Brought to you by Thewww.jacketmediaco.comManufacturing&BusinessPodcastNetworkLISTENTOOURPODCASTSAT:OURPODCASTS: AUGUST ISM PMI: 52.8% Released September 1st -The Full Executive Summary Report On Business - Page 22 [ FEATURE STORY: PROPOSING A GOAL FOR U.S. MANUFACTURING SUCCESS PAGE 10 IN MEMORIAM: THOMAS R. CUTLER INDUSTRIAL JOURNALIST PAGE 26 ASIA OUTLOOK PAGE 40 GLOBAL PMI OUTLOOK PAGE 45 ENERGY OUTLOOK PAGE 52 CYBER SECURITY OUTLOOK PAGE 58 STATE OF INDUSTRIAL MEDIA: 2022 AND BEYOND PAGE 28

3Manufacturing Outlook / September 2022 JOIN THECAUS E JOINTHE CAUSE Help change the perception of Manufacturing in the USA! www.championnow.org terry@championnow.org 847-299-2461 Finding America’s Greatest Champion Audio Book $24.99 l eBook $9.97 Paperback $21.99 l Hard Cover $27.99 Training CNC Mill and Lathe Package Table Top Champ CNC Lathe $7,795 l Table Top Champ CNC Mill $7,795 (requires laptop or PC for each ) Package with laptop $16,995 ➧ ➧ OUR FUTURE DEPENDS ONCNCYOU.RocksVirtual Manufacturing Camp 22 videos 4.5 hours in length Schools: $500 annual subscription Industry: $750 annual subscription ➧ www.championnow.org Champion Individual Annual Corporate Membership For companies of 200 or less employees — $995 For companies over 200 employees — $1,995 With your NOW!membership you receive: l Applicant Advantage Annual Membership (student video resume portal) l Annual membership certificate l Finding America's Greatest Champion Book (signed by Terry Iverson) l CNC Rocks Virtual Manufacturing Camp (annual subscription) l Access to networking community/mentoring focused on MFG workforce development l A promotional video produced by your company posted to the ChampionNOW ROKU Channel

4 Manufacturing Outlook / September 2022 © 2022 Jacket Media Co. No part of this publication may be reproduced or used in any form with out the prior written permission of the publisher. Manufacturing Outlook is a registered trademark of Jacket Media Co. Publisher LEWIS A WEISS Editor in Chief TIM GRADY Creative Director CRAIG ROVERE Contributing Writers ROYCE JEANNE-MARIETHOMASNORBERTLOWEORECHRISKUEHLR.CUTLERAMELIAROYLOWRIECHRISANDERSONLAWRENCEMAKAGONCHRISTINECASATIKENFANGER Production Manager LINDA HOPLER Advertising ADVERTISE@MFGTALKRADIO.COM Editorial Office JACKET MEDIA CO. 75 LANE ROAD FAIRFIELD, NJ 07004 (973) 808-8300 TABLE OF CONTENTS Accelerating The Next Generation of Power Electronics INNOVATION OUTLOOK 48 Forward-Looking, Forward Thinking PUBLISHER’S STATEMENT 5 How Green Is Going by Dr. Chris Kuehl NORTH AMERICA OUTLOOK 32 Chile, a New Era? by Royce Lowe SOUTH AMERICA OUTLOOK 36 Electric Trucks and Things by Royce Lowe AUTOMOTIVE OUTLOOK The F-35 and the 787 by Royce Lowe AEROSPACE OUTLOOK 50 King Coal’s Getting Richer by Royce Lowe ENERGY OUTLOOK 52 Cost Inflation Easing by Royce Lowe MANUFACTURING OUTLOOK 6 Risk Assessments and Uncovering Your Cyber Security “Why” by Ken Fanger CYBER SECURITY OUTLOOK 58 ISSUES OUTLOOK 60 CHIPS: Start of a Long Journey. by Royce Lowe MATERIALS OUTLOOK 54 Australia, Metals, Batteries, EVs ; and Ford by Royce Lowe Insights From Inside Manufacturing In Action MANUFACTURING TIDBITS U.S. Economy Expands by Norbert Ore GLOBAL PMI OUTLOOK 45 Open call for... Contributing Writers for new and existing content. Let’s start a conversation –Contact us at info@jacketmediaco.com or visit mfgtalkradio.com/writer for more information. ISM MANUFACTURING REPORT ON BUSINESS 22 The Manufacturing PMI is 52.8% 8 FEATURE STORY: PROPOSING A GOAL FOR U.S. MANUFACTURING SUCCESS by Harry Moser Future Manufacturing Africa: Trade Fair and Summit 2023 by TR Cutler AFRICA OUTLOOK 38 Making Sense of the Semiconductor Supply Chain by Christine Casati ASIA OUTLOOK 40 Eurozone PMI continues contraction by Chris Anderson EUROZONE OUTLOOK 44 by TR Cutler WMS SPACE: ACHIEVING RAPID TIMETO-VALUE (TTV) 14 ISO CERTIFICATION: THE PROS, CONS, AND LOOKING AHEAD 16 US CUTTING TOOL ORDERS TOTALED $173.2 MILLION IN JULY 2022, BRINGING YEAR-TO-DATE TOTAL TO 7.7% OVER 2021 18 COVER STORY: STATE OF INDUSTRIAL MEDIA: 2022 AND BEYOND 28 by Lewis Weiss In Collaboration With TR Cutler 56 Cass Transportation Systems CASS FREIGHT INDEX® REPORT BY CASS INFORMATION SYSTEMS INC. 20 by TR Cutler IN MEMORIAM: THOMAS R. CUTLER 26 by Lewis Weiss

5Manufacturing Outlook / September 2022 PUBLISHERS STATEMENT

SUBSCRIBE

Manufacturing Outlook is continuously tweaking its content to parse and provide forward-looking, forward-thinking information to the industry so manufacturing can navigate the currents of change, innovation, and disruption. The digital ezine partnered with Manufacturing Talk Radio, where viewers on YouTube and listeners on Apple Podcasts, Google Play, Spotify, iHeartRadio, and dozens of other podcast platforms can hear industry thought leaders contribute to the

Manufacturing Outlook examines manufacturing trends globally, with reports on Canada, the U.S., South America, Europe, Asia, and the emerging market of Africa. Although there are more than 10 million job openings in the U.S., reshoring is still a strategic alternative to labor costs and offshore production. Chip production is shifting back to plants in the U.S. with plant expansions (Texas Instruments) and new construction (Intel, Samsung, Taiwan Semi-Conductor) with the passage of the CHIPS for America Act.

Forward-Looking, Forward Thinking

around a possible recession is discussed with Dr. Chris Kuehl on the Flagship Reports. The Manufacturing Report on Business® with Tim Fiore, Committee Chair from the Institute of Supply Management, includes manufacturing industry insights that will play out over the next few months. Manufacturing is a bellwether industry because production times range from 6 months to two years in some sectors, so softening of New Orders directly impacts employment requirements well into the future. Reductions in headcount will reduce consumer spending, and this indicator has not yet appeared in any employment data. Manufacturing Talk Radio is the only source for this type of in-depth analysis, with reports from the ISM, including the Services Report on Business® with Committee Chair Anthony Nieves, and the Hospital Report on Business® with Committee Chair Nancy LeMaster, which have a track record of more than 70 years (referencing the Manufacturing Report on Business®) of key indicator information.

FOLLOW US:

Muchconversation.ofthenoise

On Moser on Manufacturing, Harry Moser highlights the need to reshore pharmaceuticals, medical devices, and medical suppliers, such as IV contrast dyes. Presently, GE Healthcare is one of four suppliers, and the other three have not been able to ramp up production to offset the shortage created by the lockdowns in Shanghai and the shutdown of the GE Healthcare production facility there (now reopened). The pandemic exposed other critical component shortages in the supply chain, and reliance on other nations for components and healthcare needs could cripple the U.S. if geopolitical relationships fracture in the future.

Manufacturers are always looking for ways to improve their operations and grow their businesses. The Internet is the Niagara Falls of information, and manufacturers are standing below it with only a cup. Readers of Manufacturing Outlook are above the falls observing what is in the information stream before it becomes a cascading torrent of “Now and How.”

A further example of geopolitical impact has been the invasion of Ukraine by Russia, which was discussed with Dr. Chris Kuehl on the Flagship Reports. Manufacturers and agriculture have already seen the effect with energy cost spikes and increased commodity demands. The U.S. has become too comfortable and dependent on overseas supplies that didn’t seem particularly strategic before the pandemic.

When manufacturers are looking for forward-looking, forward-thinking information, Manufacturing Outlook is an excellent source worth reading. Subscribe today! n Lewis A. Weiss, ContactPublisherlaweiss@mfgtalkradio.com for comments, suggestions and ideas and guest requests for MFGTALKRADIO.COM podcast or any of our podcasts.

6 Manufacturing Outlook / September 2022 MANUFACTURING OUTLOOK

The Bureau of Economic Analysis says the U.S. Real Gross Domestic Product decreased at an annual rate of 0.6% in the second quarter, according to the second estimate. This was following a decrease of 1.6% in the first quarter of

There2022.

CRUDE STEEL PRODUC TION WAS DOWN BY 6.5 PER CENT YEAR-OVER-YEAR IN THE MONTH OF JULY for the 64 reporting countries – which represent 98 percent of world crude steel production – to 149.3 million tons (MT). Production for the first seven months was down 6.4%

GLOBAL2021.

U.S. Light Vehicle sales for August are forecast to show the first year-over-year gain in 12 months. Ford, Hyundai, and Kia are doing well, Honda and Toyota are tumbling. EVs in the U.S. are at 6% of total sales, up from 3.3% in August

in the G7 countries, with Canada at 1.75%; Japan at 1.7%; France at 1.0%; U.S. at 1.0%; Germany at 0.75%; Italy at 0.7% and UK at 0.5%. Or a little over 50%, overall, of what they forecast 2022’s GDP growth will be.

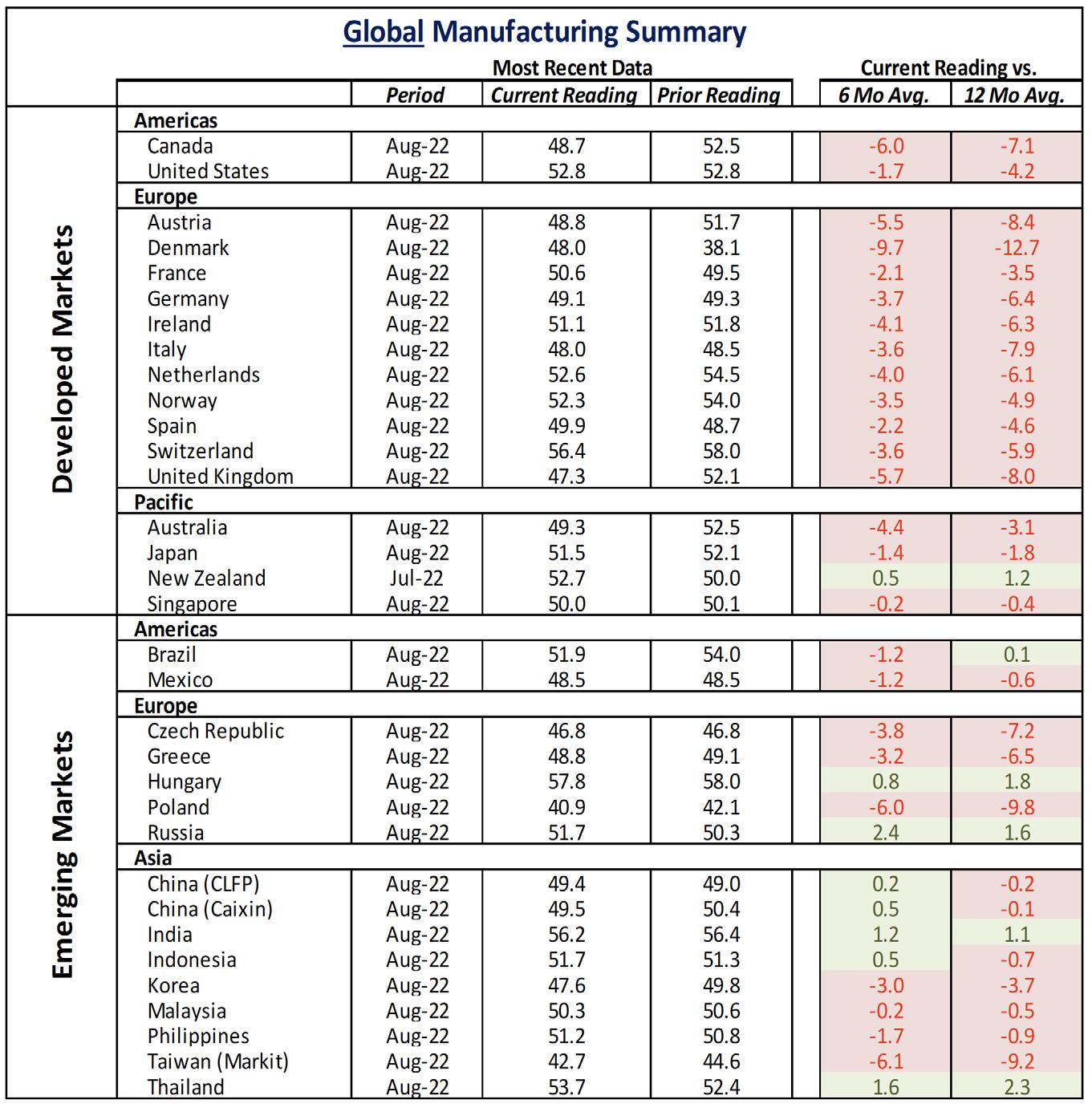

The JP MORGAN GLOBAL MAN UFACTURING PMI – a composite index produced by JPMorgan and S & P Global in association with ISM and IFPSM (International Federation of Purchasing and Supply Management) – fell from 51.1 in July, to 50.3 in August, a 26-month low. There were downturns in production, new orders, and international trade. Production fell in the consumer, intermediate, and investment goods sectors. Input cost

were 315,000 nonfarm jobs creat ed in the U.S. in August, and the unem ployment rate rose from 3.5% to 3.7%. Professional and Business services were up 68,000; Health Care 48,000; Leisure and Hospitality was up 31,000, com pared to the average 90,000 in the first seven months of the year. There were 22,000 manufacturing jobs created. The IMF recently published what it forecasts as GDP growth rates for 2023

Theyear-over-year.globalproduction of primary alu minum continued at its normal pace in July, with China producing almost 60% of the 5.848 MT total. This in spite of China’s efforts to cut down on electrici ty

Theconsumption.priceofhot-rolled coil in the U.S. in early September was around the $780

OUTLOOKMANUFACTURINGGLOBALMANUFACTURING,INTERNATIONALTRADESTILLSLIDING.U.S.,JAPAN,EUROZONEANDUKINCONTRACTION.COSTINFLATIONEASES.CARSDOINGBETTER.OPTIMISMINDEXUPSLIGHTLY. continued

By: Royce Lowe

and selling price inflation both eased. Ten of the 30 nations for which data are available showed increases in produc tion, most of which showed marginal growth. The U.S., the Eurozone, Japan and the UK were among the larger economies to show contraction. Business confidence edged up in Au gust, to a three-month high.

per ton mark. The prices of non-ferrous metals in August showed little change over the month, with aluminum from $1.20 per lb. to $1.17 per lb; copper from $3.50 to $3.60; nickel from $10.10 to $9.60; zinc from $1.53 to $1.63.

Author profile: Royce Lowe, Manufacturing Talk Radio, UK and EU In ternational Correspondent, Contributing Writer, Manufacturing Outlook.

THE ECONOMIST magazine, in its latest weekly report on world econ omies, highlights changes in Gross Domestic Product (GDP), Consumer Prices, and Unemployment Rates for what it considers the world’s major economies. These data are not neces sarily good to the present day, but are mostly applicable to at latest the past two months, and show definite trends in the world economy. The figures are qualified as being the latest available, and with reference to a given quarter or month. The figures for GDP repre sent the percent change on the previous quarter, or annual rate. The consumer price increases represent year-over-year changes. The unemployment percentag es are for the month as noted. n

7Manufacturing Outlook / September 2022 MANUFACTURING OUTLOOK

PROPOSING A GOAL FOR U.S. MANUFACTURING SUCCESS

8 Manufacturing Outlook / September 2022 continued

Making Sense of the Semiconductor Supply Chain

environment that attracts more FDI (foreign direct investment). Follow ing, I discuss the potential benefits of reshoring.

Doing the Math

Since 2010, the rate of offshoring slowed from approximately 200,000 jobs each year to about 100,000 each year. Over the same period, the rate of reshoring increased from approxi mately 6,000 jobs each year to about 150,000 each year, resulting in a net gain of approximately 50,000 jobs each year. While this is a promising start, at this rate it would take close to 100 years to close the current 5 million-job deficits. Achieving an average increase of 250,000 net jobs each year would balance the $800 billion/year goods

The future state of U.S. manufacturing depends substantially on our success in reducing, rather than further increas ing, our approximately $800 billion goods trade deficit, excluding petrole um. That deficit, after adjustment for price differences, equals about 40% of actual U.S. manufacturing output, 5 million manufacturing jobs at current U.S. productivity levels. With a diverse and educated workforce, abundant nat ural resources, top technology, and the world’s largest GDP, the United States can be less dependent on imports than other countries, but we currently have trade deficits with nine of our top 10 trading partners. Less dependence on imports reduces costs and risks related to distance—freight, delivery, invento ry, etc. and country-specific costs and

By: Harry

risks—rising wages, IP risk, political instability, etc. Companies with local supply chains fair better against disrup tion. Stanley Black & Decker reported no increase in costs and “much less im pact from the coronavirus than would have been the case if it had remained in China.” In an interview with CNBC, John Quincey, CEO of Coca-Cola said plant shutdowns were limited to “just a couple of places.” He credited the good outcome to local production of Coke’s soft drinks.

We can make great strides toward bal ancing the trade deficit by doubling the rate at which we reshore, i.e. bring off shored (sourcing shifted from the U.S. to another country) jobs back to the United States and nurturing a business

FEATUREMoserSTORY

trade deficit in just 20 years. Here is the

the current rate of offshoring at about 100,000 jobs each year. Double the rate of reshoring and FDI to about 300,000 jobs each year. Increase the rate of exports (U.S. ship ments to foreign customers) to provide about 50,000 jobs each year. (Every $1 billion in new exports of American goods supports more than 6,000 addi tional jobs here at home, the same ratio as for reduced imports.)

Economistsmarkets.inacademia have long espoused a general position that the United States should make no effort to change market outcomes. If oth

Success in balancing the manufacturing trade deficit within the next 20 years will depend on government actions that increase the price competitiveness of U.S. manufacturing and corporations implementing more rapid automation, skilled workforce training, and greater use of strategic tools like TCO in sourc ing and siting decisions. These actions will drive reshoring, which will, in turn, increase capacity utilization above 80%, and drive automation investment and workforce recruitment.

Economic

Benefits of Success

Offshoring’s impact on the world envi ronment has been significant. Moving manufacturing to developing countries drives higher carbon emissions and other pollution due to reliance on fossil fuels and less efficient power genera tion modalities. Manufacturing goods far away from their ultimate sale and use location results in commensurately higher transportation-related emis sions. In addition to lowering emis sions, less shipping reduces the global quantity and types of packaging and its associated waste. Furthermore, the less environmentally responsible locations will have added incentive to achieve higher environmental standards sooner as they lose business to the environ mentally-conscious United States.

Societal

er countries want to sell products at much lower prices, the United States is enriched by buying instead of making. Others have stated that it makes no economic difference whether we make computer chips or potato chips. For ty years of stagnant median-incomes (about 0.6% each year) and declining economic and industrial resilience, however, suggest that the United States should consider more proactive meas ures.

Importing less and exporting more are the only ways to grow manufacturing at a given level of GDP and goods consumption. We can have much more of an impact focusing on reshoring (importing less) than exporting more because of the costs or “friction” of about 15% associated with exporting or importing. U.S. products are, on average, about 30% more competitive here than exported to, e.g. Asia. Figure 1 uses China as an example. Reducing imports is a larger target since im ports are about 40% higher in value and about 100% higher in volume or weight. The idea is gaining popularity among U.S. consumers at the same time countries implement more regu latory and structural barriers to protect their home

Environmental

U.S. Competitiveness

Maintainmath:

Increasing well-paying manufactur ing jobs in the United States can be a critical factor in supporting recovery from COVID-19 pandemic-induced unemployment. More tax revenue from greater economic activity could help offset spending on stimulus programs and reduce budget deficits. Strength ening U.S. manufacturing through reshoring could increase capital investment by about 20% for 20 years and drive increases in productivity and manufacturing employment, two key factors in increasing manufacturing output and economy growth.

9Manufacturing Outlook / September 2022 continued FEATURE STORY

The United States was producing an estimated 10% of its 2019 PPE (Person al Protection Equipment) requirements. Then in 2020 the pandemic struck and demand increased three-fold and foreign sources stopped shipping. U.S. factories would have had to increase output 30X in a few months. Obvious

Resilience

Increasing reshoring of U.S. manufac turing can have a wide-ranging impact on many other national challenges. For example, reshoring will bring to urban communities well-paying jobs, which can be a critical factor in balancing economic inequality. Reintroducing good job opportunities into rural areas

would help reverse the damage done by trade-related job loss at the heart of the opioid epidemic. An increase in manufacturing will strengthen overall workforce training and recruitment. Increasing well-paying manufacturing jobs in the United States can be a criti cal factor in recovery from COVID-19 pandemic-induced unemployment.

stability, similarities to U.S. laws and culture, geographic proximity, favorable currency exchange rates, and technology savvy make them a good nearshoring choice. Mexico offers wage rates similar to China’s, minimal tariffs, low travel and freight costs, quick delivery, close technical support, and a large, underutilized Theworkforce.traderelationship

pliances and machinery. In essential products, get our annual production up to at least 50% of annual consumption. Strengthen both OEM assembly and the supply chain. Make manufacturing, once again, the career of choice for smart, aggressive youth.

Collaborative Partnerships

between the three trade partners makes it important to consider Canada’s and Mexico’s trade deficits with Asia along with the United States. At the Forum & Expo Mexico Industrial Parks in Monterrey in September 2016, I urged Mexico to focus more on reducing its trade deficit with China and less on increasing its trade surplus with the United States.

ly impossible. A key consideration, therefore, is what level of production is necessary to be resilient to potential threats? I propose that, for most prod ucts, the U.S. should produce at least 50% of what it consumes and essen tially all of what it needs for defense. If we cut our manufacturing trade deficit to zero, the resulting 40% increase in production would dramatically reduce dependencies.

FEATURE STORY continued

Work is now flowing out of China, primarily to Southeast Asia. Here’s an opportunity for expanded cooperation via the United States-Mexico-Canada (USMCA) trade agreement to shift work from offshore to nearshore in North Canada’sAmerica.political

Product Mix

10 Manufacturing Outlook / September 2022

Phasing up production over 20 years will allow for incremental and sus tained skilled workforce recruitment and capital investment. U.S. largest trade surpluses are now in aircraft and spacecraft. Europe and China will not accept our getting 100% of those mar kets. I propose that, rather than becom ing even more specialized in aerospace and defense, we become less dependent in other products, e.g. medical, ap

Reshoring is enabling a higher percent age of higher-tech product production than current U.S. manufacturing, thus improving our product mix (Fig. 2).

Offshoring to China and elsewhere has cost approximately 5 million U.S. manufacturing jobs, contributed to wage erosion, and had a dramatic and negative effect on workers and the economy. For example, for every 100 jobs lost in manufacturing, about 700 indirect jobs are lost, but the same number of lost retail jobs equals just about 120 indirect jobs lost. So, the shuttering of an automotive factory would have a greater economic impact than the closure of a retail organiza tion of the same size. As the United States reevaluates manufacturing, sourcing, and purchase decisions, due to tariff and pandemic-induced supply chain turmoil, we should consider the wide-ranging advantages of collabora tive partnerships.

The United States is considering roll ing out an alliance called the “Eco nomic Prosperity Network,” that would

FEATURE STORY continued

Like the United States does inter nationally with our allies, likewise should companies, employees, sup pliers, and communities collaborate to form partnerships that benefit all

Table 1 outlines how the three coun tries could benefit from increasing our Frompartnerships.theU.S.

OEMsstakeholders.andsuppliers

must cooperate to achieve the benefits of local operation: resilience, engineering, manufacturing and communicating easily to optimize product and process. Clusters of three or four U.S.-based companies that, in aggregate, buy from and sell to each other, shortening supply chains so that more of the content is sourced domestically from cluster partners. On incremental sales, in theory, each com pany gives up some margin but picks up volume. Ask the domestic supply chain to share the margin reduction on the incremental volume. Company earnings would be flat or improved.

include like-minded countries, organ izations, and businesses. This venture has the aim of working with U.S. companies to move jobs to U.S.-friend ly countries like Australia, India, Japan, New Zealand, South Korea, and Vietnam, if they are unable to reshore into the United States.

The United States can build consensus with other developed nations that have similar concerns about Chinese trade. The EU, Japan, and United States have all publicly discussed decreasing trade dependency on China. The countries can collaborate and coordinate efforts to convince China to play by the World Trade Organization (WTO) rules.

Employees, suppliers, community, and the company’s home market would all be strengthened. Companies should strive to eliminate silos. Dr. W. Edwards Deming, American engi neer and leading management expert in the field of quality, offered 14 key

For example, Wisconsin-based Evco Plastics has been adding generally lower skill jobs in its Mexican plastic parts plants, teaching additional skills (“upskilling”) in its U.S. plants, and downsizing in China. U.S. supplied raw materials account for 60% of costs in the Mexican plants and only 15% in the Chinese plants.

Companies, Suppliers, Employees, and Communities

perspective, Mexico and Canada provide greater partnership ad vantages than manufacturing in Asian countries. Forty percent of the value in product shipped from Mexico to the United States is U.S. content and 25% shipped from Canada is U.S. content. In contrast, only about 4% of the value of product shipped from China to the United States is U.S. content. United States policy changes can shift work from Asian countries to the United States and as much as possible of the rest to Canada and Mexico.

The interests of the United States and our key allies are similar: both want to address unfair Chinese trade practices. Working in a collaborative partnership, we could file complaints about unfair practices and develop new rules for areas not covered well by the WTO rules. Together we can be more effective by leveraging our collective strengths. On this theme, on August 16, 2020, the Trump administration announced, “Back to the Americas,” a program to attract manufacturing from Asia to the Americas.

United States and All Allies

11Manufacturing Outlook / September 2022

On August 19, 2019, BRT released a new “Statement on the Purpose of a Corporation signed by 181 CEOs who commit to lead their companies for the benefit of all stakeholders – customers, employees, suppliers, communities and shareholders.” The revised statement diverges from “shareholder primacy” toward an inclusive commitment to all

awarding business based on price tag. Instead, minimize total cost.”

Companies should eliminate silos by integrating planning and development with technology, fostering collaboration from the C-suite to the factory floor.

Deming’ssolutions4thprinciple

FEATURE STORY continued

Initiative is currently partnering with individual compa nies, MEPs in Illinois, Cleveland and Dayton, Ohio, Maryland, New York, and Rhode Island; and with economic development organizations (EDOs) to drive local reshoring. Ask your local MEP or EDO to become partners.

Import Substitution Program (ISP): The ISP was created to convince and facil itate importing companies to source more domestically.

Thestakeholders.Reshoring

deals with sourcing decisions: “End the practice of

The Supply Chain Gaps Program (SCG) was designed to identify and fill U.S. supply chain gaps. The Reshoring Initiative has developed a list of target

12 Manufacturing Outlook / September 2022

Creating partnerships within the com pany by using TCO will help ensure that the needs of all departments are taken into account. Partnerships with other manufacturing technology sup pliers can be beneficial as well. Chal lenge each other to develop solutions to reshoring challenges, and then invest in those

Job shop salespeople are often told by procurement departments “the higher warranty and inventory costs from offshoring are not part of my budget.”

Federal, state and local governments can be good partners too. The federal government allocated billions of dol lars to encourage reshoring. The U.S. International Development Finance Corporation (DFC), created in 2019, is one of the best sources of this funding. DFC partners with the private sector to finance solutions to critical challenges, investing in the energy, healthcare, critical infrastructure, and technology sectors. DFC also provides financing for small businesses and women en trepreneurs to create jobs in emerging Rhodemarkets.Island

principles for management to follow to significantly improve the effectiveness of a business or organization. Dem ing’s ninth key principle recommends collaboration: “Break down barriers be tween departments. People in research, design, sales, and production must work as a team, to foresee problems of pro duction and in use that may be encoun tered with the product or service.”

To make a dent in the reshoring movement, it’s going to take all stakeholders doing their parts not just for themselves but also for the good of the whole. The Business Round table (BRT), a Washington, D.C.based nonprofit recently redefined its statement of purpose to promote “an

economy that serves all Americans.”

is developing an ag gressive reshoring program. The partnership includes the Rhode Island Commerce Corporation working with OEMs, the state Manufacturing Enter prise Partnership (MEP) working with suppliers, the Rhode Island Manufac turers Association (RIMA) engaging with the companies, and the Chafee Center for International Business at Bryant University supporting via data analysis, and the Reshoring Initiative.

AgieCharmilles, starting as President in 1985 and retiring 12/31/10 as Chairman Emeritus. Largely due to the success of the Reshoring Initiative, Harry was inducted into the Industry Week Manufacturing Hall of Fame 2010 and was named Quality Magazine’s 2012 Quality Professional of the year and FAB Shop Magazine Direct’s Manufacturing Person of the year. Harry participated actively in President Obama’s 1/11/12 Insourcing Forum at the White House, won The Economist debate on outsourcing and

Author Profile:Harry founded the Reshoring Initiative to bring manufacturing jobs back to the U.S. after working for high end machine tool supplier GF

is frequently quoted in the Wall Street Journal, NYT, Forbes, Financial Times, New Yorker, Washington Post and USA Today and seen on Fox Business, MarketWatch, PRI, NPR, Manufacturing Talk Radio and other national TV and radio programs. He received a BS in Mechanical Engineering and an MS in Engineering at MIT in 1967 and an MBA from U. of Chicago in 1981. n

offshoring, received the Manufacturing Leadership Council’s Industry Advocacy Award in 2014 and the Made in America 2019 Reshoring Award. He was recognized by Sue Helper, then Commerce Department Chief Economist, as the driving force in founding the reshoring trend and named to the Commerce Department Investment Advisory Council in August

This article first appeared on IMTS. com, the website for IMTS — The In ternational Manufacturing Technology Show, owned and operated by AMT — The Association For Manufacturing Technology.

We want your participation. Now interviewing for additional podcast hosts Now interviewing for regular and contributing writers for Manufacturing Outlook ezine New ideas wanted for monthly Manufacturing Talk Radio topics Contact Jacket Media Co. at 973-808-8300 info@jacketmediaco.comor FEATURE STORY

Harry2019.

13Manufacturing Outlook / September 2022

ed supply chain gaps and product cat egories where there is a large volume of imports but no or minimal domestic Theproduction.Reshoring

Initiative works with companies, economic development or ganizations (EDOs), and Manufactur ing Extension Partnerships (MEPs) to fill the gaps. The free online Total Cost of Ownership Estimator will more ac curately determine the real profit and loss impact of reshoring or offshoring. After doing the math, most companies will decide to bring some work back. For help, contact Harry Moser at har ry.moser@reshorenow.org.

The report encompasses analysis on advanced warehouse technologies, including AI/ML, that can handle the complexity of managing millions of SKUs. It also examined retailers’ need for warehouse platforms to optimize operational, financial, and sustainability performance.

appropriate levels of effort, staffing, and experience. Companies face unnecessary risk, poor decisionmaking, and delays in Time-toValue (TTV). Worst case scenarios have resulted in project failure. It is not all gloom and doom, as there are many very successful WMS

Other considerations such as flow of cross-docking, putaway, wave picking, returns and enabling technologies, included robotics and automation considerations.

Warehouse Management Systems (WMS) projects can be challenging from start to finish Achieving success requires process discipline and focus, and

Aimplementations.WMSsolution requires more than technical expertise to achieve success. Extensive experience in operations and TTV recommendations must be focused on operational efficiency. WMS vendors are honest about the technology as a foundational start, rather than a finished technology outcome. Aligned with Lean Manufacturing, WMS provides better operational and quantifiable outcomes.

By: TR Cutler

14 Manufacturing Outlook / September 2022

Coresight Research published a new Insight Report, “Warehouse Management Platforms: Enhancing the Central Nervous System of the Supply Chain,” which traces the evolution of warehouses from “dusty sheds where goods are stacked in a remote location” to vital connectors of supply and demand.

A deeper dive regarding the position

of the warehouse in the modern, technology-powered supply chain and functional areas of warehouse management platforms was reviewed. Projections regarding the size of the global supply chain management software market through 2027 was also reported.

MANUFACTURING TIDBITS continued

Warehouse Management Systems Space: Achieving Rapid Time-to-Value (TTV)

finished goods, time to value must be both short-term and over time.

Cutler is the President and CEO of Fort Lauderdale, Floridabased, TR Cutler, Inc., celebrating its nearly quarter century in business. Cutler is the founder of the 9000+ Manufacturing Media Consortium which includes more than 9000 journalists, editors, and economists writing about trends in manufacturing, industry, material handling, and process improvement. Cutler has established special divisions including African manufacturing, LATAM/Colombian manufacturing, Gen Z workforce, and Food & Beverage, and Industrial Coaching. Over 5200 industry leaders follow Cutler on Twitter daily at @ThomasRCutler. Contact Cutler at trcutler@trcutlerinc.com n

MANUFACTURING TIDBITS

authors more than 1000 feature articles annually regarding the manufacturing and industrial sectors, with emphasis on robotics, lean manufacturing, technology breakthroughs, and media coverage of the sector.

Author ProfileThomas R. Cutler

Manyintegration.WMS

The laments of warehouse and operations managers are longstanding and well known; there are frequent gaps in supply chain software. Most of these limitations are mentioned in areas of document management, analytics, and robotics

vendors fail to provide solutions and products to fill those gaps and integrate natively with multiple technologies. WMS at “go-live” is just the beginning of a warehouse implementation. Issues from labor limitations may require implementation of Google glasses such as Vision-as-a-Service. Retiring fork truck drivers are replaced with AGVs (automated guided vehicles), yet the WMS integration must be solved before the robots are purchased.

A WMS platform benefits from ongoing investments using bestpractice technology and addressing ToC (Theory of Constraints) through the fast-moving B2B and B2C manufacturing, warehousing, and distribution models. Long-term partnerships are best in these vendor relationships. This is not a quick fix. With thin margins, complex supply chains, and raw material costs of

15Manufacturing Outlook / September 2022

products and services is the lifeblood of standardization and for 75 years, ISO has been at the heart of this process. It is therefore fitting that the vision of ISO for 2030 should be founded on the same tenets.”

The ISO Strategy 2030, like International Standards, will be regularly reviewed and revised ensuring that it remains purposeful and adapts to intentions and actions with the changing environment. The strategy is complemented by two key tools: the implementation plan, which outlines concrete actions and the measurement framework.

ISO is a nonprofit organization that develops and publishes standards of virtually every possible sort, ranging from standards for information technology to fluid dynamics and nuclear energy. Headquartered in Geneva, Switzerland, ISO is composed of 162 members, each one the sole representative for their home country. ISO fills the vital role as a conduit achieving agreement between individual standards developers across the world to further the goal of ISOstandardization.President,Eddy

History and Vision of ISO through 2030

ISO EddyPresidentNjoroge

Njoroge recently commented: “It is my pleasure to share with you the new ISO Strategy 2030, a result of a collaborative effort between our members, partners, and all stakeholders. Inclusiveness and finding common agreement on

ISO (International Organization for Standardization) certification is not new. Many manufacturers endure the rigor of registration because global customers require the certification to conduct business. The rigor is not imagined. ISO certification requires training to implement successfully, and it is expensive to establish quality management systems (QMS). ISO certification, no matter how automated, requires heavy emphasis on documentation and the time to achieve certification is lengthy. ISO certification comes in different “denominations” depending on the industry sector or process being certified. Of late, and unless mandated by customers, the case for ISO certification may not be as compelling as twenty years ago. There is resistance to change due to fear and misperceptions of ISO. Often there is inadequate team support or management sponsorship to dwell on the added costs and resources to implement and maintain ISO.

Poor project management or change management can spoil an ISO certification program due to unrealistic expectations prior to deployment.

The global health crises have demonstrated the universal nature of issues facing humanity and brought new perspective to the ISO work. ISO has an indispensable role to play in supporting coordinated action providing global solutions.

ISO Certification: The Pros, Cons, and Looking Ahead

MANUFACTURING TIDBITS continued

By: TR Cutler

16 Manufacturing Outlook / September 2022

Economy: Trade and Uncertainty

Cutler is the President and CEO of Fort Lauderdale, Floridabased, TR Cutler, Inc., celebrating its nearly quarter century in business. Cutler is the founder of the 9000+ Manufacturing Media Consortium which includes more than 9000 journalists, editors, and economists writing about trends in manufacturing, industry, material handling, and process improvement.

ISO’s role over the next decade.

There is acceleration surrounding profound changes in society, especially digital technologies for remote learning and working. Digital transformation and the need to find new ways of working and delivering solutions are threads that run through the new ISO 2030 strategy. The new plan moving forward is well aligned to the United Nations Global Agenda for 2030 and its 17 Sustainable Development Goals.

are all strongly interlinked and large-scale disruption or crises may affect multiple drivers simultaneously. Change presents both risks and Understandingopportunities.howitoccurs by monitoring these four drivers enables ISO and companies holding ISO certification to anticipate and respond to transformative impacts in a shifting global context.

Society: Changing Expectations and Behavior

The world faces major threats to the environment; failing to adequately address risks such as climate change, biodiversity loss, and pollution are not negotiable. These and other issues cut across national borders and cannot be solved by one individual, company, or government alone. International cooperation is required, with a view of achieving sustainability rather than short-term solutions. Despite the challenges of ISO implementation and continuous process improvement, perhaps the greatest role for International Standards is the shift towards a more sustainable future.

Theseenvironment.drivers

Identifying external drivers of change and evaluating impacts

Drivers of Change

The growth of digital infrastructures and integration of digital technologies are rapidly and significantly changing the way people live and work around the world. Advancements in digital technology boost efficiency and productivity, creating a competitive advantage, and promoting innovation. ISO harnesses the power of digital technologies to improve its own value chain and agility.

Technology: the Impact of Digital

Public and civil society actors want higher levels of transparency and collaboration. There is an expectation that individual rights be upheld. By 2030 or sooner, organizations must be more inclusive, more accountable,

ISO certification companies are invited to sponsor special issues of Manufacturing Outlook and upcoming episodes of the Manufacturing Talk Radio broadcast. To learn more call 973-808-8300.

Cutler has established special divisions including African manufacturing, LATAM/Colombian manufacturing, Gen Z workforce, and Food & Beverage, and Industrial Coaching. Over 5200 industry leaders follow Cutler on Twitter daily at @ ThomasRCutler. Contact Cutler at trcutler@trcutlerinc.com n

ISO’s Future

MANUFACTURING TIDBITS

17Manufacturing Outlook / September 2022

Environment: the Urgency for Sustainability

Author Profile

The evolution of the international trading system and its impacts on the global economy are uncertain. Even as the concepts of globalization and multilateralism are increasingly challenged, the interdependence of global supply chains remains strong and essential. This context makes it difficult for organizations to predict long-term development, as access to global markets for products and services are impacted. Changes resulting from economic and trade uncertainty affect the demand for, and relevance of, International Standards.

and better able to integrate stakeholders in the decision-making processes.

Thomas R. Cutler authors more than 1000 feature articles annually regarding the manufacturing and industrial sectors, with emphasis on robotics, lean manufacturing, technology breakthroughs, and media coverage of the sector.

The four primary drivers of change identified by ISO include the economy, technology, society, and the

US Cutting Tool Orders Totaled $173.2 Million in July 2022, Bringing Year-to-Date Total to 7.7% Over 2021

McLean, Va. (September 8, 2022)

18 Manufacturing Outlook / September 2022

– July 2022 U.S. cutting tool consumption totaled $173.2 million, according to the U.S. Cutting Tool Institute (USCTI) and AMT – The Association For Manufacturing Technology. This total, as reported by companies participating in the Cutting Tool Market Report collaboration, was down 1.5% from June’s $175.9 million and up 6.7%

when compared with the $162.3 million reported for July 2021. With a year-to-date total of $1.2 billion, 2022 is up 7.7% when compared to the same time period in 2021.

of the U.S. market for cutting tools.

MANUFACTURING TIDBITS

continued

Costikyan Jarvis, president of Jarvis Cutting Tools, spoke on demand by saying, “The July 2022 cutting tool results continue to show demand is still well off 2019 levels. 2022 dollar volume is still running about 15% lower than 2019, and when inflation is considered, total unit production is even lower. This data is supported by

These numbers and all data in this report are based on the totals reported by the companies participating in the CTMR program. The totals here represent the majority

MANUFACTURING TIDBITS

19Manufacturing Outlook / September 2022

PatCONTACT:McGibbon, AMT 703.827.5255 | com216.241.7333SusanAMTonline.orgpmcgibbon@Orenga,USCTI|sorenga@thomasamc. n

2022 vehicle sales being around 13 million units versus 17 million units in 2019 and the lower production in commercial aerospace. Expect to see improving cutting tool demand well into 2023. Improvement will be driven with increased aerospace production (Boeing reported that 737 production returned to 31-permonth rates in June) and a reduction in automotive supply chain issues. Another good indicator is North America’s premier manufacturing technology show, IMTS. The show returns this month, and attendee numbers and interest will be a good gauge for future demand.”

US industries at Oxford Economics. “This is in line with the deceleration recently seen in new orders and a moderating pace of activity in key client markets.”

Tool Market Report is available dating back to January 2012. This collaboration of AMT and USCTI is the first step in the two associations working together to promote and support U.S.-based manufacturers of cutting tool technology.

The Cutting Tool Market Report is jointly compiled by AMT and USCTI, two trade associations representing the development, production, and distribution of cutting tool technology and products. It provides a monthly statement on U.S. manufacturers’ consumption of the primary consumable in the manufacturing process – the cutting tool. Analysis of cutting tool consumption is a leading indicator of both upturns and downturns in U.S. manufacturing activity, as it is a true measure of actual production levels.

“The slowdown in shipments seen in the second quarter of 2022 continued into July, although they remain well above last year’s totals,” commented Mark Killion, director of

The graph below includes the 12-month moving average for the durable goods shipments and cutting tool orders. These values are calculated by taking the average of the most recent 12 months and plotting them over time.

Historical data for the Cutting

The shipments component of the Cass Freight Index® rose 3.6% on a y/y basis in August, ahead of the revised 1.9% y/y increase in July and the -0.3% average year-to-date through July. The August reading is the best since the record set in May

continued

The2018.July index is revised to 1.199 from 1.182.

The Cass Expenditures Index was still 20% higher than year-ago levels in August, decelerating from 29% in OnJuly.an SA basis, expenditures rose 2.1% m/m in August, with shipments

The expenditures component of the Cass Freight Index®, which measures the total amount spent on freight, rose 1.9% m/m in August after a 3.0% decline in July, with shipments up 6.6% and rates down

several of the soft August indicators are from the spot market. So, to some extent, the stronger Cass data reflect the ongoing shift from spot to

by CASS INFORMATION SYSTEMS, INC.

Cass Transportation Index Report

20 Manufacturing Outlook / September 2022 CASS INDEX OUTLOOK

The4.4%.July index is revised to 4.527 from 4.499.

Cass Freight Index - Shipments

Freight Expenditures

This CASS INDEX has been posted with the permission of Cass Information Systems, Inc.

On a seasonally adjusted (SA) basis, shipments rose 5.5% m/m in August, and were just 1.2% below the cycle peak level in December 2021. This data set stands above most other August freight indicators, but

Thecontract.improvement may not be sustainable, especially as pressure increases on interest rate sensitive sectors like capital goods and housing, but the summer improvement likely reflects a combination of: successful discounting campaigns by retailers, seasonal inventory building ahead of the holidays, easing supply constraints, particularly in auto production, and reversal of China lockdown effects in June/July.

Even with a summer volume uptick, freight markets are loose heading into peak season, largely due to the significant supply response which gained momentum this year.

During the active hurricane seasons of both 2020 and 2021 (June 1November 30), the ACT Research composite of DAT spot rates, ex-fuel, rose 8% and 4%, respectively, into Labor Day. This year, spot rates fell about 6%, ex-fuel, amid the calmest hurricane season since 2013.

The freight rates embedded in the two components of the Cass Freight Index rose 16% y/y in August, decelerating quickly from the 26% y/y increase in July.

On a m/m basis, the Cass Truckload Linehaul Index fell 1.8%, similar to the declines in June and July. The clarity of the trend change in the past three months is rather stunning: after a 22-month cycle of increases that averaged 1.2% per month, the index fell m/m 1.76%, 1.78%, and 1.83% respectively in June, July, and August.

up 5.5% m/m and rates down 3.2%. We estimate roughly 7pps-8pps of the y/y increase in the expenditures index is currently due to fuel prices alone, and part of the m/m decline in rates was due to lower fuel prices. This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges.

The report provides monthly updates of forecasts for the shipments component of the Cass Freight Index and the Cass Truckload Linehaul Index®, as well as DAT spot rates by trailer type, including and excluding fuel surcharges. n

shippers aren’t seeing any real savings yet, such relief is now highly probable for 2023, which is welcome news for the broader inflation

The Cass Truckload Linehaul Index® rose 7.4 y/y in August to 159.7, after rising 10.5% y/y in July.

Simply following normal seasonality from here, this index is on track for a 24% increase in 2022 and would turn down on a y/y basis next February.

Moreover, the looser market balance we see in U.S. freight markets is consistent with the easing happening in global ocean spot markets, where rates were 56% below year-ago levels in early September. The broader effects of these cost savings for shippers will show up more in 2023, so should gradually become more helpful to the Fed’s fight against inflation and for resolving supply chain issues. One interesting takeaway from the IANA intermodal conference in Long Beach this week is that there’s still a whole lot of inefficient freight jamming warehouses and slowing rail service.

Freight Expectations

But there’s much more at work in the freight economy than the weather. The hurricane effect is considerable, and the season isn’t over, but we think the divergence between this year’s early September rate trend with the past two is mainly due to the looser market balance. The shipment rebound is, so far, not enough to outweigh the 4%-5% growth rates in the driver and Class 8 tractor populations presently. The story concludes in ACT Research’s monthly Freight Forecast.

Whilecome.

Now that the pendulum is swinging, some crucial questions about the freight rate cycle have been raised: How bad? How long? And when will it turn? The ACT Research Freight Forecast report provides monthly, quarterly, and annual predictions for the truckload (TL), less-thantruckload (LTL), and intermodal markets through 2024, including capacity, volumes, and rates.

excludes fuel and accessorial charges, so when factoring in sequential declines in fuel surcharges, which should continue near term, the deceleration in freight costs is accelerating.

Freight Rates are a simple calculation of the Cass Freight Index data, expenditures divided by shipments, producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload representing more than half of the dollars, followed by LTL, rail, parcel, and so on.

Inferred Freight Rates

With the tight supply/demand balance in U.S. trucking markets easing considerably this year, industry rates are topping out and set to slow sharply in the months to

Casspicture.Inferred

Cass Inferred Freight Rates fell 4.4% m/m (-3.2% SA) in August. Lower fuel prices were a factor in the decline, but with looser truckload market conditions, further deceleration is very likely.

21Manufacturing Outlook / September 2022 CASS INDEX OUTLOOK

Truckload Linehaul Index

We’ve consistently previewed this trend change, so it shouldn’t be a surprise, but the stunning part is the consistency in the three consecutive 1.8% declines—enough to make us look out to the hundredths of a

Thispercent.index

Similar to what has occurred in the spot market, the surge in fuel costs to shippers, which are excluded from this index, will also likely act as a brake on linehaul rates.

22 Manufacturing Outlook / September 2022 THE INSTITUTE FOR SUPPLY MANUFACTURINGMANAGEMENT’SREPORT ON BUSINESS®BREAKINGNEWS ISM PMI at 52.8% for August 2022 ISM REPORT OUTLOOK AUGUST52.8%2022 Released September 1st ISM PMI for the past 5 years Expanding Contracting continued

Of the six biggest manufacturing industries, five — Petroleum & Coal Products; Transportation Equipment; Computer & Electronic Products; Machinery; and Food, Beverage & Tobacco Products — registered moderate-to-strong growth in August. A reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally contracting.

Manufacturing

*Number of months moving in current direction. ISM® Report On Business® data has been seasonally adjusted for the New Orders, Production, Employment and Inventories indexes.

Backlog of Orders 53.0 51.3 +1.7 Growing Faster 26

full report, visit

Production 50.4 53.5 -3.1 Growing Slower 27

The August Manufacturing PMI® registered 52.8 percent. The New Orders Index registered 51.3 percent, 3.3 percentage points higher than the 48 percent recorded in July. After three straight months of contraction, the Employment Index expanded at 54.2 percent. The U.S. manufacturing sector continues expanding at rates simi lar to the prior two months. New order rates returned to expansion levels, supplier deliveries remain at appropriate tension levels and prices softened again, reflecting movement toward supply/demand balance.

Supplier Deliveries 55.1 55.2 -0.1 Slowing Slower 78

PMI 48.7% = BreakevenEconomyOverallLine 50% = LineEconomyManufacturingBreakeven 202220212020 52.8%

Prices 52.5 60.0 -7.5 Increasing Slower 27

Inventories 53.1 57.3 -4.2 Growing Slower 13

‡Miscellaneous Manufacturing (products such as medical equipment and supplies, jewelry, sporting goods, toys and office supplies).

® Report On Business® website at

MANUFACTURING

MANAGEMENT®

New Orders 51.3 48.0 +3.3 Growing From Contracting 1

Commodities Up in Price: Caustic Soda (6); Corrugate (7); Electrical Components (21); Electronic Components (21); Freight (22); Hydraulic Components; Natural Gas (14); Paper; Plastic Resins* (8); Rubber Based Products (13); Steel Products* (24); and Styrene Based Plastics. Commodities Down in Price: Aluminum (4); Copper (2); Corn Products; Crude Oil; Freight; Gasoline; Plastic Resins* (3); Polypropylene; Steel (4); Steel — Carbon (2); Steel — Hot Rolled (4); Steel — Scrap; Steel — Stainless; and Steel Products* (2).

Overall Economy Growing Same 27 Manufacturing Sector Growing Same 27

23Manufacturing Outlook / September 2022 ISM REPORT OUTLOOK continued 12 ISM WORLD.ORG

Employment 54.2 49.9 +4.3 Growing From Contracting 1

Imports 52.5 54.4 -1.9 Growing Slower 3

The U.S. manufacturing sector grew in August, as the Manufacturing PMI® registered 52.8 percent, the same reading recorded in July. The Manufacturing PMI® continued to indicate sector expansion and U.S. economic growth in August. All five subindexes that directly factor into the Manufacturing PMI® (New Orders, Production, Employment, Supplier Deliveries and Inventories) were in growth territory.

The number of consecutive months the commodity has been listed is indicated after each item. *Reported as both up and down in price.

PMI® at 52.8%

Commodities Reported

INSTITUTE FOR SUPPLY reportonbusiness

Ten manufacturing industries reported growth in August, in the following order: Nonmetallic Mineral Products; Petroleum & Coal Prod ucts; Transportation Equipment; Computer & Electronic Products; Printing & Related Support Activities; Plastics & Rubber Products; Primary Metals; Machinery; Miscellaneous Manufacturing‡; and Food, Beverage & Tobacco Products. ISM

New Export Orders 49.4 52.6 -3.2 Contracting From Growing 1

INDEX IndexAug IndexJul %ChangePoint Direction Rate Changeof Trend* (months)

Customers’ Inventories 38.9 39.5 -0.6 Too Low Faster 71

Analysis by Timothy R. Fiore, CPSM, C.P.M. Chair of the Institute for Supply Management® Manufacturing Business Survey Committee

Note: To view the the ISM ismrob.org

Manufacturing PMI® 52.8 52.8 0.0 Growing Same 27

Economic activity in the manufactur ing sector grew in August, with the overall economy achieving a 27th consecutive month of growth, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®

Manufacturing at a Glance

Analysis

Employment (Manufacturing) 50.5% = B.L.S. Mfg. BreakevenEmploymentLine 202220212020 54.2% 20 Supplier Deliveries (Manufacturing) 2022 80 20212020 55.1%53.1% Inventories (Manufacturing) 44.4% = B.E.A. Overall Mfg. Inventories Breakeven Line 202220212020 53.1% Production (Manufacturing) 52.4% = Federal Reserve Board Industrial Production Breakeven Line 202220212020 50.4% 70

Manufacturing PMI®

ISM® Report On Business®

Supplier Deliveries

Inventories

The Production Index registered 50.4 percent. The six industries reporting growth in production during the month of August — in the following order — are: Nonmetallic Mineral Products; Electrical Equipment, Appliances & Components; Petroleum & Coal Products; Transportation Equipment; Machinery; and Plastics & Rubber Products.

The Inventories Index registered 53.1 percent. Of 18 manufacturing industries, the eight reporting higher inventories in August — in the following order — are: Petroleum & Coal Products; Miscellaneous Manufacturing‡; Machinery; Plastics & Rubber Products; Food, Beverage & Tobacco Products; Computer & Electronic Products; Electrical Equipment, Appliances & Components; and Chemical Products.

by Timothy R. Fiore, CPSM, C.P.M. , Chair of the Institute for Supply Management ® Manufacturing Business Survey Committee New Orders (Manufacturing) 52.9% = Census Bureau Mfg. Breakeven Line 2022 20 20212020 51.3%

ISM’s Employment Index registered 54.2 percent. Of 18 manufacturing industries, nine reported employment growth in August, in the following order: Printing & Related Support Activities; Nonmetallic Mineral Products; Petroleum & Coal Products; Transportation Equipment; Furniture & Related Products; Electrical Equipment, Appliances & Components; Plastics & Rubber Products; Machinery; and Fabricated Metal Products.

Employment

ISM’s New Orders Index increased to 51.3 percent. Of the 18 manufacturing indus tries, six reported growth in new orders in August, in the following order: Textile Mills; Computer & Electronic Products; Nonmetallic Mineral Products; Transportation Equipment; Primary Metals; and Plastics & Rubber Products. Production

The delivery performance of suppliers to manufacturing organizations was slower in August, as the Supplier Deliveries Index registered 55.1 percent. Nine manufacturing industries reported slower supplier deliveries in August, in the following order: Nonmetallic Mineral Products; Primary Metals; Computer & Electronic Products; Miscellaneous Manufacturing‡; Paper Products; Food, Beverage & Tobacco Products; Chemical Products; Transportation Equipment; and Fabricated Metal Products.

New Orders

24 Manufacturing Outlook / September 2022

‡Miscellaneous Manufacturing (products such as medical equipment and supplies, jewelry, sporting goods, toys and office supplies). August 2022 ISM REPORT OUTLOOK continued

2022

New Export Orders

Manufacturing PMI®

202220212020 38.9%

2020 53%

Analysis

52.6% = B.L.S. Producer Prices Index for Intermediate Materials Breakeven Line 202220212020 52.5%

202220212020 52.5%

Customer Inventories (Manufacturing)

Customers’ Inventories

Imports (Manufacturing)

by Timothy R. Fiore, CPSM, C.P.M. , Chair of the Institute for Supply Management ® Manufacturing Business Survey Committee

ISM’s Customers’ Inventories Index registered 38.9 percent. Three industries (Apparel, Leather & Allied Products; Furniture & Related Products; and Wood Products) reported customers’ inventories as too high in August.

New Export Orders (Manufacturing) 2021

25Manufacturing Outlook / September 2022

Backlog of Orders

ISM’s Backlog of Orders Index registered 53 percent. Seven industries reported growth in order backlogs in August, in the following order: Nonmetallic Mineral Products; Printing & Related Support Activities; Transportation Equipment; Plastics & Rubber Products; Machinery; Computer & Electronic Products; and Miscellaneous Manufacturing‡

2022

ISM’s Imports Index registered 52.5 percent. The eight industries reporting growth in imports in August — in the following order — are: Textile Mills; Electrical Equipment, Appliances & Components; Food, Beverage & Tobacco Products; Transportation Equipment; Chemical Products; Machinery; Plastics & Rubber Products; and Miscellaneous Manufacturing‡

Backlog of Orders (Manufacturing) 2021

Prices (Manufacturing)

ISM® Report On Business®

Imports

Prices

The ISM Prices Index registered 52.5 percent. In August, eight of 18 industries reported paying increased prices for raw materials, in the following order: Printing & Related Support Activities; Computer & Electronic Products; Miscellaneous Manufacturing‡; Furniture & Related Products; Paper Products; Machinery; Chemical Products; and Electrical Equipment, Appliances & Components.

‡Miscellaneous Manufacturing (products such as medical equipment and supplies, jewelry, sporting goods, toys and office supplies). August 2022 ISM REPORT OUTLOOK n

2020 49.4%

ISM’s New Export Orders Index registered 49.4 percent. Three industries reported growth in new export orders in August: Plastics & Rubber Products; Computer & Electronic Products; and Food, Beverage & Tobacco Products.

Tom’s passion was his Industrial Journalist Career writing about manufacturing and business. That passion took him to Africa, a continent with emerging into modern manufacturing. As he travelled, he saw some extreme poverty. His humanitarianism lead him to adopt one or more starving villages, providing them with food and other resources. The village elders in one such village that was experiencing the death of a child nearly every day from starvation reported to Tom that the village hadn’t lost a single child since Tom’s adoptive philanthropy.

My friend, Tom Cutler, returned from one of his many trips to Africa, a continent filled with people he loved. On August 30th, feeling unwell, Tom went to a hospital ER in Florida. Tragically, he suffered a fatal heart attack.

Thomas Russell Cutler: Industrial Journalist – In Memoriam

I knew Tom for three years. He was brilliant, professional, efficient, kind, funny, and a friend. He was a great help to me in my professional pursuits, and I will miss him immeasurably.

26 Manufacturing Outlook / September 2022

Tom Cutler was named the number one Industrial Journalist for 24 years in a row. He wrote nearly 1,000 industrial, manufacturing, and B2B articles annually. No easy task! He was the CEO of TR Cutler Inc., where he founded and built the membership of the Manufacturing Media Consortium to over 9,000 journalists, editors, economists, and other industrial leaders worldwide.

Lewis (Lew) A. Weiss

IN MEMORIAM - THOMAS R. CUTLER

President, All Metals & Forge Group Founder, Manufacturing Talk Radio Publisher, Manufacturing Outlook ezine President, Jacket Media Co.

*Toll free within the *U.S. ISO9001:2015 SINCE 1994 AND AS9100D SINCE 1998 NIST SP 800-171 (COMPLIANCE UNDER DEVELOPMENT)

No longer is content consumed as a form of education, professional development, or comparative analysis. Solution-seekers perform a Google Search, and find matches based on the algorithms of search engine optimized rankings. There is no triangulation. Top-ten rankings constitute information gathering, but little else. Out of sight, out of mind.

Many keep running content that could have been authored twenty years ago. No contemporaneous insights, contexts, or prognostications are offered. Just more of the same.

Thomas R. Cutler, who founded the 9000+ member Manufacturing Media Consortium in 1999 and has authored more than 8000 articles in that time span; he has been working with Jacket Media Co for some time as a regular contributor to our most popular publication Manufacturing Outlook. Cutler brainstormed with Lew Weiss and contributed to the report which follows. Tom has seen all the media shifts, the transition to a wide variety of content, webinars, YouTubes, and yes, TikTok.

by Lew Weiss In Collaboration With TR Cutler

phone. The attention span for content assimilation is measured in seconds at worst; minutes at best.

This is neither good nor bad; it is. In this vast media paradigmatic shift, survivors of the media miasma live by the maxim: eat or be eaten. Many in the media have failed to look ahead.

28 Manufacturing Outlook / September 2022 COVER StateSTORY of Industrial Media: 2022 and Beyond

I’m so old I remember Yellow Pages and Rolodexes. I’m so old that a directory was a published book with a spine. The landscape of the industrial media has changed so much over the past 50 years; it is time to reflect on where we were, where we are, and most importantly, where we are going.

With daily newspapers and many monthly B2B publications gone, the frequency and velocity of industrial news, economic information, vendor specifications, and site selection have caused tectonic shifts. These earth-shaking changes leave a media landscape without full case studies, probative thoughtful investigative journalism, and have been replaced with a ‘swipe up’ on the ubiquitous cell

continued

(VC) funded companies are a prime user of the current industrial media complex. Whether affiliated with artificial intelligence (AI), machine learning (ML), or Industrial Internet of Things (IIoT), these companies must clearly capture mindshare and market share among an interested audience. Industry 4.0 is another example where aligning company objectives with the best-practice technology becomes an effective use of media outlets. The influx of VC money in industries, particularly those impacting manufacturing, material handling, and fulfillment, have garnered several billions of dollars in the past two years. Suddenly, these new companies appear at countless tradeshows, yet too often fail to leverage those lead generation events with credible editorial content. VC-funded manufacturing organizations will spend upwards of $1M on each tradeshow; the ratio of media coverage must average 12-30%

learned, and the role of the newly merged organization adds texture for customers and potentially future acquisition targets. A media spend for a year following a merger or acquisition is critical to ensure that the market sees it was a sound business decision with a deeper explanation versus a cursory press announcement.

Beyond predictive analysis and analytics, media is more than editorial opining. In fact, the questions to examine are who wants media coverage and why? Profit-based media outlets including Jacket Media Co must balance the editorial trendspotting with those of paid sponsors, content contributors, and podcast

Newhosts/guests.venture-capital

Similarly,spend.

29Manufacturing Outlook / September 2022 continued COVER STORY

Bpipeline.andC-level

Anyone hired into a C-Suite position must make a name for themself. They become part of an industrial leadership that is synonymous with the company brand and messaging. They have both a professional and personal vested interest in being known, respected, and part of the value-added proposition of the organization. They achieve this by becoming authors of thoughtleadership feature articles, guests on podcasts, as well as keynote speakers and panelists at conferences and tradeshows. Thought leadership is fairly new nomenclature yet the industrial complex is more than the technology offered, more than the products manufactured…it is the people, the vision, the mission that must be articulated with velocity, volume, and consistency. Obstacles for accomplishing this are detailed below in this exposé.

This is where expertise in content creation, succinct and precise communication, and dynamic storytelling become a paramount function whether handled internally or externally by a PR firm.

The function of marketing has changed. It used to be building brand and product awareness and acquiring lead generation, particularly through digital and traditional methodologies. The marketing role is far more engaged in the B2B industrial complex

Even if a PR firm is engaged, 90% of these firms have no prior relationships with members of the Manufacturing Media Consortium and are therefore pitching (cold calling). Cutler reports that 100% of editorial pitches (phone or email) are summarily discarded or sent to a spam folder when sent from an unknown source. In fact, some pitch emails get sent to advertising or sponsorship departments to sell revenue generating space. Without the prior relationships and without successful demonstration of content creation by a PR firm, it is a waste of time and money. Anyone can pitch a story, few know the culture of the publications, the readers, and the editors’ expectations.

responsible for bottom-line growth and an integral part of the ‘sales AND marketing’ effort. Salespeople are rarely accountable for following up with prospects except via LinkedIn or those about to issue a purchase order in 90 days. They are bonused and rewarded on closed activities, not advancing the longer-term sales

prospects are relegated to marketing management, whether via e-blasts of newsletters, public relations, social media outreach with constant messaging, and SEO (search engine optimization). Marketing is part of the sales effort. In many small and midsized manufacturing operations, a single marketing person is attempting to handle too much from conferences, tradeshows, print advertising, product messaging, promoting C-level executives, and content creation. Add to that mix, PR (public relations). Any one of those functions could be a full-time effort; doing all of them with mediocrity speaks to the high attrition rate of these professionals.

Balancing Media Coverage: Forward Thinking and Providing a Microphone

companies in mergers and acquisitions (M&A) have a relevant story to tell yet too often do little other than a single press release announcing the new entity. Much is lost when the rationale for the M & A is given short shrift. A great public spokesperson must be a guest on a myriad of podcasts, offer guest columns in a variety of industrial publications, and offer updates about the impact of the acquisition for customers. It is too important to view these events as transactional. The rationale for acquisition, the lessons

are able to convert companies’ thought leadership into publishable content. All the great content, YouTubes, podcasts, and publications that are not seen do little to advance the cause of manufacturers looking to create definitive value propositions and clear differentiation from competitors.

30 Manufacturing Outlook / September 2022

The current state of manufacturers’ marketing efforts is a hodge-podge of activities and actions. They are not a strategic campaign. Since time is the constant constraint much of that can be sourced to effective, savvy, and experience content creators in the industrial sectors. These are not PR folks who will take on any client and offer vanilla services. These are journalists and industry experts who

The Future State of Industrial Media

Velocity is understood by operations managers as the rapidity of motion such as the time rate of change or position of a body in a specified direction. Velocity is the rate of speed with which something occurs. Applying that concept to media messaging, the rapidity of action and reaction can (and must be) quantified. Whether Google search results, analytics, lead generation, frequency of inquiry, and of course, conversion to sale, these are metrics which are Theseanalyzable.arenot

IIoT Big Data, nor do they require extensive business intelligence algorithms. Running Google analytics will quickly inform senior industrial managers what is working. Likewise, if the sales

And still these best-practice operations are failing to tell their stories. They are failing to profile their leaders, and they are failing to use the new media methodologies that all GenZers have grown up with and utilize for hours a day. This failure to connect with the new generation of communication, portends a dismal outlook without immediate corrective action.

The Media Kit is Dead (or should be) Every fall until COVID, magazines, news publications, conferences, and more media outreach vehicles had a media kit which included a media calendar. No more. Sure, there are a few anachronistic examples which still prevail that look like rehashed versions of a 2010 editorial calendar. The fluidity of world events makes the media kit obsolete.

COVER STORY: STATE OF INDUSTRIAL MEDIA continued

Two years ago, few spoke about supply chain disruption, the Russian attack on Ukraine, oil prices, inflation, ‘the great resignation,’ cybersecurity challenges, and high-level robotics to solve workforce challenges. Now those topics are omnipresent. Any media calendar that was prepared in Fall of 2021 would have missed all these topics.

Anearshoring).growingnumber of manufacturers are thriving in this challenging environment. They are adopting smart manufacturing techniques, working with the needs of the supply chain, attracting and retaining a quality workforce, and making business processes faster.

Rationale for Media Outreach Integrated Campaigns for the Industrial Sector

The future state in a value stream map MUST consist of velocity, volume, and consistency. So many industrial firms have social media accounts that are barely used. DMs (direct messages) are not answered with alacrity. Following and followers are not vetted, scrubbed, and added to with regularity. Prospects on the CRM are not included in social media activity. Potential customers’ content must be retweeted. Salespeople must follow target customers on LinkedIn.

All editorial content has multiple purposes for the readers, the publishers, and the companies (paying sponsors). Ultimately, most want to know how manufacturers can succeed now and improve moving forward. To state the obvious, potential disruptions to industrial business operations keep growing every day. There is (and will continue to be) a shortage of skilled workers. Risks are rising and difficult to mitigate. Supply chain disruptions are coming from all locations (promulgating the conversation of

Thecampaign.integrated

campaign is more than a check list of “to-do” activities on Google calendars by all involved. Too much focus is placed in the day-to-day and too little focus on the notion of a campaign. Mapping a calendarized plan is essential. The combination of advertising, podcasts, webinars, tradeshows, industry events, feature article editorials, press releases, direct mail campaigns, and social media represent a cumulative effort which drive on-going branding, messaging, awareness, and lead generation. All of these campaign elements drive the Google search results, which as referenced earlier, are paramount.

The most significant factor in limiting the media messaging in the industrial sector is time. Great thought leaders, experienced marketing managers, and digital social media mavens, have too much on their plate and regularly drop the ball on one or more important functions of an integrated marketing

Author profile: Lew Weiss, founder of Jacket Media Co, host of Manufacturing Talk Radio and publisher of Manufacturing Outlook. n

The Answer is on the Phone

Currently, prospects in the industrial sector respond when there is a problem. Prospects proactively seek

31Manufacturing Outlook / September 2022

self-explanatory; it is not. The frequent lament among sponsors and advertisers is that the marketing-spend did not convert to sufficient inquiries or new sales. This goes back to the utilization of media content. Back in the ‘olden days’ (pre-2000) verified subscribers was the gold standard. Nowadays few read content consistently, rather they search by topic (not only by Google, but also by Twitter searches). The volume is measured by the push of content, not pull. In the past, there was an assumption that a feature article in a marquis publication such as IndustryWeek, would axiomatically drive so many eyeballs to content and convert to a percentage of inquiries.

While so much has changed for those of us 55 and older, the utilization of media by Millennials, GenZers, and now Generation Alpha has been on their cell phones for most of their lives. They have never heard of CDs, 8 tracks, or albums. They consume media at a volume, velocity, and consistency unimagined previously. They swipe up with a ferocity capturing bits of knowledge. We know the fate of the dinosaurs. Dynamic, agile, and creative media remains exciting and fun for those of us committed to communicating and reporting the trends in the industrial complex.

pipeline increases ten-fold and conversion to sales lags behind, the constraint can be quickly identified and Volumecorrected.mayseem

solutions using search engines. They may need to watch a YouTube video, then listen to a podcast, then see a topic such as robotic automation in a myriad of media outlets before taking the next step. Volume means that the problem a manufacturer has is solved when found (experienced: watched, heard, read, some element of Consistencyengagement).is

the company’s stability. The division of labor (in house or by a third-party agency) to accomplish consistent message is vital.

COVER STORY: STATE OF INDUSTRIAL MEDIA

the single most important variable in the industrial media market now and for the foreseeable future. One cannot be in an airport and fail to retweet. One cannot issue one press release a month; Cutler’s motto is that if a manufacturing enterprise is open for business today, they have something to say today. Periodic efforts, such as announcing a new product, service, or new hire, produces futile and half-hearted results. Such haphazard sporadic communication efforts are actually deleterious. They provoke the customers to ask why nothing new has been presented and question