April report.

Our purpose.

To create a place where we can facilitate our people’s growth.

To create a place where we can facilitate our people’s growth.

Family.

Our colleagues are our broader family, assist when needed and when in need.

Mutuality. Respect our colleagues and our clients as you would like to be respected.

Realising potential. Unlock your full potential, encourage and support your colleagues.

Embrace change. Strive for excellence; be open minded and willing to embrace change.

Health and energy. Work towards being well balanced within yourself.

Message from Dean O’Brien

There are several reasons why investing in property can be a smart financial decision:

1 Potential for long-term appreciation: Historically, property values have tended to appreciate over time, especially in highdemand areas. This means that if you buy a property today and hold onto it for several years, it may be worth significantly more in the future.

2. Generating passive income: Rental properties can provide a steady stream of passive income through monthly rental payments. This can be especially lucrative in high-demand areas or during times of low interest rates

3. Tax benefits: Property investors may be able to take advantage of tax deductions such as mortgage interest, property taxes, and depreciation. These deductions can help lower your overall tax burden.

4 Diversification: Investing in property can help diversify your investment portfolio, reducing your overall risk. Property values do not always move in lockstep with the stock market, which means that investing in property can provide a hedge against market volatility.

5 Tangible asset: Property is a tangible asset that you can see and touch. This can provide a sense of security and stability that is not always present with other types of investments.

6. At the present moment your principal place of residency is capital gain free when you sell it.

Overall, investing in property can be a smart financial decision if done properly. It is important to do your research, understand the local market, and work with a qualified real estate professional to make informed decisions about your investment or principal place of residency.

Property investment requires financial education, asset acquisition, asset selling at time to create passive income streams through investment in real this is why when you are considering increasing your portfolio or selling your investment property the best thing you can do is reach out to your local real estate experts at O’Brien Real estate or seek out the financial position with out partners at MTNY Financial.

It’s important to seek professional advice and guidance throughout the buying and selling process, particularly when it comes to legal and financial matters. A good real estate agent, lawyer, and mortgage broker can provide valuable assistance and help ensure that you make a smart and informed decision when buying or selling a property.

Regards

Dean O’Brien Corporate Director

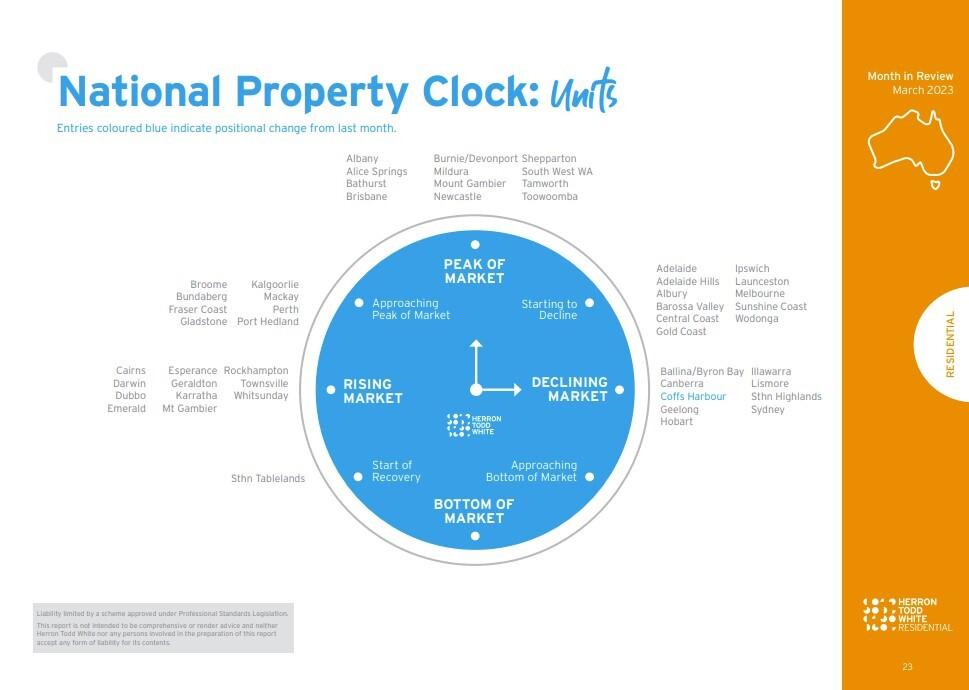

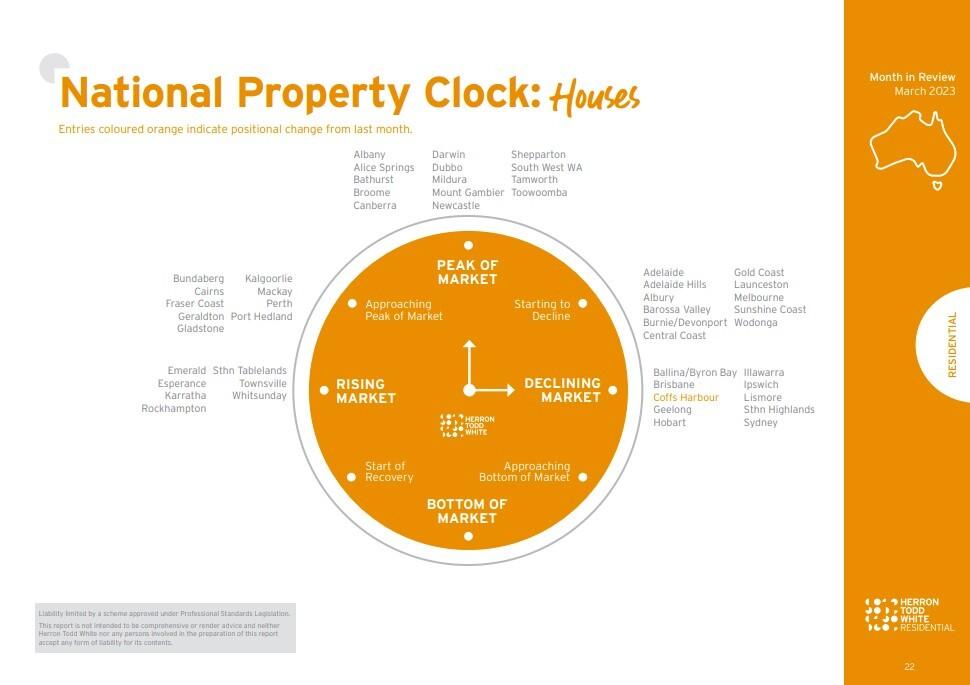

Australian’s have a fascination and even love affair with tracking house prices. The media understands this love affair and consistently bombards us with information and statistics about house prices, typically in the form of lists of hot suburbs and postcodes.

The importance of house prices to our personal wealth

But the love affair Australians have with property is more than just emotional. There are approximately 11 million residential properties in Australia worth an aggregate value of around $9 trillion. That $9 trillion is more than three times the size of the Australian stock market. And over 60% of Australian’s wealth is tied up in residential property.

No wonder Aussies are so mesmerised by the dynamics of the property market. This fixation usually takes the form of an intricate understanding of the market value of their property and the relevant properties in the suburb.

People are keenly attuned to new properties listed for sale in their local neighbourhood, what the listing price is, who the agent is and when the auction date is. But this fascination is driven by self-interest – what does it all mean for the current value of my property and my wealth?

The importance of interest rates

It also makes complete sense to keep a close eye on the competitiveness of the interest rate people are being charged – too many Aussies “set and forget” their home loan arrangements and fail to stay on top of their home loan to ensure they continue to get a good deal from their lender. This is the job of any good mortgage broker.

But I think there is a far more important thing for people to keep a close eye on than the estimated value of their home, particularly where one has no intention of selling in the foreseeable future.

That is their capacity to meet their current and projected loan repayments.

Why is that? Because any inability to meet your loan repayments creates huge emotional stress, fear and apprehension for individuals and families, can lead to more adverse personal and societal outcomes.

Lenders have a strong aversion to people defaulting on their home loans and will typically work collaboratively with borrowers under financial stress. Mortgage defaults can even ultimately lead to a forced sale of the property, and in a worst-case scenario see the lender seeking a court order to take possession of the property. In either case, the property is likely to be sold for materially less than what the owners believe is the market value, resulting in a significant loss of equity for the owners.

That’s why everyone needs to develop a keen understanding of their ability to meet the current and future repayments.

There are a few parts to this.

Understanding your current and future income and savings

The first is on the income and savings side. Having solid and stable employment, understanding likely future wage and salary increases, potential bonuses, threats to job security, plans to reduce working hours (for lifestyle and/or health reasons) are all important factors to plan in.

Then it is important to understand how much savings you have access to in the event of a rainy day in case your income drops for a brief or sustainable period. This could include both savings in the bank or in an investment that can be liquidated, or even parents or other family members you may call on in the event of an emergency.

Many borrowers also have minimal understanding of their redraw capacity from their home loan. This amount is represented by the difference between your current loan balance and the scheduled balance – basically the extent to which you are ahead of your home loans repayments. Subject to the terms and conditions of your loan, borrowers are generally able to redraw some or all of this amount to help them through a difficult period.

Understanding your mortgage structure

On the outgoings side, people should have a good understanding of their home loan structure to be able to roughly quantify the increase in loan repayments in the future, so as to be able to plan and be ready to meet any higher repayments.

Higher repayments can arise for three main reasons:

1. An increase in interest rates will increase the scheduled repayment amount. If your interest rate has fallen since you have taken out your loan and you have maintained the initial repayment schedule, this may not impact you in terms of an obligation to make increased loan repayments. However, higher interest rates typically mean higher repayments. In Australia, as at April 2022, there is a currently a strong expectation that interest rates will progressively rise in the second half of 2022 and into 2023.

2. If part or all of your loan has been structured on an interest only basis (typically IO periods last for one, two, three or five years) and the fixed rate is lower than the then prevailing variable rate at the time the loan converts from interest only to principal and interest, then the new loan repayment will be materially higher, both because the interest rate is higher and also because principal is now being repaid (whereas it was not under the interest only period of the loan).

3. The loan moves from a fixed rate to a variable rate. Most fixed rate loans taken out in Australia in the past two to three years expire in 2023, so many people can expect higher loan repayments when the fixed rate period expires.

It is great to keep an eye on house prices – it helps us understand and keep track of our wealth and our options to leverage our equity in property to create future wealth. However, for the reasons set out in this article, is arguably more important to keep a close eye on current and likely future loan repayments and your capacity to meet them under a range of different scenarios.

The quality of our service stems from the importance we place on the people behind our network.