REALTOR September 2022 Salt Lake Magazine® Utah No. 2 in New Housing Units p. 10

David

Weekley Homeowners Martha, Chad, Parker & Hutchinson Cates Ask about our limited-time incentives!

When it comes to selling homes, your name matters. That’s why we stake our reputation on helping you enhance yours. That’s The Weekley Way. See a David Weekley Homes Sales Consultant for details. Prices, plans, dimensions, features, specifications, materials, and availability of homes or communities are subject to change without notice or obligation. Illustrations are artist’s depictions only and may differ from completed improvements. Copyright © 2022 David Weekley Homes - All Rights Reserved. Salt Lake City, UT Homes(SLC-22-002741)from the high $500s to $1 million+ in the Salt Lake City area 385-799-3053

HOMEMANUFACTUREDLOANS Turning Houses into Homes® This is not a commitment to make a loan. Loans are subject to borrower and property qualifications. Contact loan originator listed for an accurate, personalized quote. Interest rates and program guidelines are subject to change without notice. WWW.SNMC.COM We’re creating home loans for even more types of homes! Single-wide manufactured homes are now eligible for Conforming, FHA, and VA loan programs.

Favors Buyers

10 These States Have Seen the Largest Growth in Housing

Melissa Dittmann Tracey FSBOs Usually Soar in a Hot Market. Not This Time

Melissa Dittmann Tracey Maximinze Seller Profits when the Market

Melissa Dittmann Tracey Realtor® Family Helps a Friend in Need New-Home Sales Plummet, but Completed Homes Find Buyers within Three Months

Rory S. Coakley 94% of Sellers Don’t Disclose Property Defects

20

More than Home Prices

Salt L ake REALTOR® Magazineslrealtors.com The Salt Lake REALTOR® (ISSN 2153 2141) is published monthly by Mills Publishing, located at 772 E. 3300 South, Suite 200 Salt Lake City, Utah 84106. Periodicals Postage Paid at Salt Lake City, UT. POSTMASTER: Send address changes to: The Salt Lake REALTOR,® 772 E. 3300 South, Suite 200 Salt Lake City, Utah 84106-4618. September 2022 volume 82 number 9

Melissa Dittmann Tracey

26

Table of slrealtors.comContents

14 Economist: Mortgage Rates Hurt Buyers

7 The

30

24

Stessa Team

16

Features

Columns Amazing Generosity

of Realtors®

Steve Perry – President’s Message

Salt Lake Realtor® Magazine is self-supporting. The advertisers in this magazine pay for all production and distribution costs. Help support this magazine by advertising. For advertising rates, please contact Mills Publishing at 801.467.9419. The paper used in Salt Lake Realtor Magazine comes from trees in managed timberlands. These trees are planted and grown specifically to make paper and do not come from parks or wilderness areas. In addition, a portion of this magazine is printed from recycled paper.

Departments 8 Happenings 8 In the News 28 Housing Watch 4 | Salt Lake Realtor ® | September 2022 Correction: Cowboy Partners, one of this year’s Salt Lake Parade of Homes builders, was incorrectly identified as Cowboy & Partners in the July issue. On the Cover: Cover Photo: Rebecca ©/Adobe Stock 24 FSBOs Usually Soar in a Hot Market. Not This Time 20 94% of Sellers Don’t Disclose Property Defects Stock©/AdobeEdwardsMdvStock©/Adobeand.one

This Magazine is Self-Supporting

KANAB GOLDMARK JOIN TODAY: M. Casey Jones, Broker (801) 671.6158 | JoinTheUNBrokerage.com Each franchise independently owned and operated. (801) 209.6654 ROG SIGNATURE (435) 724.4953 ROG SIGNATURE (801) 671.6158 ROG GOLDMARK (435) 602.4141 ROG GOLDMARK (801) 633.1990 ROG SIGNATURE (801) 703.6553 ROG SIGNATURE (801) 671.6158 ROG GOLDMARKROG GOLDMARK (435) 602.4141 NowOpen MIDVALE | DRAPER | VERNAL | PARK CITY | KANAB | FARMINGTON | ST.GEORGE | CEDAR CITY ONLY A FEW REMAINING LOCATIONS AVAILABLE IN UTAH If you’ve ever considered owning and running your own successful real estate brokerage with the support of a local expert and international powerhouse, we invite you to see what ONE can do for you. ONE Utah Regional Developer (801) 633.1990

•

•

• MA:

1. FastTrack Get a clear to close in as fast as 24 hours,2 and to the closing table in as fast as 10 days.3 Can a bank do that? 2. PowerBid Approval Give your buyers the power to compete with cash offers with our fully underwritten credit approval.4 3. Lock ‘N’ Roll Ease your buyers’ minds with a rate lock up to 90 days, with no commitment to buy.5 4. FlashClose+ eClose Like speed? Your buyers can close digitally from anywhere, at any time—in minutes, not hours.6 5. Over 100,000 top Real Estate agents choose Guaranteed Rate When you consistently deliver the best people, the best tools and the best advice, naturally the best in the biz want to work with you. The best real estate agents know to partner with the best experts—the ones who can help their clients close, and close fast. Every week, we help thousands of people buy a home. Over $20 billion worth so far this year.1 5 reasons your clients deserve the Frustratedbest:buyers? Now more than ever, you need to work with the best. 1. Source: Guaranteed Rate Internal Production Report, January-August 2022. 2. The Guaranteed Rate FastTrack provides that eligible borrowers will receive a “Clear to Close Loan Commitment” (“CTC”) within twenty-four business hours from Guaranteed Rate’s receipt of all necessary borrower documentation. Guaranteed Rate reserves the right to revoke this “CTC” at any time if there is a change in your financial condition or credit history which would impair your ability to repay this obligation. CTC is subject to certain underwriting conditions, including clear title and no loss of appraisal waiver, amongst others. Read and understand your Loan Commitment before waiving any mortgage contingencies. Borrower documentation and Intent to Proceed must be signed within twenty-four business hours of receipt. Not eligible for all loan types or residence types. Fixed rate conventional loans on single family residences only with at least 20% down payment. Eligible for primary and second homes. Property must be eligible for an Appraisal Waiver and borrower must opt in to AccountChek for automated income and asset verification. Self-employed borrowers and Co-borrowers are not eligible. Not all borrowers will be approved. Borrower’s interest rate will depend upon the specific characteristics of borrower’s loan transaction, credit profile and other criteria. Offer not available from any d/b/a or operations that do not operate under the Guaranteed Rate name. $250 Closing Cost Credit is available from 5/1/22 through 11:59 PM, 12/31/22 and is applied at closing, no cash value. Not available in New York, West Virginia, Kentucky, or Texas. Restrictions apply. Contact Guaranteed Rate for more information.

4. PowerBid Approval (the “Approval”) is contingent upon receipt of executed sales contract, an acceptable appraisal supporting value, valid hazard insurance policy, and a re-review of your financial condition. Guaranteed Rate, Inc. reserves the right to revoke this Approval at any time if there is a change in your financial condition or credit history which would impair your ability to repay this obligation and/or if any information contained your application is untrue, incomplete or inaccurate. Receipt of an application does not represent an approval for financing or interest rate guarantee. Not all applicants will be approved for financing. Restrictions may apply, contact Guaranteed Rate for current rates and for more information.

3. Guaranteed Rate cannot guarantee that an applicant will be approved or that a closing can occur within a specific timeframe. All dates are estimates and will vary based on all involved parties level of participation at any stage of the loan process. Contact Guaranteed Rate for more information.

Mortgage Broker License #MC2611 • ME: Supervised Lender License #SLM11302 • MS: 3940 N. Ravenswood Ave., Chicago, IL 60613 • NH: Licensed by the New Hampshire Banking Department, Lic #13931-MB • NJ: 3940 N Ravenswood, Chicago, IL 60613, (866)- 934-7283, Licensed by the N.J. Department of Banking and Insurance • NY: Licensed Mortgage Banker - NYS Department of Financial Services • OH: MB 804160, 3940 N. Ravenswood Ave., Chicago, IL 60613 • OR: 3940 N. Ravenswood Ave., Chicago, IL 60613 • RI: Rhode Island Licensed Lender • TX: 3940 N Ravenswood, Chicago, IL 60613, (866)-934-7283 • WA: Consumer Loan Company License CL-2611. (20220809-1173946) DANIELLE YOUNG Branch Manager, SVP of Mortgage Lending O: (801) 890-7656 C: (801) 205-0821 Danielle.Young@rate.com Why settle for less? Get your clients home with the best. call Danielle Young at (801) 890-7656.

Mortgage

•

(20220809-1173946)Guaranteed

6. Not eligible for all loan types, or investors. Conventional loans only. Eligible for primary, 2nd home and investment properties. Title company restrictions may apply, not eligible for HFA programs. Knowledge-Base Authentication (KBA) required in order to enter the digital signing session. Applicant subject to credit and underwriting approval. Full eClose is not currently eligible in California, Connecticut, Delaware, Georgia, Maine, Massachusetts, Mississippi, New York, North Carolina, Rhode Island, South Carolina, Vermont, and West Virginia. Rate, Inc.; NMLS #2611; For licensing information visit nmlsconsumeraccess.org. Conditions may apply • AR: 3940 N Ravenswood, Chicago, IL 60613, (866)-934-7283 • AZ: 14811 N. Kierland Blvd., Ste. 100, Scottsdale, AZ, 85254, Banker License #0907078 CA: Licensed by the Department of Business Oversight under the California Residential Mortgage Lending Act CO: Regulated by the Division of Real Estate, (866)-934-7283 GA: Residential Mortgage Licensee #20973 Mortgage Lender &

5. Additional fees may apply.

of the many sponsors and participants helped to raise $60,000 in a single day for Gavin. Gavin is the Salt Lake Board of Realtor’s events director. Going forward, the charity committee plans on hosting an annual event to help someone in need. The golf event reminded me again of the kindness of the Realtor® family. Realtors® are simply some of the most giving people.

will be granted in most cases, upon written request, to reprint or reproduce articles and photographs in this issue, provided proper credit

The

Last month, more than 200 Realtors®, affiliates, and friends gathered at a Golf to Give event to support Gavin Krushensky, who was involved in a UTV accident in September 2021 and suffered a C4 spinal cord injury that left him paralyzed from the chest

The

Views and opinions expressed in the editorial and advertising content of the The Salt Lake REALTOR are not necessarily endorsed by the Salt Lake Board of REALTORS . However, advertisers do make publication of this magazine possible, so consideration of products and services listed is greatly appreciated.

In recent years, the Salt Lake Board of Realtors® through its Charity Committee has given countless hours of service and tens of thousands of dollars to organizations like Christmas Box International, The Road Home, Habitat for Humanity, the Utah Food Bank, and Tools for Schools.

September 2022 | Salt Lake Realtor ® | 7

In 2022, a total of $120,000 (24 grants) will be awarded. These grants have helped single parents, first responders, school district employees, veterans/military personnel, and others in achieving the dream of homeownership. Funds for the American Dream Grants come from three sources: direct donations from Realtors®, a portion of the Realtor® license plate fee, and interest from the trust accounts of participating real estate brokerages.

The Amazing Generosity of Realtors®

This fund continues to help Americans affected by disasters. On average, RRF has disbursed roughly $1.7 million annually in housing-related assistance for disaster victims. However, at the start of 2022, $3,735,000 was awarded to five disasters, illustrating the differences year to year. There are so many ways to give and so many deserving people and causes. I am continually amazed by the giving spirit of Realtors®. Thank you for making a difference in the lives of so many people.

Salt Lake REALTOR is the monthly magazine of the Salt Lake Board of REALTORS . Opinions expressed by writers and persons quoted in articles are their own and do not necessarily reflect positions of the Salt Lake Board of REALTORS®

Thedown.generosity

October 2005 OFFICIAL PUBLICATION OF THE SALT LAKE BOARD OF REALTORS ® REALTOR is a registered mark which identifies a professional in real estate who subscribes to a strict Code of Ethics as a member of the NATIONAL ASSOCIATION OF REALTORS Graphic Design Ken CynthiaOfficePatrickMaglebyWitmerAdministratorBellSnow Sales PaulPaulaStaffBellNicholas Managing Editor DavePublisherAnderton Mills Publishing, www.millspub.comInc.PresidentDanMillerArtDirectorJackieMedina Advertising information may be obtained by calling (801) 467-9419 or by visiting www.millspub.com Salt Lake Board: (801) 542-8840 e-mail: dave@saltlakeboard.com Web Site: www.slrealtors.com Salt L ake REALTOR® Magazineslrealtors.com SecondFirstPresidioPresidentStevePerryRealEstateVicePresidentRobOckeyCentury21EverestVicePresidentDawnStevensPresidioRealEstateTreasurerClaireLarsonWoodsideHomesPastPresidentMattUlrichUlrichRealtors ® BerkshireJenniCurtisCEOBullockDirectorsBarberHathaway Morelza SignatureUtahJenniferSummitHannahRealtyPathBoratzukCutlerColdwellBankerLauraFidlerSotheby’sAmyGibbonsKellerWilliamsGilchristKeyRealEstateTonyKetterlingEquityRealEstateJohnLuckyBerkshireHathawayJodieOsofskyRealEstateUtahJaniceSmithColdwellBankerCarlyeWebbSummitSotheby’s

Steve PresidentPerry

On a national level, Realtors® have stood in solidarity with fellow Americans since the Sept. 11thterrorist attacks. More than $8.4 million poured in to provide urgent housing-related assistance for those struggling in the aftermath. Funds were raised and distributed within 100 days to ensure families remained in their homes. From that, the Realtors® Relief Fund was born.

Salt Lake Board of REALTORS® is pledged to the letter and spirit of U.S. policy for the achievement of equal housing opportunity throughout the nation. We encourage and support the affirmative advertising and marketing program in which there are no barriers to obtaining housing because of race, color, religion, sex, handicap, familial status, or national origin.

Permission is given to The Salt Lake REALTOR as well as to any writers and photographers whose names appear with the articles and photographs. While unsolicited original manuscripts and photographs related to the real estate profession are welcome, no payment is made for their use in the publication.

Over the past four years, the Board has given American Dream Grants to first-time homebuyers to help with the down payment of a home. From 2019 through 2021, the Charity Committee awarded 20 first-time homebuyers $5,000 each in American Dream Grants.

The Salt Lake Board of Realtors® held its annual business meeting on Aug. 24. Dejan Eskic, a senior research fellow at the Kem C. Gardner Policy Institute and the Board’s chief economist, was a featured speaker at the event. Eskic said that Utah’s housing shortage has improved in recent years, with more than 40,000 residential permits authorized in 2021, far exceeding the 26,698 households formed the same year. There are economic headwinds ahead, Eskic said. The rise in mortgage interest rates has sidelined many buyers, who either no longer qualify for a mortgage or are waiting to see if rates improve. Eskic said he sees a market correction coming, not a crash. Household finances remain strong with high savings, low debt service, and the Utah economy has ample jobs. Pictured: Brad Bjelke, CEO of UtahRealEstate.com; DeAnna Robbins, 2011 president of the Salt Lake Board of Realtors®, and Dejan Eskic, chief economist of the Salt Lake Board of Realtors®.

Steve Perry, president of the Salt Lake Board of Realtors®, was recently interviewed by KUTV 2 News, a CBS affiliate in Salt Lake City, on rising mortgage interest rates. “Unfortunately, the Federal Reserve’s effort to curb inflation is having a negative impact on home buyers, who are backing out of deals or don’t qualify for financing because of higher interest rates,” Perry said. “The higher rates led to an 11-year low in home sales in July in Salt Lake County.” Mortgage rates in the last week in August averaged 5.66% for a 30-year fixedrate mortgage, according to Freddie Mac. “The market’s renewed perception of a more aggressive monetary policy stance has driven mortgage rates up to almost double what they were a year ago,” said Sam Khater, Freddie Mac’s Chief Economist. “The increase in mortgage rates is coming at a particularly vulnerable time for the housing market as sellers are recalibrating their pricing due to lower purchase demand, likely resulting in continued price growth deceleration.”

8 | Salt Lake Realtor ® | September 2022

Housing Correction, not a Crash

Two Realtors® Elected to Board of Directors

Dawn Stevens

Angelina Pena, middle, broker and co-owner of Exit Realty Legacy Sugarhouse and St. George, was winner of a 2022 Honda Accord Hybrid in this year’s dues giveaway! Angelina’s $100 RPAC investment paid off big! RPAC investments are not part of members’ dues; this is money given freely by Realtors® in recognition of the importance of the political process.

Scott Colemere and Dawn Stevens were the winners of two open seats on the Board of Directors of the Salt Lake Board of Realtors®. They will begin their new terms Jan. 1, 2023. Scott previously served as director from 20152018. Colemere is the managing broker of Sandy-based Colemere Realty, which has 13 agents. Dawn is broker of Sandy-based Presidio Canyons Luxury Real Estate which has 25 agents. She has served as a director since 2019. Dawn is the National Association of Realtors’® C2Ex (Commitment to Excellence) ambassador for Utah. The C2Ex is an endorsement given by NAR.

Happenings In the News

Scott Colemere

wantWetobeyourcashcow Red Hills Pkwy Southern Pkwy Bingham Rd Virgin River St. George Blvd Dixie Dr St. RegionalAirportGeorge SnowStateCanyonPark NationalZionParkCapitolNationalReefPark Cedar City Regional Airport WASHINGTON HURRICANE CEDAR CITY ST. GEORGE 21 20 17 1918 56 9 14 7 CreekQuailHollowSand D.R. Horton is an Equal Housing Opportunity builder. Map is an artist’s conception only. Map is not to scale. Home and community information, including pricing, included features, terms, availability and amenities, are subject to change at any time without notice or obligation. See sales agent for complete details. This message is an advertisement or solicitation by D.R. Horton for a planned future community. Some communities may still be in the acquisition and development process, and D.R. Horton may elect to delay or cancel their opening for any reason at any time without notice or obligation. © Copyright 2022 D.R. Horton, Inc. 09/2022 20+ NEW HOME COMMUNITIES WAITING FOR YOUR BUYERS NORTHERN COMMUNITIES SYRACUSE 1 CRIDDLE FARMS Single Family MAGNA 2 LITTLE VALLEY GATEWAY Single Family & Townhomes GRANTSVILLE 3 SUN SAGE MEADOWS/TERRACE Single Family & Townhomes 4 GRANTSVILLE ESTATES Single Family TOOELE 5 WESTERN ACRES - COMING SOON Townhomes LEHI 6 SKYE - COMING SOON Single Family, Townhomes & Active Adult 7 COLD SPRING RANCH Single Family & Townhomes SARATOGA SPRINGS 8 NORTHSHORE Single Family & Townhomes AMERICAN FORK 9 EDGEWATER AT AMERICAN FORK Townhomes EAGLE MOUNTAIN 10 EAGLE POINT TOWNHOMES Townhomes PROVO 11 OSPREY TOWNHOMES Townhomes MAPLETON 12 MAPLETON GROVE Single Family SPANISH FORK 13 HAYMAKER Single Family 14 QUIET VALLEY - COMING SOON Single Family & Townhomes SANTAQUIN 15 FOOTHILL VILLAGE Single Family 16 SUMMIT RIDGE TOWNS Townhomes SOUTHERN COMMUNITIES CEDAR CITY 17 NORTH FIELD TOWNHOMES Townhomes 18 OLD SORREL RANCH Single Family 19 OLD SORREL TOWNHOMES Townhomes WASHINGTON 20 LONG VALLEY TRAILS - COMING SOON Single Family & Townhomes ST. GEORGE 21 DESERT COLOR Single MasterFamilyplanned community SANTAQUIN SYRACUSE SPANISHMAPLETONFORK LEHI EAGLE MOUNTAIN TOOELE MAGNA SALT LAKE CITY GRANTSVILLE SARATOGA SPRINGS AMERICAN FORK 3 4 5 8 9 11 10 1213 14 1516 1 7 6 2 84 36 Utah Lake Great Salt Lake

10 | Salt Lake Realtor ® | September 2022

One reason for the shortage in supply is significant underinvestment in new housing since the housing bubble burst in the mid-2000s. Seasonally adjusted spending on residential construction peaked above $1 trillion in inflation-adjusted dollars early in 2006, but the bottom fell out of the housing market shortly after, and spending plummeted by more than two-thirds as the Great Recession took hold. In the ensuing recovery, residential construction spending was slow to rebound

years. But the increase in demand only exacerbated larger challenges with housing supply that predated the pandemic. According to a 2021 report from federal mortgage backer Freddie Mac, the U.S. is short nearly 4 million housing units based on the country’s population and housing needs.

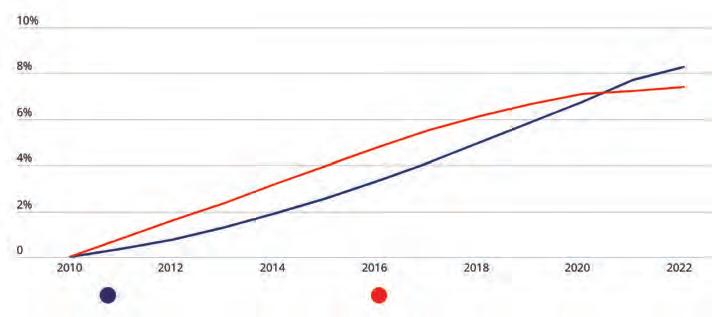

Utah ranked No. 2 in the percentage change of new housing units from 2010-2020.

The state of the U.S. housing market has been one of the dominant economic stories since the start of the COVID-19 pandemic. The market saw unprecedented price growth over the last two years, and rapidly rising housing costs have been one of the major contributing factors in the historic run of inflation experienced in the U.S. economy over the last year. Now, with interest rates rising and low- and middle-income households increasingly priced out of the market, a slowdown in the housing market could portend a recession later this year or in 2023.

Record low interest rates, strong savings rates and wage growth, and shifting consumer preferences for housing were among the conditions that spurred high demand for residential real estate over the last two

By Stessa Team

These States Have Seen the Largest Growth in Housing

Between 2010 and 2020, constructionnewgrowthpopulationoutpacedresidential Source: U.S. Census Bureau’s Current Population Survery/Housing Vacancy Survey Percentage change from 2010 Housing units (percentage change) Population (percentage change)

skip ©/Adobe Stock

but grew gradually from 2012 to 2018, before falling again amid interest rate hikes. It was not until the recent housing frenzy that residential construction began to accelerate. Spending has increased by more than 33% since the pandemic began in March 2020, and today residential construction spending is approaching peaks last seen in the housing bubble.

September 2022 | Salt Lake Realtor ® | 11

And during this period of slow growth in housing, the U.S. continued to grow in population. From 2010 to 2020, the U.S. added residents at a faster rate than it added housing units, leaving a larger number of people to compete for a limited amount of housing stock. But in 2021 and 2022, the percent change in housing units since 2010 has topped the growth in population, which

Rank State Percentage change in housing (2010-2020)units Total change in housing (2010-2020)units Total housing units (2020) Total housing units (2010) Percentage change in (2010-2020)population Percentage of housing units that are owner occupied (2020) 1North Dakota+20.4% +63,736

10

in this analysis is from the U.S. Census Bureau’s American Community Survey (2020). To determine the locations that have seen the largest

12 | Salt Lake Realtor ® | September 2022

growth in housing over the last decade, researchers at Stessa calculated the percentage change in housing units from 2010 to 2020. In the event of a tie, the location with the greater total change in housing units was ranked higher.

4Idaho

At the metro level, several fast-growing cities are rapidly adding housing stock to meet growing demand. Booming metros like Nashville, Austin, and Charlotte are among the top U.S. cities for housing growth over the last decade as they contend with an influx of new Theresidents.dataused

3 Texas +14.3% +1,394,505

could bring some relief to the market’s recent supply challenges soon.

But despite recent encouraging signs in housing investment, much of the country must catch up to meet the overall need for housing. From 2010 to 2020, 20 states added population at a faster rate than they added housing, a fact that was true even among most of the states that added housing the fastest. Of the top 10 states for housing growth over the last decade, only North Dakota, South Dakota, and Delaware added housing faster than they added residents.

6Nevada

The data used in this analysis is from the U.S. Census Bureau’s American Community Survey (2020). To determine the locations that have seen the largest growth in housing over the last decade, researchers at Stessa calculated the percentage change in housing units from 2010 to 2020. In the event of a tie, the location with the greater total change in housing units was ranked higher. To improve relevance, only metropolitan areas with at least 100,000 residents were included. Additionally, metros were grouped into cohorts based on population size: small (100,000 to 349,999), midsize (350,000 to 999,999), and large (1,000,000 or more). *Stessa is a financial technology company, not a bank. Banking services are provided by Blue Ridge Bank, N.A., member FDIC. 376,597 312,861 +15.2% 62.5% 1,110,369 952,370 +18.6% 70.5% 11,112,975 9,718,470 +17.8% 62.3% +13.0% +85,088 737,411 652,323 +14.9% 70.8% +11.3% +320,842 3,150,194 2,829,352 +14.5% 63.3% +11.2% +127,978 1,268,533 1,140,555 +15.1% 57.1% Carolina +11.1% +230,951 2,319,112 2,088,161 +12.9% 70.1% Dakota+10.9% +39,092 396,817 357,725 +10.0% 68.0% Carolina +10.8% +457,570 4,687,122 4,229,552 +12.0% 65.7% Delaware +9.9% +39,572 438,438 398,866 +9.8% 71.4%

2Utah +16.6% +157,999

Below are the 10 states that have seen the largest growth in housing over the last decade.

8South

7South

9North

SeanPavonePhoto ©/Adobe Stock

5Washington

It's our highest honor to provide our affiliated agents and brokers the resources that they use to achieve their most ambitious goals. Tools and programs that grow and strengthen their businesses. A culture of success and positivity that empowers and unites. And a commitment to industry leadership that's remained steadfast for over a century.

BRINGING THE POWER OF COLDWELL BANKER TO another utah community ESTATE BRAND THAT SHINES LIKE NO OTHER.

©2022 Coldwell Banker. All Rights Reserved. Coldwell Banker and the Coldwell Banker logos are trademarks of Coldwell Banker Real Estate LLC. The Coldwell Banker® System is comprised of company owned offices which are owned by a subsidiary of Anywhere Advisors LLC and franchised offices which are independently owned and operated. The Coldwell Banker System fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Coldwell Banker Realty 323 S 100 E | Kanab, UT 84741

kanabTHE REAL

The Coldwell Banker Brand is home to affiliated agents and brokers with drive and vision, talent and compassion. They work every day to redefine the standards of what it means to serve their clients and guide them to the homes of their dreams. They create successful and fulfilling lives for themselves and their families with the strength and support of the Coldwell Banker brand. That's the power of the Coldwell Banker Way.

Mortgage rates were back on the rise this week, hitting an average of 5.55%, Freddie Mac reported in August. Rates are nearly double what they were a year ago, and the latest housing data from the National Association of Realtors® demonstrates the impact of the jump in borrowing costs.

14 | Salt Lake Realtor ® | September 2022

Further, “apart from rising mortgage rates, home prices continue to show double-digit year-over-year gains,”

plummeted 20% year over year in July, according to NAR data. Contract signings also dropped 20% in the same month. And there’s been a significant pullback in the new-home market—sales in the sector were down 30% annually in July—causing homebuilder sentiment to slide for the eighth straight month.

By Melissa Dittmann Tracey

Creativa Images ©/Adobe Stock

Economist: Mortgage Rates Hurt Buyers More Than Home Prices

As the average for a 30-year loan rises again, higher borrowing costs have triple the impact on monthly mortgage payments.

The nation is witnessing a “housing recession,” said NAR Chief Economist Lawrence Yun, as existing-home sales

Homes haven’t been this unaffordable since 1989, NAR reports. Rising mortgage rates have made home loans more expensive, adding to the cost of homeownership. The typical monthly mortgage payment was nearly $2,000 in June, up 54%—or $679—compared to a year ago. “The combination of higher mortgage rates and the slowdown in economic growth is weighing on the housing market,” said Sam Khater, Freddie Mac’s chief economist. “Home sales continue to decline, prices are moderating, and consumer confidence is low. But amid waning demand, there are still potential home buyers on the sidelines waiting to jump back into the market.”

SPEAKER Wednesday, Sept. 21st 9:30 a.m. - 12 p.m. Join us learn how to elevate your business with the following CE classes taught by Truly’s CMO, Brian Nachlas. Megaplex Theatres at Jordan Commons 9335 State St. | Sandy, UT 84070 Breakfast will be provided. Sponsored by Chad at IBex Creating Brand Dominance in Real Estate R220817 | 1 Hour Elective CE Mastering Google: Rank at the Top of the Search R220818 | 1 Hour Elective CE Limited seating saleadmin@trulytitle.comRSVPavailable.todayto 6965 S Union Park Center, STE 180 | Cottonwood Heights, UT 84047 (801) 996-7456

Nadia Evangelou, NAR’s senior economist and director of forecasting, said. A median-priced home is worth about $40,000 more than a year earlier. While home price increases add to home buyers’ costs, the impact of higher mortgage rates is much more—triple the impact on a monthly mortgage payment, Evangelou noted. An increase of just one percentage point in mortgage rates has the same effect on mortgage payments as if home prices rose by 13 percentage points.

September 2022 | Salt Lake Realtor ® | 15

MASTERMARKETINGSERIES

5-year hybrid adjustable-rate mortgages: averaged 4.36%, with an average 0.4 point, dropping from last week’s 4.39% average. A year ago, 5-year ARMs averaged 2.42%.

Reprinted from Realtor® Magazine Online, August 2022, with permission of the National Association of Realtors®. Copyright 2022. All rights reserved.

Freddie Mac reports commitment rates along with average points to better reflect the total upfront cost of obtaining a mortgage.

Freddie Mac reports the following national averages with mortgage rates for the week ending Aug. 25: 30-year fixed-rate mortgages: averaged 5.55%, with an average 0.8 point, up from last week’s 5.13% average.

The typical monthly mortgage payment was nearly $2,000 in June, up 54%—or $679— compared to a year ago.

Brian Nachlas Chief Marketing Officer Truly Title

Last year at this time, 30-year rates averaged 2.87%.

15-year fixed-rate mortgages: averaged 4.85%, with an average 0.8 point, up from last week’s 4.55% average. A year ago, 15-year rates averaged 2.17%.

16 | Salt Lake Realtor ® | September 2022

Even though high inflation and rising interest rates are beginning to dampen homebuyer demand, we’re still in a seller’s market. There still isn’t enough inventory to meet the demand that’s out there, so your sellers continue to have some advantages in the market. Use these guidelines to help make the selling process easier, faster, and more profitable.

By Rory S. Coakley

Monitor comp sales like a hawk. Buyers and their agents are more informed than ever about what houses are selling for in the neighborhoods they’re considering. But with the market changing as rapidly as it is, you can be the first to inform them of the monthto-month or week-to-week shifts in your area. You’ll have to keep a close eye on recent sales of comparable homes and commit to frequent communication with buyers interested in your listing. Preparing a CMA and

Lightfield Studios ©/Adobe Stock

Avoid price gimmicks. Helping your seller set a reasonable list price goes hand-in-hand with your

Use these approaches to market research and pricing to ensure your listing doesn’t linger on the market.

Maximize Seller Profits When the Market Favors Buyers

Get the house market ready. Another example of how you, as an experienced agent, can help a seller is the input you can give regarding market preparation. I recently sold a home in Bethesda, Md., that received multiple offers. Before I listed it, I suggested the owners make simple cosmetic upgrades by adding fresh paint and refinishing the floors. Although these changes cost little in the grand scheme of the transaction, they may have been the most appealing characteristic of the home for the eventual buyers, who expressed appreciation that they “didn’t have to do anything before moving in.”

distributing it to potential buyers will show your listing’s value.

Make Buyers HAPPY! -APRs up to .997% LOWER! $500,000 Apples-To-Apples Lender Comparison on 9/1/2022 LendRightMortgage A Top BrokerUtah Large Utah UnionCredit A PremierLenderDirect LargeLenderNational Rate 5.250% 5.625% 5.875% 5.990% 5.990% APR 5.281% 5.670% 5.920% 6.025% 6.278% Lender Fees & Points $1,125 $2,020 $4,345 $1,374 $10,625 P&I Payment $2,761 $2,878 $2,958 $2,995 $2,995 Buyers Save Up To: $234 every month $2,808 every year $84,240 Life of Loan Interest Savings LendRight’s lower rates mean larger qualifying loan amounts & higher max purchase prices. -Get the LOWEST price, or get a $100 Amazon gift card*. Lendrightmortgage.com Variables for all quotes: $500,000 purchase loan, SFR, primary residence, 60% LTV, 760+ FICO, 30 YR fixed rate conventional loan on 30 day lock. All quotes obtained on 9/1/2022. *Gift card terms/conditions: 1. Provide detailed quote from any lender showing better same day pricing. 2 Lock rate and provide the locked loan estimate within three days 3. Provide signed CD from closing that matches the locked LE. Offer valid only on matching Conventional, FHA, VA, USDA loans with lock periods of 90 days or less. NMLS 1817019 Make Buyers Happy! -APRs up to .997% LOWER! -Up to $9,500 Less Closing Costs

It’s a good idea to remind your client that the best contract isn’t necessarily dependent on the amount of the offer. What if there are contingencies that the seller views as unfavorable? As buyers regain some advantage in the market, prepare sellers that they may have to sacrifice a little more than they would have just last year. However, a stubborn buyer who refuses to give and take could be a red flag that you’ll find a better offer somewhere else. Also, be on the lookout for incomplete or sloppy contracts, which indicate carelessness on the side of the buyer’s agent and could be a red flag that he or she will be difficult to work with moving forward.

By adhering to the guidelines listed above, whether providing help in monitoring, pricing, reviewing contracts or choosing the right offer, you are providing sellers expertise worth the investment in your services.

Alternatively, another common pricing strategy is to list for a slightly higher amount than the most recent comparable sale. With home prices appreciating quickly, this could make sense—but it also could backfire. Even in today’s competitive market, an overpriced house can alienate buyers, resulting in the house languishing unsold until the price drops. As an experienced agent, you can present an objective view based on market activity to figure out a fair and competitive asking price prior to listing to set your client on a path for success when the home goes to market.

Choose the right offer. Other questions to ask as you’re reviewing offers: Is there an escalation clause? What type of financing is the buyer using? Who are the buyer’s lender and settlement agent, and are they local? Does the proposed settlement date work for the seller? All these issues need to be weighed before your seller accepts an offer.

18 | Salt Lake Realtor ® | September 2022

While the inflation rate continued to rise in July, mortgage rates began to come down. You have to constantly monitor these economic factors while keeping a close eye on what’s actually happening in your own market to determine the best pricing strategy. Both approaches are reliable but need to be determined based on each individual market. Pricing isn’t an exact science nor a matter of quantitative analysis. There are numerous variables that need to be considered outside of just numbers. How fast do the sellers need to move?

A contingent-free, all-cash offer with a settlement date that fits the seller’s schedule is about as strong an offer as you will see. The fewer contingencies there are, the better the deal is for the seller. A strong financial position for the buyer is needed as well, shown by a large down payment and earnest money deposit, a prequalifying letter from a local lender, and personal financial information showing the buyer has the funds necessary for closing. The seller accepted an offer that was contingent-free and settled quickly, a positive for the seller.

bmak ©/Adobe Stock

role in monitoring comp sales. One strategy sellers sometimes gravitate toward is pricing their home just a little below the amount of the most recent comparable sale. The intention is to spark a bidding war. But as the market shifts slowly in buyers’ favor, there’s a risk to this: You may not generate as many offers as you anticipated, and if a high offer falls through, that gives other bidders more negotiation leverage.

I recently had a listing that received 23 offers, and buyer’s agents are entitled to an answer within 24 hours—so that’s a lot to sift through in a short amount of time. The process includes an offer presentation sheet showing all terms for each party, including price, contingencies, time frames and other factors. It enables sellers to see the merits of each offer side by side. The contract the sellers ended up accepting was clearly the strongest, but it took hours of review to determine which proposal was the best for the seller.

Reprinted from Realtor® Magazine Online, August 2022, with permission of the National Association of Realtors®. Copyright 2022. All rights reserved.

Be vigilant when reviewing contracts. The average sale contract is 60 pages long. It can be overwhelming for a seller to try and understand. Now imagine, as an inexperienced seller, being in a bidding war and having many contracts from multiple bidders to consider. Sellers need you to help them discern the contracts that most closely meet their needs.

How long have they owned the house? How strong is their emotional attachment to the house? How willing are they to make any repairs?

PICK YOUR PROMO!* Personalizing your home is the fun part. Let’s personalize your promotion too! Woodside Homes—keeping it personal •Up to 3% of Purchase Price towards closing costs, pre-paids, and/or Rate Buydown •Buydown rates starting from 3.875%** •TO BE BUILT HOMES—Up to 3% of Purchase Price towards closing costs, pre-paids, and/or Rate Buydown**, PLUS half off lot premium, and/or options and upgrades UP TO $15,000 Contract must be written between 9/1/22 12/31/22. Bonus to be paid at closing •1st Transaction—$3,000 bonus in addition to typical Woodside commission •2nd Transaction—$6,000 bonus in addition to typical Woodside commission •3rd Transaction—$9,000 bonus in addition to typical Woodside commission •4th Transaction—$12,000 bonus in addition to typical Woodside commission **Must use one of Sellers preferred lenders for financing. Only applicable on contracts written between 9/1/2022 9/30/2022 *This offer is subject to change without notice and may not be combined with other promotions or discounts. Must use one of seller’s preferred lenders. Woodside Homes and its preferred lenders are not affiliated and have no shared ownership. All applications are subject to credit and underwriting approval and receipt of an application does not represent approval for financing or an interest rate guarantee. Up to a cumulative $15,000 credit at closing towards buyers interest rate buy-down, closings costs, and prepaids. Offer valid only on new contracts signed between September 1, 2022 and September 30, 2022. No cash or credit for any unused credit. All loans are subject to program guidelines and underwriting approval. Not all applicants will qualify. Other terms, conditions, restrictions, and limitations may apply. Contact a Sales Professional for full details. CHOOSE FROM THE FOLLOWING: LOYALTY PERK FOR RETURN REALTORS:

As intense bidding wars accelerated this spring and summer, home buyers began waiving the inspection contingency in hopes of making their offer stand out from the competition. But some may come to regret that decision later. Those who discover costly defects after they move in could end up financially stressed as new homeowners—and looking for someone to blame for their predicament.

By decision.MelissaDittmann

Gamble asks her buyers to sign a special form called the

Get It in Writing

Gamble said she always advises her clients to get a home inspection, even when competition is fierce. “Home buying is an emotional process, and a lot of times, emotions can get in the way and override sensibilities,” she said. “That’s why documentation always beats conversation.”

You don’t want your clients to come back later and blame you for not warning them if they’re suddenly confronting unexpected and expensive home repairs. Set up a system you’ll use to have the contingency conversation from the start of the client relationship.

Many buyers who purchased earlier this year may have skipped the home inspection contingency to sweeten their offer. And now they might regret that

Waiving the Home Inspection: Don’t Blame Me!

20 | Salt Lake Realtor ® | September 2022

and.one ©/Adobe Stock

You may have a client now who’s living with buyer’s remorse after making a rushed home purchase in the frenzied market earlier this year. You may have one in the future, when the market inevitably reaches a hyperactive cycle again. In any market, you can protect yourself and your clients by talking to them up front about the risks of waiving contingencies.

Realty in Upper Marlboro, Md., about her business in the first half of the year. Even as late as July, 27% of home buyers were waiving the inspection contingency, according to the Realtors® Confidence Index.

“We had more buyers saying, ‘I don’t care what’s wrong with the house. I want the house,’” recalled Melanie Gamble, CRB, CRS, principal broker at 212 Degrees

Tracey

“We have clients sign this form so that they don’t come back six months down the road and say, ‘How could you let me buy this house?’” Gamble said. “I can remind them: ‘I did tell you that waiving the inspection was not going to be a good idea. So, if the HVAC goes out the first week of moving in, don’t blame me. I warned you.’”

the client of the importance of the home inspection and other contingencies. “Throughout a transaction, I’m giving my clients a list of what to do and what not to do, but they are not going to remember everything I say,” Gamble added. “They’re excited and emotional. So, that’s why I try to document everything.”

We’ve Got You Covered OM LOANES

A home inspection contingency, which enables buyers to discover structural or operational issues with a home and request repairs from the seller or cancel a contract, is one of the most common. Even if your buyer refuses your advice to get a home inspection, you could negotiate an alternative action. Your client could agree not to require the seller to make any repairs less than

H

NMLS #654272

Federally insured by NCUA. Loans subject to credit approval. current rates and terms.

September 2022 | Salt Lake Realtor ® | 21 Lifetime Servicing Multiple Loan Types No Down Payment Options LEARN MORE UFIRSTCU.COMAT

The form, similar to others some brokerages use, helps shield agents from potential liability when their clients waive contingencies, including inspection, financing, appraisal and others. It requires buyers to acknowledge that they have been advised of the potential for adverse consequences when waiving contingencies. The form also serves as an agreement that the buyer will release the agent from any liability for loss, damage or adverse results from those waivers. Some agents also are using these forms when a buyer submits an offer higher than the listing price.

Having such an addendum also provides an opening for the buyer’s agent to have the conversation, said Deanne Rymarowicz, associate counsel for the National Association of Realtors®. “They can use the form to advise the buyer of the importance of an inspection, the benefits and what all it could reveal—and that it’s part of the negotiating process for a home. If a buyer still chooses to blame [the agent] afterwards, the agent will at least have in writing that their client had full knowledge and information and agreed to give up” that contingency anyway.

“Potential Adverse Consequence Acknowledgement,” which lists exactly what items the buyers are willing to sacrifice to purchase a home. The form was created by the Greater Capital Area Association of Realtors®, Gamble’s local board.

LENDERHOUSINGEQUAL

Alternatives to a Home Inspection

BUY,BUILD,REFI

See

More real estate pros and companies are working with legal counsel to create separate addenda that can be added to the purchase agreement. This provides a paper trail showing that the buyer’s agent has advised

To minimize the chances of this happening to you and/or your sellers, Bullock recommends the following:

5. If the seller needs more space to explain something, use the Seller Property Condition Disclosure Addendum.

Curtis Bullock, CEO of the Salt Lake Board of Realtors®, said in Utah there are several seller disclosure cases that continue to be argued by attorneys when sellers fail to disclose property defects. In one instance, the sellers had experienced significant moisture and drainage problems in a home they had lived in for many years. There were faulty rain gutters causing water to drip into the basement, which caused mold and exterior damage, among other things. The defects were not visible unless it rained. The neighbors were even aware of the constant problems the seller had with the property. A buyer closed on the home and found out about the undisclosed problems and has now filed a lawsuit against the seller and their broker for: 1) breach of contract, 2) failure to disclose, 3) negligent misrepresentation, and 4) fraud.

1. Don’t just email the Seller’s Property Condition Disclosure (SPCD) form to the seller and tell them to fill it out and send it back without any explanation.

3. Make sure the seller has adequate time to fill out the SPCD form and to gather other disclosure documents by the Seller Disclosure Deadline (HOA docs, leases, etc.).

$500, for example. Buyers also could agree to request repairs only for major issues like radon or a faulty foundation, which gives them some legal recourse if they find a larger problem after moving in.

Disclosure Issues on the Rise

22 | Salt Lake Realtor ® | September 2022

Always err on the side of disclosure. Disclose, disclose, disclose.

4. When you receive the SPCD form from your seller, review it for completeness. Make sure everything is filled out. Don’t fill it out yourself.

2. Spend some time with the seller in person, on the phone, or through email and explain the importance of disclosing hidden and material facts/defects. See section 10.3(a) of the REPC which describes the law on disclosure in one sentence.

Home inspections are a chance to educate buyers about the inner workings of the house as well as to flag potential trouble with major systems, such as the HVAC, roof, plumbing, electrical system and foundation, said Adam Long, president of HomeTeam Inspection Service, which has 200-plus offices nationwide. “The number of individuals purchasing a home and waiving the inspection is higher than in the past,” Long said. “Some buyers are concerned they won’t get the home if they don’t waive it. But they could be missing out on valuable information about the home. Also, for sellers, there is a potential for lawsuits from a buyer who discovers something that was not disclosed.”

Reprinted from Realtor® Magazine Online, August 2022, with permission of the National Association of Realtors®. Copyright 2022. All rights reserved.

Image licensed by Ingram Image

Problem types and areas where buyers found issues after closing

Talking Points to Convert Leads

“As members of the National Association of Realtors®, we are unified by the Realtor® brand and its iconic trademark ‘R,’” said NAR President Leslie Rouda Smith. “It’s important for consumers to understand that distinction. We need to engage with consumers in conversation that articulates our value.”

While sellers also were in the driver’s seat last year as bidding wars exploded and list prices soared, most of them—90%—still found value in working with an agent in 2021 to get their home sold, according to NAR research. This may mean consumers are getting the message that a Realtor® is an ally in any housing market. The top issues for which sellers are seeking your guidance, according to NAR data, are:

By Melissa Dittmann Tracey

• Marketing to potential buyers

• Negotiating a deal

Housing volatility is pushing more sellers to work with real estate pros rather than go it alone.

• Finding a trustworthy, reputable professional

NAR is helping you harness your influence by

NAR is providing members with succinct language they can add to their websites and online profiles and bios, including static and animated social graphics, cover images, email signature banners and conversationstarters. This is intended to help provide a unified message around the value proposition of Realtors®, NAR said. Association members are encouraged to leverage the resources about the value of the Realtor® brand so consumers understand the Realtor® difference.

FSBO listings sold at a median of $260,000 in 2021, significantly lower than the median of agent-assisted homes at $318,000, according to NAR’s 2021 Profile of Home Buyers and Sellers.

FSBOs Usually Soar in a Hot Market. Not This Time

Mdv Edwards ©/Adobe Stock

24 | Salt Lake Realtor ® | September 2022

FSBOs Typically Sell for Less

• Pricing a home competitively

The volatile housing market over the last couple of years has driven more consumers toward using real estate professionals rather than attempting to complete a transaction independently. FSBOs made up only 7% of home sales in 2021—the lowest share since 1981—according to the latest Profile of Home Buyers and Sellers from the National Association of Realtors®. That’s a stark contrast from 15 years earlier when 12% of sellers went the FSBO route during the 2006 housing boom, the data shows.

spotlighting the difference a Realtor® makes to the success of a transaction at a new website, thedifference. realtor. The site emphasizes how Realtors® abide by a strict Code of Ethics, observe standards of professionalism and are highly trained in the industry.

On Aug. 22, the Salt Lake Board of Realtors® Charity Committee presented a $60,000 check to Gavin Krushensky. The money was raised through a “Golf to Give” event at Sleepy Ridge Golf Course in Orem. The many contributors included individual and company sponsors, family members, friends, strangers, and 144 golfers. Gavin is the Board’s event director. He was involved in a UTV accident in September 2021 and suffered a C4 spinal cord injury that left him paralyzed from the chest down. Dale Hull, co-founder and executive director of Sandy-based Neuroworx, a non-profit, outpatient facility providing innovative physical therapy for people affected by paralysis from spinal cord injuries and other conditions, said Gavin is very fortunate because he has an enormous support system. “There are people out there who have no one,” Hull said. “We have people who are disowned by their family.” The money raised from Golf to Give will help Gavin with specialized neurological care going forward. Hull co-founded Neuroworx after his own spinal cord injury in 1999, when he failed to complete a backflip on his backyard trampoline, resulting in a dislocated neck and paralysis. Since its founding, Neuroworx has provided specialized care for more than 4,000 adults and children from 28 states and four countries. “With spinal cord injuries, no two injuries are the same and no two recoveries are the same,” Hull added.

26 | Salt Lake Realtor ® | September 2022

Realtor® Family Helps a Friend in Need

September 2022 | Salt Lake Realtor ® | 27

Photos: Dave Anderton

Nationally, year-over-year sales fell 20% (6.03 million in July 2021), according to the National Association of Realtors®.

The number of homes listed for sale across Utah increased to 9,682 as of Aug. 31, up 143% compared to a year ago, according to UtahRealEstate.com. Based on sales trends over the past six months, active listings represent a 4.4-month supply of housing inventory.

“Home sales are down largely because of rising mortgage interest rates,” Eskic added. “The Wasatch Front housing market has a good long-term outlook. One solution to higher home prices is to increase housing supply. In 2021, the number of new housing units permitted in Utah far exceeded that of new households (marriages, divorces, children leaving home, net in-migration, etc.); 40,144 housing units compared to 26,689 new households.”

JULY

In Salt Lake County, active listings increased to 2,385, up 102% compared to 1,183 listings a year earlier. The median days on the market for a home to sell in July increased to 14 days, up from six days in July 2021.

“Generally, five to six months of inventory is a balanced market,” said Dejan Eskic, chief economist of the Salt Lake Board of Realtors® and a senior research fellow at the Kem C. Gardner Policy Institute. “More than six months of inventory and it becomes a buyer’s market. If it is less than five months, we have a seller’s market. Last year at this time there was less than one month supply of inventory.”

Home sales (all housing types) in Salt Lake County fell to 1,060 in July, down 36% compared to 1,666 sales in July 2021. July was the 14th consecutive month of falling sales year over year. July marked the lowest number of sales for a July month in 11 years. Sales were down across all counties on the Wasatch Front.

“We’re witnessing a housing recession in terms of declining home sales and home building,” said Lawrence Yun, NAR chief economist. “However, it’s not a recession in home prices. Inventory remains tight and prices continue to rise nationally with nearly 40% of homes still commanding the full list price.”

The median sold price of all Salt Lake County homes in July increased to $525,000, up 11% from $475,000 a year earlier. The median price of a single-family home increased to $600,000, up 9% from $550,000 in July 2021. Multi-family homes sold in July had a median price of $420,000, up 11% from $380,000 a year ago.

28 | Salt Lake Realtor ® | September 2022

Number of Homes for Sale Increases to More Than 9,500 Listings

HOUSING WATCH

September 2022 | Salt Lake Realtor ® | 29

Tamas ©/Adobe Stock

Still, new-home prices continue to stretch higher despite the recent pullback in sales. The median price for a new home in July climbed nearly 6% compared to the previous month, reaching $439,400. One culprit: Building materials have jumped 35.7% since January 2020. “The sharp drop in new-home sales is another clear indicator that housing is in a recession,” said Danushka Nanayakkara-Skillington, the National Association of Home Builders assistant vice president for forecasting and analysis. “The combination of higher prices and increased interest rates are generating a notable slowing of the housing market.”

Just a year ago, homebuilders were overflowing with new contracts and, at times, raffling off their few remaining lots to wait-listed buyers. But since then, buyer traffic has slowed significantly as costs have soared. Rising mortgage rates and high inflation have crashed the homebuilding party.

New-Home Sales Plummet, but Completed Homes Find Buyers within Three Months

Inventory for newly constructed single-family homes was at a 10.9-month supply in July, up a whopping 81.7% from a year earlier. However, of 464,000 units nationwide, only 45,000 are completed and ready to occupy; the remainder is still under construction, according to government data. Last week, Lawrence Yun, chief economist for the National Association of Realtors®, signaled some optimism for the newhome market’s long-term outlook. “Homebuilders are naturally very cautious about rising unsold inventory during the construction phase,” Yun said. “But those completed homes are finding buyers within three months, which is relatively swift for the new-home market. Improving conditions within the supply chain for the delivery of items such as lumber and appliances will lessen overall uncertainty.”

mortgage rate, those rates have nearly doubled since the beginning of 2022. In the last week of August, the 30-year fixed-rate mortgage averaged 5.66%, and the rise in borrowing costs has added hundreds of dollars to monthly mortgage payments.

30 | Salt Lake Realtor ® | September 2022

By Melissa Dittmann Tracey

It’s yet another sign of a sudden plunge in the new-home sector. Housing starts for single-family construction projects dropped 10% year over year in July; mortgage applications for new-home purchases fell 16.1% the same month; and homebuilding sentiment dipped for the eighth straight month in August. The number of buyers backing out of new-home contracts also is growing: Homebuilder cancellation rates have more than doubled since April, according to John Burns Real Estate Consulting. In July, 17.6% of builder contracts fell through, compared to 8% in HomebuildingApril. contracts tend to have longer construction timelines that can stretch six months or more. And while buyers who signed a contract earlier this year may have been banking on locking in a low

Elevated mortgage rates and higher construction costs are pushing more consumers out of the market, particularly entry-level buyers.

New-home sales in July reached their slowest pace in six years, the Department of Housing and Urban Development and the Census Bureau reported. New single-family home purchases declined 12.6% month over month and were down nearly 30% from a year earlier. “The disappointing sales pace mirrors an ongoing decline in builder sentiment as elevated mortgage rates and higher construction costs are pushing more consumers out of the market, particularly entry-level buyers,” said Jerry Konter, chairman of the National Association of Home Builders.

As part of the legendary Berkshire Hathaway family of companies, we have the depth, strength and brand power to help grow your real estate business. Our network extends globally in reputation and strength. Locally, our company is the largest brokerage in Utah, ensuring that your property reaches a broad audience of real estate professionals and buyers. We are committed to providing you with the resources and support that will create greater success and enjoyment in your real estate career. So, talk with us at Berkshire Hathaway Utah Properties and let’s get you settled without ever settling for less

©2022 BHH Affiliates, LLC. An independently owned and operated franchisee of BHH Affiliates, LLC. Berkshire Hathaway HomeServices and the Berkshire Hathaway HomeServices symbol are registered service marks of Columbia Insurance Company, a Berkshire Hathaway affiliate. Equal Housing Opportunity. LOCALLY OWNED AND OPERATED SINCE 1976 | (801) 990-0400 | BHHSUTAH.COM RESIDENTIAL | DEVELOPMENT | COMMERCIAL | RELOCATION | NEW CONSTRUCTION MORTGAGE SERVICES | TITLE & ESCROW SERVICES @BHHSUTAH LEARN MORE UTAHTHROUGHOUTOFFICES30OVER

READY TO GET REAL ABOUT REAL ESTATE?

Lexi Relleve Transaction Manager

Text Monica Draper to learn how we help agents succeed 435 313 7905

WHAT DOES IT MEAN?

Full-service support, even beyond cap In-house marketing and creative team Economic insights and continued education Your own notAwithIntegratedtransactiondedicatedmanagertechsuitehands-ontrainingfamilyofcollaborators,competitors