WINTER 2023 Buyer Beware — The Foreign Investment in Real Property Tax Act

REAL PROPERTY

3 Buyer Beware — The Foreign Investment in Real Property Tax Act

By: Eric D. Oberer, and Gil O. Acevedo

7 2022 Developments in Real Estate Finance

By: Brook Boyd

14 New York Court Holds a Pledge Agreement Does Not “Clog” a Borrower’s Equity of Redemption

By: Jose A. Fernandez

17 Destroying Charitable Conservation Easements Is Not Within Congressional Intent

By: Nancy Ortmeyer Kuhn

20 New Proposed Regulations Would Affect the Taxation of US Real Estate for Foreign Investors

By: Nickolas Gianou, Victor Hollender, David Polster and Sarah Beth Rizzo

TRUST AND ESTATE

23 Why GST Tax is Relevant for Non-US Trusts

By: Jennie Cherry and Lindsey Bronstein

26 Planning for the Massachusetts Millionaire Tax— Individuals and Trusts

Editor

Robert Steele (TE)

Articles Editor for Real Property

Cheryl Kelly (RP)

Assistant Real Property Editors

Articles Editor for Trust and Estate

Ray Prather (TE)

Assistant Trust and Estate Editors

By: Ropes & Gray LLP

29 Form 3520-A, Foreign Trust Return with US Owner

Explained

By: Sean M. Golding

33 Taxation of US Beneficiary Foreign Trust Income: an Overview

By: Sean M. Golding

John Trott (RP)

Katie Williams (RP)

Sarah Cline (RP)

Technology/Practice Editor for Trust and Estate

Martin Shenkman (TE)

The materials contained herein represent the opinions of the authors and editors and should not be construed to be those of either the American Bar Association or the Section of Real Property, Trust and Estate Law unless adopted pursuant to the bylaws of the Association. Nothing contained herein is to be considered the rendering of legal or ethical advice for specific cases, and readers are responsible for obtaining such advice from their own legal counsel. These materials and any forms and agreements herein are intended for educational and informational purposes only.

© 2023 American Bar Association. All rights reserved.

Keri Brown (TE) Brandon Ross (TE) WINTER

WINTER 2023

2023 2 eReport

Buyer Beware — The Foreign Investment in Real Property Tax Act

By: Eric D. Oberer, Esq. (CLTP), and Gil O. Acevedo, Esq.1

Liability for tax withholdings on real property sales rest with buyers under the Foreign Investment in Real Property Tax Act — and it’s not always immediately clear when the Act applies. Buyers beware!

Synopsis

The Foreign Investment in Real Property Tax Act (27 U.S.C. §1445) (“FIRPTA”) requires and obligates a buyer who purchases real property in the United States (U.S.) from a foreign seller to withhold from seller’s proceeds and submit to the Internal

Revenue Service (IRS.) 15% (or 10% for qualifying transactions) of the sales price of the U.S. real property.

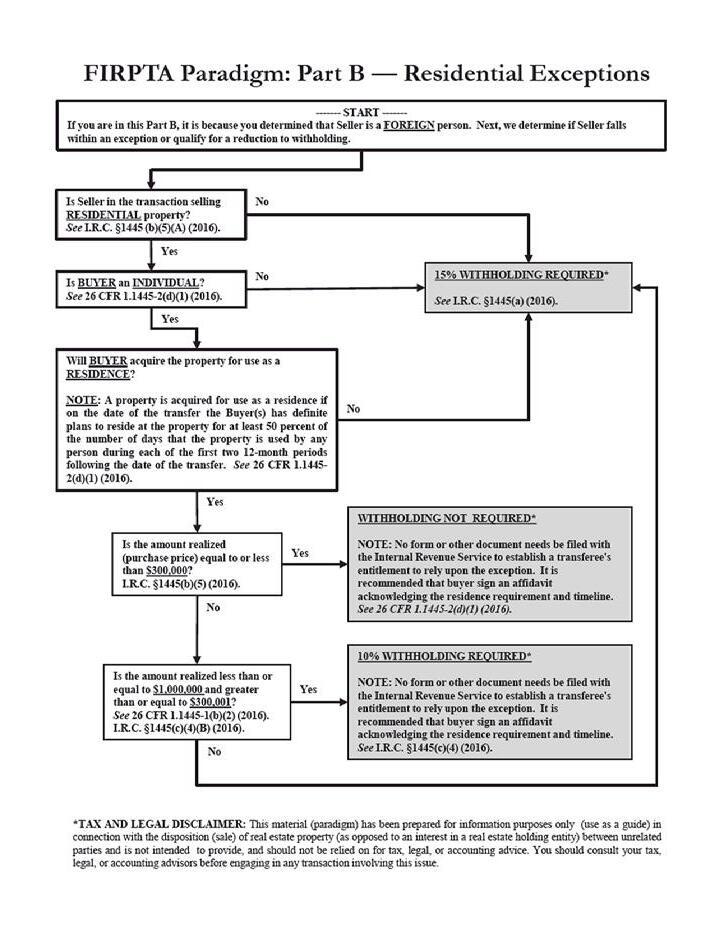

A foreign seller is an entity not organized in the U.S., or an individual person not born in the U.S., not admitted in the U.S. for permanent residence (e.g., issued a Green Card) or who has not met the IRS’s “substantial presence test” for the calendar year in which the property is sold. Determination of the foreign status of a given seller can be complicated, particularly when the seller is an entity. This is when the flow chart incorporated herein below can be useful.

Legal liability for compliance with FIRPTA and its withholding requirements rests with the buyer, because a foreign seller will often flee and be out of the U.S. government’s arm’s reach for recouping the withholding amount. A buyer’s and the settlement and/or closing agent’s liability under FIRPTA can be avoided by their reasonable reliance on a domestic seller’s certification or affidavit of non-foreign status. Where the seller is a foreign person, liability is avoided through compliance with the withholding requirements or meeting an exception to the withholding

WINTER 2023 3 eReport REAL PROPERTY

requirements (e.g., a sale for $300,000 or less, where an individual buyer will acquire the property and use it as his/her principal residence).

FIRPTA Generally

• Real estate dispositions by a foreign person are subject to income tax withholdings.

• Buyers must determine and confirm whether the seller is a foreign person.

• Buyer’s failure to withhold creates tax liability to the IRS for noncompliance with FIRPTA and its withholding requirements.

• FIRPTA applies to residential and commercial transactions.

• The main analysis under FIRPTA is to determine whether the seller is a foreigner, and, if so, whether the foreign seller falls within an exception, or qualifies for a reduction, to the required tax withholding.

Foreign Person

• A “foreign person” is an individual not born in the U.S. or nonresident alien.

• It does not include a resident alien individual, which is an individual:

m admitted in the U.S. for permanent residence (e.g., issued a Green Card); or

m who meets the “substantial presence test.”

Substantial Presence Test

The IRS’s “substantial presence test” is a complex formula. To meet the test, the seller has to be physically present in the U.S. on for at least 183 days during the current year and two preceding years, with a minimum of 31 days in the current year. The days of physical presence are counted as follows: (a) each day of presence in the current year is counted as one full day, (b) each day of presence within the year before the current year is counted as one-third of a day, and (c) each day of presence two years before the current year is counted as one-sixth of a day.

• Pro tip: Retain the services of an attorney or accounting/tax specialist to make this determination.

Liability

The buyer is responsible and required to deduct and withhold the tax, and, thus, liable to the IRS for buyer’s failure to do so. Liability can also rest with the settlement/closing agent if such agent accepts the seller’s certification of non-foreign status, where the agent knew or reasonably should have known it was false.

• Pro tip: Circulate an affidavit in which all parties swear, under oath and penalties of perjury, that they reasonably believe seller is not subject to FIRPTA.

Amount to Withhold

If the seller is indeed foreign, or if the status of seller cannot determine with certainty, then the buyer must withhold the required (or reduced) amount and submit such amount to the IRS using the correct form.

Exceptions

• Personal Residence: The property involved is residential property, the buyer is an individual and acquiring the property for use as residence, and the sales price is equal to $300,000 or less.

• Reduced Rate of Withholding: The property involved is residential property, the buyer is an individual and acquiring the property for use as residence, but instead, the sales price is greater than $300,000 but less than or equal to $1,000,000. This exception allows the buyer to reduce the withholding from 15% to 10%. (This exception arose from the Protecting America from Tax Hikes (PATH) Act of 2015.)

• Seller Certification: The seller delivers a certification (or affidavit) stating that seller is not a foreign person under the laws of the U.S. The certification must include the seller’s name, taxpayer identifying number (social security number), physical home address and a statement, under penalties of perjury, as to its truth and correctness.

• IRS Withholding Certificate: The buyer may request a withholding certificate from the IRS prior to sale of the property under certain circumstances using the applicable form, where the IRS makes the determination whether withholding is reduced or not required.

Reporting and Paying the Tax

• The buyer must use Forms 8288 and 8288-A to report and pay the tax required to be withheld.

• Forms and funds must be received by the IRS within twenty days after the date of the transfer of the property.

• The buyer’s and foreign seller’s tax identification numbers are required. If foreign seller (individual) and does not have a tax identification number but is eligible, such seller can apply for one.

Caution: It’s Not Always Immediately Clear If FIRPTA Applies

It is not always immediately clear whether the seller is foreign, that is, whether FIRPTA applies. The property may have multiple owners, where one of those owners is foreigner. Under

WINTER 2023 4 eReport

these circumstances, the withholding is prorated according to the foreigner’s ownership interest in the property. In a different scenario, the seller may be a single-member limited liability company, where the single member is an individual U.S. citizen, but the entity was organized outside the U.S. Under these circumstances, FIRPTA would apply.

The message is that due diligence is required to determine whether or not FIRPTA applies, as it may not always an easy task. Hiring a professional in this area is advisable. The Paradigms below can serve as tool in determining the applicability of a FIRPTA withholding. Part A aids in analyzing the seller’s status and Part B in analyzing which exception, if any, apply.

[Link to Florida Bar Journal Article: https://www.floridabar.org/ the-florida-bar-journal/to-withhold-or-not-to-withhold-that-isthe-question-a-step-by-step-approach-to-the-firpta-income-taxwithholding/ ]

Endnotes

1. Eric D. Oberer is Senior Underwriting Counsel at First American Title Insurance Company’s Maryland and Washington, D.C. offices. Eric is able to provide IRS forms, transaction templates and copies of paradigms that can help navigate FIRPTA.

Gil O. Acevedo is Counsel at Hunton Andrews Kurth LLP in Miami, Florida. He represents clients in acquisition and disposition of retail property, hotels, office buildings, multi-family apartment buildings and residential luxury residences, as well as financing and leasing transactions.

WINTER 2023 5 eReport

WINTER 2023 6 eReport

2022 Developments in Real Estate Finance

By: Brook Boyd1

1.THE IMPACT OF TECHNOLOGY ON REAL ESTATE FINANCE

1.1 Current Status of eDocuments Authorized By E-SIGN Act, UETA & UCC

1.11.

E-SIGN Act

The federal Electronic Signatures in Global and National Commerce Act (“ E-SIGN Act ”), enacted in 2000,2 authorized a new type of electronic document, called a “transferable record.” Pursuant to the E-SIGN Act, a “transferable record” must meet the following conditions: (1) it must be an electronic equivalent to a “note” under Article 3 of the UCC, (2) the “issuer of the electronic record expressly has agreed [it] is a transferable record” pursuant to the E-SIGN Act,3 and (3) the transferable record must relate “to a loan secured by real property.”4

1.1.2. UETA

The Uniform Electronic Transactions Act (“ UETA”) contains similar rules regarding “transferable records.”5 UETA was introduced in 1999, and has been adopted by all states except New York.6

1.1.3. UCC

The 1999 version of the Uniform Commercial Code (“ UCC ”) defined “record” to include “information . . . which is stored in an electronic or other medium and is retrievable in perceivable form.”7 The 2010 amendments to the Uniform Commercial Code (“ UCC ”) (1) authorized electronic signatures,8 (2) enabled secured parties to have “control” of “electronic chattel paper” if a “system”9 was used to store the related electronic “records,” (3) protected buyers of intangible collateral who gave value and were unaware of claims by secured parties,10 and (4) authorized electronic notices of UCC sales.11

1.1.4. Control of e-Notes by Holder in Due Course

The E-SIGN Act provides that a person (including a lender) has “control” of an electronic note (“eNote”) if “a system employed for evidencing the transfer of interests in the [eNote] reliably establishes that person as the person to which the [eNote] was issued or transferred.”12 The person with “control” of such eNote is generally deemed to be the “holder” of it.13 Such person will also qualify as a “holder in due course” or “purchaser,” as applicable, if the relevant requirements are satisfied under

This piece provides an overview of recent developments in the real estate finance arena. Table of Contents 1. THE IMPACT OF TECHNOLOGY ON REAL ESTATE FINANCE............7 1.1. Current Status of eDocuments Authorized By E-SIGN Act, UETA & UCC................................................................................................................7 1.1.1. E-SIGN Act ...................................................................................................................7 1.1.2. UETA 7 1.1.3. UCC ...7 1.1.4. Control of e-Notes by Holder in Due Course.................................................7 1.1.5. Current Fannie Mae Rules for Its Purchases of eNotes and eMortgages..........................................................................................8 1.1.6. Recording of Paper Mortgages & Other Documents May Still Be Required.....................................................................8 1.2. Impact of Cryptocurrencies & Other Digital Assets on Finance.....................................................................................................8 1.2.1. Current Practices for Loans Secured by Digital Collateral........................................................................................................8 1.2.2. Proposed 2022 UCC Amendments for Cryptocurrencies & Other Digital Assets.............................................................................................8 1.2.3. Regulatory & Other Legal Issues Relating to Cryptocurrencies & Other Digital Assets........................................................9 2. BENEFITS FOR PROPERTY OWNERS UNDER THE INFLATION REDUCTION ACT OF 2022..............................................9 3. TAX CODE LIMITS ON BUSINESS INTEREST, AND EXCEPTIONS THERETO..........................................................................10 4. WHEN REAL ESTATE LENDERS SHOULD BE REITS.............................10 5. WHEN A LOAN WILL BE RECHARACTERIZED AS EQUITY FOR TAX PURPOSES....................................................................11 6. ENFORCEABILITY OF MAKE-WHOLE PREMIUMS IN BANKRUPTCY.....................................................................................................11 7. STRUCTURING OF BANKRUPTCY REMOTE ENTITIES........................11

WINTER 2023 7 eReport

the UCC, except that delivery, possession and endorsement are not required.14 Similar rules apply under the Uniform Electronic Transactions Act (“ UETA”).15

1.1.5. Current Fannie Mae Rules for Its Purchases of eNotes and eMortgages

Registration of eNotes & eMortgages: The Federal National Mortgage Association (“ Fannie Mae”) has issued detailed rules for its purchases of eNotes and eMortgages.16 For example, Fannie Mae’s rules provide that “Lenders must . . . ensure eNotes are registered in the MERS eRegistry as soon as possible after the tamper-evident seal has been applied [to the eNote], but no later than one (1) business day of signing. All eMortgages delivered to Fannie Mae must also be registered on the MERS Residential System prior to delivery to Fannie Mae.”17 This registry is intended to comply with the requirements under UETA and the E-SIGN Act for a central registration system.18

Transmitting eNotes to Fannie Mae through MERS eDelivery: A lender that is selling an eNote to Fannie Mae must actually deliver it to Fannie Mae through MERS eDelivery, and then must transmit a request to the MERS eRegistry to begin the process of transferring “Control” and “Location” of the eNote to Fannie Mae.19

1.1.6. Recording of Paper Mortgages & Other Documents May Still Be Required

Even if an originating lender or a loan purchaser would prefer to accept only electronic documents, however, in some jurisdictions only paper mortgages (and other related recordable paper loan documents) are accepted for recording.20

1.2. Impact of Cryptocurrencies & Other Digital Assets on Finance

Cryptocurrencies and other digital assets are held by many investors, and may be required by lenders as additional collateral, even if the primary collateral is real estate or another traditional form of security. As of January 1, 2023, several U.S. states have enacted various types of laws governing security interests in, as well as purchase or sale of, cryptocurrencies and other digital assets. However, there are also many bills, under consideration by various U.S. state legislatures, that, if enacted, would provide ground rules, and a regulatory structure, for such assets.21

1.2.1. Current Practices for Loans Secured by Digital Collateral.

The following practices are customary in jurisdictions in which the proposed 2022 UCC amendments (or similar provisions) have not yet been enacted. In such jurisdictions, secured parties that are relying on digital assets, at least in part, will generally

follow at least one of the following procedures:

(1) (a) the transfer of such digital assets to a securities intermediary,22 (b) the securities intermediary consents to hold the digital assets as financial assets,23 which are credited to the debtor’s securities account, creating a security entitlement24 and (c) control25 by the secured party of the security entitlement pursuant to Article 8 of the UCC, perfecting the secured party’s security interest in the securities account;26 or

(2) (a) delivery by the debtor to the secured party of a private key for a blockchain asset, (b) the secured party transfers such asset to the secured party’s crypto wallet, and (c) perfection of the secured party’s security interest by filing the applicable financing statements.

However, in each case specified in (1) and (2) above, there is no guarantee that the debtor actually owns the digital asset, or that the securities intermediary will get title to the digital asset free from other property claims.27

1.2.2. Proposed 2022 UCC Amendments for Cryptocurrencies & Other Digital Assets.

The American Law Institute and the Uniform Law Commission approved in 2022, and recommended for adoption by all U.S. states, various proposed amendments to the UCC covering cryptocurrencies and other digital assets (the “2022 UCC Amendments”). These proposed amendments include changes to the existing Articles 1-9 of the UCC, as well as a new Article 12 of the UCC.28 However, as of January 1, 2023, according to the “Enactment Map” appearing on the website of the Uniform Law Commission, no state has adopted these amendments.29

The following are new or revised types of assets that are covered in the 2022 UCC Amendments:

Controllable Electronic Records (CERs): The proposed 2022 UCC Amendments define various new types of digital assets that are covered by such 2022 UCC amendments. Probably the most important new type of digital assets are “controllable electronic records (‘CERs’).”30 According to the 2022 UCC Amendments, a CER “is a record that is stored in an electronic medium [such as the blockchain] and that can be subjected to control.”31 The comments in the 2022 UCC Amendments say, “think of bitcoin and other virtual currencies as prototypical controllable electronic records.”32 Another example is that J.P. Morgan has proposed “adapting decentralized finance (DeFi) protocols in the finance industry using tokenized real-world assets. DeFi protocols are self-executing applications on a blockchain that can automate financial services such as lending and borrowing, trading, and asset management while reducing manual involvement from intermediaries.”33

WINTER 2023 8 eReport

Controllable Assets: CERs “also provide a mechanism for evidencing certain rights to payment—controllable accounts and controllable payment intangibles. An account debtor (obligor) on such a right to payment agrees to make payments to the person that has control of the [CER] that evidences the right to payment.”34

Payment Intangible: “Payment intangibles” were defined in the 1999 UCC as “a general intangible under which the account debtor’s principal obligation is a monetary obligation.”35 The 2022 UCC Amendments add the following to such definition: “The term includes a controllable payment intangible.”36 Courts have ruled, for example, that payment intangibles include (1) payment streams that are stripped from equipment leases,37 and (2) settled tort claims.38

Account: “Account” is a traditional UCC category that similarly has been broadened by inclusion of “controllable account” under the 2022 UCC Amendments. “Account” includes, for example, “a right to payment of a monetary obligation, whether or not earned by performance, (i) for property that has been or is to be sold, leased, licensed, assigned, or otherwise disposed of, (ii) for services rendered or to be rendered,” and certain other rights of payment, subject to various exclusions.39

Controllable Account and Controllable Payment Intangible: A “controllable account” or “controllable payment intangible” means, respectively, an account (in the case of a controllable account), or a payment intangible (in the case of a controllable payment intangible) “evidenced by a controllable electronic record that provides that the account debtor undertakes to pay the person that has control under Section 12-105 of the controllable electronic record.”40

Advantages of Control: If a party (1) acquires a CER by purchase,41 for value, in good faith and without notice of a competing claim of a property right in the CER, and (2) has control of the CER,42 then such party will be a “qualifying purchaser” of the CER. “Article 12 confers an attribute of negotiability on controllable electronic records because a qualifying purchaser takes its interest free of conflicting property claims to the record.”43

Recommendations for Lenders Secured by Digital Assets: A lender that intends to be secured, in whole or in part, by digital assets, pursuant to the proposed 2022 UCC Amendments, should (1) design closing procedures, with the borrower’s acknowledgment and consent, in order to enable the lender to have “control” over such assets from the closing date (or such other date that is designated by the lender) until the lender is repaid, (2) require the borrower not only to pay the lender (or the person designated by the lender), but also to acknowledge that the lender is the person in “control” (as defined in the proposed 2022 UCC Amendments) of the digital asset, (3) include a ”choice of law” provision in each CER, and (4) obtain the consents of trading

parties, and the borrower, to provide further assurances to the lender confirming that the lender is a first priority perfected secured party with control over the digital assets and other related collateral.44

1.2.3 Regulatory & Other Legal Issues Relating to Cryptocurrencies & Other Digital Assets

Bank Secrecy Act/Anti-Money Laundering (BSA/AML) & Combating the Financing of Terrorism (CFT). Because money laundering has been facilitated, and other crimes and terrorism have been funded, by cryptocurrencies and other digital assets, therefore the U.S. Treasury Department is devoting substantial resources to preventing this in the future.45 Accordingly, parties should expect a high level of regulatory scrutiny, if they are involved in transactions involving significant amounts of cryptocurrencies and other digital assets.

U.S. SEC & CFTC. The U.S. Securities and Exchange Commission (“SEC ”) and the U.S. Commodity Futures Trading Commission (“CFTC ”) have aggressively asserted their jurisdiction over cryptocurrencies. For example, the SEC charged that BlockFi Lending LLC both (1) failed to register, with the SEC, BlockFi’s offers and sales of its interest accounts under the Securities Act of 1933, and (2) failed to register as an investment company under the Investment Company Act of 1940. BlockFi then paid a $50 million penalty to the SEC. Also, the CFTC charged BitMEX with (1) illegally operating a cryptocurrency derivatives trading platform and (2) anti-money laundering (AML) violations. BitMEX then entered into a consent order, pursuant to which it paid a $100 million penalty to the CFTC and a $50 million penalty to FinCEN.46

U.S. IRS & Other State Tax Agencies. The U.S. Internal Revenue Service (“ IRS”) states that, in the case of the typical owner of virtual currency such as bitcoin (who purchases the virtual currency as a long-term investment and is not a dealer), the sale by such owner of such virtual currency results in long or short term capital gain. Therefore, spending bitcoin is not like spending U.S. currency, which is tax-free. Similarly, if you receive bitcoin for services rendered, that must be reported to the IRS as income.47

Money Transmitter Licenses. The District of Columbia now requires a money transmitter license to be obtained by any person who engages in any money transmission involving bitcoin or other virtual currency “used as a medium of exchange, method of payment or store of value in the District.”48

2. BENEFITS FOR PROPERTY OWNERS UNDER THE INFLATION REDUCTION ACT OF 2022

You, or some of your clients, may be entitled to benefits under the federal Inflation Reduction Act of 2022 (the “ IRA”).49 Here are some examples of the available programs that apply to

WINTER 2023 9 eReport

residential property, but there are many other benefits that apply to commercial property as well.50

The IRA extends, through 2032, the existing tax credit to individuals for residential energy property costs. The IRA also increases the rate of such credit for individuals to 30%, and permits a credit of up to $1,200 per annum for various “energy” improvements, except that such credit will be: (1) up to $2,000 per annum with respect to certain heat pump and heat pump water heaters, and biomass stoves and boilers,51 and (2) up to $150, for home energy audits.52

The IRA extends, through 2034, the residential clean energy tax credit, revises the phased reduction of such credit, and extends the credit to include qualified battery storage technology expenditures.53

The IRA continues the new “energy efficient home tax credit” through 2032, and permits (1) a $2,500 credit for new homes that meet various Energy Star efficiency standards and (2) a $5,000 credit for new homes that are certified as zero-energy ready homes. The IRA also authorizes a credit for energy efficient multifamily dwellings.54

The IRA appropriates funds for the U.S. Department of Energy (“ DOE”) for a HOMES rebate program that provides grants to state energy offices. States must then provide rebates to homeowners, aggregators, and contractors, for certain whole-house energy saving retrofits, inclding enhanced rebates for low-income and moderate-income households. A rebate provided under this program may not be combined with any other federal grant or rebate for the same single upgrade.55

Also, the IRA funds a DOE high-efficiency electric home rebate program that awards grants to state energy offices and Indian tribes. Pursuant to this program, rebates are available for qualified electrification projects in low-income or moderate-income households. Qualified electrification projects include the purchase and installation of certain heat pumps, electric stoves, electric ovens, electric load service centers, insulation, materials to improve ventilation, or electric wiring.56

3. TAX CODE LIMITS ON BUSINESS INTEREST, AND EXCEPTIONS THERETO

As interest rates rise, and as the aggregate amount of business interest continues to increase, borrowers and their attorneys should carefully monitor the amount of each borrower’s “business interest.” For taxable years beginning after December 31, 2017, “business interest” means any “interest paid or accrued on indebtedness properly allocable to a trade or business.” However, a deduction for “business interest” shall not exceed the sum of—

(A) the business interest income of such taxpayer for such taxable year,

(B) 30% of the adjusted taxable income of such taxpayer for such taxable year, plus

(C) the floor plan financing interest (e.g., loans to finance the acquisition of motor vehicles) of such taxpayer for such taxable year.

Any disallowed business interest deduction is carried forward to the next tax year.57 However, the above limit on deduction of business interest is not applicable to a corporation or partnership with average annual gross receipts not exceeding $25 million.58 Further, a “trade or business” does not include “any electing real property trade or business.”59

It is necessary to clearly distinguish “business interest” from other types of interest. For example, “business interest” does not include investment interest. “Investment interest” includes interest that “is paid or accrued on indebtedness properly allocable to property held for investment.”60 However, “investment interest” excludes both (A) “qualified residence interest”61 and “any interest which is taken into account under Section 469 in computing income or loss from a passive activity of the taxpayer.”62 Deduction of investment interest is limited to the extent of net investment income,63 which is calculated in a less generous way to taxpayers than the above deduction for business interest.

The line between a “trade or business,” and an “investment,” is not always clear-cut. It may be possible for taxpayers in some transactions to achieve a preferred tax result based on how the transaction is structured and sized.64

Other provisions of the Internal Revenue Code that may restrict excessive leverage in real estate financings include (1) restrictions on “excess business losses” (which are not allowed and are instead treated as part of the taxpayer’s net operating loss carryforward in subsequent taxable years) for taxpayers other than corporations,65 and (2) a requirement that net operating loss deductions cannot exceed 80% of taxable income.66

4. WHEN REAL ESTATE LENDERS SHOULD BE REITS

What is the most efficient deal structure for a real estate investor that collects interest? This becomes more and more relevant as interest rates continue to increase.

In some cases, a real estate investment trust (“ REIT ”) should be used (rather than a partnership or C corporation) to provide financing for income-producing real estate by purchasing or originating residential and commercial mortgage loans, and mortgage-backed securities (“ MBS”). A mortgage REIT can be formed as a corporation under Subchapter M of the U.S. Tax Code, or as an unincorporated entity that has made a “checkthe-box election” to be taxed as a corporation. A mortgage REIT, unlike a C corporation, generally does not pay entity tax on its net earnings if it distributes all of its current-year taxable

WINTER 2023 10 eReport

income to its shareholders, since a mortgage REIT is entitled to a deduction for dividends paid. Further, under Sec. 199A of the U.S. Tax Code, a U.S. individual can claim a 20% deduction for dividends received from a mortgage REIT that collects interest income. In contrast, interest income allocated to a U.S. individual partner is not eligible for this deduction.67

5. WHEN A LOAN WILL BE RECHARACTERIZED AS EQUITY FOR TAX PURPOSES

In the Tribune Media case,68 Tribune Media Co. (“ Tribune”), was the publisher of the Chicago Tribune, and the owner of the Chicago Cubs. Both were controlled by Sam Zell.

In 2009, the Tribune, and the Ricketts family (the founders of TD Ameritrade), formed Chicago Baseball Holdings, LLC (the “ LLC ”). The LLC obtained 2 loans, (1) a senior loan funded by a commercial lender, and (2) a subordinate loan (“sub loan”) funded by the Ricketts. Tribune guaranteed collection of the loans.69

The Tax Court ruled that the “sub loan” was actually not bona fide debt for tax purposes, and would be recharacterized as equity.70 The Tax Court stated that the main factors, indicating that the “sub loan” was actually equity, were: (1) there was no fixed maturity date for repayment of the “sub loan,”71 (2) the terms of the “sub loan,” and the subordination agreement, prevented any meaningful right to enforce payments of the “sub loan” as they became due,72 (3) the intent of the parties was to treat the “sub loan” as equity,73 (4) because of the interests of the Ricketts family in both the LLC and the sub lender, it was unlikely that the “sub loan” would ever be enforced,74 (5) the LLC did not meet its burden of proving that it could have obtained a similar loan from an unrelated third party,75 (6) the “sub loan” proceeds were used by the Ricketts family to purchase their equity interest (rather than funding operating expenses),76 and (7) repayment of the “sub loan” was uncertain.77

6. ENFORCEABILITY OF MAKE-WHOLE PREMIUMS IN BANKRUPTCY

When Ultra Petroleum Corp. and its affiliates (collectively “ Ultra”) obtained various loans, it agreed, if it prepaid the loans, to pay a “make-whole” premium to each lender equal to the present value of the interest payments such lender would have received if its loan had been paid at its maturity. However, when natural gas prices plummeted, Ultra became insolvent, and it filed for bankruptcy. But during the Ultra bankruptcy proceeding, natural gas prices roared back, and Ultra became solvent again. Nonetheless, Ultra proposed a plan that would not pay its lenders the agreed make-whole premium. Instead, Ultra proposed, pursuant to Section 502(b)(2) of the Bankruptcy Code (which disallows payment of unmatured interest), to pay only the sum of (1) the outstanding principal owed to its lenders, (2) all interest that had accrued before Ultra’s bankruptcy,

and (3) interest on both such amounts at the Federal Judgment Rate (which was much lower than the contractual interest rate) only for the duration of the bankruptcy proceeding.78 The lenders objected, because Ultra’s proposed payments were $387 million less than their calculation of the contractually required payments.

The Fifth Circuit recently ruled that Ultra’s lenders are entitled to their full make-whole premiums, at the agreed contractual rate, based upon existing case law to the effect that solvent debtors in bankruptcy must nonetheless pay interest at the rate they originally agreed to pay to their lenders. The Fifth Circuit decision is in accord with decisions by the U.S. Supreme Court and some other federal courts, but technically conflicts with the literal provisions of the Bankruptcy Code.79

Similarly, in an unrelated case involving Pacific Gas & Electric Company (“ PG&E”), the Ninth Circuit held that since PG&E had a net worth of almost $20 billion, and clearly was solvent, therefore PG&E was obligated to pay post-petition interest to its unsecured trade creditors, at the applicable contractual or legal rate, even though PG&E had filed under Chapter 11 of the Bankruptcy Code.80

7. STRUCTURING OF BANKRUPTCY REMOTE ENTITIES

The ABA Committee on Securitization and Structured Finance has published an article, summarizing the issues involved in structuring a borrowing entity, in order to enable it to be “bankruptcy remote” (i.e., it will be unlikely to file for bankruptcy). Such article includes discussions of topics including “special purpose vehicles,” “substantive consolidation,” “true sale,” and related case law.81 This ABA committee has also proposed a model form of “Delaware Limited Liability Company Agreement,” which is extensively annotated with comments.82 For new lawyers, or those who have not been closely following the cases in this area, these ABA articles will be invaluable. Lawyers should also be familiar with the specific requirements of the rating agencies (regarding the borrower’s structure and powers), which are available online.83

This article should not be construed as legal advice, and readers should not act upon information in this article without legal counsel.

WINTER 2023 11 eReport

Endnotes

1. Brook Boyd is Counsel to Meister, Seelig & Fein, LLP in their New York office. He is a member of the Connecticut, Florida, New Jersey and New York bars. He is the author of Real Estate Finance (Law Journal Press, 51st ed.) and has published many articles in legal and professional journals.

2. Pub. L. No. 106-229, 114 Stat. 464 (June 30, 2000).

3. 15 U.S.C. § 7021(a)(1). One commentator took the position that it is not clear who is the “issuer” of a “transferable record.” He stated, “to qualify as a transferable record, the issuer of the electronic record must agree to the treatment of the record as a transferable record under the UETA [Uniform Electronic Transactions Act]. . . . The obligor on a paper promissory note is not the issuer of an electronic record.” Whitaker, “Rules Under the Uniform Electronic Transactions Act for an Electronic Equivalent to a Negotiable Promissory Note,” 55 Bus. Law. 437, 448 n.46 (Nov. 1999).

4. 15 U.S.C. 7021(a)(1). Note that Section 16 of UETA does not require that the transferable record relate “to a loan secured by real property.”

5. However, UETA is not limited to “transferable records” that are secured by real property, since, for example, it also applies to “transferable records” that are secured by documents of title. UETA § 16(d).

6. Uniform Electronic Transactions Act § 16 (1999), available at https:// higherlogicdownload.s3-external-1.amazonaws.com/UNIFORMLAWS/21c366b3-b11c-d774-f34d-7901ab76e9a5_file.pdf?AWSAccessKeyId=AKIAVRDO7IEREB57R7MT&Expires=1673126463&Signature=XIAG9qPNXX0kWXQMeFjEMySapAM%3D (last visited Jan. 7, 2023).

7. UCC § 9-102(a)(69) (ULC 1999).

8. UCC § 9-102(a)(7)(B) (ULC 2010).

9. UCC § 9-105(a-b) (ULC 2010).

10. UCC § 9-317(d) & cmt. n. 6 (ULC 2010).

11. UCC § 9-613, cmt. 2 (ULC 2010).

12. 15 U.S.C. § 7021(b).

13. Id. § 7021(b-d).

14. 15 U.S.C. § 7021(d).

15. UETA § 16 (1999).

16. Fannie Mae, Selling Guide (Dec. 14, 2022), available at https://singlefamily.fanniemae.com/media/33041/display (last visited Jan. 8, 2023).

17. See generally, Fannie Mae, “Guide to Delivering eMortgages to Fannie Mae,” § 3.5 (June 22, 2022), available at https://singlefamily.fanniemae. com/media/4601/display (last visited Jan. 8, 2023).

18. 15 U.S.C. § 7021(b); UETA § 16(b-c) (1999).

19. See generally, Fannie Mae, “Guide to Delivering eMortgages to Fannie Mae,” § 4 (June 22, 2022), available at https://singlefamily.fanniemae. com/media/4601/display (last visited Jan. 8, 2023).

20. “State-by-State Recording and Notarization Guidance” (Blackwell April 26, 2020), available at https://hbfiles.blob.core.windows.net/webfiles/HB_State-by-State%20Recording%20and%20Notarization%20 Guidance_Responding%20to%20COVID19_April%2030%202020.pdf (last visited Dec. 3, 2022).

21. The following states enacted their own laws that facilitate the ownership and financing of cryptocurrencies and other digital assets (but are not identical with the final proposed 2022 amendments to the UCC approved by the American Law Institute, and then by the Uniform Law Commission at its July 2022 meeting):

Idaho enacted Chapter 284 of 2022 regarding the purchase and sale of digital assets, and perfection by possession or control of digital assets.

Indiana enacted Public Law 110 of 2022 adding a new chapter to the Uniform Commercial Code that applies to “controllable electronic records” such as cryptocurrencies.

New Hampshire similarly enacted Chapter 281 of 2022 based on a draft version of the 2022 amendments to the UCC.

See also Wyo. Stat. Ann. § 34-29-101 et seq.

Iowa and Nebraska adopted a preliminary version of the UCC “controllable electronic record” proposal.

Arkansas and Texas adopted the “controllable electronic record” rules only for virtual currency.

Utah enacted comparable laws for virtual currency.

22. UCC § 8-102(a)(14) (1994).

23. UCC § 8-102(a)(9) (1994).

24. UCC § 8-102(a)(17) (1994).

25. UCC §§ 8-106 (1994 & 2022) & 8-501, comments 1 & 4 (1994 & 2022).

26. UCC § 8-102, comment 9 (2022) & § 12-102, comment 2 (2022).

27. See generally “TriBar Report on Opinions Under 2022 Amendments to the Uniform Commercial Code Regarding Emerging Technologies” § II at 2-4 (Aug. 3, 2022 draft report not yet considered or approved by TriBar but presented for discussion at the 9/16/22 ABA Bus. Law Annual Meeting presentation entitled “Legal Opinion Letters on Digital Assets”) (K.A. Desmarais, S.M. Rocks, L. Safran & S. Weise, speakers) (hereinafter called “Draft TriBar Report on Opinions Under 2022 UCC Amendments”).

28. A copy of such 2022 proposed amendments to the UCC is available at https://www.uniformlaws.org (last visited Jan. 8, 2023).

29. “2022 Amendments to UCC” (Enactment Map), available at https:// www.uniformlaws.org/committees/community-home?communitykey= 1457c422-ddb7-40b0-8c76-39a1991651ac (last visited Jan. 7, 2023).

30. UCC § 12-102(a)(1) (ULC 2022).

31. Id.

32. UCC Article 12, Prefatory Note to Article 12, § 2 (ULC 2022).

33. “Institutional DeFi: The Next Generation of Finance?” (J.P. Morgan et al. 2022), available at https://www.jpmorgan.com/onyx/documents/ Institutional-DeFi-The-Next-Generation-of-Finance.pdf (last visited Jan. 11, 2023).

34. “Prefatory Note to Uniform Commercial Code Amendments (2022)” § 2(a) (ULC 2022).

35. UCC § 9-102(a)(61) (1999).

36. UCC § 9-102(a)(61) (ULC 2022).

37 In re Commercial Money Center, Inc., 350 Bankr. 465, 469, 488-489 (9th Cir. B.A.P. 2006), modified In re Commercial Money Center, Inc., 392 Bankr. 814, 824-825, 832 (9th Cir. B.A.P. 2008). In this case, Commercial Money Center, Inc. (the debtor), leased equipment to lessees, and then (1) pooled groups of leases and assigned its contractual rights (to future lease payments) to NetBank, (2) obtained surety bonds guaranteeing the lease payments, and assigned its interest in the surety bonds to NetBank, and (3) granted to NetBank a separate security interest in the leases and other property). The court ruled that the debtor’s rights (to such future lease payments) were payment intangibles.

38 In re Wiersma, 324 Bankr. 92, 106-107, 109-110 (9th Cir. B.A.P. 2005) aff’d in part, rev’d in part on other grounds, 483 F.3d 933 (9th Cir. 2007).

But see In re S-Tek 1, LLC, 635 Bankr. 860, 869 (Bankr. D. N. Mex. 2021) (“a secured party cannot have a security interest in the proceeds of a commercial tort claim under grants of collateral other than a grant of a security interest in a commercial tort claim”).

39. UCC § 9-102(a)(2) (ULC 2022).

40. UCC § 9-102(a)(27A & 27B) (ULC 2022).

41. UCC § 1-201(b)(29) and (30) (ULC 2001).

42. UCC § 12-102(a)(2) (ULC 2022).

43. “Prefatory Note to Uniform Commercial Code Amendments” § 2(a) (ULC 2022).

44 See T. Harmon, J. Moringiello, S. Sepinuck & S. Weise, “Commercial Law Developments: 2021-2022” at 34, 44 (ABA Bus. Law Sec. Annual Meet. Sept. 2022) (Powerpoint).

45. “Action Plan to Address Illicit Financing Risks of Digital Assets” (U.S.

WINTER 2023 12 eReport

Treasury Dept. Sept. 12, 2022), available at https://home.treasury.gov/ system/files/136/Digital-Asset-Action-Plan.pdf (last visited Jan. 9, 2023).

46. S. M. Humenik, C. L. Isaac, K. E. Riemer and C. Mikhael, “CFTC and SEC Perspectives on Cryptocurrency and Digital Assets -Volume I: A Jurisdictional Overview,” ABA RPTE eReport at 8-10 (Spring 2022), available at https://www.americanbar.org/groups/real_property_trust_estate/publications/ereport/ (last visited Jan. 9, 2023).

47. “Frequently Asked Questions on Virtual Currency Transactions” (IRS Dec. 1, 2022), available at https://www.irs.gov/individuals/international-taxpayers/frequently-asked-questions-on-virtual-currency-transactions (last visited Jan. 9, 2023).

48. “Bulletin 22-BB-001-08/04: Certain Bitcoin Activity Subject to DC Money Transmission Laws” (Banking Bureau of the Department of Insurance, Securities and Banking of Washington, D.C. Aug. 8, 2022), available at https://content.govdelivery.com/accounts/DCWASH/bulletins/326e069 (last visited Jan. 9, 2023).

49. Inflation Reduction Act of 2022, Pub. L. No. 117-169 (2022), available at https://www.congress.gov/bill/117th-congress/house-bill/5376/text (last visited Jan. 9, 2023).

50. See the summary of benefits, under the Inflation Reduction Act of 2022, that appears at https://www.congress.gov/bill/117th-congress/ house-bill/5376 (last visited at Jan. 9, 2023).

51. Id. § 13301.

52. Id.

53. Id. § 13302.

54. Id. § 13304.

55. Id. § 50121.

56. Id. § 50122.

57. An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018, Pub. L. No. 115-97 (2017) (“Tax Cuts and Jobs Act”), § 13301 (codified as 26 U.S.C. § 163(j)); H.R. Rep. 115-466 (2017) (“Tax Cuts and Jobs Act Conference Report”), at 385-392, available at http://docs.house.gov/billsthisweek/20171218/CRPT-115HRPT-%20466.pdf (last visited Jan. 2, 2023).

58. Tax Cuts and Jobs Act, § 13102 (codified as 26 U.S.C. § 448(c)) and § 13301 (codified as 26 U.S.C. § 163(j)(3)); Tax Cuts and Jobs Act Conference Report at 385-392.

59. Tax Cuts and Jobs Act, § 13301 (codified as 26 U.S.C. § 163(j)(7)(A)(ii)); Tax Cuts and Jobs Act Conference Report at 391-392.

60. 26 U.S.C. § 163(d)(3)(A) (2022).

61. Tax Cuts and Jobs Act, Pub. L. No. 115-97 (2017), § 11043 (codified as 26 U.S.C. §§ 163(d)(3)(B)(i) & 163(h)(3)) (applicable to tax years beginning before 1/1/26); Tax Cuts and Jobs Act Conference Report, at 256-258.

62. 26 USC § 163(d)(3)(B)(ii).

63. 26 U.S.C. § 163(d)(1).

64. See generally Vandenberg, Brignall, & Richard Schneible, “A strategy to raise a business’s interest limitation,” Tax Adviser (June 2022), available at https://www.thetaxadviser.com/issues/2022/jun/strategy-to-raise-business-interest-limitation.html (last visited Jan. 10, 2023).

65. Tax Cuts and Jobs Act, § 11012 (codified as 26 U.S.C. § 461(l)); Tax Cuts and Jobs Act Conference Report at 238-239.

66. Tax Cuts and Jobs Act, § 13302 (codified as 26 U.S.C. § 172(a) and other miscellaneous sections); Tax Cuts and Jobs Act Conference Report at 393-394.

67. Stern, “Mortgage REITs: When should one be used?,” Tax Adviser (Dec. 2021), available at https://www.thetaxadviser.com/newsletters/2021/dec/mortgage-reits.html (last visited Jan. 10, 2023). See also 26 U.S.C. § 199A.

68 Tribune Media Co. v. Comm’r, T.C.M. 2021-122, action on dec., 2022-Docket No. 20940-16. See generally R. Lipton, “Tribune Media: A Split Decision for the Chicago Cubs’ Leveraged Partnership Transaction,”

J. of Tax. at 6-16 (Feb. 2022).

69 Tribune Media Co. v. Comm’r, T.C.M. 2021-122 at 2.

70. Id at 3.

71 Tribune Media Co. v. Comm’r, T.C.M. 2021-122 at 60-63. Although the subordinate debt (“sub debt”) had a stated maturity of 15 years, however, the sub debt could not be repaid before the senior debt, and the senior lenders had the right to extend the maturity date of the senior debt. Id. pps. 60-61

72. Id at 67-70

73. Id at 74-78.

74. Id at 78-80.

75. Id at 83-86.

76. Id at 86-87.

77. Id at 89-90.

78. Ultra also argued that its lenders were “unimpaired” under 11 U.S.C. §§ 1123(a)(2) & 1124, and were therefore “conclusively presumed to have accepted the plan” per 11 U.S.C. § 1126(f).

79 In re Ultra Petroleum Corporation, 51 F.4th 138 (5th Cir. 2022).

80. In re PG&E Corporation, 46 F. 4th 1047 (9th Cir. 2022). Technically, PG&E was obligated to pay interest to its trade creditors, at the applicable contractual or legal rates, so that its creditors would be “unimpaired” by PG&E’s reorganization plan, pursuant to 11 U.S.C. § 1124(1). California generally provides for a default interest rate of ten percent on contractual obligations. Cal. Civ. § 3289(b). In contrast, the court in In re Latam Airlines Group S.A., Docket No. 22-1940 (2d Cir. Dec. 14, 2022), ruled that trade creditors were not entitled to post-petition interest since (1) the debtor was insolvent, and (2) the trade creditors’ claims were not impaired under Section 1124(1) of the Bankruptcy Code.

81. ABA Comm. On Securitization & Structured Fin., “Bankruptcy Remoteness: A Summary Analysis,” 77 Bus. Law. 1105 (ABA Bus. Law Sec. Fall 2022).

82. ABA Comm. On Securitization & Structured Fin., “Model Form of Limited Liability Company Agreement,” 77 Bus. Law. 1131 (ABA Bus. Law Sec. Fall 2022).

83 E.g., “U.S. Structured Finance Asset Isolation And Special Purpose Entity Criteria,” (Standard & Poor May 15, 2019), available at https:// disclosure.spglobal.com/ratings/en/regulatory/article/-/view/type/ HTML/id/2818845 (last visited Jan. 3, 2023); and “U.S. and Canadian Multiborrower CMBS Rating Criteria: Discussion Paper (Potential Changes to CMBS Methodology in Advance of a Likely Exposure Draft),” (Fitch Ratings Dec. 6, 2022), available at https://www.fitchratings.com/ research/structured-finance/us-canadian-multiborrower-cmbs-rating-criteria-discussion-paper-potential-changes-to-cmbs-methodology-in-advance-of-likely-exposure-draft-06-12-2022?FR_Web-Validation=true&mkt_tok=NzMyLUNLSC03NjcAAAGJKSE0qixv2I5kzWJhoBI472Ugtpt_ q7iBJEcnfGo_gdc8LweYVkzPy_im3LHR9Q5YpYRf-LkKjeCfg9rtrNvMOsrqW4H7Vv1xFjFC3zMgMRmqR_s5TpY (last visited Jan. 6, 2023).

WINTER 2023 13 eReport

New York Court Holds a Pledge Agreement Does Not “Clog” a Borrower’s Equity of Redemption

By: Jose A. Fernandez1

This article discusses Atlas Brookview Mezzanine LLC v. DB Brookview LLC, the first New York court decision to directly hold that enforcing a mezzanine pledge taken in conjunction with a mortgage as security does not violate a borrower’s equity of redemption.

Over the last decade, commercial lenders have increasingly relied on “accommodation” pledges to obtain additional security in connection with mortgage loans. The typical structure involves a property-owning borrower entity obtaining financing secured by a mortgage, while the borrower’s sole member or parent entity—often referred to as the “mezzanine entity”—

guaranties the mortgage loan. The mezzanine entity’s guaranty is separately secured by a pledge of its 100% ownership interests in the borrower.

If a borrower defaults, a mortgage lender must typically pursue a lengthy judicial foreclosure process. Armed with an accommodation pledge, however, the lender can pursue a more expeditious Uniform Commercial Code (“UCC”) sale of the mezzanine’s 100% equity interests in the borrower. Article 9 of the New York UCC requires the lender to market and conduct the public auction of the equity interests in a commercially reasonable manner. Upon consummation of the auction, the winning bidder will own 100% of the membership interests in the borrower entity, and thus control the underlying property. If the lender’s credit bid is the highest bid, the lender has effectively obtained control of the property in as little as a few months.

Unlike a mortgage foreclosure, a UCC sale of a borrower’s equity under a pledge does not extinguish subordinate liens against the assets of the borrower itself, and the lender takes ownership of the borrower via a UCC sale of the borrower’s equity subject to the obligations of the borrower and all liens on the borrower’s assets.

As accommodation pledges have become more prevalent, commercial real estate practitioners have debated whether they vio -

WINTER 2023 14 eReport

late the centuries-old equitable doctrine that prohibits lenders from “clogging” a borrower’s right to pay off its mortgage loan and redeem the property at any time prior to the foreclosure sale. This right, known as the borrower’s “equity of redemption,” generally cannot be waived by an unsophisticated borrower under New York law. But even sophisticated commercial borrowers have argued that accommodation pledges clog their redemption right, as the UCC sale process shortens the amount of time they have to redeem the debt and is not always subject to judicial oversight. “Where the redemption right is lawfully waived, or where it is not actually impaired, courts will hopefully feel comfortable ruling for the lender and rejecting “clogging” claims, which will, in turn, provide a high level of reliability in structuring multi-tiered real estate financings,” as noted by Zachary G. Newman, Co-Chair of the American Bar Association’s Section of Litigation Commercial and Business Litigation Committee, and lead counsel in the Atlas Brookview case.

The Atlas Brookview Borrower’s “Clogging” Claim

Until recently, no New York court had squarely addressed whether enforcing a mezzanine pledge taken in conjunction with a mortgage as security violates a borrower’s equity of redemption. At least one New York court had previously declined to enjoin a UCC sale based on a borrower’s clogging challenge and expressed doubt about the claim. HH Cincinnati Textile L.P. v. Acres Capital Servicing LLC, 2018 WL 3056919, at *3-4 (Sup. Ct. N.Y. Cnty. June 20, 2018) (Ostrager, J.). But the court later held that the denial of injunctive relief did not constitute a ruling on the merits.

In November 2021, the first New York court to address the issue on the merits dismissed a commercial borrower’s claim that the collateral pledge granted by its parent entity violated the equity of redemption. Atlas Brookview Mezzanine LLC v. DB Brookview LLC (Index No. 653986/2020; entered on Nov. 18, 2021). In Atlas Brookview, the borrower obtained a $64.9 million mortgage loan secured by a multifamily development in Illinois. The mortgage was governed by Illinois law, and the rest of the loan documents were governed by New York law. As additional security for the loan, Atlas Brookview Mezzanine LLC (“Atlas Mezzanine”), which owned 100% of the borrower entity, guaranteed the entire loan and entered into a pledge agreement securing the guaranty.

Following pre-maturity defaults in June, 2020, the lender scheduled a UCC foreclosure sale scheduled for August 25, 2020. The day before the scheduled auction, the court granted temporary injunctive relief delaying the sale. However, on October 15, 2020, Justice Andrew Borrok denied injunctive relief and noted that no New York court had sustained a “clogging the equity” challenge. The court also recognized that granting relief “would be upending the entire mezzanine lending business.” Following the denial of injunctive relief, the UCC foreclosure sale was rescheduled and consummated on February 17, 2021, and the lender became the owner of the borrower entity and gained control of the property.

The Motion to Dismiss

Atlas Mezzanine’s other challenges to the UCC sale procedures were rendered moot by the consummated sale, but it continued to pursue its declaratory judgment claim arguing that the pledge agreement clogged the borrower’s equity of redemption and was void ab initio, thus requiring an unwind of the sale.

The lender moved to dismiss the declaratory judgment claim and argued that upholding the claim would seriously disrupt billions of dollars of mezzanine financing in New York state. In addition, the lender argued that a borrower retains a right to redeem the debt under Section 9-623 of the UCC until the auction is conducted. Moreover, the lender noted that the borrower was a sophisticated developer represented by competent counsel of its choice and that it expressly endorsed and benefitted from the collateral pledge structure. Further, the lender pointed to Illinois statutes that explicitly allow sophisticated mortgage borrowers to waive the right of redemption.

The borrower argued that the equity pledge structure had never been sanctioned by a New York court, and that it clearly violated its equity of redemption by cutting short the time to redeem the debt. The borrower argued that New York law does not permit any borrower to waive the redemption right, and that “the market effect if the motion [to dismiss] is granted, is that the structure will be viewed as sanctioned … and mortgage lenders everywhere will slap an equities pledge on top of every mortgage loan.” The borrower also argued that the streamlined UCC sale process could allow a lender to foreclose in as little as 30 days.

The Court’s Decision

The Court did not rely on the Illinois law provisions that permit a borrower to waive its right of redemption. Nevertheless, the court rejected the borrower’s argument that the UCC sale had been conducted as a fire sale, and noted that the borrower had months to redeem the debt. Accordingly, the court appeared to recognize that mezzanine pledges do not clog a mortgage borrower’s equity of redemption because the borrower retains the right of redemption provided by UCC § 9-623.

Separately, the Court noted that “commercially sophisticated people represented by able counsel agree[d] that the collateral is sufficient to support the loan and voluntarily enter[ed] into a loan agreement that contemplates additional collateral.” Consistent with well-settled New York principles that seek to afford certainty to sophisticated commercial real estate parties, the court recognized that the borrower “entered into this structure voluntarily with the advice of good counsel” in connection with a $65 million loan. Accordingly, the court dismissed the declaratory judgment claim with prejudice.

The Court’s decision on the motion to dismiss, issued from the bench, recognized that the prior ruling in the HH Mark Twain case did not dismiss the equity-clogging claim on the merits.

WINTER 2023 15 eReport

However, the Court found that prior decision merely stood for the proposition that the denial of a preliminary injunction “didn’t foreclose the issue at the motion to dismiss stage.”

Conclusion

Justice Borrok’s decision recognized that equity pledges are regularly negotiated and consented to by commercial parties, and that they constitute consensual “business terms” that are not foisted upon unsophisticated borrowers. Because the decision relied on the principle that agreements between sophisticated parties are generally enforceable, it provides comfort to commercial lenders that continue to obtain accommodation pledges in commercial real estate transactions. Nevertheless, the decision was issued from the bench and remains unreported, and no appellate court has addressed the issue. Accordingly, borrowers may continue to lodge challenges to accommodation pledges and the case law may continue to evolve until an appeals court settles the issue.

Endnotes

1. Jose A. Fernandez is an Associate in the New York office of Thompson Coburn LLP. Zachary G. Newman , Robert Rabin , and Jose A. Fernandez at Thompson Coburn LLP were counsel of record to the lender in the Atlas Brookview case.

WINTER 2023 16 eReport

Destroying Charitable Conservation Easements Is Not Within Congressional Intent

By: Nancy Ortmeyer Kuhn1*

Charitable conservation easements have been a target for examination by the IRS for many years, resulting in the disallowance of millions of dollars of charitable deductions. Learn what the IRS is doing wrong, and in the process acting contrary to the legislative intent behind the incentives afforded to taxpayers to conserve natural resources.

The U.S. Tax Court, in Green Valley Investors, LLC v. Commissioner, 159 T.C. No. 5 (Nov. 9, 2022), analyzed whether the syndicated conservation easements at issue in the case were subject to the §6662A2 penalty, which is an additional penalty on “listed” and “reportable” transactions. The IRS in Notice 2017-10 had added syndicated conservation easements to the definition of transactions considered to be “listed” — i.e., tax

shelters. If a transaction fits within the definition, there are IRS reporting requirements with substantial penalties for a failure to report. The taxpayers argued that the IRS did not follow the procedures outlined in the Administrative Procedures Act (APA) in issuing the Notice, because they did not follow the required notice-and-comment opportunity afforded to taxpayers. The Tax Court agreed. The court held that the taxpayers were not liable for the §6662A penalties. In an apparent response to this opinion, the IRS issued proposed Treasury Regulations to, in effect, replace Notice 2017-10.3 This time the IRS is providing a Notice and Comment period, as required, before finalizing the new Treasury Regulation.

In Green Valley, a reviewed opinion, the Tax Court extensively analyzed the legislative history behind the penalty provision applicable to listed transactions, and did not find the exceptions relied upon by the Commissioner as particularly convincing. The court held: “…we remain unconvinced that Congress expressly authorized the IRS to identify a syndicated conservation easement transaction as a listed transaction without the APA’s notice-and-comment procedures, as it did in Notice 2017-10.”4

Charitable Easements After ‘Green Valley’ Reliance on Legislative History Should Apply to the Core Incentive as Well

Similarly as with the penalty provision, the Tax Court and other courts should rely upon legislative history to further protect

WINTER 2023 17 eReport

the advantages afforded taxpayers who donate conservation easements to qualified charities. Section 170(h) provides incentives for property owners to protect disappearing species, to protect open vistas, and to preserve natural habitats and scenic views. Taxpayers receive charitable deductions offsetting up to 50% of adjusted gross income for said donations. However, the IRS has been erecting roadblocks so that taxpayers are unable to take advantage of these tax incentives. By doing so, the IRS is arguably frustrating congressional intent. Notice 2017-10 classifying syndicated easements as listed transactions, the new Proposed Regulations to replace the Notice, and the IRS’s litigating posture for the hundreds of cases pending have substantially crippled the conservation easement space. Instead of focusing on the valuations of the conservation easements, the IRS and Tax Court have acted to completely eliminate these incentives — contrary to legislative intent.

Earlier courts analyzing conservation easements ---before the line of cases in which easements were completely disallowed in reliance on the Proceeds Clause in the Treasury Regulations5 — were a bit more lenient in allowing the charitable deduction. In Glass v. Commissioner6 (2005), both the Tax Court and the Sixth Circuit Court of Appeals allowed the conservation easement charitable deductions claimed by the taxpayers, with valuation reserved as a subsequent issue. The Tax Court relied upon legislative history and the intent of Congress in allowing the charitable deductions. The court noted that in promulgating §170(h), Congress stated as follows:

It is intended that a contribution of a conservation easement …qualify for a deduction only if the holding of the easement…is related to the purpose or function constituting the donee’s purpose for exemption… and the donee is able to enforce its rights as holder of the easement…and protect the conservation purposes which the contribution is intended to advance. The requirement that the contribution be exclusively for conservation purposes is also intended to limit deductible contributions to those transfers which require that the donee hold the easement…exclusively for conservation purposes (i.e. that they not be transferable by the donee in exchange for money, other property, or services). H. Conf. Rept. 95-263.7

While Congress stated strong support for protecting conservation purposes, it also indicated that the deduction was not without limits and qualifying requirements. However, there is not one word in this legislative history about the distribution of proceeds in the unlikely event of a judicial extinguishment. By turning this hypothetical event into a “make or break” criterion for purposes of qualification, the IRS and affirming courts have frustrated the intent of Congress and §170(h).

As discussed in my previous article8 the Eleventh Circuit Court of Appeals recently reversed the position of the IRS and Tax Court in favor of allowing taxpayers a deduction.9 The Sixth Circuit, on the other hand, has affirmed the IRS’s and Tax

Court’s positions completely disallowing the deductions and declaring the easements invalid. The IRS and courts rely upon language in the easement document as it relates to the Proceeds Clause.10 The Sixth Circuit taxpayers filed a Petition for Writ of Certiorari with the Supreme Court11 to gain clarity on the issues, but that Petition was denied. The split in the Circuits remains with differing outcomes for taxpayers depending upon the location of the property and taxpayers.

The Tax Court in its majority opinion in Oakbrook12 discussed that the Treasury Regulations interpreting §170(h) were promulgated in January 1986 and have never been amended. The court also relied upon its observation that Congress has amended the statutory provisions of §170 without any indication that the Treasury Regulations interpreting §170(h) were problematic.13 However, these statutory amendments do not address the extinguishment provisions and the Proceeds Clause14 which has the effect of disallowing the entire deduction. Instead, Congress has focused on whether there is actually a conservation purpose and a reasonable value. It has been easier for the IRS and the Tax Court to disallow the entire easement in contravention of the legislative history, rather than follow prior precedent that focused on charitable qualifications and valuation issues.

A Matter of Language

One solution to this quagmire would be for the IRS to offer a settlement initiative in which the taxpayers are allowed to amend the language in their easements, assuming there has not been a judicial extinguishment action and proceeds have not yet been distributed. The charitable qualification and valuation issues could be separately negotiated, with valuation limited to 2.5 times the fair market value of the property, as recently enacted in the 2023 Omnibus Legislation.15 This new law only applies prospectively and does not impact all of the cases in the Federal courts, or any of the ongoing IRS examinations. An interpretation of a Treasury Regulation regarding the distribution of proceeds of a judicial sale (that is very unlikely to happen) is also not impacted by this new statutory amendment to IRC §170.

The goal of §170(h) is for the easement to be perpetual. The standard language in easement documents specifies that the easement is perpetual. The extinguishment is hypothetical. My review of case law does not reveal a single case among the hundreds of cases pending and decided in which a judicial extinguishment has occurred and proceeds from the sale distributed. It seems there is an argument that the IRS cannot base an examination on a hypothetical set of facts that has not occurred. Nothing has happened. The easement is perpetual. Instead, the IRS finds the prototype language in the easement, used by hundreds or thousands of projects, and says “gotcha.”

The taxpayer used the wrong language and so the entire easement fails, even though the easement is perpetually valid and there will be nothing to disrupt that easement until there is a judicial extinguishment such as an eminent domain action.

WINTER 2023 18 eReport

There has been no harm, other than arguable harm to the federal fisc if the valuation of the easement is not reasonable. That loss is better dealt with in an examination of valuation of the easement. As Tax Court Judge Holmes stated in his dissenting opinion in Oakbrook: “Our holding today will likely deny any charitable deduction to hundreds or thousands of taxpayers who donated conservation easements that protect perhaps millions of acres.”16

Conclusion

Now that the Supreme Court has denied review of Oakbrook Land Holdings and thus declined to resolve the conflict between the Sixth Circuit Court of Appeals17 and the Eleventh Circuit Court of Appeals,18 the tax treatment of conservation easements will vary widely depending upon where the property is located. Property in the Eleventh Circuit, i.e., Alabama, Florida, and Georgia, will be conserved, while there will be little incentive for taxpayers in the Sixth Circuit to donate to qualified conservation charities to preserve the birds, trees, and animals of Kentucky, Michigan, Ohio, and Tennessee. This divisiveness was not envisioned by Congress when originally enacting §170(h). Moreover, the statutory requirements recently enacted19 will not prevent the IRS and courts from dealing the “gotcha” card. The IRS and courts will presumably continue to completely disallow conservation easements without regard to value everywhere except the Eleventh Circuit, based upon a technicality. These actions continue to frustrate longstanding Congressional intent. Although Congress limited the valuation of easements in its recent amendments, it did not limit the validity of conservation easements themselves. By doing so, Congress signaled that using a technicality to completely invalidate conservation easements is outside the intent of the statute. More focus should be trained on furthering legislative intent, rather than frustrating legitimate conservation activities.

Endnotes

1.* Nancy O. Kuhn is currently a shareholder at Shulman Rogers, where her practice focuses on tax controversy work. Nancy was a law clerk at the U.S. Tax Court for two years and then worked as a litigator for the IRS for approximately 10 years, handling litigation for exempt organizations the final five years. She is now in private practice and represents taxpayers before the IRS, Tax Court, and district courts. She has served as an expert witness on several matters, including charitable conservation easements.

Reproduced with permission from Tax Management Estates, Gifts, and Trusts Journal, Volume 48, Issue No. 01, 1/12/23. Copyright

©2023 by The Bureau of National Affairs, Inc. (800-372- 1033) http:// www.bna.com

2. All section references are to the Internal Revenue Code, as amended, or the Treasury Regulations thereunder.

3. Prop. Reg. §1.6011-9, REG-106134-22, 87 Fed. Reg. 75,185 (Dec. 8, 2022).

4. Green Valley, slip. op. at 23.

5. Reg. §1.170A-14(g)(6). See Kuhn, Insight: Charitable Conservation Easements — IRS and Tax Court Act to Shut Them Down, Bloomberg Tax Insights, July 22, 2020.

6. Glass v. Commissioner, 124 T.C. 258 (2005), aff’d, 471 F.3d 698 (6th Cir. 2006).

7. 124 T.C. 258 at 283.

8. Kuhn, A Split in the Circuits: Will the Supreme Court Take Up the Easement Challenge? Bloomberg Tax Insights, Apr. 4, 2022.

9. Hewitt v. Commissioner, 21 F.4th 1336 (11th Cir. 2021), rev’g and rem’g T.C. Memo. 2020-89.

10. Oakbrook Land Holdings v. Commissioner, 28 F.4th 700 (6th Cir. 2022) aff’g 154 T.C. 180 (2020).

11. Oakbrook Land Holdings, LLC v. Commissioner, Petition for Writ of Certiorari, S. Ct. No. 22-323 (Oct. 4, 2022). “Brief for the Respondent in Opposition” filed December 7, 2022. Petition denied: 598 U.S. _____ (Jan. 10, 2023).

12. Oakbrook v. Commissioner, 154 T.C. 180 (2020).

13. “… these amendments have never suggested any disagreement with the construction of the statute that Treasury adopted in section 1.170A-14(g)(6), Income Tax Regs. This ‘strongly suggests that * * * [Congress] did not view Treasury’s construction * * * as unreasonable or contrary to the law’s purpose.”

14. Reg. §1.170A-14(g)(6).

15. Consolidated Appropriations Act, 2023 (H.R. 2617)(Dec. 29, 2022).

16. Oakbrook, 154 T.C. 180 *230.

17. Oakbrook Land Holdings, LLC, supra.

18. Hewitt, supra.

19. Consolidated Appropriations Act, 2023, supra.

WINTER 2023 19 eReport

New Proposed Regulations Would Affect the Taxation of US Real Estate for Foreign Investors

By: Nickolas Gianou, Victor Hollender, David Polster and Sarah Beth Rizzo1

By: Nickolas Gianou, Victor Hollender, David Polster and Sarah Beth Rizzo1

This article discusses the Treasury Department’s recent release of a set of proposed regulations that, if finalized, would alter key rules affecting many real estate funds, sovereign wealth funds and other foreign investors in U.S. real estate.

On December 28, 2022, the Treasury Department released a set of proposed regulations that, if finalized, would alter key rules affecting many real estate funds, sovereign wealth funds and other foreign investors in U.S. real estate.1 The proposed regulations are likely to be met with a mixed reception from market participants. On the one hand, the regulations provide a helpful rule that would give foreign government investors increased flexibility in structuring their investments. On the other hand, they contain a controversial new rule for determining whether a real estate investment trust (REIT) is “domestically controlled,” threatening to disrupt the tax planning of many real estate funds, private equity funds,

real estate joint venture (JV) participants and other non-U.S. investors in U.S. real estate.

Background

The Foreign Investment in Real Property Tax Act of 1980 (FIRPTA), contained principally in Section 897 of the Internal Revenue Code (the Code), created an important exception to the general rule that a foreign investor is not subject to U.S. taxation on capital gains. Under FIRPTA, a foreign investor that recognizes gain on a “United States real property interest” (USRPI) is subject to tax on that gain at regular U.S. tax rates as if they were a U.S. person. The term USRPI includes direct interests in real property as well as equity interests in a domestic “U.S. real property holding corporation” (USRPHC). The term USRPHC generally includes any corporation if a majority of its assets consists of USRPIs. A foreign corporation may be a USRPHC if it meets the asset test (though interests in the foreign USRPHC will generally be treated as USRPIs only for purposes of determining whether an owner of such interests is itself a USRPHC).

Importantly, equity interests in a “domestically controlled REIT” are not USRPIs, regardless of the quantum of real estate owned by the REIT. Thus, a foreign investor generally may sell shares in a domestically controlled REIT without being subject to U.S. taxation. If, on the other hand, the REIT ceased to be domestically controlled, a foreign investor would generally be subject to full U.S. taxation on any gain from selling the REIT’s stock.

A REIT is domestically controlled if less than 50% of its stock is held “directly or indirectly” by foreign persons at all times during a testing period (generally, the five-year period pre -

WINTER 2023 20 eReport

ceding the sale of the REIT’s stock). The Code and existing regulations generally do not specify what “indirect” ownership encompasses for this purpose and, in particular, whether and to what extent a REIT must look through a domestic C corporation to the C corporation’s shareholders. For example, if 60% of a REIT is owned by a domestic corporation but the corporation’s shareholders are entirely foreign, is the REIT domestically controlled because the majority of its stock is held directly by a U.S. corporation, or is it foreign controlled because foreign shareholders of the U.S. corporation indirectly own more than 50% of the REIT?

Although the answer is not explicit in the Code or current regulations, it appears that taxpayers are not required to look through domestic corporations under current law. This interpretation is supported by the current regulations, which state that for purposes of determining domestic control, the “the actual owners of stock, as determined under [Treasury Regulation Section] 1.857-8, must be taken into account.” Importantly, under Treasury Regulation Section 1.857-8, the “actual owner” of REIT stock is the person who is required to include the dividends on that REIT stock in their income, which, in the case of REIT stock owned by a domestic corporation, would be only the corporation itself and not the corporation’s shareholders.

Moreover, in the Protecting Americans From Tax Hikes (PATH) Act of 2015, Congress expressly included certain look-through (and modified look-through) rules for REIT stock that is held by an upper-tier REIT, but those rules do not apply to regular C corporations. The clear implication of the PATH Act rules is that Congress did not intend similar rules to apply to regular C corporations. For these reasons, most practitioners believe that current law does not require look-through of domestic corporations. Indeed, even before the PATH Act, the Internal Revenue Service (IRS) concluded as much in Private Letter Ruling 200923001.

The general FIRPTA rules described above are modified for entities that qualify as “foreign governments” under Section 892 of the Code. Such an entity is generally exempt from U.S. taxation on income from investments in securities, including, in general, stock of a USRPHC, whether or not the USRPHC is a domestically controlled REIT. The Section 892 exception does not, however, apply if either the foreign government investor or the USRPHC in whose stock it has invested is a “controlled commercial entity” of the foreign government.

A “controlled commercial entity” is, in general, any entity that is both engaged in “commercial activities” (which includes most business or profit-making activities other than investments in securities) and is “controlled” by the foreign government.2 Thus, if the foreign government investor is itself engaged in commercial activity, it will generally not qualify for the Section 892 exemption on any of its investments, and even if it is not so engaged, the exemption will not apply to income or gain recognized from a USRPHC or other

corporation that is engaged in commercial activity and that the foreign government investor controls.

Existing temporary regulations provide that an entity will be deemed to be engaged in commercial activities if it is a USRPHC. Thus, if a sufficient portion of a foreign government investor’s assets consists of stock of USRPHCs that are not domestically controlled REITs, it would lose its Section 892 exemption even though its only activity is investing in securities (which otherwise does not constitute commercial activity).

New Proposed Regulations

Section 892: Deemed Commercial Activity