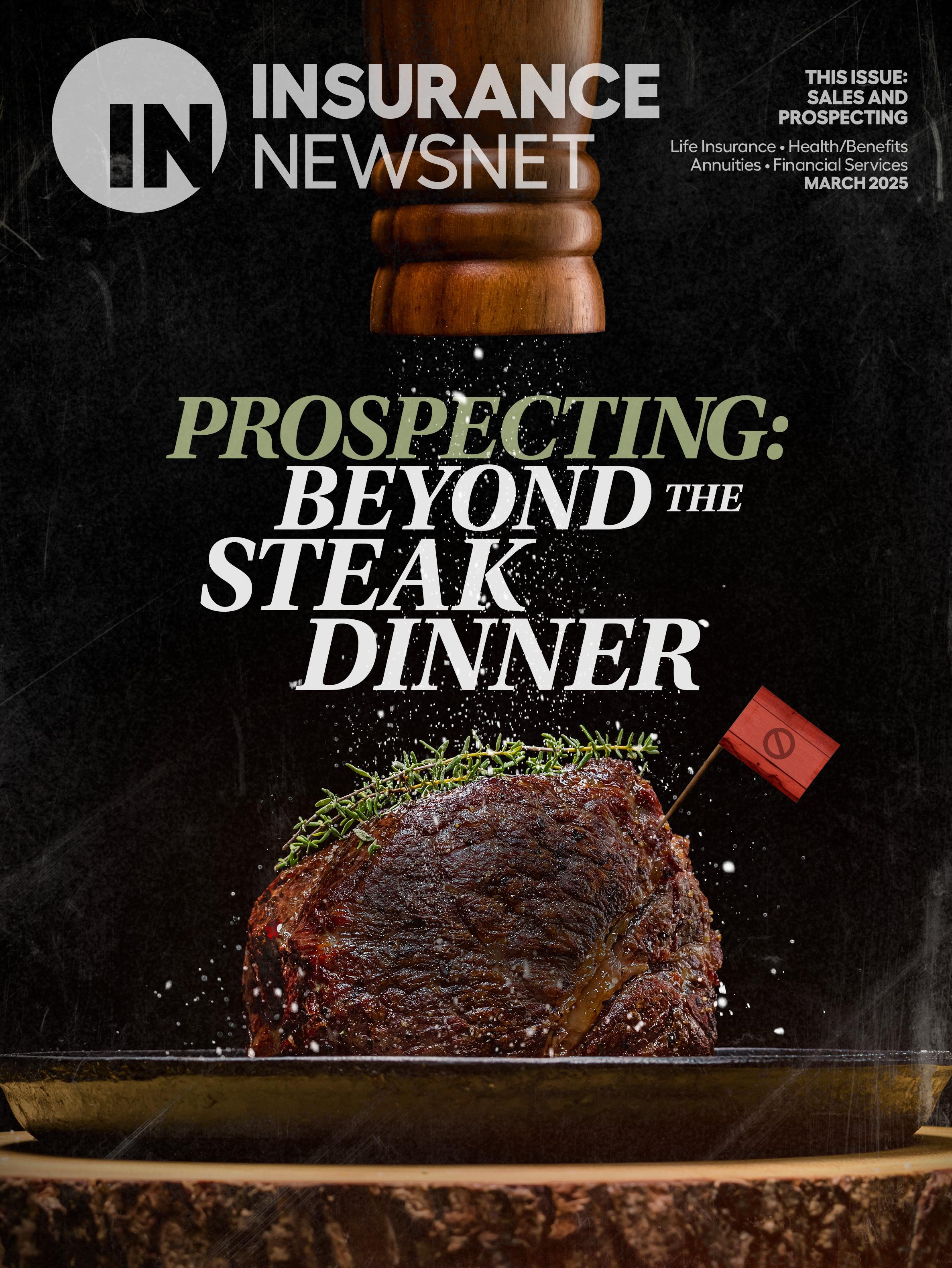

Advisors are finding novel ways to connect with prospects and turn them into clients.

PAGE 8

Is the age wave a retirement tsumani? with Ken Dychtwald

PAGE 4

“ ONE OF THE GREATEST ADVISOR MOVIES EVER CREATED.”

PAUL F.

“I WENT FROM BASICALLY ZERO TO $10 MILLION IN PRODUCTION IN 12 MONTHS… JUST USING THIS SYSTEM.”

STEVE L.

Turn the page to find out more.

Introducing Retirement Everest—the groundbreaking new film where producers go to Mount Everest to create the most compelling story ever told for financial advisors and their clients. Now, YOU can star in this incredible film and harness its power for your business.

BILL SHARPE, NOBEL PRIZE WINNING ECONOMIST FEATURED IN RETIREMENT EVEREST

The Big Idea: Decumulation is the OPPOSITE of Accumulation!

Getting to the summit of Mount Everest is great, but the descent is where the majority of the fatalities happen. By the same token, the hardest part of retirement planning is AFTER retirement because of all the risks: market risk, inflation risk, health care, interest rates, tax risk, longevity, etc.

Retirement Everest shows the challenges retirees face and why they need a different strategy (guaranteed income) and a Decumulation Expert like you to help them navigate it! Plus it includes Nobel Prize winning economists, PHDs and world renown climbers and their tragic stories, along with real life case studies of people living off annuity income!

Our Exclusive Annuity Theater Marketing System

This proven system drives registrations, fills the theater, and showcases the most effective annuity sales pitch ever created. After the movie, you’ll be positioned to convert prospects into eager appointments! Hundreds of millions have been written from Brett and Ethan’s films! As the fourth film we’ve produced, we include a complete system that turns cold leads into paying clients within weeks and makes you a celebrity

5

Reasons Why Theater Events are the Best Way to Write Annuities In 2025

1. The Perfect Pitch Every Time – Film is a powerful, emotional medium that brings your message to life.

2. Speed to Conversion – Nothing moves cold prospects to buyers faster than a well-executed film.

3. The Perfect Environment – No distractions in the theater. Attendees are focused and engaged.

4. No Presentations Required – Just welcome the audience, play the movie, and let it do the work.

5. Demonstration – Visually show the benefits of annuities and how real people live off guaranteed income and how others failed.

The Results?

INCLUDED IN THIS FREE PACKAGE:

• See the movie trailer with actual footage from Everest, world renowned experts, and real life client stories.

• Free case study “How producer Greg B. is writing over 1 million per movie event.”

• The A to Z guide on how to use movie events to explode your business.

• See how you can star in the film!

Movie theater events outperform traditional workshops. Our average event produces 105 leads, 23 appointments, and between $500,000 to $2,000,000 in premium. Plus, they’re fun, exclusive, and give you a huge edge over every other advisor doing the same old workshops.

Empowering You and Your Clients Through Education and Training

Utilize Simplicity’s Resources to Grow Your Life Insurance Business in 2025

���� Expert insights on tax-free retirement planning from best-selling author, Patrick Kelly

���� A free lead generating platform to cross sell your existing book of business

���� Marketing and sales tools to grow your business

���� Innovative proprietary platforms built to enhance your sales process

���� Networking opportunities and best practice sharing with industry experts and peers

Simplicity Partner, Patrick Kelly

IN THIS ISSUE

INTERVIEW

4 Is the age wave a ‘retirement tsunami’?

Ken Dychtwald has spent much of his five-decade career developing the concept of the “age wave,” a population and cultural shift caused by the converging global demographic forces of the baby boom, increasing life expectancy and declining fertility rates. He explains what this means to the financial services industry.

FEATURE

Prospecting: Beyond the steak dinner

By Susan Rupe

Advisors are finding ways to reach prospects that combine technology and word of mouth.

IN THE FIELD

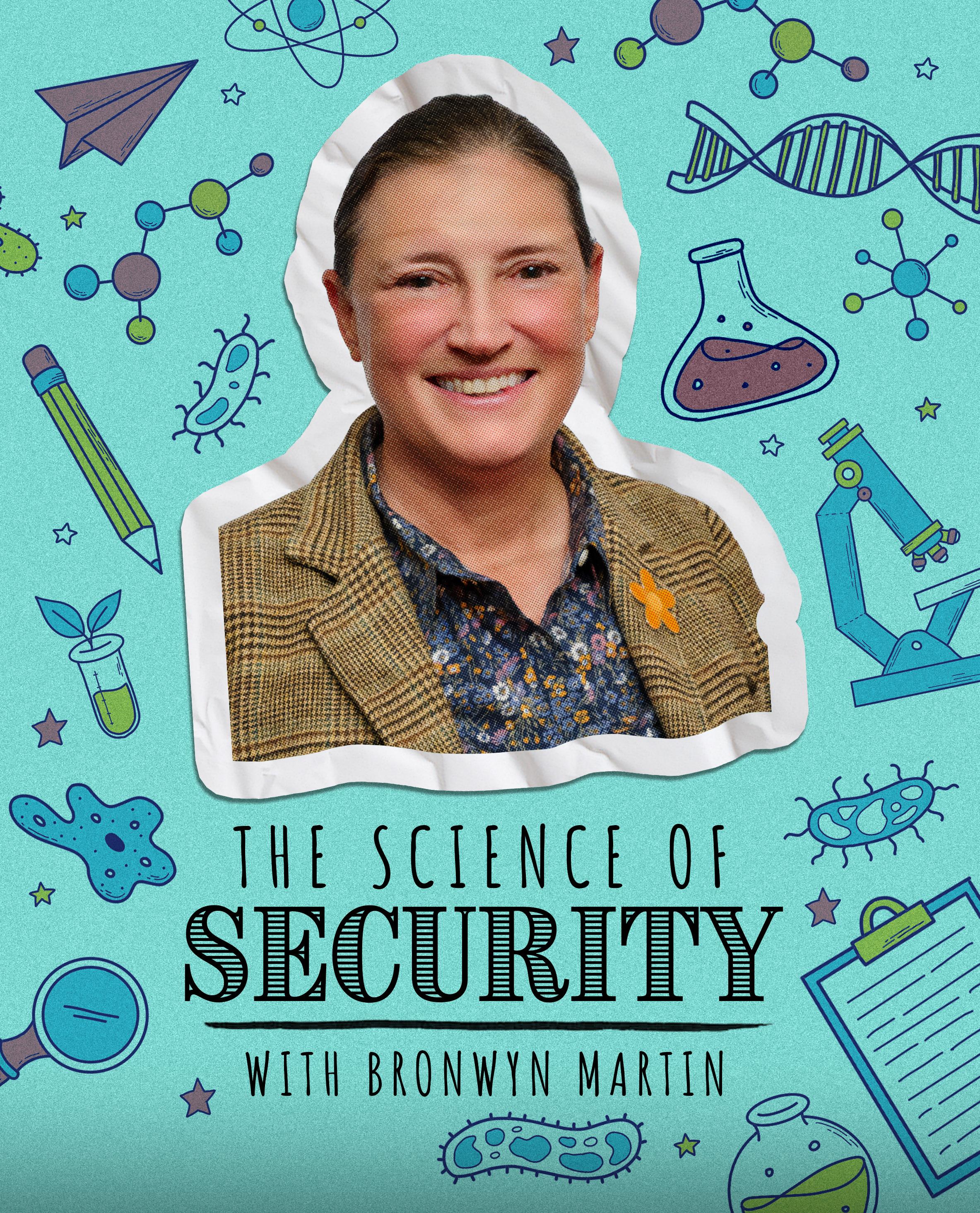

12 The science of security

By Susan Rupe

Bronwyn Martin started her career as a biochemist and researcher, but she found professional satisfaction in helping others achieve financial security.

LIFE

18 Key person insurance: A vital tool for startups

By Jonathan Selby

How this coverage can best serve earlystage businesses.

ANNUITY

22 Securing income through a fully insured plan

By Ernest J. Guerrerio

Fixed annuity contracts can fund a type of defined benefit plan for business owners.

HEALTH/BENEFITS

26 Why DI remains the best option to fund disability costs

By Frank Zuccarello

Dispelling three myths about disability insurance for high-income earners.

ADVISORNEWS

29 Unlocking hidden AUM

By Jim Farmer and Susan Danzig

An effective strategy to prospect within your current client base.

BUSINESS

31 Tech up your communication

By Michael Streit

How to reach clients and prospects without overworking your team.

IN THE KNOW

32 Whatever happened to DEI?

By Doug Bailey

Diversity, equity and inclusion programs face backlash as many companies eliminate or revamp them.

A changing approach to client prospecting

The rise of technology, particularly artificial intelligence, has revolutionized the way professionals identify, connect with and build relationships with potential clients. By leveraging these advancements and adopting new strategies, it’s possible to improve efficiency, personalize outreach and ultimately grow a business.

The role of AI in client prospecting AI has become a game changer in the realm of client prospecting. One of the most significant benefits of AI is its ability to analyze vast amounts of data quickly. For example, AI-driven tools can:

1. Identify ideal prospects. By analyzing client demographics, behaviors and preferences, AI can help insurance agents and financial advisors pinpoint their target audience. This ensures that outreach efforts are focused on individuals or businesses most likely to convert.

2. Enhance personalization. Personalization is key in today’s competitive landscape. AI tools can craft tailored messages by analyzing a prospect’s online presence, financial goals and even recent life events. Personalized communication not only grabs attention but also builds trust.

3. Automate routine tasks. Chatbots and virtual assistants can handle initial inquiries, schedule meetings and send follow-up messages. This allows professionals to focus on high-value interactions while maintaining consistent communication with potential clients.

4. Predict client needs. Predictive analytics can forecast a client’s future financial needs based on historical data. For example, an algorithm might flag a prospect who is likely to need life insurance after a significant life event such as getting married or buying a home.

Other technologies revolutionizing prospecting

Beyond AI, several other technologies are

reshaping how advisors approach client acquisition:

• Customer relationship management software. CRM platforms are indispensable tools for tracking interactions, managing leads and nurturing relationships. Features such as lead scoring and pipeline tracking provide a clear picture of where prospects are in the decisionmaking process.

• Social media platforms. LinkedIn, Facebook and Instagram have emerged as powerful tools for networking and prospecting. Through targeted ads and organic content, advisors can engage with specific demographics and establish their expertise.

• Videoconferencing tools. Virtual meetings have become the norm, making tools such as Zoom essential for building connections with clients regardless of location. The ability to share screens and collaborate in real time adds a layer of convenience and professionalism.

• Data enrichment tools. Platforms such as Clearbit or ZoomInfo provide additional insights into prospects, such as job titles, company size and recent activities. This information can help advisors tailor their outreach and make informed decisions.

New approaches to prospecting

Strategies used to engage with prospects also have evolved. Here are some of the latest approaches:

1. Content marketing. Providing value up front through blogs, e-books, webinars or podcasts positions advisors as thought leaders. When prospects perceive you as knowledgeable and trustworthy, they are more likely to reach out.

2. Hyperlocal marketing. By focusing on specific communities or geographic areas, advisors can build stronger, more meaningful relationships. Hosting local events or participating in community activities can enhance visibility and trust.

3. Referral programs. Satisfied clients

can be your best advocates. Incentivizing referrals with rewards or exclusive perks not only expands your network but also strengthens existing relationships.

4. Partnerships with complementary professionals. Collaborating with real estate agents, attorneys or tax professionals can open doors to new client pools. These partnerships create a mutually beneficial ecosystem that supports clients’ comprehensive needs.

5. Niche markets. Specializing in a specific demographic or industry, such as young professionals or small-business owners, allows for more tailored services and messaging. This focus often results in stronger connections and higher conversion rates.

Combining technology with the human touch

While technology offers incredible advantages, the human element remains irreplaceable in financial and insurance services. Trust, empathy and personalized advice are cornerstones of successful client relationships. Technology should enhance these qualities, not replace them.

The key is finding the right balance between automation and personalization. When done effectively, this combination not only attracts prospects but also fosters long-term, mutually beneficial relationships.

John Forcucci Editor-in-chief

NEWSWIRES

Insurers cite misinformation as top risk in 2024

Global insurers cited misinformation as the top risk in 2024, toppling extreme weather from the place it held in a similar survey 10 years ago. The top five risks named by insurers in 2024, according to the World Economics Forum Global Risk Report, are misinformation, extreme weather, societal polarization, cybersecurity and armed conflict. Misinformation ranked fifth in the same survey conducted 10 years earlier.

In addition, three emerging risks were identified. They are talent succession, compliance and governance, and strategic and data management.

John Romano, a principal in Baker Tilly’s financial services risk advisory practice, said insurers must focus on third-party risk management for 2025. Key third-party risks include data security breaches and regulatory compliance failures.

LAWSUITS TARGET USE OF DRIVER DATA

Connected vehicle services such as OnStar and insurance company apps that promise drivers lower rates for safe driving came under fire as several recent lawsuits alleged driver data obtained from these sources is being used unethically and illegally.

In one case that was settled recently, the Federal Trade Commission said General Motors and its subsidiary OnStar violated consumer privacy laws by sharing sensitive geolocation and driver behavior data without obtaining the consent of drivers.

Meanwhile, in Texas, Allstate is accused of unlawfully accessing and misusing the personal driving data of millions of policyholders through software embedded in third-party apps. Allstate was also hit with a proposed class action for allegedly violating California and federal wiretapping and privacy laws related to data collection practices. The

complaint, filed in the U.S. District Court for the Northern District of Illinois, said the company conspired to secretly collect and sell “trillions of miles” of consumers’ “driving behavior” data from mobile devices in-car devices, and vehicles to illicitly obtain data to build the “world’s largest driving behavior database,” housing the driving behavior of more than 45 million Americans.

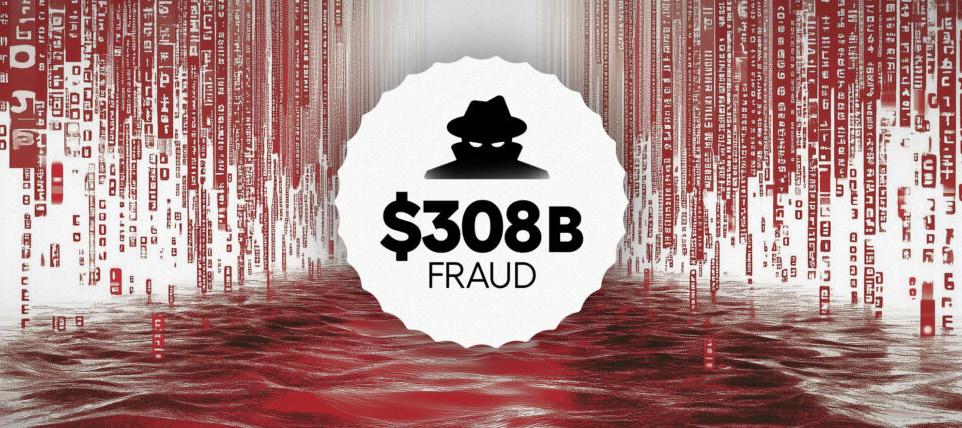

INSURANCE FRAUD IS A $308B PROBLEM

The Coalition Against Insurance Fraud estimates that insurance fraud costs the United States a whopping $308 billion a year. This amount includes all forms of insurance, with property and casualty fraud alone contributing almost $90 billion. Non-health insurance fraud costs the typical American household between $400 and $700 annually in inflated premiums, according to FBI estimates.

And it’s growing worse. Recent data shows customers reported losing more than $10 billion to fraud in 2023, a 14% rise over the year before.

The

Fed looks like Mr. Magoo, driving around, bumping into things.”

— Jeffrey Gundlach, DoubleLine Capital CEO

Some of the most prevalent forms of fraud, according to the coalition, are making inflated or fraudulent claims, falsifying data to get cheaper premium rates, inflating service costs and invoicing for unnecessary services. Arson for profit, staged auto accidents, inflated property claims, and workers’ compensation fraud involving fabricated or exaggerated injuries are examples of specific schemes.

BANKRUPTCIES HIT 14-YEAR HIGH IN 2024

Corporate bankruptcies soared to a 14-year high in 2024, underscor ing the catch-22 facing the Federal Reserve as it wrestles with inter est rate policy to bat tle sticky price inflation.

According to data gath ered by S&P Global Market Intelligence, 61 corporate bankruptcy filings were made in December, bringing the total for 2024 to 694. This was a 9.2% increase over 2023 and the highest number since 2010, in the aftermath of the Great Recession.

Businesses are going under due to a combination of debt and higher interest rates. Total debt accumulated by credit-rated nonfinancial U.S. companies reached a quarterly record of $8.45 trillion in Q3, according to Market Intelligence Data. Coupled with a higher interest rate environment, it’s a recipe for disaster.

The average credit card rate has climbed to 21.5%, or about 50% higher than three years ago.

Romano

Is the ‘Age Wave’ a RETIREMENT TSUNAMI?

‘Age Wave’ think tank founder Ken Dychtwald discusses the implications of aging, health and financial wellness

An interview with Paul Feldman, publisher

As people live longer, retirement is becoming much more challenging for financial advisors and their clients as they seek to optimize their “golden years,” enjoy continued good health and implement strategies to deal with the challenges of aging. That’s the main message of gerontologist, psychologist and lecturer Ken Dychtwald, co-founder of the Age Wave think tank. Dychtwald has spent much of his five-decade career developing the

concept of the “age wave,” a population and cultural shift caused by the converging global demographic forces of the baby boom, increasing life expectancy and declining fertility rates. Dychtwald and his wife, Maddy, founded Age Wave, a think tank and consultancy with a perspective on the social, business, health care and financial implications and opportunities of global aging and rising longevity. Dychtwald has served as a fellow and presenter at the World Economic Forum and was a delegate and featured presenter at

two White House Conferences on Aging.

In 2022, Dychtwald hosted “The Legacy Interviews,” a webcast with notable figures in the field of aging and longevity that was turned into podcasts, a book and a 60-minute documentary called “Sages of Aging” that aired nationally on public television.

In this interview with InsuranceNewsNet publisher Paul Feldman, Dychtwald describes what global aging and rising longevity will mean for the world of financial services.

Paul Feldman: What led you to study the impact of global aging on business?

Ken Dychtwald: It has been a long, winding and fascinating journey. When I was very young, I became interested in the psychology of the body, what we came to call holistic health. I was asked to head up a big research project that was going to be conducted in Berkeley and focused on preventive health and well-being for older people. I was 24 at the time — that was exactly 50 years ago. My initial introduction to the field of gerontology was setting up programs initially in the United States and then around the world to help older people feel and function better.

What struck me was how interesting these older people were. We were living in a world where the focus was on youth and we seldom paid much attention to older people. They looked a little funny, they didn’t dress the way young people did and they were from another era. But I became captivated with their view. What’s it like to look at life from 90 years? What’s it like to think back over your satisfactions and also your regrets? In 1982 — a long time ago — I became a part of a twoyear study project put on by the Office of Technology Assessment, which was the think tank of Congress; it was bipartisan.

Age Wave, with the belief that businesses and governments needed to get off their youth kick and begin to realize not only that there would be more older people, but they were going to be a different kind of older person. What were the products and services and policies that would be needed to accommodate this utterly new phenomenon? Along the way, I’ve written 19 books and given talks to about 2.5 million people. I’ve advised about half the Fortune 500. It has been a wild ride. The truth of it is the subject is heating up now more than it ever has.

syphilis and polio in the rearview mirror. But now we have all these chronic degenerative diseases, and our studies have shown that people are most frightened about cognitive health, Alzheimer’s disease. I believe that we ought to step up our research efforts and find a way to end the disease, not just produce more caregivers.

The main issue is, how do I get my health span to match my lifespan? What people would like is to live 80 or 90 or maybe 100 years and be reasonably healthy and vital and able to contribute throughout those years. The United States has done a crummy job of that. We are 50th in the world when it comes to how long we live. There are 49 countries that have a higher life expectancy than we do.

I believe that we ought to step up our research efforts and find a way to end the disease, not just produce more caregivers.

Feldman: We’re here now. We’re in that age wave, as you describe it. We have 10,000 people retiring every day. What are some of your more significant findings?

The idea was that about 20 of us would travel back and forth to Washington every month or so and we would discuss how America would be transformed as a result of the aging of our population. That’s when I got exposed to this idea of demography. What I learned early on was that there were three forces at play. One was that people were living longer. That was utterly uncharted territory.

Throughout 99% of human history, people didn’t expect to live long lives. But now they were beginning to. On the other side of the seesaw, the birth rates were dropping. After the baby boom came along, people started having smaller families, fewer kids. You look at those two together, and what you see is that the United States was going to be shifting its center of gravity to older adults.

Forty years ago, I set up a company,

Dychtwald: First, most people are uncertain about who they might be in the years to come. There aren’t a lot of good role models for 80- and 90-year-olds. You’re in a stage of life that’s emerging, that’s new. We often think of “new” as being what the young people will do next or what new technology is going to happen, but not “What are 65-year-olds thinking about?” or “How they’re going to reinvent themselves” or “How much money does a 75-year-old need if they’re going to live to be 95 or 100?”

What happens when somebody finds themselves weary of their career but they still have a lot of life in them? How people are going to pay for their longevity is a nontrivial issue. That’s something major that I’ve learned.

Another issue that really struck me is that we have not set up our health care system to produce healthy longevity. Is that anybody’s fault? I’m not sure. It may just be that we created a health care system for the acute problems of young people. Thanks to the breakthroughs of the 20th century, we’ve been able to put diseases like diphtheria, cholera, typhoid,

But when it comes to health span, how many years do we live with reasonably good health? We’re only 68th in the world. The average American only will live, let’s say, 77, 78 years. It’s been backtracking a little bit during the COVID-19 years. But we will spend the last 10, 15 years of our lives in declining health, and that’s not what anybody wants. We’ve spent 100,000 years trying to make longevity happen, and now it’s happening, and we must figure out how to do it right.

Feldman: What is the impact of the age wave on the insurance and financial services industry? Is the industry ready for it?

Dychtwald: First, I don’t think there has ever been a more opportunistic time for the insurance industry than right now. Why do I say that? There’s a whole new category of need and confusion and help required. In the past, we focused on investments for investments’ sake. Then, in the last 20 years or so, there was a lot of focus on accumulation for retirement, saving and planning for retirement. But then, all of a sudden, we have this extended life span; so you retire at 63 or 65, and you might live another 20 years. How does that work financially? We don’t even have good language to describe it. Sometimes it’s referred to as decumulation, but I’ve never heard an average citizen use that word.

About 80%, 81% of the population doesn’t really have a clue how much they’re going to need and how they’re going to pay for it. That’s a problem. Our parents’ and their parents’ generations grew up in the Great Depression and were very frugal. Also, they expected to live only a couple of years after they retired. And they were likely to benefit from the pensions that were put in place after World War II.

must be realistic that the programs that we’ve set in place, like Social Security, will survive over the next decade. Remember that when Social Security was crafted, there was a 25% unemployment rate in the U.S.

Partly what Franklin Roosevelt tried to do was to get older people out of the workforce to give young people a shot at making a life for themselves. In 1940, there were 42 workers paying in a little bit

aren’t sure where to turn in this whole issue of “who can I be in retirement?” if the retirement will last 20 years longer than anticipated. You have traditional investment advisors, and then you have insurance professionals. They must find a way to be more integrated in a more holistic fashion so that the clients can get an idea about what’s the best path and the best decisions they need to make. Right now, it’s too confusing.

Beginning in the 1990s, a lot of those pensions started disappearing and people were put in the position of being responsible for their own retirement savings, and they’ve been doing a relatively miserable job of managing those savings. You have tens of millions of people in the United States — and multiply that around the world — who are looking at their later years and are thinking “I might need some sort of a guaranteed paycheck for life.”

This is particularly an issue for women. Women will be living five to 10 years longer than the men they’ve loved and cared for.

We need to make sure we’re mindful and thoughtful about what their needs are and what the products are and what the language is. Let me say one other thing about this: I think the field itself must become more user friendly. It must be more attuned to what really matters to people as they look at their longer lives. We also

each month for each recipient and people were receiving only a few hundred dollars in benefits a year. Fast-forward to today, we have about 2.8 workers per recipient and people are getting on average about $21,000 to $22,000 a year.

You add to that this age wave, and it’s reasonable to question whether these systems will be able to handle the demographic force of what’s coming. I think individuals and families must understand what kinds of decisions they need to make in order to either work longer or save more or have some sort of an investment/insurance combination so that they can go the distance with financial peace of mind and security.

I would also say that there’s a problem in terms of the financial community, because about 32% of the population has a financial advisor, and that segment of the population tends to be financially well off. Two-thirds of the population don’t really have anyone to talk to. And people

Feldman: How do you see that improving? What can the financial community do to get a better hold of this situation?

Dychtwald: I think that there are different approaches. If I were the head of a financial firm or an insurance company, I would add some training so that your agents and professionals can understand some of the broader questions to ask, just letting the clients know that you take their lives seriously and you want to know that their families are OK. Is there about to be a life event — a marriage, a death — that you ought to be tuned into? You already have a distribution force, give them some additional human-centered skills. That’s one approach.

The second approach is to partner. There is an organization called the Retirement Coaches Association, and they’re emerging. Maybe you find a retirement coach and you put them adjacent to your person or your team and they get called in and they participate in some of the discussions and people feel like someone is paying attention to them and they’re being asked reasonable questions.

There’s the unknown, there’s disaster, there’s illness, there’s loss. For example, studies repeatedly show that 70% of our population will need longterm care at some point in their lives. It may only be for a week, it could be for a couple of years, but they will need it. But only 30% of people think they will need long-term care. “No, I’ll be fine,” people say. “I don’t want to talk about that or think about it.” We must learn

Dychtwald highlights the latest findings from Age Wave and The Harris Poll in a keynote during the SIFMA annual meeting.

how to approach these issues in a way that doesn’t freak people out.

The financial services field must get better at letting people know that they’re responsible husbands, wives, parents, children. I have been to so many conferences within the financial community, and I sit in the back of the room before it’s my turn to speak and I hear lots of talk about product. I don’t hear a whole lot of discussion about people.

People must understand what’s up ahead, to understand that retirement can be good. Offer some positive examples of that. Also, help people understand what decisions they must make to avoid any potential problems and give themselves and their family the best possible life.

Feldman: What do you project will happen in the field of longevity over the next 10 years? Where do you see this all going?

Dychtwald: I think there will be a handful of major dynamics that multiply. For me, it’s like popcorn in the microwave. My eighth book was a book called “Age Wave,” which I wrote 35 years ago. Almost everything that’s happening now I wrote about then. It’s not as though we don’t see what’s coming, but it is the fact that we avoid it.

must be made to avert that. People have avoided doing anything about that because older adults don’t want to have their benefits messed with, and they’re heavy voters. Someone must find the right way to talk about these improvements so that it seems fair.

A third thing is, we need some breakthroughs in medicine. We must put an end to Alzheimer’s. I’m hopeful that it happens. I look at the frontiers of science and research, and I see vaccines being developed to prevent Alzheimer’s. I see extraordinary new technologies that are about to come along in the CRISPR zone where we can rewrite the DNA so that

husbands die and they inherit that wealth. That demographic is not addressed as far as I can see by the media, marketing or advertising.

Dychtwald: This is not some marginal little group of people. This is where almost all the wealth will be held and where most of the buying decisions will be for everything. I’ll give you an example. We have 78 million grandparents in this country, and I guarantee you very few people know when National Grandparents’ Day is. Nobody pays attention to it. It’s considered irrelevant. That’s a big mistake. We can’t think of this new over-50 population as one big group. It’s 55-year-olds, it’s 75-yearolds, it’s healthy people, it’s people with a health challenge, and it’s women who are becoming the financial breadwinner.

I think that you will see more and more creative minds decide to target older adults. But we have this new feeling of being a 60-year-old and this new weight of financial power that we’ve never encountered before among an older population.

our brains stay healthy for life. I think that’s coming in the next 10 years.

What are some of the big things that I think will happen in the years to come? I think that you will see a president of the United States in his ninth decade of life. How about that? It’s amazing what went on with Joe Biden and Donald Trump. These were two men who were older than anyone who had ever run for the presidency. We’ve grown to find that acceptable. You will see more 80-year-olds not just be president of the United States but be managers of football teams and be teachers in high schools and running companies. It just will be more normal.

Second, I think you’re going to see a lot of drama around the Social Security and Medicare scene because the numbers don’t add up in the years to come. Right now, those systems are set up to go bankrupt or belly up in 2034. Big changes

I think that marketing and advertising must snap out of their youth obsession. Here we are now in the modern age where more than 70% of all the wealth in this country is held by people over 50. This age group is far more open to trying new things, and new things are coming along at a lightning pace. They are buying stuff for their kids and grandkids, and they are also reimagining their lives. It’s a fantastic audience for a wide range of products, from pharmaceutical products to home renovation to leisure, recreation to gaming.

I think that you will see more and more creative minds decide to target older adults. But we have this new feeling of being a 60-year-old and this new weight of financial power that we’ve never encountered before among an older population. Those are the big changes I think we will see.

Feldman: Because women survive longer on average than men, they control trillions of dollars as their

Feldman: What are the major roadblocks in the financial world for what’s coming with the age wave.

Dychtwald: There are a couple of serious roadblocks that must be dealt with, and you can’t avoid it. Number one, we must integrate the accumulation and the decumulation territories.

Second, you must learn as much about people as about their money. We just did our big research project in the health field, and we learned that people wanted their health professionals to know what mattered to them more than what was the matter with them. They wanted them to know what mattered in their life, how they define health, what they enjoyed, the reasons they wanted to be healthy. I think the financial community is far more focused on the numbers and the financial plan, which are important. But if you leave out attention to the individual and to what matters in their life, you will lose a client.

Like this article or any other? Take advantage of our award-winning journalism, licensure and reprint options. Find out more at innreprints.com.

Forget cold calling and free dinners! Advisors are finding novel ways to connect with prospects and turn them into clients.

When a prospect wants to contact Panos Leledakis, they usually encounter his avatar first.

The avatar, also known as “Panos,” is Leledakis’ artificial intelligence clone and chatbot, and appears on his website. The avatar begins a conversation with the prospect to find out what the prospect is seeking. From there, Panos can answer the prospect’s questions and serve up information on what product or service he is trained to sell. That electronic conversation eventually leads to a meeting with Leledakis.

Leledakis is founder of IFAAcademy, based in Miami, and a pioneer in incorporating AI, virtual reality and the metaverse into selling life insurance.

“Imagine being able to serve clients 24/7 with AI-powered chatbots like me that handle inquiries and provide personalized experiences without breaking a sweat,” he told InsuranceNewsNet.

Forget cold calling. Sending out invitations to free dinners? That’s so yesterday. Today, advisors are using technology as well as specialized ways of tapping into their target markets to reach prospects.

Leledakis’ latest move is to put a link to his website inside an near-field communication card and give that card to prospects and clients. “When I give that to people, I say, ‘Whenever you want, call me. If you don’t feel like talking or I’m traveling and you cannot reach me or whatever, take this card and tap it to your phone. My chatbot will come up, and you can speak with it like it’s me.”

“Panos” seems to appear everywhere in Leledakis’ universe. Leledakis is an avid blogger on insurance and technology topics, and he uses his social media channels and website to direct prospects to his blog, where they encounter “Panos” and can ask “him” questions.

“He’s like a sales representative for me,” Leledakis said. “He can start the sales pitch and have a discussion with someone. He’ll ask, ‘Are you interested in something?’ and then when a prospect replies, he can say, ‘We can do a needs analysis’ or whatever the proper response is. He gives me leads so I can follow up with the prospects. He works 24/7, in any language in the world.”

Leledakis invented two software systems for insurance need analysis by implementing the science of risk management, artificial intelligence and extensive neuroscience research on risk perception and decision-making. But although he is known in the insurtech world, he still has strong roots in insurance, with long-time membership in the Million Dollar Round Table and the National Association of Insurance and Financial Advisors.

His target market for insurance is venture capitalists and startup owners, who

have a need for key person insurance and related products. A hightech way of reaching prospects is a natural fit for those who are working to get new businesses off the ground.

Webinars add value

Leleldakis also is developing a content marketing strategy to educate prospects on his services. But one of the biggest ways he has of reaching prospects is through webinars. He began conducting webinars in 2015, but it took the COVID-19 pandemic for webinar prospecting to take off.

“At the beginning of the pandemic, we started to do webinars that had nothing to do with insurance,” he said. “We did a webinar on what to do with your children when they couldn’t go out and do anything because of COVID-19 restrictions. We sent the link to the webinar to our clients and invited them to ask their friends to participate as well. Because the webinar wasn’t about insurance, it was something extra we could bring to add value.”

He promoted the webinar on 100 social media groups and advertised it on Facebook. The result? More than 1,700

“He’s like a sales representative for me. He gives me leads so I can follow up with the prospects. He works 24/7, in any language in the world.”

—

Leledakis speaking about his AI counterpart who exists across his website

The virtual avatar called “Panos” is an AI clone of Panos Leledakis and takes care of warming up prospects who visit his website.

participated in the webinar, 1,300 of whom were not current clients. Of those participants, 500 booked an appointment with him, and 95 became clients.

He is active on many social media channels and uses those channels to discuss issues of interest to parents. “I post things that hit their pain points and get them to think about me when they think about insurance.”

Leledakis also uses virtual reality to reach prospects, particularly young adults who he says believe Zoom is outdated.

“You go inside as an avatar, and you can meet people like you’re going to a conference,” he said. “There are avatars all over the place, so you can go and introduce yourself. So I’m finding clients through these horizon worlds and VR worlds.”

Emotional intelligence speaks to prospects

Leledakis may have found the key to prospecting by using a high-tech approach, but Katie Kimball Dyer is reaching prospects through more low-key methods.

Dyer is a financial advisor and financial coach based in Boston. She relies on conversations to make prospects feel comfortable about discussing their financial concerns with her.

“If I put myself out there as a financial advisor or planner, people hear those words and they think, ‘That’s not for me. That’s for someone wealthier than I am or in a different world than mine,’” she said. “People don’t realize that I can help everybody. And those are the people I

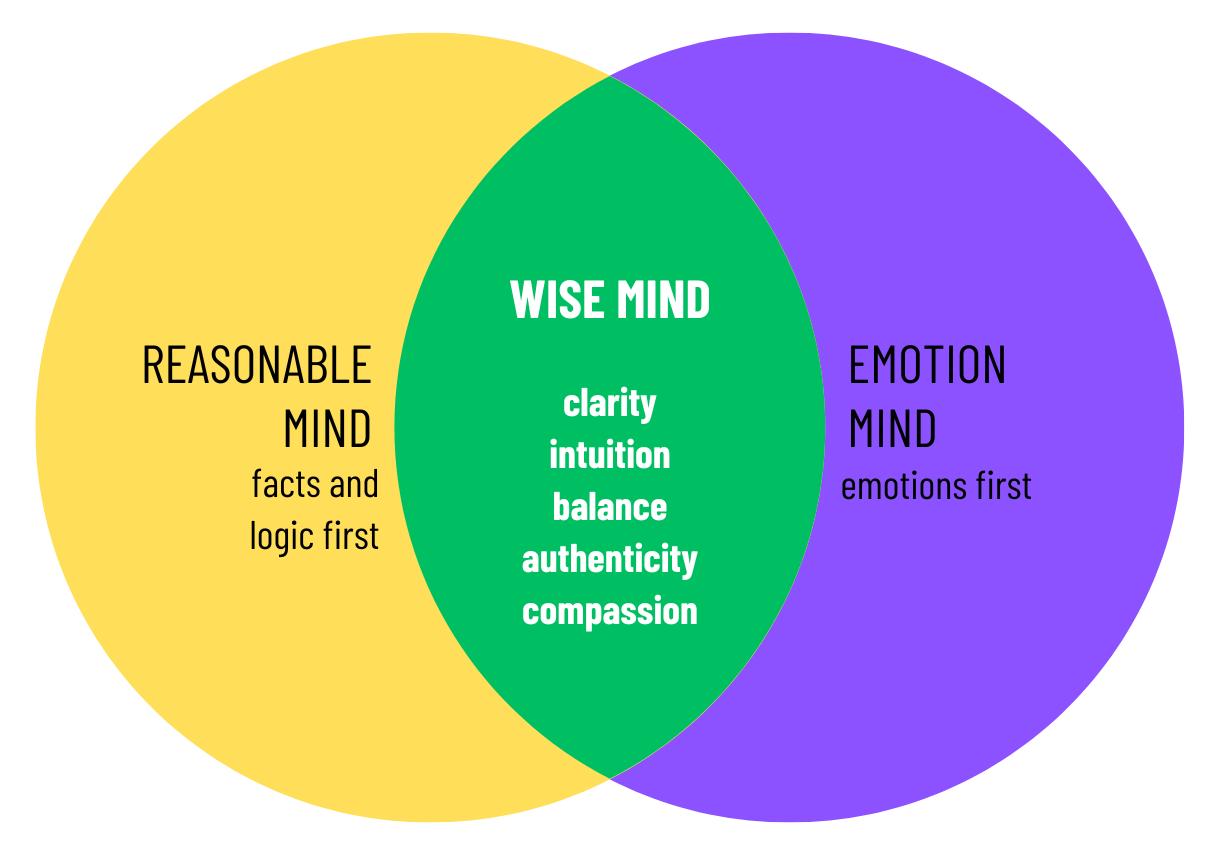

The WISE MIND is based on the concept of the three states of mind: emotion mind, reasonable mind and wise mind. The wise mind is the optimal state where rational thinking and emotions come together. It allows individuals to make sound decisions that align with their values and goals. It involves mindfulness exercises, such as observing, describing, and participating fully in the present moment.

In the practice of Wise Mind decision-making, individuals aim to find a balance between logical reasoning and emotional intuition. By tapping into the Wise Mind, which combines both the rational and emotional aspects of thinking, individuals can make decisions that are grounded in both facts and personal values This approach allows effective decision-making that considers both the practical implications and the emotional impact of choices.

want to work with — everyday people and business owners.

“So one of the things I do is approach people with the message ‘I’m here for you. The reason I’m an independent advisor is because I represent you to this larger financial world.’ But part of that conversation is understanding people’s feelings and acknowledging how this could all feel. I have started getting younger clients by having that conversation.”

Dyer said she bases many of her prospect conversations on the concept of “the wise mind.”

“It’s a psychological term,” she explained. “It’s when you take the most perfectly logical option and the most perfectly emotional option, and you combine them for a middle ground solution. And that’s how I treat people’s financial planning, because I don’t think feelings should be a secondary conversation when dealing with money. I think people’s feelings govern a lot. I don’t think they should govern the whole decision, but I do think that they play such a bigger role in how people

act with their money and make decisions with their money that it should just be part of the initial conversation.”

Dyer said she has been successful prospecting in local groups and small groups, both virtually and in person.

“I’m part of a local women’s network of business owners for my community, and they have time at the end of the meeting where you can come up to the mic after the main presentation and talk about what you do,” she said. “I serve a lot of LGBTQ+ business owners, and I attend their events as well.”

She also has been successful prospecting among virtual communities where her core prospects gather.

But guiding people through their emotions to help them take action on their finances is at the heart of Dyer’s prospecting techniques.

“I believe emotions are a valid part of this conversation,” she said, “and when I build a recommendation for somebody, I ask them, ‘How do you feel about what I just presented to you?’ Because I could

Dyer

write the greatest numbers plan in the whole world, but if they feel uncomfortable for some reason, they’re not going to follow it.”

Anxious parents make good prospects

When Brock Jolly started his career in the early 2000s, he used cold calling to prospect for long-term care insurance clients. A few years later, after he moved out of the LTCi space, Jolly found a niche in the college planning market. And prospecting in that market needed a different technique than what he had used in the past.

Jolly is managing partner at Veritas Financial and founder of The College Funding Coach, based in Tysons, Va.

Like many advisors who want to share their expertise and find clients, Jolly took the free-steak-dinner route to reach anxious parents who wanted information on how to pay for their children’s college education.

“What I found was you had a lot of people who willingly came to get a great steak dinner and a glass of wine at some of Northern Virginia’s best steak houses, and then somehow disappeared when it was time to actually meet and talk about financial planning,” he said. “I spent an awful lot of money on those types of seminars and didn’t get the results.”

As he worked in the college funding market, Jolly discovered two things about prospecting.

“No. 1, there’s a sense of urgency. Parents are a little panicked about how they’re going to pay for their kids’ college education and still be able to retire,” he said. “No. 2, although we do a lot of seminars, we found that our bread and butter

Jolly found that when promoting college planning, it made a lot more sense to conduct workshops directly in public and private schools, adding context to his presentation.

was being able to go directly to public and private schools — elementary schools, middle schools, high schools, even preschools — to conduct workshops about college funding, and we leverage these organizations to promote our workshops.”

Jolly said the schools where he conducts the workshop will promote the event, sending information home with students or doing email blasts to parents.

“The schools get the word out, and then we do our workshop,” he said. “We have a whole workflow built out before and after the workshops to be able to drip-market to these parents and give them valuable tools on how we can be a trusted resource for families when it comes to thinking about how they’ll save and plan and pay for college, and how that fits into the broader context of their overall financial plan.”

The attendance at Jolly’s workshops averages around 100. He compared that with the attendance at a steak-dinner seminar.

“I could get maybe 30 or 40 people to come, and I would pay for their steak dinner and their glass of wine and all of that, and it might cost me $10,000. Now I’m getting 100 households coming to a workshop, and I essentially haven’t paid a dime to get them there.”

The school-based workshops do more than bring parents out to gather in the local auditorium or gym. They convert these anxious parents into clients.

Jolly said that 68% of the households that attend his school workshop express interest in a follow-up appointment, and 38% end up doing some type of business with an advisor in his firm.

“They might engage with us to create a fee-based financial plan. Or it could be that they put money into a 529 plan each month, or it could be that they have a

rollover that they want to invest.

“My point is that now you have a client. And whether they do six things with you on Day 1 or they do one thing with you, you have a reason to talk to them.”

Jolly’s college funding practice attracts prospects to the other aspects of his practice the old-fashioned way — through word of mouth.

“Over the years, some of my better clients became business owners, entrepreneurs and executives, so I homed in on how I can have repeat clients who look like this,” he said. “I’ve developed the ability to provide service and value to these types of clients. And interestingly, we do a lot of events with these types of clients where we invite them to bring someone who they think might benefit from the work we do, and then we follow up with them.”

Jolly’s advice to those who are looking for a new way of prospecting is “find a repeatable system for prospecting, where you almost don’t have to think about it.

“Find a system that allows you to focus on the more important thing, which is sitting in front of someone and discussing the strategies, techniques and tools that make sense and are appropriate,” he said.

Jolly cited Ron Carson, founder of Carson Group, who uses the term “passion prospecting.”

“It’s doing work, having fun and using that as a way to leverage relationships and meet people who are good prospects,” Jolly said.

Susan Rupe is managing editor for InsuranceNewsNet.

She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at srupe@insurancenewsnet.com.

Jolly

Bronwyn Martin brings the analytical skills she learned in the scientific field to provide advice to ‘the millionaires next door.’

By Susan Rupe

Ever since she was a little girl in Australia, Bronwyn Martin knew she loved science and wanted to make it her life’s work. But she wasn’t interested in becoming a physician or a nurse — so she turned her sights to research.

Martin is CEO of Martin’s Consulting Group, a financial advisory practice of Ameriprise Financial Services with offices in Kennett Square, Pa., and Havre de Grace, Md. But before entering the financial services field, she spent a number of years as a biochemist and researcher.

Martin’s family moved from Australia to the U.S. when she was a teenager so her father could study at a university. Life in the U.S. wasn’t easy for a teen from overseas.

“I was beaten up a few times because I have an accent,” she recalled. “It was just the four of us who came over to the U.S. — my parents, my brother and I. Life as a teenager was hell. We had no friends or family when we came over here. It was definitely a culture shock.”

After high school, Martin earned a bachelor’s degree in biology and a master’s degree in biochemistry from Boston University. She went on to receive a doctorate in biochemistry from Boston University School of Medicine. She did postdoctoral research at Harvard Medical School, Massachusetts Institute of Technology and the National Institute of Mental Health.

The subjects of her research included the effects of silica on the lungs of coal miners, how the beta amyloid protein is cut out of the precursor protein and the effects of Prozac on cellular metabolism.

But Martin said she was burned out after years of scientific research and needed a change.

“It can be hard to find grant money to fund your research, let alone pay your rent,” she said. “I needed to make a change.”

She had considered getting into the business side of science, hoping to work

on mergers and acquisitions of biotechnology companies, but that didn’t work out. “I thought, ‘I have all these school loans I need to pay off. Maybe I should figure out how to better handle my money.’ Even though I had full scholarships for all my degrees in science, I still had to take out loans for a living. When you’re doing PhD work, it’s 24/7, and there’s really no time to work at a job.”

Getting the call

Martin began working on an MBA and eventually received a call from American Express in 2000 inviting her to work with them. She began her advisory career with American Express, and when the company spun off its financial advisory business in 2005, becoming Ameriprise Financial, she became an independent advisory with Ameriprise.

In her practice, Martin serves a clientele she describes as “the millionaires next door.”

risk of being out of work for an extended period of time due to illness.”

An analytical mind

Martin said her science background is an asset to her financial services career, as it makes her more analytical and inspires her to ask clients more in-depth questions.

Her future plans for her practice include bringing another associate on board and setting them up in an office in New York state, which would expand Martin’s advisory practice to three states.

“2024 was my best year ever, and my practice has been going upward ever since I started,” she said. “I was recognized for being a top producer my first year in business and have been a Million Dollar Round Table Top of the Table member the past five years.”

In addition to her plans to expand her practice, Martin will devote 2025 to serving as president of the National

“It can be hard to find grant money to fund your research, let alone pay your rent. I needed to make a change.”

“They are blue-collar and middleincome families and their children, people who are putting away money and planning for the future.”

“Most of my clients started to save before I ever met with them,” she continued. “But then when we meet, we talk about their goals. And we frame their goals in terms of how long they think they will take to achieve those goals and what they think it will cost. Then I add in the inflation factor and where they are currently in reaching that goal.

“We discuss a lot of long-term stuff. People forget that financial planning also includes having a cash reserve for paying for emergencies or making sure they have enough life insurance. I also make sure they have disability insurance. I need to remind people that their best asset is their ability to get up and go to work every day. So we need to protect against the

Association of Insurance and Financial Advisors-Pennsylvania. She took office in January.

She said she was attracted to NAIFA membership “because I have a passion for advocacy.”

“I go to Harrisburg and I go to Washington every year to talk to legislators as someone who not only represents our industry but as someone who chose to become an American citizen,” she said. “Talking to our elected representatives makes a difference, and I don’t think a lot of Americans appreciate that.”

During her year as NAIFAPennsylvania president, Martin said she wants to hold more continuing education programs and more legislative events. She also wants to encourage more members to attend the association’s political advocacy events in Harrisburg and Washington.

the Fıeld A Visit With Agents of Change

“I want to have more people be on the Hill, because that’s what I’m passionate about. And I think if other people experience that, then they’ll be there every year. So we might want to provide some incentives to some of the new members or new younger members, to maybe pay for their hotel or train costs down to D.C. or something like that. Because I think once you do it, you think, ‘Wow, that was amazing!’”

Scuba diving and soccer

Outside of work, Martin is passionate about scuba diving, fundraising for the Alzheimer’s Association and Manchester United Soccer.

She has gone on dives to Australia’s Great Barrier Reef, to Chuuk Lagoon and Palau in the Pacific Ocean, and to the Cayman Islands, to name a few places. “I like to live aboard yachts in the areas that not many divers go to, to go out there and stay out there,” she said.

Her interest in fundraising for the Alzheimer’s Association stems from her days as a researcher, when the association funded some of her scientific work. She is part of a team called Run to Remember that participates in the

Martin is an avid sponsor of the Alzheimer’s Association and she’s shown here putting in miles in their annual Walk to End Alzheimer’s.

Philadelphia Marathon each year.

As for Manchester United, Martin is such a fan that she actually owns a piece of the team.

“I literally own a piece of the franchise because it’s the only publicly traded sports team in the world. I bought it when it was an IPO, which is not advice I give to my clients. I never tell clients to buy an IPO, but I bought this. I’ve been an owner for more than 10 years now.”

Martin’s advice to women who want to succeed in financial services can be summed up in one word — “perseverance.”

“I came up with a quote for myself many years ago: ‘Successful people get things done. Others make excuses.’ Sometimes I remind myself that you’re only going to be successful because you get it done.”

Susan Rupe is managing editor for InsuranceNewsNet. She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at srupe@insurancenewsnet.com.

Insurance products issued by Minnesota Life Insurance Company

Please keep in mind that the primary reason to purchase a life insurance product is the death benefit.

Product features and availability may vary by state.

Life insurance products contain charges, such as Cost of Insurance Charge, Cash Extra Charge, and Additional Agreements Charge (which we refer to as mortality charges), and Premium Charge, Monthly Policy Charge, Policy Issue Charge, Transaction Charge, Index Segment Charge, and Surrender Charge (which we refer to as expense charges). These charges may increase over time, and this policy may contain restrictions, such as surrender periods. Policyholders could lose money in this product.

Policy loans and withdrawals may create an adverse tax result in the event of lapse or policy surrender and will reduce both the surrender value and death benefit. Withdrawals may be subject to taxation within the first fifteen years of the contract. Clients should consult their tax advisor when considering taking a policy loan or withdrawal.

These materials are for informational and educational purposes only and are not designed, or intended, to be applicable to any person’s individual circumstances. It should not be considered investment advice, nor does it constitute a recommendation that anyone engage in (or refrain from) a particular course of action. Securian Financial Group, and its subsidiaries, have a financial interest in the sale of their products.

Insurance products are issued by Minnesota Life Insurance Company in all states except New York. In New York, products are issued by Securian Life Insurance Company, a New York authorized insurer. Minnesota Life is not an authorized New York insurer and does not do insurance business in New York. Both companies are headquartered in St. Paul, MN. Product availability and features may vary by state. Each insurer is solely responsible for the financial obligations under the policies or contracts it issues.

Securian Financial is the marketing name for Securian Financial Group, Inc., and its subsidiaries. Minnesota Life Insurance Company and Securian Life Insurance Company are subsidiaries of Securian Financial Group, Inc.

For financial professional use only. Not for use with the public. This material may not be reproduced in any way where it would be accessible to the general public.

Introducing Securian

Symetra

reaches $32.5M settlement over COI charges

A group of Washington policyholders are asking a federal judge for preliminarily approval of a $32.5 million settlement with Symetra over cost-of-insurance claims. If approved, the 11-state settlement deal will cover about 43,000 policyholders in the class. The other policyholders live in Arizona, California, Florida, Illinois, Indiana, Kentucky, Minnesota, Missouri, South Carolina and Texas.

Symetra sent InsuranceNewsNet a statement: “We are pleased to have reached a mutually beneficial settlement in the class action involving universal life insurance policies issued in 11 states by American States Life. The settlement is not an admission that Symetra did anything wrong. Rather, the settlement avoids prolonged litigation, and allows us to continue our focus on serving our customers.”

Original plaintiff Dennis E. Davis, of Des Moines, Iowa, purchased a $100,000 adjustable life policy from American States Life Insurance Co. on Sept. 16, 1987, the complaint states. Symetra took over American States in 2005. The terms of the policy authorized Symetra to deduct cost-of-insurance expenses from the cash value on a monthly basis. Terms permitted the insurer to use only the insured’s age, sex, rate class and the expectations as to future mortality experience to determine cost-of-insurance rates.

Plaintiffs were completely unaware that they were allegedly being shorted on the value of their policies, the lawsuit claims.

NATIONWIDE TEAMS UP WITH BESTOW

Nationwide has teamed up with Bestow’s technology platform to streamline term life insurance solutions. Since Nationwide launched its Life Essentials in April 2023, the company’s partnership with Bestow has expanded access to life insurance, particularly in underserved markets, the insurer reported. Nationwide saw a 20% increase in term life sales as a result.

Nationwide Life Essentials delivers instant quotes and automated underwriting, eliminating the need for medical exams and enabling customers to receive coverage decisions within minutes.

The insurer said it has more than doubled application completion rates,

helping families secure necessary coverage. Notably, 69% of applicants over the past 18 months were first-time life insurance buyers , demonstrating the partnership’s success in reaching traditionally underserved consumers.

PRUDENTIAL, DAI-ICHI LIFE EYE PARTNERSHIP

Prudential Financial and Dai-ichi Life Holdings announced they intend to pursue a strategic partnership focused on product distribution and asset management capabilities

The partnership would include a product distribution agreement in Japan, where Prudential would select Dai-ichi’s wholly owned subsidiary, The Neo First

36% of Generation Z says they own

IULs are a long-term play, and making sure clients understand this will go a long way to ensuring you keep your clients for a long time.”

— Drew Gurley, Redbird Advisors

Life Insurance Co. Ltd. as an exclusive product partner. The partnership would include distributing certain Neo First life products through Prudential’s Life Planner sales channel.

In addition, PGIM, Prudential’s global investment manager, intends to provide asset management services to subsidiaries of Dai-ichi Life Holdings through its PGIM Multi-Asset Solutions business. These services would include management of asset classes such as structured products and private credit.

TWO FRATERNALS PLAN TO MERGE

BetterLife and CSA Fraternal Life have announced plans to merge, forming one fraternal benefit organization with roots in the Czech-Slovak community

The two Midwest-based insurance providers will merge in 2025, pending approval by CSA delegates and regulatory authorities.

The two organizations have complementary membership footprints, a focus on community wellness and a strong Czech–Slovak heritage.

CSA Fraternal Life is the nation’s oldest active fraternal benefit society, established in 1854 with its home office in Lombard, Ill. It has a membership of 16,000 with 59 lodges in 21 states. BetterLife was established in 1897 and has its home office in Madison, Wis. Its 55,000 members are located among 81 lodges in 20 states.

Verhille and Associates ascended to the top of Kansas City Life Insurance Company by winning the Agency Building Award (ABA) for 2024. The agency achieved the ABA Honorable Mention in 2003, 2006, 2010, 2011, and 2016. Agent Andrew Verhille accepted this award on behalf of the agency. Pictured from left: Agent Andrew Verhille and President, CEO, and Vice Chairman of the Board Web Bixby. 2024 Agency Building Award winner

The Agency Building Award is Kansas City Life Insurance Company’s most prestigious agency honor, bestowed only to agencies that embody the spirit of entrepreneurship, growth, and building for the future.

“Winning the Agency Building Award has always been a coveted career achievement for those affiliated with Kansas City Life Insurance Company. Being the third generation to represent Kansas City Life as a General Agent, I am extremely honored to be receiving this award.”

— General Agent Dave Verhille, CLU, ChFC Verhille and Associates

Verhille and Associates

500 1st St. SE Cedar Rapids, IA 52401

Key person insurance: A vital tool for startups

Startup founders may have a lot on their plates as they begin their new venture, but they need this type of coverage.

By Jonathan Selby

Key person insurance, or contract frustration insurance, is a crucial risk management strategy for startups that rely heavily on specific individuals for their success. This type of insurance provides financial protection in the event of a key employee’s death or disability, ensuring business continuity and mitigating potential financial losses. Let’s review how this policy can best serve early-stage businesses.

Understanding key person insurance

Key person insurance is a type of life and disability insurance that covers a business against the financial loss it would suffer if a key employee were to die or become disabled. It’s particularly important for

companies heavily dependent on specific individuals for their success.

The policy pays the business a set amount if the key person dies or becomes unable to work due to disability. The business is the policy owner and beneficiary, paying the premiums and receiving the benefits. The insured amount is usually based on the key person’s value to the business.

For startups, key person insurance offers several benefits. It provides financial stability during a chaotic transition period and covers the costs of finding and training a replacement. The coverage can also be used to buy out the key person’s shares if needed or repay debts that may be called upon their death or disability.

Not having key person insurance puts startups at risk. The unexpected loss of a key team member could mean project delays, lost clients or even business failure. Investors and lenders often require key person insurance as a condition of funding, so not having it could stop a startup from getting the capital it needs to grow and operate.

Identifying key employees

Criteria for identifying key employees include their unique skills, specialized knowledge, leadership abilities and direct impact on company revenue or operations. Key employees often have irreplaceable expertise and strong client relationships or play crucial roles in product development or strategic decision-making. They may also be founders or top executives whose vision and guidance are integral to the company’s success.

Company leaders must evaluate both the immediate and the long-term impact of losing a key employee. Consider how their absence would affect daily operations, ongoing projects, client relationships and overall company direction. Remember to analyze the time and resources needed to find and train a suitable replacement. Lastly, don’t forget about losing business or market share during this transition period.

Quantifying the financial value of a key employee requires a diverse approach. Start by calculating their direct contribution to revenue or cost savings.

Remember to factor in the cost of recruiting and training a replacement, estimated at 1.5 to three times the employee’s annual salary.

Also consider potential lost business opportunities and the impact on company valuation. Assess the projected decline in company performance without their expertise for highly specialized roles.

Key person insurance coverage options

Term life insurance is a popular choice for key person coverage. It offers a death benefit if the insured individual passes away during the policy term. It’s cost-effective and provides straightforward protection for a specified period.

Disability insurance complements life coverage by protecting the company if a

disabled owner’s share of the business. This approach ensures a smooth ownership transition and provides liquidity to the departing owner’s estate.

Combination policies merge multiple coverage types, such as life and disability insurance, into a single contract. These can offer more comprehensive protection and lower costs than purchasing separate policies.

Each option has its merits, and the ideal choice depends on the company’s specific needs, budget and risk profile. A thorough risk assessment can help determine the most suitable coverage strategy.

Factors affecting key person insurance premiums

The insured’s age and health matter. Younger, healthier key persons get lower

3 groups that benefit from key person insurance in a startup business

1. Investors: Key person insurance provides security that can be used to attract new investors and ease the concerns of existing investors.

2. Company: The payout can soften the blow of the disruption to operations by assisting with some of the costs associated with the loss.

3. Team: Uncertainty about job security is the last thing a business team should be worried about following a loss.

key person cannot work due to illness or injury. It can provide funds to cover temporary replacement costs or compensate for lost revenue.

While not insurance policies themselves, buy-sell agreements often incorporate life and disability insurance to fund the purchase of a deceased or

premiums because of lower mortality risk. Insurers often require medical exams or health questionnaires to assess this risk accurately.

The coverage amount is directly tied to the premium cost. Higher coverage limits mean higher premiums. Companies must balance protection with budget

when deciding on coverage amounts. Policy type affects pricing. Term life policies are generally more affordable than permanent life insurance. Disability or combination policies may be more expensive but offer more coverage.

Company size and financial strength play a role in premium cost. More oversized, established companies may get lower rates because of perceived stability and better risk management. Startups or smaller firms may get higher rates because of more uncertainty.

Industry and related risk factors are also crucial considerations. Tech startups or companies in high-risk industries may get higher rates because of more volatility and faster changes in key person value, while companies in more stable industries may get lower rates.

Insurers also consider the key person’s specific role and responsibilities. Executives or individuals with unique, hard-to-replace skills may get higher rates because of their bigger impact on the company’s success.

Knowing these factors will help your business clients make informed decisions when choosing key person insurance coverage, balancing protection needs with cost.

Best practices for key person insurance

You and your business clients must review and update the policy regularly. The coverage amounts should be in line with the key person’s current value. Have your client name beneficiaries carefully and consider changes to the business structure.

Beyond insurance, have your business clients consider other risk management strategies. Succession planning can reduce the impact of a key person’s absence, and business continuity plans can cover broader operational risks. You can help your business client tailor these plans to their specific needs.

Key person insurance is a living instrument. Review and manage it regularly with your business clients to protect their businesses and the clients themselves.

Jonathan Selby is technology practice lead at Founder Shield. Contact him at jonathan.selby@ innfeedback.com.

ANNUITY WIRES

2024 retail annuity sales set $432B record, LIMRA reports

Americans kept up the annuity buying spree throughout 2024, resulting in total sales of $432.4 billion, up 12% yearly, according to preliminary results from LIMRA’s U.S. Individual Annuity Sales Survey.

It marks the third consecutive year of record-high annuity sales. Annuity sales were $313 billion in 2022 and $385 billion in 2023.

Lower interest rates in the second half of the year undermined demand for fixed-rate deferred and income annuities. Fixed-rate deferred annuity sales totaled $153.4 billion for the year, a 7% drop from 2023.

Other than that, all products did well. Fixed indexed annuity sales totaled $125.5 billion, up 31% from the prior year. Registered index-linked annuity sales reached $65.3 billion in 2024, 37% higher than prior year.

Traditional variable annuity sales grew 19% to $61.2 billion. It marked the first increase for VAs in three years.

PENSION RIGHTS CENTER SAYS SWAPPING PENSIONS FOR ANNUITIES A TRICKY GAME

The continued transfer of pension funds to annuity sellers threatens the viability of the American retirement system if left unchecked, the Pension Rights Center said in an amicus brief filed recently.

A nonprofit consumer advocacy group, the PRC intervened in a Massachusetts lawsuit filed by AT&T retirees.

The lawsuit is one of two accusing AT&T and its independent fiduciary, State Street Global Advisors Trust Co., of taking on too much risk when it selected Athene Annuity and Life Co. to conduct its $8.05 billion pension risk transfer in May 2023.

Nearly 100,000 former AT&T employees are relying on the company pension fund

for their retirement, the lawsuit states.

An Athene spokesperson said the complaints are “entirely baseless attempts by class action attorneys to enrich themselves at the expense of retirees. Every pension group annuity participant whose benefits have been guaranteed by Athene has received and will receive their promised benefits in full.”

ALLIANZ PARTNERS WITH MORGAN STANLEY TO OFFER ANNUITY PRODUCTS

As consumer demand for annuities keeps rising, Allianz Life Insurance Co. of North America inked a partnership deal with Morgan Stanley to offer its products to a bigger audience.

Five Allianz annuity products are now available through more than 16,000 Morgan Stanley financial professionals. Available products include four Allianz registered index-linked annuities and one fixed indexed annuity.

— Bryan Hodgens, senior vice president and head of LIMRA research

“With our industry leadership and more than a decade of experience in the RILA market, we are ready to help Morgan Stanley grow in the space,” said John Helmen, vice president of distribution national accounts, Allianz Life.

AMERILIFE GROUP ACQUIRES CRUMP LIFE INSURANCE SERVICES

AmeriLife Group recently acquired Crump Life Insurance Services and Hanleigh Management from TIH Insurance Holdings in a bid to expand its life insurance and annuity reach. Per the agreement, terms of the deal were not disclosed.

“We are thrilled to welcome Crump into the AmeriLife family,” said Scott R. Perry, chairman and CEO of AmeriLife.

“Crump is a leading independent distributor of life insurance, and this partnership aligns perfectly with our vision to provide enhanced wealth solutions for our clients and partners.”

Crump is one of the largest providers of life insurance and retirement products in the United States. Crump’s footprint spans the institutional/wholesale, IMO, and BGA sectors, and it partners with more than 31,000 financial professionals to deliver a range of holistic solutions including life, annuities, long-term care, linked benefit, disability insurance and other specialty offerings.

Perry

Securing income through a fully insured plan

Fixed annuity contracts can fund a type of defined benefit plan for business owner clients.

By Ernest J. Guerriero

Your business owner prospect or client has spent years navigating the highs and lows of running a business. Now, when it comes to their own financial future, they need to make up for lost retirement savings. At this point, they are also looking for predictability with their retirement plan more than anything else. The goal is to turn the business into a steady stream of income. However, many business owners do not have a plan where they can choose the benefit (sale price), choose the time (when to sell) and choose who will buy (a willing buyer).

What if there were a plan that provided a guaranteed lump sum offering a steady stream of income and no market volatility,

at the time to be chosen by the owner, with no stress finding a buyer and a relatively large tax deduction? Solution — the fully insured plan!

A fully insured plan, or 412(e)(3) plan — for those who have been around, a 412(i) plan — is a type of defined benefit plan that must be funded by fixed annuity contracts or a mix of fixed annuities and life insurance. This funding shields the plan’s assets from market volatility, securing your client’s future income — predictably. Administration is simple and exact, and owners may contribute a substantial amount, offering larger tax deductions than a profit-sharing 401(k) plan or a 403(b) plan.

A fully insured plan is a way to provide those business owner clients who are making up for lost retirement income planning with the confidence and peace of mind that those funds will be there no matter what the market is doing, when they are ready to begin receiving their income. Not only does this strategy work in

the for-profit world, but it also works for those in nonprofits.

A fully insured plan is a qualified defined benefit plan. Like all qualified defined benefit plans, it must meet certain minimum requirements prescribed by law. Furthermore, a fully insured plan differs from other traditional (defined benefit) pension plans with respect to the method of funding. A fully insured plan must be funded solely through life insurance contracts (fixed annuity or a combination of fixed annuity and life insurance).

In addition, just like other qualified defined benefit plans, it must meet the coverage, participation, nondiscrimination, top heavy, benefit limits and incidental (death benefit) rule required by law.

Qualified retirement plans, including fully insured plans, may be designed in a variety of ways provided they do not discriminate in favor of highly compensated employees. In 2025, an HCE is anyone who is compensated more than $160,000 or owns more than 5% of the business. In

order not to violate the nondiscrimination requirements, the IRS has provided certain guidelines and tests as well as safe harbor provisions that may be used by plans for compliance purposes, though they are beyond the scope of this article.

To summarize, the client who is a best fit for a fully insured plan is one who

» is looking to play catch-up with their retirement income planning;

» would like a larger tax deduction;

» is committed to making contributions each year;

» values a plan with guarantees, with a guaranteed retirement benefit;

» may be looking for a plan that may be self-complete, providing for survivor income;

» is generally older and being compensated more than rank-and-file employees; and

» pairs well with an existing profit-sharing 401(k) plan or 403(b).

A case study will show how the fully insured plan prepared for Debra, a sole owner, carried out the goals of providing a catch-up plan for retirement income, providing a large tax deduction, and offering a valuable employee benefit. In addition, the solution also provided a benefit for a key employee. The employer has met the profile captioned above. The census is shown below.

At retirement, age 65, here’s what they receive:

Debra Owner 7/6/1969 3/12/2018

Devon Staff 5/16/1994 3/12/2018 $42,000

Tom Staff 3/7/1996 3/12/2018 $42,000

Diane Staff 11/8/1987 3/12/2018 $37,440

Sam Staff 6/2/2001 3/12/2018 $24,000

The solution is a fully insured plan.

$1,202,405

$868,403

$835,004

$625,251

$701,403

Debra received a large tax deduction, saving her $134,078 (in a combined 40%) in taxes; provided for her survivors with a permanent death benefit of more than $2.2 million, a portion of which remains income tax-free, and achieved her retirement income goal safely with more than $1.5 million with no market volatility (which may be used to fund an income annuity of approximately $7,500 per month for life, which will supplement her other savings from a profit-sharing 401(k) plan and the eventual sale of the business).

In addition, it was discovered that Paul is a key employee who eventually is targeted to take over this business; therefore, his contribution will be factored into the buy-sell arrangement and other nonqualified arrangements that are in place or will be established. In your next review or prospecting conversation, ask, “What guarantees are currently in your portfolio?” “How much of your future financial income is guaranteed?” “Are you looking for larger tax deductions today?” and “Are you concerned about the market’s impact on your retirement income?”

Ernest J. Guerriero, CLU, ChFC, CEBS, CPCU, CPC, CMS, AIF, RICP, CPFA, is the past national president of the Society of Financial Service Professionals and currently a board trustee for the National Association of Insurance and Financial Advisors. Contact him at ernest. guerriero@innfeedback.com.

HEALTH/BENEFITSWIRES

FTC goes after prescription drug middlemen