May report.

Our purpose.

To create a place where we can facilitate our people’s growth.

To create a place where we can facilitate our people’s growth.

Family.

Our colleagues are our broader family, assist when needed and when in need.

Mutuality. Respect our colleagues and our clients as you would like to be respected.

Realising potential. Unlock your full potential, encourage and support your colleagues.

Embrace change. Strive for excellence; be open minded and willing to embrace change.

Health and energy. Work towards being well balanced within yourself.

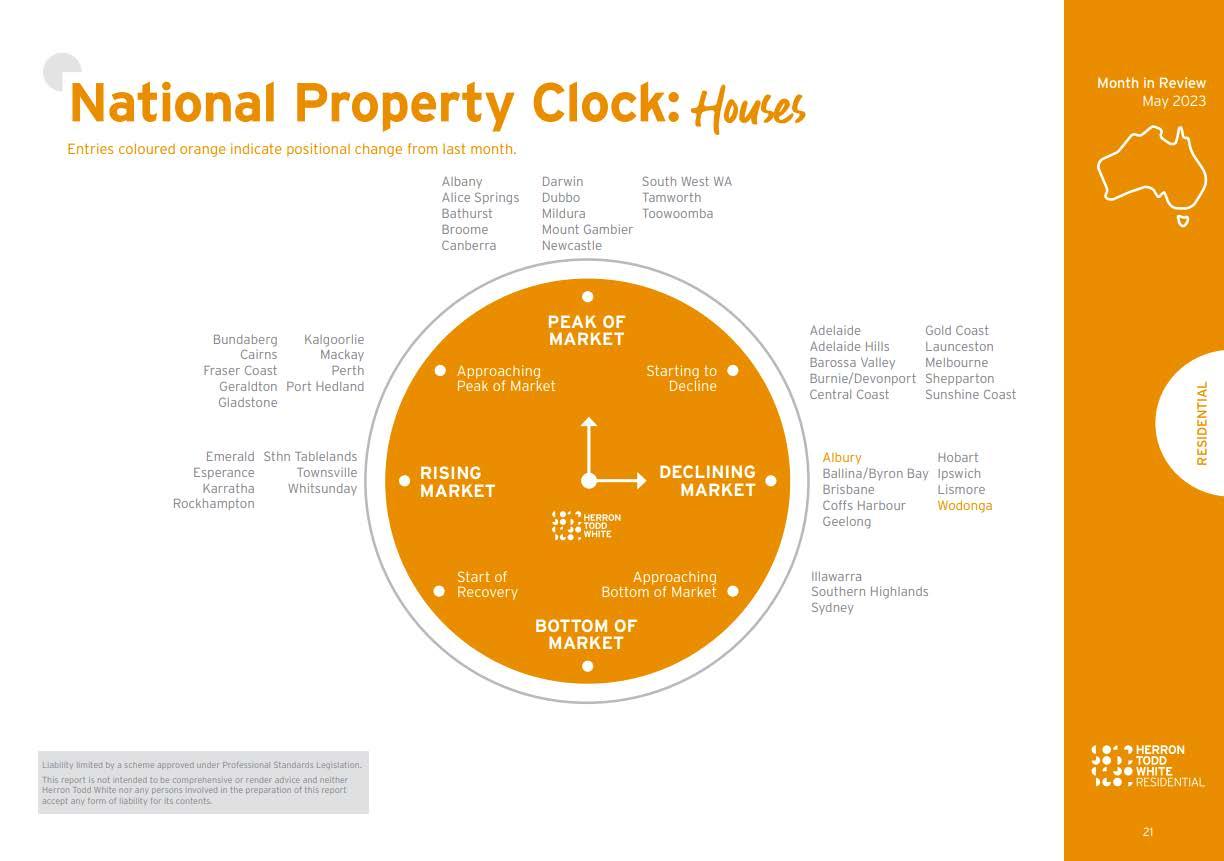

Australia has is forecasting of 400,000 people will have migrated to Australia by the end of this financial year and another 315,000 people will have moved here by the end of 2024

Immigration can have both direct and indirect effects on property prices. The importance of immigration to property prices depends on various factors and can vary depending on the specific market conditions. Here are a few key points to consider:

1. Increased Demand: Immigration can lead to an increase in population, which in turn increases the demand for housing. When more people move into an area, the demand for housing rises, which can push property prices upward. This is particularly evident in areas experiencing significant population growth due to immigration.

2. Economic Growth: Immigration can contribute to economic growth by bringing in new skills, labor, and entrepreneurship. When immigrants contribute to economic development, it can attract more investments and businesses, leading to job creation. This increased economic activity can positively impact property prices as well.

3. Localization of Demand: Immigrants may have specific preferences for certain neighborhoods or areas, leading to localized increases in demand and subsequent property price appreciation in those areas. Immigrant communities often form ethnic enclaves, where residents prefer to live in close proximity to others from their home country or cultural background.

4. Rental Market: Immigration can impact not only property prices but also the rental market. Immigrants, especially those who have recently arrived, may be more likely to rent properties rather than purchase them immediately. This increased demand for rentals can drive up rental prices in certain areas.

5. Neighborhood Revitalization: In some cases, immigrants may move into neighborhoods that have experienced decline or disinvestment. Their arrival and subsequent investment in housing and businesses can contribute to neighborhood revitalization, leading to an increase in property values over time.

It is important to note that the impact of immigration on property prices is not uniform and can vary depending on local market conditions, housing supply, government policies, and the overall economic climate. Additionally, factors such as housing affordability, availability of land, and housing regulations also play significant roles in determining property prices.

I hope this helps in the journey of either buying or selling a property.

Regards,

Dean O’Brien Corporate Director

Nadine Borschmann has spent the past five years “dipping in and out” of a quest to buy her first home in Melbourne.

The 35-year-old nurse unit manager is determined to buy somewhere a reasonable distance from work and family but like many she is struggling to find something she can afford, even in less pricey suburbs, as interest rates rise and fewer homes are listed for sale.

“I was renting in Collingwood and East Melbourne, but I moved out of my last rental to save more money, so I’m not renting now,” Borschmann said. “I want to save a bit more for a deposit, that will help especially in the context of interest rate rises.”

First time buyers like Borschmann have faced 11 interest rate rises since May last year, which has severely limited the amount they can borrow, and they are now stuck waiting in a market where potential vendors want prices to boom before they list.

More competition for fewer properties means some houses are selling well above expectations, making it harder for buyers to get their feet on the property ladder.

Agents say first home buyers are taking the opportunity to try to get into the market before interest rates or property prices, or both, rise again.

There was a 10.7 per cent uptick in new loans to first home buyers in Victoria in March, the latest month for which Australian Bureau of Statistics figures are available, compared to February. But they remain at less than half the amount granted in the peak month of January 2021.

“I think people are getting used to what is now becoming the norm with higher interest rates,” OBrien Real Estate Berwick’s Paul Rogers said.

“I’m definitely finding there’s more inquiry when we have a first home property on the market - even if the range is higher they seem to be stretching to homes priced between $800,000 and $900,000,” he said. “I sold one recently for over $1 million to a first home buyer so that’s certainly getting up there.”

Rogers said some buyers would be getting help from the Bank of Mum and Dad to get into the market, given the higher prices they were paying.

Others are using state and federal government incentives like stamp duty exemptions or concessions, the shared equity scheme and the home guarantee scheme – which allows a purchase on a deposit of 2 to 5 per cent.

Economic policy program director at the Grattan Institute, Brendan Coates, said first home buyer support like this was helping to bring forward first home buyer purchases.

But at the same time they were pushing up prices, as buyers redirected extra savings from things like stamp duty exemptions to their home-buying budgets.

Coates’ said the key focus needed to shift from financial support for first home buyers, to increasing housing supply.

“We should always be really careful about demand side intervention because the larger you make [these home buyer schemes], the more they’re likely to just push up prices,” he said.

In the inner city, fewer property listings for first time buyers has led to greater competition at auctions.

This week, four first home buyers competed at the auction of a two-bedroom unit in Brunswick.

The property at 1/811 Park Street had an advertised price range of $600,000 to $650,000 and sold for $730,000 –$100,000 above the reserve – to a young professional.

Nelson Alexander Carlton North director Nicholas West said first home buyers were definitely back in the market, getting in before any further house price hikes.

“A lot of first home buyers have had to work through a lot of confusion over interest rates, and there’s a lot of noise about rising prices,” West said. “But there is a light at the end of the tunnel with interest rate rises looking to be near the end. Buyers are thinking ‘I’ve just got to get on with it’.”

Borschmann’s buyers agent, Property Home Base’s Julie DeBondt-Barker, said first time buyers were still keen to get into the market, but were rethinking what they could afford.

“Flexible buyers are checking our new suburbs and reconsidering the type of property they can buy,” DeBondt Barker said. “Interest rates are cutting the amount first home buyers can borrow quite significantly, and there’s also the supply and demand issue, until more stock and properties come onto the market this issue isn’t going to change.”

Borschmann said that though she had her heart set on buying a house with land, she had been forced to rethink, given her budget. She is now considering a villa unit further away from the city.

“It’s hard, but I just need to be persistent and keep going really,” she said.

The quality of our service stems from the importance we place on the people behind our network.