A simple, low-cost investment to achieve hardcurrency returns in either US dollars or sterling; the Global Cautious Fund; maximising a living annuity offshore; and investing in Cyprus.

Page 14 – 19

TRUSTS

Are you fully up to date with the latest amendments when it comes to Trusts?

Page 20

NATIONAL WILLS WEEK

This annual event is the chance for advisers to touch base with clients to ensure their wills – and succession plans – are in place. Here are our tips to maximise the potential.

Page 22 - 23

INSURANCE

Are FAs offering clients the best options when it comes to life and funeral policies?

Page 28 - 29

The Two-Pot System and the value of good advice

BY SIOBHAN CASSIDY MoneyMarketing Contributor

By giving access to some of their retirement savings while enforcing the preservation of the rest, South Africa’s new Two-Pot Retirement System, effective from 1 September, goes some way to reconciling two potential crises (immediate and future) for savers. Much has been said about the dangers of allowing access to a third of savings; less about the benefits of enforced preservation of the remainder. Although, according to some experts, the potential is revolutionary.

After 1 September, retirement fund contributions will be separated into two pots, two-thirds in a Retirement Pot and a third in a Savings Pot. Savers will be obliged to use the Retirement Pot to buy an annuity to provide retirement income; funds in the Savings Pot can be accessed via one withdrawal per tax year of a minimum of R2 000. The changes are not retrospective, which means a third pot, the Vested Pot, for those with savings accumulated before 1 September, will be subject to the old rules.

Withdrawals from the Savings Pot will be taxed at the member’s marginal income tax rate, which could even push an individual into a higher tax bracket. A second potential tax impact is on the R550 000 a saver is allowed to withdraw tax-free at retirement. Depending on withdrawals you have made, this benefit could be reduced.

“Investors need to understand the actual cost of access”

Positive or negative?

Many have warned that allowing access to savings will undermine an already shaky system and potentially encourage an annual raid on the Savings Pot. Jacques Zaayman, Group Director at Prime Investments, the Johannesburg-based fund and product services provider, says, “In an investment where long-term real returns are in the single digits, allowing a double-digit withdrawal annually is akin to borrowing from your future with almost no prospect of being able to repay yourself.”

As Pieter Koekemoer, head of Personal Investments at Coronation Fund Managers, has said: “While it is great to have this option in the event of genuine financial hardship, we believe investors need to understand the actual cost of access.” He explained that every R1 accessed early could cost savers up to R30 at retirement in nominal terms. “While the numbers become less dramatic when you shorten the period between early access and retirement, they remain retirement-defining. Even for an individual making an early withdrawal 10 years before their intended retirement date, it would still cost them R3 in lost retirement benefits for every R1 taken out early.”

The enforced preservation part of the two-pot system means that savers, who have historically been allowed to cash out 100% of their savings in their company fund on leaving a job, will no longer have this self-defeating option. Prime Investments’ Zaayman says this narrows one of the biggest holes (if not the biggest) in a rather leaky system: cashing out when changing jobs.

According to data from Coronation, more than 10% of members of workplace retirement funds withdraw all their savings when changing jobs. “According to National Treasury, the net result of this leakage is that more than 60% of retirement fund members had accumulated pension pots of less than R50 000 in 2020. Put another way, the average fund member resets their retirement savings balance to zero every eight years in a system that enables compound growth to do its magic over three or four decades.”

“This action represents the most significant destruction of value and has a negative multiplier effect,” says Keri-lee Edmond, Analytics and Insights Manager at Old Mutual Corporate Consultants.

Continued

Indexation: Anything but Passive.

Indices can be actively designed, like our Factor Range

Indices can be geographically diversified, like our Global ETF Range.

Indices can be optimally designed like our Multi-Asset Range.

Indices can be designed to target themes, like our Thematic Range

While indices can take many di erent forms, all are transparent and low-cost.

Take control of what you’re investing in by incorporating indexation into your portfolio.

Contact us to learn more at institutional@satrix.co.za.

Continued from page 1

According to Palesa Mokoena, Technical Support Specialist at Glacier Business Development, the resignation rules under the two-pot retirement system present a major change for members of pension and provident funds who have become accustomed to the current system, which allows for full withdrawals each time they change jobs or leave their employer. “Many members may not be familiar with the concept of preservation and the workings of preservation funds,” she says. “Members who resign from their employer will therefore require financial education and support from their employers, funds and financial advisors in order to navigate their options under the two-pot retirement system, understand the implications for retirement savings, and make an informed decision.”

A doomed savings mentality

South Africa’s retirement savings crisis is well documented. Too many workers put off saving as long as they can, save at the lowest possible rate, and cash out their savings at the first opportunity. According to Treasury figures, which are borne out every year by the 10X Investments Retirement Reality Report, only 6% of South Africans can afford to preserve their lifestyle in retirement.

For many living in crisis, this talks to a problem for another time. The Covid-19 pandemic magnified and focused attention on a more immediate crisis. Many South African workers, who were putting their children to bed hungry and could not afford to educate them, were aware of a pot of money somewhere with their name on it: their retirement savings, which they could not access in even the most dramatic of crises.

It is not surprising that, as Edmond says, “in the time of Covid-19, we saw many South African employees resigning from their jobs, or couples going as far as to get divorced, simply to access their retirement funds in order to support their immediate financial needs”. She adds, “The ingenuity of the two-pot system lies in its ability to acknowledge the need for immediate financial access, reflecting our socio-economic reality, while still safeguarding long-term retirement goals. This marks a momentous shift in conventional thinking, and one which we believe will have a significantly positive effect on retirement outcomes into the future.”

Experts recommend saving 10 to 15 times one’s annual salary to provide a retirement income of 70-75% of previous income. Edmond says typical members of provident or pension funds save only 2.7 times their annual salary, and points to Old Mutual’s

analysis showing that the new system could enable workers starting to save at age 25 to amass retirement savings of two to three times more than that. She explains that the research indicates that the two-pot system could enable South Africans to save up to 9.5 times their annual salary by retirement, even if they use the entire savings component. If no withdrawals were made, savings could reach around 14.5 times annual salary, she adds.

Advisers will have a lot more to worry about than persuading people not to dip into their retirement savings. They will need to help clients understand the probabilities, the possibilities and the consequences of various choices. There is also potential for advisors to play a role in expanding the pool of savings. Prime Group’s Zaayman says the change really shines a light on the value of affordable and effective financial advice. And, as Keith Peter, Advice Manager at Old Mutual Personal Finance, has said: “For advisers, this is a chance to deepen customer relationships and improve financial outcomes for retirees.”

What’s the prognosis?

The two-pot system is likely to change the way South African workers view retirement saving. Research by Old Mutual Corporate, for example, shows that 40% of members will consider increasing retirement fund allocations after September 2024 due to the two-pot system. “This suggests that the perceived opportunity cost of investing in a retirement fund is now reduced, and members see the value of investing more, as they can access this money in an emergency,” says Samantha Jagdessi, Head of Advice & Best Practice at Old Mutual Corporate Consultants. John Anderson, Executive for Enablement and Solutions at Alexforbes, has noted that new system “enables saving with specific goals in mind, which has been shown to increase savings commitments”.

Advisers and the industry have their work cut out to encourage clients to leverage the best of the new system while avoiding any pitfalls.

Ideally, workers will save as much as they can in their retirement funds, thereby accessing many benefits. These include tax breaks and tax-free growth and, in the case of corporate funds, lower fees than on individual investment products. Should savers need to access some of their funds for a crisis or, indeed, a priority such as a child’s education, they can do so. If they should happen to not need to access their savings, they get the benefit of a very healthy retirement fund.

ED’S LETTER

September is a big month for the financial services industry this year, as the reformed retirement fund regulations kick in. It’s most certainly going to have an impact on financial advisers. While the industry has been doing an incredible job trying to educate and inform consumers of their options, people tend to believe that most things don’t specifically apply to them until they realise that they do. It’s also a complicated system to initially grasp – especially as although it’s referred to as the “two-pot system”, there are three pots not two, and different regulations apply if you were over 55 on a certain date. There are some false beliefs out there, including that people will be able to withdraw all their retirement savings on 1 September. I foresee advisers having to field a lot of questions and possibly counsel some disappointed clients.

While our cover story is aimed at helping you, as FAs, to fully comprehend what’s happening in the industry, we also want to help you educate your clients. To support this process, together with Glacier by Sanlam we’ve compiled a handy digital booklet that you can download and share with your clients – or even just share the link via email. We’ve tried to break down the new system in as simple terms as possible and provided answers to some of the most asked questions. The booklet will also be available in printed form from the next issue.

We’re also looking at Wills Week in this issue, and specifically the opportunities that exist to engage with your clients around this time to ensure their wills are up to date and their beneficiaries on all policies clearly named. Do your clients fully understand issues such as inheritance tax, succession planning, the job of an executor? Is their life insurance up to date or are there changes that need to be made to meet their current circumstances? It’s a great time for some September policy spring-cleaning.

Stay financially savvy,

SANDY WELCH Editor, MoneyMarketing

RYAN BASDEO

HEAD: INDEX PORTFOLIO MANAGEMENT, 1NVEST

How did you get involved in financial services –was it something you always wanted to do?

My journey into financial services wasn’t planned and neither would I call it a natural progression. I spent a bit of my youth uncertain about my long-term career plans. It was rather difficult trying to decide on a lifelong career path when I was young and had little exposure to the working world. Growing up, I had a vested interest in the environmental and wildlife landscape, which may have been sentimentally driven by my childhood memories. But, as I began to bring the puzzle pieces of my life together, I sought guidance from my parents on a way forward and that is when I started to make sense of my career aspirations. I stayed open to feedback from those with more experience and stayed attuned to the doors that opened. The combination of structured guidance and my natural competitiveness with wanting to do

my best in any task on hand, landed me on the path to building a career in the financial services industry. The industry has been a great fit for me. I am grateful to the efforts, guidance and sacrifices that my parents made to afford me opportunities to explore any path I chose.

What was your first investment – and do you still have it?

I think the typical answer for this question may be the purchase of my home, but I have a slightly different view to what’s perceived as an investment. I do believe that an investment should put money back into your pocket and if we are honest with ourselves, our homes usually demand more money from us initially. If I were to take a different view, I would say that my first investment was the upskilling and continuous education that I undertook. Through this, I was able to remain a valuable asset to the firm.

“South African government bonds look attractive at the moment. These are paying real yields for a less risky asset class”

In terms of a monetary investment, I would say my first rental property – something I was able to get funding for. It was what some may define as a ‘value’ trade. I had pinned it on the potential development that would take place in the area. When that materialised and property prices rose to where there was a high enough opportunity cost to placing proceeds in less admin-intensive and less risky assets class, I sold the property and no longer have the investment.

What have been your best – and worst –financial moments?

Let’s start with the worst. At some point in my career, I used to be a Market Maker, effectively running proprietary trading book s . There was a point in time when the software failed me, which resulted in a very large trading loss that was partly my fault for not monitoring it more tightly. It was a very tense period of investigations to prove the software did not do what it was meant to, which

saved my job. My best would be having worked on a transaction that added a lot of value to the group, where every door was being closed and it had been given up on. I was described as a “bulldog latching on to a bone” and continued to look for a way to get it done – and it did happen eventually. It is a great feeling to provide value to the organisation and, in turn, build a good and credible personal brand in a business.

What are some of the biggest lessons you have learnt in and about the finance industry?

Persistence, along with patience, is key. We all want to have quick leaps in success in everything that we do. I have learnt that one must stay consistent to be able to accept short-term disappointments, but persist in making incremental improvements – and there will be a pinnacle that will eventually emerge. I think one can probably find a few Rocky quotes to better articulate this point.

What makes a good investment in today’s economic environment?

South African government bonds look attractive at the moment. These are paying real yields for a less risky asset class. In the longer term, I have always been a fan of the tech sector. I feel this is where invention occurs and eventually becomes mainstream technology once brought to scale.

What finance/investment trends and macroeconomic realities are currently on your watchlist?

I’m on the lookout for a supportive interest rate cutting cycle, as well as looking at the US economy, which is showing signs of a sustained recession and government debt management. All will determine my risk appetite for the short to medium term.

What are some of the best books on finance/ investing that you’ve ever read — and why would you recommend them to others?

A very novice one, but one that any youngster should start off with, would have to be Rich Dad, Poor Dad by by Robert Kiyosaki. Another would be A Random Walk down Wall Street by Burton G Malkiel. Lasty, one that isn’t directly related to finance but very much linked to encourage good discipline, which is key to good investing, is Atomic Habits by James Clear.

What will it take for foreign investors to overweight South African equities?

BY JAN-DAAN VAN WYK Stonehage Fleming Investment Management Associate Director

The South African euphoria trade is not over yet, and the figures show that foreigners are nibbling in South Africa’s financial market. While the equity market is still experiencing net negative flows this year, the dial shows signs of a shift in the bond market.

South Africa’s foreign investment in the stock market has steadily declined since 2005, when active Global Emerging Market (‘GEM’) investors held 9.3% of their emerging market portfolio in South African assets, according to SBG Securities research and EPFR data. Since then, exposure has declined to less than 2.7% - more than two-thirds lower than the peak almost two decades ago.

When considering this positioning within active strategies, one has to account for the decline in SA equity representation within the MSCI Emerging Markets (‘EM’) index. Changes in active investors’ appetite for South Africa’s assets would signal a fundamental shift in sentiment. Passive investors invest based on the country’s weighting in the underlying index as their performance is intended to mimic that of the index.

Many factors are driving the size of SA within the EM index, but if stronger share price performance begets inclusions into the index and SA grows in significance, this would prompt passive flows into SA equities. This year’s upcoming MSCI index reviews in mid-August and mid-November should provide early indications.

According to Prescient Securities research based on JSE settlements data, the government bond market experienced the strongest net inflows in recent years in July, after treading water in May and June and net selling by foreigners earlier this year. However, National Treasury data reflect that the holdings of outstanding domestic government bonds are still significantly lower (25.0%) than when these holdings averaged around 40.2% in 2018.

So, what will it take to really shift the dial on South Africa?

Over the past decade, the national government has been long on promises and short on delivery. This has given rise to anemic growth weighed down by loadshedding and logistical constraints,

“The government bond market experienced the strongest net inflows in recent years in July”

which the errant implementation of structural reforms has been slow to ameliorate. We believe that a sustained shift in the vector of big-ticket economic data, such as at least two to three quarters of strong economic growth numbers, may start to dent this skepticism.

Ongoing fiscal prudence will also be crucial, and there has been good progress in this regard. For the fiscal year ending March 2024, National Treasury recorded the country’s first primary surplus since 2009. Additionally, national revenue and expenditure continues to meet expectations set by National Treasury during the budget in the first three months of the fiscal year to end June.

An improved growth trajectory combined with continued fiscal prudence should improve national credit metrics, which opens the possibility of a rating upgrade. S&P still has South Africa’s local currency debt rated at two notches below investment-grade status at BB. Credit rating upgrades would significantly enhance the country’s status as an emerging market destination and unlock billions of rand potentially available for investment in South Africa.

Political risk will remain a factor to contend with, but initial developments post the national elections leave us optimistic. The cabinet may be more bloated than ever, but it is better than it was. There’s a diverse group of decision-

makers hungry to prove themselves, with the broad representation enhancing input, oversight and accountability.

Operation Vulindlela (‘OV’) is the glue for the GNU: should all parties agree with the path ahead and allow it to continue unfettered, investor sentiment would be substantially bolstered. The achievements during the first phase of OV make us optimistic that there will be continued progress towards achieving its policy objectives over the next five years, during the second phase.

SA investment base case improves, but challenges remain We consider the prospects for SA equities attractive, particularly those counters in the ‘lost and found’ bucket. Our analysis shows that, from a valuation perspective, the aggregate SA market remains about one standard deviation cheaper than its long-term average. This backdrop is similar for SA industrials, but within the sector, there is material dispersion – with, for example, Retailers, Construction, and Industrial Transport all trading at a more than 20% discount.

We believe this is the first phase in a multi-phase recovery. Should a capex and credit cycle commence in earnest, the knock-on effects will be significant, leading to a major reversal in trend growth after the lost decade.

This outlook led us to tilt around 2-3% of the equity exposure in our multi-asset growth fund to lean into the SA mid-cap space, specifically the currently unloved sectors of the market where we think there are great opportunities. With our primary focus being on risk diversification, we feel that this positioning reflects our optimism in a prudent manner.

It goes without saying that South Africa remains an emerging market economy, historically subject to volatility and significantly impacted by global events. While there seems to be consensus on the direction of travel for global interest rates (lower), views on the potential paths followed remain fluid and continue to drive much volatility. Uncertainty around global growth remains, and geopolitical risks continue to hold investors’ attention, especially in the Middle East. However, investing is never smooth sailing.

Launch of KPMG’s ‘Clear on Climate Reporting’ hub

Climate change is driving broader stakeholder scrutiny of financial reporting, with regulators, investors and the public focusing on how companies report on climate-related matters – such as net-zero commitments – and they are demanding clarity about climate. That’s why KPMG has launched its Clear on Climate Reporting hub: to provide insights and guidance to help organisations and their stakeholders understand how to be clear on climate in corporate reporting.

Covering key reporting issues companies are facing – through FAQs, podcasts and videos – it’s the first place companies should go when considering how to clearly explain to investors and stakeholders the financial implications of climate-related matters. The resources will constantly grow and be regularly refreshed – for example, a whole new emissions section will be added soon.

Larry Bradley, Global Head of Audit, KPMG International, says, “What’s described in the front of the annual report won’t always be mirrored in the financial statements in the way users expect. This is often true for climate. It is important that companies both comply with the IFRS® Accounting Standards and connect the dots between financial and non-financial information.”

Most, if not all, companies are facing risks arising from the physical effects of climate change and the transition to a lower-carbon economy. They should consider whether these matters are material to the financial statements and ensure users can understand the impact of climate. There is no single standard that addresses everything, and there are a lot of bases to cover to get the accounting right. The essential question for companies is: would an investor make a different decision if a piece of information were included?

Ultimately, investors and regulators want to see clarity and connectivity between a company’s financial and sustainability performance. A lot is happening in the corporate reporting space and companies are at varying stages in their sustainability reporting journey. But one of the first jobs is for companies to address climate in their financial statements today

and ensure they’re complying with the relevant requirements and are clear about the policies applied and judgements made. They should also join the dots to connect all climate-related information in their corporate reporting.

Brian O’Donovan, Global IFRS and Corporate Reporting Leader, KPMG International, adds, “Essentially, companies need to tell investors what the financial implications of their climaterelated plans are; and if they believe there’s no financial impact, tell investors why. Investors are looking for a connected picture of performance, showing the financial implications of sustainability plans and actions.”

Ben April, ESG Leader Africa Financial Services, KPMG in Southern Africa, says: “South Africa and the rest of Africa are witnessing first-hand our extreme vulnerability to the impacts of a changing climate. The storms that hit parts of the Western Cape over the past week have caused devastation to homes, communities, businesses and infrastructure. Climate change is as much an economic issue as it is a nature, social justice, human rights and development issue. It has a direct and material impact on activity across the economy. Climate finance is crucial for Africa’s transition.

“Africa needs substantial investments to build sustainable infrastructure, develop green technologies, and support social programmes. The KPMG Climate Reporting hub assists African companies in disclosing their climate ambitions and improving market access to Sustainable Finance at preferential rates.”

The Clear on Climate Reporting Hub can be accessed at https://kpmg. com/xx/en/home/insights/2021/06/ climatechange-financial-reportingresource-centre.html

MiWayLife’s advancing digital evolution

BY CRAIG BAKER CEO of MiWayLife

MiWayLife has launched its stateof-the-art online platform, offering life and funeral cover that can be conveniently purchased. This move comes in response to the growing demand for digital insurance solutions, accelerated by the changing landscape of consumer behaviour and technological advancements.

MiWayLife first ventured into the digital space last year with MiWayLife Direct, allowing consumers to purchase life insurance online. MiWayLife has now launched MiFuneral, a comprehensive digital-first solution for all end-of-life insurance needs. With this latest digital offering, clients can now secure funeral insurance at their own pace, without the need to interact with an agent. This digital platform is designed to provide optionality for clients to engage via a seamless, hassle-free experience while ensuring clients have access to support when needed during business hours.

Comprehensive benefits and unique selling points

MiWayLife’s digital funeral cover comes with a host of additional benefits: Repatriation of mortal remains: Assists in the transportation of the deceased’s remains to their place of residence or nominated burial site, with respect for cultural and personal preferences.

• Funeral arrangements service: Provides support with burial or cremation arrangements, including legal document assistance and referrals to pathologists for unnatural deaths.

Final expenses cover: Offers up to R100 000 to cover end-of-life expenses, such as outstanding debt, uncovered medical bills, and property maintenance.

Income support: Ensures beneficiaries receive up to R8 000 per month for 12 months, providing financial stability during a difficult time.

Family funeral cover: Extends funeral cover to immediate family members, ensuring comprehensive cover for your loved ones.

Craig Baker, CEO of MiWayLife, explains the strategic decision behind this digital transformation: “We recognise the need for flexibility and convenience in obtaining insurance. By going digital, we empower our clients to take control of their insurance needs, backed by the reassuring support of our dedicated team of agents when required.”

He further adds, “The rise of InsureTech is a positive force driving innovation in the industry, and embracing digital was inevitable. This development is driven by evolving client needs and through understanding some of the limitations that exist for clients in the current offerings. The actual ‘shopping’ experience, however, needs to compete with those that have been created in other retail sectors where the journeys are seamless and hassle free.”

MiWayLife’s new platform offers a user-friendly and supportive digital journey. “Our online journey is simple yet comprehensive. We understand that clients often seek reassurance before making a purchase decision. That’s why we offer continuous assistance through our chat facility and the option to speak directly with a human, if needed,” notes Baker.

Future plans and commitment to innovation

Looking ahead, MiWayLife is committed to further digital advancements, including personalising client experiences and enhancing financial education through their platform. The company also plans to leverage AI technology to automate routine tasks, allowing their team to focus on providing expert guidance and personalised support.

Growing adoption and customer feedback

The strategic launch has already shown promising results. MiWayLife currently sees around 150 quotes per month through its online channel for life insurance, and this number continues to grow daily. The expectation is to see the same, if not more, for the online funeral offering.

“Innovation and client-centricity are at the core of our mission – by offering a wellcrafted digital solution, we empower our clients with control and flexibility, setting new standards in the insurance industry,” Baker concludes.

The great multi-asset athletes

BY MIKE TITLEY Business Development and Marketing at Laurium Capital

Watching the 2024 Olympic Games from the dry comfort of my living room has made the recent wet winter weather in Cape Town much more bearable! I have enjoyed discovering competitive rivalries that I have been completely unaware of in sports that I hardly ever follow, and observing the sometimes surprising and excessive patriotic zeal that seems to grip both athletes and spectators. It probably happens to me at every Olympic Games (which I then forget as our TV screens return to showing the more traditional team sports like rugby, soccer, Formula One and cricket), but I have renewed my profound respect and admiration for the dedication and commitment required by every participant at these Games, in sports as diverse as badminton, weightlifting, free climbing and kayaking.

However, one of my key observations came to me while watching the men’s decathlon event on the athletics track. Most events are defined by an exceptional outlying strength, ability or skill (examples might invite descriptions like ‘fastest woman on the planet’, ‘perfect score’, ‘highest jumper in the world’, etc). In slight contrast, the men’s decathlon/women’s heptathlon winner seems to be defined by a lack of weakness – a holistic athlete, one who is almost certainly a highly competitive athlete in every discipline, but who might not be a gold medallist in any single one, if that’s all they focused on. Instead, what defines them as exceptional athletes is their

all-roundedness and lack of weakness in any one of the events. I drew on this reflection when doing a recent presentation for our multi-asset portfolios, of which we run a high-equity, medium-equity and low-equity mandate.

“These multi-asset funds invest right across the asset spectrum, in shares, bonds, property and cash within SA and abroad”

What a multi-asset fund is really good at, and what Laurium Capital as portfolio managers are employed to do on our investors’ behalf, is protecting investors against market weaknesses, to find a well-balanced and diversified blend of assets that will protect investor capital during periods of stress over shorter time periods of up to a year, and yet also have healthy enough returns that protect investors’ savings against inflation over longer time periods. These funds invest right across the asset spectrum, in shares, bonds, property and cash within SA and abroad. While the funds have a specific mandate to perform ahead of local category Collective Investment Scheme peers, the funds are managed by Laurium Capital with a focus on downside protection. This is achieved by weighing up expected return versus the risk of loss in each investment decision and holding a diverse portfolio of assets that mitigate against ‘known unknowns’ in the market. It is the all-round strength of all parts of the investment team and the portfolio that contributes to exceptional and peer-beating long-term performance.

The recent volatile swings in markets early in August are a great illustration of the multi-asset portfolios in action. A rapid change in the outlook for US growth led investors

APPOINTMENTS

Capital Legacy appoints new Chief Executive Officer

Capital Legacy has appointed Craig Harding as its new Chief Executive Officer, effective 1 January 2025. Harding succeeds founder Alex Simeonides, who has led the company since its inception in 2012. Harding has more than 30 years of financial and operational experience in African financial services markets. For the last seven years, he has been integral to Capital Legacy’s success, initially serving as Chief Financial Officer and more recently in a leadership role of the combined Capital Legacy and Sanlam Trust fiduciary businesses. Prior to joining Capital Legacy, Harding was a shareholder in FMI before its acquisition by Bidvest, CEO of Altrisk, and Executive Director at African Life. His deep understanding of Capital Legacy operations, combined with his extensive leadership experience in the financial sector, make him ideal to steer the company’s next growth phase. Capital Legacy’s rise has been meteoric, with significant investments from African Rainbow Capital, and Sanlam in 2023 – underscoring a bright future for the business.

As founder and major shareholder, Simeonides will remain heavily vested in

the success of the business. His strengths lie in innovation and entrepreneurial thinking where he thrives in driving new business and product development, challenging the status quo, and identifying growth opportunities. His new role will focus on such projects within the group, providing technical input, advice and insights to Harding and the leadership team through his executive role, as director and member of the board. The initiative for this next phase of the business came from Simeonides. He approached Harding and the shareholders and received their full support.

Under Harding, the Capital Legacy core values, principles, and business objectives will remain steadfast. The company’s ambitious goal of reaching one million clients by 2027 continues to drive its strategic initiatives.

Reappointment of Board member at the International Accounting Standards Board (IASB)

The South African Institute of Chartered Accountants (SAICA) has reappointed Bruce Mackenzie CA(SA) as a Board member at the IASB. He will be serving his second term, ending 30 September 2030. Mr Mackenzie also serves as Chair

across the globe to alter their view on the pace and quantum of interest rate cuts likely to be made in the US. While falling interest rates are not necessarily a bad thing for asset prices in the medium term, the shift in view prompted currency volatility in Japan. The upshot was a rapid and sizeable fall in share prices in almost every stock market. Conversely, the forecast reduction in interest rates boosted the value of bonds, whose prices rise when yields/interest rates decline. This rally in bonds largely offset the decline in the share portfolio. In addition, holding a basket of foreign assets helps to cushion local SA investors further when measured in rand.

Many retirement funds are managed by picking different specialists for each asset class and then blending these together into a single fund. While intuitively appealing, there is an alternative. Using a single, multi-asset fund manager with skills in every asset class, such as Laurium Capital, gives the manager the mandate to analyse and sum up the evolving outlook, and reallocate capital within and between assets very rapidly (when and where appropriate). Having the all-round capability in a single manager, and a wellbalanced portfolio, has helped to mitigate risk during volatile shorter time periods, while over the long term, the Laurium Capital investment team strives to produce exceptional, peerbeating performance. Laurium Capital manages four multiasset funds, namely the Laurium Flexible Prescient Fund, the Laurium Stable Prescient Fund, the Amplify SCI Balanced Fund and the PPS Stable Growth Fund. For more information, please visit www.lauriumcapital.com

of the IFRS Interpretations Committee.

The IASB is a global accounting standardsetter responsible for the development and publication of IFRS Accounting Standards.

In the South African context, companies are either required by law, such as the Companies Act, to apply IFRS Accounting Standards in the preparation of financial statements, or they may voluntarily adopt these Standards.

Absa gets new CEO Absa CEO Arrie Rautenbach will take early retirement from the group from 15 April 2025. He will also stop being the CEO and an Executive Director from 15 October 2024. Charles Russon will become Interim Chief Executive Officer of Absa Group and Absa Bank, from 15 October 2024, subject to regulatory approval. He will also become

an executive director on the boards.

Russon has been the Chief Executive of Absa’s Corporate and Investment Bank (CIB) since 2018 and a member of the Group Executive Committee since 2014. He joined Absa Capital in 2006 as CFO and has held several senior roles at the group, such as Regional Head of Finance, Chief Operating Officer, and Chief Executive: Engineering Services.

Yasmin Masithela will then become Interim Chief Executive Officer of Absa’s CIB, effective 15 October 2024, subject to regulatory approval. Masithela is currently Managing Executive Corporate Transactional Banking, CIB and has held the role since May 2019. She previously worked on the Group Executive Committee as Chief Executive of Strategic Services and Chief Compliance Officer, respectively.

Transferring clients: Is buying a client book worth it?

BY TRACY WRIGHT

Masthead Compliance Officer

Transferring or acquiring a client book can boost your financial advisory business, but it’s not without its challenges. We delve into the intricacies of client transfers and the factors financial service providers (FSPs) should consider before making this decision.

There are many reasons why an FSP would like to expand their client base: increased revenue generation, diversification, and business growth, to name a few. One way to achieve this is through the transfer or acquisition of a client book from one FSP to another. While this strategy can yield substantial benefits, it’s not without its hurdles. Many financial advisers complain that the absence of an industry standard governing this process muddies the water. For instance, some product providers allow bulk transfers if they receive a client bulk transfer declaration, signed by a Compliance Officer, confirming that all clients were notified of and consented to the transfer. Others require proof of individual broker appointments, which include signed broker appointment letters from each client affected by the transfer.

Regulatory requirements

Long gone are the days when client book transfers happened without the client’s knowledge or consent. Now, informing clients and getting their consent upfront, in writing or through other appropriate means like voice recordings, is a legal obligation under the Financial Advisory and Intermediary Services (FAIS) Act. The seller of the client book must inform their clients about the termination of their services, while the buyer must secure

AND SHARREN BHAGWANDIN Masthead Compliance Officer

client consent or broker appointments for each client.

Moving a client book can also mean changing product providers, effectively replacing a financial product. Under Section 8 of the FAIS General Code of Conduct (GCOC), when this happens, an adviser must fully disclose the actual and potential financial implications, costs and consequences of such a replacement to the client. In other words, an advisor can’t move a policy without first getting the client’s consent.

Section 20(a)(i) of the GCOC stipulates that if a client cancels a policy on an advisor’s advice, the advisor must ensure that the client fully comprehends the implications of this decision. Furthermore, Section 4(1) of the GCOC requires FSPs to furnish clients with complete information about the relevant product supplier, making it obligatory for clients to be informed of the new product provider.

Section 3(3) of the GCOC states that an FSP may not disclose confidential client information without the client’s written consent. During a client book transfer, this rule inevitably comes into play, as confidential client information is disclosed to the new advisor or product provider, making the client’s written consent mandatory.

It’s also necessary to consider the obligations placed on FSPs by the Protection

of Personal Information Act (POPIA).

Safeguarding the integrity and security of client data is paramount during the transfer process. Both the seller and buyer must have the necessary processes and procedures in place to protect clients’ data.

Furthermore, client notification is a critical aspect of maintaining trust. Clients need to be appropriately informed about the transition, the reasons behind it, and the potential benefits for them.

Treating Customers Fairly (TCF)

Outcome 1 is also relevant to this process. It requires that customers are confident that they are dealing with firms where the fair treatment of customers is central to the business’s culture. If clients are transferred to a new FSP, they must be assured that the new FSP has their best interests at heart. In addition, TCF Outcome 3 states that customers should be provided with clear information and kept appropriately informed before, during and after the point of sale.

Is it worth buying a client book?

Some advisors may argue against it because of the time-consuming nature of the process. Buyers need to obtain signed broker appointment letters for all affected clients. While some product providers permit bulk transfers, they still require a signed declaration from the FSP’s Compliance Officer, confirming that all clients have been notified and have consented to the transfer. In addition, these product providers usually request a letter from the client book’s seller, permitting the transfer, alongside a product provider transfer form or a letter from the buyer accepting the business transfer.

Buying a client book can also be a compliance risk if signed broker appointment forms can’t be obtained because clients don’t respond to communications or cannot be reached due to outdated contact details. Additionally, some clients may decline the transfer and seek financial advice elsewhere.

On the flipside, acquiring a client book

“An adviser must fully disclose the actual and potential financial implications, costs and consequences of such a replacement to the client”

can drive client base growth and expand the business.

Considerations before acquiring a client book

Before taking the leap, consider the following:

In your own business:

• Does your business have the capacity to ensure a smooth transition? For example, will it be able to inform and obtain consent from all clients while the rest of the business continues to operate optimally?

Does acquiring this client book align with your long-term business objectives? Does it fit into your growth plans? And, importantly, can you financially afford it?

Are the acquired clients a good fit for your business, both in terms of the services you provide and your business culture?

With regards to the client book you wish to buy:

Assess the quality of the clients in the book, such as their revenue potential and the potential for cross-selling other financial products.

Determine a fair valuation for the client book. Factors to consider include the client’s assets under management, recurring revenue, and the potential for future income.

Scrutinise the legal and compliance status of the FSP from which you wish to buy a client book. Do they have any past or ongoing litigation or regulatory issues? What type of reputation do they have in the industry? FSPs with a strong compliance culture are usually more likely to be committed to keeping and updating client records, which will make it easier to contact clients to inform them of the transition.

Buying a client book may be a laborious exercise, and the returns might not always justify the effort. However, by doing your research – both within your own business and in the seller’s business – this strategy can indeed help you expand your horizons and grow your financial services business.

Visit www.masthead.co.za for more information.

Going global

BY MIKE ADSETTS Global Chief Investment Officer at Momentum Multi-Manager

The global investment universe is a big space, and until relatively recently – with limitations on how much a South African investor could invest offshore – the ability to access some of the investment opportunities has been limited.

Over the last few years, historically low interest rates have made the return on global cash and other asset classes related to fixed interest less attractive, especially when compared to the relatively high real rates that could be earned from South African cash and bonds.

Things have changed over the last few years as inflation has trended upward with interest rates eventually following suit. As the risk of runaway inflation now seems to have moderated, global interest rates are expected to trend downwards in the near to medium term. Although inflation has remained stickier than expected and the anticipated interest rate cutting cycle has been delayed in many parts of the world, this has made the global fixed interest universe a far more interesting prospect. If we consider global bonds, especially investment-grade credit and emerging market debt, on a prospective basis decent returns are expected. Relatively stretched valuations in components of global equities, in particular US equities, make these fixed interest assets even more appealing.

Gold has also rallied as global geopolitics has given impetus to central banks to increase their gold holdings as a diversification strategy to reduce their exposure to US dollars. This in the context of increasing polarisation across the globe where there is real concern that access to reserves can be blocked, as we saw in the case of Russian reserve holdings in western banks. This backdrop implies that there will continue to be demand for gold, which should provide an underpinning for the gold price.

“There is a significantly larger universe of investments available globally which quite simply do not exist in South African markets”

Another asset class with which we are familiar, and which is currently topical, is infrastructure. Globally, there has been an extended period of underinvestment in infrastructure in many countries, so this is not only a South African problem. We just need to look at the US to see the significant commitments being made to sectors such as transport and logistics to appreciate that we are in for an extended catch-up period as older infrastructure needs to be replaced and new capacity needs to be brought online. Although not cheap now, infrastructure funds do provide predictable cashflows and a reasonable inflation hedge. Also, a significant benefit of global infrastructure is that there are many listed vehicles available, which enhances their liquidity.

These asset classes are relatively familiar and well-known to South African investors. What is worth bearing in mind is that there is a significantly larger universe of investments available globally, which quite simply do not exist in South African markets.

Then there are a few interesting investments that are totally absent from the South African landscape. A few ones we have come across are investing in music royalties, direct lending and specialist property (e.g. lab space). These are definitely for the more niche investor!

It’s always important to remember the basics of investing, even when considering the far larger global opportunity set. Diversification is important – do not make such a big investment in a single asset that it dominates the risk in your portfolio – and always remember what your investment goals are. Any investment decision needs to be made in the context of your overall goals and needs. A sound investment strategy is to understand the role and contribution that any investment will make to your overall portfolio.

Momentum Investments Group offers a diverse range of investment and retirement solutions, with access to local and global investment markets to suit all investment needs.

Whether you want to create and grow your wealth, protect it, or earn an income from it, we have a personal investment solution for you on your journey to success. Visit our website for more about our offshore investing solutions: https://www.momentum.co.za/momentum/personal/investments/invest

Not all romances have a fairytale ending

BY MAGDELEEN CORNELISSEN Wealth Manager, PSG

Iam a romantic at heart. I can predict the script of any romance within the first five minutes. Somewhere in the middle of the storyline you can expect the main characters to stare soulfully and expectantly into each other’s eyes. Fast forward to the end, you will hear the words “I do”. The realities of life, and especially finances, are less predictable. Financial advisers are constantly faced with life’s reality checks, as we are often confronted with the less glamorous parts of the fairytale – namely, the heartbreak of relationships coming to an end.

The 2022 StatsSA report on divorces in South Africa, published in March 2024, shares data behind the increasing number of marriages ending in divorce. It is interesting to note that more women than men initiate divorce proceedings and that the peak age group of divorce for women is 35 to 39 years.

Although society has improved in empowering women, it is still evident that women are often emerging in an economically less favourable position following a divorce. Quite often the first time that many of these women meet with a financial adviser is in the process of their divorce. At this point, they are faced with the stark reality that their financial position is less than ideal and that the likelihood of them reaching their retirement goals are slim. It does not, however, have to be the end of your financial journey. JK Rowling famously said, “Rock bottom became the solid foundation on which I rebuilt my life.”

Women need to empower themselves to ensure that, regardless of the circumstances, they will be able to go through the process of divorce with the certainty of financial wellbeing.

The foundation of our financial education begins at home. Children, especially girls, should be educated about the power of financial independence from a young age. Not only will that provide them with the ability to play a leading role in their financial journey, but it will also entice them to think critically about the steps they take to create their own wealth.

“No one gets married with the idea of getting divorced, but unfortunately, marriages can end abruptly”

Women must have access to a financial adviser. Men and women do not necessarily have the same needs and objectives when it comes to managing their finances. Women often take leading roles in managing other household affairs at the expense of their own financial position. Lack of financial knowledge and control of financial affairs can be a major obstacle for women who find themselves trapped in a hopeless marriage. Women should actively engage in their household finances, even if they feel that it is not their ‘speciality’. The ability to share dreams and concerns with a financial adviser, without the fear of being judged, is imperative. Realising that discussions about the most appropriate marital regime is just as important as choosing the perfect wedding dress can lead to a better outcome in the event of divorce. These are discussion points that can change the course of a woman’s financial outcome.

No one gets married with the idea of getting divorced, but unfortunately, marriages can end abruptly. As a romantic at heart, I believe that women can indeed leap into the next chapter of their lives, without the shadow of financial troubles

Are your regular outof-office notifications hurting your business?

BY FRANCOIS DU TOIT

CFP® PROpulsion

In today’s fast-paced world, balancing personal time and professional responsibilities is crucial, especially in the financial planning profession. As financial planners, advisers and wealth managers, the trust clients place in us hinges on our availability and reliability. But what happens when you frequently set up an out-ofoffice (OOO) notification? Could it be harming your business, or does it show a healthy respect for work-life balance? Let’s explore.

The role of out-of-office notifications

Out-of-office notifications allow professionals to set boundaries while ensuring that clients and colleagues know when they can expect a response. They serve multiple purposes, such as managing expectations, preventing a backlog of emails, and providing a chance to inform clients about when you’ll be back and who to contact in your absence.

For those in client-facing roles, like financial planners, these notifications can also be a subtle way to reinforce the professionalism and organisation of your practice. However, the frequency and content of these messages matter greatly.

The potential downsides of frequent OOO notifications

Perception of unavailability

In the financial planning profession, where trust and reliability are key, being perceived as frequently unavailable can be problematic. If you regularly set up an OOO notification, clients might start to question your commitment to their financial needs. They may worry that when urgent issues arise, you won’t be there to provide timely advice.

Clients rely on financial advisers to be available, especially during volatile market conditions or significant life and financial events. A pattern of frequent absences could inadvertently send the message that your personal time takes precedence over their financial wellbeing, which could damage the trust you’ve worked hard to build.

Impact on client relationships

Strong client relationships are the bedrock of any successful financial planning business. Regularly informing clients that you’re out of the office, even with a friendly tone, can sometimes strain these relationships. Clients might feel that their needs are secondary, leading them to seek advice elsewhere, where they perceive a more consistent presence. Additionally, clients may start to feel anxious if they believe their financial adviser is not fully engaged. In an industry where confidence in your adviser is paramount, this perception can be particularly damaging.

Your brand and professional image

Your out-of-office messages also contribute to your professional brand. While it’s essential to showcase your commitment to work-life balance, doing so too frequently might lead to an image of someone who is often disengaged from their work. This could be especially harmful if clients or prospects begin to see you as less dedicated or less available compared to other advisers.

Balancing professionalism and personal life

Effective OOO strategies

So, how do you balance the need for personal time with maintaining a strong professional presence? Here are a few ideas:

1. Limit the frequency: Consider reducing the frequency of your OOO notifications. Instead of setting up an OOO message every week or fortnight, you might reserve them for longer breaks or significant holidays.

2. Delegate responsibly: Ensure your clients know who to contact in your absence. Providing an alternative point of contact can reassure clients that their needs will still be met promptly.

3. Tailor your messages: Customise your OOO messages based on your audience. A more formal

“Regularly informing clients that you’re out of the office, even with a friendly tone, can sometimes strain these relationships”

tone might be appropriate for newer clients, while a personalised, friendly message could be reserved for long-standing clients who understand your work style.

4. Communicate proactively: If you know you’ll be out of the office frequently, consider discussing this with your clients in advance. Let them know that you value both your family time and their business, and reassure them of your commitment to their financial wellbeing.

Maintaining trust and availability

Ultimately, the key is to ensure that your clients feel valued and supported, even when you’re not directly available. By carefully crafting your OOO notifications and managing their frequency, you can maintain the delicate balance between professionalism and personal time without compromising your business or your reputation. Remember, it’s not just about being out of the office; it’s about how you manage your absence and communicate your availability to your clients. Raise the bar! Francois created PROpulsion, a dynamic network for financial planners and advisers promoting growth and success. He presents the weekly PROpulsion LIVE show on YouTube, with over 268 episodes delivered, leveraging his 25 years of expertise while hosting guests both domestic and international to educate and motivate. Dedicated to learning and applying new tech, he aims to make a large-scale impact. For further details, go to www.propulsion.co.za.

Index-tracking balances costs and returns in high-fee markets

Investors worldwide are grappling with high investment fees. For example, 34% of global investors surveyed in a recent bfinance Investors’ Costs and Fees poll say their fund servicing costs have increased in the past three years. Yusuf Wadee, Head of Exchange-Traded Products at Satrix , shares insights on these fee trends and how index-tracking investment product providers balance cost-effectiveness and returns in this high-fee landscape.

“The industry is observing pressure on fees across all asset management sectors. However, index-tracking investment product providers balance cost-effectiveness with consistent performance to provide efficient, accessible, and value-driven indextracking solutions that stand the test of time. This balance can help investors harness the full power of compounding returns while minimising the erosive effects of high fees.”

The widespread phenomenon of global fee pressures

Ever-reducing asset management fees have become a global phenomenon affecting active management and rulesbased investment strategies. Wadee notes, “The fee pressures are playing out almost everywhere in the industry. However, the driving forces behind this trend differ across investment disciplines.”

He says in the active management space, the trend of investment outflows has persisted. This exodus has intensified the downward pressure on

fees in this market, particularly given the traditionally higher fee base associated with active management.

Conversely, the indexation space, which includes rules-based strategies, has experienced consistent inflows into our markets. “Here, the fee pressures among competing product providers are more related to players trying to capture more of the market and new inflows via aggressive fee positioning,” he explains.

The compounding effect of fees on returns

Understanding the long-term impact of fees is crucial for investors. Wadee draws a compelling parallel between the power of compounding returns and the eroding effect of compounded fees.

“Much has been written on the power of compounding. The fact that a simple (but consistent) investment strategy – involving investing early in the market and staying invested – yields profound results after many years, is powerful. This is due to the effect of compounding; simply put, you get growth on your growth.”

However, he adds that this same principle works in reverse concerning fees. “The eroding effect of high fees works similarly – but in the opposite direction. The long-term impact of high fees consistently levied year after year on investment portfolios over time is also driven by the same compounding force – the only difference is that the compounding force of higher fees acts in the opposite direction to the

“Satrix has been able to reach a significant scale of assets needed to effectively operate an indexation business in a very competitive market”

compounding of being invested in the market.

Wadee says even minor differences in annual fees can significantly affect wealth accumulation over time.

Balancing cost reduction and performance

In response to fee pressures, Wadee says Satrix has had the benefit of having the first mover advantage in the South African indexation market.

As such, Satrix has been able to reach, very early on, a significant scale of assets needed to effectively operate an indexation business in what is a very competitive market.

“Past a certain scale, indexation firms can extract economies of scale and efficiency benefits that allow us to ensure performance and quality for our investment strategies, despite market fee pressures.”

The case for index tracking in a challenging investment landscape

Wadee says index tracking offers significant value to investors in the evolving investment landscape, particularly in the current high-fee environment. For instance, Satrix research shows that in South Africa, almost 90% of active manager returns result from market performance, which they can track using simple, low-cost index tracker funds.

“This raises an important costbenefit question for investors: how differentiated, consistent, and successful

are actively managed funds’ returns versus how much investors are paying in fees to achieve those returns? The higher costs of active management compared to index tracking means that the median performing active fund almost always underperforms an index tracking fund on a net of fees basis.”

Minimising the effects of compounding costs

Wadee emphasises that the impact of fees is less pronounced in index tracking than in active management, particularly over the long term. “The effect of higher costs compounds over the medium to long term and creates a significant headwind for active managers and investors to overcome. In contrast, index tracking’s lower fee structure allows investors to benefit more fully from market returns, minimising the erosive effect of fees on long-term wealth accumulation.”

He says for investors, the message is clear – while low fees are essential, they should consider them in the context of overall value, performance, and alignment with investment goals.

“In an environment where every basis point counts, index-tracking investment product providers must strive to optimise their offerings and ensure investors can harness the full power of compounding returns, minimising the erosive effects of fees, and maximising long-term wealth creation potential,” concludes Wadee.

Yusuf Wadee, Head of Exchange-Traded Products at Satrix *

Celebrating the best of the best in the insurance industry

This year’s 2024 FIA Intermediary Experience Awards took place on 15 August at the Sandton Convention Centre. Widely acknowledged as the highest accolade in South Africa’s financial services sector and held for the past 20 years, this award honours insurers and product providers who excel in providing outstanding products, solutions and services through intermediaries and financial advisers.

“The FIA Awards go beyond recognising merit in the financial services sector; they highlight the crucial role our members play in ensuring sustainable financial outcomes for businesses and households,” said Lizelle van der Merwe, CEO of the Financial Intermediaries Association of Southern Africa (FIA). “The brands that rise to the top at this annual event do so through a combination of hard work and innovation – and by consistently recognising the importance of human advice in delivering needs-appropriate financial and risk management solutions for consumers.”

Winners are selected through a meticulous process that involves a thorough and unbiased evaluation of thousands of responses from FIA members. The intermediary experience survey evaluates financial product providers on various criteria, including overall satisfaction with brand, product, and service; business enablement; regulatory compliance; and trust. High scores in each of these areas are crucial for maintaining the service standards expected by FIA members.

The FIA Awards serve as a critical benchmark for assessing the integrity, innovation, and client-centricity of financial brands within the industry. According to Van der Merwe, the awards not only celebrate the recipients but also help

establish their credibility and trust within the broader financial advice community. This recognition reflects the brands’ commitment to excellence and their role in enhancing the overall experience for both FIA members and financial consumers. The overall service results for 2024 were consistent with last year, underscoring the competitive nature of the insurance and investment sectors. “The competitive nature of the industry – and the value that financial services brands place on these awards – is evidenced by how closely run the various categories are,” Van der Merwe said. She highlighted encouraging signs of a reversal in the multi-year decline in service levels within the non-life insurance cluster.

“The brands that rise to the top at this annual event do so through a combination of hard work and innovation”

The winners of the 2024 FIA Intermediary Experience Awards are:

Non-Life Insurance

Non-Life Insurer of the Year –

Personal Lines: Santam

Non-Life Insurer of the Year –

Commercial: Western National

Non-Life Insurer of the Year –

Corporate: Santam

Underwriting Manager of the Year: iTOO

Life & Investment

Long-Term Insurer of the Year –

Risk: Sanlam

• Product Supplier of the Year –

Investment Product, Lump Sum: Allan Gray

Product Supplier of the Year –

Investment Product, Savings: Allan Gray

Healthcare

Product Supplier of the Year –

Healthcare: Discovery

Non-L ife Insurer of the Year –

Non-Life Insurer of the Year –Personal Lines: Santam

Product Supplier of the Year –Investment Product, Savings: Allan Gray

The FIA wished a heartfelt congratulations to all winners for their exceptional work in supporting intermediated distribution in South Africa, saying that the achievements highlight the power of partnership and the importance of delivering the best outcomes for consumers.

On their win as Non-Life Insurer of the Year – Commercial, Western National’s CEO Jurgen Hellweg said, “To receive this recognition for three consecutive years is a testament to the excellence we strive for at Western. We are very proud of our team. Receiving this accolade at the most prestigious event in the South African financial services industry is no small feat. We are here today because of the team’s

dedication and commitment to ensuring that our clients always come first.”

iTOO Special Risks were thrilled to win the Managing Agency of the Year award.

“This incredible honour is a testament to the dedication and expertise of our team and the invaluable partnerships we have built with our brokers,” said iTOO CEO Justin Naylor.

“At iTOO,” he said, “our vision is to be an EPIC partner in speciality insurance. For us, EPIC stands for Expert, Partnership, Innovation and Commitment. We believe that partnering with our brokers is not just fundamental – it is the cornerstone of our success. We are committed to delivering quality and expert service, always.”

Taking home the coveted Managing Agency of the Year award underscores the fact that iTOO is a unique company that provides specialist insurance and a brand that pushes the boundaries of traditional insurance.

“I would like to extend a big thank you to our amazing brokers, clients and partners for your trust and support. I also want to extend a special thank you to our iTOOers for their relentless commitment to delivering expert service to our brokers and clients. Here’s to many more years of collaboration and shared success,” said Naylor.

Sanlam was once again recognised for its excellence in the financial services industry, winning the 2024 Intermediary

Underwriting Manager of the Year: iTOO

Product Supplier of the Year –Healthcare: Discovery

Experience Award in the Long-Term Insurer Life/Risk category. This is the third consecutive year that Sanlam has received this accolade, highlighting its consistent commitment to empowering South Africans through financial security.

Jean Lombard, Chief Executive at Sanlam Risk and Savings, reflected on the significance of this achievement, saying, “We are proud to be acknowledged by independent intermediaries across the country for the third year running. This award underscores our position as an industry leader. By consistently pushing the boundaries of innovation, we have redefined customer expectations.”

Santam was similarly excited for being recognised as the Best Personal Insurer and Best Corporate Insurer.

“Our success in these categories is a testament to Santam’s commitment to excellence, innovation, and customercentric service delivery,” said Santam.

“We extend our heartfelt thanks to every member of the Santam family who made this achievement possible. From those on the frontlines, engaging with our intermediaries and clients daily, to those working tirelessly behind the scenes to support us and fulfil our promises, and to the leadership teams who guide and enable seamless collaboration – this success is a testament to hard work and dedication,” added Santam.

“As we move forward, Santam will continue to build on this momentum, striving to set even higher standards in the industry.”

Congratulations to all the winners, from MoneyMarketing!

Non-L ife Insurer of the Year – Commercial: Western National

Five key considerations for your offshore investment strategy

BY MAARTEN ACKERMAN Citadel Chief Economist and Advisory Partner

South African investors who are serious about long-term wealth creation need to pay special attention to their offshore allocation. To be successful, this goes beyond picking the next Nvidia or Amazon; rather, it involves the adoption of a structured and holistic investment philosophy.

As a wealth management specialist, we have centred our investment approach around some core principles that would be applicable irrespective of where you invest. Our departure point is always that the future is uncertain, and you need to diversify. When you do diversify, you need to do so at a time when valuations make sense, and you need to ensure you have the right asset allocation.

The first key consideration for offshore investment is the investment instrument that you will be using. Is it a technology share in the United States (US)? Perhaps it is an exchange-traded fund (ETF), unit trust or structured product? Are you looking to bolster the income portion of your portfolio through global property or a combination of emerging market and developed market bonds?

If one considers the structure of the South African market, investors have a primary bourse with around 400 companies listed. The number of actual investment vehicles, whether exchange-traded funds or unit trust funds, are multiples of these. This might sound significant, but when you consider that South Africa makes up less than 1% of global assets, you realise the diversity of the global investment universe.

While the last few years have been characterised by outperformance in US technology shares, we are increasingly seeing opportunities in markets like Europe, the United Kingdom and Japan.

This brings us to our second consideration, which is understanding the objective of the investment. A key driver of offshore investment activity is protecting your wealth against rand depreciation, but we would argue that the currency is simply a tool in your investment toolbox. Instead, we believe that investors should view themselves as global citizens.

If you are earning your salary in rand but buying your car, mobile phone, or television from overseas, then you need to utilise your investment portfolio to preserve your hard currency buying power, since all of these are priced in US dollars.

Your third consideration will be around governance and compliance, which can be highlighted through two examples. The first is Russia, which was part of the BRICs grouping – characterised by well-

capitalised banks and valuable commodity assets. Investors here have been frozen out and lost money due to sanctions applied by the Western economic powers in the form of the US and Europe.

Closer to home, South Africa’s greylisting has seen the cost of compliance rise as international regulators demand additional information from South Africans moving money offshore. This additional cost of compliance and administrative burden has discouraged many people from enhancing their offshore asset allocation – something that could negatively impact their long-term risk-adjusted returns.

Understanding the investment jurisdictions and compliance requirements should not be a reason not to invest offshore.

Our fourth consideration is around the platform you will be utilising to make your investments offshore. There are two primary ways in which you can facilitate offshore investments. The first is the direct route where you move money offshore and make investments, and the second is where you make use of an asset swap arrangement. While the direct route has become far more popular as exchange control regulations have eased, investors in companies or trusts may need specialist advice when making use of asset swap arrangements.

This leads us to the fifth consideration, which is around advice and the associated fees. New platforms have made it easier for investors to go the direct or do-it-yourself route, but this should never discount the value of expert wealth management advice. Whether it is assisting with the compliance costs of the greylisting, more specific tax structuring advice, or providing you with an independent set of eyes and ears, a high-quality advisor can be an asset when deciding to go offshore.

Investors who are serious about long-term wealth creation will recognise that they cannot limit their investment universe to South Africa. By incorporating these key considerations, they can tackle an uncertain future from an informed perspective. Investors can also pair this informed perspective with a wealth management specialist who can assist them with their offshore needs. An example of this is Citadel, where the people and solutions are in place.

Protect against volatile markets with a low-risk investment

BY SCOTT COOPER Investment Professional, Marriott Investment Managers

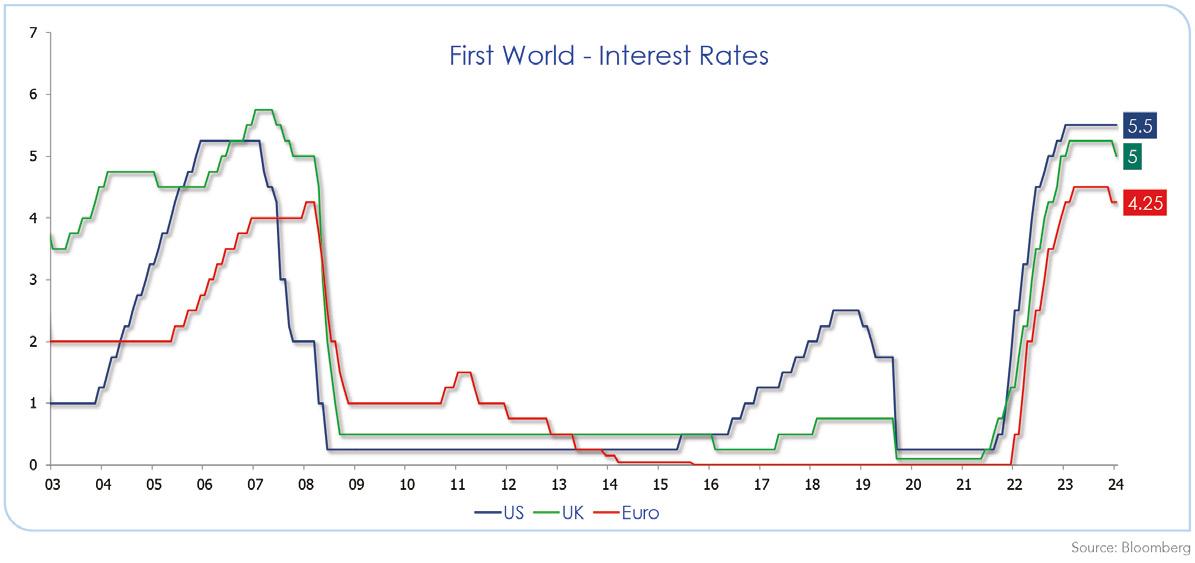

As the year has unfolded, many central banks have faced increasingly difficult interest rate decisions. On one hand, cutting too soon could lead to increased optimism, accelerating economic activity, and risk the reemergence of the inflation. On the other hand, maintaining restrictive monetary policy for too long could trigger a recession.

Although economic activity in the USA has remained resilient over the past four years, the first cracks began to emerge at the beginning of August this year when headline unemployment increased to 4.3% – its highest level since October 2021. This, coupled with low consumer confidence and disappointing job creation figures for the month of July, sent shudders through global markets, led by Japan’s Nikkei 225 stock index which fell more than 12% in a day. However, markets have since rebounded as subsequent US economic data has provided some much-needed reassurance of a ‘soft landing’.

The timing and steepness of potential interest rate cuts will continue to be a key focus of global markets as the year progresses. Although the European Central Bank and Bank of England have each implemented one 0.25% cut (in June and August respectively), monetary policy remains firmly in restrictive territory. Further, despite expectations at the end of 2023 that interest rates in the US would fall by 1.75% during 2024, the Federal Open Market Committee is yet to act. As a result, global rates have remained at 15-year highs in all three regions.