INDUSTRY DEVELOPMENT AND TECH EDITION CLAYTON UNVEILS NET-ZERO HOME FANNIE MAE AND FREDDIE MAC DUTY TO SERVE PLANS ONE HISTORIC NIGHT AT THE HALL THE MAGAZINE FOR MANUFACTURED HOUSING PROFESSIONALS JULY / AUGUST 2022 | MHINSIDER.COM

REDEFINING VALUE FOR THE MH/RV ASSET CLASS BROKERAGE & ADVISORY SERVICES CLIENT FOCUSED DRIVEN PROVEN RESULTS MANUFACTURED HOUSING GROUP Christopher Nortley President | CEO (586) 884-8416 chris@mhreinc.com Detroit HQ Location 12900 Hall Road, Suite 190 Sterling Heights, MI 48313 Tampa Location PO Box 4174 Tampa, FL 33677 www.mhreinc.com Amanda LaConte Senior Financial Analyst (407) 670-0552 amanda@mhreinc.com SERVICES OFFERED IN US & CANADA Institutional Investment Sales Acquisitions & Dispositions Distressed Assets Bank REO & Special Servicer Debt & Equity Valuation & Advisory Services Michel Mikkola Senior Advisor (407) 640-7046 michel@mhreinc.com Colleen Lannoo Broker Associate | Director of Data Research (586) 580-7322 colleen@mhreinc.com Melissa Wade Senior Transaction Manger (586) 884-8415 melissa@mhreinc.com

BUILD

MANUFACTURED & MODULAR HOMES ■ championhomes.com ■ skylinehomes.com ■ genesishomes.com PARK MODEL RVS ■ athenspark.com ■ shoreparkrvs.com ACCESSORY DWELLING UNITS (ADUS) ■ genesishomes.com EXPLORE OUR BRANDS AND DESIGNS AT THESE WEBSITES

WITH A PROVEN LEADER Strong national manufacturing footprint Vast array of home designs for builders, communities, and retailers Complete line of homes for MH Advantage® and CHOICEHome® programs Leading builder of Park Model RVs Innovative builder of Accessory Dwelling Units (ADUs)

CLAYTON UNVEILS NET-ZERO HOME

Homes unveiled its first net-zero electricity home to the public at the 2022 Berkshire Hathaway Shareholders meeting in Omaha, Neb., in May.

2 | JULY / AUGUST 2022 EDITION HAPPENINGS 6 Industry Happenings EVENTS 10 Manufactured Housing Industry Events 11 National Showcase Draws Eyes to Manufactured Housing Industry 14 SECO22 Marks Return to In-Person Event for Community Owners INDUSTRY NEWS 22 Fannie Mae and Freddie Mac Duty To Serve Plans 27 How Rising Interest Rates Erode Value COMMUNITY 30 Inspire Communities Expands in Texas 33 Sun Communities Releases Environmental, Social and Governance Report 36 Rent Butter Goes Well Beyond Credit Score CONTENTS

Clayton

PAGE 54

The RV/MH Hall of Fame in Elkhart, Ind., is celebrating multiple historic achievements in August, inducting 10 new honorees in its 50th year, as well as unveiling the much-an ticipated Manufactured Housing Museum.

MHINSIDER.COM | 3 SERVICE / SUPPLY 39 MortgageFlex Focuses on Ease, Speed 44 Plena Deploys Bots to Efficiently Perform Everyday Tasks 48 New Tech to Support Insurance Offerings BUILDER/RETAILER 53 HUD Proposes Another Round of Significant Changes for Manufactured Homes 58 Growth of the ADU 60 Impact Housing Provides Modular Homes for Storm Victims FINANCE 62 Yesterday Once More Part II 71 Regulatory Environment, Stages Of Development, And New Technology 74 INDUSTRY JOB OPPORTUNITIES THE ALLEN LEGACY 78 One Big Auction! Notable Events, Individuals In Manufactured Housing

PAGE 16

FROM THE

publisher

Prolific Development in the Manufactured Housing Industry Insight on Industry Development, Advances in Technology

TThe awe-inspiring sight of our industry’s homes on the National Mall in June once again served as a poignant reminder of just how much progress has been made, and how much change manufactured housing professionals can affect in a relatively short period of time.

Local governments nationwide are coming to realize the need for fair treatment of factory-built homes. In Florida, the state association partnered and worked tirelessly to earn a 50 percent tax break on new manufactured homes, a measure that helps builders and operators keep homes affordable and flowing to the market for eager homebuyers.

Just in the last few years, manufactured homes and manufactured home communities have become an increasingly viable option for new buyers, including Millennials. Meanwhile, growth among builders has come via strategic investment, large acquisition, and thoughtful partnerships.

Brokers and lenders, as well as many other service providers, in recent years have examined and re-imagined how they deliver value, implementing new products and enhanced tech platforms.

Back in Washington, many policymakers, administration officials, and lawmakers are coming to truly see the need for added affordable housing, and a near consensus is forming that the answer is manufactured and modular homes.

There is a continued need for advocacy on many fronts, of course, and there always will be. But it should be lost on no one that the manufactured housing industry measured in home shipments has nearly doubled its productivity in 10 years.

And more so, the wide range of public and private stakeholders are coming to learn why.

Patrick Revere is associate vice president of MHVillage and publisher for the MHInsider magazine and blog for industry professionals. His background is in print news, language, and communication.

VOLUME 5 • EDITION 4 JULY / AUGUST 2022 MHInsider.com

Publisher Patrick Revere patrick@mhvillage.com

Senior Graphic Designer

Merit Kathan merit@mhvillage.com

Contributing Editor

George Allen gfa7156@aol.com

Editor

Sean Vichinsky sean@mhvillage.com

Contributors

Nick Bertino

Erik Edwards

Kevan Enger Mitch Gonzalez Matt Herskowitz Raymond Leech Tony Petosa Adarsh Rachmale

Advertising Sales (877) 406-0232 advertise@mhvillage.com

Editorial & General Inquiries

Patrick Revere

2600 Five Mile Road NE Grand Rapids, MI, 49525 (616) 888-6994 patrick@mhvillage.com

Disclaimer

Although we make every effort to ensure that the information in this issue was correct before publication, MHVillage, Inc. and the publisher do not assume and hereby disclaim any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause. Opinions expressed are those of the author or persons quoted and not necessarily those of MHInsider or the publisher MHVillage, Inc.

Copyright Notice

Copyright ©2022 MHVillage, Inc. All rights reserved. Reproduction of MHInsider content, MHI or other contributor content, in part or in whole, is prohibited without written authorization from MHVillage, Inc.

MHInsider™ is published by:

2600 Five Mile Road NE Grand Rapids, MI 49525 (800) 397 2158 www.MHVillage.com

Joshua Mermell Senior VP of Acquisitions Email jmermell@rhp.com Cell 248.508.7637 Office/Direct 248.538.3312 rhp.com the american dream • Highest Price Paid for Your MHC • Smooth, Quick Closing • Free Property Evaluation • 100% Confidential Brokers Protected

Industry

HAPPENINGS

Transactions

Crown Communities Buys Ohio Property

Westview Estates in Sandusky, Ohio, has been ac quired by Crown Communities and will be managed by Kodiak Property Management. "This is another great acquisition for Crown Communities and our eighth acquisition in 12 months," Alex Cabot, of Crown Communities, said. "Westview is one of the highest quality manufactured housing communi ties in Northwest Ohio and represents the type of property Crown Communities seeks to acquire and operate in the future."

RHP Properties Purchases Illinois, Delaware Communities

Farmington Hills, Mich-based RHP Properties has acquired Valley View Estates in Shiloh, Ill., as well as three communities in Delaware, expanding the company’s portfolio to 15 communities in Illinois and 311 nationwide. Valley View Estates is on 57 acres and features more than 230 homes near local schools and large employers. The acquisition in Delaware consists of Colonial East, an all-ages community, and Sussex

East and Sussex West, a pair of 55+ communities. All of the properties are located in Rehoboth. RHP has seven communities in Delaware.

Yale Brokers Two Large Deals in Hot Market

Yale Realty & Capital Advisors in the second quarter topped its best single sale in the St. Louis market with a $17.5 million closing, registering $75,300 per pad in the 200-plus homesite, 95% occupied community. Upper Midwest Regional Director Ken Schefler credits his record-breaking close to the buyer's longstanding relationship with Yale. In Florida, Yale National Di rector of Brokerage James Cook closed a $19 million, 175-homesite, senior community with spacious lots, abundant amenities, and below-market rents.

California Community Added to Hometown America Portfolio

Hometown America has agreed to purchase Mary Manor Estates, a manufactured home community in Sunnyvale, Calif. The 116-site community is fully occupied, and sits about 12 miles from San Jose, and 40 miles south of San Francisco. Built in

6 | JULY / AUGUST 2022 EDITION

Happenings

1974, the Mary Manor Estates has a pool, clubhouse, and car washing station.

UMH Purchases Pennsylvania Community for $5.8 Million

UMH Properties has acquired a manufactured home community in Monaca, Pa. for $5.8 million. The community has 96 developed homesites and is situated on about 18 acres. “We are happy to announce the acquisition of this well-located community,” UMH President and CEO Sam Landy said. “This community is located near some of our communities that are at or near full occupancy and it complements our existing portfolio. Landy said UMH will upgrade the commu nity to increase revenue and community value. He said the company continues to seek opportunistic acquisitions that meet their growth criteria. UMH Properties owns and operates 128 manufactured home communities with more than 24,100 homesites in New Jersey, New York, Ohio, Pennsylvania, Ten nessee, Indiana, Maryland, Michigan, Alabama, and South Carolina, and has one co-owned community in Florida. UMH also recently opened a pair of new

home retail locations, one in Carmel, Ind., and another in Catskill, N.Y.

Industry Giving

Community Owner Provides Support, Funding for Fifth School

RHP Properties, the nation's largest private owner and operator of manufactured home communities, is providing a $10,000 donation to support Mountain »

MHINSIDER.COM | 7

View High School in El Monte, Calif. The donation is in partnership with AdoptAClassroom.org. The funding is for pre-Kindergarten through 12th grade schools and teachers in the U.S. to purchase materials and tools for their students to learn and succeed. This is the fifth school RHP Properties has adopted through the program, with a total of $50,000 in donations. Mountain View has about 1,340 students in ninth through 12th grade, including about 200 students who reside in nearby Brookside Country Club, an RHP Properties community.

Personnel Washington Association Hires New Director

The Northwest Housing Association, which represents manufactured home retailers and builders in Washington, has hired Lance Clark as executive director of the organization.

Clark brings about 20 years of association management and building industry experience to the role left vacant by the recently retired longtime Executive Director Joan Brown. “I am excited to serve as NHA’s executive and sup port members during a time of dynamic growth in manufactured home sales,” Clark said.

In Memoriam

Texas MH Professionals Mourn Passing of Industry Leader

Norman Pate, 78, of Woodway, Texas, passed away in March. Mr. Pate came to Texas from Alabama in 1973 to work with Winston Indus tries and Crimson Homes. He and his wife Susie worked at Brigadier Manufactured Plant and started Brigadier Homes of Waco. Mr. Pate loved being a small business owner, and developed many friendships from his associations in the industry; his employees, and clients. His passion was providing quality manufac tured housing to the community and developing his business. A visitation was held in early April at Grace Gardens Funeral Home Chapel. He is survived by his wife, children Lane and Ashley, sister-in-law Lola

Murphy Pate, nieces Vicki and Rhonda, nephews Scott, Chris, Ray, and Dave, as well as countless cousins and other family and friends. Memorial contributions may be made to the Alzheimer’s Association.

Michigan Community Owner, Advocate Passes Away

Joseph Adlore Chaudier, who built L’Anse Mobile Home Park in Michigan, died in March from brain cancer. He had been in the United States Air Force, and worked as a draftsman for Ford Motor Company before returning to his hometown. He served on the Michigan Manufactured Housing Commission. Mr. Chaudier is survived by his wife Doris, three daughters, eight grandchildren, and three brothers. He was preceded in death by his parents John and Gladys Chaudier and six siblings.

Wisconsin Retailer, Advocate Laid to Rest Eugene “Gene” Victor Remy, 84, of Remy’s Homes, passed away in April. Mr Remy was an entrepreneur from an early age, catching and selling minnows at his parents’ resort, and selling manufactured homes during his high school lunch breaks. What began as a business venture led him to the realization of his true passion of providing affordable housing for families. He served in the U.S. Navy and was a trained electrician. He and his wife Pat also owned and oper ated Thunderhill Estates and Gitche Gumee Resort. Mr. Remy served on the boards for the Wisconsin Manufactured Housing Association and Wisconsin Housing Alliance, and in 2001 earned the Elmer Fry Award for leadership and industry innovation.

8 | JULY / AUGUST 2022 EDITION

Happenings Have industry news you'd like listed here? Call Magazine Publisher, Patrick Revere, at (616) 888-6994, or email at patrick@mhvillage.com

GA

Atlanta Evergreen Marriott Conference Resort

What’s New at SECO This Year?

By attending SECO22, you’ll get to experience a suite of new and most requested topics and speakers. Here’s just a sneak peek of what you’ll see and do at this year’s SECO:

Tour on-site manufactured homes to see the latest developments in industry manufacturing

Take part in SECO’s first-ever golf tournament and networking roundtables

Attend THREE receptions for entertainment and networking throughout SECO22

Experience SECO’s first-ever

BAND at the event

Attend all-time favorite SECO educational sessions to further your industry knowledge

Over 500 attendees are expected to attend SECO live and in-person this year. You can’t miss your chance to be among this exclusive group and stay ahead of the curve.

To learn about sponsorship, exhibiting, and advertising opportunities, call (404) 777-SECO

LIVE

LIVE & IN-PERSON Stone Mountain Park Atlanta,

SECO22

October 3-6, 2022 presented in partnership with The Premier National Conference for Owning and Managing Successful Manufactured Home Communities Homes on display by: Register Today! secoconference.com

MANUFACTURED HOUSING INDUSTRYEvents

RV/MH Hall of Fame Induction Dinner & Ceremony

Monday, Aug. 15

Elkhart, Ind. | RV/MH Hall of Fame and Conference Center

The RV/MH Hall of Fame in its 50th year invites industry professionals, family, and friends to cele brate the milestone anniversary and honor the 2022 inductees. The event starts with a cocktail mixer, followed by dinner and the induction ceremonies. The hall in Elkhart details the careers of hundreds of RV and MH professionals, including a library, event center, and museums for each of the industries.

MH FacTOURy Summit 2022

Tuesday, Aug. 16 — Wednesday, Aug. 17

Elkhart, Ind. | Northern Indiana Homebuilding

Texas Manufactured Housing Association Annual Convention Sunday, Sept. 18 — Tuesday, Sept. 20 San Antonio, Texas | Marriott Riverwalk

The annual meeting in Texas begins with a Sun day golf event and exhibit booths opening in the afternoon, followed by a mixer and welcome dinner. Monday will start with a sponsored breakfast, ed ucational sessions, and a luncheon with a keynote speaker to be announced. The evening includes a cocktail reception and the Chairman’s Dinner. The event wraps up Tuesday morning with a networking breakfast and the fourth quarter association board meeting.

2022 Arizona Manufactured Housing Conference Sunday, Sept. 25 — Tuesday, Sept. 27

If you have an event or gathering — virtual or in person — you would like to have listed with MHInsider, please contact us at: www.mhvillage.com/pro/manufactured-housing-industry-trade-shows/

Events

10 | JULY / AUGUST 2022 EDITION

National Showcase Draws Eyes to Manufactured Housing Industry

TThree manufactured homes on the National Mall June 7-12 drew the attention and the praise of Washington D.C. lawmakers and policymakers, as well as passersby.

Cavco Industries teamed with UMH Properties to showcase a single-section manufactured home, and Skyline Champion Corporation brought out a pair of homes, one small-floorplan accessory dwelling unit, and a new CrossMod multi-section home with a pitched roof and attached garage.

“We made the decision to showcase our two homes because the country has a crisis and we have the solu tion,” Champion Homes Executive Vice President of Business Development Wade Lyall said. “Affordable, attainable housing is a crisis in our country and man ufactured housing is the solution. We need improved zoning acceptance and better access to attainable financing solutions, and by showcasing with MHI we get a chance to show members of Congress the industry’s newest products that can help solve the affordable housing issue.” »

MHINSIDER.COM | 11

Photo Courtesy of Cavco Industries

Events

New homes built in the factory dominated the event's first week. Then, in the second week of the showcase, manufactured homes were joined by panelized and modular homes. A 3D printer building homes and alternative building ma terials — such as container construction and system building — also were featured.

“When people come in the house, it speaks for itself,” MHI Chairman Leo Poggione said. “They walk in and they’re like, ‘I can’t believe how beautiful this home is.'”

Mark Sickles, from the Virginia House of Delegates, said he wished more people knew about the manufac tured housing industry and the homes it produces.

“I think if more boards of supervisors and city councils saw these homes they would be more willing

to change their codes to allow them to occur. It’s really beautiful,” Sickles said.

A Showcase for June as Homeownership Month

The Innovative Housing Showcase, hosted by the U.S. Department of Housing and Urban Development, is part of a push toward high-quality, affordable housing solutions, which is also is a White House priority. The Manufactured Housing Institute, the national advocacy group for factory-built housing, joined HUD early in the week to host Homes on the Hill, an opportunity for its members to appeal to lawmakers from their home states or states in which they operate.

“I don’t know anywhere in the country, and I travel almost every week, that I’ve seen something like this that is that affordable,” HUD Secretary Marcia Fudge said in an interview with MHI.

“It is going to be a major part of the solution,” Fudge said of manufactured homes.

Lesli Gooch is CEO of MHI.

“Our industry came together to ensure that federal lawmakers, policymakers, and the public could see first-hand how manufactured homes are delivering on the American dream of homeownership,” she said. “Thousands of people toured our homes on the National Mall during the Innovative Housing Showcase and we appreciate HUD Secretary Fudge

12 | JULY / AUGUST 2022 EDITION

Events

and her team for recognizing that our homes are making attainable homeownership a reality and for helping us share what we do with the nation.

“Manufactured homes are energy-efficient, designed with today’s families in mind, and at a price point that is attainable for millions of Americans who would otherwise be struggling to find a place to call home,” Gooch added. “The three homes will now head to their final destination, making three families’ American dreams come true. This has been a perfect way to recognize the 20th Anniversary of National Homeownership Month.”

More from the Capitol

In addition to HUD Secretary Marcia Fudge, members of Congress and administration leaders from across the federal government were impressed by the quality, design, and attainable price point of the homes.

In her opening remarks kicking off HUD’s Inno vative Showcase, Secretary Fudge said “today is the beginning of solving the country’s affordable

housing challenge" and recommitted her agency to utilizing innovative housing solutions to address the problem, including manufactured housing as part of the solution.

As part of this event, MHI members from across the country blanketed Capitol Hill to meet with their Sen ators and Representatives to advance the industry’s policy priorities and ensure manufactured housing remains an affordable homeownership option.

Manufactured housing professionals met with Congressional offices to talk about the need to update FHA’s Title I and Title II programs, to ensure DOE’s energy standards do not become effective until they are revised and adopted as part of the HUD Code, and to urge federal efforts to preserve and develop manufactured housing communities. MHV

To Advertise, call: 1-877-406-0232

NOW YOU CAN MANAGE YOUR SUBSCRIPTION ONLINE

Want MHInsider news in print and online, or just digital? Need to add or remove a colleague? Place a hold? Change an address?

Go to http://subscriber.mhinsider.com on your computer, tablet or phone.

When you subscribe, or link to your current subscription, you will be provided an individualized reader identification code to help facilitate any changes.

Thank you for reading!

Reach Over 30,000 Manufactured Housing Professionals in Print and Online

MHINSIDER.COM | 13

In Print and Online, the Premier News Source in the Manufactured Housing Industry THE MAGAZINE FOR MANUFACTURED HOUSING PROFESSIONALS

Events

SECO22 Marks Return to In-Person Event for Community Owners

TThe SECO National Conference of Community Own ers announced recently the return to an in-person format for the annual SECO Conference.

This year’s event, taking place from October 3 - 6, 2022, will welcome community owners and managers from all over the country to Stone Mountain Park in Atlanta.

Back to Tradition for SECO

The event’s website bills itself as being for “anyone who owns or has an interest in the health and opera tion of manufactured home communities.”

SECO20 and SECO21 were the organization’s first two years operating as a virtual event. With two years of virtual success in their back pocket, SECO is returning to an in-person format to kindle networking relationships between community owners and other industry professionals.

“SECO has always been about making personal connections and fostering education with small to mid-size community owners and managers,” SECO Co-Founder and organizer Spencer Roane said.

“We are thrilled to be back in Atlanta this year to continue the tradition in-person and share industry knowledge among fellow professionals,” he added.

What’s New in 2022 For SECO?

The 2022 event is set to host a number of new events and attractions while bringing back some all-time favorite sessions. This year’s educational programming is set to focus on management developments and challenges, community opera tions, management software and technology, and financing/valuation topics.

Notably, SECO22 will mark the return of on-site manufactured homes to the event for attendees to view.

Additionally, this year, attendees can take part in SECO’s first-ever golf tournament, attend three recep tions for entertainment and networking, experience SECO’s first-ever live band at the event, and see the latest developments in industry manufacturing.

On the programming side of things, attendees will also welcome the return of Manager Monday, a day of programming dedicated to community management topics, as well as the networking roundtables.

For more information on SECO22 and to register today, visit secoconference.com. MHV

14 | JULY / AUGUST 2022 EDITION

The MHWC Warranty provides unrivaled protection for your business against unexpected surprises or potential financial burdens, firmly preserving your bottom line. With MHWC, you will limit your liability, dial back your risk, and save time and money. Contact me for a quote or more info. Stress less and score big with MHWC! MHWC NEW HOME WARRANTIES Tifanee McCall 800.247.1812 Ext. 2132 sales@mhwconline.com www.mhwconline.com Written Insured Warranties specifically designed for Manufactured Housing Events

One Historic Night at the Hall

Professionals Gather to Honor New

New MH Museum

16 | JULY / AUGUST 2022 EDITION

Manufactured Housing

Inductees, Celebrate

TThe RV/MH Hall of Fame in Elkhart, Ind., is celebrating multiple historic achievements in August, inducting 10 new honorees in its 50th year, as well as unveiling the much-anticipated Manufactured Housing Museum.

“This year's induction dinner guests will get a special treat as the grand opening of the 21,000 square foot Manufactured Housing Museum will be taking place on the same day,” RV/MH Hall of Fame President Darryl Searer said. “This museum winds through time from the industry's origins, through the present day, and finishing with tomorrow.”

The museum, Searer said, is highly educational on every thing the industry has to offer and features an immersive and interactive experience that takes the Hall of Fame's new museum from being an attraction to a destination. »

MHINSIDER.COM | 17

Events

$8,900,000 ROCHESTER, NY MHC PORTFOLIO

Origins of the Hall of Fame

The RV/MH Hall of Fame was formed in 1972 by a group of industry magazine publishers, and during the ensuing years has been able to grow from a small library to a 40-acre campus featuring an RV Museum with 60 one-of-a-kind recreational vehicles, the new interactive manufactured housing museum, the world's largest industry library, a hall dedicated to Go-RVING, an exhibitor's hall, and the Hall of Fame. A 36,000 square foot convention hall is underway for the Northern Indiana Event Center, which already has a pair of halls providing 24,000 square feet of space, and a 250-unit multi-purpose rally/show site that also is a one million square foot parking lot with a 20,000 square foot climate-controlled pavilion at the center.

Induction Dinner Honorees

David J. Carter Sr. - Supplier, Florida

In 1986, Dave Carter sold a lumber yard and an

electrical supply business to concentrate on Dave Carter & Associates, supplying the electrical and building product needs of the manufactured housing industry. In three years he took DCA from a regional provider to a national supplier with a dozen distribu tion centers. In 1993 the business added plumbing products, diversified into RV in 2008, and helped rebuild the manufactured housing industry during its 15+ year recent era of growth. DCA was named MHI Supplier of the Year in 2011, and Dave Carter continues to advocate for affordable housing on the local, regional, and national levels.

Harry Karsten - Manufacturer, California

Harry Karsten built The Karsten Co. and Karsten Homes into a West Coast powerhouse. It was founded in 1995 and built its workforce to more than 700 people, including a couple hundred at the homebuilding facil ity at its plant near Mather Airport in Sacramento. »

Industry News

A modern manufactured home in a Florida marina setting.

The company expanded from California to other homebuilding sites in Albuquerque, N.M., Stayton, Ore., and Breckinridge, Texas. At the time it was purchased by Clayton in 2005, the facilities were putting out better than 1,700 homes a year in 14 states in the West and central United States.

Raylen Gritton - Dealer, California

Ray Gritton has been in the manufactured housing industry for more than 40 years. He started his first dealership in Modesto in the 1970s and has worked for large corporations in charge of hundreds of deal erships. He currently owns 13 locations in five states. Gritton has won multiple awards and has served on boards for state and national industry associations.

Tim Williams - Finance/Lender, Tennessee

Tim Williams had a long, productive, and diverse career in manufactured housing even prior to co-founding 21st Mortgage in 1995. As CEO of the organization, he has been instrumental in providing improved financing for affordable homes across the country as well as growing 21st into one of Knox ville's largest employers. In addition to his efforts in Tennessee, Williams has been a tireless advocate for manufactured housing in Washington, D.C., and nationwide.

Eugene W. Landy - Communities, New Jersey

Eugene Landy is a founder and current chairman of the board for UMH Properties, Inc., a publicly-owned REIT in the ownership and operation of manufac tured home communities. He is a graduate of the U.S. Merchant Marine Academy as well as Yale Law School, where he served for many years on the board of advisors. UMH, now operated by Eugene’s son, Sam, has a portfolio of 127 manufactured home communi ties with about 24,000 developed homesites. These communities are located in New Jersey, New York, Ohio, Pennsylvania, Tennessee, Indiana, Michigan, Maryland, Alabama, and South Carolina. UMH also owns and operates one community in Florida through its joint venture with Nuveen Real Estate.

Jim Scoular donated generously to the museum in honor of his father Ralph, a 1998 RV/MH Hall of Fame inductee.

RV Inductees

Mark Ferkey - Dealer Donald Gunden - Manufacturer Veronica Hepp - Dealer Lewis Shaum - Supplier

What Awaits Behind the Curtain of the New Scoular Museum?

A small group of industry professionals was able to get a sneak peek of the new Manufactured Housing Museum, an experience made possible by many individuals, most notably the museum’s namesake Jim Scoular, who donated to the effort in honor of his father, Ralph, who preceded him in the industry and as a member of the Hall of Fame.

The museum is a linear historical journey through time and into the future of manufactured housing, beginning with covered wagons on the American frontier and viewing the future of housing from a rather surprising vantage point.

The journey includes an appeal to all of the human senses, from crickets in the night to the aroma of fresh-cut grass, and a gentle breeze at your back. Veteran museum, zoo, and theme park designer Thomas Landgrebe left not a single trick on the table in the effort to create a remarkable experience in time and place.

“I appreciate so much what everyone who works here has done,” Jim Scoular, a South Dakota industry professional, said of the efforts in Elkhart, Ind. “It’s a dream come true for the industry, and it all comes back to the leadership here. It’s tremendous.”

With the addition of the new museum to comple ment its existing offerings, Searer said he anticipates annual visits to exceed 100,000. In the last 10 years the venue has matured from a hall, meeting space, and library valued at $500,000 to a much larger event space with two museums, a large outdoor rally site and pavilion, and the two museums now worth about $22 million.

“We’ve come a long way in a short period of time,” Searer said.

Among those who toured the hall in advance of its Aug. 15 opening was Joe Viglione, of Fairmont Homes, which donated the first modern home to the museum,

jump starting subsequent donations and partnerships that have made the effort a success.

“This addition to the hall is a great thing for our industry,” said Kim Schultz-Rainford, who owns communities in Texas.

George Allen, a former community owner and consultant in manufactured housing, continues to write about industry advances and is a longtime supporter of the hall of fame.

“I have waited 44 years , the sum of my career, to see what I saw today,” Allen said following the sneak peek museum tour. “I am very impressed.” MHV

Reach Over 30,000

Manufactured Housing Professionals in Print and Online

To Advertise, call: 1-877-406-0232

Expertise in the area of Manufactured Housing Law in Delaware

If you are thinking of purchasing or selling a community, or have questions running your community, please make us your first call.

Nicole M. Faries

We are here to help you and we look forward to assisting you.

ATTORNEYS AT LAW www.BMBde.com

Wilmington | Dover | Lewes | Georgetown 302-327-1100

MHINSIDER.COM | 21

Industry News

Fannie Mae and Freddie Mac Duty To Serve Plans

Is There Any Good News About Purchasing Chattel Loans on Manufactured Homes?

by Raymond Leech maybe

by Raymond Leech maybe

Industry News

AAs we all know, manufactured housing is one of the best sources of affordable housing avail able today and makes up to 10 percent of all of the nation’s housing stock. With the severe housing shortage in this country, estimated to be close to four million units by Freddie Mac, manufactured homes are valuable in closing this gap. But a large percentage of loans used to purchase these homes are chattel loans or personal property loans, and the convention al mortgage marketplace does not support chattel loans. This results in financing that has higher interest rates over shorter terms, and fewer consumer protections.

While Cascade Financial has been successful in creating a few securitizations in recent years, there are currently no other major investors that purchase or securitize chattel loans for MH. And the two Government-Sponsored Enterprises (GSEs), Fannie Mae and Freddie Mac, do not have policies or products in place to purchase them either.

But that could be changing. »

MHINSIDER.COM | 23

Industry News

Photo Courtesy of Cavco

What Are the Enterprises Doing on Chattel?

In April of this year, the Federal Housing Finance Agency (FHFA) released the Duty To Serve (DTS) plans of Fannie Mae and Freddie Mac. Duty To Serve is a commitment by FHFA through Fannie Mae and Fred die Mac to provide financing in three key underserved mar kets: manufactured housing, rural housing, and affordable housing preservation.

DTS commenced in 2016 and the first plans were an nounced in 2018. A new plan is announced every three years. The one released in April is for 2022 through 2024.

But the 2022 plans got off to a rocky start, and one of the reasons is both GSEs had nothing to address support for chattel loans.

In a stunning development, the original DTS proposals to FHFA in May of 2021 were soundly rejected by many housing advocates such as the Lincoln Institute, the National Housing Conference, and National Commu nity Stabilization Act. They told FHFA to hit “pause” as they did not believe the proposals met the spirit of the DTS commitment.

The advocates were upset that both GSEs were ending their plans to explore purchasing chattel loans, and disappointed in the goal levels set for rural, affordable housing preservation, and manufactured housing. FHFA listened and told Fannie Mae and Freddie Mac in January of this year to go back to the drawing board. And they did, and the new proposals were accepted in April.

But even with the improved proposals and more robust goals, do not expect significant changes regarding chattel financing in the next few years. However, there are some things happening.

Freddie Mac

In their April DTS plan, Freddie Mac announced

a definite focus and goals for chattel loans in the next few years.

Freddie Mac committed to purchasing from 1500 to 2500 chattel loans as part of their DTS goals in 2024. Over the next two years, their plan is to complete a feasibility assessment of the requirements and processes needed to support chattel loan purchase, including un derwriting, pricing, consumer protection, valuation and risk management.

And if they are successful, they want to obtain FHFA approval to move forward with a loan option that could be introduced in 2024. The big challenges they point out are a lack of lender standardization, no standard underwriting practices, and no consistent approach to assessing property values.

Freddie Mac announced a focus on MH homes in Na tive American and Alaskan American communities, which have complicated land ownership rules due to trust or tribal issues. They also are working on efforts with nonprofit developers to expand the availability of manufac tured housing. Additionally, they are focusing on expanding their outreach and loan purchases in resident-owned communities (ROCs) and nonprofit developer communities.

Fannie Mae

Fannie Mae’s plan does not include any specific goals for chattel financing by 2024. But they are still interested in exploring this area.

“We continue to work with our regulator (FHFA) to understand safety and soundness considerations and the viability of a chattel loan pilot program,” Fannie Mae said in a published statement.

So based on this, Fannie Mae may offer the chattel loan product via a pilot. Typically, pilots are done with selected lenders in specific markets. And pilots can be up to one or two years in length. So do not expect

24 | JULY / AUGUST 2022 EDITION Industry News

Freddie Mac is taking the lead on chattel financing efforts, and typically, once one GSE adopts a program or product, the other one will follow.

-Raymond Leech

a chattel loan product available nationwide to lenders from Fannie Mae for several years at least.

Fannie Mae’s plan also includes efforts to develop products and strategies to purchase more loans in manufactured home communities. These communities feature homes built in factories and delivered to the community where residents own homes and lease the land from a community owner. They also announced that all loans in these communities must have 100 percent tenant site lease protections in place.

In addition, Fannie Mae an nounced that they are exploring how to purchase more loans from MHCs to finance rental units, and also allow residents who rent MH units to report their rental

payment data to credit bureaus to help build up their credit profiles.

Some Good News

The good news for the man ufactured housing industry is that both Fannie and Freddie are increasingly committed to the purchase of more conventional loans related to MH titled as real property, with Freddie planning to purchase from 5,800 to 7,500 loans each in the next three years and Fannie planning to purchase at least 9,300 loans annually in the next three years.

So, in summary, housing advocates were able to steer both Fannie Mae and Freddie Mac toward more robust efforts and goals in the manufactured housing marketplace. Freddie

Mac is taking the lead on chattel financing efforts, and typically, once one GSE adopts a program or product, the other one will follow. This will be an interesting effort to examine during the next few years, and hopefully we will see progress down the road. MHV Raymond Leech has worked in the mortgage industry for 30 years, first with Fannie Mae and more recently with Fairway Independent Mortgage Corporation. He has developed and managed construction and renovation mortgage products, but also worked on FHFA Duty To Serve efforts involving manufactured housing, as well as rural affordable housing efforts.

MHINSIDER.COM | 25 Industry News

ATTRACT NEW RESIDENTS INCREASE YOUR REVENUE NO CONSTRUCTION, NO COST DISRUPTION-FREE Visit kwikbit.com to find out how you can deliver returns for your community today! You Can’t Have A Great Community Without Great Internet (888) 594-5248 Kwikbit extends fiber using our next-gen wireless technology to deliver high-speed internet service to manufactured home communities. Leapfrog your community’s last generation cable broadband and give your residents the high-speed connection they need for video calling, streaming, remote work, and all the modern needs of a manufactured homeowner.

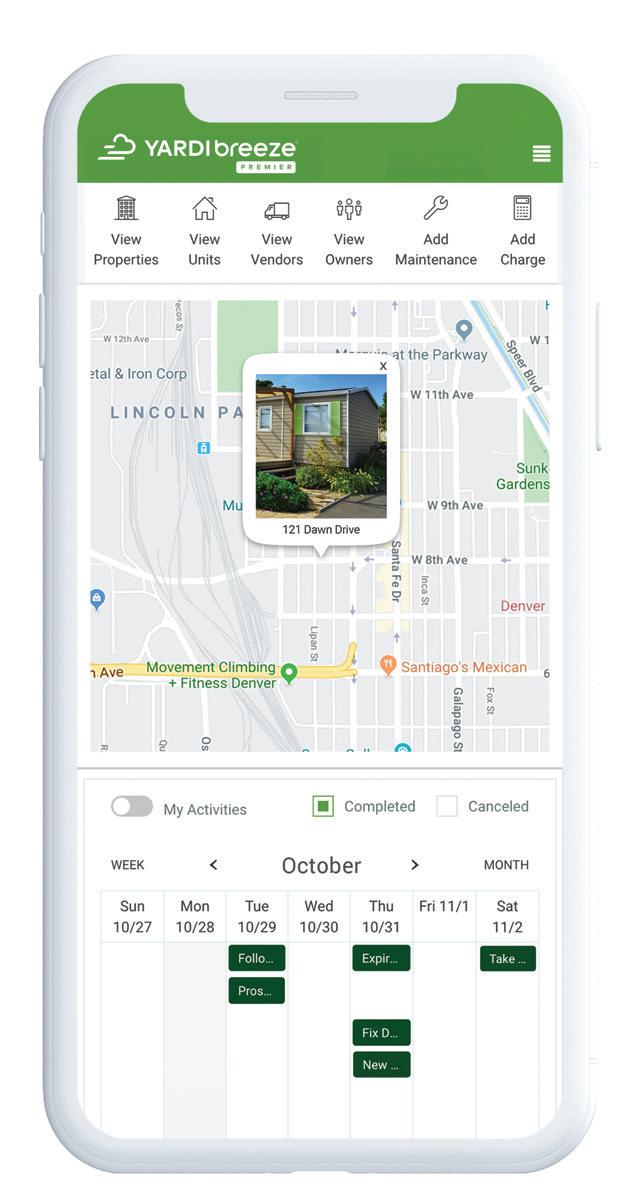

intuitive

powerful

housing software

YardiBreeze.com | (800) 866-1144 Get a personalized demo to see why Breeze Premier is the perfect tool to run your business from anywhere

&

manufactured

“All of our needs are met in Breeze Premier, making management easier and more cost-efficient.” Christine Fraser Summit Communities Everything you need to manage your communities ✓ Easy setup ✓ Live chat support ✓ ILS posting for vacant lots ✓ Online applications ✓ Online payments ✓ Online maintenance ✓ Manage lot availability, utilities & charges ✓ Manage owned or rented homes & RVs ✓ Track home inventory ✓ Vacancy & prospect tracking ✓ Violations management ✓ Email & text communications ✓ Vendor payments ✓ Property accounting ✓ Walk-in payments ✓ Owner payments & reports ✓ Property websites† ✓ Online lease execution† ✓ Utility billing & invoice processing† ✓ Investment management† *Minimums apply †Additional fees apply AffordableCondo/HOASelf StorageMH

How Rising Interest Rates Erode Value

by Kevan Enger

HHistorically low unemployment, growing payrolls, and rising con sumer spending have combined with continuing supply chain challenges in what is being called The Great Supply Chain Disrup tion. Add the war in Ukraine to the mix and we now have a historically unique combination of forces that has pushed inflation to a 41-year high of 8.5 percent in March of this year.

Inflation happens when prices go up as a result of an increase in production costs, raw materials, and labor. Over the past year, this cost-push inflation has been exacerbated by an increase in demand for goods and services that has exceeded supply and the ability to produce goods at a rate that meets that demand.

This skyrocketing inflation has led the Fed, whose job it is to promote the health of the U.S. economy and the stability of the financial system, to increase its benchmark interest rate. The first hike came in March of this year marked by a quarter of a

percentage point, followed by a second boost of half a percentage point in May, and three quarters hike in June.

The moves prompted the prime rate to increase to 4.25 percent. The prime rate is what banks charge their best and most cred itworthy customers and is used as a basis for other loans such as mortgages, home equity loans and lines of credit, small business loans, and personal loans.

What most mobile home com munity owners don’t realize, however, is that rising interest rates also have an impact on their park’s property value.

And the impact can cost you millions of dollars.

On the Horizon

The Fed raised the rate by three-quarters of a percentage at the July meeting, and is expected to raise it by at least a quarter-percentage point two more times this year.

The current prime rate of 4.25 percent is up from 4 and 3.50

percent in March but still below 2019's 5.25 percent (8/1/19) or 2018's high of 5.5 percent (12/20/2018). However, it will go back up as a result of the upcoming Fed hikes.

The majority of mobile home parks are acquired using lever age, mostly agency financing via Fannie Mae and Freddie Mac, but other types of loans as well. Although Fannie and Freddie loan rates are typically lower than stan dard loans, their rates will also increase. This means that buyers will be paying more for the capi tal they use to acquire a mobile home community.

This is significant because if the cost of capital goes up for borrowers, it follows that buyer’s returns will be impacted, and as a result, so will cap rates.

While there is still a lot of de mand for manufactured home communities as an asset class, acquisitions must have positive leverage otherwise they just won’t make sense.

And this is why sellers must pay attention. »

MHINSIDER.COM | 27

Industry News

Timing Is Everything

At the moment, the hikes hav en’t impacted deal flow but there is more trepidation in the market from buyers and more urgency from sellers.

This urgency is not unwarrant ed. Here’s why.

Let’s assume you have a park that is currently valued at $20 million. In a primary market, your community may be at a high 3 percent cap rate. If the property is located in a tertiary market you may be looking at a low 5 percent or high 4 percent cap rate.

If the park has a $700,000 NOI, and cap rates move up by 100 basis points or just 1 percent from 3.5 percent to 4.5 percent, for exam ple — it will erode your property’s value by about $4.4 million.

Instead of $20 million your property is now worth $15.56 million. I don’t know about you but I would rather keep that $4.4 million instead of seeing it simply vanish.

If the cap rate increases by just a half-percentage point, you are still down $2.5 million. That is better than the $4.4 million but still $2.5 million more than what I am willing to give up.

This amount of money alone can have a generational impact on a family, fund a worthy cause for years, or be the beginning of a new portfolio of properties or investments.

Now imagine the impact if you have multiple properties.

Aside from interest rates, buyers will also have to weigh

the increasing cost of repairs, labor, and materials — all components that will impact a community’s NOI.

With at least three more interest rate hikes forecasted this year, timing has never been more important.

Mobile home park owners who have been thinking about selling or think they may want to sell in the next three to five years should consider their timing and the repercussions of the changing economic conditions on the value of their property.

The first step toward mak ing the best decision for your property is to request a broker opinion of value from a repu table seller-focused broker that specializes in selling mobile home communities and understands the current landscape.

difference

With an estimate of your prop erty’s on-market value in hand, you can then decide if selling now makes the most sense for you, or if you rather hold for the next three to five years. MHV

Kevan Enger is a partner and man ufactured housing director for Capstone MH. He specializes in helping mobile and manufactured home park property owners across the country successfully position, market, and sell their properties to maximize their returns. Capstone has seven offices in five states throughout Florida, the Southeast, Midwest, and Mid-Atlantic.

28 | JULY / AUGUST 2022 EDITION

Industry News Discover the Credit Human

Where we’re committed to: Improving the lives of the people we serve. Crafting consumer lending programs with your needs in mind. Making a complex process smooth and simple. Federally Insured by NCUA NMLS# 486243 Contact us at: MHinfo@CreditHuman.com

Water Submetering Optimized for Mobile Home Parks Call us Now for Info: 303-217-5990 With Cellular Connectivity Save 30% on your Water Bill! www.MetronSubmetering.com with Advanced Analytics Meters For Every Application •Get alerted for leaks and infrastructure issues TM Flow Rate 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 GPM Consumption 05:00 07:00 09:00 11:00 13:00 15:00 17:00 19:00 21:00 0 10 20 30 40 50 60 70 80 G 00:00 02:00 04:00 06:00 08:00 10:00 12:00 14:00 16:00 18:00 20:00 22:00 Flow Rate 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 GPM Toilet Flush Sink Usage Shower Kitchen Use Toilet Flapper Leak! Time 5:05 5:10 5:15 5:255:20 5:30 5:35 5:40 5:45 5:50 5:55 Unit 21C TM

INSPIRE COMMUNITIES EXPANDS IN TEXAS

by Patrick Revere

by Patrick Revere

Community

OOne of the nation’s largest own er-operators of manufactured new home communities is expanding its presence in the Houston area with two new projects, including the re-de velopment of an existing bayfront setting, for individuals, families, and empty nesters seeking an affordable homeownership solution.

Inspire Communities is based in Phoenix and owns and operates 130 all-age and active-adult manufactured home communities and RV resorts. It recently completed a multi-million dollar re-development of its Oceanway community, a 17-acre enclave, in gulf coast Texas that has 150 homesites, including 32 waterfront and bayview homes on the shores of Trinity Bay.

Ten miles from Baytown, the newlook, gated community of affordable, well-built, high-style manufactured homes offers the charm of bayside living while appealing to those seeking a nearby second home for weekend getaways.

The community features homes in a variety of settings with stainless steel appliances, vaulted ceilings, upgraded cabinetry, and crown molding. Stylish, open-concept floor plans range from approximately 1,200 to 2,000 square feet. Waterfront Smart Cottages include a deck overlooking Trinity Bay. »

MHINSIDER.COM | 31

Community

“It’s the look, feel and quality of a traditional new home, but at a more affordable price,” Senior Vice President of Sales and Marketing Heidi Loftin said. “It’s truly luxury living within reach.

“This was a unique opportunity to create a com munity of affordable new homes with the bay right outside your door… It’s really a hidden gem,” she said.

The community has two-, three- and four-bedroom options including farmhouse designs and waterfront cottages. Features include an island kitchen, oversized breakfast bar, great room, primary bedroom with walk-in shower, flex space, and a two-car driveway.

Several waterfront “Smart Cottages” feature low-e double pane windows and upgraded exterior paneling with a 50-year warranty, Loftin said.

The re-development of Oceanway includes the addition of a charming main boulevard lined with white picket fences and tall palm trees, newly paved streets, a fenced sports court, and a playground.

Loftin said other amenities include a 650-foot com mercially engineered fishing pier and an expansive boardwalk sundeck with lounge chairs.

Aaron Simon, a 41-year-old accountant, recently purchased a new home in Oceanway.

“Everything they’ve done is really nice and it’s a great location right on the water,” Simon said. “I love stepping onto my patio where I can enjoy a nice breeze and a beautiful view of the water.

“Plus, I like to fish so having the fishing pier here was a big selling point for me too,” he said. “And of course, you can’t beat the price.”

New Community Near Lake Conroe

North of Houston in Willis, Inspire Communities is developing Rockrose Ranch at Lake Conroe, new construction on 170 acres for both an all-age and a gated, active-adult village.

Located two miles from Lake Conroe, the ground-up development will feature a sprawling amenity island with two swimming pools, pickleball courts, children’s playground, fire pits, miles of walking trails, lakes, and a fenced dog park. MHV

32 | JULY / AUGUST 2022 EDITION Community

Sun Communities Releases Environmental, Social and Governance Report

SSun Communities, the Michigan-based real estate investment trust, has released its annual environ mental, social, and governance report, unveiling the implementation of new initiatives, policies, and procedures within the company.

“As we grow, we view our responsibility and stew ardship to the environment, as well as to our team members, communities, and all stakeholders, with a stronger resolve than ever,” Sun Communities Chair man and CEO Gary Shiffman said. “We recognize that our team members and culture are the foundation to our success, and we demonstrate our value for their contributions by investing in various programs and benefits.”

In the last year, Sun engaged executive leadership to develop a corporate sustainability strategy that is integrated with the larger corporate vision and framework. In 2021, the ESG Steering Committee was established to align initiatives and actions addressing

and managing material issues. The committee meets quarterly to establish strategies related to these is sues, discuss the progress of initiatives, and ensure cross-functional collaboration.

Advancements made by the company in its ESG efforts during 2021 and 2022 occurred largely at corporate headquarters in Southfield, Mich., as well as in its manufactured home communities, RV resorts, and marinas located throughout the United States, Canada, and Puerto Rico.

The highlights of Sun Communities’ progress includes the following measures:

• The IDEA Council was launched to create a focus on inclusion, diversity, equity, and accessibility

• More than 5,600 volunteer hours were provided by Sun team members

• A company-wide commitment to formalize the reduction of greenhouse gas emissions and »

MHINSIDER.COM | 33

Community

improving environmental performance of the properties within the Sun portfolio

Corporate Stability, Industry Support

In 2021, Sun undertook a comprehensive assess ment of its supplier partnerships and procurement processes to identify opportunities and risks within the supply chain.

The assessment would have been a valuable effort at any time, and proved particularly insightful in the face of industry challenges with the cost and availability of goods and services. It creates better leverage for the company and provides an improved supply base, product standards, and reliability of processes.

“This information allowed the team to develop supplier and sourcing strategies, maximizing the size and purchasing capabilities of Sun,” the report stated. “The team was also creating a sustainable supply chain to accommodate our needs and geographic spread at the same time.”

An initial step was to issue the Supplier Code of Conduct, which established the baseline expectations

of what suppliers must meet to work with Sun. The company will continue these efforts and expand to include a comprehensive supplier management program, with supplier audits and business reviews throughout 2022 and beyond.

Sun Joins UN Global Compact

In addition, and as a complement to its ESG efforts, Sun has dedicated itself as a member of the United Nations Global Compact initiative, a voluntary leader ship platform for the development, implementation, and, disclosure of responsible business practices. The initiative was launched in 2000, and has be come the largest corporate sustainability initiative in the world, with more than 15,000 companies and 3,800 non-business signatories based in more than 160 countries. MHV

34 | JULY / AUGUST 2022 EDITION

Community Manufactured Home Loans In A Zip © 2022. Zippy, Inc. All rights reserved. Zippy is an Equal Housing Lender. As prohibited by federal law, we do not engage in business practices that discriminate on the basis of race, color, religion, national origin, sex, marital status, age (provided you have the capacity to enter into a binding contract), because all or part of your income may be derived from any public assistance program, or because you have, in good faith, exercised any right under the Consumer Credit Protection Act. The federal agency that administers our compliance with these federal laws is the Federal Trade Commission, Equal Credit Opportunity, Washington, DC, 20580. Home lending products offered by Zippy Loans, LLC. Zippy Loans, LLC is a direct lender. NMLS #2189776. 2807 Allen St., Suite 335, Dallas, TX 75204. Not available in all states (www. nmlsconsumeraccess.org). Full-Service Provider We finance new & used homes, LTOs, RTOs, RPOs, and down payment assistance programs. Close in As Little As 5 Days 100% digital process means loans close in a zip. No Personal Recourse We replaced the personal guarantee with a short-term community guarantee to better address community owners’ needs. The Zippy Difference Contact us today to learn how to partner with Zippy! Chris Donsbach HEAD OF COMMUNITY PARTNERSHIPS chris@zippymh.com (865) 257-8249 Innovative Funding Solutions Community Funding Zippy Funding Community-set lending criteria 100% digital experience No personal guarantee Zippy-serviced No fees out of pocket Market-set lending criteria Go to http://subscriber.mhinsider.com on your computer or mobile device Manage Your MHInsider Subscription Online!

MHINSIDER.COM | 35 Community professionals trust JLT Market Reports by Datacomp for timely and accurate manufactured home community market data. JLT Market Reports provide detailed research and information on investment-grade communities located in major markets including the latest rent trends and statistics, marketing programs, and other useful management insights. Learn More About These Markets, Identify Opportunities, and Stay Competitive! www.datacompusa.com/JLT 800.588.5426 • Number of Homesites • Amenities • Rents • Occupancy • Services The Nation’s Most Comprehensive Source of Market Data for the Manufactured Housing Industry WE HAVE THE DATA DOWNLOAD A FREE SAMPLE REPORT: DatacompUSA.com/JLT YOUR COMMUNITY Rent: $997/month Occupancy: 94% COMPETITOR #1 Rent: $949/month Occupancy: 89% COMPETITOR #2 Rent: $1,100/month Occupancy: 96% COMPETITOR #3 Rent: $1,249/month Occupancy: 98%

Rent Butter Goes Well Beyond Credit Score

New Approach Allows Rental Applicants to Show All Sources of Income

RRent Butter wants its clients to rent better, streamlining internal leasing operations and enhancing the renter’s and community owner’s screening experience.

Company founders Chris Rankin, a developer, and Tom Raleigh, an attorney, had been working in multi-family housing, largely serving the middle market on Chicago’s west and south side. They were

part of a real estate firm that grew from 100 to 10,000 apartments in five years and learned pretty quickly that they needed a more efficient way to screen and communicate with prospects and renters.

Truthfully, they had become somewhat accustomed to application acceptance on little more than a credit score, as well as a high volume of turnover and evic tion. They were certain there was a better way.

“What are your biggest pain points? We interviewed 50 landlords and they all said the same thing,” Raleigh said. “How do I assess risk when the applicant’s credit score is really low? It made sense for us to tackle that issue.

“If they make stable income and make their rent payment on time, what does the credit score matter?” Raleigh asked.

A great majority of the people who apply have the ability to pay their rent, Raleigh said, but what Rent Butter customers are looking for is the willingness to pay.

“We call that the ‘Grit Factor’,” Raleigh said.

Rent Butter’s digital applica tion runs on a smartphone and gets approval from the applicant to share banking information with the owner looking to rent. It looks at instances

Community

36 | JULY / AUGUST 2022 EDITION

Natalie Clark (right) and Claire Conti from Rent Butter talk with customers during an industry event in Arizona.

of non-sufficient funds and overdrafts, measures income stability, timely rent payments, and positive or negative trends in revenue and account balance.

“We give every landlord two reports,” Rankin said. “We give them the banking report, and credit behavior report. The real question is how they’re trending, not whether they have a 670 credit score but are they trending up to 720 or down to 550?

“The interface is easy to understand, and it really draws your eye to what’s important.”

The app pulls in info on defaults or late accounts that have yet to hit the credit score — 634 credit score six months later can be below 600 with a bad couple of months. All of the information flows into Rent Manager and other large property management software solutions.

“The decades of hard work our industry has put into place has been very rewarding,” Raleigh said, for the property owner and management team, as well as the renter.

How Rent Butter Improves Resident Experience

“We make it really easy to apply,” Raleigh said. “Go on your phone and apply in five minutes.” The easier it is for someone to apply, the more applications the property owner will receive.

The more common rental application is five or six pages to look over. With Rent Butter the appli cant uploads an image of their ID card or driver’s license and completes the rest on their smartphone in just minutes.

“Our ID verification tool is like airport technology at your property,” Raleigh said. “Their ID can be scanned and validated in real time.”

Pay stubs can be shared easily, and if no pay stubs are available, the user can provide secure access to their bank account.

“Connect your bank, and once permission is granted Rent Butter goes in to extract the needed data for the property owner,” Raleigh said. “It asks the applicant ‘Of all of these deposits, which ones are income?’ You click a box to confirm deposits that are earned income.

“Gig work and side hustles are included, so the applicant finally has a way to show their true income,” he said. MHV

MHINSIDER.COM | 37 Community

NATIONWIDE SHIPPING Nappanee, IN 46550 Ph: 574-773-7993 ext. 1 Fax: 574-773-2132 STAINLESS STEEL FASTENERS STEPS • DECKS BUY DIRECT

A PIONEER IN MANUFACTURED HOUSING

38 | JULY / AUGUST 2022 EDITION UMH PROPERTIES, INC.

As a publicly traded REIT (NYSE:UMH), we have been providing quality a ordable housing since 1968. Our portfolio provides high pro t margins, recession resistant qualities, reliable income streams and the potential for long-term value appreciation. • $2.4 billion in total enterprise value • 129 communities, 24,200 homesites, 1 joint venture community containing 200 homesites, 11 states • Housing approximately 21,000 families • 7,100 total acres, 3,600 acres in Marcellus and Utica Shale regions UMH Awarded 2021 Manufactured Home Community Operator of the Year and 2021 Retail Sales Center of the Year by the Manufactured Housing Institute For more information, visit www.umh.reit or contact ir@umh.com

MortgageFlex

Focuses on Ease, Speed

MMortgageFlex knows that the best way to make your customer happy is to be first, be flexible, and be responsive.

It’s a suite of loan and originating software solutions that brings the relationship between lender, dealer, and customer to a new place, far beyond long-held approaches that reach back to fax machines and call lists.

“Everything is tied in together and everything is bilingual and mobile,” MortgageFlex’s John McCrae said. “The way to get to that potential borrower is to react quicker. That customer’s cell phone is going off within 10 minutes to offer them a conversation in Spanish or English.”

The company has about 40 employees and is based in Jacksonville, Fla., though its employees work remotely from many different locations. The offering is 100% Microsoft hosted and is used by 40 regular customers as well as about 35 credit union service organizations.

MortgageFlex had been working with Credit Human at the time it realized the opportunity for its services in manufactured housing. »

Competitive Analysis

Ice, formerly Ellie Mae, bought Black Night, which merged the two main competitors in the loan origination and servicing technology space

MHINSIDER.COM | 39

Service / Supply

“We spent almost a year working with them on use cases just to figure out how they operate, and then we spent about eight months developing the product,” McCrae said. “We thought it was going to be a one-off and come to learn there are not a lot of active players with lending and servicing technology like this in the manufactured housing space.”

Eliminate Clunky, Duplicative Systems

In any form of lending, McCrae said, origination is the easier place to gain a foothold, but servicing is where you gain loyalty and grow your business. These are conversations that apply to all forms of products in the marketplace, including in technology.

“We set it up to where the user only sees what they need,” McCrae said. “If a client is only doing chattel loans, then they’re not going to have to look at any of the rules associated solely with conventional loans."

Integrations are made simple. For instance, Docu prep is a document provider that can seamlessly identify property and loan type, and will automati cally grab and share a complete document package

that aligns with state standards for the transaction.

“We’re putting tools into the hands of lenders to put them on the same playing field,” McCrae said.

The product was designed for conventional mort gage lending, and that remains a major part of the business. The company has dipped into commercial lending, and also handles the chattel process easily, even when dealers and in-community lenders are keeping those loans on the books.

“Servicing of chattel loans is pretty easy compara tively,” McCrae said. “Escrows are minimal and we’ve gained expertise in the whole customer service side, letting people do everything online.”

MortgageFlex continues to develop its set of services, including through artificial intelligence and optical character recognition, a tool to scan and digitize whole text for immediate readability for machine editing, computing, and analysis. MHV

40 | JULY / AUGUST 2022 EDITION

Service / Supply 2023 April 19-21, 2023 MGM Grand | Las Vegas SAVE THE DATE www.congressandexpo.com

BELOWERNEXTYEAR... YOURPROPERTYVALUECOULD

WHYGAMBLE?

Early in 2022, the Fed disclosed in their minutes that they believed the low workforce participation was due to Americans having too much equity in their real estate. To counteract this behavior, they stated their goal was to create a mini recession around real estate. They then proceeded to tell the market they would implement 5-7 rate hikes this year, including the largest increase in over 22 years of 50 basis points.

In total, we have seen all-in rates go from the low-mid 3%’s to 5-6%’s in the span of four months. Thus far, buyers have continued to focus on price per pad and rent growth due to a severe lack of housing and ignored the materially higher rates. Depending on how high rates go and how long they stay there, more and more buyers will start being priced out of the market and the Fed might eventually achieve its goal of creating a real estate correction. If your timeline or hold period is more than 5 years, we believe rent growth and inflation will eventually offset the potential coming correction. But if you have planned changes, like retirement or family planning that are motivating you to sell in the next 5 years, there is a high probability that commercial real estate will be worth less in the next few years than it is today.

EXPERIENCE THE YALE ADVANTAGE CONTACT US FOR A FREE VALUATION

| INFO@YALEADVISORS.COM

yaleadvisors

BELL Mid-Atlantic 985-373-3472

Yale Realty National Team HARRISON

Harrison@yaleadvisors.com KEN SCHEFLER Upper Midwest 323-393-0116 Ken@yaleadvisors.com BRIAN MCDONALD Rocky Mountains 720-636-6551 Brian@yaleadvisors.com CHAD LEDY Pacific Northwest 651-334-2390 Chad@yaleadvisors.com DAN COOK Pacific Southwest 305-771-3211 Dan@yaleadvisors.com DANA SMITH Southwest 303-323-5649 Dana@yaleadvisors.com CHARLES CASTELLANO Southeast 305-978-0769 Charles@yaleadvisors.com JAMES COOK National Director of Brokerage 386-623-4623 James@yaleadvisors.com MAX HERNANDEZ Grand Canyon 415-686-8694 Max@yaleadvisors.com JAMES MCCAUGHAN Midwest 305-588-5302 JMcCaughan@yaleadvisors.com CHRIS SAN JOSE President of Lending 850-443-4580 Chris@yaleadvisors.com GREG RAMSEY Vice President of Lending 904-864-3978 Greg@yaleadvisors.com Yale Capital MITCH GONZALEZ Land Sales & Development Director 734-447-6952 MGonzalez@yaleadvisors.com YALEADVISORS.COM | 1-877-899-9810 MATT WHITERMORE New England 774-217-3971 Matt@yaleadvisors.com Land & Development NEW REGION

Plena Deploys Bots to Efficiently Perform Everyday Tasks

D“Deploy the bots!” sounds like the dramatic high point to a summer blockbuster, but here in the real world of big business operations the notion of hiring robots can be a lot more surprising than any Hollywood script.

Bots already are performing many essential tasks in the life of the average American, but all we see are the results — curated content on a web page, chat conversation made to mimic human mannerisms, or moment-to-moment health moni toring — usually without a blink of consideration for how the job got done.

How did the job get done?

Jason Cook, vice president of sales for Plena.io, said in many cases the bots they deploy, and others like them, can get the job completed 90% faster than a human worker.

“Bots don’t quit, they don’t get COVID, and they do their job,” Cook said.

What Is A Bot?

Bots aren’t for every job, but they do really well with repetitive tasks that humans often refer to as “mind-numbing,” tasks that are critical to the vitality of a business but tend to be put off, or divided up among several team members in what can be a rather error-prone, inefficient process.

One bot, programmed to complete a task through a series of interrelating algorithms, doesn’t get bored, distracted, or burnt out — they work 24/7 if needed. And they’re particularly helpful in highly regulated areas, because of how they relentlessly stay on task within strictly defined parameters.

“It’s a very difficult time to hire a staff accountant,” Plena Account Executive Ted Gundersen said. “A lot of CFOs are jumping in to do some nitty-gritty stuff, like bank reconciliation, accounts payable… that’s what we alleviate.

“As a human, I need to go to the bank or bank website, pull in all the payments, open property

44 | JULY / AUGUST 2022 EDITION

Service / Supply

management software and match up every trans action in both places,” he said. “We need to match this $1.05 against that $1.05. It’s thousands of clicks, and then report back. That’s hours sitting at a desk clicking over and over.”

Bots can perform manual tasks on a computer in the same way a human would, but with much more accuracy and speed. And the bots can work with any system because they login with a username and password just like a full time employee.

“In theory, robotic process automation can abate any manual process,” Gundersen said. “We focus on finance at Plena, but we can do stuff in HR, sales, operations. It’s a digital worker, the employee you don’t see… Some people think of it as an excel macro, but on steroids.”

The company has about 50 human employees with a centralized management team in Utah, and tech developers all over the place.

CEO Dave Aditya worked at Adobe before starting Plena in 2017. Cofounder and Chief Revenue Officer Jackson Ostler was driving to dental school when Aditya called and asked him to join the venture. Last year alone the company raised $10 million in venture capital.

The Plena bots, Cook said, in one year cost less than an employee with $50,000 in salary and benefits.

Many large organizations worldwide are employing bots, and the real estate space industry is one of the main verticals Plena.io is focused on.

“It’s not a matter of if real estate organizations will adopt this type of product; it’s a matter of when. If it’s not in six months, it will be in two years,” Cook said.

Plena already is working with big names like Vineyards Management, Colliers International, D.R. Horton, Stellar senior living, Roots Management, and Rangewater. MHV

MHINSIDER.COM | 45

Service / Supply

STRENGTH

NUMBERS

IN

If you’re not on MHVillage, the most active website for manufactured housing, you’re simply missing out! 25+ MILLION UNIQUE VISITORS ANNUALLY 1.5 MILLION PHONE & TEXT LEADS SENT TO ADVERTISERS $3+ BILLION TRANSACTION VALUE OF HOMES SOLD OR RENTED More Traffic. More Leads. More Sales (800) 397-2158 | MHVillage.com Already a Client? Contact Us for a Complimentary Marketing Review of Your Account.

Contact Austin, Libba & Seth today for your community financing needs at 800-309-5008 or clt@vmf.com HUBERT, NC MH COMMUNITY $4,750,000 Acquisition 163 Sites • NC BURTON, MI MH COMMUNITY $2,135,000 Refinance 101 Sites • MI Up to 85% LTV. Earn out Program. Up to 30 year Amortization. Offered In Select States. 1st lien priority required. Approximately 45-65 days to close. FLEXIBLE TERMS: Vanderbilt Mortgage and Finance, Inc., 500 Alcoa Trail, Maryville, TN 37804, 865-380-3000, NMLS #1561, (http: //www.nmlsconsumeraccess.org/), AZ Lic. #BK-0902616. Loans made or arranged pursuant to a California Finance Lenders Law License. All Loans Subject to Credit Approval VMF.com/CommercialLending A Berkshire Hathaway Company RECENT CLOSINGS We Finance Communities. CAPE CANAVERAL, FL MH COMMUNITY $1,350,000 Purchase 100 Sites • FL CASA GRANDE, AZ MH COMMUNITY $2,400,000 Purchase 112 Sites • AZ IOWA/OHIO/S. DAKOTA/TEXAS MH COMMUNITIES $24,787,500 Refinance 863 Sites • IA, OH, SD, TX WOODLAND, WA MH COMMUNITY $1,155,000 Refinance 23 Sites • WA

New Tech to Support Insurance Offerings

by Adarsh Rachmale

by Adarsh Rachmale

48 | JULY / AUGUST 2022 EDITION Service / Supply

DDuring the past few decades, the world has wit nessed technology advance at breathtaking speeds.

Look at the first Apple Macintosh computer from 1984, and then look at the newest iPhones in Amer ican’s pockets. An iPhone 13 has enough processing power to guide over 1 million Apollo spacecraft to the moon, simultaneously. Technology is advancing at an almost incomprehensible speed, and while it can be challenging to keep up, it’s facilitating innovation in every industry nationwide.

The manufactured housing industry is no different. Modern manufactured homes are full of smart tech nology to help homeowners save energy, time, and money. Lenders can take applications online and issue approvals in minutes. Home manufacturers engineer the home building process to keep quality high and prices low for American home buyers. Did you know that the amount of waste from the construction of a single section home can fit into one trash can? Com pare that to the typical site-built home, and you’ll »

MHINSIDER.COM | 49

Service / Supply

see how well engineered a manufactured home is. Just the concept alone, building a home in a factory on an assembly line, is more advanced than building a home on a building site, out in the elements. And though it may not be as glamorous as a new home rolling off the assembly line, property insurance has its share of technological advances as well.

The key components to a great insurance product are ease, simplicity, and value - all three of which can be improved with modern technology.

The Digital Application

With any financial product (insurance, lending, or otherwise), the hardest step for the consumers is the first step, the application. A financial appli cation is long, requires lots of information, asks for uncomfortable details, and when finished, offers no reward because there is still the very real possibility of denial. Though it cannot eliminate the negative aspects of the process completely, technology can help insurance companies alleviate much of the pain of the application process and keep home buyers happy during their new home purchase.

Have you ever seen a home buyer look at a paper insurance application? Their eyes get wide as they stare at endless boxes (usually not large enough for the answer), long questions, tiny print, and seem ingly hundreds of"initial here" and "sign here" boxes. Technology in the smart phone insurance application all but eliminates that initial negative experience. Conditional logic technology allows the application to ask for only the information it needs to make a decision based on that customer — this means no extraneous questions. The application also has fewer questions per page. Studies show that there is a do pamine release from the sense of completion every time a user moves to another page on an application, which keeps them happy and moving forward.

The digital application also allows for much easier follow up from the insurance company. If a customer took a paper application home and never finished it, no one would ever know, and no one would be able to check on the status of the incomplete paper application. In the case of digital application, how ever, follow up opportunities are endless. Because the application gives their contact information at

the onset, insurance companies can follow up with incomplete applications, and pro-actively reach out to the applicant to help them complete their application. According to a study by Brevet, it takes five follow ups with a customer before a sale is made. Technology allows the insurance companies to do this more effectively, thus allowing for more sales.

Technology in Underwriting

Once the applicant has submitted their application, underwriting begins. This is the process by which the insurance company determines the amount of risk in the policy, and how to price the premium to account for that risk. Traditionally, this is very labor-intensive process that involves looking at various actuarial tables, going back and forth with the customer, performing many calculations, submitting data to supervisors, and finally submitting a decision to the applicant. This process can take anywhere from a few days to many weeks. Because of the length of underwriting, many customers are lost, either to other companies or they simply lose interest and move on.