Now is the time to work with your clients to plan their financial futures. These tips will ensure you take all their needs into consideration.

Pg 14

SOFTWARE

Choosing the right software empowers you to streamline operations, enhance client engagement, ensure compliance and make data-driven decisions. Here’s what you need to know.

Pg 16-18

RETIREMENT

What’s in store for the retirement insurance industry in 2025? We look at the impact of the two-pot system and investigate where to next.

Pg 19-23

TAX UPDATES

We update you on the tax issues that are most likely to be in the spotlight in the year ahead.

Pg 24-25

What lies ahead for 2025?

Four economists share their views on what investors can expect in the year ahead. While they aren’t expecting it to be as unpredictable as 2024, some significant challenges remain.

Ultimately, I am far less concerned than I was this time last year. While some risks remain, they’ve clearly decelerated, significantly reducing the probability of a negative outcome. From a return perspective, there’s still meaningful upside. Overall, we’re in a much better position, which is encouraging. The South African market is the most exciting part of the portfolio right now. The rand still has room to recover, and with the dollar remaining strong, offshore holdings are slightly less attractive in the near term, as a stronger rand could erode returns. Patience will be key for offshore investments, but for now, South Africa offers a promising investment landscape.

We see South African equities as a broad opportunity, with share prices catching up to earnings after prolonged pressure, particularly in the banking sector. Even bonds offer potential, with room for yields to decline. Much depends on February’s National Budget

Speech, and we remain hopeful it avoids shocks that unsettle rating agencies. While not broadly negative on the offshore environment, we are focused on the US. China offers opportunities but requires careful assessment of risk-adjusted returns. The UK, however, stands out as an overlooked market.

Like South Africa, retail investors have shifted capital toward the US, chasing its recent returns. As the cycle turns and investors reassess valuations more rationally, we expect some of that capital to flow back, unlocking potential opportunities in the UK market.

Global government debt, the risk of inflation and excessive asset valuations will be challenges going forward. US government debt levels have created a headwind by borrowing heavily against future growth. Taking on debt is essentially a bet that growth will outpace the rise in debt costs. If that growth fails to materialise, escalating debt and funding costs can become a significant burden. Persistent inflation is concerning.

With interest rates remaining high, the government’s annual interest bill on bond issuance now exceeds $1tn,

Adriaan Pask, CIO at PSG Wealth

UP-TO-DATE INDUSTRY NEWS

Stay ahead of the curve with the latest industry news & insights, or have it delivered to your inbox to read later.

Read digital issues from all our B2B titles on your PC, smart phone or tablet. PDF downloads also available.

Remove geographical barriers and expand on your expertise with knowledge-sharing webinars across a variety of topics.

Continued from previous page burdening taxpayers and diverting funds from productive economic investments. Valuation risk in the US has been a long-standing concern, even as markets surge, detached from fundamentals. Current behaviour shows signs of excessive speculation, with retail investors driving activity, obscure cryptocurrencies soaring and leveraged ETFs on unconventional assets emerging. This abundance of speculative capital is often a precursor to economic trouble.

Many private equity firms, flush with capital, now face significant reinvestment risk. As their earlier investments mature, they are pressured to deploy capital, often into lower-quality opportunities with near-term challenges. This cycle of forced reinvestment into suboptimal assets is a key concern moving forward.

Citadel Chief Economist, Maarten Ackerman

While interest rates and inflation are easing in SA and globally, economic growth is likely to stay below capacity for the next two to three years. Europe, the UK and Japan face weak growth, with a slight slowdown expected in the US, while some emerging markets may see moderate growth.

President-elect Donald Trump’s policies, including trade tariffs and immigration crackdowns, are likely to disrupt free trade and labour markets, stoking inflation and dampening growth. His fiscal reform faces revenue challenges as Republicans push for tax cuts for corporations and high earners. The US may experience sticky inflation, slower rate cuts and growth challenges. Retaliatory trade tariffs could worsen global trade struggles, adding to the slowdown and affecting net exporters. Global growth presents a mixed picture. The US is slowing toward its 2% trend growth, while other developed markets struggle to stabilise. If the US achieves a soft landing and

China revitalises growth, recovery in developed markets is possible. Conditions are better than a year ago when fears of a global recession loomed. Stable consumer confidence and a strong US labour market could help avoid a recession entirely.

Other developed markets face tougher prospects. Export-reliant nations will battle geopolitical upheaval and supply chain disruptions. Diverging growth trends are evident, with the US growing steadily while Europe, the UK, and Japan slip into recessionary territory, following early policy normalisation and rate cuts.

In SA, real GDP growth is estimated at just 1,1%, with medium-term growth expected to average 1,8% over three years. Finance Minister Enoch Godongwana emphasises improving macroeconomic stability, structural reforms, infrastructure investment and state capacity to achieve higher inclusive growth. Real growth above capacity could be seen in three to five years. Bright spots for SA include the formation of a Government of National Unity, improved energy security, lower inflation, and strong performances in equities, bonds, and the rand, placing SA among the top emerging markets. Inflation control supports further rate cuts, increasing the potential for a global soft landing and capacity growth over the next three to four years.

Schroders Capital

Johanna Kyrklund

We think there are return opportunities to be had, even after the gains of 2024. But investors may need to look beyond recent winners. Equity investors have grown used to a small number of large companies

ED'S LETTER

New Year to all our readers. I hope you’ve had a relaxing break and are ready to face an exciting year ahead. We asked some economists what they think 2025 holds in store, and the good news is everyone tends to be feeling more positive than they were at the start of 2024. South Africa’s outlook has improved, and while there is still global uncertainty around a second Trump presidency and ongoing wars, not just in Ukraine and Gaza but now in Syria as well, the overall feeling is still one of hesitant optimism.

There’s nothing like a new year to inspire you to make some changes in your business, and one of the most important

powering the stock market’s gains. But that pattern was already changing during 2024, and we think there is potential for markets to broaden out further. Different sectors and different regions may start to appear more attractive. An active approach will be needed to avoid overexposure to previous top performers, and to capture new return opportunities as they emerge.

Equity market valuations do not look expensive outside the US. And an environment of positive growth and lower interest rates should benefit corporate earnings, which is what drives shares over the long term.

We continue to view bonds favourably for the old-fashioned reason of income generation, the importance of portfolio diversification in terms of ensuring resilience amid ongoing geopolitical uncertainties and the significance of decarbonisation as a key investment theme.

Nils Rode

We anticipate 2025 to be an attractive environment for new private market investments, offering potential for both return and income generation as several cycles align favourably. These include the private market fundraising, technological disruption and economic cycles. Simultaneously, considering ongoing geopolitical tensions and the elevated risks of escalating conflicts, the role of private markets in providing portfolio resilience remains crucial. Meanwhile, and despite political changes in the US, we expect the trend towards decarbonisation to persist, with private market investments playing a significant role in driving the global energy transition.

The small/mid-buyout and venture capital space are the most attractive in private equity, with real estate also expected to enjoy a good vintage year, while the private debt premium remains attractive across several strategies.

things you could do is to upgrade your software – or installing a new package altogether. It can be a daunting prospect, but Francois du Toit from PROpulsion has some wise advice you can follow.

Cybersecurity is more important now than ever, as a data breach could result in significant financial losses for clients, irreparable damage to the firm’s reputation, and potential regulatory penalties. Additionally, as the financial industry increasingly adopts digital tools and platforms, the risk of cyber threats like phishing, ransomware and data theft continues to grow. Ensure your systems have the best cyber protection available – the investment will be worth it in the long run. Stay financially savvy.

Schroders Group Chief Investment Officer (CIO), Johanna Kyrklund, and Nils Rode, CIO for Private Markets at

Sandy Welch Editor, MoneyMarketing

Dawid Balt Portfolio Manager, Sasfin Wealth

How did you get involved in financial services – was it something you always wanted to do?

My interest in financial markets was awakened by my grade 8 economics teacher. He arranged a school trip to Absa’s dealing room in Marshalltown. The moment I stepped into the dealing room, I was hooked by the organised chaos. The ringing telephones, shouting dealers, television sets broadcasting breaking news, and computer screens flashing thousands of numbers in all the colours of the rainbow. It was an adrenalin rush of note. From that day I knew exactly what I wanted to do.

What was your first investment, and do you still have it?

It would have been a penny stock and no, I don’t have it anymore. It probably went bust. When you are young and ignorant, and you buy a stock purely because it trades below 10 cents – it’s a recipe for wealth destruction. But these ‘go big or go home’ trades played a pivotal role in

What have been your best – and worst – financial moments?

The 2007 - 2008 Financial Crisis was a horrible time in the financial industry. Very few people today truly understand the severity of the situation the world faced. If President George W Bush did not sign the Emergency Economic Stabilisation Act on 3 October 2008, the world would have been a very different place today. I experience my best moments every day. It is a privilege to show clients that they have achieved or surpassed their long-term financial goals that they identified five, 10 or 15 years ago.

What are some of the biggest lessons you have learnt in and about the finance industry?

The power of compounding. Successful investors understand this concept and, more importantly, they understand that it takes a lot of patience to reap the benefits. So many miss out on this basic investment principle because of a world that chases immediate gratification. Then, if it sounds too good to be true, it probably is. Use your common sense when deciding if you should entrust your life savings to someone that promises a risk-free high investment return. There is no such thing.

“Use your common sense when deciding if you should entrust your life savings to someone that promises a risk-free high investment return. There is no such thing”

Always check if the product and the person selling the product is regulated by the Financial Sector Conduct Authority.

What makes a good investment in today’s economic environment?

The economic environment should not impact your investment methodology and approach. Peter Lynch, an American investor and mutual fund manager, said, “If you spent over 13 minutes a year on economics, you’ve wasted over 10 minutes.” My apologies to all economists out there! Invest in companies with management teams that are good allocators of capital. I’m always on the lookout for management teams with a track record of

consistent above-average returns on the capital they have invested. These teams have the experience to circumnavigate any economic environment on behalf of their investors.

What finance/investment trends and macroeconomic realities are currently on your watchlist?

Again, you should not allow the macro environment to change your investment approach. There is always something happening somewhere in the world that could increase short-term market volatility. The return of President Donal Trump to the White House is perceived to be good news for the US stock market. I don’t think it is as clearcut as that. He might implement policies that could fuel inflation, meaning that interest rates stay higher for longer. Higher interest rates equal higher cost of capital, which could squeeze company profit margins. The first time in more than a decade, US Treasuries are trading at very attractive yields. For the lower risk profile investor, this could be a great portfolio diversification opportunity. I also subscribe to the Ivy League universities’ approach to allocate capital in their endowment portfolios to alternative and real assets. Done correctly, investors could decrease their investment portfolio’s volatility and increase long-term returns by allocating capital towards these asset classes.

What are some of the best books on finance/investing that you’ve ever read, and why would you recommend them?

I’ve just finished The Changing World Order by Ray Dalio. I’m probably biased as Dalio is one of my investor ‘mentors’, but this is a must read for someone that believes in the principle of history repeats itself. And a firm favourite of mine is The Intelligent Investor by Benjamin Graham. There are so many great enduring principles and investment insights in this book.

By Wayne Epstein Head of Standard Bank Personal & Private Banking Moonshots

How diversity and AI drive business success

The past few weeks have undeniably been some of the most eventful of the year. The reelection of Donald Trump as President of the United States has prompted discussions worldwide, as his return to office will certainly have global implications, including in South Africa. As the old saying goes, “When America sneezes, the world catches a cold.”

Regardless of one’s feelings toward him, it’s evident that his perspectives and policies are deeply polarising. One of the most debated has been his stance on Diversity, Equity, Inclusion, and Belonging. I’d like to make a case for diversity requirements from a purely business perspective, advocating that all organisations – regardless of political views – can benefit from embracing these values. As a committed capitalist and someone responsible for building new business lines and products within Standard Bank’s Moonshots division, I consistently find that the diversity principles can enhance the major aspects of business and product development. These are particularly evident in some of the key elements we consider, namely: sourcing skilled talent for required business objectives; designing and delivering compelling products, propositions, and solutions; and optimising sales and distribution. When these principles are applied, each of these elements can become stronger and better positioned for success.

“Businesses should therefore view AI as a supplement rather than a substitute for diverse perspectives”

Finding the right people: attracting the best talent is the foundation of any successful business venture. A few fundamentals I have discovered in my career is that the team is more important than the individual (think about the league-winning Leicester football team of 2015/2016), and employee job satisfaction and workplace culture are key ingredients for success.

Diversity initiatives are therefore not just ‘nice-to-haves’ – they can be strategic ingredients that enable business success. Creating an environment where employees feel valued and heard is directly linked to productivity, employee engagement, and innovation. When people feel safe bringing their unique perspectives to the table, they

contribute more actively and passionately, which enhances performance across the board. A diverse workforce inherently brings a wide range of perspectives, which is invaluable in designing products that truly meet customer needs. It enables us to view challenges through multiple cultural and social lenses, which can reveal insights we might otherwise miss.

Without these differing viewpoints, our understanding of customer issues and our ability to create effective solutions may be limited. Developing products that cater to diverse cultural nuances can make the difference between success and failure in new markets. As an example, Stanbic’s Dada offering in Kenya was borne from understanding the challenges that women face in accessing financial solutions. A wellrounded approach ensures that products are inclusive, relevant, and commercially viable, thereby increasing their appeal and acceptance among customers from various backgrounds.

One of the most effective sales strategies is the concept of the ‘empathetic sale’, which requires sales teams to deeply understand and identify with a customer’s problem. Diversity fosters the mindset to analyse, appreciate, and empathise with varied perspectives, helping salespeople better connect with customers at all levels. This empathetic approach strengthens trust and builds long-term relationships, which are key to successful sales outcomes and customer retention. In a large corporation like Standard Bank, we see the benefits in action daily, but a common question arises: How can small businesses without the same scale or manpower leverage these advantages? Additionally, how can businesses gain insights about new markets and audiences when resources are limited?

This is where Generative Artificial Intelligence can become an invaluable tool. The major applications (like those owned by Google and Microsoft, among others) have datasets that incorporate apparently trillions of parameters that, when prompted appropriately, can return human-like responses to questions posed. Therefore, small and mid-sized businesses can now access anything from how a 60-year-old male in Kampala, Uganda, would feel about funeral insurance, to what may be the appeal for rainbow-coloured candies among children aged six to nine based in a favela in Sao Paulo, Brazil.

The advent of this technology now allows business leaders to gain a preliminary understanding that can be used to build indicative business cases, in many instances for free. It is, however, essential to acknowledge that while Generative AI can simulate perspectives, it cannot replace genuine human experiences.

Businesses should therefore view AI as a supplement rather than a substitute for diverse perspectives. Engaging directly with target audiences and cultivating a diverse internal team are still optimal to authentically understanding different viewpoints and developing products that resonate.

Therefore, in my view, while diversity has historically been framed as an ethical or social issue, it is also a powerful business strategy. Organisations that prioritise it can gain a competitive edge, improving not only internal dynamics and customer connections but also their overall bottom line.

With the emergence of advanced AI tools, the benefits of diversity are within reach for businesses of all sizes, from global corporations to local startups. Embracing it is not just about doing what’s right; it’s about doing what’s smart for sustainable business success.

By Ettienne Bezuidenhout Wealth Manager at Alexforbes

IThe importance of having a will in South Africa

n South Africa, the need for a will is often overlooked, particularly by younger individuals or people who believe they lack substantial assets. However, regardless of financial situation or age, having a will is crucial for ensuring your wishes are carried out after death.

Legal framework governing wills

In South Africa, wills are governed by the Wills Act No. 7 of 1953, which stipulates the legal requirements for creating a valid will. For a will to be legally binding here: It must be in writing (either typed or handwritten).

• The testator (the person making the will) must be 16 years or older. The testator must sign the will at the end of the document in the presence of two witnesses.

• The two witnesses must also sign the will, and they must not be beneficiaries or spouses of beneficiaries in the will.

Failure to comply with these requirements could result in the will being declared invalid, meaning the deceased’s estate would be distributed according to the rules of intestate succession.

“By carefully drafting a will and considering estate planning, the tax burden on the estate can be minimised”

Ensuring wishes are honoured

A will allows a person to choose exactly who inherits their assets, including property, money and personal items. Without a will, their estate is distributed according to the Intestate Succession Act, which may not align with their preferences.

Minimising family disputes

The absence of a will often leads to confusion and conflict among surviving family members. Disputes over inheritance are common, especially if there is uncertainty about the deceased’s wishes. Having a clear and legally sound will helps prevent such disputes by

providing clear instructions on how assets should be distributed.

Without a will, families can end up in prolonged and expensive legal battles, potentially damaging relationships and depleting the estate in the process. A well-drafted will can prevent this by clearly stating intentions, reducing the risk of conflict and protecting your family’s future.

Appointing guardians for minor children

One of the most essential functions of a will is the ability to appoint legal guardians for minor children in the event of a parent’s death. In South Africa, if a parent dies without a will and there is no surviving parent, the court is responsible for appointing a guardian. While the court aims to act in the best interests of the child, it may not always align with what the parent would have wanted.

The listed guardian still has to be appointed as a guardian. It helps to nominate a South African guardian as it minimises the legal requirements and disruptions for the minor.

Tax efficiency and financial planning

South Africa has estate duty, which is a tax on the deceased’s estate. By carefully drafting a will and considering estate planning, the tax burden on the estate can be minimised. Proper estate planning, often done in conjunction with a financial adviser or estate planning expert, can help structure assets to reduce estate duties. This ensures that more assets go to beneficiaries rather than the state.

In addition to tax efficiency, having a will also ensures that assets are distributed efficiently and without unnecessary delays. The presence of a will streamlines the process of winding up the estate, making it easier for loved ones to access their inheritance without lengthy legal procedures.

Flexibility and control

A will offers flexibility in terms of how and when beneficiaries receive their inheritance. Trusts can protect the interests of minor children or manage complex family dynamics, such as ensuring that an inheritance is used responsibly or where

there are children from different marriages involved. Using a trust can protect the minor’s inheritance from abuse by their guardians, such as where the guardians could spend all the inheritance before the child becomes an adult.

Wills can be updated or changed at any time, as long as the person is mentally capable of doing so. This ensures that the will always reflects their circumstances and wishes. If the beneficiaries in a will are changed, retirement fund nominees as well as beneficiaries on life policies must be changed too.

Appointing an executor

The executor of the deceased estate must be named. It’s not always a good idea to nominate a family friend, spouse or even an adult child, as it could potentially lead to complications and delays if they are not experienced. If this is the case, the Master will appoint a professional executor. If the idea is to appoint a professional as the executor, it’s better to stipulate this in the will. It also affords the opportunity to discuss any wishes with the executor, and to fix the executors’ fees, as some professionals will allow a discount from the standard 3.5% (ex VAT) fee, depending on the size of the estate.

Common misconceptions

Many people believe that wills are only necessary for wealthy or elderly people. The reality is that anyone with assets –no matter how modest – should have a will. Even personal items such as family heirlooms, sentimental possessions or bank accounts should be accounted for in a will to avoid complications later. Retirement funds do not form part of an estate.

Another common misconception is that a surviving spouse automatically inherits everything. In reality, the rules of intestate succession can result in the estate being divided between the spouse and children, which may not align with the deceased’s wishes.

It’s important to seek assistance to ensure that wills are valid and comprehensive. Taking this simple step can save your loved ones from unnecessary stress and provide clarity in a time of emotional difficulty.

A new digital platform homes in on unclaimed benefits

Unlocking unclaimed benefits has the potential to release R90bn back into the South African economy. Robin Hood, in partnership with Standard Bank’s OneHub, is a digital platform created by a group of entrepreneurs, business leaders, and industry experts to transform the process of reconnecting unclaimed assets with their rightful owners. By teaming up with corporate institutions and administrators, Robin Hood efficiently and costeffectively traces, verifies, and distributes assets to beneficiaries. MoneyMarketing asked Rowan Gordon, CEO of Robin Hood, to go into more detail about the offering.

What’s the thinking behind Robin Hood?

The team behind Robin Hood is deeply committed to addressing societal challenges. Unclaimed benefits emerged as a clear starting point – a significant societal issue, plagued by credibility issues which, until now, has lacked the technological innovation needed to develop a scalable solution. By partnering with Standard Bank, Robin Hood aims to bring credibility, along with bank-level governance and security, to the platform. Unlocking unclaimed benefits has the potential to release R90bn and benefit the South African economy on a similar scale to the two-pot system.

Who can benefit from this platform?

• All South African citizens who are owed unclaimed assets. The Robin Hood solution utilises multiple databases to digitally match South African citizens with their unclaimed asset. Any citizen that we are not able to digitally match will be able to use the Robin Hood mobile app (to be launched in Q1 2025)

to search for their benefit and start the digital claiming process.

• All corporate institutions who are custodians of unclaimed assets and need to trace beneficiaries. These institutions have a duty to reconnect unclaimed assets with their rightful beneficiaries, but the traditional process is manual, expensive, and prone to credibility challenges. Robin Hood streamlines this process by efficiently and cost-effectively digitally tracing, verifying, and distributing even the smallest benefits.

What success rate have you had to date?

We are constantly enhancing our success rates by refining and expanding our data-matching capabilities. A major challenge lies in the poor quality of basic data for many unclaimed benefits, which can make tracing beneficiaries difficult. As a result, our success rates vary depending on the quality of the initial data. To date, we have been able to trace between 30% and 55% of beneficiaries.

What success rate are you anticipating in the future?

Our estimate is that the industry's current solve rate is between 6% and 8% annually. Robin Hood would at least like to triple this annual rate. While solving the problem entirely would be an incredible achievement, our immediate focus is on reuniting living South African citizens with their rightful benefits.

How does SA compare in terms of unclaimed benefits with the rest of the world? Unclaimed benefits are a global challenge,

EARN YOUR CPD POINTS

The FPI recognises the quality of the content of MoneyMarketing’s January 2025 issue and would like to reward its professional members with 2 verifiable CPD points/hours for reading the publication and gaining knowledge on relevant topics. For more information, visit our website at www.moneymarketing.co.za

primarily driven by outdated contact information, lack of beneficiary awareness, and complex regulatory environments. In South Africa, this issue is further compounded by its unique socioeconomic factors, including labour migration and historical gaps in record-keeping. Different countries have adopted various mechanisms to address this issue. For example, countries like the United States and Australia have established centralised databases and proactive tracing systems to manage unclaimed assets. In contrast, in South Africa, the responsibility for tracing and managing unclaimed benefits falls on individual corporate institutions, resulting in a more fragmented approach.

How could Robin Hood assist financial advisers in terms of educating their clients?

Financial advisers can play a crucial role by guiding their clients on how to check for unclaimed assets and encouraging them to regularly update their personal details, as well as the information of any named beneficiaries. Unclaimed benefits often stem from outdated contact information, and Robin Hood is here to help beneficiaries reconnect with their lost funds. We are actively onboarding additional corporate institutions holding unclaimed assets to create a unified search portal for beneficiaries.

Please stay updated by following our LinkedIn page for the latest information: https://www.linkedin.com/company/robinhood-unclaimed-benefits/

By Karen Rimmer Head of Distribution at PSG Insure

Cover for alternative energy sources and power outages

Eskom is proposing a 36% power tariff hike for 2025, which means South Africans could soon see a steep rise in electricity costs. For this reason, many home- and businessowners are still seeking alternative energy sources. Solar power remains a popular choice, but it’s important to remind clients there are insurance implications to consider. Homeowners should ensure that their property values are adjusted in line with the installation cost. It’s also crucial to use a qualified and compliant installation company. This will ensure all regulations are met, and reduce the risk of malfunction.

For businesses, these adjustments are equally important. Installing solar panels

By Laurence Rapp CEO, Vukile Property Fund

Wcan be a considerable investment, adding substantial value to the premises. Any new addition like this should be communicated to your insurance adviser, who can accurately reflect these improvements in your policy. It’s important that power supply plans are factored into business processes, to ensure that all staff know how to operate and maintain new devices. In addition, solar panels are being increasingly targeted by criminals, so it’s important to take preventative measures with anti-theft mechanisms and to consider additional security enhancements.

Is additional cover for other alternative power sources necessary?

Inverters, battery packs, generators, and solar systems can be life savers during

power outages, but they need to be factored into policies to avoid unexpected costs.

What about power surges?

In areas where load reduction is still prominent, power surge protection, including insurance, is advisable. Policies previously automatically covered power surges up to a certain limit, but this is no longer standard. Today, surge cover generally incurs an additional premium. Help your clients to review and understand these options to protect against unexpected repair costs from surges or power inconsistencies. Fires are a common concern when there is a power surge, which is why it’s important to have property fully insured from the structure to the contents inside.

Specialisation vs diversification: Why you don't have to choose

Conventional wisdom pits diversified property funds against specialist ones. But, as Vukile shows, a well-crafted specialist fund can also reap the rewards of diversification for its investors.

hen researching investment in real estate investment trusts (REIT), you've likely read that you must choose between diversified and specialist funds. But is this really an either-or proposition? Yes, investing in a diversified REIT offers a shortcut to cross-sector diversification. However, companies excelling in their specialised areas often yield superior results. Private investors may benefit from building their own diversified portfolios by selecting top-performing sectorspecific funds. At Vukile Property Fund, we believe that with the right approach, you can get the best of both worlds in one fund. Our model combines retail real estate sub-sector specialisation with geographical diversification across South Africa and the Iberian Peninsula.

Mastering our niche

As a specialist fund focused on retail property, we've found that deep expertise in a specific sector can be a powerful driver of value. Concentrating efforts and resources on what we know best achieves a level of insight and understanding that more generalist funds simply can't match. This drives the ability to identify opportunities, manage risks, and drive returns in ways that would be impossible with a more scattered approach. Take Vukile’s scalable consumer-led business model. By understanding

our shoppers’ needs, we create experiences at our shopping centres that exceed expectations. This leads to increased time and spending at our centres, and builds loyalty. Our customercentric approach drives value creation for all our stakeholders. Our model is scalable and relevant to each community and country where we invest.

Multi-layered diversification

But specialisation doesn't have to mean putting all your eggs in one basket. At Vukile, we've built a diversified portfolio that spans South Africa and the Iberian Peninsula in Spain and Portugal. We further diversify across regions and retail property types, encompassing everything from large malls to smaller convenience centres, as well as retail brands and, finally, individual shop units. A single shop closure has minimal impact on the overall portfolio. This diversification provides a robust foundation, spreading risk and increasing the potential for consistent returns over the long term.

Disciplined dealmaking

Of course, diversification is only as good as the quality of the underlying assets. That's why we're so selective about the properties we bring into our portfolio and our value-adding developments. Strong capital allocation lies at the heart of our strategy, and this is where our

specialisation truly comes to the fore. Every potential acquisition is subjected to rigorous scrutiny. We're not interested in simply chasing yield and growing for scale’s sake – our goal is to build a portfolio of truly exceptional properties that are strategically aligned and financially accretive in our core markets of Spain, Portugal and South Africa.

A consistent track record

Combining a specialist's focus with the benefits of diversification provides a strategic approach to capitalise on retail property sector opportunities while mitigating its challenges.

Over the past 20 years, Vukile has delivered consistent dividend growth (bar one Covid-19impacted year), outperforming the SAPY Index and industry peers. This is a testament to the power of a specialised yet diversified model, clear strategy, best-of-breed governance, robust financial management, and strong, skilled teams that operate on the ground, locally.

With our proven business model and performance record, our investors continue to demonstrate confidence that their capital is in good hands.

Get the best of both worlds

So why choose between specialisation and diversification when you can have both? At Vukile, we're redefining what's possible for REIT investors. We believe there are exciting returns and opportunities to be found in the world of retail property and across our core markets of South Africa, Spain and Portugal – and we look forward to unlocking them.

OUR 220 MILLION SHOPPER VISITS A YEAR CREATE SUSTAINABLE GROWTH AND SUPERIOR VALUE .

This is Faith M, aged 55. She shops weekly, mostly mid-morning when the roads are quiet. It’s a short drive, and this is her favourite community centre close to home.

She used to shop monthly, but now enjoys doing more frequent top-ups. She likes to spend time in the centre and will often arrange to meet a friend at the local coffee shop.

Faith and her husband like to pop in at the centre over weekends, especially when there’s a spice festival or other community event, or when they’re with their grandchildren in the school holidays.

We know all this and more about Faith M and our other visitors, too. Our multi-faceted consumer behaviour research, combined with our deep understanding of the needs and desires of the communities we serve, leads us every step of the way.

Our unique focus on a superior customer experience ultimately benefits all our key stakeholders, including our tenants and investors.

As a Vukile stakeholder, you too will benefit from our extensive analysis of shopper behaviour and the factors that drive continuously evolving retail trends.

There’s never been a better time to invest in people like Faith M.

BUILDING COMMUNITIES, GROWING VALUE.

Is South Africa back on track?

South Africans are generally optimistic, but the long, dark years of state capture and loadshedding have weighed heavily on the national psyche. With an energy availability factor hovering in the mid-fifty percent range in 2023, South Africans braced themselves for stage 7 or higher loadshedding as winter approached. The electricity crisis acted as a permanent handbrake on our economy, leaving consumers and businesses idling in the parking lot of SA Inc.

There’s nothing like a crisis to force change

Most of the required reforms to alleviate loadshedding were already enacted at the peak of the electricity crisis. The President’s establishment of a ‘war room’, in the form of the National Energy Crisis Committee (NECOM), allowed government, business and consumers to all play a pivotal role in finding ways out of the energy crisis. Since late March this year, we’ve had no loadshedding, and the energy availability factor is above 70%. Businesses and households have invested substantially in renewable energy, resulting in reduced demand on Eskom generation. It has also allowed the national power utility to perform critical maintenance at its power stations. Renewable energy has become a much larger component of the energy mix, effectively doubling from around 10% of installed capacity to 20% over the last two years. The huge acceleration of private-public partnerships means that NERSA-registered projects are sitting at 9.7GW,[1] with their capacity close to Eskom’s Medupi and Kusile power stations. Additionally, rooftop solar energy has almost trebled over the last two years to 6GW.[2] While rapid growth in energy generation is helping to get South Africa back on track, we are also seeing much-needed transmission reform.

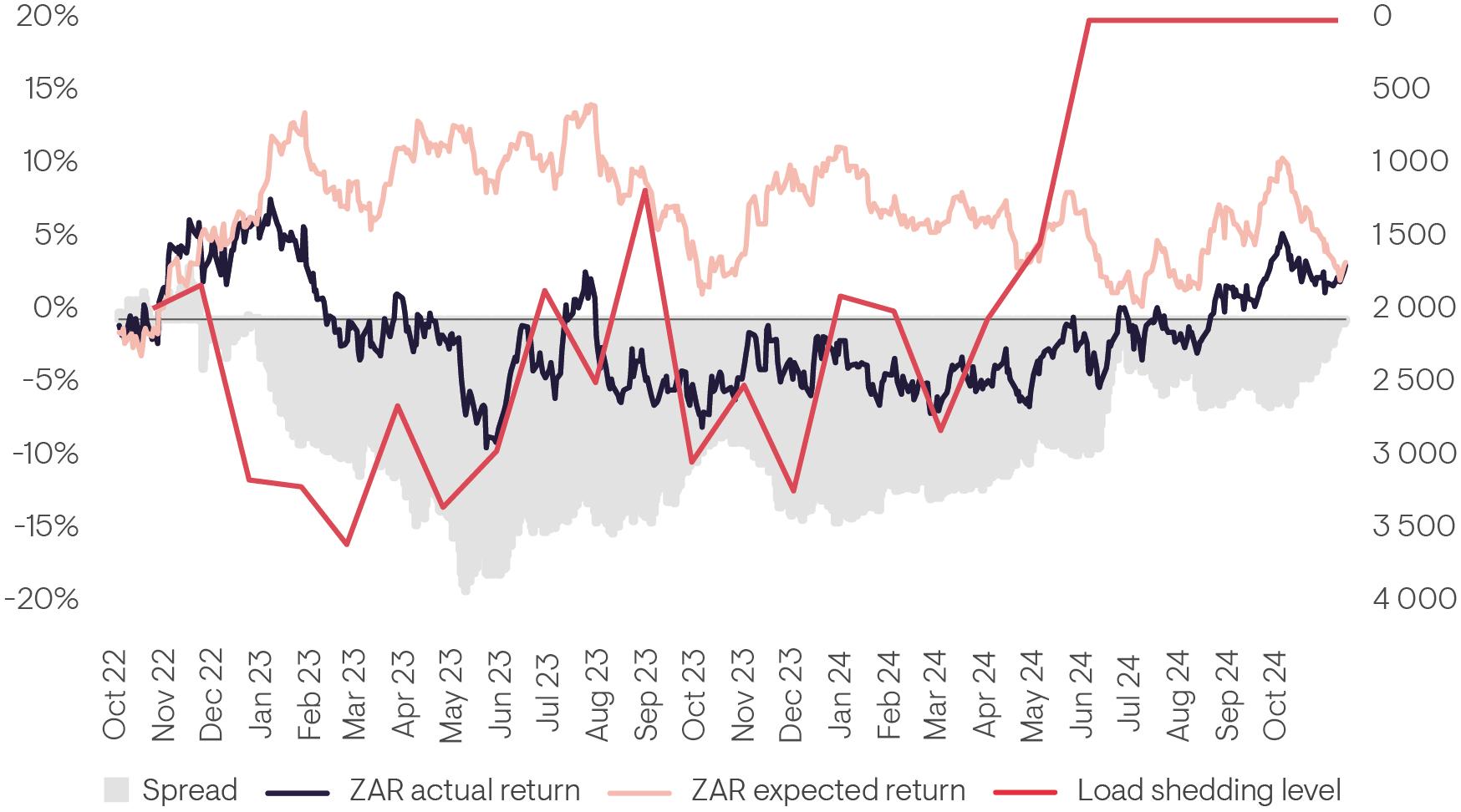

Rand bouncing back

Substantial improvements on the electricity front have helped the rand to recover. A staggering 75% of the rand’s underperformance over the last two years can be attributed to loadshedding. Figure 1 shows how the gap between the currency’s expected return and actual return widened dramatically as SA reached record-breaking levels of loadshedding in 2023. The peak of the rand’s underperformance was in May last year, but since then, the discount in the rand has steadily closed.

By Malcolm Charles Portfolio Manager, Emerging Market Fixed Income, and Sisamkele Kobus Economics Analyst at Ninety One

With the SA election out of the way and no loadshedding since late March, the rand looks fairly valued. We expect the currency to be more stable than in the past. Improving terms of trade, softer oil prices and stronger commodity prices also support the rand.

Infrastructure spend to provide much-needed ‘juice’ to SA economy

The government of national unity (GNU) delivered a pragmatic medium-term budget, vowing to get the debt-to-GDP ratio under control. This was in line with the fiscal consolidation path that National Treasury committed to ahead of the 2023 medium-term budget policy statement (MTBPS). In last year’s MTBPS, significant spending cuts were pencilled in to address revenue slippages. Ahead of the election, there was scepticism about whether politicians would give National Treasury the necessary space to maintain fiscal prudence. The GNU medium-term budget has stayed the course, with debt consolidation an essential strategy for putting government finances on a healthier footing. While the government will have to do some tap dancing to keep investors, rating agencies, and public sector unions happy, a better growth rate will go a long way to help South Africa out of the debt hole.

Finance Minister Enoch Godongwana outlined additional reforms to support public and private investments in growth-boosting infrastructure, with the MTBPS dedicating a chapter to this important issue. The GNU’s strong commitment to infrastructure investment was evident in the MTBPS. The

second phase of Operation Vulindlela[3] will build on this foundation, targeting critical infrastructure bottlenecks that stem from municipal capacity constraints. Areas of focus will still be along the broad categories of energy, transport, digital infrastructure and water. These initiatives will not only be a ‘life saver’ for communities and businesses but will serve as an important engine of growth. While public infrastructure spending has been largely absent over the last few years, the South Africa National Road Agency (SANRAL) has been carrying the infrastructure torch. The parastatal has reached for its wallet, allocating R26bn to essential road upgrades from its R42bn cash pile. Further tenders are in the pipeline. SANRAL’s infrastructure projects are already having a powerful multiplier effect across the broader economy, supporting job creation, local businesses, and community upliftment.

Can the GNU deliver growth?

It’s too early to tell whether the GNU has moved the growth dial. While there are some policy disagreements among the GNU parties, they are united in getting growth going. Our new system of governance has sparked competition and cooperation among ministers, which should ultimately benefit SA Inc. Some ministries now have a DA minister paired with an ANC deputy minister, and vice versa. They must cooperate to get results. But the GNU ministers are also in competition mode, as they need to sell their party’s service delivery success to voters in the next local and national election.

Figure 1: Loadshedding was the key driver of rand weakness

Source: Ninety One, Bloomberg and Deutsche Bank, 5 November 2024

This situation has created some healthy competition, and like fund managers, ministers must now worry about relative performance – how are they faring relative to their peers? Some ministers are already hogging the limelight. For example, Home Affairs Minister Leon Shriver is spearheading visa reforms to boost growth, while Trade and Industry Minister Parks Tau is forging a closer relationship with business, focusing on policy reforms that will help attract investments into the economy.

Benign inflation outlook and rate-cutting cycle bolstering the economy

Growth has been limping along this year, but decelerating inflation and a lower interest rate environment are helping to lift business and consumer confidence. Two-pot withdrawals are also providing a short-term boost to households. CPI inflation has remained comfortably within the target band, and we expect it to move lower, averaging less than 4% over 2025. This should give the South African Reserve Bank room to continue cutting interest rates. SA is now aligned with the global economic cycle for the first time in many years, which bodes well for local assets. Against this backdrop, we anticipate economic growth of 1.7% next year.

By Steven Amey Head: Intermediate Distribution, Ashburton Investments

A

supportive

environment for SA bond market

The favourable outlook for the rand, inflation, interest rates and growth supports our bond market. We believe the high yields on SA bonds sufficiently protect against the risks and represent good value over the medium to longer term. Income will remain an important driver of returns, with high yields offering investors the opportunity to earn returns well ahead of inflation.

In conclusion, South Africa is in a much better place than a year ago, but the GNU needs to ensure it delivers on its promises. Now that the electricity handbrake is being lifted, there’s every chance that South Africa will get back on track.

1 Ninety One and NERSA, September 2024.

2 NERSA and Eskom, July 2022 to June 2024.

3 Operation Vulindlela is a joint initiative of the Presidency and National Treasury to accelerate the implementation of structural reforms and support economic

Is my money still safe in South Africa? A resounding yes!

In the current economic climate, many locals may be wondering if their investments are safe in South Africa. Such concerns are understandable, given negative news reports about the South African economy, the rising cost of living for consumers, and large volumes of investment flowing out of the country.

The question to be asked is: Is South Africa still a safe place for regular South Africans to invest for their retirement? The answer is yes, it can be. There are challenges, but we see a lot of investment opportunity in South Africa. The sentiment may be surprising considering Ashburton’s recent announcement of a partnership with global investment powerhouse Morgan Stanley Investment Management to strengthen its global capabilities. The company, which is the Asset Manager of the First Rand Group, also recently made headlines for its strong performance on local equities through its purely South African equity fund. Only 62 local funds out of about 1 852 domestic unit trusts or Collective Investment Schemes (CIS) are 100% invested in local stocks.

There is reason to be positive about investing in SA right now

Investment sentiment is positive in SA at the moment. A global survey from Credit Suisse Group AG and the London Business School recently revealed that South Africa was the global leader in equity returns over a 117-year period, from the year 1900 to 2016, due to its commodity-rich nature. And while past performance is not always a predictor of future performance, we have many reasons to feel positive about investing in South Africa into the future.

Firstly, local interest rates were reduced in September and November, echoing similar cuts by the US Federal Reserve. Secondly, South Africa has had more than six months without loadshedding, and the local renewable energy industry is showing good growth – all of which is good news for producers who boost our economic development. Thirdly, we are seeing positive moves towards more privatisation in South Africa, especially with struggling stateowned entities like ESKOM and Transnet. In the local mining sector, we’ve also seen more than R170bn worth of new deals, mergers and acquisitions. Consumer confidence also

reached a five-year high, as the economy continues to recover from the COVID pandemic. And finally, it is very positive to see that 140 local CEOs recently committed to support the government’s economic reform targets.

The recent introduction of the two-pot retirement system, which allows South Africans to access the savings portion of their pension funds to provide relief from financial distress, was also good news for local pension fundholders, as it gives some financial flexibility to individual investors.

Achieving alpha with SA-only equities

The Ashburton Equity Fund, which has had a healthy exposure to smaller and mid-cap stocks over the past three years, managed to deliver 95bps per annum of positive alpha over the benchmark FTSE JSE Capped SWIX. The Fund is invested in companies such as Grindrod, AlexForbes, Massmart, Raubex and WBHO.

In general, we are very positive about the long-term investment prospects of our local equities. We have also made the decision to pivot our strategy, with our equity fund now being 100% invested in SA equity in 2024.

Figure 2: More rate cuts are on the table SA inflation and interest rate expectations

Forecasts are inherently limited and are not a reliable indicator of future results.

Source: Ninety One, October 2024

recovery. Operation Vulindlela aims to modernise and transform network industries, including electricity, water, transport and digital communications.

Social protection was always meant to be in the plan – where did it all go wrong?

Acritical regulatory gap is undermining the risk-pooling principles that medical schemes are built on – principles designed to maintain affordable membership fees through crosssubsidisation and social solidarity. “Medical schemes, as not-for-profit entities, operate under tight constraints to meet members’ healthcare needs. Over time, regulations supporting the Medical Schemes Act 131 of 1998 have either failed to materialise or become outdated,” says Naidoo. “As a result, the 9 million South Africans funding their healthcare through medical scheme contributions are struggling to afford this cover.”

Childs notes that schemes face financial risks because reforms intended to accompany the Act were never implemented. “Since 2000, attention has been diverted to the NHI, overshadowing reforms in the current system that could reduce costs and extend private healthcare access to millions, well before the NHI can deliver these crucial services,” he says. “The principles of open enrolment and community rating were meant to ensure equitable protection for all members, guaranteeing access to Prescribed Minimum Benefits [PMBs],” Childs adds.

“What we are seeing in medical scheme increases for 2025 so far reflect the cumulative effect of regulatory neglect since 2000”

By Barry Childs Actuary at Insight Actuaries and Consultants, and

Insight Actuaries and Consultants found that over 22 years, Gross Contribution Income (GCI) per life per month for schemes rse by 8.2% annually, compared to a 5.5% annual increase in the Consumer Price Index (CPI). Keeping contributions in line with CPI would have made schemes 43% cheaper today.

The impact of Covid

Christoff Raath of Insight Actuaries has observed that a contributing factor to 2025’s contribution increases stems from the Covid era, when medical schemes experienced surpluses due to decreased utilisation. In accordance with the Medical Schemes Act, schemes temporarily lowered contributions or enhanced benefits to return these surpluses to members. This led to deliberate losses, as trustees worked within legal constraints to ensure reserves were gradually redistributed. By 2022, schemes’ finances began normalising, with losses reflecting this strategy. Although data for 2023 is not yet public, most schemes are back to pre-Covid reserve levels, resulting in schemes having to adjust contribution increases in the interest of sustainability, according to Raath.

Furthermore, data indicates that when healthcare consumers eventually returned to healthcare facilities post-Covid, they were often in poorer health, leading to significantly higher treatment costs. Various healthcare studies, such as those from the South African Medical Research Council (SAMRC), have reported this phenomenon.

The result of regulatory neglect

The other major contributor to this gap is the regulatory limitations that prevent medical schemes from being able to contain the utilisation increases of a medical scheme population that is ageing, and this drives up costs that in turn discourages new entrants from joining the scheme.

“Late joiner penalties are among the measures designed to protect the interests of the members who contribute throughout their working lives, thereby supporting the intended social solidarity framework; however, even these measures have not been adequate.” Childs points out: “Anti-selection is a major cost driver for medical schemes, because

Thoneshan Naidoo Chief Executive Officer of the Health Funders Association (HFA)

the lack of regulatory completeness does not adequately deter people from joining medical schemes only when they need to access high-cost treatments, then leaving the scheme having used more funds than they contributed. For this reason, many open schemes must apply underwriting – that is, waiting periods for new applicants before they can claim for certain categories of benefits, within the regulated constraints.

“Had a risk equalisation fund been established, as intended to help schemes offset costs for sicker and higher risk members, this would have served as a buffer against the high contribution increases that deter younger members,” Childs says. “What we are seeing in medical scheme increases for 2025 so far reflect the cumulative effect of regulatory neglect since 2000, when a change in policy direction meant that the much-needed remaining pillars of social solidarity were never implemented.”

Urgent changes needed

The overdue regulatory reforms and lack of regular reviews of PMBs have escalated costs for all members. Despite this, medical scheme benefits remain invaluable for families and alleviate pressure on the public health sector. “Social security is the backbone that health funding seeks to achieve, fully considering the economic importance of promptly available quality medical care for the workforce, extending into retirement. In the private health funding realm, medical scheme members support each other by paying contributions, and the country by funding public health services they do not use, freeing up capacity for those reliant on the state,” Naidoo says.

“The implementation of the Health Market Inquiry’s recommendations, which identified opportunities to address inefficiencies that inflate costs and promote affordability, would attract young, healthy members to help balance the higher healthcare costs of older members. This would reduce membership costs for everyone, extending private healthcare benefits to more South Africans,” Naidoo notes. “The HFA continues to advocate for urgent progress to address regulatory gaps, restore affordability, and uphold social solidarity principles to positively impact healthcare for all South Africans,” he concludes.

As an independent DFM, we empower you to prioritise your clients and business growth with our optimised, advice-led solutions.

Guide your clients to set effective financial goals

By Sandy Welch Editor, MoneyMarketing

Solid financial goals are one of the key steps to achieving financial stability and long-term prosperity. As a financial adviser, your role in this process is pivotal. You act as a guide, mentor and strategist, helping clients identify their aspirations and map out realistic plans.

1 Understand your client’s values and priorities

Every financial goal is tied to personal values and life priorities. Before diving into the numbers, spend time understanding what matters most to your client. Is it financial security for their family, early retirement, travelling the world, or building a business? Encourage your clients to think deeply about their ‘why’. Why do they want to save? Why is financial freedom important? This conversation helps ensure that their goals are meaningful and aligned with their life aspirations.

2 Conduct a comprehensive financial assessment

Before setting goals, it’s crucial to understand your client’s starting point. Conduct a thorough financial review that includes:

Income and expenses

Savings and investments

• Debt levels

• Insurance coverage

• Retirement savings.

This assessment not only highlights gaps but also identifies opportunities for improvement. For instance, if a client’s expenses exceed their income, focusing on budgeting and debt reduction might take precedence before setting long-term savings goals.

3 Encourage SMART Goals

The most effective financial goals are SMART: Specific, Measurable, Achievable, Relevant and Time-bound.

• Specific: Goals should be clear and welldefined. Instead of saying, “I want to save money”, a specific goal might be, “I want to save R500 000 for a down payment on a house”.

• Measurable: There should be a way to track progress. For example, if the goal is to save R500 000, clients can track monthly or yearly contributions.

• Achievable: Goals should stretch clients but remain realistic given their financial situation.

• Relevant: Ensure the goal aligns with their broader life priorities and values.

• Time-bound: Every goal needs a deadline to create urgency and accountability.

4

Categorise goals by time horizon

Help clients organise their goals into shortterm, medium-term, and long-term categories.

• Short-term goals (1–3 years): Examples include building an emergency fund, paying off highinterest debt, or saving for a vacation.

• Medium-term goals (3–10 years): These might include saving for a child’s education, buying a home, or funding a significant life event.

• Long-term goals (10+ years): Common longterm goals include retirement planning, wealth accumulation, or creating a legacy.

Breaking goals into these time frames helps clients prioritise and manage their resources effectively.

5 Create a personalised financial plan

Once goals are established, the next step is creating a financial roadmap. This plan should outline the steps, timelines and resources needed to achieve each goal. Key elements of the plan might include:

• Budgeting: Ensure clients allocate funds toward their goals. A ‘pay yourself first’ strategy can help prioritise savings.

• Debt management: Help clients reduce high-interest debt, freeing up resources for future goals.

• Investment strategy: For medium- and longterm goals, create an investment plan that aligns with their risk tolerance and time horizon.

• Insurance and protection: Ensure they have adequate insurance to safeguard against unforeseen risks.

6

Discuss flexibility

Life is unpredictable, and financial goals may need to be adjusted over time. Whether it’s due to unexpected expenses, a job loss or new opportunities, it’s important to remind clients that flexibility is a key part of financial planning. Encourage clients to regularly review their goals and progress. Reassess their financial situation annually or after significant life changes, such as marriage, the birth of a child or retirement.

According to Momentum Financial Adviser, JJ van Wyk, establishing a routine to assess financial progress is essential. That means regular reviews, either monthly or quarterly, to ensure plans align with financial goals and current reality. “Annual reviews and a financial needs analysis with a financial adviser are a must,” says Van Wyk.

“Provide education, break big goals into manageable steps, and celebrate small wins along the way”

7

Address emotional barriers and mindset

For many people, achieving financial goals is as much about mindset as it is about numbers. Fear, procrastination, or a lack of financial literacy can prevent clients from taking action. As an adviser, you can play a critical role in building their confidence and overcoming these barriers. Provide education, break big goals into manageable steps, and celebrate small wins along the way. Additionally, encourage clients to avoid lifestyle inflation – the tendency to increase spending as income rises. Remind them of their long-term goals and the importance of staying disciplined.

8

Leverage technology and tools

Technology can be a powerful ally in helping clients track and achieve their financial goals. Introduce them to budgeting apps, investment platforms, or financial management software that simplifies the process. Many tools allow clients to automate savings, set reminders and monitor their progress in real-time. Automation, in particular, is a game-changer – it reduces the temptation to spend and ensures consistency.

9

Measure progress and celebrate milestones

Regular check-ins with your clients are essential. Review their progress, adjust strategies as needed, and celebrate milestones. Achieving even small goals can provide a psychological boost and motivate clients to stay on track. For example, if a client has successfully built an emergency fund or paid off a credit card, acknowledge their accomplishment. Positive reinforcement can strengthen your relationship and inspire them to pursue bigger goals.

10 Emphasise long-term benefits

Remind clients of the long-term benefits of setting and achieving financial goals. These benefits go beyond monetary gains – they include reduced stress, financial independence and the ability to live a life aligned with their values. By consistently reinforcing the ‘big picture’, you can help clients stay focused and motivated, even when challenges arise.

Remember, your role extends beyond numbers – it’s about inspiring confidence, fostering discipline and helping clients achieve their dreams. It’s an opportunity to build trust and loyalty, ensuring a lasting and successful partnership.

By Michelle Noth Head: Financial Intermediaries Channel, 10X Investments

Financial planning in focus

At 10X, we recognise that financial advisers are under pressure. Running a successful, independent financial advice practice involves carefully striking a balance between seeing and advising clients, and managing and growing the business. The former is what generally attracts people to the industry. The latter is becoming more challenging due to multiple factors like increased regulation and the need to adopt technology to remain competitive.

“We’re all struggling with the same things when it comes to practice management,” Elke Zeki, director at Foundation Family Wealth, said during a panel discussion at the 10X Think Investing convention 2024. “What’s breaking the camel’s back is the combination of all of them. They take a lot of time and effort. A lot of independent advisers are owner-managed, and that means you end up spending time and energy doing something you are not, typically, good at. I often find that sometimes more than half my time is spent working on the business as opposed to working in the business, and that’s not sustainable.”

DFMs are looking at how they can help practices to thrive.

Kathryn van Dongen, Group COO of Carmel Wealth, said that the industry needs to find innovative ways to address these challenges.

Carmel Wealth’s approach is to invest in a diverse range of reputable, independent practices and offer them quality business support. “The business model is to respect the independence of the advisers as sacrosanct,” Van Dongen said. “We create very tailored solutions based on what a practice needs and how we can help. We do that without comprising independence when it comes to product choice, losing brand identity, or the adviser’s ability to run their own business.” She said that the biggest practice management challenge IFAs encounter is around succession planning.

“I think that’s because it’s really hard to get right,” Van Dongen said. “It can be complicated, take a very long time, and there isn’t a one-sizefits-all solution. Every independent FA practice is like an evolving living organism with different aspirations, and a succession plan needs to be fitted to that specific business.

“Most of the options available to solve for succession planning needs haven’t fitted independents very well. The current models tend to rely very much on vertical integration into a larger, product-led organisation, meaning that to find succession or growth capital comes with some form of compromise to independence.”

A second significant issue she has seen is the massive growth in the need for advisers to have proper tech enablement, where one such example is having proper cybersecurity protections in place. “Even really good practices don’t necessarily have good enough cybersecurity infrastructure,” Van Dongen said. “We recently assisted in addressing this for one of the companies 100% owned by Carmel Wealth, and it took significant research to figure out what a good standard and operating model looks like.

“We had to navigate providers, do due diligence on them, negotiate pricing, and implement the solution. The bill came to a few hundred thousand rand, but the cost wasn’t the biggest issue. It was the time involved. When do the leaders of these practices, who are often attracting and retaining clients themselves, find the time to address something as complex as cybersecurity?”

This challenge is precisely why independent firm Galileo Capital made the decision recently to hire an experienced chief operating officer. “For a small business, it’s phenomenally expensive if it’s a good resource, but it’s an investment in the future of the business,” said Warren Ingram, co-founder of Galileo Capital.

Many independent advisers are also finding support from discretionary fund managers (DFMs), who are increasingly offering a range of services beyond their core investment expertise. These including marketing, compliance and technology.

“For us, it is about time and expertise,” Zeki said. “We are very good at building relationships with clients and helping clients understand what their needs are. For us to spend our days understanding funds and doing due diligence on managers is just not conducive to building sustainable business.”

Ingram added that Galileo Capital had shied

away from using a DFM for some time because they viewed it as an additional cost to the client. But with DFMs reaching scale and being able to negotiate better fees with managers, that is less the case.

“I think that DFMs are starting to add value,’ Ingram said. ‘The ecosystem they can provide in addition to the pure multi-management function is valuable.”

Van Dongen said that there has clearly been an evolution within the industry, with DFMs now looking to enable advice practices to scale up and be more efficient in the planning process.

“It’s not just investment management anymore,” she said. “DFMs are looking at how they can help practices to thrive. But what’s important is that those peripheral services shouldn’t come at the cost of the clients’ investment outcomes. Because if a client could get a better investment solution somewhere else, but the practice is getting all the benefits of the DFM’s business support, you have a moral dilemma. How do you replace your DFM if your practice is operationally reliant on them, but your client is not getting what you deem to be the best investment solution for them?

“It’s clear there is an acute need that has been solved. It is so expensive and time consuming to run a practice that doesn’t have scale. Independent advisers need support, and DFMs have offered one way of doing that. But I think we also need to look at innovative options for solving that need in different ways.”

10X Investments takes pride in being a trusted partner to financial advisers, providing low-cost, high-quality funds designed to support their vital work. By offering efficient and reliable investment solutions, 10X empowers advisers to focus on what they do best: guiding their clients toward a secure and prosperous financial future.

By

Choosing the right CRM for your financial advisory business

Choosing the right Customer Relationship Management (CRM) system for your financial advice business can feel overwhelming. With so many options available, it’s easy to feel lost in the jargon and features. However, finding the right fit isn’t about chasing the fanciest tool on the market. It’s about understanding your business and choosing a CRM that helps you achieve your goals.

Recently, I had a conversation with a financial adviser who had spent considerable time reflecting on their business and technology needs. This clarity allowed them to select tools that worked for their team and supported their vision. Inspired by this discussion, I’ve put together a guide to help you think through the important questions.

Start with your business needs

Before diving into the world of CRMs, it’s essential to understand your business. Think about:

• What do I need the CRM to do? List your nonnegotiables such as client management, data tracking, or seamless communication.

• What’s my work style? Do you need a system that accommodates remote work, integrates with existing tools, or provides a collaborative platform?

• What’s critical for my success? Pinpoint the features that will genuinely make a difference versus those that are nice to have.

Clarity about your business will help you evaluate CRMs based on what truly matters.

Focus on collaboration

For many businesses, collaboration has changed significantly in recent years. Teams often work remotely or in hybrid setups, making

it critical to consider how you and your team will work together. Think about:

• Document sharing: Do you need realtime collaboration on documents? Some CRMs allow multiple users to edit and view documents simultaneously.

• Communication: Does the CRM offer tools for easy team communication? Features like inplatform messaging or task assignments can be valuable.

• Integration: Will the CRM work seamlessly with tools like email or file-sharing platforms? Having everything in one place can simplify workflows.

By having a clear picture of your ideal way of working, you can choose a system that supports effective teamwork.

Consider record-keeping

A CRM’s ability to handle records is crucial. But it’s not just about storing information; it’s about maintaining and using it effectively. Think about:

• What do I need to record? Consider the types of client information you handle, such as contact details, meeting notes, or financial goals.

• How will I use this information? Will it feed into reports, client communications, or compliance checks?

• Is it easy to update? Ensure the system allows for quick and straightforward updates, so your data stays current and accurate.

A well-organised CRM can become the backbone of your client interactions.

Simplify communication management

One common frustration among advisers is juggling emails and client communications across multiple platforms. A good CRM can help consolidate and organise this. Think about:

• Email integration: Does the CRM integrate with your email system, whether it’s Outlook, Gmail, or another platform?

• Tracking conversations: Can you easily log and retrieve past communications with clients?

• Notifications: Will the CRM remind you of follow-ups or upcoming tasks?

Streamlined communication management can save you time and ensure a professional experience for your clients.

Ensure secure access to information

Client data is sensitive, and keeping it secure should be a top priority. When assessing CRMs, consider:

• Access control: Can you limit access to specific information based on roles within your team?

• Data security: Does the CRM provide encryption or other measures to protect client data?

• Compliance: Is the system compliant with South African data protection laws?

These features are particularly important if your team works remotely or if multiple users need access to the CRM.

Understand industry-specific needs

Not all CRMs are built with financial advisers in mind. If you rely on platforms like Astute, you’ll need a CRM that integrates with it. This might rule out popular systems like HubSpot or Zoho. By understanding your requirements (nonnegotiables), you can focus on options that genuinely meet your needs.

Remember, the goal isn’t to find the flashiest CRM but one that aligns with your business and supports your growth. There’s no single ‘best’ CRM – only the best one for your business. Stay curious!

Francois du Toit CFP® PROpulsion

You are the gatekeeper

Compiled by Sandy Welch

According to the World Economic Forum Global Risks Report 2024, cyberattacks now rank fifth in the global risk landscape, at a staggering 39%. The cost of global cybercrime is expected to reach $9.5tn by the end of this year, according to Cybersecurity Ventures. Small businesses are particularly vulnerable, with nearly half of all cyberattacks targeting this sector, many of which do not survive the aftermath of a breach.

The Mimecast’s 2023 ‘State of Email Security’ report identifies data breaches as a bigger risk than climate change, with South Africa ranking sixth on the list of countries most affected by cybercrime. Interpol’s African Cyberthreat Assessment Report 2022 revealed a total of 230 million cyber threats were detected in South Africa, out of which 219 million, or 95.21%, were email-based attacks. And businesses –regardless of size – are alive to the threat. The 2023 Santam Insurance Barometer Report showed a 12% increase in the number of commercial respondents who cited cybercrime within their top five risks.

Cybercrime expert Dr Craig Pederson says, “In the last seven years, we’ve seen a dramatic increase in both the volume of cybercrimes and the variety of types of cybercrime perpetrated in South Africa. In fact, South Africa is very close to being considered the cybercrime capital of the world.”

Cybersecurity is essential for a financial adviser’s software systems because it protects sensitive client data, ensures regulatory compliance and maintains trust. As your business handles highly confidential information such as personal identification, income details, investment portfolios and banking data, a breach could expose this data to theft or fraud, causing significant financial and reputational damage.

For clients, trust is paramount. Any lapse in cybersecurity undermines confidence in the adviser’s ability to safeguard their financial interests. Implementing strong cybersecurity measures – like encryption, multi-factor authentication, regular updates, and employee training – ensures a secure digital environment, safeguarding both the adviser’s business and their clients' financial wellbeing.

Joe Szemerei, Chief Operations Officer (COO) of financial services provider Indwe Risk Services (Indwe), emphasises the growing risk: “Businesses need to be more vigilant now than ever, as cybercriminals are increasingly finding new and innovative ways to bypass security measures. Cybersecurity should be a priority for every organisation, regardless of size, and it requires proactive risk management.”

“As African markets continue to evolve, grow, and become highly digitalised throughout the customer journey, we see the imperative for businesses to integrate advanced fraud prevention mechanisms to safeguard both their operations and their clients,” says Grozdana Maric, Head of Fraud & Security Intelligence, EMEA Emerging and Asia Pacific at SAS. Employees are also increasingly targeted by scammers who use a variety of methods to manipulate them into revealing sensitive information, says Pederson, granting unauthorised access, or making payments to fake accounts. For instance, many businesses have reported scammers impersonating legitimate vendors that the company regularly deals with, submitting fake invoices or altering banking details on actual invoices. This often results in funds being transferred into scam accounts.

Regulatory frameworks like GDPR, POPIA, and others require stringent data protection practices. Non-compliance can result in hefty fines and legal consequences, making robust cybersecurity measures non-negotiable. Additionally, cyberattacks such as phishing, ransomware or malware can disrupt operations, leading to downtime and loss of productivity.

The rise of cyber threats

In 2024, Business Email Compromise (BEC) tops the list of cyber threats, with a 20% rise in BEC scams this year, Szemerei says. AI-generated BEC content is responsible for nearly 40% of such attacks, with fraudsters increasingly using artificial intelligence to impersonate internal communications and deceive employees.

Cloud-based systems, while highly beneficial, are another area of vulnerability. Cybercriminals can easily penetrate weak firewalls, exposing sensitive information. Additionally, the rise of AI tools – many available on platforms like GitHub – makes it easier for attackers to automate phishing, malware, and Distributed Denial of Service (DDoS) attacks.

Common cyber threats