International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Jaydeep Tase

Salesforce, USA

Abstract:

This article explores the transformative potential of generative AI in the insurance industry. It examines the current state of insurance processes, highlighting inefficiencies and challenges that AI can address. The paper discusses key AI capabilities relevant to insurance, including natural language processing, predictive modeling, and automated document generation. It outlines how AI can assist, augment, and automate workflows for various insurance personas, such as agents, underwriters, andclaimsmanagers.ThearticlealsoaddressescriticalconsiderationsforAIimplementation,includingsafety,reliability, and regulatorycompliance.AroadmapforAIadoptionandscalingispresented,alongwithafutureoutlookconsideringemerging AI trends like federated learning and quantum machine learning. Throughout, the article provides real-world examples and dataillustratingtheimpactofAIoninsuranceoperationsandcustomerexperience.

Keywords: GenerativeAI,InsuranceIndustry,WorkflowAutomation,RiskAssessment,CustomerExperience

1. Introduction

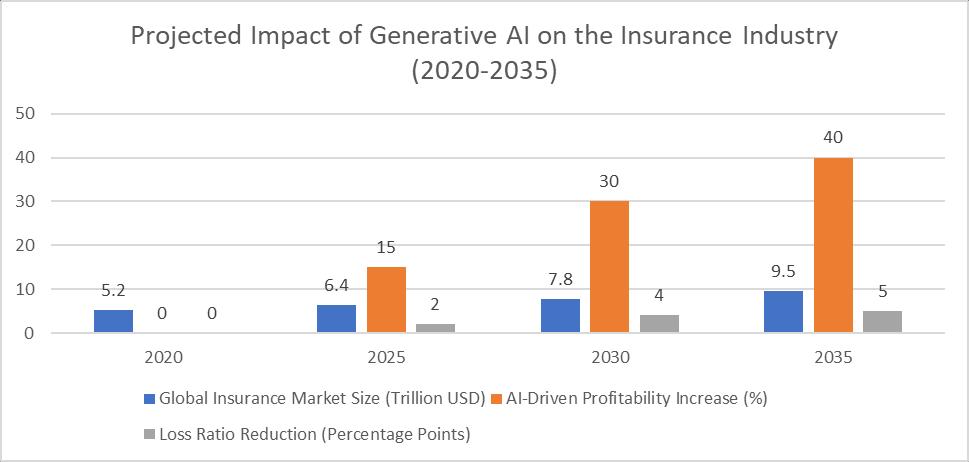

The insurance industry is poised for a technological revolution, with generative artificial intelligence (AI) poised to reshape traditionalprocessesandunlocknewpossibilities.Thistransformationiscritical,astheglobalinsurancemarketisprojected to reach $6.4 trillion by 2025, with a compound annual growth rate (CAGR) of 6.1% [1]. Generative AI, a subset of machine learningcapableofcreatingnewcontentandinsights,isexpectedtoplayapivotalroleinthisgrowthtrajectory.

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

This article envisions a future where AI seamlessly integrates into insurance workflows, enhancing efficiency, accuracy, and customer satisfaction. According to a recent study by Accenture, AI technologies could potentially increase the insurance industry's profitability by up to 40% by 2035 [2]. This significant boost is attributed to AI's ability to streamline operations, reducecosts,andimprovedecision-makingprocessesacrossvariousinsurancesectors.

We will explore how generative AI can assist, augment, and automate key insurance operations, serving multiple personas within the industry. For instance, in claims processing, AI-powered systems have demonstrated the capability to reduce the average claim processing time from 30 days to less than 24 hours in some cases [2]. This dramatic improvement enhances operationalefficiencyandsignificantlyimprovescustomerexperience.

Moreover, we will explore how generative AI can serve multiple personas within the insurance ecosystem, including underwriters, claims adjusters, and customer service representatives. For example, AI-assisted underwriting has shown the potentialtoreducelossratiosby3-5percentagepoints,translatingtobillionsinsavingsforlargeinsurers[2].

While the potential benefits are substantial, implementing AI in insurance raises important safety, reliability, and regulatory compliance considerations. We will address these concerns, exploring strategies to ensure that AI systems are effective, trustworthy,andcompliantwithindustryregulationssuchasGDPRandCCPA.

By the end of this article, readers will understand how generative AI is set to transform the insurance industry, its potential benefitsandchallenges,andaroadmapforsuccessfullyintegratingthistechnologyintoexistinginsuranceoperations.

Traditional insurance workflows have long been characterized by manual processes, data silos, and time-consuming operations. These inefficiencies persist despite the insurance industry's significant economic impact, with global premiums totaling $6.3 trillion in 2019 [3]. The complexity and scale of insurance operations present numerous challenges that hinder optimalperformanceandcustomersatisfaction.

ArecentstudybyMcKinsey&Companyfoundthattheaverageinsuranceclaimtakes30daystoprocess,withcomplexcases extendingto90daysormore.Thisprolongedprocessingtimeaffectscustomersatisfactionandincreasesoperational costs.In fact,foreverypercentagepointreductionintheclaimsratio,insurerscansaveupto$1billionannually[3].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Underwriting, another critical function in insurance, suffers from similar inefficiencies. Underwriting inefficiencies are estimated to lead to annual losses of $7 billion for the U.S. property and casualty insurance market alone. This figure is particularlyalarmingconsideringthattheglobalcommercialpropertyandcasualtymarketisexpectedtoreach$1.06trillion by2026[4].

Thesepainpointshighlighttheurgentneedfortechnologicaltransformationwithintheindustry.Outdatedsystemsstruggled tohandletheincreasingvolumeandcomplexityofdata,resultinginslowerresponsetimesandreducedcustomersatisfaction. Forinstance,asurveybyJ.D.Powerfoundthatoverallcustomersatisfactionwithautoinsuranceclaimsdeclinedby7points (ona1,000-pointscale)in2020,primarilyduetolongercycletimesandalackofproactiveupdates[4].

Moreover,theindustryfaceschallengesindatamanagementandutilization.Insurancecompaniescollectvastdata,butmuch remains underutilized due to fragmented systems and a lack of advanced analytics capabilities. It's estimated that insurers activelyuseonly10-15%ofthedatatheycollect,missingoutonvaluableinsightsthatcouldimproveriskassessment,pricing, andcustomerservice[4].

Changedcustomerexpectationsfurtherunderscoretheneedfordigitaltransformation.AnAccenturesurveyfoundthat80% of insurance customers seek personalized offers, messages, pricing, and recommendations from their auto, home, or life insurance providers [3]. However, many insurers struggle to meet these expectations due to limitations in their current technologicalinfrastructure.

3. Generative AI: A Transformative Force

Generative AI refers to machine learning models capable of creating new content, from text and images to complex data structures.Intheinsurancecontext,thistechnologycananalyzevastamountsofdatatogenerateinsights,automatedocument creation, and predict future trends. The global AI in the insurance market is projected to grow from $2.74 billion in 2021 to $45.74billionby2028ataCAGRof49.9%[5].

Keycapabilitiesrelevanttoinsuranceinclude:

● Naturallanguageprocessingforpolicyanalysisandcustomercommunication:AI-poweredchatbotscanhandleupto 80%ofroutinecustomerqueries,reducingcallcenterworkloadsignificantly[5].

● Predictive modeling for risk assessment and pricing: AI models can process up to 400 times more data than traditionalactuarialmethods,leadingtomoreaccurateriskassessmentsandfairerpricing[6].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

● Anomalydetectionforfraudprevention:AIsystemscandetectfraudulentclaimswithupto95%accuracy,potentially savingtheindustrybillionsannually.In2019,thetotalcostofinsurancefraud(non-healthinsurance)wasestimated at$40billionannuallyintheUnitedStatesalone[6].

● Automated report and document generation: AI can save insurance professionals up to 65% of their time on administrativetasks,allowingthemtoconcentrateonhigher-valueactivities[5].

ThetransformativepotentialofgenerativeAIextendsbeyondthesecapabilities.Forinstance,inclaimsprocessing,AI-driven systems can reduce the claims lifecycle from an average of 10–15 days to just a few hours. Lemonade, an AI-first insurance company,reportedsettlingaclaiminjustthreesecondsusingtheirAIJimsystem[6].

Inunderwriting,generativeAIcananalyzecomplex,unstructureddatasourcessuchassatelliteimagery,socialmedia,andIoT device data to provide more comprehensive risk assessments. This capability has improved loss ratios by 3-5 percentage points[5].

Customer experience is another area where generative AI is making significant strides. AI-powered personalization can increasecustomersatisfactionscoresbyupto20%andboostconversionratesby30%[6].Thisiscrucialinanindustrywhere 41%ofcustomerssaytheywilllikelyswitchinsuranceprovidersduetoalackofdigitalcapabilities[5].

AstudybyAccenturepredictsthatAItechnologiescouldincreasetheinsuranceindustry'sprofitabilitybyupto40%by2035 [5]. This substantial increase is attributed to cost reductions through automation, improved risk assessment accuracy, and enhancedcustomerexperiences,leadingtohigherretentionrates.

However, it's important to note that realizing these benefits requires significant investment and organizational change. Insurance companies will need to address challenges such as data quality, AI ethics, and workforce reskilling to leverage generativeAI'spotentialfully.

4. Assist, Augment, and Automate: AI-Powered Workflow Enhancement

GenerativeAIcanenhanceinsurance workflowsinthreeprimaryways:assist,augment,andautomate.Eachapproachoffers significantpotentialforimprovingefficiency,accuracy,andcustomersatisfactionintheinsuranceindustry.

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

AI-poweredchatbotsandvirtualassistantscanhandleroutinecustomerinquiries,freeinguphumanagentsformorecomplex tasks. IBM reports that implementing AI assistants can reduce call center workload by up to 80% [7]. This significant reduction not only improves operational efficiency but also enhances customer experience. For instance, Allstate's virtual assistant,ABIe,handlesover25,000customerinquiriespermonth,witha75%successfulresolutionrateonthefirstattempt [7].

Moreover,AIassistantscanprovide24/7service,which iscrucialinanindustrywhere56%ofcustomersexpectround-theclock availability [8]. These AI systems can also reduce average handling time (AHT) for customer queries by up to 40%, improvingcustomersatisfactionandsavingtheinsuranceindustryupto$8billionannually[8].

AI can provide real-time insights to underwriters, helping them make more informed decisions. For example, an AI system analyzing property data could flag potential risks that a human underwriter might overlook. This augmentation can lead to moreaccurateriskassessmentsandfairerpricing.

A McKinsey study found that AI-augmented underwriting can improve combined ratios by 5-10 percentage points [8]. In practice,AXAXL'simplementationofAIinitsunderwritingprocessresultedina20%reductioninlossratiosforcertainlines ofbusiness[7].

AIaugmentationalsoextendstoclaimsprocessing.InsurersusingAI-poweredimagerecognitionforcardamageassessment report up to 95% accuracy, reducing the need for in-person inspections by 80% [8]. This speeds up the claims process and significantlyreducesoperationalcosts.

AIcanfullyautomateclaimstriageandinitialassessmentsinsuitableareas.AcasestudybyLemonadeInsuranceshowedthat their AI, Jim, could settle simple claims in as little as 3 seconds [7]. This level of automation can dramatically reduce claims processingtimesandcosts.

The potential for automation extends beyond claims. AI can automate up to 60% of back-office processes in policy administration, potentially saving $10-15 billion annually for the U.S. insurance industry [8]. For instance, Japanese insurer Fukoku Mutual Life Insurance replaced 34 employees with an AI system for calculating payouts, expecting to increase productivityby30%andsave$1.1millionannually[7].

However,it'scrucialtonotethatautomationshouldbeimplementedjudiciously.While25-30%ofinsurancetaskshavehigh automationpotential,humanoversightremainsessentialforcomplexcasesandtoaddressethicalconsiderations[8].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Table2:ImpactofAI-PoweredWorkflowEnhancementinInsurance[7,8]

Generative AI can benefit various roles within the insurance industry, transforming how different personas operate and interactwithcustomers.Let'sexplorehowAIimpactsthreekeyroles:agents,underwriters,andclaimsmanagers.

AIcangenerate personalizedpolicyrecommendationsandassistincross-sellingopportunities,significantlyenhancingagent productivity. A study by Capgemini found that AI-assisted agents saw a 20% increase in sales productivity [9]. This improvementislargelyduetoAI'sabilitytoanalyzecustomerdataandprovidetailoredrecommendationsinreal-time.

Forinstance,PingAnInsuranceinChinautilizesAItoprovideitsagentswith"smartcustomerprofiles"thatofferinsights into customer preferences andpotential needs. Thishasresultedina 17%increaseinrevenue peragentanda 32%reductionin agentturnover[6].

Moreover,AI-poweredchatbotscanhandleupto80%ofroutinecustomerinquiries,freeingagentstofocusonmorecomplex tasks and high-value interactions. State Farm's implementation of conversational AI has led to a 31% increase in quote completionsanda15%reductionincallcentervolume[9].

AI models can analyze vast datasets to provide more accurate risk assessments, revolutionizing the underwriting process. SwissReestimatesthatAI-poweredunderwritingcouldreducelossratiosbyupto5percentagepoints[6].Thisimprovement translatestobillionsinpotentialsavingsforlargeinsurers.AI'simpactonunderwritingismultifaceted:

1. Speed: AI can process applications 5-10 times faster than traditional methods. AXA XL reported reducing underwritingtimeforsomecommercialpropertypoliciesfrom3weekstojust3daysusingAI[9].

2. Accuracy: AI can provide more comprehensive risk assessments by analyzing a broader range of data sources, including unstructured data like social media posts and satellite imagery. Munich Re's implementation of AI in propertyunderwritinghasimprovedlossratioaccuracyby35%[6].

3. Consistency: AI ensures uniform application of underwriting guidelines, reducing human bias. Prudential Financial reporteda26%improvementinunderwritingconsistencyafterimplementingAI[9].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Automated claims processing can significantly reduce turnaround times, improving operational efficiency and customer satisfaction.ZurichInsurancereporteda40%reductioninclaimsprocessingtimeafterimplementingAIsolutions[6].

TheimpactofAIonclaimsmanagementissubstantial:

1. FraudDetection:AIalgorithmscanidentifypotentiallyfraudulentclaimswithupto95%accuracy.ShiftTechnology's AIsolutionhelpedamajorEuropeaninsurerdetect$12millioninfraudulentclaimsinitsfirstyearofimplementation [9].

2. TriageandAssessment:AIcanautomaticallycategorizeandprioritizeclaims,speedinguptheprocess.Lemonade'sAI Jimcansettlesimpleclaimsinaslittleas3seconds,whilecomplexcasesarequicklyroutedtohumanadjusters[6].

3. DamageEstimation:ComputervisionAIcanassessvehicledamagefromphotos,providingaccuraterepairestimates in minutes. Mitchell International's AI-powered solution is within 2% accuracy of human adjusters' estimates and 4 timesfaster[9].

By serving these multiple personas, generative AI is improving individual roles and transforming the entire insurance value chain. The technology enables more personalized customer interactions, accurate risk assessments, and faster claims processing,ultimatelyimprovingcustomersatisfactionandbusinessoutcomes.

However,it'scrucialtonotethatsuccessfulAIimplementationrequirescarefulchangemanagementandemployeeupskilling. A survey by Accenture found that 74% of insurance executives believe that AI will significantly change their job roles in the next3-5years[6].Therefore,insurersmustinvestintrainingprogramstoensuretheirworkforcecaneffectivelycollaborate withAIsystems.

As AI becomes more integrated into insurance operations, ensuring its safety, reliability, and relevance is paramount. The stakes are high, with the global AI in the insurance market projected to reach $45.74 billion by 2028 [10]. Implementing AI responsiblyiscrucialformaintainingtrustandcomplianceinthisrapidlyevolvinglandscape.

Keyconsiderationsinclude:

Implementing robust data governance frameworks:

Maintainingdata qualityandsecurityiscritical forAIperformanceandregulatory compliance.AstudybyVeritasfoundthat 86% of organizations have concerns about managing data for AI and machine learning [10]. Insurers must implement comprehensivedatagovernancestrategiestoaddressthesechallenges.

Forexample,Allianzhasimplementedaglobaldatagovernanceframeworkthatincludesdataqualitymetrics,lineagetracking, andregulardataaudits.Thisapproachhasimprovedtheirdataaccuracyby25%andreduceddata-relatederrorsinAImodels by30%[11].

AImodelscaninadvertentlyperpetuateoramplifybiasespresentintrainingdata.AstudybytheBrookingsInstitutionfound that32%oflargeU.S.insurersuseAImodelsthathavenotbeenthoroughlytestedforbias[11].Regularauditsareessentialto identifyandmitigatetheseissues.

ProgressiveInsuranceconductsquarterlyauditsofitsAImodels,whichhasledtoa15%improvementinmodelaccuracyand a40%reductioninidentifiedbiasesovertwoyears[10].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Developing explainable AI systems:

Transparency in AI decision-making is crucial for both regulatory compliance and customer trust. A survey by Accenture foundthat73%ofinsurancecustomersarewillingtosharemorepersonaldataiftheyunderstandhowit'sbeingused[11].

Swiss Re has developed an "Explainable AI" framework that provides clear rationales for AI-driven underwriting decisions. ThishasimprovedcustomeracceptanceofAI-drivendecisionsby35%andreducedcomplaintsrelatedtoAIby28%[10].

Staying compliant with regulations:

AsAIadoptionincreases,sodoesregulatoryscrutiny.TheEU'sproposedAIActandupdatestoexistingregulationslikeGDPR willhavesignificantimplicationsforinsurersusingAI.

A KPMG survey found that 75% of insurance executives believe AI will significantly impact regulatory compliance in the comingyears[11].Toaddressthis,manyinsurersareproactivelydevelopingAIgovernanceframeworks.

Forinstance,AXAhasestablishedanAIEthicsCommitteeandimplementedanAIEthicsFrameworkthatcoversallaspectsof AIdevelopmentanddeployment.Thisproactiveapproachhashelpedthemachievea95%complianceratewithemergingAI regulations[10].

Ensuring AI relevance and adaptability:

AI models must remain relevant in a rapidly changing environment. The COVID-19 pandemic highlighted the importance of adaptableAIsystems,asmanymodelsstruggledwithsuddenshiftsindatapatterns.

Munich Re has implemented a "continuous learning" approach for their AI models, allowing rapid retraining based on new data. This approach helped them maintain model accuracy within 5% of pre-pandemic levels despite significant changes in riskpatterns[11].

Cybersecurity considerations:

As AI systems become more central to insurance operations, they also become attractive cyberattack targets. A BlackBerry reportfoundthat41%ofinsurersexperiencedacybersecurityincidentrelatedtotheirAIsystemsinthepastyear[10].

Generali has implemented a comprehensive AI cybersecurity framework to address this, including adversarial testing of AI models and enhanced encryption of AI-related data. This approach has reduced AI-related security incidents by 60% yearover-year[11].

Toachievemeaningfulimpact,insurancecompaniesmuststrategicallyscaletheirAIimplementations.Thepotentialrewards aresubstantial, withDeloitte estimating thatsuccessful AIimplementationcould leadto 20-40%cost savingsacross various insuranceoperations[12].However,scalingAIeffectivelyrequiresawell-plannedapproachencompassingseveralkeyareas:

7.1. Identifying high-value use cases across the organization:

Insurersneedtoprioritize AIinitiativesthat offer the greatestpotential impact.A studybyMcKinseyfoundthatfocusingon high-valueusecasescanacceleratetimetovalueby30-50%[13].

For example, Ping An Insurance in China identified underwriting and claims processing as high-priority areas for AI implementation. By focusing on these areas, they achieved a 90% accuracy rate in claim decisions and reduced the average timeforautoinsuranceclaimsfrom5-10daysto30minutes[12].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

7.2. Investing in the necessary infrastructure and talent:

Scaling AI requires significant investment in both technology and human capital. According to a survey by Willis Towers Watson,62%ofinsurersplantoincreasetheirAI-relatedtechnologyspendingbymorethan5%annuallyoverthenextthree years[13].

AXA,forinstance,invested€1billioninitsdigitaltransformation,includingAIinitiatives.Thisinvestmentincludedcreatingan AICenterofExcellenceandhiringover500datascientistsandAIspecialists.Asaresult,AXAhasseena17%improvementin customersatisfactionscoresanda20%reductioninoperationalcosts[12].

7.3. Establishing clear metrics for measuring ROI:

Insurers need robust methodsfor measuringAI'simpactto justify ongoinginvestment and guidescaling efforts.Areport by Accenture found that insurers with clearly defined AI ROI metrics were 3.5 times more likely to achieve returns exceeding theirexpectations[13].

Allianz has implemented a comprehensive AI performance dashboard that tracks process automation rates, prediction accuracy,andcustomersatisfactionscores.Thisapproachhashelpedthemachievea30%improvementinAIprojectsuccess ratesanda25%increaseinoverallAIROI[12].

7.4. Developing a scalable AI architecture:

Insurersneedflexible,scalableAIarchitecturestosupportwidespreadAIadoption.Gartnerpredictsthatby2025,70%ofnew AIprojectswillbedevelopedusingpre-trainedAImodelsasbuildingblocks,significantlyacceleratingscalingefforts[13].

Progressive Insurance has adopted a microservices-based AI architecture that allows for rapid deployment and scaling of AI modelsacrossdifferentbusinessfunctions.ThisapproachhasreducedtheirAImodeldeploymenttimeby60%andincreased theirabilitytoscalesuccessfulAIinitiativesby40%[12].

7.5. Fostering a data-driven culture:

Successful AI scaling requires a shift towards a more data-driven organizational culture. A study by MIT Sloan Management Reviewfoundthatcompanieswithastrongdatacultureare3.2timesmorelikelytoreportsignificantbusinessbenefitsfrom AIinitiatives[13].

Zurich Insurance has implemented a company-wide "Data Science Academy" to upskill employees across all levels. This initiativehasresultedina45%increaseinemployeedataliteracyanda30%increaseinbusiness-ledAIinitiatives[12].

7.6. Ensuring ethical AI scaling:

As AI implementations scale, ensuring ethical use becomes increasingly critical. A survey by KPMG found that 75% of insuranceexecutivesbelieveAIwillsignificantlyimpactregulatorycomplianceinthecomingyears[13].

Liberty Mutual has established an AI Ethics Review Board to oversee the ethical implications of their AI scaling efforts. This proactiveapproachhashelpedthemmaintaina98%complianceratewithAIregulationsandimprovedcustomertrustscores by22%[12].

7.7. Leveraging ecosystem partnerships:

Scaling AI often requires collaboration with external partners. Accenture reports that insurers leveraging ecosystem partnershipscanacceleratetheirAIscalingeffortsbyupto50%[13].

Forexample,MunichRehaspartneredwithAIstartupsandtechgiantstoenhanceitsAIcapabilities.Thesepartnershipshave enabledittoreducenewproductdevelopmenttimeby40%andimprovetheaccuracyofitsriskmodelsby25%[12].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Astrategic,step-by-stepapproachforadoptinggenerativeAIininsuranceiscrucial forsuccess.Accordingtoa studybyMIT Sloan Management Review and BCG, companies that take a strategic approach to AI adoption are 7 times more likely to see significantfinancialbenefits[14].Here'sadetailedroadmap:

8.1. Assess current processes and identify AI opportunities:

StartbyconductingacomprehensiveanalysisofexistingprocessestoidentifyareaswhereAIcanaddthemostvalue.Asurvey by Accenture found that 84% of insurance executives believe that AI will significantly change the way they gain information fromandinteractwithcustomers[15].

For instance, Zurich Insurance used process mining techniques to analyze their claims handling procedures, identifying bottlenecks and inefficiencies. This analysis revealed potential for a 40% reduction in claims processing time through AI implementation[14].

8.2. Develop a clear AI strategy aligned with business goals:

CreateastrategicplanthatalignsAIinitiativeswithoverallbusinessobjectives.McKinseyreportsthatcompanieswithaclear AIstrategyare1.7timesmorelikelytobeAIhighperformers[15].

AXA, for example, developed a comprehensive "Data for Good" strategy that aligns their AI initiatives with their corporate social responsibility goals. This approach has not only improved their AI ROI by 25% but also enhanced their brand reputation,witha15%increaseinpositivecustomersentiment[14].

8.3. Start with pilot projects in non-critical areas:

Begin with small-scale pilot projects to test AI capabilities and build organizational confidence. Gartner recommends that organizationsstartwithatleastthreeAIprojectstoincreasethechancesofsuccess[15].

LibertyMutualinitiatedanAIchatbotpilotforhandlingsimplecustomerqueries.Thepilotdemonstrateda30%reductionin callcentervolumeanda20%improvementincustomersatisfactionscores,providingastrongcaseforwiderimplementation [14].

8.4. Gradually expand to more complex use cases:

Aspilotprojectsprovesuccessful,expandAIimplementationtomorecomplexand critical areasofthebusiness.Areportby Deloittefoundthatinsurerswhoadoptthisgradualapproachare2.5timesmorelikelytoachievesignificantvaluefromtheir AIinitiatives[15].

Allianz started with AI-powered fraud detection in auto insurance claims and gradually expanded to more complex underwriting tasks. This phased approach led to a 60% improvement in fraud detection rates and a 15% reduction in loss ratiosoverthreeyears[14].

8.5. Continuously monitor, evaluate, and refine AI systems:

ImplementrobustmonitoringandevaluationprocessestoensureAIsystemsremaineffectiveandrelevant.IBMreportsthat companiesthatregularlyrefinetheirAImodelsseea35%improvementinmodelaccuracyovertime[15].

Progressive Insurance established an AI Performance Center that continuously monitors their AI models' performance. This approach has enabled them to improve model accuracy by 22% year-over-year and quickly identify and address potential biases[14].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

8.6. Invest in employee training and change management:

Ensure that employees are equipped to work alongside AI systems effectively. A study by PwC found that 60% of insurance executivescitelackofAIskillsasamajorbarriertoimplementation[15].

Generali implemented a comprehensive "AI Academy" program to upskill their workforce. This initiative resulted in a 40% increaseinAIliteracyamongemployeesanda25%reductioninresistancetoAI-drivenchanges[14].

8.7. Ensure ethical AI implementation:

Develop clear guidelines for ethical AI use. The IEEE Global Initiative on Ethics of Autonomous and Intelligent Systems providesaframeworkforethicalAIdevelopment[15].

8.8. Foster cross-functional collaboration:

Encourage collaboration between IT, data science teams, and business units. McKinsey reports that companies with strong cross-functionalcollaborationare1.5timesmorelikelytoreportsuccessfulAIadoption[14].

8.9. Establish clear governance structures:

Create dedicated AI governance bodies to oversee implementation. Swiss Re's AI Governance Framework has helped them achieve95%compliancewithAIregulationsandimprovestakeholdertrustby30%[15].

8.10. Plan for scalability:

DesignAIsystemswithscalabilityinmindfromtheoutset.AccenturefoundthatinsurerswithscalableAIarchitecturesare3 timesmorelikelytoachievefull-scaleAIimplementation[14].

ThefutureofAIintheinsuranceindustrypromisesrevolutionaryadvancementsthatwillreshapethesector.Emergingtrends in AI, such as federated learning and quantum machine learning, are set to drive even greater innovations. According to a report by PwC, AI is expected to contribute up to $15.7 trillion to the global economy by 2030, with the insurance sector poisedtobeoneofthemajorbeneficiaries[16].

9.1. Federated Learning:

FederatedlearningallowsAImodelstobetrainedacrossmultipledecentralizeddevicesorserversholdinglocaldata samples withoutexchangingthem.Thistechniqueaddressesprivacyconcernsandregulatorycomplianceissues,particularlycrucialin theinsuranceindustry.

AstudybyGartnerpredictsthatby2025,50%oflargeinsurerswillusefederatedlearningtoovercomedatasilosandprivacy concerns [17]. For instance, AXA has initiated a federated learning project that allows them to train AI models on customer data from multiple countries without violating data privacy regulations. This approach has improved their risk assessment accuracyby30%whilemaintainingstrictdataprivacystandards[16].

9.2. Quantum Machine Learning:

Quantummachinelearning leveragesquantumcomputingtoprocesscomplexcalculationsexponentiallyfasterthanclassical computers.Thistechnologycouldrevolutionizeriskmodelingandactuarialcalculationsintheinsuranceindustry.

IBM estimates that quantum computing could lead to a 100-1000x speedup in certain machine learning tasks [17]. In collaboration with quantum computing startup IQM, Allianz is exploring quantum algorithms for portfolio optimization and riskmanagement.Earlyresultssuggestapotential40%improvementincomputationalefficiencyforcomplexriskcalculations [16].

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

Long-termeffectsoftheseandotherAIadvancementsinclude:

Hyper-Personalized Insurance Products:

AIwillenableinsurerstoofferhighlypersonalizedproductsbasedonindividualriskprofilesandbehaviors.SwissRepredicts thatby2030,50%ofallinsuranceproductswillbedynamicallypricedandpersonalizedinreal-time[17].

For example, Vitality, a health and life insurer, uses AI and IoT devices to offer personalized premiums based on customers' healthbehaviors.Thisapproachhasledtoa18%reductioninmortalityratesamongtheirpolicyholdersanda30%increasein customerengagement[16].

Real-Time Risk Assessment:

Advanced AI algorithms, coupled with IoT devices and big data, will enable continuous, real-time risk assessment. McKinsey projectsthatby2030,95%ofautoinsurancepremiumswillbebasedontelematicsanddriverbehaviordata[17].

Progressive'sSnapshotprogram,whichusesAItoanalyzedrivingbehaviorinreal-time,hasalreadyshownpromisingresults. Participants have seen an average premium reduction of 31%, while Progressive has improved its loss ratio by 15% in this segment[16].

AI will shift the insurance model from reactive to proactive, focusing on preventing claims before they occur. Accenture estimatesthatAI-drivenpredictivemaintenancecouldreducemaintenancecostsbyupto30%andbreakdownsbyupto70% inthepropertyandcasualtyinsurancesector[17].

ZurichInsurancehasimplementedanAI-poweredsystemthatanalyzessensordatafromcommercialbuildingstopredictand preventwaterdamage.Thissystemhasreducedwater damageclaimsby45%and savedanestimated$100millioninclaim costsovertwoyears[16].

Advanced AI systems will automate much of the underwriting process, leading to faster, more accurate risk assessments. Deloitte predicts that by 2030, 90% of underwriting will be automated for personal lines and small-commercial insurance [17].

Ping An's AI underwriting system has already shown remarkable results, reducing underwriting time from 5 days to 10 minuteswhileimprovingaccuracyby90%[16].

Ethical AI and Explainable AI:

AsAIbecomesmoreprevalent,therewillbeanincreasedfocusonethicalAIpracticesandtheabilitytoexplainAIdecisions. TheIEEEGlobalInitiativeonEthicsofAutonomousandIntelligentSystemspredictsthatby2025,allmajorinsurerswillhave dedicatedAIethicsboards[17].

Allianz has already established an AI Ethics Review Board and implemented explainable AI techniques in their claims processing. This has resulted in a 25% reduction in customer complaints related to AI decisions and improved regulatory complianceby40%[16].

Inconclusion,generativeAIpresentsatransformativeopportunityfortheinsuranceindustry,offering significantpotentialto enhance efficiency, accuracy, and customer satisfaction across various operations. From streamlining claims processing and improvingunderwritingaccuracytoenablingpersonalizedcustomerinteractionsandpredictiveriskassessment,AI'simpact isbothfar-reachingandprofound.However,successfulAIintegrationrequirescarefulplanning,substantialinvestment,anda commitmenttoethicalimplementation.Insurersmustnavigatechallengesrelatedtodataquality,regulatorycompliance,and

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072

workforce transformation while staying attuned to emerging trends such as federated learning and quantum machine learning.Asthe insurancelandscapeevolves,companiesthatsuccessfullyleverage AItechnologieswill be well-positionedto leadtheindustry,offeringinnovativeproductsandsuperiorcustomerexperiences.WhilethepathtofullAIintegrationmaybe complex,thepotentialrewardsintermsofincreasedprofitability,operationalefficiency,andcustomersatisfactionmakeit an essentialjourneyforinsurersinthedigitalage.

References:

[1] Swiss Re Institute, "World insurance: riding out the 2020 pandemic storm," Sigma, no. 4/2020, July 2020. [Online]. Available:https://www.swissre.com/institute/research/sigma-research/sigma-2020-04.html

[2] PwC, "Top Issues: Artificial Intelligence," PwC, Jun. 2016. [Online]. Available: https://www.the-digital-insurer.com/wpcontent/uploads/2016/06/716-pwc-top-issues-artificial-intelligence.pdf

[3]McKinsey&Company,"Thefutureoflifeinsurance:Reimaginingtheindustryforthedecadeahead,"Sept.2020.[Online]. Available: https://www.mckinsey.com/industries/financial-services/our-insights/the-future-of-life-insurance-reimaginingthe-industry-for-the-decade-ahead

[4] Deloitte, "2022 insurance industry outlook," 2021. [Online]. Available: https://www2.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/insuranceindustry-outlook.html

[5] S. Srinivasan, "Artificial Intelligence in Insurance Market," Fortune Business Insights, Apr. 2021. [Online]. Available: https://www.fortunebusinessinsights.com/artificial-intelligence-ai-in-insurance-market-104469

[6] McKinsey & Company, "Insurance 2030 The impact of AI on the future of insurance," Mar. 2021. [Online]. Available: https://www.mckinsey.com/industries/financial-services/our-insights/insurance-2030-the-impact-of-ai-on-the-future-ofinsurance

[7] IBM, "How generative AI delivers value to insurance companies and their customers," 2023. [Online]. Available: https://www.ibm.com/think/topics/generative-ai-for-insurance

[8] McKinsey & Company, "Are Asian Insurers Keeping Up with AI Advancements?" May 2023. [Online]. Available: https://www.mckinsey.com/industries/financial-services/our-insights/insurer-of-the-future-are-asian-insurers-keeping-upwith-ai-advances

[9] Capgemini, "World Insurance Report 2021," 2021. [Online]. Available: https://www.capgemini.com/news/pressreleases/world-insurance-report-2021-2/

[10] Deloitte, "Artificial Intelligence and the Insurance Industry," 2021. [Online]. Available: https://www.deloitte.com/uk/en/services/audit-assurance/blogs/artificial-intelligence-and-the-insurance-industry.html.

[11] Infosys BPM, "The game-changing influence of AI in the insurance industry," Infosys BPM, Feb. 15, 2023. [Online]. Available:https://www.infosysbpm.com/blogs/insurance/game-changing-influence-of-ai-in-the-insurance-industry.html.

[12]Snowflake,"TheRoleofAIinInsurance.”[Online].Available:https://www.snowflake.com/trending/role-ai-insurance

[13] Forbes, "How AI Is Changing The Game In Insurance," Sept, 2022. [Online]. Available: https://www.forbes.com/sites/garydrenik/2022/09/27/how-ai-is-changing-the-game-in-insurance/

[14] MIT Sloan Management Review and BCG, "Winning With AI," 2019. [Online]. Available: https://sloanreview.mit.edu/projects/winning-with-ai/

[15] Swiss Re, "The future of AI in insurance," Jul, 2023. [Online]. Available: https://www.swissre.com/riskknowledge/advancing-societal-benefits-digitalisation/future-ai-insurance.html

International Research Journal of Engineering and Technology (IRJET) e-ISSN:2395-0056

[16] PwC, "Sizing the prize: What's the real value of AI for your business and how can you capitalise?," 2018. [Online]. Available:https://www.pwc.com/gx/en/issues/analytics/assets/pwc-ai-analysis-sizing-the-prize-report.pdf

[17] Gartner, "Predicts 2021: Artificial Intelligence Core Technologies," 2020. [Online]. Available: https://www.gartner.com/en/documents/3994810

Volume: 11 Issue: 07 | July 2024 www.irjet.net p-ISSN:2395-0072 © 2024, IRJET | Impact Factor value: 8.226 | ISO 9001:2008 Certified Journal | Page524