2022 FINANCIAL LITERACY SUPPLEMENT • OCTOBER 13, 2022 PRESENTED BY CONTRIBUTING SPONSORS Financial Literacy 101: A Basic Guide to FINANCIALFREEDOM

In Memoriam

Calvin W. Rolark, Sr. Wilhelmina J. Rolark

THE WASHINGTON INFORMER NEWSPAPER (ISSN#0741-9414) is pub lished weekly on each Thursday. Periodi cals postage paid at Washington, D.C. and additional mailing offices. News and ad vertising deadline is Monday prior to pub lication. Announcements must be received two weeks prior to event. Copyright 2016 by The Washington Informer. All rights reserved. POSTMASTER: Send change of addresses to The Washington Inform er, 3117 Martin Luther King, Jr. Ave., S.E. Washington, D.C. 20032. No part of this publication may be reproduced without written permission from the publisher. The Informer Newspaper cannot guarantee the return of photographs. Subscription rates are $45 per year, two years $60. Papers will be received not more than a week after pub lication. Make checks payable to:

THE WASHINGTON INFORMER 3117 Martin Luther King, Jr. Ave., S.E Washington, D.C. 20032

202 561-4100

202 574-3785

www.washingtoninformer.com

Denise Rolark Barnes

STAFF

D. Kevin McNeir, Senior Editor

Ron Burke, Advertising/Marketing Director

Shevry Lassiter, Photo Editor

Lafayette Barnes, IV, Editor, WI Bridge DC

Jamila Bey, Digital Content Editor

Austin Cooper, Our House Editor

Desmond Barnes, Social Media Stategist

ZebraDesigns.net, Design & Layout

Mable Neville, Bookkeeper

Angie Johnson, Office Mgr./Circulation Angel Johnson, Admin. Asst.

Kayla Benjamin, (Environmental Justice Reporter) Stacy Brown (Senior Writer), Sam P.K. Collins, Will Ford (Prince George’s County Editor), Curtis Knowles, Brenda Siler, Lindiwe Vilakazi, Sarafina Wright, James Wright

Shevry Lassiter, Photo Editor, Roy Lewis, Jr., Robert R. Roberts, Anthony Tilghman, Abdula Konte, Ja'Mon Jackson

Wells Fargo has an incredible opportunity to make an impact on the lives of millions of customers every single day. We’re in the business of empowering customers to achieve their dreams. And as we do that work, we’re deeply focused on ensuring that the door to opportunity is open to all on an equitable basis.

am honored to lead the Wells Fargo Home Lending Diverse Segments team. Our group leads the Home Lending team’s strategy to increase opportunities for low-to-moderate income and multi-cultural homeowners and buyers. I believe deeply in this work and appreciate, every day, the opportunity our team has to make an impact on the lives of our customers and the communities we serve. Owning a home, after all, is one of the most important pathways to intergenerational wealth creation. The steps we take as individuals, as a company, and as an industry can play an important role in making homeownership – and all the benefits it entails – more equitable.

Throughout this supplement, leaders from across Wells Fargo share commentary about the work we’re doing to help our customers achieve their goals and promote racial equity in all of the work we do. That means more than just helping today’s customers thrive – it’s also about doing what we can to pave the way for wealth creation across generations.

Whether it’s buying a home or estab lishing a trust, the actions we take to day to support our customers can have impacts that resonate through the years for future generations. Taken together, these steps can make a real contribution to reducing the racial wealth gap and advancing equity across the financial system.

Large financial institutions like Wells Fargo are uniquely positioned to move the needle on issues of financial inclu sion. I believe that we’re making great progress – and that we can do even more when we work together. We’re committed to doing all we can to make an impact both through our own actions and through our efforts to drive collab oration across the industry in pursuit a shared belief in building a financial sys tem that works for all. g

Throughout this supplement, leaders from across Wells Fargo share commentary about the work we’re doing to help our customers achieve their goals and promote racial equity in all of the work we do.

One of the crown jewels of his torical insight can be found in the commonsense approaches African Americans made towards financial growth and stability against ag gressive contrary forces following Emancipation. In addition to es tablishing entire towns and cities across the country, these newly en franchised Americans established financial institutions, including banks that promoted self-determi nation and independence.

Today, many African Americans lack a clear understanding of the nation’s financial systems, institu tions, and policies – and even less clarity about how their own mon ey operates within them. n 2018, just one-third of Americans could correctly answer at least four out of five financial literacy questions on concepts such as mortgages, interest rates, inflation, and risk, according to a 2018 study by the Financial Industry Regulatory Au thority (FINRA). The disparity is greatest among African Americans. According to the 2022 TIAA In stitute-GFLEC Personal Finance Index, African Americans answered an average of 37 percent of the study’s financial literacy questions correctly, whereas white Americans answered an average of 55 percent of questions correctly.

So, what happened in the last century that seems to have erased such economic strength?

Remember, whether it was a few pennies at a time earned by washer

North Carolina Mutual Life Insurance Company founders, John Merrick, Charles Clinton Spaulding, Dr Aaron. M. Moore. (Courtesy of NC Mutual )

women or the salaries of hard-work ing Pullman Porters, money held by African Americans found its way into savings clubs, investment opportunities, benevolent societies, and the actuaries that generated wealth for successive generations. Said plainly: African Americans took time to learn how the nation’s financial systems worked and then made those systems work for them.

One great example was The North Carolina Mutual Life Insur ance Company, founded in 1898. Its goal of uplifting Black families by insuring policyholders against accidents and death, also included providing expert financial literacy programs for Black communities. The success of this mutual enter prise was a tremendous source of pride for African Americans in Durham and across the country.

Its Mutual Thrift Club Policy targeted children as a monetary benefit as well as a financial literacy plan. An ad from their 1940 cam paign reads: “Most children need

The Bowser Administration is committed to providing information about student loans to District borrowers and their parents as they prepare for college. The Student Loan Ombudsman ensures that student loan servicers comply with the law and treat borrowers fairly. The Ombudsman educates District residents about their student loan and repayment plan options.

The Ombudsman conducts outreach events and offers one-on-one office appointments to address your student loan concerns.

202.727.8000 | DCLoanHelp@dc.gov disb.complaints@dc.gov DISB.dc.gov/studentloanhelp

DC Department of Insurance, Securities and Banking, 1050 First Street NE, Suite 801 Washington, DC 20002

available resources

college funding

Public Service Loan Forgiveness

Student loan consolidation

Student loan repayment options

student loan default

and report scams

complaints with student loan servicers

lessons in THRIFT and practical knowledge about the advantage of a systematic long-range SAVINGS PLAN. If you have young sons or daughters, give serious consider ation to starting them off RIGHT with Life Insurance… ‘What gift has Providence bestowed on man that is so dear to him as his chil

Like North Carolina Mutual Life Insurance Company, The Washing ton Informer is dedicated to pro viding the tools Black communities need to move forward successfully in an increasingly challenging fi nancial environment. We believe that the greatest lessons and assets

have roots in the past, so we are reaching back to retool our read ers with basic information about economics and finances. We invite you to use this supplement as a quick reference to financial terms, policies, and resources.

Read, Learn, Grow.

Brandi McLean believes that people need financial skills to survive. That’s why she’s made it her mission to ed ucate people about it. McLean, an accountant in Virginia, participated in the nonprofit Society for Financial Ed ucation & Professional Development’s (SFE&PD) Student Ambassador Pro gram, which trains college students to teach their peers about personal finance. Thirty-four historically Black colleges and universities (HBCUs) participate in the program, including Bowie State University, McLean’s alma mater and the first HBCU established in Maryland in 1865.

“If I could describe the program in one word, it would be ‘necessary,’” McLean said. “Personal finance is not discussed in everyday school, and stu dents need it to adapt as adults.”

The Wells Fargo Foundation is the largest funder of the Student Ambas sador Program, providing more than $1 million in grants since 2017. This is one way Wells Fargo is working with HBCUs to empower Black students, who disproportionately face greater financial challenges that impact finan cial growth and wealth creation.

Too many college students graduate without the financial skills needed to navigate complex financial decisions and climb the economic ladder, and this issue disproportionally impacts African American, Black, and other students of color. HBCUs are known for helping generations of Black peo ple achieve academic and professional

success, making them ideal collabora tors in tackling these issues.

Student ambassadors lead financial workshops on campus and at commu nity outreach events to help their peers build financial capabilities in money and credit management, student loans, budgeting, savings, planning for life af ter college, and more. Business school professors and SFE&PD represen tatives mentor ambassadors to create their own lesson plans and interactive activities.

As a creative example, McLean and fellow ambassadors at Bowie State performed a skit about the terms and conditions of a loan. At anoth er school, ambassadors taught their peers about budgeting by relating it to a spring break trip. Ambassadors also integrate resources from Hands on Banking®, Wells Fargo’s free, non commercial online learning program offering money management lessons and resources in English and Spanish, into their sessions.

You can read more about the Stu dent Ambassador Program in this Wells Fargo Stories article: https://stories. wf.com/financial-health-is-foundation al-to-everything-we-do-with-hbcus/

In a complementary effort, the Wells Fargo Foundation collaborated with the HBCU Community Devel opment Action Coalition to develop and launch Our Money Matters, a $5.6 million comprehensive financial wellness initiative. Our Money Matters is developing, supporting, and scaling access to financial education and sound financial practices for students at HB CUs and Minority Serving Institutions (MSIs), as well as customers of minori ty depository institutions (MDIs).

The initiative aims to equip more than 35,000 students and communi

It’s an exciting and hopeful time,

probably have questions

First Home®

is a great place to start.

This site was designed with your home financing needs in mind: You can check your credit score, find out your debt level, review your savings, and more with just a few clicks. Knowing where you stand financially makes it easier to plan next steps. You can also tackle any areas that might need improvement.

From start to finish, we’ll work with you. Because a home is more than just four walls. It’s where the celebration of the present meets the promise of the future.

To learn more,

to

Whether you’re eyeing the latest model car or an outfit that is beyond your budget, experts say it’s important to think about how decisions will im pact the next generation.

Cecil Burrowes, Senior Vice Pres ident of Diverse Customer Segment Mass Market Strategy with Wells Fargo, spoke with the Washington Informer about building generational wealth and how financial decisions made today can have an impact on generations to come. He added that protecting assets can contribute to reducing the racial wealth gap.

“Understanding that when we talk about generational wealth, wealth meets a myriad of qualifications. When we mention wealth, people disqualify themselves. Wealth can be your check-to-check living. Wealth can be the savings you have in your piggy bank,” Burrowes said adding that people need to eliminate fear when having conversations about wealth. “We think it’s something

that doesn’t necessarily speak to us.”

Burrowes said, he wants people to re alize that a portion of their income and assets can take care of daily expenses, but they can also make their disposable income work for them.

“Individuals making ends meet still have disposable income and have to fig ure out how it moves to the next level,” he said. “What is the thing that you can get to work for you and your legacy?”

“The challenge is that when we lose a generation, each new generation starts at zero,” he said. “Without the proper education and the awareness of tools that are available to individuals to over come that, we keep falling in that con sistent trap over and over again.”

Burrowes said Wells Fargo is focused on ensuring everyone has access to all of the available resources.

“I think we have to be intentional. With intentional focus, we can ulti mately help more customers from a wealth transfer perspective,” he said.

In addition to educating families on transferring wealth, earlier this year, Wells Fargo committed $210 million

Sustainable homeownership rep resents one of the most important pathways to wealth creation – not just today, but also for generations that follow. But systemic inequities in the United States have prevented too many minority families from achiev ing their homeownership and wealth building goals for too long.

As the one of the nation’s leading originators of home loans, we have an opportunity to develop solutions to close the gap – both through our own work and the actions we take to lead the industry in a collective focus on closing the racial homeownership gap.

The hurdles that stand in the way of homeownership have been present for decades. Amid renewed focus on racial justice nationwide, housing stakeholders are doing more to uti lize solutions that reach beyond the

baseline framework of the housing finance system.

Special Purpose Credit Programs (SPCPs) represent an “outside the box” approach to advancing equity in homeownership. Under Federal law, lenders are permitted to deploy SPCPs to expand access to credit for

to advancing racial equity in home ownership. The initiative includes the creation of a Special Purpose Credit Program to help refinance the mort gages of minority homeowners with a Wells Fargo Mortgage. The purpose is to lower mortgage rates and reduce costs of refinancing, according to a press release from the bank.

In an effort to broaden community outreach, Wells Fargo will also expand its partnerships with the National Urban League and Unidos US. The

company will provide homebuying readiness and counseling, and work to eliminate systemic obstacles that prevent many Black and Hispanic cus tomers from becoming homeowners.

The company will also use $60 million to fund partnerships to im plement plans to address the root causes of homeownership gaps through the “Wealth Opportunities Restored through Homeownership” (WORTH) grants. The program is ex pected to support 40,000 homeowners of color in eight markets through 2025.

“Homeownership is a key pillar of the American dream. It represents a means of intergenerational wealth,” Burrowes said.

Wells Fargo has long been a leader in the housing finance industry. Be tween 2017 and 2021, Wells Fargo has helped more than 425,000 Black and Hispanic families achieve their home ownership goals with $110 billion in fi nancing, according to the press release.

But with that, Burrowes said the company wants to ensure homeowner ship is sustainable, and that customers

have the tools and resources they need to transfer their wealth.

It’s important to have a plan in place so you can ensure what you’ve built during your lifetime can be passed to the next generation. Planning is a key to ensuring that you’re able to make a proper handoff when the time comes.

When making the plan, Burrowes said, the first step is having conver sations with other family members. Those can be difficult conversations, but they are important in the planning process. Once those conversations have occurred, depending on your needs, you can use self-service tools, or contact an estate attorney to help de fine how to move forward.

Most importantly, consumers need to complete the process. Many people start the planning but fail to complete it for a number of reasons, Burrowes said, adding that some hesitate with the price of final planning.

“There is a cost associated with plan ning, but it far outweighs the probate costs,” he said.

g

groups who may have been under served in the mortgage market, im pacting their ability to build wealth through homeownership. SPCPs ar en’t new, but they’re being used with greater frequency as lenders work to create more equitable access to home ownership.

At Wells Fargo, we’re excited to add to our longstanding commitment to minority homeownership through the launch of our own SPCP. Wells Fargo announced a new initiative to advance racial equity in homeowner ship this spring. The initiative centers on the launch of a new SPCP to help eligible minority homeowners whose mortgages are serviced by Wells Fargo lower their interest rates and reduce their monthly mortgage payments without extending their current loan term.

The program has launched for eligible Wells Fargo customers with Veterans Administration and Federal Housing Administration loans. We plan to launch an SPCP for select customers with Government-Spon sored Enterprise (GSE) loans later this year, and a program for purchase loans is in development.

We’re excited about the new pro gram, which adds to products like the Dream. Plan. Home.SM mortgage (available nationwide) and closing

cost credit (available in 18 markets)— two existing Wells Fargo offerings aimed at helping low-to-moderate income borrowers. We’re also enthu siastic about working across the sec tor to foster collaboration in pursuit of a shared belief in homeownership.

Wells Fargo plays a leadership role in Project REACh – a govern ment-led working group dedicated to promoting economic access and affordable homeownership. We are a strong supporter of the SPCP “tool kit” developed by the National Fair Housing Alliance and Mortgage Bankers Association to help other lenders navigate the complex process of launching their own SPCPs.

We also work extensively with non profit organizations, and our head of Home Lending, Kristy Fercho, is the 2022 chair of the Mortgage Bank ers Association. During her time as chair, Kristy launched the Home for All Pledge, which represents the in dustry’s long-term commitment on a sustained and holistic approach to address racial inequities in housing.

Advancing racial equity in home ownership is essential to meaning fully tackling the racial wealth gap. Exciting work is underway in pursuit of this goal across the housing finance sector, and Wells Fargo is proud to do our part to lead the way. g

CONTINUED FROM PAGE FS4

ty members with financial capability skills, personalized tools for managing finances and student loans, and access to support services like career closets and emergency financial assistance. Since it began in 2021, Our Mon ey Matters has engaged 17 HBCUs/ MSIs, with thousands of students and community residents using the resources on its platform.

For over 11 years, Wells Fargo has invested more than $32 million in scholarships and programing to HB CUs via UNCF, the Thurgood Mar shall College Fund (TMCF), and the Jackie Robinson Foundation. Wells Fargo funds programs like TMCF’s Leadership Institute, which develops students’ leadership skills, and UN CF’s Empower Me Tour, which helps students prepare for college and their careers. Additionally, Wells Fargo’s virtual learning program, the Beyond College Webinar Series – covers a wide variety of topics for HBCU students from personal finance to professional development.

Through our work with nonprofit partners who bring a deep under standing of HBCUs, we aim to help equip the next generation with the financial knowledge, tools, access, and opportunities to close the racial wealth gap. g

Coppin State University has received a multi-year grant from Schwab Advisor Services, in part nership with the Charles Schwab Foundation to develop programs in financial planning and wealth man agement, that will lead to meaning ful impact in the lives of Coppin students in Wealth Management, the Registered Investment Advisor (RIA) Industry, and the surrounding community.

The considerable grant to Cop pin State University, a historically Black public anchor institution in West Baltimore, Maryland, will es tablish registered financial programs for Certified Financial Analysts or Certified Financial Planners. The programs will provide faculty de velopment and curriculum that will produce education pathways for students to explore careers in wealth management, establish a communi ty-focused center, as well as create a Minority Registered Investment Ad visor Mentorship Program.

“The future of financial services is wholly dependent on young pro fessionals entering the space and re flecting the diversity of tomorrow’s investors. We are grateful to join Coppin State University in its mis sion to help students explore careers in financial services, particularly the RIA industry, which is all about people serving people and their lo cal communities,” said Bernie Clark, head of Schwab Advisor Services.

“We are excited to develop this partnership with the Charles Schwab Foundation, and deeply appreci ate their belief in our mission and vision to become a major player in the financial education and services landscape. As two, well-respected institutions, we look forward to a

long-term partnership with Charles Schwab as we collaborate to diver sify and improve the wealth gap in underrepresented communities,” said Coppin State University Presi dent, Anthony L. Jenkins.

“We are thrilled to be able to launch this very significant program that will introduce various aspects of finance to our students and to the community, which will ultimately increase the diversity in the indus try. The launching of this program is timely as it coincides with excite ment around the College of Busi ness move to its new building which is currently under construction at the heart of campus,” said Dean of the College of Business, Dr. Sadie Gregory.

The grant will also provide Cop pin an opportunity to host an annu al Closing the Wealth Gap summit on the campus and scholarships to Coppin students.

“This is the largest gift that the University has received, to date,” said Vice President for Institutional Ad vancement, Joshua Humbert. “We couldn’t be happier to work with the Charles Schwab Foundation in this partnership. We’ll be able to help our students get a bit of an edge in being prepared for careers in the fi nance industry while addressing the wealth gap that exists in our society and provide real-time solutions,”

The partnership will bring more diversity to the financial services industry where, currently, 76.3 percent of finance professionals are white, and 68.8 percent are men. This partnership will aid Coppin State University in grooming the next generation of students and community members, as they mas ter the financial landscape and nur ture community, financial health, and insight. g

Center for Financial Inclusion has designed a suite of services that puts you in the driver's seat to build a secure financial future. Our Center is a pathway for you to take control of your wealth building by redefining and powering up

relationship

money.

highly interactive classes and coaching sessions were created with you in mind. Connect with us and jumpstart your journey to financial freedom!

By Lee Ross WI Staff Writer

By Lee Ross WI Staff Writer

ability to

The interest rate is the amount a lender charges a borrower and is a percentage of the principal—the amount loaned. The interest rate on a loan is typically noted on an annual basis known as the annual percentage rate (APR).

A cash reserve that’s specifically set aside for unplanned expenses or financial emergencies. Some common examples include car repairs, home repairs, medical bills, or a loss of income.

Disposable income, also known as disposable personal income (DPI), is the amount of money that an individual or household has to spend or save after income taxes have been deducted. At the mac ro level, disposable personal income is closely monitored as one of the key economic indicators used to gauge the overall state of the economy.

A plan that outlines what money you expect to earn or receive (your income) and how you will save it or spend it (your expenses) for a given period of time; also called a spending plan.

An open-ended loan that allows you to borrow money up to a cer tain limit and carry over an unpaid balance from month to month. There is no fixed time to repay the loan as long as you make the min imum payment due each month. You pay interest on any outstanding credit card loan balance.

A summary of your credit activity and current credit situation such as loan paying history and the status of your credit accounts. Lenders use these reports to help them decide if they will loan you money and what interest rates they will offer you. Other businesses might use your credit reports to determine whether to offer you insurance; rent a house or apartment to you; or provide you with cable TV, Internet, utility, or cell phone service. If you agree to let an employer look at your credit report, it may also be used to make employment decisions about you.

Consolidation means that your various debts, whether they are credit card bills or loan payments, are rolled into a new loan with one monthly payment. If you have multiple credit card accounts or loans, consolidation may be a way to simplify or lower payments. But a debt consolidation loan does not erase your debt. You might also end up paying more by consolidating debt into another type of loan.

Interest rates are getting the best of us these days, it seems. The mortgage scenario of a year ago is a total budget blowout now. Homebuyers could use some ideas on how turn the tables on mortgage rates where possible.

While nobody will be partying like it’s 2021, I have a few ideas. I have been around a while, and these almost seem like blasts from the past given the low rates of the past few years. But discount points, adjustable rate mortgages, and now the coming increase in conforming loan limits are all po tential paths to lower a mortgage payment. (I also have a credit re porting insight at the end of the article for current renters.)

Paying a lender to lower the rate? Sounds painful. However, it could make sense now that mort gage rates are higher. A point is simply one per cent (1%) of the loan amount. On a $400,000 loan, for example, paying one dis count point to buy down the in terest rate would cost $4,000.

Four thousand dollars is not nothing. So, why do it?

Because it can lower the inter est rate by .375% to .5%, saving hundreds per year. On that same $400,000 loan, the discount point will be recouped in 2.5 years. Meanwhile, the lower payment is happening right now (and as long as one has the loan). Even better, sellers and builders can help pay closing costs, including discount points. Be sure to talk to a realtor about sellers concessions before hand.

ARMs typically have lower in terest rates than fixed-rate loans,

providing a more affordable option upfront. With the lower initial rate, one may be able to afford more house than with a fixed-rate loan.

The rate is fixed only for the initial term. Before entering into an ARM, a borrower should feel confident they can either meet the obligation, refinance, or sell the home before any reset. ARM rates adjust after the initial period agreed upon – generally 3, 5, 7, or 10 years. ARMs also have different caps, or limits, on the periodic rate changes. Knowing the adjustment caps can make a difference since most ARMs that are offered have caps of either 1, 2, or 5%. (Imag ine your interest rate going up by 5% next month!)

Increased buying power is roll ing out this fall. Fannie Mae and Freddie Mac conforming loans generally have lower interest rates and are less difficult to qualify for, as opposed to jumbo loans for higher loan amounts. Kudos to Fannie Mae and Freddie Mac for keeping pace with home prices in high-cost areas.

The 2023 conforming loan limit was recently revealed at $715,000 for one-unit properties in the Washington, DC Area. A potential game-changer for some, mortgages at the increased limits are available now at some lenders, including EagleBank. Super-conforming loan limits will adjust, too, allow ing even more borrowers to fit into non-jumbo categories.

Keeping an eye on the news for 2023 loan limits can help in plan ning for home purchase, especially for those who do not seek to go through jumbo loan underwriting.

Taking the sting out of mort gage rates is not a given. Not ev eryone will be able to buy down a rate or feel comfortable entering

into an adjustable rate mortgage. Neither will everyone will be able to stretch their buying power with new limits on conforming loans. The DMV is a high-cost area to begin with. If someone is in a posi tion to buy a home, chipping away at the rate is not a bad idea and may be accomplished by talking options with a lender.

For years, rental payments have not been included in the major cred it bureaus’ scoring model. This is a problem. A lack of credit, or poor credit, can disqualify a borrower from obtaining a home loan or other type of loan. Landlords do not have to re

Community Banking

port rental history, which is a shame. However, it is possible through vari ous subscription services.

Renters are hereby encouraged to check with their property man agers to see if their building is enrolled in any of the reporting services. If not, individual rent-re porting services (for a fee) will also get some bureaus to reflect positive rental payments.

Maceo Clark (NMLS# 807001) has extensive experience in the mort gage industry as a community lender and loan originator. Maceo who can be reached at MClark@EagleBank Corp.com or 301-850-2655.

As a community bank, EagleBank offers knowledge of Home Buyer re

sources, as well as refinance services. Contact us at HomeLoans@Eagle BankCorp.com.

This is not a commitment to lend. To be eligible, buyer must meet min imum down payment, underwriting and program guidelines. All loan applications are subject to credit and property approval. Property taxes, flood and/or property hazard insur ance may be required. This informa tion is for educational purposes only and is not to be taken as guidelines or guarantees to improve your credit or financial situation or eligibility to secure a home loan. EagleBank is an Equal Housing Lender. Eagle BankCorp.com/mortgages (NMLS# 440513) g

use

Maceo

The time is not only approach ing to make a list and check it twice, but tis the season to practice discipline with your spending and write down your goals. In addition, to decking the halls, it’s important to check the four walls this hol iday season,

said Presley Nelson, a branch manag er at Chase.

“The four walls are home, trans portation, utilities, and food. Those are the things you want to make sure are in order and once they are in or der you know what extra money you have,” Nelson said.

The key to avoid overspending during this holiday season is to have discipline.

“Discipline is a way to not spend all of your money, especially in your savings. A lot of times we use our emergency fund and that’s only sup posed to be for emergencies. If your car breaks down or you have to fix something in the house, that’s an emergency.”

One way to practice discipline is write out your budget to see where you can save extra money. Once you have that number Chase offers a dig ital tool called, Autosave. Autosave allows you to create an automatic savings goal. Which can be especially helpful for holiday spending.

Nelson also said that avoiding un necessary spending requires a mental ity shift. “You have to own that you don’t want to overspend. It’s a choice we can make a choice to go to work, we can choose to spend,” Nelson said. We can choose to do everything and anything. Once you stay within your guidelines you won’t overspend. That goes into creating barriers.”

With a budget builder, spending is itemized so consumers can see what they’re spending money on.

Nelson said another way to control spending is by using a check ledger.

“This is going to sound very old school, but the check ledger is your friend. A lot of times we depend on the mobile app and online banking, but if you have a pending transaction you may think you have more money in your account than you do. This is how people can easily go into over draft.”

Nelson also cautions about credit card usage during the holidays.

“Sometimes people think it’s free money. It’s not. You get a limit, but you have to make sure you don’t go over that limit,” Nelson said, adding that credit card balances should be paid off monthly. “Be responsible with your credit cards. The holiday season is credit card season, and if you’re going to get a credit card be responsible. if you’re not able to pay the balance in full every month, the balance starts to build up and you’ll end up in debt. If you’re not able to cover your statement balance don’t use credit cards.”

Nelson advises consumers to delay instant gratification and really think about purchase.

“We have to be mindful of our spending,” Nelson said as he gave the following scenario.

Tirzah Farley, a 26-year-old Gal laudet University student who re cently took a financial health work shop, said budgeting is the key to staying on track this holiday season.

“A budget builder is the best way to save knowing people typically spend more around this time period. Budgeting is one of the important skills to have in our daily life,” Farley responded through email.

“If you go get breakfast from Star bucks every day, that’s about $5 or $6 for a cup of coffee. A breakfast sand wich is another $5. You have spent $12, and you haven’t even eaten lunch. Lunch is $15. You’re at $27 a day. That’s $135 a week. You can ac tually go to a grocery store, meal prep for $50, have lunch for two weeks and put the rest of the money in sav ings,” Nelson said. g

One way to practice discipline is write out your budget to see where you can save extra money. Once you have that number Chase offers a digital tool called, Autosave.5 Tirzah Farley, a 26-year-old Gallaudet University student 4 Presley Nelson, a branch manager at Chase.

Buying a home is one of the most important purchases you will make in your lifetime, and the pressure is mounting for those looking to buy right now, with home prices fluctuat ing and mortgage rates at their high est levels in over a decade.

While existing home sales have fallen month-over-month since the beginning of the year, prices still hit a record high above $400,000 in May, according to the National Associa tion of Realtors, as low levels of hous ing inventory and supply chain con straints have created an affordability squeeze for homebuyers. Mortgage rates have nearly doubled in the last six months – from 3% in 2021 to close to 6% in 2022 – making it increasingly challenging for many Americans to purchase a home, espe cially for those with limited income.

So, how do you know when you’re ready to buy a home? More impor tantly, how much home can you af ford? We sat down with Justin Cot ton, Senior Home Lending Advisor at Chase, to answer those questions and discuss what the current state of the market means for you and your family’s homebuying dreams.

Q: What are the main factors mortgage lenders look at when evaluating an application?

Justin Cotton: Your credit score and debt-to-income ratio are major factors in the application process.

Your credit score is set based upon how you’ve used credit, or not used credit. For example, do you pay bills on time? Higher credit scores can help you qualify for the lowest inter est rates. A score at 700 or above is generally considered good.

Additionally, lenders look at your debt-to-income ratio. This is a simple equation of how much debt you have relative to how much money you make. Borrowers with a higher debtto-income ratio are considered more risky while a lower debt-to-income ratio may allow you to qualify for the best rates on your home loan.

Q: What are some tips for improv ing your credit score?

Justin Cotton: Starting with review ing your credit report to understand what might be working against you. You can also pay down your revolving credit and dispute any inaccuracies.

Additionally, there are services like Chase Credit Journey to help mon itor and improve your credit score. Credit Journey monitors all of your accounts and alerts you to changes in your credit report that may impact your score. You’ll get an alert any time Chase sees new activity, includ ing charges, account openings and credit inquiries. Chase will also notify you if there are changes in your credit usage, credit limits or balances. You don’t have to be a Chase customer to take advantage of Credit Journey.

Q: What are some factors that can affect the cost of a mortgage?

Justin Cotton: There are two basic types of mortgage interest rates: fixed and adjustable. While adjustable rates are initially low, they can change over the course of a loan, so your mortgage payments may fluctuate. Loan term indicates how long you have to pay off the loan. Many homebuyers tend to opt for a 15-year or 30-year mortgage, though other terms are available. A longer loan term generally means you’ll have lower monthly payments, but you’ll pay more in interest over the life of the loan. A shorter loan term may come with higher monthly payments, but you’ll likely pay much less in interest over time.

Potential homebuyers should con tact a home lending professional to understand and review the options available to them.

Q: What are the costs of homeownership beyond the monthly mortgage payment?

Justin Cotton: People often think of the down payment and monthly mortgage, but buying and owning a home carries additional costs. Closing costs, for example, can

amount to up to 3% or more of the final purchase price. Other factors that could add on to your monthly payments are property taxes, home owner’s insurance, and homeowner’s association (HOA) fees. To get an idea of what this may look like for you, use an affordability calculator.

While there is no way for a buy er to completely avoid paying these fees, there are ways to save on them. Some banks offer financial assistance

3 Justin Cotton Senior Home Lending Advisor at Chase

3 Justin Cotton Senior Home Lending Advisor at Chase

for homebuyers. As an example, Chase’s Homebuyer Grant offers up to $5,000 that can be used toward a down payment or closing costs in eli gible neighborhoods across the coun try. There may also be homeowners’ or down payment assistance offered in your city or state. Contact a Home Lending Advisor to learn about re sources you may be eligible for. For a deeper dive into this topic, Chase’s Beginner to Buyer podcast – episode three, “How Much Can I Afford?” is a great resource for pro spective homebuyers to get answers to all their homebuying questions.

g

JPMorgan Chase is building on our investments in Washington, D.C. and around the country to help close the racial wealth gap and build a more equitable future.

As part of our commitment, we are taking actions to help improve financial health and access to banking in Black, Latino and Hispanic communities. Learn more

Winter is on the way. Just as the cold and flu season can challenge our immune systems, it can also be the time of year that creates the greatest financial strain on budgets and financ

As we increase our use of natural gas this winter—from the furnaces that heat our homes to other appliance usages—the U.S. Energy Information Administration reports that multiple factors have led to national natural gas price increases.* These include storms, fluctuations in imports/exports vol umes, changes in natural gas invento ry levels and other sudden changes in demand.

These factors have caused wide spread price fluctuations which could directly impact your gas bill and over all finances.

Understanding how gas prices are set is helpful when managing your monthly budget.

Many factors influence gas prices, but the most common are supply and demand, the price and availability of other fuels, weather variations and import/export volume. Like many energy sources, natural gas is generally subject to supply-and-demand forc es. Market prices are higher this year based on the economic recovery from COVID-19, increased natural gas demand from last winter and slower than anticipated production.

Washington Gas does not profit from the sale of gas. This means that our customers pay the same price that we do for the purchase of natural gas.

While these forces will affect this winter’s energy costs and may feel outside of your control, you do have powerful options to help manage your budget during the heating season.

When you winterize your furnace, complete an online home energy as

sessment or upgrade to high-efficiency appliances with rebates, you are mak ing your home more energy efficient. From replacing water heaters to add ing weather stripping, small changes go a long way toward lowering your energy bills. Learn more at https://wg smartsavings.com/.

With the Washington Gas Budget Plan, you pay the same amount ev ery month. Because home and water heating can be the highest utility costs, a predictable monthly utility bill can help manage expenses with less stress. Enroll at https://www.washingtongas. com/budgetplan.

You may qualify for energy assis tance programs that help offset costs and provide relief for utility bills. If you are an energy assistance recip

ient, the Installment Plan may be right for you and help manage your bills through 12-month or 24-month payment plans. These programs are available throughout our service ter ritory in Maryland, DC and Virginia and can help you through uncertain times. Visit https://www.washington gascares.com/ and https://www.wash

As we adjust to the changing weather, Washington Gas is here to help. Here’s to your good health and a bright financial future! WI

*https://www.eia.gov/todayinenergy/ detail.php?id=53579

Wendy Zelond is a finance executive with over 20 years of experience in the energy, airline and public accounting sec tors. She is currently the senior vice pres ident of finance for the utilities segment of AltaGas, which includes Washington Gas, SEMCO and ENSTAR. She is a certified public accountant and holds an MBA from the University of St. Thomas in Houston.

Throughout her career, Wendy’s pas sion for people has inspired her to devel op teams and spaces where everyone can flourish. Her love for team building and encouraging others led to her first book, We Talk, We Lead: A Reflection of One Women’s Stories to Inspire and Empower Others. She is proud to sponsor employ ee resource groups and mentor others for success. Her experience has shaped her leadership approach, along with insights from her teams, continuous self-improve ment and challenging her comfort zones.

The sooner you reach out to us, the sooner we can explore your options and

a solution for you. By working together, we can help you choose the right payment solution that fits your budget, eliminates some stress and gives you

of mind going forward.

Nearly half of your energy budget is spent on heating and cooling, and rising natural gas prices may increase your winter gas utility bills. Simple changes can help decrease energy costs. Stay safe, warm and energy-smart as temperatures drop!

• You may qualify for energy assistance programs to offset costs and provide relief for utility bills. These programs are here to help and are available throughout our service territories in Maryland, DC and Virginia. Learn more about available assistance at washingtongascares.com.

• Enroll in the Budget Plan: spread your cost of winter heating over the entire year.

TIP 1: Keep your water heater below 120°F using the warm or low setting.

TIP 2: Wash full loads of laundry and dishes, as opposed to numerous smaller loads.

TIP 3: Use cold water for laundry and specially formulated cold water detergents.

TIP 4: Caulk and weather-strip around doors and windows.

TIP 5: Change or clean furnace and air filters once a month.

TIP 6: Consider installing high-efficiency appliances when possible.

TIP 7: Look for the ENERGY STAR® energy-efficient product label when shopping for new appliances.

TIP 8: Consider purchasing a programmable thermostat that automatically lowers and increases the temperature based on when you’re home.

For more information, visit washingtongas.com or call 844-WASHGAS (927-4427).

The more you talk openly about money in your household, the easi er it will be to talk to your children about their financial futures. For tunately, there are plenty of great resources available to support you in making your family financially steady. Here are a few incentives for you.

Tiffany James, 27, started trad ing two and a half years ago and turned her initial $10,000 invest ment into $2 million. Today, she burns to pass this knowledge on. She’s the founder of Modern Blk Girl, which started as a room on the app Clubhouse to become an online community with 100,000 followers. As part of Modern Blk Girl, James is reintroducing Teen University, a 30-day course de signed to teach 14- to 19-year-olds about investing. Financial literacy rates in America are low, but they are lowest among members of Gen Z. According to a 2021 study by

TIAA, on average 50 percent of Americans couldn’t an swer more than 50 percent of TIAA’s financial literacy quiz. For Gen Z this jumps to two-thirds, even though Gen Z is more likely than any other generation to have exposure to financial literacy classes. g

The Jumpstart Coalition for Financial Literacy is a free clearinghouse of publications, games, teaching plans, and other resources designed to teach financial responsi bility.

SaveAndInvest.org is a project of the FINRA Investor Education Foundation. It offers free, unbiased resources dedicated to improving people’s financial health.

Moneytopia is a free immersive game helping teens learn more about managing their money while having fun online. There is also a page of short video guides for teaching your teen more about topics including the power of compound interest and how much apartment living will cost.

FamZoo is an award-winning app acting as a private family banking system. It’s designed to help parents teach kids to earn, save, spend, and donate money wisely in a safe, friendly environment.

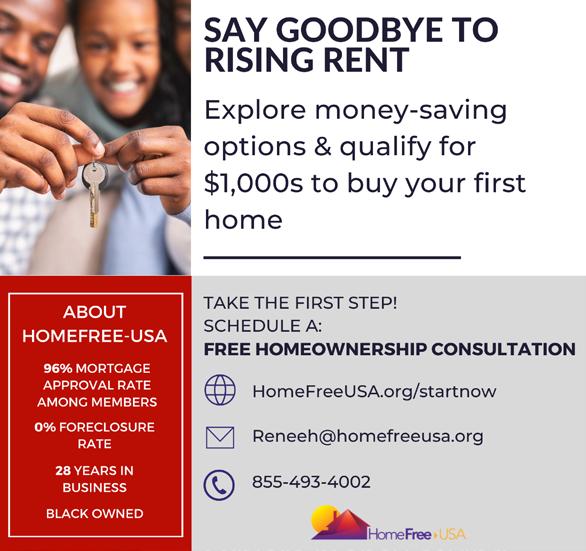

According to Freddie Mac, 3.4 million African American renters are in a position to buy a home.

So, why aren’t we, in larger num bers, with homeownership as one of the foundational steps to build ing wealth?

Because African Americans still face major obstacles. According to the Consumer Financial Protec tion Bureau, we are consistently denied conventional home and refinance loans at higher rates than our white counterparts.

For example, out of 108 mort gage applications filed by African Americans last year, one of Mary land’s largest banks approved only 20 (19%) and denied 69 (64%).

Another 19 (18%) “fell out” of the process; although clients ultimate ly got approved, they walked away from the loan, frustrated by the long, arduous process.

The numbers show the deck is stacked against Blacks even more than others. The good news? There is a way to beat these odds, with the right partner by your side in the process.

Work with a partner such as HomeFree-USA to get approved, fast.

Over 25+ years in the housing industry, helping people of color get the financing they deserve, this is what we’ve observed: All too of ten, applicants are just a few sim ple changes away from being cred it-ready for the mortgage process.

With the right guidance, you can prepare for success and get the information you need to navigate the mortgage or refinance process quickly and easily.

By way of example, 96% of homebuyers who go through HomeFree-USA’s programs get approved on their FIRST applica tion.

You want to choose a partner who can help you build a mean ingful relationship with your lend

5 Having the right partner can help make closing on a home bring joy and happiness

er and make the process—and your life!—easier.

Here’s how to choose the right partner:

• DO seek an experienced credit counseling agency that can connect you with down payment assistance and credit preparation programs, with a proven track record of success. Ask about their process and approval rates.

• DON’T expect a “quick fix,” or confuse credit repair with credit counseling. Avoid companies that charge you high fees to “fix” your credit. (Most of these firms leave you no better prepared for the home buying process.)

• DO look for advisors willing to speak candidly with you, ask questions and give impartial ad vice you can’t get from a lender. The best advisors will explore is sues affecting your readiness, an alyze your situation, and provide solutions to improve your stand ing, which will require simple ac tions on your part.

• DO seek a counseling agency first, before talking to a lender. They can help identify issues that may cause your application to be denied before it happens—with out impacting your credit score.

• DON’T go to a lender, loan officer, or broker before consulting with a counseling partner. Finan

cial institutions are obligated to run a loan application if you ask for one, which can impact your credit.

• DO find nonprofit partners who have trusted relationships with multiple lenders and will work directly with the lender on your behalf.

You want to create a better fu ture. You’re eager to put in the work. You just need the right part ner to cut through a process that’s stacked against you.

Where to find the best credit counseling partners

Bridging the gap between finan cial strength and homeownership for people of color across Amer ica, HomeFree-USA is just one of many organizations that help aspiring homeowners prepare for a mortgage application, get ap proved, and get access to resources they might not otherwise know about.

We have a nationwide network of trusted agencies dedicated to closing

the homeownership gap for people of color and other marginalized com munities. You can also check out the U.S. Department of Housing and Urban Development for a compre hensive list of local, recommended intermediaries ready to help.

We are ready to support you to get approved for your mortgage or refinance. To begin a conversation with HomeFree-USA, contact us at info@homefreeusa.org, call 855-493-4002, or visit our web site at homefreeusa.org. g

Jessica Gordon Nembhard

Jessica Gordon Nembhard

In Collective Courage, Jessica Gordon Nembhard chronicles African American co operative business ownership and its place in the movements for Black civil rights and economic equality. Not since W. E. B. DuBois Economic Co-operation Among Negro Americans in 1907 has there been a full-length, nationwide study of African American cooperatives. Collective Courage extends that story into the twenty-first century and includes the experiences of DuBois, A. Philip Randolph, the Ladies’ Auxiliary to the Brotherhood of Sleeping Car Porters, Nannie Helen Burroughs, Fannie Lou Hamer, Ella Jo Baker, and the Black Panther Party. Adding the cooperative movement to Black history results in a retelling of the African American experience, with an increased un derstanding of African American collective economic agency and grassroots economic organizing.

Sabrina Lamb

Sabrina Lamb

Youth financial education is an urgent issue, and author Sabrina Lamb believes that African American parents first must reeducate themselves about finances to make sure the next generation does not fall into the spending trap that can be a family legacy. The lack of a healthy financial education has generational impact, causing families to be financially vulnerable, squander financial resources, and fail at wealth accumulation.

By Lee Ross WI Staff WriterWith step-by-step advice and exercises for parents and young people, Do I Look Like an ATM? sets out to establish new financial behavior so children will avoid the personal economic problems that have plagued the culture. The book guides parents through self-examination of their financial habits. By performing the exercises in this book and having candid discussions, parents can, together with their children, become en gaged citizens in the world of money.

Over the past three decades, racial prejudice in America has declined significantly and many Af rican American families have seen a steady rise in employment and annual income. But alongside these encouraging signs, Thomas Shapiro argues in The Hidden Cost of Being African American, fundamental accounts, stocks, bonds, home equity, and other investments. Shapiro reveals how the lack of these family assets along with continuing racial discrimination in crucial areas like home ownership dramatically impact the everyday lives of many black families, reversing gains earned in schools and on jobs, and perpetuating the cycle of poverty in which far too many find themselves trapped.

With over a million copies sold, Economics in One Lesson is an essential guide to the basics of economic theory. A fundamental influence on modern libertarianism, Hazlitt defends capital ism and the free market from economic myths that persist to this day. Economic commenta tors across the political spectrum have credited Hazlitt with foreseeing the collapse of the global economy which occurred more than 50 years after the initial publica tion of Economics in One Lesson. Hazlitt’s focus on non-governmental solutions, strong — and strongly reasoned — anti-deficit position, and general emphasis on free markets, economic liberty of individuals, and the dangers of government intervention make Economics in One Lesson every bit as relevant and valuable today as it has been since publication.

Economic Literacy: Basic Economics with An Attitude explains the logic, language, and world view of economic theory while maintaining the engaging and accessible style that has made earlier editions so successful. While covering the funda mentals of the discipline, the author also includes a wide range of new material focusing on the struc ture, causes and results of the ‘Great Recession’. From microeconomics and macroeconomics to the composition of international and domestic econo mies, Economic Literacy also makes the key distinction between econom ics as an academic discipline and the economy as a practical reality. Using this approach, readers will be enabled to understand both current affairs and professional economics literature, making this book uniquely beneficial for students both practically and theoretically. g

Whatever our clients’ backgrounds and ambitions, we offer education and advice that empowers them to build their preferred future. We’re committed to providing extensive, personalized support to help people gain the knowledge they need to make confident financial decisions.

Better Money Habits® offers free, easy-to-understand tools, which help people make sense of their money and take action to improve their financial picture.

Learn more at https://bettermoneyhabits.bankofamerica.com

Visit us at bankofamerica.com/about.

Don’t lecture. Instead, use stories and share your experi ences. As much as you think appropriate, share your fam ily’s situation, including your budget, savings, insurance, and investments. Take money out of the closet.

Make concepts and examples relevant to their lives.

By Lee Ross WI Staff WriterWalk the talk. Kids watch what you say and do. Often the unspoken messages are the most powerful of all.

Nothing should be off the table.

Having a savings or investing account, an allowance, or making them an authorized user on a credit card all are ways to help your teen learn by doing.

Among African American youth, girls tend to outpace boys in understanding finances, and later in life, tend to manage finances better. Be careful with implicit and ex plicit biases when talking to boys. Help your sons become as financially strong as any of his female counterparts by giving him the same skills and knowledge to succeed.

So much of money man agement has to do with our personal priorities, so show your teen how they can connect the two. Fancy car or college fund? Expensive vacation or helping an aging parent? Include your teen in these important decisions.

Don’t be afraid to say, ‘I don’t know.’ Seek out the answer together!

According to Fortune, twothirds of Americans cannot pass a financial literacy test. For those in juvenile detention cen ters or prisons, being unable to budget, understand how debt works, and learn the importance of balancing finances, could not only impair their plans for the future, but also encourage be haviors that could return them to prison.

The Federal Bureau of Prisons reported in 2018 that out of the 18-65-year-olds incarcerated in federal prisons, many entered prisons at formidable stages of their development and subse quently missed the benefit of learning money management.

In addition to education pro grams that promote literacy and help incarcerated individuals earn GEDs, education advocates are increasingly calling for the advancement of financial litera cy courses in prisons.

Why?

Simply put: financial literacy promotes self-sufficiency and re duces recidivism.

“Many young people enter the system as juveniles and have lit tle to no understanding of how the world around them operates, financially. When a young per son’s education is stunted by a stay in prison, they are more in clined to seek extra-legal means of caring for themselves upon their release,” Darryl Markham, former Lorton prison peer coun selor and founder of Finance Forward told the Informer. “We have to include financial literacy to prisoners so that upon release, returning citizens can thrive as productive, financially aware citizens.”

Markham spent more than twenty years in prison – convict ed at 18 – after having dropped out of school in the 10th grade. While he claimed excellent grades and a clear grasp on most coursework, his arrest halted ac cess to formal learning and ways to make money legally.

“I was wilding out as a youth, but I was never dumb. I under

stood money and how to make it – supply, demand, inflation, and competition – but all in a very illegal way,” he said laugh ing. “But because we were slam ming down thousands of dollars in cash on a countertop to buy cars and designer clothes, I nev er understood banking, saving, investing, or safeguarding mon ey in a legal way. I did not un derstand credit cards and leasing apartments… these are the skills necessary for incarcerated people to learn while inside so they do not go back to bad habits.”

To combat this problem, in places like Pennsylvania, correc tions opened a dialogue in 2016 with the Pennsylvania State Agency Financial Exchange (PA $AFE). PA $AFE, a group of 20+ state agencies work togeth er to provide financial education for consumers. Corrections be gan working with the organiza tion to provide financial educa tion as part of a re-entry strategy.

“We have found that inmates too often do not have funda mental knowledge, skills, or experience to face the complex financial realities of life. Upon re-entry into society, too often they repeat poor financial deci sions that helped put them on the path to incarceration,” said John Wetzel, Pennsylvania secre tary of corrections, and Robin L. Wiessmann, Pennsylvania secre tary of banking and securities.

Although the program is in its early stages, both inmates and Corrections report positive feed back.

The program will be mea sured against four attainable outcomes: to see if those that received financial education in prison have a lower recidivism rate than those that did not, to see if past-offenders that are back in society and had financial literacy training are more suc cessfully employed than those that did not, to see if the released offenders are more motivated to use financial tools such as a bank account and are more willing to engage in entrepreneurship; and to see how satisfied the staff and inmates are with the overall pro gram results. g

a home may be possible

down payment.

next

Dream. Plan. Home.SM mortgage is a fixed-rate loan with a 3% down payment option.

It provides flexibility if you have limited credit history or credit challenges, and is available for a variety of loan amounts, including in high-cost areas. I’ll help you understand your available options so you can choose what works for you. We’ll discuss the loan amount, type of loan, property type, income, and homebuyer education requirements for eligibility. We’ll also talk about mortgage insurance that’s required with a low down payment and how it will increase the cost of the loan and monthly payment.