge and ability to help make a positive difference in their lives.

On any given day, Metzger will have three or four meetings with various clients. She also sets aside time for estate and retirement planning, which, she said, “Is fascinating, as each client’s plan differs and their needs and goals are different. I can be working on a retirement plan, an education plan or a complicated

estate plan for multiple generations.”

Working side by side with Metzger is her husband, Brian. She said this working arrangement has its rewards and challenges.

One reward is having a husband as a business partner who understands the way she works, as well as her personality, she said. Another is that both bring different strengths to the business.

everything about a topic, she knew how to research and get an answer.

“I’ve used this approach to this day,” she said, “as I engage clients with more complex problems. My resources allow me to work with even the most complex cases.”

She has also pushed to be a lifelong learner and continues to expand her knowledge. She obtained her master’s

“For example,” she said, “he is the best person I know for prospecting, which allows me to focus on the planning aspect of the business. And there is the accessibility that comes with working with someone who is also available at home.”

And one of the challenges? “Trying to keep work at work and not take it home with us,” she said.

Encountering hurdles

As a female professional in a largely male-dominated industry, Metzger encountered a few hurdles as she navigated her way to the top. The biggest hurdle, she said, centered on the presumptions that many people had about her knowledge of financial matters.

“At the beginning, in all honesty, you don’t have as much knowledge as you know you will with experience,” she said. So she leaned on resources and people with the expertise she needed. This allowed her to demonstrate to her clients that even if she didn’t know

degree as well as her Certified Financial Planner and Accredited Estate Planner designations.

Collecting accolades

Metzger’s years of hard work and dedication to her clients have paid off handsomely. She has received numerous awards and accolades. She is a member agent of The Nautilus Group, a service of New York Life, and a select group of less than 250 member agents nationwide focusing on business and estate planning.

She is also on the advisory board of directors at New York Life. In addition, she has been a member of Million Dollar Round Table’s Top of the Table since 2014 and is on the list of the 2023 Forbes’ America’s Top Financial Security Professionals.

Metzger is a past recipient of NAIFA’s Advisor Today’s Four Under Forty Award, which annually recognizes four financial professionals who have achieved excellence in their profession

the Fıeld A Visit With Agents of Change

by or before the age of 40.

It’s not her plan

Metzger believes that her success in the business can be attributed to many factors, including her grit and determination to succeed.

“I think my grit and pure determination to help my clients are reasons for my success,” she said. “When you have your clients’ best interests at heart, everything falls into place.”

In addition, she said, she has always had a great support system in her friends and family, who have supported all of her aspirations.

Metzger said many of her clients appreciate her honesty and integrity. “I pride myself in always giving my best financial guidance and recommendations, even if it is not necessarily what my clients came in for or what they wanted to hear. This is something that I think a lot of my clients come to me for, as they know I will maintain honesty through my practice,” she said.

The following piece of professional advice that Metzger received early in her career — and one that she has adhered to throughout her time in the business — has also played a key role in her success: “It’s not my plan, it’s my client’s plan. It’s not my money, it’s their money. When I put myself in my clients’ shoes, I can work best for them,” she said.

Metzger said her advice to young advisors is “Understand that this is your business.”

“No one tells you how to run your day. To succeed, you must set up processes and systems that are repeatable for success. The most basic piece of advice is activity. If you don’t meet with people, you will never succeed. Don’t presume that because a client didn’t engage during a meeting that it was a bad meeting. These are all steppingstones to having the experience and expertise you need for a long career!”

Giving back

Despite her busy days at the office, Metzger still has time to give back to numerous charitable organizations in the El Paso community. She and her family support the United Way, Boy Scouts and the Paso del Norte Children’s Development Center. They also sponsor

the Children’s Oncology Unit Playroom at the El Paso Children’s Hospital. The Dipp Metzger S.A.M. Foundation Oncology Unit Playroom is one of the busiest playrooms in the hospital because pediatric oncology patients spend the longest amount of time in the hospital. The playroom is the home of the hospital’s therapeutic art program and puzzles, games and story hours.

“I have always had a commitment and connection to children,” Metzger said, in explaining her support of the unit. “One of my previous jobs was as a teacher for 3-year-olds. When I saw the playroom, I knew it was something I wanted the kids to have access to during the difficult times they were going through.”

Sharing her reading list

With all that Metzger has on her plate, she still manages to achieve a healthy work/ life balance. And how does she accomplish this feat? “I schedule my family and personal events on my calendar,” she said. “I always put my family first, and this is important as well for my staff. With this focus, we are more efficient in the time we are concentrating on our work.”

Something else that is helping her maintain a healthy work/life balance is the time she makes for fun and relaxation. She loves to garden, spend time with her family during her down time and read. Among the books she has read recently:

» Conquistador — about the Spanish conquest of the New World, because she loves history and her family is from Mexico.

» Seabiscuit — Because she always likes stories about the underdog.

» Willpower — “I believe grit is a huge reason for my success, and I am always looking to expand my knowledge and my perspective of the capabilities of determination,” she said.

Ayo Mseka has more than 30 years of experience reporting on the financialservices industry. She formerly served as editor-in-chief of NAIFA’s Advisor Today magazine. Contact her at amseka@ INNfeedback.com

An annuity is intended to be a longterm, tax-deferred retirement vehicle. Earnings are taxable as ordinary income when distributed, and if withdrawn before age 59½, may be subject to a 10% federal tax penalty. If the annuity will fund an IRA or other tax qualified plan, the tax deferral feature offers no additional value. Qualified distributions from a Roth IRA are generally excluded from gross income, but taxes and penalties may apply to nonqualified distributions. Please consult a tax advisor for specific information. There are charges and expenses associated with annuities, such as surrender charges (deferred sales charges) for early withdrawals. These materials are for informational and educational purposes only and are not designed, or intended, to be applicable to any person’s individual circumstances. It should not be considered investment advice, nor does it constitute a recommendation that anyone engage in (or refrain from) a particular course of action. Securian Financial Group, and its subsidiaries, have a financial interest in the sale of their products.

Insurance products are issued by Minnesota Life Insurance Company in all states except New York. In New York, products are issued by Securian Life Insurance Company, a New York authorized insurer. Minnesota Life is not an authorized New York insurer and does not do insurance business in New York. Both companies are headquartered in St. Paul, MN. Product availability and features may vary by state. Each insurer is solely responsible for the financial obligations under the policies or contracts it issues.

Securian Financial is the marketing name for Securian Financial Group, Inc., and its subsidiaries. Minnesota Life Insurance Company and Securian Life Insurance Company are subsidiaries of Securian Financial Group, Inc.

For financial professional use only. Not for use with the public. This material may not be reproduced in any form where it would be accessible to the general public.

Man who lost $16M in life policies revives lawsuit

A federal appeals court gave a partial win to a Connecticut man claiming that AXA Equitable allowed his life insurance policies to lapse without any payment reminder

Malcolm Wiener retired in 1986 and bought three life policies from AXA totaling $16 million, court documents say. The universal life insurance policies did not require regular premium payments. Wiener could skip premium payments or change them, as long as he maintained enough funds in each policy account to cover his monthly deductions for the cost of insurance and other fees.

AXA agreed to send two notices to Wiener yearly to remind him of the required premiums. When he bought the policies, Wiener was 51 years old and chose to delegate policy management to his former company, Millburn, which reviewed notices from AXA and made necessary payments.

AXA claimed that it sent lapse notices, but Wiener denied receiving any. Because no payment was made by Dec. 1, 2013, AXA terminated the policies, costing Wiener $16 million in potential death benefits.

WILL LIFE INSURANCE GO ‘GREEN’?

With so much consumer interest in healthy living and sustainability, will the life insurance industry begin to offer “green” life insurance? A panel of researchers gave their views during a recent Society of Insurance Research educational session.

Studies have found a link between reduced carbon footprint activity and improved mortality risk , said Matt Berkley, director of strategic research with RGA Reinsurance.

Corporate Insights also found that between 20% and 30% of survey respondents said they would be willing to share personal data such as information about their driving, diet and spending habits in return for a premium discount.

WHY MIDDLE-INCOME AMERICANS AREN’T BUYING IT

Middle-income Americans, those with annual household incomes of $50,000 to $149,999, represent the largest market opportunity for the financial services industry, according to the 2024 Insurance Barometer Study by LIMRA and Life Happens. Why aren’t more consumers in this bracket buying coverage? They believe it’s too expensive, the survey revealed.

Yet, since the first annual study was conducted in 2011, consumers have consistently overestimated the cost of life insurance, the survey said. The most recent study shows that about three-quarters (72%) of Americans overestimate the true cost of a basic term life insurance policy, and younger Americans are likely to think it is three times its actual cost.

QUOTABLE

The

consumer must prioritize life insurance as they do other expenses. If they prioritize it, they’ll find the money.

WHAT THE INDUSTRY MUST KNOW ABOUT GEN Z

Generation Z is the newest generation to reach adulthood, and the industry must pay attention to the unique needs of this age group if it expects to reach its members. Gen Z gets most of its information from social media and seeks to have a personalized experience when buying products and services. So insurers that want to reach this age group must up their social media game while delivering an experience that meets the needs of these young adults. That was the word from a recent Society of Insurance Research discussion.

Gen Zers make up about 18% of the U.S. population and have grown up using social media in their daily lives, said Kendall Gadie, associate director at Comperemedia. Gen Z is also the most diverse generation, he said, with more than one-quarter identifying as a race other than white and a large portion identifying as part of the LGBTQ+ community.

Growing up in a digital world has given Gen Zers an elevated expectation of being offered a personalized experience in all their transactions, Gadie said. “This puts more pressure on insurers, and really all brands, to be able to do that.”

— Stafford Thompson Jr., former senior vice president of life and executive benefits business management, Lincoln Financial Group

The role of life insurance in estate and gift tax exemptions

How life insurance can be an alternative to grandfathering the large federal estate and gift tax exemptions.

By James G. Blase

With the November election rapidly approaching, discussion about the need to grandfather the current $13.61 million federal estate and gift tax exemptions has heightened. “Use it or lose it” is the common pronouncement. But for high net worth individuals, are large lifetime gifts as beneficial as they may first appear? Is there any other alternative out there that can produce better overall results for the individual and their family?

Grandfathering the exemptions

The sunset of the current large federal estate and gift tax exemption is scheduled

to take place in 2026. It is likely that when we get to that sunset, the federal estate and gift tax exemptions may be reduced by 50% or more — from as much as $14 million or more to less than $7 million. For a married couple, these numbers double from as much as $28 million or more to less than $14 million. At a federal estate tax rate of 40%, the resulting estate tax differential for a married couple may be $5.6 million or more.

With tax savings this large, isn’t it a no-brainer for high net worth individuals to gift away the large federal estate and gift tax exemption before any potential sunset takes place? After all, estate planning attorneys have developed techniques, such as the spousal limited access trust (or SLAT for short), as a way for married couples to gift away a large amount of assets and still retain use of the same, directly or indirectly, during their lifetimes. The answer may not be clear-cut for several reasons, and at least one other alternative should first be explored.

One of the reasons? Because of the way the tax code is structured, lifetime gifts around $6 million or so per person have zero grandfathering effect. Individuals must gift more than this amount in order to produce any grandfathering of the current $13.61 million exemption. The problem is that this is a lot of assets to gift away during the taxpayer’s lifetime, especially if a married couple seeks to double this amount.

Further, and despite the best-laid plans of estate planning attorneys, it is questionable whether any estate plan designed to allow a married couple guaranteed access to all the transferred assets during their joint lifetimes will survive a successful attack by the IRS. Even if a “reciprocal” plan were to pass IRS muster during the couple’s joint lifetime, there is a good chance that after the first spouse dies, the surviving spouse will have at best access to only one-half of the transferred trust funds and potentially have access to none of them.

Another reason is that the after-tax benefits of large gifting are more limited than they may appear at first blush. Assume, for example, that a single individual makes a $10 million gift of securities in 2024 and that the 2026 exemption ends up at $6.5 million. The individual has thus grandfathered $3.5 million of the larger federal estate and gift tax exemptions and saved $1.4 million in estate taxes in the process. Also assume that the individual’s income tax basis in the $10 million of gifted securities was $4 million and that the donee’s combined net capital gains tax rate, including the net investment income tax and net state income taxes (i.e., after the federal tax deduction then is in effect) is 23%. The built-in capital gains tax on the gifted securities is $1.4 million, or the same as the federal estate tax savings.

Of course, the facts involved will be different than these, but you get the picture. Large gifts of securities or business interests typically carry with them a significant amount of built-in capital gains taxes, taxes that would be avoided if the taxpayer held the assets until death. And if sunset does not occur, or if the tax laws are later changed during the taxpayer’s lifetime to reinstate the large federal estate and gift tax exemptions, taxpayers making a large transfer may have only hurt their family, at least in the short term.

The potential adverse income tax consequences compound if the individual has a significant “portability election” amount available from a predeceased spouse. The portability election amount essentially is already grandfathered, and lifetime gifts by the surviving spouse use up the portability amount before they use up the surviving spouse’s own exemption amount. As a result, there is zero tax savings immediately after the transfer of the portability amount there, but as with all lifetime gifts, there can be a significant carryover income tax basis involved.

What if one of the purposes for making the grandfathered gifts is to remove future appreciation from the taxpayer’s gross estate at death? Would this make the decision to make a large gift simpler? At the assumed 23% effective capital gains tax rate, the net tax advantage in favor of a large lifetime gift should be approximately 17% (or 40% minus 23%) of the future appreciation. Now assume the original $10 million in transferred assets doubles in

value each 10 years, or to $80 million after 30 years. Of the $70 million in growth, the net tax savings to the taxpayer’s family by investing the original $10 million in an irrevocable trust would be $11.9 million ($70 million plus 17%).

The life insurance alternative

The question is whether there is an alternative that will produce the same or greater overall financial benefits to the taxpayer and the taxpayer’s family but without causing the taxpayer to lose the full economic benefit and/or control over the transferred assets.

monthly for 30 years at an annual rate of 7%, could have grown to $14 million. If the $14 million were part of the surviving spouse’s taxable estate, the net amount, after 40% estate taxes (and assuming no state estate taxes on the same) would be $8.4 million, or approximately 70% of the $12 million of income- and estate-tax-free life insurance proceeds inside of the irrevocable life insurance trust, payable when the surviving spouse dies.

Now assume that the same $148,700 was instead invested annually for 30 years inside of an irrevocable trust outside the couple’s taxable estate. The net amount,

The sunset of the current large federal estate and gift tax exemption is scheduled to take place in 2026. It is likely that when we get to that sunset, the federal estate and gift tax exemptions may be reduced by 50% or more.

Assume, for example, a couple with a 62-year-old husband and a 61-year-old wife who both are in preferred health. Instead of gifting $10 million in securities, the couple decides to keep full control over the securities and use a portion of the ordinary income generated by the same each year, or approximately $148,700 (based on their ages and health status), to pay the annual premium on a $12 million second-to-die life insurance policy owned inside of an irrevocable life insurance trust. The $148,700 annual premium would be covered by the couple’s $18,000 per Crummey power donee annual gift tax exclusions.

Because the proceeds of the second-todie life insurance policy will be free of income tax and estate tax, at an annual cost of $148,700 the couple has effectively nullified the need to give up control over the $10 million in assets, even if they live into their 90s. The question is: Is this effective nullification worth the cost to achieve it?

If the couple pays the $148,700 premium for 30 years, or until the husband is age 92 and the wife is age 91, the total amount expended would be $4,461,270. The same $148,700 annual amount, compounded

after the assumed 23% capital gains rate (that could be much higher because a trust gets to the 20% basic capital gains rate much faster than an individual does) on all growth, would be $11.8 million. This is about the same as the $12 million of income- and estate-tax-free life insurance proceeds inside of the irrevocable life insurance trust, payable when the surviving spouse dies.

Although the facts will obviously vary in each situation, what the above analysis demonstrates is that grandfathering the current high federal estate and gift tax exemption may not always be necessary or even financially beneficial. Before proceeding down a path of lost control and potentially higher future capital gains taxes, studying the use of life insurance as an alternative to grandfathering the current high estate and gift tax exemptions should be considered.

James G. Blase, CPA, JD, LLM, is principal with Blase and Associates, attorneys at law, St. Louis. Contact him at james.blase@ innfeedback.com

ANNUITY WIRES

Annuity sales list tightens up at halfway point

Athene Life & Annuity again led the way in annuity sales through the first half of 2024. But the gap closed quite a bit, LIMRA reports.

Athene sold more than $18.7 billion worth of annuities during the period, bettering its 2023 pace, LIMRA announced. Athene sold $35.5 billion in a triumphant 2023.

But other annuity sellers are doing even better. Four insurers are on pace to top $21 billion in sales this year: Corebridge Financial, New York Life, MassMutual and Equitable Financial. Two companies topped $20 billion in 2023.

Sales for all annuities were $109.6 billion when compared with the previous quarter, according to Wink’s Sales & Market Report. Deferred annuities led the way.

Total second-quarter sales for all deferred annuities were $104.6 billion, up 4.1% when compared to the previous quarter and up 31.2% compared to the same period last year, Wink said.

Among other highlights, structured annuity sales in the second quarter were $15.6 billion; up 12.2% compared to the previous quarter, and up 44.6% compared to the same period the previous year.

ANNUITY INTEGRATION TOOLS SOUGHT FOR ADVISORS

Financial advisors are warming up to annuities in a positive trend for the industry.

Annuities could soon benefit from simpler integration if the Insured Retirement Institute is successful in its bid to develop a new digital, standardized infrastructure.

IRI’s Digital First for Annuities is an industry-wide annuity integration initiative that aims to introduce a single, consistent source of product data and new infrastructure for standards.

Annuities are not easily pulled into the tools financial advisors use right now because of inconsistent or missing data, which can cause the annuity to be inaccurately represented within a portfolio, IRI noted. According to IRI’s data,

while 83% of financial professionals use financial planning software, just 18% leverage annuities in those tools.

The Digital First for Annuities annuity integration initiative would address a lack of standardization and ensure the value of annuities is accurately represented in a way that works both for financial professionals and for their clients.

AM BEST: LIFE/ANNUITY REINSURERS FACE GROWING COMPETITION

Higher interest rates and more favorable mortality trends have led to improved conditions for life/annuity reinsurance companies, an AM Best report found. It also has created more competition, with some backed by alternative investment

Rates on [indexed] products haven’t been this attractive since I’ve been in the business.

— Sheryl Moore, CEO of Wink Inc.

managers or large private equity firms.

This new report states that new capital continues to flow into the segment, primarily via reinsurers owned by investment managers focused on annuity business. These newer entrants have sought to coinsure assets that can be rolled into high-yielding positions, mainly in public, private or alternative fixed income products.

These reinsurers also can offer attractive ceding commissions based on higher anticipated investment returns once the transferred assets are rolled into a wider set of investment opportunities.

STUDY: FIXED-RATE DEFERRED ANNUITANTS ARE NOT SURRENDERING EARLY

A new study by the Society of Actuaries and LIMRA found that most fixed-rate deferred annuity owners are at least waiting until their surrender charge period is up before surrendering. The two organizations jointly studied fixedrate deferred annuity surrenders from 2015 through 2022.

Dale Hall, managing director of research for the SOA, shared the data with regulators during the National Association of Insurance Commissioners’ summer meeting.

“In the previous studies, I think you’d see higher levels of contract surrenders even two years to expiry, one year to expiry of the surrender charge,” Hall explained. Surrender rates by both contract count and contract value peaked in the year the surrender charge expired, at a rate of 38.6% by contract count and 46.3% by contract value, the study found.

Source: Wink Inc.

Put your client’s retirement income dollars on the right path

Set yourself apart from the competition by providing your clients a guaranteed income for life with Kansas City Life Insurance Company’s Lifetime Income Rider that:

• Offers 7.2% guaranteed increase to Lifetime Income Amount for the first 10 rider years if no withdrawals in years 1 – 10.

• Provides a secure, guaranteed retirement income stream for life.

• Helps clients grow their retirement savings with a competitive fixed interest rate.

• Protects the value of a fixed annuity during market turmoil.

• Allows clients the ability to maintain the flexibility and control of their deferred annuity contract even after they start receiving income.

The Lifetime Income Rider provides guaranteed income for life and is an optional benefit available on all of Kansas City Life’s fixed annuity portfolio.

The ‘perfect storm’ driving annuity sales momentum

Interest rates, market volatility and a growing demographic are fueling higher demand for annuities.

By Susan Rupe

Annuity sales are on track to a third consecutive year of record sales. What’s driving that momentum, and how does the annuity market build it? Two LIMRA executives looked at the factors behind the annuity wave during a recent LinkedIn Live event.

“An interesting intersection where things have lined up perfectly over the last three years,” is how Keith Golembiewski, assistant vice president and director of LIMRA annuity research, described the current annuity sales environment.

Higher interest rates, volatility in the equity markets and a growing number of Americans approaching age 65 are among the factors that converged to create “this sort of perfect combination for annuity sales and the momentum we see behind them,” he said.