Enjoy a dining experience that’s unique to your taste. Choose anything you like from our extensive regional menu at any time throughout your flight, from delicious canapés to a five-course meal, or indulge in dessert first.

EMIRATES FIRST

23 19 31 10

10 Could the Airlink model be Pakistan’s Shining City on a Hill?

17 Haval sales dip amid year-end effect, poised for January rebound

19 Inside the raid that halted Pakistan’s agricultural trade

22 Systems Ltd: The growth engine the market continues to believe in

23 An IPO resurgence at the PSX in 2024 may signal an economic turnaround

28 Has Jazz finally broken the jinx on the sale of Deodar?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

By Zain Naeem

You either believe in the free market or you don’t. And no, we are not referring to free market ‘types’ whose lives are dictated by stock prices, cryptocurrency, and whatever it is that characters like Elon Musk are doing on any particular day. We mean you either believe a free-market economy is the best way to promote the growth and well-being of a people or you don’t.

This is an economic system defined by low taxes, few capital restrictions, and even fewer barriers to entry. And without an economy to micromanage, a government should ideally have the time to complement this environment through reasonable social services like housing, healthcare, and, perhaps most importantly, education.

At Profit, our reporting is often greatly informed by this belief. By all indications, the raw ingredients for a successful and thriving economy exist in Pakistan. We have a young population with rising literacy and sufficient domestic savings, that is a domestic banking sector large enough to result in relatively lower costs of capital. But unlike the model we have discussed above, in Pakistan, the government is less a helping hand and more a mountainous road-block made worse by constant political instability.

Despite this, the signs are clear if you take a closer look at some of the companies that have emerged in the past couple of decades. Case in point: Airlink.

Starting off as an Association of Partners (AOP) in 2010, Airlink began as an importer and distributor of 3G enabled smartphones and tablets when 3G licences first went live in Pakistan. They were an early mover at a time when smartphones and fast, reliable, mobile internet was making a splash in Pakistan. In the 14 years since, Airlink has gone from importing, to packaging, and now assembling technological devices inside Pakistan.

On the surface, the success of Airlink might seem like a drop in the ocean. And someone might justifiably ask what the big deal is about a company that has been around since 2010 starting to assemble certain products domestically. It isn’t like they are manufacturing them on their own.

That is fair enough. It really could be nothing. But then again, it could be the start of something. Beginning to assemble products is the first step companies in any developing economies take.

In August this year, Airlink announced it would begin assembling Acer laptops, one of the largest laptop manufacturers in the world. As we noted back then as well, it is tempting to think of this development as being similar to the launch of the electronics manufacturing capabilities of East Asian companies, including Acer itself, which originally started off as an importer of Japanese and American electronics (like Air Link), before moving into assembling those products (like Air Link) be-

fore eventually developing complex manufacturing capabilities originally made available for contract for foreign brands before eventually launching its own global brands.

Only time will tell whether or not Airlink could be that company for Pakistan. What we can say for sure is that this country clearly has the chops to be home to a company like Airlink. Which is why it might be worth looking into how they get where they did, and what it tells us about Pakistan’s economy and its future.

Airlink would barely have been noticed when they first took root in 2010. So much so that when the company started out, it was not even incorporated, instead existing as a loose Association of Persons. This was a time when Pakistan was first entering the 3G world, and the demand for mobiles and tablets capable of supporting this new bandwidth was going to increase.

Airlink was initially an importer and distributor of mobile cellphones in Pakistan, taking advantage of a conducive regulatory environment that allowed the tax-free import of cellphones, as the government was keen to encourage the adoption of mobile telephones by the wider population.

It quickly expanded from just cellphones into the import and sale of laptops and tablets as well, eventually growing to a point where it decided to incorporate itself formally in 2014. By this point, their business had already expanded into import, export distribution, indenting, wholesale and retail business. Airlink was dealing in mobile phones, tablets, laptops and accessories which came under the AOP but the assets were acquired by the incorporation.

In the industry that existed before Airlink, retailers and wholesalers would contact and procure the phones either from vendors or companies in the other country. It was the responsibility of the retailer to be able to get the latest phone and then sell it in the local market as soon as possible. With the nature of technology, the retailer had to make sure he could sell his product at a profit as quickly

as possible. This forced the retailers to not be picky in terms of only importing a single brand and they tried to get as much of the revenue as possible in each release cycle. Airlink changed all that. The primary attraction was that it would become an authorized dealer who would import and distribute only certain brands that it had a contract with.

It started off small by only importing from Huawei and Samsung but has slowly gained additional authorizations from Apple, TCL and Tecno as well over the years. Airlink now boasts a wide network of distributors who make up 20 to 25% of the market share in terms of the import market alone. Due to its success, the company has been awarded by Huawei and Samsung and now has 16 regional hubs with more than 1,000 wholesalers and 4,000 retailers as a part of its network.

Their initial revenues and success can be boiled down to two simple words: Value addition. This is a process by which some additional value is attached to the product that either was not present in the past or was not being valued to the same degree. Imagine a fruit manufacturer who brings a piece of fruit from the farm to the market. He takes the fruit from the farmer, picks out the best of the produce, washes it, packages it and then puts his name on it. The customer relies on the person packaging to be doing the picking and sorting for him and trusts the brand to be of high quality. Even though the one packing it did not grow it, his name on the label acts as a guarantee for the market. Airlink was doing something similar.

It buys the completely built unit (CBU) from a phone manufacturer it has contracted with and then sells it in the local market. It

attaches warranty, after sale service guarantee and a seal of approval on the product which gives ease of mind to the customer that the product they are buying is of good quality. Similar products are also available but Airlink is able to add its trust and certification which becomes part of the product. In return, the customers divert a higher amount of revenues towards them. With a widespread distribution network, this advantage has been capitalized on as well.

By operating a distribution network initially, Airlink was able to gain a foothold in the market which was leading to higher profits. With exclusive distribution rights and experience in the field, Airlink was showing that it could keep earning more revenues in the future. At this juncture, the government took the decision of clamping down on illegal imports that were flooding into the country. Rather than buying in the Pakistani market, certain people were bringing phones purchased in the international markets and selling them locally. This allowed them to circumvent the duties and taxes applicable on the imports leading to higher profits. As the grey market started to grow, the government implemented Device Identification Registration and Blocking System (DIRBS). Simply put, the phones that had been imported through one route or another had to pay all the fees and duties due on them before they could be operated using a Pakistani sim card. Bad news for the illegal importers became good news for Airlink as they were importing and distributing on official terms.

Airlink hasn’t done anything revolutionary here. They followed a simple model. They began by importing products and distributing them. Eventually, they grew their list of associates and started packaging and providing after sale services for these products as well.

The next step that was under consideration was to establish an assembling facility in Lahore. The secret sauce that had been used till this point was to establish relationships between the manufacturers across the border

and the customers. Airlink was the facilitator or the conduit that was allowing this relationship between producers and consumers to be formed. By establishing a local assembly facility, the company was going to import semi knocked down or completely knocked down parts and then assemble them using the Pakistani workforce. In 2020, they expanded into smartphone assembly. They initially signed on to assemble Android phones made by the Chinese manufacturer Tecno.

This was a gentle wade into the water from Airlink. Tecno was a low-value brand with cheaper phones and they found some initial success with it. With their existing and expanding import and distribution business, Airlink was growing fast.

On the back of their financial performance, Airlink went for an Initial Public Offer (IPO) in 2021. The revenues and profits being generated were conducive for such a move, and an offer of 60 million shares was carried out in order to generate funds to pay off some of its Term Finance Certificates and to increase its working capital. It was felt that, with the use of smartphones expanding in the country and introduction of 4G technology, the demand for low cost smartphones was going to increase and it was poised to capitalize on it. With a bigger war chest, the revenues were given a further boost as the additional funds could be used to establish in more far flung areas to reach a wider customer base.

Following the IPO, in 2022, Airlink also signed on to assemble Xiaomi phones in Pakistan, a comparatively high-end brand. Almost immediately it was clear the local assembly business was significant not just for them but for Pakistan. For Air Link, it constitutes about 70% of its total revenues, and gives it a market share of between 30-40% among domestically assembled smartphones. Xiaomi and Tecno have rapidly climbed the ranks in Pakistan’s smartphone market, with Xiaomi now the fifth-largest brand and Tecno the fourth among

locally assembled phones. In aggregate, Air Link now accounts for approximately 6% of all cellphones sold in Pakistan.

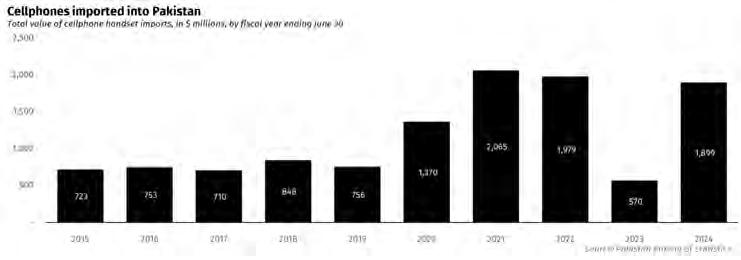

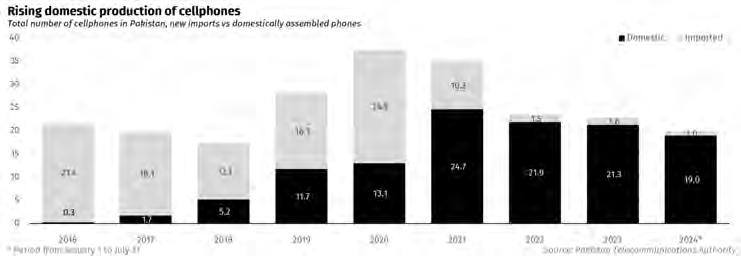

As recently as 2016, just 1% of the cellphones sold in Pakistan were assembled inside the country, but in the first seven months of 2024, almost 95% of all cellphones sold in the country were assembled domestically. And locally assembled phones are increasingly more likely to be smartphones. According to the PTA’s data, in 2019, only 1% of domestically assembled phones were smartphones, a number that rose to 62% during the first seven months of 2024.

All of this is happening in an environment where the demand for cellphones continues to rise. Like most countries in Asia, smartphone penetration rates have been rising in Pakistan. About 56% of the population has a broadband internet connection that they access through their mobile phone, implying that they have a smartphone. According to data from the Pakistan Telecommunication Authority (PTA), annual mobile phone demand is rising by 6% per year for the past decade, with a particular surge expected this year. Total sales are expected to reach 33 million units in 2024, up from 22.9 million in 2023, which was a uniquely bad year as a combination of a sharply depreciating rupee, high inflation, and government-imposed import bans all conspired to severely limit the sale of new mobile phones in the country.

The year 2024 is therefore one of recovery, and the expected surge in demand comes despite the recent imposition of an 18% sales tax on mobile phones in the federal budget for the fiscal year ending June 30, 2025.

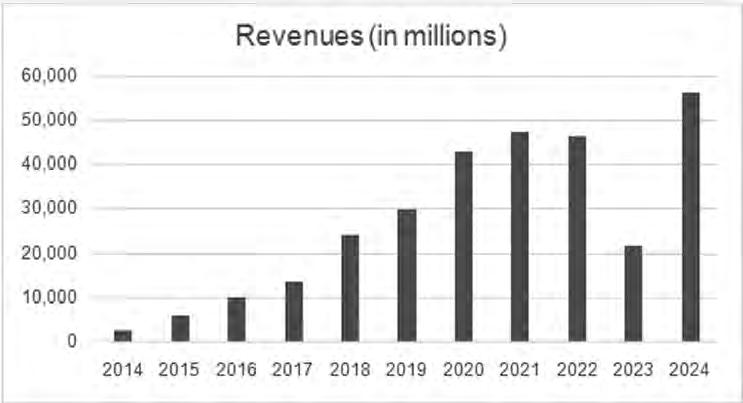

The revenues of Airlink have grown substantially from where they were in 2014. Airlink recorded revenues of Rs 2.3 billion in 2014 which grew to Rs 56 billion by 2024. A compound annual growth rate of 38% over a period of 10 years is not something to scoff at.

However, the road has not always been easy. One of the biggest problems for Airlink had been the fact that it had too much debt on its books which were used to finance its working capital. One of the reasons that an IPO had been considered was down to the fact that it had carried out excessive borrowing. In 2017, accounts showed a debt of Rs 2 billion which had grown to Rs 9.3 billion by 2020. In terms of its assets, 35% was being used through liabilities in 2017 which grew to 53% by 2019. The profitability being generated was able to mask some of this impact as its equity was growing at a more rapid pace. The cause for concern could be seen by the fact that in 2020, interest expense of Rs 1.4 billion was paid out which made up 95% of its net profit.

One of the big moves that helped this problem in this time was the establishment of a local assembly. Rather than importing the whole phone, only their parts would be imported which would reduce some of the burden on the import bill. Secondly, customers would be able to buy slightly cheaper products and have access to genuine spare parts which can be sourced from local shops rather than having to be imported as well. Airlink was already importing the parts individually so consumers would be able to buy them directly. The last benefit was going to be for Airlink itself. In the past, it could only charge a markup on the price at which the phone was being sold for. These margins were growing in value, however, they made up a small percentage of the total price. By establishing an assembly unit, the company was essentially vertically integrating another process of production. By

bringing this element under its own control, it was able to absorb another source of profitability and margin which was not available to it before.

The expansion of companies authorizing Airlink has kept growing steadily as it is now associated with Itel and Xiaomi. The company has also ventured into the laptop assembling business with a cooperation with Acer to assemble their computers in Pakistan. There has also been an investment of Rs 8 billion in a subsidiary called Select Technologies (Private) Limited which has collaborated with Xiaomi for assembly of handsets and televisions. With the recent interest in electric vehicles, the CEO also announced that they had imported 2 units of the XU7. Even though no plans of an assembly are being promised for now, the company still has a brighter future ahead of it.

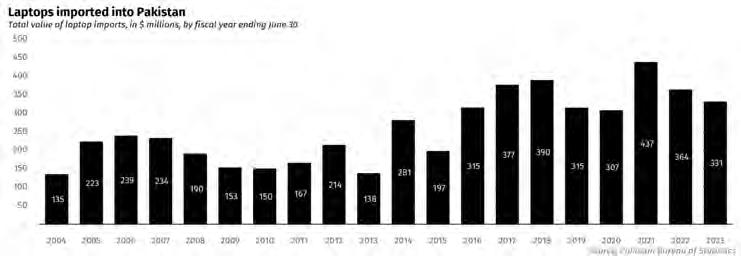

The decision to start assembling Acer laptops is also one that could prove important given Pakistan’s demographics. The median age in the country is 21, and in urban areas at least, youth literacy rates are very high, as much as 90% in some metropolitan areas, meaning that the largest cohort of Pakistan is just now aging into becoming part of the workforce, is literate, more likely to be urban than the past, and is more technologically savvy than its parents, creating the demand for smartphones, but also for laptops. Cheaper laptops are particularly in demand because students, young professionals, and people working remotely all require reliable laptops. Companies also need these for their employees, where work is increasingly done on laptops rather than desktop systems.

The company aims to sell 120,000 units in the Rs125,000 to Rs175,000 price range, which could result in around Rs15-20 billion in annual revenue in the first year. Pakistan’s laptop market, estimated at around 400,000 to 500,000 units annually, though this represents a sharp slowdown from the nearly 900,000 units the country imported during fiscal year

2022, according to data from the Pakistan Bureau of Statistics (PBS). The industry has so far relied heavily on imports. According to Airlink’s management, local production of these devices could not only boost its market share in this large and growing market but also position the company to secure lucrative contracts with federal and provincial governments for their laptop distribution schemes for students.

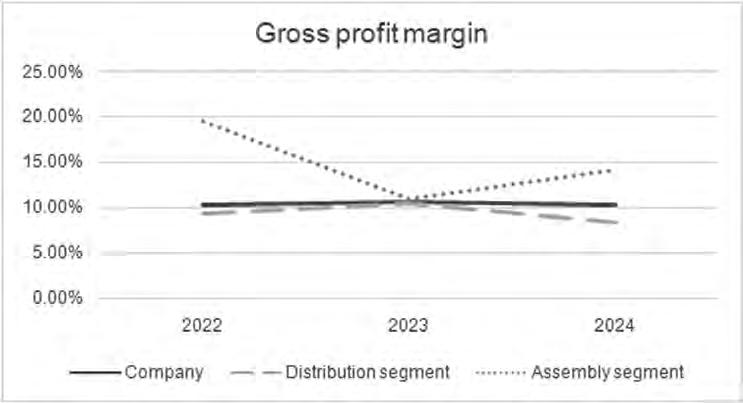

In terms of profitability, Air Link operates on relatively low single-digit gross and net margins. Even this has seen a marked improvement since the company began assembling products in Pakistan.

Taking a closer look at the financial performance, it can be seen that there has been consistent growth in revenues from 2014 till now. The only year there was a fall in income was in 2023, which was a uniquely horrible year for the sector thanks to multiple factors. The appreciation in the dollar meant

that there was an increase in the price of the phones which were being imported or made locally. Compounded by inflation, people did not have the capacity to buy big ticket items like phones. The government also placed a ban on imports owing to the disastrous current account situation which also had an effect on the supply of phones.

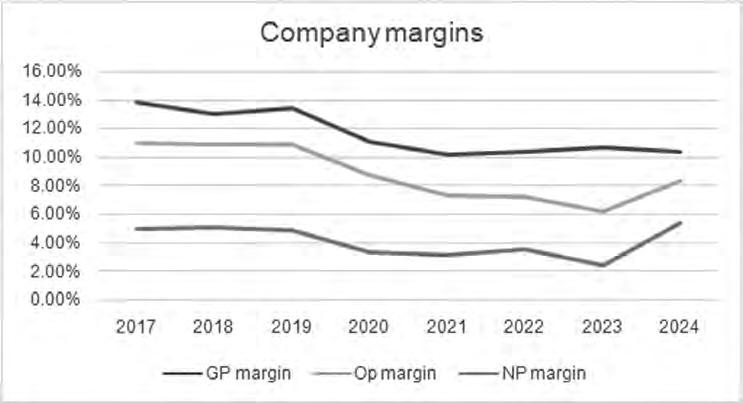

After a slump, Airlink was still able to bounce back by recording its best ever year crossing the Rs 50 billion threshold in 2024. In 2017, a gross profit margin of 14% was seen which has steadily fallen to 10% by 2024. The margin that Airlink can charge on a phone is dictated by the phone manufacturers on the CBU which means that there is a constant balance that has to be carried out to make sure the products are attractively priced and yield a better margin.

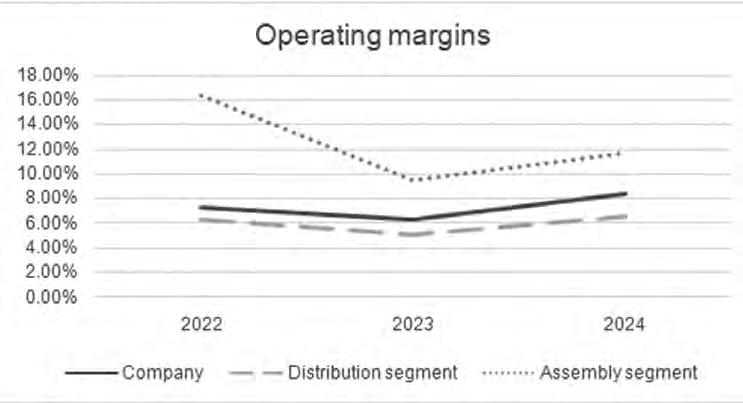

The reality is that the situation would have been much worse if the company had not branched out into the assembly business. In 2020, before the assembly came online, Airlink made a gross profit margin of 11% from its retail and distribution business. In 2022, the assembly was operating in conjunction with the distribution. The assembly earned a gross profit margin of 19.5% compared to retail which accounted for only 9.33%. This shows that the decision to manufacture using an assembly proved to be beneficial as there was more control over the supply chain. By 2024, the gross margins for assembly and retail business stood at 14.1% and 8.32% respectively. Due to its diversification to go into assembly, it was able to get a bigger chunk of the profits than it was before. If the same trend continues, being able to assemble a larger product portfolio in terms of phones and laptops, the company can expect to see gross margins growing further as well.

A similar trend was seen down the profit and loss statement. Operating margins stood at 11% in 2017 and started to fall to 8.36% for the whole company by 2024. Before

the assembly started, operating profits were around 8.78% from the retail business in 2020 which fell to 6.26% in 2022 when the assembly started and stabilized at 6.54% in 2024. In contrast, the assembly segment saw an operating margin of 16.4% in 2022 which decreased to 11.7% by 2024. Even though both ratios fell, the assembly was still able to generate better returns.

Lastly, the net margin was hovering around 5.08% in 2017 and stayed around the same levels by 2024. From 2020 to 2024, the retail business was able to earn net margins of 3% while the assembly business saw its margins of 16.4% in 2022 decreasing to 9.4% by 2024. All this analysis shows is that the company was able to supplement its revenue streams by adding assembly to its retail business. The additional benefit of this move was that the assembly business was generating a higher return leading to greater profits.

Another important fact that has changed over time is the fact that in 2020, all of the revenues were being generated from retail business which has fallen to 65% as assembly revenues have started to make up a greater percentage of the total revenues. With greater proportion and better margins, Airlink can expect its bottom line to grow as it relies more on locally produced products rather than selling imported phones.

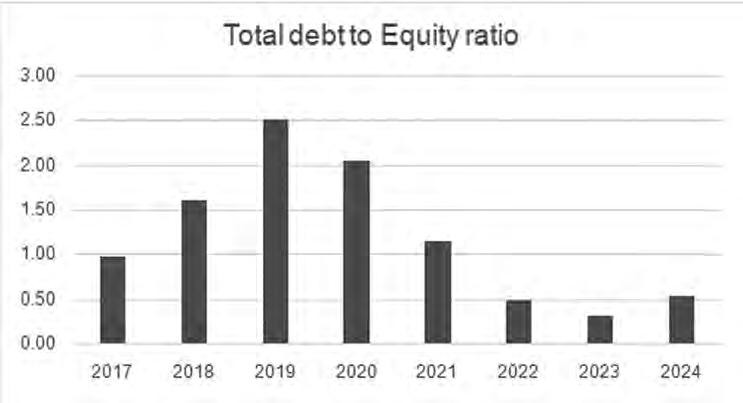

As the profits increase, the debt to equity ratio has also seen much improvement owing to the IPO and appropriated profits racking in. In 2019, this ratio was 2.5 times which meant that for every rupee invested, it was taking 2.5 rupees in loan. In 2024, this ratio has fallen to 0.52 times which means that it is only taking Rs 0.5 rupee against Rs 1 that it holds in equity.

Another card up the sleeve is that it is not allowed to export under the agreements that it has signed with its principal. However, in case of low inventory movement, Airlink does export to international markets. From

2017 to 2020 and even 2022, the company has exported its devices to international markets which shows that local as well as international markets can be catered to.

In a way, the circle is finally complete. From a company which imported its products primarily, Airlink has been able to not only assemble the phones locally but also look to export phones abroad which is the goal of any such business model. In normal circumstances, the aim of a business is to establish itself, consolidate its position and then grow in size. In the case of Airlink, its objective was to first establish itself. It was able to do so by importing all its goods and attaching some value to the product they were selling. Once they gained a foothold, their next step was to gain a bigger piece of the pie. They did so by setting up their own assembly line. As Pakistan does not have much of the raw material, the next best thing was done by importing the materials and then using local workforce. This allowed for further value addition and some level of import substitution which allowed for greater margins to be earned. It has also shown

that the new assembly line was more profitable and was able to sustain the revenue and margin growth as well.

The last step in the value addition process has been that the company has assembled the phones locally and then exported them which has not only added to the bottom line but also improved the financial standing of the country. As the assembly line broadens and the laptops are also added to the product portfolio, it can be expected that the topline will continue to grow further.

Air Link assembled about 1.2 million cellphones in Pakistan in 2022. Despite the fact that it is utilising only a fraction of its 3.2 million units smartphone assembling capacity, the company appears bent on continuing its expansion, both into laptops as well as the production of smart television sets. Airlink is set to launch Xiaomi Smart TVs in Pakistan, tapping into the country’s growing demand for smart home devices. The smart TV market, currently dominated by brands like TCL, Haier, and Samsung, is estimated to reach 1.2 million units by 2025, according to estimates by Topline Securities. Airlink’s entry into this market is a strategic move, with the company planning to assemble and distribute Xiaomi Smart TVs at a slightly lower price point than its competitors.

All of this points towards a company that has what it takes. They have followed a path that is not unique or a great discovery. What they have done very well is identify demand, stick to their plans, reinvest in themselves at the right time, and they are poised to continue being a force in Pakistan’s tech gadgets sector. We also have proof that they have and can export their products too. If they stay the course, there is no reason to think they cannot take the next step as well. While this final very important step remains, what matters is it has given us proof that it can be done. That alone is a win for anyone that believes in Pakistan’s economic future. n

The tractor manufacturer turned SUV assembler is not immune from the trend of Pakistani consumers preferring to buy the newest models rather than buying the year-end model of the outgoing year

In a development that underscores the cyclical nature of Pakistan’s automotive market, Sazgar Engineering Works Limited (SAZEW) reported a significant decline in its four-wheeler sales for November 2024. The company, which has become a notable player in Pakistan’s evolving auto sector through its partnership with Chinese automaker Great Wall Motors, saw its monthly sales drop by 42% compared to the previous month.

According to a flash note released by Topline Securities, SAZEW sold 584 units of its Haval brand vehicles in November, marking a substantial decrease from October’s figures. This decline, however, is largely attributed to what industry experts call the “year-end effect,” a phenomenon well-known in Pakistan’s automotive circles.

The year-end effect refers to a common trend where potential car buyers postpone their purchases in the final months of the year, preferring to wait for vehicles with new-year registrations. This preference is driven by the perception that newer registrations enhance resale value, a crucial consideration in Pakistan’s price-sensitive auto market.

Asad Ali, an auto sector analyst at a leading brokerage firm, explained, “It’s a pattern we observe every year. Customers often delay their purchases in November and December, aiming for deliveries with the print of the new year. This trend is particularly pronounced in the four-wheeler segment.”

Despite the sales slowdown, SAZEW’s production numbers remained relatively stable, declining by a mere 1% month-on-month. This stability in production, coupled with the sales dip, signals robust demand for Haval vehicles, with deliveries likely to surge in January 2025.

The company’s dealership network is already adapting to this anticipated demand. Channel checks conducted by Topline Securities reveal that dealers are now offering 2025 registrations to customers, a strategy aimed at capturing the pent-up demand expected to materialize in the new year.

This sales pattern is not new for SAZEW. In December 2023, the company experienced an 89% month-on-month drop in four-wheeler

sales. However, this was followed by a remarkable rebound in January 2024, when sales soared to 967 units – a figure 3.9 times higher than the monthly average observed from July to November 2023. Industry analysts are optimistic about SAZEW’s prospects for early 2025. If the current trend persists through December 2024, projections suggest that January 2025 could see sales skyrocket to between 1,700 and 2,000 units. This potential surge would clear the inventory being produced in November and December 2024, setting a strong tone for the company’s performance in the new year.

SAZEW’s journey in Pakistan’s automotive landscape is a testament to the changing dynamics of the industry. Founded in 1982, the company initially focused on manufacturing auto rickshaws and motorcycle wheel rims. Its entry into the four-wheeler market came through a strategic partnership with Great Wall Motors, one of China’s largest automakers, in 2021. This collaboration marked a significant milestone for SAZEW, allowing it to introduce the Haval brand to Pakistan. Haval, known for its SUVs and crossovers, has quickly gained traction in the Pakistani market, offering a blend of modern features and competitive pricing that appeals to the country’s growing middle class.

The partnership with Great Wall Motors is part of a broader trend of Chinese automakers entering Pakistan, a market long dominated by Japanese brands. This influx of Chinese auto companies has intensified competition and provided Pakistani consumers with a wider range of choices, particularly in the SUV segment.

SAZEW’s transition from a components manufacturer to a full-fledged automaker reflects the evolving landscape of Pakistan’s auto industry. The sector has seen significant changes in recent years, with the government’s Automotive Development Policy (2016-2021) encouraging new entrants and fostering increased competition.

Despite the current dip in sales, SAZEW’s overall performance in 2024 has been robust. The company has maintained a standard delivery time of up to 3 months for its Haval models, with some variants available for immediate delivery with a nominal premium. This indicates a healthy demand-supply balance and efficient inventory management.

Financial analysts remain bullish on SAZEW’s prospects. Topline Securities maintains a “Buy” stance on the company’s stock, citing attractive valuation metrics. The brokerage firm projects a forward price-to-earnings (PE) ratio of 4.17 and 3.57 for fiscal years 2025 and 2026, respectively. These figures compare favorably to the broader auto sector’s PE ratios of 9.1 and 7.2 for the same periods.

Moreover, SAZEW is expected to offer dividend yields of 6% and 7% based on projected annual sales of 10,993 units (monthly average: 916) and 11,543 units (monthly average: 962) for fiscal years 2025 and 2026, respectively. These projections underscore the company’s potential for both growth and shareholder returns.

The company’s performance is particularly noteworthy given the challenges facing Pakistan’s economy. The country has grappled with high inflation, currency depreciation, and balance of payments issues in recent years. However, the auto sector, particularly the SUV segment, has shown resilience, buoyed by changing consumer preferences and the entry of new players like SAZEW with its Haval brand.

Looking ahead, SAZEW faces both opportunities and challenges. The growing demand for SUVs in Pakistan presents a significant growth avenue, but the company must navigate issues such as potential supply chain disruptions, currency fluctuations, and evolving government policies in the auto sector.

The broader context of Pakistan’s auto industry also plays a crucial role in SAZEW’s outlook. The sector has been a focal point of economic discussions, with policymakers keen on increasing localization, boosting exports, and creating employment opportunities. SAZEW’s success with the Haval brand could potentially contribute to these national objectives.

As Pakistan’s auto market continues to evolve, companies like SAZEW are at the forefront of shaping its future. The upcoming months, particularly January 2025, will be crucial in determining whether the current sales dip is indeed a temporary year-end phenomenon or indicative of broader market trends.

For now, all eyes are on the new year, when SAZEW and its Haval brand are expected to hit the ground running, potentially setting new benchmarks in Pakistan’s increasingly competitive automotive landscape. n

An investigation into the DPP over rice exports brought trade operations to a halt last week. This is what went down

arly last week, agricultural trade in Pakistan came to a grinding halt. Overnight, the Federal Investigation Agency (FIA) arrested nine inspectors of the Department of Plant Protection, which is a department of the Ministry for National Food Security and Research.

The raid, by some accounts, was given the final green light by Prime Minister Shehbaz Sharif himself. With nine of their inspectors in custody, the remaining DPP inspectors stationed at Pakistan’s ports became reluctant to inspect and clear shipments leaving and entering Pakistan, afraid they could get caught up in the situation.

So what was going on? Behind the scenes, a government committee had been investigating issues in consignments of Basmati Rice going from Pakistan to the European Union this year. Many of these consignments had been stopped at the ports because they had certain contaminants in them.

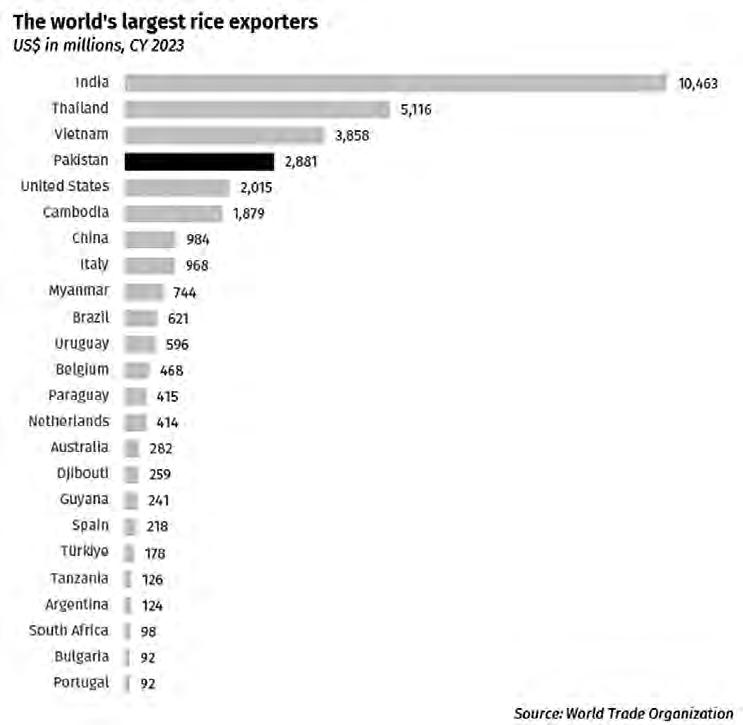

This is a bigger deal than it sounds. Over the past few years, Pakistan has become the dominant exporter of Basmati to the EU precisely because Pakistani consignments have been cleaner and contaminant free compared to rice shipped out from India. This year’s export, at a time when India is already reopening its export of rice, may be detrimental to Pakistan’s foothold in the EU’s Basmati market.

Let us get this part out of the way. The DPP has a very simple job. They are supposed to keep certain contaminants out of Pakistan, and not allow other contamination in the shipments of agricultural products that Pakistan exports.

You see, agricultural trade the world over is party to many protocols and biosafety rules. There are certain foreign bodies and organisms that are harmless in a particular region through centuries of evolution, but are particularly brand new in other regions. If these organisms are transported, they could wreak havoc on the natural habitat of other global regions. In addition to this, agricultural products are also strictly tested for genetic modification, pesticides, toxicity, heavy metal poisoning and all sorts of other contaminants.

It is the job of the DPP to monitor this and meet strict conditions. In this regard, Pakistan’s export have been pretty clean, and have met very strict European standards.

Overall, the European market has proven a rich area for Pakistani rice, and the Indian exporters have failed to capture it in the same way. In 2019/20 Pakistan’s exports to the EU grew to over 250,000 metric tonnes while those from India fell to under 120,000 metric tonnes. During the last two decades, Basmati rice imports into Europe increased significantly, were valued at $ 551.8 million in 2020,

and are projected to reach $ 866.5 million in 2031. In 2021 imports of rice from Pakistan valued at 329 million euros in comparison to 166 million euros from India according to the European Commission.

This success of the Pakistani rice over rice from India was mainly due to pesticide residues in Indian Basmati and in particular to a decision by the EU commission to decrease the maximum residue level (MRL) for the fungicide tricyclazole from 1 to 0.01 mg/kg starting January 1st, 2018. Instantly the imports from India decreased significantly and Pakistani imports took over. The trend has continued in the past couple of years. In fact, even in 2024, the EU flagged 400 different Indian products.

Naturally, it was worrying when a number of rice shipments to the EU were stopped by the European port authorities. What was the reason for these interceptions? The prime minister formed a fact finding committee to get to the bottom of this sudden change.

The primary task of the committee is to investigate the reasons behind the non-compliance with food safety standards that have led to rice interceptions in EU countries. The main force being investigated by this committee was the DPP, which has failed to enforce these

standards, which has negatively impacted Pakistan’s external trade. The stated aim was to identify responsible officers within the DPP who issued inaccurate phytosanitary certificates and investigate claims that DPP employees created monopolies by selectively licensing fumigation services for personal gain. The inquiry committee, led by retired bureaucrat Shahid Ali Khan, was formed to investigate the interceptions. However, critics note that the committee lacked experts in sanitary and phytosanitary (SPS) measures. While food safety does not fall under the DPP’s mandate—which primarily handles biosecurity—the committee alleged that 46 of the 72 interceptions were linked to phytosanitary certificates issued by DPP officers without proper documentation.

What followed was a dramatic turn of events.

Sources reveal that prior to the raid on the DPP office, FIA Karachi also raided the official residence of the DPP Director General, Dr. Muhammad Tariq Khan. Allegedly conducted without a search warrant or registered case, the raid involved FIA personnel, including two female sub-inspectors, and occurred late Thursday night. The team, led by Malik Junaid Hassan, Inspector of the FIA Corporate Crime Circle, reportedly harassed Dr. Khan’s family while conducting a search of the premises.

The FIA’s actions came from a directive issued by Prime Minister Shehbaz Sharif during a high-level meeting on Thursday evening. The directive followed a report by the Economic Minister at Pakistan’s Embassy in Brussels, Omar Hameed, highlighting 72 interceptions of Pakistani rice shipments at EU ports. The Prime Minister ordered arrests of those responsible for issuing phytosanitary certificates without proper verification of food safety risks.

The FIA’s case centers on procedural lapses by DPP officers. According to the FIR registered by the FIA’s Anti-Corruption Circle in Karachi (FIR 40/2024), officials bypassed required procedures, such as field inspections, lab tests, and compliance verification, when issuing phytosanitary certificates. The accused officials include Fakhar-u-Zaman, Muhammad Waleed Mukhtar, Shahzad Salman, and Shehzad Salman who were previously implicated in FIA FIR 4/2024 dated 23-02-2024 along with Dr. Muhammad Qasim Khan Kakar, Director Admin in DPP (who is on deputation from Balochistan Agriculture Research Institute, Quetta) related to clearance of highly infested food consignment.

Critics within the Ministry of National Food Security and Research (MNFSR) point out that food safety inspections and certifi-

cations are not part of the DPP’s mandate. Instead, these responsibilities fall under the Ministry of National Health Services Regulations and Coordination. Furthermore, Pakistan lacks federal legislation governing food safety, as the subject has been devolved to provinces following the 18th Constitutional Amendment.

This is where things get a little dicey. Who is supposed to be checking all of these things? The DPP has claimed the committee completely ignored their explanations and gave them no prior warning before the arrests. Of course this makes sense. Why would you warn someone they are about to be arrested?

The DPP is claiming their mandate is limited to phytosanitary measures and does not cover food safety inspections, compliance procedures, or certifications, which fall under the jurisdiction of provincial food safety authorities and the Federal Health Ministry. Responsibilities for managing Maximum Residue Limits (MRL) at the farm level rest with provincial agriculture departments, while exporters are accountable for controlling aflatoxin levels during storage, processing,

packaging, and transportation.

Now, this is true but the job to give the final phytosanitary certificate does rest with the DPP. It is classic blame shifting that goes on in government departments. When no questions are being asked, you want to take as much control as possible, but when time comes to take responsibility, everybody says the issue is beyond their jurisdiction.

Since its inception in 1947, the DPP has faced chronic neglect. As Pakistan’s designated National Plant Protection Organization under the International Plant Protection Convention (IPPC), the DPP plays a critical role in regulating agricultural trade. Yet, successive governments have routinely appointed non-technical officials to key positions, ignoring the need for expertise in entomology, plant pathology, and regulatory experience.

Temporary and politically influenced appointments have hindered the department’s capacity to enforce proper biosecurity protocols, jeopardizing Pakistan’s export potential. While the committee found no evidence of bribery, the arrests of DPP officials appear to reflect political pressures rather than substantive wrongdoing.

The controversy underscores the urgent need for structural reforms in the DPP and broader export compliance frameworks.

Addressing systemic weaknesses, including chronic understaffing, lack of accountability, and political interference, is essential to restoring confidence in Pakistan’s agricultural export procedures.

Pakistan is already in a very delicate position when it comes to rice production and exports. The arrests come at a disastrous time for Pakistan’s rice exports. In the financial year 2023-24, Pakistan saw a boom in its rice trade because India, otherwise the world’s largest producer and exporter of rice, had placed a ban on exporting its rice to control prices domestically. Pakistan had filled in some of this void because of the high quality of rice produced in the sub-continent.

Overall, the European market has proven a rich area for Pakistani rice, and the Indian exporters have failed to capture it in the same way. In 2019/20 Pakistan’s exports to the EU grew to over 250,000 metric tonnes while those from India fell to under 120,000 metric tonnes. During the last two decades, Basmati rice imports into Europe increased significantly, were valued at $ 551.8 million in 2020, and are projected to reach $ 866.5 million in 2031. In 2021 imports of rice from Pakistan valued at 329 million euros in comparison to 166 million euros from India according to the European Commission.

This was a small window of opportunity for the first time in decades where Pakistan could have become a large exporter of rice and given India a tough time.

Since the late 1990s, Basmati has become an international phenomenon. The demand for this unique variety of rice has increased in the European and American markets, and where there is demand there is supply. Supermarkets

all over the European Union and the United States are stocked full with Basmati, and this special kind of rice comes only from India or Pakistan.

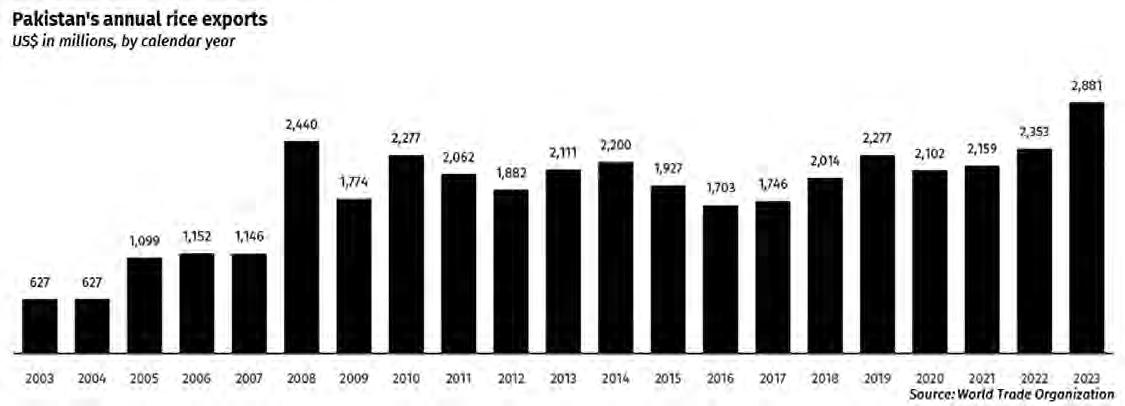

In the United States, it even inspired a copycat that tried passing itself off as basmati, until a lawsuit by the Indian government prompted it to change its name to Texmati, so called because it is grown in Texas. In the past 10 years, Pakistan has exported Basmati Rice in the range of 4.8 lakh metric tons at its lowest in 2016-17, to 8.65 lakh metric tons at its highest in 2019-20.

On average, Pakistan has exported around 6 lakh metric tons of Basmati Rice, mostly to Europe and the Middle East in the past decade. Production of Basmati is much higher than exports, but there is also a very strong domestic demand for Basmati. In the year 2023-24, early estimates suggest Pakistan has increased its Basmati exports by at least 24%, raising them to nearly 7.5 lakh metric tonnes. The export of non-basmati rice, on the other hand, has risen by nearly 32% to over 40 lakh metric tonnes.

The cause of this rise does not have to do with increased productivity, or more farmers turning towards rice. It is simply a result of India’s decision to clamp down on its own rice exports last year. Why do India’s actions have such a ripple effect? Because they are the largest rice producers and exporters in the world.

Of course, this was not always the case. Back in the 1960s, India was consistently one of the largest importers of rice in the world. Pakistan, in comparison, was a significant exporter all the way through to the late 1980s. This started to change in the 1990s, and in what has been a dramatic turn of events, in the past decade India has consistently beaten Pakistan and the rest of the world in both Basmati and non-Basmati exports. The secret to India’s success is a progressive and aggressive rice export policy that has made very effective use

of marketing despite Pakistan’s superior quality and variety of Basmati. But perhaps more importantly, India has been aided by the sheer complacency on the part of Pakistani farmers, millers, exporters, and the government. What we could see in the next few years is the complete decimation of the competitive advantage Pakistan’s variety of Basmati has over India.

The raids and arrests have sparked concerns about their potential fallout on Pakistan’s international trade reputation. Industry insiders fear the EU could impose a blanket ban on Pakistani rice exports, similar to the ban on PIA flights following controversies over pilot credentials.

Notably, 26 of the 72 intercepted rice shipments had all required documentation, yet they were still flagged at EU ports. This indicates that issues extend beyond procedural lapses at the DPP. On the other hand, some shipments issued certificates without proper documentation were not intercepted, further complicating the narrative.

Experts argue that such interceptions are common in international trade, even for countries with robust food safety systems like India, China, and the USA. They question the FIA’s approach, emphasizing that the DPP’s role is limited to biosecurity measures and not food safety compliance. Section 8 of the Pakistan Plant Quarantine Act 1976 provides indemnity to DPP officers for actions performed in good faith.

Legal experts suggest that unless malafide intent or bribery is proven, disciplinary action—not criminal proceedings—should be pursued. Critics also highlight the lack of legal grounds for charges like forgery and fraud in the absence of complaints from rice exporters. The Rice Exporters Association of Pakistan (REAP) has denied any allegations of misconduct by DPP officers, further undermining the FIA’s case. n

Pakistan’s largest publicly traded technology company has continued to surprise the market on the upside with its revenue growth

It is the largest Pakistani information technology company by revenue, and has been growing rapidly for the past decade, having become a market darling for investors of stocks listed on the Pakistan Stock Exchange. The question has always been the extent to which Systems Ltd can keep its stellar trajectory going. Market analysts seem to believe that the answer is “for the foreseeable future”.

According to a comprehensive report by Topline Securities, the company is expected to outperform the broader IT industry, with its market share in Pakistan's IT exports projected to rise to 6.8% by 2027.

Founded in 1977 as one of Pakistan's first software companies, Systems Ltd has evolved into a global player with a diverse portfolio of services and an expanding international footprint. The company, which went public on the Pakistan Stock Exchange (PSX) in 2015, has seen its market valuation soar from Rs4 billion at the time of listing to an impressive Rs166 billion today.

Topline Securities has reiterated its "Buy" recommendation for Systems Ltd, setting a December 2025 target price of Rs707 per share. This represents a potential upside of 24% from the current market price of Rs568.95, with a total expected return of 26% including dividend yield.

The optimistic outlook is underpinned by several key factors.

Systems Ltd is expected to deliver impressive earnings growth in the coming years. The company's earnings per share (EPS) is forecast to grow at a compound annual growth rate (CAGR) of 33% over the next three years (2025-2027) and 26% over the next five years (2025-2029). This compares favorably to the company's remarkable five-year CAGR of 52% from 2019 to 2023.

For the years 2025 and 2026, earnings growth is projected at 38% and 35%, respec-

tively. This rebound comes after an anticipated 24% decline in earnings for the first nine months of 2024, primarily due to economic challenges in Pakistan.

The company's gross margins are expected to improve from 23.9% in 2024 to 25.6% by 2027, driven by cost optimization strategies and the likely absence of exchange losses. EPS is forecast to reach Rs36.5 in 2025, Rs49.1 in 2026, and Rs62.6 in 2027, following an estimated 11% decline in 2024.

Systems Ltd's geographical diversifi-

cation strategy has been a key driver of its growth. In the first nine months of 2024, the company derived 58% of its revenue from the Middle East, 22% from North America, 13% from Pakistan, 4% from Asia Pacific, and 4% from Europe.

The Middle East region has become the company's largest revenue contributor since 2022, with its share more than doubling from 27% in 2020 to 58% in 2024. Topline Securities expects Middle East revenue to grow at a three-year CAGR (2025-2027) of 28% in USD

terms and 35% in PKR terms, reaching US$296 million or Rs96 billion by 2027.

The company's expansion into the Asia Pacific region, which began in 2022, has shown promising results. Revenue from this region is projected to grow at a three-year CAGR (20252027) of 35% in USD terms and 42% in PKR terms, reaching US$21 million or Rs6.9 billion by 2027.

Systems Ltd has consistently outpaced the growth of Pakistan's overall IT export sector. While Pakistan's IT exports have increased at a five-year (2019-2023) and tenyear (2014-2023) USD CAGR of 20% and 12% respectively, Systems Ltd's exports have grown at 37% and 30% over the same periods.

The company's share of Pakistan's IT exports is expected to rise from 5.8% in 2024 to 6.8% by 2027. Topline Securities forecasts that Systems Ltd's exports will grow at a three-year (2025-2027) USD CAGR of 23%, reaching US$391 million by 2027.

Systems Ltd has been strategically expanding its workforce outside Pakistan to tap into diverse talent pools and better serve international markets. The share of employees based in Pakistan has decreased from 95.0% in 2019 to 84.6% by 2024, with a notable increase in resources based in the United Arab Emirates (UAE) from 5.0% to 10.5% over the same period.

The company has also established a resource center in Egypt, which now accounts for 2.5% of its total workforce. This move allows Systems Ltd to leverage Arabic-speaking talent to support its growth in the Gulf Cooperation Council (GCC) region.

Despite this international expansion, Pakistan remains a cost-effective base for IT talent. The average monthly package for a senior software developer in Pakistan is approximately US$1,500, significantly lower than in other popular IT outsourcing destinations such as India (US$2,000), the Philippines (US$2,300), and China or Singapore (US$5,500).

Systems Ltd is expected to generate robust EBITDA of Rs13.0 billion in 2025, Rs17.3 billion in 2026, and Rs21.8 billion in 2027. This strong cash flow generation positions the company well for future acquisitions and inorganic growth opportunities.

The company has already demonstrated its appetite for strategic acquisitions, having invested approximately Rs5.3 billion in recent years (2021-2023) to acquire subsidiaries such as Ndc Tech and Treehouse Consulting, along with their related intellectual property and licenses.

Systems Ltd currently trades at a 2025/2026 forward price-to-earnings (PE) ratio of 15.6x and 11.6x, respectively, compared to its five-year average PE of 16.0x and ten-year average of 14.1x. These valuations are particularly attractive when compared to regional peer companies, which trade at an average PE

of 24.0x.

The company also trades at 2025 and 2026 price-to-sales (PS) ratios of 1.9x and 1.5x, respectively, significantly lower than the regional peer average of 4.1x. This suggests that Systems Ltd's stock may be undervalued relative to its growth prospects and industry peers.

Pakistan's IT industry has been experiencing robust growth, with the country ranked 4th globally for freelance income growth according to Payoneer's Global Gig Economy Index. The government has also been supportive of the sector, with the State Bank of Pakistan recently allowing IT companies to retain up to 50% of export proceeds in specialized foreign currency accounts and permitting foreign acquisitions from those proceeds without prior approval.

These favorable regulatory developments, coupled with Pakistan's competitive advantage in terms of cost-effective IT talent, position Systems Ltd well to capitalize on the growing global demand for IT services.

Despite the positive outlook, investors should be aware of potential risks facing Systems Ltd and the broader IT sector in Pakistan. These include:

1. A potential slowdown in global IT spending, which could impact demand for the company's services.

2. High employee turnover due to competition from startups, freelancing opportunities, and talent migration.

3. Unfavorable government policies that could affect export growth.

4. Substantial appreciation of the Paki-

stani Rupee, which could impact the company's profitability.

5. The possibility of normal taxation being applied to services exporters, similar to goods exporters.

6. Existential threats such as the rise of Artificial Intelligence (AI) that could disrupt the IT industry.

Systems Ltd stands at the forefront of Pakistan's rapidly growing IT industry, with a strong track record of outperformance and a promising outlook for the years ahead. The company's geographical diversification, focus on high-growth markets like the Middle East and Asia Pacific, and strategic workforce expansion position it well to capitalize on global opportunities in the IT services sector.

With attractive valuation metrics, robust financial projections, and a demonstrated ability to generate strong cash flows, Systems Ltd presents a compelling investment case for those looking to gain exposure to Pakistan's thriving IT sector. As the company continues to expand its global footprint and enhance its service offerings, it is well-positioned to maintain its leadership in Pakistan's IT exports and potentially emerge as a significant player on the international stage.

However, investors should remain mindful of the inherent risks in the rapidly evolving IT industry and the broader economic challenges facing Pakistan. Nonetheless, for those with a long-term investment horizon and a bullish outlook on the global IT services market, Systems Ltd appears to be a stock worth watching closely in the coming years. n

Seven companies were listed in 2024, compared to just one the previous year; sponsors appear happier with the valuations on offer in the public markets

Profit Report

The Pakistan Stock Exchange (PSX) witnessed a remarkable revival in initial public offerings (IPOs) during 2024, marking a significant turnaround from the previous year's subdued activity. The bourse saw a total of seven IPOs, including two on the Growth Enterprise Market (GEM) Board, compared to a solitary offering in 2023. This resurgence in capital market activity

reflects growing investor confidence and improved economic conditions in the country.

Companies raised a total of Rs8.4 billion (approximately $30 million) through these offerings, the highest amount in the past three years. The last time the market saw such enthusiasm was in 2021 when eight offerings raised Rs19.9 billion. All seven IPOs in 2024 were oversubscribed, indicating robust demand for new equity investments.

The renewed interest in IPOs can be attributed to several factors, including macroeconomic stability under the International Monetary Fund (IMF) program, positive market sentiment, high liquidity, falling interest rates, and political stability. These conditions have encouraged both companies to go public and investors to participate in new offerings.

The benchmark KSE-100 Index reflected this positive sentiment, surging by an impressive 83% in Pakistani Rupee (PKR) terms and 85% in US Dollar terms year-todate in 2024. This remarkable performance underscores the renewed investor interest in Pakistani equities. Trading activity also saw a significant uptick, with the average daily traded volume increasing by 69% to 545 million shares, while the daily traded value rose by 108% to Rs21 billion during the year.

Let's take a closer look at the companies that made their debut on the PSX in 2024:

1. Secure Logistics Group Ltd (SLGL)

Secure Logistics Group Ltd, a company involved in logistics, tracking, and fleet management services, was the first to list on the main board in April 2024. SLGL offered 50 million shares at a strike price of Rs12 per share, raising Rs600 million. The IPO was oversubscribed by 1.02 times.

SLGL's primary purpose for going public was to deleverage its balance sheet amid a high-interest-rate environment, enhance infrastructure and technology to support its Tech-Pivot initiative, facilitate expansion into regional markets, and optimize fleet-related efficiencies. The company has established itself as a growth-oriented logistics player with a focus on long-haul and distribution segments, serving a wide variety of clients under long-term contracted B2B models.

2. TPL REIT Fund I (TPLRF1)

TPL REIT Fund I, part of the prominent TPL Group technology conglomerate, listed in May 2024. The fund offered 33.5 million shares at a fixed price of Rs17.6 per share, raising Rs589 million with an oversubscription of 1.46 times.

The principal activity of TPLRF1 is investing in real estate projects through Special Purpose Vehicles (SPVs) to generate

income for investors through rental income and capital appreciation. The fund's listing aims to comply with REIT regulations, unblock units, attract foreign investors, and facilitate price discovery.

3. International Packaging Films Ltd (IPAK)

International Packaging Films Ltd, a manufacturer of flexible packaging materials, primarily BOPP (Biaxially-oriented Polypropylene) films, went public in June 2024. IPAK offered 70.1 million shares at a strike price of Rs25.2 per share, raising Rs1.767 billion with an oversubscription of 1.73 times.

The company sought listing to raise funds for repaying long-term debt obtained to finance its expansion project. This project aimed to increase BOPP film capacity from 41,000 tons to 100,000 tons and introduce Biaxially Oriented Polyethylene Terephthalate (BOPET) films with a capacity of 42,000 tons. The total cost of expansion was approximately Rs22 billion.

4. Fast Cables Ltd (FCL)

Fast Cables Ltd, a leading local manufacturer of electrical cables and conductors in Pakistan, listed in June 2024. The company offered 128 million shares at a strike price of Rs24.5 per share, raising Rs3.13 billion with an oversubscription of 1.57 times.

FCL plans to use the funds for acquiring new land, constructing a state-of-the-art building, installing new plant and machinery, repaying debt associated with machinery, and developing building components. The company's successful IPO marks a significant milestone in its nearly four-decade journey, which began with a mission to promote industrialization in Pakistan and contribute to the socio-economic uplift of its citizens.

5. BF Biosciences Ltd (BFBIO)

BF Biosciences Ltd, a joint venture between Ferozsons Laboratories Ltd and Argentina's Bagó Group, went public in October 2024. The company offered 25 million shares at a strike price of Rs77 per share, raising Rs1.925 billion with an impressive oversubscription of 3.4 times.

BFBIO intends to use the raised funds for purchasing raw and packing materials to meet post-expansion working capital needs, acquiring plant and machinery to broaden its product base and improve process efficiencies, and obtaining export certifications such as PIC/S and SRA. The company also plans to support new product development, including Glucagon-like Peptide (GLP-1).

In addition to these main board listings, two companies made their debut on the Growth Enterprise Market (GEM) Board:

6. Mughal Energy (GEMMEL)

Mughal Energy listed on the GEM Board in June 2024, offering 19.4 million shares at Rs16.7 per share and raising Rs325 million.

7. Burj Clean Energy (GEMBCEM) Burj Clean Energy joined the GEM Board in October 2024, offering 10 million shares at Rs10 per share and raising Rs100 million.

The success of these IPOs in Pakistan stands in contrast to the global trend, which saw a slowdown in IPO activity. According to Ernst & Young (E&Y), a total of 870 IPOs were witnessed globally till the third quarter of 2024, raising US$78 billion, compared to 983 IPOs raising US$101 billion in the same period last year. This global decline is attributed to factors such as economic deceleration, the upcoming US presidential elections, geopolitical frictions, and regulatory shifts, which have created uncertainty in the investment landscape.

Looking ahead to 2025, market analysts anticipate more companies coming to market as valuations have significantly increased. The abundant availability of liquidity, partly due to conversion from fixed income investments, is expected to encourage more companies to offer shares in the market.

The success of these IPOs and the overall positive performance of the Pakistan Stock Exchange in 2024 signal a potential turning point for the country's capital markets. As Pakistan continues to navigate economic challenges and work towards stability, the renewed interest in equity investments could play a crucial role in driving economic growth and development in the coming years.

However, potential investors should remain cautious and consider the broader economic context. While the IPO market and stock exchange have shown impressive performance, Pakistan continues to face macroeconomic challenges, including high inflation, currency depreciation, and external account pressures. The country's ability to maintain political stability and continue its economic reforms will be crucial in sustaining this positive momentum in the capital markets.

As Pakistan looks to attract more foreign investment and develop its financial markets, the success of these IPOs and the overall market performance in 2024 could serve as a catalyst for further growth and development in the country's corporate sector. The coming years will be critical in determining whether this resurgence in IPO activity represents a lasting trend or a temporary uptick in an otherwise challenging economic environment. n

The PCB has decided if the BCCI won’t play-ball with them, they are going to get stubborn too.

Cricket is truly a ridiculous sport. Think about the predicament Pakistan found itself in recently. More than a year ago, they bid for rights to host the Champions Trophy. The tournament is owned by the International Cricket Council (ICC), which awards hosting rights to a particular country. That country then receives a hosting fee for their services, which is usually a hefty sum.

In fact, according to informed sources, Pakistan was set to pocket a neat $15 million for this. And even though all other member boards have agreed to travel to Pakistan, India has played spoil sport and refused to visit Pakistan. There has long been a criticism of the ICC that it is less a governing body and more an events organiser. But in this case it seems they aren’t even in control of their own events, with the BCCI making its own rules on the fly.

The new agreement that has emerged between the PCB and the BCCI is some strange, hybrid, garbled mixture. The Indian team will play all of their games in Dubai instead of in Pakistan, and in exchange, Pakistan will do the same when India hosts the 2026 T20 World Cup. Ok but what happens if both India and Pakistan reach the final? Will Jasprit Bumrah throw the ball from Sharjah and Babar Azam face it in Karachi? Or will the game be played with a book over Zoom? The ICC seems uninterested in answering these questions, mostly because they know in the end India will get its way.

For now, Pakistan has gotten a moral victory by refusing to go to India if they don’t come to Pakistan. This will last until 2027, when the ICC’s current me-

dia broadcasting deal expires. The question is, when the next broadcasting deal comes in, will broadcasters have complaints about the “tum katti kar rahay ho toh mai bhi kar raha hoon” nature of Indo-Paki cricketing relations.

Remember, from a broadcasting point of view, India Vs Pakistan is the biggest ticket item in all of cricket. Already the PCB is losing out on a major chunk of revenue by splitting hosting rights. They also don’t know if they will host the final of the tournament or not.

It really is a question of money. The ICC is hungry for the money that India generates. The reason India has such a disproportionate amount of sway in the ICC is because they have the single biggest market in the world when it comes to cricket. With a population of nearly 1.5 billion people and cricket played across the entire country, just the broadcast revenue from India is huge. It is this colossal number of eyeballs that India uses to also run tournaments such as the Indian Premier League (IPL), which has broadcasting rights worth $1.5 billion a year. The ICC knows matches involving India will have the most eyeballs, which is also when advertisers will advertise the most. As a result, India gets preferential treatment. Simple enough. The ICC is greedy. India has money. Pakistan would love to get in on it also, but the BCCI could not care less. As a consequence, Pakistan has to put up a brave face. To be fair, they have done well. The PCB is financially independent, and is probably the only board resisting the BCCI’s ridiculous actions. In this situation, we should take the small wins and run with them.

As of now, a piecemeal approach is being adopted with the approval of a new plan for IPPs

The Cabinet’s approval of settlement agreements with eight Independent Power Producers (IPPs) has opened the door to lower electricity tariffs. Why? Because the old pay-for-capacity-and-fuel model is being swapped out for a more sensible produce-and-pay setup.

Translation: IPPs will now only be paid for the electricity they actually generate, not for sitting around looking capable. This approval means the Central Power Purchasing Authority (CPPA) can now politely nudge the National Electricity Power Regulatory Authority (NEPRA) to tweak the tariffs accordingly. No grand, triumphant tariff reduction announcement here—just a piecemeal, let’s-see-how-this-goes approach. Once the National Task Force, an ad-hoc squad assembled by the Energy Minister, wraps up its review, we can expect a few more tweaks to follow.

But wait, there’s more. The Task Force didn’t just find ways to save money—it also uncovered a treasure trove of past corruption. Think over-invoicing, over-pricing, and other shady practices in the IPP setup. This juicy scandal has made it possible to renegotiate agreements, which likely came with a side of immunity for the IPPs and their partners-incrime over at the Energy Ministry. Nice deal, huh? Meanwhile, the Task Force is now sniffing around

the thermal plants WAPDA set up, and let’s be honest—chances are, they’ll find more skeletons in those closets. The real question: Will the government be as lenient with its own folks as it has been with the IPPs?

While accountability hangs in the balance, there’s also the issue of credibility. These revisions don’t exactly scream “trustworthy.” One way to save face? Make sure the country never stumbles into the dreaded loadshedding abyss again. That means riding the solarization wave, not just paddling behind it.

Speaking of solarization, WAPDA has some soul-searching to do. Its old-school centralized generation model is fast becoming a relic. Sure, dispatch and transmission are still on the table, but in a solarized world, they’ll look very different. WAPDA needs to figure out how to make consumers pay for sending their surplus electricity to the grid and pulling some back when their solar panels take the night off. And let’s not forget the rapid advancements making oilfired generation look like the rotary phones of the power sector. Ever heard of price-ambient electricity? Night-time solar generation? Fusion reactors? Are these science fiction—or the science fact of tomorrow? Recent developments suggest it might just be the latter.

Encouraging EVs is well and good, but there are other barriers to entry

The government has ordered all petrol pumps in Islamabad to install charging stations for electric vehicles. This move theoretically makes owning an EV in Islamabad less of a pipe dream. But will this actually work, or is it more of an attempt to appear woke and have something nice to put up in government presentations about the ‘potential’ of a ‘green revolution’ in Pakistan when donors come knocking.

EV manufacturers are still complaining about low demand, and the cars are less affordable for the average person. On top of this, EVs come with a whole host of problems even if electric vehicles were a viable and affordable option in Pakistan already. While charging stations might help, they can’t magically solve one glaring issue: charging time. Unlike the quick splash-and-dash of a petrol fill-up, EVs require drivers to park and wait. If EVs become even moderately popular, we could see long lines of impatient drivers tapping their fingers while their cars slowly sip electrons.

Then there’s the fact that Islamabad isn’t exactly an EV-friendly playground. It’s a city of commuters, most of whom need a single-charge round-trip range that can’t yet stretch to, say, Lahore, or at least whatever village the average Islamabadi goes back to for Eid.

Of course charging stations, as it turns out, aren’t strictly necessary. You can always plug your EV into a domestic socket and let it juice up overnight while you sleep. Sounds convenient—until you try selling your car. Here’s the catch: EV batteries don’t last forever, and replacing one is so expensive that you might as well buy a new car. That’s why early Teslas, now facing battery expiration dates, are slowly turning into glorified paperweights.

And what about those promised savings in foreign exchange? Don’t hold your breath. We still have to import fuel to generate the electricity needed to power all these charging stations. Plus, can the already stretched power distribution system even handle the extra load?

It’s worth noting that the government initially thought EV charging would help soak up Independent Power Producers’ (IPPs) surplus capacity. But now that IPPs are shifting to a take-and-pay model, the capacity charge headache seems to be fading into the background.

Still, a transport revolution is undeniably on the horizon, and the government deserves credit for at least pretending to be ahead of the curve. Whether these steps lead to progress or just a lot of awkward EV queue selfies remains to be seen. But hey, progress starts somewhere, right?

Jazz’s tower divestment strategy has found a potential savior

By Hamza Aurangzeb

In the 21st century, telecommunications infrastructure has emerged as the fundamental backbone of digitally advanced economies, serving as a critical conduit for connectivity that drives industrial functionality and national economic progress. Over the past two decades, this infrastructure has been a pivotal catalyst for economic growth, yet in recent years, the telecom sector has encountered a complex array of challenges that have significantly tested its resilience and potential for expansion. The industry’s evolution has been marked by strategic transformations prompted by escalating market pressures. While some operators responded with extreme measures— such as Telenor’s market exit—others adopted more nuanced approaches like divesting noncore assets to enhance operational efficiency. Jazz exemplifies the latter strategy, pursuing multiple tower sale agreements to streamline its operations. Its recent deal with Engro Connect represents its third attempt at infrastructure divestment, following unsuccessful negotiations with Edotco and the TPL-TASC consortium.

Profit aims to unravel the strategic motivations behind Jazz’s persistent efforts to shed its passive infrastructure, exploring the underlying rationale for selling Deodar and its tower portfolio, and illuminating the broader implications for Pakistan’s telecommunications landscape.

The telecommunications industry in Pakistan is characterized by multiple network operators that have been engaged in a gruelling battle to dominate the market for an elongated term, which resulted in diminishing ARPU and declining margins for all the telcos involved. Furthermore, the Pakistani’ Rupee’s depreciation exacerbated the situation as it undermined the significance of the numbers even further in USD.

The launch of the mobile broadband internet in Pakistan served as a pivotal juncture that changed the rules of the game of the telecom industry. Until this point, phone calls and messaging services were the main modes of communication, which also happened to

be the primary sources of revenue for telcos. However, as telcos embarked on the journey of affordable data packages, customers swarmed towards digital platforms like WhatsApp that allowed them to call and message for free. Thus, cannibalizing their major sources of revenue.

When the telecom operators entered the Pakistani market in the mid-2000s, they were generating an ARPU of $9, but as things stand now, it has dropped below a dollar. In parallel, costs for these telcos have been on the rise. For instance, costs for maintaining and operating towers have been increasing at an unprecedented rate due to the soaring prices of electricity and diesel, which means operating towers have become unviable for telcos.

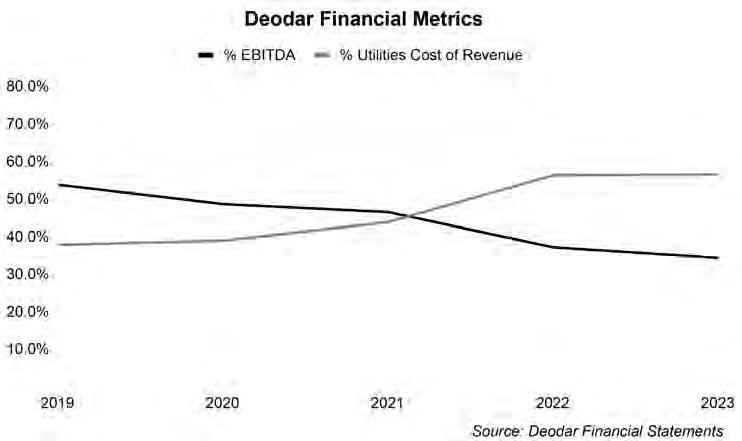

Deodar’s standalone financials make the escalation in utility costs (actually, energy costs) even more glaring, as it has become equivalent to 56.5% in 2023, whereas, it stood at 43.8% just a couple of years ago. The average energy cost for one Deodar tower (Jazz’s tower subsidiary) stands at Rs 230,000 per month. Hence, its EBITDA margin has plunged to 34.4%, which is nothing similar to its five-year average of 44.1%.

The rising energy costs, diminish-

ing profit margins and lack of expertise in managing infrastructure have compelled Jazz to conform to an asset-light business model, which is one of the three main pillars of its value-creation strategy that was developed by its parent company Veon in 2021.

Following the asset-light business model will enable Jazz to optimize its asset base and free up a significant portion of its capital fixed in its tower infrastructure. Additionally, it will allow the company to rationalize its operating costs, creating a conducive environment for its second and third pillars, which are focusing solely on achieving sustainable growth in core business with digital operator strategy and exploring digital products in spheres like financial services, entertainment, education, and healthcare.

Veon has been following this asset-light business model across all its markets. In November 2023, its wholly owned subsidiary in Bangladesh, Bangalink signed an agreement with Summit Towers to sell 2,012 of its towers, about one-third of its portfolio for a sum of BDT 11 billion ($100 million). The deal was finalized to enhance the efficiency of infrastructure utilization and expedite the transition towards the digital operator model.

Hence, following the strategy of its parent company, Jazz is determined to go asset-light. It formed a new subsidiary, Deodar, in August 2016, where the ownership of all of its towers was transferred to the subsidiary. The primary purpose of creating this subsidiary was to restructure the company and streamline operations, nurturing a favorable environment for the sale of Deodar and its towers in a seamless manner.

However, its deal with Engro Connect is not the first one as it has attempted to sell its towers multiple times before.

In November 2017, Jazz finalized the first agreement to sell its subsidiary, Deodar, and its portfolio of towers to Edotco, a telecom infrastructure services firm based out of Malaysia for a substantial amount of $940 million after the issue of a No-Objection Certificate from the Competition Commission of Pakistan. Edotco announced the acquisition of the towers through its subsidiary, Tanzanite, in partnership with Dawood Hercules Corporation Ltd (DH Corp), where it intended to invest up to Rs. 17.453 billion (165.7 million) in the company for an equity stake of 45%, while the remaining rested with Edotco.

The Malaysian firm raised capital for the transaction with a 50:50 debt-equity ratio, where debt was raised through domestic channels, while it arranged equity from offshore sources. However, the deal was called off due

to extended delays in regulatory approvals from various stakeholders including the Pakistan Telecommunications Authority (PTA), the State Bank of Pakistan, and the Federal Board of Revenue (FBR).

The deal was in limbo for a year, when, it was supposed to be completed by July 2018, however, its deadline was extended to September 2018, but to no avail as the industry was not granted any approvals for seven months due to the absence of a chairman of PTA. Moreover, the SBP placed restrictions on the outflow of foreign exchange earned from the deal and the FBR stamped exorbitant taxes amounting to a ludicrous figure of Rs. 22,033 million on the commercial transaction. However, Jazz later appealed the demand in the Islamabad High Court. Thus, all of these elements combined coerced the stakeholders to scrap the deal by September 2018.

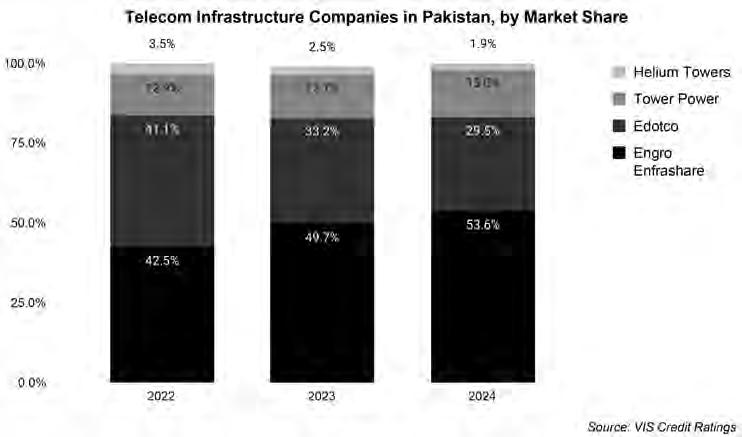

Afterwards, Jazz found a suitable buyer in the form of a consortium of Pakistani conglomerate TPL and UAE-based TASC Tower Holdings after four long years. In December 2022, Jazz announced that it had decided to sell Deodar and its 10,500 towers to the consortium for around $600 million, provided certain conditions were fulfilled.

The structure of the deal was established such that Jazz would transfer the ownership of Deodar Towers to a holding company Veon Pakistan Tower Holding B.V (VPHL) based out of the Netherlands, whereas the TPL-TASC consortium would create a Special Purpose Vehicle in Abu Dhabi and a feeder fund in Pakistan. Then, the SPV would invest in the domestic feeder fund along with other local investors to eventually purchase Deodar’s assets.