2001-2024 | SIXTH EDITION

ISSN: 2688-383X (print) | 2688-3848 (online) ISBN: 978-1-970078-51-0

Published by: Irving Levin Associates, LLC P.O. Box 1117 New Canaan, CT 06840

Phone (203) 846-6800 | Fax (203) 846-8300 info@levinassociates.com

Managing Editor: Advertising:

Benjamin Swett Cristina Blazek-Hearty

© 2024 Irving Levin Associates, LLC

All rights reserved. Reproduction or quotation in whole or part without permission is forbidden. First Class Postage is paid at New Canaan, CT.

This publication is not a complete analysis of every material fact regarding any company, industry or security. Opinions expressed are subject to change without notice. Statements of fact have been obtained from sources considered reliable but no representation is made as to their completeness or accuracy.

POSTMASTER: Send address changes to Irving Levin Associates, LLC P.O. Box 1117, New Canaan, CT 06840

Irving Levin Associates Publications and Services

Subscriptions & Memberships

Long-Term Care:

LevinPro LTC

LevinPro LTC News

The SeniorCare Investor

Health Care:

LevinPro HC

The seniors housing and care merger and acquisition market has grown tremendously since the turn of the century in terms of deal and dollar volume but faces some potential and fundamental risks that buyers need to know.

The senior care industry has been through the ringer in the last several years but is still poised to see enormous growth for the rest of the decade. Several challenges shook the industry to its foundations, from the pandemic and a staffing crisis to soaring inflation and capital costs. However, demographic tailwinds, little new construction, attractive pricing for properties and a general belief in the industry's future success has led to record-breaking M&A volume that has only strengthened throughout 2024.

That belief is tempered somewhat by a few significant risks facing the industry, hence the lower property pricing providing some safety margin for buyers today. First, although it is fading into memory, the COVID-19 virus targeted the sick, frail and elderly, prompting a negative perception of communal living among seniors by both seniors themselves and their adult children, not helped by an unfriendly and oftenmisleading media. The long-term impact on demand as a result of this perception is not yet known.

Second, rampant inflation combined with a calamitous staffing shortage in the pandemic's aftermath led to significantly higher wages and excessive use of expensive agency labor. These factors permanently cut into the profitability of the vast majority of seniors housing and care properties in operation. And historic resident rate increases of as much as 6%, 8% or even 12% mostly benefitted the higher quality, "A" properties. High rate increases also serve to price out a portion of the population each time and/or potentially lead residents to question the value proposition of seniors housing if the quality and services do not improve in turn. Nevertheless, most properties will not be able to catch up to rising expenses and return to their pre-pandemic operating margins.

Lastly, there is a worry that baby boomers could reject

much of the current product available today. Aging physical plants, smaller room configurations or the day-to-day activities and services offered in seniors housing today may not appeal to many boomers, who have more tools to live comfortably, sociably and healthily at home than ever before. Or they may choose active adult communities over traditional independent living. Either way, the penetration rate and average length of stay could decline, and should be a consideration to any investor entering the industry.

However, new construction activity has slowed to near-historic lows, meaning that the existing seniors housing and skilled nursing units and beds will likely be better occupied and more valuable in the coming years. Capital that would otherwise be directed to development will be funneled to M&A. And the attractive yields and demographic trends of senior care, compared with other real estate asset classes, will continue to attract investors to the industry.

Ben Swett is the Managing Editor of The SeniorCare Investor, The Senior Care Acquisition Report and the LevinPro LTC & HC products at Irving Levin Associates. Since joining the company in 2014, he has reported on the senior care M&A, finance, and development markets. He has a BA in History from Hamilton College and an MBA in Finance from UConn.

Contact Information: editorial@levinassociates.com 203-846-6800 www.levinassociates.com

Long-term care and health care investment intelligence. Gain an informational edge with focused news briefs, expert analysis, and in-depth deals intelligence spanning long-term care and health care industries.

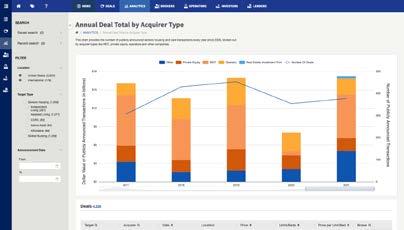

The number of mergers and acquisitions steadily increased throughout the 2010s in the seniors housing and care industry, until the pandemic led to an understandable drop in M&A activity. Dealmaking quickly rebounded to record highs and is on track to shatter records in 2024.

Investor interest in the senior care sectors has boomed since the Great Financial Crisis, rising steadily from 89 publicly announced transactions in 2009 to a then-high of 365 deals in 2015, according to statistics from LevinPro LTC. After a couple of years of lower activity, deal making took off again in 2018, reaching 436 deals (a 41% increase over the 308 transactions announced in 2017) and peaking at 459 deals in 2019. Including transactions that were confidentially disclosed or took place off market, that total would be even higher.

The buying frenzy came to a temporary hiatus for a reason nobody could have predicted. The first confirmed case of COVID-19 was announced early in the first quarter of 2020 (January 21st, officially), and investors halted much of their activity by the end of the first quarter and through Q3:20. COVID-19 raged through the population (especially the frail and elderly), lockdowns forced providers to shut their doors,

unemployment soared, political uncertainty persisted through the summer and fall, and much was still unknown about the virus or the prospect for vaccines.

The M&A market rebounded quickly, resulting in 363 deals in 2020, which was the fourth-highest deal total ever at the time, before buyers announced 456 deals in 2021 and 559 deals in 2022, the busiest year on record. That year could have turned out more active, as the first half of 2022 annualized came to 588 deals, which would have been an annual record by nearly 100. But then interest rates started to rise, slowing acquisition demand and lowering prices. Calendaryear 2022 cooled from that initial pace, ending with 559 deals announced in the year (still a record), and the "relative" slowdown continued into 2023, with just 219 transactions reported in the first half of the year, for an annualized total of 438 deals.

However, by the middle of 2023, interest rates had

stabilized, albeit at a much higher level than any time in the previous 10 years. That rate stability, as well as the belief that inflation would not be solved quickly and that rates would stay elevated for longer than most originally thought, led many owners with a time horizon on their properties (either because of poor operations, expiring fund life or maturing debt) to sell instead of holding out for higher prices.

So, M&A activity reached new heights starting at the end of 2023. The year finished with 510 transactions, averaging 46 transactions per month in the second half of the year as opposed to 39 deals per month in the first half of 2023. And the first half of 2024 recorded 335 deals, for a monthly average of 56 deals. Annualized, 2024 activity would come to 670 transactions, which would break the previous record (559 deals in 2022) by more than 100 deals.

The size of deals also dropped with the rise in interest rates, and buyers were not willing to make big bets and sellers were less willing to divest large portfolios when values were low. The lack of large deals can actually help explain the record number of transactions being announced in 2024, as a large portfolio deal that would have once included 10, 20 or more properties in a single deal (and entered once in the M&A database) is now being divided into two, three, five or even 10 separate deals (and entered 10 times in the database).

Breaking up portfolio deals helps attract more and different groups of buyers to the bidding table for the smaller pieces. The portfolios can also be divided between the performing properties, which can usually be financed with debt at a higher price, and the non-performing ones that usually must be purchased with cash at a steep discount.

Dollar volume also remained low in the first half of 2024 at $4.2 billion, which, annualized, would reach $8.4 billion and be the second-lowest dollar volume since 2009. This can be explained by a combination of smaller deals and lower values for properties.

In the last several years, only one transaction is in the top-10 since 2001, based on purchase price, which was the 2021 sale of DigitalBridge Group’s healthcare assets for $3.21 billion. The portfolio consists of 53 managed seniors housing communities (4,756 units and 69.4% occupied in Q1:2021, on average), 106 managed MOBs (3.8 million square feet and 82.6% occupied as of March 31, 2021), 65 triple-net leased seniors housing communities (3,534 units and 70.8% occupied in Q4:20, on average), 83 triple-net skilled nursing facilities (9,723 beds and 68.2% occupied in Q4:20) and nine triple-net hospitals.

There were no mega deals (over $1 billion) announced in 2024, either. The largest was close, however, when Welltower announced that it was paying $969 mil-

lion, or $248,000 per unit, for a portfolio of 25 active adult communities. With an average age of less than eight years, these communities comprise 3,900 units, mostly concentrated in the Pacific Northwest, with a near-60% operating margin. Welltower paid in cash and with $523 million of below-market rate debt.

Another publicly traded company made the nexthighest priced deal in the United States. National HealthCare Corporation entered a purchase and sale agreement to acquire the White Oak Senior Living 15-property, majority-SNF portfolio for $221.4 million, or $97,000 per bed/unit.

Nearly all industries have seen a dearth of mega deals because of the difficult debt markets. But within senior care, the change has been more pronounced in the seniors housing market. The skilled nursing sector has continued to see numerous portfolio deals (although nothing approaching $500 million or $1 billion), as buyers in that space believe they can more easily turn around operations through better referrals, patient coding and new contracts with often-related ancillary service businesses.

And SNF buyers have had a larger stable of lenders willing to deploy capital at decent leverage because of the believed operational strength of their operating partners and in their ability to increase revenues.

The strength of the skilled nursing market, from a valuation perspective, surprised many in the immediate wake of the pandemic. That is because facilities were often caring for the sickest and frailest populations who were especially vulnerable to the coronavirus, they received a lot of negative attention in the early days of the pandemic because of outbreaks and higher numbers of patient deaths, and they saw census plunge due to lack of elective surgeries and home health options (most of which were/are inappropriate for patients that require skilled nursing care). Many proclaimed the death of the industry.

However, with the return of elective surgeries, strong referral relationships that filled beds and the lingering benefits of the PDPM (Patient Driven Payment Model) rule change at the end of 2019, investors still saw a huge opportunity for profit in the skilled nursing industry. Investors that could wrap around ancillary services such as therapy, staffing or food services that benefitted from an increased patient population could earn revenues not just from the facilities themselves, adding to their appeal. Bidding wars ensued among investors trying to increase their bed counts, which pushed up prices for skilled nursing facilities to levels never before seen.

Before this opportunity was noticed, the skilled nursing sector’s average price per bed did drop 14% from $93,000 in 2019 to $79,700 in 2020. We had seen larger percentage declines in the past, most recently an 18% decline from the $99,200 per bed average price in 2016 to $81,355 per bed in 2017. Considering the circumstances of 2020, there could have been a steeper fall in average price, with the sale of many ailing facilities by highly motivated owners. Plus, federal and state aid programs prevented many owners from having to sell, leading investment demand for SNFs to outpace supply of facilities and beds available for sale.

That trend was only exacerbated throughout 2021 and into 2022, when the average price per bed rose to $98,000 in 2021 and to $114,200 in 2022, which was a record by some 15% from the next-highest average in 2016.

The sale of Stonerise Healthcare’s 17 skilled nursing facilities in West Virginia was emblematic of the

new market, with an estimated price of more than $315,000 per bed. For a variety of factors, the deal stands out among all the rest, with its geographic concentration, favorable reimbursement environment in West Virginia, relatively young age, high quality facilities and ancillary businesses.

In 2022, interest rates had risen and squeezed the spreads of other real estate sectors like seniors housing and multifamily, leading investors in search of yield to the SNF business, where cap rates have traditionally stuck between 12% and 13.5% in good economic times and bad.

However, sustained high interest rates finally began to eat into SNF valuations in 2023, as lenders pulled back from the market or pushed back on pricing. The operating risks (like the threat of a federal minimum staffing mandate), let alone the capital costs, were just too high to justify the kind of value that the market was consistently seeing. As such, the average price per bed for skilled nursing facilities in the four quar-

Oxford Finance LLC provides capital for growth and development to life sciences and healthcare services companies worldwide.

We have remained a leader in the lending industry because of our financial strength and commitment to be fair, flexible and responsive to the changing needs of our clients.

Providing More Than Monetary Value

Over the years, Oxford has been steadfast in our commitment to:

Offer Flexible Solutions – Ensuring that the loan terms, draw-down period, availability, interest rates, collateral mix and loan amounts meet the expectations and needs of our clients

Approve and Execute Transactions Quickly –Avoiding bureaucratic layers and empowering our professional team to perform a thorough screening, promptly prepare accurate loan documents and close in a timely manner

Establish Personal Relationships – Having a knowledgeable team of experts from our Business Development, Credit & Portfolio and Legal departments dedicated to individual clients from the beginning to the end of each loan transaction

Oxford Overview

• Origination of over $13 billion in loans

• Credit facilities ranging from $5MM to $200MM

• Real estate and cash flow term loans

• Revolving credit facilities

• Headquarters in Alexandria, Virginia, with offices in California, and the greater Boston and New York City metropolitan areas

Offering Multiple Financial Products

REAL ESTATE TERM LOANS

• Bridge, mini-permanent and mezzanine

• Range from $5MM to $150MM

• Two- to five-year term

• Up to 25-year amortization period, with interest only option

• Delayed draw feature to fund additional acquisitions available in select situations

REVOLVING LINES OF CREDIT

• Asset-based

• Range from $5MM to $50MM

• Two- to five-year term

• Interest only

STRUCTURED PRODUCTS

• Customizable financing solution available to facilitate the acquisition of qualified healthcare properties

• When paired with our traditional Real Estate Term Loan, potential financing up to 95% loanto-cost available

• Buyer retains 100% of ownership

Trazy Maziek

Senior Managing Director, Head of Healthcare Services

Phone: 858.750.2563

tmaziek@oxfordfinance.com

Kevin Harbour

Managing Director, Healthcare Services

Phone: 949.558.3677

kharbour@oxfordfinance.com

Richard Russakoff

Senior Director, Healthcare Services

Phone: 424.252.2845

rrussakoff@oxfordfinance.com

Katherine Thornett

Senior Director, Healthcare Services

Phone: 703.236.2939

kthornett@oxfordfinance.com

ters ended June 2023 dropped 6.5% to $106,800 and another 8% to $97,700 per bed in calendar-year 2023. The four quarters ended June 2024 settled at $91,300 per bed, on average, or close to the prepandemic average of $93,000 per bed in 2019.

Quality and case mix will continue to be a major factor in SNF values, with the introduction of the PDPM reimbursement rule change in October 2019 rewarding those facilities with more medically complex Medicare patients. CMS also announced significant reimbursement rate increases for its traditional Medicare patients, staving off a downward rate readjustment to account for inflationary and labor issues. Most states also provided generous, and needed, increases to Medicaid rates.

For two decades, skilled nursing cap rates continued their general downward trend. However, they did not compress to the degree that seniors housing communities had experienced and largely stayed between 12.0% and 13.5%. The sector maintained that consistency amid more volatile interest rate changes and global economic trends.

During the Great Financial Crisis, the sector saw a moderate increase in cap rate, rising from 12.1% in 2007 to 12.9% in 2008 and peaking at 13.1% in 2010.

Other real estate classes were not so lucky. In the years afterward, the consistently high yields that skilled nursing offered drew investors to the sector, helping to compress the average cap rate to around 12.0%. Incredibly low interest rates after the Great Financial Crisis and abundant capital also contributed to the cap rate compression, but not nearly as much as on the seniors housing side.

Then, the risk of owning and operating a skilled nursing facility shot up as COVID-19 cases and deaths rose across the country, unfortunately all too often in the facilities themselves. And the average cap rate followed, increasing 50 basis points from 12.2% in 2019 to 12.7% in 2020. But then came 2021, when low interest rates combined with high investor demand (and higher prices) depressed the average skilled nursing cap rate below the standard 12.0%-13.5% range to 11.3%, which is the lowest average cap rate ever for the sector.

In 2022, as interest rates started to rise, the average slightly increased to 11.4% and then jumped to 12.9% in 2023, the highest average in more than 10 years. Interest rates settled, and the average cap rate for the four quarters ended June 2024 fell to 12.6%, on average. However, it must be noted that the average cap rate only reflects a portion of the SNFs sold during

$240,000

$220,000

$200,000

$180,000

$160,000

$140,000

$120,000

$100,000

$80,000

$60,000

the year (those with market cap rates), and reflects the financials used to calculate each cap rate, which were almost always trailing figures excluding government aid. Because of the stress on the sector, mostly affecting smaller operators, there were many struggling SNFs that sold in 2023 and 2024 with negative trailing EBITDA that were not included in the cap rate average. Facilities with little positive cash flow that yield very small cap rates would also not have been included in our calculations, since they were not “cap rate” deals but rather “per-bed” deals. This happens every year but was only exaggerated in the last three years. There were simply so few stabilized deals, with market cap rates, that the average cap rate is not totally representative of the recent M&A market.

While pricing remained strong in the SNF space in the years following the pandemic, the average price per unit for seniors housing communities, which include independent living, assisted living and memory care, has steadily declined since 2019. The sector hit a peak back then, with an average of $244,200 per unit in 2019. The market readjusted to a post-COVID world that included staffing shortages, rising expenses and lagging census, dropping the average price per unit by 20% to $196,000 per unit in 2020 and another 7% to $182,300 per unit in 2021.

As the sector started to stabilize post-pandemic, with improving census and resident rate hikes, prices rebounded in 2022, averaging $211,800 per unit. There were also a few more owners of high-quality communities that were tempted off the M&A sidelines knowing that their well-performing properties would command a premium in a market flooded with struggling operations.

However, rising interest rates forced many potential buyers from the market while also lowering the prices that investors and lenders were willing to pay and finance. So the price for seniors housing communities dropped on an apples-to-apples basis, fewer owners of high-quality owners chose to sell and accept a lower price (if they could help it), and the market was flooded with struggling and value-add properties. That combination caused the average price per unit, unsurprisingly, to plummet to $156,300, the lowest average since 2012. The average price per unit continued its descent into 2024, with an average of $140,200 in the four quarters ended June 2024, the lowest level since 2010.

It is important to remember that the average price per unit is derived from the property sales included in the average in a given time period. That is an obvious statement, but in some years you may have an apples-to-apples increase in pricing of certain

Ken Assiran, Managing Director, Senior Housing | Capital Funding Group sponsored content

While recent capital markets challenges have caused many to stop lending with some slowly getting back into the game, Capital Funding Group (CFG) - the original one-stop shop - continues to be an unwavering partner to the national senior healthcare industry and embraces the challenges as opportunities. CFG Managing Director Ken Assiran discusses the latest industry trends, CFG’s entrepreneurial approach to executing solutions for clients, and how CFG supports the industry beyond its financing expertise.

1. What are the latest trends you are seeing with long-term care industry M&A transactions? What trends do you anticipate for the next year?

M&A activity has been steadily rising since the slow start of 2023, with 2024 on track to be a record year in the industry. When it became clear that challenging capital market conditions - higher interest rates and lower leverage - would persist through 2024 and into 2025, those who initially tried to wait out the challenges had to make decisions as debt maturities approached. This sentiment along with the well capitalized groups being opportunistic with discounted acquisitions available in the market has spurred 2024 towards a record setting year in terms of M&A activity. We expect similar trends in 2025, with growing optimism for potential interest rate cuts by the end of 2024 and therefore, increases in M&A activity.

Despite concerns about post-pandemic operating expenses and capital market conditions, the outlook on the industry remains positive over the next year due to the ever-growing demand seen from encouraging demographics and the lack of inventory growth, a result of minimal new construction starts caused by high interest rates and high construction costs. With this, we should continue to see efforts allocated to mergers and acquisitions, away from new construction. However, investors who are well capitalized enough to continue with construction starts and navigate the stringent capital markets will be well positioned in the future to capitalize on the increased demand for senior housing.

Recent capital markets challenges have led many banks to stop or slow lending, but not us. In fact, these conditions have created an opportunity for us to focus on Class A and B deals with strong in-place cash flow. In some cases, lower leverage is needed to ensure projects can support debt. We are also requiring borrowers to use derivatives to mitigate interest rate risk.

We continue to build on our relationships with borrowers and our success providing lending through historically challenging capital market conditions. We leverage our deep industry understanding and creative financing approach to provide bridge loans for long-term agency financings. Our focus has been on converting floating rate bridge debt into long-term, fixed-rate permanent financing with HUD. Although HUD rates have increased significantly, the relative increase is less steep than short-term benchmarks like SOFR. This allows us to help clients refinance in the future. With our flexible capital, we creatively solve for shortfalls on HUD takeouts, easing the burden of rising rates for our clients.

Flexible capital is in large part how we continue to support and lead the M&A markets over the last year. Our one-stop-shop loan offerings allow us to provide subordinate debt, mezzanine loans, and other private credit instruments, which allow us to fill the void left in the capital structure with senior lenders largely dialing back their risk appetite.

3. What sets CFG apart from other healthcare lenders in the space?

We have a holistic viewpoint with everything we do, and our commitment to the industry goes beyond that of your typical lender. We are strong supporters of organizations such as AHCA/NCAL, ASHA, NIC, and actively work with HUD, Congress and state healthcare associations to champion the industry and help develop solutions.

Our leadership team brings extensive experience in senior housing, skilled nursing, and healthcare lending. This expertise allows us to offer financing solutions tailored to the unique needs and goals of our borrowers in the industry.

Further, our CEO, Jack Dwyer, founded Dwyer Workforce Development in 2021. An innovative 501(c)(3), DWD provides Certified Nursing Assistant (CNA) and Geriatric Nursing Assistant (GNA) training, job placement support in skilled nursing and assisted living facilities, need-based wraparound services, and person-centered case management to individuals who lack opportunity and aspire to pursue a career in the healthcare industry. DWD’s mission also alleviates a severe healthcare workforce shortage and improves the lives of seniors.

$280,000

$260,000

$240,000

$220,000

$200,000

$180,000

$160,000

$140,000

$120,000

$100,000

$80,000

communities year over year but still see a decrease in the average price per unit if there were relatively fewer high-quality/high-priced sales included in the average in a given year. For those more granular pricing comparisons, check out the latest edition of The Senior Care Acquisition Report or visit LevinPro LTC

Since the turn of the century, assisted living communities have accounted for the majority of sales and of dollar volume in the overall seniors housing market, and 2024 was yet again no exception, with assisted living representing close to four of every five seniors housing properties sold.

However, it was the smaller independent living side that dragged down the average price per unit for the entire seniors housing sector. A dearth of high-quality IL sales caused the significant drop.

Being a much smaller market compared with assisted living, the independent living sector is prone to more wild swings in its average price per unit, and one or several large transactions with especially high or low prices can have an outsized impact on the average. There was some remarkable stability in the average

price in the years leading up to the pandemic, when the average price hovered between $228,200 per unit and $238,100 per unit, which was possibly a reflection of the sector’s more stable operating environment. However, a few high- or low-priced sales can sway the average price, and the sector has been on a roller coaster since the pandemic, experiencing a significant 24% drop in 2021 to $177,400 per unit followed by a 46% increase in 2022 to $259,400 per unit.

Then, the average dropped by 24% to $196,200 per unit in 2023 and by another 43% to $111,000 per unit in the four quarters ended June 2024. That is the lowest average price per unit for the sector in 20 years and was precipitated by a number of high-quality sales from the first half of 2023 dropping from the average, and almost no high-quality sales replacing them.

Proponents of independent living touted its durability during the pandemic, especially relative to the AL market, since it required fewer staff, catered to a younger, healthier population and did not suffer from the effects of overdevelopment. The sector’s average occupancy hovered around the healthy level of 90.0% just before the pandemic, so it had a larger census cushion to absorb the impacts of COVID-19.

That strong occupancy also gave these communities more flexibility to charge higher rents, resulting in surer financial footing going into the pandemic as well. Independent living is also a lot closer to attracting the oncoming baby boomers, since the average move-in age is theoretically lower than assisted living.

However, occupancy has been slower to rebound across the sector, and the burgeoning active adult sector, which is not a subsector of IL, may be poaching some of IL’s younger potential residents. Once in active adult, it is possible those residents will bypass independent living services and go straight into assisted living or skilled nursing, as needed.

Because active adult communities come with fewer services, they typically charge lower rents than IL. But they usually still offer activities and a better social life than if the seniors just stayed at home, which is a big selling point for IL. Sometime down the road as their resident population ages, active adult communities could begin to add IL-like features, such as communal dining and laundry services and even certain care options. That could have ramifications across the entire seniors housing spectrum.

On the other hand, the rise of active adult could also

prove to be a boon for other seniors housing sectors, including IL, since it gets those elderly adults out of their homes, a major barrier to moving into seniors housing anyway, and out living among their peers, another major draw to seniors housing communities.

As the average price per unit dropped in the IL sector, the average cap rate correspondingly rose. The sector set a record for the lowest average cap rate in 2021 and 2022 at 6.6%, back when interest rates were close to historic lows. However, with rising capital costs and a lower quality of property being sold, on average, the cap rate rose to 7.5% in 2023 and a further 30 basis points to 7.8% in the four quarters ended June 2024.

Anecdotally, the "floor" for cap rates effectively rose to 6.5% or 7% when interest rates were at their peak in 2023 and early 2024, which still did not leave much room for error when a long-term mortgage from Fannie Mae or Freddie Mac carries a 5.5% interest rate, or when acquisition debt far surpasses 6.5%. With those terms and in this current market, most IL investors probably are not using the cap rate when valuing their purchases. And many of the IL deals featured struggling properties that did not have a market cap rate. So, the lack of movement in cap rate is not always

emblematic of the typical IL community that sold in the most recent four-quarter period. However, logic and history dictate that as the price for properties falls, the cap rate correspondingly rises, and that is what is happening in 2024.

In the four quarters ended June 2024, there has been a dearth of major independent living acquisitions, as buyers turned to the more need-based assisted living or popular skilled nursing sectors, or even active adult. Few sellers were willing to accept a higher cap rate for their portfolios, too. The largest IL deal of 2024, so far, totaled $180.5 million and involved Retirement Housing Foundation's 15 seniors housing communities across six states. Acquired by Pacifica Companies, the portfolio comprises 3,200 independent living units, 850 assisted living/memory care units and 563 skilled nursing beds.

The lack of big deals reveals that investors were not confident to make large bets on the independent living space, or that seller expectations in price did not fall accordingly with the rise in capital costs. As a result, few large portfolios were put up for sale because owners could theoretically weather the effects of inflation and staffing shortages (and not turn to an M&A event) better than in assisted living.

Comparing the two main seniors housing sectors, assisted living beating independent living in terms of average price per unit used to be a rare occurrence, but it repeated in three of the last five years. However, the average value of independent living communities sold in the four quarters ended June 2024 dropped so precipitously that it fell below the average for assisted living. The assisted living sector even registered an increase in average price per unit compared with 2023.

Looking forward, there is certainly a case that more “need-based” services will rebound more quickly after the pandemic and amid economic issues, and that a “luxury” such as independent living could be looked over by potential residents deciding to stay home. A drop in home values as a result of higher interest rates may not allow many seniors to feel financially secure enough to cash out and move into an IL community.

On the other hand, a yearning for socialization and the convenience of living in an IL community may actually boost demand in the next several years, unless active adult communities absorb many of those residents. It is too early to tell, but some caution from investors (in the form of a slightly higher cap rate) could be warranted, even for high-quality communities.

Assisted living has received the majority of investor attention for much of the 21st century, for good and bad. After developing a “recession-resistant” reputation, demographic-fueled enthusiasm led to a period of overbuilding in the mid-2010s and decreased occupancy as a result. Increased competition in many markets across the country exacerbated the problems caused by an already-tight labor market, with poaching of key staff an all-too-common and expensive trend. These issues hit lower-end and middle market assisted living communities more, as they could not raise rents as easily to counteract higher wages and rampant discounting. And they left the sector in a more precarious position going into 2020.

The pandemic did take a heavier toll on assisted living communities than independent living, not only because of their older, frailer patients but also for their greater staffing needs. But investor interest still targeted the higher acuity sector, since those communities accounted for four-fifths of the seniors housing communities sold in 2024, so far. Demographics will come to the sector’s aid at some point, but likely not starting until the late-2020s.

In the years following the pandemic, the sector’s aver-

age price remains well below the pre-pandemic high of $248,400 per unit in 2019. It plunged by 30% to $174,700 per unit in 2020 before rising modestly in 2021 to $186,800 per unit and to $195,200 in 2022 as a result of two straight years of post-pandemic performance gains by operators and a higher share of properties sold being “A” quality communities in this sector. Those highest quality communities could charge higher rents, attract and retain staff and did not require major capex to stay competitive, and they sold at a premium as a result.

However, as capital costs soared throughout 2023, owners of those highest quality communities did not see the value of selling because the buyers could not justify the prices for their well performing, “A” quality assets. If they did not have a debt maturity or fund life horizon, or were not bailing out struggling operations, most did not need to sell, and so they stayed on the M&A sidelines. On the other hand, the properties that were selling were often in distress and owned by highly motivated sellers. Buyers have fewer options compared with skilled nursing to quickly turn around operations of a struggling assisted living business and accounted for that fill-up risk and general margin compression. As such, it became a buyer’s market, and the average price per unit plunged to $145,400 per unit in 2023, the lowest average since

2010. Prices did stabilize slightly in the four quarters ended June 2024, with the average rising to $151,600 per unit, but that is still the lowest average value for the sector since 2013, other than 2023. Scarcity of new development, a stabilization (or slight decrease) of interest rates and continued operational improvements across the sector could lead to further pricing increases in assisted living in 2024 and beyond.

Assisted living has come a long way from the throes of the GFC, when average cap rates exceeded 9%, and when 6% cap rates were nearly unheard-of. Despite the numerous risks facing the industry, average cap rate kept declining throughout the pandemic, eventually to 7.5% in 2022. Even during the pandemic, there were still 6% or lower cap rate deals, as buyers clamored for the few stabilized, high-quality deals on the market. But there have been few actual “cap rate deals” involving stabilized assets in 2024.

Soaring interest rates eventually pushed cap rates to their highest level since the early 2010s. The average cap rate spiked to 8.6% in 2023 and by another 20 basis points to 8.8% in the four quarters ended June 2024. Anecdotally, the cap rate "floor" rose to around 7.0% in the first half of 2024, with sub-7% cap rate deals just not making sense in a world with the 10-Year Treasury rate above 4%.

As rates steadily declined in mid-2024, investors and lenders started to see a few sub-7% cap rate deals close, which could spur more owners of high-quality properties to re-enter the M&A market. But the higher cap rates also account for some of the serious and fundamental risks facing the assisted living sector.

Some risks include the aging physical plants of thousands of AL communities across the country, the attractiveness of the current inventory to the future baby boomer customers, the trend towards home health, the affordability factor for middle- and lowermarket seniors, shortening lengths of stay for an older and frailer move-in population, permanently higher labor needs and costs, plus any major, future disruptive event yet to be considered (like a pandemic).

All of these risks could potentially lower the penetration rate for assisted living (and all seniors housing) services and defy many of the all-too-rosy supply and demand projections for the industry. This makes it more important for operators to demonstrate the value of their services and the positive impact on seniors' quality of life, as well as to adapt to the preferences of the boomers. Capital providers will also have to help fund needed capex and conversion projects to meet that need, in addition to investing prudently and with more conservative leverage going forward.

Trusted by investors, advisors, providers, payors, academics, and government agencies to understand the nuances of healthcare investment and consolidation. Gain access to the most detailed healthcare acquisition data available.

Request Demo

From the one-doctor physician practice to a large-cap business, we track all healthcare transactions.

Private Equity

Speed up diligence and sector thesis development research

REITs

Rely on proprietary, privatelysourced valuation data

Deal Database

• Acquirer or target company

• Target sector and subsector

• Acquirer sector

• Acquirer type

• Deal value

• Location

• Key words and phrases

Phone: 203-846-6800 Email: info@levinassociates.com

12 key sectors with drill-downs into physician group specialties, hospital types, behavioral health types, etc.

Our analysts speak to company leaders and key advisors to gain insight on valuations and strategic roadmaps.

Medical Groups

Use data to refine your growth and partnership strategy

Advisors

Track subsectors and identify trends with ease

34,000+ transactions, searchable by:

Key Analytics

Health Systems

Tap extensive hospital M&A data and valuation stats

Academics

Study market structure and consolidation impacts

Easily spot trends with:

• Monthly deal volume by sector

• Top physician group specialties by deal total

• Private equity activity by sector

• Number of hospitals and beds acquired

• Price per bed (hospitals)

• Acquisitions by PE firms and their portfolio companies