24.03

RISING TO THE CHALLENGE

Aggregators back brokers in competitive market AUSTRALIA’S TOP BROKERAGES

Best broker businesses unveiled BROKERS ON AGGREGATORS

Survey reveals how networks performed

24.03

RISING TO THE CHALLENGE

Aggregators back brokers in competitive market AUSTRALIA’S TOP BROKERAGES

Best broker businesses unveiled BROKERS ON AGGREGATORS

Survey reveals how networks performed

Brokerages reap the rewards of hard work and a pioneering support model

Got a story or suggestion, or just want to find out some more information? twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

Record market share shows high trust in brokers

04 Statistics

Where homebuyers are looking to put their money

06 Opinion

Sharing opinions is fine, but avoid absolutes about interest rates, says Mark Bouris

Leading aggregators discuss their support for brokers as market share continues to rise

16 Alt-doc lending

Non-banks share their knowledge of alt-doc lending and the advantages for brokers and clients

64 Team culture

Brokers reveal the aggregators that are winning their loyalty in MPA’s annual survey

Lendi Group’s chief distribution o cer explains how the network has helped propel the growth and performance of Aussie stores, with a record nine recognised as Top Brokerages this year

How empowering people to share their views can build a dynamic team

66 Ethical leadership

MPA puts the spotlight on Australia’s most outstanding brokerages in 2024 and some of the secrets to their success

Tips for navigating ethical challenges as a business leader and why it’s important to get it right

70 Brokerage insight

The appeal of work flexibility and strong aggregator support drew Jennifer Lemme to success as an LNS Wollongong broker

72 Other life

Solvere Wealth director John Pidgeon blends AFL coaching and mortgage expertise to empower others

Experts from two major banks give their insights into current refinancing trends and prospects for brokers

Re cent mainstream media commentary has painted mortgage brokers in an unflattering light, depicting them as wealthy, brash and beating the banks in a battle for the home loan market.

Opinion columns have suggested that brokers are raking in the cash as property prices rise, claiming that they are earning much more than bankers and that the average Sydney broker is making over $670,000 annually in upfront and trail commissions. The articles claimed that commissions paid to brokers weren’t clearly spelled out to borrowers, and that homebuyers were paying more than they should for their mortgages because banks factor in broker commissions when pricing their home loans.

Not surprisingly, the mortgage broking industry has been outraged by the comments, with LMG executive chairman Sam White, MFAA CEO Anja Pannek, FBAA managing director Peter White and other leaders defending brokers and labelling the depiction of the way brokers operate as misleading and inaccurate.

Brokers know the truth – that they act with their clients’ best interests at heart (it’s called best interests duty, after all); that many of them don’t earn anywhere near the suggested average incomes; that their expertise and hard work has helped millions of

The numbers don’t lie, and Australians are voting with their feet: brokers wrote a record 74.1% of new home loans in Q1

customers get a better deal on their home loans; and that they’re not at war with the banks – lenders are competing with each other.

The numbers don’t lie, and Australians are voting with their feet: brokers wrote a record 74.1% of new home loans in Q1 2024, the MFAA reports, their highest market share ever. Brokers continue to provide a valued service to their customers, who rely on their knowledge of the market and its intricacies to help them find the most suitable home loans. But it goes beyond a simple transactional relationship – brokers are there to help educate clients about their finances and assist them in achieving their life goals, whether that means buying a business, purchasing an investment property, or helping a family member get a car loan. Many brokers are diversifying beyond home loans and cementing deep and trusting customer relationships.

In this edition, MPA highlights all the fantastic work brokers and their partners do. The 2024 Aggregators Roundtable brought together the heads of Australia’s leading broker networks for a positive discussion about industry challenges, diversification, payroll tax and succession planning. MPA also takes an in-depth look at alt-doc lending and the refinancing market, and reveals the winners of this year’s Top Brokerages in Australia. Enjoy reading the July issue!

Antony Field, editor, MPA

JULY 2024

EDITORIAL Editor Antony Field Writers

Kim Champion, Mina Martin Contributors

Mark Bouris, Michelle Gibbings, Paige Williams

Lead Production Editor Roslyn Meredith

ART & PRODUCTION Designers

Cess Rodriguez, Noel Avendano, Joenel Salvador

Customer Success Manager Isabella Concepcion

Customer Success Executive Shara Cruzat

SALES & MARKETING

Publisher Claire Tan

CORPORATE

Chief Executive

EDITORIAL ENQUIRIES tel: +612 8437 4711 antony.field@keymedia.com

SUBSCRIPTION ENQUIRIES tel: +61 2 8311 5831 • fax: +61 2 8437 4753 subscriptions@keymedia.com.au

ADVERTISING ENQUIRIES claire.tan@keymedia.com

4599 www.keymedia.com

Australia, Canada, USA, UK, NZ and Asia

MortgageProfessionalAustralia is part of an international family of B2B publications and websites for the mortgage industry

AUSTRALIAN BROKER simon.kerslake@keymedia.com

T +61 2 8437 4786

NZ ADVISER alex.knowles@keymedia.com

T +61 2 8437 4708

CANADIAN MORTGAGE PROFESSIONAL chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGEBROKERNEWS.CA corey.bahadur@keymedia.com

T +1 416 644 8740

MORTGAGE PROFESSIONAL AMERICA katie.wolpa@keymedia.com

T +1 720 316 7423

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 7525 456869

12 - 15 November 2024

1.2 million

Number

$10.6trn

Driven by its affordability and attractive lifestyle, Adelaide secured eight of the 10 most-viewed suburbs in April 2024, surpassing

Queensland,

1

Given the unpredictability of interest rate changes, brokers must tread carefully when sharing their views with customers, says Mark Bouris

AS THE cost of living crisis persists, intense speculation about interest rates endures. In any corner of the internet or traditional media, you can find two economists suggesting the opposite conclusion. Heck, I’ve even seen some commentators predict impending rate hikes this year.

It’s obvious why: it gets clicks.

The reality is that interest rates impact all corners of Australian life, and articles predicting rate changes grab the attention of concerned mortgage holders, who in turn reach out to their mortgage brokers to ask about where rates are headed.

So, how do you navigate this challenge as a mortgage broker?

You must avoid absolute statements about the direction of interest rates. As we’ve seen, the ‘expert’ can’t accurately predict where rates are headed.

Of course, it’s fine to share your opinions and reasoning behind your thought process, but to present these beliefs as advice is where alarm bells start ringing.

If pressed for an opinion, I would suggest that, until substantial and consistent economic data justifies a shift, a period of interest rate stability is the most probable scenario for the short to medium term. Most economists and financial markets anticipate a period of interest rate stability.

Sharing opinions is fine, but avoid absolutes about interest rates. Similar risks emerge if you are asked for advice on the direction of property prices. Remember, you are providing credit advice, not investment guidance.

My take? Supply shortages appear to be outweighing the negative e ects of higher interest rates in most Australian markets.

With supply issues unlikely to be resolved soon and interest rates steady, the current trend of modest property price growth should continue. However, this will vary across markets.

The rental squeeze, expected interest rate stability and continued modest property price growth should create favourable conditions for first home buyers. However, the challenge is obvious: a ordability in desired locations.

GOT AN OPINION THAT COUNTS? Email antony.field@keymedia.com

relief and is a mutually beneficial solution for both borrower and broker. However, what sets you apart from the pack is how well you react when potential solutions are not so easy to come by.

So, step up.

How you can assist:

1. Utilise the lender panel: Lenders o er reduced interest rate bu ers for refinance customers, providing a ‘wow’ moment for your client. O ering solutions clients may not know about is part of why they come to you.

2. Assist non-qualifiers: Exploring options and presenting justifications for a rate review approval, such as a significant drop in the estimated LVR since origination, or suggesting a loan term reset can produce outstanding results for clients.

3. Negotiate e ectively: If you introduced the current loan, negotiate with the

If pressed for an opinion, I would suggest that, until substantial and consistent economic data justifies a shift, a period of interest rate stability is the most probable scenario

Set yourself apart from the pack by leveraging these conditions and o ering advice to those considering their options for entering the market. Keep abreast of first home buyerspecific incentives in your market and o er obligation-free advice, even for those not ready to transact. This will help you build a great customer and, importantly, referral base.

Be it for customers you have already assisted or potential new borrowers reaching out to you, helping someone in their hour of need to navigate one of the largest financial decisions of their life creates an exceptionally loyal customer base.

Now is the moment to rise to the occasion and deliver the transparency and clarity that mortgage holders and prospective homeowners urgently need.

Refinancing clients to a lower-rate product with lower repayments, possibly set up with a new, longer loan term, can provide obvious

lender on behalf of your client. If not, provide clients with the necessary information for direct negotiations.

The short-sighted may see this as unpaid work; however, the reality is that this is the groundwork for creating an exceptionally loyal client base.

Naturally, this sort of work does not pay the bills, so for any brokers su ering from a downturn in revenue, I would implore you to diversify your income, if you have not already done so, by looking at commercial and equipment finance as well as other potential revenue opportunities.

Running a business can often feel like navigating the ocean without a map, a compass or a sail. To succeed you don’t just need intelligence and hard work, you need the right support and the right tools. With AFG you have a tried and tested partner by your side. One who can provide you with confidence, support, and the tools you need to grow your business, your dream and your future.

Aussie Home loans is celebrating after nine Aussie stores were named in the 2024 Top Brokerages list. Lendi Group’s Brad Cramb discusses the great result and how the network supports its franchisees

and brokers to achieve success

LENDI GROUP chief distribution officer Brad Cramb couldn’t be prouder of Aussie Home Loans franchisees, with a record nine stores featured in MPA’s Top Brokerages of 2024.

That means a whopping 18% of the 50 brokerages featured on this year’s winners’ list were Aussie stores and the franchise network has tripled its performance from

in these stores, and customers can walk into their appointments with certainty that they’re dealing with a trusted expert.”

Cramb says the nine incredible businesses recognised in 2024 is a significant uplift from the three last year. “We know that there are several stores who wouldn’t have been too far off qualifying, so we’re hopeful of seeing more entries next year.

“Aussie is providing Australians with the platform to build a thriving broker business, while also giving the Australian public the support they need to secure their homeownership dreams”

last year when three stores made the top 50.

Cramb says for Aussie franchisees this recognition is a wonderful payoff for their tireless dedication to growing their businesses and supporting their customers.

“We know our winning franchisees are delighted to have received this recognition, and they’re all very much deserving,” he says.

“This kind of recognition also adds authority to the expertise of our franchisees and brokers

“It’s great recognition that Aussie is providing Australians with the platform to build a thriving broker business, while also giving the Australian public the support they need to secure their homeownership dreams.”

Of the nine Aussie stores, six are owned by multi-site franchisees.

“One of the primary reasons people enter a franchise partnership is to leverage an established brand and centralised support to

achieve business growth, so we’re proud to see so many of our franchisees driving growth and scale in their businesses,” Cramb says.

He says the Aussie retail channel drives significant volume for Lendi Group and is critical to its success.

Given Aussie’s strong commitment to helping franchisees achieve growth, new territory opportunities are strictly capped.

Cramb says Aussie has identified a series of “hot territories in high-opportunity areas with significant growth prospects”.

“These provide an opportunity for prospective franchisees to service the local area and become the CEO of their own business.”

While globally retail businesses cut costs and close branches, Cramb says Aussie is continuing to invest heavily in revolutionising the retail experience for franchisees, brokers and customers. This includes refreshing signage and storefronts, piloting interactive new touchpoints in-store and executing campaign activity to drive customer foot traffic.

“Following the migration of our network onto the new Aussie Platform in 2023, we’re able to facilitate seamless in-store-to-online experiences for our customers,” says Cramb.

The aim is to elevate the functionality and appeal of Aussie stores without excessive cost.

To expand the reach of franchisees and

Name: Brad Cramb

Title: Chief distribution officer Company: Lendi Group

Years in the industry: More than 20 years’ senior leadership experience. Has been at Aussie/Lendi Group since 2017

Fun fact: On weekends, Cramb swaps his business suit for a wetsuit and goes surfing with his two sons

Highlight of working at Lendi Group:

“Seeing the value of the Aussie-Lendi merger come together in the last 12 months has been a huge highlight. Watching our Aussie franchisees and brokers embrace new technology and leverage pioneering support models to drive growth in their businesses is truly inspiring.”

brokers in their local areas, the ‘Great Aussie Summer Giveaway’ was held in late 2023. It was Aussie’s largest-ever competition, with a prize pool of $250,000.

During the launch week, the record for customer appointments held in a single week was broken.

“We leveraged the campaign to support

our new Aussie mobile app, downloadable property reports and credit score checks as a means of driving enquiry and facilitating new engagements.”

As Australia’s largest retail mortgage broking network, Aussie’s footprint of over 1,000 brokers and 220 stores means it can serve customers nationwide, Cramb says.

“One of the primary reasons people enter a franchise partnership is to leverage an established brand and centralised support to achieve business growth”

stores in driving engagement at grassroots level, matching their local area marketing spend dollar for dollar,” says Cramb.

Aussie contributed $60,000, allowing brokers to “flex their lead-generating muscles” with reduced financial barriers.

The Great Aussie Giveaway returned in May with another $200,000 in prizes, and brokers and franchisees embraced the campaign to reach more people.

“We’ve also equipped our brokers with a suite of product-led sales tools, including

“Importantly, we o er our customers choice – whether they would like to engage with their broker in-store or virtually, via a mutually convenient location, or even in their own home or workplace.”

Aussie franchisees and brokers also get involved in their communities by sponsoring footy teams, donating to schools, connecting with local businesses, and more.

When it comes to building growth for Aussie stores, Cramb highlights the group’s Platform technology, Platform Plus and

Danny Blair joined Aussie as a store broker over 12 years ago, before venturing into franchising at Aussie Ipswich in 2013. He has grown his portfolio and established a prominent retail presence in the west Brisbane corridor, with stores in Mount Ommaney (opened 2020), Kenmore (existing store purchased in 2021) and Forest Lake (opened 2023).

Blair has expanded his team to include three franchise partners, 14 brokers and ve administrative sta . He is now in the nal stages of acquiring his fth Aussie store, which adds another three brokers to his team. He fully leverages Aussie’s Platform Plus model to streamline operations across his stores, and the proof is in the results, with his group of stores experiencing a 17% uplift in settlements in 2023.

Blair is now the CEO of his business, and rather than actively writing loans, he focuses on accelerating customer growth, providing career opportunities for local talent, and developing his team to achieve their own success.

supported model; connecting brokers and customers in new ways (such as via the Aussie mobile app); and seamless in-storeto-online experiences.

“It’s about scalable systems and processes, growing footprint and driving e ciency and productivity.”

Woodley and Rose have been in partnership as franchisees of Aussie Prospect for the last 11 years, and for the past nine consecutive years, Prospect has ranked as the No. 1 store in the Aussie network of more than 220 stores. The pair have ascended an impressive 17 places in MPA’s Top Brokerages this year, after ranking at No. 32 in 2023.

Woodley and Rose were part of the rst cohort who opted in to the Aussie Platform Plus model when it began rolling out to stores in 2023, ready to further accelerate their growth. The duo also invested heavily in their business last year, with Aussie Prospect undergoing signi cant renovations to now feature multiple consultation spaces, back-o ce workstations for up to 26 brokers and team members, and new design elements to enhance the broker and customer experience.

Harnessing Aussie’s Platform Plus model allows Woodley and Rose to spend more time mentoring their brokers. The pair are working towards a goal of $1 billion in annual settlements.

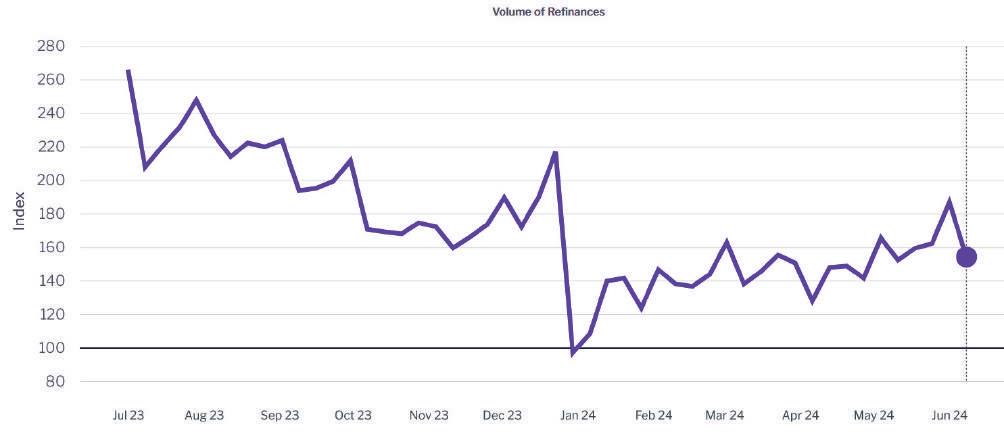

While refinancing has dropped markedly, there are still borrowers rolling off fixed rates and others looking for better loan options who need brokers’ support

REFINANCING BOOM is well and truly in the rear-view mirror, and activity has dwindled since the peak in mid-2023. It will be no surprise to mortgage brokers as the data backs up what many will have experienced – fewer clients are refinancing their mortgages.

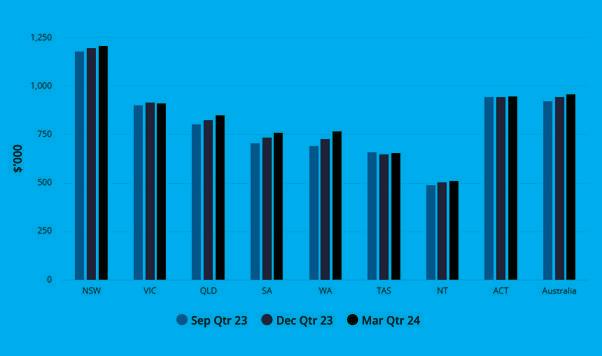

The PEXA Refinance Index, which measures the volume of refinances, shows that as of 9 June 2024, the level of refinances was down 28.8% compared to the previous year, although it had risen almost 12% quarterly.

ABS lending indicators for April show that the value of external refinancing for total housing was 16.3% lower than a year prior. For owner-occupier housing it was down 22.8% and for investor housing it fell 2.8%.

There are a number of factors behind the drop-off in refinancing activity. Cashback offers from lenders have declined considerably; the Reserve Bank hasn’t changed the official cash rate since October 2023; borrowing capacity has eroded; and due to serviceability constraints, some mortgage holders are unable to refinance.

On the flip side, brokers are in a strong position to help borrowers, enjoying record home loan market share of 74.1%, with more and more Australians relying on their expertise to get them a better loan deal.

There are still opportunities for brokers to assist customers wanting to refinance, especially those who are only now coming off their fixed rate loan terms.

To understand what’s happening in the refi-

nancing market, MPA sought expert insights from Natalie Smith, general manager at ANZ Retail Broker, and Johnny Lockwood, general manager broker and strategic partnerships at BOQ Group, which includes ME Bank.

Refinancing volumes peaked around June 2023, following the cycle of RBA interest rate increases that led to customers seeking better rates.

“External refinancing has declined notably since peaking in 2023,” Smith says. “It’s likely that there are less borrowers seeking to refinance to a loan with lower rates, with most

rates not changing over the last six months.” There are also fewer borrowers rolling off fixed-term loans and looking for the lowest available variable rate loan, with expiring fixed rate loans having peaked in 2023.

Lockwood says there was a surge in homeowners refinancing their home loans early last year. “As borrowers moved from lower fixed rates to higher variable interest rates, they sought more competitive loan options and attractive cashback offers, resulting in record levels of refinancing activity,” he says. Momentum began to taper off in the second half of 2023 as lenders, who were facing increased funding costs, started to

Volume of refinances, year to June 2024

Source:

scale back their acquisition strategies. Some lenders reduced or removed cashback o ers that had previously enticed borrowers to refinance, leading to a decline in loan volumes, Lockwood says.

“With interest rates likely at peak levels, borrowing capacity has weakened … Coupled with the challenges of higher borrowing costs, ongoing cost of living pressures and economic uncertainty, the demand for home loans is expected to remain subdued until there is some relief in interest rates.”

For brokers, it’s important to understand which customer segments are seeking to refinance now. At ANZ, Smith says most current ‘refinance’ customers are owneroccupiers. They equate to about 70% of the refinance book, with investors at 30%.

“No matter their circumstances, customers want to deal with brokers who understand their needs, provide accurate information and explain their loan options clearly,” she says. “Whilst borrowers are reviewing their loans more regularly, they still value the support, choice and convenience that brokers have to o er.”

Smith says brokers can find ANZ product information, rates and o ers on the ANZ

“ME continues to see predominantly low-LVR owner-occupied refinancers ... However, there is an emerging upward trend in the higher-LVR segment, specifically for owner-occupied loans exceeding 80% LVR” Johnny Lockwood, BOQ Group

Broker Portal and anz.com. The bank has also introduced the ANZ Home Loan O er Selection tool, a digital process available through the ANZ Broker Portal. Smith says it’s a time-saving and convenient way for brokers to request available home loan o ers for their eligible customers.

“Now is a great time to consider ANZ for your home loan customers eligible for a great refinance o er. Refinance your customer’s eligible home loan of $250,000 plus and 80% or less LVR to ANZ and they could get $2,000 cashback*.”

ANZ is aware that some brokers are working with self-employed customers, Smith says,

and “where these customers have a home lending need, we have a range of income verification options for self-employed applicants”.

Lockwood says, “ME continues to see predominantly low-LVR owner-occupied refinancers in the market. However, there is an emerging upward trend in the higherLVR segment, specifically for owneroccupied loans exceeding 80% LVR.”

He advises brokers to take the time to thoroughly understand their clients’ unique situation before presenting them with loan options. “There is no one-size-fits-all approach when it comes to choosing between fixed and variable rates; in fact, splitting between the two

In April 2024, in seasonally adjusted terms, the value of external refinancing:

for total housing rose 1.7% to $16.3bn but was 16.3% lower year-on-year

for owner-occupier housing fell 0.4% to $10.2bn and was 22.8% lower year-on-year for investor housing rose 5.5% to $6.1bn but was 2.8% lower year-on-year

Source: ABS Lending Indicators, April 2024

could be a beneficial strategy for certain clients, balancing stability and flexibility in times of uncertainty,” Lockwood says.

“Keep an eye out for customers who have built up equity in their home, as you might be able to secure them more competitive loan terms.”

Lockwood says in late 2023 the number of ME customers transitioning o fixed rates reached its peak. “While most of our customers who were on lower fixed rates have now reached maturity, there are still some customers in this category who are yet to transition.”

To support these customers, he says ME maintains a close partnership with its broker network. Fixed rate expiry notifications via email serve as a proactive tool for brokers, alerting them when a shared customer is nearing the end of their fixed rate. “This prompts timely outreach from brokers, enabling them to check in with clients and facilitate pricing requests for retention.”

ME has developed a robust engagement plan tailored for customers approaching fixed rate maturity. It uses multiple touchpoints, including email, phone, mail and SMS, over a 12-month period, to empower customers

with knowledge and options well in advance.

Lockwood says new procedures also help the contact centre team identify potential triggers for home loan retention. And rate rise navigation hubs have been launched, o ering calculators, tips and tools to educate customers about rate changes and the options available.

Smith says about 5,100 customers who were refinanced to ANZ and introduced via a broker are yet to roll o low-rate fixed term loans.

“It’s important that we continue to provide a compelling proposition for our existing customers as well as for those looking to refinance through a broker. Our existing customers want confidence that they’re receiving a good deal, so ANZ proactively contacts brokerintroduced customers with expiring fixed rates at di erent points of their journey.”

a convenient refinance process for eligible customers, with less paperwork.

It’s available to eligible PAYG borrowers, and self-employed customers who meet ANZ’s company wage policy, who are switching between similar term loans or to a lower-cost ANZ home loan, where the minimum repayments on the new ANZ home loan are equal to or less than the current repayments on their OFI loan. Certain other eligibility criteria also apply. Smith says because Simpler Switch uses comprehensive credit reporting to verify a customer’s ability to meet their existing commitments, there’s no need to supply any income documents as part of an eligible application.

Lockwood says ME plays a crucial role in BOQ Group’s multi-brand business strategy.

“Customers want to deal with brokers who understand their needs, provide accurate information and explain their loan options clearly” Natalie Smith, ANZ

Smith says eligible customers can opt to receive a discount on the applicable variable rate once their fixed rate expires, or to take advantage of ANZ’s current fixed rate o ers.

Customers who seek to increase their loan or apply for further lending are referred back to their broker in the first instance. For new customers exploring a better home loan deal through their broker, a streamlined OFI refinance process is available when certain eligibility criteria is met.

Brokers are busy people dealing with multiple clients, so fast turnaround times and e cient loan processes are important.

Smith says ANZ has several streamlined processes for brokers to ensure refinancing is fast and e cient. These include ANZ’s Simpler Switch policy enabling brokers to provide

Focused on simple, low-LVR lending, the bank o ers brokers and customers competitive rates and impressive turnaround times. Broker partners also benefit from the dedicated support of their BDMs.

“We are committed to investing in and expanding our ME broker channel,” says Lockwood. “One of the most exciting advancements is the ongoing development of our new digital end-to-end home loan o ering, designed with the broker experience as top of mind.”

ME is dedicated to enhancing service e ciency and satisfaction for brokers and shared customers, Lockwood says.

* O er can be withdrawn at any time. Limit of one cashback within any 12-month period. O er is $2,000 cashback with 80.00% LVR or less; loans with LVR above 80% are not eligible for cashback. Paid within 60 days to an eligible ANZ account. You must draw down the Eligible ANZ Home Loan(s) within 120 days from applying. Fees, charges, eligibility criteria apply

A large proportion of the Australian population find it difficult to access finance due to their income records and work patterns. However, a growing number of borrowers are discovering a better path through alt-doc loans

ALL BORROWERS are facing challenges in the current lending environment. Higher interest rates mean that borrowing capacity has been reduced, and loan serviceability buffers can make it difficult for some people to refinance their home loans.

But these difficulties can seem even bigger for a particular customer cohort – the selfemployed. This segment can include people who are sole contractors, small business owners and gig economy workers.

Not having the usual income patterns and accompanying paperwork that their PAYG counterparts are able to provide can put them at a disadvantage when seeking loans, especially from the major banks.

This is where non-bank lenders and alt-doc lending come in – non-banks specialise in helping borrowers such as the self-employed. They understand this growing customer segment and can work with brokers to assist clients who would benefit from alt-doc loans.

The self-employed made up 61% of Australia’s total employment base in 2023. That means there are millions of borrowers that brokers could be helping with their finance needs.

MPA asked Pepper Money general manager mortgages and commercial Barry Saoud and Liberty chief distribution officer David Smith to share their knowledge about alt-doc lending and the advantages for brokers and clients.

What does alt-doc lending cover?

Saoud says alt-doc loans have emerged as a beacon of hope for a niche yet significant segment of the market: the self-employed.

“These loans are designed to cater to the unique financial situations of entrepreneurs and business owners, contractors, seasonal workers and even property investors,” he says.

“These borrowers often have non-standard income streams or need financial solutions for business debt consolidation, outstanding tax payments or cash flow management.”

These loans can also accommodate borrowers with intricate financial arrangements such as those involving companies or trusts. Saoud says alternative income documents such as a six-month BAS (business activity statement) may be a more accurate reflection of their ability to service the loan.

“Brokers who understand the unique income structures of these individuals have an opportunity to reassure them that there are still options for them.”

“For brokers, alt-doc loan customers offer a chance to tap into a growing market segment and deliver solutions that align with the modern workforce’s financial realities” Barry Saoud, Pepper Money

Alt-doc loans are particularly suitable for self-employed individuals and investors who face challenges in providing proof of traditional income, due to fluctuating income or irregular cash flow, says Saoud.

“Alt-doc loans allow them to provide alternative income evidence, such as bank account statements or an accountant’s letter, to support their loan application.”

Smith points out that all borrowers are unique when it comes to their income and financial records.

“Our alt-doc (AltA®, Nova and Express) solutions provide options for those who may not be able to – or prefer not to – satisfy traditional loan application requirements. Alt-doc loans cater for borrowers who are self-employed, contract or seasonal workers, or

who may not have access to all the typical financial documents that lenders often ask for.”

Alt-doc lending is an important part of Liberty’s business, says Smith.

“Demand for alt-doc solutions has been consistent since COVID, and we are starting to see an uplift as small businesses look for flexible solutions to help manage their finances.”

He says small business is the backbone of Australia, but many small businesses are struggling.

“While inflation drives up expenses, increased cost of living is causing decreased consumer spending. And with cash flow and profitability concerns, we are seeing an increase in the need to support small

businesses through alt-doc products.”

Liberty has always taken great pride in its close relationship with the broker channel and the accessibility of its BDMs and credit assessors, Smith says.

“With a dedicated local team, support is only a phone call away, and our teams thrive on working through scenarios with brokers to help them find a way to ‘yes’. ”

Saoud says Pepper Money has seen a rising trend in alt-doc applications year-on-year. “We expect this trend to continue, driven by economic changes and the growing number of mainly self-employed individuals.

“Growth in the alt-doc lending space is also dependent on broker education and understanding of how lenders like us can help their customers who aren’t traditional PAYG Australians obtain a loan.”

Alt-doc is no different to recommending a traditional loan, Saoud says. The basic requirements and lodgement process for brokers are virtually the same.

“It’s just that Pepper Money asks for a different type of supporting documentation in order to verify the customer’s income.”

Brokers offering alt-doc loans can expand their market to clients with non-traditional income and help them access flexible loans for debt consolidation or business cash flow management.

The clients that benefit from alt-doc lending are also a good target for cross-selling opportunities, particularly leasing, insurance and equipment finance products, says Saoud.

“Often they are much ‘stickier’ clients with more regular finance needs as their business needs regularly change. For brokers, they offer a chance to tap into a growing market segment and deliver solutions that align with the modern workforce’s financial realities.”

Smith says there is often a misconception that alt-doc or custom loans are more difficult and time-consuming, but there’s little difference when it comes to submitting an application.

“There is plenty of help available for brokers new to this area, including our highly experienced Liberty BDM team who can help walk a broker through the process and equip them with the right skills.”

Liberty is committed to enhancing the knowledge and capabilities of brokers who are currently working with alt-doc borrowers and empower those yet to diversify into this area, he says. “With access to Liberty’s specialised training and support, brokers can discover new opportunities to provide tailored solutions and build their business.”

Smith says alt-doc lending requires a highly skilled team, “which we pride ourselves on”.

“Liberty has an operations and BDM team willing to get on the phone and talk through

*Seasonally adjusted

individual customers’ situations. We listen, understand and strive for the best customer outcomes,” Smith says.

“Our bespoke systems allow us the flexibility to treat every customer based on their circumstances. Brokers look to Liberty for our ability to accept a range of income types,

“We recently raised the acceptable loan limit on our accountant letter to $2.5 million, in addition to o ering single verification of income across all of our alt-doc options, from prime through to specialist.”

Pepper Money’s ongoing investment in technology has created a smooth process,

“Alt-doc loans cater for borrowers who are self-employed, contract or seasonal workers, or who may not have access to all the typical financial documents that lenders often ask for” David Smith, Liberty

consider non-genuine savings and look beneath the surface with each application assessment.”

Saoud says Pepper Money has three options to verify income within its alt-doc range: an accountant’s letter, six months’ BAS, or six months’ business bank statements.

says Saoud, including fast turnaround times, digital verification of identity and digital documentation, with the Pepper Product Selector providing quotes for customers in a matter of minutes.

Saoud says the cascading credit model provides a broad range of solutions to meet

the ever-changing needs of the selfemployed customer. Features include unlimited debt consolidation, including refinance of tax debt, cash-out for business use, 40-year loan terms, and options for customers who may have previously experienced a life event resulting in adverse credit listings such as defaults or judgements, bankruptcy or arrears.

Saoud says about a third of Pepper Money customers have used alt-doc.

“We see a massive opportunity to help [mainly] self-employed customers and their families get into homes and have better deals by allowing alternative documentation.

“We anticipate that the alt-doc lending market will continue to rise due to the changing economic circumstances and the growing self-employed segment wishing to utilise documentation that reflects their current financial position and income profile.”

For nearly 25 years, nMB has built a reputation for providing a genuine partnership model, with award winning service.

We know all brokers are not the same, that’s why selecting nMB as your aggregator can help you nd the approach that is best for your business! With our team’s experience, support and resources, you will have all the tools you need to stand out.

nMB is home to some of Australia’s best brokers. So, if you’re seeking an authentic aggregator that truly understands business, get in touch with us today to discover what you’ve been missing out on.

MPA’s Top Brokerages of 2024 are a collection of innovative and skilled operations. Features that drive the success of these outstanding brokerages include:

• targeting niche clientele

• upskilling brokers and team members

• strategic planning

While all have their own secrets to success, each brokerage is resolute in its desire to be

$1.58bn

Average total loan book value 76%

Average conversion rate 13.6

Average number of years in operation

a trusted industry partner to its customers.

Rethink Financing

Top Brokerage rank: 25

Location: Liverpool, NSW

Years in operation: 7

Conversion rate of loans settled or written: 82%

While Rethink Financing is currently riding high, it is set to go even higher. It has built its

$478m Average total settlements from 1 January to 31 December 2023

12

Average number of loan writers

“We’ve come a long way in a short amount of time. My team is better than the average broker; they’re writing more than the average broker, and I’m very happy to see where we’re headed”

Son Pham, Rethink Financing

name on commercial property investing and being a partner to its clients dealing with:

• complex structures

• self-employment

• trust companies

• SMSF

Bankwest has the ambition to be the best broker bank in Australia and continues to support brokers in the critical role they play in improving customers’ financial wellbeing across the country. This is one of the many reasons why brilliant brokers choose Bankwest.

Rethink managing director Son Pham says, “We’re not transactional. We’re about wealth building. Our clients don’t come to us saying they want the lowest rate. They want another property; they want to build their portfolio and need funding.”

The firm has developed deep expertise due to the complexity of its clients having multiple properties. “We understand their long-term vision of what they want to do, and we explain how we’re going to utilise certain

Joanne Liu, Weme Finance

lenders to get them where they need to go. We may need to go to one lender first before we get to the next spot,” says Pham.

Commonly, clients first encounter Rethink after being referred due to other brokerages being unable to help them.

“I love it when someone says, ‘I’ve spoken to three brokers, and none of them can do

it’, ” says Son. “Then I really look into it and go, ‘I think it’s possible.’ I might not get there straightaway, but with a bit of digging and restructuring, we can make it happen.”

The 10-strong broking team often workshops deals in order to find these solutions. Typically, Rethink’s clients make up about 1% of the market and have multiple investment properties.

“Sometimes you can’t use a standard bank because their policies start charging you

“We spend a lot of time educating our clients and explaining the possible solutions, but we also tell them the details so they know why”

these investor loadings, and banks have to hold more capital reserves when they’ve got more exposure to a client. It does put more pressure on me, but I like the challenge.”

Post-pandemic conditions have also driven the firm’s growth, as it can now sign deals electronically, meaning it can work with customers nationwide.

To find the Top Brokerages of 2024, MPA invited Australian brokerages to submit their figures for the period 1 January to 31 December 2023. The online form also asked for details such as the number of active brokers working at each brokerage, as well as its total loan book value and conversion rate.

To be eligible, brokerages needed to have five or more loan writers in a single o ce headquartered in Australia. Aggregator information was also provided by applicants, and their aggregators were then required to verify the details submitted.

The final ranking is weighted across three areas: total loan book size, total settlements in the specified 12-month period, and conversion rate. Each brokerage was ranked in each of these areas, and the ranks were then combined to produce a final tally.

While being able to access more of its niche target clients is positive, finding brokers with the skill set to support them is challenging. Most of the leading commer-

“The team deserves all the credit for everything we do. When I make a decision, I think about whether it’s going to help someone stay in the business. As long as my North Star is trying to retain as many people as possible, it generally tends to be the right decision”

Nitish Kumar, Loan Market Canberra

cial brokers are employed by banks. “They typically don’t move unless we pay them big money,” says Pham.

“We’ve been finding residential brokers with experience who want to learn and be better, so I bring them on board. I put them through training and mentoring with myself, and the feedback is that it’s very intense and a big learning curve.”

That upskilling is set to continue across the brokerage as it prepares for a relaunch later this year. Under Pham’s leadership, there is a detailed plan that aims to build the business out and capture a slice of the residential market.

“All I say is ‘watch out’ for all those other businesses out there,” Pham says. “People are always searching for professionals who know a bit more to help them get more. We have the expertise and knowledge, and the team is good. We’re going to expand a lot in that space –that’s the big plan for the next 12 to 24 months.”

Top Brokerage rank: 47

Location: Mount Waverley, Victoria Years in operation: 4

Conversion rate of loans settled or written: 66%

Weme Finance director and principal finance broker Joanne Liu isn’t surprised by her brokerage’s growth, as she was her own target customer. Previously working in a corporate role and as a certified practice accountant, she could see her peers needed mortgage brokers to satisfy their needs.

“Coming from a professional background, I wanted to help people like me,” Liu says. “Even though I had a master’s degree in banking finance and the knowledge, I didn’t have the time to manage my own mortgage.”

Weme was created to target professionals

such as lawyers, doctors, accountants, etc. Liu also pitches towards self-employed business owners, as her accounting skills mean she can decipher their financials and understand their limitations. All eight of the firm’s brokers share the same background as Liu.

“That’s the main point of di erence; we are a band of people who are coming from finance and accounting backgrounds,” says Liu.

With such a targeted customer base, Weme must operate accordingly. It is open to booking meetings between 9 p.m. and 11 p.m.

Liu says, “We make ourselves available even at weekends, especially for that first meeting, to understand their goals and show them the possible options. They’re super busy, but we accommodate them, as I believe it’s far better to meet each other to form a bond and create a sticky relationship.”

The major driver of the brokerage’s success is Liu’s determination. She founded the business on 6 June 2020, had her accreditation by the end of July, and secured her first client by August.

By the end of the first financial year, Weme had settled 50 loans, and then this rose to over 100 in the second. The brokerage is currently doing more than double that.

“We deal with a lot of complex cases and complicated structures; that’s how I’ve also made the brokerage di erent,” says Liu.

Getting those tricky cases over the line isn’t the end point for Weme. Liu has instilled a deeply service-oriented mindset.

She says, “We always believe we need to provide outstanding service to the clients, as a lot of brokers focus on just winning business.”

Weme prides itself on presenting clients with a range of options and letting them choose what is best for them.

“We don’t promise anything we can’t deliver, and we don’t push people to take the option that we prefer. Everything is trans-

parent, and we make the client understand using simple language, so what they choose is in their best interest, not ours,” says Liu.

Another feature of Weme’s service is monitoring each client’s situation and reaching out to see if something else can be done.

Liu says, “Maintenance doesn’t create any revenue, but it does create potential revenue in the future.”

Top Brokerage rank: 50 Location: Canberra, ACT Years in operation: 4

Conversion rate of loans settled or written: 72%

Loan Market Canberra’s success allows its people to play to their skill sets.

Franchise owner Nitish Kumar says, “Most brokerages get so caught up in admin, so one of the big things I wanted when I started the business was for brokers to be able to focus on the client and not worry about the backend. That’s why we built out a really large admin team.”

This has a twofold benefit:

• Brokers focus on being in front of the client

• The client gets an enhanced service experience and can reach their broker much more easily

The second arm of Kumar’s overarching strategy is to ensure that brokers are as productive as possible with their clearer schedules.

“It’s important for me that the brokers are not working six or seven days a week. I make sure that they have a good work-life balance and can spend time with their families.”

To this end, Loan Market Canberra oper-

ates a nine-day fortnight, giving those with children or other commitments a day back solely for them.

The rapid rise of the brokerage isn’t down to chance; Kumar had a clearly defined blueprint from inception.

“I started with, ‘What does 2030 look like?’ And then I worked backwards so I thought of all the problems.”

The building blocks are:

• 20 brokers

• avoiding burnout by promoting work-life balance

• large admin team to take the load

• end target of $1 billion annually (2,000 loans)

Remarkably, every person in the business has come in via referral, fortifying the internal atmosphere.

“They are automatically part of the culture because they already know someone, and that person ends up taking accountability for inducting them into the business,” says Kumar. “We know that a sta member would not recommend a person who’s not going to be good.”

Loan Market Canberra sees most of its sta choosing to come to the o ce daily, even though they do have the option to work remotely.

Kumar has correspondingly moved into a supervisory role, devoting time to solving complex cases due to his experience.

He says, “When I had clients, my ability to actually be available was pretty limited, so the idea behind getting o the tools was to have a bit more time. But the brokers all help each other and come together if they need to find a solution. If they’re really struggling, then I end up being the last resort, but we definitely aren’t set up in a way where I am the first resort.”

Simplicity Loans & Advisory (SLA) has retained its crown as MPA’s Top Brokerage of 2024.

Co-founder and managing director Matthew Johnson says, “To be recognised among all these top businesses and to actually be number one two years in a row is a fantastic honour for our team.”

Despite its success and industry standing, SLA still views itself as a young business after only being in operation for seven years.

“We’re always looking for ways to do things better or efficiently because we’re still in that mindset of not necessarily a startup but maybe not far off it,” says Johnson.

One element of the firm’s continued success is linked to its youth, as its team is now a year older with greater experience under its belt. It has been able to refine its skills, gain more expertise and understand how best to leverage its tools.

According to Johnson, a key driver of SLA’s repeat win is providing clearer focus to brokers. The firm has been given more definitive boundaries for the markets to operate in.

“That’s from the really complex large transactions through to property specialists who are focused on developments, construction and helping developers with every part of their deal cycle, through to our trading business and mid-market specialists who are doing the slightly higher volume deals,” says Johnson. “Having that bit of a clearer focus has meant they have gotten better at those types of deals, rather than trying to do a little bit of everything.”

The other major development has been

SLA’s tech platform. It has gone live and has enabled the team to do higher volumes and be more efficient. The ominous news for the rest of Australia’s brokerages is that there’s an update coming that’s predicted to be a ‘game changer’.

Johnson says, “I think we’ll see a massive jump in that efficiency dividend for our guys off the back of that technology.”

Efficiency is the key word when it comes to SLA. The firm operates with nine loan writers, whereas brokerages with similar total loan book values have up to three times as many loan writers.

This ability of SLA to punch above its weight has been embedded in the business from the start.

“From the very beginning, we’ve tried to create processes and systems to leverage technology,” says Johnson. “To give an example, when a lead comes in, it goes through a standardised channel even though we’re commercial and a lot of people say every commercial deal is bespoke. To a large extent, I agree, but you can still leverage the technology to allow that to move through from start to finish as efficiently as it can.”

Proving how effective its system is, SLA’s average ticket size is around $4 million, up from $1.3 million when it began. To do this, the brokerage has created a team by honing the skills of young brokers.

Johnson says, “Our bias is to bring in more junior staff and promote them. So, they very much become part of the DNA and understand how we like to go about things.”

The standard for anyone joining the

Phone: 1300 022 022

Email: enquiries@simplicity.net.au

Website: simplicity.net.au

business is the internal phrase, ‘we want people that want to play for Australia’.

“If you want to just play park football for your local suburb, there’s nothing wrong with it,” says Johnson. “But we want people who are aspirational and who want to really push themselves for excellence. That doesn’t mean killing yourself at your desk for 24 hours a day. It just means wanting to really push yourself to be the best you can.”

That drive is maintained by Johnson’s business partners, Jean-Pierre Gortan and Ryan Nelson, who have complementary skill sets to support and energise the team, ensuring that there is a strong sense of care, while also instilling a belief in continual improvement.

Johnson says, “We always make sure we celebrate our wins, then we pick ourselves up the next day and go again.”

The executives are keen to share the award with the entire staff, the lenders they work with, their aggregator partners and also their clients, who have all empowered SLA to shine brightly and retain its title.

$4.49bn

Total loan book value (all loan types)

$1.15bn

Total value of settlements (all loan types) from 1 January to 31 December 2023

89%

Conversion rate of loans settled or written

Ian Rakhit, representing Bankwest, the proud sponsor of MPA’s Top Brokerages 2024, presents the prestigious award to the accomplished team from Simplicity Loans & Advisory (SLA)

MPA’s annual survey unveils how brokers ranked Australia’s aggregators in 2024 across time-tested metrics such as commission payments, lending panel quality, IT, CRM and BDM support

BROKERS CONTINUE to assert their influence in Australia’s mortgage market, shedding light on the dynamics of the third party distribution channel and the standout support aggregators provide amid ongoing market fluctuations.

MPA’s Brokers on Aggregators 2024 report uncovers that broker satisfaction levels have experienced a moderate decline, dropping seven points, despite brokers being indispensable partners.

This shift in sentiment doesn’t mean the sky is falling, as aggregator loyalty remains deep, with 74% of brokers indicating they are extremely unlikely to take their business to a competitor.

This year’s top mortgage aggregators fiercely advocate for broker interests in a demanding consumer and lending market, providing the key ingredients to ensure broker success.

progressive approach that goes beyond simple loan applications and CRM, using innovation to make the process easier for brokers and customers.”

“Successful aggregators treat brokers as more than just a number,” says Liberty chief distribution o cer David Smith. “They understand and invest in their business at the grassroots level and maintain strong relationships with key lenders.”

He adds, “The aggregators that set themselves apart embrace technology with a

The top-ranked aggregators have surpassed expectations on trusted performance indicators, as demonstrated by these comments from respondents on the broking community’s top three priorities:

Timely commissions

• “They allow us to access the commission before it is o cially received, aiding cash flow”

Lending panel quality

• “Continually adding new lenders to the panel provides brokers with more choice for loan products and better variation of lending policy”

IT and CRM support

• “Improved technology helps reduce application time, helping with client refinance growth”

pivotal role aggregators play in the evolving mortgage market.

For award-winning non-bank lender Liberty, Smith asserts that technology is proving to be a challenge and an opportunity, underscoring the critical capability of an aggregator to engage with lenders in ensuring the best outcomes for brokers and customers.

In the first quarter of 2024, the broker market share of residential home loans reached an all-time high of 74.1%, according to the MFAA. This statistic bolsters the

“Customer care and retention will always be vital for brokers to nurture their existing business while attracting new borrowers and marketing for growth,” he explains.

“Looking ahead, we believe the aggregator space will likely see further consolidation, while smaller, boutique aggregators will strengthen competition.

“We expect broking, generally, to face a steady increase in digital competitors, with limited property market supply, elevated interest rates, and living costs all contributing to make aggregators and brokers compete harder for customers.”

As Australia’s broking elite appear poised to expand their share of mortgage originations, the aggregators assisting them in weathering the current storm stand out as essential allies.

Continue reading to explore detailed survey results and other highlights.

In MPA’s 14th annual Brokers on Aggregators survey, brokers were asked to rank their aggregators across 11 categories: accurate and on-time commission payments; IT and CRM support; quality of lending panel; communication with brokers; BDM support; compliance support; training and education; additional income streams; marketing support; white label o ering; and lead generation. Brokers ranked their aggregator with a score from 1 to 5 in each category.

Due to the varying sizes of aggregator groups and the disparity in the number of respondents per aggregator, only those that achieved a response rate of at least 10% of brokers for each aggregator were included in the final list.

MPA also asked brokers a series of questions relating to their aggregator’s service and other needs, but these did not a ect the overall score.

Brokers re-evaluate loyalty as they prioritise tech, service and support, with finances a persistent issue

SURVEY RESPONDENTS attributed the downward shift in aggregator loyalty, falling from 81% in 2023 to 74% in 2024, to various factors, including market conditions, service quality changes and competitive offerings. Still, a majority of brokers expressed strong allegiance to their current aggregators, with one broker commenting, “They’ve given me great support over the years and are excellent to work with.”

Another broker said, “I’m very happy where I am, and I could do more myself to learn from them.”

The top three reasons brokers gave for switching to a competitor have remained consistent since the 2021 report. They included subpar IT, CRM and BDM support, as well as inaccuracies and commission payment delays.

For the fourth consecutive year, commission payments ranked as the most important aggregator service, followed by lending panel quality and IT and CRM support.

The competition for accurate and timely payment of commissions in 2024 was fierce among aggregators with over 600 brokers. Finsure emerged as the gold-medal winner, claiming the top spot from last year’s champ, National Mortgage Brokers, who secured the bronze. Loan Market maintained its solid silver standing.

In the boutique aggregators group, MoneyQuest rose to gold from its silver finish last year. Nectar Mortgages debuted with a silver win, and bronze went to Liberty Network Services, which claimed the gold last year.

“The competition for accurate and timely payment of commissions in 2024 was fierce among aggregators with over 600 brokers”

Brokers were vocal about commissions, highlighting concerns and suggestions related to commission structures, clawbacks and aggregators’ perceived processing methods:

• “Better commission splits should be implemented once brokers reach a certain book value. Establish a target, and once achieved, the trail commission should increase”

• “Fight harder against clawbacks”

• “Commission processing should be stronger and more automated”

• “Petition all lenders for higher commissions. Brokers are handling double the workload, and lenders should process these deals within minutes”

The proportion of brokers who said they were very happy with their aggregator’s fees and commission split also showed a slight decrease in 2024, from 68% last year to 65%.

A small but slightly higher margin of brokers expressed dissatisfaction, while just under a third indicated mild satisfaction, resembling results in the previous year.

The specifics of brokers’ annual settlement values were roughly the same for the past two years, showcasing their resilience to persistent economic challenges and ability to work effectively with their aggregator

partners to help clients achieve their goals.

The 2024 brokers’ settlement values were:

24% $0–$10m (two points less than last year)

24% $10,000,001–$20m (one point higher than last year)

25% $20,000,001–$40m (one point higher than last year)

13% $40,000,001– $60m (one point higher than last year)

14% More than $60m (one point lower than last year)

Unsurprisingly, survey respondents’ top reasons for leaving their aggregator correlate to the core services they appreciate most: commission payments, IT, CRM and BDM support.

Brokers pulled no punches in expressing their opinions on the issues, signalling the essentials that the best mortgage aggregators need to retain their business:

• Service and support: administrative and compliance assistance, as well as

communication, transparency and leadership from the top down

• Technology and tools: user-friendly CRM systems, calculators, IT support, and investment in emerging tech stacks and solutions

• Financial factors: competitive financial arrangements and incentives, diversification opportunities

Among aggregators with 600+ brokers, the reigning champ, outsource Financial, retained its gold medal for IT and CRM support. Loan Market successfully battled back to take silver after scoring bronze last year, and Specialist Finance Group took third place in a tight race.

For boutique aggregators, MoneyQuest’s three-year gold reign continued, Nectar Mortgages took silver, and the bronze went to Liberty Network Services.

“Working with highly rated aggregators ensures consistency and quality of applications, minimal back-and-forth and a deep understanding of the regulatory environment,” Liberty’s Smith says.

HIGHLIGHTS: MONEY AND IT SUPPORT ACCURATE AND ON-TIME COMMISSION PAYMENTS

INCOME STREAMS

HIGHLIGHTS: LENDING PANEL AND SUPPORT

QUALITY OF LENDING PANEL

Aggregators

COMPLIANCE SUPPORT

Aggregators Aggregators

value the quality and diversity of an aggregator’s lending panel, as evidenced by its three-year run as No. 2 on their priority list.

Lending options significantly influence brokers’ decisions to jump to a competitor, consistently ranking among the top five reasons they would leave their aggregator.

Loan Market has clinched the gold medal by a commanding margin for its lending panel quality among aggregators with 600+ brokers for three consecutive years. outsource Financial netted silver, and Specialist Finance Group won bronze.

Among boutique aggregators, Nectar Mortgages won the gold medal, MoneyQuest nabbed silver, and Purple Circle Financial Services took the bronze.

lending panel, with some noting they would like to have:

• “greater access to lower-tier lending solutions”

“If aggregators could offer quality leads with sufficient borrower income to service average loans, that would be helpful”

The size and diversity of aggregators’ lending panels appear to coincide with overall broker satisfaction, as brokers often prioritise access to a wide range of lenders offering competitive rates and products, facilitating greater flexibility and opportunity for their clients’ needs.

MPA’s survey data suggests that brokers are mainly satisfied with their aggregator’s

• “a better comparison tool for commercial lending”

• “more private lenders to assist with shortterm funding”

• “improved panels with more non-banks and major banks”

When asked which lenders they would like added to their panel, long-standing favourites

Liberty, HSBC and Bank Australia were most often mentioned.

Compliance support endures as a fourthplace broker priority, in tandem with a reason they might leave an aggregator. Some respondents, however, believe that some aggregators have been slow to adapt to market changes, and concerns about clawbacks and fees draw the ire of many:

• “The broker industry needs to apply pressure to the banks to keep their interest rates competitive, as well as reduce clawback terms extensively”

• “They do not understand the franchise model and have made it harder for us to do the same thing we were doing before”

• “Our aggregator is destroying the legacy and goodwill built by generations past”

• “They have been too slow to change to a purchase market from a refinance market”

Other brokers offered kudos to their aggregators for their unwavering support in providing professional indemnity insurance coverage within their fee package, and education on interest rates and compliance.

Another trend among brokers revealed an increasing concern about hidden costs imposed by their aggregators. Since the strong trust level of 90% was recorded in 2021 when brokers indicated it wasn’t a problem, there has been a drop in that figure to 76% this year, compared to 82% in both 2023 and 2022.

Those who stated that it was either a minor or major problem also increased to 24% from 18% in last year’s survey. Combined with an 8% bump recorded in the 2021 data, this indicates a substantial rise, suggesting that broker confidence in their aggregator’s commitment to transparency has been eroding.

Brokers have highlighted this issue:

• “From my perspective, they want to increase the fees generated per broker. I’m not sure

how that assists brokers to reduce costs”

• “Marketing costs are charged per deal, not per customer. That means if I settle three loans for one customer, I get charged three times”

• “Every add-on costs money, so monthly fees end up being very high”

BDM support held strong in fifth place again this year with a marginally higher importance rating of 4.6 out of 5. This result suggests a continued emphasis on business development support focused on education, coaching and proactive communication.

“Get the BDMs out of Sydney for the country brokers,” a respondent said.

Another broker said, “There is a vast array of products and services available for a fee, and it is hard to know what to focus on.”

For the third consecutive year, over half of brokers cited the lender reaccreditation process as a stubborn obstacle to switching aggregators.

“Lenders and aggregators appear not to support a streamlined reaccreditation process across all parties,” one broker asserted.

Data migration and IT issues ranked as the second biggest issue for two years running, with notably fewer brokers saying lack of time was a hurdle.

If brokers could change aggregators tomorrow, their favoured choice would be Connective at 20%, Finsure at 11% and Australian Finance Group at 8%.

While Connective is down significantly as a top broker pick from 33% last year, brokers repeatedly lauded its flat-fee model and superior CRM, technology and tech tools.

“I have switched to Connective in the last six months; their commission splits are more reasonable, and the CRM and branding system is much more flexible,” one broker said.

Brokers commented that Finsure had good IT and internal processes, compliance

support, flexibility, a flat-fee model and positive referrals.

Helping brokers adjust and thrive in a rapidly changing mortgage market with higher interest rates and inflation is a hallmark of the best mortgage aggregators.

This broker captured what places the industry-leading aggregators at the forefront: “I have been with my aggregator for over 10 years and will be with them for life. They are supportive in all areas of broker development.”

HAS YOUR AGGREGATOR DONE ENOUGH TO SUPPORT YOUR PROFESSIONAL DEVELOPMENT, INCLUDING DIVERSIFYING INTO COMMERCIAL LENDING?

With broker market share of residential loans at more than 74%, MPA asked the broking community if their aggregator was doing enough to boost this share further, and what more they could do

“Brokers are doing this by default. I would rather my aggregator fought harder against clawbacks, which should not be worn by the hard-working broker who is forever living in fear”

“Simplify compliance processes to improve brokers’ cost competitiveness vs direct bank channels”

“Yes. They are constantly advertising and pushing for more people to use brokers and improving the competitive reach of our panel. They always offer to help with more outsourcing or external offerings to keep buyers coming to us instead of banks”

“That’s a role for brokers themselves, but the cost of advertising a small broker service is prohibitive”

“Run more broker workshops to hear our ideas and feedback”

“Have smart BDMs and support for leading brokers who are writing $100 million to grow further”

“Get us faster approvals from banks, our biggest competitor. Waiting five to 10 days for a major to get approved, when customers can walk into a branch and get it done within 24 hours, highlights our need for speed”

“Be more proactive in ensuring commissions are paid on time”

“They are doing enough by being so actively involved in the market”

“Focus on existing brokers to increase market share, as opposed to increasing broker numbers”

“My aggregator has bent over backwards to help me grow my book”

“BDMs that do more than try to sell add-ons. If a BDM could understand my business and give me one recommendation that would provide a better lead stream based on their knowledge of other like-sized businesses, then this would assist”

MPA presents the final ranking of Australia’s top aggregators and boutique aggregators in 2024 based on brokers’ votes across 11 award categories

Leading aggregators discuss hot topics such as broker market share, serviceability, payroll tax and diversification at MPA’s annual roundtable

THE MORTGAGE BROKING industry is enjoying unprecedented levels of support from the Australian public.

The latest MFAA figures show that in the March 2024 quarter, 74.1% of all new home loans were written by mortgage brokers – a record figure, which has surpassed the previous record of 71.8% for the October to December 2023 quarter.

Australians are increasingly placing their faith in the skills and knowledge of brokers to help them buy their first home, refinance for a better deal or purchase an investment property. But that doesn’t mean everything is rosy in the world of broking. Five increases to the Reserve Bank’s o cial cash rate since the beginning of 2023 and a higher cost of living mean reduced borrowing capacity, with some

people unable to refinance due to serviceability constraints.

Brokers are working harder than ever for customers in a competitive market, and the level of refinancing has fallen since the peak about 12 months ago, with fewer lenders o ering cashbacks. This means diversification into areas such as commercial and asset finance will become increasingly important

for brokers as they look to cover all their clients’ finance needs.

The issue of payroll tax also looms large after the Federal Court found that LMG was liable for payroll tax, albeit with exemptions, with ramifications for the way brokerages are structured and operate.

New technology and ongoing training are necessary to ensure brokers can continue to

serve their customers well and grow their businesses. The support of aggregators remains crucial as brokers navigate both the challenges and opportunities of the market in 2024.

MPA invited leading aggregators to join its annual roundtable at Sydney’s Nobu restaurant. Attending the event were Blake Buchanan, general manager, SFG; Brad

Cramb, chief distribution officer, Lendi Group; Gerald Foley, managing director, nMB; Them Lam, head of sales and distribution, AFG; Daniel Marsi, CEO, Liberty Network Services; Tanya Sale, CEO, outsource Financial; Aaron Slater, general manager distribution, REA Group (Mortgage Choice), and Sam White, executive chairman, LMG.

Two brokers also attended: Kristie Gould, franchisee, Mortgage Choice Warners Bay, and Adriana King, principal finance broker, Expand Equity.

How have aggregators worked closely alongside their broker members to support them and their customers in a challenging lending environment?

There have been a variety of challenges for mortgage brokers over the last 12 months, with fewer customers borrowing for property purchases and refinances dropping, while interest rate rises and inflation have affected borrowing capacity and serviceability, with borrowers rolling off low fixed rate loans onto much higher rates.

The aggregators said serviceability was one of the biggest challenges, but all shared a sense of optimism about the future, with a focus on supporting brokers through

education to adapt to a changing market.

Sale said the challenges hadn’t just been interest rate rises or lender policies.

“I think it’s about the brokers getting guidance and education on sticking close to the consumer,” she said. “I think that’s been the challenge all the way through the turmoil with these interest rate rises.

“I think the lending’s going well. There’s now more competition outside of the majors, which I feel brings some balance within our industry.”

Sale said the industry had to stop giving such a large percentage of loan business to the major banks.

“The non-majors and other lenders have got to step up so we have a very vibrant, dynamic and competitive industry.”

White said, from LMG’s perspective, loan serviceability had been one of the biggest challenges for brokers, and hopefully that would change next year.

“In the last 12 months, brokers are probably working harder than they ever have for probably the same, maybe slightly less in some cases,” he said.

Brokers had put a lot of energy into looking after customers in an environment in which it’s been difficult to get serviceability. “The implications are having to stay in contact with clients for longer, deals taking longer.”

White said LMG was training brokers in this area, including “engaging customers beyond the transaction”.

Sale said it wasn’t the lending policies that were a challenge, it was the serviceability.

Lam noted that wage growth hadn’t caught up, and unemployment had risen slightly. He said AFG’s focus was on its broker members and their customers. “We’re looking at the whole broker business and ways to help our brokers improve profitability, given that some are not settling as much, or loans are taking longer to settle.”

Everyone was talking about broker diversification, he said, and AFG was educating brokers to “take that first step to identify the customer” that needs diverse services.

Lam said AFG not only led the charge in introducing approved policies to enable brokers to utilise (1%) serviceability buffers for their “mortgage prisoner” customers, but had also created a brand-new product including the 40-year interest-only (evergreen) loan for mature-age borrowers looking for greater repayment flexibility as they transitioned into retirement.

White said the value of brokers was on display when it came to tackling serviceability.

“You need to have niches, you need to understand where your product is. It just goes to show why broker market share is going to keep growing, because the tighter it gets, the more customers are going to need an adviser, and that’s been a real upside this year for the industry.”

Foley agreed with White and said the value of brokers was that they were across all the lenders’ activity when it came loans.

“The banks seem to be revisiting their mix more frequently now,” Foley said. “They see

an opening – they’ll price to win and get a good inflow. Then they’ll tighten a bit or someone else will come in.”

He said one of the major banks had been almost “double sharing” off the back of policy and pricing changes, which was good for brokers and their customers.

Sale said it was a challenge to ensure the major banks didn’t dominate again. “At one stage in the industry, we got to a really nice balance, where the [loan] percentages were a really nice spread. We need the other

constraints and the challenges brokers faced with customers rolling off fixed rates.

Cramb said Lendi Group had approached these issues from an industry advocacy perspective, setting up and publishing a ‘loyalty tax index’ 18 months ago, which looks at front-book and back-book pricing.

“The great news is … customer awareness of this then drove a reduction in that index,” said Cramb. “We were at 70 points only 18 months ago, between back book and front book; we’re now tracking at 10. So

“It’s OK for pundits to talk about diversifying and tell people to do it –[but] when the rubber hits the road, they need to know how, and that’s where education and training come in”

Blake Buchanan, SFG

lenders to lift so it can become a very balanced environment.”