Evolving to meet the needs of millennials and Gen Z PAGE 24

Peak 65 to fuel digital boom in annuities

PAGE 28

50 Years of ERISA PAGE 38

Creating the Preeminent Partnership with Simplicity Group’s Bruce Donaldson

PAGE 6

Find out more on page 11.

Do your clients long for the lifetime income their parents got from a pension plan? The ApexAdvantage fixed index annuity provides the guaranteed income* they’re seeking—along with unmatched flexibility and control:

IMMEDIATE INCOME—Turn on competitive income payouts in as soon as 30 days.

TRUE INCOME DOUBLER—Receive double payouts for impairment in 2 of 6 ADLs:

• No confinement required.

• No medical underwriting.

• No fortune telling: Select joint or single lives and increasing or level payouts when income starts, not at issue.

LIFE INSURANCE FUNDING—Leverage direct-to-third-party-payouts to fund life insurance or leave more to charity!

Learn more about this exciting FIA from “A” rated** Ameritas Life Insurance Corp.

In approved states, ApexAdvantage Index Annuity (Form ICC22 2707 with ICC22 2707-SCH or 2707 with 2707-SCH) and riders are issued by Ameritas Life Insurance Corp. (Ameritas) located at 5900 O Street, Lincoln, NE 68510. Products are designed in conjunction with Ameritas and exclusively marketed by Legacy Marketing Group® Ameritas and Legacy Marketing Group are separate, independent entities. ApexAdvantage Index Annuities are modified single premium deferred annuities that offer a fixed interest option and index interest options. The index options are not securities. Keep in mind, your clients are not participating in the market or investing in any stock or bond. Policies, index strategies, and riders may vary and may not be available in all states. Optional features and riders may have limitations, restrictions, and additional charges. Product guarantees are based on the claims-paying ability of Ameritas Life Insurance Corp. Refer to brochures for additional details. ApexAdvantage is a registered service mark, and FutureNow Rider is a service mark, of Legacy Marketing Group. Ameritas® is a registered service mark of Ameritas Life Insurance Corp.

* A Guaranteed Lifetime Withdrawal Benefit is available for a current annual charge of 1.25% for the FutureNow Rider and 1.35% for the FutureNow Rider With Booster, multiplied by the premium accumulation value during the accumulation phase and by the benefit base during the withdrawal phase. ** A (Excellent) for insurer financial strength. This is the third highest of AM Best’s 13 ratings. Rating as of 5/4/2023. Ameritas Mutual Holding Company’s ratings include Ameritas Life Insurance Corp.

IN THIS ISSUE

INTERVIEW

6 Creating the preeminent partnership

Bruce Donaldson, partner and CEO of Simplicity Group, believes “the best days for the insurance industry are ahead of us” and discusses why the profession must embrace the accumulation side of the business.

IN THE FIELD

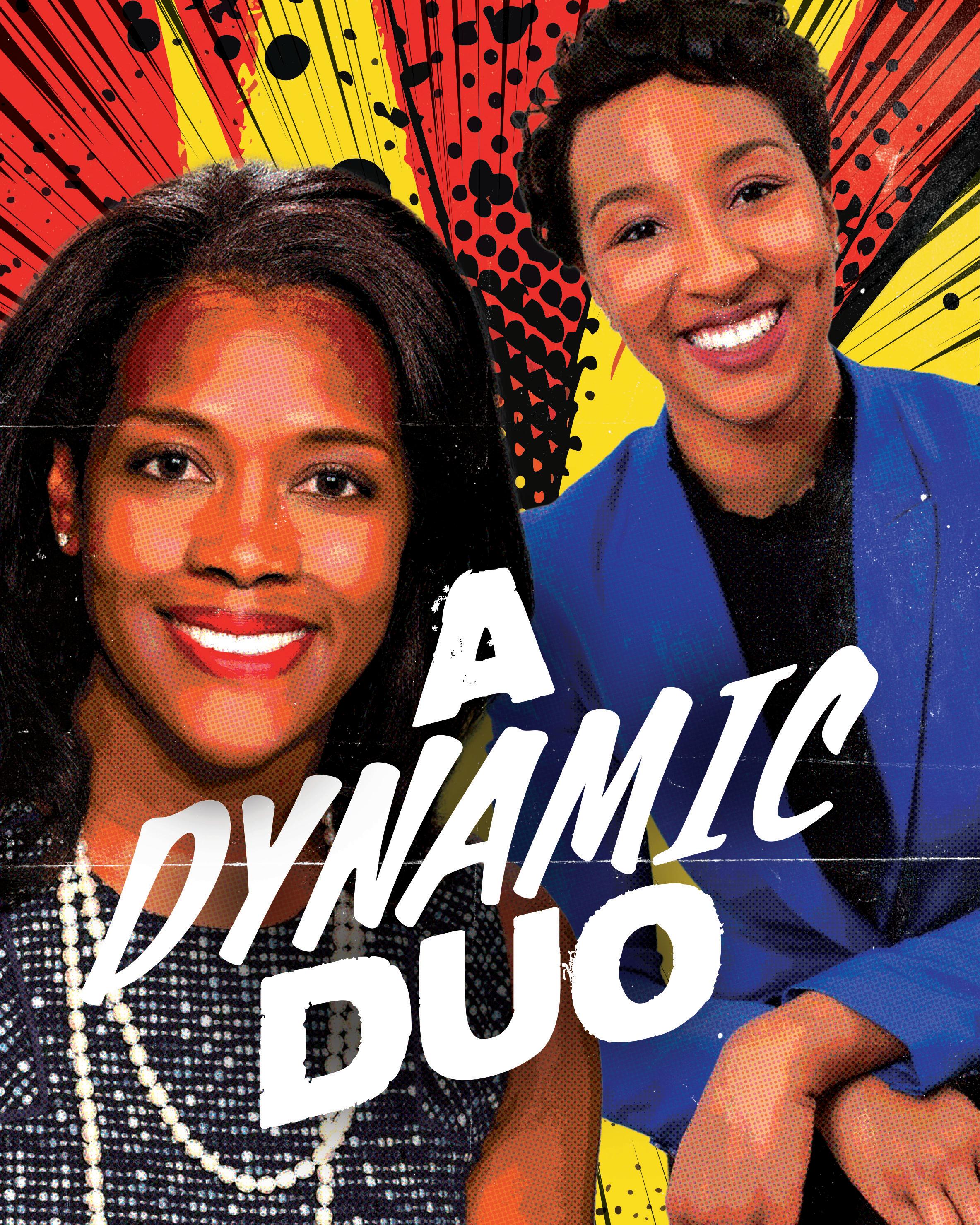

18 A dynamic duo

By Susan Rupe

Judith Lee is living her American dream while her daughter, Simone Lee, helps her build a practice dedicated to serving those who are living out their own dreams.

FEATURE

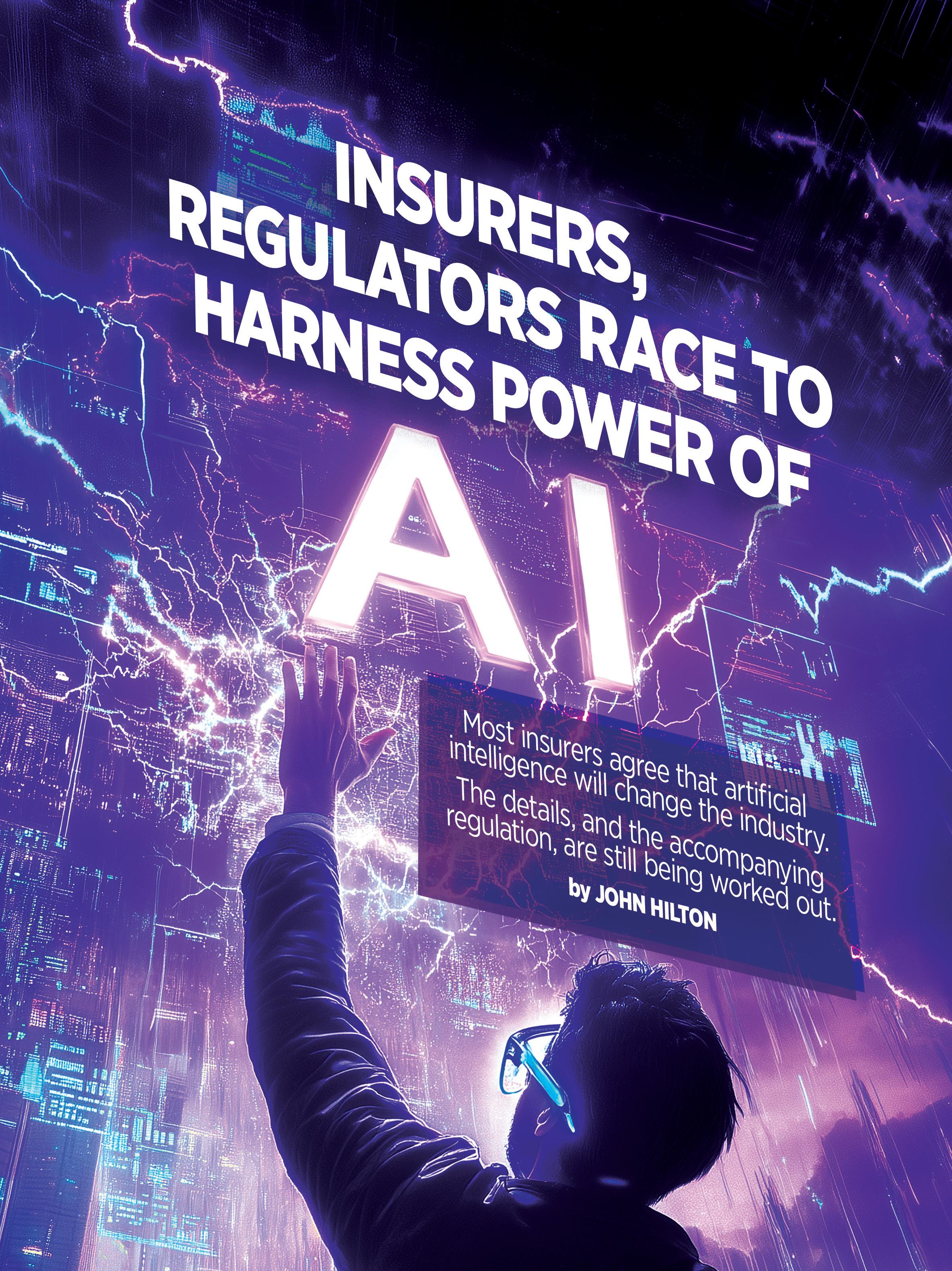

Insurers, regulators race to harness power of AI

By John Hilton

Data drives insurance. And that makes insurance a natural fit for an artificial intelligence revolution.

LIFE

24 Crisis to creativity: Evolving to meet needs of millennials and Gen Z

By Samantha Chow

Life insurance must shake off its image as death insurance.

ANNUITY

28 Peak 65 to fuel digital boom in annuities

By Katie Kahl and Adam Ducorsky

The most significant surge of retiring Americans in U.S. history could push annuity sales even higher.

HEALTH/BENEFITS

32 ICHRAs: A choice for small employers

By Susan Rupe

Individual coverage health reimbursement arrangements represent a sliver of the group health market, but that segment is poised for growth.

ADVISORNEWS

36 Transferring generational wealth involves more than financial assets

By Philip Richter, Carolyn Yun and Alan Bazaar

Family dynamics, philanthropic goals and the family’s legacy all play a part.

IN THE KNOW

38 50 years of ERISA

By Doug Bailey

Nearly 150 million American workers enjoy secure pension funds today, thanks to this landmark legislation.

Pros and Cons of AI in the industry

Despite its relatively recent appearance on the scene, artificial intelligence has become one of the most transformative technologies of the 21st century. The insurance industry, traditionally reliant on human judgment and paper-heavy processes, is no exception to this transformation. While AI’s integration into the insurance sector offers opportunities for agents, it also introduces some dangers and complexities.

Pros of AI in the insurance industry

1. Improved customer insights

One of the key advantages AI offers agents and advisors is its ability to analyze massive datasets and provide actionable insights. With AI-powered algorithms, agents can understand their clients better, anticipate their needs and provide personalized policies that are more likely to appeal to them. Predictive analytics, a subset of AI, can identify patterns in customer behavior, enabling agents to offer timely recommendations. This results in a more personalized customer experience, which can enhance client satisfaction and loyalty.

2. Automation of administrative tasks

AI-driven automation can significantly reduce the administrative burden that agents and advisors face. Tasks such as processing claims, underwriting and even routine customer inquiries can be automated through AI tools. Chatbots, for example, can handle initial or routine customer interactions, freeing agents to focus on more complex tasks that require human expertise.

3. Improved risk assessment and fraud detection

AI can enhance the accuracy of risk assessment and improve fraud detection processes. By analyzing vast amounts of data, AI can identify suspicious activities

or inconsistencies that would otherwise go unnoticed. This helps insurers minimize fraud-related losses and allows agents to better protect their clients from potential risks. AI also can provide more accurate risk profiles for customers.

4. Faster decision-making

AI enables faster decision-making in various aspects of the insurance process. Whether it’s offering instant quotes, automating claims adjudication or streamlining policy approvals, AI reduces the time taken for each step. In a competitive market where speed is often a critical factor, this can give agents a significant edge.

5. Scalability

AI tools can help insurance agents scale their operations. By automating routine tasks and leveraging AI-driven customer insights, agents can handle a larger client base.

Cons of AI in the insurance industry

1. Reduced human interaction

As AI takes over more customer-facing roles, such as handling queries via chatbots or automating claims processing, there is a risk that the traditional personal touch will be lost. Removing human interaction could alienate some clients, particularly those who prefer face-toface communication. Agents must strike a balance between using AI for efficiency and maintaining a strong human connection with clients.

2. Job displacement concerns

The rise of AI brings with it fears of job displacement in the insurance sector. As AI systems become more advanced, they can handle more complex tasks that were once the sole domain of agents. However, while AI may reduce the need for some tasks, it is unlikely to replace the human element in insurance. Agents are crucial to provide the personal understanding,

judgment and nuanced decision-making required to best serve clients.

3. High implementation costs

Adopting AI technologies can be expensive, especially for smaller insurance agencies. The initial investment in AI tools, along with the training required for agents to use these tools effectively, can be a significant financial burden. Smaller firms or independent agents may struggle to keep up with technological advancements, potentially putting them at a competitive disadvantage.

4. Data privacy and security issues

AI systems rely on vast amounts of data to function effectively. The increased use of AI introduces new challenges related to data privacy and security. Agents and insurers must ensure that their AI systems comply with emerging regulations.

5. Bias in AI algorithms

Another potential pitfall is the risk of bias in AI algorithms. AI systems are only as good as the data they are trained on, and if that data contains biases — whether racial, gender-based or socioeconomic — then the AI’s recommendations and decisions may reflect those biases.

Will AI improve success for insurance agents?

In the long run, AI has the potential to significantly improve the success of agents and advisors. By automating mundane tasks, enhancing customer insights and providing more accurate risk assessments, AI enables agents to work more efficiently and effectively. Those who embrace AI and leverage its strengths will likely find themselves better equipped to serve clients in an increasingly competitive market.

Despite the advantages provided by AI, the human element remains irreplaceable. Clients still value trust, empathy and personal interaction. The future of insurance will not be about choosing between AI and human agents — it will be about using both to deliver superior service.

John Forcucci Editor-in-chief

Americans fear Medicare won’t be there

Americans are increasingly concerned about the future of Medicare, with nearly two-thirds (63%) fearing the program will not be there when they need it, according to the annual Nationwide Retirement Institute Health Care Costs in Retirement survey. In addition, 20% said their biggest retirement fear is that Medicare will run out of money.

Other retirement fears the survey revealed include inflation (44%), Social Security running out of funds (36%), higher taxes (22%) and a stock market crash (12%)

As Americans’ fears about the long-term solvency of Medicare grow, many want meaningful reforms. When thinking about the 2024 U.S. presidential election, more than 2 in 5 (42%) said the top health care priority for the next administration to address should be ensuring Medicare’s stability, just behind lowering out-ofpocket health care costs (43%) and lowering prescription drug prices (43%).

HIGHER CAR AND HOME PREMIUMS ADD TO FINANCIAL STRESS

Insurance costs for auto and homeown ers coverage continue to surge across the U.S., the Bureau of Labor Statistics revealed. The price of car insurance is up 18.5% compared to a year ago up 75% since the COVID-19 pandemic in 2020. That compares to overall U.S. pric es being up 23% since the pandemic, ac cording to BLS.

Homeowners insurance premiums have also increased. In 2019, the aver age homeowners insurance premium in the U.S. was $1,272 — now it is $2,511 Homeowners insurance prices are even higher in some states. The average homeowners insurance premium with $300,000 in dwelling coverages is $5,531 annually in Florida — 144% higher than the national average for the same coverage ($2,270), according to Bankrate.

LATINAS CONTRIBUTED $1.3T TO THE US ECONOMY

The female Hispanic population contributed $1.3 trillion to 2021’s U.S. gross domestic product, up from $661 billion in 2010, according to a recent report funded by Bank of America. The economic output of Latinas was more than Florida’s economy that year, with only the GDPs of California, Texas and New York being larger. Still, some economists believe that Latinas’ total contribution to the country’s GDP could actually be more than what’s being reflected in the data.

When it comes to labor force participation, Latinas are outpacing other groups, From 2000 to 2021, the participation rate for Latinas rose 7.5 percentage points. On the other hand, the participation rate of the non-Hispanic women in the same period was flat.

The group has also been more resilient than others. Although labor force growth slowed overall in 2020, the growth rates

I’m going to do everything I can to get pharmacy benefit manager cost containment on medicine.”

— Sen. Ron Wyden, D-Ore.

for Hispanic men and women were still positive. Conversely, the non-Latino labor force growth rate was negative that year, meaning that more people left the labor force than entered it.

MORE CHOOSE TO BE A SINK, DINK OR DINKY

“Childless cat ladies” became a catchphrase in the 2024 presidential campaign. But they may not be as rare as you think. About 25% of Generation Z and millennials who don’t have children say they don’t intend to have any in the future, according to a MassMutual report.

A preference for financial freedom and the inability to afford children are equally cited by 43% of younger generations as the reason why they want to remain child-free.

In many cases, being a SINK (single income, no kids), DINK (dual income, no kids) or DINKY (dual income, no kids yet) does come with certain financial planning considerations that differ from the standard strategy. For example, most child-free adults don’t prioritize passing money down to the next generation. to the next generation. But child-free adults also must bear the brunt of caregiving for aging parents, so they must consider how to fund their parents’ and their own future care.

37% of parents worry their children will need financial assistance well into adulthood.

YOUR

Insurance agents face the challenge of navigating complex options while delivering a personal touch. LifeShield is dedicated to helping your clients and your business thrive.

Why Choose LifeShield?

• Agent-Centric Approach: Agents are the heart of LifeShield’s strategy. Products are affordable, feature-rich, and reward agents with fair commissions.

• Personalized Service: A dedicated support team of real experts committed to delivering personalized, effective solutions.

• Innovative Solutions: Top-tier products from Life Insurance to Medicare Supplement with exceptional flexibility tailored to meet clients’ financial and coverage needs.

• Decades of Excellence: A rich legacy of nearly 50 years, delivering unparalleled solutions with a commitment to enduring success for both policyholders and agents.

With LifeShield, you don’t just offer insurance — you deliver excellence. Transform your client offerings, enhance your earnings, and stand out in the marketplace.

Step up and stand out — offer the extraordinary.

Visit www.lifeshieldcombo.com, your choice for Medicare.

Creating the Preeminent Partnership: Protection & Accumulation

An interview with publisher

Paul Feldman

The genie is out of the bottle when it comes to the marriage of protection and accumulation in providing true holistic financial planning, says Bruce Donaldson, partner and CEO of the Simplicity Group, a leading financial products distribution firm.

Since its formation in 2016, Simplicity has continued to build its success through a series of acquisitions, improving its One Simplicity platform for agents and advisors and, more recently, enabling further reach into the wealth-building side of the business.

“We all know that there is a better way to hedge longevity risk and only one way to address mortality risk — and that’s with insurance products. That simple principle has always been at the heart of Simplicity,” said Donaldson. “The trick is properly marrying the best accumulation products with the best protection products in a way that helps clients meet all their key financial objectives.”

Donaldson said the way Simplicity has accomplished this goal is by creating a tech-enabled sales process, driven by consumer needs, that delivers the best of accumulation and protection for each consumer. “We’ve seen double-digit organic growth for the past four years exactly because we’re penetrating markets that used to be the preserve of the ‘fee-only’ advisor.”

In this interview with InsuranceNewsNet Publisher Paul Feldman, Donaldson describes why he thinks “the best days for the insurance industry are ahead of us” and how it will be incumbent on those in the insurance profession to embrace the accumulation side of the business.

Paul Feldman: You’ve had an amazing run in this industry. How did you get involved in it? Tell us about how you started with Simplicity.

Bruce Donaldson: I’ve been lucky enough to be in and around financial planning and financial advisory for almost 35 years now. So many of the things that we’re doing at Simplicity, I’ve learned along the way through the course of my career. Before starting Simplicity as an insurance sales organization — which has evolved into a financial products distribution business — I built an institutional

asset management business and then started a new insurance company. In 2016, I saw an opportunity to build a business to better serve independent insurance agents and financial advisors across the country as they dealt with an ever-shifting landscape of technological needs, increasing consumer demands and, frankly, misguided regulatory oversight proposals.

Today, I serve as a proxy for our 250plus employee-owners — “partners” — of Simplicity and the 1,000-plus employees we have across the country. I’m thrilled to be a partner at Simplicity.

Feldman: Tell us how Simplicity started.

Donaldson: Tracing our roots back to our formation in April 2016, you will recall that we had an uncertain economic environment; we had a highly fragmented insurance distribution industry; and we

Our goal is to work with all our agents and advisors to increase the delivery of insurance products with a growth rate that equals or exceeds what we see in the securities industry.

right way to address these objectives. Not selling insurance to address protection needs is almost the definition of not acting in a fiduciary or best interest manner. I find this ironic given how Washington has been fixated bringing “regulatory parity” to our industry without addressing this issue.

Today, Simplicity is 100% committed to working with our independent agents and advisors and supporting financial institutions across the country that see the benefits of outsourcing to an unrivaled national sales platform. We’re not a direct-to-consumer model as some of our competitors are. Our goal is to work with all our agents and advisors to increase the delivery of insurance products with a growth rate that equals or exceeds what we see in the securities industry.

Feldman: Tell us how Simplicity is addressing this “underinsured” issue.

had regulatory overreach concerns. Our belief was that a national wholesale platform could properly support all the great insurance agents and financial advisors across the country.

Simplicity was founded on the idea that the American consumer was not being sufficiently served with the appropriate protection products as a complement to their accumulation investments. We felt that businesses in adjacent industries (the fee-only advisors) avoided insurance or openly advised against it (the “we don’t sell commissionable products” mantra). Many of these very same advisors hold themselves out as “fiduciaries,” but when addressing a client’s longevity risk, what they were really doing was just recommending a higher-yielding security and/ or slowing down retirement withdrawals. We know that protection products are the

Donaldson: We all know that there is a better way to hedge longevity risk and only one way to address mortality risk. That’s with insurance products. This principle has always been at the heart of Simplicity: great insurance distribution, a 100% commitment to supporting independent agents and advisors across the country, and building the One Simplicity platform to grow our industry. By positioning our protection products as a part of a broader a financial plan, we can focus on the hallmark of pooled risk mitigation that no other financial product can replicate. We then combine that solution with an easier issuance process that our scale affords us. Over time, we believe that by focusing the sale of insurance on the hallmarks of protection and by reducing the friction of policy issuance, we can change the misperception

of insurance and grow the protection market.

Feldman: Tell me about the most recent investment in your organization. What does that mean to your advisors and partners?

Donaldson: We recently announced that we have again recapitalized our business. This is the third capital event that we have provided over the past eight years. These capital events reinforce our employee-ownership model, and they provide new capital to invest in operations and technology to better serve our agents.

Simplicity has been, and will always be, committed to employee-ownership. We are driven by our employees and therefore think the value that we are creating with Simplicity must be available to our employees. A commitment to employee-ownership was critical to how we started and will always be central to how we operate.

We have 1,000-plus employees across the country. Each of them is in a different stage of their own personal financial planning. Some of our partners are a little closer to the end of their careers, and they are thinking about succession and liquidity. Some of our employees are in the growth phase of their careers, and they really appreciate our unrivaled growth equity opportunity. Some of our employees are just appreciative of Simplicity’s permanence and consistent growth. What binds us all together, however, is the employee-ownership mentality — a distinguishing hallmark of Simplicity. Interestingly, this employee journey is one of the many things Simplicity helps our agents and advisors navigate in their own businesses, and we tell them “There is no substitute for employee-ownership.”

We believe that to properly instill the employee-ownership mentality, businesses must have regular liquidity events. Of the Big Three distribution businesses, we are the first to deliver multiples of invested equity capital back to all of our partners, and because we do this every three or four years, we’ve created the virtuous circle of increasing employee-ownership.

As our older partners execute their succession plans, we then recycle their equity, which becomes available to the younger, newer employees in our organization who

haven’t yet had their wealth creation opportunity. They know that not only does Simplicity offers a great platform to grow their day-to-day sales and generate a great regular income, but they also get to experience the benefits of employee-ownership.

That has been our model. That will always be our model. We love that equity in Simplicity becomes a virtuous circle for us to recruit and retain financial professionals. We can recruit through employment, through independent agent affiliation or through [mergers and acquisitions], but we want the best and brightest financial professionals across the industry to hitch their wagon to Simplicity, and we’ll help them experience a great outcome like this most recent recapitalization.

Feldman: In 2024, you didn’t have as many M&A events as you’ve had previously, from what I’ve seen. How does that differ for next year and the future?

Donaldson: Executing a multibilliondollar recapitalization required several months of time and attention, and we needed to lock down our balance sheet for a period. Now that we have successfully recapped, we are back to full speed from an M&A perspective. As happened the last time (the 2020 recap), we expect that our 2024 recap will lead to more partners looking to join Simplicity because they know we offer an unrivaled equity and growth opportunity, and we expect a big uptick in both our M&A and our affiliation model.

We are always in the market, and we are always looking for great partners.

Feldman: How have you reinvested some of the recapitalization in technology? Where do you see technology going?

Donaldson: I would say, in an industry that is lagging in some ways on technological developments, we have a somewhat easier path than other national players, in the sense that we are exclusively focused on financial planning.

We are not trying to bring together health and wealth. We have the ability to solve health needs, but the One Simplicity platform is all around tech enabling that one operating platform.

The latest example of our focus is Simplicity LifeLink, the newest life insurance quoting tool that, unlike other technologies, was purpose-built to support independent agents. This technology is not a recycled direct-to-consumer technology. Simplicity LifeLink was built with independent agents in mind.

Everything we are doing from a technology perspective is focused on removing friction from policy issuance. Our agents never have to wonder, If I embrace this technology, am I facing disintermediation? We are committed to the long-term business of our independent agent clients.

Another example of our technology focus is ILIA, which is the technology behind Kai-Zen, a supplemental retirement savings program that is gaining popularity across the country. We will continue to invest our refreshed capital into growing this industry.

Feldman: You have discussed recapitalizations, technology investments, and mergers and acquisitions; how should the insurance industry think about these aspects of your business? Do these things help our industry?

Donaldson: It is a fair question to ask: If we’re in the insurance industry, why are we investing time and resources in the wealth management industry? And frankly, it is fair to ask whether all the recent M&A deals are good for the insurance distribution industry. If executed in a sustainable way (which we believe we have done), then the platform size we gain from M&A should bring all market participants the benefits of our scale. We have seen these benefits be realized by both our agent base and also our insurance carrier partners. We are knocking down the walls and removing the friction that has historically kept Americans underinsured. In this regard, we think recapitalizations and M&A have brought a lot of positives to the insurance industry.

Having said that, we think the insurance industry has to find a way to push into new markets to drive overall growth. This is not a novel thought. The industry has been trying to do this for decades. We do think, however, Simplicity’s One Simplicity approach to growing insurance by penetrating the wealth markets is what gives us optimism that we can grow the

insurance market. Our One Simplicity platform integrates, or “marries,” the best of protection with accumulation and brings our products into new markets.

At Simplicity, we do not think our competition is in the insurance industry — we think the competition is in the new markets we are trying to penetrate. We also don’t spend time thinking about where we sit relative to other insurance distribution organizations. We spend all our time thinking about how we can grow the overall market and capture more wallet share, by helping our agents and advisors capture more wallet share from their consumers. The only way to do that is to have wealth services and programs that those consumers can tap into.

The trick is, can you bring all those accumulation products and marry them with the protection products? And the way we’ve done that is by creating a straight-through, tech-enabled sales process driven by consumer needs that delivers the best of accumulation and protection for that consumer.

We’ve seen double-digit organic growth for the past four years exactly because we’re penetrating new markets.

Feldman: Tell us how you are combining accumulation and protection for advisors. Are you helping them get registered?

Donaldson: We help our agents with all the regulatory requirements, but we have a number of different ways we can help agents penetrate new markets. If an agent says, “I’m never going to get my Series 65, but I want to be able to work on a platform that allows me to refer to appropriate securities advice,” we can deliver that solution in a compliant way.

But the heart of your question, because it applies equally to the insurance industry and to the securities industry, is how do we put agents and advisors in a position where they feel empowered to deliver the best of those two worlds? Because almost without exception, all those agents and advisors — whether they’re in the insurance industry or the securities industry — grew up in one world and not the other.

We have built easy-to-understand client education programs, and we provide agent training that makes our agents expert in the marriage of accumulation and

New fluidless underwriting option for death benefits up to $5 million. Allianz Life Insurance Company of North America (Allianz) now offers three pathways to help expedite the underwriting process. And it’s making a difference: We’ve had a 22% increase in policies approved via our Accelerated Underwriting.¹

¹2022-2024 For

Products

This

protection. After the first client meeting, our agents gather the pre-identified key client information and then send the information to our planning department. What comes back to that agent is a fully built-out, uniform financial plan that leverages these two product types, accumulation and protection. Now the agent is in a great position because they can capture 100% wallet share. They look smart. They educated their clients and delivered a plan that meets the clients’ pre-identified goals. At the final client onboarding meeting and annual reviews, our agents are delivering a fully integrated plan — it is not like the old days of stapling an annuity policy or a life policy to a securities portfolio printout.

Feldman: What advice would you give to an agent who is selling universal life and wants to get into the wealth side of the business?

Donaldson: First, their clients are on the wealth side of the business. Second, if done correctly, just like selling a UL policy or a fixed indexed annuity, the approach no longer involves trying to impress consumers with your mastery of all the complexities of the different products that we sell, those days are waning.

What we sell generally is more homogeneous than not. Every policy has different riders and different features. But at the end of the day, what will appeal to those consumers who want both accumulation and protection? You’re only talking to them about protection, and you need to address both worlds. And you need to do it in a way that’s simple and easy to understand.

Done well, financial planning should be simple and easy to understand. That doesn’t mean consumer challenges are simple. There are lots of complexities in life. But when you think about the inherent values of the products that we deliver, which you can only get with insurance companies — 100% mortality risk mitigation, 100% longevity risk mitigation — it makes capturing the wealth side much easier.

You are better educated as an insurance agent to start talking about mortality and longevity as part of a holistic financial plan. Your clients’ wealth advisors aren’t talking about mortality and longevity. Capturing those wealth assets is, frankly,

not as complicated as some of the products and processes that they need to master to sell protection.

What you are doing as a part of that financial planning process is having the client fill out a financial planning consideration questionnaire that then feeds into a plan that gets delivered back to you.

It’s something every agent and advisor needs to do because the world of distribution is continuing to come together. The distinctions between securities licenses and insurance licenses are going to wane over time. What consumers will really demand is great holistic financial planning. That’s where the world’s going.

This is the wave of the future, and Simplicity is driving the platform to meet those changes.

Feldman: With life insurance and, to some extent, with annuities, underwriting has been one of the biggest challenges. What are you doing at Simplicity to solve those challenges?

Donaldson: With our size and scale, we have a fully built-out underwriting desk that our partners can tap in to the day they join Simplicity. The underwriting staff is expert at working with their carrier counterparts — to either work through particular issues on an individual application or engage in senior-level dialogue with carriers about a different perspective on the risk that they’re looking at.

I don’t think that underwriting will ever go away, but I think you will see the carriers become more sophisticated. From a tech perspective, they’ll become more streamlined. Good underwriting requires a human touch, just the same way good financial planning requires a human touch. What we want to do with our technology and our platform is enable efficiency and remove some of the friction so that the experts in our industry can better serve their clients.

Feldman: Where do you see this industry going in 2025 and beyond?

Donaldson: I’ll give you a short-term answer and a long-term answer.

Short term, I think there are legitimate concerns about the election that could impact our industry. If we look back to 2020 and political and electoral machinations

that occurred, we remember that there was a period of uncertainty that slowed business. I don’t know if we will face the same level of uncertainty at the end of this year and moving into 2025. It is hard to predict, but this is one of the main reasons that we executed a recapitalization earlier this year. The recap validates and strengthens our business. Our agents and advisors, our financial institution clients, and our insurance carrier partners now know that Simplicity is especially well positioned to survive any year-end challenges.

We are a perfect home for our agents and advisors who may themselves be facing uncertainty from a business perspective as we go through this election cycle. We can help them pivot their business, we can train them on new products, new processes. We can create efficiencies in their business to deal with any short-term challenges that may come up. So that’s my answer to the short term.

Long term, I think the election cycle is irrelevant to what I think will continue to happen. I think we have seen a sea change over the past 12 to 18 months on the value of protection products for our securities counterparts, banks, broker/dealers, RIAs, even those fee-only advisors.

They now understand — and I think it was the interest rate shock of March 2023, when FIAs were clearly a better bond alternative and MYGAs way outperformed CDs — that insurance products deliver unique protection benefits.

The days of Ken Fisher banging the drum and trying to get everyone to look at commissions — ignoring the fact that fiduciary advice and sound holistic financial planning require the use of protection products — are going to wane. I think the best days of the protection market are ahead of us. It will be incumbent on us — those in the insurance profession — to embrace the accumulation side. We should not view accumulation as a threat. Instead, we should continue to invest in technology, to grow protection in what used to be exclusively accumulation turf and deliver the best planning, products and services to the American consumer.

I think that genie is out of the bottle. I’m excited about the prospects for our insurance industry. I think the best days are ahead, both for Simplicity and, more broadly, for the insurance industry.

The Future of Digital Transformation in Life Insurance: How cloud technologies are leading the way

By Matthew Segreti, CTO & SVP Product Development at LIDP

The life insurance industry is transforming to keep pace with today’s digital era. Cloud technology is central to the industry’s evolution — driving innovation and operational efficiency. But while the industry’s excitement is presently over the potential of artificial intelligence, it’s essential to recognize that life insurers must modernize their environments to utilize AI effectively. Cloud technologies provide immediate benefits while creating a foundation to test and implement AI use cases, positioning insurers to take advantage of AI in the future.

Cloud as the foundation for agility and scalability

Adopting new technologies faster has been difficult in the industry due to the complexity of managing large volumes of sensitive data, regulatory requirements, and the need for seamless customer interactions. However, market demands are shifting, and customers now expect personalized digital experiences. Cloud-based platforms offer unparalleled agility and scalability, allowing insurers to respond to these evolving expectations.

Cloud infrastructure allows insurers to scale operations rapidly to meet fluctuating demands. Whether processing an influx of new policies during a new product launch or handling unexpected claims spikes, cloud platforms allow life insurance companies to adjust their resources quickly. This scalability ensures optimal performance without the high upfront costs associated with traditional on-premise infrastructure.

At LIDP, we’ve seen how cloud technology has empowered life insurers to streamline operations and lay the groundwork for future advancements like AI. By moving away from the limitations of legacy systems, insurers are creating a platform that can grow with their business and evolve to incorporate next-generation technology.

Enhancing security and compliance

As insurers embrace digital transformation, data security, and regulatory compliance are the most significant concerns for life insurance companies. In an era of rising data breaches and cyberattacks, protecting a client’s sensitive data is paramount.

Cloud technologies offer advanced security measures far exceeding many traditional on-premise systems. Leading cloud service providers employ multi-layered security protocols, including encryption, continuous monitoring, and automated threat detection. For life insurance companies, this level of protection ensures that sensitive data is secure at rest and in transit.

In addition, the life insurance industry is subject to complex regulations, including GDPR, HIPAA, and other local

data privacy laws. Cloud-based systems are designed to help streamline the compliance process, offering built-in auditing, tracking, and reporting capabilities that simplify regulatory adherence. By centralizing these tools in the cloud, organizations ensure they remain compliant across different jurisdictions and as new regulations emerge.

Driving innovation with data and analytics

The future of life insurance depends on the industry’s ability to harness data effectively. By migrating to cloudbased platforms, life insurance companies have access to sophisticated analytics tools that extract meaningful insights and help decision-makers drive business forward.

Data and analytics are essential for underwriting and risk assessment. With cloud-based data analytics, life insurers can accurately assess risk by analyzing more comprehensive data points, including lifestyle, medical records, and even real-time information collected from wearable devices. This shift from traditional actuarial methods to data-driven decision-making can lead to more personalized policies and pricing models, as seen throughout the property and casualty market.

Enhancing the customer experience

In today’s digital world, customer expectations have never been higher. Policyholders want fast, seamless interactions. Whether purchasing a policy, filing a claim, or updating personal information, policyholders want it now.

Cloud-based platforms allow life insurance companies to offer these experiences with greater efficiency and personalization with customer portals, mobile apps, and self-service tools that give policyholders direct access to their information. When integrated with AI-powered analytics, these tools have the potential to provide real-time updates, personalized recommendations, and proactive customer service. However, cloud technology is the first step toward realizing this potential.

As the life insurance industry evolves, cloud technology will remain essential for immediate benefits like scalability, security, and compliance — and as a critical enabler of AI. While AI holds incredible promise for the future of life insurance, the journey begins by moving off legacy systems and into the cloud. At LIDP, we are committed to helping insurers navigate this transformation by providing cutting-edge cloud-based policy administration software that meets today’s needs while laying the groundwork for tomorrow.

Realize the immediate benefits of cloud technology today — and start your AI journey. Request a demo at lidp.com

Many people think if they don’t use their long-term care coverage, they’ve lost all the money they’ve paid into it.

But with Bridge®, the fixed index annuity delivers principal growth with protection from market losses when your clients don’t need long-term care services. And the Long-Term Care Rider provides benefits when they do. It’s a win-win! Visit Agents.EquiTrust.com/Bridge to learn more.

Bridge® combines a fixed index annuity with long-term care coverage — plus the NeverStopSM Wellness Program through Assured Allies. And everyone’s approved for long-term care coverage!1 1

Leave “use it or lose it” LTC coverage behind

There’s a better solution for building long-term care expenses into a comprehensive retirement plan

There’s a missing piece to many retirement strategies today — how to manage potential long-term care (LTC) expenses. In fact, just 28% of Americans nearing retirement age say they have money set aside to pay for future living assistance expenses.1

This creates a disconnect from the reality that many will face in their later years. An estimated 70% of people turning 65 today will need LTC services or support in their lifetime. 2 And if they’re unprepared to manage these expenses, the financial impact can be devastating.

The downside of traditional LTC plans

Due to its reputation of being expensive and difficult to obtain, many clients have grown weary of traditional LTC insurance. And because it’s generally “use it or lose it” coverage, they risk paying the premium, but perhaps never using the coverage. It’s a tough sell. However, the need remains — and there are now innovative options beyond traditional LTC insurance.

The next generation of LTC coverage

There’s a new way to cover the LTC gap with your clients. Some carriers are offering an innovative solution — a fixed index annuity (FIA) with an LTC rider. There are several perks to this approach:

Tax advantages — The annuity premium grows tax-deferred, and benefits for qualified LTC services are tax-free. 3

Dual benefits — The LTC rider offers LTC coverage when clients need it, and the FIA offers accumulation value when they don’t.

Simplified underwriting — FIA/LTC hybrid solutions make it easier for clients to get approved, and some carriers even guarantee approval.

Principal protection — The FIA provides protection from market losses when the client doesn’t need LTC services.

Some carriers even go a step further, offering personalized wellness programs that help clients live healthy lifestyles and potentially delay or prevent the need for LTC services.

Chart a course for the future

If you haven’t talked with your clients about building potential LTC costs into their retirement strategy, the time is now. An FIA/LTC hybrid is an effective way to close the LTC coverage gap, while avoiding the pitfalls of traditional LTC insurance.

Learn more about an innovative fixed index annuity with a long-term care rider and wellness program.

1 “The Affordability of Long-Term Care and Support Services: Findings from a KFF Survey”; Kaiser Family Foundation; November 14, 2023; https://www.kff.org/ health-costs/poll-finding/the-affordability-of-long-term-care-and-support-services; accessed September 6, 2024.

2 “How Much Care Will You Need?”; Department of Health and Human Services; Administration on Community Living; February 18, 2020; https://acl.gov/ltc/ basic-needs/how-much-care-will-you-need; accessed September 6, 2024.

The business of insurance is powered by data. Always has been.

Data sharpens underwriting decisions, produces the most accurate risk assessments and helps to better connect insurance producers with potential buyers.

In short, data drives insurance. And that makes insurance a natural fit for an artificial intelligence revolution.

“It reminds me of the early days of the internet when it was exploding and everybody knew that it was going to change everything, but we weren’t sure exactly how it was going to change things,” said Mitch Dunford, chief marketing officer with the Risk and Insurance Education Alliance, during a recent webinar. “Here we are again. We know AI is going to be a bigger and bigger deal, and the insurance industry is embracing it.”

halting steps forward with its incorporation of AI strategies — but one that is finding it harder to proceed with any deliberateness in a new AI world that is evolving fast.

Hopes are high.

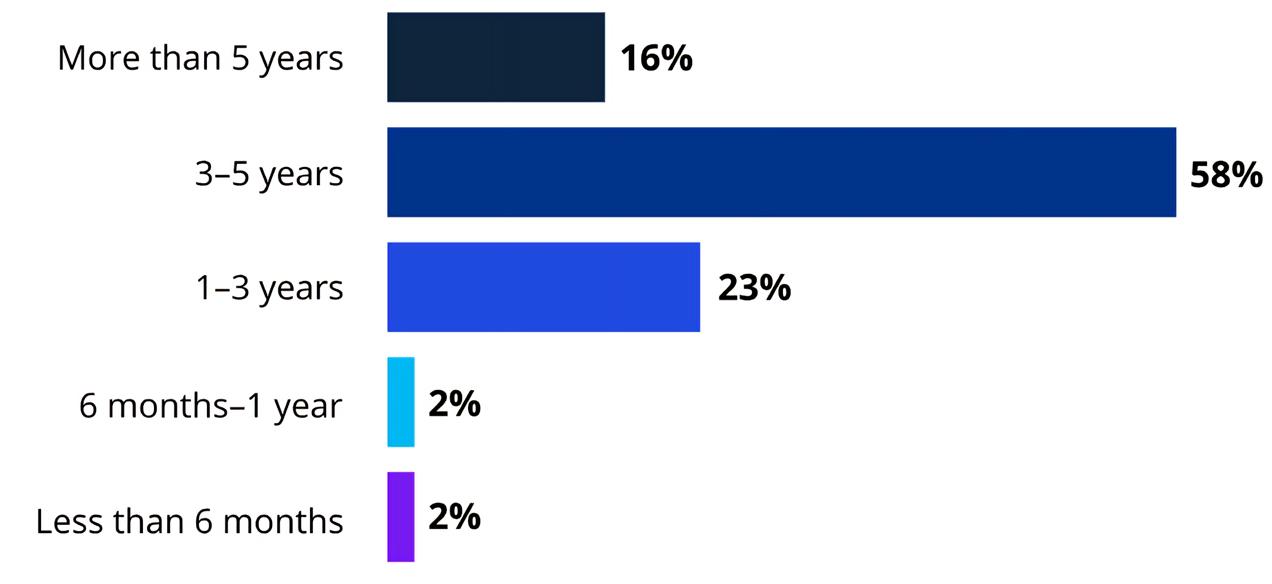

The KPMG 2023 Insurance CEO Outlook highlights a significant degree of trust in AI, with 58% of CEOs in insurance feeling confident about achieving returns on investment within five years.

“Artificial intelligence has the opportunity to be significantly transformative over the next five years,” said Dave Levenson, CEO of LIMRA and LOMA. “I would say that our industry is still moving carefully and cautiously, and of course, that’s going to vary a little bit by company, but for a technology that everybody really believes is going to be transformative, I don’t think we’ve invested as much as perhaps we can and should at this point.”

Return on investment in the implementation of gen AI

Of course, embracing the quick-change world of AI technology is not an easy move for many traditional insurance companies. It is not an industry known for its adventurous nature.

That leads to statistics like this one: 47% of technology executives say AI will have a significant impact on the insurance industry in the next three years, according to a LIMRA survey, but 48% of insurers do not have an AI training program yet.

Then there are the obvious concerns over privacy and the unintended consequences of combining AI with mounds of data. Regulators are busy working on rules upon rules for those issues. Add it up and you get an industry taking

Widespread uses

Some of the most intriguing integration of AI into insurance processes is happening in the property and casualty world.

Metromile is using telematics and AI as the basis of its pay-per-mile auto insurance concept. The insurer relies on a device installed in the vehicle to collect data on mileage, speed and driving habits. AI algorithms then analyze the collected data and generate a personalized rate for each driver.

Nauto takes AI technology to the next level. The AI-driven vehicle safety system employs a dual-facing camera, computer vision and algorithms to identify hazardous driving situations in real time. The

company claims its AI technology is seeing an 80% reduction in collisions.

Jennifer Kyung, vice president of P&C underwriting with USAA, said artificial intelligence is helping to speed up underwriting and gain more insights for underwriters.

In addition, AI can look at aerial images of property and determine whether there is a potential risk, enabling insurers to reach out to their customers about mitigation tactics. AI also can read through call transcripts and categories themes that help insurers with action items to improve their member service.

“It helps us look at broader swaths of data in claims files,” Kyung said during a September Insurance Information Institute webinar. “We look at it as an aid as opposed to a black box.”

Life insurers tread

lightly

AI integration on the life and annuity sides of the insurance world is not as dramatic as steering vehicles away from certain accidents. But some forward-thinking insurers are pushing ahead with a commitment to technology.

Insurers are moving forward in five key areas.

Enhanced risk assessment. AI can analyze vast amounts of data to identify risks more accurately, allowing insurers to offer more tailored policies and premiums.

Predictive analytics. By forecasting trends and potential claims, AI can help insurers make informed decisions about underwriting and pricing.

Customer experience. AI-powered chatbots and virtual assistants can provide instant support, answer queries and streamline the claims process, improving overall customer satisfaction.

Claims processing. Automated systems can expedite claims handling, using AI to assess damages through image recognition and process claims more efficiently.

Fraud detection. Machine learning algorithms can detect unusual patterns and flag potentially fraudulent claims, reducing losses for insurers.

Attend any big industry conference and when artificial intelligence comes up, life insurers are quick to mention generative AI. Unlike traditional AI, which often focuses on data analysis, gen AI can create original content — text, images, music and

Source: KPMG International “KPMG 2023 Insurance CEO Outlook” (December 2023)

The biggest challenges for implementing gen AI

more — based on learned patterns.

Gen AI has the potential to comprehend sentiment, empathize with consumers and respond with more relevant, personalized product offerings. That has the industry excited.

“We’ve seen a lot of interest and activity in the insurance sector on this topic, which is not surprising given that the insurance industry is knowledge-based and involves processing unstructured types of data,” said Cameron Talischi, partner with McKinsey & Co., on a recent podcast.

“That is precisely what gen AI models are very good for.”

Yet, despite moving ahead with gen AI test cases and capabilities, many insurance companies are finding themselves “stuck in the pilot phase, unable to scale or extract value,” McKinsey found.

Talischi blames a “misplaced focus on technology” as opposed to what is truly important from a business perspective.

“A lot of time is being spent on testing, analyzing and benchmarking different tools such as LLMs [language learning

models] even though the choice of the language model may be dictated by other factors and ultimately has a marginal impact on performance,” he explained.

Likewise, insurers are often not focused on the right test cases that can have the most impact, he added.

“The better approach to driving business value is to reimagine domains and explore all the potential actions within each domain that can collectively drive meaningful change in the way work is accomplished,” Talischi said.

The dark side of AI

AI comes with major potential to save insurers money through efficiency and information analysis. But one misstep could turn into a lawsuit liability award that could wipe out all the savings and then some. That context explains in part why insurers are somewhat hesitant to go all-in with AI before doing their due diligence.

“I think when you deal with new technologies like artificial intelligence, it’s really important that everybody understands what the good things are that technology can do [and] what are the dangerous things that technology can do,” Levenson said.

To that end, LIMRA helped the industry form a committee composed of nearly 80 executives representing over 40 U.S. insurance companies. The LIMRA and LOMA AI Governance Group aims to “create a foundation for sustainable and inclusive AI practices to improve the life insurance industry.”

Its first study, “Navigating the AI Landscape: Current State of the Industry,” was completed earlier this year. It found that 100% of carriers are experimenting with or using AI in some form.

They don’t have to look further than the front pages to see the risks.

State Farm was sued in the Northern District of Illinois over claims that its AI discriminates against Black customers. The class-action suit claims State Farm’s algorithms are biased against African American names.

Plaintiffs cited a study of 800 homeowners and found discrepancies among Black and white homeowners in the way their State Farm claims were handled. Black policyholders faced more delays, for example.

Another class-action lawsuit in California alleges that Cigna used an AI

Source: KPMG International “KPMG 2023 Insurance CEO Outlook” (December 2023)

Source: LIMRA/LOMA

algorithm to screen claims and toss them out without human review. The 2023 lawsuit was preceded by a ProPublica investigation headlined “How Cigna Saves Millions by Having Its Doctors Reject Claims Without Reading Them.”

Training is one way to reduce liability risks, but insurance companies are falling short there as well.

Regulation disparities

The rapid rise of AI and its potential for discrimination and invasion of privacy prompted some state insurance regulators to bypass the National Association of Insurance Commissioners and push through their own laws.

Colorado led the way with a sweeping bill governing the use of AI by the insurance

other states — including New York and California — are considering AI legislation to restrict how insurers handle personal and public data.

“Really what we worry about when we are building these models is, where is all this data coming from?” said Derek Leben, president of Ethical Algorithms and associate teaching professor of ethics at the Tepper School of Business at Carnegie Mellon University. “Do people have control and ownership and a say over how their data is used? Do we understand how and why models are making these decisions?”

Leben participated in the general session titled: “AI: How Is It Powering the Future?” during the LIMRA Annual Conference in September.

We believe the process-oriented guidance presented in the bulletin will do nothing to enhance regulators’ oversight of insurers’ use of AI Systems or the ability to identify and stop unfair discrimination resulting from these AI Systems.

BIRNY BIRNBAUM

industry. The law is so thorough in its novel requirements for developers and deployers of high-risk AI systems that progressive Gov. Jared Polis, D-Colo., wrote the Legislature expressing his “reservations.”

Polis urged the Legislature to “finetune the provisions and ensure that the final product does not hamper development and expansion of new technologies in Colorado that can improve the lives of individuals” as well as “amend [the] bill” if the federal government does not preempt it “with a needed cohesive federal approach.”

Colorado’s AI regulation requires life insurers to report how they review AI models and use external consumer data and information sources, which includes nontraditional data such as social media posts, shopping habits, internet of things data, biometric data and occupation information that does not have a direct relationship to mortality, among others.

Life insurance companies are also required to develop a governance and risk management framework that includes 13 specific components.

Although Colorado acted first, several

Leben told a LIMRA audience that “the regulations we need are already on the books” about topics such as product safety liability and discrimination.

NAIC tackles AI

NAIC regulators are trying to keep up with AI, but work is going slowly.

The executive committee and plenary adopted the Model Bulletin on the Use of Algorithms, Predictive Models, and Artificial Intelligence Systems by Insurers in December after a deliberate process.

The bulletin is not a model law or a regulation. It is intended to “guide insurers to employ AI consistent with existing market conduct, corporate governance, and unfair and deceptive trade practice laws,” the law firm Locke Lord explained.

Some consumer advocates were disappointed by the mild language in the bulletin.

“We believe the process-oriented guidance presented in the bulletin will do nothing to enhance regulators’ oversight of insurers’ use of AI Systems or the ability to identify and stop unfair discrimination resulting from these AI Systems,” wrote

Birny Birnbaum, executive director of the Center for Economic Justice.

When this issue went to press, 17 states had adopted the bulletin and an additional four states “have adopted related activity,” an NAIC spokesperson said.

In addition, regulators are surveying segments of the industry to gauge its use of AI. Fifty-eight percent of life insurers are either using or have an interest in using artificial intelligence in their businesses, an NAIC working group found.

The 58% figure is well below the use of AI or the desire to use the technology expressed during earlier surveys by home (70%) and auto (88%) insurers.

Third-party vendors are developing a lot of the AI and machine learning technology that is proliferating in the insurance industry. That creates a lack of control for insurers and regulators. NAIC regulators were concerned enough to establish a 2024 task force devoted to regulation of third-party systems.

The Third-Party Data and Models Task Force began meeting in March. It is charged with:

» Developing and proposing a framework for the regulatory oversight of third-party data and predictive models; and

» Monitoring and reporting on state, federal, and international activities related to governmental oversight and regulation of third-party data and model vendors and their products and services.

Regulators all but confirmed that it will be difficult to keep pace with the evolving power of AI.

“I feel like the industry is moving very fast in this space,” Vermont Insurance Commissioner Kevin Gaffney said during a work session on the topic. “We are trying to keep up. It would be nice to say we could stay ahead, but I think the realistic vision right now is to make sure that we’re still in the rearview mirror of industry.”

InsuranceNewsNet

Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at john.hilton@innfeedback. com. Follow him on Twitter @INNJohnH.

JUDITH LEE is living her American dream while her daughter SIMONE is helping her build a practice dedicated to serving those who are building their own dreams.

By Susan Rupe

Judith Lee was 12 years old when she moved from Jamaica to Brooklyn with her parents, who were seeking a better life and a wider range of opportunities. She enrolled in public school as a grade 7 student, but her academic life quickly took off like a rocket.

She skipped grade 8, ended up graduating early from John Dewey High School and soon earned a degree from Hofstra University.

“I am a child of immigrants who have a culture that stresses education, that stresses hard work and the importance of family, and so I wanted to make my parents proud,” she said.

Today, Judith is senior vice president and resident director of The Lee Casey Group, a Merrill Lynch Wealth Management practice in Bedminster, N.J. Judith’s daughter Simone Lee is a financial advisor in her mother’s practice. Earlier this year, Simone became the 100,000th financial professional to earn the Certified Financial Professional designation.

“My parents left Jamaica with little and had to start over,” Judith said. “So understanding the concept of this and taking advantage of the opportunity to be a first generation in building wealth is something that is not lost on me.”

Judith entered the Macy’s management training program following her graduation from Hofstra. “I enjoyed the retail business because it is very dynamic. It is very fast paced, and I had many opportunities to interact with the public. I didn’t know where my path was going to take me, but I always knew that I enjoyed having a career that allowed me maximum interaction with people.”

Her Macy’s career also enabled her to travel to Asia on buying trips, something she enjoyed as well. But Judith had two young daughters and faced a two-hour commute to work each day. Something had to change.

She was always interested in the

financial markets and bought her first mutual fund while she was still in college. “Anything to do with money and wealth sounded very exciting to me,” she said.

A bank comes calling

In 1997, Judith received a call from a recruiter who was interested in her retail background. The recruiter worked on behalf of Summit Bank, which was opening branch offices in supermarkets.

“They believed I could learn about banking because of my retail experience and my interest in finance,” she said. She became a branch manager, but she didn’t stay in that position for long.

“A manager in the bank’s financial service division said to me, ‘Judith, I think you’d make a really good financial advisor. Why don’t you think about coming on our side?’ And ultimately that’s what I did.”

Judith became securities licensed in 2000 but realized she needed something more.

“In 2005, I obtained my CFP designation because I believed that — No. 1 — as a Black woman in the industry, I needed to have the requisite certifications that would allow me entry into the business and that would allow me to have the confidence and, more importantly, the broad product knowledge, to be able to help high net worth individuals in all aspects of their finances.”

Summit Bank was absorbed by another bank that eventually was absorbed by Bank of America. Bank of America completed the acquisition of Merrill Lynch & Co. on Jan. 1, 2009.

many high-net-worth clients, Judith said her firm also works with many “blue-collar clients, clients who are first generation in terms of building wealth, some individuals who are the first in their families to go to college. We work with senior executives who have risen to the highest ranks in corporate America and are building wealth through their 401(k) plans or stock options.”

She said her immigrant experience has served her well in relating to her clients.

“The very nature of having to leave your original birth country and having to start over, I think gives someone a unique level of drive. Even though the majority of my client base is Caucasian, I came from a community that gave me the ability to talk with anyone.”

“Merrill Lynch recruited me from what was Bank of America at the time, so I have been working for those predecessor firms since 1997,” she said.

Working in many worlds

As resident director of her firm, Judith said that she is a producing manager. “I still serve my clients, hold on to my book of business, but I get to be in management as well.”

Although The Lee Casey Group serves

Judith and Simone both are mothers who are employed outside the home, and Judith said that gives them a special interest in working with women.

“We understand that women face unique financial challenges, whether it be longevity risk or the fact that you know women don’t have income parity with men. Therefore, women are behind in terms of acquiring and building wealth throughout their working years and being able to catch up because of the income gap. It’s appealing to us to have a practice that is interested in working with high net worth women, single

The Lee Casey Group (left to right): Simone Lee, Michael Tillberg, Judith Lee and Thomas Casey.

the Fıeld A Visit With Agents of Change

women, women who are heads of households.”

A people person finds her career

Simone earned a mathematics degree from the University of Maryland and worked in project management before joining her mother’s practice.

“I’m very much a people person, and although I interacted with people in project management, I never believed I had any type of significant impact in their lives,” she said.

a career that was going to be flexible but also allow me to be my own boss.”

Simone recently gave birth to her second child and said being a young mother “puts me in a unique position to help a lot of my friends who are newly married or starting a family, they’re starting to build their wealth, or they might even be inheriting wealth. I’m able to help a lot of them understand the importance of maximizing your earnings during your prime earning years and saving more of what you earn.

“I think it’s extremely fulfilling to build relationships with families and individuals where you’re making an impact that can help them achieve their life goals.”

“I watched my mother in her career over the years, and I saw the flexibility and autonomy that she had in her career. She was her own boss, she set her own hours. This was appealing to me. And I saw the deep relationships that she built with her clients. She was always going to clients’ weddings, clients’ birthday parties. She became close with a lot of her clients, which told me that she was really making an impact in their lives. And I saw how happy she was in her role, and that ultimately led me to make the career switch.”

Simone said she has childhood memories of her mother taking her along to visit clients.

“Sometimes they would cook lunch or dinner for us because she had such a personal relationship with her clients. But I was too young to understand what was going on. It wasn’t until I was older that I had a better understanding of what she did.”

Simone said that building relationships while having personal flexibility are what attracted her to financial services.

“I think it’s extremely fulfilling to build relationships with families and individuals where you’re making an impact that can help them achieve their life goals. There’s also the flexibility and autonomy that I love because I’m so very much a family girl. I knew I wanted a family of my own in the future, and I knew I needed

Outside of work, the Lees enjoy traveling with their families.

“We’ve traveled extensively to a number of countries,” Judith said. “And when we travel, we don’t just spend all our time hanging out at a resort. We rent a car; we check out the landscape, the environment of the place we visit. We like to get down with the culture, eat where the natives eat, go to where they have fun. We’re an adventuresome family, and we like traveling and taking risks.”

Simone said that she and her mother “have a dynamic relationship.”

“I am able to learn so much from her because she’s been in this career for so many years. Each day is a different day, and I have the unique opportunity to work with someone in a mentor capacity who is also my mother. That’s appealing, and something that I hope to continue for the next 30 years of my life — to continue to build on our legacy, continue the work she started and build our team.”

Susan Rupe is man -

aging editor for InsuranceNewsNet.

These materials are for informational and educational purposes only and are not designed, or intended, to be applicable to any person’s individual circumstances. It should not be considered investment advice, nor does it constitute a recommendation that anyone engage in (or refrain from) a particular course of action. Securian Financial Group, and its subsidiaries, have a financial interest in the sale of their products. Insurance products are issued by Minnesota Life Insurance Company in all states except New York. In New York, products are issued by Securian Life Insurance Company, a New York authorized insurer. Minnesota Life is not an authorized New York insurer and does not do insurance business in New York. Both companies are headquartered in St. Paul, MN. Product availability and features may vary by state. Each insurer is solely responsible for the financial obligations under the policies or contracts it issues.

Securian Financial is the marketing name for Securian Financial Group, Inc., and its subsidiaries. Minnesota Life Insurance Company and Securian Life Insurance Company are subsidiaries of Securian Financial Group, Inc.

For financial professional use only. Not for use with the public. This material may not be reproduced in any way where it would be accessible to the general public.

She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at srupe@insurancenewsnet.com.

Looking good

How about looking great?

Gen Z feels overwhelmed about insurance

Generation Z is the newest generation to reach adulthood, and the thought of dealing with insurance makes Gen Zers overwhelmed and anxious. That was one of the findings from a National Association of Insurance Commissioners survey of Gen Z attitudes about insurance.

More than half of Gen Zers surveyed (54%) said they felt overwhelmed or anxious about dealing with insurance. More than 1 in 5 (22%) said they feel frustrated about dealing with insurance, while 14% said that thinking about insurance makes them feel old.

Gen Zers aren’t in any hurry to buy insurance either, the survey showed. Although 39% of them said they already own life insurance, more than one-third (34%) said they are putting off buying it as long as possible.

Despite their lack of knowledge about insurance, Gen Zers do believe it has value. The survey showed 76% said they believe life insurance is somewhat or very important.

MISUNDERSTANDINGS MAY CONTRIBUTE TO COVERAGE GAP

Americans have a good understanding of key life insurance principles, but nearly 6 in 10 either do not have coverage or do not know if they do, according to the 2024 Corebridge Life Insurance Insights & Awareness Survey. Misunderstandings around cost could help explain this life insurance coverage gap.

While 8 in 10 (80%) Americans correctly recognize that the most affordable time to buy life insurance is when they are young and healthy, the No. 1 reason keeping individuals from buying life insurance is cost, with nearly half (45%) of those who do not have coverage saying that cost was a reason they have not yet purchased a life insurance policy.

At the same time, the survey added, many Americans do not appear to have a clear picture of how affordable life insurance is. Only about 1 in 10 could correctly

identify the approximate monthly cost for a healthy 30-year-old to get a 20-year $250,000 term life insurance policy.

HISPANIC AMERICANS REPORT GREATEST INSURANCE NEED

Effectively engaging the Hispanic American market represents a big opportunity for the life insurance industry, LIMRA reported.

The 2024 Insurance Barometer Study, by LIMRA and Life Happens, reveals only 43% of Hispanics report having life insurance coverage. This is the lowest ownership among any racial or ethnic group over the past decade. Additionally, most Hispanics (53%) say they need, or need more, life insurance protection — 11 points higher than the general population. In addition, 46% of Hispanic families reveal they would face financial hardship within six months should the primary wage earner die unexpectedly.

QUOTABLE

The problem is private placement life insurance has been oversold. It's not for everybody.

— Chris Gandy, founder, Midwest Legacy Group

So why aren’t they buying life insurance? Many Hispanics perceive the cost of life insurance to be well above the actual cost. The study shows that more than 4 in 10 (44%) Hispanic Americans feel life insurance is too expensive. Yet more than 7 in 10 Hispanics (72%) overestimate the cost of a term life insurance policy.

WHAT THE INDUSTRY MUST KNOW ABOUT GEN Z

Offering “risk prevention” services is something life insurance customers overwhelmingly want, and a strategy that the few carriers that have tried it are having success with. So why aren’t more life insurance companies jumping in the pool? Good question, agreed Andrew Schwedel, global partner, Bain and Co., said during the 2024 LIMRA annual conference.

“The carriers that are really going to succeed and win will be the ones who are kind of all in,” Schwedel said. “It’s not something that you dabble with as one of five strategies that you’re kind of throwing spaghetti against the wall and seeing what works. So, it starts with this ambition to say, ‘I’m going to make this a core part of how I do business.’”

He listed the top five services desired by U.S. life insurance consumers as health checkups or remote diagnostics, rewards for healthy living, advice on healthy living and remote health monitoring, reminder of prevention measures, and digital access to all personal health records

Schwedel

Put your client’s retirement income dollars on the right path

Set yourself apart from the competition by providing your clients a guaranteed income for life with Kansas City Life Insurance Company’s Lifetime Income Rider that:

• Offers 7.2% guaranteed increase to Lifetime Income Amount for the first 10 rider years if no withdrawals in years 1 – 10.

• Provides a secure, guaranteed retirement income stream for life.

• Helps clients grow their retirement savings with a competitive fixed interest rate.

• Protects the value of a fixed annuity during market turmoil.

• Allows clients the ability to maintain the flexibility and control of their deferred annuity contract even after they start receiving income.

The Lifetime Income Rider provides guaranteed income for life and is an optional benefit available on all of Kansas City Life’s fixed annuity portfolio.

For information about a career with Kansas City Life Insurance Company, call Dwane Turnage, Vice President, Marketing, 855-277-2090

Crisis to creativity: Evolving to meet needs of millennials and Gen Z

Life insurance must shake off its reputation as death insurance.

By Samantha Chow

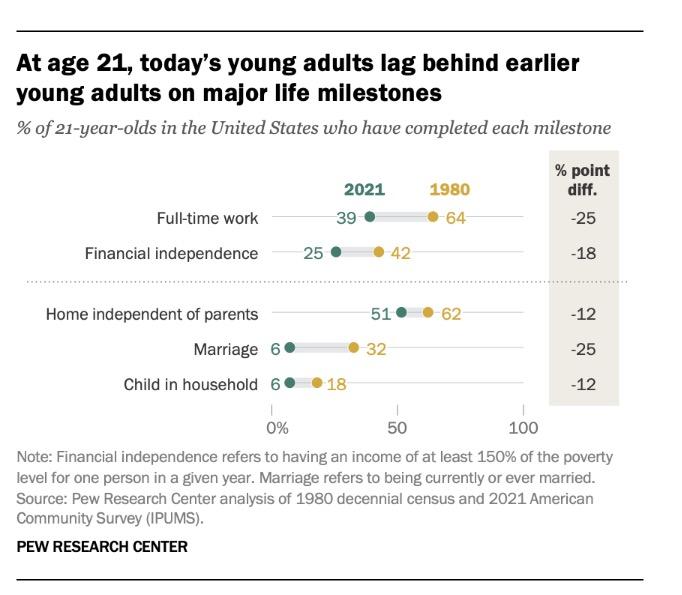

Insurance is designed to shield against uncertainty. However, while it was once a universal safety net, life insurance has seen a decline in ownership in recent years. This is especially marked among younger generations. Young adults today are hitting life milestones like marriage, having children and home-buying much later than their parents. As per data from Pew Research Center, in 2021, only 22% of 25-year-olds were married compared with 63% in 1980, 17% had children compared with 39% in 1980, and 68% were living independently compared with 84% in 1980.

This shift is evident in my own family. For generations, newborns were insured from birth. My great-grandmother bought a $1,500 policy for my grandmother, a tradition continued with my mother and brother. But as a child of the 1970s, I was the first in my family who did not receive a life insurance policy at birth. This was clearly a result of changing relevance given the stable economic conditions at the time, unlike past generations who faced more uncertainty.

Today, less than 60% of Americans have life insurance, a number that has been dropping since 1971, with a 13% decline in the past decade. There is a growing trend among Americans to focus on short-term financial priorities.

The 2024 Insurance Barometer Study from LIMRA and Life Happens reveals

that people prioritize vacations (29%), recreational activities (23%) and paying monthly bills (49%-60%) over saving for retirement or planning for potential catastrophes. The survey also suggests that most people overestimate the price of life insurance. More than 60% of respondents believed the cost of a life insurance policy would be $500 or more when in fact the average policy costs around $200 per year.

Life insurance is battling a misconception that it is “too expensive,” with consumers valuing it below other financial priorities. At the same time, advances in health care, shifting socioeconomic

conditions and fewer war casualties have made the threat of death feel less imminent. As a result, less than half of millennials and Generation Z individuals currently have a life insurance policy.

But there is still light at the end of the tunnel for the life insurance industry.

Younger adults are open to innovative, tech-driven insurance solutions. Life insurance is not just about death benefits; it can replace income, serve as an investment, cover long-term care and more.

Insurers might consider offering products that resonate with millennials and Gen Zers. For example, a return-of-premium term policy not only provides protection in case of death, but also aligns with the savings mindset of the younger generation. Unlike a typical term policy, policyholders won’t lose the money if they outlive the term, making it more appealing for those planning for early retirement.

Engaging with consumers in meaningful ways

The consumer behaviors, goals, needs and expectations of millennials and Gen Zers are markedly different from those of their baby boomer predecessors. As baby boomers phase out of the target market for life insurance, the U.S. is poised to experience

an unprecedented wealth transfer. This generational shift highlights a critical challenge: bridging the gap between the evolving needs of younger consumers and the traditional life insurance market.

The Insurance Barometer Study shows that in 2024, the need gap among adults with or without life insurance has widened to 42%, compared with 40% three years ago. This gap underscores the urgent need for education and communication efforts that clearly convey the multifaceted value of life insurance.

Creative marketing and clear communication are crucial to engaging this new generation. Reaching millennials and Gen Zers means meeting them where they are — on digital platforms. Using storytelling to showcase real-life scenarios where life insurance makes a tangible difference is now table stakes. However, it’s also important to be prepared for face-to-face interactions, phone calls and other engagement platforms, as these generations have diverse preferences for how they interact.