COVID-19: A Litmus Test for Private Lenders’ COMMON MISTAKES When Brokering a Loan THE OFFICIAL MAGAZINE OF GERACI AUGUST 2020 Eric Abramovich Roc 360 HOW DEFERMENT of Mortgage Payments May Affect Borrowers CULTURE CORNER SHARESTATES INSIDE: RECENT ILLINOIS DECISION Could Have Sweeping Impact on Force Majeure Interpretation

August 2020 Originate Report 3 AUGUST 2020 CONTENTS 6 12 16 20 28 Who To Know 6 Eric Abramovich, Roc360 By

Peckman, Contributing Writer 12 Wisdom From The CEO By

Founder & CEO of Toorak

20 Industry Spotlight By

Golhar, CEO & President of Abhi Speaks, LLC Features 16 Culture Corner: Sharestates By Originate Report Staff 24 COVID-19: A Litmus Test of Private Lenders’ Self-Regulation Capability By Kat Hungerford, American Association of Private Lenders 28 Common Mistakes When Brokering a Loan to Rodeo By

Sarah Epstein, Rodeo Lending 32 How Deferment of Mortgage Payments May Affect Borrowers in the Long Run By Edward Brown, Pacific Private Money 34 Recent Illinois Decision Could Have Sweeping Impact on Force Majeure Interpretation by Darlene Hernandez, Esq., Geraci LLC In Every Issue 38 Lender Directory

Charles

John Beacham,

Capital Partners

Abhi

Marc Rabkin and

4 2020 WE’RE GOING VIRTUAL! We hear YOU . We understand your needs in this ever-changing industry. We asked, pivoted, and are now ready to provide you connections, education, and fun – VIRTUALLY. Stay tuned for more details! Networking & Education For More Information: Alicia Carter • (949) 379-2600 • a.carter@geracillp.com • https://geracicon.com/ SAVE THE DATE September 22, 2020 COMING SOON!

CEO

ANTHONY GERACI, ESQ.

a.geraci@geracillp.com

Senior Vice President, Marketing and Media

LESLEY BOYD

l.boyd@geracillp.com

Vice President of Geraci Media

RUBY KEYS

r.keys@geracillp.com

Lead Graphic Designer

LYNDA HIGHT

l.hight@geracillp.com

CONTRIBUTORS

Eric Abramovich • John Beacham

Abhi Golhar • Kat Hungerford

Marc Rabkin • Sarah Epstein

Edward Brown • Darlene Hernandez, Esq.

FOUNDING UNDERWRITERS

MARK HANF

President, Pacific Private Money

ORIGINATE WEBSITE

https://originate.report

GERACI LAW FIRM

https://geracilawfirm.com

MEDIA WEBSITE

https://geracimediagroup.com

CONFERENCE WEBSITE

https://geracicon.com

Welcome to the August Edition of Originate Report!

The ability to pivot and adapt to changing times is the signature of success in this industry and Roc360 has built their business upon this ideal.

In this edition, we cover the story of Eric Abramovich and his journey with Roc360 , a leading financial service platform for residential real estate investors. A group of professionals who have been working together for over 20 years make the core of Roc360, which is one of the main reasons for their success to date.

At the core of Roc's values lies a data-driven and risk-minded cognizance and the early adoption of new market trends. The entire Roc team takes great pride in managing risk and making sure that the leverage stays low. While 2020 has been a challenging year, Roc has embraced the obstacles they’ve been handed and have used this to their advantage. Though Roc360 had to go through an initial adjustment period, Abramovich said that he is proud of his team's ability to adapt to a lessthan-desirable atmosphere and is excited to see where this journey will lead them in the upcoming months.

In the words of Albert Einstein, “In the middle of difficulty lies opportunity”. While the world we are living in continues to create a unique set of obstacles in our industry, your ability to cater to the current needs of your clients will create opportunities you never knew existed.

Till next month…

Letter from the Editor Lesley

Lesley Boyd Senior Vice President, Marketing & Media

August 2020 Originate Report 5

www.originate.report

Eric Abramovich Roc360

By Charles Peckman, Contributing Writer

Roc360, a financial service platform for residential real estate investors, knows a thing or two about the intricacies of the often cantankerous housing market. The group's vision is simple, yet incredibly complex: to be the most innovative, trusted, and disci-

plined financial services platform in the space.

At the core of Roc360, which has offices that overlook New York City's Central Park, is a group of professionals who have been working together for over 20 years. The group's

co-founder and chief credit officer, Eric Abramovich, sat down with Originate Report to discuss the company's re-branding, the ins and outs of navigating the financial crises, and the impact the 2019 Novel Coronavirus has had on lending.

Abramovich, who studied finance and actuarial science at the NYU Stern School of Business, said that he has always been a "quantitatively inclined kind of person." While in school, Eric had the opportunity to work part-time with Deutsche Bank, which served as an introduction to the "fascinating world" of finance.

"I was a finance major so it's not like [the opportunity to work at Deutsche Bank] came completely by

6

PROFILE

Eric Abramovich, Co-Founder and Chief Credit Officer Roc360

chance, but it felt like it," he said. "At that time, it certainly felt that way. I got into one of the most successful groups within Deutsche Bank, an equity prop trading group. They were managing the bank's money and they were buying and selling stocks – the strategy was a quantitative equity long/short strategy."

This strategy, he explained, involved buying one stock and selling a similar, corresponding stock to hedge. This, in turn, created a market-neutral position. All of this was transpiring while Eric was still in school, which he said often felt bizarre (being a teenager, that is, surrounded by billions in capital in Midtown Manhattan.)

"I learned on the ground, at that time, the importance of bringing a data-driven mindset to the work I was doing. I was helping traders with their portfolios, doing operational work, and I learned to program as well," he said. "I learned how to build models and program up all sorts of processes and strategies and once I graduated, that led to a full-time position with Deutsche Bank. The cool thing was that I was a young kid who was quickly trusted with hundreds of millions of dollars in capital. When I look back on that now I say to myself 'Wow, I was just a kid, what were they thinking?' But it was an invaluable experience for which I will be forever grateful."

Deutsche Bank was also where he met the co-founders of Roc360, Arvind Raghunathan, CEO and Maksim Stavinsky, COO. Raghunathan, who has a PhD in computer science from UC Berkeley, was Abramovich's manager at Deutsche Bank He added that the quantitative, data-driven environment in his group was fueled by the 'incredibly bright people working alongside him. Within a few years of working with the group, Eric had established a Tokyo office for his division and was working back and forth between Japan and London.

Although the team was doing very well at Deutsche Bank, the oft-forgot 'quant crisis of 2007,' paired with the housing crash led to the next chapter in the foundation of Roc Capital.

was the banks were no longer allowed to take massive risks and what spun out of that was Roc Capital, or what I like to call Roc 1.0. In 2009, when we first launched, we were the world's largest hedge fund launch of that year, raising $1.3 billion in an acutely challenging fund-raising environment. We were able to do that while the world was going to hell, and partly due to our track-record of risk-control and preservation of investor capital. "

Initially, Abramovich said Roc 1.0 had tremendous success and raised large amounts of capital, but in the post-crash quantitative easing fueled environment Roc was growing up in, it was difficult for most quantitative strategies to maintain returns. This led the partners to return investor capital with most investors exiting with flattish or positive returns and subsequently to a period of self-reflection and transformation within the core group, which materialized into what Abramovich proudly refers to as 'Roc 2.0.’

"While we were working on Roc 1.0, Maksim and I started making investments in fix-and-flip properties. We came to understand how our borrowers go about their business today," he said. "We were investing with our own money – buying distressed properties and flipping them – we were doing that on the side, and that was making a lot of money while the returns of the equity trading strategies were diminishing. At some point, I think you realize that if something is not working, it must

"Not even two years after the quant quake came the housing crash," he said. "Essentially, what happened Eric Abramovich: Continues on pg. 8

August 2020 Originate Report 7

Eric Abramovich: Continued from pg. 7

be time to move on. We then formed Roc Capital 2.0, and although it retained a similar name to the original company, we were doing completely different things and it was actually an entirely new company."

The way the opportunity for Roc 2.0 was presented to Abramovich and his partners came by the way of reviewing portfolios of non-performing loans. In 2012, in the direct aftermath of the housing bubble, Abramovich said that there was still a considerable amount of distressed inventory; this exploration led them to what is referred to as the private lending industry today but was then called hard money lending and was often viewed through a negative lens at the time.

"When I first started calling these professionals, I had no idea of the scale of hard money lending, but I was soon acquainted with some lenders that were originating over $100 million in loans per year and yet these groups were still relatively unsophisticated on the capital raise side," he said. "The investors were using the borrowed funds and buying all of the inventory that was stuck in the aftermath of the crash. They bought the properties to fix them up and resell them. What I thought at the time was 'how big could this opportunity be if I could aggregate 100 of these lenders?'"

vate lenders in the Roc family. An important ingredient in this continued expansion, he added, was Roc's status as an early adaptor to the post-crash finance world.

"At that time, no one else was really getting involved in lending against repurposing of distressed property in an institutional way," he reiterated. "Many people still viewed the loans as risky and there was a negative connotation attached to 'fix-nflip.' The housing market was viewed as risky as well, and when I started going to conferences there was hardly any competition at all."

Even though Roc was one of the only players in the space at that time, Abramovich added that the initial mindset – that of perseverance, due-diligence, risk mitigation, and providing value for customers – is something that continues to this day. He also said that some groups tend to get caught up in their status as a 'first mover' in any given space, and that initial confidence creates an atmosphere of cockiness that reduces long-term brand value. At Roc, Eric said the group continues to offer the best product at the most competitive rates.

It comes as no surprise that 2020 has been difficult for business owners of every stripe; after all, the 2019 Novel Coronavirus has left millions unemployed. Though Roc360 had to go through an initial adjustment period, Abramovich said that he is proud of his team's ability to adapt to a less-than-desirable atmosphere.

"The coronavirus is unique in terms of a financial crisis," he said. "Every crisis has its own unique features, and we knew that some sort of crisis was coming. Did we predict a pandemic would spread across the world? No, not at all. That being said, we did predict that a crisis would happen, absolutely. We were able to keep the lights on, we had a disaster recovery plan, and everyone was able to work from home. We are a capital provider to private lenders, and the most important thing is to actually provide your clients with the liquidity to keep lending, not to shut down lending. That's what differentiated us from our competitors during the crisis."

Since this initial aggregation, Abramovich said that the platform has since expanded to over 400pri-

At the core of Roc's values, he said, lies a data-driven and risk-minded cognizance. In addition to the early adoption of market trends, he added that a quantitative background has bolstered Roc360's bottom line. The entire Roc team takes great pride in managing risk and making sure that leverage stays low.

Although Eric said the business has not been impacted operationally, he added that some precautionary measures, such as installing plexiglass barriers at the office, are attributes of management he never thought he would have to think about.

"We've adjusted and I think we'll certainly be coming back to our office with a renewed thankfulness for working in an office! All kidding aside, I think we were able to quickly adjust and get in the rhythm of things," he said. "And we are help-

8

ing people rebuild their businesses today – a lot of our clients, their lending volumes went down to almost zero. In March, even the fact that you could provide capital did not mean that clients were actually transacting. The way our business is coming back now, though, is truly remarkable."

What is also remarkable, Abramovich said, is Roc’s ability to manage a rebrand during a historic pandemic. Seeking to do more than just provide capital to the space, Roc rebranded as Roc360 in January of 2020. The new name communicates the firm’s offerings as a full life cycle platform for real estate investors and accompanies the broadening of Roc360’s suite of products and services. Today there are several subsidiaries under the Roc360 umbrella which collectively seek to simplify a day in the life of a real estate investor. There is the flagship Roc Capital, capital provider to private lenders, which has successfully lent close to $3 billion to real estate investors and developers. There is also Elmsure, an insurance subsidiary which has bound close to $1 billion in builder’s risk and other real estate related coverages. Roc’s newly formed title insurance agency is called Wimba Title. Roc has also created a lead generation and matching platform called Haus Lending.

"This rebranding is a relatively new endeavor, but you know, Roc Capital is a capital provider to private lenders, but we wanted to be more than just capital for the real estate industry," he said. "We have much bigger and grander plans, and we

really seek to be top of mind for all things residential real estate related. To that end, we started an insurance company called ElmSure and a customized product to serve residential real estate investors offered through the Berkshire Hathaway Group. When you buy a property you need to im-

mediately insure it and make sure you're safe against all the events that can occur like floods, hurricanes, and things like that. To a certain extent, we're very neurotic and risk-minded."

August 2020 Originate Report 9

Eric Abramovich: Continues on pg. 10

Partners Roc360

Eric Abramovich, Co-Founder and Chief Credit Officer Roc360

This neuroticism, he said, does not come from a place of unnecessary anxiety. When working on a property, a seemingly small pitfall could have massive implications on developments. An important aspect of being a full-service partner, he added, is keeping this inherent risk in mind.

"Roc360 is the platform around which we are building all of these divisions," he said. "Our visions, of course, go much deeper than insurance – right now we're starting a collaborative venture with Home Depot, where Roc borrowers will

the ground?' I've done it many times over my career so far, like with starting a trading business in Tokyo, and the house flipping, and we've done it at Roc360 too with our strategic partnership with Home Depot," he said. "We find a problem and look for a solution."

One such problem-turned-solution began in 2016-2017 when Wall Street began realizing the opportunity of private lending, Eric said. As more players began pumping institutional capital into residential real estate investments, Eric added that it was more important than ever to differentiate Roc from the rest of the

ue lending and severely constrained on a forward-looking basis."

While some lenders are feeling the heat of a disjointed marketplace, Eric said the Roc360 team has used the pandemic as an opportunity to sharpen their pencils, raise even more committed capital, and start additional strategies and business lines. More important than this, however, is Roc's commitment to maintaining the lion’s share of the team when many have had drastic headcount reductions.

have access to subsidized material pricing as a result of the pooled buying potential of Roc’s clients …we're excited about this growth, and we're excited about what this means for our clients."

Before any opportunity is pursued, however, Eric said copious amounts of research is conducted.

"Once we [assess] an opportunity from the top down, we go to the ground level. I think that's how any opportunity should be looked at –you have the total size of the market and you have to figure out 'how do I get this done in terms of boots on

pack. Although some of these competitors enjoyed early success, their business strategy did not partner well with the coronavirus pandemic.

"Some of our competitors have been severely dislocated by COVID-19," Eric said. "When you look at Wall Street, and some of the groups who have come into the space in the last few years, the mistake there is that the capital starts chasing the opportunity, and then the opportunity zone becomes tighter and tighter. Ultimately leverage is what fuels these binges, but when a crisis comes seemingly out of nowhere, leverage really bites. Margin calls have left many levered plays unable to contin-

"We really tried very hard to maintain full employment even as lending volumes plummeted in March," he said. "Now as things recover, we’re very thankful that we were able to do so. Indeed, we decided to not let a crisis go to waste and are now back in hiring mode. You have to re-intensify your focus and obviously see if the things you were doing make sense in a post-COVID world. From my standpoint, I think the things we are doing now still make sense. Even though we are intensifying our focus, that doesn't mean that we've had to dramatically shift our course of action in any of the sectors we're involved in."

Eric said he fully understands that many people on Main Street are feeling the strain of the coronavirus right now, but eventually the housing market, the country, and the world will return to a state of normalcy. Even though his day-to-day activities as a co-founder of Roc360 have not changed during the pandemic, he said that the work-fromhome time has allowed him to revisit

10

9

Eric Abramovich: Continued from pg.

"At the core of Roc360, which has offices that overlook New York City's Central Park, is a group of professionals who have been working together for over 20 years."

a regret he has from childhood: not practicing the piano enough.

"I didn't practice as much as I should when I was a kid, and I'm telling my kids that now," he said. "I have been re-learning some pieces and picking up where I left off. And certainly, I’m not focused on classical music anymore! With so many apps out there now, it's so much easier to learn."

Moving forward, Eric said he is looking forward to returning to the of-

fice, catching up with colleagues in the 'post-COVID' world. As for Roc360? Eric said he is confident in the group's ability to continually innovate and change the private lending space and the world of real estate investing.

"I think, looking back over my career so far, I am incredibly proud of the work we have done at Roc360," he said. "I've been working with the co-founders for years and there is a

LOOK WHO’S HIRING!

Looking to fill a position? Advertise it here in Originate Report’s Industry Jobs to get it in front of thousands of qualified candidates. Contact us at (949) 629-3961.

synergy there that you'll have a hard time finding at other outfits. I can't wait to see what we do as Roc360 continues to act as an innovator for residential real estate investors."

To learn more about the products and services offered by Roc360, visit roc360.com

Eric Abramovich Co-Founder and Chief Credit Officer Roc360 https://roc360.com

Eric Abramovich Co-Founder and Chief Credit Officer Roc360 https://roc360.com

Fidelity Mortgage Lenders, Inc. has been funding real estate loans in Southern California since 1971.

Founded as Fidelity Home Loan Co. Inc., we originally specialized in residential equity loans, and later expanded in to commercial lending. We make loans on both commercial and residential properties in the state of California, providing first trust deeds, refinances, and/or purchases.

Now in our fifth decade, Fidelity Mortgage provides loans to borrowers which larger institutions are unable to fund. We grew by responding to the needs of a changing real estate marketplace while serving a growing community of property owners and investors.

Our reputation for fairness and reliability brings us referrals from our borrowers and other professionals. As a result, we service a network of real estate brokers, attorneys, accountants and business managers who seek our professional help for their clients. All of our combined departments work together to completely service loans. From loan advisers to escrow officers to loan servicing, there is only one goal… our clients’ total satisfaction.

The Role:

We are seeking a candidate with knowledge of commercial lending to be part of our loan servicing team.

Responsibilities:

• Service Loans

- Monthly payments processed and scanned

- Monthly check to investors

• Collections

- Track and file late notices

- Read fees and statements, and conduct appropriate follow-ups

- Use judgement to escalate concerns to immediate Manager or to the Company’s Chief Operating Officer

• Insurance

- Read and understand Property Fire Insurance

- Track insurance notifications

- Monitor requisite insurance on properties

- Communicate to investors and property owners

• Customer Service with Investors and Borrowers

- Answer general questions, and display problem-solving skills

• Knowledge “The Mortgage Office*” loan servicing software system

Qualifications:

• ~3 years Real Estate Loan Service Specialist

• Knowledge “The Mortgage Office” loan servicing software system

• Familiarity with foreclosures

• People skills and rapport with borrowers, customers

• Computer skills: proficient in Word, Outlook and excel

• Able to manage multiple projects, deliverables, milestones, and schedule

August 2020 Originate Report 11

INDUSTRY JOB WATCH

John Beacham

Founder & CEO of Toorak Capital Partners

12

WISDOM FROM THE CEO

Can you explain a time where you faced adversity or had struggles early on in your career? How did these experiences mold and shape you into the leader you are today?

After college, I worked in investment banking at Credit Suisse First Boston in New York. After a few years, I was offered the opportunity to work in the firm’s in Melbourne, Australia office. This was the first time I lived abroad in a country where I didn’t know anyone. I left my comfort zone, advanced my career and fell in love with the country. I lived in the area

outside Melbourne called ‘Toorak,’ which is incredibly beautiful.

What did you do in the beginning of starting your business? What risks did you have to take and how did you have the courage to continue to push forward?

After I left B2R, I decided I wanted to create a new company and fund. Naturally, the first step was to go out and raise money. So, I developed a pitch-book with my 10 best investment ideas. When I presented the ideas before potential investors and

didn’t find success, I wasn’t dissuaded. I actually realized that I didn’t need 10 ideas, I only needed one great idea. Four years later, the best of those initial ten ideas, that of introducing institutional capital to the bridge lending industry has proven successful. The moral of the story here is that, you only have to pick one unique thing and become the best at it. This strategy focuses your attention and sets you up to be an expert.

What habits, mindset, or perspective have helped you succeed as a business owner?

It is important to understand your customer. I’ve found that the best question to ask is ‘what can we do better?’ Seeking real feedback is critical.

What excites you about your role as CEO currently today?

I am proud to lead my team of more than 50 colleagues who are committed to upholding the highest lending standards, while providing the capital necessary to address American’s housing shortage. As the firm grows, the construction we fund reinvigorates low-income communities by providing new housing stock and additional employment opportunities. It is exciting to play an important part to address the nation’s housing crisis.

What has been your favorite aspect of being an entrepreneur over the years?

Starting my own firm two-times over has been incredibly rewarding. Today, I am grateful to the investors

August 2020 Originate Report 13

John Beacham, Founder & CEO Toorak Capital Partners

John Beacham: Cont. on pg.

14

who entrust Toorak to serve as responsible stewards of their capital.

What piece of advice do you have to share with other entrepreneurs and CEO’s that are in the early stages of building their company?

Echoing what I said earlier, the key is to find something that’s you’re the best at and differentiated on. You can’t follow the herd and do what 100 other people would do, or else you won’t be able to scale and be successful.

What activities or resources would you recommend other entrepreneurs to invest their time in?

Invest in your company.

How do you make sure your company stays ahead in this industry?

The pandemic had a massive impact on our industry and demonstrated that industry-leading companies needed to be adaptable to stay ahead. For example, at Toorak, we temporarily increased our focus on asset management so that we could best serve our customer and our borrowers. Ultimately, we remain focused on credit, customers and delivering for our customers.

Who is someone that has had a significant effect on your career and why?

Dan Pieterzak and I worked together at Deutsche Bank earlier in our careers. We have a great working relationship and I appreciate that

as he selected to support Toorak in 2016. Today he sits on the Board of Directors at Toorak.

Is there anything that you wish you could go back and tell yourself at the inception of your company?

The market opportunity is bigger than we expected.

What tools do you use to aid you in your role as CEO to be most efficient, organized, and focused?

Technology keeps me hyper-connected with my team internally and externally with Toorak’s stakeholder network that includes borrowers, lenders, originators and investors.

John Beacham Founder & CEO

Capital Partners

14

Toorak

https://toorakcapital.com

John Beacham: Cont. from pg. 13

Jasen Portero as Chief Operations Officer

LONG BEACH, Calif., May 5, 2020 - Applied Business Software, Inc., (“ABS”), leader in loan servicing and origination software in the private lending space, announced today that Jasen Portero, its current Vice President of Development for the last 12 years, has been appointed Chief Operations Officer.

As a Full Stack Developer, Jasen oversees the Development Department, manages all online services, and spearheads all new projects. As VP of Development he has created a multitude of Front-End Service capabilities: iPad app, electronic signature, online loan application and borrower portal, text notifications, loan geo-mapping, API, and the first fully browser based version of The Loan Office® servicing software. As a Chief Operations Officer he will be extending the online services and will oversee development of both products, The Mortgage Office® and the Loan Office®. Prior to joining ABS, Jasen spent 18 years working for Universal Music Group, WellPoint, Warner Bros., and Evite where he took part in developing some of the technology people around the world have come to use and love.

“I am honored and humbled to take on this new role and take ABS to a new level. Our software is a testament to hard work, excellence in coding, and continuous innovation. ABS as a trusted brand is experiencing incredible growth, and I am excited to be a part of it and take the company to the next phase.”, said Jasen Portero.

“Since joining in 2008, Jasen has been instrumental in our growth. He is an excellent addition to our senior management team and will play a critical role in ABS’ future product development strategy. His proven track record and ability to build a winning team are a great combination for what lies ahead”, said Carlos Nodarse, ABS’ CEO.

About Applied Business Software

Applied Business Software is a market leader and global provider of software systems and solutions to the lending industry. ABS offers a complete suite of software products designed from the ground up to specifically address the needs of those who originate and service loans. All our products are consistently rated superior in design, system interface, expandability, and ease of use. ABS is based in Long Beach, California. For additional information about ABS’s products and services, visit https://themortgageoffice.com or call (800) 833-3343.

August 2020 Originate Report 15 ABS Appoints

Elizabeth Morales, Chief Marketing Officer https://themortgageoffice.com | (800) 833-3343 | elizabeth@absnetwork.com PRESS RELEASE

SHARESTATES A Fun-Loving Family

By Originate Report Staff

The culture at Sharestates, a real estate crowdfunding platform based in Great Neck, N.Y., is best described as a fun-loving, family environment. The Sharestates team is tight-knit and values kindness, respect, commitment, and a dose of good humor.

After two years of building a network of investors and borrowers, co-founders Allen Shayanfekr, Radni Davoodi, and Raymond Davoodi officially launched the Sharestates platform in February 2015. In the five years since, Sharestates has grown into a powerhouse lending

platform that has closed over 2,800 loans worth 2.5 billion.

Behind this growth is a dedicated team who have kept the Sharestates values of kindness, respect, and commitment alive since day one. Rooted in the idea of family, the team val-

16

CULTURE CORNER

ues quality time over shared meals. Sharestates employees take part in everything from informal birthday lunches to monthly team outings and barbecues. The love of food and a shared meal is a small but important part of creating a sense of family at Sharestates.

Within this work family, Sharestates is committed to upholding diversity and inclusion as central to its culture. It demonstrates this commitment by hiring a diverse staff and creating a dynamic, respectful environment where every team member feels empowered to share their ideas. And,

as a team that loves to break bread together, Sharestates employees are encouraged to celebrate their cultural backgrounds through food at company potluck dinners.

This positive team culture is reinforced by giving back to the community together. For example, last year, Sharestates raised $100,000 for children in need at its annual charity poker tournament benefiting Share4Kids. This year, in lieu of in-person fundraising, employees have been working to give back to essential workers battling the COVID-19 pandemic on the front-

lines. Employees switched gears from crowdfunding real estate deals to crowdfunding donations to feed workers at local hospitals.

In addition to adapting its fundraising efforts, the team continues to stay close during the pandemic with virtual happy hours and trivia nights. Sharestates’ leadership believes the closeness of its team is fundamental to the success of the company. Its unique culture enables employees to not just love what they do, but also love their job and take pride in where they work.

Sharestates: Continues on pg. 18

August 2020 Originate Report 17

Sharestates Holiday Party

Sharestates: Continued from pg. 17

Sharestates

Sharestates

Sharestates Mets Game Outing

Sharestates Mets Game Outing

18

St.

Charity

1B Milestone

Halloween

Corona Food Donations

Marys Big Hearts

Walk Sharestates

Sharestates

Sharestates

Birthdays

Connect With Us: https://sharestates.com

August 2020 Originate Report 19

Sharestates Mets Game Outing

Sharestates 1B Milestone

Sharestates Charity Poker Tournament

Sharestates Halloween

Sharestates BBQ

INDUSTRY SPOTLIGHT Abhi Golhar

CEO of Abhi Speaks, LLC

SPOTLIGHT SPOTLIGHT

How has your outlook on the private lending industry changed in light of the new normal?

It’s clear that short-term lending practices have changed. And the impact of COVID-19 long-term? Noone knows. The truth is - staying in the game, in front of your audience/ potential clients, and implementing stringent underwriting is more important now than ever.

What are you doing differently today to move your company forward than you were 6 months ago?

I’m getting aggressive building out custom technology and dashboards

to help sort through opportunities so I can make smarter decisions on already-filtered borrowers. My algorithms (with a built-in robo-advisor) automatically match borrowers with my lending criteria.

How has your company evolved since its inception? (ie: new products, new divisions, grown, merged, etc?)

New relationships with capital partners give us the ability to expand our offerings and with smarter, more streamlined technology, we can become a quicker and smarter conduit of opportunities for the right capital partner.

What is something most people don’t know about your company?

I’m a geek that works with other geeks. We love real estate and lending, but geek out on building smarter AI algorithms and decision trees for our platform to help us and our partners make more informed decisions.

What has been the highlight so far in your career?

Realizing my technical expertise can be used to help private lenders streamline their processes and build and integrate smarter dashboards and technology to enhance borrower experience and make smarter, automated decisions.

What advice would you give to your younger self?

Fail hard earlier, network more, and build a business, not a job. Too often as an entrepreneur, I’ve found myself serving my business more than the business serves me. Flipping the script on this is crucial; life is meant to be lived, not done.

What piece of advice did you personally receive early in your career that has helped shaped the decisions you’ve made?

If you do your homework and help others master the material, you’ll get an A. It’s always worked, especially in business.

Tell us about a person or organization you admire. How have they made an important impact on you, the industry, or the world?

I’m a HUGE fan of Big Brothers Big Sisters. It’s a constant reminder we

August 2020 Originate Report 21

Abhi Golhar CEO of Abhi Speaks, LLC

22

Abhi Golhar : Continues on pg.

need each other to grow and learn on this journey of life, and sometimes a little boost can go a long way.

How have you turned a career mistake or failure into success in your career?

As a cautiously optimistic investor, I can’t stand a high margin of error with renovation budgets. One of my biggest mistakes early in my career was trusting the wrong contractor and not creating enough buffer in my renovation budget to see my rehab in Detroit through to the finish line. So instead, I aggregated local data (cost of materials, labor, etc) and created a series of IF/THEN statements to help me determine if a contractor was lying to me. Needless to say, I trusted the software I build to help

me make smarter decisions and apply that skill even today.

What do you predict for the future in private lending throughout the end of this year and beyond?

Predictions:

COVID-19 vaccine available Q3 2021. Regular surges of COVID-19 until a vaccine is ready will continue to damper lending with a lessening impact with each wave.

Lenders that get creative to find short-term opportunities with marketing strategies (e.g. Noble Capital) to cultivate and nurture borrowers will win the game.

Lenders with strong risk management processes will be resilient allowing a bigger cushion from conservative assumptions on the loan amount to property value.

Post COVID-19, conservative underwriting will beat aggressive underwriting any day.

If you had a clean slate to start over and do anything you wanted to do, what would that be?

Exactly what I’m doing today - helping companies grow and scale with a human-centric lens.

How do you want to be remembered? What have you done to cultivate that feeling from others?

I want to be remembered as the quirky nationally syndicated radio host turned podcaster with an affinity for all things business and media with an extreme focus on family, living life to his fullest, and helping others.

Abhi Golhar CEO of Abhi Speaks, LLC abhi@abhigolhar.com https://abhigolhar.com

22

Abhi Golhar : Continued from pg. 21

August 2020 Originate Report 23 Private Money Loan Servicing Software Powerful, Flexible and Easy to Use! Borrower and Investor Text Alerts (800) 833-3343 www.TheMortgageOffice.com Applied Business Software, Inc. 2847 Gundry Avenue, Long Beach, CA 90755 sales@absnetwork.com Online Investor Access Multi-Lender Loans Integration Mortgage Pools Online and Over The Phone Payments Enhanced Reporting and Forecasting Rehab, Commercial, Construction, HELOC, ARM RESPA Compliant Escrow Analysis The ® Your Ultimate Lending Platform

COVID-19: A Litmus Test of Private Lenders’ Self-Regulation Capability

By Kat Hungerford, American Association of Private Lenders

The private lending industry of today can trace its near-exponential growth in the past decade back to government regulation. Regulation of parallel industries, that is. Strictures that have reined in traditional institutional lending practices have largely benefited private lenders, spurring borrowers to come knocking at the door.

Private lenders have for the most part operated outside licensing and reporting requirements affecting institutional lenders by virtue of their clientele being primarily businesses transacting business-purpose loans secured by dwellings, rather than consumers looking for traditional mortgages. Today, only 11 states require a mortgage license

to transact these loans, with federal regulation being limited to a few (albeit still burdensome) disclosure and reporting requirements. Private lenders have for the most part operated outside licensing and reporting requirements affecting institutional lenders by virtue of their clientele being primarily businesses transacting business-purpose loans secured

24

GUIDE TO NAVIGATING PRIVATE LENDING BY AAPL

by non-owner-occupied dwellings, rather than consumers looking for traditional mortgages on a primary residence.

tate Settlement Procedures Act). The latter exempts private lenders where the former does not.

Whether state or federal, most recent regulation impacting private lenders seems almost accidental, effected through vague wording like “lien on a dwelling” (Equal Credit Opportunity Act and Home Mortgage Disclosure Act) instead of the more widely adopted “credit offered or extended to a consumer primarily for personal, family, or household purposes”

(Truth in Lending Act and Real Es-

The past several years have only seen one state – Florida – attempt to change that status quo to purposefully regulate private lenders. The bills did not pass, or were passed without the regulating language, as a result of advocacy efforts from the American Association of Private Lenders and its general counsel, Geraci LLP.

This is not to say that private lenders are completely unregulated. They must still comply with anti-usury,

anti-discrimination, fair advertising, loan servicing, foreclosure laws and more. Speaking of the private lending industry as “largely unregulated” applies in the context of comparison with institutional lending and other financial industries.

The regulation gap between private and institutional lending is not only what has allowed private lending to grow, but to exist as a recognized industry at all. While large national private lenders might be able to survive regulatory hurdles, the smaller lenders that make up much of the

August 2020 Originate Report 25

AAPL: Cont. on pg. 26

industry would not: their operational costs would skyrocket as demand shrinks with fewer differentiators between “bank” and “not bank.”

Ok, we’re “largely unregulated.” What do we have to worry about?

The common answer is that as any industry grows, its practices increasingly come under the watchful eye of legislators. Private lenders need to establish and follow best practices now to be able to be able to mitigate bad actors that can become the face of the industry and a reason to regulate.

But while the soundbite makes sense, it’s still unhelpfully vague. When does the industry magically become large enough to regulate? Who is the “we” that establishes things? What “best practices” will avoid regulation? How do we stop “bad actors”?

As with much of history, it often takes a crisis to shine a light on what’s wrong. In the aftermath, government picks up the slack – often clumsily – to prevent it from happening again. While the 2007 financial crisis is a clear example of possible impacts to an industry for unwise decisions, a more immediate one is the present COVID-19 crisis.

COVID-19 is a litmus test of our ability to self-regulate.

As with pre-COVID-19, the nature of most private lenders’ business means that there is limited regulation in play. Federal foreclosure and eviction moratoriums only apply to government-backed loans from Fan-

nie Mae and Freddie Mac. And while some states enacted regulation that applies to private loans, most such moratoriums are ending soon if they haven’t already.

Court closures and local ordinances may slow down proceedings, but private lenders without federal or state considerations are under no legal obligation to extend forbearances or deferrals, or to delay foreclosure. There is also little regulation on when the missed payments from forbearance or disclosure are to be made up – allowing lenders to call the total of the deferment due when the borrower (and most of the nation) is still recovering from the crisis.

This is what is legally permissible. But following the letter of the law does not prevent future regulation should the industry come under scrutiny and it is decided private lenders profited from the crisis and/or contributed to its economic impacts.

While the American Association of Private Lenders and Geraci LLP published a Forbearance Request Guide and Request Form (available at aaplonline.com/covid19), not all private lenders will see them, and for those that do, not all will follow them. While most lenders feel a sense of “we’re all in this together” during a crisis that impacts everyone, lenders face their own resultant financial hardships, with some having to

26

AAPL: Cont. from pg. 25

weigh compassion against possibly having to shut their own doors.

The balance between legal, business, and best practice considerations is delicate, and we often don’t realize we’re failing until the crisis has passed and we’re in the post-mortem.

There is a silver lining that has or the most part kept us on the right

track: Unlike decision-makers at banks, private lenders for the most part are not so far removed from the borrower as to lose feeling for what they are going through. It’s harder to pass the buck in our industry.

If private lenders can show the help they provided to borrowers in the face of this crisis, they will have a

powerful platform from which to speak when talking to legislators about their ability to self-regulate, and the industry will be less likely to be lumped into the regulatory aftermath of COVID-19 and future issues. Where institutional lenders may fail in eyes of the public and legislators, private lenders need not. Ultimately it is our choice.

ABOUT THE AUTHOR: Kat Hungerford is executive editor of Private Lender magazine and project development manager at the American Association of Private Lenders (AAPL). Hungerford also acts as secretary for the association’s Government Relations Committee, which serves as AAPL’s advocacy arm in state and federal legislatures. Specializing in project management, marketing, and process automation, she leads the association’s many initiatives, including the launch of its member directory, conference site, online courses, and more.

AAPL is the first and largest national organization representing the private real estate and peer-to-peer lending industry. Its three core principles – Ethics, Advocacy, and Education – provide a foundation for a new generation of real estate capital. The association serves as a catalyst for industry growth by fostering awareness, promoting best practices, and encouraging a standardized code of ethics for its membership. CONTACT: https://appraisalnation.com

August 2020 Originate Report 27

Common Mistakes When Brokering a Loan to Rodeo

By Marc Rabkin and Sarah Epstein, Rodeo Lending

When originating a loan, it is not only the best pricing that lands the deal. There are so many layers to successful pricing, structuring, and closing with Rodeo Lending’s Bridge product. Rodeo Lending prides itself on funding all types of loans including those that require a complicated structure. I decided to sit down with Marc Rabkin, a loan originator who has been with Rodeo for the past 9 years. Marc started with Rodeo at the end of “The Great Recession.” As you can imagine, he has seen it all and dealt with every kind of referring broker and borrower. I have been his Loan Coordinator for the past 4 years and have seen the weird, the good, the bad, and the ugly. Marc

started as a stockbroker and became an L.O. after 2008-2009. He has a deal with literally thousands of loan brokers and knows how to help structure a loan, so what better time to pick his brain considering we are yet again facing another tumultuous time in our industry. Believe it or not, through Covid-19, as Rodeo Lending is well-capitalized and never stopped lending, Marc had the best month of his career with Rodeo. When I asked Marc how he could shed some light on the industry, it all came down to how the loan was packaged by the loan officers and brokers.

Marc Rabkin, Senior Loan Originator: Through these past 9 years, I have always conducted a “post-mortem” of every call I am on, every email

exchange, every deal I review, every deal that ends up in underwriting, and every deal that ends up being funded. What I am doing is reviewing what went right and what went wrong (whether it was with me or the other side of the communication) so that the next call I am on, the next deal I review, the next deal in underwriting; may have a greater chance of succeeding and getting to the outcome I want… which is a closed loan. We all don’t get paid unless the loan funds.

In my 9 years of working with all types, I have noticed some behaviors that tend to get in the way of a file’s success. Which brings me to “Common Mistakes When Brokering a Loan to Rodeo.”

28

FEATURE

Mistake #1 Pushing Paper

This is where the broker has not looked through the file and is not versed or aware of the deal they are sending. A classic example is when I get an email from a broker with 40 attachments and all that is written in the email is “What do you think?” What I think is if you are going to represent a borrower and try to get their deal funded, you should prepare and present a well thought out scenario. How you initially propose a deal will greatly impact getting interest from a lender and motivate them to dig deeper. That should include a synopsis of the loan that documents all the relevant information needed to make an informed decision. This makes my job easy and allows

me to present your deal to the decision-makers at Rodeo Lending, and having the benefit of an organized back story, results in a Letter Of Interest (LOI) more often than not.

Mistake #2 Broker Chains where the broker who presented is not direct with the borrower.

We have all played the game “telephone” and without a doubt, information gets lost in translation. In the case of a Broker Chain, during the loan process, the borrower and lender need to get on a call. This is to hear the story directly from the borrower, hear the borrower’s expectations directly, and for the borrower to understand the lender’s process and capabilities. This

doesn’t mean a Broker cannot be involved on that call, but it should only be the Broker running point on the transaction or the Broker directly connected to the borrower. Managing expectations is the key to getting deals funded and it’s hard to manage expectations with multiple middlemen relaying these expectations. If you are worried about poaching… get an NDA. Rodeo Lending always protects its referring brokers as they are an integral part of our business.

Mistake #3 Blasting requests to 30 lenders at a time or using the bcc function.

This is similar to the pushing paper mistake. Why is this a mistake?

Common Mistakes: Cont. on pg. 30

August 2020 Originate Report 29

Lenders know borrowers and brokers shop their deals but when I see 30 other lenders on an email my desire to even review the deal diminishes greatly. Take the time to send out individual emails to potential lenders. I can almost guarantee that your chances of finding an interested party will increase. It is not only the lender that charges the least, or where you can make the most money, it is important to know that the lender will close the deal, and not re-trade during the process.

Mistake #4 Referring Brokers Asking for Outrageous Fees.

This shows that the broker is out there looking for the home run over really trying to get the deal funded to help their clients. Borrowers’ shop; that’s a fact. Lenders will try to beat the borrower’s last quote, especially on quality loan requests. You cannot forget that we work in a competitive and relatively small space, I know this based on how many repeat deals we see. I recently had a broker ask for 3 points on a very high loan amount, in addition to Rodeo’s points. For a borrower to agree to pay a significant amount in broker fees is a red flag and will signify that there is a potential flaw in the file. Plus, isn’t it easier to get repeat business and/or referral business by realistic broker

fees vs searching and fishing for new clients? If you are looking to make a killing on every deal, I can assure you that repeat business and referrals will not occur. Building a relationship with a borrower is important, and giving great service at a fair price will help you build a great business. That is how I built my business at Rodeo Lending, along with the brokers that are willing to do the same.

Mistake #5 Broker refusing to get on a call with the lender to discuss. There comes a time when I need to get on a call with the broker to manage expectations; your clients’ requests vs. what we as the lender are willing to do. This is always easiest having an actual conversation where questions can be asked and answered right away giving opportunity for follow up questions and comments. I know I sound like the old man yelling “No jumping in the pool” or “get off my lawn” but more and more I see referring business being communicated through texting and emailing only. Texts and emails don’t always convey everything involved. To succeed in a high fee business like lending and brokering you need to have actual conversations to overcome objections, and straighten out any misconceptions if you want to get your deals funded. We are in an inhdustry of relying on and referring

to each other and you can establish trust much easier when you talk to someone. In my experience when getting on the phone with the broker and borrower and I include one of Rodeo’s principals, the closing ratio skyrockets. Taking the time to make this call will exponentially increase your chance of success.

We all have different styles and ways we conduct business. That is what makes this job interesting. The more we can interact and collaborate effectively, the faster deals get done and we can move on to the others. And obviously, there are so many other layers to getting our loans to the finish line, but hopefully, these observations will help you achieve a little more traction on your pipeline or at least give you a glimpse of a direct lenders perspective. Rodeo Lending is about closing good loans with good brokers who take the extra time and effort to truly understand the loan and present it in the most coherent way. Remember, that extra effort will help you end up with a Letter of Interest that turns into a closed loan and a happy client. The Loan originators at Rodeo Lending look forward to reviewing your scenarios and structuring deals with you, however, whatever company you present your loans to, make sure to take more time and effort to ensure success.

CONTACT: https://rodeolending.com

30

ABOUT THE AUTHOR: Marc Rabkin has been a Loan Originator with Rodeo since 2011. A graduate of the University Of Maryland's School of Business, in Marketing, he worked for various Wall Street Companies for 20 years before moving over to the Private Money space.

ABOUT THE AUTHOR: Sarah Epstein has been in the Mortgage industry since 2004 and has been the Loan Coordinator at Rodeo since 2016. After studying Communications and many years in customer service and management, her passion has always been the satisfaction of the clients.

Common Mistakes: Cont. from pg. 29

THE IMPORTANCE OF CONTENT

Webinars have grown in popularity in recent years and have become an important marketing tool. These live web-based seminars can connect you with leads from all over the world. They encourage interacti by allowing the audience to ask questions orJust how beneficial can a webinar be to your business? Here are 7 reasons why webinars are a fantastic marketing strategy. Webinars are a cost-effective way to extend your reach globally. Rather than pay for flights and hotels to meet with individual leads, you can engage with a larger group over their computer screens. People from all over the world can attend, providing your brand or product with the potential to see huge results. This global reach creates networking opportunities for building relationships and partnerships. our audience has invested time in registering and listening to the information you plan to share. They’re expecting valuable takeaways from the webinar, even something they can put into place at their own company. This positions you and your brand as an industry leader, or expert.

Webinars can give your audience the chance to ask questions and provide feedback. This is valuable because you can address concerns, reservations, or any lingering questions they may have about your training or product in real-time.

You can customize your presentation to your audience based on their questions and feedback to keep them engaged. Ask them to take an action, such as completing a task or answering a question. This will increase audience participation and interest.

Include guest speakers, such as industry leaders or affiliates, to speak during your webinar. These individuals should be familiar with your industry and value of your product. They will be able to educate the audience on the benefits or impact, validating information you have or will be sharing.

By inviting a guest speaker, you can also increase the webinar’s attendance by including your guest’s audience and following. This can grow the number of leads you may gain substantially.

5. Results:

Results can be seen quickly from webinars. After hosting a webinar you’ll have metrics to measure

how well it performed. These metrics include the number of attendees, number of those registered, and total views. The webinar can and should be recorded for you, the audience, and affiliates to share with others, growing the results even more. Each time a person completes your webinar’s registration form they should be considered a new potential lead, whether it be for a sale or a potential partnership. Webinars adds a personal interaction that videos and commercials don’t. Webinars put a face and name with your product making you approachable, human, and someone they can trust. Educating them on how your product can benefit their company is the first step in opening the door to future discussions and partnerships. It is essential to show both new and established leads how your product or service can improve or enhance their workplace. Depending on the prospect, the sales process can be slow. Businesses want to convert a lead into a cusWhile it’s certainly important to provide useful information and tips to your audience, it’s equally important to share how your brand or business can help them achieve this. How can your product be a solution to their problems? Your webinar should show the audience the value of your brand. Garnering interest in the product and its potential impact is the first step in completing a sale.

There are numerous benefits to hosting a webinar. Though this article only touches on a handful of them, it should be clear that webinars are an effective tool for engagement and growth. As you take these benefits into account, you should begin to think how you can use a webinar for lead generation and to increase traffic, which will yield great results for your business. Webinars have grown in popularity in recent years and have become an important marketing tool. These live web-based seminars can connect you with leads from all over the world. They encourage interaction by allowing the audience to ask questions or provide feedback in real-time. Just how beneficial can a webinar be to your business? Here are 7 reasons why webinars are a fantastic marketing strategy.

Webinars are a cost-effective way to extend your reach globally. Rather than pay for flights and hotels to meet with individual leads, you can engage with a larger group over their computer screens.

People from all over the world can attend, providing your brand or product with the potential to see huge

results. This global reach creates networking opportunities for building relationships and partnerships. Your audi ence has invested time in registering and listening to the information you plan to share. They’re expecting valuable takeaways from the webinar, even some thing they can put into place at their own company. This positions you and your brand as an industry lead er, or expert. Webinars can give your audience the chance to ask questions and provide feedback. This is valuable because you can address concerns, reser vations, or any lingering questions they may have about your training or product in real-time. You can customize your presentation to your audience based on their questions and feedback to keep them engaged. Ask them to take an action, such as completing a task or answering a question. This will increase audience participation and interest. Include guest speakers, such as industry leaders or affiliates, to speak during your webinar. These individuals should be familiar with your industry and value of your product. They will be able to educate the audience on the benefits or impact, validating information you have or will be sharing. By inviting a guest speaker, you can also increase the webinar’s attendance by including your guest’s audience and following. This can grow the number of leads you may gain substantially. Results can be seen quickly from webinars. After hosting a webinar you’ll have metrics to measure how well it performed. These metrics include the number of at tendees, number of those registered, and total views. The webinar can and should be recorded for you, the audience, and affiliates to share with others, grow ing the results even more. Each time a person com pletes your webinar’s registration form they should be considered a new potential lead, whether it be for a sale or a potential partnership. Webinars adds a personal interaction that videos and commercials don’t. Webinars put a face and name with your prod uct making you approachable, human, and someone they can trust. Educating them on how your product can benefit their company is the first step in opening the door to future discussions and partnerships. It is essential to show both new and established leads how your product or service can improve or enhance their workplace.Depending on the prospect, the sales formation and tips to your audience, it’s equally important to share how your brand or business can help them achieve this. How can your product be a solution to their problems? Your webinar should show the audience the value of your brand. Garnering interest in the product and its potential impact is the first step in completing a sale.There are numerous benefits to hosting a webinar. Though this article only touches on a handful of them, it should be clear that webinars are an effective tool for engagement and growth. As you take these benefits into account, you should begin to think how you can use a webinar for lead generation and to increase traffic, which will yield great results for your business. Webinars have grown in popularity in recent years and have become an important marketing tool. These

August 2020 Originate Report 31

Business Development • Fintech/Newest Loan Programs • Automation in Today’s Evolving Society • Upcoming Trends & Changes • Marketing & Outreach • Essential Tools & Technologies • New Legal Issues and Regulations Share your ideas! Email submissions@originate.report for more information.

LET US HELP YOU!

CURRENTLY

ACCEPTING ARTICLES

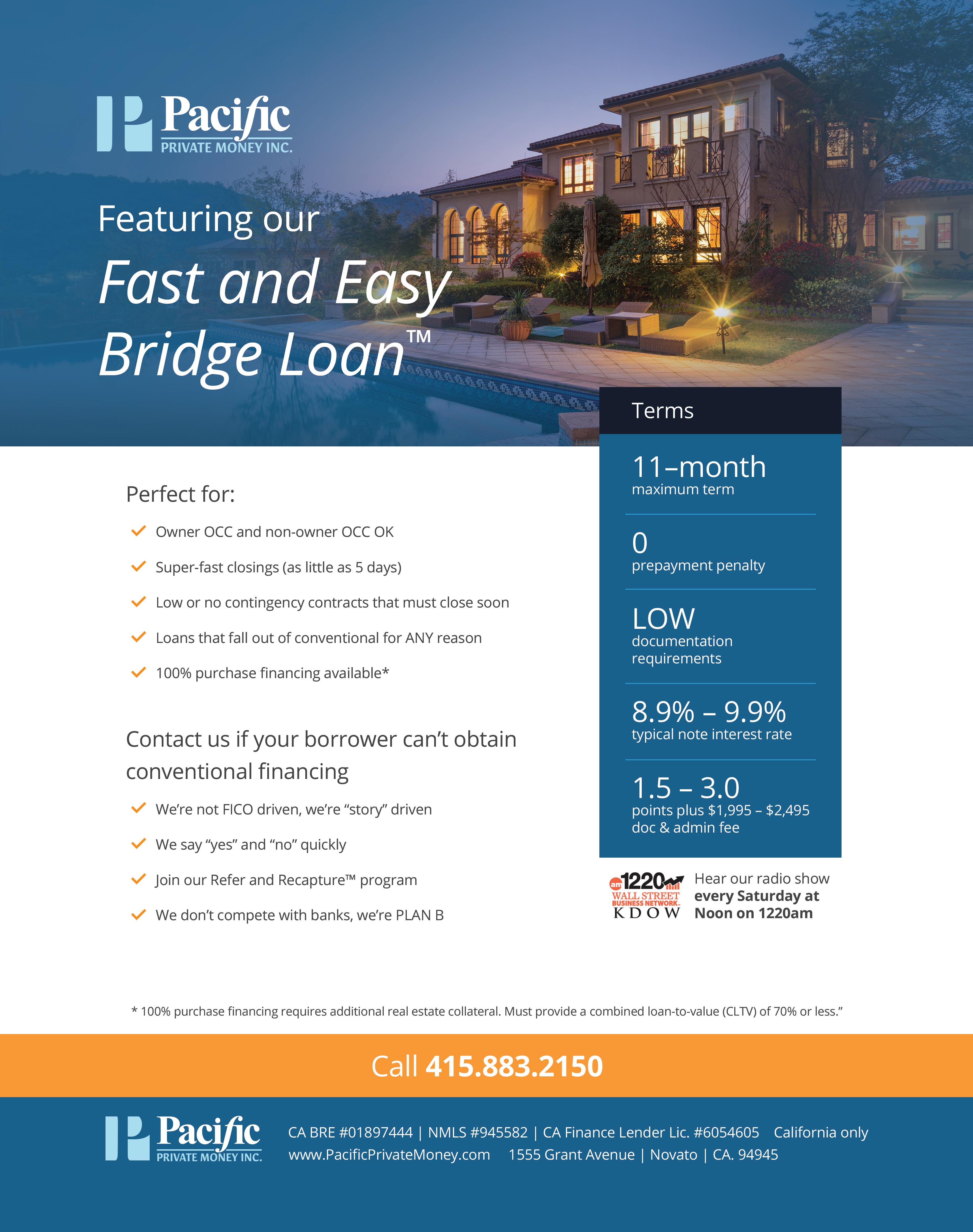

How Deferment of Mortgage Payments May Affect Borrowers in the Long Run

By Edward Brown, Pacific Private Money

When Congress passed Section 4021 of the CARES Act in response to the effects of COVID-19, their intent was to help borrowers who were having problems making their mortgage payments. Little did Congress realize that they were

potentially setting up borrowers for trouble in the future when it comes to credit worthiness as assessed by the lending community.

According to Mark Hanf, president of

Pacific

Private Money, “Section 4021 of the CARES Act contained

a regulation that loan servicers “shall report the credit obligation or account for those participating in forbearance as current”. In other words, those participating in a forbearance program should not see their credit scores drop. However, there is a loophole that allows

32

FEATURE

lenders to discover whether or not a borrower is actually making payments. It is the “comments” section of a credit report. The CARES Act does not mention the comments section of credit reports, and that’s where forbearance notations are going.” What borrowers are not being told is that any reference in a credit report to forbearance can be a Scarlet Letter for an applicant seeking a new mortgage, according to Kathleen Howley in an article she wrote in early May 2020.

ceived a loan request from a home buyer who was denied credit from a major bank for just this very situation. Although the bank sees the existing mortgage as “current” the forbearance has let the world know via the comment section that this borrower has requested a deferment. The major bank involved would most likely not deny the loan on its face due to the deferment, as this would violate the law; however, banks are notorious for coming up with a myriad of reasons for denying a loan and still stay within the guidelines set out for them.

Conventional lenders desire to have plain vanilla borrowers who pay back loans in a timely manner. When a borrower changes terms of the loan by requesting principal forgiveness or other aspects of the loan, the lenders generally do not usually extend credit again to these borrowers and can negatively affect the borrower’s ability to borrow again from unrelated lenders. Such is the case back during the Great Recession wherein some borrowers took advantage of the economic climate by asking their lender to reduce the principal of their loan [total forgiveness rather than just a deferment]. The borrowers may have gotten a reprieve, but the longterm effects may have been more drastic. Similarly, to when a borrower

files bankruptcy. The borrower may get out of paying creditors, but their ability to borrow in the future is usually severely hampered.

In one case, back in 2009, during the heart of the Greta Recession, one banker tells a story of how a wealthy borrower first asked for a principal loan reduction of $500,000 because his collateralized real estate had decreased and his request was granted. But, when this borrower was faced with the prospects of having this reduction reported on his credit report or the fact that he would have to inform any new lender that he requested a principal reduction [as this question is usually on bank applications], he voluntarily requested that the $500,000 abatement be reinstated. He decided his ability to borrow in the future was worth more than the $500,000 principal reduction.

Borrowers will have to decide if requesting deferments is worth the risk of potential future lending restrictions based upon the lender’s desire to lend to borrowers who choose to defer mortgage payments when the opportunity arises. Whoever said, “there’s no free lunch” must have been talking about these very situations.

ABOUT THE AUTHOR:

CONTACT:

edward@pacificprivatemoney.com

According to Hanf, within a week of Howley’s article, his company re-

https://pacificprivatemoney.com

August 2020 Originate Report 33

Edward Brown is in the Investor Relations department at Pacific Private Money in Novato, Calif.

Recent Illinois Decision Could Have Sweeping Impact on Force Majeure Interpretation

by Darlene Hernandez, Esq., Geraci LLC

On June 3, 2020, an Illinois bankruptcy court held that a financially strapped restaurant organization will not have to perform certain contractual obligations that were initially outlined in its lease agreement with the landlord, thanks to a force

majeure clause included in the same document.

The ruling may have a significant impact in a destabilized economy reeling from the aftereffects of the COVID-19 pandemic—in which businesses across all industries have

been forced to shutter their operations by state and federal health organizations in an attempt to stem the spread of the viral outbreak.

The Case

The Chicago-based Hitz Restaurant Group declared Chapter 11 bank-

34

FEATURED

ruptcy at the close of February, prior to the coronavirus pandemic. The restaurateur advocated that they should not be obligated to pay their monthly rent from April to June due to the state-mandated quarantine. The force majeure clause at issue specifically stated that “Landlord and Tenant shall each be excused from performing its obligations or undertakings provided in the Lease, in the event, but only so long as the performance of any of its obligations are prevented or delayed, retarded or hindered by laws, governmental action or inaction, orders of government.”

The landlord in the case, Kass Management Services, countered that

they were owed the rent because the tenants could still generate revenue via takeout and delivery services in addition to availing itself to the Paycheck Protection Program—a loan designed to provide a direct incentive for small businesses to keep their workers on the payroll. The PPP allows loans to be forgiven if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent mortgage interest, or utilities.

Judge Donald Cassling of the United States Bankruptcy Court for the Northern District of Illinois ultimately sided with Hitz Restaurant

Group, stating that the measures implemented by the Illinois state government qualified as force majeure per the terms of the contract. Cassling, however, specified that the restaurateur was still obligated to fulfill other duties laid out in the initial lease document. Cassling pointed out that approximately a quarter of the tenant’s space could be utilized to make profits even with the state’s stay-at-home order remaining in effect—mainly via delivery and pickup. Accordingly, the judge found that Hitz still had to pay 25%–or just over $2,600—of the total rental amount per the terms of the lease.

August 2020 Originate Report 35

Recent Illinois Decision: Cont. on pg. 36

Recent Illinois Decision: Cont. from pg. 35 the rent outline in their lease agreement. Legal experts feel that the case was an early test of whether states’ orders to suspend dine-in service due to COVID-19 invoked force majeure, a common lease stipulation that negates the obligations of renter or landlord if certain conditions are met. Cassling’s decision comes at a time where many restaurant opera-

Judge Cassling also rejected the landlord’s argument that the outstanding payments could have been acquired via the Paycheck Protection Program, claiming that the force majeure clause as worded in the contract did not obligate Hitz to obtain outside financing by way of a loan in order to meet its financial obligations.

Impact of the Opinion

The opinion is one of the first to address the issues as to whether force majeure clauses can be used as a valid justification for a business tenant—specifically one involved in the restaurant industry—to not pay

tors are claiming that their ability to stay in business is dependent on the willingness of their landlords to be flexible when it comes to either adjusting rental payments or forgiving them altogether. Complicating the matter further is the fact that now, on-site restaurant service has been given the green light to at least some degree in every state jurisdiction.

ABOUT THE AUTHOR: Darlene Hernandez is a Sr. Litigation Associate Attorney at Geraci Law Firm. She has represented various institutional clients in the consumer financial services industry for national and regional foreclosure/real estate and bankruptcy firms since 2008. Her practice covers a broad range of mortgage lending and banking litigation, including litigation relating to loan servicing, title, loan origination, post-foreclosure and REO, nuisance abatement, and foreclosure trustee and predatory lending defense, RESPA/TILA issues, title defects/ claims, judicial foreclosure, deficiency judgments, and receivership. CONTACT: d.hernandez@geracillp.com | https://geracilawfirm.com

36

August 2020 Originate Report 37 June2018 THEOFFICIALMAGAZINEOFGERACI Cities to Watch: Phoenix Marketing to MILLENNIALS Industry Spotlight: Adam Child THEOFFICIALMAGAZINEOFGERACI Industry Spotlight: Michael Schumacher BiCoastal Capital Capital You Can Count On MAY2019 Briana Malkoon (R) with Co-Founders Alexandra Yellin and Ben Stoodley THEOFFICIALMAGAZINEOFGERACI Celebrating of The Mortgage Office NOVEMBER2018 PRIVATE LENDING STORAGE, BABY! THE OFFICIAL MAGAZINE OF GERACI JULY 2019 WEBINARS AFAS INSIDE: MONEY360 CREATING CREDIBILITY IN PRIVATE CAPITAL Allen Shayanfekr Sharestates INDUSTRY SPOTLIGHT: A Voice of Experience THE OFFICIAL MAGAZINE OF GERACI MARCH 2020 Karey Geddes VIANOVA CAPITAL Women in Real Estate To the Young Professionals Light Your Own Fire, Kid BETH O’BRIEN, COREVEST FINANCE Advice from the Lady on the Leaderboard INSIDE: Linda Hyde AAPL SPECIAL EDITION FEATURING FREE OF CHARGE! SUBSCRIBE NOW Get the Originate Report Magazine in Your Inbox Every Month ORIGINATE.REPORT/SUBSCRIBE

Fidelity Mortgage

www.fidelityca.com

psteigleder@fidelityca.com

Peter Steigleder

(818) 422-8879

Inc.

Helvetica Group

www.helveticagroup.com

loans@helveticagroup.com

(310) 575-3301

Pacific Private Money

www.pacificprivatemoney.com

loans@pacificprivatemoney.com

(415) 883-2150

Redwood Mortgage Corp.

www.redwoodmortgage.com

RMC@redwoodmartgage.com

(800) 659-6593

San Mateo, CA 94402

Zinc Financial Inc.

www.zincdinancial.com

office@zinc.net

Tom Valentino

38 LENDER TYPES OF LOANS TYPES OF PROPERTIES * = STATES LENDING IN REV. 06.25.19 2019 2020 LET LENDERS KNOW YOU FOUND THEM IN ORIGINATE REPORT! LOAN HOME MAXIMUM LOAN$ MAXLOAN-TO-VALUE (%)/MAXTERM(YRS) MINIMUM LOAN$ CommercialConsumerBridgeCorporations/ Trusts/ Legal Entities Acquisitionsand Developments NotesPurchasedRehab/Remodeled/ Renovated Blanket Loans Second Mortgages JointVenturesForeignNationals Other Churches/ Temples/ Synagogues Land (Bare/ Commercial/Lot) AutomotiveRetail(Shops/ Strip Malls) Entertainment GasStationsLeisure(Golf Courses/ Marina) Hospitality (Hotels) Industrial Mixed-useResidentialPropertiesInvestment Properties Ranches and Farms Self-storageRestaurantsOffice *AZ, CA, NV *All 50 States 50K 100K 15M 10M 55/33 75/30

Lenders,

Direct Lender Direct Lender Direct Lender Direct Lender Direct Lender LENDER DIRECTORY 200K 7M500K 65-5*/70/5* *CA *65% For commercial and mixed-use and 70% for multi-family and residential investment. 5 years (custom terms are available) AZ, CA, CO, IN, MI, NM, OH, TN, TX, WA 50K 2M 90/2 *CA 150K 5M 70/30

AAPL has a long history of firsts, and we’re adding to it by hosting the first fully hybrid private lending event for both in-person and virtual attendees. We will launch our AAPL Annual Conference app for desktop, IOS, and Android on July 15th.

The app enables attendees who have purchased a virtual ticket to watch and participate in live-streamed sessions, network in virtual meeting rooms with both in-person and virtual attendees, and connect with sponsors.

App features for both in-person and virtual attendees include:

• Visit virtual exhibitor booths designed for an online experience.

• Live stream sessions with real time Q/A participation.

• Build your own schedule with reminders so you never miss a session.

• Watch session recordings so you don’t have to make difficult decisions on what to attend.

• Create a profile to connect with both in-person and virtual attendees.

• Network through virtual meeting rooms and one-on-one chat capability.

• Navigate the Vegas event with interactive maps.

• Stay up-to-date with non-invasive notifications.

• Win prizes by interacting.

• And more!

August 2020 Originate Report 39

AAPLONLINE.COM • (913) 888-1250

40 WE PROVIDE PEACE OF MIND Geraci LLP is a law firm, media, and consulting company that caters to the non-conventional lending space. We are the “go-to” provider for all lending-related matters and are your resource to help you grow your business. CORPORATE AND SECURITIES Securities Offerings & Compliance* Entity Formation* Corporate Governance* Licensing* BANKING AND FINANCE Loan Documents* Lending Compliance* Foreclosure/Loss Mitigation LITIGATION AND BANKRUPTCY Creditor Representation Title Claims Loss Mitigation MEDIA SERVICES Branding Consultation Pitch Decks Logo Design Web Development Graphic Design CONNECT WITH US! 90 Discovery Irvine, CA 92618 | Phone: 949.379.2600 | Fax: 949.379.2610 https://geracillp.com | https://geracicon.com | https://geracimediagroup.com IT’S NOT JUST ABOUT IDEAS. IT’S ABOUT THE EXECUTION. *All 50 States