When you choose us as your realtor, you ' re gaining the support of an entire team dedicated to your success! You can trust in our integrity and reliability to confidently guide you through the process.

As full-time brokers, we are honored to be part of Cascade Hasson Sotheby's International Realty. In 2023, our Sisters team sold over $16M in real estate Let's work together!

Suzanne Carvlin: 818-216-8542

Maddie Fischer: 541.419.5551 team@homeinsisters.com

What you can expect working with us

We are always one step ahead, anticipating potential roadblocks and finding creative solutions to overcome them. We’re Curious We’re Committed We’re Proactive We’re Personal

We want to have a clear understanding of your goals, who you are, and what your home means to you

We bring our A-game to every transaction, and we are committed to achieving the best possible outcome for our clients.

We believe in building relationships with our clients and treating them like family, because in the end, that's what leads to the best possible results

Maddie was an absolute We always felt like she h heart, whether it was for another. She was helpfu being pushy. We apprec knowledgeable she was and her willingness to pr and everything we reque resourceful, a wonderful consistently went above our needs. Since we we was imperative for us to ground and Maddie cam time. 5 star service! Than

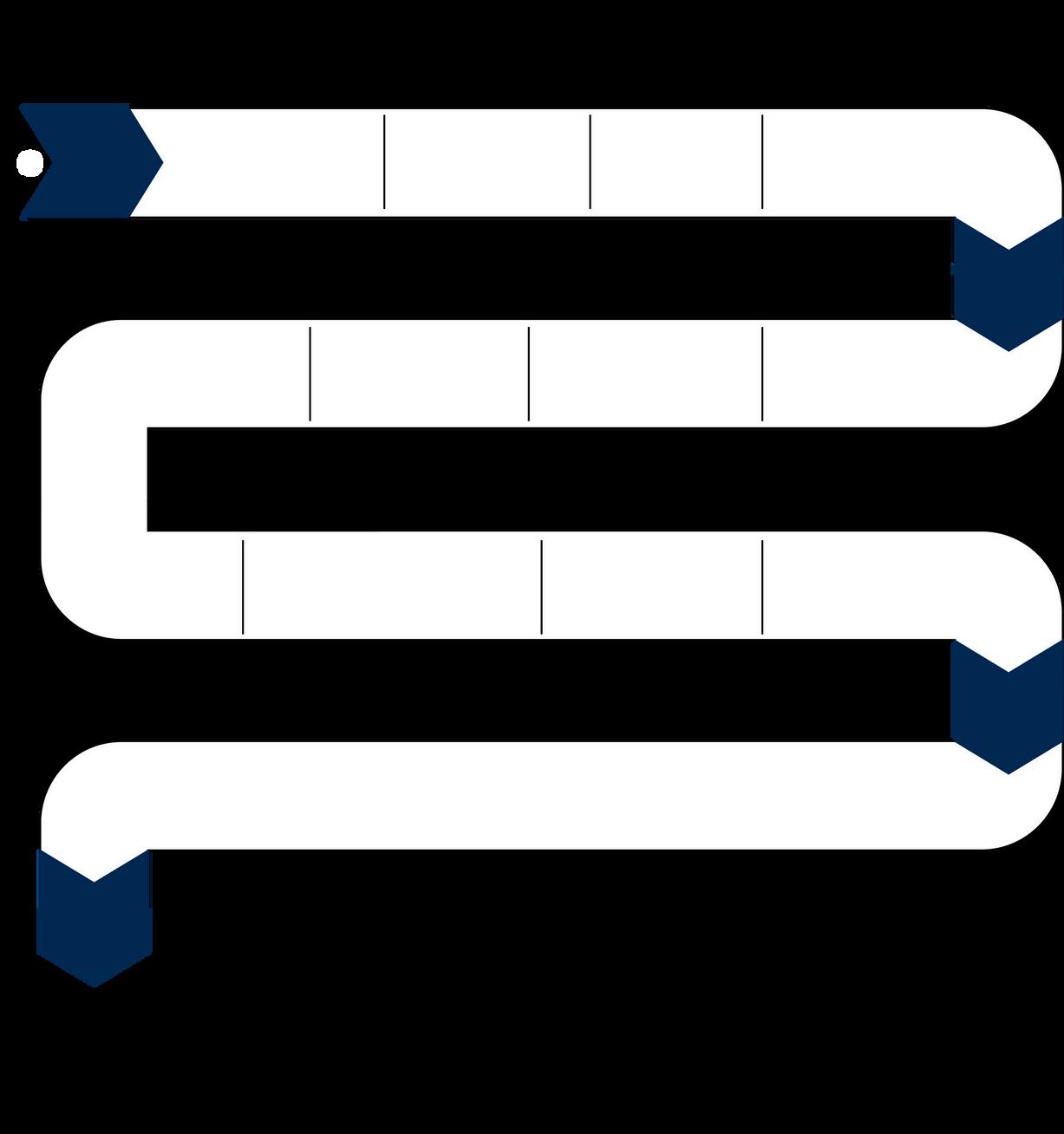

INITIAL CONSULTATION

Buying process overview

Determine needs and wants

Agent services

Market conditions

Lending qualification

Define agency relationship

INSPECTIONS AND PROPERTY

CONDITION REVIEW

Buyer inspections: Property, Pest, Roof etc

Second review of Seller disclosures

LOAN UNDERWRITING & APPRAISAL

Underwriter reviews files

Appraisal ordered by lender

LOAN PRE -APPROVAL

Obtain loan pre-approval letter from lender

Determine budget for home

SUBMIT HOME INFO TO LENDER

Escrow officer orders Preliminary Title Report Buyer funds are deposited into escrow account

HOME SHOPPING Tour properties that meet your “ideal home” criteria Monitor market inventory

OPEN ESCROW

Escrow officer will order Preliminary Title Report Buyer funds are deposited into escrow account

FIND HOME & MAKE OFFER

Review and sign off on available disclosures and reports

Discuss appropriate offer strategies with agent

Prepare and submit appropriate offer package

PRESENT & NEGOTIATE OFFER

Agent will present offer to sellers, Deal with any counteroffers, multiple offer situations or requests for changes in offer conditions

RECORD/TRANSFER TITLE & CLOSE OFE SCROW

Deed is recorded by the County Recorder’s Office

Get the keys to your new home!

UNDERWRITER REVIEWS FILES APPRAISAL

ORDERED BY LENDER If critical issues are discovered during buyer inspections or seller disclosure review determine appropriate action e g request for repairs, change to terms, price etc

LOAN FUNDING

Arrange for down payment and closing costs to be in escrow (e g cashiers check, wire transfer)

Lender sends balance of funding to Escrow Company

HOME INSURANCE

Select home insurance company and initiate coverage process Submit insurance information to escrow

SIGN-OFF DOCUMENTS

Review closing costs settlement

Sign loan documents

Return documents to lender for funding review

REMOVE CONTINGENCIES

After property inspections and confirmation of loan document approval, contingencies are removed

FINAL WALKTHROUGH

Final walkthrough is performed to confirm condition & completedrepairs if necessary

Property conditions should be consistent with condition on date of ratification

What is an escrow?

An escrow is a method of dosing a real estate transaction The escrow agent is given the responsibility to oversee and coordinate the closing activities, acting as a neutral third party between the buyers and sellers Your escrow officer must follow the instructions of both parties {buyers and sellers) involved in the transaction, and will remain unbiased.

Conditions Met Application

File Setup by Mortgage Specialist

Truth in Lending and Good Faith Estimate Sent to Borrower Send Verification(s)

Order Credit Report

Order Appraisal & Preliminary Title Report

Final Documentation to File

Underwriting Review

Approval

Loan Documents Sent to Escrow Agent

Borrower Sign Loan Documents Fund

Documents Recorded

What are your closing costs?

Lender Title Policy Premiums

Escrow Fee (shared 50/50 with Seller)

Document Preparation (if applicable)

HOA Transfer fees if applicable

Recording Charges and fees

Tax Prorations from date of close

New Loan charges, if any of home is financed

Make sure you ’ re financially prepared for homeownership Do you have a lot of debt? Plenty saved for a down payment? What about closing costs? Ask yourself “how much house can I afford?” before you go further Additionally, know that lenders look closely at your credit score when determining your eligibility for a mortgage loan Check your credit score and do anything you can to improve it, such as lowering outstanding debt, disputing any errors and holding off on applying for any other loans or credit cards.

Just like you want to get the home that best suits your needs, you’ll want to find a lender that best suits you. We suggest you consider using a broker to help you find a lender, talk to your agent we are here to help, ask friends and family for referrals, and compare at least three lenders.

A lender will need information from you in order to get you pre-approved for a mortgage loan Here are few things to have ready for them:

W-2 forms from the past two years

Pay stubs from the past 30 days

Tax returns from the past two years

Proof of other sources of income

Recent bank statements

Details on long-term debts such as car or student loans

ID and Social Security number

*If you ’ re self-employed, you may have to provide proof of your financial stability, including reasonable credit score, profit & loss statement, Year-to-date revenue, and possibly providing business tax returns.

This is where we discuss what type of home best suits your needs.

How long have you been looking for a new home?

What areas and neighborhoods are you considering?

What is your Plan B, if you can't find the home you have in mind?

What are some of your must haves?

What are deal breaker items?

We personalize the listings based on your specific criteria. We carefully select the best properties Now is an exciting time! When you are ready to write an offer, we will guide you through the contract. It's crucial to craft a fair offer to avoid the risk of the seller not responding or losing the property to another buyer

Negotiate the Offer

Fulfill Conditions for you to view and filter out the ones that don't meet your requirements.

We personalize the listings based on y specific criteria. We carefully select t properties for you to view and filter o ones that don't meet your requiremen

Typically, most buyers review around 1 properties before being ready to mak offer. If you haven't found the right ho then, it's highly advisable for us to rev review your criteria to ensure we are searching for the perfect house

Once you ' ve found a home you adore, to assess its market value. We will com the property to others that have recen allowing us to determine its true value.

This is a quick necessary process the h narrow down and determine how muc can afford!

Lenders typically recommend a home costs no more than three to five times annual household income, with a 20% payment. However, there are MANY d finacing structures that they can make for you!

er is accepted, the next crucial dule a home inspection within a ber of days. The home inspection ure that any defects or safety ressed before the closing.

f "title" refers to the right to use, and control a property. chase a home, you are quiring the seller's title to the to the closing, a title search is ensure there are no liens or at could hinder you from ear title to the property

s an evaluation of the property's s to not only justify the lender's t also to prevent the buyer from the property. Typically, your st the services of an appraiser u the associated fee at the g.

mitment lender's letter signifies f your home loan You will r detailing the terms of your loan is will include information such as rcentage rate, monthly fees, and repayment details for the loan

The closing process finalizes your hom purchase

A few things to bring to clos

A valid government issued photo Cashier's check payable for the t amount due

Any outstanding documents for t company or loan officer

Fees typically total 4% - 9% of purchase price and can include Escrow Fees

Recording fees

Application and underwriting fe

SIDs and/or LIDs

Appraisal Fees

Local Transfer Taxes

Homeowners Insurance

Homeowners Association Fees

Thinking it's impossible? It's actually not When you decide to buy a home, start thinking of yourself as a businessperson and investor rather than just a future homeowner. In fact, forget that you ' re the "Buyer" altogether. By looking at the transaction from a purely financial perspective, you'll distance yourself from the emotional aspects of buying the property While it is important to factor in certain emotional aspects, don't let it cloud your judgment Real estate is an investment Don't let emotions distract you from that.

It's often more exciting to tour potential homes than to dive into financial discussions with a lender This leads many first-time home buyers to begin their search before determining their borrowing capacity. As a result, they may experience disappointment when realizing they were looking at properties outside their price range or when they find their dream home but are unable to make a strong offer To avoid this scenario, it's advisable to speak with a mortgage specialist to get pre-qualified or even pre-approved for a home loan before embarking on your house-hunting journey. This pre-qualification or pre-approval process involves a thorough assessment of your income and expenses, and it can enhance the competitiveness of your offer by demonstrating to sellers that you have the financial backing to support your bid

If you purchase a pre-owned home, it's almost certain that unexpected repairs will be necessary shortly after Whether it's replacing a water heater or covering a homeowner's insurance deductible due to severe weather, these unforeseen expenses can add up. To avoid this situation, it's essential to save enough money to cover the down payment, closing costs, moving expenses, and potential repairs Lenders can provide estimates for closing costs, and it's advisable to reach out to multiple moving companies to obtain accurate estimates for your moving expenses. This proactive approach will help you prepare for any unforeseen costs associated with purchasing a home

When it comes to shopping for a mortgage, it's similar to shopping for a car or any other big-ticket item: it's worth it to compare offers. Mortgage interest rates and fees such as closing costs and discount points can vary from lender to lender

Surprisingly, the Consumer Financial Protection Bureau reports that almost half of borrowers don't shop around for a loan. To avoid this common mistake, it's recommended to apply with multiple mortgage lenders. By comparing offers from five lenders, the average borrower could potentially save $430 in interest just in the first year It's important to note that all mortgage applications made within a 45-day window will count as just one credit inquiry.

Know what you ' re looking for before you begin looking for a home. Create your own Wish List to help you identify all the things that you absolutely must have, as well as those items that would be nice but that you could live without. Print out the checklist, fill it in, and share it with us.

Price Range

Approx. Square Footage

Newer Home

Two Stories

Master Bedroom Upstairs

Family Room

Family Room Fireplace

Formal Dining Room

Gas/Heat

Central Air

Eat-in Kitchen

Tub & Separate Shower

Refrigerator

Electric Range/Cook top

Den/Office

Built-In Range/Oven

Self-cleaning Oven

Hardwood Floors

Microwave Oven

Disposal

Dishwasher

Laundry Room

Newer Roof

Automatic Garage Door

Basement

Security System

Landscape Sprinklers

Swimming Pool

Property Address

Date of Visit

Square Feet

Number of Bedrooms

Number of Bathrooms

Family room

Separate dining room

Eat-in kitchen

Formal living room

Separate den

Greatroom

Laundry room

Basement

Hardwood floors

Wall-to-wall carpet

Ceramic tile

Fireplace

Storm windows

Ceiling fans

Central air conditioning

Energy-efficient features

In-law apartment

No interior steps

Close to schools

Close to public transportation

Close to work

Close to childcare

Close to relatives/friends

Gated community

Community pool

Tennis courts

Close to parks

Close to hospitals

Basketball courts

Golf course

There are two types of conventional loans: the fixedrate and the adjustable-rate mortgage In an adjustable-rate mortgage, the interest rate can change over the course of the loan at five, seven, or ten year intervals For homeowners who plan to stay in their home for more than a few years, this is a risky loan as rates can suddenly skyrocket depending on market conditions.

This is the process of combining both interest and principal in payments, rather than simply paying off interest at the start. This allows you to build more equity in the home early on.

In order to get a loan from a bank to buy a home, you first need to get the home appraised so the bank can be sure they are lending the correct amount of money The appraiser will determine the value of the home based on an examination of the property itself, as well as the sale price of comparable homes in the area.

Assessed value

This is how much a home is worth according to a public tax assessor who makes that determination in order to figure out how much city or state tax the owner owes Buyer’s agent

This is the agent who represents the buyer in the homebuying process. On the other side is the listing agent, who represents the seller

Cash reserves

The cash reserves is the money left over for the buyer after the down payment and the closing costs

Closing

The closing refers to the meeting that takes place where the sale of the property is finalized. At the closing, buyers and sellers sign the final documents, and the buyer makes the down payment and pays closing costs

Closing costs

In addition to the final price of a home, there are also closing costs, which will typically make up about two to five percent of the purchase price, not including the down payment Examples of closings costs include loan processing costs, title insurance, and excise tax

Comparative market analysis

Comparative market analysis (CMA) is a report on comparable homes in the area that is used to derive an accurate value for the home in question.

This term refers to conditions that have to be met in order for the purchase of a home to be finalized. For example, there may be contingencies that the loan must be approved or the appraised value must be near the final sale price

Dual agency

Dual agency is when one agent represents both sides, rather than having both a buyer’s agent and a listing agent

Equity

Equity is ownership In homeownership, equity refers to how much of your home you actually own meaning how much of the principal you ’ ve paid off The more equity you have, the more financial flexibility you have, as you can refinance against whatever equity you ’ ve built. Put another way, equity is the difference between the fair market value of the home and the unpaid balance of the mortgage If you have a $200,000 home, and you still owe $150,000 on it, you have $50,000 in equity.

Escrow

Escrow is an account that the lender sets up that receives monthly payments from the buyer

Fixed-rate mortgage

There are two types of conventional loans: the fixedrate and the adjustable-rate mortgage In a fixed-rate mortgage, the interest rate stays the same throughout the life of the loan.

Home warranty

This warranty protects from future problems to things such as plumbing and heating, which can be extremely expensive to fix

Inspection

Home inspections are required once a potential buyer makes an offer. Typically, they cost a few hundred dollars The purpose is to check that the house’s plumbing, foundation, appliances, and other features are up to code Issues that may turn up during an inspection may factor into the negotiation on a final price. Failing to do an inspection may result in surprise costly repairs down the road for the home buyer.

Interest

This is the cost of borrowing money for a home Interest is combined with the principal to determine monthly mortgage payments The longer a mortgage is, the more you will pay in interest when you have finally paid off the loan.

Listing

A listing is essentially a home that is for sale. The term gets its name from the fact that these homes are often “listed” on a website or in a publication

Listing agent

This is the agent who represents the seller in the homebuying process. On the other side is the buyer’s agent, who represents the buyer.

Mortgage broker

The broker is an individual or company that is respo care of all aspects of the deal between borrowers whether that be originating the loan or placing it w source such as a bank.

Offer

This is the initial price offered by a prospective buy seller may accept the offer, reject it, or counter wit offer

Pre-approval letter

Before buying a home, a buyer can obtain a pre-ap from a bank, which provides an estimate on how m lend that person This letter will help determine wha afford

Principal

The principal is the amount of money borrowed to p Paying off the principal allows a buyer to build equ The principal is combined with interest to determin mortgage payment

Private mortgage insurance

Private mortgage insurance (PMI) is an insurance p buyer pays to the lender in order to protect the len on a mortgage. These insurance payments typically buyer builds up 20% equity in a home.

Real estate agent

A real estate agent is a professional with a real est works under a broker and assists both buyers and s home-buying process

Real estate broker

A real estate broker is a real estate agent who has broker’s exam and met a minimum number of transa brokers are able to work on their own or hire their o Realtor

A Realtor is a real estate agent who specifically is National Association of Realtors NAR has a code o ethics that members must adhere to

Refinancing

Refinancing is when you restructure your home loan old loan with an entirely new loan that has differen payment structures The main reason people refina loans is to get a lower interest rate on their mortga lower not only the monthly payment but also the ov

Title insurance

Title insurance is often required as part of the closi research into public records to ensure that the title and ready for sale If you purchase a home and find there are liens on the home, you’ll be glad you had