ELITE WOMEN 2023

Exceptional female leaders revealed

COMMERCIAL LENDERS ROUNDTABLE

Key figures in the sector discuss the market

AUSTRALIAN MORTGAGE AWARDS

Excellence Awardees chosen ahead of big night

ELITE WOMEN 2023

Exceptional female leaders revealed

COMMERCIAL LENDERS ROUNDTABLE

Key figures in the sector discuss the market

AUSTRALIAN MORTGAGE AWARDS

Excellence Awardees chosen ahead of big night

Exploring the many ways the industry is creating an inclusive space for all

Got a story or suggestion, or just want to find out some more information?

Commercial lenders and brokers meet to discuss the strengths and challenges of this growing sector

MPA honours this year’s exceptional female leaders who are breaking boundaries as influential role models in the mortgage and finance industry

CommBank’s acting

GM third party banking wants to “pay it forward” by supporting her mentees and the bank’s commitment to advancing gender equality and cultural representation

In this special edition, MPA highlights the e orts of brokers, lenders and aggregators to embrace and encourage D&I

Lendi Group’s Pathways program is tailored to developing brokers at all stages of their journey

twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

The way forward to broader industry representation of people

04 Statistics

Rental growth is still well above average

06 Opinion

How customer-owned banks prioritise strong social values

20 Community outreach Support for the community has driven success for Mortgage Choice franchisee

22 Paving the way

The FBAA’s Artemis Space enables women to connect, grow and succeed

24 Winning workplace culture

OnDeck gives its people a shared sense of purpose as a Best Place to Work

26 Women in broking

The MFAA continues to build on its initiatives to boost female participation

28 Pride with a purpose

NAB Pride works to empower the bank’s LGBTI+ employees and customers

30 Building financial literacy

SFG member Niti Bhargava talks about her program to educate migrant women

62 Brokerage insight

The fintech providing a gateway to fast and flexible non-bank solutions

64 Other life

Broker Narelle Kerstan takes time out to support her son’s go-kart racing dream

MPAMAG.COM/AU

NOW ONLINE:

Our daily newsletter. Keep on top of property market trends, business strategy, and what industry leaders have to say.

You can’t be what you can’t see. It’s a well-known phrase that’s used a lot when it comes to discussions about diversity and inclusion in the financial services industry. The idea is that people are more likely to follow a particular career path, such as broking or banking, if they can see others in those roles who share the same gender, culture, class, religion, sexual orientation or disabilities.

It sounds obvious, but if you see a successful broker who looks like you, speaks the same language and shares the same values, you’ll hopefully be inspired and realise that if they can do it, so can you.

The mortgage and finance industries were long considered an arena in which you were more likely to find white, middle-class males, particularly in senior positions. While this is now changing, particularly as Australia becomes a more multicultural society and we are far more accepting of di erences, more needs to be done to create an industry that is truly reflective of our nation.

The MFAA Industry Intelligence Service 15th Edition report, covering 1 April to 30 September 2022, revealed that the proportion of female brokers had decreased by 0.2 percentage points to 25.4%, the lowest level on record. While the number of

www.mpamag.com/au

EDITORIAL

Editor Antony Field Writers

Kim Champion, Mina Martin

Contributors

Chris Green, Fleur Heazlewood, Michael Lawrence

Lead Production Editor Roslyn Meredith

Production Editor Allison Ingusan

ART & PRODUCTION

Designer Cess Rodriguez

Customer Success Manager

Isabella Concepcion

Customer Success Executive Shara Cruzat

SALES & MARKETING

Publisher Claire Tan CORPORATE

Chief Executive Officer

Mike Shipley

Chief Operating Officer

George Walmsley

Chief Commercial Officer

Justin Kennedy

Chief Information Officer Colin Chan

Chief Revenue Officer Dane Taylor

Director – People and Culture

Julia Bookallil

EDITORIAL ENQUIRIES

tel: +612 8437 4711 antony.field@keymedia.com

SUBSCRIPTION ENQUIRIES

tel: +61 2 8311 5831 • fax: +61 2 8437 4753 subscriptions@keymedia.com.au

ADVERTISING ENQUIRIES claire.tan@keymedia.com

KM Business Information Australia Pty Ltd tel: +61 2 8437 4700 • fax: +61 2 9439 4599 www.keymedia.com

Australia, Canada, USA, UK, NZ and Asia

females recruited grew 26.9% year-on-year during that period, compared to male recruits at just 10.6% growth, the actual number of females joining the industry paled in comparison to the number of males – typically, they amount to less than half the number of new male recruits in each six-month period.

This issue of MPA puts the focus on diversity and inclusion and highlights the e orts of various aggregators and lenders to ensure that their sta or members and partners empower and embrace di erent communities. Among the topics explored are the importance of supporting women in the industry; e orts to improve financial literacy; working with people of non-English-speaking backgrounds; support for the LGBTI+ community; and creating a great workplace culture.

We also look at the latest issues a ecting business finance in MPA’s annual Commercial Lenders Roundtable; reveal the Elite Women for 2023; and discover how Lendi Group creates career pathways for its brokers.

We hope you enjoy the latest edition.

Antony Field, editor, MPAMortgageProfessionalAustralia is part of an international family of B2B publications and websites for the mortgage industry

AUSTRALIAN BROKER simon.kerslake@keymedia.com

T +61 2 8437 4786

NZ ADVISER alex.knowles@keymedia.com

T +61 2 8437 4708

CANADIAN MORTGAGE PROFESSIONAL john.mackenzie@keymedia.com

T +1 416 644 8740

MORTGAGEBROKERNEWS.CA corey.bahadur@keymedia.com

T +1 416 644 8740

MORTGAGE PROFESSIONAL AMERICA katie.wolpa@keymedia.com

T +1 720 316 7423

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 7525 456869

If you see a successful broker who looks like you, speaks the same language and shares the same values, you’ll hopefully realise that if they can do it, so can you

$9.6trn Total worth of Australian real estate

Median rents in Australia increased by 2.5% in the June quarter, down from the 2.8% rise seen over the three months to May. Despite the slowdown in the pace of growth, national rental growth remained well above average, CoreLogic data showed.

REGION

Sydney

Melbourne

Brisbane

Adelaide

Perth

Hobart

Darwin

Canberra

Combined capitals

10.9 million

Combined regionals

National

$2.2trn

Value of outstanding mortgage debt

The total number of dwellings approved in Australia jumped by 20.6% in May, in seasonally adjusted terms, after a 6.8% fall the prior month, according to ABS data. The approvals growth was driven by a 59.4% increase in private sector dwellings, including houses, and particularly by the large number of apartment developments approved in NSW in May.

56.1% Percentage of household wealth held in housing

The CommBank Household Spending Intentions index dipped by 1.7% over the month of June in original terms, taking the index down to 116, with homebuying, one of the main drivers of the decline, down 26.2% month-on-month.

CHANGE IN HOUSEHOLD SPENDING INTENTIONS, JUNE 2023

National vacancy rates increased marginally in June, providing renters with some much-needed relief. PropTrack data showed a quarterly rise of 0.14 ppts in vacancy rates, the most significant easing in rental market conditions since November 2020.

CHANGE IN RENTAL VACANCY RATES FOR ALL DWELLINGS, JUNE 2023

More than two-thirds of mortgage holders are planning to refinance or seek a rate review in the next year, the inaugural InfoChoice Real Mortgage Survey shows. Leading the charge are millennial and Gen Z homeowners. with 78% of 27- to 42-year-olds looking to refinance or seek a rate review.

OVER THE NEXT YEAR, WILL YOU REFINANCE OR SEEK A RATE REVIEW?

whether that be people working in a particular industry such as the police, members of a regional community, or Aboriginal and Torres Strait Islanders.

Amid a heightened consciousness around issues like equality, inclusion, justice and climate change, people increasingly expect their service providers to contribute to solving them. Mortgage brokers can strengthen their relationships with clients by validating this requirement, and helping them find a bank that meets their needs on a more holistic basis.

When we talk about delivering more than competitive interest rates, what do we mean?

WHILE SOARING interest rates and increased living costs are prompting homeowners to consider their existing arrangements to ease their budget stress, we know that people want their banks to do more than just meet their fundamental financial needs.

For many people, purchasing a property will be the biggest financial commitment they will make in their lives. The broker community can provide a level of added value and service to their clients by o ering to put their business with an institution that sits outside the main Australian banking brands – and, in turn, provides other benefits to the community.

As more people choose services that align with their ethics and values, our research at the Customer Owned Banking Association has found that 84% of people want a higher purpose from their bank.

The much-discussed mortgage cli is an opportunity for people to find not just a better rate but a bank that aligns with their values – whether that be through sustainability, supporting a charity they care about, or giving back to the local community.

Brokers account for nearly 70% of the mortgage market and play a powerful role in helping consumers find a bank that does more than just meet their financial needs. Smaller banks can deliver competitive rates, but they can also provide critical community support. And they do all this while aspiring to treat every member engagement as a personal one, which is another of the key di erentiators between the large banks and member-owned banks.

Because customer-owned banks don’t squeeze customers to pay shareholder dividends, they can do things that other banks can’t and put people before profits – meaning that customer-owned banks focus on strong customer outcomes, building better products and services, and paying it forward into the community.

COBA members create great outcomes for customers because of an innate emphasis on customer service and community engagement. According to Roy Morgan research, customer-owned banks have market-leading

We mean community support, local sports and event sponsorships, education programs, disaster support, and in many cases profession-based education services and product development. With no shareholders to appease, all profits are reinvested in delivering customer outcomes and supporting the community.

Customer-owned banks are leaders in making a positive impact on the world. Bank Australia is at the forefront of environmental responsibility as the first bank to pledge to be net zero carbon by 2030. Six of COBA’s members are B-Corp certified, meaning they meet the highest standards of verified perfor-

satisfaction at 91.6%, compared to 77% for the major banks.

Importantly, our members also compete hard with the majors on pricing, and when tough times strike, we’re there – with 97% of our customers saying they were pleased with how their bank supported them in their hour of need, compared to 76% for major banks.

Customer-owned banks were established as purpose-driven organisations to support a group of people with common interests,

mance, accountability and transparency. Four COBA organisations are members of the Global Alliance for Banking on Values, a network of independent banks using finance to deliver sustainable economic, social and environmental development.

Would your customers benefit from being with a customer-owned bank?

Because customer-owned banks don’t squeeze customers to pay shareholder dividends, they can do things that other banks can’t and put people before profits

Brokers can help clients find the financial solutions that not only suit their needs but also align with their social values, says COBA CEO Michael Lawrence

RAZIA KHAN knows the power of a good mentor when it comes to inspiring women and people of diverse backgrounds to carve out a successful career in financial services.

Khan started her career at CommBank 15 years ago, working as a collections officer and then taking on a variety of roles throughout the retail bank. More recently, she was leading CommBank’s acquisition, retention and customer experience team for the homebuying business and worked closely

“I always think about how I can identify the types of opportunities that were given to me and pay that forward to my mentees,” she says. “This is especially the case for some of the women I work with, who are more than capable of taking the next step but who don’t always have the confidence to try something new.

“As a leader I hope to be able to provide a support network where people can be encouraged out of their comfort zone and flourish,

solving always leads to better outcomes.”

Khan wants to advocate for more industry diversity within the broker channel.

“I have a genuine passion for bringing more women into the industry and advocating for their success.

“I feel so fortunate to have started and grown my career at CBA,” Khan says. “I have been granted many opportunities to learn new things and have been fortunate enough to have been encouraged and supported to take opportunities that were outside of my comfort zone. I think we all have a role in helping to bring more diversity into leadership roles.”

The bank sets goals to support its commitment to advancing gender and cultural representation across leadership roles. Women represent more than half of CommBank’s overall workforce.

with teams across technology, marketing, frontline and broker relationships.

Khan has now stepped into the role of acting general manager third party banking.

“I’m enjoying diving deeper into the broker industry and meeting many of our broker and aggregator partners,” she says.

As Australia’s largest bank, CommBank offers plenty of opportunities for career advancement, and Khan mentors a number of staff.

not fail. I think this all comes back to CBA’s core values of care, courage and commitment.”

Khan says there have been many leaders and peers who inspired her career, and she’s “particularly inspired by people that have had quite different experiences and possess different skills to me”.

“Hard work, curiosity and humility are traits that I will hold on to, and I believe allowing different perspectives into problem-

“We’re working towards a goal of about 50% gender equality in our middle management and leadership roles by 2025 – a goal that is gender inclusive to consider people who don’t identify with a binary gender –male or female.”

Khan has been a member of CommBank’s Inclusion and Diversity Council for over four years, working on mentoring and growing diverse talent through focused programs.

“One of our key focuses is wanting to help

Razia Khan

“Hard work, curiosity and humility are traits I will hold on to, and I believe allowing different perspectives into problem-solving always leads to better outcomes”

Name: Razia Khan

Job title: Acting general manager third party banking

Company: Commonwealth Bank

Years in the industry: 15

Favourite quote: “If you fail to plan, you plan to fail”

Career highlight: “A theme that sticks out to me is stepping into domains throughout my career that I didn’t have a large amount of experience in, learning new things whilst building my personal confidence”

ensure that our leaders and teams reflect the communities that they serve,” she says.

The bank’s Diversity, Equity and Inclusion strategy aims to enable an inclusive workplace anchored in CommBank’s values of care, courage and commitment. The bank also supports the MFAA’s Opportunities for Women report and the important role of diversity more broadly.

CommBank’s diversity strategy is based on three key pillars. The first is fostering care, equality and respect for sta and customers. The second is strengthening courageous, inclusive decision-making by listening to customer and sta experiences and reviewing metrics and decisions to ensure they are fair and equitable. The third pillar is amplifying the bank’s impact and

Khan says the third party banking team is motivated by building strong relationships with brokers.

“Broker partnerships are incredibly important to CommBank. Over 70% of market activity at the moment is through brokers, and we want to ensure we work with our brokers to continue to grow their businesses … we want to o er best-in-class experiences that align with what our brokers and customers need.”

Technology is key to the bank’s ongoing investment and transformation agenda, Khan says, and its focus is on “making it easier to work with us through consistent and transparent experiences”.

CommBank is working on “ongoing digitisation of the application process to

Women represent more than half of CommBank’s overall workforce, and the bank is aiming to achieve 50% gender equality in middle management and above leadership roles by 2025.

CommBank’s Diversity, Equity and Inclusion strategy is centred on three key pillars:

1. Fostering care, equality and respect to help sta and customers feel safe and included

2. Strengthening courageous, inclusive decision-making through listening to sta and customers’ experiences and regularly reviewing metrics and decisions to ensure they are fair and equitable

3. Amplifying CommBank’s impact and delivering on its commitments by partnering with community organisations and academic experts to ensure the bank’s approach is evidence-based and accelerates positive outcomes

delivering on its commitments through partnering with community organisations and experts to ensure an evidenced-based approach that accelerates positive outcomes.

Looking at her own career, Khan says her focus has always been on collecting di erent skills, which has o ered her great opportunities and resulted in her leadership of frontline, data and analytics, workforce planning, strategy roles and sales teams.

“I’ve always been drawn to roles that I know will keep me close to the customer while still allowing me to gain further skills. This approach helps me combine my understanding of how the organisation works with what the customer needs to ensure the work we do supports our customer and broker-facing teams.”

make things faster, and [putting] further investment into our newly launched portal”, she says.

“We have also invested heavily in learning and development for our brokers through our training hub and hope to be able to provide genuine value to our brokers through that portal.”

Over the last 18 months, CommBank has increased its team of relationship managers and has dedicated technology teams to service capabilities.

“A key part of building and maintaining relationships over the long term revolves around taking on board feedback from our brokers and making changes, or working towards those changes, to ensure our approach is simpler, better and easier,” Khan says.

“We’re working towards a goal of about 50% gender equality in our middle management and leadership roles by 2025 – a goal that is gender inclusive to consider people who don’t identify with a binary gender”

Australia’s female leaders in the mortgage industry are creating new opportunities with their inspirational vision and values

AUSTRALIA recognises the Elite Women of 2023 as trailblazing female leaders who serve as infl uential role models in a fi eld marked by declining female representation, which, at 25%, is the lowest proportion observed by the MFAA.

Through their extraordinary achievements and impact, this year’s cohort pushed through barriers and inspired other women in the mortgage industry to create their own destiny by:

• prioritising integrity, honesty and transparency

• being authentic and staying true to their principles and values

• fostering supportive networks

• promoting fair and inclusive workplaces

• advocating for and mentoring aspiring female leaders

“The women who maintain high levels of confidence are good at knowing what their beliefs, values and purpose are,” says Jane Counsel, co-founder and executive coach at thrive4women and research lead for the MFAA’s Opportunities for Women initiative.

The FBAA’s national partnerships manager, Leah Renwick, feels that a commitment to learning, professional development, and diversity and inclusion should be high on an Elite Woman’s agenda.

“It is up to all of us to foster education and understanding for the next generation that this is an industry of acceptance and gender diversity, and we will lead the way for equality and inclusion in the workplace,” she says.

What is an exceptional female leader?

While 2023’s Elite Women share similar challenges across the mortgage industry,

their solutions-driven approach is as unique and compelling as their accomplishments.

Founder and CEO of Credit Fix Solutions Victoria Coster has changed the face of the country’s credit repair industry by building a business that brokers and industry partners trust.

“I’ve shone a light on the fact that credit repair can be a valuable support service for the broking industry,” she says. “It’s taken me nine years to gain respect from other heads of businesses within finance, but how I overcame that is by working together and collaborating; this is the only way we’re going to move forward.”

Coster counts among her career highlights:

• serving as vice president on the NSW Council for the FBAA

• creating a toolkit and credit reporting essentials guide for brokers

Fellow winner Kristy Clucas is BOQ

“Be there for each other in a genuine way, be open-minded and let everyone know you’re here for them”

ANZ is a proud sponsor of the second annual MPA Elite Women, designed to spotlight the leading women in the mortgage industry. This prestigious list celebrates and recognises the role that women play in supporting Australians to achieve their homeownership or business goals as brokers, aggregators or lender representatives.

We’re excited to partner with MPA once again to highlight the value, skill and talent that these

Group’s head of broker strategy, partnerships and performance for its multibrand (BOQ, ME and Virgin Money) broker channel. Her achievements include:

• shaping the organisation’s digital banking platform

• building out its new home loans end-to-end process

• being a team leader in BOQ’s women in leadership program

“It’s been a long time in the making. Lots of people contributed, and I’m super proud of what my team and I have accomplished

exceptional female leaders bring to mortgage broking and finance. We remain committed to working better together with brokers, aggregators and industry partners to foster an inclusive culture and enhance the diversity of our industry.

nition throughout the mortgage broking community for her thought leadership, social media content and dedication to client service. She has also cemented her status as a top sales performer and her brokerage as an industry-leading business.

“It’s an inspirational aspect, but I’m proud of being that person that people look up to as a young female in the mortgage industry and sharing how you can run a business that’s not just about mortgages,” Clark says. “It’s important to stay true to our power as females because that has gotten us our success; clients want to work with women because we’re good at building relationships

In May of this year, MPA invited industry professionals from across the country to nominate exceptional female leaders for its Elite Women 2023 list. Nominees had to be working in a role that related to, interacted with, or in some way impacted the industry and should have demonstrated a clear passion for their work.

Nominators were asked to describe the nominee’s standout professional achievements over the past 12 months, initiatives and innovations, and contributions to the mortgage industry. After a thorough review of all the nominations, the MPA team narrowed down the list to the final 66 Elite Women who have made their mark on the industry.

in building it,” Clucas says. “By embracing gender diversity in our workplaces, we create a better perspective and culture. I’ve been lucky to have worked with supportive leaders who have encouraged me to remain true to myself.”

Elite Women prioritise giving back to the community and industry

Everlend finance broker and director Evelyn Clark has earned widespread recog-

with our customers and peers.”

Clark’s accomplishments include:

• launching a podcast, You Have My Interest, in partnership with the brokerage’s wellness specialist, aimed at women aged 25 to 35

• being a member of LMG’s Young Business Owners community

• supporting and mentoring young women along their career paths

Jane Counsel Co-founder and Executive Coach, thrive4women Research Lead, MFAA’s Opportunities for Women initiative Leah Renwick National Partnerships Manager FBAAAfter two decades of success in a related financial services field, Adele Andrews, director and mortgage broker at Australian Property Home Loans, took a leap of faith to build a thriving brokerage.

“Advocate for each other, encourage them to step out of their comfort zone and give support and recognition”

Kristy Clucas, BOQ GroupAs part of our editorial process, Key Media’s researchers interviewed the subject matter experts below for their independent analysis of this report and its findings.

“It’s more difficult as a mature entrant to a new industry, but it’s been lifechanging for me, especially with the impact you can have on people and their lives,” she says. “I think there’s so much opportunity in this industry for women, and working with a female mortgage broker has distinct advantages in their ability to relate and connect. It would be lovely to see that marketed more heavily.”

Among Andrews’ notable achievements are:

• creating New Beginnings, a project founded in collaboration with a family lawyer to support women coming out of a relationship with education and guidance on navigating finances and the mortgage of the family home • providing informative and educational media contributions

These female leaders have eschewed a stereotype of success that solely centres around writing high business volumes. Instead, they subscribe to their own definitions that align with their personal and professional goals.

Coster: “I wake up every day and get to do what I love to do. I give back to charities, and when someone calls and says, ‘Thank you. You’ve just changed my life’, that’s success for me.”

Clucas: “It’s about allowing myself to excel professionally and make a positive impact in the workplace, continuing to grow as a leader, but at the same time, I want to be actively involved in my children’s lives. I’m a lot more present now for my family,

which makes me a better employee because I’m happier.”

Clark: “When I started, I didn’t clearly understand what I wanted to achieve, but I realised what I love about the industry is working with customers. That expanded to include helping other brokers. Success isn’t just about what I’m achieving; it’s about creating a sustainable environment for everyone on the team.”

Andrews: “With every person I approach, I want them to walk away and say, ‘Wow! That was amazing!’ I want everyone to feel empowered or wowed by their conversation with me and be better o for the experience.”

Getting to the top of their industry hasn’t been a linear progression, with challenges and pitfalls along the way, so each of MPA’s featured Elite Women of 2023 shares the lessons they have learned.

Coster: “It’s been so important in the past year for me to get out there and reconnect with my broker partners and have meaningful conversations.”

Clucas: “The mortgage industry is forever changing, and we’ve had to change from the banking side of things. You can’t get comfortable because there’s always something else that’s going to pop up, and you need to be ready for it and continue to flow with that change.”

Clark: “I’ve worked a lot on the business, its vision, team and culture, and the biggest lesson I’ve learned is when everyone is working towards a common vision, your business will go to the next level.”

Andrews: “You have to keep showing up and being the face of your brand, pushing boundaries, trying new things and getting uncomfortable. Often, the most uncomfortable things turn out to be the most rewarding.”

“Always be willing to give advice, support and your time because they, in turn, will give back to others”

Evelyn Clark, Everlend

Victoria Coster

Founder and Chief Executive O cer

Credit Fix Solutions

Phone: 0416 525 233

Email: sales@creditfixsolutions.com.au

Website: creditfixsolutions.com.au

Adele Andrews Director and Mortgage Broker

Australian Property Home Loans

Phone: 0409 099 603

Email: adele@aphl.com.au

Website: australianpropertyhomeloans.com

Chuyu (Kiki) Feng

Senior Mortgage Broker AUSUN Finance

Phone: 0452 579 116

Email: kiki@ausunfinance.com.au

Website: ausunfinance.com.au

Debbie Hutchings

Director, Endorsed Mentor and Trainer

REFS Australia

Phone: 0407 314 287

Email: info@refsaustralia.com

Website: refsaustralia.com

Alissa Childs Director Two Birds One Loan

Andrea McNaughton Group Executive, Residential LMG

Angela Tracey

Director of Broker Success LMG

Anita Hyde

Former Head of Specialised and Private, Commercial Broker NAB

Anja Pannek

Chief Executive O cer MFAA

Evelyn Clark Director and Finance Broker

Everlend

Phone: 0402 724 003

Email: evelyn@everlend.com.au

Website: everlend.com.au

Kristy Clucas

Head of Broker Strategy, Partnerships and Performance BOQ Group

Website: boq.com.au

Nancy Youssef

Business Mentor, Speaker and Author Classic Mentoring

Phone: 1300 219 119

Email: nancy@classicfinance.com.au

Website: nancyyoussef.com.au

Ashleigh Pakis Director

Panache Financial Mortgage Specialist

Belinda Gibson Director

TM Finance Group

Carol King Mortgage Broker LMG

Caroline Jean-Baptiste Lending Specialist and Owner Mortgage Choice Fortitude Valley

Catherine McFarlane

Chief Operating O cer FINSTREET

Deslie Taylor Owner-Manager Mortgage Choice Ormeau, Beenleigh and Surrounds

Elouise Dooley Director and Finance Broker Two Birds One Loan

Rachel Farrell

Managing Director Bloom Capital

Phone: 0403 696 789

Email: rachel.farrell@bloomcapital.com.au

Website: bloomcapital.com.au

Kathy Crawford Director

Australian Mortgage Assist

Phone: 0404 804 585

Email: kathy@australianmortgageassist.com.au

Website: australianmortgageassist.com.au

Michelle Bannister

Director – Head of Distribution

La Trobe Financial

Phone: +61 408 566 518

Email: mbannister@latrobefinancial.com.au

Website: latrobefinancial.com.au

Emma Cattermole Director

Wealthfolio Financial Services

Gordana Bailey

Business Development Manager Allianz Insurance

Gouthami Minupala Relationship Manager Secure Finance

Heather Gallagher

Head of Training and Education outsource Financial

Helen Avis

Director of Finance – Specialist Finance Specialist Mortgage

Isabella Constantinou

Associate Director

Simplicity Loans & Advisory

Joanna James

The Artemis Space

Joanne Croft

Owner/Director

Mortgage Choice Tweed Coast/Northern NSW

Kat Tunnock Head of Learning and Development Cinch Loans

Kelly Carter Owner-Manager Mortgage Choice

Kerri Buurman Director Buurman Finance Solutions

Kirsty McKinnon Director Flair Finance

Kylie Quenon Business Owner GO Mortgage

Leanne Johnstone Owner-Manager Mortgage Choice Lane Cove

Liz Ford Director Finestream Capital

Louisa Sanghera Principal Broker Zippy Financial Group

Madeleine Dart Executive Assistant to CEO and Business Support O cer outsource Financial

Maele Alchin Senior Mortgage Broker Hubbl.it

Maninder Kaur Director LMG

Meleah Taylor Customer Service Manager Foster Ramsay Finance

Melissa Wright Director and Mortgage Broker Zest Mortgage Solutions

Natalie Denyer Mortgage Broker Birdie Wealth

Natalie Smith General Manager, Retail Broker ANZ

Navjeet Kaur Mortgage Broker Everest Loans Melbourne

Nicole Tosev Sales Operations Manager – Aggregation AFG

Nicole Walton Finance Broker Finch Financial Services

Nikki Berzin Director Cherry Lending + Finance

Patti Eyers Chief Executive O cer First Mortgage Services and First Title

Pauline Blight-Johnston Chief Executive O cer Helia

Mhairi MacLeod Managing Director and Principal Broker Astute Ability Group

Preeti Kowshik Senior Mortgage Broker Home Loan Experts

Renee Blethyn Head of Broker Partnerships NextGen.Net

Rooma Nanda Director All R Loans

Sarah Thomson Director LMG

Sarah Madigan State Manager WA/QLD/SA/NT ubank

Sarah Willsallen State General Manager NSW/ACT Westpac Group

Sharon Piening Director The 500 Group

Sonja Pfitz Executive Director – Pedagogy and Advocacy Women’s Commercial Finance Forum

Susan George Business Development Manager Suncorp Group

Suzi Trajanovski National Director, Growth LMG

Tanya Sale

Chief Executive O cer outsource Financial

Tes Anderson Partnership Manager Bankwest

Vivienne Than Senior Mortgage Broker Home Loan Experts

Yasmine Shah Chief Impact Broker Impact Brokers

Australia’s leading mortgage professionals will be gathering for the Australian Mortgage Awards, where the deserving winners will receive their awards at a highly anticipated formal gala event.

AWARD SPONSORS PREMIUM PARTNERS

EVENT PARTNER PHOTOBOOTH SPONSOR CHAMPAGNE SPONSOR SOCIAL MEDIA SPONSOR

VIP POST AWARDS EVENT SPONSOR ENTERTAINMENT PARTNER

career you have to fight more than normal … where I came from, our cultural background, for women to start their careers, they have to go through many battles.”

Adjusting to life in Australia wasn’t easy at first. Vira says her family knew no one. “I remember in the first one and a half months, my husband booked tickets to go back to India almost three times,” she says with a laugh.

While Vira says she didn’t experience culture shock, the family had to adapt to a different way of living, without the household support they were used to in Mumbai.

Despite having worked in business in India, she says they “started from scratch” in Australia. Vira worked in fashion and jewellery stores before securing a job at Commonwealth Bank in 2011, where her love of maths and strong customer service skills came in handy.

MOVING TO another country, experiencing different cultures and navigating a path to a new career as a successful mortgage broker is no easy task, but Mortgage Choice franchisee Smita Vira has shown it can be done.

Conscious of the opportunities she has been able to take advantage of but also of the barriers that migrant women can face, the Adelaide broker is heavily involved in community programs, and reaches out to help and inspire others.

Originally from Mumbai, India, Vira and her husband and two young daughters migrated to Australia in 2008. After working in the family’s shoe business in India, they decided to move away from the hectic pace of Mumbai, opting for a better family life and greater career opportunities in Australia.

“We wanted to experience something different,” Vira says.

“When you talk about diversity, women are treated a bit differently in India. To start a

She started as a teller and then moved into different roles at CommBank, including home lending, SMSF and business banking. Vira says the skills she picked up at the bank were invaluable when she decided in January 2020 to “start her career in broking”.

Vira set up her own mortgage broking franchise in Adelaide. Now part of Mortgage Choice, her franchise covers the northern Adelaide suburbs of Prospect, Campbelltown, Enfield and Klemzig.

She says her work in the community helped her meet a lot of people, which was helpful

when it came to building her customer base as a broker. Vira is a follower of guru Pujya Shri Rakesh Jhaveri and is involved in supporting the work of his charitable foundation, the Srimad Raj Chandra Mission. Every week, the Adelaide Group runs a spiritual session in Adelaide so people can listen to the words of the guru. “In this crazy world of stress and anxiety, it helps you to cope with a lot of things,” she says.

The group helps provide hot food for the homeless in partnership with Adelaide organisation Cos We Care every Saturday.

Vira is also a sound healer and runs her own not-for-profit organisation, Divinage, which conducts regular activities, including weekly sound healing sessions and monthly mental health programs featuring mandala art, pranayama (breath control exercises) and yoga. It recently supported Catherine House (pictured at right), an organisation in SA that helps homeless women.

“Divinage also buys products from overseas

While a lot of people from the local Indian community attend Vira’s programs, she says word of mouth means that more Australians from different backgrounds are attending, including colleagues and other people in the mortgage and finance industries.

Vira says it’s important as a broker to build connections with the community you serve so customers can see you o er more than just a transactional relationship.

“For anything you do in life, trust is a big factor. [Customers] can be assured that the advice I give is not biased. If it’s my daughter sitting in front of me versus my client, if I’m doing something for my daughter, I’ll 101% do it for my clients.

“This is the kind of attitude and customer service we provide, and it encourages people to put their faith in you.”

Vira says there’s a large Indian community in Adelaide, and it’s beneficial that she’s from Mumbai, a multicultural city, with many di erent languages and customs.

few female brokers. “I strongly promote diversity in this space, and we need to get more women of all cultures taking up a career in broking. There are so many amazing women with so many skills, but they don’t always get the platform or exposure. Every woman has a di erent story and a di erent struggle.”

In February, Vira was a panellist at a Mortgage Choice event run by the Aspire program (pictured on opposite page), which supports and promotes female talent in the broker network.

from not-for-profits and sells them here to create employment for tribal women,” Vira says. “Funds raised from some of our activities are donated to local charities as well as to support kids from the state of Gujarat in India – enrolling them in school and paying their yearly fees.”

One of Vira’s biggest fundraising events was the staging of an Indian play, Yugpurush, in Adelaide in 2016. She says the sold-out event raised funds to help build a hospital in rural India.

“A lot of people in the community knew that I was behind the play and were aware of my activities in the community, so that helped with my branding and recognition as a broker.”

“I can speak almost eight languages, which enables me to connect to di erent people and deeply understand their culture. It helps a lot; people refer others to me. That’s the biggest part – the referral business,” she says.

“Some of our customers call me ‘baji’, which means sister in Hindi.”

While people often know Vira from her community activities, she says it’s not about “talking the talk but walking the walk”.

Many of Vira’s clients are women from di erent cultures. “As soon as they see that you are a woman mortgage broker, that trust is di erent. I get a lot of Afghani Muslim women who come to me for advice.”

Vira says in her community there are very

At the latest Aspire event held in Adelaide in July, leadership strategist and behavioural scientist Shadé Zahrai spoke about diversity and female empowerment.

“It was amazing to hear her. We need more women like her to encourage other women to come forward,” Vira says.

In July, Mortgage Choice won the Diversity & Inclusion award for its Aspire program at the 2023 MFAA National Excellence Awards. The award recognises the work of the teams and brokers involved in shaping the Mortgage Choice Aspire program and e orts to boost representation of women in the network and broking industry.

To learn more about Aspire, the latest events and the exceptional women in the Mortgage Choice network, go to mortgagechoice.com.au/ franchises/aspire.

“I can speak almost eight languages, which enables me to connect to di erent people and deeply understand their culture” Smita Vira, Mortgage Choice

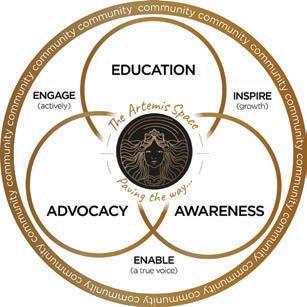

The FBAA has set up a community forum known as The Artemis Space, which is designed to enable women to connect with each other, share their journeys and achieve success in the industry

WHEN THE FBAA was looking for someone to lead its new forum for women in the finance industry, Joanna James was the ideal choice.

A highly respected industry leader, entrepreneur and author, James began her career as Australia’s youngest female architect and builder. She then went on to become a successful broker and general manager of mortgage manager and non-bank lender Mortgage Ezy for more than 20 years.

James was also the chief ambassador of global movement The Successful Woman, which empowers women to grow their skills in business.

Now she is overseeing the FBAA’s The Artemis Space. Named after the Greek goddess of nature, women and archery, it symbolises reaching an objective with the greatest speed, accuracy and focus.

FBAA managing director Peter White says he met James and other women in the industry on International Women’s Day in 2022 to discuss bringing about real change for women.

“It certainly isn’t about ‘men are bastards’ or ‘let’s burn the bra’ style of campaigns; it must be driven by purpose and with real, tangible outcomes that are beneficial,” White says. The Artemis Space is based on equality for all and to achieve this “we need to reset the pendulum swing to find that balance and put right the failings of the past that created those inequalities”.

“So, with a like-minded group led by women, The Artemis Space was born, and I felt Joanna would be the right person to lead this for the FBAA, and we march on from here,” White says.

After a full year of research into the concerns of women, The Artemis Space was

officially launched on International Women’s Day 2023.

James says, “Here we presented our vision to create a safe and supportive community where women/womxn can have open-minded, matter-of-fact discussions to understand what holds them back in order to pave the

“This program supports women to better advocate for themselves, which is the most powerful position of all”

Joanna James, The Artemis Space

Sponsored by

way forward.” The Artemis Space’s mission is to transform constructive discussions into practical change while supporting women/ womxn to connect, grow and succeed with excellence in the finance industry.

“We choose to focus on practical solutions at a grassroots level across three main areas: awareness, education and advocacy,” James explains. “The team of forum contributors are first class, choosing to serve others without pretence or parade.”

In the awareness series, a di erent expert each month focuses on enhancing skills that heighten self-awareness.

“Streamed live into the Facebook group, we cover topics such as creating work-life balance, managing time, improving focus, setting boundaries, achieving goals, developing discipline and mastering emotions, to name just a few,” James says.

The recordings also form a resource library of easy-to-digest 30-minute segments that support women in different times of need.

Each quarter, The Artemis Space holds education forums focusing on specific areas of upskilling not covered by traditional avenues. This year, topics include “Essentials in Business – Planning for the New Financial Year Ahead”; “Confidence in Communication”; and “All Things Networking”. Each 90-minute forum features two speakers who share valuable knowledge and practical tools.

For the advocacy program, James says The Artemis Space identified the need for an enhanced network of mentors to help women make progress across many areas of their careers.

“In essence, this program supports women to better advocate for themselves, which is the most powerful position of all. The Artemis Space has partnered with [mentoring program] Rare Birds in providing access to quality, ongoing business mentoring from top-level business professionals predominantly outside of the industry to give a di erent perspective to their growth.”

The community also hosts regular walking meet-ups in each state, and forum members attend industry conferences and events.

“They say large oak trees grow from little acorns, so this year we plan on planting that seed, growing to 500 members by focusing on delivery quality over quantity,” James says.

“At The Artemis Space we aim to keep things real, personal, and applied at an individual level.”

James says it’s vital that women have a supportive forum “where we are able to share our journeys”.

“Where we can feel free to be open and honest about the challenges we face, as well as a space where we can celebrate each other, is key to having a balanced life within the industry.

“Many women juggle personal, family and professional needs, and it’s usually in the intersection of these areas that both the joy and the difficulties reside. Being able to share constructive tools and extend genuine support and encouragement can

a former back-up singer for Tina Turner who James met in the US last year.

“Robbie, now 83, is sharp as a tack, rocking her wardrobe like a boss in heels,” James says. “She actively owns two di erent businesses, and yet she still finds time to share her valu-

make all the di erence to how we navigate these obstacles.”

As women learn to collaborate and support one another, “we actively break down the barriers inherent in competition and exclusion”, James says.

“Connecting in this way is the fastest pathway to sustainable growth on all levels within the industry.”

James says she has met many amazing women from across the world. “Each unique in their talents and gifts, I take inspiration from them all. If I were to focus on a particular group of women who excite me, it is women who are over 70 who choose to contribute in a constructive and meaningful way.”

One of these women is Robbie Montgomery,

able insights about life with other women.

“Robbie is an example of a woman who is vibrant, fully alive, generously sharing her wisdom with others. Forget preconceived ideas about ageism or working-life expiry. That is something we can all aspire to.”

James says that as a passionate advocate for the advancement of women, she loves the inclusive and collaborative nature of The Artemis Space. “It serves as a beacon for more women to achieve excellence within the finance industry, illuminating a new path forward.”

Women are encouraged to connect with The Artemis Space by joining its Facebook group. Membership is free and is open women and men across the industry.

“We need to reset the pendulum and put right the failings of the past that created inequalities” Peter White, FBAA

OnDeck has been declared Australia’s 2023 Best Place to Work among businesses with less than 100 employees, beating 55 other companies in the same category.

The award was bestowed by WRK+ and was based chiefly on the results of a survey completed by over 43,000 employees across 101 companies nationally.

In today’s environment of record-low unemployment coupled with a skills shortage, no employer can afford to take a business-asusual approach to attracting and retaining quality staff.

It’s also of benefit to businesses to reflect on current recruitment practices to see where they can do better. Participating in the Best Place to Work survey allowed OnDeck to do this.

More than 93% of OnDeck employees participated in the Best Place to Work survey, with strong results across several metrics. OnDeck’s employees celebrated the achievement of their company being recognised as the Best Place to Work.

As a lender that’s a pioneer when it comes to being data-driven, OnDeck conducts regular mini pulse surveys and participates in the independent Best Place to Work Study to measure employee satisfaction and engagement.

“As a small business lender, we understand the need to have a strong and dedicated

team to support our small business clients and broker network,” says OnDeck Australia CEO Cameron Poolman.

He believes one of the factors that set OnDeck’s workplace apart is authenticity. Poolman says the lender genuinely cares about its staff and has achieved considerable success in aligning employees with business goals. “This has allowed us to successfully give all our employees a shared sense of purpose, even amid a difficult economic climate,” he says.

Values play a pivotal role in fostering a thriving workplace culture, and underpin how teams interact with each other and their customers.

“We really are very strongly aligned to our values as a business, and they are absolutely not just words on the wall,” says Cherie Habashi, head of people and culture at OnDeck. “In fact, 97% of our team agreed that OnDeck’s leadership team is true to the company’s values.”

Each month, the OnDeck team nominate

people they believe have lived the company’s values. The executive team review each nomination to determine a monthly winner. The winner is then announced at a Town Hall meeting, receives a prize and goes into the running for an annual award.

That said, it’s important that employees understand the company’s goals and how their roles contribute to achieving these goals. The rise of presenteeism in the workplace – employees who turn up but are not engaged – is often a function of teams not understanding the ‘why’ behind what they are doing.

“We launch our goals for each half via ‘OnReview’,” Habashi says. “Following this, each team member sets their own individual goals. This allows everyone to set personal goals that align with our broader company goals.”

The process is proving e ective, with 95% of the OnDeck team reporting that they can see a clear link between their work and the company’s goals and objectives.

“We take this process very seriously and from the top down always ensure our goals fundamentally serve our vision – to set the standard for small business lending,” Poolman says.

Just as strong as its value orientation is its leadership support: 97% of OnDeck’s team agree that the lender’s leadership team are competent at running the business.

“We celebrate wins and consistently and respectfully challenge our team to do better for our customers,” Habashi says.

From its earliest beginnings, OnDeck’s ethos has always been to put its people first, and part of this involves having a strong emphasis on communication within the business. Every month at a Town Hall, the CEO answers all questions that have been submitted anonymously by the team that month – questions are not filtered, and nothing is o -limits.

Habashi says OnDeck provides very clear communication when things are good, as well as when things are more challenging. “This

allows our team to understand the business decisions we make.”

Further communication is shared through regular ‘team huddles’, and major business initiatives are shared with employees via ‘Switched-On’ announcements.

Poolman says a further strength is OnDeck’s team culture, with 90% of employees agreeing the lender has a team spirit.

“They feel they can be themselves, and that diversity of backgrounds, talents and

perspectives is encouraged by the organisation,” he says.

“When we say our people are our greatest asset, we mean it. So we engage in anonymous external audits to keep ourselves honest in terms of how well our people are really engaged – and if we are doing right by them.

“Our people really are the foundation of how we are able to be a strong lender to small businesses and our broker partners.”

OnDeck is working hard to bring gender diversity to the business – and the broader industry. A few of the steps the lender has implemented can be applied to every business. These initiatives include:

O ering work flexibility and a hybrid work environment

Providing a private room where breastfeeding women can pump in a comfortable space

Providing paid parental leave (for both the primary and secondary carer) above the statutory entitlement

Conducting annual salary benchmarking and internal pay audits to ensure pay parity

Proactively developing and implementing compulsory leadership training to ensure the respect@work reforms are incorporated into the organisation

Providing an anonymous reporting line to ensure all workplace concerns can be voiced if someone doesn’t want to be identified

Results at OnDeck:

Women fill 40% of leadership roles

One in three roles across the business are held by women; by comparison, the proportion is closer to 20% in the fintech industry

“As a small business lender, we understand the need to have a strong and dedicated team to support our small business clients and broker network”

Cameron Poolman, OnDeck

IT’S BEEN almost a year since Anja Pannek was appointed CEO of the MFAA.

Speaking to MPA in September 2022, Pannek said she wanted people to actively think of mortgage broking as a “career of choice”, and diversity and inclusion played a big part in this. Fast-forward almost 12 months and she says that while progress has been made on D&I, more needs to be done.

The MFAA Industry Intelligence Service 15th Edition report shows that the proportion of female brokers is at 25.4% – the lowest on record.

“We clearly have work to do as an industry,” Pannek says. “The results aren’t on par with the broader Australian community and are below what’s reported for financial services more broadly.

“We’ve seen a significant, and positive, shift in how diversity and inclusion overall is viewed in our industry. The awareness is there, and the industry is in a position to be able to unlock the enormous potential of the talent pool out there, but we aren’t there yet.”

Pannek says consideration of gender diversity as well as overall diversity is an issue “we at the MFAA feel needs to remain front and centre for us all”.

“We should be striving for our industry to reflect the community it represents and be a

nurturing environment, welcoming to people from all walks of life, regardless of background.

“A great attribute of Australia is our diversity, and our industry needs to reflect this diversity in all forms, whether it be gender, sexuality, cultural and linguistic diversity, or disability, and so on. We need to show clients that we represent them, we understand them, we want them to reach their goals.”

to call out behaviour that is not supportive of females and other diverse groups in our industry and protect those who do speak up,” Pannek says.

“The commercial business case for diversity is clear and compelling – quite simply, it’s good for business”.

Research backs this argument up time and time again, Pannek says. The Diversity Council

While gender pay inequality exists in other industries, there are clear benefits for women who seek a career in mortgage and finance, Pannek says. “There is no pay differential, something that can be highlighted to attract new talent.”

The MFAA is keen to celebrate those who are taking action to support greater diversity and inclusion. “But most importantly, we need

of Australia’s Inclusion@Work Index 2019–2020 found that workers in inclusive organisational structures were three times less likely to leave their current employer.

“So it’s important for businesses who want to retain their staff to be welcoming and inclusive, but it’s also about clients – the homebuyers and business owners looking for the support a mortgage and finance broker provides.”

The MFAA is working hard to encourage more women to become brokers through several industry initiatives and by lobbying the federal government

“We should be striving for our industry to reflect the community it represents and be a nurturing environment, welcoming to people from all walks of life, regardless of background” Anja Pannek, MFAA

For many people, having a broker they can relate to, or who they feel understands them, is important, “for example, people whose first language isn’t English”, Pannek says. “And the 2021 Census showed that almost six million Australians use a language other than English at home; having someone they can talk to in their native language can be extremely comforting.”

Brokerages that have multilingual sta can boost client relationships, providing opportunities not only to reach a new pool of clients but also for “wonderful career development for these sta ”.

Pannek says people with disabilities may also be looking for a broker who is respectful and accommodating of their circumstances and needs.

For some clients, particularly women, working with a broker of the same gender may also be important.

CoreLogic research shows that 26.8% of dwellings are female-owned, and if dwellings owned jointly by females and males are also considered, females own more than 70% of properties in Australia.

“Females are making household financial decisions; they have their own goals and they, quite rightly, expect to be taken seriously and treated with respect,” Pannek says.

The MFAA’s key platform for boosting female broker participation is its industry-leading Opportunities for Women initiative, established in 2018.

Pannek says the MFAA has consistently put the spotlight on the issue, bringing it to the attention of decision-makers and producing data to support the industry to take action. Its annual Diversity and Inclusion survey revealed a narrowing perception gap when it comes to the di erences in the experiences of men and women; and a greater willingness to promote the mortgage and finance broking industry to diverse individuals.

The MFAA provides a range of resources to assist people in bringing diversity into their businesses, including the published

MFAA Opportunities for Women reports: www.mfaa.com.au/professional-development/research/opportunitiesforwomen Inclusive community hub: www.mfaa.com.au/inclusive-community-hub

Mental health and wellbeing hub: www.mfaa.com.au/mental-health-and-wellbeing Balancing Work, Life and Everything Else e-book: www.mfaa.com.au/balancing-work-life-and-everything-else

Champions of Diversity series, which showcases how individuals demonstrate leadership in their e orts to create a more diverse and inclusive industry.

The MFAA has also launched an ‘inclusive community hub’ featuring online resources and information about diversity, including tools to “improve hiring practices and identify our unconscious biases”.

The association’s Women in Finance Broking networking events give women as well as men an opportunity to support broader diversity and inclusion.

The MFAA has also made a number of recommendations to the federal government’s Employment Whitepaper – Equal Opportunities for Women and Labour Force Participation.

Pannek says the Australian government

wants to be a world leader in gender equality, a goal the MFAA supports. The association’s submission to the Employment Whitepaper outlines how it believes the government can assist the industry in achieving this goal. Its recommendations include investing in female-led small broking businesses so they can grow and scale.

Federal and state financial support programs can also be a significant tool to facilitate entry or re-entry of women into our industry, Pannek says.

“Our members have told us they value the financial assistance of government-sponsored pathways programs as a key opportunity to help them take on and train new female sta members in a variety of roles, giving them the opportunity to grow and progress to becoming a broker themselves.”

As a major bank that values diversity and inclusion, NAB is supporting and empowering its lesbian, gay, bisexual, transgender and intersex (LGBTI+) employees and customers through the strong work and advocacy of NAB Pride

ONE OF Australia’s largest banks, with more than 32,000 staff, NAB understands the importance of fostering a welcoming and inclusive workplace. One of the ways it does this is through its support of LGBTI+ employees and customers.

NAB Pride executive co-sponsor and group executive, personal banking, Rachel Slade says NAB Pride is the bank’s dedicated LGBTI+ employee resource group

comprised of passionate volunteers and a strong network who drive a safe and inclusive workplace for LGBTI+ colleagues and their allies.

“The purpose of this employee resource group is to be the voice of LGBTI+ colleagues and customers by raising awareness and advocating for a safe, inclusive workplace and experience,” Slade says. “The group provides networking, mentoring and educational oppor-

tunities, as well as helping to build diverse talent pipelines.”

Slade says diversity is deeply valued at NAB, not just by its dedicated employee resource groups but right across the bank.

“We have more than 32,000 colleagues, and across our organisation we have a huge wealth of experience, beliefs and backgrounds.

“We see it as our job to nurture a safe and inclusive workplace that celebrates the diver-

sity of our people and empowers them to be a voice in the community. We believe that when you fully embrace who you are and can be your whole self, you will thrive.”

Slade shares the same commitment to NAB’s more than 8.5 million customers, “making sure they are respected and valued for who they are, no matter how they identify”.

“Overall, we’re intent on building a culture based on trust and respect that we can all be proud of, where each of our colleagues feels appreciated and empowered to be their authentic self.”

NAB Pride supports this goal through activities such as hosting networking events for NAB Pride members and allies, running seminars and providing training and awareness sessions for employees.

As well as promoting an inclusive and welcoming workplace for colleagues and customers, NAB actively promotes big events on the LGBTI+ calendar, Slade says. Some of the key events it supports each year include International Transgender Day of Visibility; International Day Against Homophobia, Transphobia and Biphobia (IDAHOBIT); Wear it Purple Day in support of LGBTI+ youth; Pride Month Australia; and World AIDS Day.

NAB is also the proud partner of Pride Cup, an organisation dedicated to changing sporting culture so that LGBTI+ people feel safe, welcome and accepted.

Slade says the bank has been a passionate supporter and principal partner of the Midsumma Festival (pictured on opposite page) for more than 10 years.

The Midsumma Festival started out as a Melbourne-focused LGBTI+ community event and is now recognised internationally.

“The festival includes a wonderfully diverse program of arts, culture and community events, and connects people in person and virtually via streamed online events that are accessed right across the world,” Slade says.

“NAB’s role as principal sponsor sends a clear message to our diverse colleagues and the community that they have every opportunity to share their true selves.”

The major bank is also a member of Pride in Diversity, Australia’s only not-for-profit workplace program supporting the country’s employers with LGBTI+ inclusion.

In 2022, NAB achieved Platinum Tier employer status in the Australian Workplace Equality Index (AWEI), Australia’s national benchmarking instrument for LGBTI+ workplace inclusion, Slade says.

“As a Platinum organisation, NAB is one of only 12 organisations nationally to achieve this level of workplace inclusion, and this achievement is a testament to our ongoing dedication to creating a workplace where we all belong and are all welcome.

“Most importantly, this reflects upon everyone at NAB and celebrates us as a vibrant and diverse team.”

NAB plays a role in supporting the LGBTI+ community more widely by helping other organisations connect with LGBTI+ networks in business and across the broader community.

“Our commitment to inclusion and diversity also applies to the relationships we have with industry partners,” Slade says.

“We use our status as an AWEI Platinum Tier employer to influence and educate organisations about the importance of building an inclusive and welcoming workplace for colleagues and customers.”

“We believe that when you fully embrace who you are and can be your whole self, you will thrive” Rachel Slade, NAB

Resolve Finance broker and SFG member Niti Bhargava has drawn on her own experiences as a migrant to set up a financial literacy program for women

AFTER MIGRATING from India to Australia in 2007, one of the most stressful experiences for Niti Bhargava and her husband was buying their first home.

Now a successful mortgage broker at Melbourne’s Resolve Finance and a member of broker aggregator Specialist Finance Group, Bhargava reflects on the situation at the time.

“We did not sleep for nights,” she says. “We were making such a big decision without our immediate family’s presence and guidance. We definitely felt that there was no proper guidance available.”

Luckily, everything went well with the home loan, Bhargava says.

“Not until I started working in banking myself did I realise that there are thousands of customers out there who are feeling exactly the same way we felt.”

Motivated by her experience, Bhargava has set up a financial literacy program to educate recent migrant women about their finances, wealth management and how to better equip themselves for the future. The program is a mix of online and face-to-face workshops. The most recent workshop was held in the Melbourne suburb of Caroline Springs and supported by the Victoria MP for Kororoit, Luba Grigorovitch.

Bhargava grew up as the eldest child in a middle-class family in northern India and says

she was a sincere and responsible child who excelled in school and college and in extracurricular activities such as public speaking and debates.

She completed two master’s degrees in India and got married at 21, before migrating to Australia in 2007 on a student visa, seeking a better future in a “land of opportunities”.

of challenges, including having her qualifications recognised; facing difficulties with language and communication; and being “picked up many times for my different accent”.

“But I was ready to accept this challenge because I knew my work should speak louder than any words … it took me couple

“My grandfather always used to teach me two things: one, it takes only one person to break the line and excel in every single opportunity, and two, you should always earn your own money and feel the power of financial freedom,” Bhargava says.

“Regardless of your gender, you need to learn to be financially independent asap – it’s an essential life skill.”

Bhargava got her start in finance working as a relief bank teller at one of Australia’s big four banks. She says she faced a number

of months to realise that the systems are different here, and job selection is not based on your degrees only but practical experience is way more important.”

Adjusting to Australian culture was also a challenge, Bhargava says, and for a time she felt homesick, missing India’s colourful festivals.

“The best thing about staying in Australia is that there are so many different cultures around you that before you realise it, you are already loving other cultures, respecting

“I have faced scenarios like women going through domestic violence and financial abuse – this accelerated my plans for a financial literacy program”

Niti Bhargava, Resolve Finance

their values and becoming part of the other festivities,” she says.

Bhargava has progressed in her career from teller to home loan consultant, and she says she was fortunate to receive worldclass training.

“I have not only gained practical experience, customer service skills and advanced training in lending and finance, but also learnt soft skills like cultural adaptability, gender equality and workplace inclusivity.”

She says these skills were invaluable when she started working as a broker three years ago.

“As an ex-banker I brought a solid foundation of financial knowledge to my role as broker, allowing me to understand a client’s financial situation comprehensively … e ective communication skills gained from banking helped me explain financial concepts clearly to my clients, empowering them to make informed decisions.”

Bhargava began marketing herself as a broker via social media during the COVID pandemic. She says this enabled her to connect with di erent communities, clients and a diverse range of women.

“I have faced scenarios like women going through domestic violence, mental health and wellbeing [problems] and financial abuse. Experiences like these helped accelerate my

plans to set up a financial literacy program.”

Workshops were run via Zoom and other online formats, and broadcast on radio, but Bhargava says this year she has been able to run in-person workshops (pictured below) with the help of Grigorovitch.

“I have also been supporting women empowerment-based programs and social events financially,” Bhargava says. “These are all community programs where issues such as gender equality, female participation in finance and cultural restrictions on women are addressed.”

As a big supporter of women in sport, the broker also organised “Our Girls Our Pride” on Facebook in March to honour young girls who excel in sports and entertainment.

When it comes to the financial literacy program, Bhargava says some of the challenges include both time and cultural restrictions, as well as di culties “generating the interest of women, language barriers and hesitation”.

“But we are working continuously to keep our motives alive and educate as many migrated people as we can.”

Bhargava, who speaks Hindi, Urdu and Punjabi, says it can be highly beneficial for customers to connect with a broker who shares a similar background.

Try to understand the specific needs, challenges and cultural backgrounds of the targeted community

O er multilingual resources to cross the language barrier

Adopt a culturally sensitive approach Collaborate with community leaders and other local businesses

Focus on empowering participants, and measure impact

“There is a language and cultural understanding, and you can clarify complex financial concepts and processes, reducing miscommunication. Empathy and relatability create a stronger sense of trust and rapport … this also enhances chances of higher referral opportunities once trust is built.”

Bhargava encourages other brokers to run financial literacy programs for multicultural communities, saying it can help boost their business growth.

SFG provides an immensely supportive company culture that encourages brokers to actively participate in community outreach, she says. “Recognising and celebrating my e orts in last year’s annual conference has definitely been a great source of motivation and commitment for me to increase my e orts in engaging with the community.”

Digital tools provided by SFG help brokers engage their targeted community and provide useful data and insights.

“I’m a big fan of their continuous support, especially for financial literacy programs and for my ‘breast cancer events’ throughout the year. They are always a call away. I feel fortunate to be part of the group,” Bhargava says.

DEVELOPING THE right people for the right role at the right time – this sums up the aim of Pathways, Lendi Group’s industryleading broker recruitment and development program.

Matthew Whyte, Lendi Group’s general manager, national distribution growth, says the aim of Pathways is really simple. “It’s leveraging our multibrand, multichannel

right through to franchise opportunities, “or what we would call [being] the CEO of their own business”.

“Having a structured Pathways program in place will ensure we are setting up our brokers for success, transitioning them into the business model that best suits their professional and personal goals and requirements,” he says.

manager before moving into his current role as GM of distribution growth five years ago.

“I’ve been very fortunate to have had some fantastic mentors during this time, who focused just as much attention and conversation around growth and development as around the work itself,” Whyte says.

“Personal growth is the first step in professional growth, and the two are not mutually exclusive, so my advice is to align yourself with mentors that can provide support in both areas.”

Whyte says that while Aussie and Lendi provide different experiences, ultimately “they have a shared desire of seeing things done differently for brokers and customers alike”.

“When these brands merged two years ago, they brought together a raft of complementary capabilities, unlocking key benefits for our brokers. One of the major benefits is our multichannel model and the sheer breadth of opportunities this provides for brokers to build a business or career in a manner that suits them.”

Through Pathways, many brokers have progressed within the same brand, Whyte says, whether these were Lendi associates being promoted to Lendi home loan specialists, or Aussie store or mobile brokers becoming store owners and franchisees.

“Our Pathways program is now entering a new phase to provide further opportunities to our expanded network of 1,400 brokers.”

model by having the framework in place to attract, recruit, develop and progress the right people for the right role at the right time.”

Following the merger of Aussie and Lendi, Whyte says a range of roles are now available across the group, from salaried broker and independent contractor roles

Whyte knows a thing or two about the best way to develop a broker’s career. He’s been in the mortgage industry for almost 25 years, since starting as a broker in the late 1990s at Wizard, after which he progressed through a range of sales and sales leadership roles.

He’s been at Aussie for 17 of those years, five of which he spent as Queensland state

Whyte says Aussie brokers have had many opportunities to learn about the Lendi brand and vice versa. “There’s been an increase in enquiry around transitioning across brands – in particular, Lendi brokers looking to build increased scale by becoming Aussie franchisees.”

He says now that the work to migrate the Aussie network onto the new Aussie Platform and consolidate operating models across the group is complete, it’s a logical time to develop the next stage of Pathways through collaboration and consultation with brokers groupwide.

Lendi Group’s multibrand, multichannel approach to broking is supported by its state-of-the-art training and development Pathways program

“Our Pathways program is now entering a new phase to provide further opportunities to our expanded network of 1,400 brokers”

Matthew Whyte, Lendi Group

Due to be finalised in September 2023, the next phase will include a framework for cross-brand channel transitions and will outline important logistical considerations and capability indicators for channel movement as a broker achieves significant growth or their needs evolve.

The Pathways program has di erent tailored components that cater to a broad spectrum of requirements and appeal to brokers at di erent stages in their journey. Lendi Group has five di erent broker channels:

• Lendi and Domain home loan specialist: salaried brokers who are employed directly by Lendi Group and can work remotely or in a Lendi Group o ce

• Lendi home loan consultant: selfemployed, independent contractor brokers who primarily transact with customers virtually via phone, email and video chat

• Aussie mobile broker: self-employed, independent contractor brokers who meet customers face-to-face or virtually

• Aussie store broker: self-employed and salaried opportunities available across

225+ stores; employed by or contracted to franchisees

• Aussie franchisee: the ultimate opportunity to build scale. The franchise model empowers franchisees to be the CEOs of their own businesses

Some of the programs helping Lendi Group brokers enter and thrive within the mortgage industry include:

Graduate program