Aerospace Outlook: Inventory Correction is Likely to Continue Japan Titanium Society Shares Research

Rick Sutherlin Decides it’s Time to Pass the Torch

IATA Touts Commercial Aerospace Recovery

International Titanium Association Announces New Directors to the Board

By Michael C. Gabriele

The International Titanium Association (ITA), Denver, CO, has announced three new members to its board of directors: Steve Chavez of All-Met Recycling; Brett Paddock of Titanium Industries; and Olivier Maillard of Airbus.

Olivier Maillard

Olivier Maillard, Airbus vice president, metallic raw materials and fasteners procurement, is joining the ITA board. A Master of Engineering graduate of the Ecole Centrale Paris (France) and of the Technical University of Munich (Germany), Maillard began his career in 2006 within the Airbus Hamburg plant, contributing to the ramp-up and leadtime reduction programs of the A320 and A330/340 programs, along with the industrialization of the A330 Freighter.

In 2011, he became head of Aerostructure Procurement Strategy and Business Operations, being notably responsible for the roll-out of raw materials enablement schemes in the Airbus Aerostructures Supply Chain. With the launch of the Beluga XL program in 2014, he was appointed as Program Leader for the Rear Fuselage development that occurred in partnership with Spanish-based AERNNOVA.

After successful delivery of the first components to the final assembly line, he moved in 2017 to the Airbus Group CTO to lead the E-Fan X HybridElectric Propulsion Demonstrator in partnership with Rolls-Royce. When the Covid pandemic hit in 2020, he joined the Industrial Strategy task force that designed the contours of today’s Airbus Atlantic and Airbus

Aerostructures and the new operating models and governance. Following the creation of these new entities early 2022, he took over a leadership position in Airbus General Procurement before his appointment in June 2023 as vice president, metallic raw materials and fasteners procurement.

Steve Chavez is the chief executive officer of All-Met Recycling Inc., a family owned and operated recycling company located in Anaheim, CA. Chavez has 40 years of experience in the recycling industry. All-Met services a variety of different business sectors, but specializes in the aerospace industry in both commercial and defense. During his years with AllMet he has directed sales and marketing as well as customer development.

For the past 40 years All-Met has processed aluminum, ferrous and steel alloys for smelters and foundries globally. In 2016 All-Met expanded its processing capabilities to include titanium alloys and has quickly become a prominent supplier of all types of titanium feedstocks to most of the titanium melters in the United States. Today he works closely with the third generation of Chavez’s to work in the industry—his son and partner Nick Chavez who handles the day-to-day operations of the titanium division.

All-Met Recycling was founded in 1957 by Manuel A. Chavez. AllMet was originally located in Los Angeles and later moved to its existing facility in Anaheim in 1984. Manuel Chavez’s legacy proudly lives on with a management team comprised of three generations of the Chavez family. AllMet has become one of the leaders in the

scrap metal industry with its effective and efficient processes and programs that help serve its growing customer base.

The Anaheim facility occupies over four acres of land and this expansion has given All-Met the ability to process, bale, and export over 6 million pounds of scrap metal per month. Today, All-Met services over 200 industrial accounts throughout Southern California and over 20 local scrap dealers.

Over the years, All-Met has built relationships with many consumers both domestic and abroad. By working with All-Met, customers receive organized, prompt, and professional metal recycling services. All material is sorted and processed by trained and experienced metal processors.

Brett Paddock Brett Paddock of Titanium Industries Inc., Rockaway, NJ, is returning to the board. He previously served as the president of the ITA group. Paddock is the president and chief executive officer of Titanium Industries, and his diverse metals background consists of engineering consulting, fabrication, manufacturing, contracting, and sales. He has held positions of vice president of sales and marketing, director of operations, and chief operating officer at Titanium Industries (T.I.).

Prior to joining T.I. in 2001, Paddock served as the director of operations for one of the nation’s largest structural steel fabricator/erectors and principal of an Eastern US engineering design and consulting firm. Holding a bachelor’s of science degree in engineering and a master’s of science degree in structural mechanics from Lehigh University, is a licensed engineer in multiple states.

Titanium Industries, established in 1972, provides specialty metals solutions for the aerospace, medical, industrial and oil and gas markets and maintains a global service center network.

Steve Chavez

BOARD OF DIRECTORS

Executive Committee

ITA President: Martin (Marty) Pike

ATI Specialty Materials, reporting to CEO and President Kim Fields Marty brings more than two decades of ATI experience to this role, leading the Specialty Materials team to successful execution in meeting the demands of the aerospace ramp today and in the future

In addition, Marty currently serves as Vice President, Global Commercial Strategies Marty is the primary point of contact across ATI with strategic customers seeking to grow and expand their partnerships with ATI A long with his responsibility for strategic customers, Marty leads our International Sales organization, the Defense Market Sector and Hypersonics teams He also serves on the boards of Shanghai STAL Precision Stainless Steel Co , Ltd, a joint venture between ATI and Baowu Special Metallurgy and as Vice President on the Board of Directors for the International Titanium Association

ITA Vice President: Sam Stiller

VP Commercial for Howmet Aerospace. All Sales, Marketing, and Customer Service, globally, is led by Sam’s commercial team

ITA Secretary/Treasurer: Phil MacVane

Phil MacVane was named VP of Sales –Americas for PCC Metals Group in January 2016 In his role he is responsible for the sale of all titanium and nickel products in the Americas He began his career at TIMET as North American Engine Manager in September 2000

Past President:

Dr. Markus Holz

Professor, ITA academic member

Dr Holz is currently Professor at University of Applied Sciences Anhalt starting from 2020 T here he is the program director of Logistics Management, teaching Operations Management and is currently involved in several national and international research programs in the field of sustainability and digitization in the industry

Continuing Directors

About the ITA

Michael Marucci

Chief Technology Officer

Kymera International

Safety Education Co-Chair

John J. Scherzer

Vice President – Medical Markets

Carpenter Technology Corporation

ITA Committee Medical Technology Member

Edward Sobota Jr.

Vice President, New Product Development

STS Metals

ITA Awards Committee Chair

Jennifer Simpson

Executive Director

Ex-Officio Member of the Board

International Titanium Association

ITA (https://titanium.org/) is a membership-based international trade association dedicated to the titanium metal industry. Established in 1984, the ITA’s main mission is to connect the public interested in using titanium with specialists from across the globe who may offer sales and technical assistance. Working through its extensive membership resources, the ITA seeks to expand the knowledge base for the metal, providing technical literature and sponsoring seminars and conferences.

Membership Drive for 2025 Ends January 31st –Contact ITA today to join.

MEET THE ITA

Safety Education Co-Chair

Robert G. Lee President Accushape Inc

Industrial Applications

Christopher Wilson Director of Research and Development NobelClad

Michael C. Gabriele

Chris Olin Managing Director, Northcoast Research Analysts LLC

CONGRATULATIONS

Jacob Beddome

Colorado School of Mines

Mechanical Engineering

Women in Titanium

Holly Both Vice President of Marketing Plymouth Tube / Plymouth Engineered Shapes Medical Technology

Dr. Colin McCracken Product Manager, Biomedical, Titanium Oerlikon Metco (Canada) Inc

Japan Titanium Society

Brooke Galcik Waynesburg University Biochemistry

Special Thanks to Academic Scholarship Sponsors: ATI

Howmet Aerospace

Kymera International

Perryman Company

STS Metals

Alexander Weiss West Virginia University

Mechanical and Aerospace Engineering

Ti Today Contributor

ITA Committee Chairs

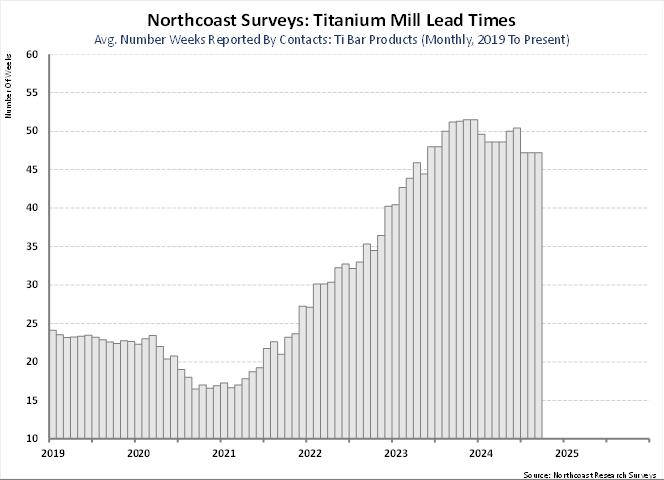

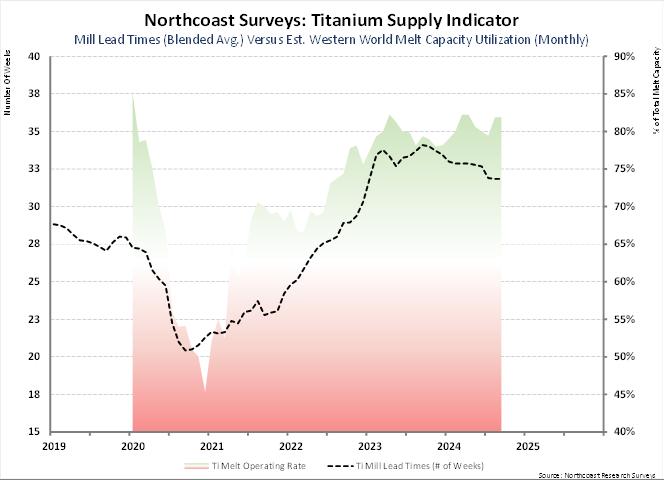

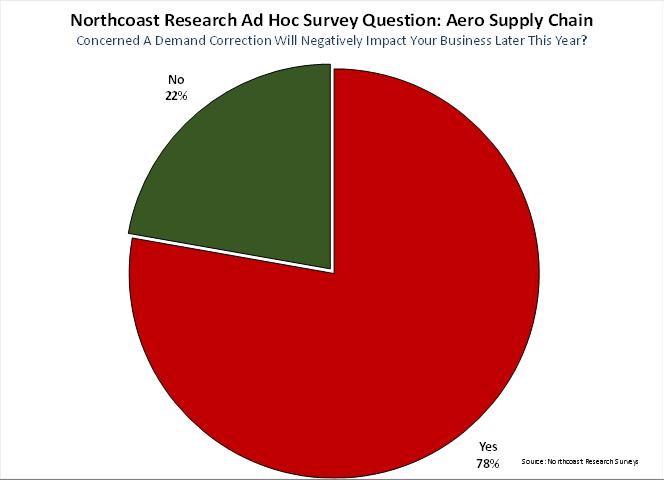

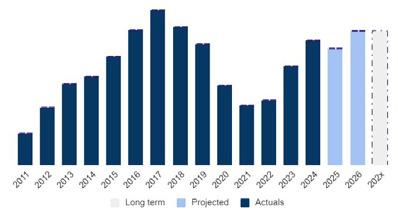

Aerospace Outlook: Inventory Correction is Likely to Continue Well Into 2025

By Chris Olin, Northcoast Research Analysts LLC

Brace Yourselves, the Downturn is Coming

Commercial aerospace suppliers will face a more challenging flight path in the coming two to three quarters as a result of coordinated efforts to reduce channel inventory and the inability for the OEMs to meet previously communicated aircraft production targets. The majority of key sub-markets, according to our proprietary survey work, are experiencing slowing or negative demand growth. This could lead to lower-than-expected shipment levels for upstream aero suppliers and several members of the International Titanium Association, particularly those suppliers connected to large aircraft structures and/or the Boeing 787 Dreamliner.

Narrowing the focus down to titanium, we would rank this product group at or near the bottom of our confidence list due to the apparent downside to forward-looking market expectations and the lack of channel visibility. Companies involved with the production, distribution, and fabrication of titanium appear to be in the most precarious position today, in relation to the other actively monitored aerospace-related product groups, due to the amount of excess material held within the channel and likely to fall short of 2025 expectations. On many occasions, we have labeled the titanium group its “own worst enemy” due to an inability to maintain active supply controls and/or decisions to limit

Companies involved with the production, distribution, and fabrication of titanium appear to be in the most precarious position today, in relation to the other actively monitored aerospace-related product groups, due to the amount of excess material held within the channel and likely to fall short of 2025 expectations.

The aerospace market correction has begun early, and we fear titanium industry participants may feel the brunt of early demand weakness.

—Chris Olin, Northcoast Research

transparency. Bottom line, the aerospace market correction has begun early, and we fear titanium industry participants may feel the brunt of early demand weakness.

Revised Macro Outlook

We have reduced commercial aircraft production targets several times in the last year due to unexpected changes in

master schedules, risks associated with extended Federal Aviation Administration (FAA) oversight of the Boeing 737 program, supply chain bottlenecks or aircraft parts shortages, and a shortage of new jet engines. The revised calendar year 2025 build outlook of 1,672 total jets is about 300-350 units lower than our forecast issued last December, on top of the significant shortfall expected in calendar year 2024.

The Bad News May Not Reflect Current Market Expectations

Our aerospace industry production forecast assumes that Boeing Company will not meet its stated year-end build rate targets for the 737 and 787 aircraft programs, which are 38 and 5 per month, respectively. According to recent channel checks, Boeing’s supply chain order activity is down 3-4 percent from last year, and the giant aerospace OEM has warned its suppliers that new orders will decrease over the next two to three months. The procurement slowdown was attributed to the company’s efforts to

reduce aircraft part inventories, but the conservatism also coincides with the expiration of the International Association of Machinists (IAM) labor contract in mid-September. Given the aggressive new contract demands made by union leadership and Boeing’s financial situation, we believe there is a reasonable chance of a work stoppage. Quick math shows that the company would lose approximately 35-40 jets from planned production each month the assembly lines in the Pacific Northwest are halted.

Potential Demand Weakness in Early 2025?

Upstream supplier expectations seemingly stabilized in the current quarter, following the aggressive resetting of internal calendar year 2024 sales forecasts that took place over the previous two months. Still, the peer group has not emerged from the short-term period of demand turbulence just yet. Highlevel industry contacts believe the aerospace market correction is unlikely to end until next summer,

assuming no further changes to master production schedules.

The newest Titanium Snapshot report issued by Northcoast Research focuses on these weaker-thanexpected demand trends, channel overfill, and a subdued market expectations, relying heavily upon the results of our nearly completed quarterly survey. We updated the industry model to reflect increasing aerospace market headwinds, macrorelated demand weakness, and widespread supply chain efforts to draw down inventory. The net-result of the modeling revisions is a lower calendar year 2025 global titanium market growth forecast of plus 2 to 3 percent, year over year, (down 300 basis points), including a negative outlook for the Western World region, following what appears to be a low-single-digit growth environment in 2024

Survey Read No. 1: A Severe Market Correction

Channel checks are showing a clear downturn in titanium-related demand driven by a sharp pullback in commercial aerospace and medical orders, a pre-election pause across many industrial markets, and concerted supply chain efforts to liquidate excess inventories. Average volume growth seems to be holding in the plus 6-7 percent year-over-year range for a secondconsecutive quarter, which is down from the plus 10-11 percent comp to start 2024. Distributors are seeing a more pronounced slowdown in order activity, as evidenced by the plus 3-4 percent growth realized by the survey group in relation to the plus 10-12 percent comp calculated for the upstream-levered titanium subgroup.

Survey Read No. 2: Mixed Spot Price Trends

The recent drop in titanium scrap costs (or negative mill surcharge revisions) has caused some downward pressure in the spot market, but the nearterm outlook appears stable. However, they reported a slightly higher average mill quote for premium-grade downstream mill products in third quarter of 2024. A lack of large-volume customer orders appears to be the cause of the 8-percent sequential drop in the spot price of grade-two titanium plate, and there are other indications of weakness in the commercially pure titanium product space.

Survey Read No. 3: The Bullwhip Effect

Conservation industry management is likely to prompt stronger demand headwinds in the first half of this year, as companies within our survey network recently confirmed plans to accelerate liquidation efforts over the next two to three months. Countermeasures implemented by aerospace suppliers to address near-term balance sheet stress or liquidity constraints have exacerbated the inventory pressure, along with distributor reactions to limited demand visibility and negative communications with large customers. In the third quarter of this year, industry contacts described internal inventory positions as overinflated and instructed most procurement officers to reduce warehouse holdings by 6-7 percent. That said, “invisible inventory” may

be the core problem for the titanium channel, given that both major buyers and subcontractors appear to be holding more than six months of excess buffer stock, seemingly unable to install appropriate titanium supply contracts.

Survey Read No. 4: Aerospace Shortfall

The Boeing supply chain is showing significant demand weakness, with suppliers reporting negative comps for the third quarter of this year prior to a three-month inventory drawdown effort that will soon reverberate throughout the global market. The aerospace OEM has warned aerospace suppliers

about significant changes to future order rates, with the planned changes to procurement coinciding with the expiration of a major labor contract. The weakness in commercial airframe demand is likely to negatively impact titanium suppliers over the next three to four quarters. This market represents roughly 25-30 percent of titanium market consumption.

Top Quote from the Channel

“In terms of market demand, it looks like 2025 will be a difficult year for titanium. For the major producers, excluding military/defense, we expect a 20-percent unit volume decrease compared to 2024. The stock levels are high at all stages.”

Disclosures

The research presented in this article is produced by Northcoast Research Partners, LLC, Cleveland (https:// northcoastresearch.com/) (“Northcoast Research” and/or the “Firm”) a registered broker dealer, member of the Financial Industry Regulatory Authority (FINRA; www.finra.org) and the Securities Investor Protection Corporation (SIPC; www.sipc.org), and an Ohio Registered Investment Advisor offering equity research and trading. Research is produced and distributed to institutional investors only. The research does not provide individually tailored investment advice and has been prepared without regard to the circumstances and objectives of those who receive it.

Reports are for informational purposes only and are not intended as an offer to sell or solicitations to buy securities. The services provided by Northcoast Research to clients may depend on a specific client’s preference regarding the frequency and manner of receiving communications, the client’s risk profile, investment horizon, and the size and scope of the overall client relationship with the Firm, as well as legal and regulatory constraints. The information provided is as of the issuing date indicated on this document and subject to change. Northcoast Research may offer other customers alternative products and services that may reach different conclusions or recommendations that could impact the price of the equity security. Certain information has been obtained from thirdparty sources we consider reliable, but we do not guarantee that such information is accurate or complete. Opinions expressed in this financial analysis are our current opinions as of the issuing date indicated on this document. The

companies covered by Northcoast Research are continuously followed by the analyst. Based on developments with the relevant company, the sector, or the market, which may have a material effect on the research views, research reports will be updated as deemed appropriate. Targets, forecasts, estimates, valuations, and opinions concerning the subject company or its securities, and information involving composition of market sectors included in this report reflect the analyst judgments as of this date and are subject to change without notice.

The analyst(s) that authored this report may have had discussions with company to ensure factual accuracy prior to publication. Past performance is not indicative of future results. A change in any assumptions may have a material effect on the projected results, future returns are not guaranteed, and loss of original capital may occur. The information transmitted is intended only for the person or entity to which it is addressed. Any review, retransmission, dissemination, or

other use of, or taking of any action in reliance upon this information by persons or entities other than the intended recipient is prohibited. If you receive this in error, please contact the sender and delete the material from any computer. n

[Editor’s note: Chris Olin joined Northcoast Research in 2023 as a Managing Director and Senior Research Analyst following the Aerospace Supply Chain and Specialty Materials Group. He has written a number of guest articles over the years for TITANIUM TODAY. Prior to joining Northcoast, Olin was President and Lead Analyst at Tier4 Research, a research boutique founded in 2000 offering high-level research to investors and industry executives. Earlier in his career, he was a founding partner of Cleveland Research Company and Longbow Research, holding a senior analyst position following the Metals and Mining Group. He has been awarded for stock picking accuracy several times and was named the sixth best stock picker on Wall Street by Forbes Magazine in 2006 and number one in the metals sector (repeated in 2017). With a 25-year background in sellside research, Olin has been cited by numerous publications, highlighted on Mad Money, and a live guest on CNBC and Bloomberg Television. Chris earned a Bachelor of Science degree in Economics at Eastern Michigan University while a member of the college football and track teams. He holds the FINRA Series 7, 24, 63, 86, and 87 licenses.]

Leading Titanium Manufacturer

—TC

Premium Quality, Stability and Reliability.

One-Stop titanium alloy production and service.

ABOUT US

A dozen years of titanium alloy production and research experience, with more than 100 patents and achievements to its credit, mastering a number of core technologies; Accredited with Nadcap non-destructive testing certificate and AS9100D, ISO14001, ISO 45001 and other certifications;

CORE PRODUCTS

Titanium bar/billet

Size range: Φ15-500mm

Grade: Ti6Al4V, Ti-6242, Ti-6246, Ti-38644, Ti-15333, etc.

Titanium wire rod coil

Size range: Φ1.0-20.0mm

Grade: Ti6Al4V, Ti6Al4V ELI, Ti-38644, Ti-6242, Ti-6246, Ti-15333, Ti-422, etc.

Titanium forging

Size range: customized, disc, bar, ring, etc.

L(max):14m, W(max):4m, H(max):4m.

Grade: Ti6Al4V, Ti6246, Ti6242, Ti662, Ti38644, Ti15333, Ti1023, Ti422, etc.

For more information, please visit www.tcae.com/en/

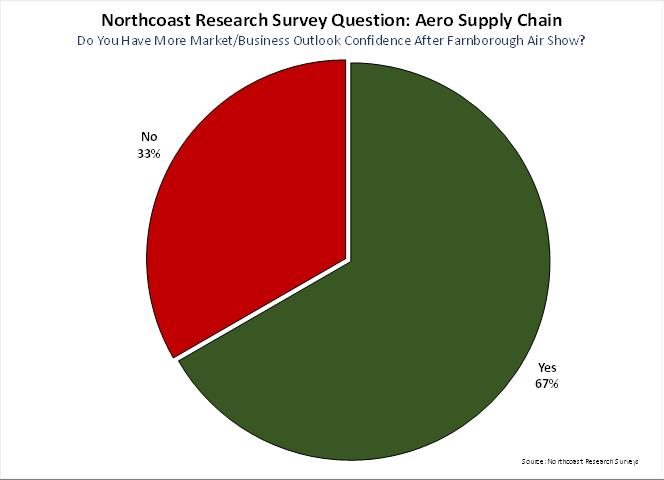

Insights on Commercial Aerospace Trends Set the Tone for 2024 TITANIUM USA Event

By Michael C. Gabriele

The global commercial aerospace industry’s continuing recovery from the recent Covid pandemic set the tone for the International Titanium Association’s (ITA) 2024 Conference and Exhibition held Oct. 6-9 in Austin, TX. Presentations by executives, engineers, researchers and manufacturers, appearing from various corners of the world, followed suit and seemed to share that assessment. While concerns still remain, especially due to disruptive conflicts in the Middle East and the war in Ukraine, along with questions about the global supply chain, the overriding message was that business conditions are improving and reflect a cautiously optimistic near-term future.

Over 700 conference attendees were eager to hear presentations by the giant commercial aerospace OEMs, Boeing and Airbus. Jeff

Carpenter, senior director, supply chain contracts and operations, Boeing Commercial Airplanes, addressing the ITA conference in his Commercial Market Outlook via video, began his presentation on an upbeat note. “For those of you in the titanium world, I’ll remind everybody that the 787 is still operating normally and is still our major consumer of titanium.” News sources estimate that titanium accounts for about 14 percent of the 787 airframe.

Carpenter assured the attendees that commercial aerospace has moved past the disruptions caused by the recent pandemic. “All the fundamentals for selling planes

are still in place. Demand for travel remains high. There’s a steady long-term forecast driven by fundamentals.” As a result, airlines will need 43,975 new airplanes over the next 20 years, with the growth driven by single-aisle jets (33,380 units) and wide-body jets (8,065 units), according to Carpenter. Major regions for growth will be Asia/ Pacific, China, North America and Eurasia. Global fleet will double, with nearly half of deliveries for replacements; old aircraft and new markets. Global air cargo traffic continued a strong recovery in 2024.

Carpenter did note that the global fleet for commercial jets has seen constrained capacity by Boeing and Airbus, delaying retirements of aging fleets. “It’s not a demand problem; it’s a capacity problem, but the industry supply chain getting up to rate. Average fleet age is rising. We’re flying older

‘Our scrap utilization for melt operations has increased dramatically, especially due to sponge pricing and availability. Sponge is tight, but more producers are coming online. We need your help. We’re going to see you soon. If you’re a machine shop or a forger, we’re going to be buying back our titanium scrap and we’re going to be enforcing that. We expect our scrap back.’

—Jeff Carpenter, Boeing Commercial Airplanes

airplanes longer. But our planes are safe. Markets are resilient and the industry is recovering (from Covid). Long-term growth looks promising.”

Regarding Boeing’s ongoing “titanium industry investigation,” Carpenter said that “we have identified suspect documentation, learned about sources, identified material properties and replaced parts in our factory. We will identify process improvements and develop training material. We ask industry support of enhanced certification of conformity, including adding spec requirement to address any gaps.” He added that this effort seeks to achieve a more robust certification system and called on the titanium industry for cooperation. “This can’t be just OEM driven.”

Participant forecast data indicates that inventory burndown for titanium will continue through 2027, according to Carpenter. “Boeing suspended purchasing titanium from Russia in 2022, with a conservative burndown to mitigate risk. Boeing’s product mix has evolved. When we were buying a lot of our forgings out of Russia, they (Russia) in-sourced their billet and ingots for their forgings. We now have to supply all that ingot and billet to more forgers. (Boeing) is shifting to more intermediate titanium products (like slab) to give us more flexibility in the supply chain, which will reduce our lead times.”

Carpenter reaffirmed the importance of titanium scrap for Boeing’s manufacturing operations, noting agreements and commitments with mills and melters. “Our scrap utilization for melt operations has increased dramatically, especially due to sponge pricing and availability. Sponge is tight, but more producers are coming online. We need your help. We’re going to see you soon. If you’re a machine shop or a forger, we’re going to be buying back our

titanium scrap and we’re going to be enforcing that. We expect our scrap back.”

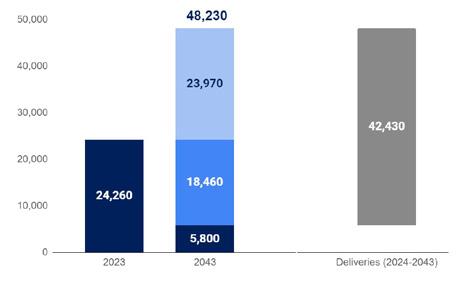

Olivier Maillard, Airbus vice president of metallic material

procurement, offered a forecast for the European aerospace giant. He showed a bar chart predicting that there would be a demand for 42,430 new aircraft between 2024 and 2043. Demand

opening new markets from 2024

He said the commercial aerospace market has recovered faster than expected (since Covid-19), “with a strong focus on Airbus’ single-aisle family, and an increasingly one over the past two years on the wide-body market. The continued steady rampup on all Airbus’ programs is calling on the titanium industry to prepare and anticipate demand in 2026 and beyond.”

This year (2024) has shown a strong ramp-up cumulated with a stock buildup effect, according to Maillard. “Beyond the A320 and A220 ramp-up, demand for widebody aircraft is now back on track. Airbus is committed on sharing long term visibility. The aerospace market (single-aisle and wide-body) has now

recovered from Covid, boosted by passenger demand and by the need of fuel and cost-efficient, new-generation aircraft.” However, he noted that the

current the geopolitical situation, with conflicts in the Middle East and Eastern Europe, remains a concern.

“Airbus leadership and strong order backlog is calling for a robust production ramp-up to the highest rates in the aerospace history until 2030 and beyond. The Airbus titanium demand has recovered 2019 volumes in 2024 and, despite adjustments in 2025, is set for further growth according to our target rates. In a world of uncertainties and geopolitical crisis, this robust demand is an opportunity. Anticipation and resilience versus demand bullwhip will be a key for catching this opportunity. Turning raw material and energy inflation risks into investment opportunities in circularity approaches and sustainable energy sources remain a priority.”

During his presentation, he displayed slides of the Airbus A321XLR single-aisle “Xtra longrange route opener.”

Commercial Aerospace—Other Points of View

There were many other presentations that focused on business conditions in the commercial aerospace sector. Stephen Fox of Titanium Metals Corp. (TIMET)/

Single aisle economics, up to 4,700 nm range

Low risk route opener

Profitable partnership with the A330neo

DUOPOLY PERFORMANCE 2024

continued improvement needed.” He added that the rate at which Boeing can improve operational performance is uncertain.

Fox summarized by saying deliveries, sustaining rates of orders, and strong backlog all indicate that the long-term projections for commercial aviation are being realized. Key commercial aerospace metrics such as revenue passenger kilometers (RPKs) and available seat kilometers (ASKs) and the macro picture all point to good airline health, although operational challenges remain.

well above pre-pandemic levels.

Nearly 10* years of narrowbody demand and 9* years of widebody.

PCC Metals Group examined “Global Demand Trends for Aerospace Structures.” Fox said that in 2023 deliveries improved as supply chain pressures eased: 1,263 total deliveries, up 10 percent, year over year.

He said deliveries as of August 31, 2024 showed 705 jets (down 9 percent), with Airbus at 447deliveries (up 3 percent) and Boeing at 258 deliveries (down 25 percent).

Despite challenges, the outlook for an aggressive production improvement is still expected. “Orders have slowed, year to date. Demand remains ahead of supply. Key programs are sold out through the end of the decade. Production and deliveries will be paced by the supply chain, anticipating Boeing’s operational improvement.”

However, Fox said there are headwinds on the horizon. “The supply chain will remain a constraint to build rates in the medium term. Airframes are beholden to single points of failure. Labor productivity remains a key bottleneck. The steep slope of planned production means that

“Underlying titanium demand is growing strongly. As suppliers, we all have to step up to meet that demand. Investments in capacity, especially in the United States, are moving ahead at pace. Quality hit the headlines in 2024. It must be addressed at every level.”

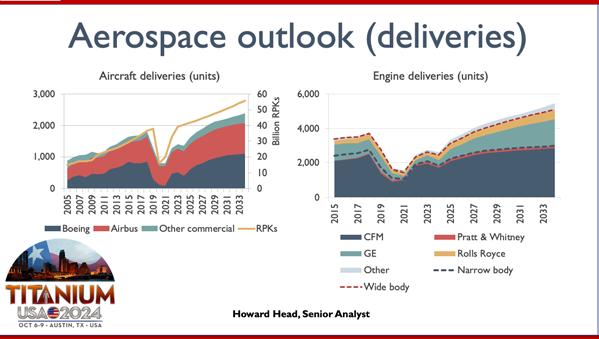

Marty Pike, president of ATI Specialty Materials, incoming President of the ITA board of directors, spoke about “Commercial AeroEngine Trends and Demands.” Pike said that aerospace industry demand is breaking historic

Engine growth continuing ramp

Aircraft backlog increasing TER

• 2024 backlog at all-time record

• Represents ~10 years of work in hand

• 15,668 aircraft on backlog (Airbus 55%, Boeing 39%)

High near - term growth

• WB platforms growing 18% faster than NB through 2026

• LEAP/GTF grow 53% 2024 -2026

• GE9X and GEnX drive WB growth

Delayed fleet retirements increasing MRO

Narrowbody Engine MRO Demand

CFM56 and V2500 driving primary MRO activity through 2033

LEAP and GTF initiating MRO cycle with first wave of scheduled activity in 2024/2025

Widebody Engine MRO Demand

GE90 and CF6 provide steady ongoing spares

Spares are at significantly higher volumes than historic estimates Sources: ATI Internal, Aviation Week

TRENT and GEnX activities expected to double over next decade

TITANIUM USA 2024 – Executive Summary

Supply chain constraints leading to diversification

Stability & Availability ISSUE IMPACT

Supply chain cannot keep up with record high demand

Growing pains with current generation engines

Increasing MRO activity to maintain legacy engines

Eliminating single points of failure in customer supply chains

Derisking supply chains through diversification and localization

supply: Premium Quality (PQ) titanium bar, billet

High inflation, sponge challenges increasing costs

Pressures

Global inflation projected to be 5.9%, a 1% drop from last year

Labor shortages and supply chain issues adding to increased costs

U.S. titanium industry is no longer vertically integrated back to sponge

Inflation resulting in increased pressure for cost pass -throughs

Higher costs leading to capital expenditure headwinds for suppliers

Upstream material capacity investments increasingly require government funding

records, with net profits at $30.5 billion (the highest since 2017); year-over-year revenues (more than 9.7 percent) that are rising faster than expenses (more than 9.4 percent; and with air travel expected to double by 2043 (3.8 percent compound annual growth rate—CAGR).

He also pointed out the continued ramping up of jet engine growth.

He then shared information on supply chain constraints, sponge challenges that are increasing costs, and geopolitical risks affecting titanium availability. Pike said titanium demand will grow as commercial aerospace fleets expand, citing titanium “demand drivers” such as the expansion of engine fleets, surging engine MRO (maintenance, repair and overhaul), and opportunities from future engine designs.

Global conflicts: Ukraine & Israel Wars Replacing VSMPO capacity with an already constrained supply chain

Ongoing sponge uncertainty has become a reality

Global competitiveness drives OEMs to use lowest cost, globally sourced raw material inputs

Industry utilization of Chinese sponge requires significant time and risk for engine qualification

subjected to alternating loads, leading to a phenomenon called fatigue and fatigue failure,” he stated. “This is a progressive deformation of a material or structure under repeated stress levels, much lower than the stress required to cause failure in a single application. During this process, small cracks initiate and grow, potentially leading to failure. Fatigue crack growth (FCG) examines the entire process from crack initiation to crack propagation and eventual failure due to cyclic loading.”

He said this process is divided into three main stages: Crack Initiation—Cracks typically start at notches or surface discontinuities. The crack propagation rate is very

Element in Aerospace

Materials and Product Qualification Testing

Frank Nguyen of London-based Element (www.element. com) discussed “Fatigue Crack Growth” for aerospace systems. Element is involved in testing, inspection and certification services to a diverse range of industry sectors.

Nguyen began with a slide that illustrated various points for aerospace metallic testing, which includes mechanical fatigue, tensile, stress rupture and creep, thermal-mechanical fatigue testing and fracture toughness.

“All engineered components and structures are

Aerospace Metallic Testing

Metallurgical Testing

• Casting Evaluations •

Defense spend in U.S. and

low during this stage, and continuing until the crack becomes large enough to move to the next stage; Crack Propagation—the crack grows in a direction perpendicular to the applied stress, with a higher propagation rate and can be divided into three regions (threshold, Paris and Final

Fracture); and Ultimate Failure— this stage occurs when the fatigue crack becomes long enough that the remaining cross-sectional area can no longer support the applied load, leading to failure.

Sam Stiller, vice president, commercial, Howmet Engineered

Structures, a division of Howmet Aerospace Inc. examined “Titanium Demand Trends in Defense Aero structures.” Stiller said military expenditures grew for the ninth consecutive year, reaching $2.44 trillion in 2023.

He said that current political headlines mask broader bipartisan consensus on defense industrial base issues. Bipartisan House and Senate majorities support strong defense budgets as well as supplemental spending requests Candidates are united on strengthening U.S. deterrence with a focus on China as the pacing challenge.

As for the United States’ industrial base, he said policies in Washington are focused on on-shoring, reshoring, and near-shoring, with continued funding for investment in domestic supply chains and the use of export controls to restrict adversaries’ access to sensitive technologies. Regarding defense aerospace modernization, he said the Biden and Trump administrations have focused on near-peer competitors, with a focus on research and development priorities including the F-35 and B-21, hypersonic, loyal wingman and sixthgeneration fighter concepts.

“The evolving global, sixthgeneration fighter picture could bode well for titanium aero structures, as stealth, light-weighting and higher temperature engines all play to titanium’s strengths. The U.S.

Titanium Stainless steel Polymers

ACNIS

GROUP SETS UP A NEW SUBSIDIARY IN CHICAGO

Established in France (Lyon), the stockist Acnis Group is one of the world leaders in the distribution of metal alloys especially in TITANIUM, in all forms : sheets, bars, tubes and powder for 3D printing.

ISO 13485 certified since 15 years, the family business has specialized in the medical field since its creation in 1991, to meet the demand of orthopedic manufacturers and dental implants, as well as surgical instruments.

ACNIS Group acts as a buffer between producers and users, thanks to its 600 to 700 tons rotating stock and 1,300 references of different origins. Our unique cut-to-size service center (15 machines: waterjet, high-definition waterjet, plate sawing, bar sawing, shearing, machining, chamfering) allows us to reduce your costs by optimizing scrap rates.

As a result, the company is able to deliver very quickly its customers, in barely a week, no matter the ordered quantity. Major implant manufacturers among the main American and European OEMs themselves call on ACNIS Group to source their metal alloys.

The last creation of ACNIS USA stock in 2023 in Chicago has changed the game. Acnis Group is now the only distributor that can stock and deliver any quantity in North America (ACNIS TITANIUM & ALLOYS USA-Chicago), South America (ACNIS DO BRAZIL-Sao Paulo), Europe (ACNIS FRANCE-Lyon), South Asia (ACNIS CHINAShanghai) for global worldwide contracts.

Acnis is your one-stop shop for all TITANIUM grades, stainless steel (316L, 420B, cobalt chrome, 17/4 PH, high nitrogen alloy, Custom 455, Custom 465…) and polymers

Our dental subsidiary BCS, a European leading distributor of CAD CAM products for additive manufacturing, is registered with the FDA for titanium powder & discs, and cobalt chromium powder.

defense market trends play to the strength of titanium aerostructures, which drives innovation.”

According to a July 2024 online article in Defense News (https://www.defensenews.com/air/2024/07/19/ how-the-sixth-generation-fighter-jet-will-upendair-warfare/), the next generation of fighter aircraft could feature a revolutionary new type of engine. “The aviation world has seen five generations of fighters, ranging from the subsonic F-86 Sabre after World War II to the current, stealthy F-35 Joint Strike Fighter,” the Defense News article stated. “Now, militaries around the world are working on jets they believe will represent technological leaps significant enough to qualify as sixth-generation aircraft.” The Air Force’s effort to build a sixth-generation fighter family of systems is known as “Next Generation Air Dominance” or NGAD.

Peter Zimm, principal with management consulting firm Charles Edwards, presented an “Aerospace Raw Material Outlook.” He began by outlining total aircraft production, valued at $150 billion in 2023, an 11-percent increase. Total maintenance, repair, and overhaul (MRO) value was $226 billion in 2023, a 7.1-percent increase. MAX production slowed when Boeing began reworking their production and quality systems, now halted due to the ongoing strike of 33,000 factory workers. (Several online news reports indicated that, as of early October, negotiations between Boeing management and factory workers remained deadlocked.)

Zimm also said that Airbus pushed their 75-month production goal for the A320neo family out to 2027, “but the rate of production increases needs to increase even more. We want to get back to where we were, which seems to be defined as getting back to prepandemic build rates.”

In order for (aerospace) OEMs to achieve desired build rates, sub-tier suppliers need incentives to invest in capacity.

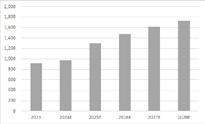

Zimm forecasted that aircraft production value is expected to increase at 6.1 percent CAGR over the next five years, expected to reach over $200 billion by 2028. He also pointed out that MRO value is expected to grow at 3 percent CAGR from $226 billion in 2023 to $262 billion in 2028.

“Aerospace raw material demand is expected to increase at 5.9 percent CAGR from 1.36 billion pounds in 2023 to 1.82 billion pounds in 2028.” He said long lead times for mill products will persist across all materials, including titanium, composites, nickel, steel and aluminum. Aircraft production mix (narrow-

body versus wide-body) will continue to be highly variable.

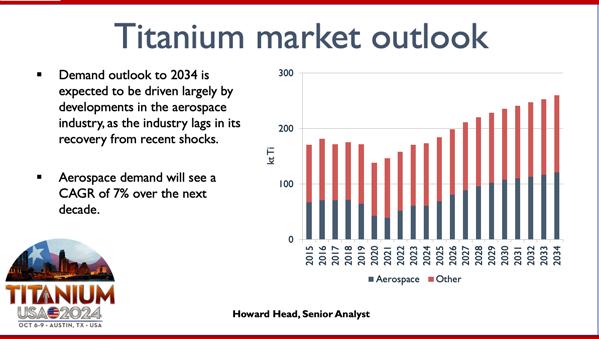

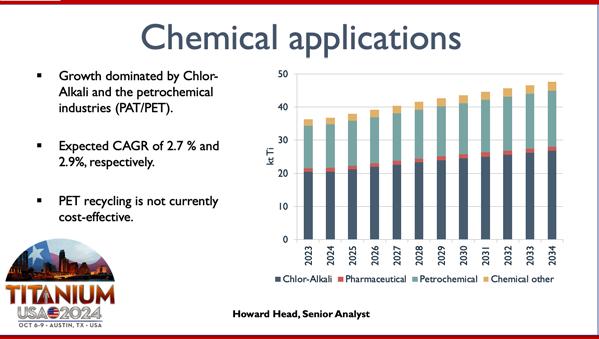

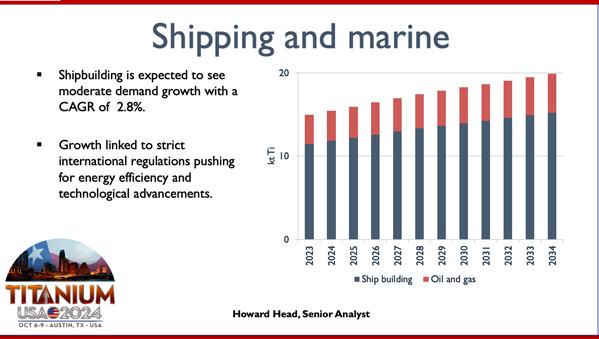

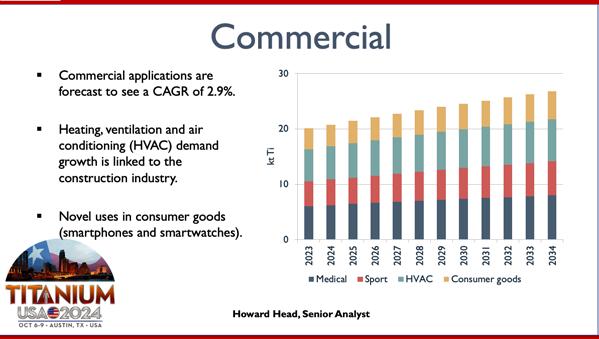

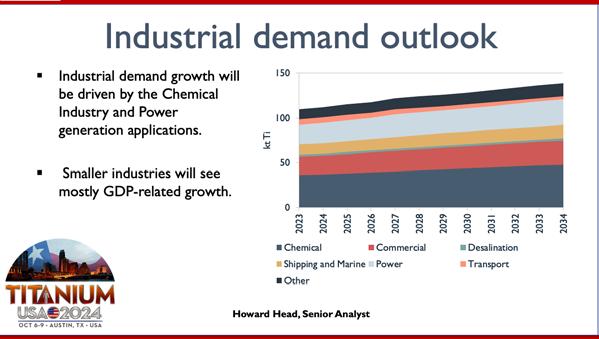

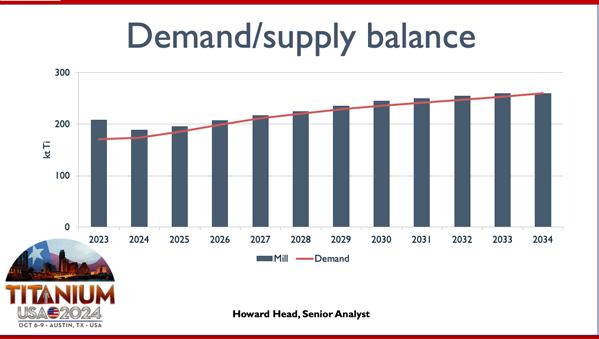

Howard Head, Project Blue, London, presented a titanium market outlook, focusing on a demand forecast for industrial applications. He began with a bar chart market outlook for demand through the year 2034, largely driven by developments in the aerospace industry.

Head presented a bar chart that illustrated the titanium market outlook through the year 2034. He moved to an outlook for commercial aerospace. He then displayed bar charts that projected the outlook for chemical applications, power generation, shipping and marine, commercial and industrial demand. Another slide charted the demand/supply balance for titanium through the year 2034.

Absorbing Observations on Titanium Sponge

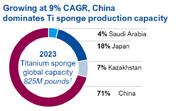

John Porter of CCMA shared his thought on “Titanium Sponge: The Advancement of China.” Porter said China accounts for roughly 50 percent of global titanium sponge production and continues to expand capacity rapidly. “Greenfield projects account for a vast majority of newly added capacity and output. New facilities possess state-of-the-art equipment and control systems suitable for the production of aerospace-quality titanium sponge.”

China is now a net exporter of sponge, he pointed out. “Large capacity expansions and a softening of domestic demand have resulted in China becoming a significant net exporter of sponge for the first time in 10 years. In 2023, China’s net exports totaled more than 6,700 metric tons (14.9 million pounds); 2024 has resulted in year-to-date net exports through July of 5,000 metric tons (11 million pounds), setting an annualized pace of nearly 9,000 metric tons (19.8 million pounds).”

Meanwhile, sponge prices in the United States are on the rise. “The import window is open for Chinese sponge to the United States.” He listed a number of sourcing decisions that drive titanium sponge: quality; chemistry; hazard identification and control; fixed practice agreements; continuous improvement mindset; cost; on-time delivery and clean documentation.

Based in Gertzville, NY, CCMA’s primary business is the marketing and distribution of alloying metals and ores to the iron, steel, ferro-alloys and aluminum industries.

David McCoy, executive chairman of ZTMI, reviewed “Minerals that Feed the Global Titanium

Where are the sponge plants?

for 2024 is 9.02 million TiO2 units, bringing the latest yearon-year demand growth to 11.2 percent. Global titanium feedstock demand is projected to increase 1.7 percent CAGR during the next four years to reach 9.66 million TiO2 units in 2028.

He attributed the rise in demand to the titanium enduse, which remains robust, with the bulk of the growth driven by sponge output expansion in China. “Overall consumption in the other end-use (mainly welding) is expected to be flat in 2024, with moderate growth in East Asia excluding China, offset by declines in other regions due to lower industrial and construction activities.”

Industry.” He began by introducing TZMI as an independent consulting company, operating since 1994, that works with a wide range of global clients to provide insight and expert advice on opaque mineral, metal and chemical sectors. The company has grown over the years by adding business units operating in Shanghai, China (TZMI Management Consulting (Shanghai) Co., Ltd) and Houston, USA (TZMI, Inc.) as well as taking full ownership of Allied Mineral Laboratories Pty Ltd (AML) based in Perth, Western Australia.

He provided two maps: one that showed world titanium resources (dominated by China, Australia, India and Brazil); and a second map that showed titanium sponge plants throughout the world.

McCoy pointed out that demand for titanium minerals expanded significantly in 2024. “TZMI’s demand estimate

A bar chart illustrated titanium sponge production by region.

McCoy posed the question: “Is Chinese sponge production real?” His answer: “Yes. The newest plants are world scale and high quality. Sponge from China is starting to feed melters outside of China, and this is expected to continue. TZMI expects some rationalization of older, low-quality plants in the next couple of years. Cumulative oversupply of Chinese sponge (would be) more than 100,000 metric tons in 2024-2026 if rationalization of older capacity doesn’t happen.”

According to McCoy, TZMI’s latest estimate of Chinese titanium sponge production in 2024 is 257,700 tonnes, an increase of 22 percent from 2023, bringing global titanium sponge output to 393,400 tonnes for 2024. “This translates to a titanium feedstock demand of just under 800,000 TiO2 units for 2024, up another 17.7 percent year-on-year. The outlook remains largely unchanged, with TZMI projecting demand for this end-use to reach 876,000 TiO2 units by 2028, a 5.3-percent increase (CAGR) from 2023.”

“The minerals (feedstocks) used to make chloride TiO2 pigment and titanium sponge are the same,” he continued. “The impact of tariffs on Chinese TiO2 pigment will push supply to Western producers, predominately chloride producers in the near term. This will increase demand for chloride feedstocks that are also required by sponge producers. Sponge cash margins are not large. Feedstock

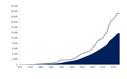

Yasuji Yamao, chairman of The Japan Titanium Society, and president and representative director of Toho Titanium Co. Ltd., addressed the “Outlook on Current Titanium Trends in Japan.” He presented a bar chart that outlined trends in Japan’s titanium sponge shipments, saying that they’ve fluctuated with aerospace demands in the past. “Sponge demands surged after 2021 due to the recovery of the aerospace industry and the alternative demands. Sponge shipments in 2023 were close to the record high reached in 2019.”

‘Japanese sponge manufacturers strive to meet the increasing demands in the aerospace industry and hope to grow and develop together with the industry. Sponge prices have finally started to rise since last year with the understanding of customers, in response to rising costs. In order to meet the current sponge demands, two Japanese sponge manufacturers plan to make capacity increases. It is essential to maintain a reproducible price level for the stable production of titanium sponge, and we need the support of the entire supply chain related to titanium sponge.’

—Yasuji Yamao, Japan Titanium Society

Pie charts and bar charts from Yamao illustrated trends in Japan’s titanium sponge shipments. He said most of sponge exported to the United States was for aerospace applications. Shipments to United States recovered sharply in 2022 and surpassed the 2019 level in 2023.

Another bar chart tracked trends in for Japan’s titanium mill product shipments. He said mill shipments dropped from 2019 to 2021, but began the road to recover in 2022, along with the recovery of economic activity from the pandemic.

1 Trends in Japan Titanium Sponge Shipments

1 Trends in Japan Titanium Sponge Shipments

1 Trends in Japan Titanium Sponge Shipments

3 Trends in Japan Titanium Mill Products Shipments

“As a titanium sponge supplier, Japanese sponge manufacturers strive to meet the increasing demands in the aerospace industry and hope to grow and develop together with the industry,” Yasuji Yamao said. “Currently, sponge prices have finally started to rise since last year with the understanding of customers, in response to rising costs. In order to meet the current sponge demands, two Japanese sponge manufacturers plan to make capacity increases. It is essential to maintain a reproducible price level for the stable production of titanium sponge, and we need the support of the entire supply chain related to titanium sponge.”

Safe Hydride Storage

Anna Poberezhna, the cofounder ClearHub/Underslab, discussed the “Selection and CostEffective Manufacturing of Ti Alloy Hydride Storage Devices, Enabling Mass Adoption of the Safest Hydrogen Storage Method.” She posed the question: are titanium alloys the future of “Green” energy applications?” She then listed Department of Energy requirements: High hydrogen capacity; rate of absorption and release of H2; mechanical stability during charge/ discharge cycles, accompanied by cyclic compression and expansion of the crystal matrix; availability and industrial production costs; operating temperature; scalability; and customization.

Poberezhna then asked: “Is intermetallic the holy grail of H2 storage tech?” She offered a slide that compared storage method, advantages and disadvantages, cchoosing the optimal with a costeffective and reliable technology for mass-scale H2 storage.

She said alloyed sponge can eliminate several production steps, resulting in material cost savings

across all titanium applications. “Titanium alloy sponge brings cost effectiveness to H2 metal hydride storage and wider applications.” Titanium powder, pros: time and resource-efficient technology; considerations: operate with hydrogen, control alloying element distribution. Titanium melted products: pros: highly promising, multiple applications, low cost. Cons: number of sponge operating facilities. Emissions reduction: shortening of the production cycle and increase in the metal utilization rate.

Notes on Nitinol

Peter Koslowski, director of commercial at Metalwerks Inc., discussed “Beta-Titanium and NiTinol: Properties, Applications, and Production.” He reviewed the properties, applications and production of beta-titanium alloys and Nitinol in the medical device industry. “Why did titanium break up with iron? Because it found something stronger, thinner, more attractive and less rusty!”

“Let’s talk about how betatitanium alloys are applied in the medical field. Orthopedic implants are one of the most common uses of beta-titanium alloys. Their high strength and low elastic modulus make them ideal for hip, knee, and spinal implants. These implants must withstand repeated mechanical loads while closely mimicking the behavior of human bone. Beta alloys reduce stress shielding, allowing bones to heal and bear the appropriate load.”

“In dental implants, beta alloys are highly valued for their biocompatibility and durability,” he continued. “Dental implants need to last for many years inside the body without causing adverse reactions, and the corrosion resistance of beta alloys ensures they maintain their integrity over time.”

“For fracture fixation devices, such as bone plates, screws, and nails, betatitanium alloys offer a perfect balance of strength and flexibility. These devices need to be strong enough to stabilize bones while being flexible enough to avoid causing further damage to the surrounding tissue.”

Kozlowski explained that beta alloys are produced through several different melting paths. Vacuum Arc Remelting (VAR) can be used for either primary or final melting operations. For primary melting operations, the VAR utilizes either compacts of titanium sponge and alloying elements or other primary melts produced by either hearth melting or induction skull melting (ISM). In either case, the raw materials are welded into an electrode and arc melted inside a water-cooled copper crucible. After primary melting, the resultant ingot is melted one additional time to ensure chemical homogeneity and uniform microstructure.

“More specialized furnaces such as plasma arc or electron beam hearth melting (E-Beam) furnaces can also be employed. In either furnace, titanium sponge and alloying elements are pressed into briquettes and fed into a water-cooled copper hearth. The electron beam or plasma arc melts the material in the primary hearth and the metal then flows or is cast into a withdrawable crucible. The flowing nature of hearth melting restricts the movement of unmelted alloy elements into the resultant ingot. This is critical when refractory elements are large portions of the alloying content.”

ISM requires no compacting of raw material or welding of electrodes for melting. Rather, the raw materials are loaded directly into a water-cooled copper crucible for melting. An induction field couples to the metal to produce heat and an electromagnetic

field which melts the metal and stirs the bath. This ensures homogenous alloy content and minimizes the risk for elemental segregation.

“There are unique challenges with melting and processing of beta alloys,” he said. “One critical issue is the occurrence of high-density inclusions (HDIs), which are pieces of unmelted refractory metals like tungsten, niobium or molybdenum. The melting points make them difficult to dissolve fully during the melting process. These elements can accumulate in the alloy, leading to localized regions with significantly different properties, compromising fatigue resistance and overall material integrity.”

Nitinol is an alloy of 50 percent nickel and 50 percent titanium that has revolutionized the medical industry due to two unique properties: shape memory and super elasticity. “The shape memory effect allows the metal to ‘remember’ and return to a pre-set shape when heated above a specific transformation temperature. This behavior occurs due to a reversible phase transformation between the alloy’s martensite (low temperature) and austenite (high temperature) phases. At lower temperatures, Nitinol can be easily deformed in its martensitic phase. When heated, it reverts to its stronger austenitic phase and recovers its original shape without permanent deformation”.

Artificial Intelligence

In addition, he said Nitinol displays super elasticity, unlike conventional materials like 316 stainless steel, which can only elastically deform up to about 0.5-percent strain before yielding. Nitinol can endure strains as high as 8 percent without permanent deformation.

Kozlowski concluded by saying the use of beta alloy and Nitinol alloys in medical applications presents significant advantages due to their unique material properties. Beta alloys offer a combination of low elastic modulus, high strength, fatigue resistance, and biocompatibility.

“Nitinol, with its remarkable shape memory and super elasticity, has revolutionized minimally invasive surgical techniques with devices such as stents, guidewires, and orthodontic wires. Its ability to undergo large elastic deformations and recover its original shape is invaluable in medical scenarios requiring flexibility, precision, and durability. However, processing challenges such as controlling inclusions content and the nickel-to-titanium ratio remain significant hurdles in manufacturing these advanced materials. Next-generation Nitinol utilizes high purity raw materials and optimized melting practices to deliver the highest possible fatigue properties for ultracritical applications.”

Dr. Jeremy Frank, the CEO and co-founder of KCF Technologies, gave a presentation on “Leveraging AI and Analytical Efficiency for Predictive Maintenance.” Frank showed a graphic depicting three arrows identifying manufacturing challenges: worker and supply shortages; competition and sustainability; and technology and transformation. His next slide was a pie chart titled “the problems we solve.”

Frank said KCF proprietary sensors monitor industrial machines 24/7. “AI and machine learning (ML) diagnose malfunctions, provide alerts, and issue remediation recommendations. From shop floor to C-Suite, (there’s) full visibility of facility improvement opportunities as well as enterprise views. Our ML platform sees data from 100,000-plus assets at a rate of over 1.2 billion data sets per month. (We) leverage input from the largest body of CAT II plus analysts to identify and develop optimal features for classification. (We) leverage the data pipeline to achieve weekly model improvement. Workflows (are) built into software to validate issue remediation, yielding insight into model performance and value.”

The Problem We Solve

The Right Data

Aerospace Vacuum Heat Treating Services

Advantages

•

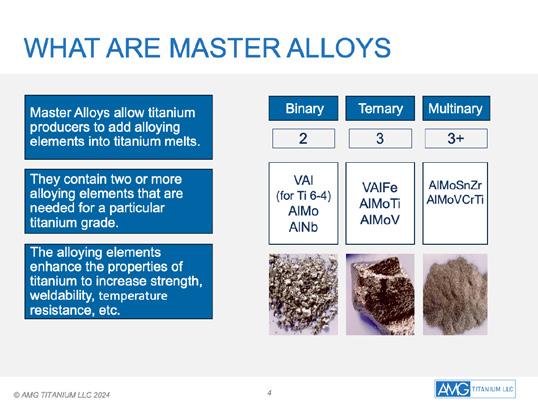

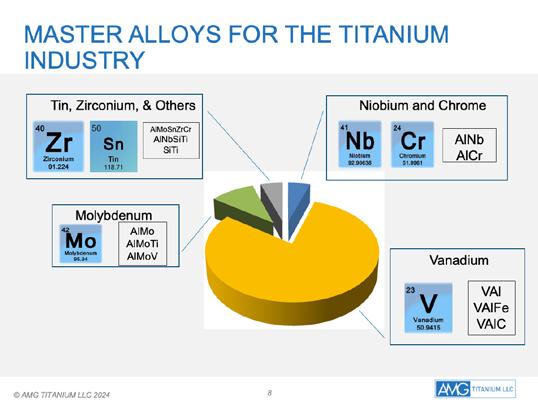

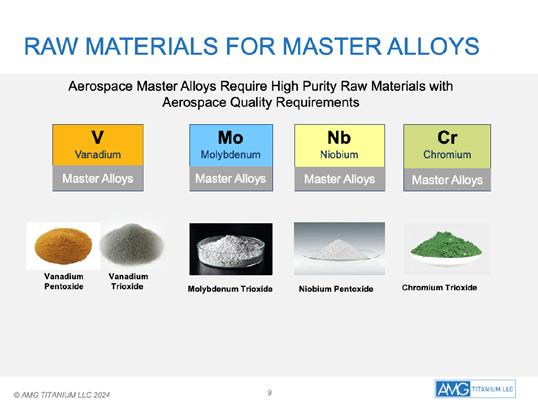

Master Class on Master Alloys

Paul Godown, Vice President, Sales and Marketing for AMG

TITANIUM LLC defined the value of master alloys for the titanium industry. Master Alloys allow titanium producers to add alloying elements into titanium melts. They contain two or more alloying elements that are needed for a particular titanium grade. The alloying elements enhance the properties of titanium to increase

strength, weldability, temperature and resistance.

Master alloys are highly engineered products necessary to the titanium industry. Master alloy raw materials are sourced globally. Current supply chain issues also affect master alloy producers. The geopolitical environment has added an additional element of risk to the industry. Single sourcing and long qualification processes have left titanium producers and end users vulnerable. Increased titanium melting capacity in the United States will require continued close communication and coordination between melters and master alloy suppliers.

“We oversee the complete technological process chain for elastic mesh implants. Starting with the development of titanium microwires designed specifically for medical use and thinner than human hair, we manufacture medical textiles optimized for their intended use in soft tissue repair. Building upon our technology, we are committed to becoming the leading company for the development and manufacture of metal-based surgical mesh implants.”

A New Type of Furnace

Harald Korbel, INTECO Melting and Casting Technologies GmbH, provided an update on the “First Operating Results of a New Type of Vacuum Arc, Cold Hearth, Skull Melting Furnace and Casting Process.”

Talking About Titanium Textiles

Dr. Florian Ehlers, CEO of Titanium Textiles AG, Rostock-Bentwisch, Germany, discussed titanium textiles, wired innovation; the next-generation surgical implants.” Ehlers said Titanium Textiles is developing and manufacturing elastic mesh implants made of pure titanium “microwire” for medical applications. “Defects in human soft tissue usually need to be repaired with a permanent mesh implant. Polypropylene meshes as current standard of care are subject to complications which may cause pain and functional impairment. There is widespread consensus that an optimal mesh implant has not yet been developed, and that a material with improved biostability is required for the repair of soft tissue. Metal-based mesh implants are increasingly the focus of scientific attention

Korbel reported that “hot commissioning has been successfully finished in the fourth quarter of 2023 and the furnace is already in full commercial production. More than 50 heats were performed during the hot commissioning, using both the round skull melting and oval-shaped cold hearth skull melting crucible. Commercially pure (CP) grades, Grade 5 (Ti-6Al-4V) and the Zr grade has been melted and cast.”

In addition, he said new findings with regard to energy consumption, melt and scrap feed ratio, process parameters (V; kA) in relation to melt rate kg/min were made. “The influence of the magnetic stirring mode in the oval cold hearth crucible on the liquid metal was tested by variation of field strength, stirring interval times and stirring direction.”

The main focus of the process is for recycling titanium scrap: effective dissolution of hard alpha phases (low density inclusions [LDI], e.g. titanium nitride) and foreign particles (high density inclusions [HDI], e.g. tungsten, molybdenum). LDI inclusions below a certain size are dissolved by multiple VAR melting steps. HDI inclusions are hardly being dissolved during the VAR process.

Measures to improve dissolution of LDI’s and HDI’s in the new “VACHSM” process include longer dwell times and multi-melting cycles for a “risk particle” in the liquid phase compared to a standard VAR, SM, EB or PAM process. There is a controlled hot spot and pool depth by x-axis oscillation of the oval shape cold hearth. Controlled magnetic stirring of the melt pool uses a floating mechanism towards the rim zone of the cold hearth skull, along with gravity segregation trap mechanism during the

melting and casting process.

Korbel summarized by saying the new INTECO Vacuum Arc Cold Hearth Skull melting and casting furnace has been developed to meet the titanium industry’s demand for increasing scrap usage in producing high quality products, thus reducing the carbon footprint.

“This technology has been developed as a cost efficient and energy saving process compared to EB and plasma arc melting (PAM) cold hearth process targeting a high material quality level,” he said. “A specially designed oval-shaped cold hearth skull crucible and scrap feeding system is the tool to enable the feeding of scrap and other raw materials between the melting and casting cycles. Two casting techniques are combined in one plant, allowing the highest product flexibility and process integration. A highly efficient stirring coil increases the homogenization by dwell time of the material in the turbulent liquid phase for improved dissolving of LDIs and HDIs and by arc dwell space control.”

Safety Factors for Additive Manufacturing

Dr. Roger Lumley, senior technical specialist, AWBell Pty Ltd, Dandenong South, Australia, discussed “Safety Factors for Design of Additive Manufactured Titanium.” Lumley began by noting the limitations to the standard AM process: storing and handling challenges; fire hazards; degradation and contamination of powder metal; density variations in complex geometries; quality of surface finish; and difficulties in scale up.

Lumley gave examples from the principles of AMS 2175, saying four classes need definition. “Class 1; a manufactured product, the single failure of which would endanger the

ASTM F3530, “Standard Guide for Additive Manufacturing”.-Design

a manufactured product not included in Class 1 or Class 2 and having a margin of safety greater than 200 percent.

lives of operating personnel or cause the loss of a missile, aircraft, vessel, or other vehicle. Class 2; a manufactured product, the single failure of which would result in a significant operational penalty. In the case of missiles, aircraft, vessels and other vehicles, this includes loss of major components, unintentional release or inability to release armament stores, or failure of weapon installation components. Class 3; a manufactured product not included in Class 1 or Class 2 and having a margin of safety of 200 percent or less. Class 4;

“The inherent variability of the AM process means that different manufacturing equipment, facilities or contracted services cannot be considered equally, which further strengthens the argument for the application of an “AM Factor” in design. For a design engineer, it may be suggested that a worthwhile activity when qualifying a supplier of titanium additive manufactured components would be to conduct a survey similar to the generation of data that has been presented. This is the same criteria as for aerospace castings. In context, if a guideline is provided that reduces risk, design engineers who are not experts in AM will use it.”

He concluded by saying that the major impediment to utilization of AM more widely is the absence of consensus on design guidelines, validation criteria and certification processes. “The ongoing risk to a normal design engineer is too great. Development of factors of safety that may be used in the design

Roger Lumley, Consideration

Surface Finish on AM Components

The surface finish of an AM Ti-6Al-4V alloy test piece.

Roger Lumley, Consideration of Safety Factors for Design of Additively Manufactured Titanium

process will significantly facilitate use and increase application of AM products. A method based around the determination of safety factors (an ‘AM Factor’) would provide meaningful design safety data. This may increase component weight in topological optimization, but will significantly increase utilization.”

Spotlighting

the “4” in Titanium 6-4

Vincent Rocco, vice president of sales and marketing for US Vanadium, talked about “In with

the New, Out with the Old.” He first noted that vanadium is used as an alloying agent to enhance titanium’s strength, hardness and heat resistance. “Vanadium brings the “4” to Ti64,” he said. “Titanium 6 percent aluminum and 4 percent vanadium represent about 50 to 60 percent of all titanium production. Vanadium is introduced into titanium melts via master alloy additions. Master alloy production uses high purity vanadium oxides. Most vanadium oxide is commodity grade used for steel production.”

will be needed to satisfy expected growth. Current supply of high purity presents elevated risks for consumers due to geopolitical and logistics concerns.”

Considering its importance to the titanium industry, he suggested that “titanium producers should diversify their vanadium supply to ensure their requirements are covered while minimizing the risk of supply disruptions.”

Tune in to Titanium Tube Trends

Rocco offered insights into the near-term dynamics of the global vanadium market. “The macro vanadium market is currently unsustainable and should eventually correct to a more sustainable level. China will continue to drive the vanadium market at a macro level. Global steel demand is expected to show minimal growth in the shorter term. Demand for high purity vanadium should be strong due to titanium, chemical, and vanadium redox flow battery (VRB) applications. Vanadium for VRB uses is showing signs of dramatic growth. New sources of high purity vanadium

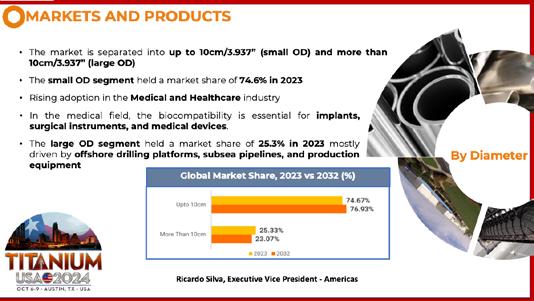

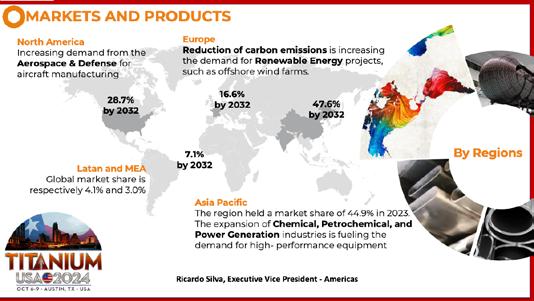

Ricardo Silva, executive vice president/Americas for Neotiss, reviewed “Global Industrial Application Trends for Titanium. Silva began with his own executive summary, stating that the titanium tubes (welded and seamless) market was valued at $2.85 billion in 2023 and is projected to grow at a CAGR of 6.9 percent throughout the forecasted period of (2024-2032). By 2032, the market is anticipated to witness a substantial increase, reaching $5.21 billion. Asia/Pacific held 44.9-percent share in the market in 2023 driven by expanding aerospace, automotive, and chemical industries. The aerospace segment held a 32.4-percent market share in 2023 and it is anticipated to grow at a CAGR of 7.6 percent due to popularity of titanium tubes for applications in hydraulic systems, landing gear, engine components, and aircraft structural parts.

Silva said the global titanium market was valued at $30.4 billion in 2023 and is expected to reach $57 billion by 2032, expanding at a CAGR of 6.5 percent during the forecast period.

SLIDES 9, 10, 11, 12, 13

Titanium tubes are increasingly used in the aerospace and defense industries due to their high strength-

to-weight ratio, corrosion resistance, and ability to withstand high temperatures. “The demand for lightweight and fuel-efficient aircraft is driving the market, with titanium tubes being used in various components such as hydraulic systems, fuel lines, and engine parts. For example, the Boeing 787 Dreamliner extensively uses titanium for its structural components, contributing to its efficiency and performance.”

“Biocompatibility of titanium makes it a popular choice for medical implants and surgical instruments. Titanium tubes are used in manufacturing medical devices such as bone screws, plates, and artificial joints. The rise in healthcare expenditure and advancements in medical technology are boosting the demand for titanium tubes

in the medical industry. For instance, titanium tubes are used in spinal implants and hip replacements due to their durability and compatibility with human tissue.”

He said the chemical processing industry is increasingly adopting titanium tubes due to their excellent corrosion resistance to harsh chemicals and acids. This trend is particularly notable in applications involving chlor-alkali, pulp and paper, and desalination processes, where the durability and longevity of titanium tubes are crucial.

“For instance, titanium tubes are used in heat exchangers and reaction vessels, where they effectively withstand harsh environments and extend equipment life. This trend reflects the growing reliance on titanium in industries requiring robust materials for chemical handling and processing.”

Silva identified automotive as a growth sector for titanium tubing. “There is a growing trend of using titanium tubes in the automotive industry, especially in high-performance vehicles. Its lightweight properties contribute to fuel efficiency and performance enhancement. Components such as exhaust systems and suspension parts are increasingly made with titanium. Companies such as Ferrari and Lamborghini are incorporating titanium components to enhance vehicle performance. With the rise of electric vehicles (EVs), the use of titanium tubes in EV batteries and lightweight

The project funded by Innovate UK

Epoch Wires is pleased to announce their involvement in an Innovate UK research project as part of the “NATEP helping SMEs innovate in aerospace - Autumn 2021” competition. The project entitled “NanoTi - Grain refinement of Ti-6Al-4V wire to enable Aerospace DED AM” is led by Epoch Wires and supported by TWI.

The project aims to design novel-alloy wire chemistry to minimise the grain growth in Ti6Al4V alloys deposited by Additive Manufacturing. In this work, Epoch Wires will produce new wires with a nanoparticle injection, forming equiaxed grains to enhance the mechanical properties of Ti6Al4V alloys. TWI will be depositing the wires using laser, plasma, and electron-beam additive manufacturing techniques. Epoch Wires will be utilising it’s proprietary technology of producing metal-cored wires using continuous laser-seam welding technology, designed for titanium alloys.

The NanoTi project has received funding from Innovate UK under grant agreement No. 10030392.

Nano Ti Wires

Innovative and cost-effective titanium wires for the aerospace industry

Laser-seam welded Ti6Al4V wire

Ti6Al4V material deposited using Nano Ti wires, with laser additive manufacturing technology (image courtesy of TWI)

Contact

Serdar Atamert (CEO) serdar.atamert@epochwires.com +44 (0) 7414 866801

Epochwires.com info@epochwires.com Unit 8, Burlington Park, Cambridge, CB22 6SA, UK

TITANIUM USA 2024 –

structures is anticipated to increase in the coming years.”

Tracking Titanium Scrap

Stacie Greenfield Stone, vice president, Goldman Titanium, Buffalo, NY, offered a “Titanium Scrap Outlook.” She said Goldman Titanium, established in 1958, is a privately held, world-class processor of titanium scrap, including

both solids and turnings. “Goldman Titanium purchases titanium scrap from suppliers throughout the world. Our company‘s products have been approved by major U.S., European, and Asian titanium melters.”

According to Stone, there are favorable business trends for titanium scrap, given a “healthy order book for new planes and strong outlook for aerospace.” However, she added that aerospace supply

chain and quality concerns could affect build rates. She also identified uncertain geopolitical issues that might affect the scrap market: global conflicts in Russia, Ukraine and Middle East; freight affected by Middle East conflicts and global trade balances; and evolving tariffs and trade policies.

She concluded her presentation with a bar chart that tracked the estimated supply and demand for Titanium 64 scrap through the year 2025.

Brian Morrison, vice president of 6KAdditive, share his thoughts on “Best Practices on Managing Revert for Maximum Value.” He said 6K Additive is the world’s only premium metal 3D powders from sustainably sourced feedstocks.

It’s possible to increase the value of scrap streams, shifting from a disposal cost to revert sales, according to Morrison. “The primary tasks are ensuring the correct mindset and procedures are in place. Safety, quality, and packaging are as important to revert streams as they are to new products. Environmental sustainability requires all of us to focus on waste generation and identifying a better outlet.

if the mindset and training aren’t in place

ManagementOperators & Maintenance Procurement / Sales FACT: All proceeding steps will be

• What is your revert “product”?

• In what configurations?

• What outlet options exist?

• Who owns revert sales?

• What metrics will be tracked?

• Is the team trained on by-product as a produced “product”?

• Are handling procedures defined?

• Are segregation protocols in place, error proofed, and enforced?

Morrison shared slides that spelled out his best practices and thoughts on the “mindset of the organization” when it comes to collecting and processing scrap.

“Know your revert customer,” he declared.

• Instructed to sell or pay for removal?

• Finding the highest bidder?

• Are we collaborating with buyers on suiting their needs?

Titanium Mill Products:

Sheet, Plate, Bar,Pipe,Tube,Fittings, Fasteners, Expanded Sheet & Ti Clad Copper or Steel.

Titanium Forgings and Billet:

Staged intermediate ingot & billet to deliver swift supply of high quality forgings in all forms and sizes including: rounds, shafts, bars, sleeves, rings, discs, custom shapes, and rectangular blocks.

Titanium, Zirconium, Tantalum & High-Alloy Fabrication & Field Repair Services: Vessels, Columns, Heat Exchangers, Piping, Anodes, Custom Fabrications, Field & In-House Reactive-Metal Welding & Equipment Repair Services Available 24/7.

Plate Heat Exchangers:

Plate Heat Exchangers to ASME VIII Div 1 Design, Ports from 1” through 20” with Stainless Steel, Titanium and Special Metals, Plate Heat Exchanger Refurbishing Services & Spare Parts.

Two Service Centers & Fabrication Facilities in Ohio & Texas with Capabilities in: Waterjet, Welding, Machining, Sawing, Plasma Cutting & Forming.

Serving a Wide Variety of Industries: Chemical Processing, Mining, Pulp & Paper, Plating, Aerospace, Power and others.

TITANIUM USA 2024 – Executive Summary (continued)

“Win-win relationships produce the highest value. Open communication with buyers will enable safe selling of even hazardous materials. Each buyer has unique needs. Working together maximizes the value for all parties.”

Dispatches from Titanium Wires

Anna Poberezhna, co-founder ClearHub, in her second presentation at the TITANIUM USA confab, talked about “Ti-Based Cored Wires: Niche Powerhouse for HighPerformance Solutions. Science author: Dr. Serhiy Schwab, Paton Welding Institute, National Science Academy, Ukraine, was listed as a co-author for the program. Poberezhna provided a slide that illustrated titaniumcored wires and titanium flux-cored wire.

She explained that titanium-cored wires represent a “paradigm shift, from niche to essential to mainstream.” She listed several points to support this observation: ultraprecision, extra lifespan and strength more than 800MPa; more than 25 percent tensile strength and hardness enhancement; solve challenges that traditional materials and melting methods cannot.

These improvements are particularly crucial in demanding sectors like offshore energy and aerospace, where weight-to-strength ratios and corrosion resistance are key factors, she said. In addition, they offer three to four times a cost and time savings (repair, coatings: of the time and materials when welding or surfacing high-stress aircraft components, reducing production bottlenecks and extending component lifecycles) and 30-40 percent more energy efficiency by avoiding the complexity and energy consumption of high-temp melting processes.

As for titanium-flux cored wires, Poberezhna said that even with decades of advancements, achieving 800 Mpa strength in titanium-based wires has been a persistent challenge. “What hasn’t changed is the metallurgical reality: titanium’s inherent rigidity, compounded by its sensitivity to impurities during processing, limits ductility. The flux-core method allows us to push beyond the traditional 800 MPa threshold without sacrificing structural integrity,

to the internal shielding

control over oxidation. The shift to cored wire systems for maintenance has reduced lead times in military aviation part refurbishments by 30 percent, according to recent industry reports.”