CONTRIBUTING AUTHORS: Alex Vaxmonsky, Andrés Fígoli, Anjali Sugadev, Glenn Hovermale, John Maguire, Kieran Clark, Kristian Nielsen, John Tibbles, Philip Pilgrim, and Syeda Humera

Submarine Telecoms Forum, Inc. www.subtelforum.com/corporate-information

BOARD OF DIRECTORS: Margaret Nielsen, Wayne Nielsen and Kristian Nielsen

Contributions are welcomed and should be forwarded to: pressroom@subtelforum.com.

Submarine Telecoms Cable Industry Report is published annually by Submarine Telecoms Forum, Inc., and is an independent commercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical fiber technologies and techniques. Submarine Telecoms Forum may not be reproduced or transmitted in any form, in whole or in part, without the permission of the publishers.

Liability: While every care is taken in preparation of this publication, the publishers cannot be held responsible for the accuracy of the information herein, or any errors which may occur in advertising or editorial content, or any consequence arising from any errors or omissions, and the editor reserves the right to edit any advertising or editorial material submitted for publication.

New Subscriptions, Enquiries and Changes of Address 21495 Ridgetop Circle, Suite 201, Sterling, Virginia 20166, USA, or visit www.subtelforum.com.

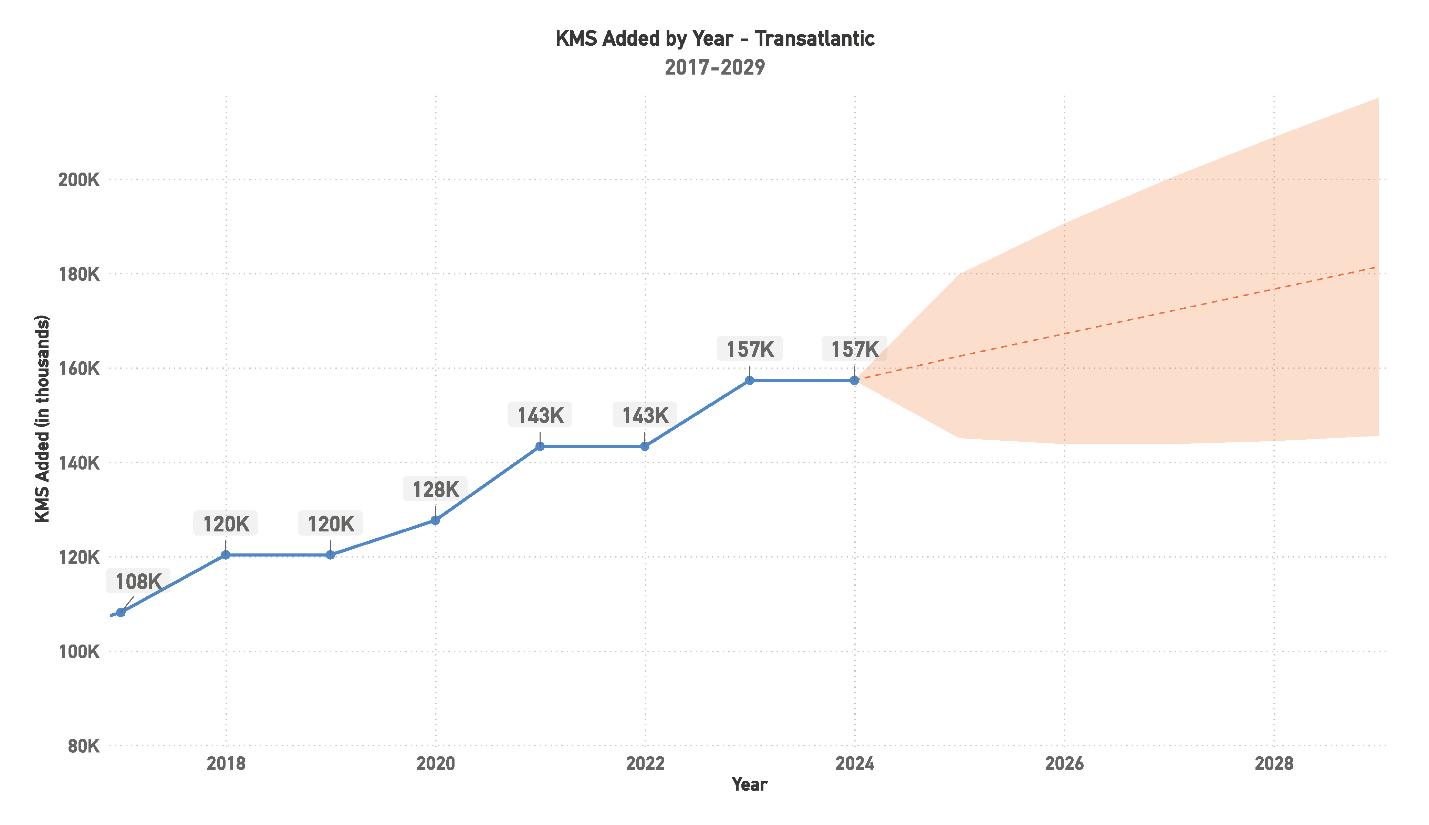

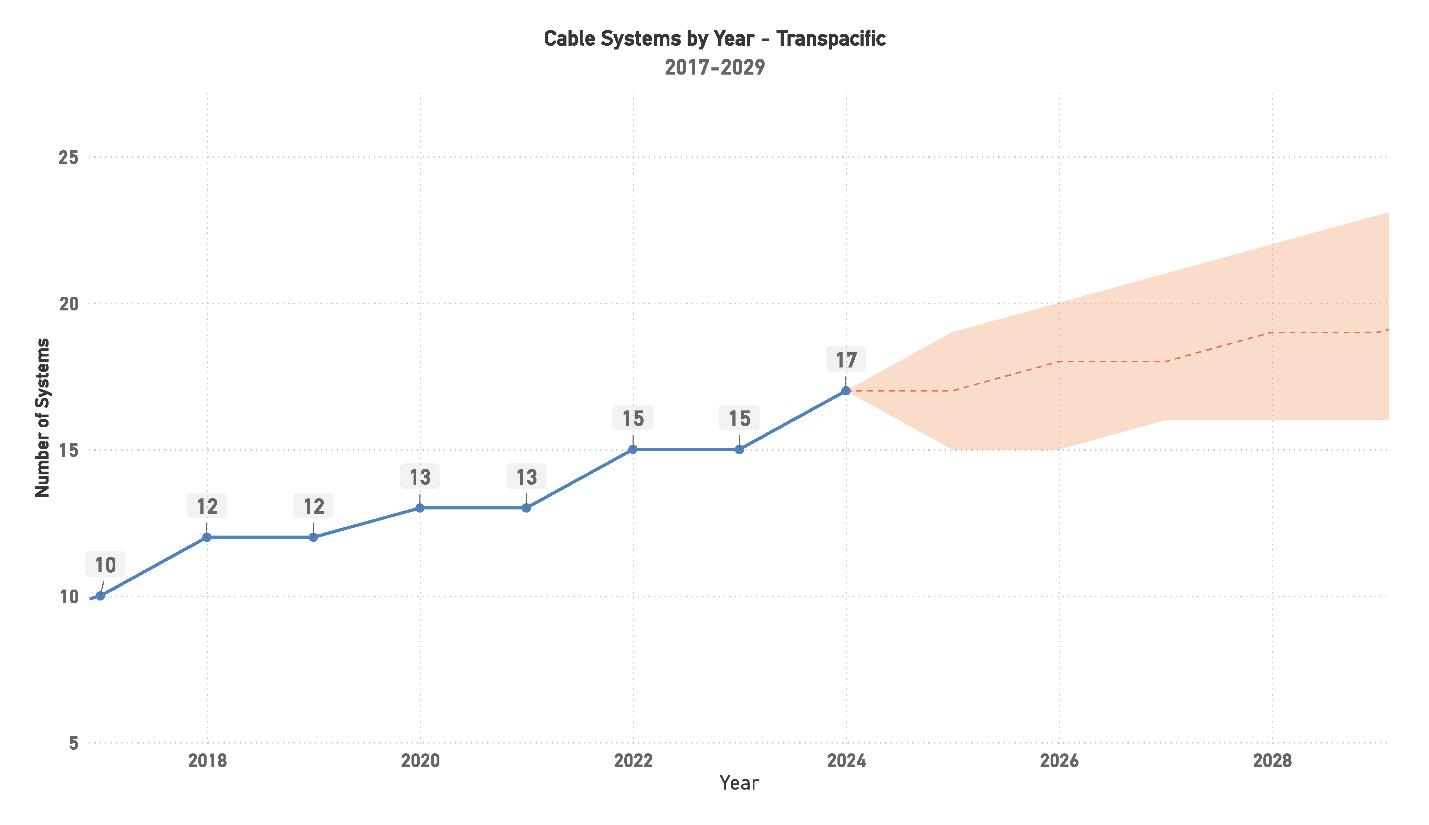

Figure 106: Cable Systems by Year – Transpacific, 2017- 2029.........................................................................194

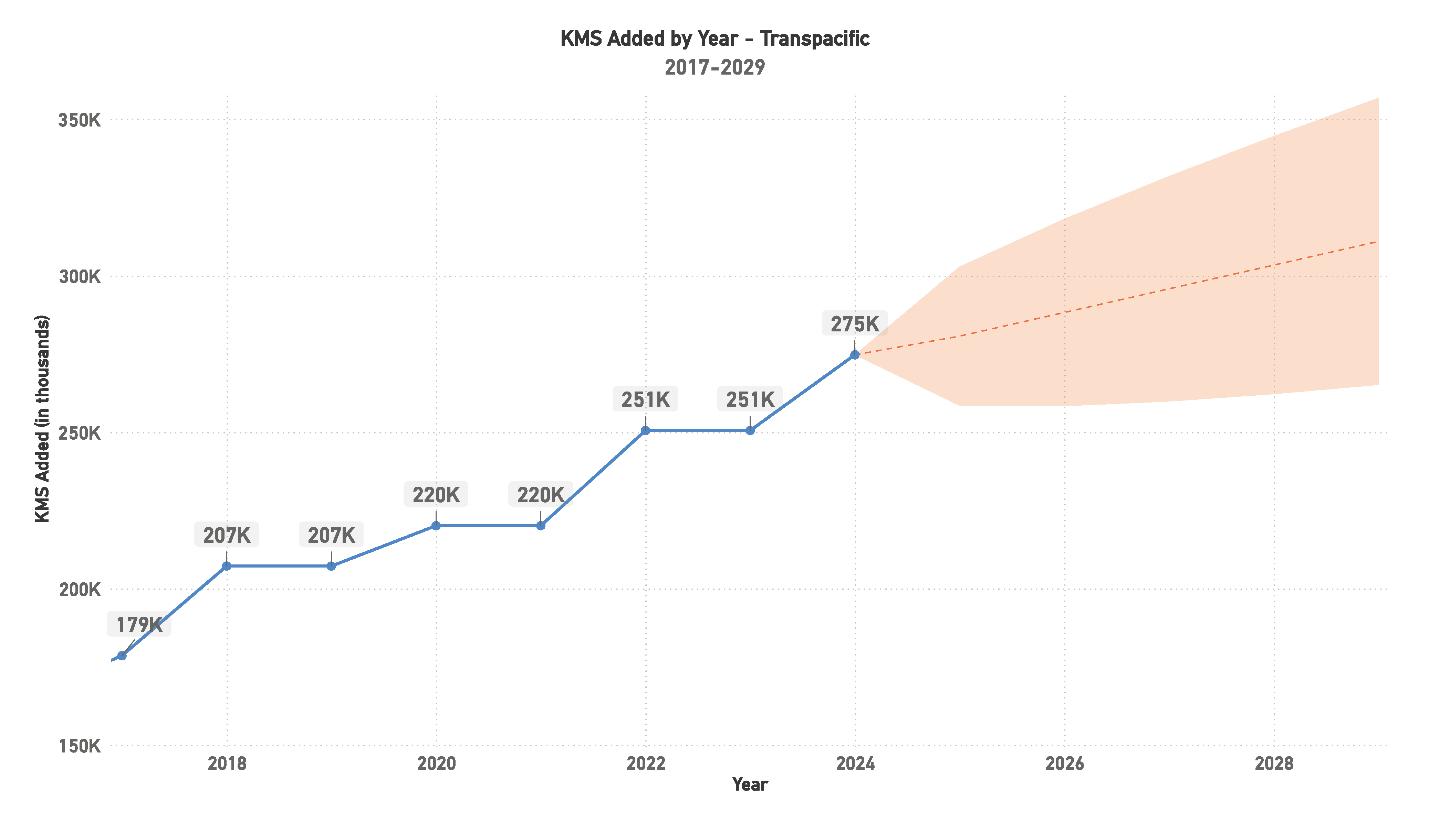

Figure 107: KMS Added by Year – Transpacific, 2017- 2029........................................................................ 195

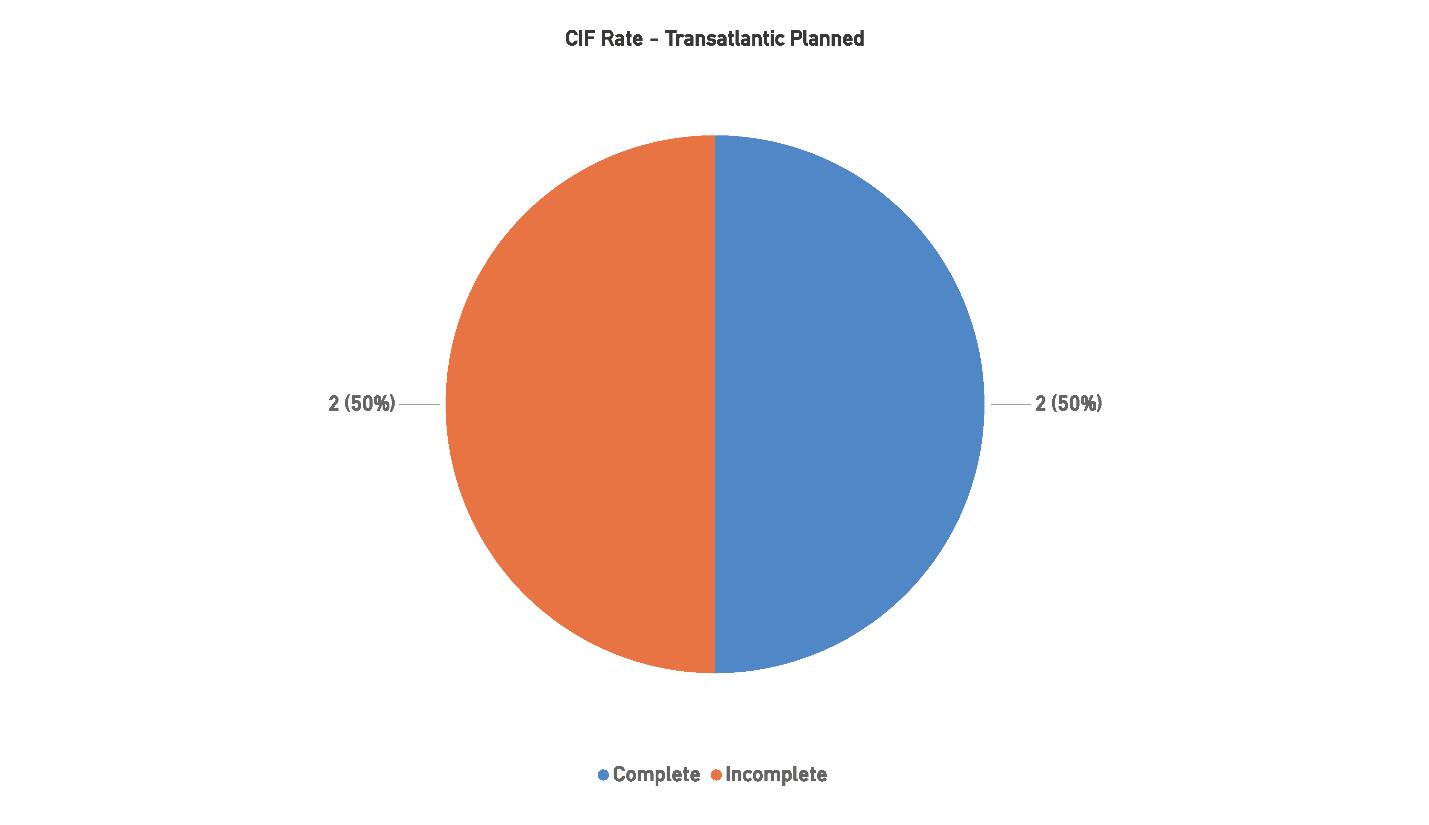

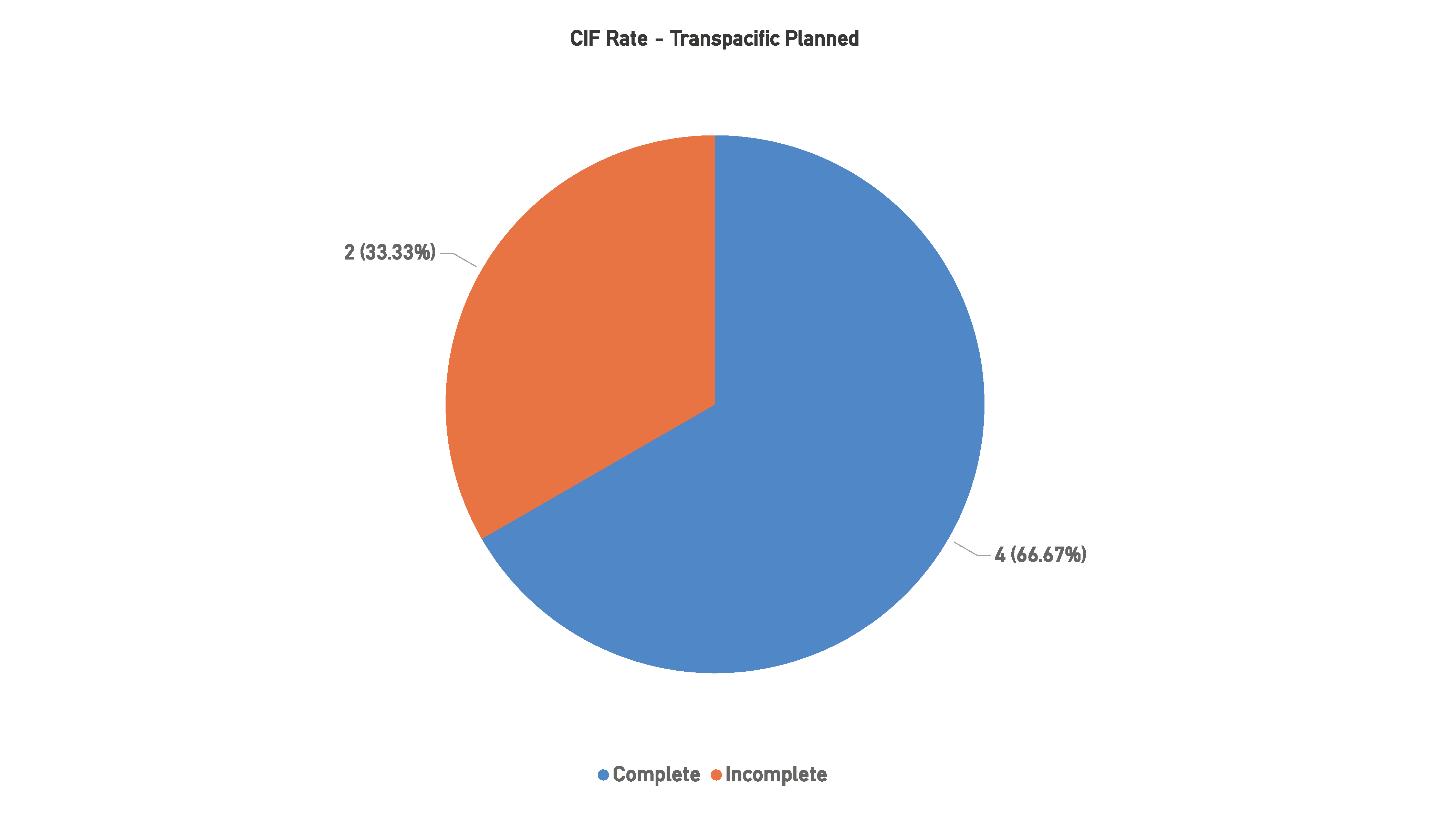

Figure 108: CIF Rate – Transpacific Planned 195

LIST OF VIDEOS

Video 1: Wayne Nielsen, PublisherSubmarine Telecoms Forum, Inc. 6 Video 2: Kieran Clark, Senior AnalystSubmarine Telecoms Forum .............................................. 10

Video 3: Glenn Hovermale, Marine CoordinatorWFN Strategies 82

Video 4: Syeda Humera, AnalystSubmarine Telecoms Forum .............................................. 94

Video 5: Andrés Fígoli, Lawyer – Figoli Consulting 142

The year 2024 marked a pivotal period for the submarine cable industry. Amid geopolitical tensions, economic volatility, and supply chain disruptions, the industry has demonstrated remarkable resilience and adaptability. Positioned to meet the accelerating demand for global data, the industry stands at an exciting crossroads of growth and innovation.

This report delves into the critical trends shaping the future of submarine cables, from expanded data capacity and evolving ownership models to fortified regulatory frameworks aimed at enhancing security and resilience. Global initiatives like the “New York Principles” spotlight a collective commitment to cable security, while major hyperscalers drive growth on key routes across the Transpacific and Transatlantic. Innovative financing, strategic mergers, and advanced technologies continue to propel the industry, which is navigating an increasingly complex landscape through collaboration, resilience, and technological advancement.

Our annual Industry Report aims to be a cornerstone ana -

This report delves into the critical trends shaping the future of submarine cables, from expanded data capacity and evolving ownership models to fortified regulatory frameworks aimed at enhancing security and resilience.

lytical resource, complementing our other SubTel Forum offerings: the Submarine Cable Map printed in January, May and September, plus the Submarine Cable Almanac released quarterly, and the online Submarine Cables of the World Interactive Map. This report provides comprehensive analysis and forecasts, serving as an invaluable guide for those seeking to understand the health and trends of the submarine cable industry. It delves into both global and regional markets, addressing

Video 1: Wayne Nielsen, Publisher - Submarine Telecoms Forum, Inc.

The year 2024 marked a pivotal period for the submarine cable industry.

key issues such as new systems, upgrades, ownership structures, financing, market drivers, and anticipated geopolitical and economic impacts.

Last year’s edition was downloaded over 500,000 times and cited extensively in business journals and periodicals. We are both optimistic and confident that this year’s report will withstand similar scrutiny, and we hope you’ll agree.

We are honored to have Doreen Bogdan-Martin, Secretary-General of the International Telecommunication Union, once again contribute this year’s foreword, sharing insights on the ITU’s initiatives and the current state of submarine cables.

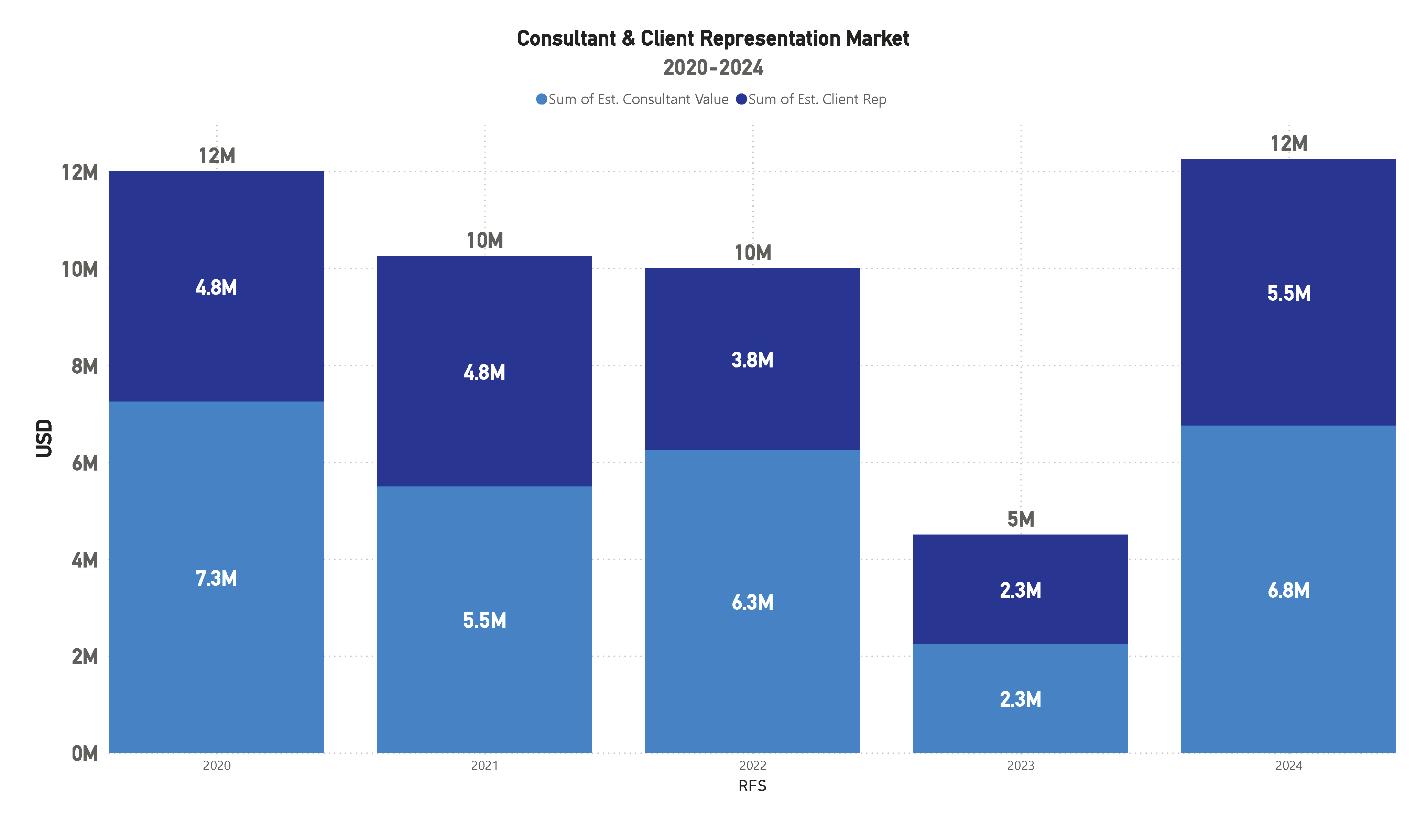

In this report, we’ve identified more than $15.4 billion in new projects actively being pursued. Of these, contracts worth $8.2 billion are already in force, with $6.7 billion of those slated for completion in 2024 alone.

We’ve drawn insights from various articles in recent issues of Submarine Telecoms Forum Magazine and our proprietary Market Sector Reports to enrich our discussion on various industry topics. Special thanks go to this year’s contributing industry specialists, namely: Alex Vaxmonsky

• Andrés Fígoli

• Anjali Sugadev

• Geoff Bennett

• Glenn Hovermale

• John Maguire

• Kieran Clark

• Kristian Nielsen

• John Tibbles

• Philip Pilgrim

• Syeda Humera

We also extend our heartfelt thanks to this year’s sponsors, who have played a crucial role in making the annual Industry Report possible:

• APTelecom

• Figoli Consulting

• Infinera

• WFN Strategies

While the future may be uncertain, one fact remains clear: our industry, with its rich 175+ year history, continues to be a thriving, essential, and ever-evolving enterprise.

In the coming months, we are committed to providing as much new data as possible in a timely and useful manner. As the saying goes, an informed industry is a productive industry.

Thank you for your continued interest and trust in SubTel Forum’s 13th annual “Submarine Telecoms Industry Report.”

Good reading and Slava Ukraini ,

Wayne Nielsen Publisher & President, Submarine Telecoms Forum, Inc.

WAYNE NIELSEN is Publisher & President of Submarine Telecoms Forum, Inc. and possesses more than 35 years’ experience in submarine cable systems, including polar and offshore Oil & Gas submarine fiber systems, and has developed and managed international telecoms projects in Antarctica, the Americas, Arctic, Europe, Far East/Pac Rim and Middle East. In 2001, he founded Submarine Telecoms Forum magazine, the industry’s considerable voice on the topic. He is also Managing Director of WFN Strategies, which provides design, development, and implementation support, as well as commercial and technical due diligence of submarine cable systems for commercial, governmental, and Oil & Gas clients. He received a postgraduate master’s degree in International Relations, and bachelor’s degrees in Economics and Political Science, and is a former employee of British Telecom, Cable & Wireless and SAIC.

Thoughts From Doreen Bogdan-Martin, ITU Secretary-General Foreword

Greetings from New Delhi, where we are wrapping up the governing conference for ITU standardization work, the 2024 World Telecommunication Standardization Assembly (WTSA-24).

WTSA-24 encompasses work on standards for submarine telecoms cables — the arteries of our interconnected world carrying the lifeblood of global communications.

As our economies and digital ambitions grow, so does our reliance on this vital global infrastructure.

On behalf of the United Nations agency for digital technologies, I applaud the submarine telecoms industry for building the solid foundation our shared digital future needs.

ITU is proud to have supported this industry from its very beginnings.

to improve resilience of this vital infrastructure that powers global communications and the digital economy.

This Advisory Body will bring together governments, regulatory authorities, industry leaders, and key stakeholders in areas related to enhancing the safety, redundancy, and protection of submarine cables.

We are fully committed to delivering this same value to innovation for climate action.

On behalf of the United Nations agency for digital technologies, I applaud the submarine telecoms industry for building the solid foundation our shared digital future needs.

This year marks 40 years since ITU first standardized optical fibre, highlighting the remarkable speed at which today’s expansive optical networks have been built.

Over the past four decades, ITU standards have also supported optical-network capacity to grow at an average of 40 per cent each year.

Not only have our standards helped the submarine telecoms industry evolve in a cost-effective manner, but they also offer certainty when it comes to reliability and interoperability.

Right now, in partnership with the International Cable Protection Committee (ICPC), ITU is setting up an International Advisory Body for Submarine Cable Resilience to promote dialogue and collaboration on potential ways and means

Two new ITU standards for both SMART (scientific monitoring and reliable telecommunications) cables and cables dedicated to scientific sensing have just been completed.

The climate and hazard monitoring sensors included in SMART cables are designed to coexist with telecom components and match the lifespan of commercial cables.

The prospect of a real-time ocean observation network creates compelling opportunities for disaster risk reduction, such as more accurate early warnings of tsunamis. This network could also capture a wealth of valuable data for climate science.

These new standards build on the pioneering work of the ITU/WMO/UNESCO/IOC Joint Task Force on SMART Cable Systems, which helped develop the technical and financial feasibility of SMART cables. The task force now supports ongoing SMART cable deployments and continues to study potential new capabilities for future deployments.

EllaLink, the transAtlantic cable system connecting the European and South American continents, was the first to

As our economies and digital ambitions grow, so does our reliance on this vital global infrastructure.

dedicate a fibre of a commercial telecoms cable to environmental sensing between Madeira Island and the trunk cable.

Portugal is now set to build SMART into the new ContinentAzoresMadeira (CAM) ring cable linking the mainland to islands a thousand kilometres out in the Atlantic Ocean.

SMART capability will form around 10 per cent of the total cost to deploy the new government sponsored CAM cable, expected to enter service in 2025.

An Italian demonstrator project is using 21 kilometres of SMART cable to monitor seismic activity on the seafloor near Mount Etna. Other SMART projects are underway in Indonesia, the Vanuatu–New Caledonia island area, and even Antarctica.

This year’s Submarine Telecoms Industry Report provides a platform for industry leaders and experts to share views on the latest developments in submarine telecoms and associated hopes for the future.

With its global scope and strong support from the community it serves, ITU is proud to support this report – especially in a WTSA year.

WTSA-24 comes at a time when reaching consensus on international technical standards is more important than ever, especially to ensure that new and emerging technologies are used as a force for good for all.

The Global Digital Compact, adopted at the UN General Assembly last month as part of the UN Pact for the Future, and the upcoming WSIS+20 Review next year, provide a framework to ensure that new technologies benefit everyone, everywhere.ITU standards help create the confidence to continue innovating and investing in digital technologies with the aim of achieving universal connectivity and sustainable digital transformation, ITU’s dual strategic objectives and my top priorities.

To reach these goals, we need all hands on deck and a range of diverse perspectives.

ITU’s standardization inclusive processes ensure that all participants’ voices are heard.

If you are not already a contributing member of the ITU standards community, I encourage you to join us and help create the shared digital future we want — one built on collaboration, consensus, and innovation. STF

Doreen Bogdan-Martin ITU Secretary-General

DOREEN BOGDAN-MARTIN took office as Secretary-General of the International Telecommunication Union (ITU) on 1 January 2023.

With over three decades of leadership experience in global telecommunications policy, Ms. Bogdan-Martin has emphasized the need for digital transformation to achieve economic prosperity, job creation, skills development, gender equality, and socio-economic inclusion, as well as to build circular economies, reduce climate impact, and save lives. Her historic election by ITU Member States in September 2022 made her the first woman ever to head the nearly 160-year-old organization. Known for mobilizing innovative partnerships, she aims to promote meaningful connectivity, intensify cooperation to connect the unconnected, and strengthen the alignment of digital technologies with inclusive sustainable development.

Methodology

This edition of the Submarine Telecoms Cable Industry Report was developed by analysts at Submarine Telecoms Forum, Inc., who also contribute analysis for SubTel Forum’s Submarine Cable Almanac, online and print Cable Maps, and Industry Newsfeed.

For this report, a multi-faceted approach was utilized, combining interviews with industry leaders and data from our proprietary Submarine Cable Database. The database, continuously updated since 2013, tracks over 500 active and planned domestic and international cable systems. It allows queries based on various parameters including client, year, project, region, system length, capacity, landing points, data centers, owners, installers, system cost, upgrade status, and more.

The Submarine Cable Database is maintained by a dedicated team and powered by MySQL. Maps are created using ArcGIS Pro, following the same visual style as the Submarine Cables of the World print map. All data visualizations, such as charts, are produced in Power BI, which is connected in real-time to the database to ensure the most current data is represented.

For this report, a multifaceted approach was utilized, combining interviews with industry leaders and data from our proprietary Submarine Cable Database. The database, continuously updated since 2013, tracks over 500 active and planned domestic and international cable systems.

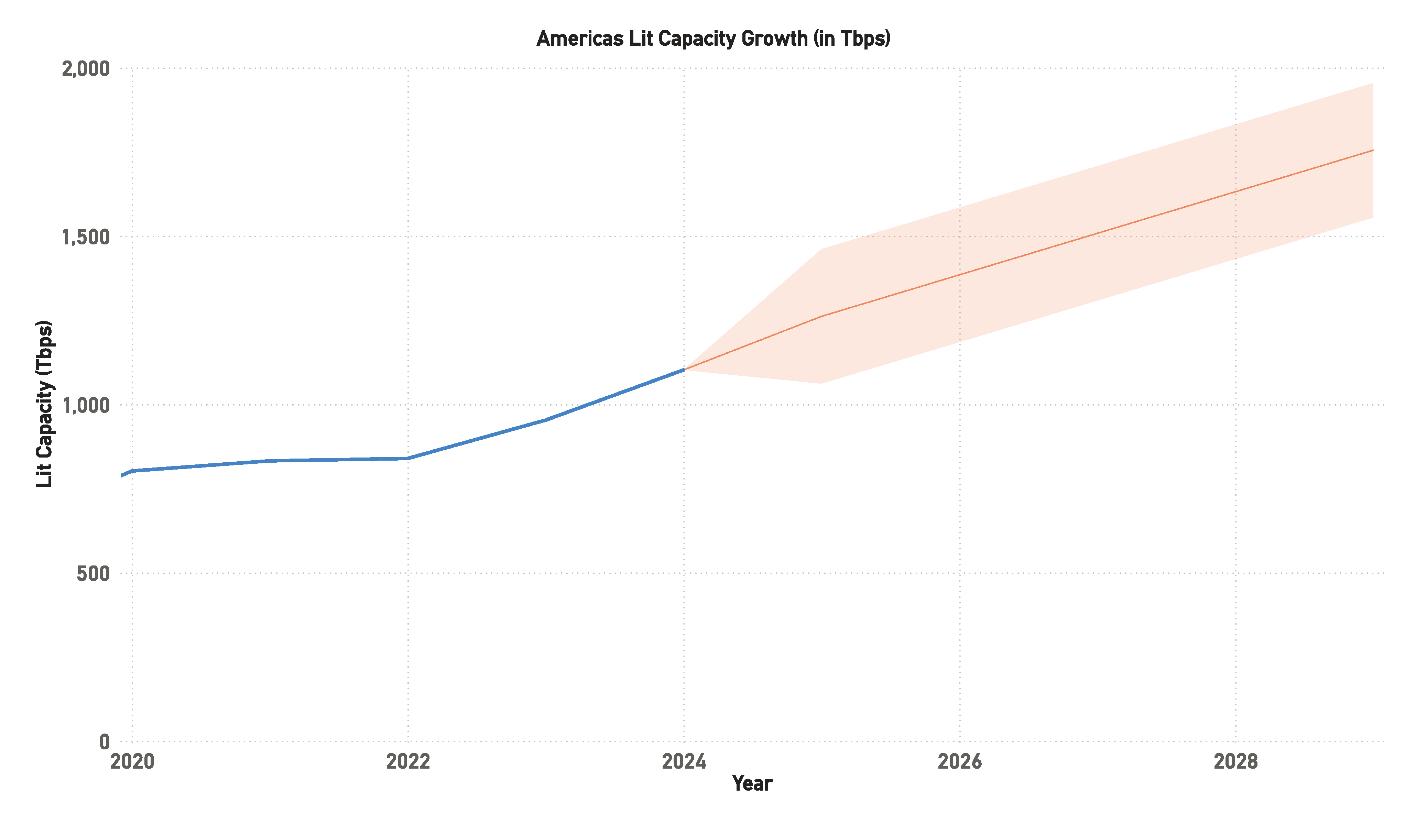

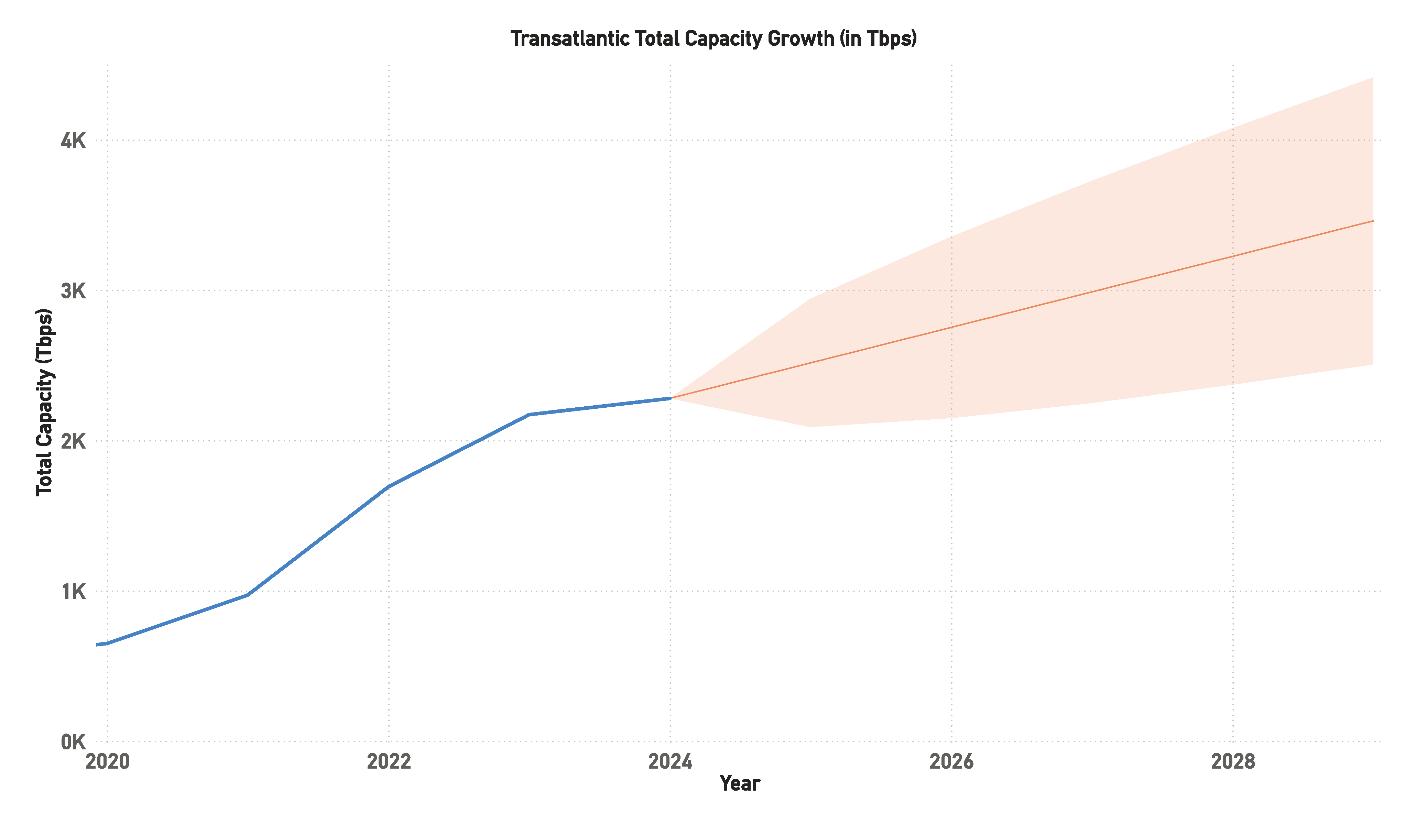

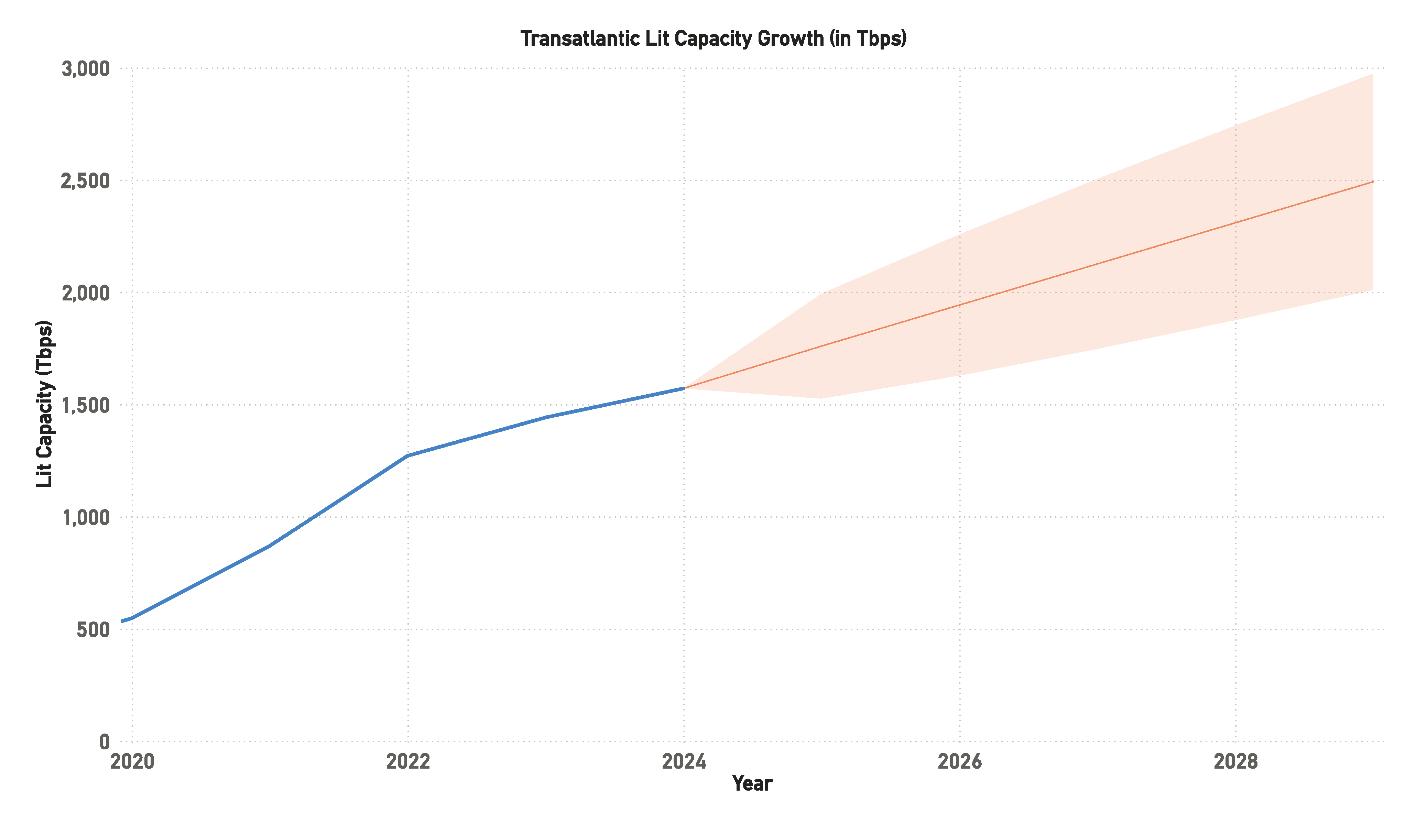

Projections in the report are generated using the Power BI forecast function, which leverages the Exponential Smoothing (ETS) algorithm to predict future data points based on historical trends. This method accounts for seasonality, trends, and noise in the data, providing a well-grounded basis for forecasting future market conditions.

Data gathering for the report is a continuous process throughout the year, drawing from public, commercial, and scientific sources. Data assimilation is conducted in

Video 2: Kieran Clark, Senior Analyst - Submarine Telecoms Forum

Projections in the report are generated using Power BI.

parallel to ensure accurate market projections.

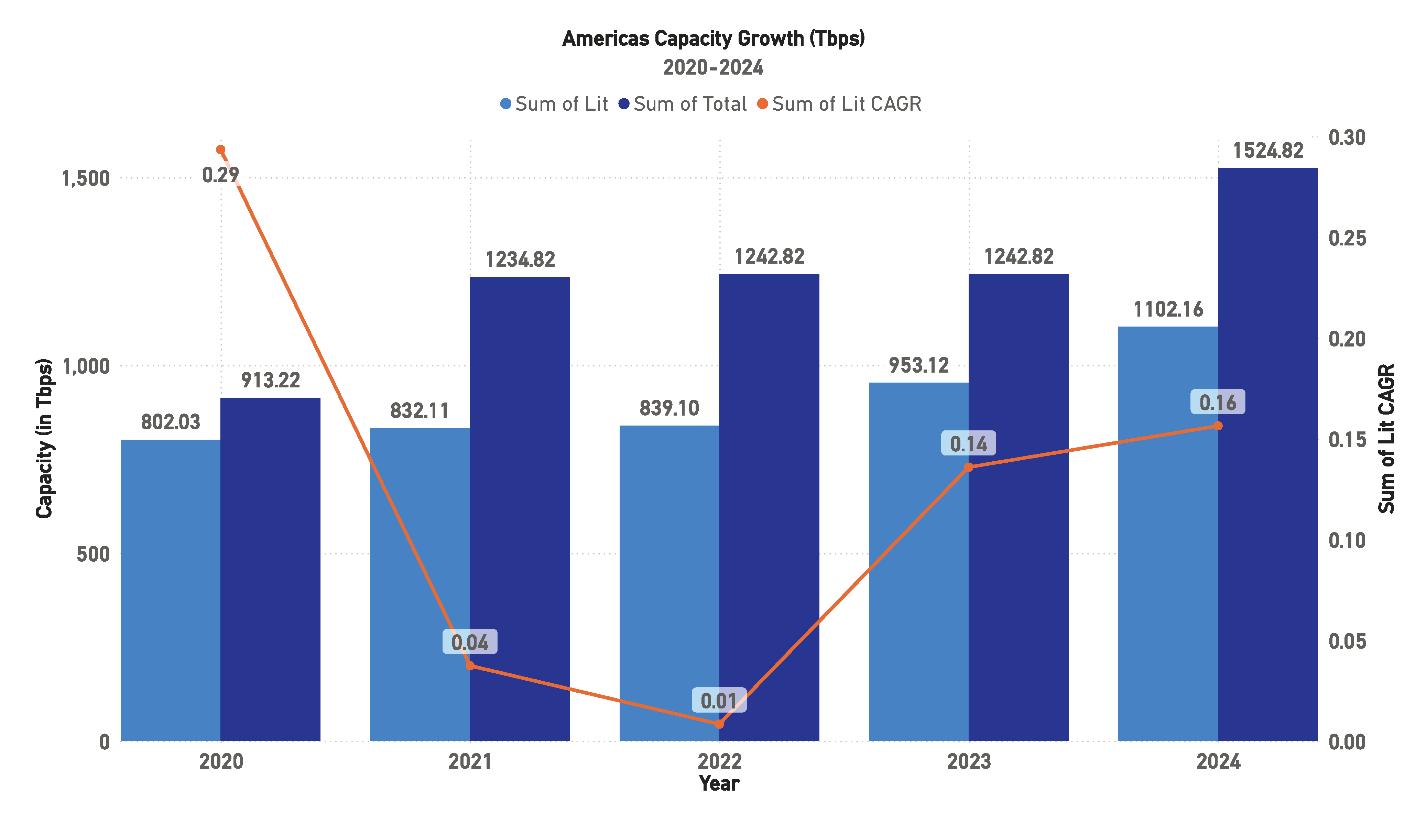

To determine Compound Annual Growth Rate (CAGR) for capacity growth, two methods are applied: one calculates CAGR over a specific period, while the other uses a rolling two-year CAGR to minimize extreme variances, enabling a year-to-year comparison. Since 2019, adjusted FCC reporting requirements have necessitated the use of modeling to estimate capacity growth, using average growth rates from 2015-2018 as a basis for projections from 2019 onward.

For unrepeatered systems, a maximum cable length of 250 km is applied, with exceptions for systems publicly announced as unrepeated. Trending is based on known data, with linear growth estimates for future years. Power BI’s forecast model is used for line graph projections, employing time-series algorithms to predict future values based on historical data.

In estimating system cost, when public information is unavailable, a standardized formula of $50,000-$70,000 USD per kilometer of cable is used, based on industry averages.

While every effort is made to ensure the accuracy of this report, the projections and estimates provided are based on the best available information at the time of publication. STF

KIERAN CLARK is the Lead Analyst for SubTel Forum. He originally joined SubTel Forum in 2013 as a Broadcast Technician to provide support for live event video streaming. He has 6+ years of live production experience and has worked alongside some of the premier organizations in video web streaming. In 2014, Kieran was promoted to Analyst and is currently responsible for the research and maintenance that supports the Submarine Cable Database. In 2016, he was promoted to Lead Analyst and his analysis is featured in almost the entire array of Subtel Forum Publications.

SYEDA HUMERA, a graduate from JNTUH and Central Michigan University, holds a Bachelor’s degree in Electronics and Communication Science and a Master’s degree in Computer Science. She has practical experience as a Software Developer at ALM Software Solutions, India, where she honed her skills in MLflow, JavaScript, GCP, Docker, DevOps, and more. Her expertise includes Data Visualization, Scikit-Learn, Databases, Ansible, Data Analytics, AI, and Programming. Having completed her Master’s degree, Humera is now poised to apply her comprehensive skills and knowledge in the field of computer science.

Executive Summary

The global submarine cable industry continues to experience dynamic growth, driven by increasing demand for digital connectivity and the rising importance of resilient, secure communications infrastructure. Throughout 2024, the industry has faced new challenges and opportunities, shaped by a confluence of geopolitical, technological, and economic factors. This report provides a comprehensive overview of the most significant trends, examining key developments in capacity growth, ownership, financing, supplier activities, and regulatory changes, while offering a regional analysis of current and future systems.

Subsea cables have increasingly become focal points of national security discussions. Once considered solely as commercial assets, they now play a critical role in geopolitics, particularly as they are responsible for the vast majority of global communications, including financial transactions, internet traffic, and even military operations. In response, governments around the world are taking steps to protect these networks from potential threats.

The establishment of the “New York Principles,” endorsed by over thirty nations, is a notable development in cable security, aiming to bolster resilience against both state and non-state actors. However, there are growing concerns about a potential bifurcation of global internet connectivity, with some nations embracing these security frameworks while others, such as China, may not.

At the same time, the industry is grappling with the complexities of nationalization and public-private partnerships (PPPs). The drive to nationalize subsea cable infrastructure, while aimed at protecting national interests, has the potential to stifle innovation. Case studies from the oil and telecommunications sectors offer insights into the potential pitfalls of state ownership. PPPs, however, have emerged as a viable middle ground, blending government oversight with the efficiency of private-sector operations. Successful projects like the Hawaiki Submarine Cable and the Coral Sea Cable System illustrate the benefits of this approach, showing how it can balance strategic priorities with operational needs.

The global demand for data continues to grow unabated, driving capacity expansion across submarine cable systems.

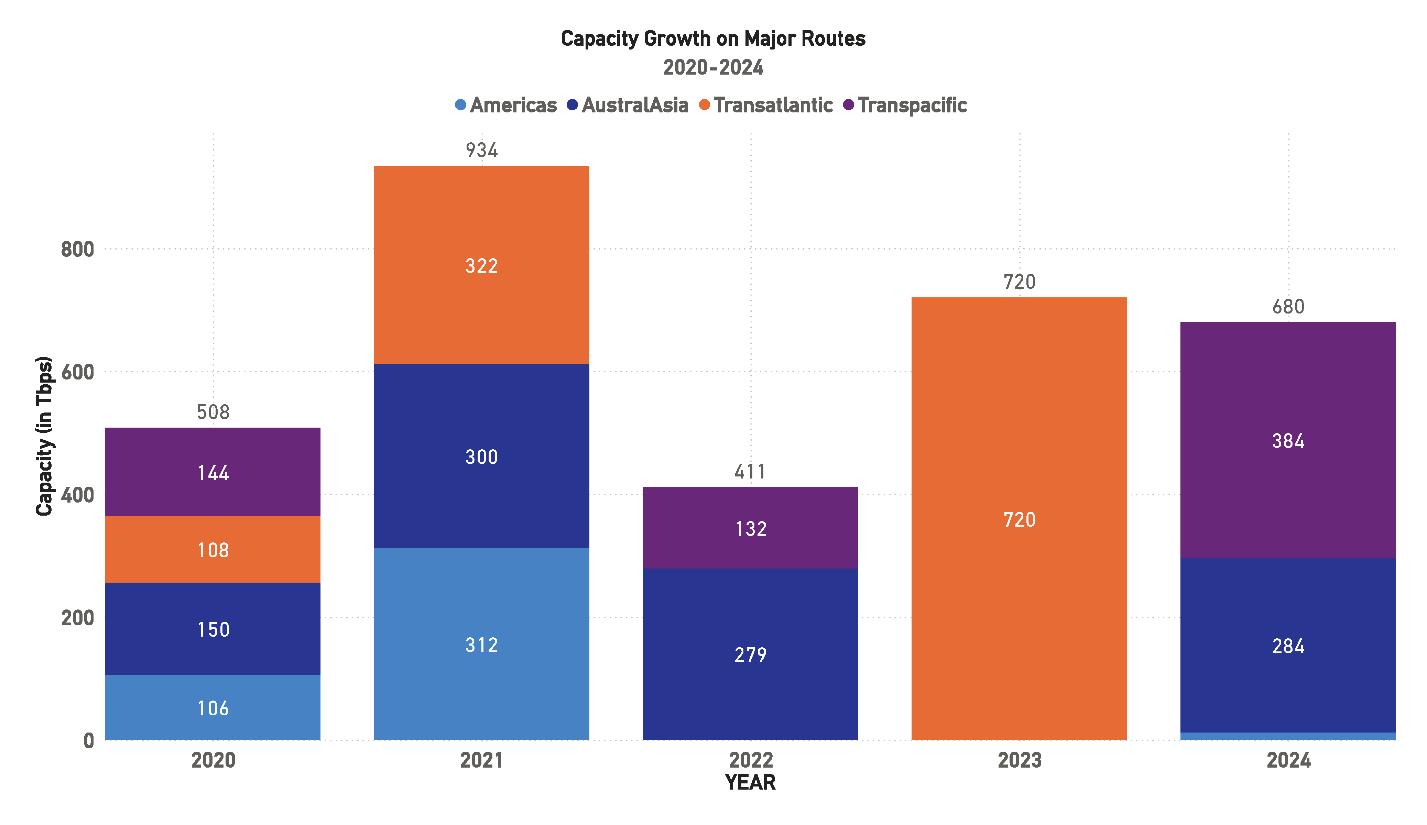

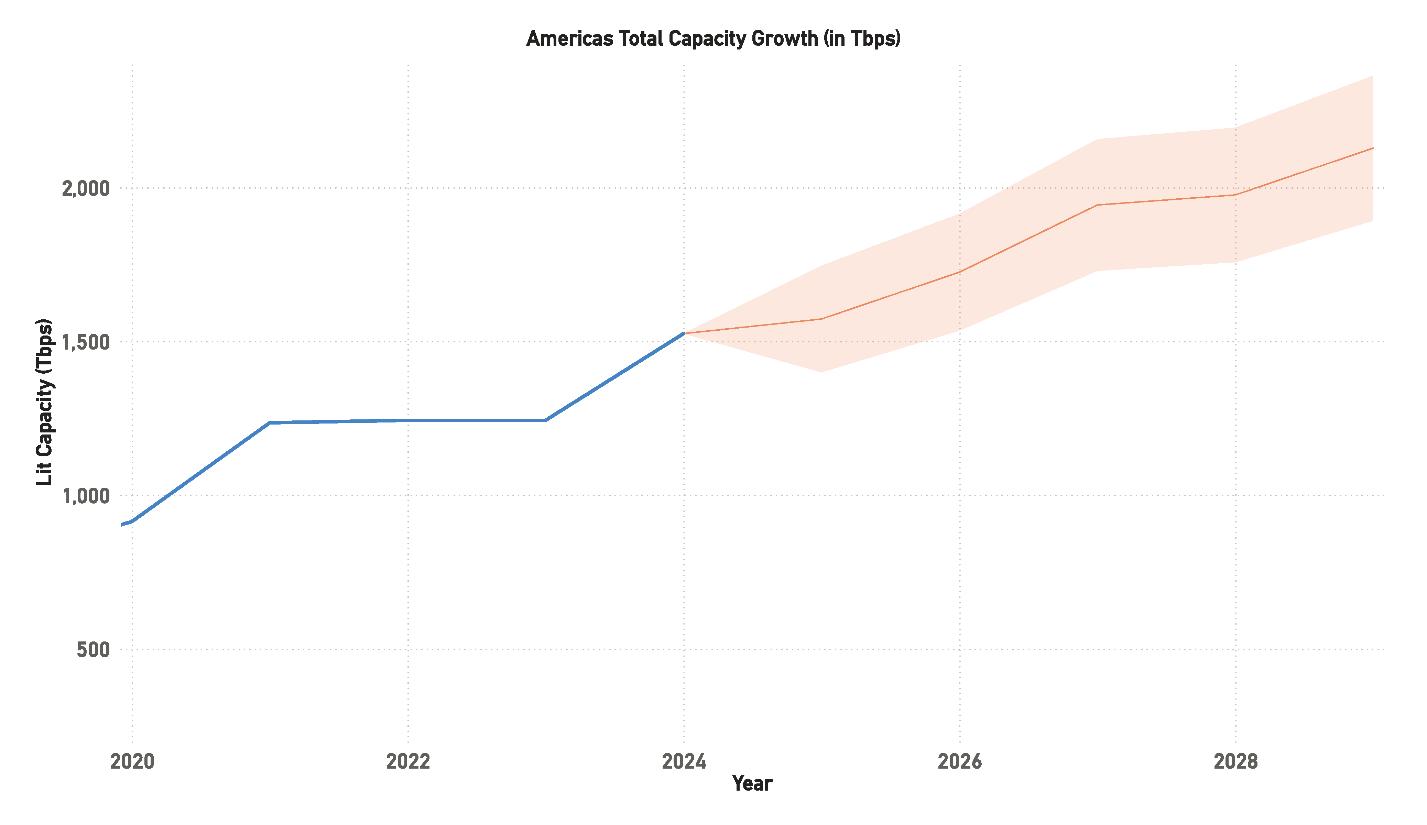

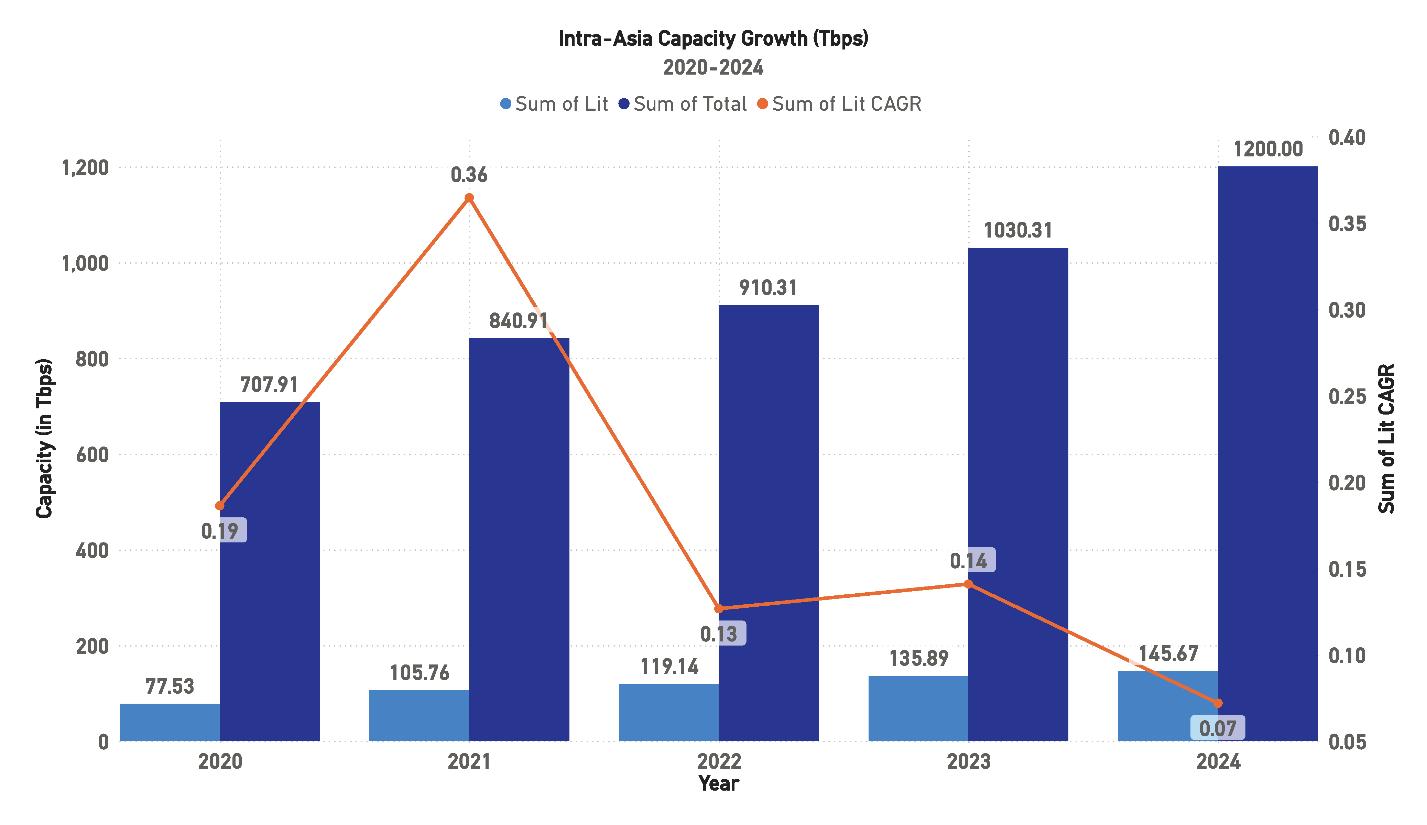

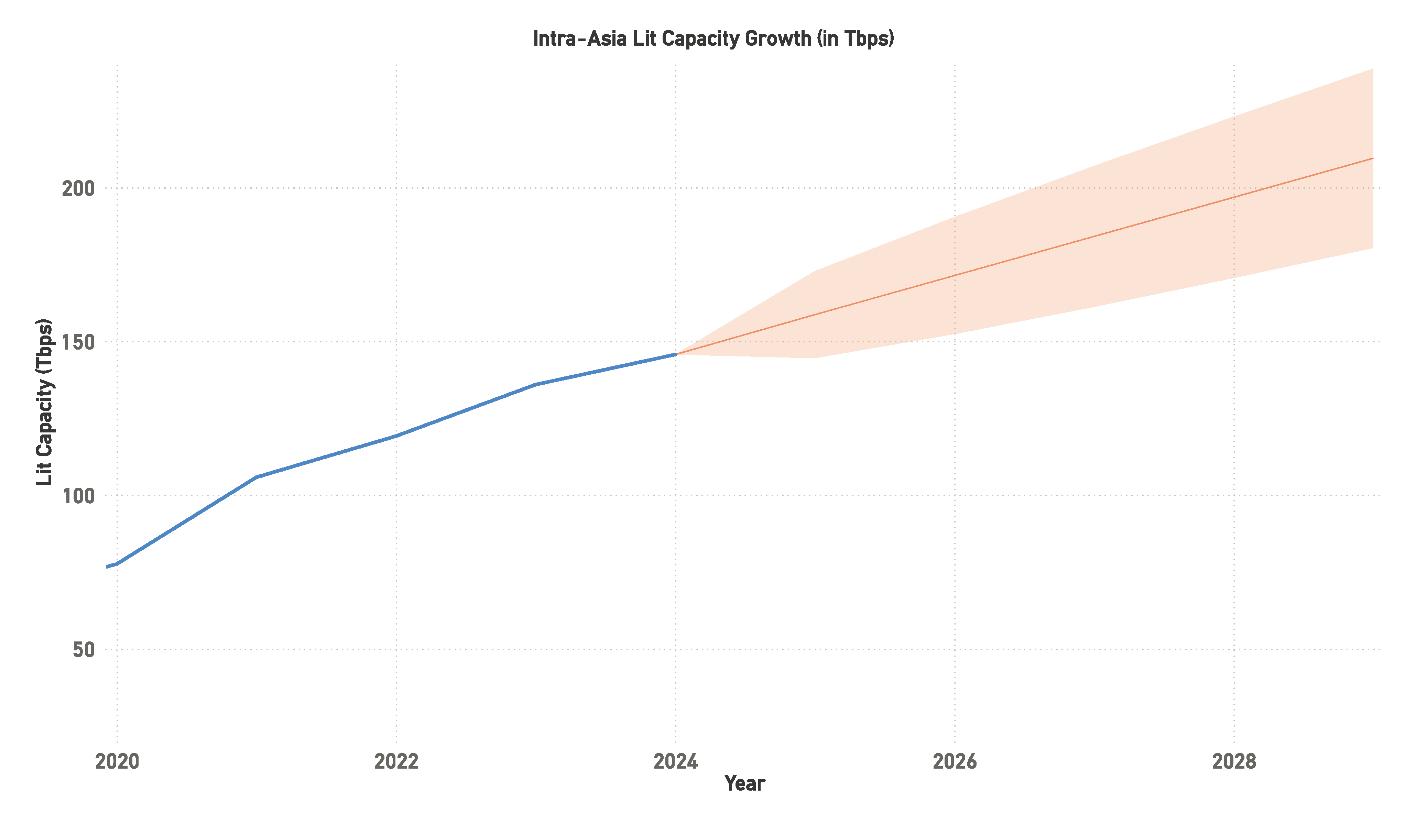

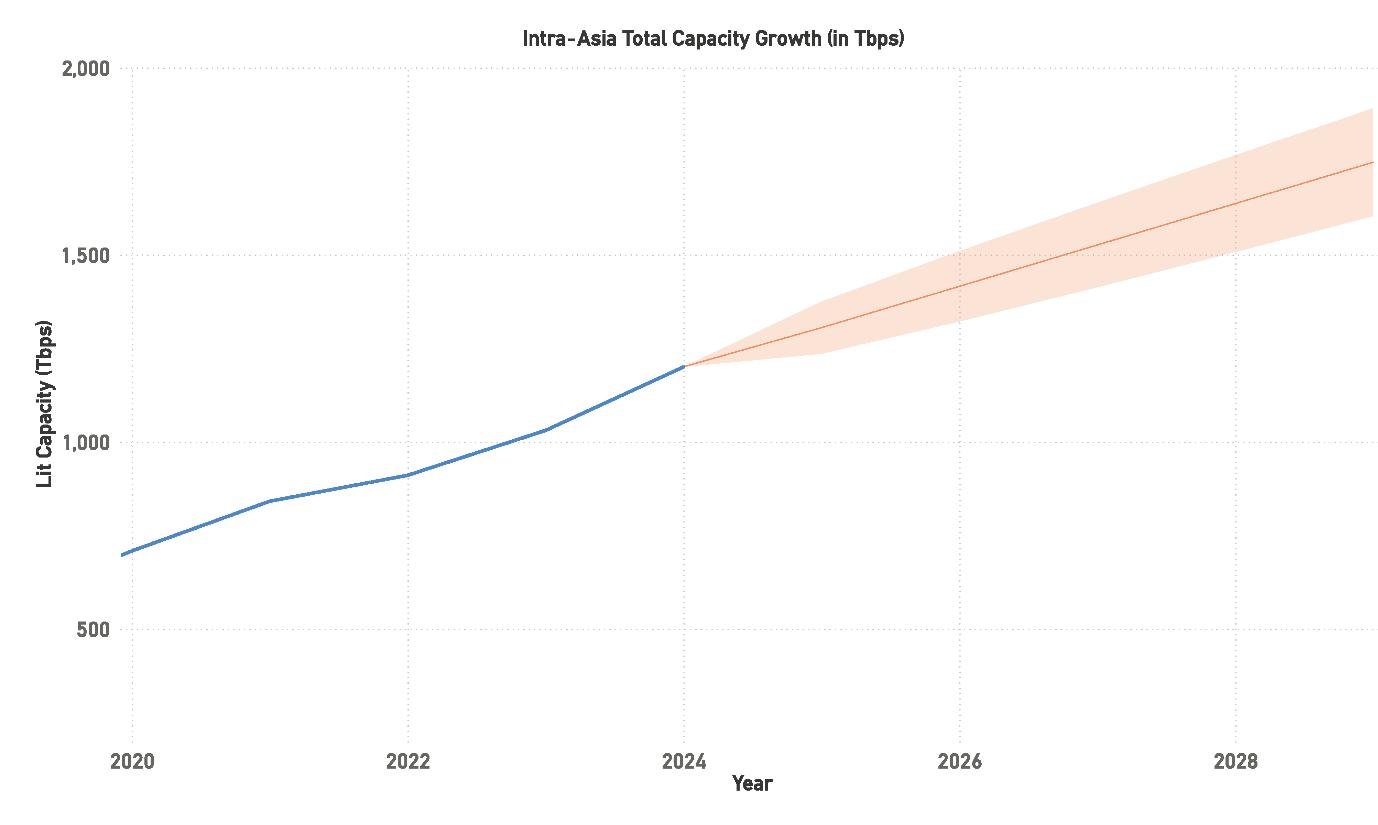

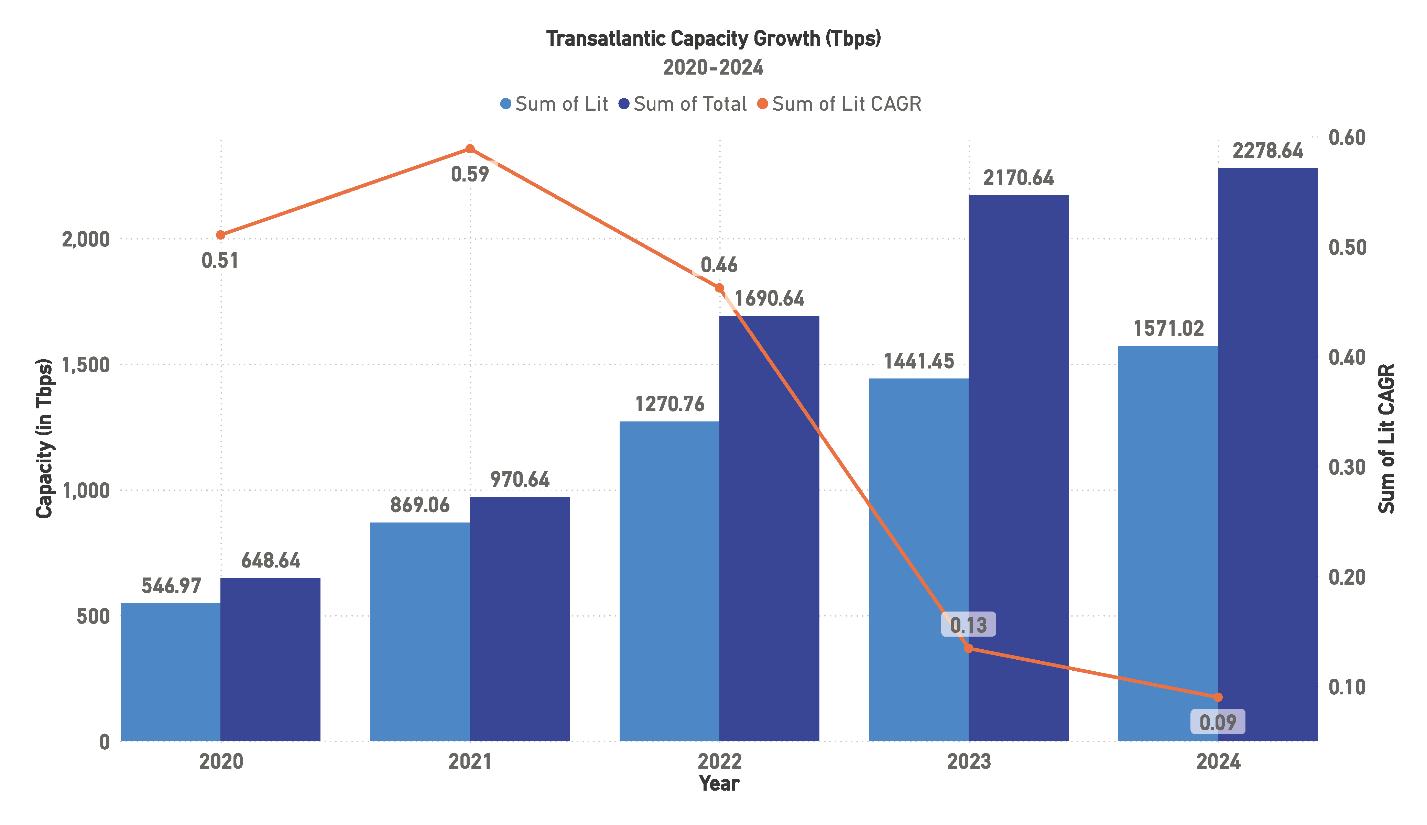

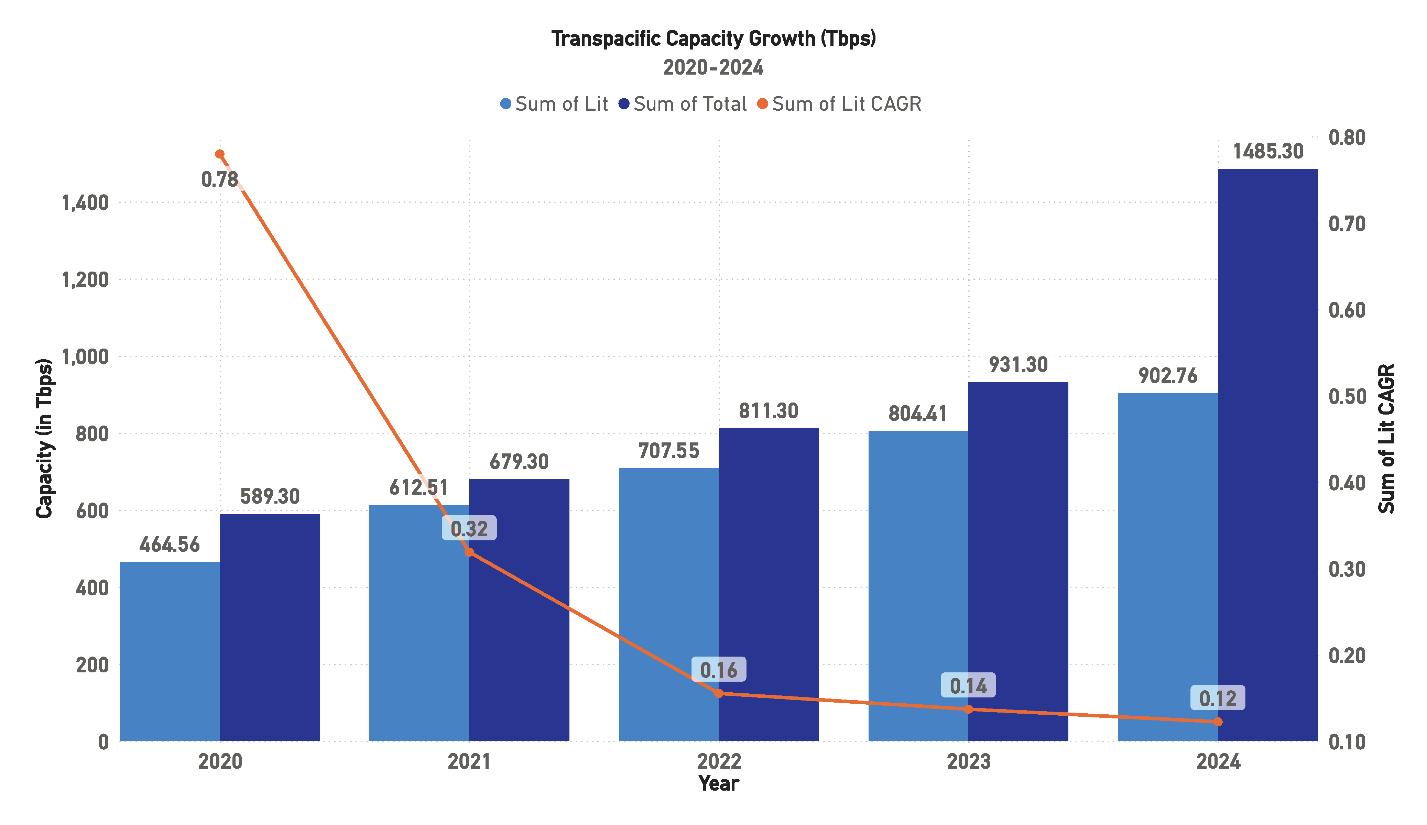

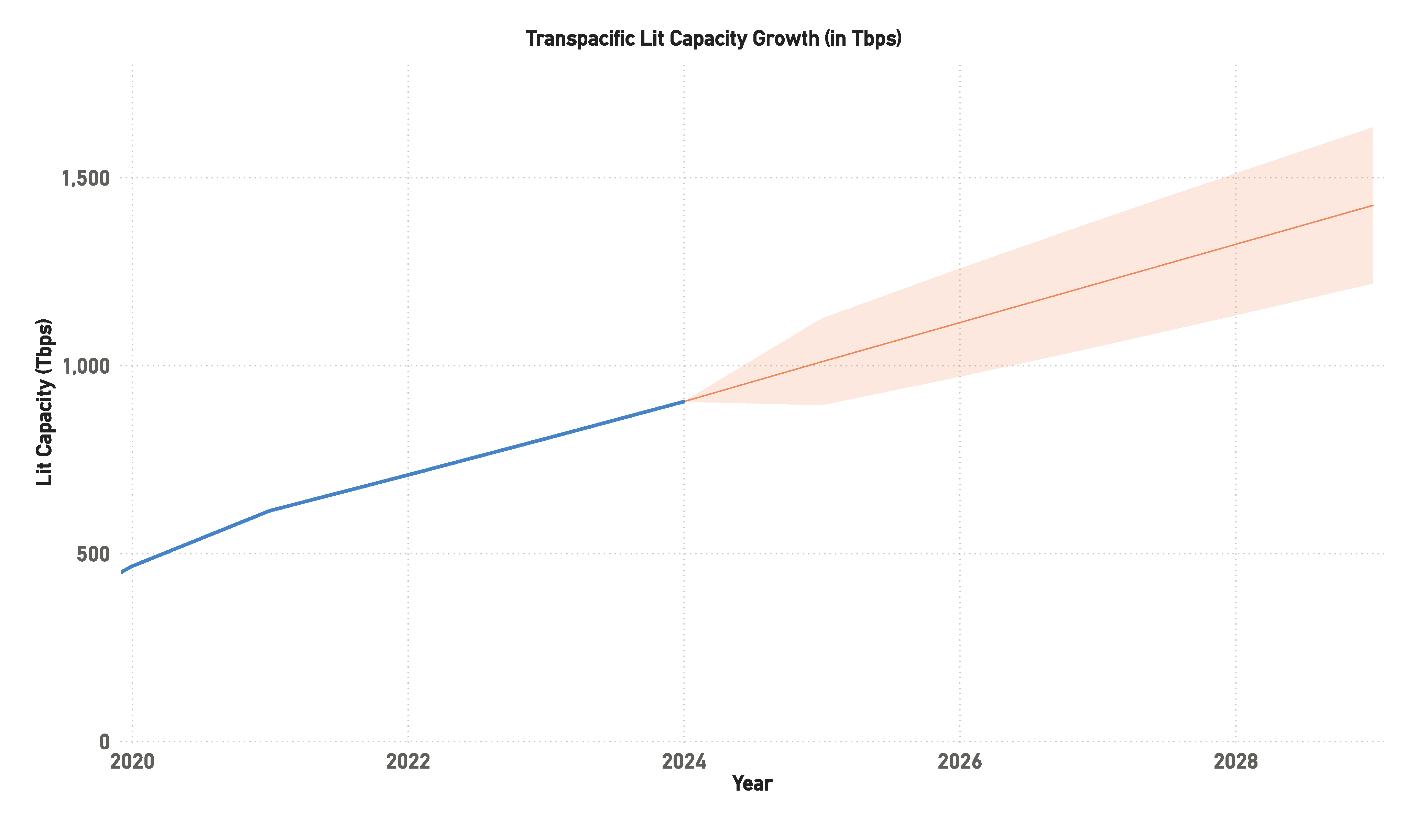

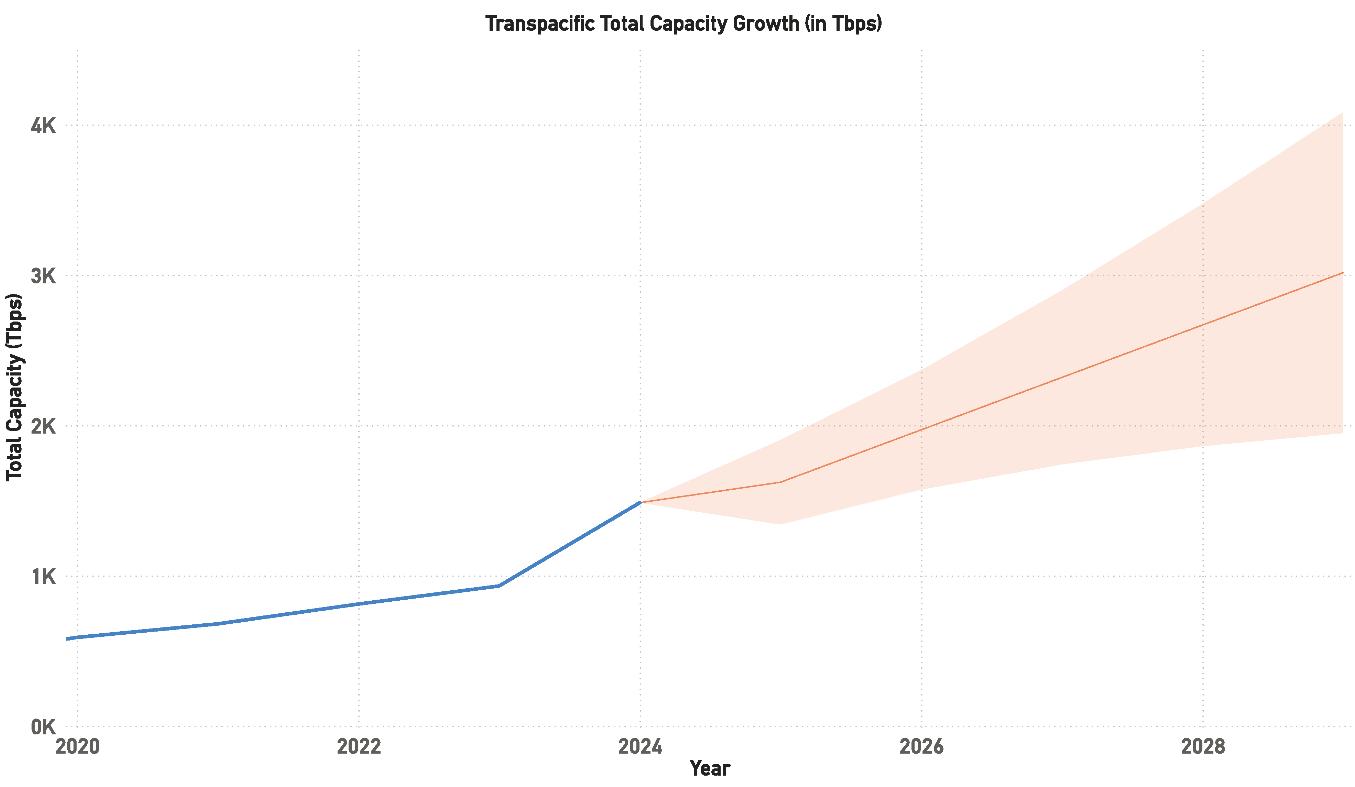

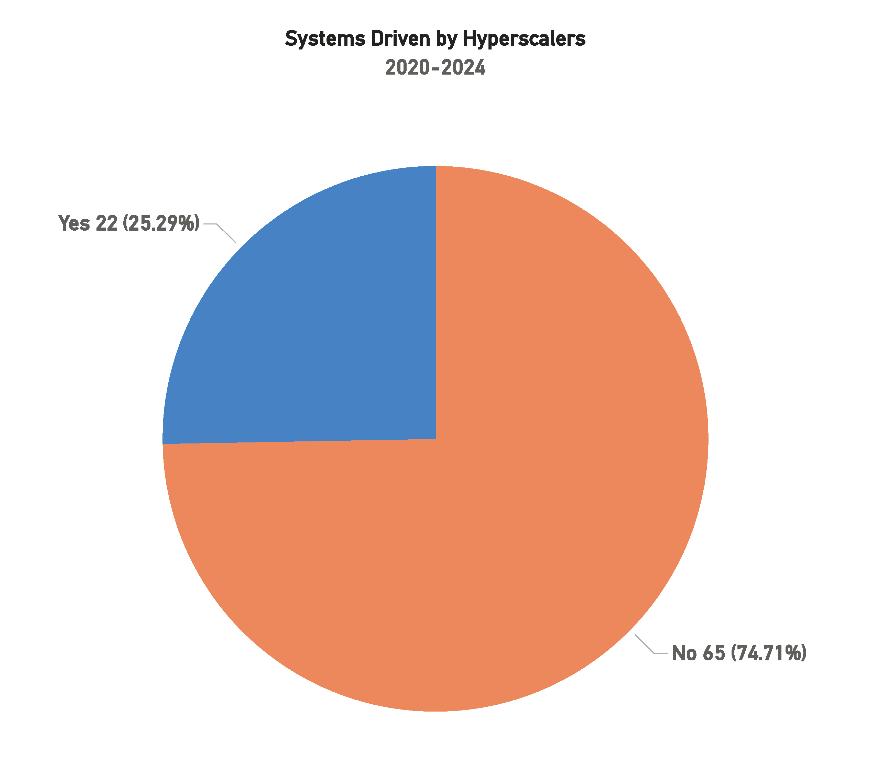

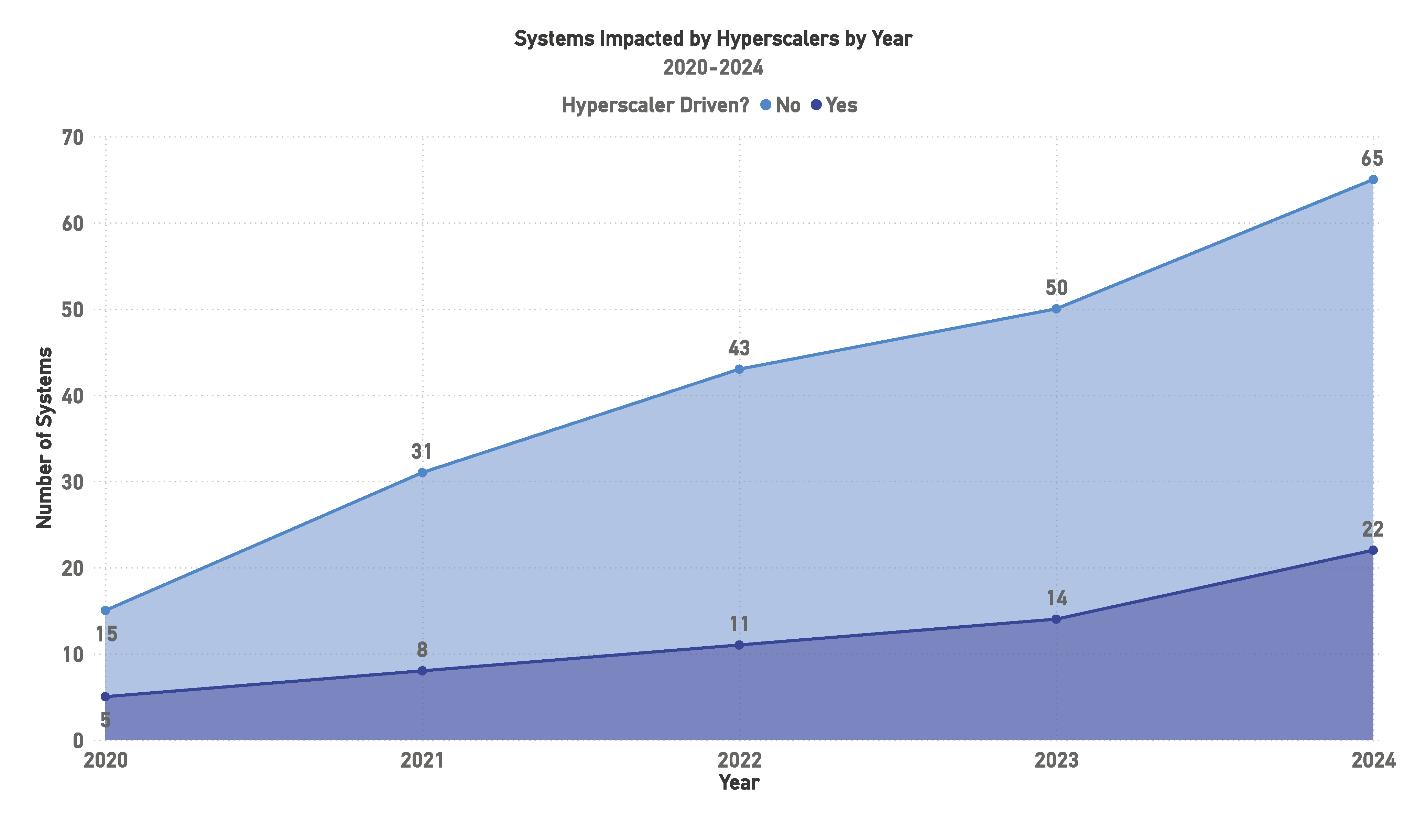

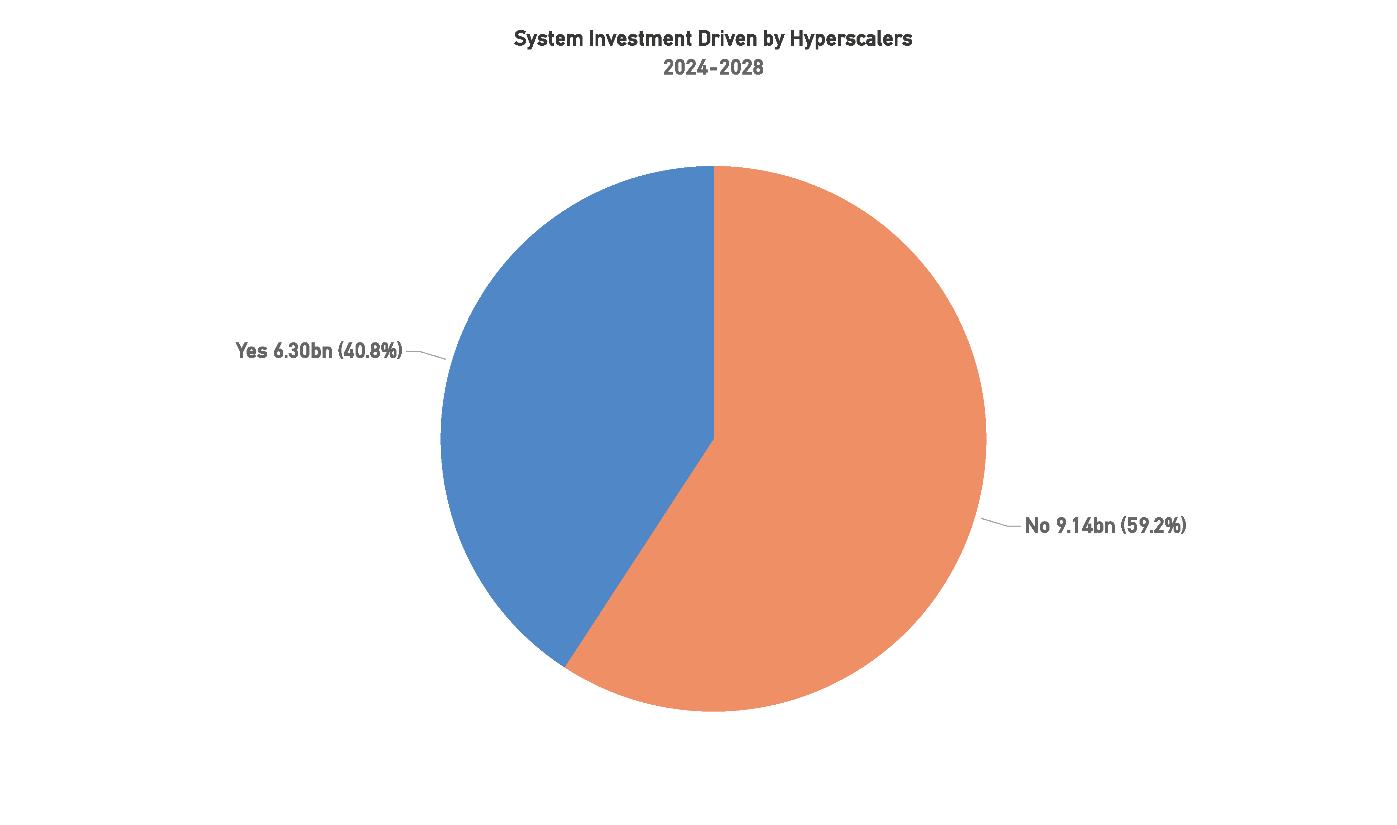

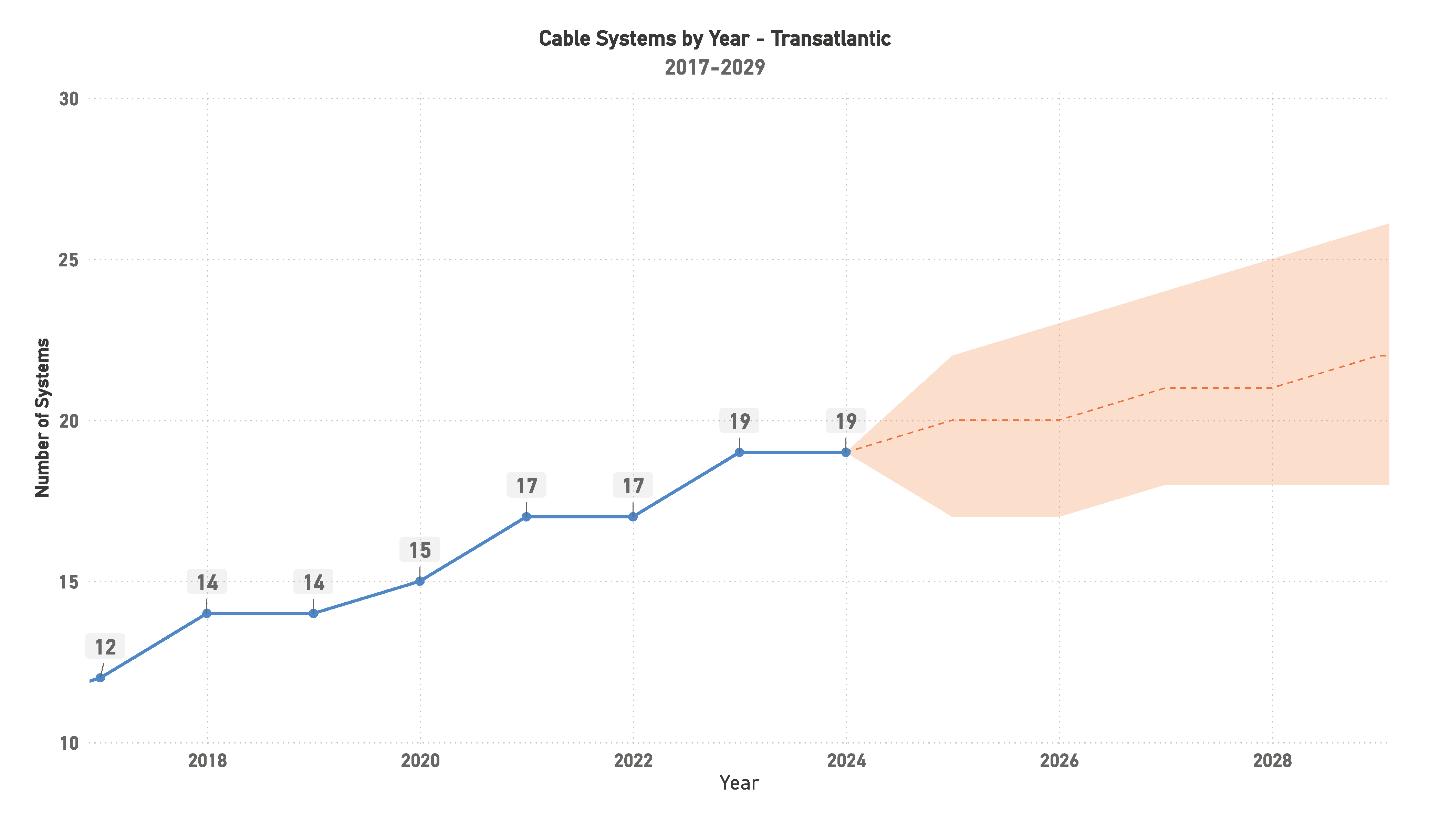

Between 2020 and 2024, capacity on major routes such as the Transpacific and Transatlantic regions has surged, propelled by increasing data transmission needs, cloud services, 5G networks, and streaming platforms. Hyperscalers—companies like Google, Amazon, and Microsoft—have played a key role in this expansion, particularly on routes between the Americas, Asia-Pacific, and Europe. While the Americas has seen more modest capacity growth, the Asia-Pacific region has rebounded strongly, reflecting the region’s growing importance in global data flows.

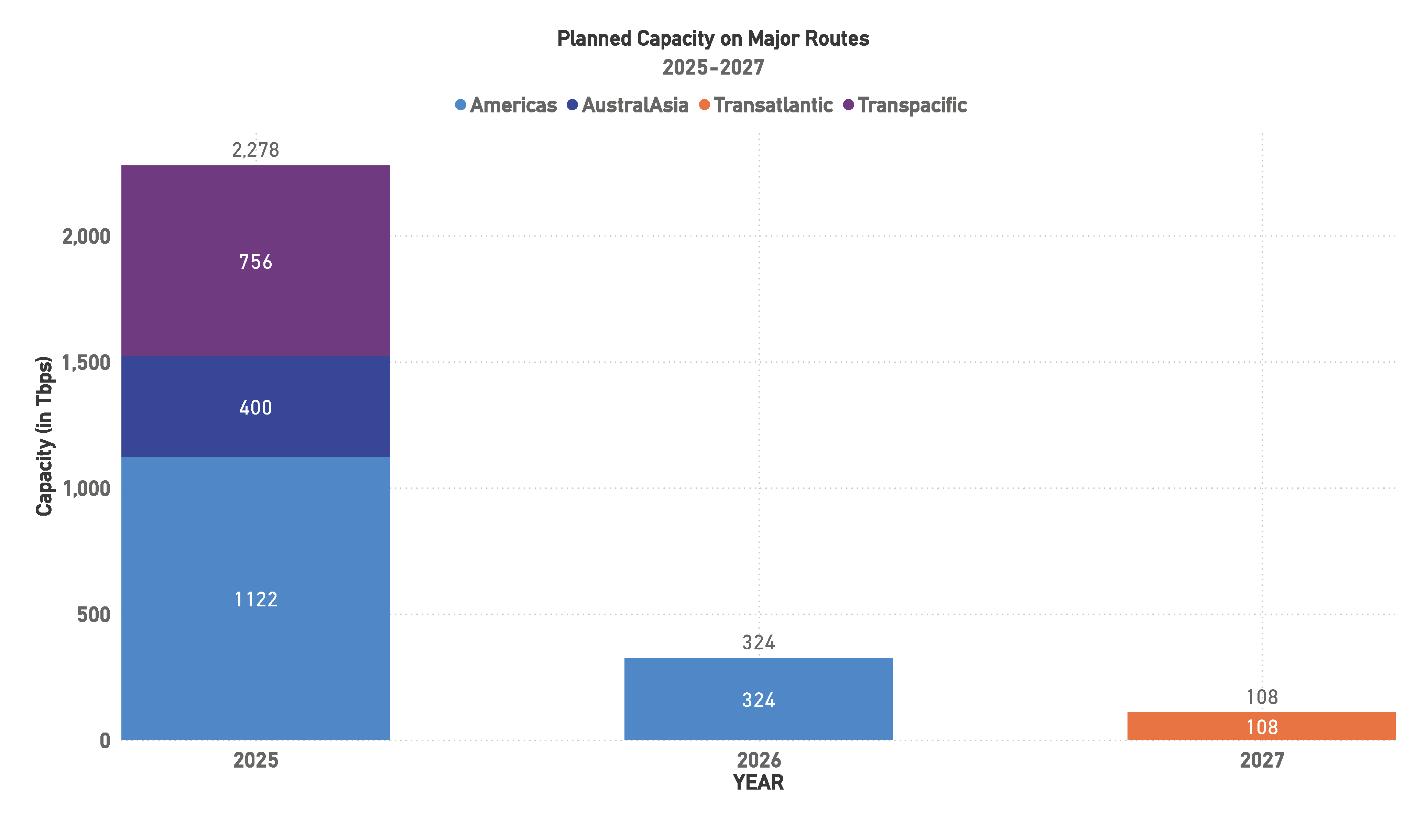

Despite these capacity expansions, there are signs that growth may taper off in the coming years. Projections for 2025 suggest a more measured increase in capacity, with the industry’s focus shifting towards system upgrades and efficiency improvements rather than new deployments. Technological advancements, such as 400G wavelengths and Space Division Multiplexing (SDM), are expected to play a pivotal role in supporting continued demand. Additionally, the rise of open cables and advances in optical technology have made it possible to extract greater performance from existing infrastructure.

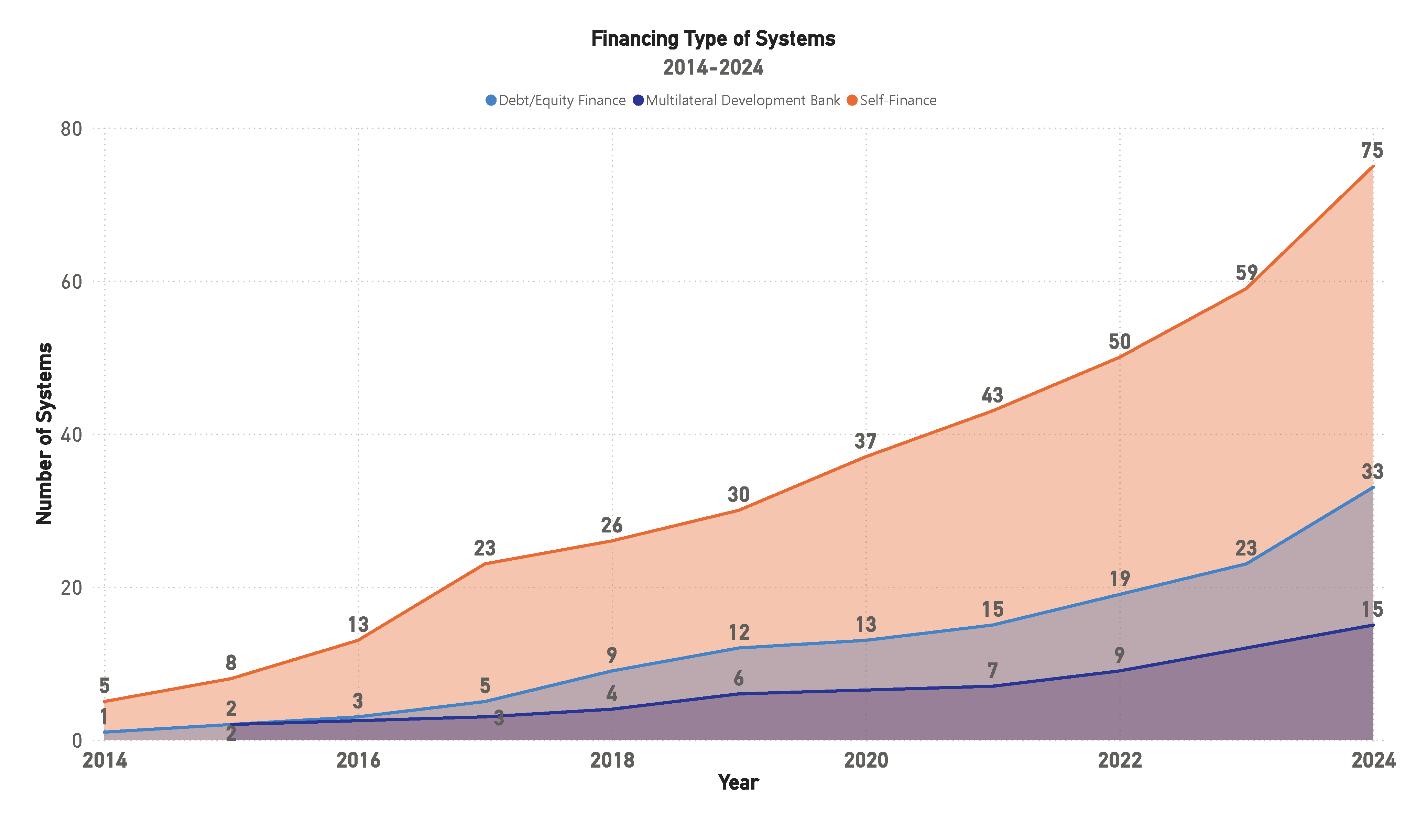

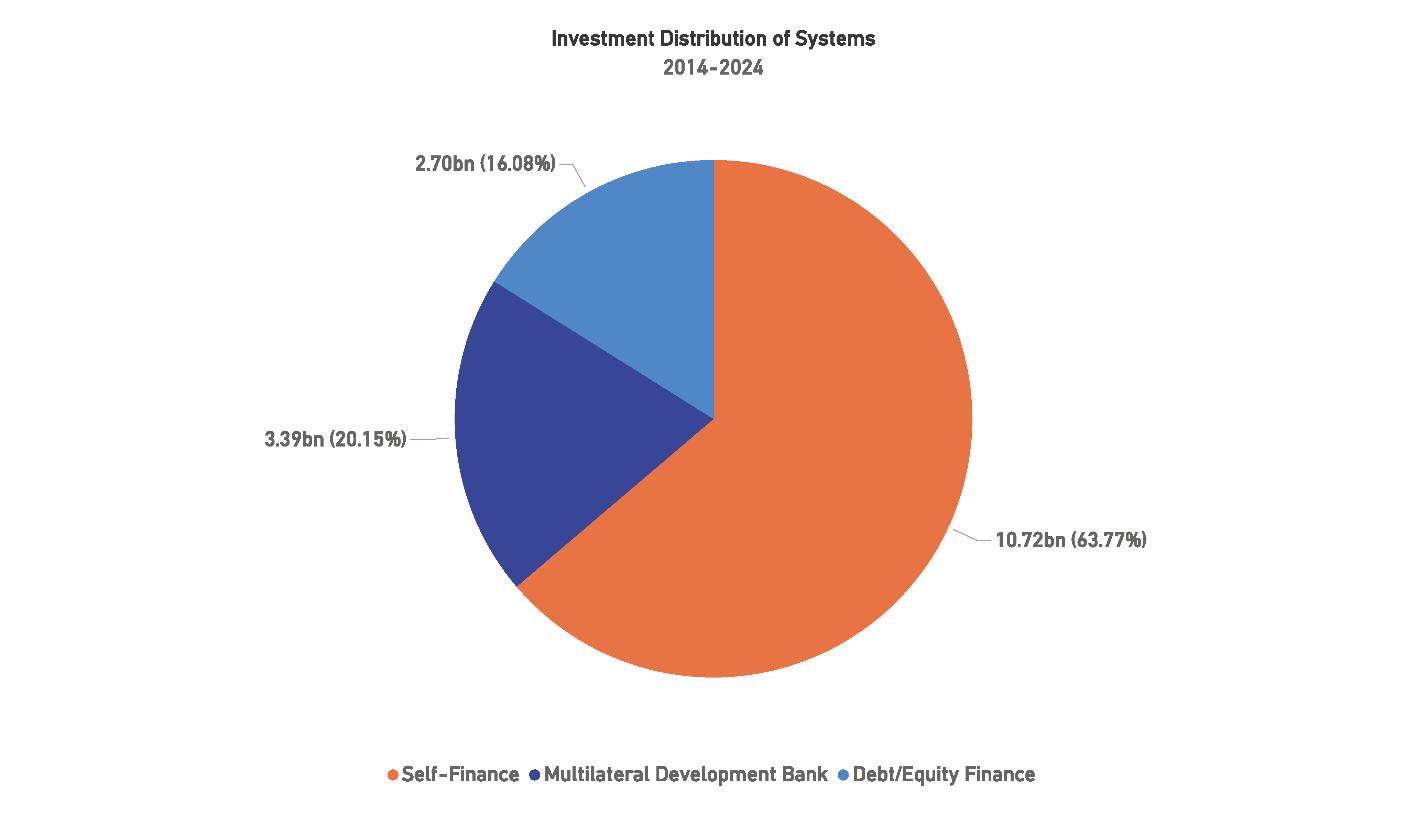

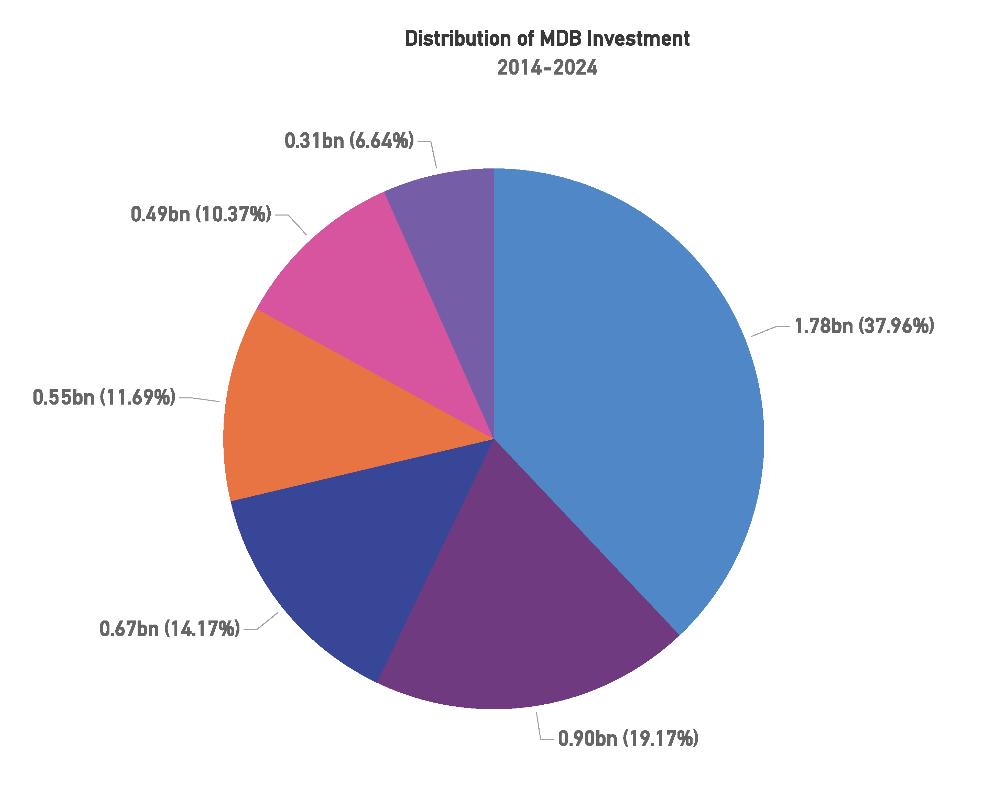

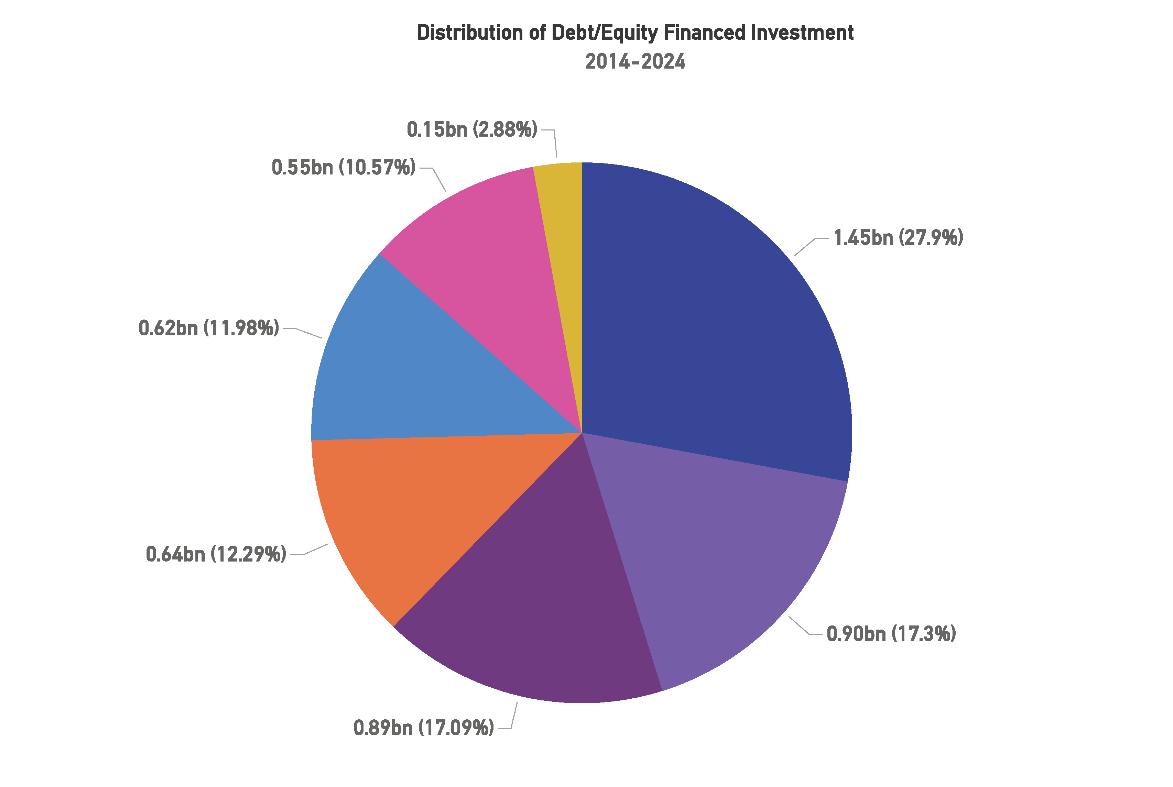

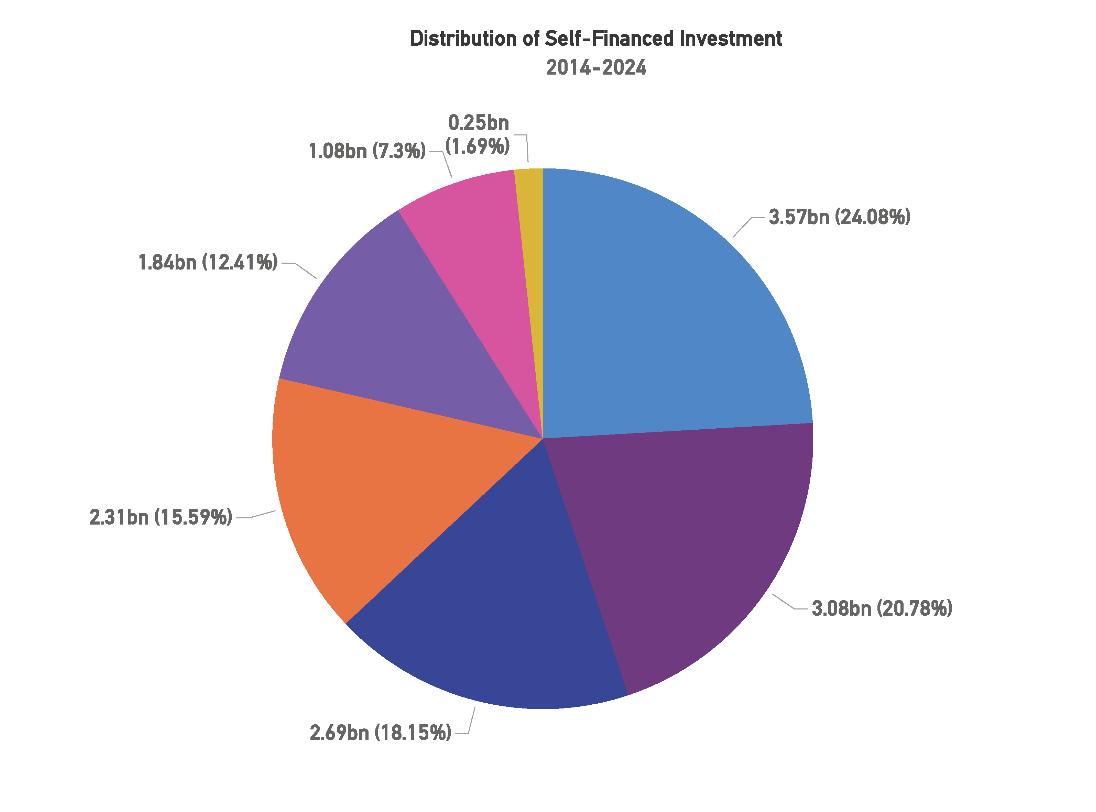

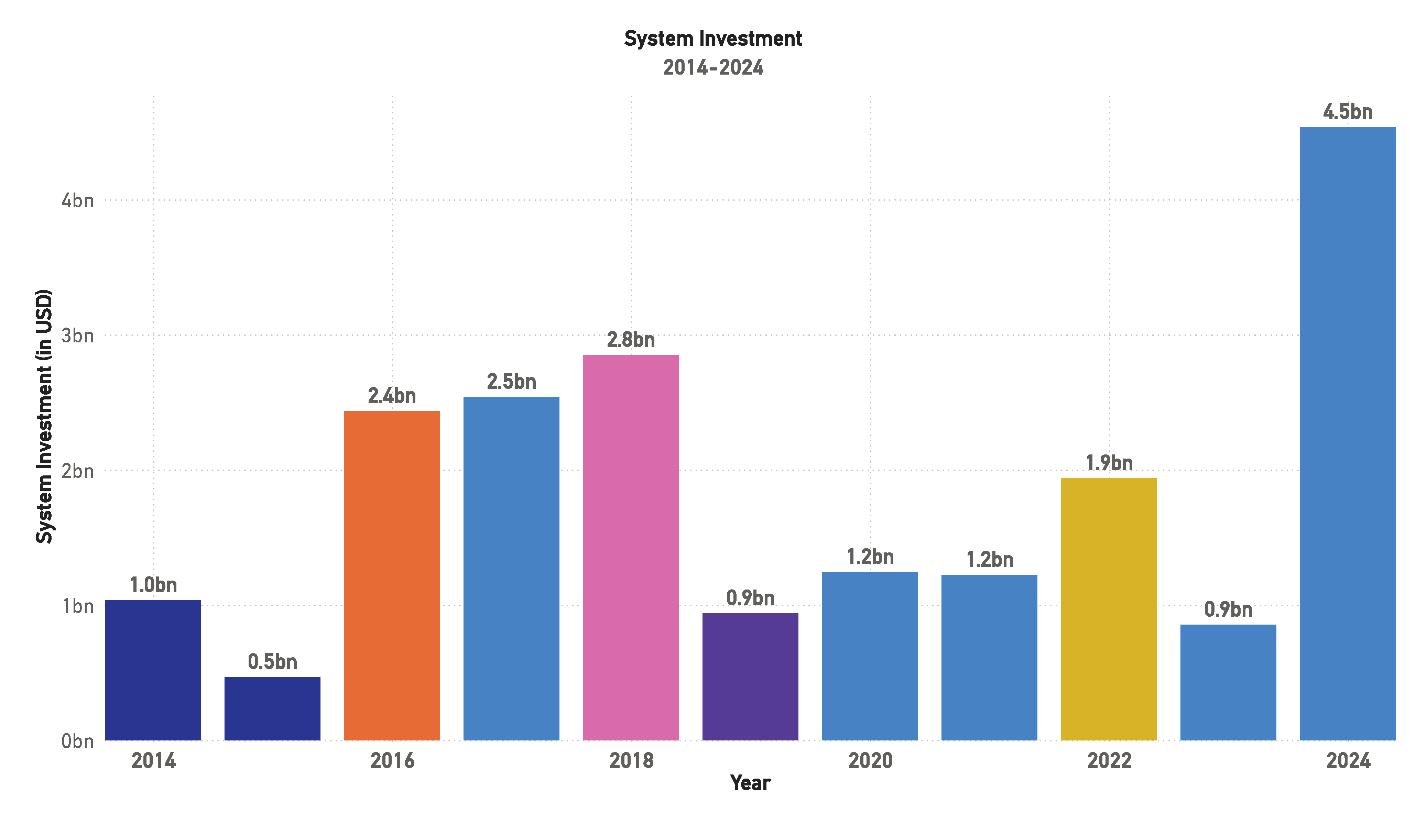

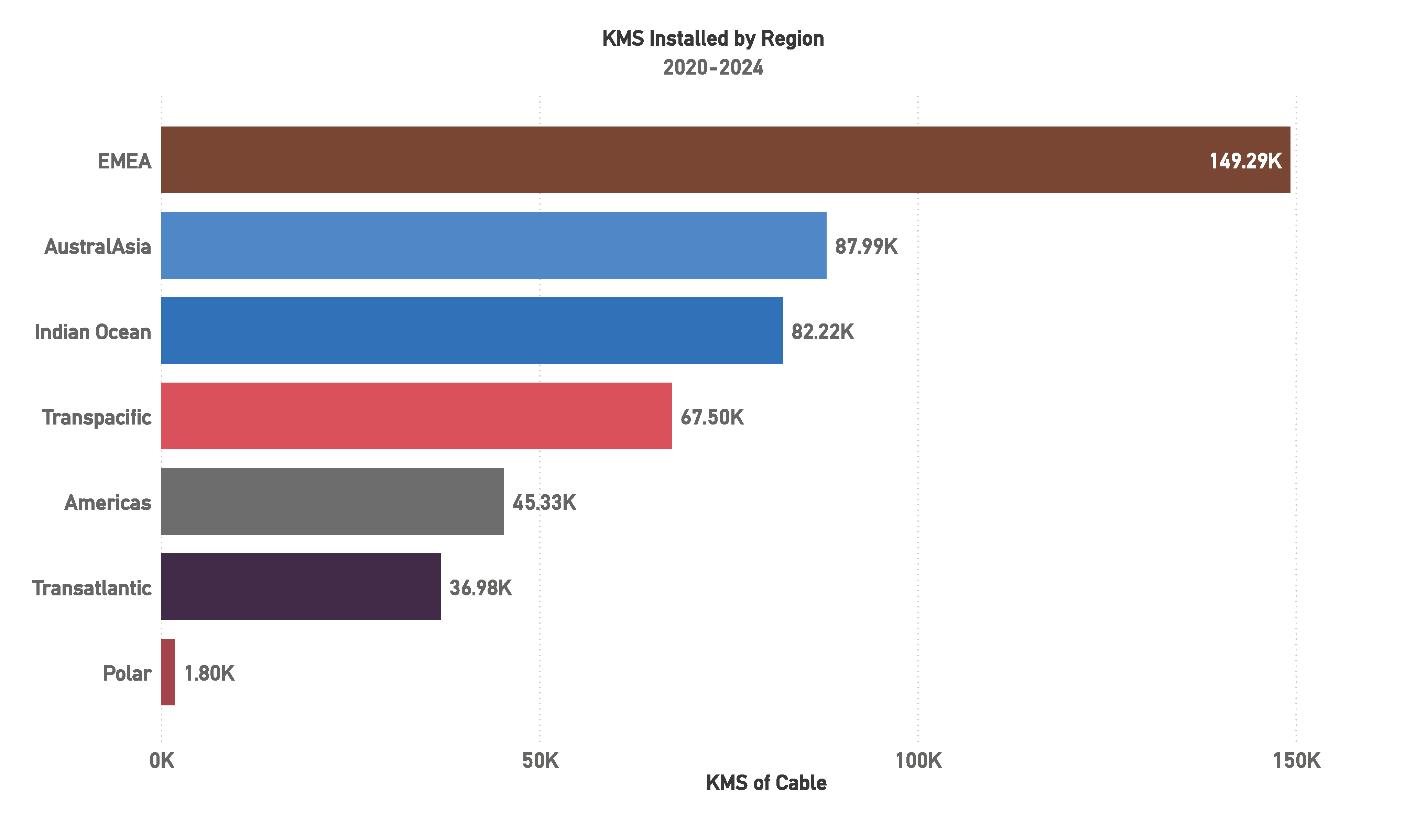

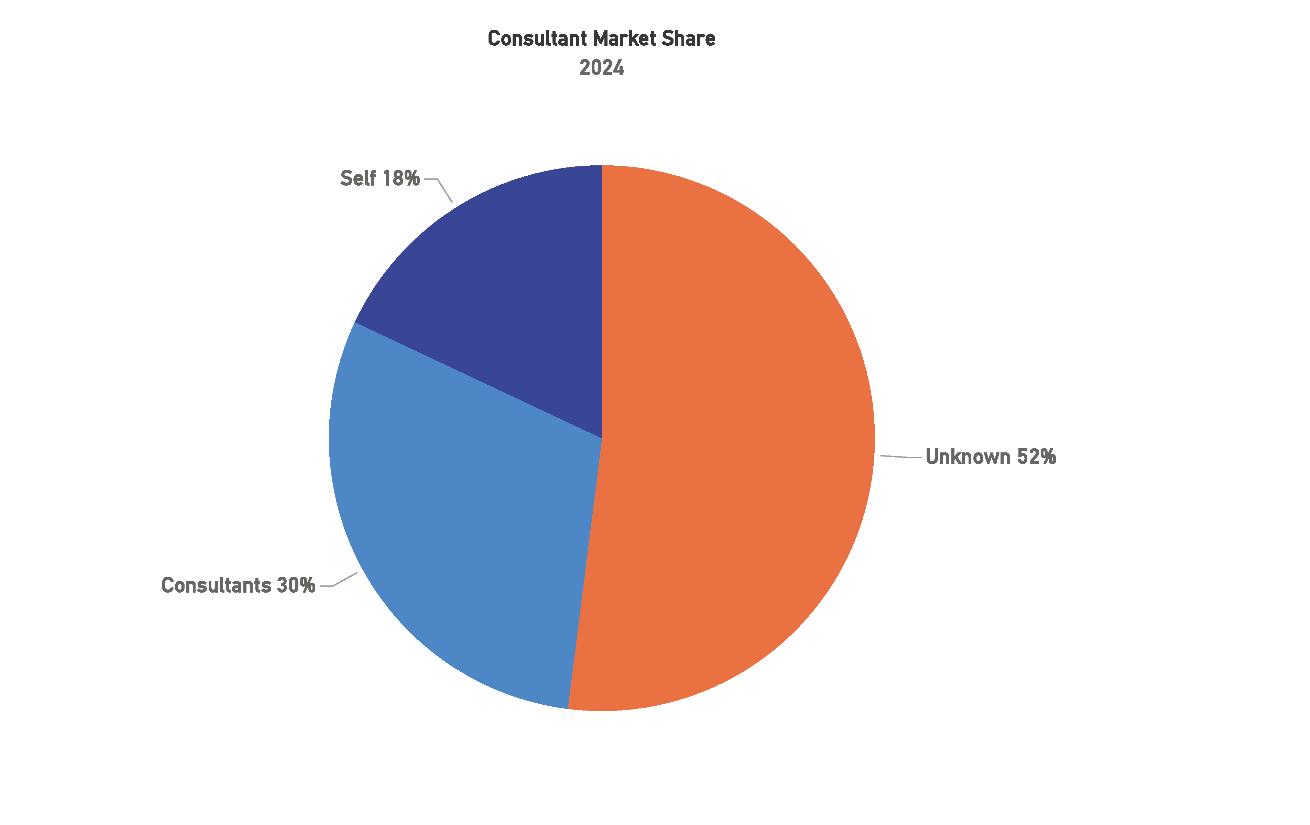

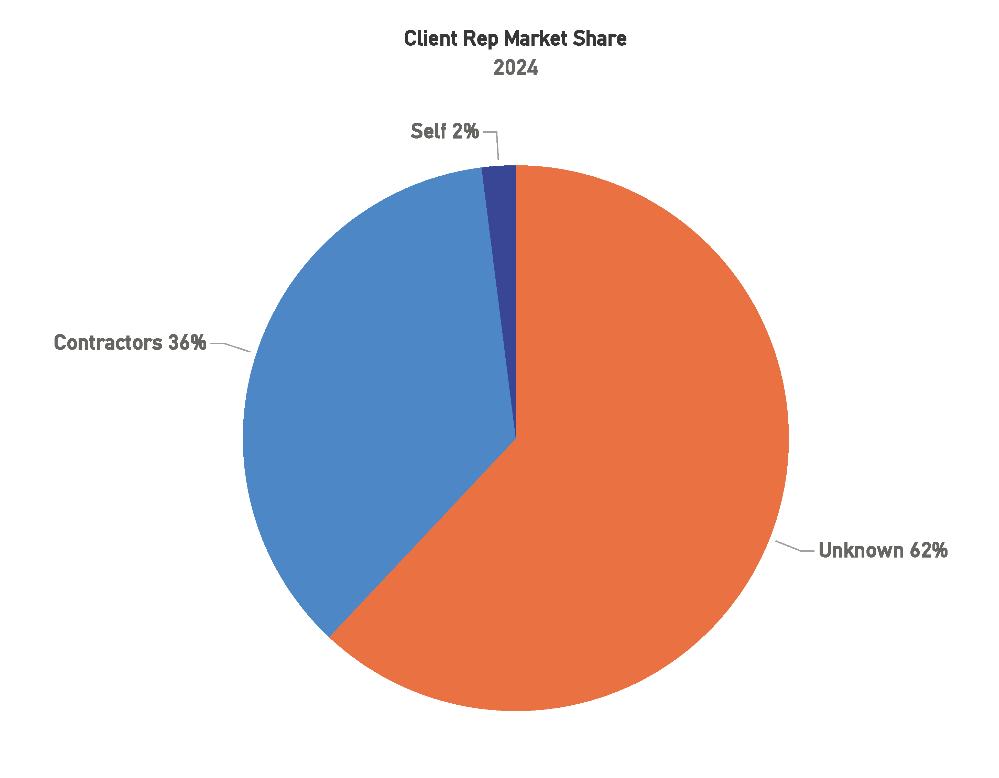

Ownership and financing trends in the submarine cable industry highlight the growing financial autonomy of operators. Self-financing now accounts for nearly two-thirds of all investments, underscoring the industry’s maturity and the ability of operators to independently fund large-scale projects. Multilateral Development Banks (MDBs) continue to provide essential support in developing regions, where access to traditional financing is limited. Debt and equity financing, while smaller in scale, have gained traction as operators increasingly seek to share financial risk. Regionally, MDB financing has been concentrated in EMEA and the Transpacific regions, reflecting ongoing efforts to address connectivity gaps in these areas.

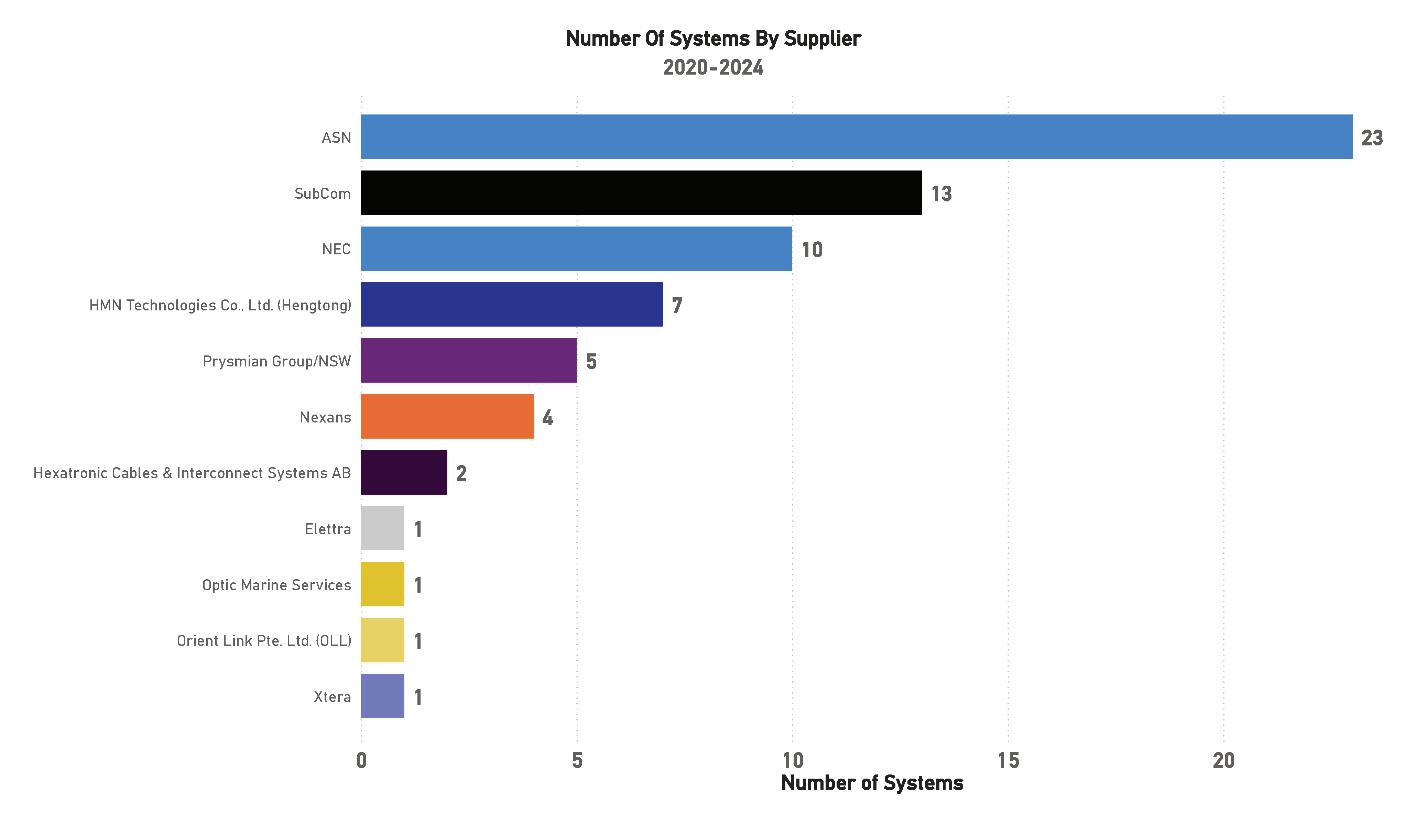

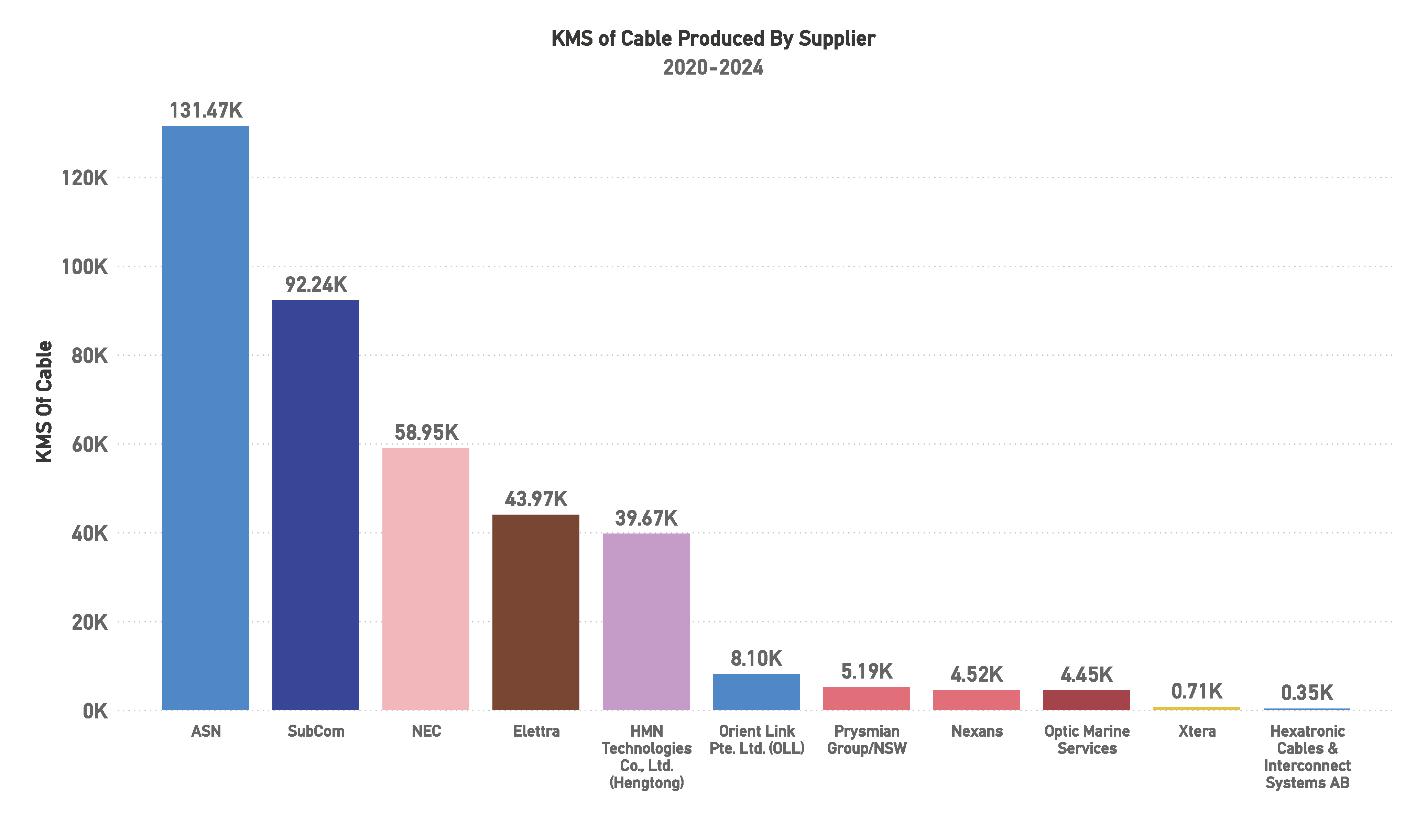

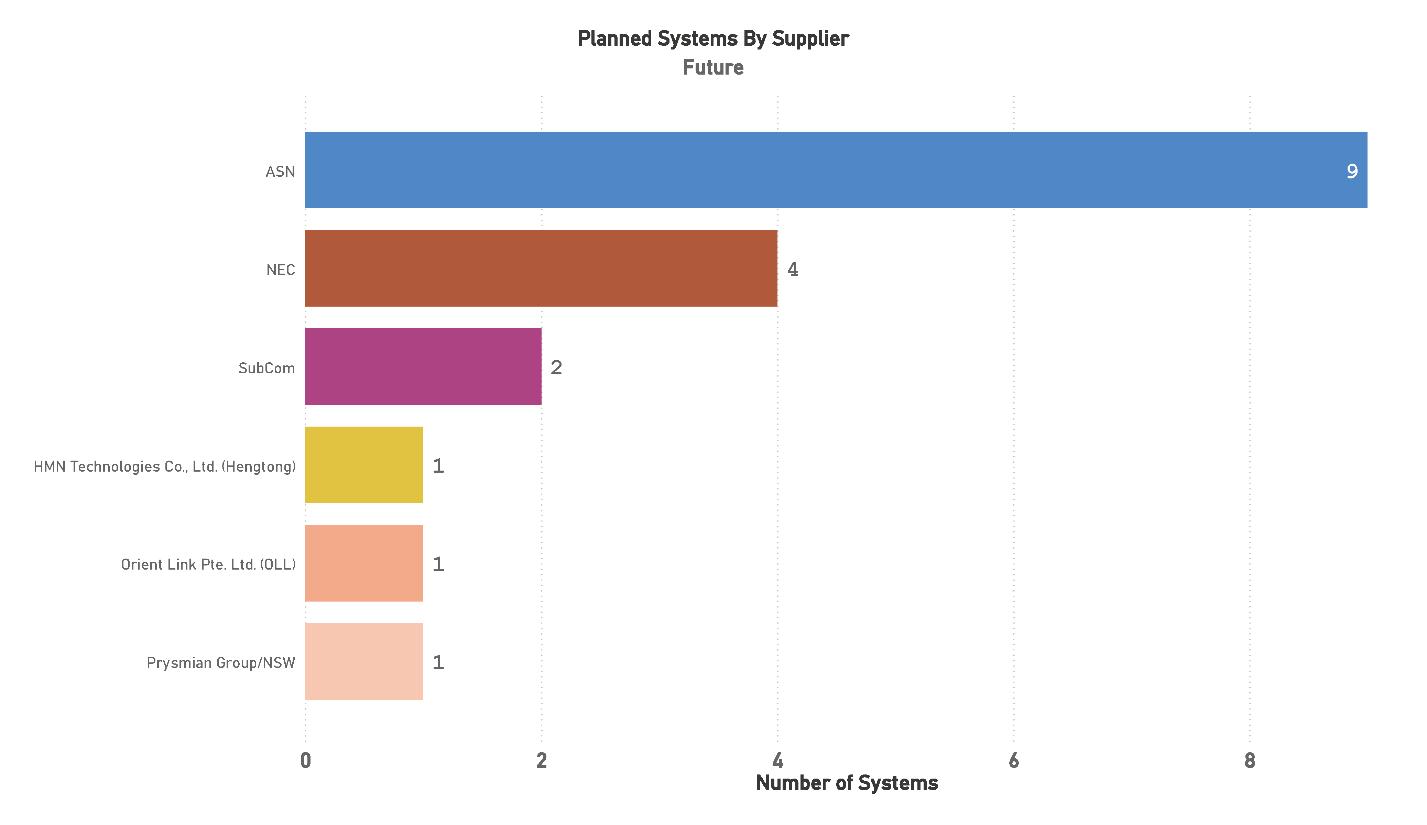

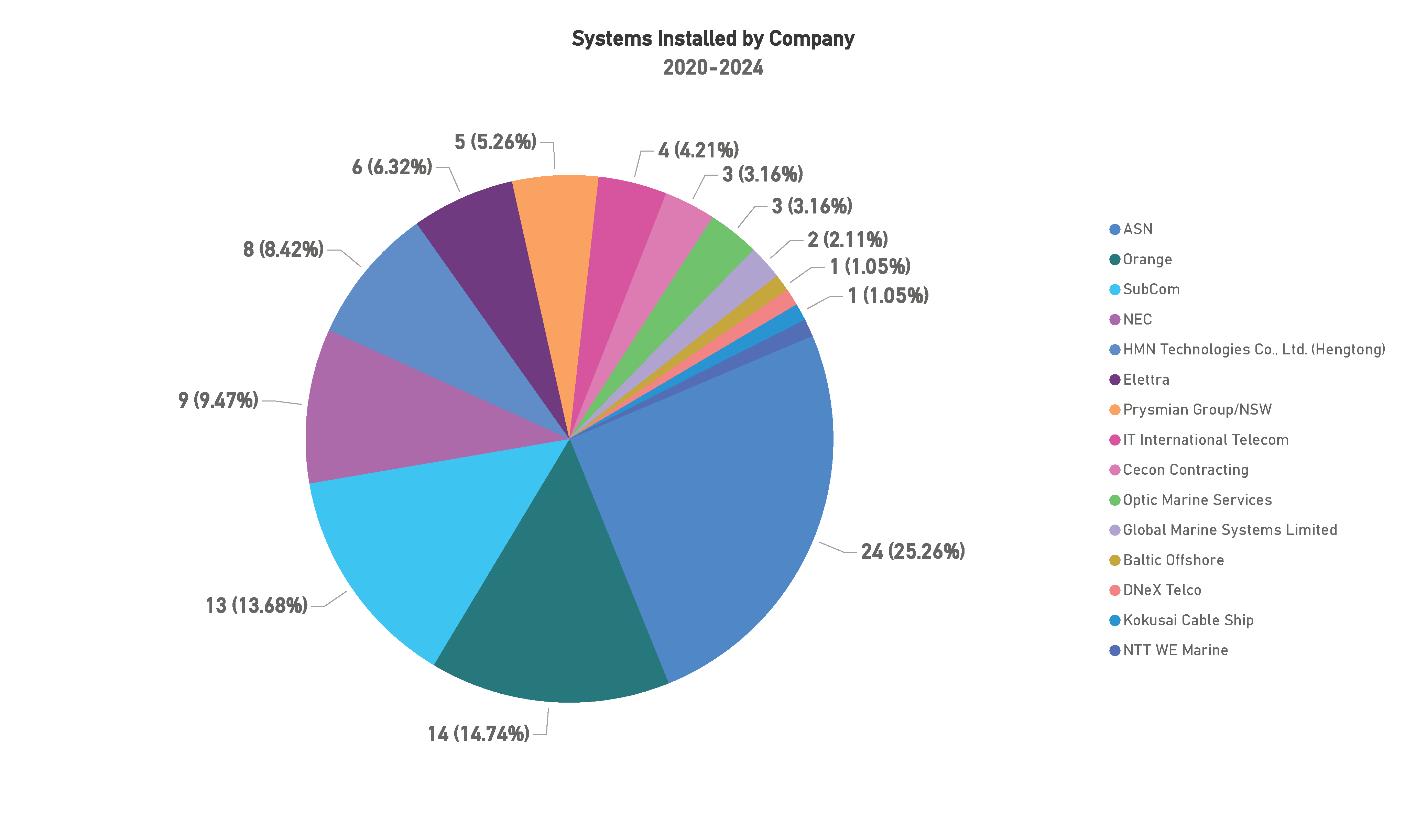

Suppliers such as Alcatel Submarine Networks (ASN), SubCom, and NEC have dominated the market from 2020 to 2024, with ASN emerging as the industry leader. These suppliers are also diversifying into offshore wind projects, capitalizing on synergies between subsea communications and energy infrastructure. Looking ahead, ASN is poised to maintain its lead in the market, with several major projects

The global submarine cable industry continues to experience dynamic growth

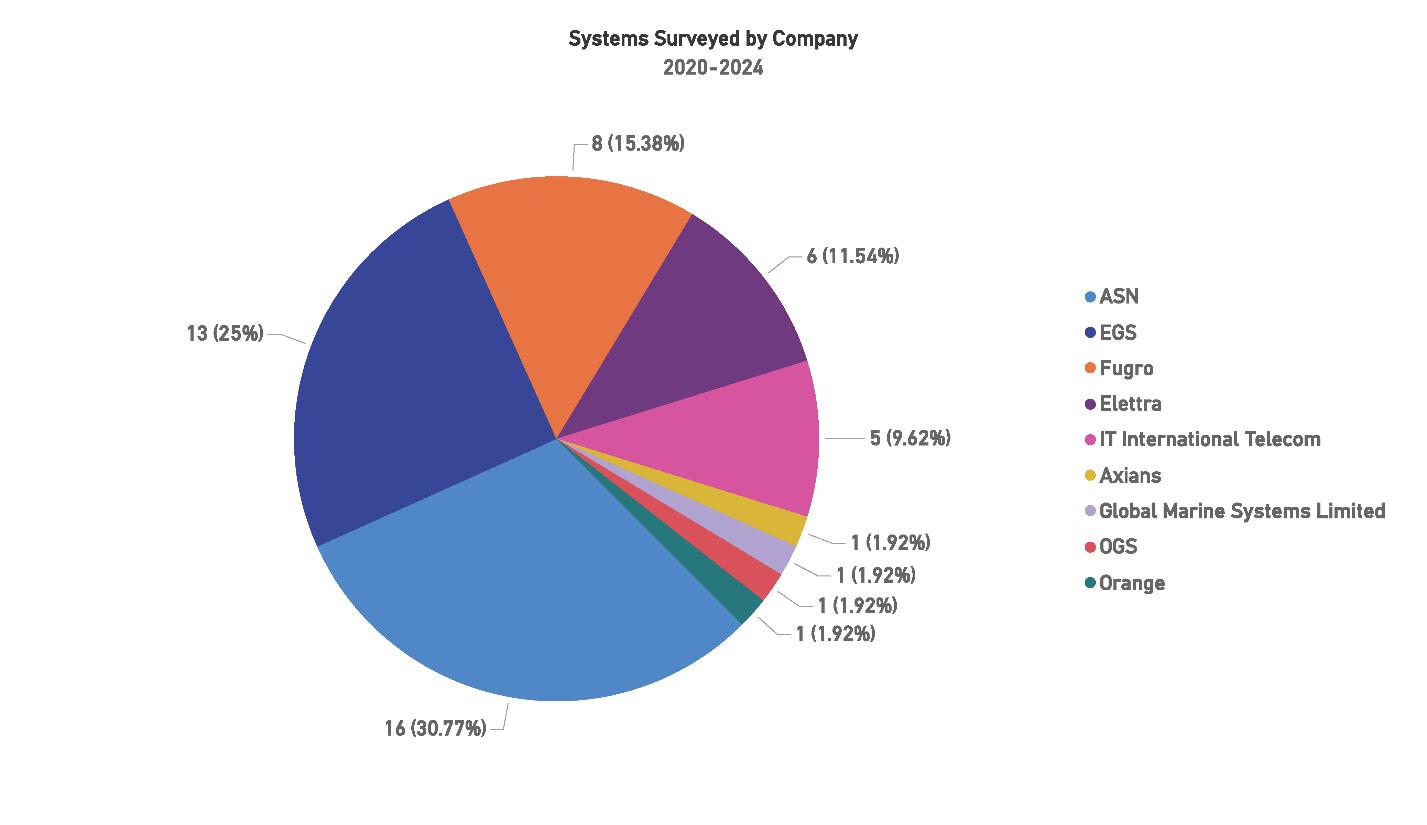

planned for 2024-2027. Surveying activity, a critical component of cable deployment, has also seen growth, with ASN and EGS leading the field in ensuring the safe installation of new systems.

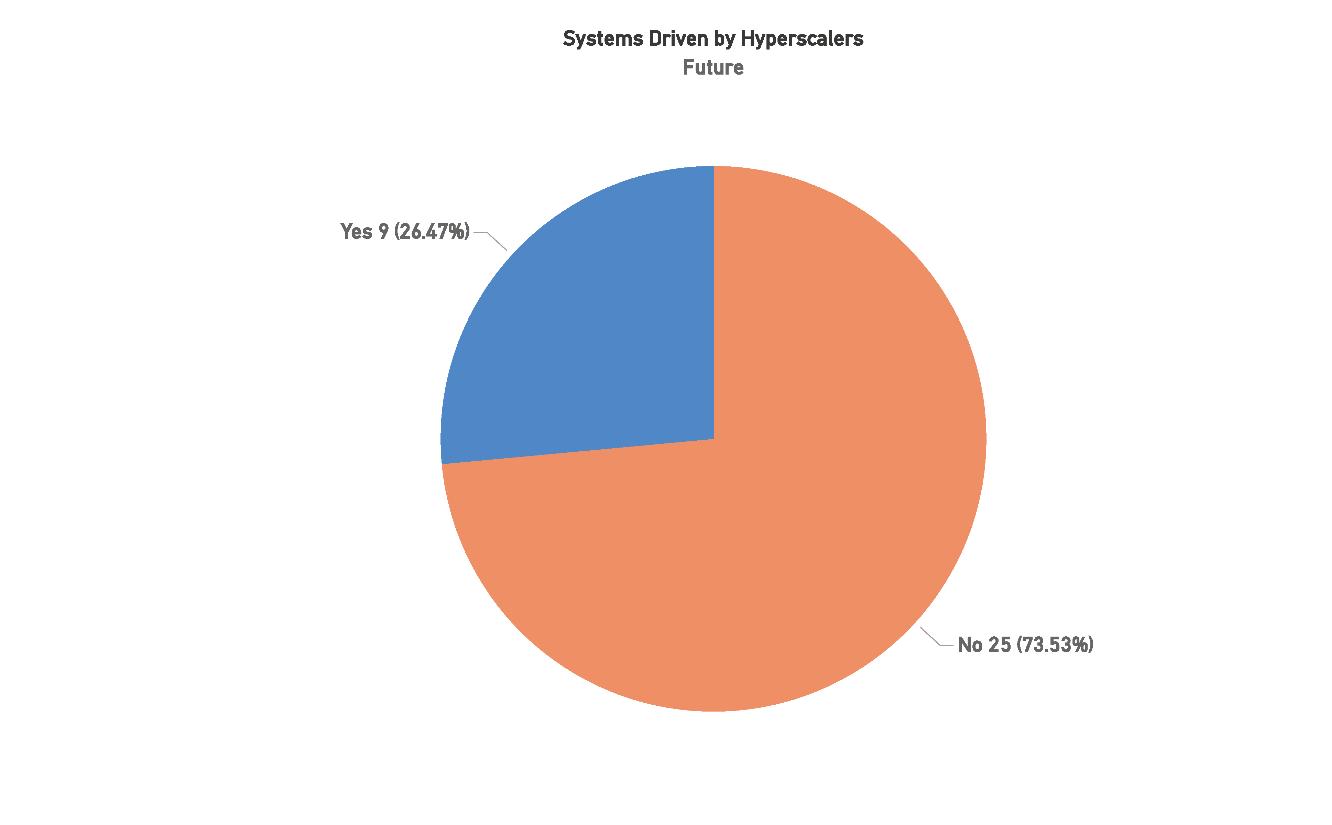

The submarine cable industry’s regulatory landscape has evolved significantly in 2024, with global initiatives aimed at improving resilience and security. The International Telecommunication Union (ITU) and the European Commission have spearheaded efforts to foster international collaboration, creating advisory bodies and expert groups to address vulnerabilities in subsea infrastructure. In parallel, the dominance of Hyperscalers in building and controlling new cable systems has raised concerns about competition and market diversity. Regulatory strategies are being developed to protect national telecom sectors while ensuring the resilience of global connectivity.

Geopolitical tensions, particularly in regions like the South China Sea, have also impacted the industry’s regulatory focus. Security initiatives, such as NATO’s critical infrastructure monitoring, reflect the increasing global attention on safeguarding submarine cables from malicious actors. At the same time, countries such as Kenya, Ghana, and South Africa have streamlined their licensing processes for cable installation, promoting international investment. These regulatory adaptations highlight the industry’s growing importance in both economic and security contexts.

Mergers and acquisitions continue to reshape the industry landscape. Notable deals in 2024 include Nokia’s sale of a majority stake in Alcatel Submarine Networks to the French government, and Nokia’s acquisition of Infinera to bolster its optical networking capabilities. These transactions, alongside the acquisition of Telecom Italia’s Sparkle unit by KKR and the Italian government, signal a continued focus

on enhancing capacity, security, and resilience in the face of growing demand. Such moves reflect the industry’s strategic importance in maintaining global connectivity amid increasing geopolitical risks.

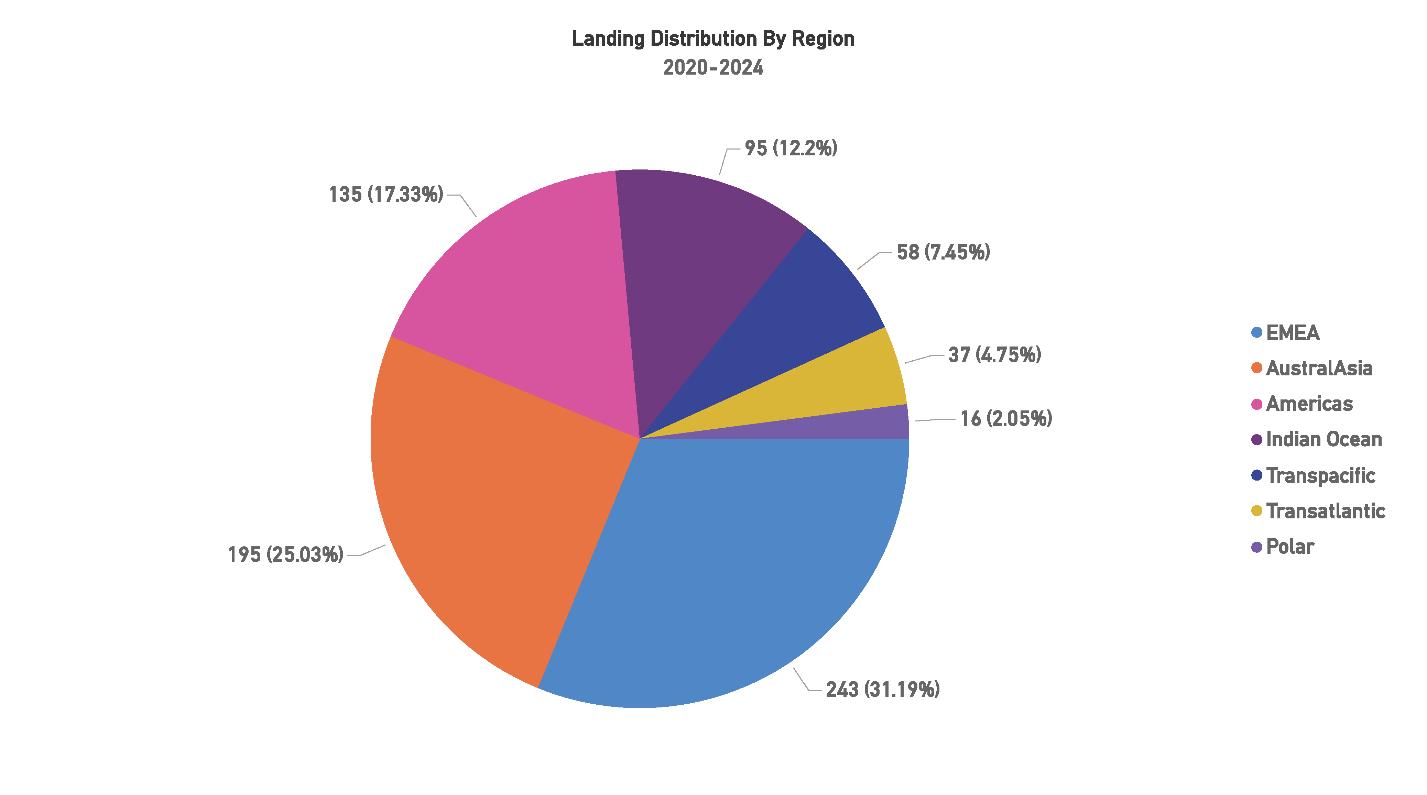

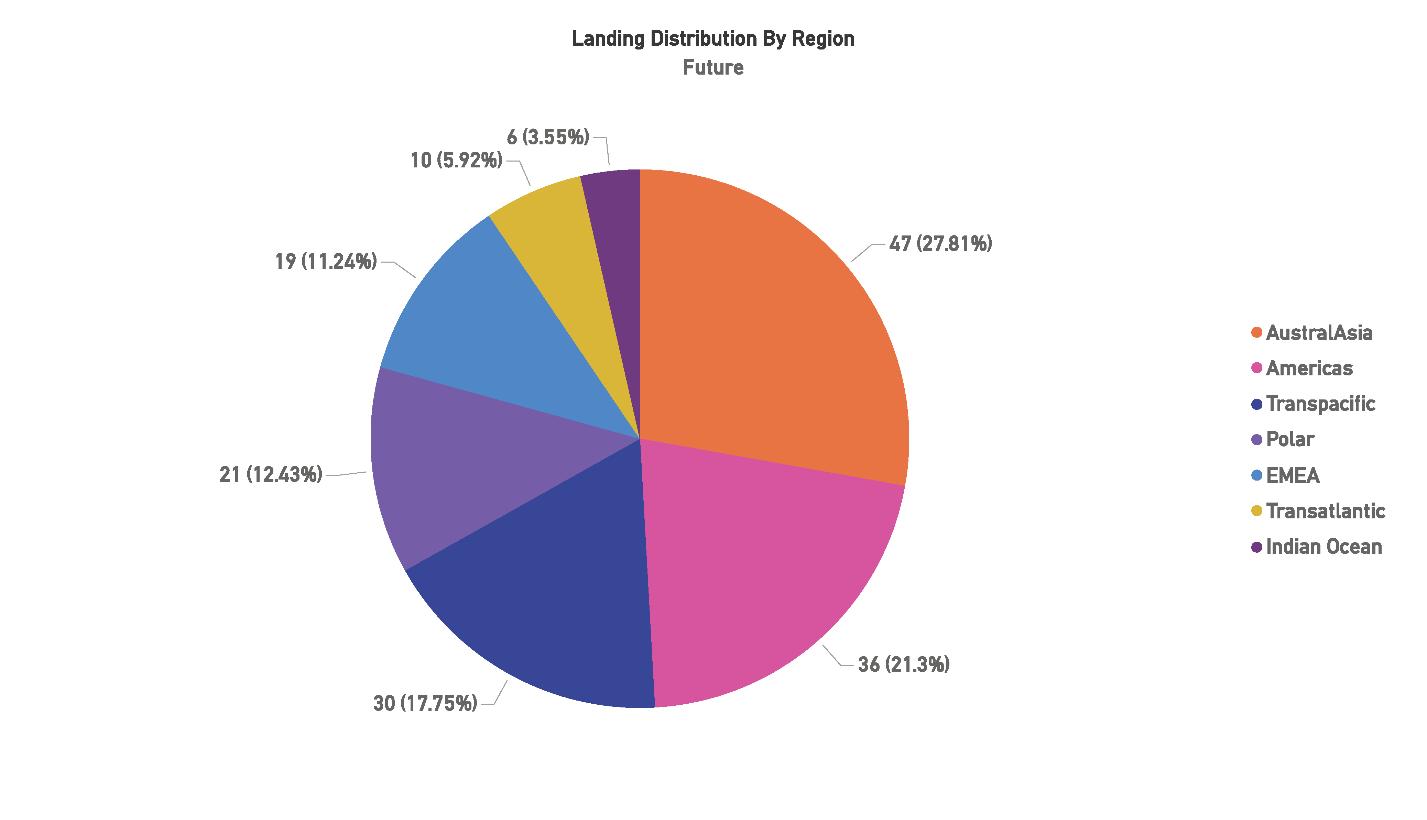

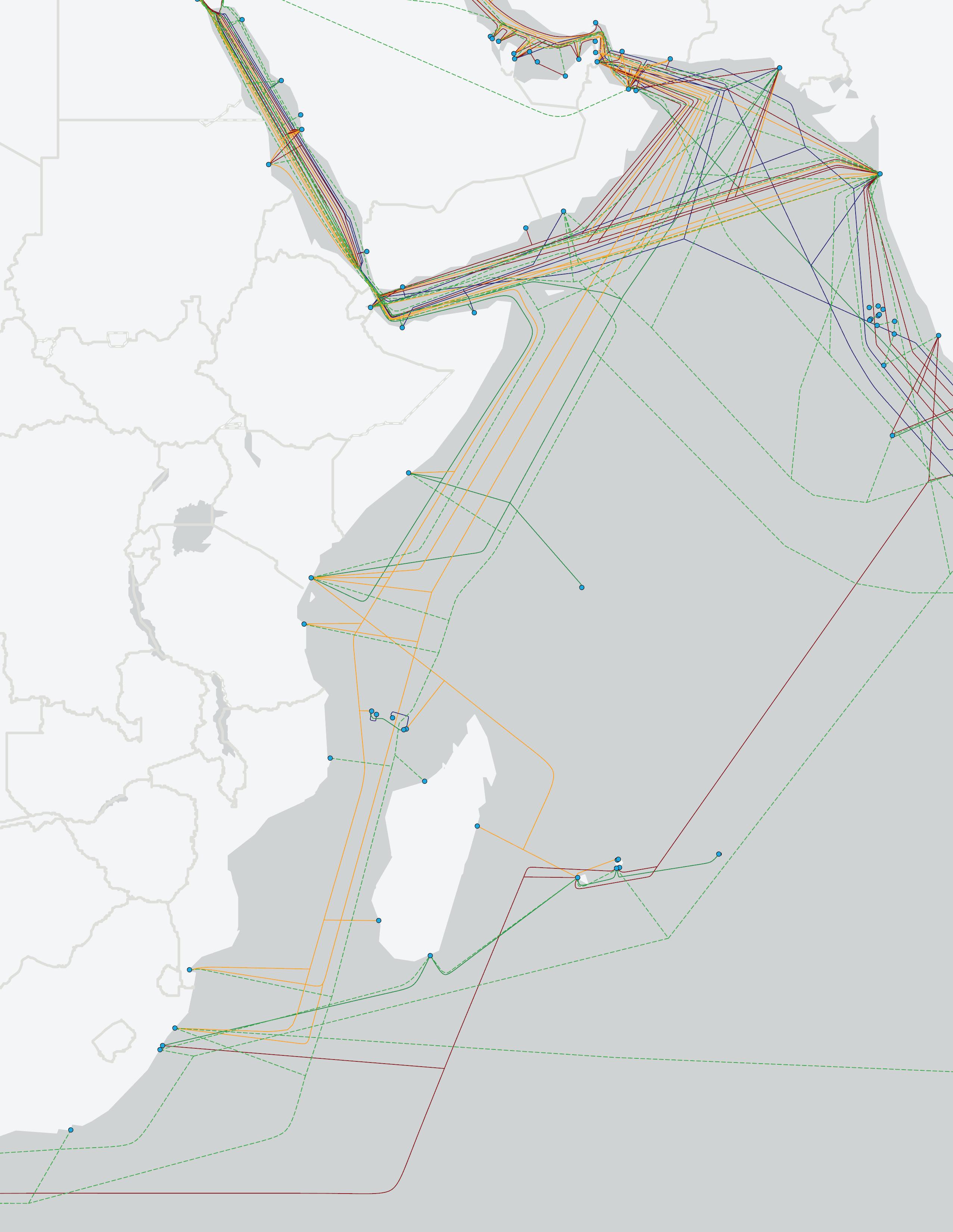

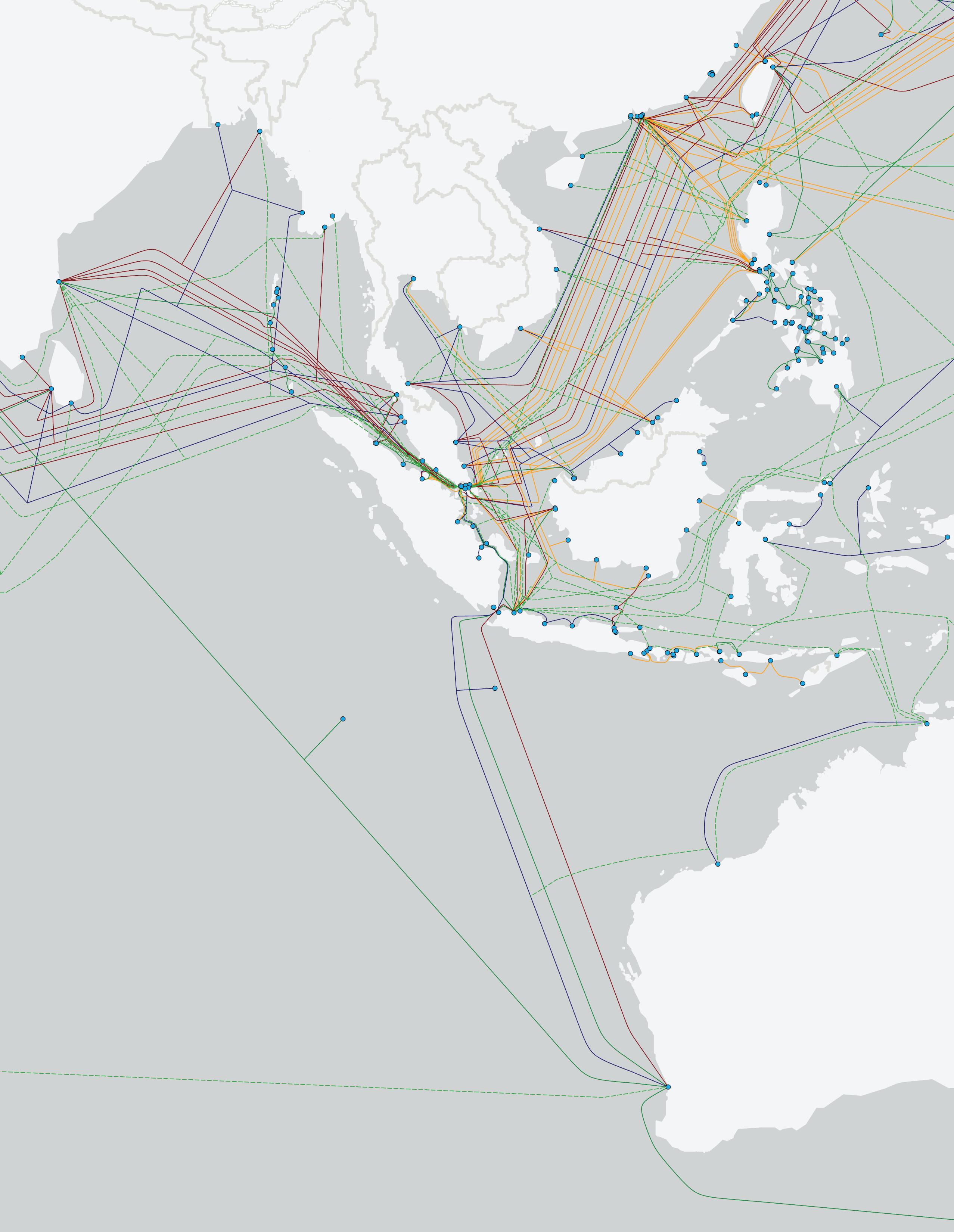

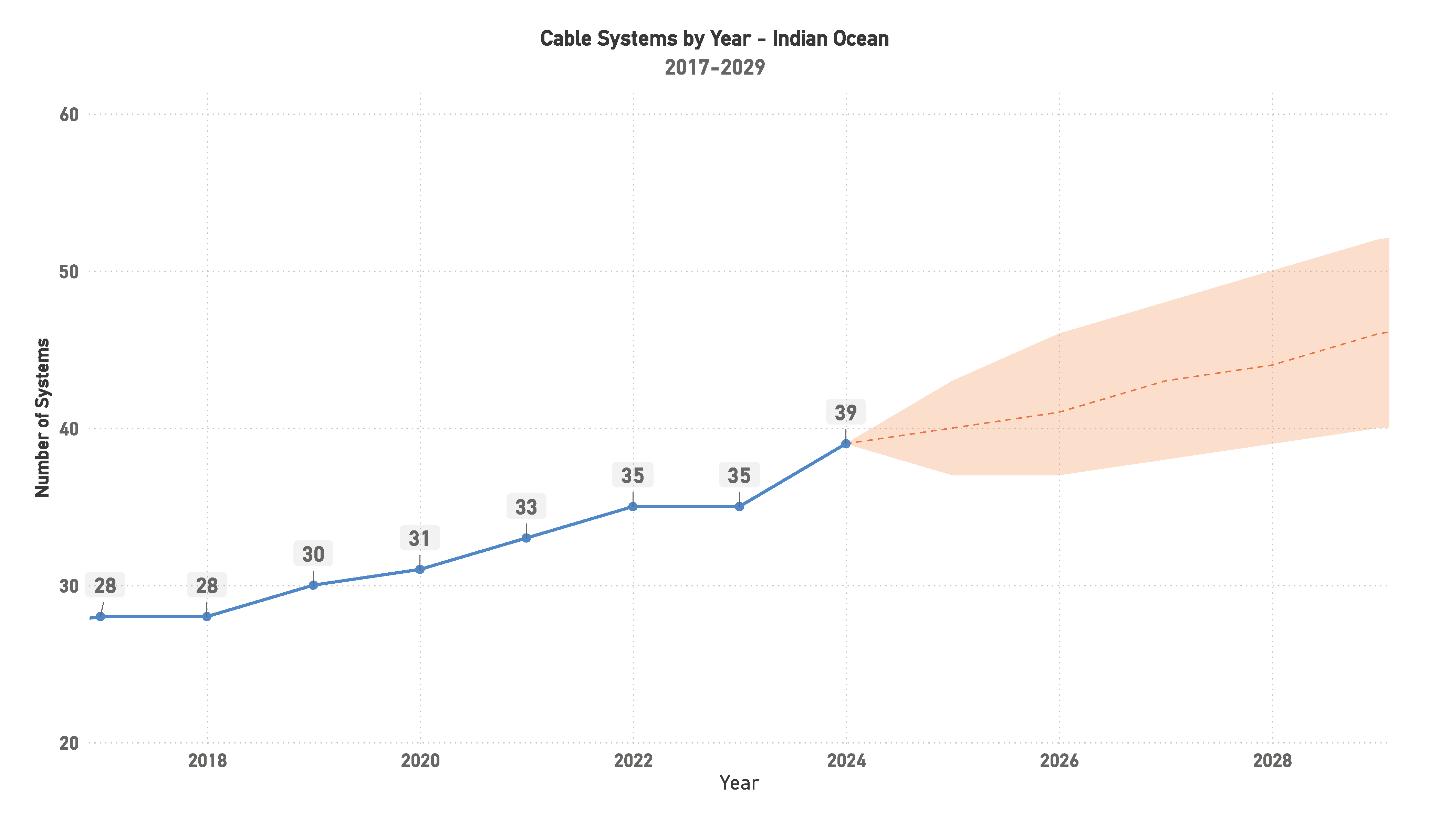

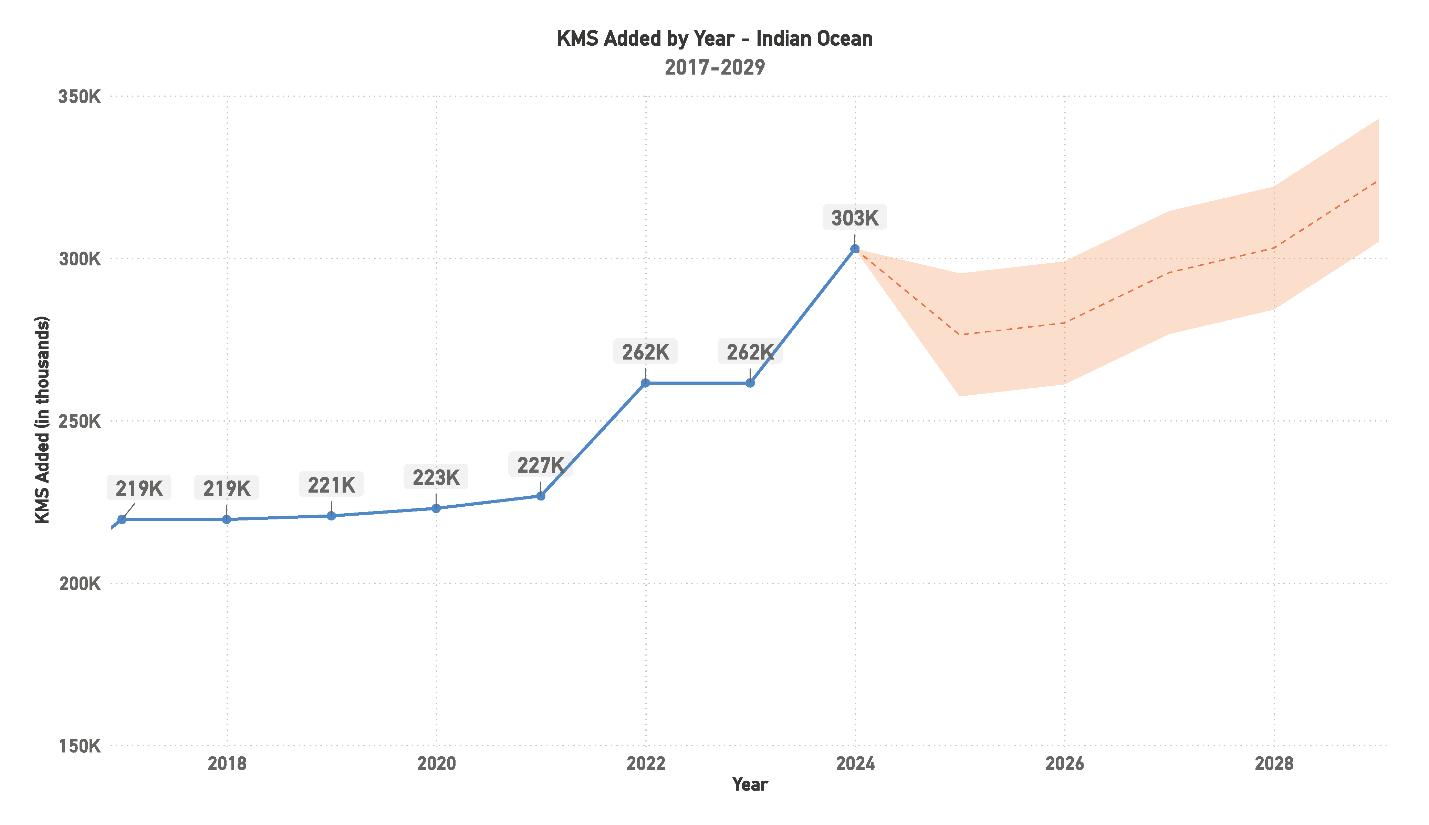

Across all regions, the submarine cable industry has seen steady expansion. The Americas region has added new systems to meet growing connectivity demands, though challenges such as regulatory instability and environmental risks remain. In AustralAsia, the market has matured, with Southeast Asia driving growth, while the EMEA region remains a critical hub for international connectivity, supported by ongoing and planned projects. The Indian Ocean region, a vital trans-regional connector, has made consistent progress despite logistical and political hurdles.

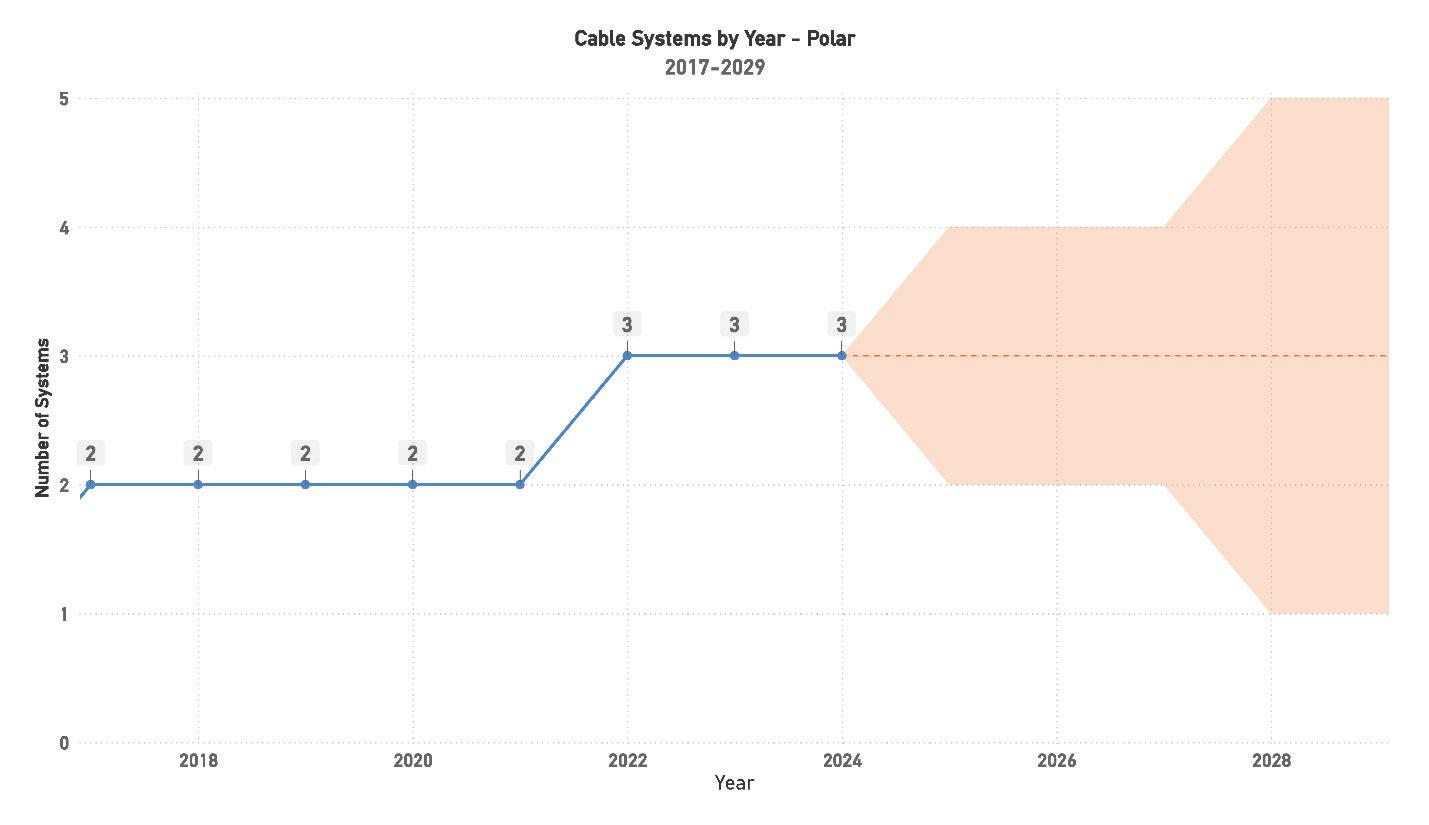

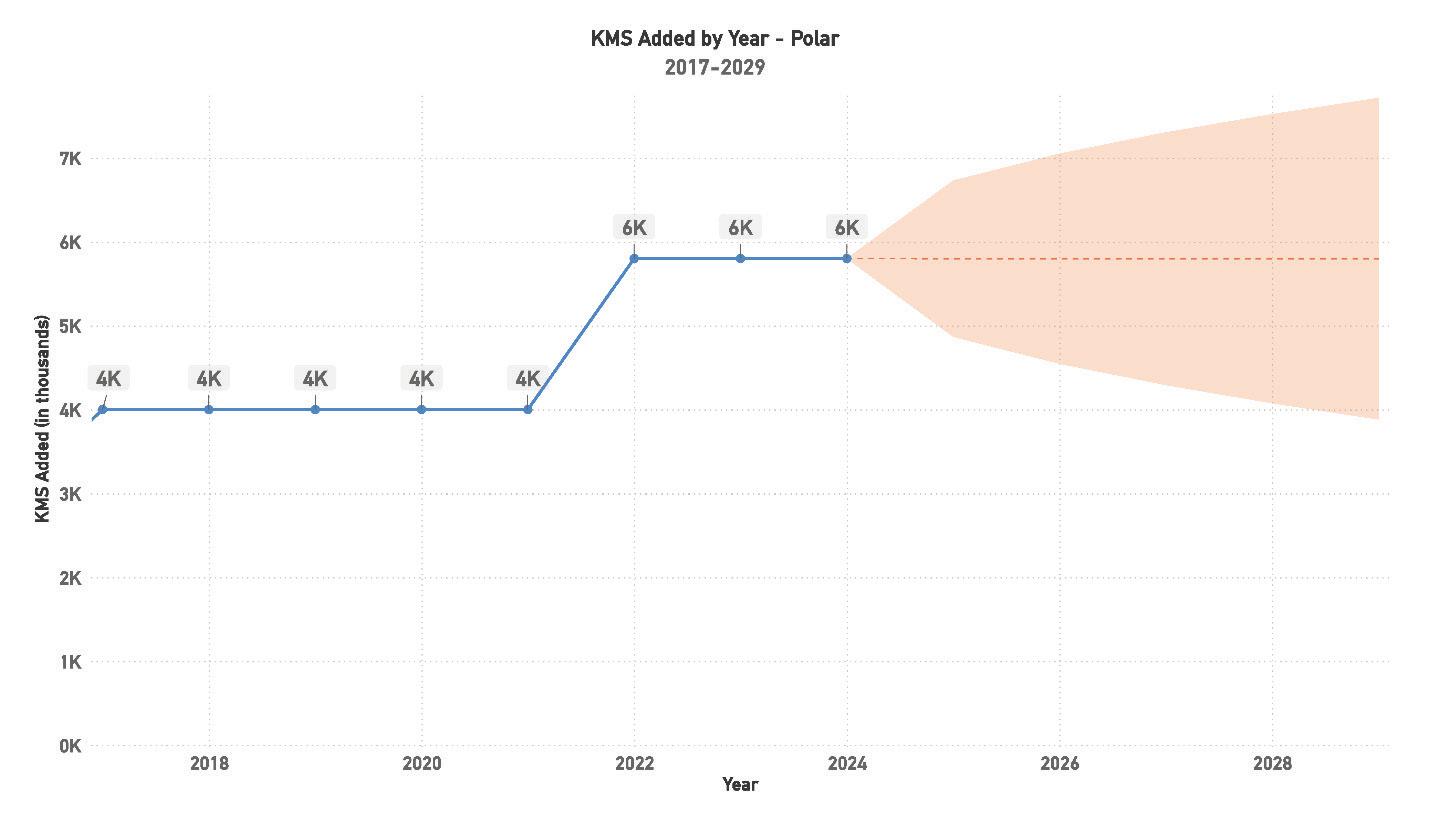

The Polar region, though smaller in scale, holds promise for the future, as its strategic position could reduce latency between continents. However, extreme environmental conditions and high costs present significant challenges. In the Transatlantic and Transpacific regions, Hyperscalers continue to lead growth, focusing on optimizing system performance and increasing resilience to support the growing global demand for data traffic.

The future of the submarine cable industry is poised for continued growth, with a strong emphasis on upgrading existing systems and ensuring the resilience of new infrastructure. Collaboration between governments, private companies, and international organizations will be key to navigating the financial, regulatory, and environmental challenges that lie ahead. As global data demand continues to rise, the submarine cable industry remains an essential backbone of the digital economy, providing critical links that enable global connectivity in an increasingly complex geopolitical landscape. STF

INSIDE THE WORLD OF SUBTEL FORUM: A COMPREHENSIVE GUIDE TO SUBMARINE CABLE RESOURCES

TOP STORIES OF 2019

The most popular articles, Q&As of 2019. Find out what you missed!

NEWS NOW RSS FEED

Welcome to an exclusive feature in our magazine, where we explore the captivating world of SubTelForum.com, a pivotal player in the submarine cable industry. This expedition takes us on a detailed journey through the myriad of resources and innovations that are key to understanding and connecting our world beneath the oceans.

mapping efforts by the analysts at SubTel Forum Analytics, a division of Submarine Telecoms Forum. This reference tool gives details on cable systems including a system map, landing points, system capacity, length, RFS year and other valuable data.

DISCOVER THE FUTURE: THE SUBTEL FORUM APP

CONNECTING THE DEPTHS: YOUR ESSENTIAL GUIDE TO THE SUBTEL FORUM DIRECTORY

Keep on top of our world of coverage with our free News Now daily industry update. News Now is a daily RSS feed of news applicable to the submarine cable industry, highlighting Cable Faults & Maintenance, Conferences & Associations, Current Systems, Data Centers, Future Systems, Offshore Energy, State of the Industry and Technology & Upgrades.

PUBLICATIONS

Submarine Cable Almanac is a free quarterly publication made available through diligent data gathering and

Submarine Telecoms Industry Report is an annual free publication with analysis of data collected by the analysts of SubTel Forum Analytics, including system capacity analy sis, as well as the actual productivity and outlook of current and planned systems and the companies that service them.

CABLE MAP

In our guide to submarine cable resources, the SubTel Forum Directory shines as an essential tool, providing SubTel Forum.com readers with comprehensive access to an array of vetted industry contacts, services, and information. Designed for intuitive navigation, this expansive directory facilitates quick connections with leading vendors, offering detailed profiles and the latest in submarine cable innovations. As a dynamic hub for industry professionals, it fosters community engagement, ensuring our readers stay at the forefront of industry developments, free of charge.

2024 marks a groundbreaking era for SubTel Forum with the launch of its innovative app. This cutting-edge tool is revolutionizing access to submarine telecommunications insights, blending real-time updates, AI-driven analytics,

The online SubTel Cable Map is built with the industry standard Esri ArcGIS platform and linked to the SubTel Forum Submarine Cable Database. It tracks the progress of

and a user-centric interface into an indispensable resource for industry professionals. More than just a technological advancement, this app is a platform fostering community, learning, and industry progression. We encourage you to download the SubTel Forum App and join a community at the forefront of undersea communications innovation.

YOUR DAILY UPDATE: NEWS NOW RSS FEED

Our journey begins with the News Now updates, providing daily insights into the submarine cable sector. Covering everything from the latest technical developments to significant industry milestones, this feed ensures you’re always informed about the latest trends and happenings. It’s an essential tool for professionals who need to stay on top of industry news.

THE KNOWLEDGE HUB: MUST-READS & Q&AS

Dive deeper into the world of submarine communications with our curated collection of articles and Q&As. These insightful pieces offer a comprehensive look at both the history and current state of the industry, enriching your understanding and providing a broader perspective on the challenges and triumphs faced by submarine cable professionals.

IN-DEPTH PUBLICATIONS

• Submarine Cable Almanac: This quarterly treasure trove provides detailed information on global cable systems. You can expect rich content including maps, data on system capacity, length, and other critical details that sketch a vivid picture of the global network.

• Submarine Telecoms Industry Report: Our annual report takes an analytical approach to the industry, covering everything from current trends to capacity analysis and future predictions. It’s an invaluable resource for anyone seeking to understand the market’s trajectory.

VISUALIZING CONNECTIONS: CABLE MAPS

• Online SubTel Cable Map: An interactive tool mapping over 550 cable systems, perfect for digital natives who prefer an online method to explore global connections.

• Printed Cable Map: Our annual printed map caters to those who appreciate a tangible representation of the world’s submarine fiber systems, detailed in a visually appealing and informative format.

EDUCATIONAL OPPORTUNITIES: CONTINUING EDUCATION

SubTel Forum’s commitment to education is evident in our courses and master classes, covering various aspects of the industry. Whether you’re a seasoned professional or new to the field, these learning opportunities are fantastic for deepening your understanding of both technical and commercial aspects of submarine telecoms.

SCAN THE QR CODE TO ACCESS ALL THE RESOURCES THAT SUBTELFORUM.COM HAS TO OFFER

FIND THE EXPERTS: AUTHORS INDEX

Our Authors Index is a valuable tool for locating specific articles and authors. It simplifies the process of finding the information you need or following the work of your favorite contributors in the field.

TAILORED INSIGHTS: SUBTEL FORUM BESPOKE REPORTS

• Data Center & OTT Providers Report: This report delves into the evolving relationship between cable landing stations and data centers, highlighting trends in efficiency and integration.

• Global Outlook Report: Offering a comprehensive analysis of the submarine telecoms market, this report includes regional overviews and market forecasts, providing a global perspective on the industry.

• Offshore Energy Report: Focusing on the submarine fiber industry’s oil & gas sector, this report examines market trends and technological advancements, offering insights into this specialized area.

• Regional Systems Report: This analysis of regional submarine cable markets discusses capacity demands, development strategies, and market dynamics, providing a detailed look at different global regions.

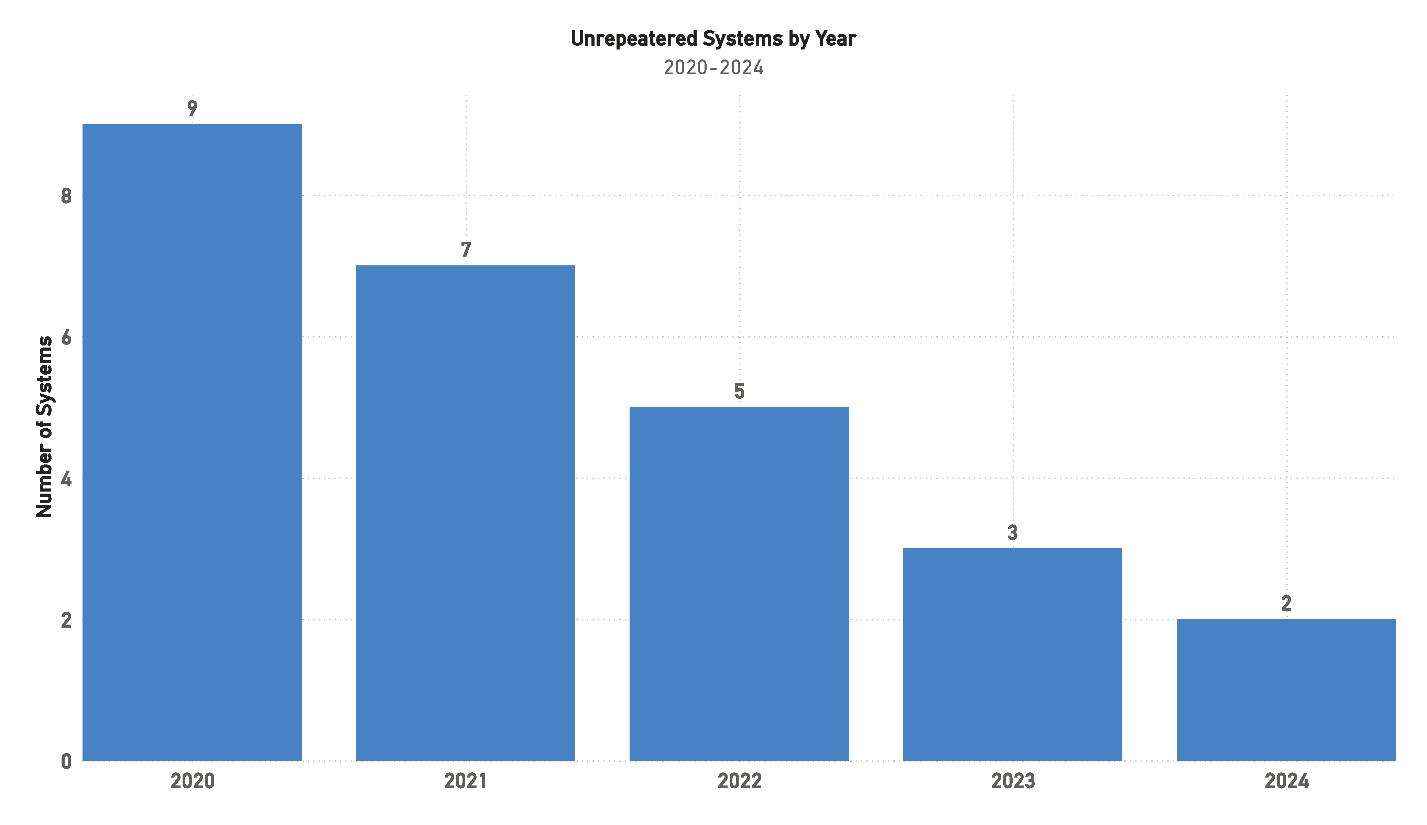

• Unrepeatered Systems Report: A thorough examination of unrepeatered cable systems, this report covers project timelines, costs, and operational aspects, essential for understanding this segment of the industry.

• Submarine Cable Dataset: An exhaustive resource detailing over 550 fiber optic cable systems, this dataset covers a wide range of operational data, making it a go-to reference for industry specifics.

SubTelForum.com stands as a comprehensive portal to the dynamic and intricate world of submarine cable communications. It brings together a diverse range of tools, insights, and resources, each designed to enhance understanding and engagement within this crucial industry. From the cutting-edge SubTel Forum App to in-depth reports and interactive maps, the platform caters to a wide audience, offering unique perspectives and valuable knowledge. Whether you’re a seasoned professional or new to the field, SubTelForum.com is an indispensable resource for anyone looking to deepen their understanding or stay updated in the field of submarine telecommunications.

Global Overview

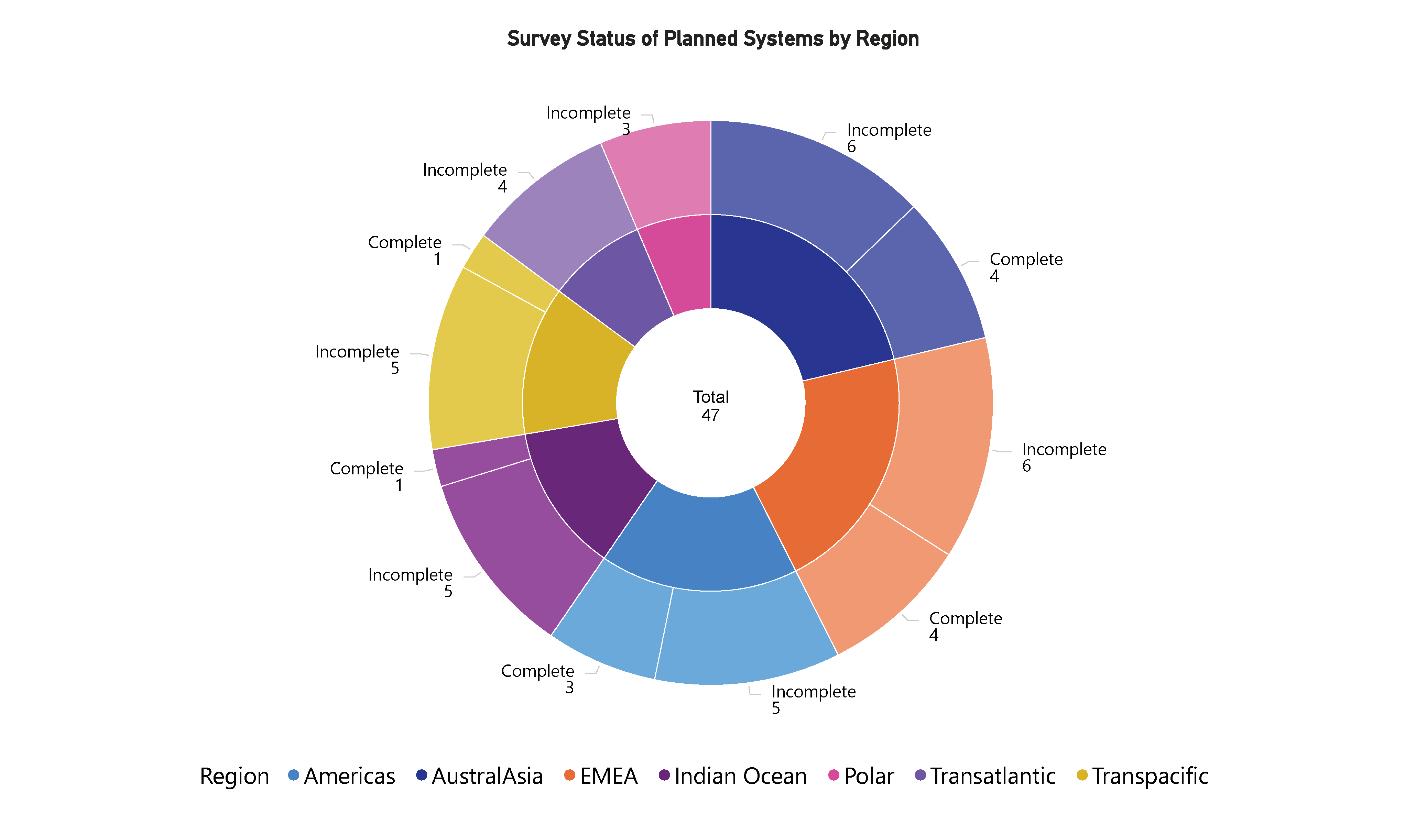

INDUSTRY SENTIMENT

This year’s Industry Sentiment Survey received over 100 responses, maintaining consistent participation levels compared to last year. The overall outlook remains highly positive, reflecting the industry’s robust growth. The results of the survey provide insight into market optimism, work levels, regional activity, and investment trends.

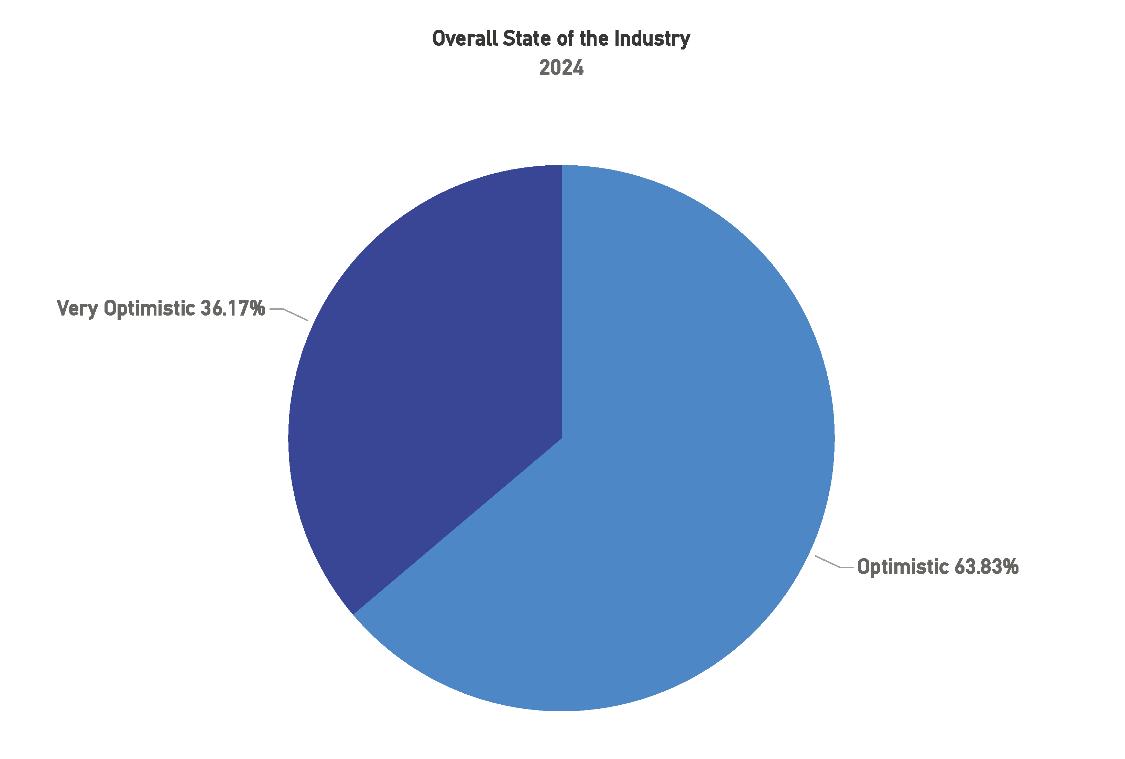

The overall sentiment is optimistic, with a combined 100% of respondents selecting either “optimistic” or “very optimistic.” Notably, the “very optimistic” category saw an increase of approximately 15% from last year, which highlights the growing confidence in the industry. Respondents indicated that their businesses and the industry at large are poised for continued growth in 2024, with expectations of new projects and more active markets.

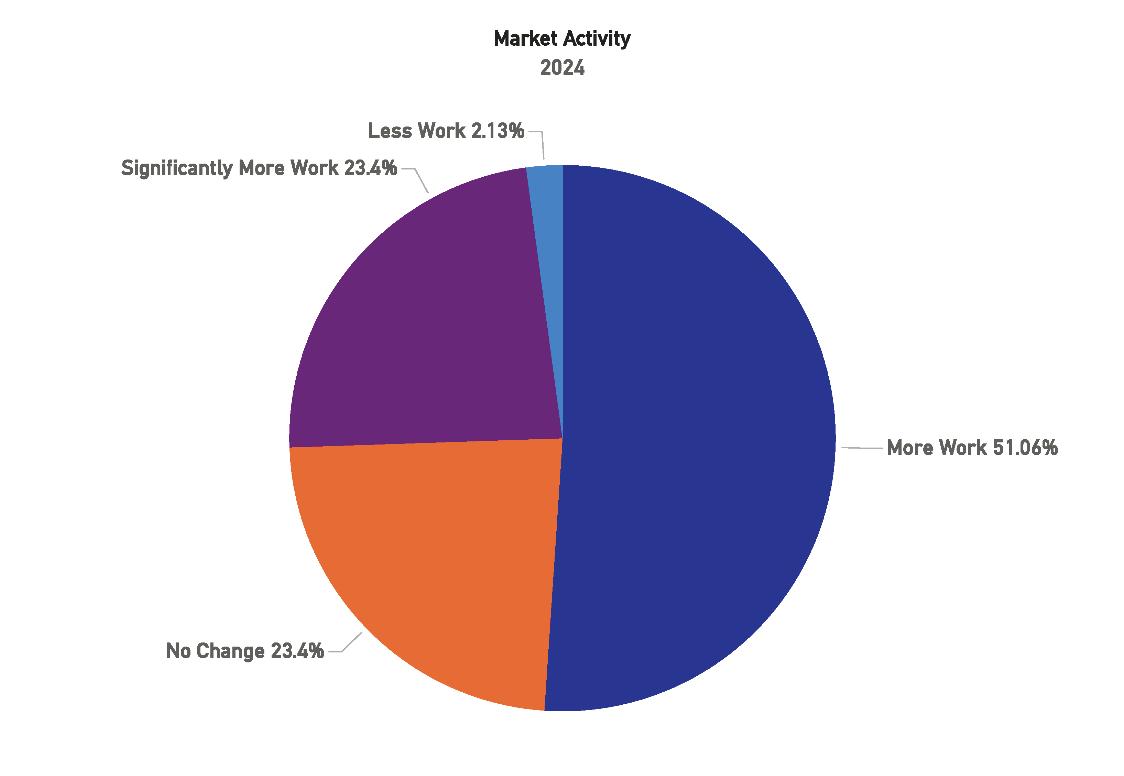

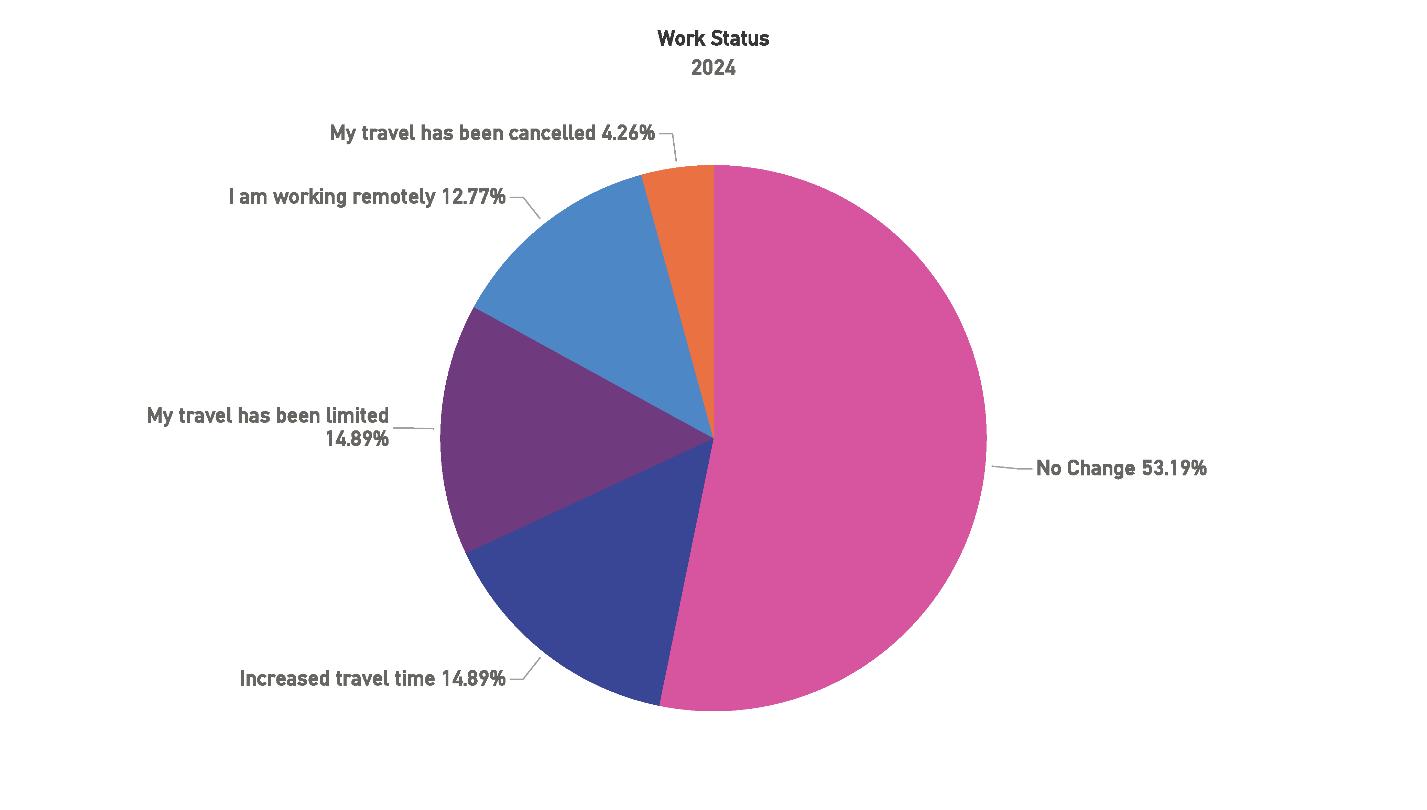

The survey also captured trends in market activity, revealing that over 50% of respondents have seen increased workloads. This reflects an ongoing demand for projects in both traditional and emerging markets. However, there is a notable balance of respondents, around 23%, reporting no change in work levels, while a smaller fraction (about 2%) saw less work than in previous years.

shift from last year, where delays were less prominent. This could be a reflection of the industry’s growing pains as more work pours in, straining resources and timelines.

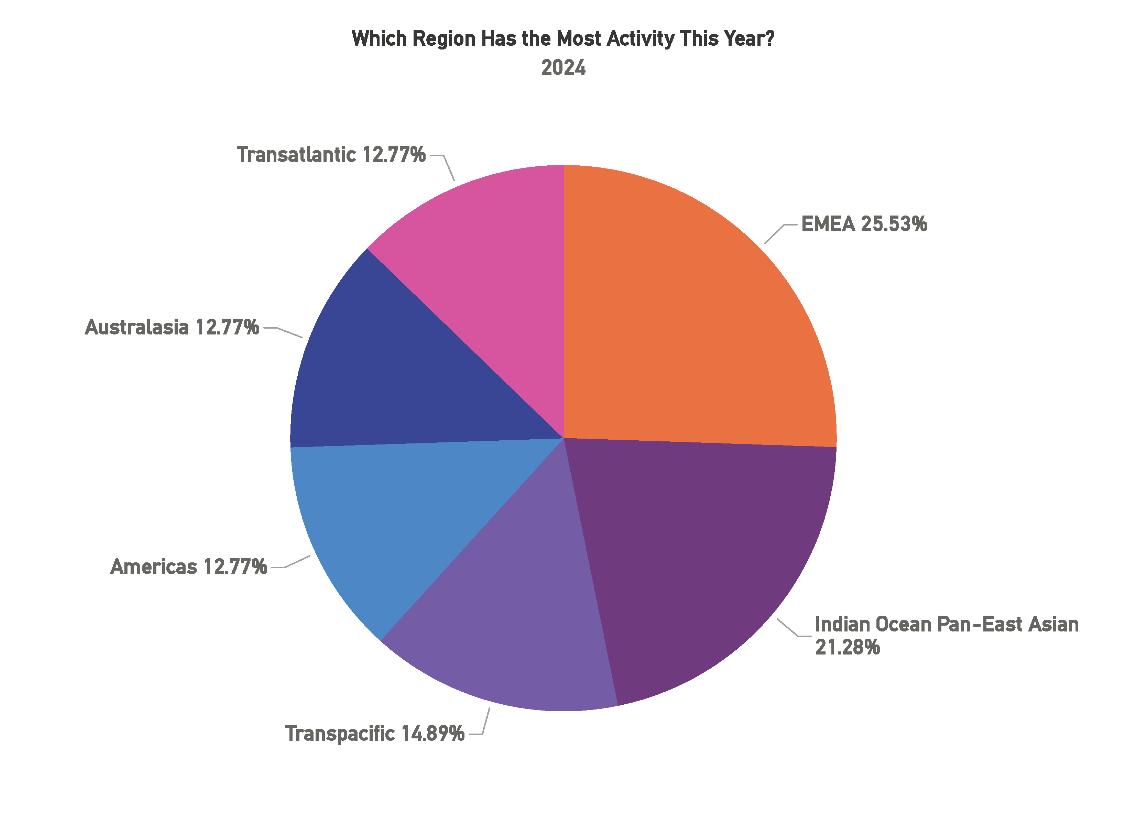

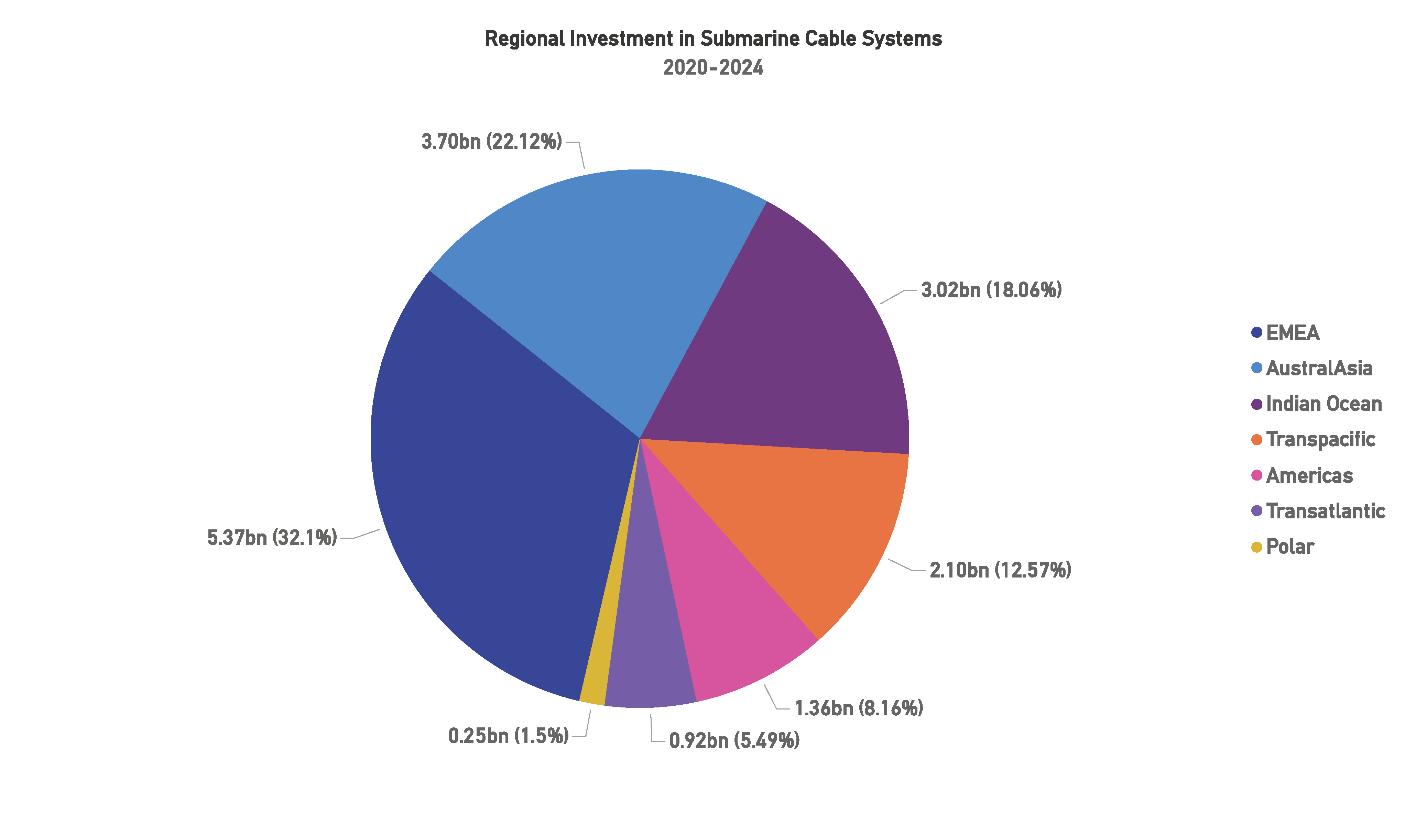

Regionally, the EMEA (Europe, Middle East, and Africa) market remains the most active, accounting for 25.53% of industry activity, with major projects like 2Africa and SeaMe-We 6 still playing a prominent role. Following closely is the Indian Ocean Pan-East Asian region, which saw over 21% of activity. Other regions, such as Australasia and Transpacific, also showed consistent work levels, indicating a broad global distribution of industry focus.

The overall sentiment is optimistic, with a combined 100% of respondents selecting either “optimistic” or “very optimistic.” Notably, the “very optimistic” category saw an increase of approximately 15% from last year, which highlights the growing confidence in the industry.

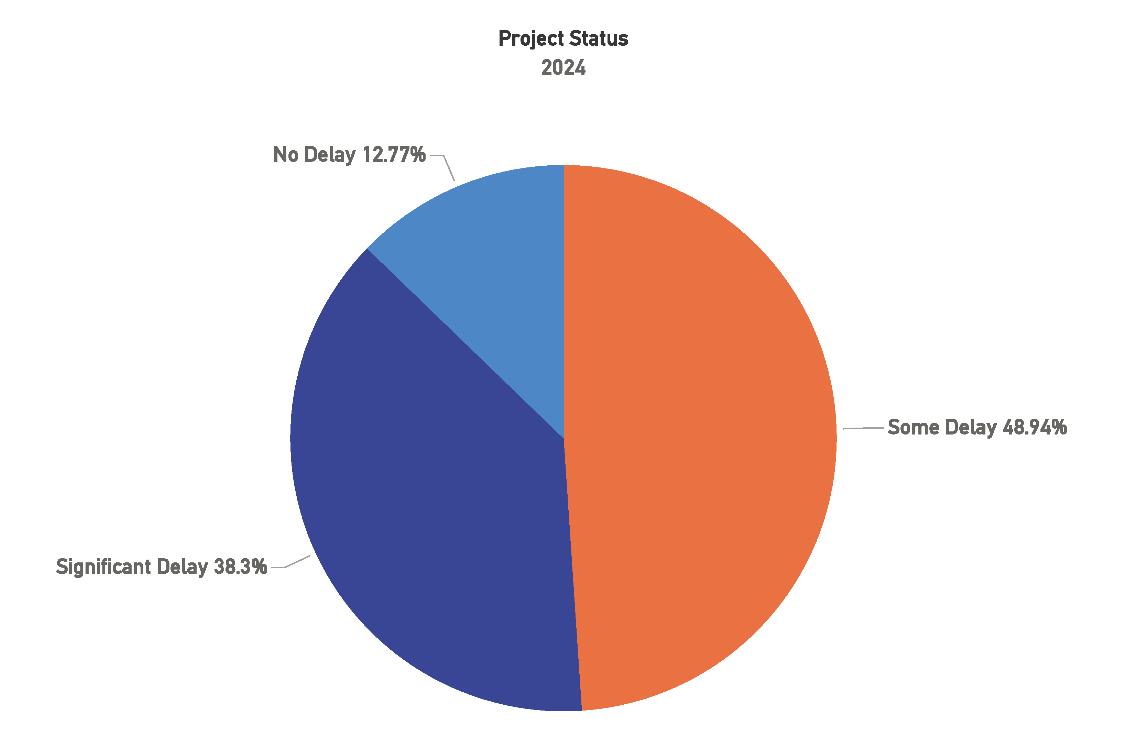

With the rise in market activity, project delays have become a growing concern. The survey showed that about 48% of respondents have faced some delays in their projects, while nearly 38% reported significant delays. This is a

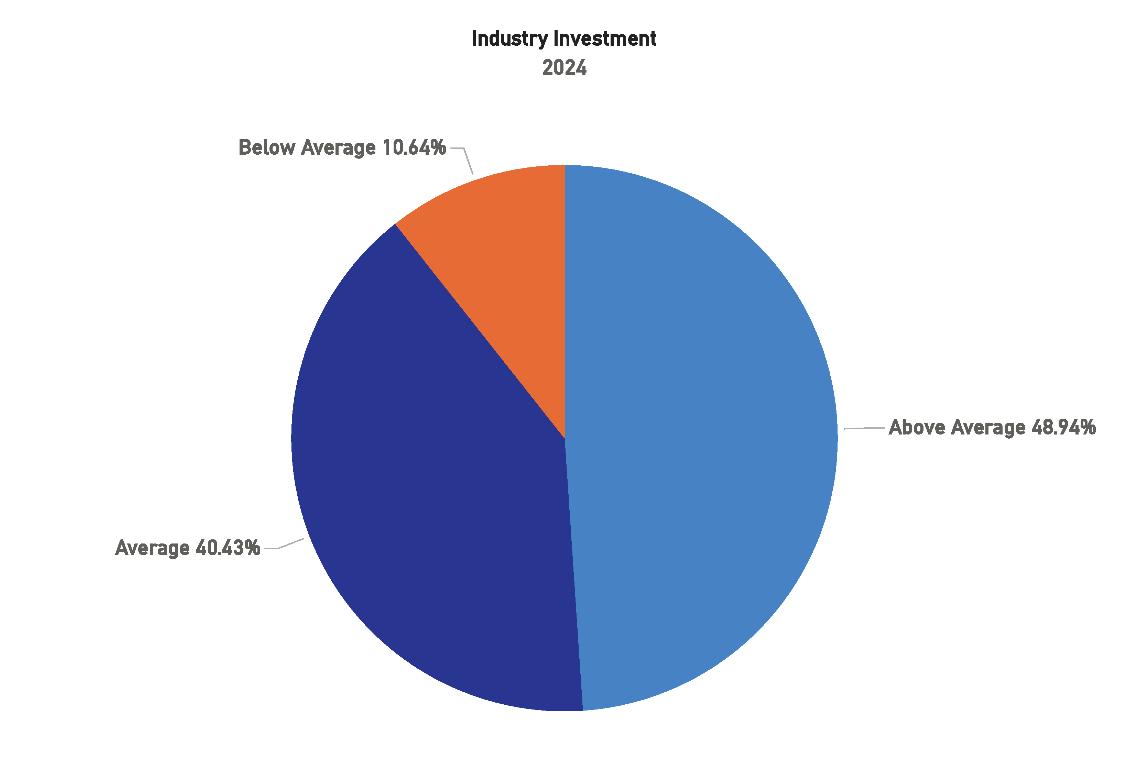

In terms of investment, nearly half of the respondents indicated that industry investment is above average, which aligns with the growing optimism. However, 10% reported below-average investment levels, a slight increase compared to previous years. This could indicate a cautious approach from some segments of the market, perhaps influenced by global economic uncertainties or concerns about project timelines.

Overall, the survey results point to a strong year for the submarine cable industry, with high optimism, growing work levels, and continued investment. However, there are challenges ahead, particularly regarding project delays and uneven regional investment. As the industry continues to expand, balancing growth with operational efficiency will be key to sustaining its positive trajectory. STF

INDUSTRY SENTIMENT

Figure 1: Overall State of the Industry

Figure 2: Market Activity

INDUSTRY SENTIMENT

Figure 3: Project Status

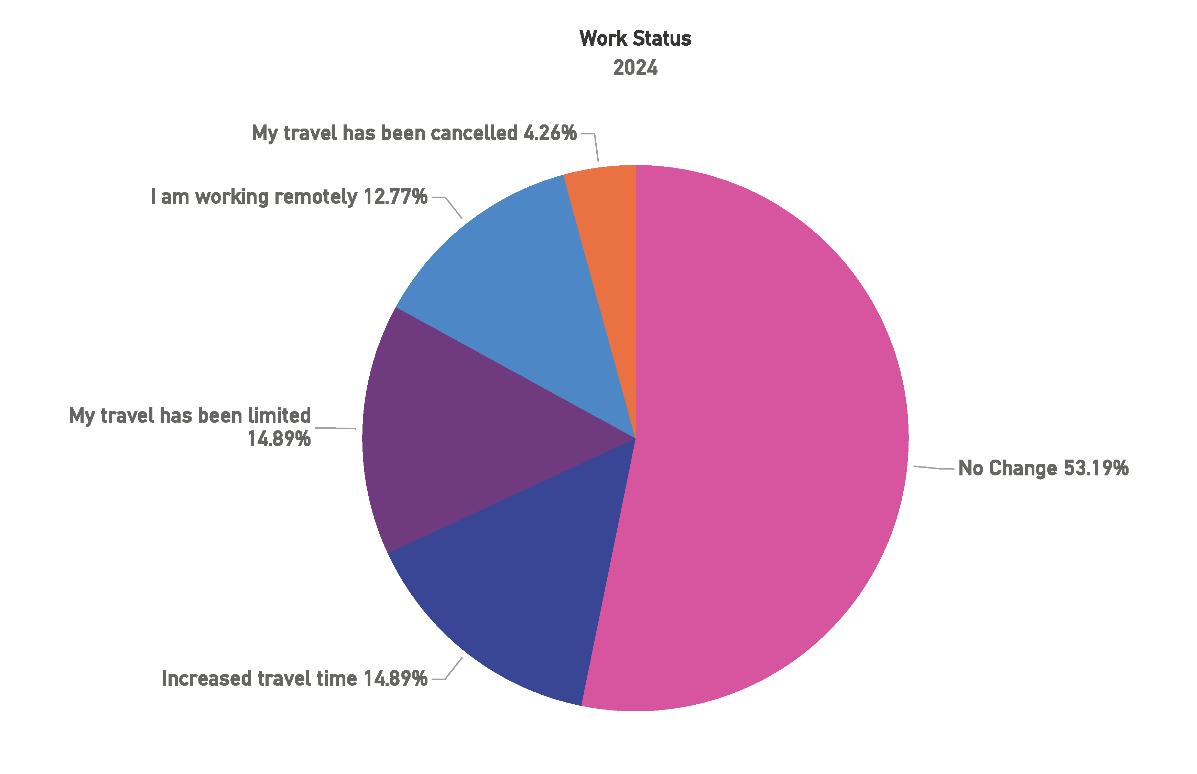

Figure 4: Work Status

INDUSTRY SENTIMENT

Which Region Has the Most Activity This Year?

Figure 5: Industry Investment

Figure 6:

GETTING TO KNOW YOU

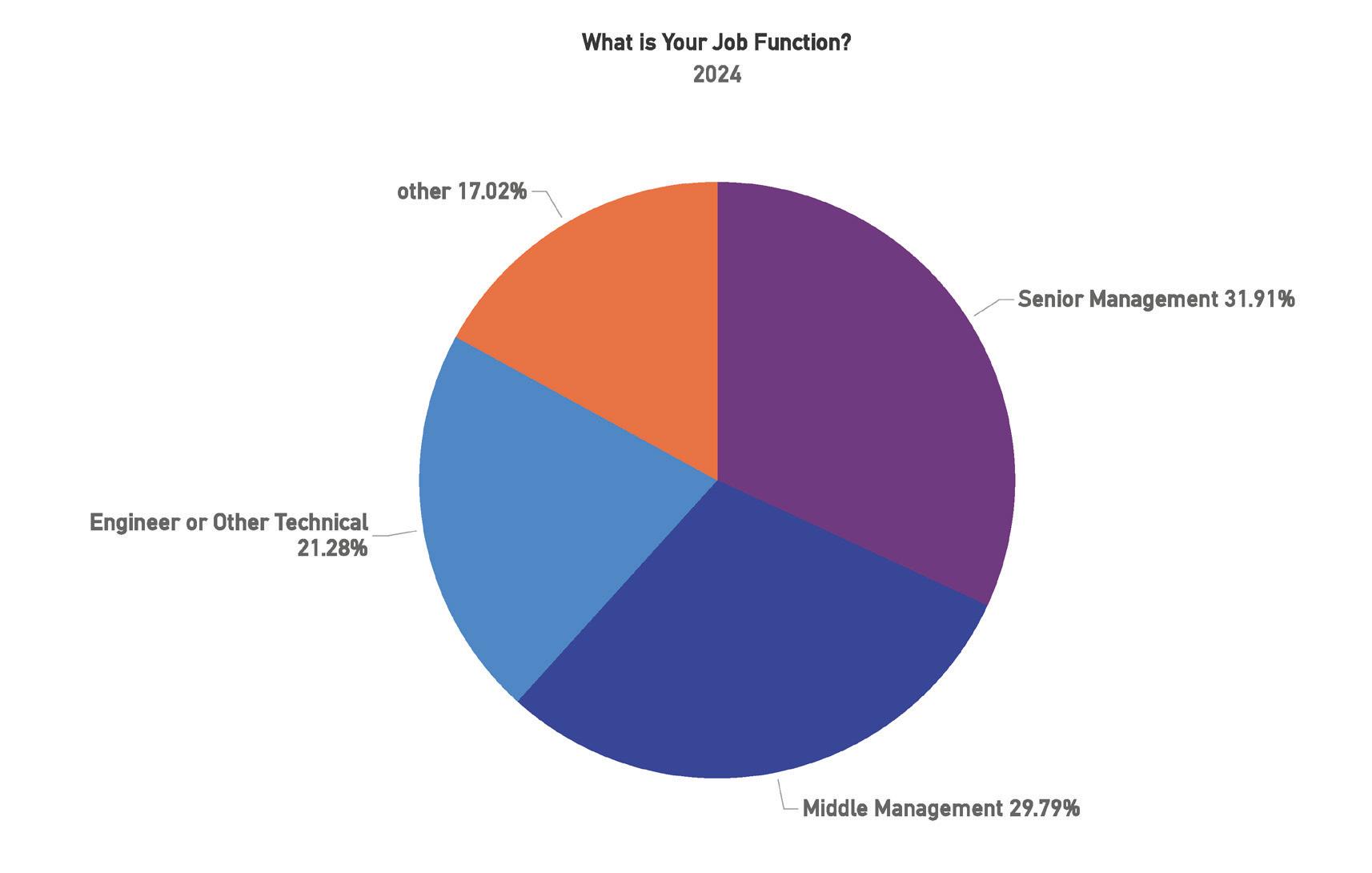

7: What is Your Job Function?

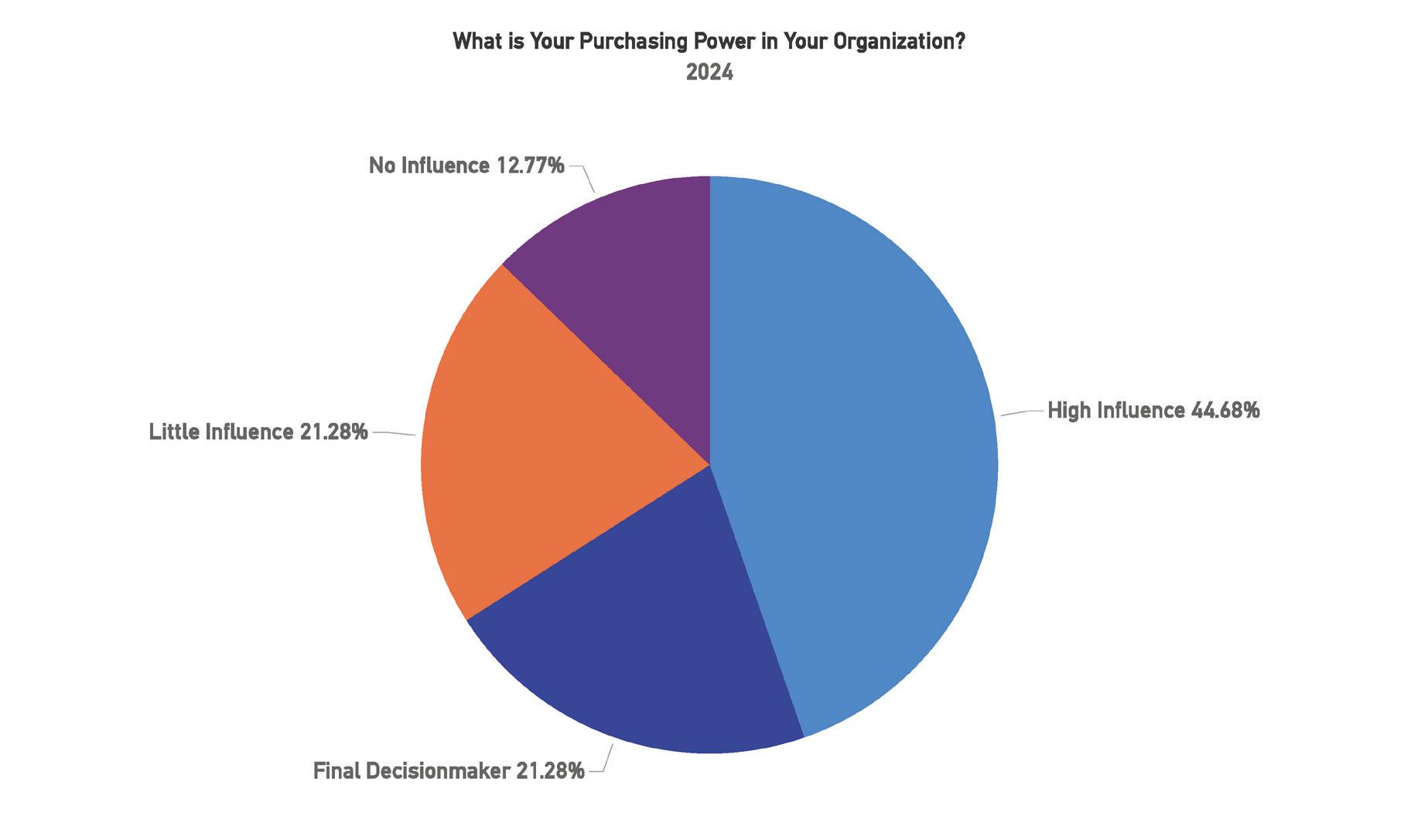

8: What is Your Purchasing Power in Your Organization?

Figure

Figure

GETTING TO KNOW YOU

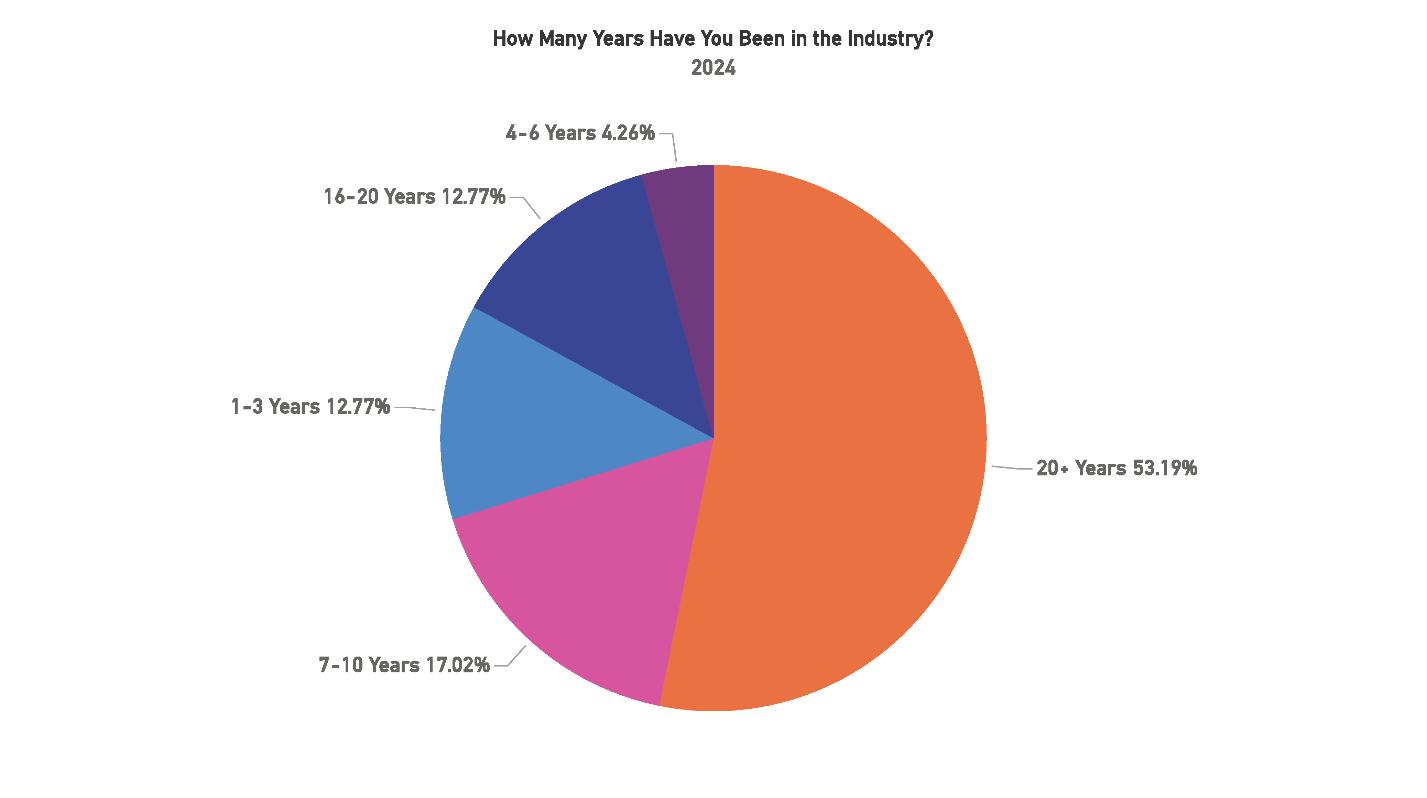

Figure 9: How Many Years Have You Been in the Industry?

Figure 10: Where Do You Reside?

REFLECTIONS FROM THE DEPTHS

A Subsea Journey: Perspectives of Phillip Pilgrim

This Back Reflections, for the 2024 Industry Report Edition, is a collection of interesting and hopefully amusing submarine telecom items. Many are from my 34 years working in the industry, past colleagues, and recent historical research in this field. Hopefully, some wisdom and a few laughs can be gleaned.

NAKED TRUTH

An SLTE installer was on site for a few weeks. He was part of a team installing a new system in the early 1990’s. He enjoyed nature and took a daily walk along the cable path to the beach after lunch. One day, he returned sooner than normal. He had a shocked look on his face. He met a man with nothing on but a backpack walking casually towards him along the cable path. The nudist beach was in a cove 1 km south of the beach manhole. Our CLS was 1 km to the north.

FIRE & 24 / 7 COVERAGE

Back in the 90’s, our station was growing. New construction was underway for a new wing. This was our first expansion. It would provide more room for an upcoming new submarine cable terminal and new satellite terminals. At that time, we operated 24 / 7 in three shifts: 08:00 to 16:00, 16:00 to 24:00, and 00:00 to 08:00. The full crew worked the day shift, and one man worked each back shift, with co-workers available “on call”. The facility was huge, and the technician would conduct a

walking “round” inspection every hour. On this occasion, the evening technician noted remnant welding smells during most of the evening shift, then he eventually saw smoldering in the new ceiling interface between the existing building and the expansion. It caught fire and he quickly called the local fire department. All was made good; the volunteer fire department did an excellent job. Welding from earlier in the day had ignited insulation that smoldered for hours, then eventually ignited. If the site was unmanned, much worse could have happened. These days, with submarine cable stations and submarine cable being listed as critical infrastructure, it is strange for cost saving measure to push for unmanned sites, it is strongly recommended that all reconsider the 3 top avoidances for subsea systems: Risk, Risk, Risk.

Belts and braces approach is always the best way forward. Our CLS was very remote, as are most, so experienced boots on the ground 24 / 7 is the best low-cost guarantee for a 25 year (Beginning to End-of-Life) up time.

ICE & CHRISTMAS STORMS

By 1867, the many cables in Atlantic Canada were damaged by ice. The wind and tides piled broken “spring” ice on the beach as if it was God’s giant bulldozer at work. The first significant North American cable of 1852, between Prince Edward Island & New Brunswick, was lost to ice as well as the 1856 and 1866 cables on this same route. Further east, the first successful transatlantic

Figure 11: Compass Error

cable of 1866 suffered the same fate, but in its case, the instigator was an iceberg in the spring of 1867. The locals and cable station staff watched the grounded berg pass through Trinity Bay, Newfoundland. It was stuck in place for about 4 days before it continued to scrape along the bottom and then cut the 1866 cable. Fortunately, the 1865 cable, in the same vicinity but deeper, was not cut, so transatlantic communications remained up.

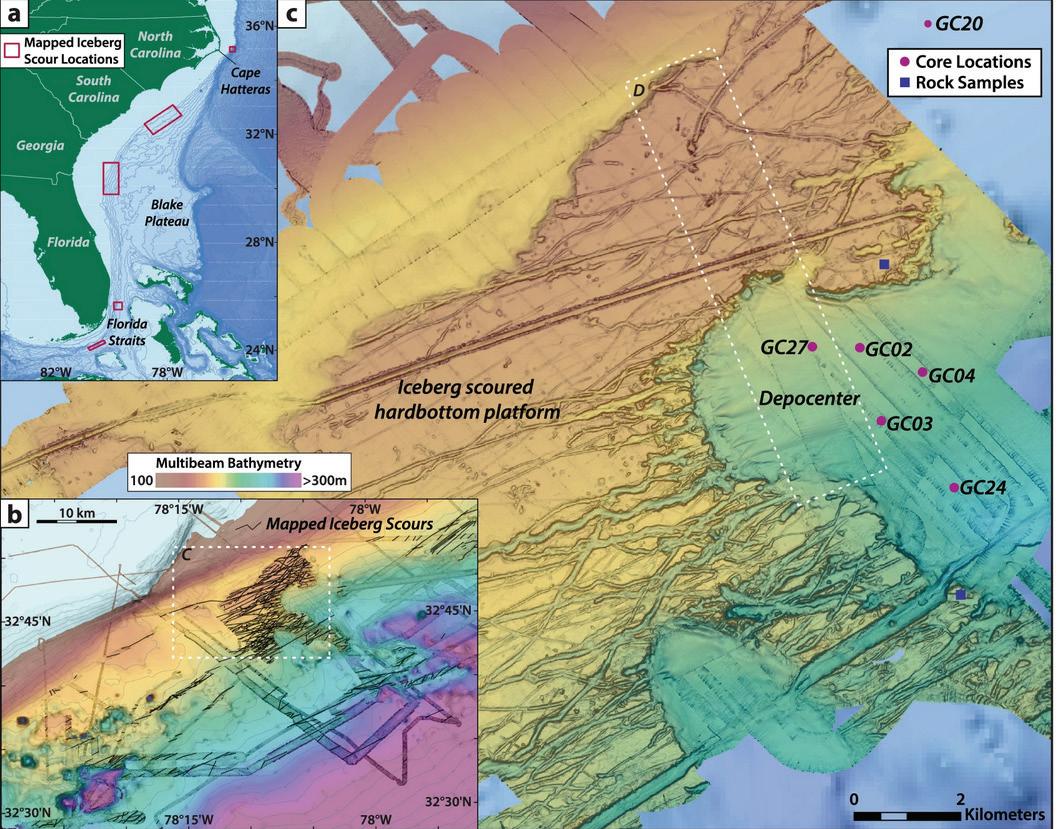

Even to this day, ice piling on beaches damages cables. As new cable routes expand further north, it is best practice to plan for this. The earth is now passing towards its cyclical (~100,000 year) interglacial temperature peak, and the remaining northern ice will inevitably melt / break up.

Digression: Back in the 1980’s, while in university, a fellow geophysics student landed a summer job that entailed reviewing bathometric seafloor images for iceberg scour (historical gouges where iceberg bottoms had dragged across the bottom). This work was for risk mitigation: predicting the rate and size of bergs that could cause future “discomfort” for planned oil field platforms in this area. The same data is available, and applicable, for subsea cables.

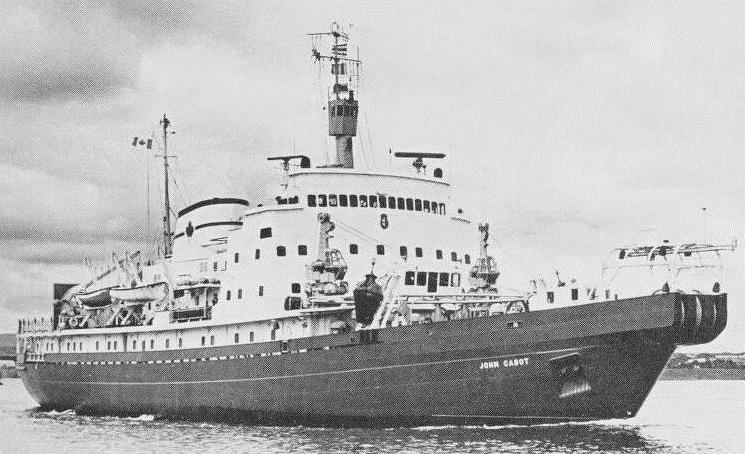

When I started in subsea telecoms in the early 90’s, my father, and many of his colleagues, had worked on submarine cables since the 1960’s. They mentioned many times that the first cables to Greenland and to Iceland that suffered greatly from icebergs. So much care and consideration were taken for repairs that icebreakers were on call to support cable ships. A famous Canadian cable ship from that time was the CS John Cabot. It was a purpose-built icebreaker / cable ship for these northern cables. It was the rescue ship of the Pieces III submersible off Ireland in 1973 and sadly, the recovery vessel in the 1985 Air India Flight 182 crash, also off Ireland, and nearly in the same location.

I also recall the story of a ship in the English Channel during the 80’s, that dragged an anchor and cut many cables. This was during the Christmas holidays when traffic and revenue was greatest. It was a significant disruption.

Digression: In the patch where I mostly worked, the North Atlantic, most cable faults were “shunt faults”. These faults are not complete cuts but are electrical “shorts”, and the cable can usually operate while damaged. In other parts of the world, such as the South China Sea, most faults are

clean cuts. Shunt faults are electrical in nature and require precise, and careful measurements, using calibrated test equipment or calibrated power feeds. Cuts are much easier to locate as the end of the optical fibre is viewed using a test instrument called a Coherent Optical Time Domain Reflectometer (COTDR). It usually has an accuracy of 300m or less. I will toot my own horn in saying that the last electrical fault I located, nearly 20 years ago, was within 200m of the fault. The ship’s crew were delighted as the ship was placed nearly right above the fault and there was no delay in the repair. This shunt fault location was carefully calculated using electrical techniques where each 1V of error placed the ship 2.5km further from the fault.

SHOCKING. SHUNTS, AND SAFETY

“Death on Contact” is the grim High Voltage warning on many power feeds. In my early career, once I had earned my transmission “chops”, I focused on locating cable faults using electrical and passive optical supervisory methods. It was an academic challenge to pinpoint the fault, as well as a considerable saving to the company. You could validate your whole year’s salary (and more) by reducing cable repair by a single day. I was very lucky to have mentors who had done this work since the 1960’s as well as new brilliant engineers to the industry like Daniel Welt and Ahmed El-Sakkary, and the brilliant trainers from AT&T

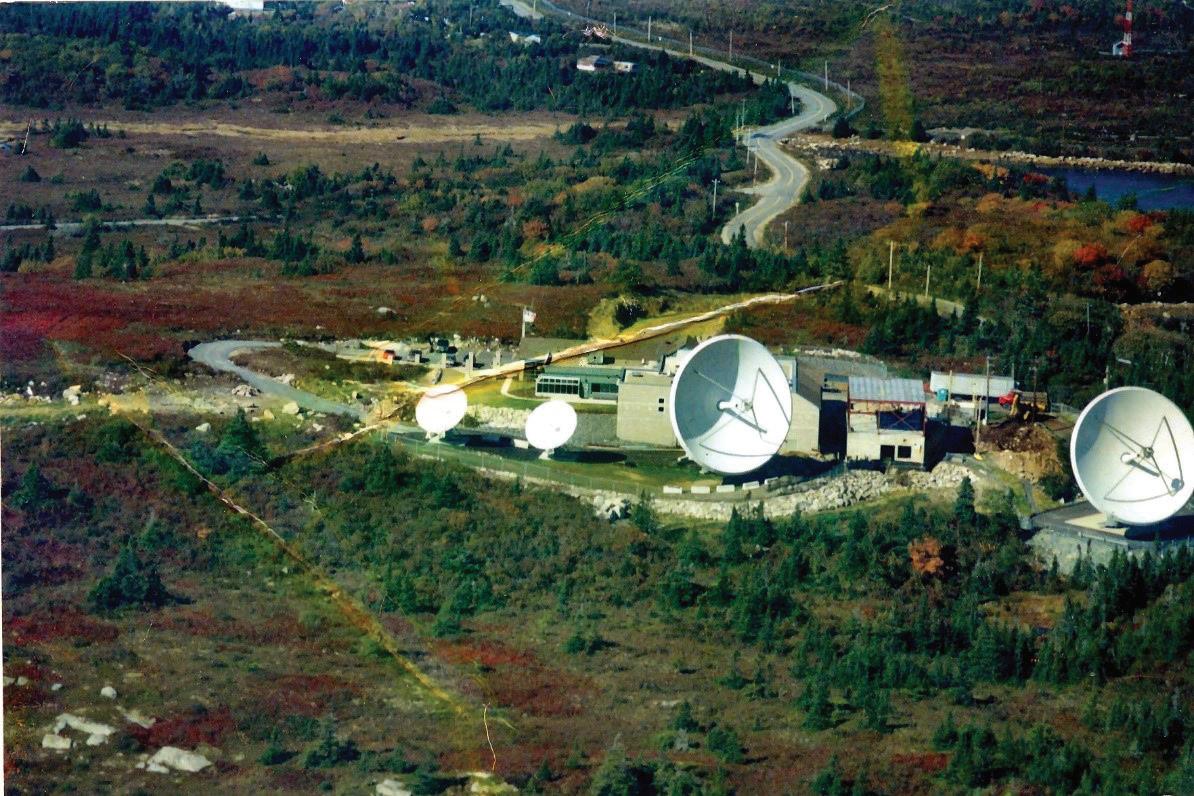

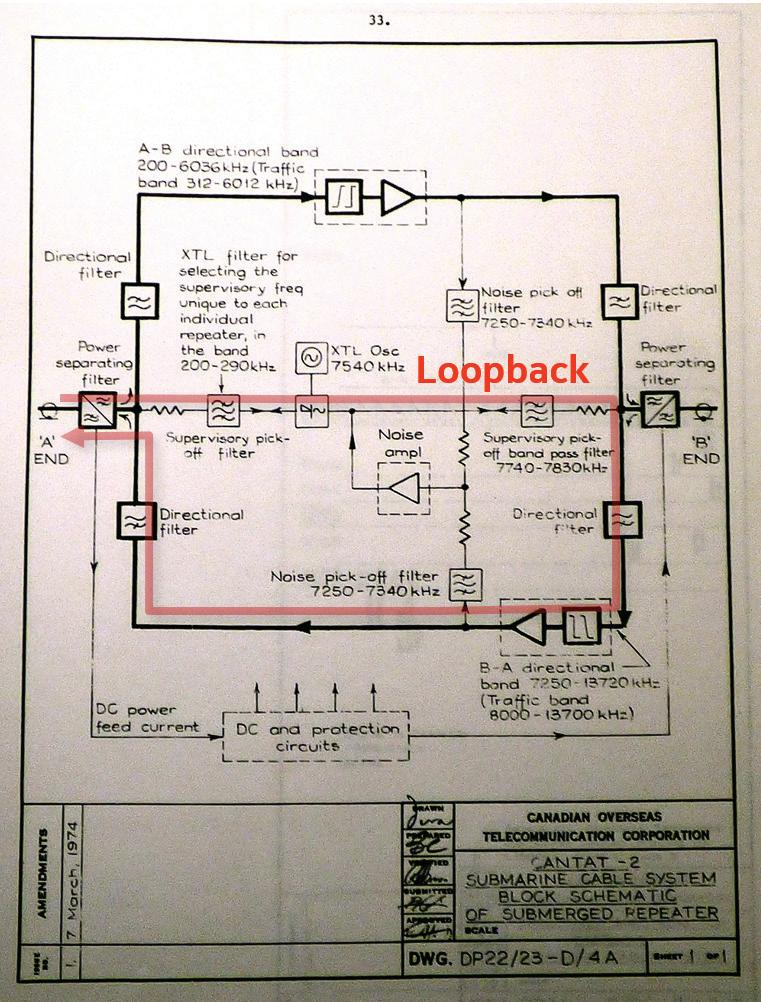

Figure 12: Third CLS Expansion (CANTAT-3), Pennant Point

Figure 16: PFE Danger

Submarine Systems Incorporated.

Digression: The passive loop-gain measurements now used in optical cables evolved from the same principals used on the first coaxial telephone transatlantic cables from the 1950’s. Likewise, the same electrical methods used for locating electrical faults on the power conductors of today, were used since the early telegraph cables of the 1850’s by the likes of Lord Kelvin, Michael Faraday, James Clerk Maxwell, Oliver Heaviside, the Siemens brothers, and Charles Wheatstone.

Submarine cable power supplies, aka Power Feed Equipment (“PFE” if you talk-thetalk), are just giant DC testbench power supplies that you may have used in science classes. Their maximum voltage outputs and maximum current outputs have increased over the years from literally a battery cell, made in a sewing thimble with acid, to approximately 20,000 V at 3 A these days. This makes a submarine cable as lethal as an overhead high-voltage power line. There is |ALWAYS| great risk of injuring an engineer anywhere along the cable. Because of this, comprehensive training, mechanical safety interlocks (with secure keys), power safety protocols, and safety warning stickers

are used to protect all who operate, maintain, and repair submarine cables. Although these are in place, Murphy’s law exists. Here are a few notes from my work with PFE’s over the years.

The first PFE I became acquainted with was at two years old, in 1967. My father worked on the CANTAT-1 cable and I recall being terribly startled by the sound of the motor alternator room where a matrix of whirring electrical motors sounded. These converted 60Hz AC power to a higher voltage and higher frequency. The motor alternators were a stage in the PFE’s buildup to the high voltage needed to drive the cable.

The second PFE was for CANTAT-2. It had a similar motor-alternator step-up architecture but it was not so scary in 1991. Inside this PFE was a “Hot Transfer Switch” (HTS) which was used to switch power to the cable head from a pair of PFE “cubicles” that operated in parallel. Transferring between working and standby would allow one to take a “cubicle” offline for repairs and maintenance. The HTS was a make-before-break. In our case on that day, it was a break. The HTS had failed during a scheduled maintenance transfer and dropped the cable. My well-trained elder colleagues instantly restarted the cable

Figure 14: Iceberg Scour off Florida.... Yes, Climate Does Change

and noted the cause. They saw it before. The silver coating on the switch contacts had corroded. “Go figure”: PFE’s being near beaches and exposed to remnant “salty air” 24 / 7. When the system was taken down, the faulty switch was exercised with the lights out in the equipment room to better investigate the troubled device. The switch gave a wonderous display of sparking much like you saw when Scotty cross-linked power bus A to bus B in a cramped Jeffery Tube. The new spare switch was then efficiently installed, and the cable system brought back online. The old switch was sent back to the factory for re-plating. This is the real-world stuff that MTBF, MTTR and time without a spare is based upon.... RISK, RISK, RISK.

Many interesting PFE events transpired over the next 10 years, but I’ll save them for a future “technical” article on fault locating methods. Here are three additional interesting cable power stories:

When commissioning a new cable system, I worked with an experienced engineer from the system provider. The system was still being installed, but there were many delays at sea due to the weather. All parties were keen to progress the acceptance tests, so we began the PFE testing. It was understood that the PFE being tested was connected to a test load of resistors and the cable end was terminated in the overhead racking where the outside plant cable would be pulled into the facility the following week. Upon powering, the meters on the PFE were jumping wildly. This was not expected as the PFE should have been powering into a very stable test load of resistors. Moments later two LAN engineers came white-faced and running into the equipment room. They observed HV arcing above their heads in the ladder racking in the LAN room. The PFE was directed to the cable rather than to the dummy load. This was a scary

event but also a bit comical in hindsight. As a customer, you never see all the details so I will guess that the cables inside the PFE were incorrectly connected. Fortunately, it was a low voltage PFE, and the maximum voltage was 3kV. A year later, we found the ocean ground and station ground cables crossed over in a different station. Similarly, this would have occurred during installation of the PFE and was a potentially deadly mistake: any work on the “thought to be isolated” ocean ground would have put full cable voltage on the ground cable if the ground was lifted (disconnected) at the beach.

An early “computer controlled” PFE with automated start-up had poorly written software code. When in Current-Regulation mode, it would ramp the voltage as high as it could to achieve the desired current. If the cable was open, no current would flow so the PFE would ramp the voltage to maximum then shutdown. Unfortunately, the same dangerous, and poorly written automation software, had a volatile default High Voltage shutdown. Every time the PFE was repowered, or the controller reset, the HV shutdown would return default to the maximum 18 kV. So, when the PFE ramped up int no load, it would hit 18kV then shut down. On one occasion, newly trained

Figure 17: CANTAT-2 Loop Gain Path in Repeater

Figure 15: Icebreaking Cable Ship John Cabot in 1965

engineers at this cable station were working with a cable ship and were asked to turn on the PFE and power towards the vessel. The cable ship fortunately had the cable end safely in a termination box but in open (unterminated). The newly trained engineers attempted to turn the cable up 3 times before the ship called yelling “STOP!!!”. I could imagine the sound of an 18kV arc within a metal test room on a ship.

These same PFE’s had a design challenge, where socalled “blind-mate” high voltage contacts would occasionally crack under use and arc (similar sparking like on the HTS). At this time, I was part of the team operating the system, so we took it upon ourselves to do the repair. Yours truly, with a colleague standing-by, turned off the PFE, did all safety checks, discharged all HV points, applied safety grounds, and crawled into the PFE to make the repair. 10 years earlier, I had a similar privilege of dangerous work to bypass the Resistor-Capacitor lightning arrestor array inside the beach manhole. Even when using safety grounds in the work area, voltage checks, confined-space checks, and written confirmation that all PFE’s in the system are down, it was very nervous work.

those days); and by the time you exposed these, the safety interlock procedure also depowered the equipment. Our satellite equipment, on the other hand, had no safety interlocks. With a Philip’s screwdriver, you could simply remove a back panel and expose to 30 to 50 kV power supplies and cables. The TWT and Klystron amplifiers required very high voltages to operate. The back panels were typically sharp-edged floppy sheet metal and the HV cables were soft spark-plug-like automotive cables.

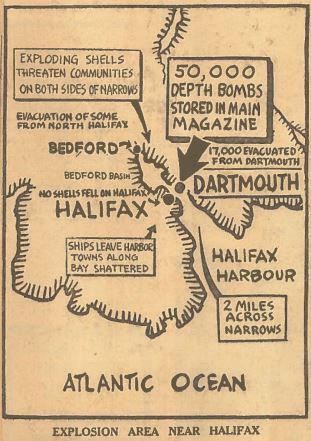

Digression: Around this same time, on a flight back to Europe, I had the privilege to sit beside an underwater ordinance remover from Holland. He was returning from his job of removing shells in Halifax Harbour. I remembered hearing on the news they were discovered in the mud on an anchor pulled onboard a waiting ship.

A final note on high voltage safety. Back in the 1990’s, our cable station was also a satellite earth station. We found it ironic that one needed to “jump through hoops” to access the high voltage areas of the submarine PFE, (~ 12kV max in

UNFIT?

Just an interesting trivia: Submarine cable (without repeater), has a Failurein-Time (FIT) of 0 per billion hours of operation. FIT values are used in statistics to estimate probabilities of failure / down time. Submarine cables are one of the most reliable devices on the planet. As an example, a deep-water section of the 1875 Direct Cable was in service into the mid 1950’s. It operated for over 75 years.

OVER THE TOP COST CUTTING

Now for your optical transmission lesson: Total Output Power of an optical repeater is often referred to as TOP. TOP is effectively how much optical power is pushed into the fibre. One would think that a higher TOP is better. For example, the Optical Signal to Noise Ratio (OSNR) at the far end, is the key metric for the performance of a submarine cable and OSNR is directly related to TOP. A higher TOP can translate to better performance BUT.... there are two other very important considerations:

1. If the TOP is too high, the optical signals are severely distorted, just as high-volume sound systems reach a point where they distort pleasant music, the invisible interactions of the high-power optical traffic signals with

molecules in the glass fibres, can deteriorate the signal’s quality significantly.

2. If the TOP is high, one could space repeaters further apart and reduce the number of repeaters in a cable. A significant initial cost saving.

I have had the good fortune to either operate, or design, o r test over 50 submarine cable systems worldwide. In general terms, system designs with a high ratio of repeater count to distance, and moderate TOP, are the best practice. These ensure maximum system performance (and capacity) for years to come. Any upfront savings on repeater count reduction are a poor trade-off for loss of traffic revenue due to loss of optical performance. Likewise, extending submarine terminals further than required will sacrifice maximum capacity & sacrifice performance. Studies can easily be done to quantify the trade-offs.

OFF-CABLE DCN & WHAT GOES AROUND, COMES AROUND: RESTORATION

A DCN is a data communication network. It is usually used for the terminal equipment at each cable end to interwork. 99.99999% of the time, an internal communication DCN network path through the working cable is fine, but when a cable is cut, this path is lost. Therefore, any cable system requires a diverse external “off-cable” network for internal communications.

of 3, we would each pull our restoration patches. The phone call went “3... 2... 1... dead silence...”. We immediately called each other, had a laugh, and verified the traffic was normalized. We both knew that our dropped phone call was also on the traffic path we were normalizing. Not ideal, but all worked out well in the end.

Although cable restoration became passé in the year 2000, when the submarine industry was turned upside down, the newer high-capacity cables of today carry so much traffic that consideration for reserving off-cable capacity for restoration, and cable restoration agreements will inevitably return.

GHOSTS & LIGHT SOURCES

Again, with this early November issue aligning well with Halloween and with All Souls Day, here is a true cable-related ghost story that will make you think twice about physics and light sources, and true sources.

In the 1990’s we worked a cable to Blaabjerg, Denmark and satellite links to Blaabjerg, Denmark. At the end of one cable repair, I was working from Canada with a cable engineer in Blaabjerg. We coordinated traffic normalization to switch the traffic from satellite restoration path back to the cable path. While on the phone, we agreed that after a count

In 1973, the CANTAT 2 submarine cable system was under construction. Teams of engineers and construction workers overwhelmed the short-term accommodations of the tiny village of Beaver Harbour Nova Scotia and vicinity. This location was the western end of the cable. Our family was one of many that relocated from Newfoundland, all families had members who had operated the older cables landing there. Other cable operators relocated from North Sydney, Nova Scotia. Engineers and managers from the offices of the Canadian Overseas Telecommunications Corporation (COTC) travelled to the area from across Canada. The system providers of STC (cable) and PYE (mux & microwave backhaul), both out of the UK, sent teams of engineers and managers to install, commission, and train. The towns in the area overflowed. Our family

Figure 20: “Faraday Station” 1875 Direct Cable Station, Torbay, Nova Scotia

Figure 21: Chekov said: “But Kiptan, the OSNR is off the scale! We would only need one repeater!”

settled for a time in a motel, then to a company trailer, others in apartments, and others in rental houses. One family from the UK rented a house across from the funeral home in the nearby town of Sheet Harbour. I recall my parents becoming friends with this family. One day, I recall my mother and her friend from the UK talking in our trailer’s living room, with very troubled looks on their faces. Years later I learned the story: My mother’s friend awoke one night in the small house with a strange man standing motionless at the end of the bed. She woke her husband who also saw the man. It was a ghost. I am not sure what occurred after that, but two eyewitnesses viewing light energy without a source certainly shows there is more to our corporal world than physics can explain. If you happen to read historical writings of Israel, you will see several references to such “light events”, so it is not really a new phenomenon, but perhaps poorly understood by most.

HOCKEY STICKS FOR EVERYONE!

Let’s end on a positive note and have a laugh at me at the same time :)

In the early 2000’s, during the dot-com boom, I was a hum-bug. I thought I was clever by theorizing that there was a maximum data consumption per-human, and the new growth curves of 2000 were not sustainable. Effectively you could assume that each human could only consume the

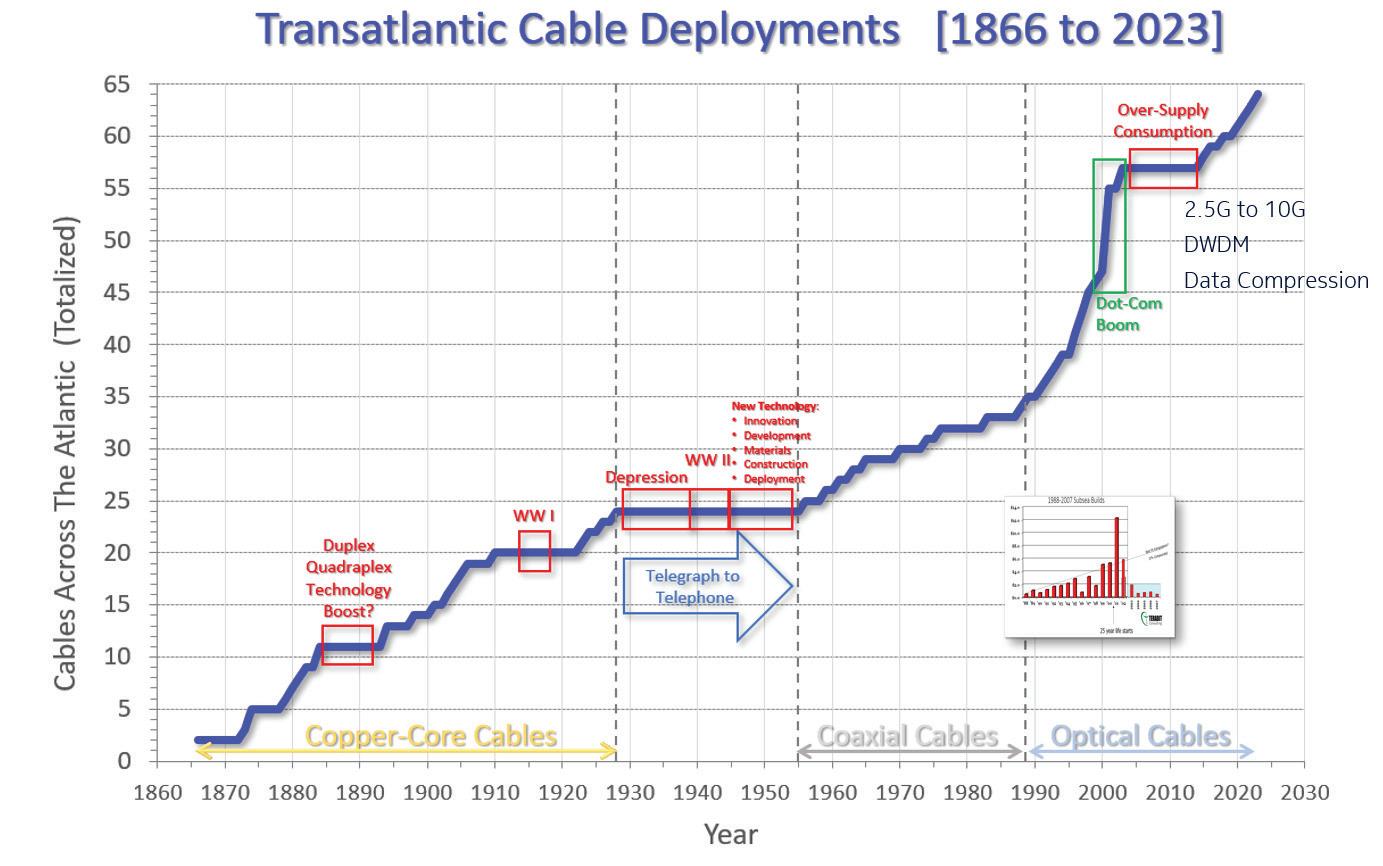

maximum data of serial video feed, at that time ~3 Gb/s for 3G-SDI. You could make corrections for statistical multiplexing, sleeping, bidirectional flow gaps, age of people, data compression, etc. Once you came up with a number, that was it, a consumption limit per human. You could then theorize that the consumed data was mostly stored or generated locally, and a small portion of the consumed data came from remote sites, requiring submarine cables for transmission. Basically, the theory distilled down to data transfer to / from a region being directly proportional to population in a modern, well-connected population. A crude calculation would go like this. Population of USA = 340 million, Maximum data stream per individual = 50 Mb/s. Total Data Consumption of USA = 17 Pb/s. If you assumed most of this data was generated locally and 10% was from overseas cables, then the USA would only need 1.7 Pb/s of total subsea capacity (to Europe, to Asia, and to South America). A contemporary SDM cable of 24 fibre pairs with 30Tb/s per fibre pair can supply 720 Tb/s. Just a few cables would provide more than my theory predicts, so I am clearly, and thankfully, wrong. Long live machine-machine comms and cute cat videos!!! So, I resigned from forecasting the future and now look backwards. Things now paint a very nice picture for our industry. Here is a plot of all transatlantic cable growth (qty) from 1866 to the present: STF

GEOPOLITICS

Perspectives of John Tibbles

INTRODUCTION

I began writing this article about three weeks ago but have constantly revised it, as there have been numerous articles about subsea cable systems in both mainstream and trade media during that time. Who would have thought this five years ago?

This is part of a series I’ve written, offering personal perspectives on the subsea world where I spent most of my career. Initially, they focused on increasing awareness of the subsea network, but they have increasingly covered geopolitical issues and their effects on our industry. Now, subsea cables are a geopolitical issue—and a significant one. How has this concerning transformation come about?

THE WHY

Cable capacity has grown massively due to the demands of the internet, providing an economic vehicle for the internet’s development—from the fledgling world wide web to the needs of hyperscale users. The network has remained highly reliable, considering its complexity. Interruptions have almost always been caused by factors such as mudslides, subsea volcanoes, and fishing, typically referred to as external aggression.

THE WHO

Governments were once more deeply involved with telecoms than they have been in recent years. Telecom operators were usually government bodies that owned the cables. However, with global telecom deregulation spreading, things became much more laissez-faire, and regulation was more about enabling than overseeing, though licenses and permits remained tricky issues. Generally, there was little interest in what telcos did or how they operated. Competition meant lower prices and new services, so all seemed well in the world.

Of course, this hands-off approach could go too far. It did when doubts began to surface about the potential that critical equipment in the new 5G mobile networks might be compromised. Could monitoring or disconnection be remotely controlled by a foreign entity? The supplier of the equipment in question was Huawei, from China. The anxiety over this issue was so great that the U.S., which had first raised the concerns, used its political influence to ensure operators in certain allied countries reconsidered using Huawei 5G equipment, which would have formed the backbone of their cellular networks.

Cable capacity has grown massively due to the demands of the internet, providing an economic vehicle for the internet’s development— from the fledgling world wide web to the needs of hyperscale users.

However, cables are global infrastructure, and eventually, geopolitics was bound to catch up. Now, “aggression” seems to mean just that: deliberate, targeted efforts to damage or disrupt a cable, or even monitor and extract the data being transported. That data carries the internet in all its forms—from international banking to amusing cat videos, from social gatherings to military secrets, from airline holiday bookings to the management of global logistics. All of this is jumbled together in a maze of commercial and state-level encoding. Thanks to the diversity of the global network, the internet can reroute itself quickly and securely. It has become the internet—and we cannot live without it.

Huawei was becoming a major player in subsea operations, offering innovative equipment and often significantly lower prices. Before long, the same alarm bells started ringing. Concerns were raised in Washington and other capitals that Huawei’s equipment might have more capabilities than advertised. It was suggested that users in those countries not only reconsider Chinese-made equipment but also avoid using cable systems with significant elements of Chinese control, such as cable stations or maintenance vessels. The result was disastrous for Huawei, which eventually sold its business to Hengtong. At the same time, China was extending its influence over the South China Sea—critical geography for Transpacific cables. Incidents and political tensions there led to the postponement of an

almost complete transpacific system and the costly rerouting of new systems.

That covered the technical concerns, but geopolitics isn’t only about technology. Russia’s invasion of Ukraine has divided international opinion and led to western sanctions. While Russia is a huge country, with minimal oceanic coastline, subsea cables matter little to them and their allies. However, many military and security bodies in the West now express concern, almost to the point of alarm, that while Russia may have little dependency on subsea cables, it doesn’t mean they fail to recognize their strategic importance and vulnerability. Deliberate damage to undersea cables is nothing new.

Technological advances and international collaborative efforts, such as those led by the International Cable Protection Committee, have greatly improved the protection of cable systems. However, these cables are now potential targets for military operations, which is a wholly different issue— cables now face deliberate threats.

THE WHERE – RESPONSES

In the last 18 months, there have been more and more media articles expressing the vulnerability of subsea systems and speculating about who might benefit from interference or eavesdropping. Memories of the Ivy Bells project during the Cold War, when U.S. submarines secretly tapped Russian cables in the northwestern Pacific, come to mind.

risk assessments regularly across the cable life cycle, taking into account technical and non-technical risk factors such as undue influence by a third country on suppliers and service providers,” or “Managing security risks, including from highrisk suppliers of undersea cable equipment.”

What does “undue influence” or “high-risk” actually mean in a market where there are only four suppliers worldwide, three in countries that signed the accord and one that didn’t, along with another 130 or so nations? If you are a nation that might be considered to exert “undue influence” or might be seen as a “high-risk supplier,” you might be China.

REACTIONS AND QUESTIONS

Does this sow the seeds of two internets: those signed up to this accord and their allies, versus those who haven’t signed because they have a different worldview or a different relationship with the country where the fourth supplier is based?

Does this sow the seeds of two internets: those signed up to this accord and their allies, versus those who haven’t signed because they have a different worldview or a different relationship with the country where the fourth supplier

is based?

Could the same thing be done with fiber optics? How can these vital but seemingly vulnerable arteries be protected? Diplomacy can be slow-moving, but this time there have been significant and rapid responses to such potential threats (and prompted more rewriting). Announcements from the U.S. State Department, the UN, and the EU have resulted in the proclamation of the ‘New York Principles.’ Although it sounds like an episode from The Sopranos, the Principles represent an accord among over thirty countries to cooperate on the security, protection, resilience, and even usage of the subsea network. These steps and actions, if adopted, might mitigate perceived risks. This is a positive approach because cables are never unilateral. They connect, at a minimum, two countries, often with several intermediate landings along their overall length of thousands of kilometers.

However, amidst the collaborative language are some curious expressions. Take, for example, “Consider security

Will this begin to divide the internet into two? If so, how will hyperscale content providers expand their businesses into developing countries, often with large populations? Will some parties view the Principles as a step toward American hegemony, not just over subsea cables but the entire seabed? Two recent articles in Australian media have expressed concern over such a possibility. It’s interesting that these concerns come from Australia—a nation with its head in the West but its body very much in the Asian hemisphere.

Can the world’s two largest economies really distance themselves from one another through the very medium that has brought the world together more than at any other time in history, despite numerous global conflicts? How will one of the world’s largest trading relationship function with no long-term internet connectivity, considering that for international data transfer, subsea cables are the internet?

SOME CONCLUSIONS

This is why I am writing this version at Cork Airport after attending the Valentia Island Subsea Cable Security and Resilience Symposium—a far-sighted event hosted by the Government of Ireland, local historical bodies, and the ICPC, where I presented a paper on subsea network resilience. Underlining the seriousness of the event was an informed keynote address from the Taoiseach (Irish PM), who traveled five hours from Dublin to speak. It was a novel, though perhaps not for long, unique event, with nearly 100 attendees.

These included European military representatives, Irish, Australian, and U.S. academics, Irish and European government officials, and numerous experts from the subsea cable industry around the world.

There were some very interesting discussions, such as how the military might protect cables and who should pay for enhanced protection—government or cable owners (the latter is the right answer, but it might not be the easiest to implement). How might certain countries react to the Principles? I was particularly struck by a presentation on this topic by someone who, in past years, would have been called a “China watcher.” Dr. April Herlevi, who speaks the language and has lived in China, offered a balanced and nuanced presentation. This gave me hope that global responses to the Principles might be equally balanced and nuanced, as China—with its 1.3 billion people—is a complex country with immense industrial and economic resources. It cannot simply be shut out from a world in which it has many friends and the capability to become the hub of a second internet.

divided Berlin. With two unconnected and politicized internets, could events like these happen again?

If you look at the footnote below, you’ll see where our meeting was held. Adorning the walls in the old cable station, now a museum, were numerous excerpts from press commentaries of the time. They all extolled the virtues of cables as bringing peace and goodwill to the world. Perhaps we should remember that.

In 1858, the first successful transatlantic telegraph cable was laid between Valentia Island and Heart’s Content in Newfoundland, Canada. It connected the Old World with the New World and forever changed the world in general.

(For more informed commentary on China and its neighboring seas from Dr. April Herlevi, see War on the Rocks.)

Do I have concerns? I do. At my age, I have vague memories of my parents’ anxiety over the Cuban Missile Crisis and a split Europe, with Russian and U.S. tanks nose to nose in

FOOTNOTE

Valentia Island is a beautiful part of County Kerry in the far southwest of Ireland. We were blessed with sunny weather that only enhanced its beauty. It is remote—three hours’ drive from Cork Airport and over five from Dublin.

So, why there? Because in 1858, the first successful transatlantic telegraph cable was laid between Valentia Island and Heart’s Content in Newfoundland, Canada. It connected the Old World with the New World and forever changed the world in general. The meeting was held in the original cable station complex, restored and maintained by the Valentia Island Transatlantic Cable Foundation (https://www.valentiacable.com/), which is working toward gaining UNESCO Industrial World Heritage Status. I wish them luck. STF

NATIONALIZING SUBSEA COMMUNICATIONS IN THE 21ST CENTURY

Perspectives of Kristian Nielsen 1.4

Subsea communication cables are the invisible backbone of the modern digital age. They carry over 95% of international data traffic, enabling everything from financial transactions to social media interactions. As global dependency on these cables intensifies, the debate over their management has gained prominence: Should governments nationalize these critical infrastructures to protect them, or should private investment continue to drive innovation and efficiency?

This article explores the complexities of managing subsea communications by examining academic insights from Stephen Korbin and D’Souza & Megginson. We will delve into the potential benefits and challenges of nationalization and privatization and consider how Public-Private Partnerships (PPPs) can offer a balanced solution that leverages the strengths of both models.

KORBIN’S INSIGHTS: UNDERSTANDING NATIONALIZATION

Stephen Korbin’s research in the 1980s provides a foundational understanding of why governments choose to nationalize industries. His studies show that nationalization is often a strategic decision driven by economic motivations, rather than political opportunism.

Stephen Korbin’s research in the 1980s provides a foundational understanding of why governments choose to nationalize industries. His studies show that nationalization is often a strategic decision driven by economic motivations, rather than political opportunism. It is typically selective, targeting industries of strategic importance, such as oil and telecommunications, where national control can significantly influence economic stability and security.

One of Korbin’s key concepts is the ‘Domino Effect.’

During the 1970s, Libya’s decision to nationalize British Petroleum’s assets inspired a wave of similar actions across the Middle East. Countries like Algeria, Iraq, and Iran followed suit, driven by a desire to control their natural resources and assert economic sovereignty. These actions were not merely reactive; they were part of a broader strategic effort to increase state revenue and reduce foreign dependency. Korbin’s methodology was rigorous. He analyzed political and economic factors across a broad range of countries and industries from 1960 to 1980. By identifying patterns and outcomes of nationalization efforts, he highlighted how these actions align with broader national goals. His research suggests that governments may consider nationalizing subsea cables for similar reasons: to protect national interests, secure critical infrastructure, and reduce reliance on foreign entities.

THE CONSEQUENCES OF NATIONALIZATION: A DECLINE IN INNOVATION

While nationalization can increase state control over critical assets, it often comes at a cost—particularly to innovation. Several factors contribute to this decline:

1. Reduced Incentives for Innovation: Nationalized companies typically focus on stability and employment rather than risk-taking and innovation. In Venezuela, for example, after the nationalization of the oil industry in 1976, the state-owned company PDVSA initially maintained high levels of technical competence. However, over time, po-

litical interference and underinvestment in research and development (R&D) led to a significant decline in technological advancement. By the early 2000s, PDVSA’s exploration and production capabilities had deteriorated compared to its global peers.

2. Bureaucratic Constraints: State-owned enterprises (SOEs) often have less flexibility in decision-making due to bureaucratic structures. A study by the OECD on SOEs across various sectors found that these entities generally have lower productivity and innovation levels compared to private firms. The lack of competitive pressures and profit incentives reduces the urgency to innovate, leading to stagnation.

3. Decreased R&D Investment: Nationalization frequently results in a decline in R&D spending as funds are redirected toward meeting state priorities. In the telecommunications sector in Latin America during the 1980s, state-owned companies were slow to adopt advancements like digital switching and fiber optics. The privatization wave in the 1990s led to a surge in innovation and infrastructure upgrades, highlighting the innovation gap during the period of state ownership.

assets, marking the start of a broader nationalization campaign across its oil sector. This action significantly increased state revenues and reduced foreign influence, allowing Libya to assert its economic sovereignty.

The impact was profound. Libya gained control over its most valuable asset and set a precedent that inspired other countries in the region, such as Algeria, Iraq, and Iran, to take similar actions. However, the nationalization of Libya’s oil industry also had drawbacks. The efficiency of the sector declined as state-owned companies lacked the technological expertise and management skills of their private predecessors. This led to decreased production capacity and strained relations with foreign investors and governments.

This case illustrates the double-edged sword of nationalization: while it enhances state control and revenue, it can also lead to operational challenges and reduced efficiency.

D’SOUZA & MEGGINSON: THE CASE FOR PRIVATIZATION

State-owned enterprises (SOEs) often have less flexibility in decision-making due to bureaucratic structures.

A study by the OECD on SOEs across various sectors found that these entities generally have lower productivity and innovation levels compared to private firms.

4. Shift in Operational Focus: Nationalized industries often prioritize strategic goals over profitability. In the Indian banking sector, for instance, nationalization led to an increased focus on financial inclusion and employment generation. While these are valuable social objectives, they were achieved at the expense of technological innovation and service improvement.

These examples illustrate the complex trade-offs associated with nationalization. While it provides governments with greater control over critical industries, it often results in a decline in innovation and efficiency. For the subsea communications industry, where technological advancement is crucial for maintaining secure and reliable connections, these potential drawbacks are particularly concerning.

CASE STUDY: NATIONALIZATION OF THE LIBYAN OIL INDUSTRY

A prime example of nationalization is the Libyan oil industry in 1970. Driven by rising nationalism and a desire to control its resources, Libya nationalized British Petroleum’s

In contrast to Korbin’s findings on nationalization, D’Souza & Megginson provide a compelling argument for privatization. Their analysis of 85 countries found that privatization often leads to significant performance improvements, particularly in utilities and telecommunications. Privatized firms tend to be more profitable, efficient, and innovative due to competitive pressures and a focus on profitability.

A notable example is the privatization of Mexico’s national telecommunications company, Telmex, in the 1990s. Before privatization, Telmex struggled with inefficiencies, poor service quality, and limited network coverage. However, after being sold to private investors, including Grupo Carso, led by Carlos Slim, Telmex underwent a remarkable transformation. The company invested heavily in expanding its network, improving service quality, and modernizing its infrastructure. Within a decade, the number of fixed telephone lines had nearly doubled from 6.4 million in 1990 to over 12 million by 2000.