6 minute read

Market snapshot Market

Oleochemicals are chemical compounds derived from natural fats and oils which can be used to substitute petroleum feedstocks when producing a wide range of everyday products.

They have a significant breadth of applications and are used in the production of coatings and resins; food and animal feed; personal care and cosmetics; soaps and detergents; rubber and plastics; lubricants; waxes; textile softeners; mining and oilfield chemicals; and pharmaceuticals.

The oleochemicals sector is split into the fatty acid and fatty alcohol markets, with key vegetable oil feedstocks being lauric oils – palm kernel oil (PKO) and coconut oil.

While fatty acids can only be produced from vegetable oils or animal fats, fatty alcohols can also be produced from petrochemical feedstocks, with competition between natural and synthetic alcohols a factor in this market.

Growth forecast

The oleochemicals market is expected to grow by around 3.5% in volume from 23.5-24.5M tonnes this year to 27.29M tonnes in 2028. Value growth could be higher (5.4% CAGR in revenue), from US$24-26bn this year to US$31-33bn in 2028, due to potential higher pricing.

The biggest revenue gain by sector will occur in personal care and cosmetics, which will grow from 30% in 2022 to 33% in 2028 (see Figure 1, p35), while the most R&D and innovation will be seen in green detergent products and lubricants.

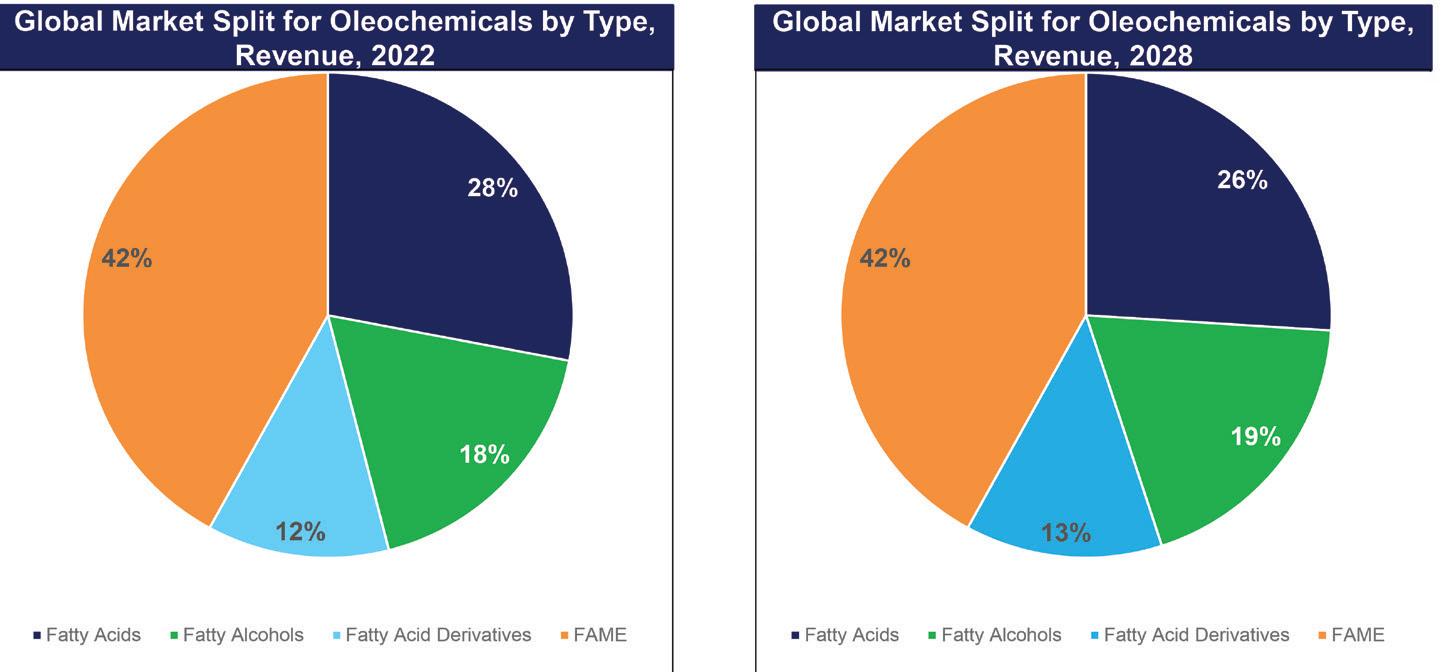

The market split for oleochemicals by type – fatty acids, fatty alcohols, fatty acid derivatives and fatty acid methyl ester (FAME) – will remain stable between 2022 and 2028 (see Figure 2, p35), with fatty acid derivatives being a key area of growth. Fatty acid derivatives will see a

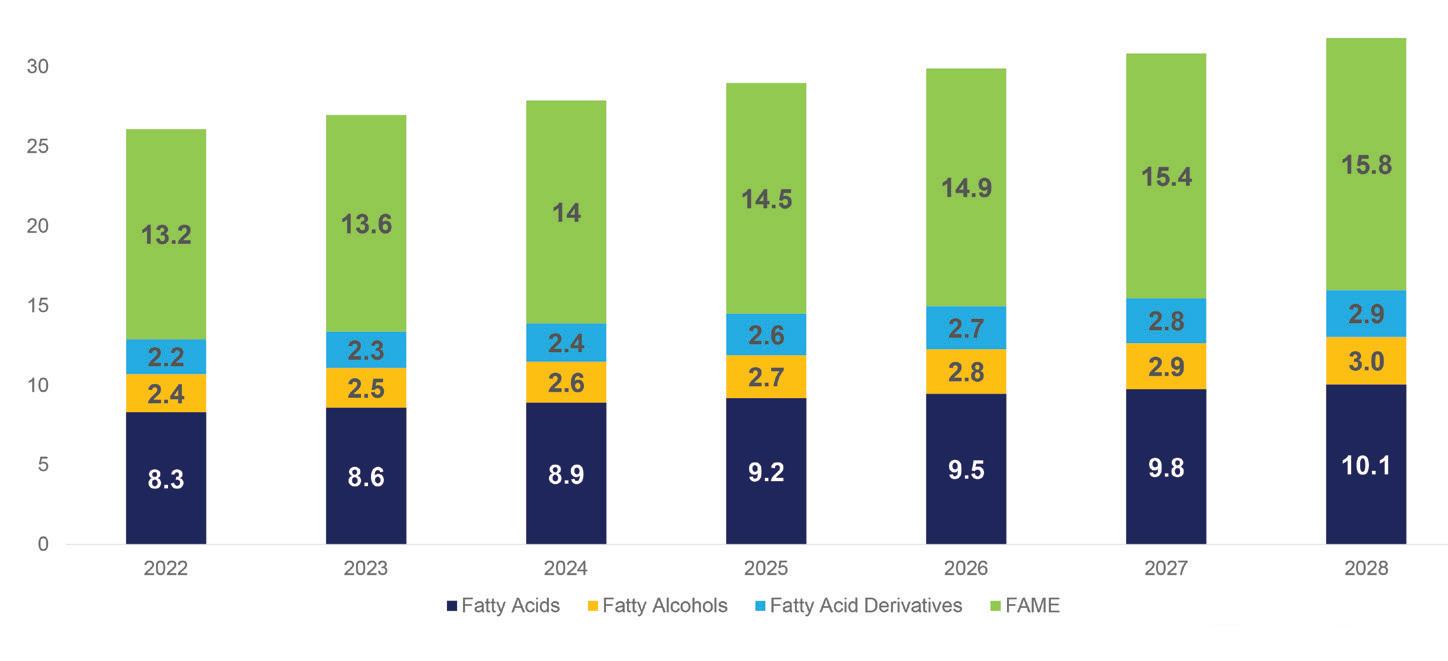

CAGR growth of 4.3% by volume from 2025 onwards (see Figure 3, p35).

The Asia Pacific region, which leads the oleochemicals market by regional share, will also lead growth in the next decade. Several industries that require oleochemicals, such as soaps, have moved to countries in Asia Pacific due to better economics and logistics. Additionally, the availability of raw materials, such as palm and oil, has helped development.

Europe is moving towards maturity and its oleochemicals demand is growing at a slower pace compared with Asia Pacific, although the region continues to be a strong consumer of FAME for biodiesel. In the Americas, demand growth is also lower although the region will see expanding economies, industrialisation and urbanisation in Latin American countries, mainly Mexico and Brazil.

Sector applications

Key end-user sectors of oleochemicals include personal care and comestics; soaps and detergents; food and feed; rubber and plastics; and waxes. Across all these industries, fatty acids and derivatives will play a key role.

Personal care & cosmetics: The European and North American soap industry has been a big consumer of tallow- and vegetable-based fatty acids but Asia Pacific is now the current leader. Growth products include caprylic acid (C8), lauric acid (C12), myristic acid (C14), palmitic acid (C16), stearic acid (C18:0) and oleic acid (C18:1).

Soaps & detergents: Growth products in this sector include capric acid, caprylic acid, palmitic acid, stearic acid and oleic acid for speciality and metallic soaps.

Food & feed: Short-chain fatty acids, such as caprylic acid, are mainly used to produce medium chain triglycerides, with growth products including lauric acid (C12) and myristic acid (C14).

Rubber & plastics: Fatty acids improve the viscosity of rubber by reducing stickiness and improving the curing process during vulcanisation. A growth product in this sector is caprylic acid.

Growth sectors

All end-use sectors in the oleochemicals market have seen strong post-pandemic growth following COVID-19 lockdowns and disruptions.

Personal care is the largest consumer of oleochemicals globally, including short chain fatty acids (such as caprylic acid) and medium/long chain fatty acids to produce toilet soaps and shampoos.

In the soaps and detergents sector, strong post-pandemic growth continues to be observed, with fatty alcohols showing the most consistent growth.

The green consumer trend has gained further momentum in emerging countries such as China and India with non-ionic surfactant fatty alcohol ethoxylates (FAE) – derived from vegetable oil –experiencing high growth.

In North America, green surfactants now account for about 50% of the surfactant markets, with detergent alcohols and long-chain dicarboxylic acids (LCDAs) as key applications.

In Europe, REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations limit the emission of volatile organic compounds (VOC) into the environment. The regulation came into force in June 2007 and is designed to improve the protection of human health and the environment from the risks that can be posed by chemicals. Oleochemicals can facilitate the development of low VOC, emissionfree and solvent-free products.

Value chain and outlook

Crude palm oil and PKO oil are major feedstocks for the oleochemicals industry.

In the upstream process, investments in new plantations and expansion have become increasingly difficult and the emphasis is on yield improvement through technology. Mid-stream, producers of basic oleochemicals will see stable growth. Downstream, investment in value addition within the fatty acids and fatty alcohols sectors, especially in derivatives, will result from stronger growth in personal care and cosmetics, leading to higher future margins (see Figure 4, below, right).

Future challenges

The oleochemicals sector is always subject to fluctuating feedstock prices, with supply of palm, palm kernel and other oils dependant on weather and geopolitics. As well as general price volatility related to feedstock supply, specific issues are also expected to impact the market:

EU anti-dumping duties: In January, the European Commission (EC) imposed anti-dumping duties ranging from 15.2% to 46.4% on fatty acids imported from Indonesia, following a complaint lodged in 2021 by EU oleochemical producers. The EC said the duties were imposed because the EU industry was being harmed by dumped imports as it could not compete on price and was losing market share as a result. The new duties are set to be supportive for the EU oleochemical industry.

Petrochemical competition: North America has historically been a big market for synthetic alcohols and large shalebased ethylene investments and resulting derivatives could impact the growth of oleochemicals.

B35 in Indonesia: On 1 February, Indonesia increased its blending of palm oil in diesel fuel to 35% (B35) from B30. As the world’s largest producer and exporter of palm oil, Indonesia’s B35 rule is expected to lead to a drop in its exports, by some 20% from 2022, affecting oleochemical feedstock supply and leading to increased fluctuations in the global pricing of palm oil. ● This article is based on a presentation made by Nikhil Vallabhan, director of Asia Pacific at global consultancy service Frost & Sullivan, at the Palm & Lauric Oils Price Outlook Conference (POC2023) in March

Source: Frost & Sullivan, POC 2023

Source: Frost & Sullivan, POC 2023

Source: Frost & Sullivan, POC 2023

Source: Frost & Sullivan, POC 2023

Prices of selected oils (US$/tonne)

Soyabean

Crude palm

Palm olein

Coconut

Rapeseed

Sunflower

Palm kernel

Average

Index

Statistical News

Palm oil

The price for Crude Palm Oil (CPO) CIF Rotterdam was assessed at US$931.60/tonne on 24 May, declining US$25.70 week-on-week. This downward trend can be attributed to increasing production estimates for Malaysia, which indicate a potential increase of approximately 17% from 1-20 May, as calculated by Mintec. Furthermore, demand for palm oil has been sluggish, with exports from Malaysia over the 1-20 May period showing a marginal increase of 1-2%, according to market players. Trades have been reported with prices CNF (cost and freight) to India at US$880/tonne and US$875/tonne, respectively.

A trader expressed to Mintec that “the current focus lies in the uncertainty surrounding demand, given the increasing supplies in the market. Market participants are adopting a ‘wait-and-see’ approach, observing if there will be further price declines before engaging in substantial purchases, apart from occasional transactions. The lack of active demand is unsettling sellers, some of whom are looking to sell at cheaper levels, which is causing a downward price spiral as everyone else lowers prices to compete.”

Soyabean oil

The bearish sentiment in the soyabean market remains, with US crop planting progress reaching 66% in the week ending 21 May, 17 percentage points (pp) higher than the previous week and 14 pp higher than the 20182022 average. Albeit lower by 13 pp compared to the five-year average, planting in North Dakota – which was of concern to market participants due to the slow planting pace – has improved, with plantings reaching 20% as of 25 May. Conversely, plantings in Illinois – historically, the top US soyabean producer, reached 85% (+27 pp compared to the 2018-2022 average).

The positive outlook for this season’s crop supply has continued to pressure futures prices. Consequently, the CBOT soyabean and soyabean oil futures price (July 2023) on 23 May settled at US1,322.4c/60 lbs bushel, and US47.76c/lb respectively, 1.4% and 2.1% lower than the previous day’s settlements after climbing on technical buying. The US Department of Agriculture’s weekly export sales report released on 18 May showed a 70.4% year-on-year (y-o-y) decline in soyabean exports and a 44.0% y-o-y fall in soyabean oil exports in the week ending 11 May, compared to the same period the previous year, with a significant decrease in weekly soyabean exports to China (–5123% y-o-y).

Mintec provides independent insight and data to help companies make informed commercial decisions.

Tel: +44 (0)1628 851313

E-mail: sales@mintecglobal.com

Website: www.mintecglobal.com