17 minute read

World Soda Ash conference review

World Soda Ash Conference focuses on renewable energy

� Hazel Kreuz (left), Vice President of Chemical Market Analytics, Ertugrul Kaloglu (middle), CEO of Sisecam Chemicals Resources, and Marguerite Morrin (right).

After being postponed due to the pandemic, the World Soda Ash conference took place last month at the Hilton Sorrento Palace Hotel in Italy.

The event was the largest World Soda Ash conference in 10 years with over 300 attendees and 20 speakers from approximately 35 countries and 200 companies.

Keynote speakers included glassmakers Sisecam, NSG and Ardagh, as well as soda ash industry expert Marguerite Morrin (Fig 1), Executive Director of Chemical Market Analytics by OPIS.

The last three years have proven eventful for the industry, with the price of soda ash skyrocketing due to a shortage of raw materials and increasing energy prices.

However, demand for glass, and consequently soda ash, remains strong. In her talk, Ms Morrin said 59% of world soda ash demand comes from the glass industry.

Unsurprisingly, many companies are looking at renewable energy sources to save costs and reduce emissions.

Overview of Soda Ash Market – Marguerite Morrin

Recent events have had a huge impact on the market. Ms Morrin said no-one could have predicted what was to come at the last World Soda Ash conference in 2019. A global pandemic, the Russia-Ukraine war, the risk of global recession and climate change have resulted in some of the highest soda ash prices on record.

She said: “Soda ash markets this year have been the tightest we’ve ever seen. We’ve seen some of the highest prices on record, even heard of spot prices $1000 per million tonnes - something unheard of for this industry.”

Europe was relying on Russian gas for 40% of its supply, which has resulted in record high natural gas prices and crude oil prices – but the consequences are still not fully known.

This has also increased the risk of global recession due to rampant inflation, interest rates rising sharply, and currency volatility. The Chinese economy is also slowing for the first time since the 1990s.

World capacity

Although Ms Morrin said some consequences were due to the Great Recession, which occurred from 2007 to 2009, post-2009 much soda ash capacity

The largest World Soda Ash conference in 10 years took place in Sorrento, Italy. As the energy crisis threatens the industry, the conference focused on decarbonisation and cost reduction through renewable fuels. Jess Mills was in attendance.

of approximately 1 million tonnes. In Central Europe capacity losses have been offset by other capacity gains, with a similar situation in the Commonwealth of Independent States (CIS).

In 2023, there will be 1.5 million tonnes less capacity in the United States (US) than predicted. In 2027, this will increase to 300 million tonnes.

However, there has been a 6 million tonne increase in capacity in the Middle East. Much of the increase has been in Turkey (mostly natural soda) with some capacity in Iran also. 1.1 million tonnes of capacity is planned for the coming years, including 800,000 tonnes in Turkey and a synthetic plant in Saudi Arabia. Meanwhile, India will remain a net importer of soda.

Elsewhere, China dominates with capacity expansions. In recent decades, China has added 30 million tonnes of capacity, mostly to meet its own domestic demand (Table 1).

The most ambitious Chinese expansion is an 8 million MT per year natural soda ash project in Inner Mongolia.

Overall, natural soda ash is taking a bigger share of the total world capacity. In 2017 it was 25%, which has increased by 3% this year. Based on what’s scheduled, this will increase to 38% by 2032.

Demand

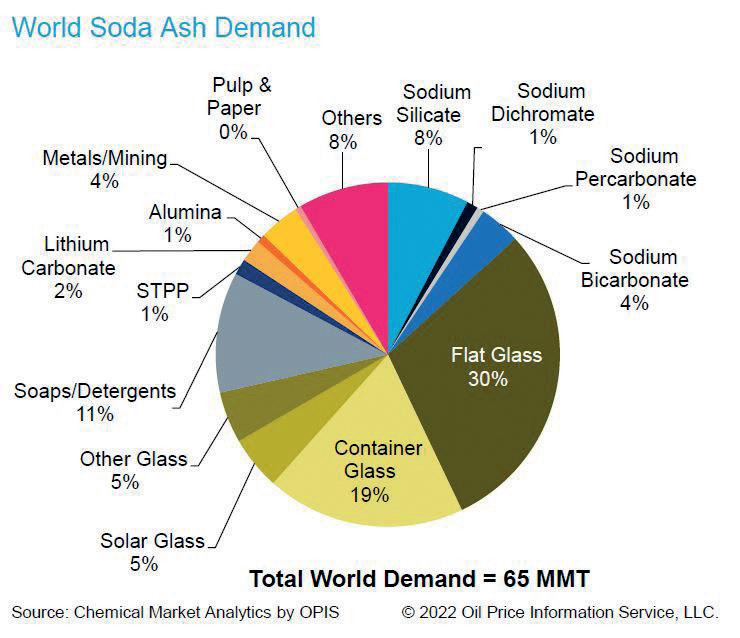

Ms Morrin said the total world soda ash demand is expected to be 65 million metric tonnes (MMT) this year, with the

glass industry dominating at 59%. (Fig 2)

While fl at glass has the single biggest end use at 30%, solar glass has become an important growing application at 5%. Meanwhile, container glass accounts for 19% of total world demand.

Flat glass has been a larger driver for demand growth, and will remain a driver in the forecast period as well. It will account for the second biggest volume of new demand by 2027 at an approximately 2.1 million net increase in terms of soda ash.

Ms Morrin said total world soda ash demand is projected to grow by 2.4% in 2023, and has grown by just over 2% this year.

In the world excluding China (ROW), 1.1 million tonnes of new demand is predicted per year until 2027. While China has 660,000 tonnes of growth predicted per year out to 2027.

Meanwhile Russia accounts for 4% of world demand per capita, but this is mostly self-contained in terms of supply/ demand dynamics.

Flat glass

Flat glass has remained important for all regions. It has grown about 4% per year in the historic time period, and will grow by approximately 2% growth in forecast period. There has been a net increase in demand of approximately 2 MMT, so it is still a very important demand driver.

China is by far the biggest fl at glass producer in the world. Flat glass has driven demand growth for soda ash in China, which has infl uenced world demand overall.

Construction (not including solar glass) is the main driver, with 1.7% growth even during the pandemic (from 2020). Construction spending is slowing

down next year, although the long-term potential is still positive.

Meanwhile, global automobile production accounts for less than 10%

� Fig 2. World soda ash demand.

� Fig 1. Marguerite Morrin, Executive Director of Chemical Market Analytics by OPIS.

closed around Europe.

In total, this was approximately over 2 million tonnes, including West Europe, Central Europe, and the Commonwealth of Independent States (CIS). The biggest net impact was in West Europe.

West Europe had a net loss of capacity Continued>>

� Fig 3. Demand growth container glass vs soda ash. � Fig 4. Soda ash operating rates.

� Fig 5. Ertugrul Kaloglu, CEO of Sisecam Chemicals Resources.

of world demand for soda ash, although it has seen a 3.8% growth post-pandemic.

Container glass

Container glass production has not grown as fast as fl at glass. The expected growth for container glass through the forecast years is a modest 1% per year, and a net increase in soda ash demand of about 600,000 tonnes. (Fig 3)

However, Ms Morrin said container glass had seen a ‘renaissance’ in recent years, with West Europe being the biggest producing region.

She said many believe container glass to be a better packaging material relative to plastics due to its environmentally friendly properties, such as its infi nite recyclability.

Europe has the highest recycling rates in the world at approximately 80%. There have also been recent movements to increase recycling in Australia, which has gone from 30% to between 50-60%.

However, in the US, production has shown a decline year on year and its recycling rate of 31% has hardly budged. Although some states have particularly high rates, such as Oregon at 73% and California at 67%. The US target is to reach an average recycling rate of 50% by 2030.

There is also an ongoing effort globally to use more recycled glass, which has lowered the consumption level for soda ash. For example, a 10% cullet increase will reduce CO2 emissions by 5% and energy consumption by 2.5%.

Ms Morrin estimated that if there was no recycling in West Europe, the region would consume an extra 1.5 million tonnes of Soda Ash.

She said: “We could say [recycling] is bad for soda ash, but it’s clearly good for container glass demand, because we see container glass as a packaging material still growing in Europe.”

She also believed soda ash production correlated with the regions responsible for the most CO2 emissions. China, the US, West and Central Europe, and India are responsible for approximately 85% of world soda ash production. In comparison, China, the US, India, and the EU account for 50% of global CO2emissions.

Solar Glass

Ms Morrin said solar energy was one of the fastest growing sources of renewable energy, if not the fastest. Photovoltaic (PV) installations grew last year and even during the pandemic, which resulted in a growth of 22%. This year, demand growth has surged to 44% year over year. Despite many companies signing up to the Paris Agreement, pledges to date still fall short of what’s needed to meet net zero. However, high energy prices have given an incentive to transition to renewable energies, as well as a new focus on energy security after the RussiaUkraine war.

Fossil fuels still account for 80% of the world’s energy, but solar energy is widely available.

Ms Morrin said estimates suggest that the amount of energy that shines on the Earth for an hour is more than enough to supply demand for all energy requirements for the world for a year.

However, to reach net zero, PV installations would have to grow at a rate of 25% per year to 2030. This would equate to soda ash requirement of 17 million tonnes.

� Fig 6.The location of Sisecam’s projects in Wyoming, US.

Raw materials

Table 1 - Soda Ash Investments

Company Project Capacity Location Estimated completion date

-

Natural soda ash project planned 8 MMT per year Sisecam with Ciner Group Pacifi c Soda 10 MMT per year Inner Mongolia, China Ongoing Wyoming, US 2025-2027

WE Soda Project West ~3 million mtpa of initial production capacity Green River in Wyoming, US By 2030

WE Soda Kazan Soda ~1 million mtpa Russia Ongoing

Solvay Solvay with Sisecam Solvay Dombalse plant Devnya plant Green River plant +60,000 tonnes +200,000 tonnes (sodium bicarbonate) +700,000 tonnes France Bulgaria Wyoming, US Ongoing Completed Rescheduled from 2019

in Europe. Coal and coke availability remains a problem, and anthracite is no longer available.

Russia was responsible for approximately 90% of anthracite. Since August 2022, the EU banned imports from Russia. This meant many plants switched to coke, leading coke prices to become

incredibly high and less available.

Ms Morrin said this has left natural gas-based plants exposed due to the high energy prices.

In West Europe, 46% of plants use natural gas for soda ash fuel production, while coal accounts for approximately 70% of world soda ash fuel sources.

Ms Morrin said that while some companies may be able to switch back to coal, in terms of CO2 emissions, more sustainable fuel sources should be used instead.

She continued that the 8 million MT Inner Mongolia plant could export soda ash to Europe cheaper than the European natural gas producers, and in-line with the US natural gas producers. Meanwhile, Turkey would remain competitive, and coal-based producers would remain competitive.

Although producers in China are less competitive Turkey and America, she said the new Inner Mongolia plant had the potential to be more competitive than any of them.

Summary

This year, the market had lower capacity in the world than last year, which resulted in net loss of approximately 600,000 tonnes of soda ash. This, combined with positive demand growth, caused world

operating rates of the highest on record, which is why the market fell so tight. (Fig 4)

Looking at forecast period, Ms Morrin thought that this year would peak for world operating rates.

In China, the Inner Mongolia project could ramp up quicker than expected. Also unconfi rmed capacity in China could come on stream, which would pull operating rates even further down.

Without Chinese capacity, operating rates will come down to almost to what they were prior to this year’s peak.

Overall, she believed it was unlikely that the market would return to normal in the short term.

However, she concluded that sustainability was the one certainty for the soda ash industry.

� Fig 7. John Sadlier, Chief Sustainability & Procurement Offi cer of Ardagh. � Fig 8. - Alasdair Warren, WE Soda CEO. � Fig 9. - Philippe Kehren, President of Solvay’s Soda Ash & Derivatives.

Sisecam

Ertugrul Kaloglu (Fig 5), CEO of Sisecam Chemicals Resources, spoke on Sisecam’s soda ash expansion project in the US and its sustainability targets.

Annually, Sisecam produces 5 million tons of soda ash and 5.6 million tons of glass. Of the soda ash produced, 55% goes to glass manufacturers.

Sisecam doubled its soda ash capacity after acquiring the rights to the Sisecam Wyoming business in 2021, which was

previously owned by Ciner Resources.

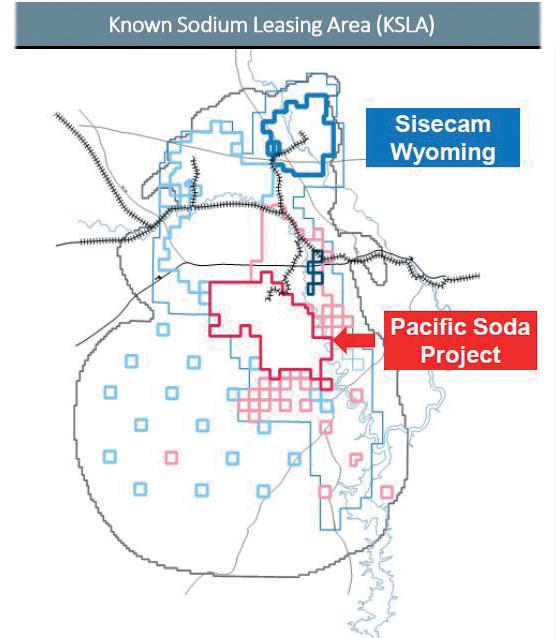

To further increase its capacity, Sisecam will make a $4+ billion natural soda ash investment (Pacifi c Soda) in the US together with Ciner Group (60% Sisecam and 40% Ciner off take agreement). (Fig 6)

With this starting investment, Sisecam will manage 10 MMT per year of global soda ash production.

Sisecam is expected to become the world leader in soda ash production with the additional soda ash capacity that will be produced by the Pacifi c Soda Ash Project.

The investment includes the establishment of the largest soda ash production facility in a single location. Consequently, Sisecam is expected to be the largest natural soda ash producer in the United States. By 2028, it plans to supply 7.8 million tonnes of soda ash to the global market.

Sisecam will manage ~40% of the global planned new capacities (including expansions) until 2026. Excluding China, it will operate ~70% of the global new natural soda ash capacities (including expansions) until 2026.

Of the company’s planned global capacity expansion until 2026, >80% is natural soda.

Production related to CO2 intensity in natural soda is ~70% lower in comparison to synthetic soda ash, while energy usage is ~60% and water usage is ~85% lower.

Ardagh Group

John Sadlier (Fig 7), Chief Sustainability & Procurement Officer of Ardagh, discussed the group’s plans to reduce its GHG emissions.

The Furnace of the Future Project was a consortium of 19 EU glass container manufacturers which was initiated by Ardagh with the help of FEVE, the European Container Glass Federation.

The project aimed to develop a fullsized container glass furnace that would run on 80% green electricity and 20% natural gas.

The furnace would reduce CO2 emissions by up to 50%, and allow for amber and green glass production – which would not be possible with a fullelectric furnace.

However, the project was unsuccessful in its grant application. Despite this setback, Ardagh plan to continue the project by finding a way to make it themselves or as a smaller consortium.

Mr Sadlier said another alternative was to use green hydrogen. He said the group was highly considering deploying a 5MW hydrogen electrolyser at one of its sites as a pilot project.

The electrolyser would use 100% renewable energy, which would generate 1,000 m3 of green hydrogen per hour.

This would reduce natural gas consumption by 20% in the furnace (This is the Limmared furnace news story we published last week) .

The aim would be to go live with the pilot project in 2023.

Mr Sadlier said Ardagh was initially focused on Europe for the project, but the recent Inflation Reduction Act of 2022 in the US offered a more attractive alternative.

The Inflation Reduction Act will make a down payment on deficit reduction to fight inflation, invest in domestic energy production and manufacturing, and reduce carbon emissions by 40% by 2030.

The act makes hydrogen a more competitive fuel in North America, and in states with low electricity cost, green electricity is more readily available.

Mr Sadlier said that Ardagh believes in hydrogen as a future fuel, and is looking to be part of future hydrogen pipeline projects.

He continued that the group’s next steps would be to replace the 20% natural gas used in the Furnace of the Future with hydrogen.

This would create a furnace with zero CO2 emissions from fossil fuels in the combustion process, and contribute to the Ardagh’s overall goal of reducing its Scope 1 and 2 GHG emissions by 42% by 2030.

WE Soda

WE (West East) Soda is the UK incorporated holding company for the global soda ash operations of Ciner. The company’s CEO, Alasdair Warren (Fig 8), revealed WE Soda’s latest greenfield project, Project West, at the conference.

Project West will be located near the Green River in Wyoming, US. It is in addition to the company’s participation in the Pacific Soda project with Sisecam, in which WE Soda has a 40% interest.

The project is expected to produce ~3 million mtpa of initial production capacity, and will then be scaled over time to meet growing global demand.

It is export focused, given the profile of demand around the world, and will export through new facilities that WE Soda are developing in California, US. The project will target the markets of Asia and Latin America in particular.

WE Soda plans to target production by 2030, which means Project West will target the ~3-4 million tonne gap in supply between 2028 and 2030.

The project will use solution extraction, which will target the largest deep trona beds. This is the same technology currently being used for the company’s plants in Turkey, and which will be deployed for the Pacific project.

For the first time, WE Soda believes it has the technical capability to develop a project which utilises up to 100% renewable energy.

Mr Warren said Wyoming had characteristics that would allow WE Soda to create solar and wind power generation, as well as solar steam.

Together with existing projects, We Soda will invest ~$4 billion and add over 6 million mtpa capacity by 2030.

Solvay

Philippe Kehren (Fig 9), President of Solvay’s Soda Ash & Derivatives, outlined Solvay’s projects to increase soda ash capacity and achieve carbon neutrality.

Mr Kehren highlighted the need to transition out of coal and gas to achieve decarbonisation, suggesting that trona based production units could increase capacity sustainably.

Trona-based soda ash is less CO2 intensive, due to it being a mix of solution and mechanical mining.

However, there are only three reserves in Wyoming, Inner Mongolia and Turkey - all of which would have to be exported. Based on this, Solvay predicted that tronabased soda ash would grow up to 38% by 2030.

Overall, Mr Kehren believed exploiting trona would not be enough to meet global demand.

Therefore, Solvay will pilot a new soda ash manufacturing process at its plant in Dombasle, France which will cut its CO2 emissions by 50%.

The technology, based on electrochemistry, has been in development for the last 30 years. It will preserve natural resources by using 20% less water and salt, 30% less limestone consumption and eliminate limestone residues.

Once validated, the process will be implemented across all Solvay sites, including Spain, Bulgaria, Italy, France and Germany.

Further environmental initiatives include Solvay’s plan to use biomass boilers at its Rheinberg plant in Germany. The boilers will use discarded woodchips to produce steam and electricity, which will replace coal.

This will make Rheinberg the first soda ash plant in the world to be powered primarily by renewable energy. Solvay plans to use 100% of renewable energy at the site by 2025. This will reduce the plant’s emissions from 1 to 0.3 tonnes of CO2 per tonne of soda ash.

Also in Dombasle, Solvay will use a locally sourced, non-recyclable waste to fire up RDF (Refused Derived Fuel) boilers. This means it can cut its imported fossil fuels and create a new outlet for local waste (400 tonnes) currently going into landfill. �