Shooting for the Stars — with Augustar’s Cliff Jack

PAGE 8

Playing the long game — with Ronnie Kaymore

PAGE 12

Your client wants to borrow from their life insurance. Now what? PAGE 22 In-plan annuities are picking up steam PAGE 26

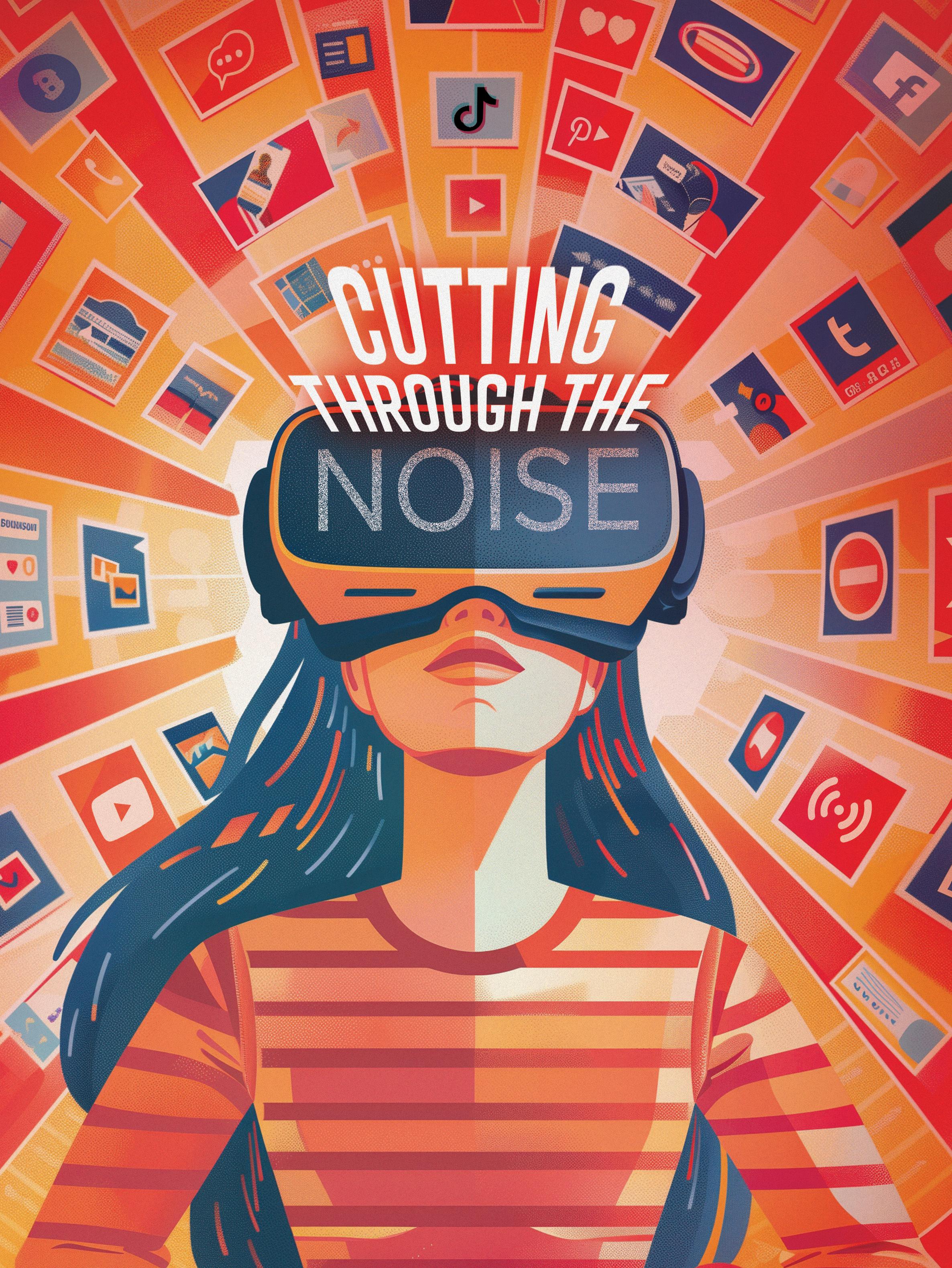

The younger generations can get caught up in unrealistic investment ideas they find on social media. For advisors, the challenge is to cut through the noise and help them set realistic expectations.

16

Foresters Financial –focused on what’s next

Through digitized solutions, advanced underwriting and an amazing suite of member benefits, Foresters is rapidly expanding the opportunity for independent agents.

The Foresters Financial™ fully digital process

Mobile quotes e-Applications

Certificate details

BizApp

Quick POS decisioning

Quick POS decisioning

Quick certificate issue

Scan to get the facts

Put your client’s retirement income dollars on the right path

Set yourself apart from the competition by providing your clients a guaranteed income for life with Kansas City Life Insurance Company’s Lifetime Income Rider that:

• Offers 7.2% guaranteed increase to Lifetime Income Amount for the first 10 rider years if no withdrawals in years 1 – 10.

• Provides a secure, guaranteed retirement income stream for life.

• Helps clients grow their retirement savings with a competitive fixed interest rate.

• Protects the value of a fixed annuity during market turmoil.

• Allows clients the ability to maintain the flexibility and control of their deferred annuity contract even after they start receiving income.

The Lifetime Income Rider provides guaranteed income for life and is an optional benefit available on all of Kansas City Life’s fixed annuity portfolio.

For information about a career with Kansas City Life Insurance Company, call Dwane Turnage, Vice President, Marketing, 855-277-2090

IN THIS ISSUE

INTERVIEW

8 Shooting for the stars

AuguStar’s president and CEO Cliff Jack has been on the job for only 18 months, but he sees upside potential ahead for his company. In this interview with publisher Paul Feldman, Jack describes how his company is starting fresh with a new team and a new brand.

IN THE FIELD

12 Playing the long game

By John Hilton

Ronnie Kaymore traded in the football field for an agent’s license.

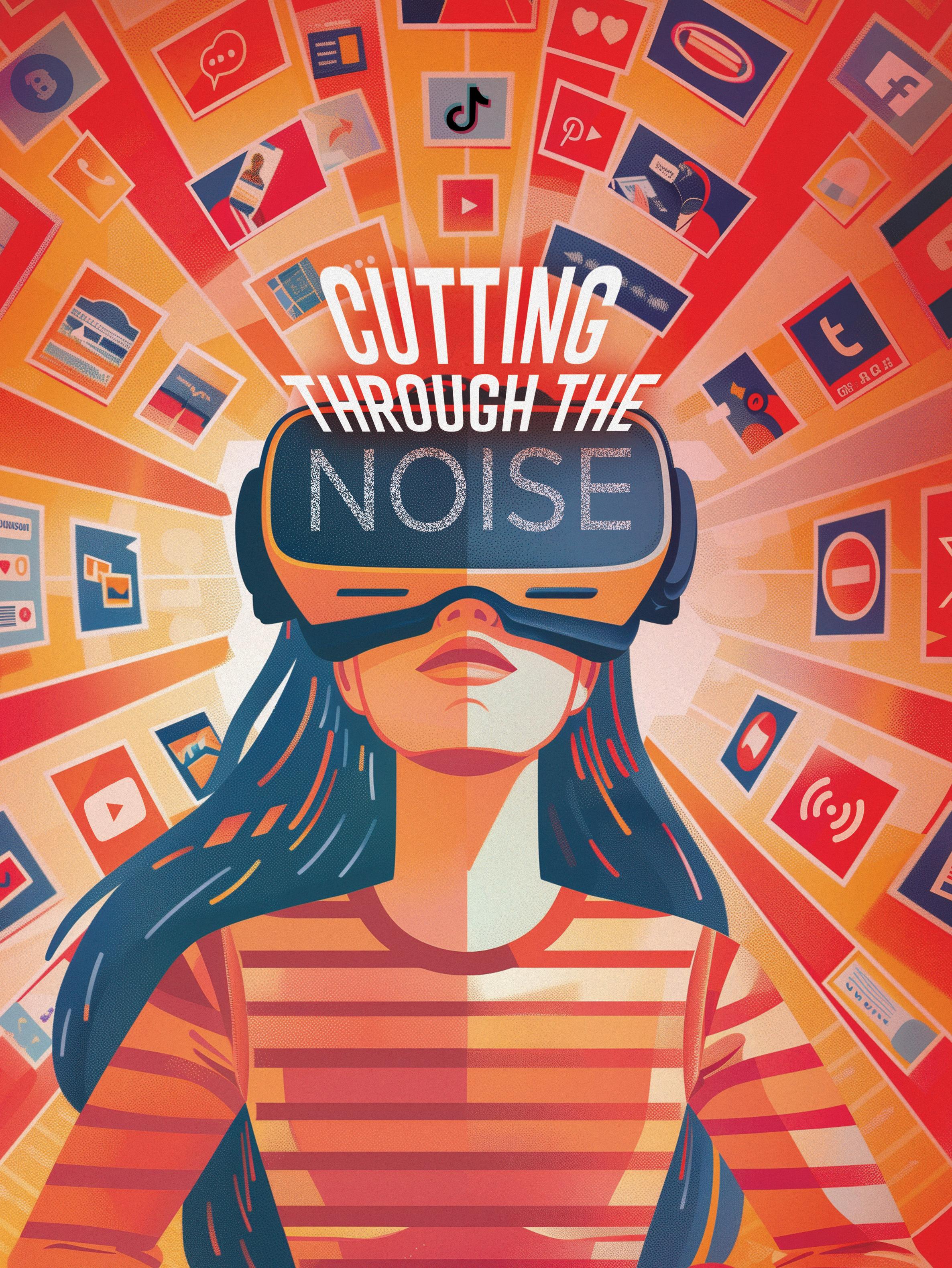

FEATURE Cutting through the noise

By Doug Bailey

Advisors

HEALTH/BENEFITS

30 Protecting clients amid the ‘triple threat’ in LTC services By Larry Nisenson

Why it’s critical to discuss the need for long-term care with clients.

ADVISORNEWS

14

We

22 When your client wants to borrow from their life insurance

By Lyle D. Solomon

The benefits and drawbacks of borrowing from a cash value policy.

ANNUITY

26 In-plan annuities picking up steam

By Susan Rupe

Annuities are becoming more common in defined contribution plans, but where do they go from here?

INSURANCE & FINANCIAL MEDIA NE TWORK

John Forcucci

34 Should you recommend a CLAT or a reversionary CLAT in wealth planning?

By Derek Miser

Exploring the nuances between charitable lead annuity trusts and reversionary charitable lead annuity trusts.

IN THE KNOW

36 Retirement success? Plan for a marathon and not a vacation By Susan Rupe

The three Ps that will guide your client to a successful life in their post-employment years.

Financial services for the next gen

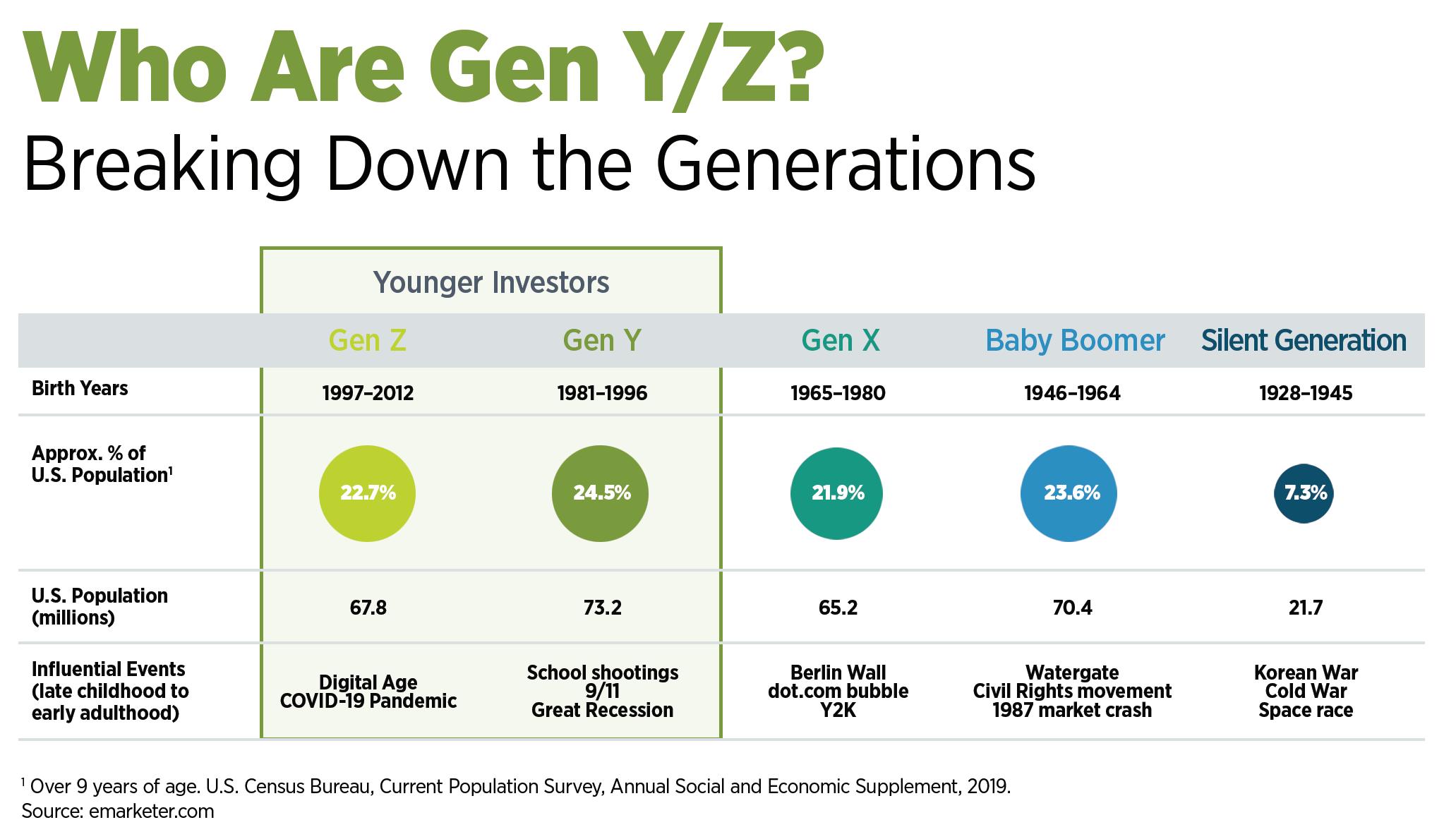

Financial advisors are at a crossroads. The industry is evolving rapidly, driven by technological innovation and changing consumer behaviors. As a member of the baby boomer generation, I have seen it all — from paper-based marketing, sales and purchasing transactions to seeing my financial information on a single dashboard with live updates and doing Zoom calls with my advisor. Younger generations — Generation X, millennials, and Generation Z — are playing a key role in reshaping the demand for financial services. Understanding their distinct financial habits and preferences is crucial for advisors who aim to remain relevant in this dynamic landscape.

Gen X: Bridging traditional and digital finance

The generation that followed the boomers, Gen X (those born between the mid-1960s and early 1980s), has witnessed the digital revolution firsthand. This generation balances traditional financial practices with a growing acceptance of digital solutions. They are also the first generation to retire under the shift to 401(k)s. Many are currently rethinking their retirement and may end up working longer than they had originally planned. Gen Xers generally are comfortable managing their investments online but also value the personal touch of human advisors, particularly for complex financial decisions such as estate planning or retirement strategies.

For financial advisors targeting Gen X, understanding their retirement concerns and blending digital convenience with expert, personalized advice can be a winning strategy.

Millennials: The tech-savvy investors

My older daughter’s generation, millennials, born from the early 1980s to the late 1990s, are the first truly digital-native generation. They grew up in an era of smartphones and social media, which influences their approach to finance. Many millennials prefer using apps for daily transactions and are comfortable using online platforms for investing through robo-advisors such as Betterment or Wealthfront. These tools offer a low-cost, accessible entry point to investing, aligning with millennials’ preference for efficiency and autonomy. However, the personal element also is not lost on this generation — most still seek financial advisors for major financial decisions or when navigating life changes such as buying a home or planning for a family. For advisors, offering a mix of high-tech solutions and high-touch personalized guidance could effectively meet the nuanced needs of millennial clients.

Gen Z: The future of finance

My younger daughter’s generation, Gen Z (born from the late 1990s through the 2010s), is entering their financial formative years with even more technological fluency than millennials. This generation is

more likely to use digital wallets and invest in cryptocurrencies. They are drawn to platforms that offer instant, transparent and mobile-first services, reflecting their preferences for immediacy and innovation. While I had preached saving and investing to my kids from an early age, my younger daughter took that advice and signed up to start investing online. The service she used offered both human advisors and a robo-advisor component.

Studies have shown that Gen Z shows a surprising interest in financial literacy, expressing a keenness to learn about managing and investing money effectively. This is certainly true of both of my daughters. This opens an opportunity for advisors to engage through educational content delivered via platforms that resonate with this generation, such as YouTube or Instagram.

The crucial role of human advisors

Across generations, while the adoption of digital tools is high, the importance of human advisors remains significant. Most young people still recognize the value of personalized advice, especially for complex financial situations that require expert understanding or a strategic approach. Financial advisors are increasingly expected to offer more than just investment guidance — they must be coaches, educators and partners in their clients’ financial journeys.

Adapting to serve the next generation

The financial services industry must continue to adapt by integrating technology with traditional advisory services. Embracing technological solutions — including artificial intelligence — that automate routine tasks can free up advisors to focus on providing strategic, tailored advice where they add the most value.

For financial advisors, the challenge is to understand and embrace the diverse preferences of younger generations. By leveraging technology and maintaining the irreplaceable human element, advisors can meet the evolving needs of Gen X, millennials and Gen Z.

John Forcucci Editor-in-chief

What does a successful 150-year-old fraternal life insurance company do for a next chapter? It does what it’s always done — it focuses on what’s next.

“You get to celebrate your 150th anniversary by being entirely focused on the future,” said Matt Berman, CEO of Foresters Financial. “We were founded on the spirit of innovation, with the goal to provide protection with a purpose that meets the ever-changing needs of the marketplace. Today, the spirit of innovation at Foresters Financial is as strong as ever.”

Mr. Berman added: “Through the use of data, technology, and advancements in underwriting, we’re going full speed to help shape the future of life insurance and the customer journey.”

Faster, easier, and seamless: What’s next at Foresters Financial

End-to-end process improvement to accelerate the journey to approval

Foresters knows what agents want: easier and faster approvals. That’s why the company is dedicated to improving the life insurance sale process from end-to-end through a combination of world-class tech platforms.

On the front end, Foresters has implemented a reflexive application that provides structured data to underwriting engines. This optimizes Foresters straight through application process leading to faster point-of-sale decisions with the goal of improving approval rates.

Using risk scoring as its underlying underwriting, Foresters is able to evaluate mortality risk that places greater emphasis on relative mortality — significantly expanding the market opportunity for independent

“Through the use of data, technology, and advancements in underwriting, we’re going full speed to help shape the future of life insurance and the customer journey.”

— Matt Berman, CEO of Foresters Financial

Driving the opportunity for independent agents by making it easier and faster

Using a combination of digitized solutions, product design, and member benefits unique to a fraternal insurer, Foresters is focused on making it easier and faster for more independent agents to provide financial security to everyday families, including those that may not have qualified for coverage in the past. The end goal: create more opportunity for agents to grow their business.

New independent agents: JIT to success

It starts by simplifying the agent appointment process. Foresters has created a new digital licensing program it calls JIT — Just In Time — that allows agents to get appointed quickly and easily.

The simplified online registration process only requires completing a short form to obtain an independent agent code within minutes. This enables new agents to write business before contracting paperwork is submitted to Foresters for processing.

agents by giving more people a chance to qualify for life insurance; including those who may not have in the past.

“Risk scoring is a dynamic approach that analyzes data in real-time, with observations based on multiple characteristics or attributes. This modeling helps us look beyond classic negative mortality risk toward other factors that can improve someone’s profile and increase eligibility,” said Doug Parrott, Chief Underwriting Officer — North America.

Expanding markets to give independent agents more opportunity

To understand what’s next you need to listen to the market. That’s helped Foresters continuously provide agents with innovative products that address all life stages and new markets. From its early success with one of the most unique final expense products, to being an early adopter and eventual leader of non-medical “fluidless” solutions, to its contemporary children’s whole life — when Foresters spots an opportunity, it can move fast.

For instance, in 2023, independent agents were increasingly talking to Foresters about life insurance solutions for the ITIN (Individual Taxpayer Identification Number) market. Given the company’s commitment to expanding markets by providing life insurance to more people in need, Foresters quickly developed its ITIN program with a customized set of parameters so independent agents can help more potential clients.

Recognizing the demand for life insurance for people living with diabetes, Foresters launched an industry-first in the US: Non-medical life insurance products built with diabetes in mind. This includes relaxed underwriting on non-medical products offering up to table 6 ratings at no additional premium — and one product that goes from table 7 to 12 ratings. This way, more people living with diabetes can apply for life insurance — once again expanding the market opportunity for agents.

Similarly, Foresters has a game-changing approach to tobacco: The use of cigars, pipes, chewing tobacco, nicotine patches, vape pens, marijuana and other substitutes fall under non-tobacco definitions for one product.

“Have you ever met a 150 year old that moves as fast as we do?” Mr. Berman said.

The digital journey accelerates member engagement

Foresters recently launched its robust MyPolicy platform, which is a milestone on the Foresters digital adoption roadmap.

MyPolicy is a self-serve portal that allows policy owners to access and manage their accounts. They can view policy details, initiate transactions and complete specific service-related activities.

Importantly, via MyPolicy policy owners can initiate loan and repayment requests. Foresters has made arrangements to provide a digital disbursement program so members can receive funds quickly and securely into their accounts electronically.

Benefits: the fraternal advantage that makes a difference

“When you consider how we are giving agents a competitive advantage through product innovation, advanced underwriting, and tech-driven end-to-end sales, then our member benefits are the icing on the cake,” Mr. Berman said.

The Foresters fraternal purpose is to enrich the well-being of its members, their families, and their communities. This has propelled the insurer to deliver a modern suite of complimentary member benefits including the Foresters Go™ wellness app, education and career advancement funding, and community grants that empower members to support the local causes and organizations they believe are most important. In this way, members and agents can make a difference in their communities.

150 years of financial stability

Foresters Financial is proud of its financial stability. For the past 23 consecutive years, A.M. Best Company has affirmed The Independent Order of Foresters (IOF) Financial Strength Rating (FSR) of “A” (Excellent) with a stable outlook. A.M. Best Company also affirmed an issuer credit rating (ICR) of “a+” for the entity.

Member benefits are a source of pride at Foresters: they reflect the insurer’s larger purpose of giving back that it was founded on 150 years ago.

Mr. Berman said: “Our founders had a vividly clear vision of what mattered in society. That vision is as relevant today as it ever was. We celebrate those who share in our purpose of giving back — the volunteers who are our members, employees, and agents we serve.”

What’s next?

According to Mr. Berman, what’s next is faster, easier, and seamless.

“That’s what the market is telling us,” he said. “Fluidless is a great advantage, but what else can we do to get to instant decision and issue? That’s the entire focus of our digital strategy driving our new product pipeline and approval process. I invite agents who want to accelerate their growth to join us, because this 150 year old is moving fast.”

For more information please scan the QR code to visit ezbiz at Foresters today.

Foresters member benefits are non-contractual, subject to benefit-specific eligibility requirements, definitions and limitations and may be changed or cancelled without notice or are no longer available. Some of these benefits may be administered by third parties such as Foresters Go, which is operated by dacadoo AG.

Foresters Financial, Foresters, Helping Is Who We Are, Foresters Care, Foresters Moments, Foresters Renew, Foresters Member Discounts, Foresters Go and the Foresters Go logo are trade names and/or trademarks of The Independent Order of Foresters (a fraternal benefit society, 789 Don Mills Road, Toronto, ON, Canada M3C 1T9) and its subsidiaries.

For producer use only. Not for use with the public. 423407 US (05/24)

Washington state LTCi program faces ballot threat

A unique benefits plan in Washington state to provide public long-term care insurance for residents is in danger of dying on the vine by a November ballot question that would allow voters to opt out of the groundbreaking program.

The state in 2019 approved the first-in-the-nation Washington Cares program and last year began collecting a 0.58% payroll tax from employees to support the plan. The Washington Cares plan would provide aging individuals with $36,500 over their lifetime for long-term care costs.

Since then, 14 other states are considering adopting similar plans to help with the need for access to long-term care insurance, the cost of which is exploding.

Supporters of the ballot referendum, Initiative 2124, say they only want to make participation in the insurance plan voluntary, rather than mandatory. Critics, including the hedge fund manager that bankrolled the initiative, Brian Heywood, also say the tax is too high and the benefits too low. The state sponsor of I-2124, Republican Rep. Jim Walsh, said he only wants to allow people to opt out of the benefit plan, which he says is already insolvent.

INSURERS URGED TO BE READY FOR OZEMPIC CRAZE

“Oh-oh-oh Ozempic,” may be the latest earworm coming from TV commercials, but with weight-loss drugs like Ozempic rising in popularity across the U.S., credit rating agency Morningstar DBRS says insurers need to talk with their clients to determine coverage solutions

In the short term, insurance carriers should speak to their group benefit insurers, clients and client sponsors about whether they want to offer that coverage as a benefit — and under what conditions coverage for Ozempic and similar drugs should be offered, said Patrick Douville, vice president, North American Insurance Ratings, Morningstar.

Douville noted that a critical point of discussion will be whether GLP-1 drugs are covered specifically for diabetes or just for weight loss. Currently, many insurance plans either do not cover them or only cover them for diabetes, which

the drugs are primarily designed to treat. He said insurers will have to deal with the challenge of clients attempting to get a diabetes diagnosis just to get coverage. In some cases, he suggested, insurers may have to “police” claims to determine which are real diabetes claims and which are not.

MOST AMERICANS BELIEVE WE’RE IN A RECESSION

Even though gross domestic product has been on the rise for several years, more than half of Americans believe the U.S. is in a recession, a Guardian/Harris poll reported.

A recession is an extended period of economic decline, usually designated when GDP has declined for two or more consecutive fiscal quarters. Under those terms, the U.S. is not in a recession. But that means little to consumers, who are still struggling with high costs of living caused by stubbornly high inflation.

U.S. GDP grew by 1.6% in the first quarter of 2024 and has been outpacing that of other developed nations.

QUOTABLE

The highest gift we can give to our clients is the confidence that no matter what happens in Washington, their retirement will be secure.”

— Becky Ruby Swansburg, CEO of Stonewood Financial

STUDENT DEBT MAY HURT OLDER WORKERS’ RETIREMENT SECURITY

Older workers who are still carrying student loan debt may have a harder time saving toward retirement. The bottom 50% of older earners owe the highest average student loan debts, research from the Schwartz Center for Economic Policy Analysis at the New School for Social Research found.

The research evaluated more than 2.2 million people over age 55 with outstanding student loans. That includes more than 1.4 million workers and more than 820,000 unemployed people aged 55 and over who had taken out student loans for themselves or their spouses. The data does not include older Americans who have taken on student loan debt on behalf of their children.

Half of the borrowers over 55 and still working were earning less than $54,600/ year. For older workers aged 55 to 64, it may take an average of 11 years to pay off their student loans, according to the research. Workers 65 and up may need 3.5 years.

SHOOTING FOR THE STARS...

Less than 18 months after taking the helm of AuguStar Reitrement, President and CEO

Clifford

Jack touts the firm’s success … as well as the unlimited upside he sees going forward.

In July 2023, Constellation Insurance announced it had purchased Ohio National, which had run into some turbulence in 2018, and was changing its name to AuguStar.

“The CEO of Constellation, our holding company, called and had a story that was too good to say no to,” said Clifford Jack, president and CEO of AuguStar Retirement. “I tried to say no a bunch of times. In fact, I even recommended other people for the job. But he was pretty persistent, and I had the opportunity to meet with the board. And the board had great passion for what is now AuguStar. By the time that I joined, the company had already purchased the old Ohio National.

“Our job was to hire a new team. If you look at the team, everybody is new; the ownership structure is new, the brand is new, there’s no one left from the senior management team. We tried to start fresh, and it has been very successful. The brand has started to get significant traction in the market. We’ve had wonderful success in terms of brand adoption, but also in product and platform adoption with our new strategies and our new products. We’re pleased with the success that we’ve had so far.”

Jack said, “I stumbled into the industry because my dream of becoming an NBA point guard was cut short by lack of ability and lack of ambition. I interned for a bunch of different brokerage firms when I was in college. All the ones that I wanted to go to turned me down. I ended up with Dean Witter. And at that time, I launched my career in the illustrious Sears, Roebuck stores.”

At the start of his career, Jack described himself as “a financial advisor whose directions to the washing machines were probably better than my financial advice.”

In this interview with InsuranceNewsNet Publisher Paul Feldman, Jack describes how all that changed, though, with a rise to the top and many successes over the course of his career.

Paul Feldman: Tell me a bit about your history in the business. How did you get into the industry?

An interview with Paul Feldman, publisher

Cliff Jack: I graduated from school a little early, and so I was at the ripe age of 21 when I got my Series 7 and started to

We now have what I would call two of the three legs of the stool available from a product standpoint. We have traditional fixed annuities in the form of MYGAs, and we have FIA products across all channels, institutions and IMOs.

give financial advice. I ended up working for one of my largest clients who, at the time, was running a bank financial services organization. In those days, the back offices for brokerage firms and insurance operations were outsourced to third-party marketing companies and broker-dealers. And so that was how I moved away from the advisor’s business and into a management type of a situation.

That led me to work for a company that is no longer in existence, SunAmerica. I was hired by the president of SunAmerica, who called me and said, “Hey, I want to talk to you.” I didn’t know many presidents at the time, and so it was a great opportunity for me to learn. He went on to become CEO of Jackson National, now Jackson, and asked me to come with him. And I was at Jackson for 20 years. I was there when we launched the variable annuity business. I still remember our first few tickets and how exciting that was to have people say yes.

That turned into a great run, where we became the largest variable annuity provider in the country. And while I was at Jackson, I had the good fortune of having a great group of people above me in the organization who allowed me to do wonderful things. I wrote a business plan to create an independent broker-dealer; I thought that there was a need in the marketplace.

I was the first CEO of National Planning Holdings. We ended up having a very good run there as well. I think we had 4,500 advisors when I left, and we did about $1.4 billion, $1.5 billion or so in revenue. Sadly — and unfortunately in some ways — that organization no longer exists because it was purchased by LPL Financial, but it was a great run with a

great group of people.

At Jackson, I was able to build a wealth management business in a way that hadn’t been done. We were one of the first to bring unified managed accounts to the advisory world using fractional shares in a fractional share facility. I did a number of things while I was at Jackson. I was executive vice president in charge of all retail at Jackson. I had the insurance business, which I love very much, but I also had wealth management and the asset management business as well.

Feldman: Which go hand in hand.

Jack: They do. I enjoyed my time there. I left the corporate world to go do my own thing with private equity and private equity real estate and had a very nice run there. And then I had a personal situation that caused me to have to step away from the industry for a while. After that was resolved, I was able to consider getting back into the game. And that was right around the time when Constellation called.

Feldman: Tell me about your new direction with AuguStar as well as the product lines you are developing and have already introduced into the market.

Jack: I’ve been fortunate enough to bring a number of my former colleagues to the organization. We had worked together for a long time, and there was a lot of trust built up. We had to revamp our product lines and reinitiate product lines. We created a fixed indexed annuity product specifically tailored towards the independent marketing organization. We created multiyear guaranteed annuities, a suite of

MYGA products that were rolling out not just in FIAs but also in institutions, banks and broker-dealers.

We had to go about the process of obtaining selling group agreements, making sure that we onboarded lots and lots of advisors to make sure that we got their experience right. We had to change the brand and introduce the brand and change our messaging to be consistent with AuguStar and what we stand for.

We had to restart our ops and our IT stack, which is not insignificant in any way. So, we have been definitely busy, and that has gone well. We now have what I would call two of the three legs of the stool available from a product standpoint. We have traditional fixed annuities in the form of MYGAs, and we have FIA products across all channels, institutions and IMOs. We’re not in the registered product space currently, but that’s forthcoming. We have been busy. It has definitely been a quick-paced environment, but one that is consistent with the way I believe a business needs to be built.

Feldman: The shift of Ohio National to the IMO market is significantly different. How do you see that playing out?

Jack: Depending upon how you measure, there are 300,000 or 400,000 advisors and agents in the country that can do business with organizations like ours. We want to make sure that we provide our resources and our capabilities and our products in the ways that meet the need of the agent and the advisor, whether they are in independent broker-dealers, whether they’re in IMOs, whether they’re in banks, whether they do business directly — all of that needs to be agent choice. They need to decide what’s best for them.

We don’t mandate any of that. We try to create great suites of products and support our agents and our advisors to make sure that they are getting what they need from us to help them grow their business. The natural extension of that, of course, is the IMO marketplace, which Ohio National was never in. For us, setting up AuguStar as a new brand with new ownership, it was important for us to be in all channels with all products, thereby giving the advisors what they need. They can determine how their business is best written, and we want to be able to support that.

Feldman: Where do you see your future as a company between life and annuities? Ohio National had a big product mix. Where do you see that going in the future? Do you see more on the annuity side? Do you see more on the life side? Is there a certain blend that you’re shooting for?

Jack: I can’t stress enough that what we bought was a platform and the organization that was in the past is very different than our organization today. What you have in Constellation, our parent company, is an organization that first and foremost is global, and it will grow through acquisitions as well as organically both in and out of the U.S. And that’s demonstrated by a number of acquisitions that we’ve already done and/ or that we’ve announced.

We intend to focus on traditional life insurance sold by either agents who are attached to IMOs or through a traditional brokerage general agency structure. I think you’ll see us focusing more on indexed universal life-related products than we are on other products of the past or products that other organizations might choose. We think there’s a significant overlap in the IMO space between IMOs that write annuity products and life insurance products.

Annuities are a bit more in favor now in the interest rate environment that we are in. You can just look at that from a flow standpoint. But we think that having all products available in the markets that we are actually servicing is key. We’re not going to be able to predict the future of markets. We think that clearly annuities are in favor now, or at least certain aspects of the annuity business are in favor now. Other aspects of the life insurance business may be somewhat out of favor, but we think those things are likely to be cyclical. So again, all products in all distribution channels are our real focus, and we think there’ll be a lot of synergy between the annuity and the life insurance platforms.

Feldman: I was talking the other day with one of the larger manufacturers of products in the industry, and it was interesting to see somebody who is mostly in the annuity space now is getting into the life space. Do you think

I think demographics will have a significant impact on life insurance flows, and I think that product innovation will have significant impact on life insurance flows, but I don’t believe that the DOL rule will trigger much of that.

the life space is a big opportunity? How do you think that might be affected by the threat of the Department of Labor fiduciary rule?

Jack: I do think that the life insurance industry provides great complementary opportunities to insurance companies because it does a number of things. First of all, getting a deeper wallet share with your agents is never a bad thing. Clearly there’s a lot of crossover between agents who sell annuity products and life insurance products. If we can generate more wallet share and more mindshare from those agents, that is a very significant opportunity for us. So we like that.

We also like the fact that the balance sheet obligations and requirements for annuities are very different than they are for life insurance. Obviously with life insurance you have mortality risk, and with annuities, you either have market risk or spread-based risk. And we like having the opportunity to have diversification of risks on our balance sheet.

That doesn’t mean that originating annuities or life insurance are the only ways to go. When we look at it, certain products may be out of favor, certain platforms may be out of favor, and they may be a better opportunity to purchase at any given time in the market cycle than it would be to originate or vice versa. Sometimes things are so hot that it’s better to originate than to buy. And the inverse of that can be the case as well. As it pertains to the DOL rule, I don’t believe that the DOL rule is going to have a significant impact on life insurance flows. I think demographics will have a significant impact on life insurance flows, and I think that product innovation will have significant impact on life insurance flows, but I don’t believe that the DOL

rule will trigger much of that. And with respect to the DOL rule, we agree with the recent lawsuits filed by some of our trade associations.

I believe that limiting consumer choice is always a bad thing. I think consumers are smart, they have access to lots of information. Having more options is good. Limiting the advice that they can receive from agents, from advisors and intermediaries is never a good thing. I think it leads to a significant portion of the market being underserved. If the lawsuits are unsuccessful, we believe that we’re well-prepared should the DOL rule not be overturned. We feel like we’re in good shape either way. We believe in the validity of the lawsuits, and we look forward to seeing the conclusion of that.

I think no matter where this ends up, having clear rules is incredibly important because it’s always damaging to have it be arbitrarily done either by the carrier or by the intermediary and the IMOs and the broker-dealers or by the agents. So, hopefully, the lawsuits will be successful; we believe they should, and if not, then I think we need a significant level of clarity with respect to what is required in order to comply not just at the agent level, but in the intermediary level and at the carrier level as well.

Feldman: How does your structure compare to other private equity companies in the industry?

Jack: I think we probably are in the middle, in the intersection, if you will, between the traditional carriers with more traditional ownership, whether it be mutual or public, and the private equitybacked carriers. Because we are owned by two of the larger North American pension funds, we are not under pressure to

do anything other than have reasonable risk-adjusted returns.

I would say that we are in a very good place to be able to compete favorably with the traditional carriers from a balance sheet standpoint and from private equity-led or -owned organizations with respect to the products that we create. We believe we have a unique story. We think that story is identifiable to advisors and to intermediaries, distribution firms, corporate dealers, banks and IMOs.

Feldman: One of the things that I’ve heard from the agents and advisors is that when a new company comes in, they’re not always friendly to the existing policyholders. What’s your take on that?

Jack: We want to be very policyholder friendly in everything that we do. I think that ultimately if you’re serving advisors, we view advisors as our clients, and we view policyholders as our clients. And we think we have an obligation to treat everybody appropriately and consistently. We hope to be able to demonstrate that. And some of the organizations that I’ve been with in the past have demonstrated that, and I intend to do the same thing here.

The team that we have been able to recruit has demonstrated excellent, predictable track records, and that’s why I asked them to join. If they didn’t have excellent track records, they wouldn’t be here. We hope that will allow us to be able to continue to earn our reputation in the industry. I was with a group of advisors two weekends ago, and I always love spending time with advisors. And an advisor said, “You bought a restaurant, you bought the footprint of the restaurant, the countertop and all of the equipment and the oven and all of that, but you have

a new chef, and you have a new wait staff and all of your contractors are different.” I thought it was a pretty good analogy. We have earned the opportunity to have people give us the benefit of the doubt. We know that we need to earn that. We’ve had great success. Some of the recent data has been released; we’re now a top 10 seller of FIAs in Q1.

Feldman: Where do you see your future — and maybe the industry’s future — going?

Jack: Our future is going to carve out more market share from this huge, massive opportunity we have ahead of us, both in the annuity space and in the life space. I think there’s a lot of opportunity for us to disintermediate from other organizations that aren’t as nimble, that may not have the balance sheet that we do, that may not have the relationships that we do, that may have been given a shot and didn’t do a great job on behalf of the agents and advisors.

I think we’ll do that with respect to the products that we are developing currently. And I think that you’ll see us dramatically increase the distribution footprint that we have in terms of the partners that we do business with. We want to be thoughtful. Our goal is to roll out a significant distribution partner per quarter, not do it all at once.

These things are delicate. You need to make sure that you do a good job. I’ve always said that the first ticket experience for every agent, every advisor, every broker-dealer, every distribution partner must be excellent. No one wants you to learn on their dime or on their ticket.

Feldman: They don’t want their clients getting beaten up over the customer experience.

I’ve always said that the first ticket experience for every agent, every advisor, every broker-dealer, every distribution partner must be excellent. No one wants you to learn on their dime or on their ticket.

Jack: That’s exactly right. So we are going to be very deliberate in the way that we roll out products and about our distribution capabilities, and then we want to make sure that our brand is adopted.

I believe the industry has a chance to be able to do what it has been trying to do forever, and that is compete on a level playing field with the asset management industry and become a bigger part of global wealth management. It’s amazing to me that as an industry, we have competitive advantages that the asset management industry doesn’t. If we choose, we can, of course, own an asset management company or two or three — obviously there are lots of examples of that. But asset management companies can’t take on balance sheet risk in the way that we can.

I think our opportunity presents itself now because the industry has grown so significantly in terms of wallet share. We have an opportunity to make sure that it’s not just one and done, that you didn’t have all this velocity coming out of low interest rates and there’s no stickiness to it. There are a lot of things that we as an industry can do if we learn from some of the mistakes of the past. And it feels as though the industry, and the annuity industry in particular, is well positioned to do that.

Feldman: How can we do that?

Jack: I always laugh when people say you should make your products simple. I don’t believe that simple products are what consumers really need. I think what consumers need is to have complex products made simple for them to understand. There is nothing of significant value that I can think of in the asset management industry that is simple to pull off. It’s not simple, for example, to pick the right stock if you’re a portfolio manager for a mutual fund company. But I think the insurance industry must have complexity because we have balance sheet obligations that we are making commitments to with respect to our consumers, of course. The insurance business is complex. But the way that we talk about it and the way that we present it and the way that we illustrate it and the way that we report on it to the consumer, I think leave an awful lot of opportunity for improvement.

Ronnie Kaymore

traded in the football field for an agent’s license. He helps dozens of NFL and NBA athletes plan their financial futures.

By John Hilton

Ronnie Kaymore began providing financial advice and assistance to athletes more than 15 years ago when a decades-old system largely decided when they would make money.

Today, the “amateur” athlete who doesn’t get paid is almost an anachronism. Even more change is on the way as the last remnants of big-time amateur sports fade away and billions are shared with younger players.

Those athletes are going to need plenty of help, said Kaymore, CEO of Kaymore Sports Risk Management and Consulting in South Orange, N.J.

“You get some of these five-star recruits or All-Americans, and they’re being recruited by some of the top universities athletics wise in the country. And that creates a need for them to now be seniors in high school receiving financial literacy,” Kaymore said. “The financial planning industry will have a very unique opportunity to be a blessing to these kids as well as their families a lot earlier than usual.”

Kaymore shares a lot with the athletes he works with. A prep football star in New Jersey, Kaymore played college ball for Texas A&M Kingsville. In 2003, he joined the Bismarck Roughriders of the National Indoor Football League.

Kaymore later played for the WilkesBarre/Scranton Pioneers, a team in the Arena Football League’s AF2 player development league, and then the AFL’s Las Vegas Gladiators before moving beyond football in 2006.

Having that playing experience is immensely helpful in relating to athletes and their financials, Kaymore said.

“That can be an advantage in terms of knowing what they have to deal with both physically and mentally,” he explained. “And knowing and understanding that you can be the first pick of the draft and yes, you’ve got a lot of money now, but that’s not even your concern. Your

concern is the playbook and becoming acclimated to being a professional.”

Football to finance

Once his own playing days ended, Kaymore wasted little time pondering his next career. He had worked for two years in banking, and his wife, Monique, worked at a bank. With the move to financial services decided, Kaymore did not have to look far for potential clients.

Research shows that athletes start declaring bankruptcy as early as two years after the end of their athletic careers, according to the Global Financial Literacy Excellence Center. The reasons are well known: Short careers, lack of financial awareness and the quick onset of wealth are three.

It starts with education, said Kaymore, father to two girls, Kirsten and Kayla, and two boys, Caleb and Joshua.

“I do think that there’s a great need to educate athletes in particular, relative to all sorts of financial planning,” he said. “I’ve never met an athlete that understands what a stock, bond or ETF is. I’ve never met a young man that understands what a whole life policy or index [universal life] is. It’s just information that they were not privy to.”

or both of their parents in charge. For Kaymore it creates a true family atmosphere that makes his job easier.

“What we try to do is make sure we get Mom and Dad some training, or whoever those family members are,” Kaymore explained. “We’ve done things like cash balance plans and defined benefit plans to make sure that when this player retires, Mom and Dad also have a retirement stream of income.”

Having the parents involved adds another benefit as well. Young athletes who go from virtually no money to a multimillion-dollar bonus check do not always respond responsibly. The immediate tax bite alone shrinks that big bonus check significantly. Then there are friends and family and girlfriends all wanting to share in the bounty.

‘Educating the parents’

Having that strong parental influence can go a long way to establish guardrails on spending, Kaymore said. Kaymore Sports created a Parental Advisor Council, which counts Stacy Elliott, father of NFL star Ezekiel Elliott, as a close “strategic connection.”

“Our model has always been to educate the player by educating the parents,”

I do think that there’s a great need to educate athletes in particular, relative to all sorts of financial planning.

Kaymore got his life insurance producer license and his accident/health insurance license in 2009. His agency focuses on insurance and risk management, and has partnerships with other experts, such as accountants and registered financial advisors, to provide holistic financial services.

“We run it that way just to present that collaborative effort,” Kaymore explained. “One hundred percent of our clients at Kaymore Sports are athletes, and a lot of the time that permeates into their family.”

For example, players will often create a business or foundation and put one

Kaymore said. “I think a lot of these kids do come from good homes, maybe sometimes not real affluent homes, yet the love is there. The care is there. The nurture is there. And I think that if the parents are educated and empowered, they’re able to provide some guidance to their children.”

Kaymore primarily represents NFL and NBA players. Many clients play for the hometown Philadelphia Eagles, but Kaymore Sports counts players on all 32 NFL teams.

Since 2010, Kaymore Sports has been

the Fıeld A Visit With Agents of Change

affiliated with American Business for agency support. An Integrity Marketing Group company, American Business is led by Bruce Mesner, a former NFL player with the Buffalo Bills.

“What that did for me was it gave me in essence a partner that understood the NFL pension plan, understood the benefits,” Kaymore said. “So, when we’re designing these plans for these NFL and NBA kids, we’re also taking into consideration the benefits that the league provides.”

The way Kaymore fights for clients is what differentiates him from other agents, Mesner said. For example, insurers will attach exclusions to a typical disability policy. While many agents just accept it, “Ronnie will fight them on it,” Mesner said.

“When somebody goes on claim, Ronnie is there to help and support the family as opposed to just leaving it to the family and whomever they can hire to help them,” Mesner added. “I’ve seen it over and over and over again. He does not take the path of least resistance when working with these players and their families.”

Kaymore, a member of the Million Dollar Round Table, a group for top financial services producers, is a fan of what annuities can provide clients in terms of lifetime income. The COVID-19 economic turmoil and resulting inflation showed how valuable annuities are to a financial plan, he added.

“They ended up providing really good buffers and performed really well during that volatility,” he said.

Dramatic NCAA changes

The dramatic and ongoing changes to how NCAA athletes can be compensated

are something Kaymore is watching with interest. First came name, image and likeness rights. NIL originated with former UCLA basketball player Ed O’Bannon arguing that college athletes should be compensated for the use of their name and image in video games.

That led to a class action lawsuit, which led to new NIL rules three years ago. The college sports world responded swiftly, with athletes signing million-dollar deals and moving from school to school yearly.

In May, the NCAA settled another class action lawsuit by agreeing to share $2.7 billion with past athletes who were denied NIL opportunities. More importantly, the settlement would come with a corresponding commitment from conferences and schools to share revenue with athletes moving forward, ESPN reported.

It all means that a lot of real-world financial concerns are starting even earlier for the best-paid athletes, Kaymore said.

“The need for financial literacy for athletes, in my professional opinion, has always been there,” he said. “But now this has just accelerated that even further. I think it even shifted a little bit of the burden to now high schools to educate their student-athletes for what the kids are going to soon embark on once they’re being recruited by these universities.”

InsuranceNewsNet

Senior Editor John Hilton covered business and other beats in more than 20 years of daily journalism. John may be reached at john.hilton@innfeedback. com. Follow him on X @INNJohnH.

2024 FINANCIAL SERVICES

does the industry serve the next generation of investors? In this year’s Financial Services for the

Series, we look at Cambridge Investment Group and their plans for the newest generation in the investing area. A New Wave of Investors Is Here: Meet Gen Z with Amy Webber, CEO of Cambidge Investment Group

15

Ronnie Kaymore, far right, and wife Monique pose with their four children and Odell Beckham Sr. at a New York Giants game.

A New Wave of Investors Is Here: Meet Gen Z

By: Amy Webber, CEO, Cambridge Investment Group

Baby Boomers, Gen X, Millennials, and now. . . Gen Z. All four of these generations are defined by their unique preferences and expectations — outlooks on life that are often shaped by the social and environmental conditions they grew up in. These preferences and expectations often have a major influence on how financial professionals serve each of their clients. How could they not? Older generations of investors, for example, still typically prefer to meet in person, while younger generations tend to gravitate toward virtual meetings and instant messaging applications. A prudent financial professional understands that a “one-size fits all” approach to wealth planning isn’t sufficient.

Gen Z, defined as individuals born between 1997-2012, is the latest generation to enter the investing arena, with Generation Alpha not far behind. What defines Gen Z perhaps more than any previous generation is its appetite for technology. Many Gen Zers grew up during one of the most exciting stretches in tech that we’ve ever seen, highlighted by the release of the iPhone in 2007, when the oldest Gen Zers were barely 10 years-old. By the time most Gen Zers hit their teenage years, mobile devices, WiFi, social media, and ondemand entertainment were a major part of everyday life.

Why should any of this matter to financial professionals? Influenced by the environment they were raised in, younger generations expect a fast and high-quality tech experience in all areas of their life, including financial planning. And as these investors continue to build and inherit wealth, start families, and make important financial decisions, it is vital that financial professionals make them a priority.

Let’s go over a few of the best ways you can appeal to the younger generations of investors.

Build a Digital Reputation

Younger generations are accustomed to using technology, and they want to work with financial professionals who can provide an overall experience that meets their expectations. The good news is that there are a variety of ways you can leverage the digital platforms that move the needle with younger generations. Examples include enhancing your online presence through social media content, developing a user-friendly and interactive website, and possibly even building a dedicated mobile app. The possibilities are nearly endless in today’s digital world, and many financial solutions firms even provide services to support financial professionals in these areas.

You can elevate your digital reputation even further by engaging with potential clients through educational content, webinars, and interactive tools. All of these methods help demonstrate your understanding and command of today’s technology while building trust with your target audiences.

Tap Into Technology

Demonstrating that you know how to use technology is the first step to attracting younger generations of investors, but proving that there’s more than meets the eye demands an even more focused approach.

AI, machine learning, data driven insights, and other automated solutions can completely revolutionize how you do business, allowing you to get more done in less time and with fewer resources.

Finding ways to implement AI is a great place to get started — 60% financial professionals in one report1 have expressed interest in leveraging AI to execute administrative tasks, assist with client interactions (e.g. scheduling and routine questions), research investment opportunities, anticipate needs, write emails and blog posts, and provide a generally more personalized experience across the board. Automated scheduling and support tend to appeal to younger clients who value efficiency and convenience, and datadriven insights can help you make informed decisions and optimize portfolio performance.

The important point to remember here is that technology should be used to compliment, not replace, your services. With great power comes great responsibility. Applied correctly, these technologies can be used to enhance your services while opening up more time to spend with clients. Technology has provided the opportunity to do business smarter and faster, and financial professionals who don’t embrace these capabilities risk being left behind.

Recruit Tech-Savvy Financial Professionals and Associates

Yet another way you can resonate with younger clients is to hire financial professionals and associates who are proficient with today’s technology platforms. This approach taps into the power of relatability, shared experiences, and cultural understanding, which are important elements in establishing trust and rapport with clients, especially among younger generations.

Accomplishing this rapport starts with expanding traditional recruitment routes. In a service-focused industry, it’s not just about what (or who) you know, but perhaps more importantly, what you have to offer. It’s great to have new candidates with a background in finance or business, but soft skills such as communication, critical thinking, and the ability to work with teams are becoming increasingly important and valued not only within the industry, but for those the industry will be serving. This means recruiting from outside traditional education fields, and widening your recruiting net. A great place to start is sourcing talent from higher education institutions of all types, including women’s colleges, HBCUs, and alternative educational programs.

To summarize, financial professionals have a significant opportunity to attract and serve younger clients in today’s tech-driven world. By understanding the unique needs and preferences of this demographic and tailoring strategies accordingly, you can build long-lasting relationships and position yourself for long-term success.

Odeniran, W. (2023). 60% of Financial Advisors Use or Are Iterested in Using ChatGPT — 2023 Survey. SmartAssett. | Member FINRA/SIPC

The younger generations can get caught up in unrealistic investment ideas they find on social media.

For advisors, the challenge is to cut through the noise and help them set realistic expectations.

By DOUG BAILEY

Ron Tallou, the founder of Tallou Financial Services, says working as a financial advisor to young people is not about convincing them or persuading them of the virtues of saving and investing. It’s frequently not even about selling them products.

More often, it’s about talking them out of ideas and decisions that they’ve picked up who knows where.

“The younger generation is very much social media driven, and they can get caught up in what they see from others and not always realize it is an illusion and if you try to keep up with what you see you can set yourself back,” says Tallou, himself a comparative youngster at 35 years old. “I also find the younger generation does not have a good sense of where to invest. They get caught up in what someone posts online about a particular crypto, or stock, so I have to talk them out of not putting too much of their savings into speculative investments.”

“Cutting through the noise requires strong personal relationships, consistent messaging and compelling illustrations of how prudent budgeting and longterm investing can drastically impact one’s financial well-being,” he says, in spite of the notion that the tried-and-true methods are the least interesting to the younger crowd.

Blake Pinyan, a senior financial planner and tax manager at Anchor Bay Capital Inc. in Carlsbad, Calif., has a checklist for dealing with Gen Z investors that combines old-school methods with significant upgrades and additions for the emerging cohort.

» Be ready to be flexible. Gen Y and Gen Z are generations living busy lives, with full-time jobs, new family and many outside activities. “If you want to serve this market, you need to be open to accommodating meetings in the evening or the occasional weekend,” says Pinyan. “They have many more life changes than a retiree, so they want an advisor that can adapt to potentially meeting more frequently than once or twice a year as things come up within their life.”

It is a familiar refrain among financial planners who concede that young clients don’t come looking for information — they are awash in information from TikTok, Twitter, Instagram and the myriad social media platforms. The biggest challenge is getting them to tune out a lot of what they’ve heard or read.

“In my experience, a broad swath of the Gen Z cohort is hindered by two things — unrealistic expectations about income potential, and a propensity to spend rather than save and invest,” says Thomas Brock, CPA, a 20year veteran of financial investments consulting, corporate finance and accounting. “Helping them increase their economic awareness and embrace a more disciplined financial lifestyle is the way to overcome these deterrents.”

» Give them the “what” and the “why.” Education and transparency are important to Gen Z clients, but they tend to want to know more about how or why an advisor is making a recommendation. “They need to understand the rationale that goes into each of the advisor’s recommendations,” says Pinyan. “So, when working with these types of clients, it’s very important to clearly explain concepts in simple terms and then confirm that they understand what’s being recommended.” And some want short-term coaching engagements that empower them to be able to manage finances on their own.

» Be up to date with technology and alternative investments. This is a group that’s used to doing everything over the computer or phone, and advisors have to be prepared for that. “They’re fluent in technology, so they definitely expect their advisor and the associated company to be the same,” he says. “They wouldn’t want to be part of an organization that’s paper intensive and has little in the way of the latest software or technology.” Gen Zers are comfortable with secure portals and accustomed to everything being done digitally. “So, you have to have virtual meetings as an option,” Pinyan says. Moreover, they may already have some cybercurrency or cryptocurrency tucked away somewhere, and it is incumbent on the advisor to at least be conversant in that topic.

But that’s so old school to many young investors given the myriad of social media “influencers” touting get-rich-fast gimmicks and a general fear of missing out, Brock says.

» Forget about AUM fees. This age group is in “an accumulation phase,” with housing, children, college loans, and other costs and debts to worry about. They don’t have a lot of assets to manage, and they aren’t too keen on paying fees. “They don’t have money in retirement accounts for outside advisors to manage, but they certainly have a need as far as financial advice and are willing to pay for it, like an annual subscription, or a project, or even an hourly consultation basis,” Pinyan says.

» The next-generation investors want next generation advisors. “They like the idea of an advisor that can grow with them over time and is not going to retire in a few years. Someone that can resonate with the struggles, challenges, risks and opportunities that they’re facing.”

Surveys indeed show stark differences in Gen Z expectations, desires and needs, compared with older generations when it comes to financial advice and management, Consumer research and data analytics firm J.D. Power, for example, finds that younger clients working with an advisor are much more likely to say they already have a financial plan that they put together themselves, or they want one, compared with other generations. And 60% of those younger

Ron Tallou

Thomas Brock

Blake Pinyan

consumers with a plan said that they were heavily involved in the process of building the plan (vs. an advisor building it for them) compared with 28% of baby boomers or older customers.

Only 16% of Gen Y/Z said that investment decisions are made by advisor on their behalf, which is about half the rate of boomers and older clients. And 66% of Gen Y/Z said their advisor has discussed the financial needs of their heirs vs. fewer than 50% of older generations.

Craig Martin, executive managing director and global head of Wealth & Lending Intelligence at J.D. Power, recalls the old Smith Barney TV ads with their impersonal slogan: “They make money the old-fashioned way. They earn it.”

“It was like, ‘we’re smart, we make money; you pay us because we make you money,’” Martin said. “Gen Z is much more about money as a means to an end. It’s much more about goals, peace of mind and fulfillment. Not just ‘How can I get the best return?’”

Moreover, the life paths of younger investors have changed greatly from the days of the traditional straight lines of temporarily living with parents, getting an education, starting a career, getting married, buying a house, having kids and working with one company until retirement. Today’s career path for Gen Zers looks more like a spiderweb, Martin said.

“It’s totally different now,” he said. “You start a career, change jobs frequently, maybe move back into your parents’ house for a while, you work at home sometimes, you move around a lot. So, if you think about that in the context of this generation, what they are looking for financially is very different than previous generations.”

In addition, a significant number of young investors want to put their money where it might generate some positive social benefits.

“Something I’ve noticed

is that younger investors want their investments to have a positive impact instead of just generating a profit,” said Dre Villeroy, founder and CEO of Los Angeles-based investment manager Beyorch. “Individuals who are interested in investing in ESG (environmental, social and governance) want to know that their funds are making a positive impact on society.”

And it’s not like Gen Z and Gen Y don’t have money to spend or will have. Gen Y and Gen Z together make up more than 47% of the U.S. population, and Cerulli Associates of Boston projects wealth transferred between 2021 and 2045 will total $84.4 trillion (roughly $2 trillion per year for 20 years). More than twothirds of Gen Y/Z investors have already received an inheritance or are set to receive an inheritance.

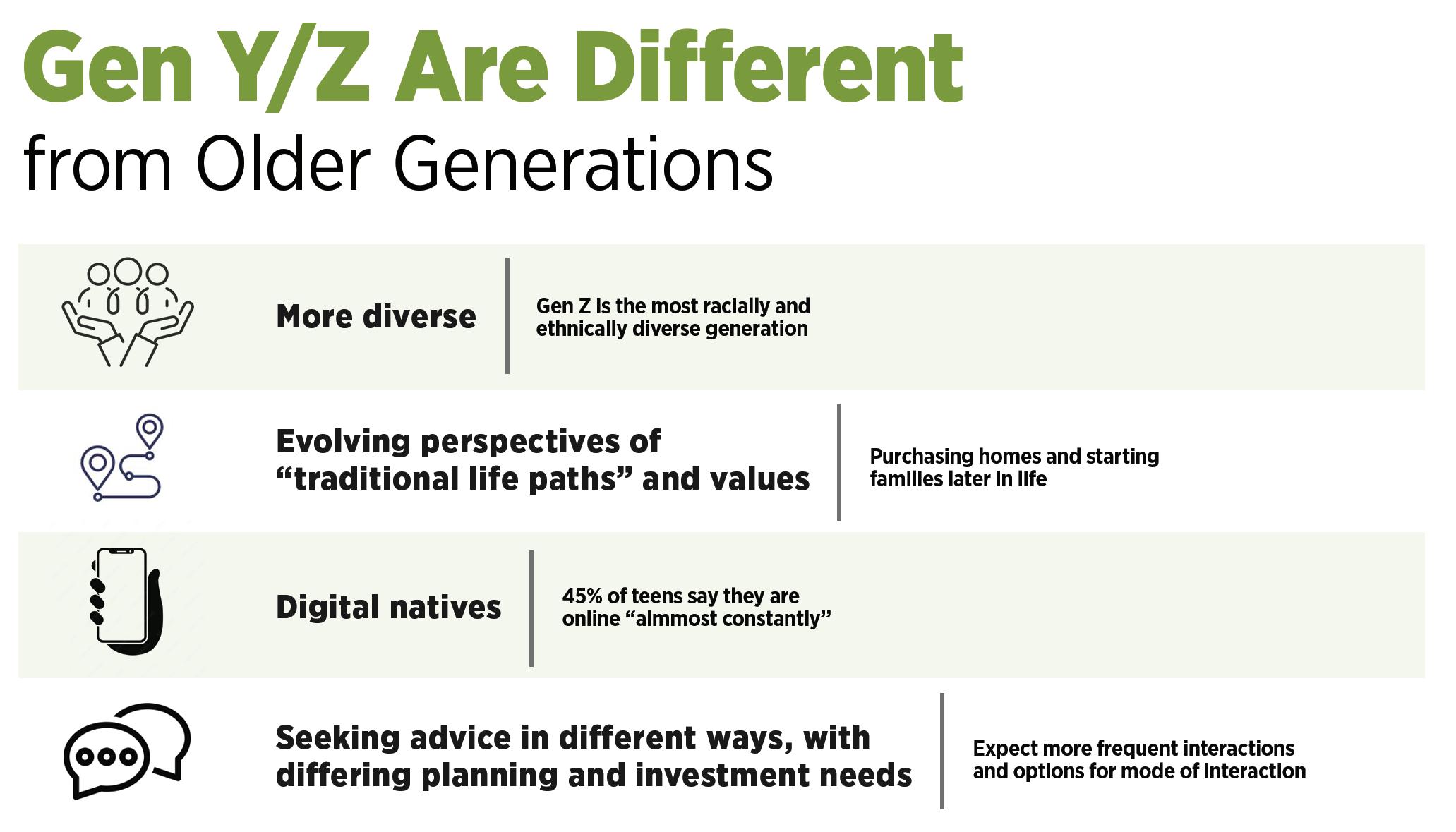

A recent study by Fidelity Investments confirms many of the comments and anecdotal offerings from investment advisors. Gen Y and Gen Z are more racially and ethnically diverse than

Craig Martin

Dre Villeroy

previous ones. They have “evolving” paths and values and are more likely to purchase homes and start families later in life than older generations did.

They are digital natives and 45% said they are “online almost constantly.” They seek advice in different ways, with differing planning and investment needs, and they expect more frequent interactions and options for mode of interaction.

“A lot of the fundamental things still hold true, but what I find with this group is that they’re coming into the meeting with more a lot of information and education about you; they’re comfortable with researching for themselves,” said Kimberly Mamaril, vice president of Las Olas Capital Advisors in Fort Lauderdale, Fla. “And I think they really want to look at you as a partner in what they’re doing. My older clients are essentially looking at it as though they’re outsourcing. The young generation is looking for someone who wants to really partner with them and make good decisions together.”

investors typically are underinsured, and haven’t thought much about things like life, health and disability insurance, retirement funds, and savings plans.

Fidelity found that among Gen Y/Z investors, 73% would like their financial professional to provide comprehensive services (vs. 30% of boomers). About 64% consolidate assets with a primary financial professional (vs. 21% of boomers). And they are focused on maximizing savings so they can retire early and pursue passions.

As a result of these differences 8 out of 10 advisors say that their firms have either changed or are contemplating a change in pricing models, considering subscription services or by-the-hour models among others.

Another major change Fidelity advises is that financial planners should consider modeling scenarios assuming the client might live to 105 or even longer.

explore investments that are going to be tax favorable like 401(k)s, IRAs and Roth IRAs, advises Tallou. “If their company offers a match, take advantage of it and make that the first place to invest. I always recommend to younger adults that are unsure how much to save to start with 10% of your income — ideally you should be able to live off 90% of your income — and if not 10% of gross, then make it 10% of your net paycheck, and slowly increase the increments by 1%. It’s easier to start off with a percentage of earnings because it can be tailored automatically as you make more or less money than carving out a larger dollar amount that might not be sustainable long term.”

Doug Bailey is a journalist and freelance writer who lives outside of Boston. He can be reached at doug.bailey@ innfeedback.com.

Mamaril says she finds younger

Once clients have the short-term emergency fund saved up, they should

Like this article or any other? Take advantage of our award-winning journalism, licensure and reprint options. Find out more at innreprints.com.

Kimberly Mamaril

Life insurance sales dip slightly in Q1

Life sales experienced a hiccup in the first quarter as total U.S. individual life insurance new annualized premium slipped 1% year over year to $3.76 billion in the first quarter, according to LIMRA’s preliminary U.S. Life Insurance Sales Survey. The total number of policies sold also dropped 1% in the first quarter.

“Overall, a large proportion of carriers reported gains in both premium (7 in 10) and policy sales (6 in 10) in the first quarter. Every product line except whole life posted positive growth,” said

John Carroll, senior vice president, head of Life & Annuities, LIMRA and LOMA.

Term life experienced its fifth consecutive quarter of growth in both premium and policy sales. For the third consecutive quarter, fixed universal life new premium increased.

The number of whole life policies sold fell 5% in the first quarter, compared with the first quarter of 2023. Despite the decline, whole life remains the dominant product in the U.S. market, representing 38% of the total new annualized premium sold in the first quarter.

BESTOW TO SELL ITS LIFE INSURANCE COMPANY TO SAMMONS

Bestow Inc. announced it will sell its life insurance company to Sammons Financial Group. Bestow Life Insurance Co. is expected to transition to Sammons after the state of Iowa approves the deal.

Bestow Inc. will continue to leverage its technology and platform as part of the company’s strategic plan “to become the dominant technology platform for the life and annuities industry,” Bestow CEO and co-founder Melbourne O’Banion said.

Sammons Financial Group has been a partner and investor with Bestow for many years. O’Banion said the two companies will work together to explore future growth opportunities that will benefit both organizations.

With the sale of Bestow Life, Sammons will own a third life insurance company,

Preliminary FirstQuarter Life Insurance Sales Results

• Total life insurance new premium was $3.76 billion in Q1, down 1%.

• Term life, IUL, VUL and fixed UL all posted new premium gains in Q1.

• Whole life new premium fell 8% in Q1 to $1.43 billion.

joining member companies Midland National Life Insurance Company and North American Company for Life and Health, a Sammons spokesman said.

JOHN HANCOCK AND MIT AGELAB TEAM UP

In a continuing effort to understand how the world’s increasingly aging population can live better and healthier lives — and how the company can possibly profit from the knowledge — John Hancock has entered into a five-year, multimillion-dollar collaboration with the Massachusetts Institute of Technology’s AgeLab, which researches longevity issues.

QUOTABLE

Of all the people who care about you living a long and healthy life, your insurance company is right at the top of that list.

Hancock, with its parent company, Toronto-based Manulife, is arguably a leader or early adopter among life insurers of “wellness programs” that educate, encourage and reward policyholders to live longer and healthier lives. The company said its alliance with MIT will explore the future of “longevity innovation, developing research, thought leadership and workshops with the goal of driving actionable insights for the business community, policyholders, individuals, and families.”

Hancock President and CEO Brooks Tingle said the collaboration with MIT fits nicely with the goals the insurer set years ago with its Vitality program to empower sustained health and well-being of its customers.

LGBTQ+ POPULATION IS UNDERINSURED

While the LGBTQ+ adult community is very diverse in terms of age, wealth, gender and ethnicity, LIMRA research shows this group is disproportionally uninsured and underinsured leaving those who rely on them at financial risk should they die unexpectedly.

Only 40% of LGBTQ+ adults say they own life insurance, a rate considerably lower than that of the general population (51%). Even those who have life insurance coverage may not have enough. LIMRA research shows 46% of LGBTQ+ consumers — representing 8 million adults — say they need (or need more) life insurance.

The 2024 Insurance Barometer study found almost 6 in 10 insured LGBTQ+ adults feel financially secure, compared with just 41% of uninsured individuals.

— John Hancock CEO Brooks Tingle

Source: LIMRA

FAILURE TO SURVIVE

Failure to Survive Product Line

With liberal underwriting standards and unique flexibility, the Failure To Survive coverage provides a death benefit, and can accommodate impairedrisk cases that would typically be declined or postponed by traditional market carriers.

• Contract Indemnity FTS

• Key Person FTS

• Buy/Sell FTS

• Business Loan FTS

When your client wants to borrow from their life insurance

There are benefits and drawbacks to borrowing from a cash value policy.

By Lyle D. Solomon

You may be dealing with clients who are drowning in credit card debt. Many who are in this situation may even want to borrow from life insurance to pay off debt.

Your role as an advisor is crucial in this situation. Your guidance can make a significant difference in your client’s financial future. So, what should be your stance on this matter? Let’s look at the answer.

Can someone borrow from their life insurance policy?

The simple answer is “yes.”

Your clients can borrow from their insurance policies. However, much depends on the type of insurance policy your clients have. If your clients have a universal life or whole life insurance policy and always make payments on time, they must have accrued cash value in the policy.

Your clients can borrow from the cash value in the policy to pay off credit card debt. For example, your clients have $20,000 in credit card debt, and they are not eligible for a debt settlement program or a debt consolidation loan. However, they have a life insurance policy with a cash value of $30,000. In that case, they can withdraw a certain amount from it and settle credit card debt. They can repay the borrowed amount over time.

If your clients’ financial circumstances don’t improve, they may also avoid repaying the total amount.

Should somebody borrow from their life insurance policy?

Well, this is a tricky question. Borrowing against the cash value of the life insurance policy has a few advantages. The first advantage is that clients only must pay the

interest on the loan each year. They don’t have to pay off the principal.

The second advantage is that they don’t have to apply for a loan anywhere else, so they won’t face loan rejections.

What is the process to borrow from a life insurance policy?

The process is simple. All your client needs is an internet connection. The client can call you or the insurance company to find out whether they own a cash value policy. If the client owns a cash value policy, you or the company can provide the client with the in-force illustration statement, which is proof of owning a cash value policy. This statement includes information such as the overall amount the client can borrow from their insurance policy.

After the client has read the in-force illustration statement, they can request the insurer to email them a policy loan request. In this form, your client (the policyholder) must share their contact details (Social Security number, name, address) and how much money they want to borrow from the policy. Instruct your client to enter the necessary details, sign the form and ask the insurer to send a check to the client’s mailing address within 10 working days.

Inform your client that they don’t need to pay any application fees. There are no application fees, credit checks or multiple questions from a financial institution. No one will ask them how they plan to use the funds.

Can your clients borrow money from all types of life insurance policies?

The simple answer is “no.”

Most people have term life insurance policies, and there is no cash value in those policies. Keep in mind that consumers can take out a loan from cash value life insurance policies only.

Borrowing from life insurance has several benefits as well as drawbacks.

The benefits

1. Clients are borrowing their own money, so they are not answerable to anyone. They are borrowing money from their insurance. They have to pay themselves back eventually.

2. Clients can spend the money as they wish. They can use it to repay creditors, consolidate credit card debt or cover emergency expenses. There is no need to explain to anybody.

3. Repaying the loan is not compulsory. The client must pay annual interest, but there is no compulsion to repay the principal amount. However, there is a catch. If the policyholder fails to pay off the principal, that amount and interest will be removed from the policy’s death benefit.

4. There is no minimum credit score requirement. The insurance company won’t check your client’s credit report. Your clients won’t have to pay application fees or additional expenses.

5. Your client’s credit score won’t be affected in any circumstance. This is irrespective of how many payments your clients eventually make. These payments are not reported to credit bureaus.

6. The interest rates charged on life insurance loans are lower than those of credit cards and debt consolidation loans. Check your client’s life insurance policy. How long have they been paying insurance premiums? Is it more than 10 years? If so, your client could qualify for an interest rate of as low as 4%.

The drawbacks

There are drawbacks to borrowing from life insurance policies. Here are a few of them.

• Only policyholders can borrow from life insurance policies.

• Your clients may lose some death benefits if the loan is not repaid.

• This feature is not available on term life insurance policies, which most people buy.

• Policyholders must pay premiums for a prolonged period. This may extend for 15-20 years.

Are there any tax liabilities?

Although there are no tax liabilities for borrowing against a life insurance policy, there are a few things people should be aware of.

If there isn’t enough cash value or the insurance policy has lapsed, the client may have to pay a tax. Although this is less likely to happen, speaking to a financial advisor before borrowing any money is better.

How much can someone possibly borrow?

Policyholders can borrow a large fraction of the cash value of the life insurance policy. The annual statement gives policyholders an idea of the total cash value. If policyholders are unsure of the correct

Your clients can borrow from their insurance policies. However, much depends on the type of insurance policy your clients have.

amount, they can speak directly to the customer service representative or the insurance agent. They can give the insurance policy number to get the right details.

What to do after taking out a life insurance loan

Borrowing from a life insurance policy can be a good way to get out of high-interest credit card debt. But there are a few things policyholders must do after borrowing money.

• Calculate the compounding interest rate on the loan.

• Set up a loan repayment schedule.

• Stick to the repayment schedule and make payments accordingly.

Ask your clients to read the terms and conditions of the life insurance policy. It is important to remember that not all policies are the same. Clients must abide by all the terms to implement this form of debt consolidation. But the good part is that policyholders can pay off any kind of debt with a life insurance policy loan. From student loans to credit card debt, nothing is exempt. Life insurers offer borrowers great flexibility.

Lyle D. Solomon is principal attorney for the Oak View Law Group in Los Altos, Calif. He may be contacted at lyle.solomon@ innfeedback.com.

KEEPING PROMISES

CONVENIENCE

ANNUITY WIRES

Q1 annuity sales see big movers