The Value of U.S. Downtowns and Center Cities CALCULATING THE VALUE OF DOWNTOWN WEST PALM BEACH, FLORIDA A 2021 IDA STUDY A 2021 PUBLICATION CREATED BY THE INTERNATIONAL DOWNTOWN ASSOCIATION

ABOUT IDA

The IDA Research Committee is composed of industry experts who help IDA align strategic goals and top issues to produce high-quality research products informing both IDA members and the place management industry. Chaired and led by IDA Board members, the 2019 Research Committee advances the work set forth in the IDA research agenda by publishing best practices and case studies on top issues facing urban districts, establishing data standards to calculate the value of center cities, and furthering industry benchmarking.

TheIDAInternational Downtown Association is the premier association of urban place managers who are shaping and activating dynamic downtown districts. Founded in 1954, IDA represents an industry of more than 2,500 place management organizations that employ 100,000 people throughout North America. Through its network of diverse practitioners, its rich body of knowledge, and its unique capacity to nurture community-building partnerships, IDA provides tools, intelligence and strategies for creating healthy and dynamic centers that anchor the wellbeing of towns, cities and regions of the world. IDA members are downtown champions who bring urban centers to life. For more information on IDA, visit downtown.org

IDA Director of Research: Cathy Lin, AICP IDA Research Coordinator: Tyler Breazeale International Downtown Association 1275 K Street NW, Suite 1000 Washington, DC 20005 downtown.org202.393.6801©2021International Downtown Association, All Rights Reserved. No part of this publication may be reproduced or transmitted in any form—print, electronic, or otherwise—without the express written permission of IDA.

IDA Research Committee Chair: Brian Douglas Scott, Principal, BDS Planning & Urban Design

IDA Board Chair: Tami Door, President & CEO, Downtown Denver Partnership IDA President & CEO: David T. Downey, CAE, Assoc. AIA, IOM IDA Research Committee

THE VALUE OF U.S. DOWNTOWNS AND CENTER CITIES Stantec’s Urban Places Project Advisors for The Value of U.S. Downtowns and Center Cities Stantec’s Urban Places is an interdisciplinary hub bringing together leaders in planning and urban design, transportation including smart and urban mobility, resilience, development, mixed-use architecture, smart cities, and brownfield redevelopment. They work in downtowns across North America—in cities and suburbs alike—to unlock the extraordinary urban promise of enhanced livability, equity, and resilience. Vice President, Urban Places Planning and Urban Design Leader: David Dixon, FAIA Albuquerque Karen JonathanIversonTeeters Birmingham David Fleming Rob Buddo Evansville Josh AdamArmstrongTrinkel Little Rock Gabe ChellieEllenCarolineHolmstromBrownLampeLongstreth Los Angeles Suzanne Holley Cole Judge Elan Shore West Palm Beach Raphael Clemente Teneka James-Feaman Shelly Williams IDA would like to thank the following individuals for their efforts on the 2021 edition of this project:

CONTENTS Section One: Project Overview Introduction 8 About the Value of Downtowns Study 9 Urban Place Management Organizations 10 Methodology Overview 12 Known Limits to this Study 13 Improvements and Areas for Future Research 13 Section Two: Downtown Profile Overview 16 Economy 19 Inclusion 26 Vibrancy 33 Identity 37 Resilience 39 Downtown Profile 44 Appendices Project Framework and Methodology 48 What factors make a vibrant downtown? 50 Principles and Benefits 56 Data Sources 61 Selected Study Definitions 62 Additional IDA Sources 64 References Endnotes 66 Photo Credits 67

1SECTION ONE OVERVIEWPROJECT

8 IDA | The Value of U.S. Downtowns and Center Cities

No city or region can succeed without a strong downtown, the place where compactness and density bring people, capital, and ideas together in ways that build the economy, opportunity, community and identity. Downtowns across the U.S. experienced unprecedented change in 2020 and 2021, which were fundamentally impacted by the COVID-19 pandemic. In some ways the pandemic highlighted the importance of vibrant urban places. The prolonged absences from our favorite places and activities in some measure deepened our appreciation for them. As the pandemic recedes, downtowns will once again be focal points for commerce and activity. Typically, despite a relatively small share of a city’s overall geography, a downtown delivers significant economic and community benefits across both city and region. Downtown serves as the epicenter of commerce, capital investment, diversity, public discourse, socialization, knowledge and innovation. It provides social benefits through access to community spaces and public institutions. It acts as a hub for employment, civic engagement, arts and culture, historical heritage, local identity, and financial impact. In short, the proximity and density that downtown and center cities create drive the city around them to thrive.

While proximity and density were challenged in the shortterm due to the pandemic, the urgency of responses in 2020 and 2021 also presented new opportunities to adapt downtowns and center cities to a more human-centric future. The success of open streets and outdoor dining in cities large and small have started to lead to permanent programs that prioritize people over cars. Stronger public-private partnerships have streamlined regulations for everything from new business permits to cocktails-to-go. Responding to the racial awakening of 2020, many organizations are working to address bias internally, and in their public programming. Several urban place management organizations are creating programs to specifically support minority entrepreneurs so that downtown better represents the community.

Introduction PROJECT OVERVIEW 1

Longer-term, the effects of the pandemic on urban cores are still emerging. The permanence of remote work remains an open question. Richard Florida cites work by economist Nick Bloom that estimates that ultimately, remote work will account for one-fifth of all work-days, compared with just 5% pre-pandemic.1 This shift will decrease the daytime population in urban centers and affect consumer spending downtown, but it also presents an opportunity to pare down auto-centric infrastructure and create justification for districts to evolve beyond a 9 to 5 worker-focused dynamic to more complete live, work and play communities. The concept of the 15-minute city, the idea that everyone living in a city should have access to essential urban services within a 15 minute walk or bike ride, has gained in popularity in the past year and reinforces the value of the mixed-use nature of many of our downtowns and center cities.2 In the coming years the ways we use and evaluate downtowns and center cities may shift, but downtowns’ resilience across economic, social, and environmental measures positions them well to lead citywide recovery. Downtowns have emerged from past crises even stronger, and there’s no reason to think they won’t this time.

GREAT CITIES START DOWNTOWN

IDA began this research in 2017, working with Stantec’s Urban Places group and the first cohort of 13 UPMOs to develop a methodology for compiling and evaluating data from those 13 downtowns. In 2021, our analysis has expanded to include 43 downtowns and center cities across the U.S.

PROJECT OVERVIEW 1

Buildingfigures. on IDA’s unique industry-wide perspective and expertise, this study quantifies the value of U.S. downtowns and center cities across more than 150 metrics organized under five core value principles, with a focus on how downtowns contribute to the city and region around them. The Value of U.S. Downtowns and Center Cities study is a partnership between IDA and local urban place management organization (UPMO). UPMOs have invaluable insights into the areas they manage and have the relationships that help them unlock essential data sources for this study.

9downtown.org | © 2021 International Downtown Association About the Value of Downtowns Study

The study aims to emphasize the importance of downtown, to demonstrate its unique return on investment, to inform future decision making, and to increase support from local decision makers. The primary project goals are to: Provide a common set of metrics to communicate the value of downtown. Expand the range of arguments UPMOs can make to their stakeholders using publicly available data.

The analysis focuses on how downtown provides value in the five organizing principles of economy, inclusion, vibrancy, identity, and resilience. IDA and our UPMO partners work together to collect hundreds of individual data points, including historic and current data, and three geographic levels (study area, city, and MSA/county). In addition, for employment data we collect three different jobs totals (primary, all jobs, and all private) for all years between 2002 and 2017 to show more nuanced employment trends over time. In total, we utilize more than 8,400 individual pieces of data for each participating downtown, and our downtown database now contains around 310,000 datapoints. The demographic and jobs data included in the study predates the COVID-19 pandemic, but some real estate, tax and assessment data include 2020 and 2021

IDA’s members are urban place management organizations that manage growing districts to create prosperous city centers, commercial neighborhoods and livable urban places for all—from residents to visitors to business owners. These UPMOs shape and activate dynamic downtowns, city centers and neighborhood districts. Since 1970, property and business owners in cities throughout North America have realized that revitalizing and sustaining vibrant downtowns, city centers and neighborhood districts requires focused attention beyond the services municipal governments alone can provide. These private-sector stakeholders come together to form and fund nonprofit management associations that deliver key services and activities within the boundaries of their districts. UPMOs typically operate as business improvement districts (BIDs), business improvement areas (BIAs), partnerships or alliances.

1

10 IDA | The Value of U.S. Downtowns and Center Cities

Urban Place Management Organizations

PROJECT OVERVIEW

The ability of vibrant places to attract visitors and new residents, as well as a regionwide consumer base, creates value. Vibrancy means the buzz of activity and excitement that comes with high-quality experiential offerings like breweries, restaurants, theatres, or outdoor events. Many unique regional cultural institutions, businesses, centers of innovation, public spaces and activities are located downtown. As the cultural center of their cities, downtowns typically attract a large share of citywide visitors and account for a large share of citywide hotels and hotel rooms.

PROJECT OVERVIEW 1

Downtownsactivities. and center cities are valuable due to their roles as economic anchors for their regions. As traditional centers of commerce, transportation, education, and government, downtowns and center cities frequently serve as hubs of industry and revenue generators, despite their only making up a small fraction of the city’s or region’s land area. Downtowns support high percentages of jobs across many different industries and skill levels. Because of a relatively high density of economic activity, investment in the center city provides a greater return per dollar for both public and private sectors than investments elsewhere.

IDENTITY

ECONOMY

RESILIENCE

Downtowns and center cities often serve as iconic symbols of their cities, creating a strong sense of place that enhances local pride. The authentic cultural offerings in downtown enhance its character, heritage, and beauty, and create an environment that other parts of the city can’t easily replicate. Combining community history and personal memory, a downtown’s cultural value plays a central role in preserving and promoting regional identity.

As the literal and figurative heart of their cities, downtowns represent and welcome residents, employees, and visitors from all walks of life. Residents of strong downtowns often come from a wide range of racial, socioeconomic, cultural, and educational backgrounds, and from across all ages. This diversity ensures that as an inclusive place, downtown has a broad appeal to all users and a strong social fabric. Downtowns provide access to all to opportunity, essential services, culture, recreation, entertainment and civic

11downtown.org | © 2021 International Downtown Association

Downtowns and center cities serve as places for regional residents to come together, participate in civic life, and celebrate their region, which in turn promotes tourism and civic society.

Downtowns and center cities play a crucial role in building stability, sustainability, and prosperity for the city and region. Their diversity, concentration of economic activity, and density of services better equip them to adapt to economic and social shocks than more homogenous communities. They can play a key role in advancing regional resilience, particularly in the wake of economic and environmental shocks, which often disproportionately affect less economically and socially dynamic areas.

INCLUSION

VIBRANCY

Methodology Overview

The analysis includes meaningful qualitative observations to acknowledge unique features or add nuance and context to trends revealed in the data. As an example, universities often sit on the edge of a downtown study area. Even if not technically inside downtown, the university’s students typically represent a large user and consumer base for downtown and the analysis describes how the student presence influences the downtown environment. The analytical focus of the report is to make and support value statements about downtown by comparing it to the city, identifying its growth trends over time, and illustrating its density. For instance, data patterns revealed this for 2017 employment totals in downtown Seattle: Downtown is a strong employment and industry hub for the city, with a concentration of high-paying and high-growth employment sectors. 43% of all citywide jobs are located downtown, as are 58% of citywide knowledge jobs. Overall, employment has increased 14% since 2010, outpacing both the city and region. In addition, the number of knowledge jobs grew 28% during that period. Each square mile supports 85,924 workers on average, more than ten times the average job density citywide.

i

IDA worked with each UPMO to identify the boundaries of their downtown for this project, giving priority to alignment with census tracts for ease of incorporating data from the U.S. Census. To measure the value of downtowns relative to their cities, the analysis relies on data that could be collected efficiently and uniformly for a downtown, its city, and its region. IDA collects data from multiple national databases, such as the U.S. Census, LEHD, and ESRI. In addition, IDA gives each participating UPMO a list of metrics to collect from local sources like county assessors or commercial real estate brokers. IDA then analyzes the data to identify study area trends and benchmark the area against the city, the region, and other downtowns in the study.

12 IDA | The Value of U.S. Downtowns and Center Cities PROJECT OVERVIEW 1

i Refer to the appendix for the full methodology. The first step to this study is to identify the right boundaries that capture a downtown district. Geographic parameters often vary across data sources and may not align with a UPMO’s jurisdiction. This study has adopted a definition of the commercial downtown that moves beyond the boundaries of a development authority or a business improvement district. IDA’s Value of Investing in Canadian Downtowns report expresses the challenge well: “Overall, endless debate could be had around the exact boundaries of a downtown, what constitutes a downtown and what elements should be in or out. Yet it is the hope of this study that anyone picking up this report and flicking to their home city will generally think: Give or take a little, this downtown boundary makes sense to me for my home city.”3

PROJECT OVERVIEW 1 Improvements Over Previous Years and Areas for Future Research 17,550 47,118 108,900 264,624 704,000 VODT Pilot - 2017 2018 2019 2020 2021 Value of Downtowns Total Datapoints

This year has seen yet another evolution of the Value of Downtowns product featuring new tools, more data, and new methods of analysis. Our Value of Downtowns database now integrates with Tableau, a data visualization software. With this software, we are able to make connections and draw comparisons between downtowns in a far more nuanced and intuitive way. This report includes some of these new visualizations. For example, charts like households by income over time, or housing units by gross rent over time reveal trends and relationships that we previously were not able to analyze.

While this study aims to provide a comprehensive quantification of the value of downtowns, there are still several limitations to our approach. Not all local sources consistently collect the same data, or collects it in the same way, which hinders our ability to make comparisons between downtowns. In some cases, the data we ask for simply does not exist or has not been collected on the relatively small scale of census tracts or downtown sub-area. This makes it challenging to rely on local data for analysis and can result in some missing pieces in our narrative. Our most recent data also comes predominantly from the 2019 American Community Survey (ACS), the 2018 Longitudinal Employer-Household Dynamics (LEHD) On the Map tool, and ESRI Business Analyst. Due to the lag in data

Known Limits to this Study

The Value of Downtowns database has grown exponentially over past iterations, particularly as this year we have included demographic and jobs data for all years available since 2000, rather than only collecting four benchmark data years. This level of additional data and capability has increased our ability to understand comparisons between downtowns and center cities. This is reflected within this report, as well as with the launch of IDA’s newest research offering, the Value of Downtowns: Comparisons. The Comparisons study focuses on understanding how a given downtown’s performance stacks up to its closest peers, and evaluates a smaller number of metrics than this Value of Downtowns study. availability, some metrics may not align with more recent data from local downtown, municipal, or proprietary sources. This will be especially true in coming years as change in employment during COVID-19 will not be observed in our data sources for several years. Finally, citywide context plays a large role in the analysis. Significant variance in overall city size (from Spartanburg’s 20 square miles to Oklahoma City’s 606) can skew comparisons of the proportion of citywide jobs or population in different districts. However, since downtowns operate within the context of their city, understanding the proportion of jobs, residents, and other metrics as a percentage of their cities still provides an important perspective on a downtown’s contribution to its city and region.

13downtown.org | © 2021 International Downtown Association

2SECTION TWO PROFILEDOWNTOWN

Source: U.S. Decennial Census (2000); American Community Survey 5-Year Estimates (2015–2019)

24%14.3%25,422n/an/a26,439 37%28%1,56320%31%84,087 31%26%2903%5%570K

Source: LEHD On the Map (2018)

City RegionDowntown Primary jobs District share of primary jobs District share of private growthPrivategrowthEmploymentsquareEmployeesjobspermile2010-2018jobs2010-2018

PopulationEmployment2018

While the long-term impact of the COVID-19 pandemic remains to be seen, in the short-term, the significance of the downtown and how it intertwines with the rest of the city and region has never been more apparent. Many of the hardest hit industries – retail, food, entertainment, tourism, arts and culture, and nonprofit organizations – are most visible downtown and make a downtown so compelling. But it is these very sectors, and their return to business that is marking the start of the recovery and accelerate the return of a strong citywide economy. All demographic data used in this report predates the COVID-19 pandemic.

16 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE Downtown Profile | Overview 2 60%8.95,709n/a5,937 12%3.22,0405.4%109,767 13%1.27460.4%1.46M City RegionDowntown ResidentialPopulation share Residents per square Residentsmileper acre Growth 2010-2019 PopulationResidential

Downtown West Palm Beach is a fast-growing center for people and jobs. Despite comprising just 2% of the citywide land area, there are approximately nine residents per acre downtown, a density that is nearly three times higher than the citywide average and greater than the median for downtowns participating in IDA’s Value of U.S. Downtowns and Center Cities study. At the same time, downtown comprises roughly one-in-three primary jobs citywide, with the average square mile hosting 16 times as many jobs as the city average.

Study Area PARTNER West Palm Beach Downtown Development Authority CITY West Palm Beach, FL

A city’s strength and prosperity depend on a strong downtown and center city, which serve as centers of culture, knowledge, and innovation. The performance of districts and center cities strengthens an entire region’s economic productivity, inclusion, vibrancy, identity, and resilience.

17downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2 Inventory (SF)RETAIL 2,9757,7242,000,0008,148,505 Downtown 53% 9.05M 11% 2.22M 16% 8,582 58% 2,861 % of City Per mileSquare (SF)OFFICERESIDENTIALUNITSHOTEL(ROOMS) n/a19%n/an/a 2010–2019Growth Source: CoStar (2021); Convention and Visitor’s Bureau (2021) Residential growth downtown has been a regional success story, led by a shift toward a population that is largely higherincome, non-White, and older. Using the latest available data from the American Community Survey, the number of residents living downtown in the period between 2010 and 2019 grew by 60% to 5,937 residents. Although complete data from the 2020 Census was not yet available at the time of publication to use for analysis, the initial data shows the 2020 downtown population to be around 9,300. Based on the number of residential units counted by CoStar in 2021, average household size, and vacancy rate, we estimate that the 2021 population could be close to 10,000 people. Downtown is a strong economic engine for the city, but despite outpacing IDA’s study median on job growth downtown still falls behind the city and region on percent growth since 2010. Between 2010 and 2018, downtown gained more than 3,300 jobs, experiencing a growth rate of 14.3%. This growth was led by the private sector, which expanded by 24% in this same period. Downtown has a commanding share of the city’s public administration jobs—99%—with the sectors of professional scientific and technical services (40% of citywide jobs), accommodation and food services (35% of citywide jobs), and health care (13% of citywide jobs) also concentrating downtown. As a sign of the vibrancy of downtown, the total number of jobs in the accommodation and food services sector increased by more than 50% between 2010 and 2018, a direct result of increased demand for hospitality and dining downtown.

18 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Defining Boundaries

The study area extends beyond the boundaries of the business improvement district, as geographic parameters vary across data sources and don’t typically align with a place management organization’s jurisdiction. IDA recommended that the urban place management organizations participating in this study use the commonly understood definition of downtown and match boundaries to hard edges, roads, water, natural features or highways. IDA worked with each group to align its downtown study area with census tract boundaries for ease of incorporating publicly available data from the U.S. Census. In this study, the city is the City of West Palm Beach and the region refers to Palm Beach County.

Economy | Impact, Innovation

Source:

On

Downtown Employment CITY’S JOBS 31% CITY’SJOBSCREATIVE 26% CITY’SINDUSTRYKNOWLEDGEJOBS 24% ANDACCOMMODATIONFOODSERVICEJOBS 35% CITY’SJOBSPRIVATE 20%

19downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2

Downtowns make up a small share of their city’s land area but have substantial economic importance. Home to 31% of all jobs citywide, downtown West Palm Beach has a larger share of citywide jobs than most of the downtowns participating in IDA’s Value of U.S. Downtowns and Center Cities study, demonstrating that downtown offers an exceptionally high value to its city as an employment Thecenter.four largest employment sectors make up nearly three-quarters of all downtown jobs. Downtown’s largest employment sector is public administration (11,073 jobs), which contributes more than three times as many jobs downtown as the next largest sector. The second-largest sector—professional, scientific, and technical services (3,068 jobs)—also has a strong presence downtown, concentrating 40% of citywide employment. The sectors of accommodation and food services (2,751 jobs) and healthcare and social assistance (1,833 jobs) round out this list, with each gaining traction in the past two decades. Since 2002, downtown has added more than 1,200 jobs from these two sectors combined, with the accommodation and food services sector growing by more than 50%. This sector is of particular importance, with growth translating to increased vibrancy as new restaurants, bars, and other types of amenities open their doors, attracting more people downtown. LEHD the Map (2018)

Source: LEHD On the Map (2018) *Downtown jobs have been excluded from District 3 Jobs by Commission District Downtown contains 24% of the city’s jobs across all knowledge industry sectors, a share that is on par with other downtowns in this study. Due to the outsized presence of the health care sector beyond the borders of downtown, if these jobs were excluded, downtown’s share of knowledge industry jobs would rise to 31%. Growth is occurring across all knowledge sectors, contributing to a 17% increase in knowledge industry jobs downtown between 2010 and 2018, relative to an 18% increase citywide. Although it is one of the smallest sectors comprising fewer than 500 jobs downtown, the information sector has more than doubled in size since 2010, adding more than 200 jobs by 2018.

20 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2

Following national trends, the finance and insurance industry experienced a significant decline during the Great Recession, shedding approximately 700 workers between 2006 and 2010 and never recovering to its pre-Recession levels of employment. However, in a departure from trends in most urban places, the manufacturing sector has experienced a steady increase in jobs since the early 2000s, more than quadrupling in size since 2002 with more than 800 jobs by 2018. It is likely that the craft beer and spirits movement, motivating the opening of breweries and distilleries downtown, has carried this surprising uptick in manufacturing jobs.

21downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2 Source: LEHD On the Map (2010–2018) Knowledge jobs include those in finance and insurance; real estate; management of companies and enterprise; professional, scientific and technical services; information; and health care and social assistance. RegionCityDowntown 24%13%26% 20%72%13% 36%1%3% 149%22%35% 20%27%21% 25%18%17% Job Change in Top Private Industries Downtown 30,00025,00020,00015,00010,0005,000014,00012,00010,0008,0006,0004,0002,0000 JobsTotalIndustryIndividualbyJobs Total Jobs Downtown Public ConstructionandRealRetailManufacturingFinanceRemediationManagementSupport,AdministrationAssistanceHealthcareFoodAccommodationandProfessional,AdministrationScientific,TechnicalServicesandServicesandSocial&WasteandandInsuranceTradeEstateandRentalLeasing 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Source: LEHD On the Map (2003-2018) Finance, Insurance, Real Estate and Rental and Leasing Management of andCompaniesEnterprises TechnicalScientifiProfessional,c,andServices Information Health Care and Social Assistance KnowledgeTotal Job Change Knowledge Industry Employment Growth 2010–2018

Entrepreneurial Environment

48%32%20% 59%23%18% 52%25%23% Downtown < 20 250+20-249PEOPLEPEOPLEPEOPLE City Region Jobs by Firm Size Source: LEHD On the Map (2017) 70%16%14% 76%14%10% 72%17%12% Downtown < 3 11+4-10YEARSYEARSYEARS City Region Jobs by Firm Age Source: LEHD On the Map (2017)

22 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2

A strong entrepreneurial environment that supports both small businesses and startups in all industries is critical to a thriving downtown. Small businesses generate new jobs, promote innovation and competition, and account for almost half of U.S. economic activity.1 Downtown provides a friendly environment for small businesses and startups. However, with growth among firms that are smaller and younger occurring at a faster pace citywide and regionally, downtown is on track to lose its entrepreneurial edge to other areas of West Palm Beach. As of 2017, 20% of downtown’s private sector jobs were at firms with fewer than 20 people, a slightly higher share than the city but below the regional share of 23%. Downtown has seen 8% growth in workers at these smaller businesses since 2011, falling behind the city and region, where growth has been 14% and 19% respectively. Also in 2017, 14% of downtown’s private sector jobs were at businesses less than three years old, a slightly higher share than the city or region. However, since 2011, there has been a 42% uptick in jobs at these younger firms, which is an encouraging level of growth but still falls behind citywide figure of 77% and regional figure of 51%. One important caveat on this data is that it does not count those who are self-employed, which may omit a number of workers.

Fiscal Impact With only 4% of downtown workers also living within the study area, downtown West Palm Beach draws almost all its workers from throughout the region. About 7% of all downtown workers come from one zip code—33411— an area with many subdivisions located on the edge of downtown. A large share of downtown workers (87%) commute from outside the city limits, injecting money into the local economy. Wages earned downtown are also recirculated into the broader local economy, with downtown jobs generating 7% of Palm Beach County’s private sector employee earnings.

Since these figures do not include public sector workers, which comprise downtown’s largest sector, the share of pay

Where Downtown Workers Live by ZIP Code

23downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2

Source: LEHD On the Map (2018) attributed to downtown workers is even higher than this representation. Furthermore, that downtown generates 7% of the county’s pay is particularly significant given that downtown only makes up 0.2% of the county’s total land Wagesarea. downtown are also greater than those earned in the city or region. On average, downtown workers earn $12,000 more than those working in the rest of the county. A greater share of downtown workers—61%—earns $40,000 or more annually than in the city or county, where fewer than 50% of all workers meet this pay threshold. This demonstrates how downtown is not only a concentrator of jobs, but a concentrator of high-quality, high-paying work.

24 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 61%28%11% 49%35%16% 45%37%18% Downtown $15,000 OR $40,000$15,000–$40,000LESSORMORE City Region Jobs by Earnings ANNUALLY Source: LEHD On the Map (2018) $61.7K$1.84B $49K7% Downtown Total WageAveragePayroll**Annual County Payroll and Wage* Source: Census Business Patterns (2018) *Data excludes payroll of public administration employees. As a result of its density, downtown generates an outsized economic benefit for the city. The land within the boundaries of the West Palm Beach Downtown Development Authority (DDA) is nearly thirteen times as valuable per square mile as the citywide average, with downtown concentrating 17% of the city’s taxable value in territory comprising less than 2% of the city’s total land area. This land is only gaining more value over time. Since 2015, downtown’s assessed value has increased by 56% compared to an increase citywide of 35%, showing that investment is growing from the inside out. Downtown’s place at the epicenter of the economy of West Palm Beach underscores the important role that organizations like the DDA play in creating and sustaining a healthy local economy. Founded in 1967, the DDA is devoted to improving and maintaining downtown by offering information and services to visitors, residents, and business owners. This kind of block-level support is critical to preserving not only the fiscal health of the city, but also the prosperity of the entire region.

25downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2 Land Value and Assessment ASSESSED VALUE** ASSESSED VALUE PER SQUARE MILE Downtown*$3.45B$2.59B City$271M$14.6B Region$75.4M$148B DT8.5%17%%ofCity Source: City of West Palm Beach (2019) *The downtown boundary used here is the DDA boundary **Assessed value also refers to the taxable value

Downtown West Palm Beach is home to a two-thirds majority White population. This is a striking difference from the city overall, which is only 37% White, but not too far off from the region at 55% White. Notably absent among downtown residents is representation among individuals who identify as Black. Only 10% of downtown residents are Black, compared to 34% of residents of the city and 18% of those living in the region. The share of Hispanic or Latino residents downtown—20%—is more in line with the city and the region, where between one-in-four and one-in-five residents is Hispanic or Latino. cities’ downtown

Source: American Community Survey 5-Year Estimates (2015–2019) DOWNTOWN PROFILE 2 “ ” Inclusive spaces in the public realm, particularly in our

26 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities Inclusion | Diversity, Affordability Downtowns and center cities invite and welcome all residents, employees and visitors by providing access to jobs, housing, essential services, culture, recreation, entertainment, and participation in civic activities. A strong sense of inclusion and social cohesion keeps communities strong in times ofResidentscrisis. By Race Benefits of Inclusion: Equity, Affordability, Civic Participation, Civic Purpose, Culture, Mobility, Accessibility, Tradition, Heritage, Services, Opportunity, Workforce Diversity Demographics

downtowns, can help break down the social barriers that often divide us. Thriving

districts and public spaces promote not only economic prosperity, but also social cohesion.2 37% 67% WHITE 55% 20%25% HISPANIC OR LATINO22%34%10%18% 2% ASIANBLACK AND PACIFIC ISLANDER NATIVE AMERICAN OR OTHER0%0%2%3% TWO OR MORE0%1%2%2% RegionCityDowntown

27downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association Employment By Race Source: LEHD On the Map (2018) *Percentages do not add up to 100% because this dataset double counts Hispanic/Latino with the other racial groups. DOWNTOWN PROFILE 2 71%75% WHITE RegionCityDowntown 73% 24% 0% 20%AMERICANBLACK INDIAN OR ALASKAN NATIVE ASIAN0%3%3% 21% NATIVE HAWAIIAN OR PACIFIC ISLANDER0%0%0%0%3% TWO OR MORE 1%1%1% HISPANIC OR LATINO 21%22%23% Despite having lower representation among non-White residents, downtown demographics are shifting towards more diversity. Since 2016, downtown’s share of residents who are White alone has decreased by 12% with gains greatest among the Hispanic or Latino population. This follows a citywide trend in which the share of White residents has declined steadily by nearly ten percentage points since its decade high in 2011. Meanwhile, the share of residents who are Black or Hispanic or Latino was at a ten-year high in 2019. Viewing the data outside these percentages though it is important to note that this shift is occurring in part due to a loss in total White residents and not simply the addition of residents of other racial and ethnic groups. Since 2016 downtown has lost 440 White residents, accelerating these percentage shifts. In terms of diversity in employment the downtown workforce closely reflects citywide and regional workforce demographics. A notably high share of workers are White relative to residential demographics, this is due to the employment dataset not separating Hispanic or Latino from the racial groups – meaning a large share of White workers are Hispanic or Latino. If we combine regional White and Hispanic or Latino residents in the residential demographics chart, approximately 77% of residents are White and/or Hispanic or Latino, a similar share to the percentage of White workers. As stated, a sizable percentage of workers are commuting to downtown from outside the city which makes it unsurprising that employment demographics align closer to regional residential demographics.

28 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Age Diversity Downtown skews older than the city or the region. Nearly half of all downtown residents are over the age of 50, compared with approximately 37% of residents citywide and 43% regionally. Comprising nearly one-third of all downtown residents, the largest age group downtown is residents over the age of 65. This is also the fastest-growing age group, increasing downtown by 26% between 2011 and 2019 and outpacing a regional trend that saw 23% growth among those over the age of 65 in this same period. This is uncommon for urban places, where it is typically the 25- to 34-year-old age group that leads population growth. Citywide, there appears to be a diverse mix of ages, with each age group making up between 15% and 20% of the population except for those between the ages of 18 and 24, which comprise roughly 10% of the population. Source: American Community Survey 5-Year Estimates (2009–2019) Source: American Community Survey 5-Year Estimates (2015–2019) Residents by Race Over Time Downtown Age Diversity < 18 years 18 - 24 25 - 34 35 - 49 50 - 64 65+ 8% 6% 20% 18% 19% 29% Source: American Community Survey 5-Year Estimates (2015–2019) City Age Diversity < 18 years 18 - 24 25 - 34 35 - 49 50 - 64 65+ 18% 10% 15% 19% 19% 19% Downtown City 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8 2 0 1 9 2 0 2 0 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8 2 0 1 9 2 0 2 0 YearYear 0 % 1 0 % 2 0 % 3 0 % 4 0 % 5 0 % 6 0 % 7 0 % 8 0 % PopulationofShare American Indian Alone Pacific Islander Alone Asian Alone Some Other Race Alone Black Alone Two or More Races Hispanic or Latino White Alone

29downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2 Household Income Over Time Socioeconomics With a median household income of more than $77,000, downtown is more affluent than the city or the region, where the median household income is $54,000 and $63,000, respectively. In fact, within downtown, all but one block group exceeds the median household income of both the city and region, topping $100,000 in two block groups located in the southwest portion of downtown. Downtown incomes have risen drastically over the past decade, far outpacing citywide growth. Between 2010 and 2019, downtown gained more than 900 households earning more than $40,000. This translates to a growth rate nearing 70% downtown—more than four times the rate of growth in this income bracket citywide. The number of the highest earning households—those earning over $100,000 annually—nearly doubled within this same period downtown compared to an increase of just over 40% citywide. The influx of higher income households is Source: American Community Survey 5-Year Estimates (2010 to 2019) 2 0 1 0 2 0 1 2 2 0 1 4 2 0 1 6 2 0 1 8 2 0 2 0 0 1 0 0 2 0 0 3 0 0 4 0 0 5 0 0 6 0 0 7 0 0 8 0 0 2 0 1 0 2 0 1 2 2 0 1 4 2 0 1 6 2 0 1 8 2 0 2 0 0 K 1 K 2 K 3 K 4 K 5 K 6 K 7 K 8 K 9 K 1 0 K IncomebyHouseholds Downtown Year IncomebyHouseholds City Year $40,000 to $59,999 $60,000 to $99,999 Less Than $20,000 $20,000 to $39,999 $100,000 to $149,999 $150,000 or more Median Household Income by Block Group Source: American Community Survey 5-Year Estimates (2015–2019)

Survey 5-Year Estimates

30 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Downtown 62% 50% 30%% WHORESIDENTSRENT $1,700 $1,303 $1,398GROSSMEDIANRENT 53% 29% 24% MEDIAN 2010–2019INCREASERENT 40% 55% 56%BURDENEDRENTCity Region Renters Source: American Community Survey 5-Year Estimates (2015–2019) 38% 50% 70%% WHORESIDENTSOWN $365K $252K $283KMEDIAN HOME PRICE 14% 5% 8% MEDIAN PRICE 2010–2019CHANGE 31% 40% 32%BURDENEDHOUSING83% 61% 75%HOMEOWNERSWHITE 17% 39% 25%HOMEOWNERSNON-WHITE Downtown City Region Homeowners Source: American Community Survey 5-Year Estimates (2015–2019) an encouraging nod to the appeal of downtown. Because wealthier households have greater means to live wherever they want, the fact that a disproportionately higher number of wealthy individuals are choosing to live downtown over other parts of the city is a statistical expression that downtown has a lot to offer. While equity concerns typically accompany drastic shifts like these, there does not appear to be demonstrable displacement happening downtown within the past decade. The number of households earning less than $40,000 has held steady downtown, even as the city saw a 16% decrease in the number of households falling within this income bracket. Sustaining lower-income households in the face of such pronounced growth among upperincome households can be attributed to the work of West Palm Beach’s Community Redevelopment Agency, which has largely enabled downtown to stay ahead of potential displacement by incentivizing the development of affordable housing downtown. These incentives offer $10,000 per affordable unit in a mixed-income multifamily development. Housing and Affordability Even though downtowns generally have higher housing prices, their density of housing, concentration of jobs, and access to public transportation can make living downtown less expensive than living in other neighborhoods. This is true when comparing West Palm Beach to the rest of the city and Palm Beach County, but not to other urban places. According to the Housing and Transportation Index, a typical family (earning the regional median household income) living downtown would expect to spend around 58% of their income on housing and transportation combined, which is comparable to the rates for those living MEDIAN INCOME DOWNTOWNCITYREGION MIDDLE-CLASS HOUSEHOLDS* $77K $54K $63K 52% 50%48%

Source: American Community (2015–2019)

* Middle-class defined as 66% to 200% AMI ClassMiddle

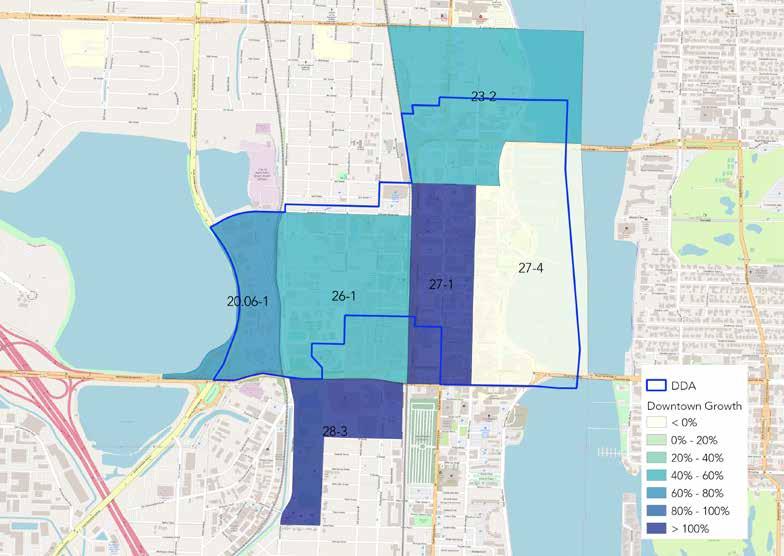

31downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2 Housing and Transportation Index Downtown 58% City 58% Region 63% Source: Center for Neighborhood Technology (CNT) Housing and Transportation Index (2017) Rent Over TimeHousehold2009–2019Income and Rent Growth Over Time Downtown 2 0 1 0 2 0 1 2 2 0 1 4 2 0 1 6 2 0 1 8 2 0 2 0 Year 0 1 0 0 2 0 0 3 0 0 4 0 0 5 0 0 6 0 0 7 0 0 8 0 0 9 0 0 1 0 0 0 1 ,1 0 0 1 2 0 0 RentbyUnitsOccupiedRenterofNumber City 2 0 1 0 2 0 1 2 2 0 1 4 2 0 1 6 2 0 1 8 2 0 2 0 Year 1 0 0 00 1 0 0 0 2 0 0 0 3 0 0 0 4 0 0 0 5 0 0 0 6 0 0 0 7 0 0 0 8 0 0 0 9 0 0 0 1 0 0 0 0 1 1 0 0 0 1 2 0 0 0 1 3 0 0 0 1 4 0 0 0 Less Than $600 $600 to $799 $800 to $999 $1,000 to $1,999 $2,000 or More Source: American Community Survey 5-Year Estimates (2010–2019) in the city and slightly lower than those living elsewhere in the region. However, this percentage is the highest of any downtown participating in IDA’s Value of U.S. Downtowns and Center Cities study, which has a median Housing and Transportation Index of 39%, reflecting poorly on downtown’s affordability. Within downtown, some block groups are more affordable than others. However, with the exception of block group 23-2, the Housing and Transportation Indices for the remaining five block groups range between 53% and 71%—an alarmingly high range whose upper end approaches double the median of this study. This has real-world consequences; two-in-five downtown renters are rent-burdened, meaning rent alone is more than 30% of their income. Even though it may seem high, the share of rent-burdened individuals in the city and region is even higher. This is likely due in part to the higher-income residents of downtown who can comfortably afford even more expensive units while still spending less than 30% of their income. Between 2010 and 2019, median household income and median gross rent both increased by more than 50%—a very high rate of growth that has seen downtown overtake and now greatly surpass the city and regional Higher-than-averagefigures. incomes also seem to be driving an atypical rate of homeownership downtown. Nearly 40% Source: American Community Survey 5-Year Estimates (2006–2010, 2015–2019) $ 0 $ 1 0 ,0 0 0 $ 2 0 ,0 0 0 $ 3 0 ,0 0 0 $ 4 0 ,0 0 0 $ 5 0 ,0 0 0 $ 6 0 ,0 0 0 $ 7 0 ,0 0 0 $ 8 0 ,0 0 0 Median Household Income $ 0 $ 2 0 0 $ 4 0 0 $ 6 0 0 $ 8 0 0 $ 1 ,0 0 0 $ 1 ,2 0 0 $ 1 ,4 0 0 $ 1 ,6 0 0 $ 1 ,8 0 0 $ 2 ,0 0 0 Median Gross Rent RegionCityDowntown 5 4 % 2 1 % 1 9 % 2 4 % 2 9 % 5 3 % 2010 2019

Educational

for

Residents of downtown are highly educated. 85% of downtown residents have attained at least some higher education, a share that is more than 20% greater than it is among residents living in the city or region. This figure has increased by 11% since 2010, showing a continued shift towards a more educated population. Among those employed downtown, slightly more workers have achieved some higher education compared with those employed in the city or region. Attainment Residents 25+

Economic Inclusion

32 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Jobs by AttainmentEducational HIGH SCHOOL OR LESS 32%32%36% 28%31%40% 29%31%40%SOME COLLEGE OR ASSOCIATE’S DEGREE BACHELOR’S OR ADVANCED DEGREES Downtown City Region Source: LEHD On the Map (2018) Source: American Community Survey 5-Year Estimates (2015–2019) 14% 23% 28% 36% 14% 20% 27% 39% 24% 28% 15% Advanced Degree Bachelor’s Degree Some College High School or DowntownLess City Region Downtown 2010 33% of downtown housing units are owner-occupied, which is especially high for urban places, even though the price for a home in downtown is more than $100,000 higher than the median for the city. This gap in home prices has only widened over the past ten years, indicative of a market in which wealthier homebuyers are in high supply. The outsized presence of seasonal residences, which is more than twice as high downtown as it is in the city, is undoubtedly feeding into this housing frenzy, with outside wealth driving a greater share of the development that is underway in the downtown core. While beneficial to the outward growth of the city, the opportunity to invest in the future of downtown has not been available to everyone. Data show that downtown homeowners are disproportionately White, with fewer than one-in-five homeowners identifying as non-White despite making up approximately one-third of the population downtown.

DOWNTOWN PROFILE 2 GrowthResidential 2010–2019GROWTHPOPULATIONRESIDENTIAL

60%19% 12%-4% 13%3%2010–2019UNITRESIDENTIALGROWTH

33downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association

Downtown City Region

Source: American Community Survey 5-Year Estimates (2015–2019), West Palm Beach DDA (2019) *Downtown data on residential units is from local data while city and region are census data.

infrastructural,

Residential Growth Residential growth signals a fast-changing and vibrant downtown, one that not only has a working population in the daytime but also activities and people around throughout the day and night. Downtown is growing at a faster pace than most of West Palm Beach, adding more than 2,200 residents between 2010 and 2019 for a growth rate of 60%. That’s five times faster than the city and region, which still experienced impressive growth topping 12% over the same period. Within downtown, four of the six block groups that comprise the study area saw growth well in excess of 50%, with only one block group contracting, primarily due to a loss in nonHispanic White residents and lower-income households. Development has struggled to keep up with such rapid growth in the number of people living downtown. Between 2010 and 2019, the total number of residential units on the market increased by 12%, falling nearly 50 percentage points behind the rate of population increase. This is undoubtedly fueling the rapid increase in both rent and home prices downtown, which is far outpacing rising prices in the city and region. Housing development has continued through the last two years; nearly 500 new units have been added since 2019. Due to their expansive base of users, center cities can support a variety of unique retail, and institutional uses that offer cross-cutting benefits to the region.

Vibrancy | Spending, Fun Benefits of Vibrancy: Density, Creativity, Innovation, Investment, Spending, Fun, Utilization, Brand, Variety, Infrastructure, Celebration Downtowns and center cities typically form the regional epicenter of culture, innovation, community, and commerce. Downtowns flourish due to density, diversity, identity, and use. An engaging downtown “creates the critical mass of activity that supports retail and restaurants, brings people together in social settings, makes streets feel safe, and encourages people to live and work downtown because of the extensive amenities.”3 Physical distancing measures during the COVID-19 pandemic have only emphasized how valued a vibrant downtown with restaurants, concerts, outdoor events, and festivals is. The recovery of storefront businesses, event venues, and hotels post-pandemic will be essential for restoring a sense of vibrancy and normalcy.

34 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Downtown Population Growth 2010 to 2019 by Block Group County Population Growth 2010 to 2019 by Block Group Source: American Community Survey 5-Year Estimates (2015–2019) Source: American Community Survey 5-Year Estimates (2015–2019)

Retail Vitality Typically, a downtown’s retail environment acts as the heart of the community and a key reason for residents, workers, and visitors to come downtown. This is true for downtown West Palm Beach, which is responsible for 12% of retail sales generated citywide, a strong indication of the vibrancy of the retail sector that places downtown between the 60th and 80th percentile across all cities examined for IDA’s Value of U.S. Downtowns and Center Cities study. In fact, the average square mile downtown generates six times as much in retail sales than the average square mile citywide, with total sales exceeding $300 million annually. Data also reveals that most of these sales are made to non-residents, further underscoring how downtown has become a regional destination for shopping and dining. Within the food and beverage industry alone, nearly four out of every five sales are purchases made by non-residents.

Source:

Retail Sales SHARE OF CITY 12% DOWNTOWN RETAIL SALES $303 Million RETAIL SALES PER SQUARE MILE $291.4 Million All Retail TOTAL RETAILDowntownBUSINESSES 290 City 1,441 FOOD AND BEVERAGE BUSINESSES 134 433 Source: ESRI Business Analyst Business Total Data (2019) Retail Real Estate SQUARE FEET OF SQ.INVENTORYRENTAVG.RETAILVACANCYPERSQ.FT.PERMILE Source: West

DDA (2021) Downtown

2.2M$4411%2.0M 298K$23.374%16M

A critical part of what makes downtown West Palm Beach a vibrant shopping district is the density of its storefronts, whose proximity to one another contributes greatly to the area’s walkable feel. One-fifth of the city’s retail storefronts are located downtown, which has a density of storefronts 11 times greater than the density of storefronts citywide. Because of this, downtown has become one of the most sought-after investments for businesses, which are willing to pay a premium for a location along one of downtown’s concentrated retail corridors. The average price per square foot for commercial storefronts downtown is $44—nearly twice the average elsewhere in the city. One concerning caveat: downtown does have an elevated vacancy figure of 11%, which is 7 points higher than the city’s vacancy rate and slightly higher compared to other urban places. Oftentimes, higher than average commercial rents can adversely impact storefront occupancy because of credit-worthy businesses being priced out of the market. This, in turn, can drive up vacancy rates. ESRI Business Analyst Marketplace Data (2017) Palm Beach City

35downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2

36 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Live Events and Entertainment Downtown is a regional destination for live events and entertainment, with a total of ten live entertainment venues and two theaters. Opened in 1992, the Kravis Center is a state-of-the-art performing arts venue that hosts approximately 550 performances each season, ranging from concerts to musicals. Nearly 500,000 people visit the Kravis Center each season to see a production in one of the building’s three theaters, which range in size from the 300-seat Marshall E. Rinker, Sr. Playhouse to the 2,195-seat Alexander W. Dreyfoos Concert Hall. In addition to yearround entertainment, downtown is also home to annual traditions including SunFest, Florida’s largest waterfront music and art festival attracting more than 100,000 visitors each May, and the city’s 4th on Flagler Independence Day Toevent.support the influx of people taking part in these activities and events, downtown’s lodging industry has grown to include nearly 60% of all hotel rooms citywide. In addition to traditional accommodations, the short-term rental market downtown includes more than 300 owner-operated hotel alternatives like Airbnb, which comprise 22% of the market within this hospitality subsector citywide. It should be noted that these figures do not include hotels in the neighboring and competing Palm Beach. District Events and Activities FARMERSMARKETENTERTAINMENTWITHVENUESLIVETHEATERSTOTAL 1102 Source: West Palm Beach DDA (2021) Hotels OCCUPANCYAVERAGEROOMSHOTELHOTELS CITYDOWNTOWN 515 5,0952,975 n/a68% Source: West Palm Beach DDA (2021)

Benefits of Identity: Brand, Visitation, Heritage, Tradition, Memory, Celebration, Fun, Utilization, Culture

Born out of affluence and opportunity at the turn of the 20th century, downtown West Palm Beach sits at the center of paradise in South Florida. Its dazzling waterfront vistas, historic streetscapes, and year-round warmth have helped downtown gain recognition as a place where ideas flourish and dreams become reality.

Like much of South Florida, the land now known as West Palm Beach was inhabited for centuries by generations of Native Americans who were the first to recognize the bounty of the region. The modern city, brought into existence through the vision of oil baron and Florida railroad magnate Henry Morrison Flagler, was incorporated in 1894 just as the first railroad tracks to reach this far south were laid through what is now the city’s downtown. Over the next century, the population of West Palm Beach grew to encompass more than 100,000 people, with popular thoroughfares like Clematis Street showcasing an eclectic mix of architectural styles that embody the spirit of progress in a turn-of-thecentury downtown. Like so many urban places, downtown West Palm Beach experienced a period of neglect beginning in the 1960s as shoppers, distracted by the trend and convenience of shopping malls, turned their attention away from the center city. By the 1990s, investors began taking a fresh look at downtown, with major retailers like Gap, Loft, and Banana Republic opening flagship outposts in historic storefronts.

Nightclubs that dotted Clematis Street eventually gave way to chain and chef-run restaurants as new wealth flocked to the area, attracted by the appeal of city life and the opportunity to live in modern condominiums overlooking the inner coastline. In 2000, developers transformed a desolate stretch of land northwest of Okeechobee and Quadrille Boulevard into CityPlace, a mixed-use district anchored by luxury retail, offices, housing, cultural facilities, and public spaces.5 The area, now known simply as The Square, bills itself as an “experiential neighborhood” that is home to more 50 shops and restaurants.

The authentic cultural offerings in downtown enhance its character, heritage, and beauty, and create a unique sense of place not easily replicated in other parts of the city.

SocialINSTAGRAMMediaPOSTS WITH #DOWNTOWNWESTPALMBEACH TWITTER FOLLOWERS FOR @ DOWNTOWNWPB FACEBOOK21,80036,350FOLLOWERS33,616 As of January 6, 2022

Downtowns and center cities preserve the heritage of a place, provide a common point of physical connection for regional residents, and contribute positively to the brand of the regions they anchor.

Identity | Visitation, Heritage, Tradition

Downtowns are “iconic and powerful symbols for a city and often contain the most iconic landmarks, distinctive features, and unique neighborhoods. Given that most downtowns represent one of the oldest neighborhoods citywide, they offer rare insights into their city’s past, present, and future.”4

37downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association DOWNTOWN PROFILE 2

Today, downtown West Palm Beach is home to more than 25 local and national historic structures, nine parks and natural areas, and four public art installations. Nearly half of the city’s museums are located downtown, including the Richard and Pat Johnson Palm Beach County History Museum, located in the city’s historic 1916 courthouse, and the nearby Norton Museum of Art, which houses more than 8,200 works of art at the edge of downtown. Other popular attractions include the Mandel Public Library of West Palm Beach, the city’s four-story public library located within the City Center complex, and GreenMarket, a long-running farmers market that showcases 100 vendors and was recently named the #1 farmers market in the United States by USA TODAY

38 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities

DOWNTOWN10Best. PROFILE 2 Destinations and Unique Features PARKSNATURALANDAREAS 9 MUSEUMS 11 STRUCTURESHISTORIC 26 Source: National Register of Historic Places (2017); City of West Palm Beach Parks Department (2021); West Palm Beach DDA (2021) PUBLIC INSTALLATIONSART 4

|

Benefits of Resilience: Health, Equity, Sustainability, Accessibility, Mobility, Durability of Services, Density, Diversity, Affordability, Civic Participation, Opportunity, Scale, Infrastructure Region YOY 2009–2010 2010–2011

Source: LEHD On the Map (2009–2011) At its broadest, resilience means a place’s ability to withstand shocks and stresses. Thanks to their diversity and density of resources and services, center cities and their residents can better absorb economic, social, and environmental shocks and stresses than other parts of the city. The COVID-19 pandemic has brought resilience to the forefront of many people’s minds.

Diversity and economic vitality equip downtowns and center cities to adapt to economic and social shocks better than more homogenous communities. Similarly, density better positions downtowns and center cities to make investments needed to hedge against and bounce back from increasingly frequent environmental shocks and stresses.

Economic Resilience

DOWNTOWN PROFILE 2 Recession Impact and Recovery2%11% Downtown -1%7% City 7%0%

Job growth was nearly flat across the city and region during the emergence from the Great Recession between 2009 and 2010, with downtown seeing a small 2% uptick in the number of jobs in the same period. By 2011, downtown was on a strong path toward recovery led by an 11% growth in jobs, outpacing the city and region where the job market expanded at a still-impressive rate of 7%. At this rate, the job market downtown and across West Palm Beach rebounded faster than most other cities examined to date for IDA’s Value of U.S. Downtowns and Center Cities study, revealing that businesses located downtown have a sturdy and resilient economic foundation. The diverse mix of industry sectors within downtown ensures that shocks or disruptions to any one industry will not undermine the downtown economy.

On the economic side, downtowns and their cities are able to mobilize to offer economic relief quickly. Over the longer-term, downtowns have proven to bounce back quickly from economic downturns. Social resilience means that residents are able to access necessary health services and health workers, but also that strong community support enables community members, both residents and businesses alike, to depend upon each other for support. The green spaces and trails that contribute to environmental resilience have seen renewed importance as safe outdoor respites. Each of these elements illustrates how downtown contributes to the holistic resilience of the community and city at-large.

39downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association

Resilience Sustainability, Diversity

YOY

Economic resilience describes the ability of a downtown to weather adverse economic events, including the COVID-19 pandemic, as a result of having a balanced mix of employment sectors and other factors that are essential to a community’s long-term success. Like many communities, the Great Recession was a major disruptive event that impacted multiple employment sectors in West Palm Beach and serves as a good litmus test for how downtown, the city, and the region might fare under similar economic stressors.

40 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2 Health AVERAGE PHYSICALNOEXPECTANCYLIFELEISURE-TIMEACTIVITY CITYDOWNTOWN 8277 29%25% 16%10%WITHOUT INSURANCEHEALTHCOVERAGE

Source: American Community Survey 5-Year Estimates (2015–2019)

Social Resilience Downtowns act as hubs for social resilience. Their dense nature means that a diverse mix of residents and employees have access to a multitude of community resources in a small area. With nine parks and natural areas, one library, and four religious institutions, residents, employees, and visitors in downtown West Palm Beach can meet, learn, and participate in civic life in multiple places. Social resilience also means having a healthy population, particularly in a public health crisis. Across multiple measures used in this study, residents of downtown fare better than those living in the city or region. However, the life expectancy of downtown residents—77 years old—is surprisingly low relative to the citywide average of 82. Data reveal that the situation is more nuanced, with Census Tracts 20.06 and 23, located on the west and north sides of downtown, having among the lowest life expectancies downtown at between 70 and 73 years old, which weighs down the average. This stands in contrast to other metrics— including the percentage of individuals with no leisuretime physical activity and the percentage of those without health insurance—both of which are lower downtown than elsewhere, indicating that, on average, downtown residents live healthier lifestyles. Downtown is also home to fewer residents living beneath the poverty threshold. However, about as many households downtown lacks a computer as those living in the city and the region, and a greater share of households downtown do not have internet access. That nearly one-in-five households cannot access the internet is an especially troublesome sign. As more work, schooling, entertainment, and other daily activities move online—a shift accelerated by the public health response to COVID-19—access to a suitable computer or mobile device and to reliable internet service has grown increasingly important

41downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association 43 DOWNTOWN PROFILE 2 Access to OpportunityEconomic Downtown 17%8%12% City 10%9%11% Region 8%8%12%RESIDENTS UNDER POVERTY ACCESSWITHOUTHOUSEHOLDSCOMPUTERWITHOUTHOUSEHOLDSLINEAINTERNET Source: American Community Survey 5-Year Estimates (2015–2019) Source: West Palm Beach DDA (2021) Downtown Community Resources LIBRARY 1 INSTITUTIONSRELIGIOUS 4 PARKS AND NATURAL AREAS 9 POSTSECONDARYINSTITUTIONS 2 PRIMARY SECONDARYANDSCHOOLS 3

ResilienceEnvironmental41914K843.359540HOUSEHOLDEMISSIONSANNUALSPACEACRESPOINTSCHARGINGELECTRICBUILDINGSLEEDCAROFOPENGHGPER CITYDOWNTOWN

A downtown’s environmental resilience plays a major role in assuring long-term sustainability in its region. By every environmental measure consulted for this report, downtown West Palm Beach fares better than the city. Downtown leads the city in sustainable infrastructure as home to nearly a quarter of the city’s LEED certified buildings, almost half the electric car charging points, and a greatly reduced carbon footprint per household.

Source: West Palm Beach DDA (2021), CNT (2017)

42 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities DOWNTOWN PROFILE 2

Environmental Resilience

Parks and green spaces permeate the urban core providing access to recreational space in a city dotted with lakes and other waterways. Even though West Palm Beach is largely a car-dependent city, downtown is home to a greater share of residents who choose an alternative to driving to get to and from work. Nearly 10% more people walk or use public transit for commuting than those in the city or region. On top of this, downtown’s Walk Score is 40 points higher than the city’s Walk Score, making it the most walkable neighborhood in West Palm BuildingBeach.onthis foundation and driven by the influx of new residents to the area, city leaders have made significant investments towards a more sustainable transportation future.

The nation’s only privately-owned and operated intercity passenger railroad in the United States, Brightline, has serviced West Palm Beach since 2018, removing an estimated 72,000 metric tons of carbon dioxide emissions from the communities they serve every day.6 Additionally through a partnership with micro-transit company Circuit, the West Palm Beach Downtown Development Authority (DDA) has piloted a free shuttle service with stops between downtown and Palm Beach. This service, and the recently introduced BrightBike bike share program offered as a companion to Brightline, aim to provide convenient first- or last-mile alternatives to car travel for shorter trips, helping cut carbon emissions.

43downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association 45 Downtown City Region 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8 2 0 1 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8 2 0 1 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5 2 0 1 6 2 0 1 7 2 0 1 8 2 0 1 9 0 % 1 0 % 2 0 % 3 0 % 4 0 % 5 0 % 6 0 % 7 0 % 8 0 % Transit Walk Drive Alone DOWNTOWN PROFILE 2 Source: American Community Survey 5-Year Estimates (2010–2019) Commute Mode Share

Growing

CITYWIDE IN18-TO-34-YEAR-OLDSPOPULATIONLIVINGTHEDISTRICT DOWNTOWN WEST PALM BEACH5.4%6.8% DOWNTOWNSGROWING5%6% DOWNTOWN WEST PALM BEACH DOWNTOWNSGROWING CITYWIDE JOBS GROWTH IN EMPLOYMENTDOWNTOWN(2002–2018) 31% 24% 8% 38% 26% 34%CITYWIDE CREATIVE JOBS 24% 27%CITYWIDE KNOWLEDGE JOBS 57% 57%RESIDENTS WITH A BACHELOR’S DEGREE OR HIGHER EMPLOYMENT DOWNTOWN WEST PALM BEACH GROWING DOWNTOWNS GROWING CITY 2020 MEDIANRESIDENTSDENSITY/ACREINCOMEHOUSEHOLDDIVERSITYINDEX 98% 9 $77K 60.5 61% 9.7 $58K 59.8 21% 6.32 $61K 68.6 AVG.GROWTH2000–2019RESIDENTSANNARBORATLANTAAUSTINBOISECHARLOTTEDALLAS NORFOLKLOSLEXINGTONINDIANAPOLISHUNTSVILLEDURHAMANGELES WESTTEMPESANTASAINTSACRAMENTOPAULMONICAPALMBEACH DOWNTOWN PROFILE 2 *The compendium report is available at the IDA website, downtown.org. Average of 3% of the citywide land area; average assessed value of $8 billion (20% of citywide assessed value); accounting for:

44 IDA | The Value of U.S. Downtowns and Center CitiesIDA | The Value of U.S. Downtowns and Center Cities

Downtown Profile | Summary

Using data collected for The Value of U.S. Downtowns and Center Cities study, we identified three tiers of districts, defined by their stage of development. We divided the study districts into established, growing and emerging tiers based on the citywide significance of downtown population and jobs, density of residents and jobs within the district, assessed value per square mile, and the rate of growth in population and jobs from 2000 and 2018. These tables show how West Palm Beach compares to its peers in the growing tier and to the citywide averages for the tier. For the full set of cities by tier, accompanying data points, and methodology, please refer to The Value of U.S. Downtowns and Center Cities compendium.*

The rapid growth rate, density, and concentration of citywide resources all contribute to downtown West Palm Beach ranking as a growing downtown in our analysis. Typically, growing downtowns have lower citywide significance in terms of jobs and population (averaging 24% of the city’s jobs and 5% of population), but have medium-high density and are making progress toward the established tier. With 31% of the city’s jobs and 5.4% of its population, downtown West Palm Beach exceeds the targets of IDA’s Value of U.S. Downtowns and Center Cities study for downtowns in the growing tier and easily ranks as one of the highest-performing and most contextually valuable downtowns in this tier of rising stars. One of downtown’s greatest strengths has been its ability to attract new residents, which has contributed significantly to its vibrancy. Its residential population grew nearly 100% between 2000 and 2019, outpacing other growing downtowns by almost 40%. Using the latest data available, we can estimate that this growth trend will continue, and as of 2021 downtown is home to nearly 10,000 people—more than three times as many residents as two decades ago. With more residents living downtown today than at any point in the history of West Palm Beach, downtown now houses the growing tier-standard of approximately nine residents per acre, nearly three times as many residents per acre as the city and eight times as many as the region. Despite having a median household income of $77,574— approximately $20,000 more than other downtowns within Downtowns

45downtown.org | © 2021 International Downtown Associationdowntown.org | © 2021 International Downtown Association the growing tier—downtown West Palm Beach has managed to grow equitably thus far, keeping room for lower-income households. With a 60.5 Diversity Index rating, which exceeds the average for growing downtowns, downtown shows itself to be diverse in its residential population. Residents of downtown are also highly educated, with a tierstandard 57% attaining a bachelor’s degree or higher. Despite its strong residential growth, downtown has been outperformed by other growing downtowns in employment growth. With the size of its workforce increasing only 8% between 2002 and 2018, downtown falls 30 points behind other growing downtowns that have averaged 38% growth within the same period. It also lags behind its peer cities in its share of both knowledge jobs and creative jobs, measures that are used to assess the quality of a district’s jobs. Despite having nearly one-in-three of the city’s jobs, downtown has also been outpaced by the city and the region in terms of employment growth, which stands to dilute the citywide value of downtown’s labor market. Further gains in this area will help downtown make progress towards the established Intier.other areas, downtown has clear strengths that see percent-of-citywide figures approach tier averages.

78 81 56 BIKE SCORE DOWNTOWN WEST PALM BEACH 83 GROWING DOWNTOWNS 87 GROWING CITIES 45 WALK SCORE DOWNTOWN WEST PALM BEACH 25% GROWING DOWNTOWNS 29% GROWING CITIES 11% SUSTAINABLE COMMUTE DOWNTOWN PROFILE 2 $291M12%% RETAILRETAILCITYWIDESALESSALES PER SQUARE MILE $302M10% DOWNTOWN WEST PALM BEACH DOWNTOWNSGROWING 2,9755HOTELHOTELSROOMS 3,96818 DOWNTOWN WEST PALM BEACH DOWNTOWNSGROWING

Downtown retail sales make up a larger share of citywide retail sales in downtown West Palm Beach than they do in average growing downtowns, and with $291 million in annual sales per square mile, downtown comes close to the tier standard. Even though downtown has fewer hotels than most growing downtowns, it contains nearly 60% of all hotel rooms in the city, an impressive share by any standard. Downtown is also making noteworthy strides in sustainability, introducing new alternatives to car commuting in a city heavily dominated by the automobile. This will help improve the measures used to evaluate a district’s environmental resilience, which fall slightly behind the averages for tier cities but are enough within range that even small improvements could make a big impact.

aAPPENDICES

BIBLIOGRAPHYSOURCESADDITIONALDATABENEFITSPRINCIPLESMETHODOLOGYPROJECTANDSOURCESIDA

• How do downtowns strengthen their regions?

• How does a downtown’s diversity make it inclusive, inviting, and accessible for all?

Guiding questions for this project included:

What stands out about land values, taxes, or city investments?

• How can downtowns measure their distinctiveness, cultural and historical heritage?

• Can we standardize metrics to calculate the value of a downtown?

• What inherent characteristics of downtown make it an anchor of the city and region?

48 IDA | The Value of U.S. Downtowns and Center Cities

BACKGROUND In 2017, IDA launched the Value of U.S. Downtowns and Center Cities study. IDA staff and the IDA Research Committee worked with an initial group of 13 downtown organizations, Stantec’s Urban Places as a project advisor, and HR&A as an external consultant to develop the valuation methodology and metrics. Since 2017, IDA has added another 30 downtowns or urban districts to the study database, and worked with their respective urban place management organizations (UPMOs) to collect local data, obtain data from agencies in their cities, and combine these metrics with publicly available statistics on demographics, economy, and housing. Data collected included publicly available census figures (population, demographics, employment, transportation), downtown economic performance, municipal finances, capital projects, GIS data, and the local qualitative context. The 43 downtowns and urban districts studied to date represent diverse geographic regions and have relatively comparable levels of complexity and relationships to their respective cities and regions.

• What is the economic case for downtowns?

a APPENDICES

Project Framework and Methodology

• Due to its mix of land-uses, diversity of jobs, and density, is downtown more socially, economically, and environmentally resilient than the rest of the city and region?

Appendix I:

• Standardizes key metrics for evaluating the economic, social, cultural and environmental impacts of American downtowns.

• Provides individual analysis and performance benchmarks for participating downtowns in this standardized framework, including supplemental qualitative analysis.

• Empowers and continues to support IDA members’ economic and community development efforts through comparative analysis.

49downtown.org | © 2021 International Downtown Association a APPENDICES

VIBRANCY IDENTITY ECONOMYRESILIENCE INCLUSION THE FIVE PRINCIPLES

PROJECT PURPOSE The project measured the performance of U.S. downtowns using metrics developed collaboratively and organized under five principles that contribute to a valuable urban center. This study:•Provides a framework of principles and metrics to guide data collection for evaluating the value of downtowns and center cities.

• Develops an industry-wide model for calculating the economic value of downtowns, creating a replicable methodology for continued data collection.

The study team sought arguments that would appeal to multiple audiences and worked to identify metrics that could support multiple statements about downtown value. The workshop identified these value statements:

DETERMINING PRINCIPLES FOR A VALUABLE DOWNTOWN

This project began with a Principles and Metrics Workshop held in 2017 with representatives of UPMOs from the 13 pilot downtowns. The workshop focused on developing value principles that collectively capture a downtown’s multiple functions and qualities, and its contributions to the city and region. They identified five principles that became the organizing framework for determining benchmarking metrics.