The market continues to face significant pressure across various categories, driven by a combination of economic and agricultural factors. Supply shortages, inflation, and fluctuating demand are recurring themes affecting multiple sectors.

In the protein market, chicken, lamb, and beef prices are rising due to factors like reduced supply, increased demand, and production challenges. Meanwhile, supply disruptions and disease outbreaks, such as avian flu and Foot and Mouth, continue to impact pricing and availability.

Fish prices are also increasing, fuelled by tariffs, lower quotas, and regional supply challenges. The dairy market shows mixed trends, with some products under price pressure due to weak demand, while others like skimmed milk powder (SMP) are seeing price increases.

Grain markets remain volatile due to regional trade uncertainties, and the sugar market has seen a decline, providing cost savings. Conversely, cocoa and coffee prices are rising, driven by production issues and market speculation.

Overall, the market outlook remains cautious, with tight supply conditions and rising costs affecting both producers and consumers.

As always, we are committed to offering long-term customer value whatever the short-term market challenges. We offer a range of alternative products across tiers and our team is here to help you explore your options.

YOUR SPECIALIST FOODSERVICE TEAM

The global food market can be unpredictable, but your supply doesn’t have to be. Our specialist team is here to help you stay stocked with quality options that fit your budget. Whether it’s discovering new products, exploring different price tiers, or finding the best value, we’ve got solutions for you. Talk to your ASM to arrange a meeting.

Centre of Plate

MICHAEL JOYCE

Mick has been in the industry for over 30 years. He is a qualified master butcher and provides his customers with expert information to add value to their business.

Centre of Plate

NEIL BRISLANE

Neil has been part of the Sysco team for over 20 years, with the last decade dedicated to Centre of Plate. His deep knowledge helps customers make informed decisions, adding real value to their business.

Centre of Plate

PHILL WARING

Phill joined the business in 2023 after 18 years working as a Chef. His roles were primarily in Fine Dining establishments throughout Northern Ireland, but he also spent time in Australia.

Produce

NOEL RYAN

Noel joined Sysco in 2022, however with 35 years in the produce business he brings a wealth of experience to his role. Noel’s belief in Sysco’s customer centric values plays an important role in how he does his job.

Produce

ALASDAIR MacINNES

Alasdair joined the business over 20 years ago, following 25 years as a chef working in busy restaurants. He began his career with Sysco in purchasing before moving to a produce specialist role.

Produce

RUTH POLLOCK

Ruth joined Sysco in 2024 and has over 20 years’ experience within fresh produce. Ruth enjoys working in partnership with her customers to come up with the best solution for their business.

Centre of Plate

KELAN McMICHAEL

Kelan has worked in the industry as a chef for over 25 years, in some of the finest kitchens in the UK and Ireland. He was honoured to be part of a team that cooked in the Hague, representing Ireland and Irish produce.

Produce

SIMON DOHERTY

Simon has over 35 years’ experience in the industry and is an expert in the industry and the produce category. Simon is always willing to go above and beyond to ensure the highest quality service.

Produce

ALISON KIDD

Since joining Sysco in 2022, Alison has cultivated strong relationships with many of our key customers. With a deep understanding of the fresh produce market, Alison provides solutions that drive growth and success for her customers.

Bakery & Dessert

ELAINE MEADE

Elaine joined the business in 2024 and brings over 15 years experience in the industry to her role. After training as a chef, Elaine worked in restaurants, hotels and cafes across Ireland and London, later opening her own café In Clare.

Bakery & Dessert

BRONAGH BEATTIE

Bronagh joined Sysco in 2023 and has over 20 years’ experience as a chef, working in fine dining restaurants, cafes and hotels worldwide. She enjoys supporting her customers with new ideas and innovation.

Produce

PATRICK KEOHANE

Patrick joined Sysco 6 years ago. He has a wide range of experience in the sector from growing potatoes on his family farm to the early days of his career prepping veg in a hotel and working as a kitchen porter. Patrick enjoys meeting new people as part of his role, supporting his customers to improve their business.

Catering Supplies & Beverage

JONATHAN O’SHEA

Jonathan joined Sysco in 2022 with over 18 years experience as a chef. Jonathan has vast knowledge and experience in the hospitality industry having worked in restaurants across all levels – from Gastro pubs to Michelin Star.

Catering Supplies & Beverage

DEBBIE BLACKBURN

Debbie joined Sysco in 2022 following 15 years in the coffee industry. She is passionate about customer service, always going the extra mile for her customers.

Bakery & Dessert

BRENDAN SEWELL

More than 32 years’ experience in the food industry in Ireland gives Brendan a deep understanding of the sector. Previously working as a Chef and a pastry chef in 5* Hotels, Brendan has a wealth of knowledge to share with his customers.

Catering Supplies & Beverage

JOANNE McCUSKER

Joanne joined Sysco in 2024 and brings over 30 years’ experience to her role. She began her career in the licensed trade and has owned two coffee shops before progressing into sales.

MACROECONOMIC UPDATE

The annual inflation rate in Ireland rose to 1.9% in January 2025, up from 1.4% in the previous month. This was the highest reading since July 2024 and was driven by price increases in the following:

FOOD AND NON-ALCOHOLIC BEVERAGES

2.6% v 2.0%

ALCOHOLIC BEVERAGES AND TOBACCO

3.8% v 3.1%

0.4% v 0.1% HOUSING AND UTILITIES

2.7% v 1.3% HEALTH 3.9% v 1.6% TRANSPORT 1.2% v 1.1% COMMUNICATION 3.9% v 3.7% RESTAURANTS AND HOTELS 2.5% v 2.2%

MISCELLANEOUS GOODS AND SERVICES

By contrast, price growth slowed in recreation and culture (1.5% vs 3.3%), remained steady for education (at 2.3%), and dropped at a softer pace for clothing and footwear (-6.5% vs -8%) and furnishings, household equipment and maintenance (-0.8% vs -1.3%).

On a monthly basis, consumer prices fell by 0.8% in January, after a 0.9% rise in December. However, the inflation rate in Ireland is expected to be 2.8% by the end of this quarter, according to Trading Economics global macro models and analysts’ expectations.

Source: Central Statistics Office Ireland

PROTEIN

BEEF

Irish beef prices are rising due to tight supply and strong demand, with a 35-40% YOY increase expected by the end of Q1. Retail demand is growing in Ireland and the UK, with further growth anticipated in 2025. The UK, a key export market, forecasts a 5% drop in domestic production in 2025, likely increasing reliance on Irish beef. EU exports grew 3% YOY, but production is expected to dip slightly in 2025. Irish production is forecasted to fall 5%, driven by prime cattle reductions. Global demand remains strong, with South Africa and Australia filling gaps in the US and Chinese markets. Sysco offers diverse beef options to help manage rising prices.

R4 Steer Price Trend 2023 - 2025 C/KG

KEY POINTS

Prices

Rising due to tight supply and high demand; 35-40% YOY increase expected by end of Q1.

Demand

Growing in Ireland (+1.2% in 2024) and UK (+2.2% in 2024), with further growth expected in 2025.

Exports

• 46% of Irish beef went to the UK in 2024 (+5% from 2023)

• UK production to drop 5% in 2025, increasing reliance on Irish beef

• EU exports grew 3% YOY, but production to decline 0.5% in 2025

Production

Irish output to fall 5%, mainly due to prime cattle reductions.

Global Demand

Strong, with South Africa and Australia filling US and Chinese market gaps.

PORK

Pig prices in 2024 have remained stable after early-year surges driven by supply constraints and increased demand. However, challenges such as reduced supply in Germany, seasonal demand, and external cost pressures are expected to impact prices in the coming months.

KEY POINTS

Price Stability

Pig prices stayed steady for most of 2024 following significant increases early in the year due to lower supply and higher demand.

Increased Competition

New slaughtering capacity on the Island intensified competition for live pigs, further driving prices up.

Q2 and Q3 Outlook

Prices are expected to face upward pressure in Q2 (April-June) and Q3 (July-September), with Q3 potentially seeing greater strain due to reduced pig supply in Germany (down to 700,000/week from nearly 1 million three years ago).

Seasonal Demand

High BBQ demand during the summer could further push prices up.

Foot and Mouth Disease in Germany

Germany’s inability to export pork to the UK may disrupt supply chains, forcing UK processors to source pork from other countries like Ireland. The UK, only 70% self-sufficient in pork, relies heavily on imports.

Cost Pressures

Processors face rising costs, including minimum wage, packaging, and energy, which may contribute to price increases throughout the year.

LAMB

The Irish lamb market is facing unprecedented challenges, leading to record-high livestock prices and significant supply constraints. A combination of reduced production, strong demand, and external factors like religious festivals is driving prices upward, with no relief expected in the near future.

KEY POINTS

Record Prices

Livestock prices are at least 30% higher year-on-year, driven by tight supply and strong demand.

Production Decline

Throughput levels have dropped by 26% in the last six weeks, with total year-to-date slaughter down 32% (70,274 head) compared to 2024.

Supply Constraints

A smaller lamb crop, difficult lambing conditions, and inconsistent grass growth have significantly reduced lamb availability.

2025 Forecast

Lamb availability is expected to decrease by approximately 430,000 head in 2025, exacerbating supply challenges.

Strong Demand

Demand for lamb remains robust, with no signs of slowing into 2025. Manufacturing product demand has surged in the last 8-10 weeks due to reduced supply and strong market interest.

Global Factors

A shortage of southern hemisphere lamb in Europe has further intensified demand for specific products (e.g., middles and manufacturing).

Seasonal Pressure

Upcoming religious festivals (Easter and Ramadan) are expected to drive additional demand for lamb carcasses, further straining supply.

Price Outlook

Livestock prices are likely to remain elevated into 2025 due to ongoing supply challenges and sustained demand.

CHICKEN

The European fresh poultry market is facing significant inflationary pressures and supply challenges in Q2 2025, driven by rising costs, disease outbreaks, and reduced production capacity. With strong demand expected during the BBQ season, prices are forecasted to increase further, compounded by global competition and reduced export quotas.

KEY POINTS

Price Inflation

Fresh poultry prices have risen by an estimated 10% since mid-Q1 2025, with further increases of 5-10% expected by the end of summer due to seasonal demand.

Supply Challenges

Bird Flu and Newcastle Disease outbreaks, particularly in Poland, have led to the culling of 8-9 million birds, severely impacting new bird placements for the April cycle.

Production Reductions

The European Chicken Commitment (ECC) and Better Chicken Commitment (BCC) are strategically reducing growing capacity in Europe and the UK, straining supply to meet demand.

Expana Benchmark Price for Fresh Polish Chicken Breast Grade A (9A05)

Export Constraints

The EU has cut Ukraine’s export quota by 50%, further tightening supply availability.

Operational Disruptions

Many Polish slaughterhouses are operating on 4-day weeks, a situation expected to persist until at least the end of April.

Global Competition

Countries outside Europe (e.g., Middle East, China, Mexico) are offering higher prices for poultry, making it difficult for EU countries to secure stock at reasonable costs.

Outlook

Continued inflation and supply constraints are expected to dominate the European chicken market through Q2 and beyond.

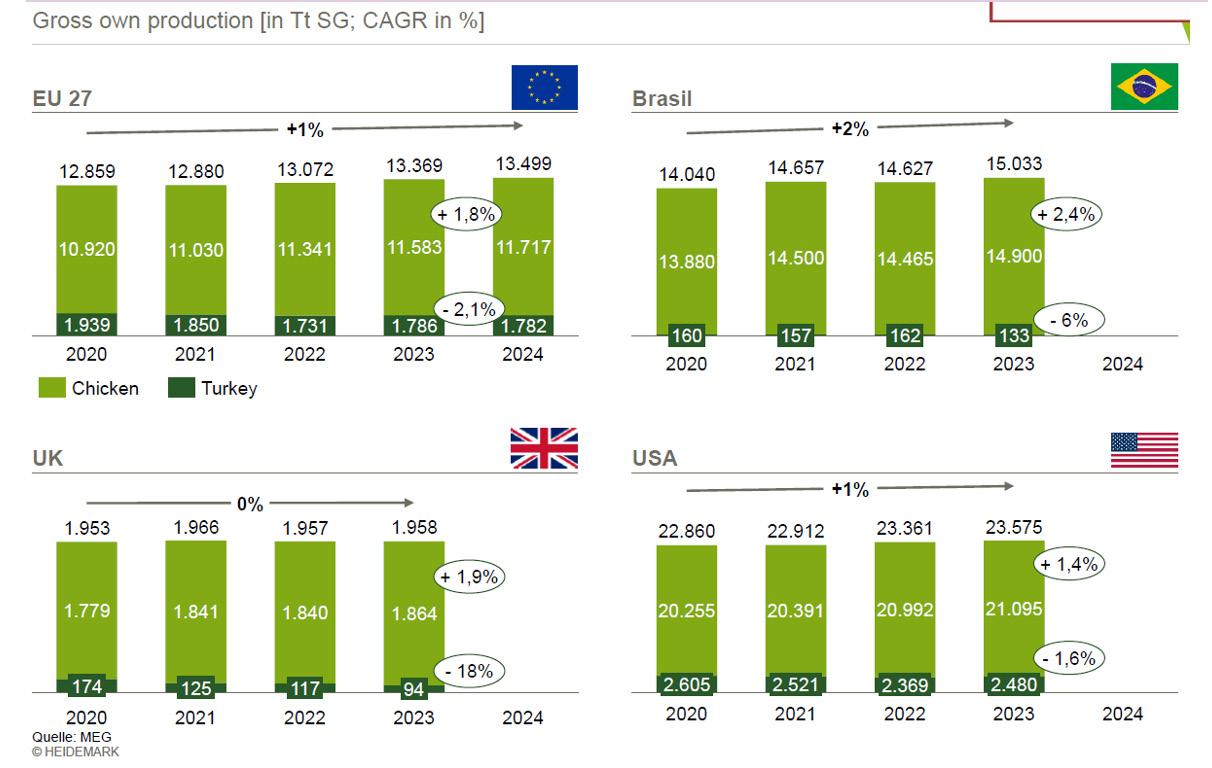

EUROPEAN TURKEY

Global turkey meat production is declining amid rising avian flu outbreaks, while chicken meat production continues to grow. The ongoing impact of avian flu has significantly affected turkey supplies, keeping prices elevated with potential spikes expected in Q2 2025.

Gross own production [in Tt SG; CAGR in %]

KEY POINTS

Production Trends

Turkey meat production is declining globally, while chicken meat production is increasing.

Avian Flu Impact

In the 2024/25 reporting year (01.07 - 30.06), 420 avian flu outbreaks affected 27 million birds, including 1.9 million turkeys.

Key Losses

The largest turkey losses occurred in Poland (660,000), Italy (582,000), England (261,000), Hungary (177,000), and Germany (146,000).

DUCK

Duck continues to see stabilisation in the market coming into Q2 2025.

Supply Constraints

Fresh and frozen turkey stocks are under pressure due to avian flu, with market prices remaining 40% higher than Q3 2024 levels.

Price Outlook

European turkey prices are expected to stay elevated in Q2 2025, with potential spikes reaching peak levels seen during Christmas 2024.

COOKED MEATS

COOKED MEATS

The industry is experiencing supply shortages and price inflation across multiple protein commodities, leading to price adjustments for cooked sliced and whole chicken fillets, as well as sliced beef products.

KEY POINTS

Cooked Sliced Beef

Prices are increasing by 5-6% heading into Q2 2025.

Cooked Chicken Supply

Vendors have secured sufficient stocks of fresh cooked sliced whole and sliced chicken to meet Q2 demand. A 1% price increase will be applied due to rising National Insurance contributions and minimum wage adjustments implemented at the end of February.

Gluten-Free Breaded Chicken Range

Prices will increase by 5% in Q2 due to supply constraints as a result of Avian Flu and Newcastle Disease outbreaks across Europe which are reducing chicken availability.

• Production Constraints Farms adhering to the European Chicken Commitment (ECC) guidelines for chicken welfare are reducing placement capacity, further limiting supply.

SEAFOOD

SALMON

Salmon prices have stabilised after December-January peaks but remain high. Production and consumption are expected to grow by 3.5% in 2025, but prices will rise again before Easter and stay elevated until H2 2025.

KEY POINTS

• Prices remain high despite stabilising post-December peaks

• Production and consumption to grow by 3.5% in 2025

• Prices will rise before Easter and stay high until H2 2025

HADDOCK

Haddock prices are rising sharply, following a similar trend to cod, with reduced volumes, higher costs, and increased demand due to US tariffs on Chinese whitefish. Quota cuts and spawning season are further tightening supply.

KEY POINTS

• Prices are rising, with Week 6 volumes half the previous week

• US 10% tariff on Chinese whitefish has shifted focus to European markets

• 2025 haddock quota reduced by 5%

• Spawning season (until May) means less meat content and higher costs

• Poor catches are keeping prices high

COD

The 2025 cod quota has been set at 350k tonnes, a 30% reduction from 2024 and a 65% drop over the last five years. Record-high prices are driven by extremely tight supply, with no immediate relief expected despite a slight supply improvement in April. Cod will remain a challenging species in 2025 due to ongoing supply and price pressures.

KEY POINTS

2025 Quota

350k tonnes, a 30% reduction from 2024 and 65% lower than five years ago.

Current Prices

Cod prices are at record highs, up over 30% this year, with further increases expected.

Supply Constraints

Spawning grounds are closed until April,

reducing allowable catches and keeping fresh North Atlantic cod prices extremely high.

Stock Shortages

Large processors have no stock, and prices will not ease even with a slight supply improvement in April.

Outlook

Cod will remain a problem species in 2025 due to limited supply and high prices.

HAKE

The Irish hake quota for 2025 has been reduced by 20%. Spanish vessels fishing in Irish waters are landing most of their catches in France and Spain due to higher prices there, with very little being landed in Ireland or the UK. This trend is expected to continue as catches are insufficient to meet demand, driving prices up in both fresh and frozen markets.

PRAWNS

Following Chinese New Year, prices for Vietnamese product have risen, while Indian prices have remained steady. Supply is expected to recover slightly with the first crop harvest in late March, but prices are likely to stay at elevated levels.

SQUID

Squid prices have surged to multi-year highs due to poor catches and significant shortages. The supply squeeze has worsened after China’s New Year holiday, with catches down 75% year-onyear. All species (Ilex, Todarodes, and Gigas) and sizes remain expensive, and prices are unlikely to soften unless fishing conditions improve.

DAIRY

EGGS

Bird flu (avian influenza) continues to pose a significant threat across the island of Ireland, driven by wild bird populations and poor infection controls. To mitigate the risk, a compulsory housing order for poultry and captive birds was introduced on 17 February 2025, following confirmed cases in the North and over 112,000 birds culled due to suspected infections.

KEY POINTS

Recurring Threat

Bird flu, a highly infectious disease, has been facilitated by wild bird populations and global influenza fluctuations.

Housing Order

A compulsory housing order for poultry and captive birds was implemented on 17 February 2025 to prevent contact with wild birds and reduce virus spread.

DAIRY MARKET

Human Risk

While low risk to humans, people can spread the virus.

Culling

Over 112,000 birds have been culled due to suspected cases.

Government Action

Minister Martin Heydon emphasised the need to protect the poultry industry and farmers’ livelihoods through these measures.

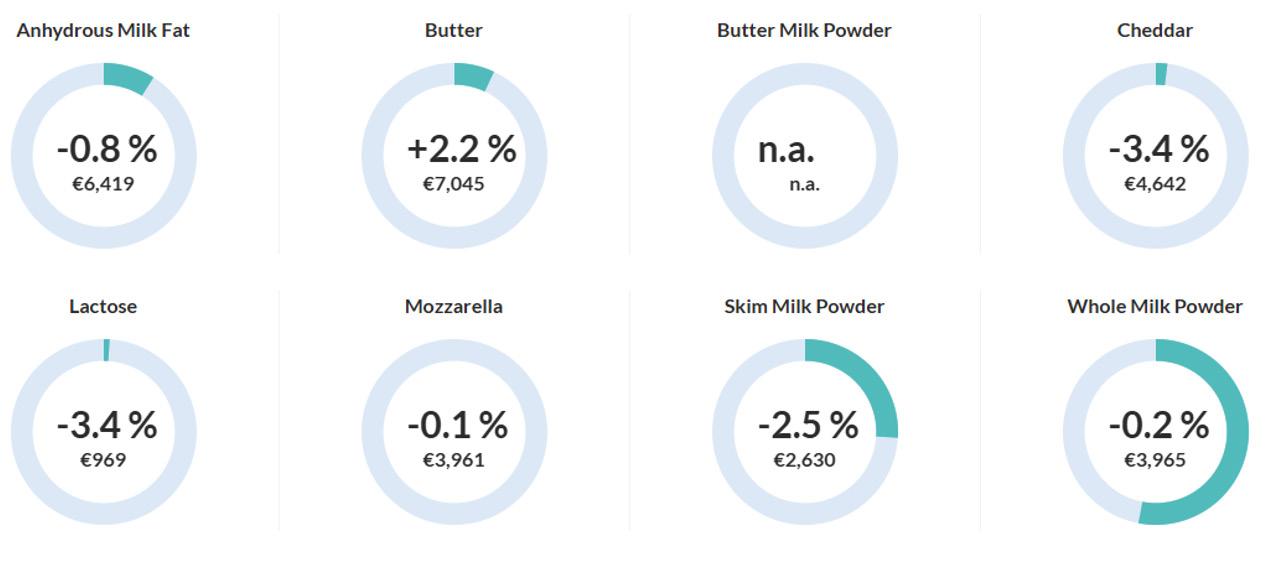

UK cream and butter prices have decreased while UK skimmed milk product (SMP) prices rose week-on-week (w-o-w). Dairy fat prices remain mixed across the EU. Price spread between offers and bits continues to persist for milk powders. The cheese market remains steady this week with limited activity.

MILK

The UK milk market remains ‘bearish’, with stable prices and steady demand amid mild temperatures boosting milk intakes. Meanwhile, the German milk market sentiment is mixed, with prices fluctuating and strong retail and industrial demand supporting spot milk. Across the EU, milk supply is increasing seasonally, with fat and protein levels slightly above expectations. Dairy fat prices remain mixed, while UK cream and butter prices fell, and SMP prices rose week-on-week.

KEY POINTS

UK Market

• Prices unchanged; demand steady due to mild weather boosting milk intakes

• Milk fat and protein levels are in line with market expectations

• Cream and butter prices decreased, while SMP prices rose week-on-week

German Market

• Mixed sentiment with prices fluctuating above and below last week’s levels

• Strong retail and industrial demand supported spot milk prices

EU Trends

• Milk supply is increasing seasonally

• Milk fat and protein levels are slightly above expectations but vary regionally

• Dairy fat prices remain mixed across the EU

• Price spreads between offers and bids persist for milk powders

BUTTER

The UK and EU butter markets face continued downward price pressure, with bearish sentiment driven by weak demand, sufficient supply, and growing milk intakes. Limited market activity, seasonality, and efforts to clear older stocks further contributed to the subdued outlook.

KEY POINTS

EU Butter Market

• Prices unchanged, with bearish sentiment across the dairy fat complex

• Demand was weak, though end-users sought to cover additional demand compared to the previous year

• Producers and traders focused on clearing older butter stocks before the new milk season

• Weak cream demand and lackluster spot demand further weighed on prices

Products

UK Butter Market

• Prices rose slightly despite bearish sentiment, with limited activity due to Gulfood event attendance

• Demand declined due to seasonality and weak food service demand

• Supply remained sufficient, with growing milk intakes expected to boost butter production in coming weeks

Expana Benchmark Prices for European Butter

BAKERY

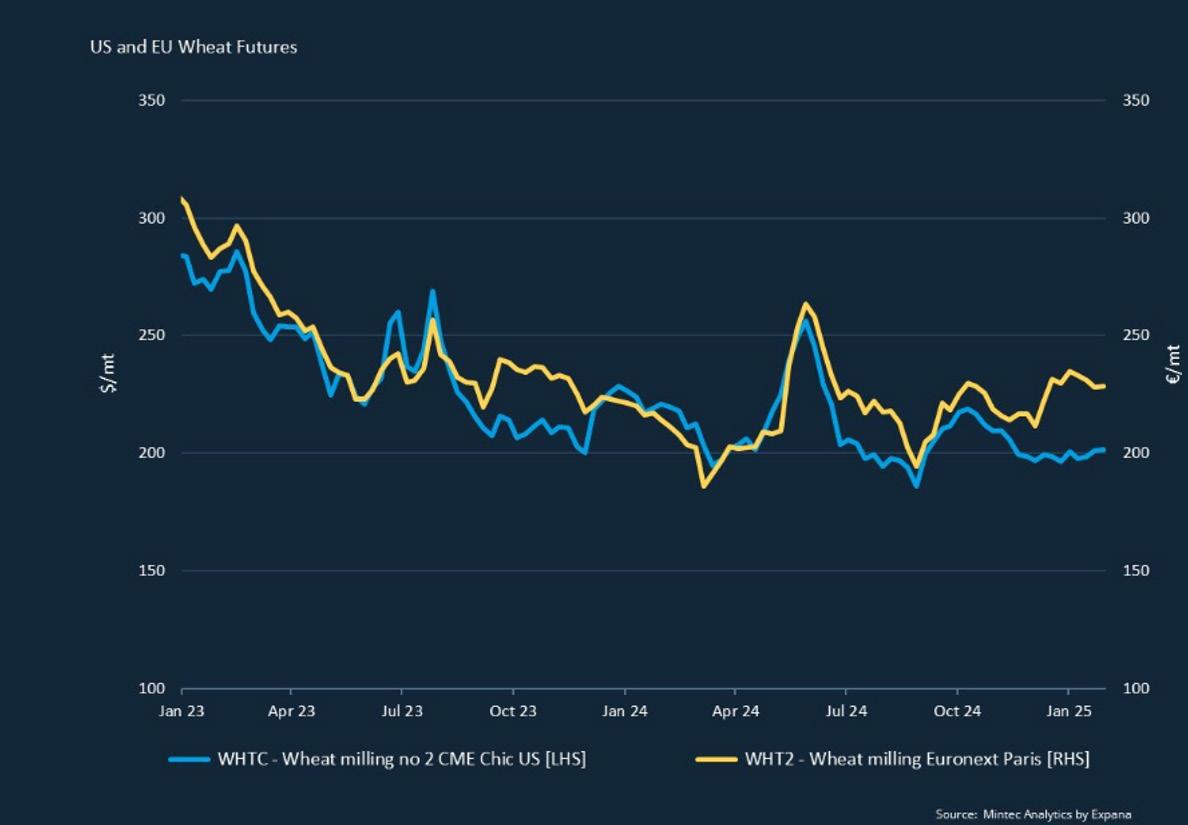

FLOUR

The grain market remains volatile due to cold weather concerns in the Black Sea region and the USA, coupled with renewed trade uncertainties. Russia’s wheat crops are under stress from low temperatures and minimal snow cover, significantly slowing exports, while Ukraine faces ongoing drought conditions. Additionally, fresh trade concerns have emerged following President Trump’s reaffirmation of plans to impose tariffs on Mexican and Canadian imports.

Monthly Price Movements

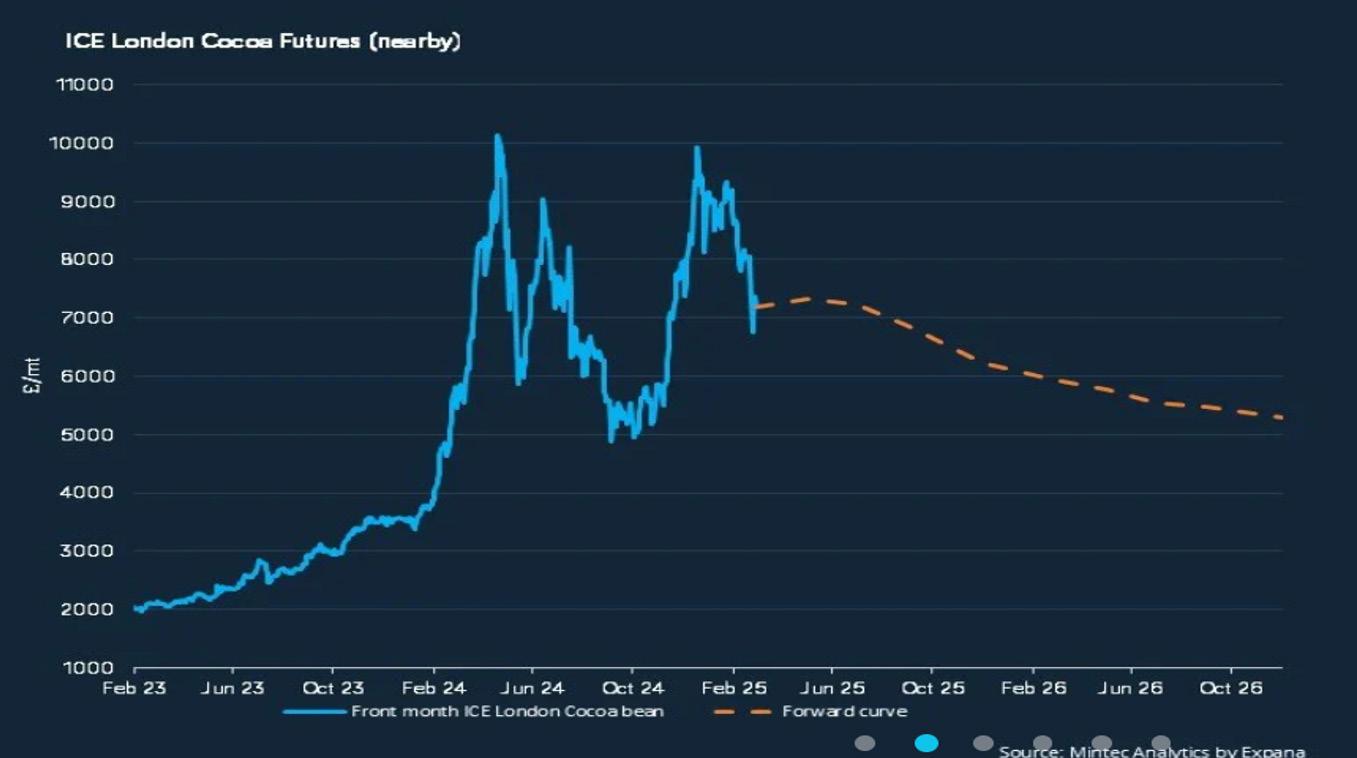

COCOA

The Ivory Coast, the largest cocoa producer, expects its new harvest to match last year’s levels, falling short of industry expectations of 4.8 million tonnes. While West African production continues to decline, increased output in Brazil and Peru is partially offsetting the shortfall. Speculators are driving the market, with cocoa prices currently trading 32% higher year-on-year. As a result, Callebaut and chocolate decoration lines will be reviewed in the April cost forum. Monthly Price Movements

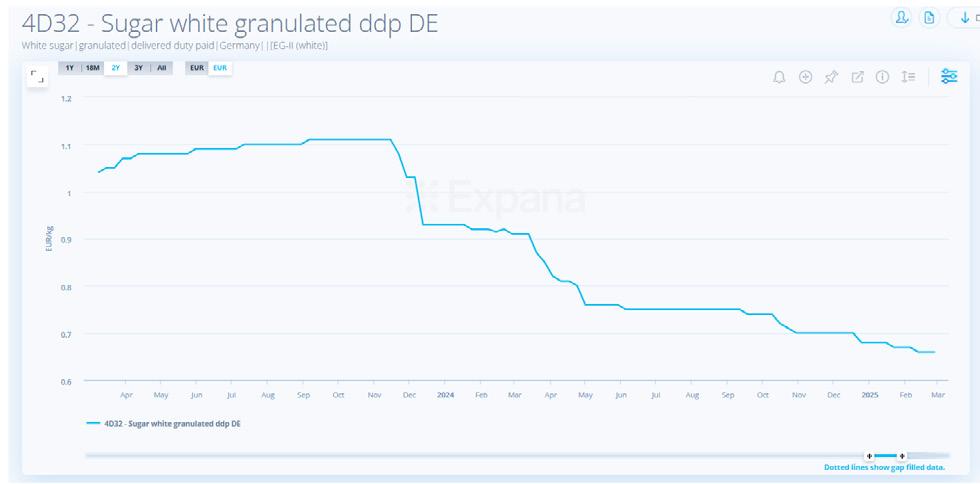

SUGAR

Sugar prices have declined by 27% year-on-year, leading to cost savings that were passed on to customers across most sugar lines. All sugar products are under contract, with price adjustments finalised in January.

CANNED & DRIED

OIL

With some stabilisation in the market on core commodities in Canned & Dried, this is being overshadowed by the expediential increases in Cocoa & Coffee.

Global demand for edible oils and fats continues to grow, driven by rising populations and biodiesel mandates, though this season’s consumption growth is expected to slow to 1%. With consumption likely to outpace production, prices remain supported by reduced rapeseed and sunflower seed harvests and lagging palm oil production. Market conditions remain uncertain, influenced by tariff discussions and the potential impact of Spain’s bumper crop, though quality considerations will be key in supplier selection.

KEY POINTS

Demand Growth

Global demand for edible oils and fats has risen by 4% annually over the past two years, though this season’s growth is expected to slow to 1%.

Supply Constraints

Reduced rapeseed and sunflower seed harvests, along with slower palm oil production, are supporting prices.

Market Uncertainty

Ongoing tariff discussions and fluctuating production levels add volatility to market conditions.

Price Outlook

Prices may decline slightly due to Spain’s bumper crop, but quality remains a critical factor in supplier selection.

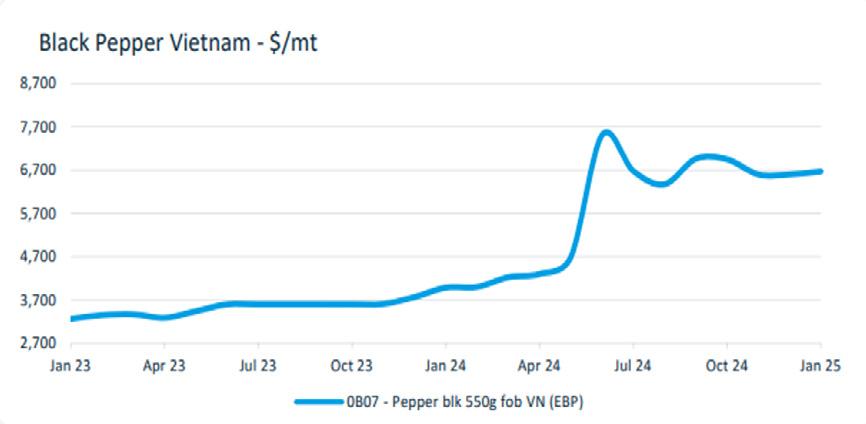

PEPPER

Cyclone activity and weather volatility caused significant price spikes in black pepper earlier this year. While the market has stabilised in recent months, prices are expected to remain elevated through 2025 due to anticipated increases in demand.

In January, the average price of Vietnamese Black Pepper increased by 1.1% m-o-m and rose by 67.4% y-o-y to $6,670/mt. The market remains relatively balanced with stable supply and demand. The delay of the February harvest until March/April has dampened market activity, but many expect prices to remain elevated through Q1 2025 as demand is expected to increase, particularly from Chinese importers, according to market players.

BEVERAGE & IMPULSE

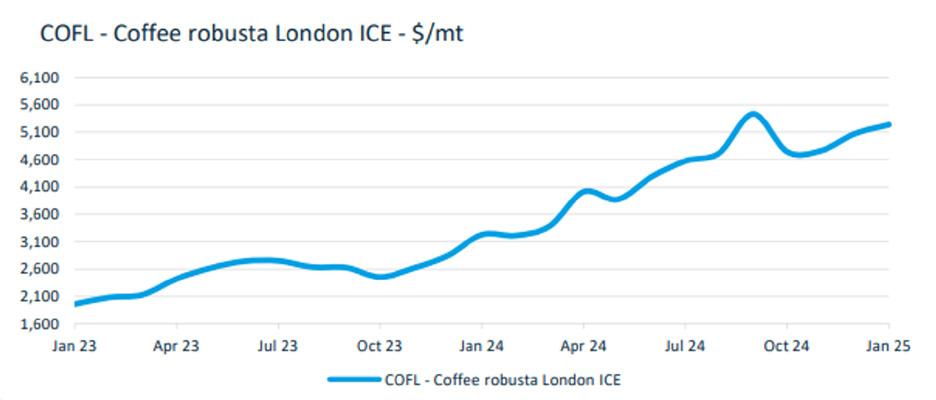

COFFEE

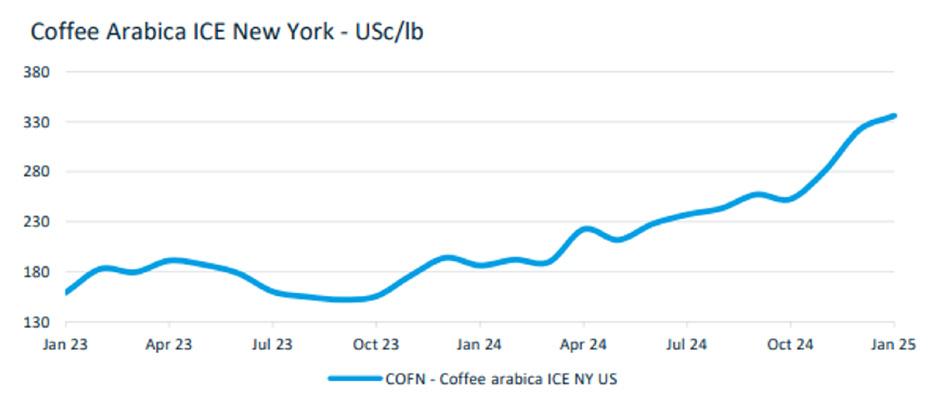

Arabica and Robusta coffee prices have reached all-time highs, driven by thin trading, speculative buying, and a stronger Brazilian Real. Physical trade remains low due to poor availability from key origins following Brazil’s record exports in 2024. Concerns about lower production, drier weather in Brazil, and supply security for 2025 are further fueling market pressures.

COFN - Coffee Arabica ICE NY US

Coffee | Arabica ‘C’ contract | several Central and South American | Asian and African countries | Intercontinental Exchange (ICE) USA | [futures]

KEY POINTS

Price Surge

Arabica and Robusta prices hit record highs due to speculative buying and a stronger Brazilian Real.

Low Physical Trade

Availability from many origins is limited after Brazil’s record export year in 2024.

Increased Demand

Interest in landed coffee in consuming regions has grown, with certified stocks declining for the first time in over a year.

Weather Concerns

Drier conditions in Brazil since late January have raised worries about crop development.

Supply Risks

High export rates in 2024 and potential lower production in 2025 are prompting buyers to secure supply, with analysts warning of potential supply challenges.

FRESH PRODUCE

FRESH PRODUCE

We remain committed to supporting local growers and are eagerly anticipating the arrival of Irish seasonal vegetables, herbs, and fruit crops, which will begin in mid-May and early June. The transition from Spanish to Dutch seasonal vegetables will take place in early May, following the end of the Spanish season in late April.

TOMATOES

• Production of some tomato varieties has declined due to cooler weather and rain in Spain

• Seasonal factors and strong demand are expected to drive price increases in the market

• The Irish seasonal carrot crop will soon finish, transitioning briefly to Scottish and Dutch supplies

• Spanish carrots will then be sourced for a few months, with Irish carrots expected to return by mid-July

ONIONS

We hope to see better availability of Dutch White and red onions over the next few months, but prices may increase due to Spanish Onions finishing up early due to internal breakdowns.

Potato supply has improved compared to last season, though costs remain higher than pre-2023 levels. Supply and demand are expected to align well until the new season crop arrives, with planting set to begin in late March/early April, weather permitting.

The Global Packaging Index fell slightly in February but remains 1.2% higher than last year, driven by sharp increases in paper prices. While packaging and cleaning products have seen some price pressures due to macroeconomic factors, our buying power has helped maintain flat pricing in key areas. However, tableware, particularly glassware, faces significant cost increases due to rising energy prices and reduced production output.

KEY POINTS

Packaging & Disposables

Raw material prices on paper-based products have risen by around 10% year on year, but we have managed to maintain flat pricing across this subcategory.

Cleaning & Hygiene

Paper hygiene products (e.g., centrefeed, toilet tissue) remain flat in price.

Chemical products from Ecolab and Diversey

are increasing by 3-5% due to rising Employer NIC costs.

Tableware

Annual price reviews have led to increases of 2-15% across Genware, Churchill, and Utopia lines. Glassware is most affected, with higher energy costs and reduced factory output driving price hikes.